Embed Size (px)

Citation preview

High Quality Growth At Sensible Prices

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Emerging Markets Equity

November 3, 2011

Henderson-WessendorfFoundation

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Representing Vontobel Asset Management, Inc.

Business Address:

Vontobel Asset Management, Inc.

1540 Broadway, 38th Floor

New York, NY 10036

(212) 415-7000

www.vusa.com

Page 2

Amit Mukadam, DirectorInstitutional Clients – North America

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Content

Page 3

Part I: Firm Overview

Part II: Investment Approach and Team

Part III: Portfolio Characteristics

Part IV: Performance and Competitive Standing

Part V: Appendix

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

What Sets Us Apart?

Page 4

Organizational stability and independence Strong investment culture and incentives designed for

long term talent retention

Focused Focused on long-only global equity investing

Bottom-up, fundamental approach focused on high

quality growth at sensible prices

Seasoned 22 investment professionals averaging 18 years industry

experience

Key players with combined 100 years at Vontobel

Manager tenure (since 1994)

Disciplined Performance consistent with philosophy and process

Alpha generated from bottom-up fundamental research

Key

Ben

efit

s

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

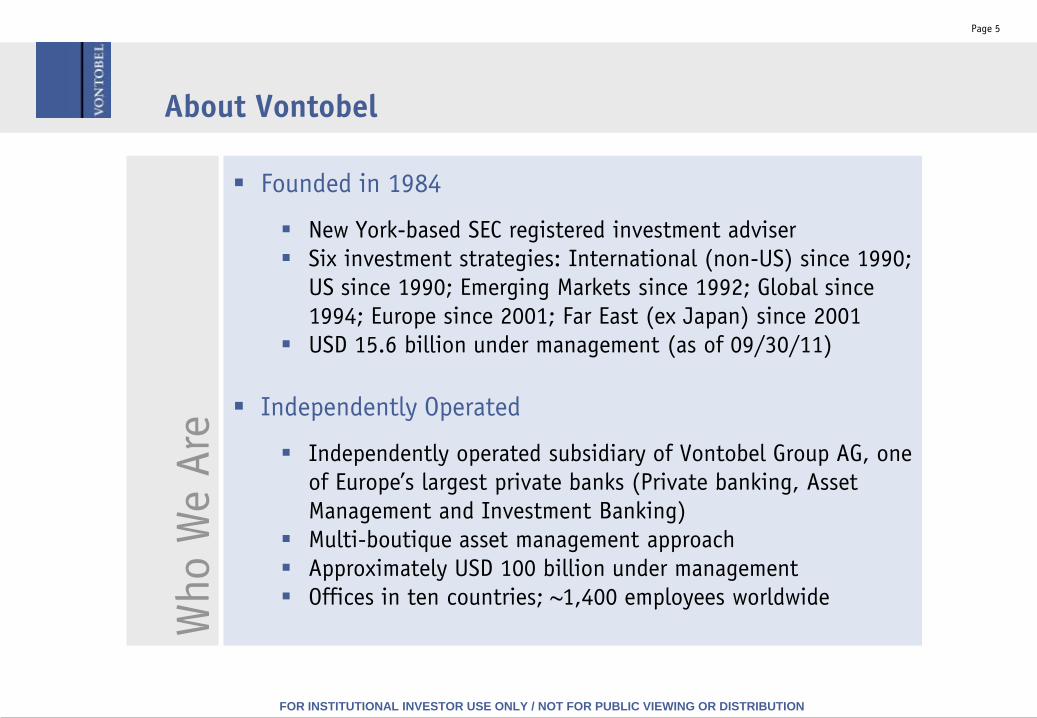

About Vontobel

Page 5

Founded in 1984

New York-based SEC registered investment adviser

Six investment strategies: International (non-US) since 1990;

US since 1990; Emerging Markets since 1992; Global since

1994; Europe since 2001; Far East (ex Japan) since 2001

USD 15.6 billion under management (as of 09/30/11)

Independently Operated

Independently operated subsidiary of Vontobel Group AG, one

of Europe’s largest private banks (Private banking, Asset

Management and Investment Banking)

Multi-boutique asset management approach

Approximately USD 100 billion under management

Offices in ten countries; ~1,400 employees worldwide

Who W

e Are

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

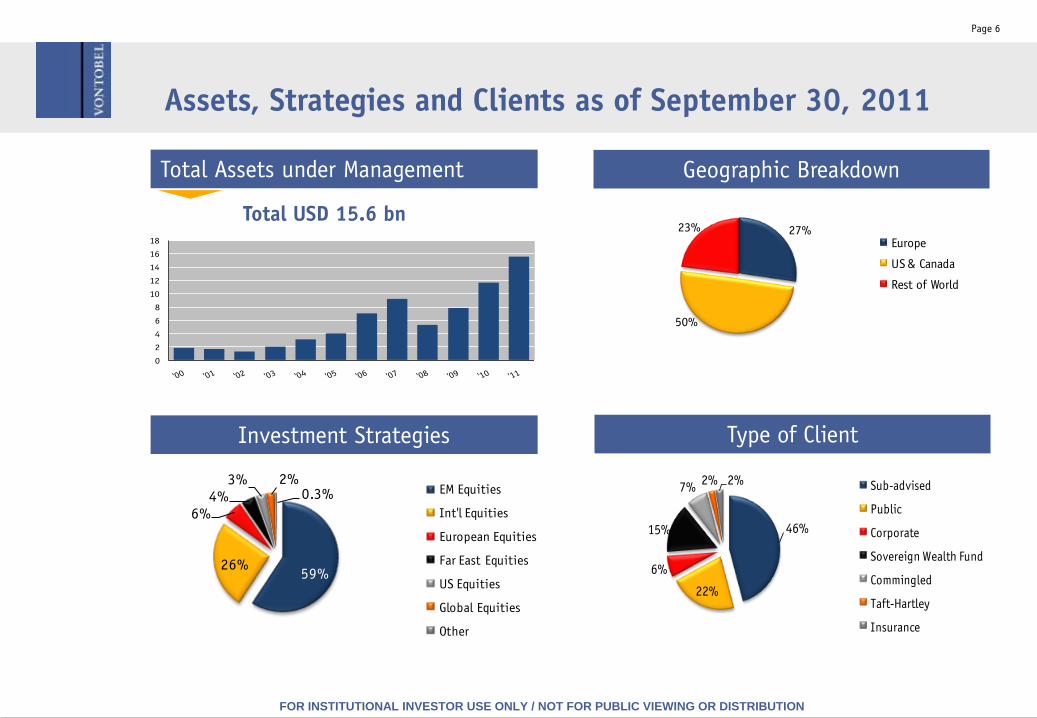

Assets, Strategies and Clients as of September 30, 2011

Page 6

Investment Strategies

Geographic Breakdown

27%

50%

23%

Europe

US & Canada

Rest of World

Type of Client

46%

22%

6%

15%

7%2% 2% Sub-advised

Public

Corporate

Sovereign Wealth Fund

Commingled

Taft-Hartley

Insurance

59%26%

6%4%

3% 2%0.3% EM Equities

Int'l Equities

European Equities

Far East Equities

US Equities

Global Equities

Other

Total Assets under Management

Total USD 15.6 bn

0

2

4

6

8

10

12

14

16

18

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Content

Page 7

Part I: Firm Overview

Part II: Investment Approach and Team

Part III: Portfolio Characteristics

Part IV: Performance and Competitive Standing

Part V: Appendix

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Investment Philosophy:High Quality Growth At Sensible Prices

Page 8

We believe there is a close correlation between earnings

growth and stock price appreciation over time. By

identifying sensibly priced high quality companies that can

grow earnings faster than the market on a sustainable basis,

we believe we will be able to achieve superior returns for

our clients.

Philoso

phy

* Source: Securities Research Company, chart by Vontobel.

13.8%

12.0%

8.1%

11.7%

9.2%

7.4% 7.8%

5.8% 5.4% 5.5%

3.7%

6.1%

11.9% 11.7%11.6%

11.3%

8.6%

7.1%

6.0%5.3% 5.0% 4.6%

2.1%

0.0%

Industry Groups

Annual Rates of Growth, 1985-2010

Stock Price Earnings

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

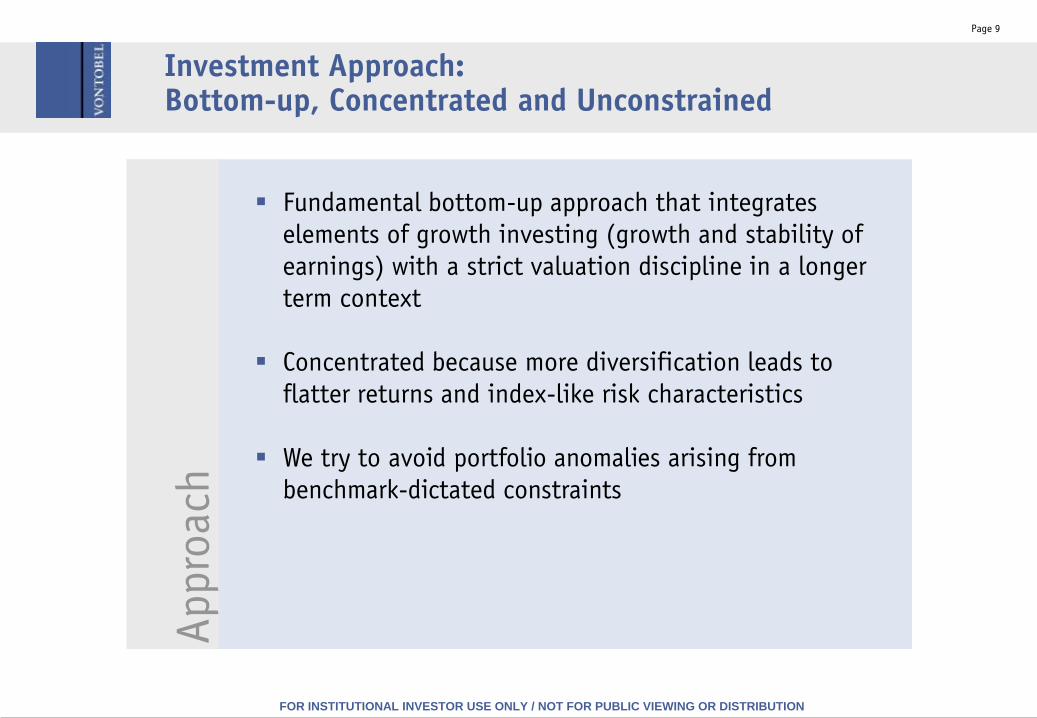

Investment Approach: Bottom-up, Concentrated and Unconstrained

Page 9

Fundamental bottom-up approach that integrates

elements of growth investing (growth and stability of

earnings) with a strict valuation discipline in a longer

term context

Concentrated because more diversification leads to

flatter returns and index-like risk characteristics

We try to avoid portfolio anomalies arising from

benchmark-dictated constraints

Appro

ach

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Product Profile

Page 10

High Quality at Sensible Prices

High-Conviction Portfolio

Benchmark Unconstrained

Multi-Cap Blend

Downside Protection

Char

acte

rist

ics

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

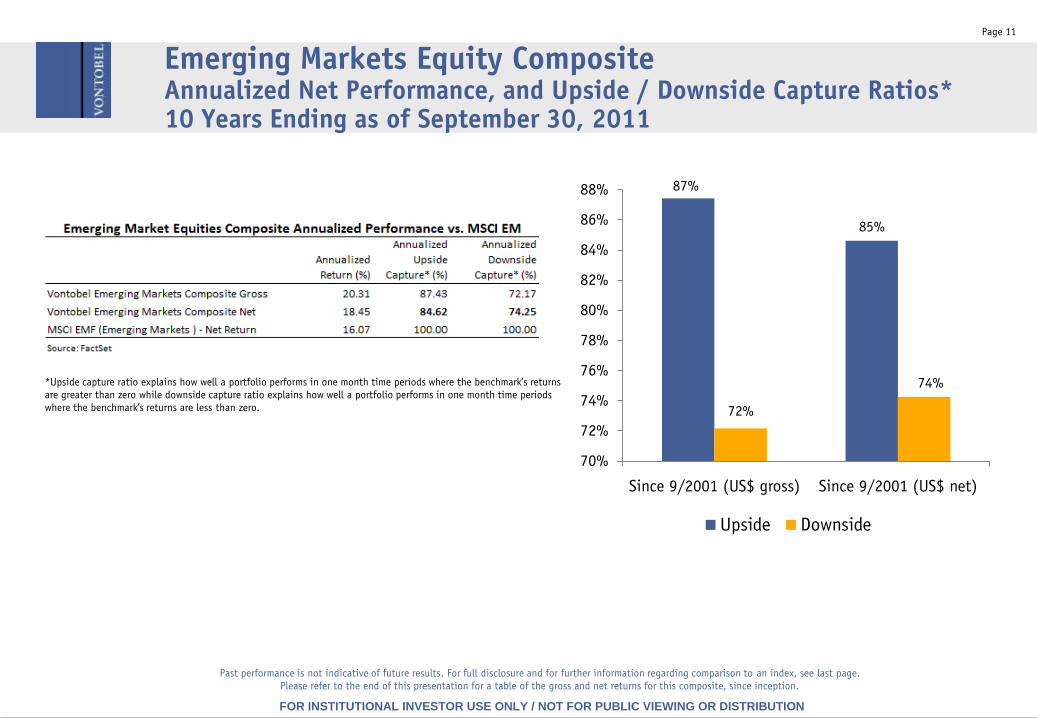

Emerging Markets Equity CompositeAnnualized Net Performance, and Upside / Downside Capture Ratios*10 Years Ending as of September 30, 2011

Page 11

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

*Upside capture ratio explains how well a portfolio performs in one month time periods where the benchmark’s returns

are greater than zero while downside capture ratio explains how well a portfolio performs in one month time periods

where the benchmark’s returns are less than zero.

87%

85%

72%

74%

70%

72%

74%

76%

78%

80%

82%

84%

86%

88%

Since 9/2001 (US$ gross) Since 9/2001 (US$ net)

Upside Downside

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

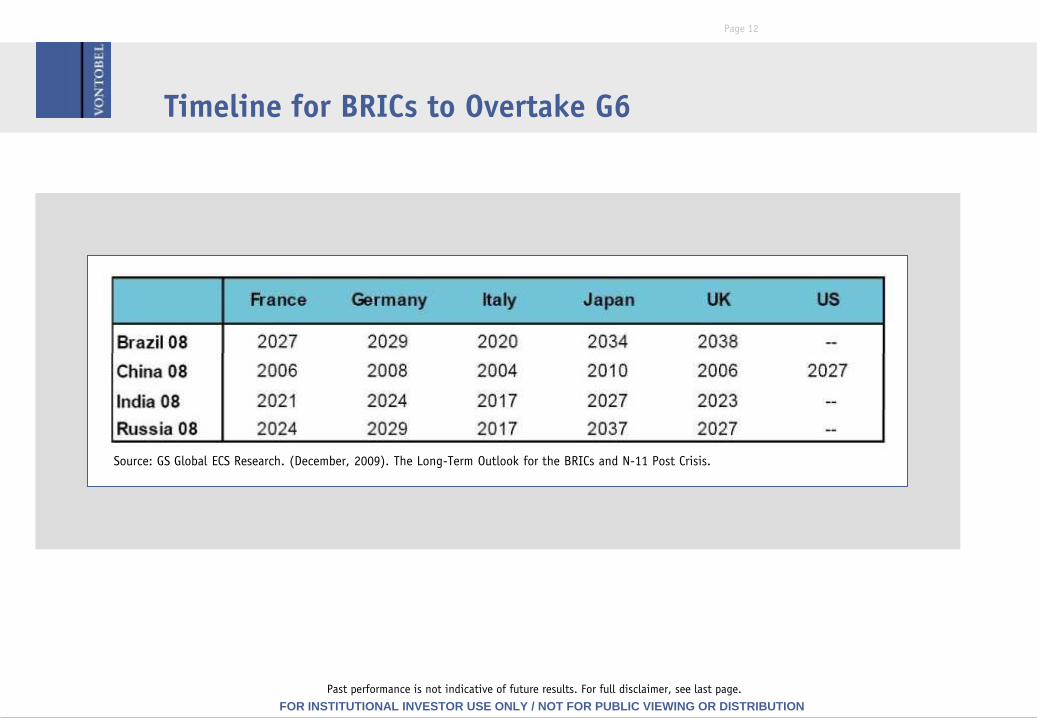

Timeline for BRICs to Overtake G6

Page 12

Source: GS Global ECS Research. (December, 2009). The Long-Term Outlook for the BRICs and N-11 Post Crisis.

Past performance is not indicative of future results. For full disclaimer, see last page.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

0

100

200

300

400

500

600

700

800

1994

1995

1995

1996

1996

1997

1997

1997

1998

1998

1999

1999

1999

2000

2000

2001

2001

2002

2002

2002

2003

2003

2004

2004

2004

2005

2005

2006

2006

2007

2007

2007

2008

2008

2009

2009

2009

Mexico and China Real Equity Returns Since 1994

China Total Returns in USD Indexed to 1994 Mexico Total Returns in USD Indexed to 1994

China Real GDP Growth Indexed to 1994 Mexico Real GDP Growth Indexed to 1994

Two Opposites

China Mexico

Annualized Equity Returns 1.8 12.9

Annualized real GDP Growth 9.7 2.7

Source: MSCI; Datastream; Bloomberg

Page 13

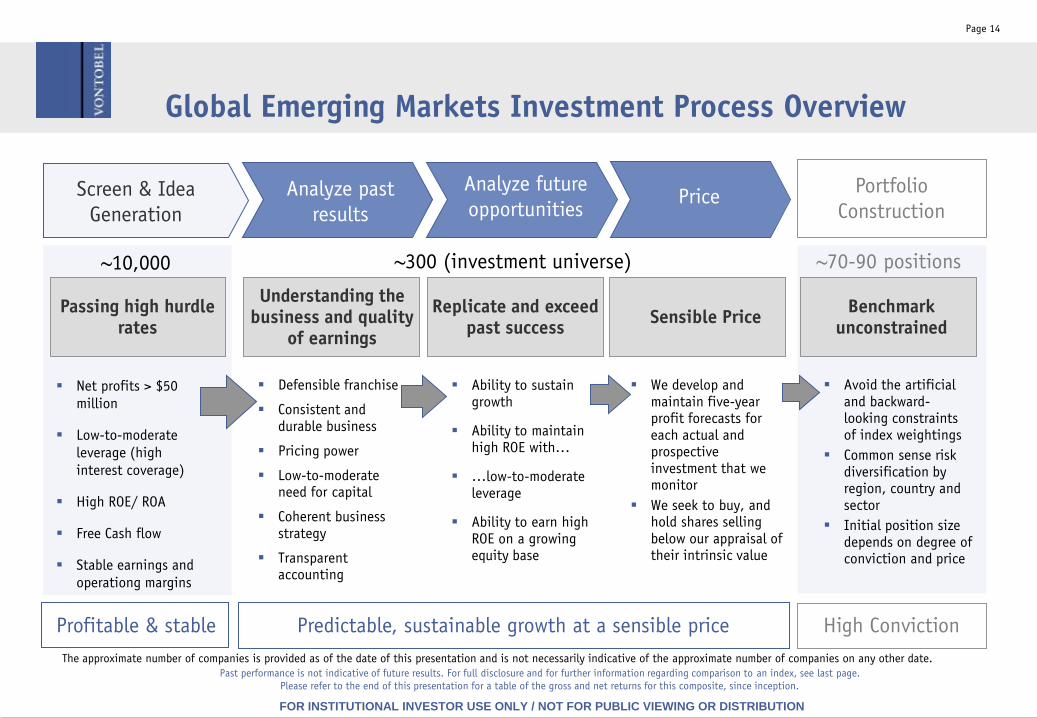

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Page 14

~300 (investment universe) ~70-90 positions

Understanding the business and quality

of earnings

Replicate and exceed past success

Sensible Price Benchmark

unconstrained

Profitable & stable High Conviction

~10,000

Predictable, sustainable growth at a sensible price

Screen & Idea

Generation

Analyze past

results

Analyze future

opportunitiesPrice

Portfolio

Construction

The approximate number of companies is provided as of the date of this presentation and is not necessarily indicative of the approximate number of companies on any other date.

Global Emerging Markets Investment Process Overview

Passing high hurdle rates

Net profits > $50

million

Low-to-moderate

leverage (high

interest coverage)

High ROE/ ROA

Free Cash flow

Stable earnings and

operationg margins

Defensible franchise

Consistent and durable business

Pricing power

Low-to-moderate need for capital

Coherent business strategy

Transparent accounting

Ability to sustain growth

Ability to maintain high ROE with…

…low-to-moderate leverage

Ability to earn high ROE on a growing equity base

We develop and maintain five-year profit forecasts for each actual and prospective investment that we monitor

We seek to buy, and hold shares selling below our appraisal of their intrinsic value

Avoid the artificial and backward-looking constraints of index weightings

Common sense risk diversification by region, country and sector

Initial position size depends on degree of conviction and price

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

EPS growth estimate

20% p.a. (vs. 29% p.a.

for past 10 years)

Page 15

Buy Discipline: Valuation… Price is what you pay…- Value is what you get.

Discount rate 7%

(normalized 10

year bond)

Terminal multiple

19x (vs. 22x

historical median

and 20x currently)

Discount ~10%

Assumptions

For illustrative purposes, to demonstrate the process

2009 (a) 2010 2014

68.8

FV 1929PV PV Div 2421

82.5

171.1

Vontobel EPS estimate Terminal multiple on

year 5 earnings estimate

19.0 x

Vontobel

Intrinsic Value

(PV+PV Div)3250

2340

81

Undervalued/Margin of Safety

Legend:

FV = Future Value

PV = Present Value

Div= Dividends

R$ = Brazilian Real

A = Actual

Current Price

For illustrative purposes, to demonstrate the process

2010 (a) 2011 2015

INR 13.6

FV INR 460PV PV Div INR 503

17.0

35.0

Vontobel EPS estimate Terminal multiple on

year 5 earnings estimate

19.0 x

Vontobel

Intrinsic Value

(PV+PV Div)INR 664

INR 485

INR 18

Discount

Legend:

FV = Future Value

PV = Present Value

Div= Dividends

A = Actual

Current Price

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Sell Discipline

Page 16

Price target met

Major merger/acquisition-related activity

Portfolio considerations

Deterioration in fundamentals

Better alternative identified

Sell D

isci

pline

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Portfolio Construction Global Emerging Markets Equity

Beware the tyranny of the index – Build a concentrated high-conviction portfolio.

Construction

Number of stocks

Cash

Page 17

Position size

Sector

Country

Conviction/Discount Min/Max position size at purchase: ~1%/5%

~70-90

At least 5 sectors at all times

Max. 20% absolute deviation relative to the MSCI Emerging Markets Index

Fully invested

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

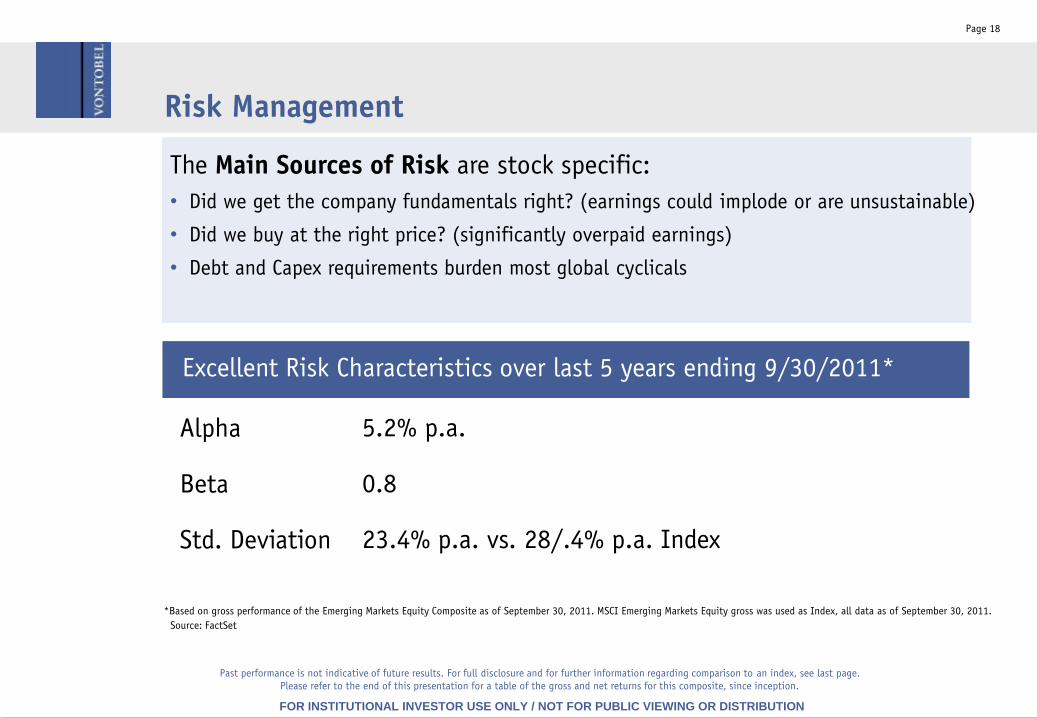

Risk Management

Page 18

Alpha

Beta

Std. Deviation

Excellent Risk Characteristics over last 5 years ending 9/30/2011*

5.2% p.a.

0.8

23.4% p.a. vs. 28/.4% p.a. Index

The Main Sources of Risk are stock specific:

• Did we get the company fundamentals right? (earnings could implode or are unsustainable)

• Did we buy at the right price? (significantly overpaid earnings)

• Debt and Capex requirements burden most global cyclicals

*Based on gross performance of the Emerging Markets Equity Composite as of September 30, 2011. MSCI Emerging Markets Equity gross was used as Index, all data as of September 30, 2011.

Source: FactSet

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

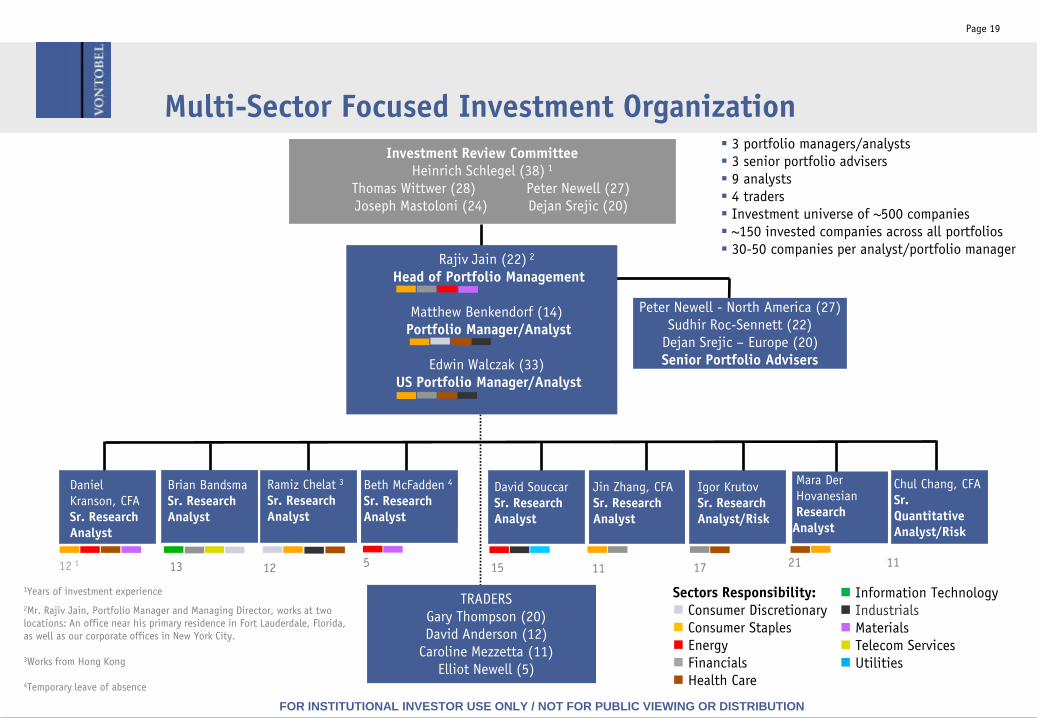

Multi-Sector Focused Investment Organization

Investment Review Committee

Heinrich Schlegel (38) 1

Thomas Wittwer (28) Peter Newell (27)

Joseph Mastoloni (24) Dejan Srejic (20)

Igor Krutov

Sr. Research

Analyst/Risk

Chul Chang, CFA

Sr.

Quantitative

Analyst/Risk

David Souccar

Sr. Research

Analyst

Sectors Responsibility:

Consumer Discretionary

Consumer Staples

Energy

Financials

Health Care

Information Technology

Industrials

Materials

Telecom Services

Utilities

Beth McFadden 4

Sr. Research

Analyst

Brian Bandsma

Sr. Research

Analyst

Daniel

Kranson, CFA

Sr. Research

Analyst

Jin Zhang, CFA

Sr. Research

Analyst

TRADERS

Gary Thompson (20)

David Anderson (12)

Caroline Mezzetta (11)

Elliot Newell (5)

3 portfolio managers/analysts

3 senior portfolio advisers

9 analysts

4 traders

Investment universe of ~500 companies

~150 invested companies across all portfolios

30-50 companies per analyst/portfolio manager

1Years of investment experience

2Mr. Rajiv Jain, Portfolio Manager and Managing Director, works at two

locations: An office near his primary residence in Fort Lauderdale, Florida,

as well as our corporate offices in New York City.

3Works from Hong Kong

4Temporary leave of absence

21171115121312 1 11

Mara Der

Hovanesian

Research

Analyst

Page 19

Peter Newell - North America (27)

Sudhir Roc-Sennett (22)

Dejan Srejic – Europe (20)

Senior Portfolio Advisers

5

Ramiz Chelat 3

Sr. Research

Analyst

Rajiv Jain (22) 2

Head of Portfolio Management

Matthew Benkendorf (14)

Portfolio Manager/Analyst

Edwin Walczak (33)

US Portfolio Manager/Analyst

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Page 20

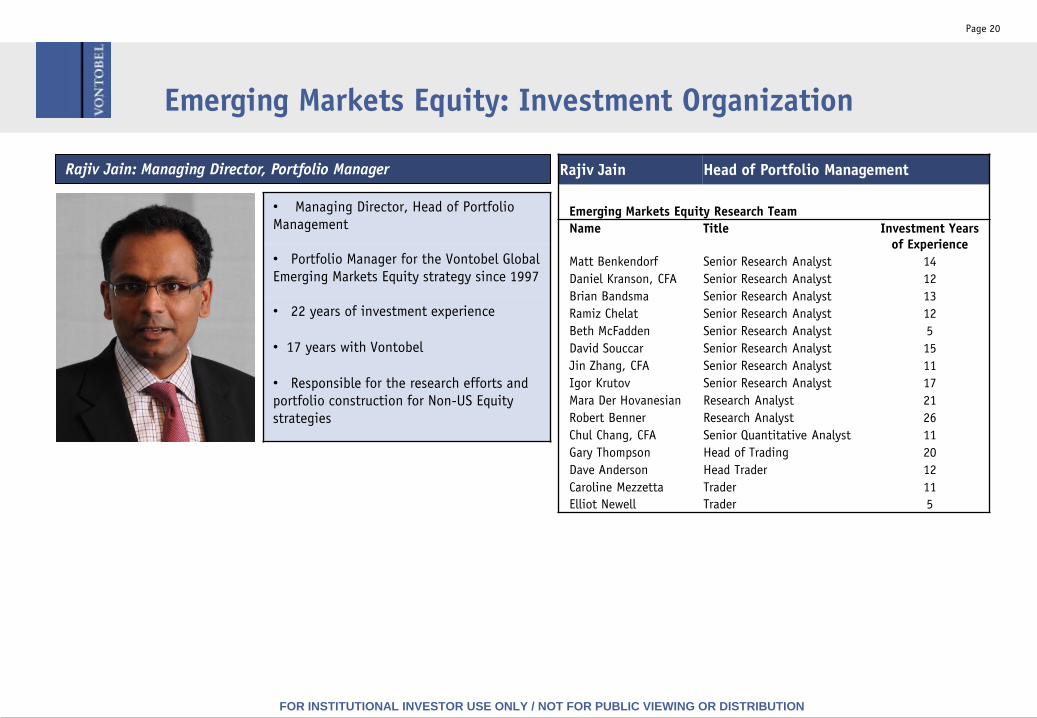

Rajiv Jain Head of Portfolio Management

Emerging Markets Equity Research Team

Name Title Investment Years

of Experience

Matt Benkendorf Senior Research Analyst 14

Daniel Kranson, CFA Senior Research Analyst 12

Brian Bandsma Senior Research Analyst 13

Ramiz Chelat Senior Research Analyst 12

Beth McFadden Senior Research Analyst 5

David Souccar Senior Research Analyst 15

Jin Zhang, CFA Senior Research Analyst 11

Igor Krutov Senior Research Analyst 17

Mara Der Hovanesian Research Analyst 21

Robert Benner Research Analyst 26

Chul Chang, CFA Senior Quantitative Analyst 11

Gary Thompson Head of Trading 20

Dave Anderson Head Trader 12

Caroline Mezzetta Trader 11

Elliot Newell Trader 5

• Managing Director, Head of Portfolio

Management

• Portfolio Manager for the Vontobel Global

Emerging Markets Equity strategy since 1997

• 22 years of investment experience

• 17 years with Vontobel

• Responsible for the research efforts and

portfolio construction for Non-US Equity

strategies

Rajiv Jain: Managing Director, Portfolio Manager

Emerging Markets Equity: Investment Organization

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Content

Page 21

Part I: Firm Overview

Part II: Investment Approach and Team

Part III: Portfolio Characteristics

Part IV: Performance and Competitive Standing

Part V: Appendix

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Page 22

Company*** % of Portfolio Country

British American Tobacco PLC 5.1 United Kingdom

HDFC Bank Ltd. 4.4 India

Housing Development Finance

Corp. Ltd.4.1 India

Companhia de Bebidas das

Americas4.1 Brazil

ITC Ltd. 3.4 India

Souza Cruz S.A. 3.2 Brazil

Itau Unibanco Holding S.A 3.2 Brazil

Baidu Inc. ADS 2.7 China

SABMiller PLC 2.6 South Africa

Companhia Energetica de Minas

Gerais-CEMIG1.9 Brazil

Top Ten as % of Portfolio 34.7

Portfolio Valuation & Statistics*

Portfolio MSCI EME

Capitalization ($ bn), weighted average 21.8 37.8

Capitalization ($ bn), weighted median 13.4 15.1

P/E - Forecast 12-month, weighted harmonic

average14.2 8.4

Dividend Yield (%) 2.8 3.3

5 Yr Historical EPS Growth 23.3 15.7

Return on Equity, weighted average 32.4 20.7

Return on Equity, average 31.1 18.4

Composite Statistics**

Anlzd Alpha 5 years 5.2 N/A

Beta 5 years 0.8 1.0

Sharpe Ratio 5 years 0.4 0.1

Anlzd Standard Deviation 5 years 23.4 28.4

Emerging Markets Equity Portfolio - Characteristics

As of September 30, 2011

***The securities identified and described do not represent all of the securities purchased, sold or

recommended for client accounts. The reader should not assume that an investment in the

securities identified was or will be profitable.

*Based on a representative portfolio and shown as supplemental information to the Composite presentation.

Other accounts contained in the composite could have materiallydifferent statistics. The basis upon which the

representative portfolio was selected is that the portfolio is the largest, and most representative account.

Source: FactSet

** Based on gross performance of the Emerging Markets Equity Composite as of September 30, 2011.

***The Top Ten Holdings are based on a representative portfolio, and are shown as supplemental

information to the Emerging Markets Equity Composite presentation. Source: FactSet

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

Portfolio Turnover: 53.7% (2010)

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Page 23

Emerging Markets Equity Portfolio - Sector Allocation*

As of September 30, 2011

*Emerging Markets Equity Representative Account vs. MSCI EME Index

The sector holdings are based on a representative portfolio, and are shown as supplemental

information to the Emerging Markets Equity Composite presentation.

Source: FactSet

Port. Bench.

Vontobel Sector Weight Weight Difference

Consumer Discretionary 7.15 7.85 -0.70

Consumer Staples 38.01 7.74 30.27

Energy 3.39 13.97 -10.57

Financials 18.91 23.75 -4.84

Health Care 1.19 1.10 0.09

Industrials 2.86 6.64 -3.78

Information Technology 10.26 12.21 -1.95

Materials 3.92 13.80 -9.89

Telecommunication Services 2.09 9.47 -7.38

Utilities 10.21 3.49 6.73

[Cash] 2.01 -- 2.01

Total 100.00 100.00 --

-15 -10 -5 0 5 10 15 20 25 30

Energy

Materials

TelecommunicationServices

Financials

Industrials

InformationTechnology

ConsumerDiscretionary

Health Care

[Cash]

Utilities

ConsumerStaples

-10.57

-9.89

-7.38

-4.84

-3.78

-1.95

-0.70

0.09

2.01

6.73

30.27

Vontobel Sector 9/30/2011

Difference

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

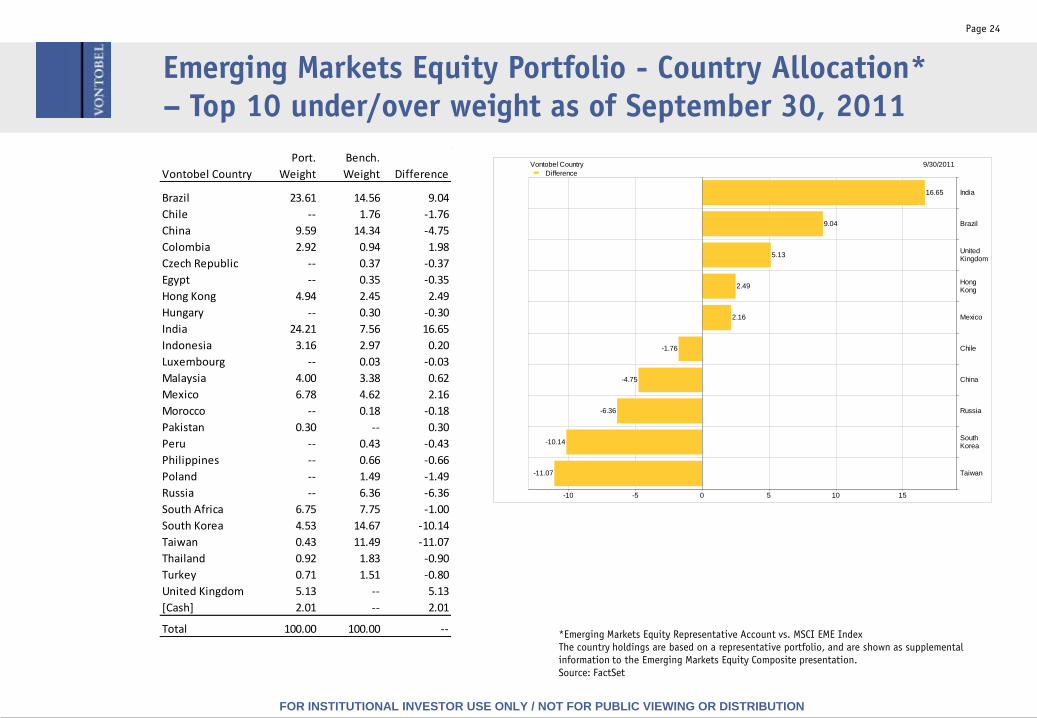

Page 24

Emerging Markets Equity Portfolio - Country Allocation*

– Top 10 under/over weight as of September 30, 2011

*Emerging Markets Equity Representative Account vs. MSCI EME Index

The country holdings are based on a representative portfolio, and are shown as supplemental

information to the Emerging Markets Equity Composite presentation.

Source: FactSet

Port. Bench.

Vontobel Country Weight Weight Difference

Brazil 23.61 14.56 9.04

Chile -- 1.76 -1.76

China 9.59 14.34 -4.75

Colombia 2.92 0.94 1.98

Czech Republic -- 0.37 -0.37

Egypt -- 0.35 -0.35

Hong Kong 4.94 2.45 2.49

Hungary -- 0.30 -0.30

India 24.21 7.56 16.65

Indonesia 3.16 2.97 0.20

Luxembourg -- 0.03 -0.03

Malaysia 4.00 3.38 0.62

Mexico 6.78 4.62 2.16

Morocco -- 0.18 -0.18

Pakistan 0.30 -- 0.30

Peru -- 0.43 -0.43

Philippines -- 0.66 -0.66

Poland -- 1.49 -1.49

Russia -- 6.36 -6.36

South Africa 6.75 7.75 -1.00

South Korea 4.53 14.67 -10.14

Taiwan 0.43 11.49 -11.07

Thailand 0.92 1.83 -0.90

Turkey 0.71 1.51 -0.80

United Kingdom 5.13 -- 5.13

[Cash] 2.01 -- 2.01

Total 100.00 100.00 --

-10 -5 0 5 10 15

Taiwan

South Korea

Russia

China

Chile

Mexico

Hong Kong

United Kingdom

Brazil

India

-11.07

-10.14

-6.36

-4.75

-1.76

2.16

2.49

5.13

9.04

16.65

Vontobel Country 9/30/2011

Difference

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

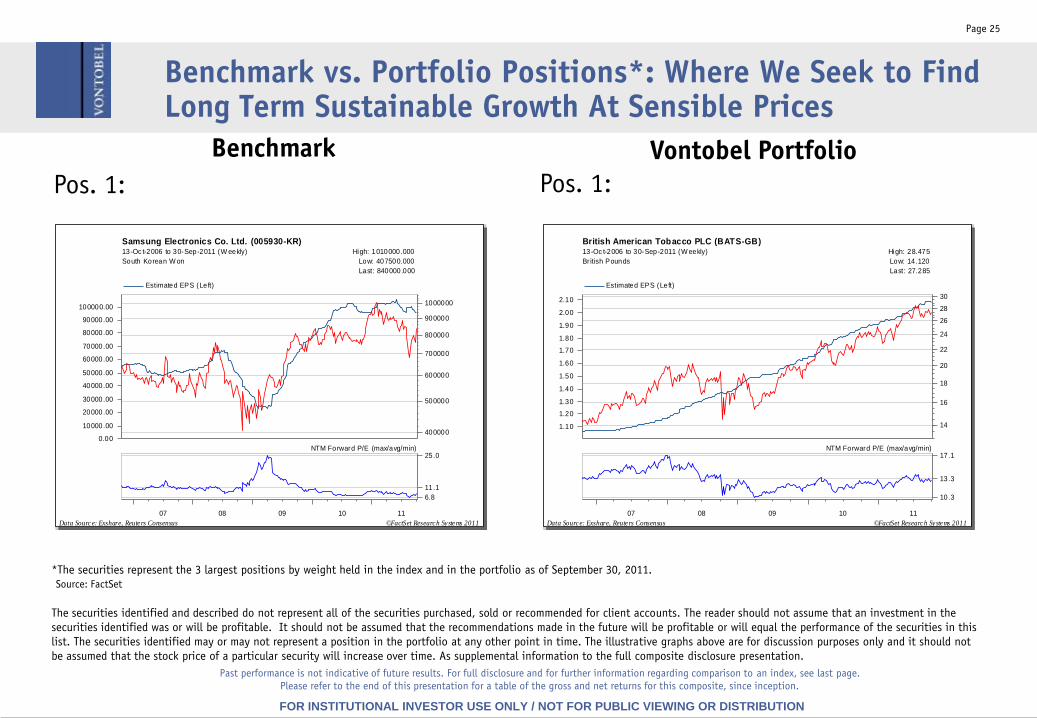

Page 25

Pos. 1: Pos. 1:

Benchmark vs. Portfolio Positions*: Where We Seek to Find Long Term Sustainable Growth At Sensible Prices

*The securities represent the 3 largest positions by weight held in the index and in the portfolio as of September 30, 2011.

The securities identified and described do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the

securities identified was or will be profitable. It should not be assumed that the recommendations made in the future will be profitable or will equal the performance of the securities in this

list. The securities identified may or may not represent a position in the portfolio at any other point in time. The illustrative graphs above are for discussion purposes only and it should not

be assumed that the stock price of a particular security will increase over time. As supplemental information to the full composite disclosure presentation.

Benchmark Vontobel Portfolio

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

Source: FactSet

07 08 09 10 11

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

2.10

14

16

18

20

22

24

26

28

30

17.1

13.3

10.3

NTM Forward P/E (max/avg/min)

Estimated EPS (Left)

British American Tobacco PLC (BATS-GB)13-Oc t-2006 to 30-Sep-2011 (W eekly) High: 28.475

Br itish Pounds Low: 14.120

Last: 27.285

Data Source: Exshare, Reuters Consensus ©FactSet Research Systems 2011

07 08 09 10 11

0.00

10000.00

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

80000.00

90000.00

100000.00

400000

500000

600000

700000

800000

900000

1000000

25.0

11.1

6.8

NTM Forward P/E (max/avg/min)

Estimated EPS (Left)

Samsung Electronics Co. Ltd. (005930-KR)13-Oc t-2006 to 30-Sep-2011 (W eekly) High: 1010000.000

South Korean W on Low: 407500.000

Last: 840000.000

Data Source: Exshare, Reuters Consensus ©FactSet Research Systems 2011

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

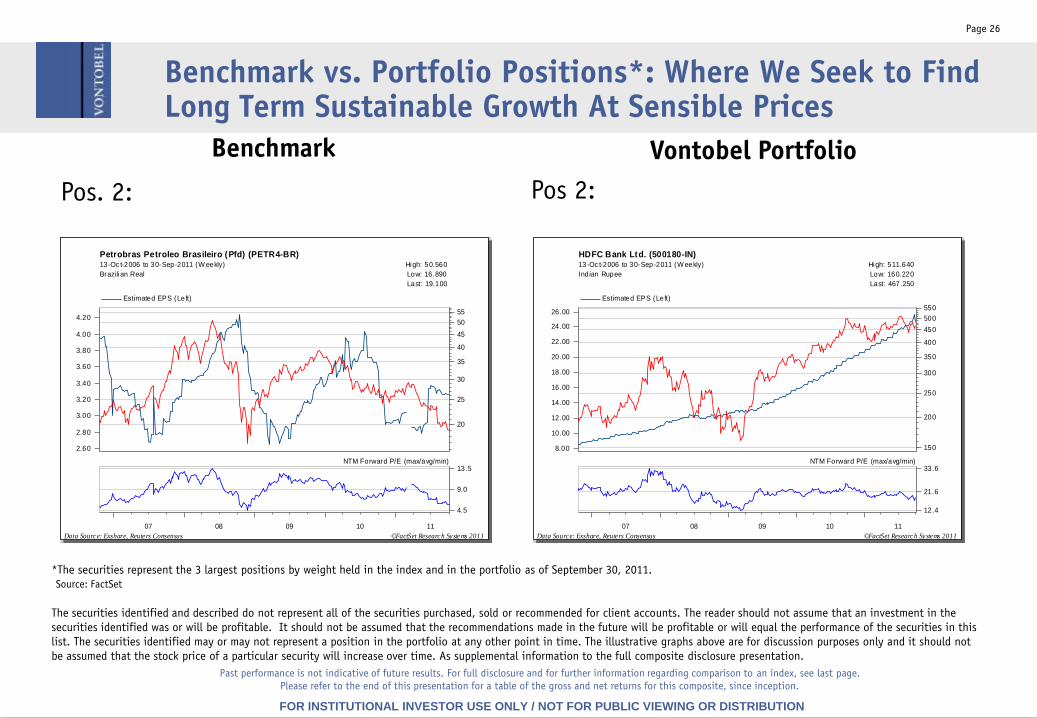

Page 26

Pos. 2:

Benchmark Vontobel Portfolio

Pos 2:

Benchmark vs. Portfolio Positions*: Where We Seek to Find Long Term Sustainable Growth At Sensible Prices

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

07 08 09 10 11

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

150

200

250

300

350

400

450

500

550

33.6

21.6

12.4

NTM Forward P/E (max/avg/min)

Estimated EPS (Left)

HDFC Bank Ltd. (500180-IN)13-Oc t-2006 to 30-Sep-2011 (W eekly) High: 511.640

Indian Rupee Low: 160.220

Last: 467.250

Data Source: Exshare, Reuters Consensus ©FactSet Research Systems 2011

*The securities represent the 3 largest positions by weight held in the index and in the portfolio as of September 30, 2011.

The securities identified and described do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the

securities identified was or will be profitable. It should not be assumed that the recommendations made in the future will be profitable or will equal the performance of the securities in this

list. The securities identified may or may not represent a position in the portfolio at any other point in time. The illustrative graphs above are for discussion purposes only and it should not

be assumed that the stock price of a particular security will increase over time. As supplemental information to the full composite disclosure presentation.

Source: FactSet

07 08 09 10 11

2.60

2.80

3.00

3.20

3.40

3.60

3.80

4.00

4.20

20

25

30

35

40

45

50

55

13.5

9.0

4.5

NTM Forward P/E (max/avg/min)

Estimated EPS (Left)

Petrobras Petroleo Brasileiro (Pfd) (PETR4-BR)13-Oc t-2006 to 30-Sep-2011 (W eekly) High: 50.560

Brazilian Real Low: 16.890

Last: 19.100

Data Source: Exshare, Reuters Consensus ©FactSet Research Systems 2011

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Content

Page 27

Part I: Firm Overview

Part II: Investment Approach and Team

Part III: Portfolio Characteristics

Part IV: Performance and Competitive Standing

Part V: Appendix

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

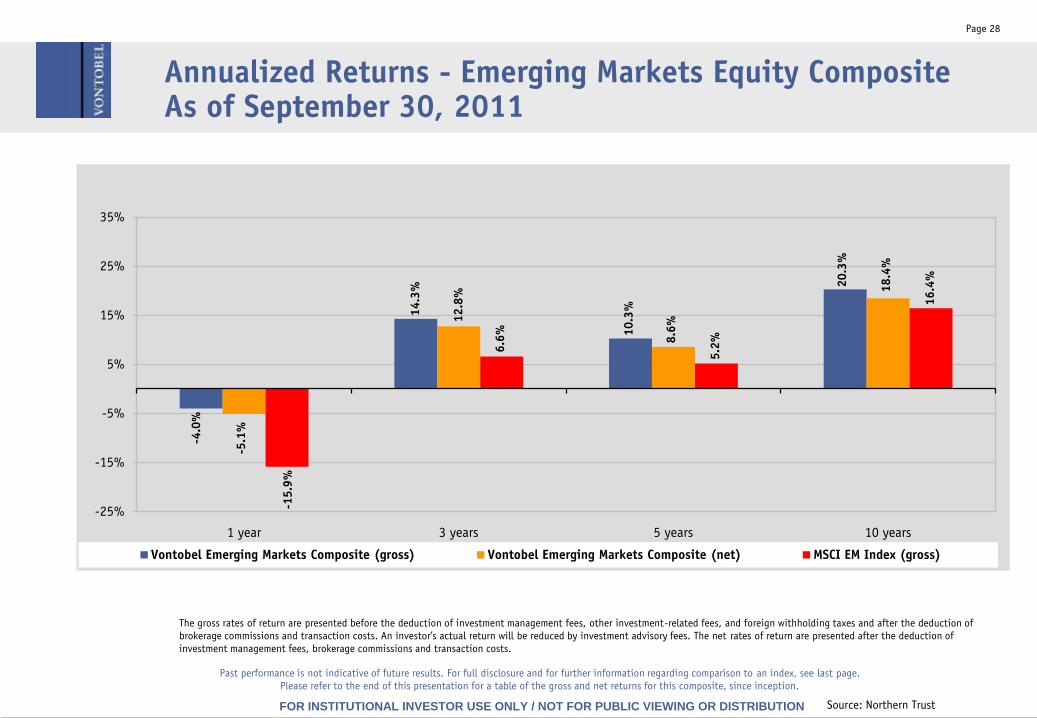

Annualized Returns - Emerging Markets Equity Composite As of September 30, 2011

-4.0

%

14.3

%

10.3

%

20.3

%

-5.1

%

12.8

%

8.6

%

18.4

%

-15.9

%

6.6

%

5.2

%

16.4

%

-25%

-15%

-5%

5%

15%

25%

35%

1 year 3 years 5 years 10 years

Vontobel Emerging Markets Composite (gross) Vontobel Emerging Markets Composite (net) MSCI EM Index (gross)

Source: Northern Trust

Page 28

The gross rates of return are presented before the deduction of investment management fees, other investment-related fees, and foreign withholding taxes and after the deduction of

brokerage commissions and transaction costs. An investor’s actual return will be reduced by investment advisory fees. The net rates of return are presented after the deduction of

investment management fees, brokerage commissions and transaction costs.

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

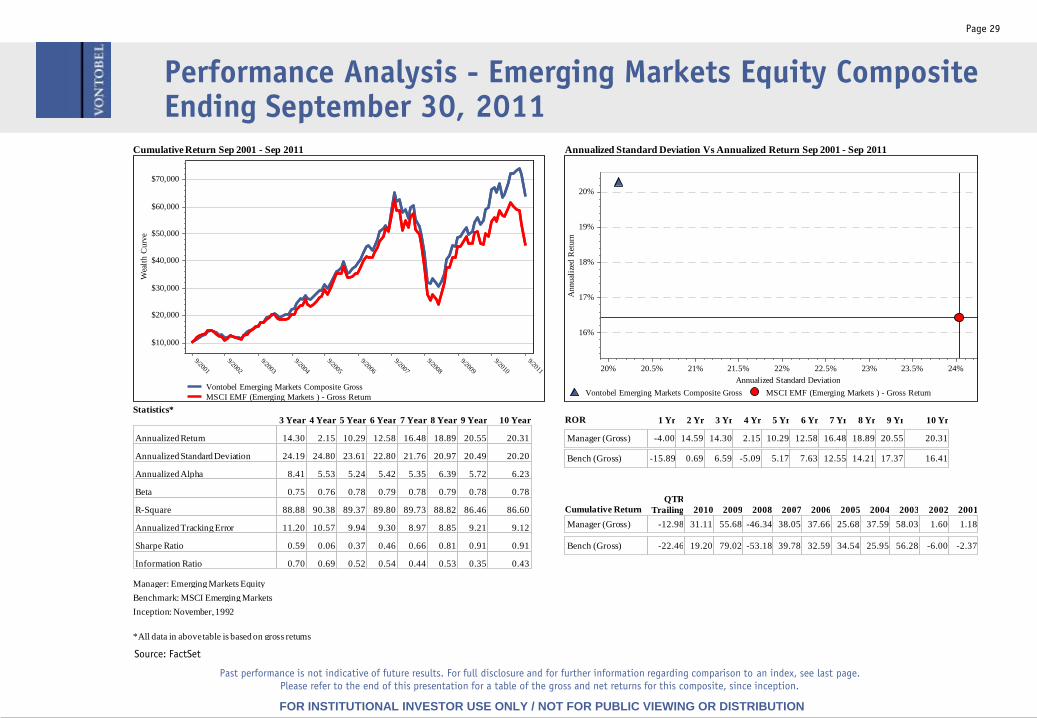

Performance Analysis - Emerging Markets Equity CompositeEnding September 30, 2011

Page 29

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

Source: FactSet

*All data in above table is based on gross returns

Cumulative Return Sep 2001 - Sep 2011

9/2001

9/2002

9/2003

9/2004

9/2005

9/2006

9/2007

9/2008

9/2009

9/2010

9/2011

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

Wea

lth C

urv

e

Vontobel Emerging Markets Composite Gross

MSCI EMF (Emerging Markets ) - Gross Return

Annualized Standard Deviation Vs Annualized Return Sep 2001 - Sep 2011

20% 20.5% 21% 21.5% 22% 22.5% 23% 23.5% 24%

Annualized Standard Deviation

16%

17%

18%

19%

20%

Annual

ized

Ret

urn

Vontobel Emerging Markets Composite Gross MSCI EMF (Emerging Markets ) - Gross Return

Statistics*

3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Year

Annualized Return 14.30 2.15 10.29 12.58 16.48 18.89 20.55 20.31

Annualized Standard Deviation 24.19 24.80 23.61 22.80 21.76 20.97 20.49 20.20

Annualized Alpha 8.41 5.53 5.24 5.42 5.35 6.39 5.72 6.23

Beta 0.75 0.76 0.78 0.79 0.78 0.79 0.78 0.78

R-Square 88.88 90.38 89.37 89.80 89.73 88.82 86.46 86.60

Annualized Tracking Error 11.20 10.57 9.94 9.30 8.97 8.85 9.21 9.12

Sharpe Ratio 0.59 0.06 0.37 0.46 0.66 0.81 0.91 0.91

Information Ratio 0.70 0.69 0.52 0.54 0.44 0.53 0.35 0.43

ROR

Manager (Gross)

Bench (Gross)

1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10 Yr

Manager (Gross)-4.00 14.59 14.30 2.15 10.29 12.58 16.48 18.89 20.55 20.31

Bench -15.89 0.69 6.59 -5.09 5.17 7.63 12.55 14.21 17.37 16.41

Cumulative Return

Manager (Gross)

Bench (Gross)

QTR

Trailing 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001

Manager (Gross)-12.98 31.11 55.68 -46.34 38.05 37.66 25.68 37.59 58.03 1.60 1.18

Bench -22.46 19.20 79.02 -53.18 39.78 32.59 34.54 25.95 56.28 -6.00 -2.37

Manager: Emerging Markets Equity

Benchmark: MSCI Emerging Markets

Inception: November, 1992

*All data in above table is based on gross returns

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

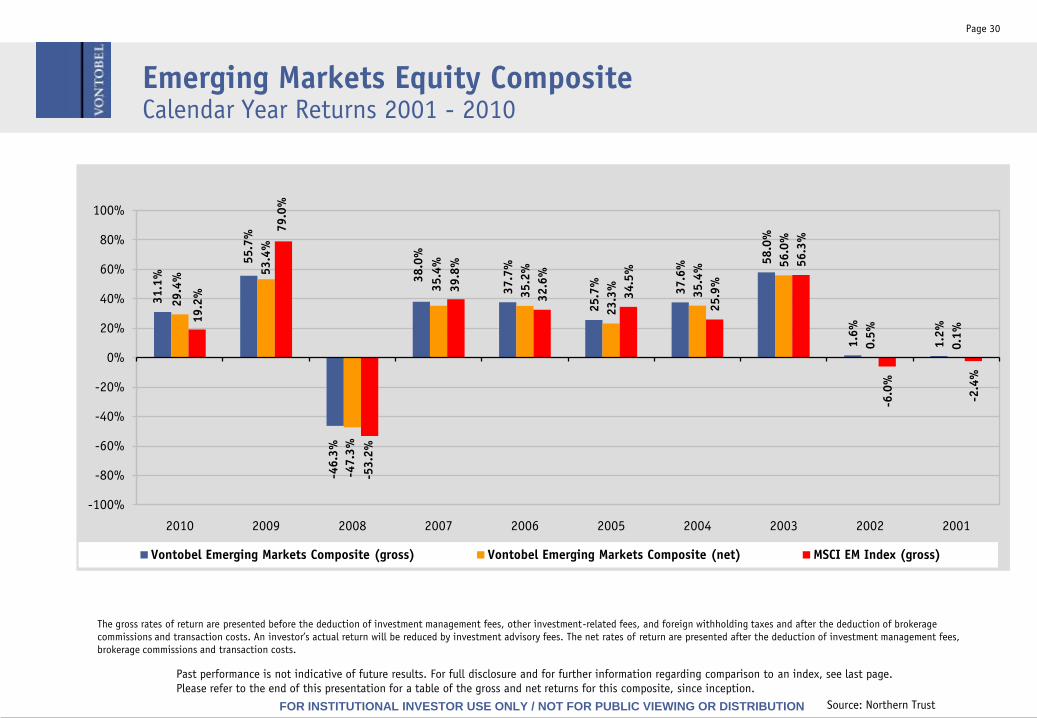

Emerging Markets Equity CompositeCalendar Year Returns 2001 - 2010

31.1

%

55.7

%

-46.3

%

38.0

%

37.7

%

25.7

%

37.6

%

58.0

%

1.6

%

1.2

%

29.4

%

53.4

%

-47.3

%

35.4

%

35.2

%

23.3

%

35.4

%

56.0

%

0.5

%

0.1

%

19.2

%

79.0

%

-53.2

%

39.8

%

32.6

%

34.5

%

25.9

%

56.3

%

-6.0

%

-2.4

%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

2010 2009 2008 2007 2006 2005 2004 2003 2002 2001

Vontobel Emerging Markets Composite (gross) Vontobel Emerging Markets Composite (net) MSCI EM Index (gross)

Source: Northern Trust

Page 30

The gross rates of return are presented before the deduction of investment management fees, other investment-related fees, and foreign withholding taxes and after the deduction of brokerage

commissions and transaction costs. An investor’s actual return will be reduced by investment advisory fees. The net rates of return are presented after the deduction of investment management fees,

brokerage commissions and transaction costs.

Past performance is not indicative of future results. For full disclosure and for further information regarding comparison to an index, see last page.

Please refer to the end of this presentation for a table of the gross and net returns for this composite, since inception.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

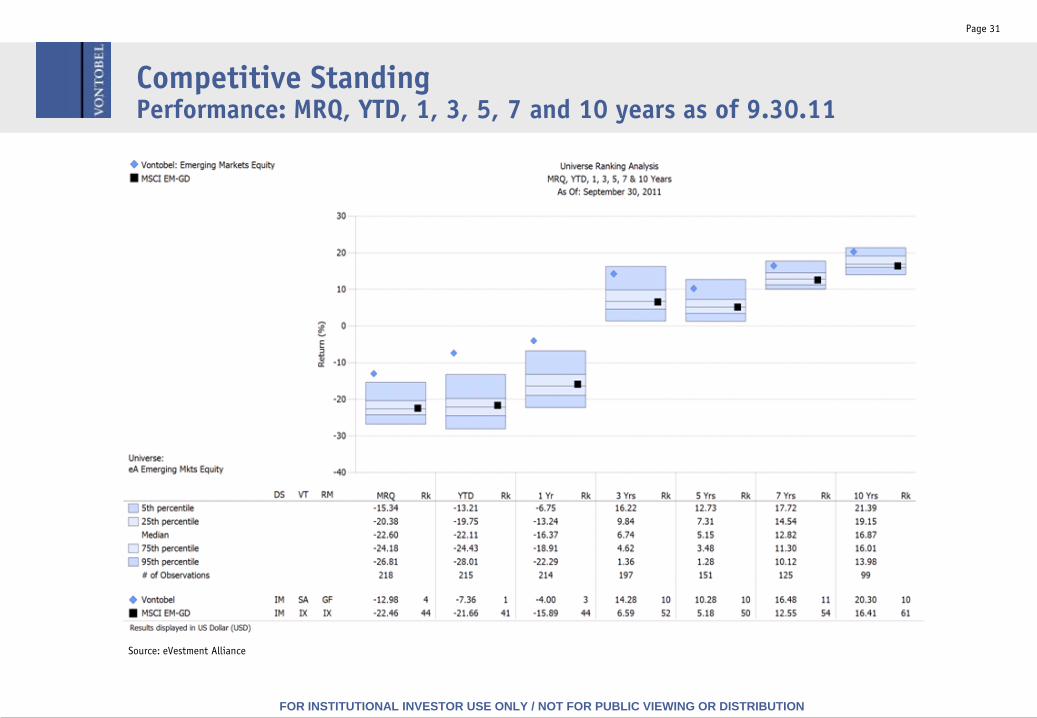

Competitive StandingPerformance: MRQ, YTD, 1, 3, 5, 7 and 10 years as of 9.30.11

Source: eVestment Alliance

Page 31

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Source: eVestment Alliance

Page 32

Competitive StandingMPT Statistics: Annualized 5 years as of 9.30.11

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Source: eVestment Alliance

Page 33

Competitive StandingReturns vs. Standard Deviation: Annualized 5 yr. periods as of 9.30.11

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Content

Page 34

Part I: Firm Overview

Part II: Investment Approach and Team

Part III: Portfolio Characteristics

Part IV: Performance and Competitive Standing

Part V: Appendix

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Vontobel Emerging MarketsFee Schedule

Page 35

Minimum initial investment is $5 million in the Institutional Commingled Fund. Fees are based

on the total net assets of the Fund. Includes management, custody and administrative fees.

The Vontobel Global Emerging Markets Institutional Commingled Fund has $225 million across 9

Institutional Clients as of September 30, 2011

Vontobel Global Emerging Markets Institutional Commingled Fund

First $50 million 1.10%

Next $150 million 1.00%

Over $200 million 0.85%

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

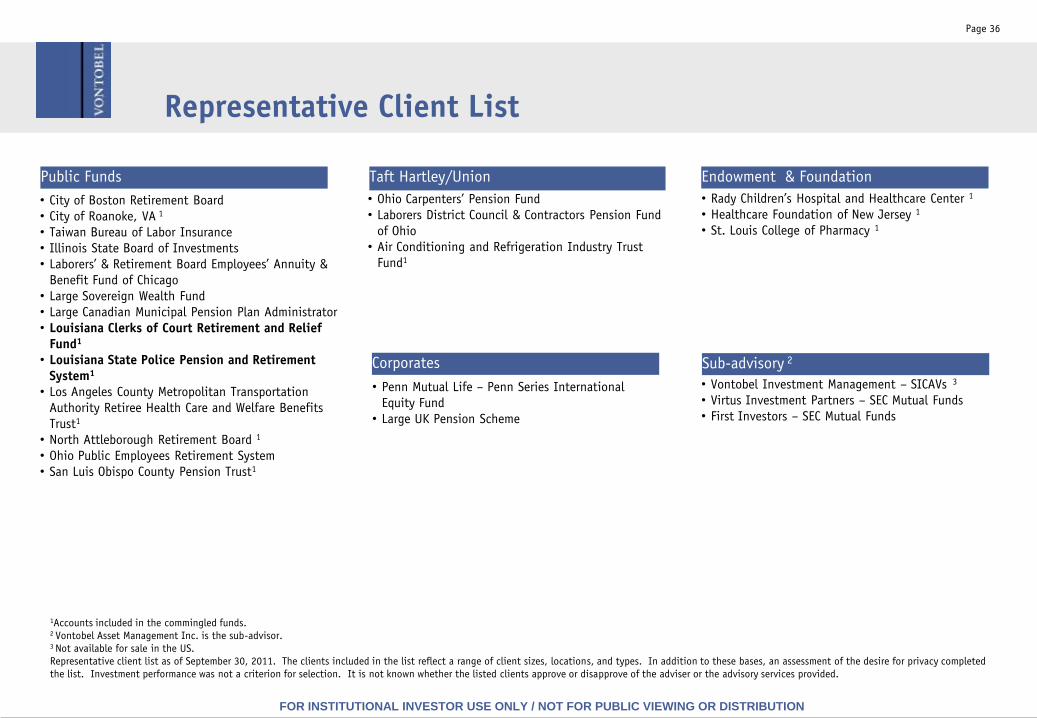

Representative Client List

Taft Hartley/Union

• Ohio Carpenters’ Pension Fund

• Laborers District Council & Contractors Pension Fund

of Ohio

• Air Conditioning and Refrigeration Industry Trust

Fund1

Sub-advisory 2

• Vontobel Investment Management – SICAVs 3

• Virtus Investment Partners – SEC Mutual Funds

• First Investors – SEC Mutual Funds

1Accounts included in the commingled funds.2 Vontobel Asset Management Inc. is the sub-advisor.3 Not available for sale in the US.

Representative client list as of September 30, 2011. The clients included in the list reflect a range of client sizes, locations, and types. In addition to these bases, an assessment of the desire for privacy completed

the list. Investment performance was not a criterion for selection. It is not known whether the listed clients approve or disapprove of the adviser or the advisory services provided.

Public Funds

• City of Boston Retirement Board

• City of Roanoke, VA 1

• Taiwan Bureau of Labor Insurance

• Illinois State Board of Investments

• Laborers’ & Retirement Board Employees’ Annuity &

Benefit Fund of Chicago

• Large Sovereign Wealth Fund

• Large Canadian Municipal Pension Plan Administrator

• Louisiana Clerks of Court Retirement and Relief

Fund1

• Louisiana State Police Pension and Retirement

System1

• Los Angeles County Metropolitan Transportation

Authority Retiree Health Care and Welfare Benefits

Trust1

• North Attleborough Retirement Board 1

• Ohio Public Employees Retirement System

• San Luis Obispo County Pension Trust1

Endowment & Foundation

• Rady Children’s Hospital and Healthcare Center 1

• Healthcare Foundation of New Jersey 1

• St. Louis College of Pharmacy 1

Corporates

• Penn Mutual Life – Penn Series International

Equity Fund

• Large UK Pension Scheme

Page 36

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

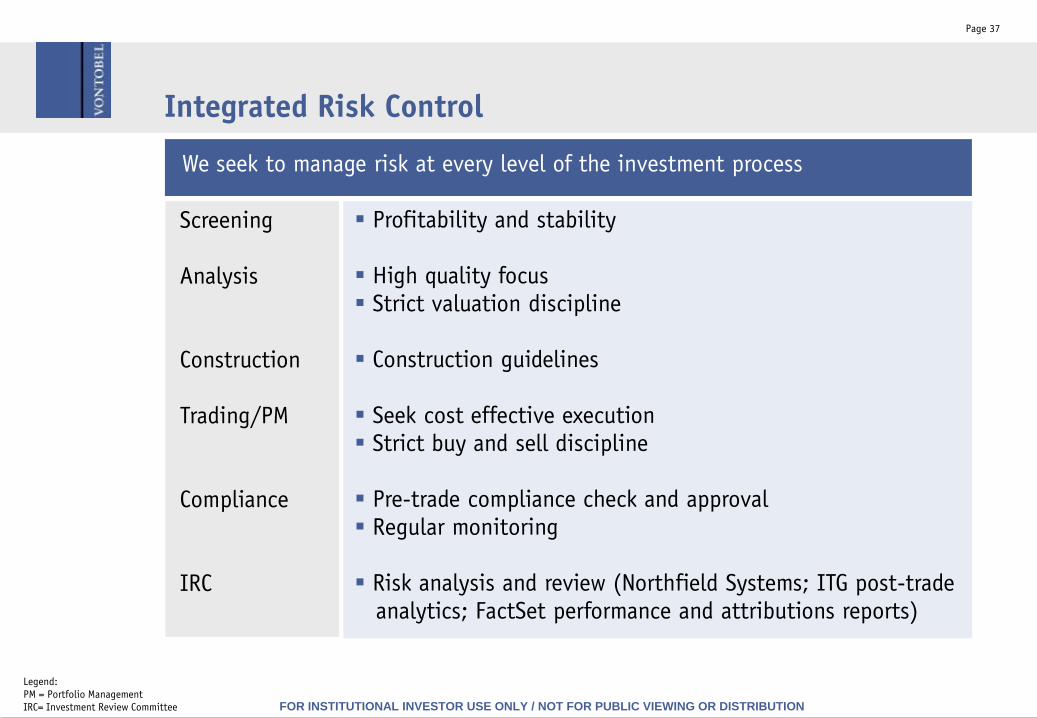

Integrated Risk Control

Page 37

Screening

Analysis

Construction

Trading/PM

Compliance

IRC

We seek to manage risk at every level of the investment process

Legend:

PM = Portfolio Management

IRC= Investment Review Committee

Profitability and stability

High quality focus Strict valuation discipline

Construction guidelines

Seek cost effective execution Strict buy and sell discipline

Pre-trade compliance check and approval Regular monitoring

Risk analysis and review (Northfield Systems; ITG post-tradeanalytics; FactSet performance and attributions reports)

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Commitment to Excellence

Dedicated relationship

manager serves as single

point of contact

Regular updates:

- Portfolio updates

- Quarterly reporting

- Portfolio manager access

Comprehensive website

Client Services

Committed to highest

standards of governance

Oversee that Vontobel

employees adhere to

rules and regulations.

Monitor employee trading

Ensure adherence to client

specific investing

guidelines

Compliance Program Technology

Infrastructure

Total outsourcing of

non-core business:

Backoffice-> Northern Trust

IT -> external IT

HR -> Administaff

All data backed up nightly

Fully operational business

continuity plan

Page 38

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

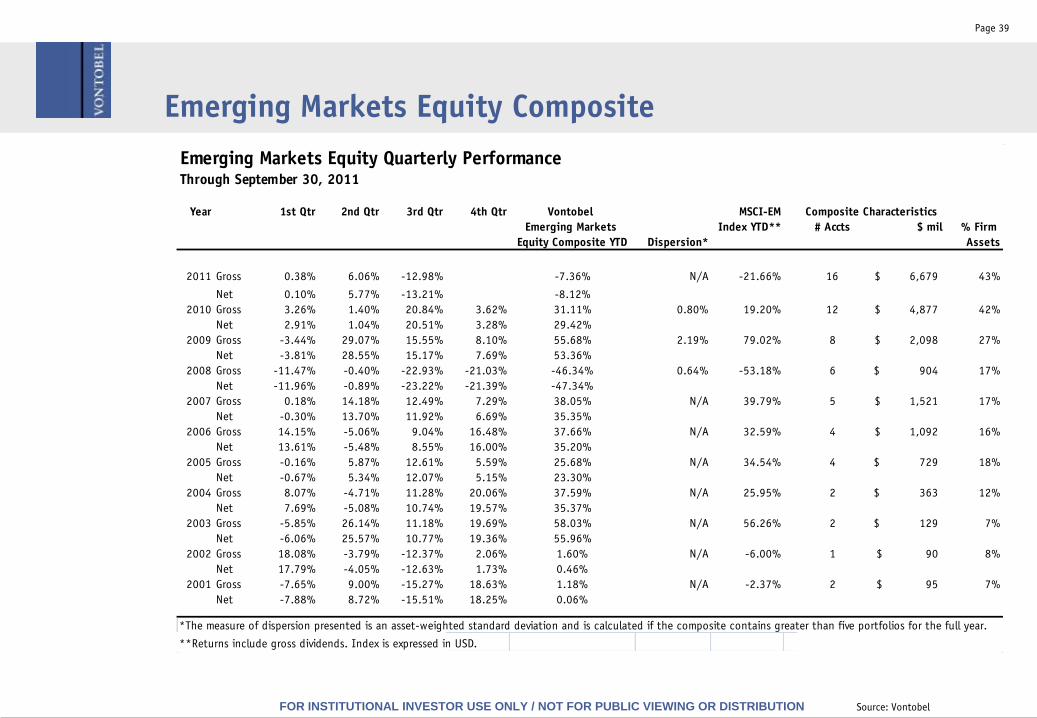

Page 39

Emerging Markets Equity Composite

Source: Vontobel

Emerging Markets Equity Quarterly Performance Through September 30, 2011

Year 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Vontobel MSCI-EM

Emerging Markets Index YTD** # Accts $ mil % Firm

Equity Composite YTD Dispersion* Assets

2011 Gross 0.38% 6.06% -12.98% -7.36% N/A -21.66% 16 6,679$ 43%

Net 0.10% 5.77% -13.21% -8.12%

2010 Gross 3.26% 1.40% 20.84% 3.62% 31.11% 0.80% 19.20% 12 4,877$ 42%

Net 2.91% 1.04% 20.51% 3.28% 29.42%

2009 Gross -3.44% 29.07% 15.55% 8.10% 55.68% 2.19% 79.02% 8 2,098$ 27%

Net -3.81% 28.55% 15.17% 7.69% 53.36%

2008 Gross -11.47% -0.40% -22.93% -21.03% -46.34% 0.64% -53.18% 6 904$ 17%

Net -11.96% -0.89% -23.22% -21.39% -47.34%

2007 Gross 0.18% 14.18% 12.49% 7.29% 38.05% N/A 39.79% 5 1,521$ 17%

Net -0.30% 13.70% 11.92% 6.69% 35.35%

2006 Gross 14.15% -5.06% 9.04% 16.48% 37.66% N/A 32.59% 4 1,092$ 16%

Net 13.61% -5.48% 8.55% 16.00% 35.20%

2005 Gross -0.16% 5.87% 12.61% 5.59% 25.68% N/A 34.54% 4 729$ 18%

Net -0.67% 5.34% 12.07% 5.15% 23.30%

2004 Gross 8.07% -4.71% 11.28% 20.06% 37.59% N/A 25.95% 2 363$ 12%

Net 7.69% -5.08% 10.74% 19.57% 35.37%

2003 Gross -5.85% 26.14% 11.18% 19.69% 58.03% N/A 56.26% 2 129$ 7%

Net -6.06% 25.57% 10.77% 19.36% 55.96%

2002 Gross 18.08% -3.79% -12.37% 2.06% 1.60% N/A -6.00% 1 90$ 8%

Net 17.79% -4.05% -12.63% 1.73% 0.46%

2001 Gross -7.65% 9.00% -15.27% 18.63% 1.18% N/A -2.37% 2 95$ 7%

Net -7.88% 8.72% -15.51% 18.25% 0.06%

*The measure of dispersion presented is an asset-weighted standard deviation and is calculated if the composite contains greater than five portfolios for the full year.

**Returns include gross dividends. Index is expressed in USD.

Composite Characteristics

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Disclaimer

Page 40

The index comparisons in this presentation are provided for informational purposes only and should not be used as the basis for making

an investment decision. Further, the performance of the composite and the Index may not be comparable.

Investments discussed in the presentation are hypothetical investments and there is no assurance that Vontobel will make any

investments with the same or similar characteristics as the hypothetical investments presented. The hypothetical investments are

presented for discussion purposes only and are not a reliable indicator of the performance or investment profile of the composite.

Any projections contained in this presentation are based on a variety of estimates and assumptions. There can be no assurance that the

assumptions made in connection with the projections will prove accurate, and actual results may differ materially. The inclusion of

projections should not be regarded as an indication that Vontobel considers the projections to be a reliable prediction of future events

and projections should not be relied upon as such.

This disclaimer applies to this presentation and the oral or written comments of any person presenting it.

The inclusion in the composite of the performance of wrap accounts and private client assets could result in a material difference in the

performance returns.

There can be no assurance that investment objectives will be achieved. Clients must be prepared to bear risk of a total loss of their

investment.

As fees are deducted quarterly, the compounding effect will be to increase the impact of the fee by an amount directly related to the

gross account performance. For example, on an account with a 0.5% fee, and gross performance of 20% over one year, the compounding

effect of the fee will result in performance of approximately 19.4%. A $10,000 initial investment would grow to approximately $14,256

gross of fees, versus $14,000 net of fees, over a two-year period.

FOR INSTITUTIONAL INVESTOR USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION

Performance Disclosure

Page 41

Emerging Markets Equity Composite includes all discretionary accounts, excluding wrap accounts and private client assets, that invest mainly in equity securities of issuers located in emerging market countries in Asia, Latin America, Africa, and Europe. Results of the composite are shown compared to the Morgan Stanley Capital International - Emerging Markets Index (the “MSCI Emerging Markets Index”), an unmanaged index based on share prices of a select group of global emerging market stocks that are available to global investors. The benchmark is used for comparative purposes only and generally reflects the risk or investment style of the investments in the composite. The index is a free float-adjusted market capitalization index of approximately 750 stocks that is designed to measure equity market performance in 21 emerging markets countries. The index is calculated on a total return basis with gross dividends reinvested, but does not reflect fees, withholding taxes or other investment expenses, and is expressed in U.S. Dollars. Investments made by the Company for the portfolios it manages according to respective strategies may differ significantly in terms of security holdings, industry weightings, and asset allocation from those of the MSCI Emerging Markets Index. The minimum account size for this composite is $1 million.

Vontobel Asset Management, Inc. ("VAMUS") claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. VAMUS has been independently verified for the periods between January 1, 2001 through June 30, 2011. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. The Emerging Markets Equity composite has been examined for the periods between January 1, 1994 through June 30, 2011. The verification and performance examination reports are available upon request.

VAMUS is an investment advisory firm registered under the Investment Advisers Act of 1940 and a subsidiary of Vontobel Holding AG, Zurich, Switzerland. For GIPS purposes, the firm is defined as all institutional accounts at Vontobel Asset Management, excluding wrap accounts and private client assets. The firm maintains a complete list and description of composites, which is available upon request. Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Results are based on fully discretionary institutional accounts under management, including those accounts no longer with the firm, and excluding wrap accounts and private client assets. Net composite performance is presented after the deduction of foreign withholding taxes. Capital gains, dividends and interest income received may be subject to withholding taxes imposed by the country of origin and such taxes may not be recoverable. Past performance is not indicative of future results.

No portfolios contained in this composite were carved out from balanced portfolios or multi-manager portfolios currently or historically. Leverage and short positions are not used in the composition of client portfolios. Derivatives in the form of forward currency contracts are used in the composition of client portfolios for opportunistic currency hedging.

The Vontobel Global Emerging Markets Fund, an unregistered private investment trust, pays a bundled fee, the components of which include: investment management fees; custodial fees; legal fees; and, other administrative expenses. Bundled-fee portfolios as a percentage of composite assets at year-end are as follows: 3.5% in 2007, 3.1% in 2008, 3.9% in 2009, 2.1% in 2010.

The U.S. Dollar is the currency used to express performance. Returns include the effect of foreign currency exchange rates. Returns are presented gross and net of management fees and include the reinvestment of all income. The gross rates of return are presented before the deduction of investment management fees, other investment-related fees, and foreign withholding taxes and after the deduction of brokerage commissions and transaction costs. An investor’s actual return will be reduced by investment advisory fees. The net rates of return are presented after the deduction of investment management fees, brokerage commissions, transaction costs and bundled fees. Such investment management fees are actual fees, as distinguished from model fees, and do not contain any performance-based fee components.

The standard annual management fees charged by the Company for the Composite are: 0.95% on the first $100 million, 0.85% over $100 million. Certain accounts may have higher management fees than the standard fee schedule. The Company’s investment advisory fees are further described in Part II of its Form ADV.

The Emerging Markets Equity Composite was created October 31, 1992. Compliance with GIPS has been verified firm-wide by Ashland Partners & Company LLP from January 1, 2005 through June 30, 2011. In addition, a performance examination was conducted on the Emerging Markets Equity Composite beginning January 1, 2005. For the period January 1, 2001 through December 31, 2004, the Company was verified firm-wide by, and the performance results of the Emerging Markets Equity Composite were examined by, Ernst & Young LLP. Performance results from January 1, 1994 to December 31, 2000 have been examined by PriceWaterhouseCoopers.

Composite assets for Emerging Markets Equity at end of 2006 was incorrectly shown as $1,341 million and was changed to $1,092 million on March 7th, 2011.