Embed Size (px)

Citation preview

ACCOUNTING STANDARDS BOARD JANUARY 2006 DISCUSSION PAPER

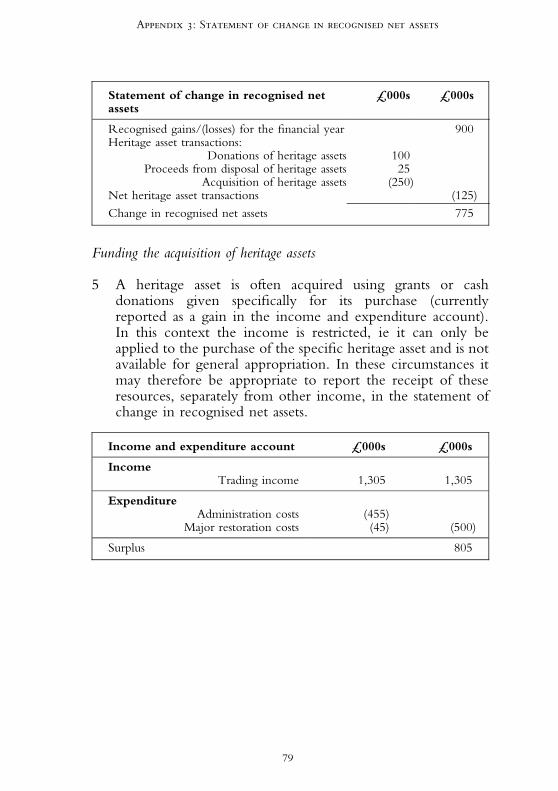

ACCOUNTING

STANDARDS

BOARD

HERITAGE ASSETS:

CAN ACCOUNTING DO BETTER?

For ease of handling, we prefer comments to be sent by e-mail (in Word format), to:

Comments may also be sent in hard copy form to:

Duncan Russell

ACCOUNTING STANDARDS BOARD

5th Floor Aldwych House

71-91 Aldwych

London WC2B 4HN

Comments should reach us by 31 May 2006.

All replies will be regarded as on the public record unless confidentiality is requested by the commentator. If

you are sending a confidential response by e-mail, please include the word 'confidential' in the subject line of

your e-mail.

Cover image: The Rosetta Stone. Copyright The Trustees of The British Museum.

For the convenience of respondents in compiling their responses, the text of the 'Questions for respondents'

in the Preface can be downloaded (in Word format) from the relevant project page in the Current Projects

section of the ASB website (www.frc.org.uk/asb)

HERITAGE ASSETS:

CAN ACCOUNTING DO BETTER?

ACCOUNTINGSTANDARDSBOARD

DISCUSSION

PAPER

#The Accounting Standards Board Limited 2006ISBN 1-84140-744-5

C O N T E N T S

Page

Preface 3

Summary of proposals 9

Section 1: What are heritage assets?Heritage assets meet the definition of an asset 13

Inalienability 14Examples of heritage assets 15A definition for heritage assets 16

Existing definitions 16Proposed definition 17

Section 2: What should accounting try to do?Financial information should be relevant and reliable 19Financial information should be comparable 20Financial information should be understandable 21Non-financial information is also useful 21Conclusion 22

Section 3: Approaches to accounting for heritage assetsThe existing UK approach – capitalise recent acquisitions at cost 23A full capitalisation approach 25

Historical cost 26Current value 26Notional value 27

A non-capitalisation approach 27Acquisitions and disposals 27

Proposals 28

Section 4: Some practical considerationsCapitalisation approach 30

Practical issues 30Practicability of the capitalisation approach 33Valuation of heritage assets: some practical difficulties 33

Non-capitalisation approach 34Statement of change in recognised net assets 34Reporting related transactions 35

1

First time adoption of proposed accounting treatments 36Capitalisation approach 36Non-capitalisation approach 36

Conclusion 36

Section 5: Disclosure requirementsExisting disclosure requirements 37Proposals for disclosures 38

The nature and scale of heritage assets held 38Accounting policies 39Preservation and management policy 39Acquisitions and disposals 39Funding sources for acquisitions 40Five year financial summary of activity 40Groups of heritage assets 41Other useful information 41

Illustrative examples of disclosures 42Illustrative disclosures under the capitalisation approach 42The Vintage Car Museum 42

Illustrative disclosures under the non-capitalisation approach 46The Barsetshire Museum 46The Ancient Monument Museum 53

Section 6: Historic assets used by the entity itself 55

Section 7: Corporate art 59

Appendix 1: Definitions of heritage assets used in the UKand other jurisdictions 60

Appendix 2: Current reporting requirements in the UKand other jurisdictions 68

Appendix 3: Statement of change in recognised net assets 77

Appendix 4: Reference material 83

Accounting Standards Board january 2006 discussion paper

2

P R E F A C E

Introduction

1 In 1799, a company of French soldiers was demolishing awall near the Egyptian village of Rashid to clear the way foran extension to a fort, when it discovered a slab of greygranite. This was the Rosetta Stone, and its inscriptionsprovided the breakthrough for the decipherment ofEgyptian hieroglyphs. In 1801 the stone was acquired bythe British; the following year it was deposited in the BritishMuseum in London where it has remained ever since1.

2 The Rosetta Stone exemplifies, perhaps in extreme form,the challenges that are faced in the financial reporting ofheritage assets. The stone is incomparable: there is no othersimilar asset. As a result, its market value is imponderable: itis, quite literally, priceless. It was acquired at little or nodirect cost: even if it had been purchased, it is unlikely thatthe cost would have any relevance in financial reporting twocenturies later.

3 The stone is one of over 100,000 objects held by the BritishMuseum in its Egyptian collections. The Egyptiandepartment is one of the Museum’s eight departments2.There are some 2,500 museums and galleries in GreatBritain3 and while few have the range and diversity ofobjects held by the British Museum, the problems they facein accounting for heritage assets are similar in kind, if not inscale.

4 Heritage assets are assets with historic, artistic, scientific,technological, geophysical or environmental qualities thatare held and maintained principally for their contribution toknowledge and culture and this purpose is central to theobjectives of the entity holding them. As well as museumcollections such as those of art, antiquities and books theterm ‘heritage assets’ includes assets such as landscape andcoastline, historic buildings and archaeological sites.

3

Preface

Why the Board is issuing the Discussion Paper now

5 Financial Reporting Standard (FRS) 15 ‘Tangible fixedassets’$ requires all tangible fixed assets to be capitalised inthe balance sheet; in principle this includes heritage assets.The Statement of Recommended Practice{ for Charitiesissued in October 2000 reflected the requirements ofFRS 15 but continued to allow heritage assets acquired inprevious periods to be exempted from capitalisation on cost-benefit grounds. However, recent additions of heritageassets, where adequate purchase information is availablewithout significant additional cost, are required to becapitalised. Similar requirements apply to centralgovernment entities.

6 A number of entities in the museum and galleries sector doreport values for their total holding of heritage assets in theirprimary financial statements.

7 However, many entities only began to capitalise heritageassets acquired in 2001 and later years. This gives rise to anumber of problems. The accounting treatment isdetermined with reference to when a heritage asset wasacquired, rather than its inherent features and so verydifferent accounting treatments may be applied to similarassets: the balance sheet value will reflect an item acquired in2004, but not an asset acquired in 1994. Perhaps of mostconcern is that the balance sheets of museums and galleriesdo not include their most significant assets. The volume ofacquisitions by museums and galleries is often quite smalland only a fraction of heritage assets held by these entities isreflected in the balance sheet even after many years.Capitalisation of acquisitions may give rise to significant

$

FRS 15 was issued in February 1999 and became effective for accounting periods ending on or after 23

March 2000.{ SORPs are recommendations on accounting practices for specialised sectors in the UK issued by sectoral

bodies recognised by the ASB.

4

Accounting Standards Board january 2006 discussion paper

amounts in the balance sheet yet these are unlikely to berepresentative of the total value of heritage assets held.

8 Some entities aim to compensate for this by providingsupplementary disclosures although the quality of these isuneven, with significant differences in the informationprovided by different entities, which impairs its usefulness.

9 The Financial Reporting Advisory Board$ (FRAB) hasreported its concerns over the existing accounting treatmentapplied by charities and public sector bodies including thenational museums and galleries, citing the problems notedabove. The FRAB recommended that application of theapproach in the charity and public sectors should bemonitored carefully and asked the ASB to review itsimpact once accounts had been prepared under the newrequirements4.

10 It is therefore appropriate to consult on issues concerningthe current accounting and reporting requirements forheritage assets in the UK, to determine whether a change tothese requirements is desirable and if so, to developalternative approaches.

Main features of the Discussion Paper

11 The proposals set out in this Discussion Paper have beendeveloped taking as the starting point the guidance set out inthe Board’s ‘Statement of Principles for financialReporting’{, and the proposals set out in the ExposureDraft for its proposed interpretation for public-benefitentities{. It is clear that the best financial informationreported by entities that hold heritage assets is secured where

$

The FRAB is an independent statutory body which advises the Treasury and devolved administrations in

the UK on financial reporting principles and standards applicable to government departments, executive

agencies, executive non-departmental public bodies, trading funds and health bodies.{ Statement of Principles for Financial Reporting. Accounting Standards Board, December 1999.{ Statement of Principles for Financial Reporting – proposed interpretation for public-benefit entities. ASB

Exposure Draft, August 2005.

5

Preface

all heritage assets are reported as assets, at values that provideuseful and relevant information at the balance sheet date.

12 It is also clear that these principles must be implementedwith due regard to the practical difficulties of preparingmeaningful financial statements for entities that hold heritageassets. The proposals set out in this Discussion Paper areintended to be practical for entities responsible for thecustody of heritage assets.

13 The objective of the Discussion Paper’s proposals is toimprove the quality of financial reporting of heritage assets.Whilst it is clear that the best financial reporting requiresheritage assets to be reported as assets at current value, it issimply not practicable for many entities to implement thispolicy. Current accounting standards attempt to resolve thisissue by requiring only recently acquired heritage assets to bereported as such: but this is at the cost of internal consistencywithin the financial statements of a single entity. TheDiscussion Paper proposes that an entity should adopt apolicy of recognising heritage assets where it is reasonablypracticable but that, where it is clear that practicalconsiderations prevent this a ‘non-capitalisation’ approachshould be adopted. Specifically, a capitalisation approachis to be required where it is practicable to obtainvaluations which, when supplemented withappropriate disclosures, provide useful and relevantinformation sufficient to assist in an assessment of thevalue of heritage assets held by an entity. Where thiscannot be achieved, entities would be required to providerelevant disclosures (including the reasons why valuation isnot practicable) and consistently apply a policy of reportingtransactions in heritage assets in a way that does not distortthe reported financial performance.

14 Museums and galleries that currently recognise and capitaliseheritage assets in the balance sheet at valuation wouldcontinue to do so. Those that do not will need to considerwhether it is practicable for them to do so in light of the newrequirements.

6

Accounting Standards Board january 2006 discussion paper

15 A summary of the proposals is set out on pages 9 to 12 of theDiscussion Paper.

Questions for respondents

16 The Board is requesting comments by 31 May 2006. TheBoard would welcome responses not only from its UK andIrish constituents, but also from those based in otherjurisdictions facing similar issues in the financial reporting ofheritage assets.

17 Comments are invited on any aspect of the DiscussionPaper, but would be particularly welcome on the followingissues:

(a) Do you agree with the definition of heritage assetsproposed for financial reporting purposes? If not, whatdefinition would you propose? (paragraph 1.16)

(b) The Discussion Paper proposes that where heritage assetsare reported in the balance sheet this should be at acurrent value rather than at historical cost as thisprovides more useful and relevant information. Doyou agree? If not, please give reasons. (paragraph 3.16)

(c) The objective of the proposals is to improve the qualityof financial reporting of heritage assets. Do you agreethat, to meet this objective, it is impractical to require allentities to adopt a capitalisation approach for thefinancial reporting of heritage assets? (paragraph 3.18)

(d) Do you consider the proposals in paragraphs 4.8 and 4.9will encourage the adoption of a capitalisation approachin appropriate cases? If not, what modifications toexisting reporting requirements would you propose?

(e) Where it is clear that practical considerations prevent anentity adopting a policy of recognising heritage assets anon-capitalisation approach should be adopted. Do youagree that, in reaching this decision, an entity should

7

Preface

have regard to whether it can obtain—at a reasonablecost—reliable valuations on an ongoing basis for themajority, by value, of heritage assets held and that thisshould be explained clearly in the notes to the accounts?If you do not agree, how should an entity support itsdecision to adopt a non-capitalisation approach?(paragraphs 4.12 and 4.13)

(f) Under a non-capitalisation approach, it is proposed thatacquisitions and disposals of heritage assets should bepresented outside of the income and expenditureaccount in a statement of change in recognised netassets. Do you support this proposal? If not, how shouldthese transactions be reported? (paragraphs 4.15 and 4.16)

(g) Do you consider that it is appropriate to report othertransactions related specifically to heritage assets—suchas donations, grants for their acquisition and restorationcosts—in a statement of change in recognised net assets?If not, how should these transactions be reported?(paragraph 4.18 and Appendix 3)

(h) Do you agree with the proposed disclosure requirementsfor heritage assets? Are there other disclosures that arepracticable and would provide useful information?(paragraphs 5.6 to 5.17)

(i) It is proposed that, for financial reporting purposes,historic assets used by the entity itself and corporate artare not heritage assets. Is it appropriate at this stage toclarify the accounting treatment of these assets? If so, doyou agree with the proposals in Sections 6 and 7 of theDiscussion Paper?

18 The Discussion Paper has been prepared by the Board’sCommittee on Accounting for Public-benefit Entities incollaboration with the International Public SectorAccounting Standards Board. The input from CAPE andmembers, technical advisors and staff of IPSASB is gratefullyacknowledged.

8

Accounting Standards Board january 2006 discussion paper

SUMMARY OF PROPOSALS

1 The Discussion Paper proposes to replace the existingmixed capitalisation accounting treatment for heritageassets with approaches that are intended to be practical toapply by entities responsible for the custody of heritageassets and to improve the quality of their financialreporting. The proposals take as the starting pointguidance set out in the Board’s ‘Statement of Principlesfor Financial Reporting’ and the proposals set out in theExposure Draft of the Statement’s interpretation forpublic-benefit entities.

Objective

2 The objective of the proposals is to improve the qualityof financial reporting of heritage assets. Heritage assetsshould be reported as assets at values that provide usefuland relevant information at the balance sheet date. Acapitalisation approach is to be required where it ispracticable to obtain valuations which, whensupplemented with appropriate disclosures, provideuseful and relevant information sufficient to assist in anassessment of the value of heritage assets held by anentity. Where this cannot be achieved, an entity wouldbe required to provide relevant disclosures (including thereasons why valuation is not practicable) and consistentlyapply a policy of reporting transactions in heritage assetsin a way that does not distort the reported financialperformance.

Capitalisation approach

3 Where an entity can obtain at reasonable cost reliablecurrent values for the majority, by value, of heritageassets held these values should be reported in the balancesheet. To support this approach, some modifications toexisting accounting requirements are proposed forheritage assets such as wider use of internal valuations

9

Summary of proposals

SUMMARY OF PROPOSALS continued

and indices based on reference guides or recenttransactions and extended intervals between revaluations.

4 Consistent with the requirement to provide useful andrelevant information at the balance sheet date,measurement at a notional value would not bepermitted. And historical cost would not be permitted(except where it provides a good proxy for currentvalue) since many heritage assets were acquired sometime in the past so that historical cost becomesincreasingly less relevant. Information on historical costmay have been lost over time or will not be availablewhere heritage assets were acquired through donation.

Non-capitalisation approach

5 However, if an entity can demonstrate that it cannotobtain reliable values at reasonable cost for the majority,by value, of its heritage assets then consistent with theobjective to adopt a consistent and transparentaccounting treatment, values should not be reported inthe balance sheet. Additional disclosures should be givento provide useful and relevant information about theheritage assets held by an entity.

6 The acquisition and disposal of heritage assets should beclearly reported and in a way that does not distortfinancial performance. To achieve this, a separatestatement is proposed to reconcile total gains and losseswith the change in recognised net assets taking accountof heritage asset acquisitions and disposals.

7 The Discussion Paper also considers, tentatively,whether related transactions such as donations andgrants to acquire heritage assets and the costs of theirmajor restoration should also be reported separately insuch a statement.

10

Accounting Standards Board january 2006 discussion paper

SUMMARY OF PROPOSALS continued

Disclosures

8 In the notes to the financial statements it is proposed thatentities disclose which accounting treatment has beenfollowed with supporting reasons; details of majoracquisitions in the period together with sources offunding; and, a five year financial summary of activity(including acquisitions and disposals of heritage assets). Itis also proposed that disclosures should be made aboutthe nature and scale of heritage assets held and policiesfor their preservation. Entities may wish to providedetailed information for some of these disclosures inaccompanying information such as the Operating andFinancial Review or Trustees’ Annual Report and it maybe appropriate to refer in the notes to the financialstatements to this more detailed accompanyinginformation.

Definition

9 Heritage assets meet the definition of an asset as theyembody service potential as well as or instead of cashflows. The following definition is proposed to clarify thescope of the proposals in the Discussion Paper:

‘‘An asset with historic, artistic, scientific, technological,geophysical or environmental qualities that is held andmaintained principally for its contribution to knowledge andculture and this purpose is central to the objectives of the entityholding it.’’

10 It follows that, for example, an historic building used bythe entity itself would not meet the definition as it is heldfor purposes other than a contribution to knowledge andculture. And works of art held by a profit-orientedcompany would fall outside of the definition as thecompany’s primary objective is to make a profit rather

11

Summary of proposals

SUMMARY OF PROPOSALS continued

than a contribution to knowledge and culture. Theseassets should be accounted for under existing reportingrequirements for tangible fixed assets.

12

Accounting Standards Board january 2006 discussion paper

S E C T I O N 1 :W H A T A R E H E R I T A G E A S S E T S ?

1.1 This section examines whether heritage assets are indeedassets from an accounting perspective and so should, at leastconceptually, be reported in the balance sheet. It thenexamines the specific issue of assets that are ‘inalienable’.Finally, it proposes a definition for heritage assets.

Heritage assets meet the definition of an asset

1.2 The ASB’s Statement of Principles defines assets as ‘‘rights orother access to future economic benefits controlled by anentity as a result of past transactions or events’’5. TheStatement notes that future economic benefits usuallyeventually result in net cash inflows to the entity. Manyheritage assets held by entities do not provide cash inflowsfor the entity and it is argued by some that for this reasonthey should not be regarded as assets. This issue isparticularly acute for assets that are ‘inalienable’ (seeparagraphs 1.5 to 1.8).

1.3 Yet heritage assets are central to the purpose of an entitysuch as a museum or gallery: without them the entity couldnot function. An artefact held by a museum might berealisable for cash, it might generate income indirectlythrough admission charges or the exploitation ofreproduction rights. However, and in most cases muchmore importantly, the museum needs the artefact tofunction as a museum. The artefact has utility: it can bedisplayed to provide an educational or cultural experience tothe public or it can be preserved for future display or foracademic or scientific research. The future economicbenefits associated with the artefact are primarily in theform of its service potential rather than cash flows6.Therefore, a heritage asset meets the definition of an assetnoted in paragraph 1.2 above.

13

Section 1: What are heritage assets?

1.4 Accounting standards-setting bodies in other jurisdictionswhich have considered this issue also conclude, in general,that heritage assets meet the definition of an asset.

Inalienability

1.5 Heritage assets are often described as ‘inalienable’ ie theentity cannot dispose of them without external consent.Such a restriction may, for example, be imposed by trustlaw, arise from the charity’s governing documents or insome cases by statute. The key feature of inalienability is thatit prevents an asset being readily realisable. Some argue thatinalienable assets held in trust are not assets of the entity,equating the inability to sell such items with forgoing theeconomic benefit inherent in them. But assets that areinalienable may well have utility to the entity and therefore,as noted in paragraph 1.3 above, meet the definition of anasset.

1.6 A charitable entity might acquire an office building, throughdonation, which the donor has specified is for the charity’sown use and therefore cannot be sold. In substance thecharity has acquired the rights to future economic benefits(embodied as the service potential of officeaccommodation). Few would dispute that such a buildingshould be reported as an asset even if it is inalienable. Thisreasoning should apply similarly to heritage assets.

1.7 Inalienability is not a robust concept—it is possible that adonor’s wishes may be revoked and even statutoryrestrictions are not immutable from amendment orrevocation by Parliament. Some assets are so central to thepurpose of an entity it is inconceivable they would ever besold, so in substance they are inalienable, yet this should notprevent their recognition in the balance sheet.

1.8 Inalienability should not therefore be regarded as an absolutebarrier to the recognition of heritage assets7. Other factorssuch as their utility, their contribution to the entity’sobjectives and the reliability of their measurement would

14

Accounting Standards Board january 2006 discussion paper

appear to be significant factors in determining theaccounting treatment. However the restrictions over theiruse means that it is appropriate to distinguish inalienableassets from other assets in the balance sheet.

Examples of heritage assets

1.9 The following examples illustrate the range of items typicallyregarded as heritage assets:

(a) Works of art, antiquities or other exhibits such asbiological and mineral specimens or technologicalartefacts, typically held in collections by museums andgalleries. Their heritage value may arise from theirprovenance or their particular association with historicalor cultural events. Some of these objects may bedisplayed to the public, whilst access to others may berestricted to those who need it for research purposes;

(b) Collections of rare books, manuscripts and otherreference material held by libraries and preserved fortheir historical and cultural value as a reference source;

(c) Historic monuments such as standing stones and burialmounds;

(d) Historic buildings reflecting unique architecturalcharacteristics or which have significant historicalassociations. They may not necessarily be old; somemodern buildings are regarded as worthy ofpreservation; and

(e) Elements of the natural landscape and coastline.Typically these might include distinct geological andphysiographical formations and discrete geographicalareas encompassing the habitats of threatened species ofanimals or plants. They are preserved for scientific,cultural or environmental reasons.

15

Section 1: What are heritage assets?

1.10 In considering these examples, a common definingcharacteristic of heritage assets is that they are held andmaintained for public-benefit purposes such as thecontribution to knowledge and culture.

A definition for heritage assets

Existing definitions

1.11 UK accounting standards do not provide a specific definitionof heritage assets. FRS 15 ‘Tangible fixed assets’ refers toinalienable, historic and similar assets of particular historic,scientific or artistic importance. In the UK charity sector,the requirements of FRS 15 are supplemented by aStatement of Recommended Practice, the CharitiesSORP$ which defines heritage assets as:

‘‘...assets of historical, artistic or scientific importance thatare held to advance preservation, conservation andeducational objectives of charities and through publicaccess contribute to the national culture and educationeither at a national or local level. Such assets are central tothe achievement of the purposes of such charities andinclude the land, buildings, structures, collections,exhibits or artefacts that are preserved or conserved andare central to the educational objectives of such charities.’’

1.12 The United Nations Educational Scientific and CulturalOrganisation has developed definitions of ‘cultural heritage’(monuments, groups of buildings and archaeological sites)and ‘natural heritage’ (natural features consisting of physical,biological, geological and physiographical formations andsites). These objects, sites and natural features are ofoutstanding universal value from the point of view ofhistory, art, science, aesthetics, ethnology, anthropology,conservation or natural beauty. These definitions are

$

The Charities SORP 2005 sets out recommendations on accounting practices for charities in the UK. It is

issued by the Charity Commission.

16

Accounting Standards Board january 2006 discussion paper

reflected in a number of jurisdictions’ accounting standards,which are summarised in Appendix 1.

1.13 Many of these pronouncements also reflect characteristicsdisplayed by heritage assets. For example:

(a) they are protected, kept unencumbered, cared for andpreserved;

(b) they are rarely held for their ability to generate cashinflows or sale proceeds, and there may be legal or socialobstacles to using them for such purposes;

(c) they are often irreplaceable and their value may increaseover time even if their physical condition deteriorates;and

(d) it may be difficult to estimate their useful lives, which insome cases could be several hundred years..

1.14 However, while these characteristics are often displayed byheritage assets, they are not unique to them and so cannot beconsidered as defining characteristics.

Proposed definition

1.15 A heritage asset meets the definition of an asset as it canembody service potential as well as or instead of cash flows.Covenants on its use and restrictions on its disposal do not inthemselves determine whether an asset is a heritage assetalthough these factors may impact on how such an asset isreported in the financial statements.

17

Section 1: What are heritage assets?

1.16 Given the absence of a formal definition of a heritage assetfrom existing UK accounting standards, and in light of theexamples considered above, the following definition isproposed:

An asset with historic, artistic, scientific, technological,geophysical or environmental qualities that is held andmaintained principally for its contribution to knowledge andculture and this purpose is central to the objectives of the entityholding it.

1.17 As well as museum collections the definition includes assetssuch as landscape and coastline, historic buildings andarchaeological sites.

1.18 Entities may hold assets that might be regarded as heritageassets but the assets do not meet the definition proposedabove. For example, a university may use an historicbuilding to house teaching facilities – this rather thanheritage is the building’s principal purpose. A profit-oriented company may own works of art which it holdsfor decorative purposes but contribution to knowledge andculture is not central to its primary objective which is tomake a profit. The accounting treatments of these examplesare considered in sections 6 and 7 of the Discussion Paper.

18

Accounting Standards Board january 2006 discussion paper

S E C T I O N 2 :W H A T S H O U L D A C C O U N T I N G T R Y T O D O ?

2.1 The ASB’s Statement of Principles states that the objectiveof financial statements is to provide information about thereporting entity’s financial performance and financialposition that is useful to a wide range of users for assessingthe stewardship of the entity’s management and for makingeconomic decisions8. This section draws on the Statement’sconsideration of the qualities of financial information thatmake it useful in order to determine the requirements thatare desirable for the financial reporting of heritage assets.

2.2 In the UK, heritage assets are held by public-benefitentities$. Rather than investors, the defining class of userof the financial statements of public-benefit entities is thefunders and financial supporters9. A financial supporter issomeone such as an individual or ‘friends’ group makingdonations to assist with the purchase of heritage assets. Afunder is someone such as a taxpayer. Financial supportersand indeed funders will be interested in financialinformation that helps them to assess how effectivelymanagement has fulfilled its stewardship role and used theresources at its disposal.

Financial information should be relevant and reliable

2.3 Financial information should be timely and sufficient toinfluence users’ economic decisions and their assessment ofmanagement’s stewardship. The nature and level ofacquisitions and disposals of heritage assets, and associatedmonetary values, particularly if these are linked to specificdonations or grants, are important to determine how the

$

Reporting entities whose primary objective is to provide goods or services for the general public or social

benefit and where any risk capital has been provided with a view to supporting that primary objective rather

than with a view to a financial return to equity shareholders.

19

Section 2: What should accounting try to do?

entity has used the resources available to it and assess theextent to which the entity relies on external funding.

2.4 It is concerning that, under current reporting requirements,the balance sheets of many museums and galleries do notcurrently include their most significant assets. In such cases itis unclear how the financial information is sufficient toinfluence users’ economic decisions and their assessment ofmanagement’s stewardship. Therefore, the financialinformation provided should give a complete and faithfulrepresentation of an entity’s holdings of heritage assets. If thisis not the case supplementary disclosures should be given tocomplete the picture. This is considered further inparagraphs 2.10 to 2.12.

Financial information should be comparable

2.5 Information is more useful if it can be compared with similarinformation about the entity for some other period or pointin time. The same accounting treatment should be appliedto heritage assets with similar characteristics from oneaccounting period to the next. The notes to the financialstatements should state clearly the accounting treatmentapplied to heritage asset balances and transactions.

2.6 Information is also more useful if it can be compared withsimilar information about other entities to evaluate theirrelative financial performance and position. For example, itmight be expected that art collections are reported in asimilar way in different galleries’ financial statements.

2.7 But if an entity itself accounts for similar assets in differentways this will limit both internal and external comparabilityand provide less useful information. Therefore consistencywithin an entity should be paramount in financial reportingrequirements. Inconsistent treatment should be theexception and, where it arises, sufficient disclosure shouldbe given to enable the user to understand why and its impacton the financial statements.

20

Accounting Standards Board january 2006 discussion paper

Financial information should be understandable

2.8 Users need to be able to perceive the significance ofinformation provided by financial statements. Whetherfinancial information is understandable will depend on theway in which the effects of transactions and other events areaggregated and classified and the way in which informationis presented. An accounting treatment applied consistently toall relevant transactions will assist understandability.

2.9 Heritage assets and the acquisition and disposal of themshould be clearly distinguished from other assets andtransactions. This presentation might be supplementedwith disclosures to explain particular transactions and events.

Non-financial information is also useful

2.10 Other quantitative and qualitative information about theheritage assets (for example, the number of heritage assetsheld and management’s policies for their display) will beuseful in order to understand how they provide publicbenefit. Presentation of the information should reflect thenature of the heritage assets held and the way they aremanaged, for example, the conservation policy and thedegree to which access to them is permitted.

2.11 Preservation is an important function of entities holdingheritage assets. It therefore seems reasonable for entities toprovide information about their preservation policies. Thismay put into context any expenditure on repairs andmaintenance and explain what commitments the reportingentity has to future maintenance particularly with regard tothe level of annual funding required to meet thesecommitments.

2.12 It may be more appropriate to report non-financialinformation outside of the financial statements in theaccompanying information such as the Operating andFinancial Review or Trustees’ Annual Report.

21

Section 2: What should accounting try to do?

Conclusion

2.13 Good financial reporting of heritage assets in generalpurpose financial statements should inform funders andfinancial supporters about the nature and, where available,value of assets held; report on the stewardship of the assets bythe entity; and inform decisions about whether resources arebeing used appropriately. This will require an entity to adopta consistent and transparent accounting treatment. Proposalsconsistent with this requirement are developed in Sections 3to 5 of this Discussion Paper.

Accounting Standards Board january 2006 discussion paper

22

S E C T I O N 3 :A P P R O A C H E S T O A C C O U N T I N G F O RH E R I T A G E A S S E T S

3.1 This section reviews three possible accounting approachesfor heritage assets, in the light of the desirable reportingrequirements identified in Section 2. These approaches are:

. The existing ‘mixed’ capitalisation approach;

. A ‘full’ capitalisation approach; and

. A non-capitalisation approach.

The existing UK approach – capitalise recent acquisitionsat cost

3.2 FRS 15 ‘Tangible fixed assets’ requires all tangible fixedassets to be recognised and capitalised: in principle thisincludes heritage assets. However, FRS 15 recognises thatfor some heritage assets the cost of obtaining a reliablevaluation may outweigh the benefit to users, in particular inthe case of assets that had not been capitalised in the past, andsome donated heritage assets.

3.3 A number of entities in the museum and galleries sectorreport amounts for their total holding of heritage assets inthe balance sheet. However, many public-benefit entitieshave only capitalised subsequent acquisitions of heritageassets since the adoption of FRS 15 in 2001.

3.4 This approach appears to have some practical advantages inthat reliable cost information is readily available for recentpurchases and there is no requirement for retrospectivevaluation where cost information might not be available.

3.5 However, it also gives rise to some pervasive problems and itis unclear how readers of the financial statements make senseof the reported information. Specifically:

Section 3: Approaches to accounting for heritage assets

23

(a) Inconsistent treatment of similar assets: In effect two verydifferent accounting policies (capitalisation and non-capitalisation) are applied to the same class of asset$. Forexample, an entity may own two similar heritage assets,but one was acquired some time ago and is notrecognised in the balance sheet, whereas the other wasacquired recently and has been capitalised at what iseffectively the current market price. This treatment mayalso have a perverse impact on the performancestatement; if the entity sells one asset it will recognisea very different gain from that recognised on the sale ofthe other.

(b) Subsequent expenditure: Further inconsistencies arise fromthe treatment of subsequent expenditure. Suchexpenditure, for example, to restore an historicbuilding may significantly extend its life, and shouldtypically be capitalised. However, where the underlyingheritage asset has not been capitalised these costs wouldbe expensed.

(c) Incomplete information: A typically low volume ofacquisitions means that, for museums and galleries inparticular, those heritage assets that are capitalised reflectonly a small part of the total held. Over time thecapitalisation of additions may give rise to significantamounts in the balance sheet yet these are still unlikelyto be representative of the total held. Consequently,users will have to look to other sources of information toput these transactions into context.

(d) Impact on reserves: Some charities are concerned thatcapitalisation of recently acquired heritage assets leads to

$

Inconsistent accounting such as this exists elsewhere in financial reporting. Under FRS 10 ‘Goodwill and

intangible assets’, purchased goodwill should be capitalised and classified as an asset on the balance sheet but

internally generated goodwill should not. However, capitalised values for purchased goodwill will be

reviewed for impairment on a regular basis and may be depreciated. This is not usually the case for heritage

assets which have indeterminate lives and are usually not depreciated.

Accounting Standards Board january 2006 discussion paper

24

an increase in reserves and misleads readers of theaccounts, including potential donors, as to the level ofaccessible funds. However, the relative liquidity of theassets should be discernable from their presentation inthe balance sheet and disclosures in the notes to theaccounts.

A ‘full’ capitalisation approach

3.6 In principle, there are the same benefits and advantages inrecognising and valuing heritage assets as there are for othertangible fixed assets: to inform funders and financialsupporters about the value of assets held; to report onstewardship of the assets by the owner entity and to informdecisions about whether resources are being usedappropriately.

3.7 Under a capitalisation approach, heritage assets, includingthose acquired in previous accounting periods, should berecognised and capitalised in the balance sheet. This wouldensure that the accounting policy is applied consistently toall heritage assets held. Such an approach is consistent withthe Statement of Principles which requires the recognitionof an asset if there is sufficient evidence it exists and it can bemeasured at a monetary amount with sufficient certainty10.

3.8 Heritage assets might be reported at historical (transaction)cost or a current value; some jurisdictions permit the use ofnotional values. These bases of measurement have theirrelative merits and disadvantages (see box on page 26 fordiscussion). In considering these it is clear that notionalvalues will not provide useful and relevant information. Thenature of heritage assets means that historical cost is notgenerally an appropriate measurement basis for them and sothe basis of measurement under a capitalisation approachshould be a current value based on market values.

Section 3: Approaches to accounting for heritage assets

25

Historical cost

A heritage asset being measured using the historicalcost basis is recognised at transaction cost. Thisinformation is straightforward to ascertain for recentacquisitions and readily understandable. However,heritage assets tend to have indeterminate lives andconsequently no further accounting adjustment fordepreciation or impairment is made to the initialcarrying value. Also, many heritage assets wereacquired some time in the past; the passage of timeand the subsequent changes in market values—wherethey exist and which can be unpredictable—mean thata reported historical cost is often not a useful guide totheir value. Over time the historical cost will provideinformation that becomes less useful and relevant.

Information on cost may not be available. It may havebeen lost over time or, as is often the case, heritageassets are acquired by donation. In these circumstances,under existing requirements, a current value should bedetermined as the deemed cost11.

Current value

A current value is determined by reference to amarket-based value. Many heritage assets are extremelyvaluable and, from a stewardship perspective, it isdesirable that the balance sheet should reflect this. Insubsequent reporting periods re-measurement takesplace to ensure that assets are reported at an up-to-datecurrent value. This provides relevant informationabout heritage assets at the balance sheet date unlikehistorical cost.

However, there are many practical difficultiesassociated with determining a current value forheritage assets. These are considered further inSection 4.

Accounting Standards Board january 2006 discussion paper

26

Notional value

Some take the view that it is preferable that the balancesheet should report a value however unreliable ratherthan no value, for stewardship purposes. Whilstnotional values may be relatively easy to determine itis questionable whether they provide useful andrelevant information to assist in an assessment of thevalue of heritage assets held. They may indeed bemisleading even if their limitations can be clearlyexplained and it would be preferable instead to reportno value in the balance sheet.

A non-capitalisation approach

3.9 Under a non-capitalisation approach entities would not bepermitted to capitalise heritage assets acquired in the past orduring the current reporting period. This would ensure thatan accounting policy is applied consistently to all heritageassets. This approach would clearly be straightforward toimplement as it avoids practical problems in determiningvalues.

Acquisitions and disposals

3.10 However, in applying a non-capitalisation approach, thetreatment of acquisitions and disposals in the currentreporting period will need to be determined.

3.11 One treatment might be to record the acquisition of aheritage asset as an expense in the income and expenditureaccount. This approach is permitted in a number ofjurisdictions (see Appendix 2). However, this could beseen to misrepresent the substance of the transaction in thatan asset has been acquired and has not been consumed. Thisdistorts the level of reported expenses and does not properlyreflect financial performance. Reporting the full proceedsfrom the disposal of heritage assets as income in theperformance statement is also distorting.

Section 3: Approaches to accounting for heritage assets

27

3.12 An alternative treatment would be to present the acquisitionand disposal of heritage assets separately, outside of theincome and expenditure account, to distinguish clearly thesetransactions from other activities of the entity. This approachis similar to that required by SFAS 116 ‘Accounting forcontributions received and contributions made’$.

3.13 It is proposed that under a non-capitalisation approachacquisitions and disposals of heritage assets should bepresented separately from income and expenditure. Thiswill aid transparency of reporting and, linked to enhanceddisclosures, should provide a clearer picture of heritage assettransactions for the reporting period.

Proposals

3.14 It was concluded in Section 2 that good financial reportingof heritage assets will require an entity to adopt a consistentand transparent accounting treatment. This could beachieved by requiring all heritage assets to be recognised asassets at current value but this is simply not practicable formany entities. Alternatively, this could be achieved byprecluding the recognition of any heritage assets. But thiswould be a retrograde step for those entities which currentlyrecognise their heritage assets, and would reduce the level offinancial information available to financial supporters andfunders. However, it is clear that consistent and transparentaccounting cannot be achieved under the existing mixedcapitalisation approach.

3.15 The existing ‘mixed’ capitalisation approach that hasarisen from the application of FRS 15 shouldtherefore be replaced. The inconsistent treatment ofsimilar heritage assets in an entity’s financial statementsresults in incomplete information that is not readilyunderstandable and does not meet the requirement forgood financial reporting noted above.

$

Issued by the US Financial Accounting Standards Board and summarised in Appendix 2.

Accounting Standards Board january 2006 discussion paper

28

3.16 Heritage assets should be reported as assets at valuesthat provide useful and relevant information at thebalance sheet date. A heritage asset meets the definition ofan asset as it can embody service potential as well as orinstead of cash flows. Valuation should be at a current valuebased on market values. Historical cost will not generallyprovide information that is useful and relevant and notionalvalues will not assist in an assessment of the value of heritageassets held.

3.17 Wherever it is practicable to obtain valuations, theseshould be capitalised in the balance sheet. Whensupplemented with appropriate disclosures, these valuationsshould provide useful and relevant information sufficient toassist in an assessment of the value of heritage assets held byan entity. Information will be sufficient if valuations can beobtained for the majority, by value, of heritage assets heldand any limitations of the valuations are disclosed.

3.18 Where it is not practicable to obtain valuations, anentity should instead adopt a non-capitalisationapproach. Acquisitions and disposals should be reportedseparately from financial performance and additionaldisclosures should be given to provide useful and relevantinformation about the heritage assets held.

3.19 The practicability of obtaining valuations and otherimplementation issues arising from these proposals arediscussed in Section 4. Disclosure requirements areconsidered in Section 5.

Section 3: Approaches to accounting for heritage assets

29

S E C T I O N 4 :S O M E P R A C T I C A L C O N S I D E R A T I O N S

4.1 The objective of the proposals set out in Section 3 is toimprove the quality of financial reporting of heritage assetsby requiring an entity to adopt a consistent and transparentaccounting treatment. Heritage assets should be reported asassets at values that provide useful and relevant informationat the balance sheet date. A capitalisation approach istherefore proposed where it is practicable to obtainvaluations which, when supplemented with appropriatedisclosures, provide useful and relevant informationsufficient to assist in an assessment of the value of heritageassets held by an entity. Where this cannot be achieved, anentity should instead adopt a non-capitalisation approach.

4.2 This section considers some practical implications ofapplying these approaches.

Capitalisation approach

4.3 Under this approach, it is proposed that all heritage assets,including those acquired in previous accounting periods, arerecognised and capitalised in the balance sheet at valuation.

4.4 The capitalised values for heritage assets should bemaintained at an up-to-date current value through regularrevaluation. The existing requirements for recognising gainsand losses on revaluation in the Statement of RecognisedGains and Losses would be applied12, although these gainsand losses should be distinguished from changes arising fromthe revaluation of other assets.

Practical issues

4.5 It is proposed that heritage assets should be recognised as aseparate class of tangible fixed asset to aid presentation anddisclosure. For example, if an entity used the Companies Act

Accounting Standards Board january 2006 discussion paper

30

format 1 balance sheet , it might include a heading forheritage assets between ‘fixtures, fittings, tools andequipment’ (B,II,3) and ‘payments on account and assetsin the course of construction’ (B,II,4).

4.6 Heritage assets acquired in previous accounting periods aremeasured at a current market-based value. Acquisitions inthe current accounting period are reported at transactioncost or, where donated, at a current value in order toprovide useful and relevant information at the balance sheetdate.

4.7 Under the existing requirements of FRS 15 ‘Tangible FixedAssets’ property should be professionally revalued every fiveyears supplemented by interim valuations. Certain tangiblefixed assets other than property may instead be valued byreference to active markets or appropriate indices13. It isnoted in FRS 15 that these requirements may not beappropriate for heritage assets and alternative approachesmight be developed.

4.8 Therefore, to support the capitalisation approach andprovide useful and relevant information to assist in anassessment of the value of heritage assets held somemodifications to existing accounting requirements forrevaluation are proposed for heritage assets. For example:

(a) wider use of internal valuations and indices based onreference guides or recent transactions could bepermitted in place of formal revaluations;

(b) the interval between formal revaluations could beextended; and

(c) historical cost may be used where it is a reasonable proxyfor current value.

4.9 Valuation difficulties should not necessarily precludeapplying the capitalisation approach where a pragmatictreatment might still provide useful and relevant information

Section 4: Some practical considerations

31

sufficient to assist in an assessment of the value of heritageassets held by an entity. For example:

(a) where some individual heritage assets cannot be valuedreliably but the majority can, it would be appropriate toexplain the difficulties with valuation for such assets;

(b) the number of heritage assets to be valued should notpreclude adoption of the capitalisation approach if mostof the value of the heritage assets held by an entity restsin a small number of objects; and

(c) it may be practicable to obtain valuations for some butnot all groups or collections of heritage assets so thatmost of the value of the entity’s total holdings of heritageassets is recognised in the balance sheet$.

4.10 A museum might be able to value some groups orcollections of heritage assets that represent only a smallportion of the value of the total. Some consider that thevalues should be reported in the balance sheet. However, itwas noted in paragraph 2.7 that a consistent accountingtreatment should be paramount in financial reportingrequirements. Therefore, where limited valuationinformation is available, it should be disclosed in the notesto the accounts rather than be reported in the balance sheet.

4.11 In many cases heritage assets are held in perpetuity. They arenot ‘consumed’ in the normal sense and with preservation orregular maintenance will have long and useful lives. Forexample, a 2,000 year old Roman statue may well exist foranother 2,000 years. In most cases, therefore, a policy ofnon-deprecation is appropriate.

$

For example, a motor museum may be able to value and therefore capitalise its collection of vintage cars but

not its collection of motoring ephemera.

Accounting Standards Board january 2006 discussion paper

32

Practicability of the capitalisation approach

4.12 It is recognised that there are practical difficulties associatedwith determining a current value for heritage assets—theseare summarised in the box below. A reporting entity mightdetermine that it is not practicable to obtain valuationswhich, even if supplemented with appropriate disclosures,are sufficient to assist in an assessment of the value ofheritage assets it holds. In reaching this decision it shouldhave regard to whether:

. reliable valuations can be obtained for the majority, byvalue, of heritage assets held;

. the cost of obtaining valuations is prohibitive;

. the valuations can be kept up to date.

4.13 However, a reporting entity should explain this decisionclearly in the notes to the accounts. Where it cannot adopt acapitalisation approach a reporting entity should insteadadopt a non-capitalisation approach.

Valuation of heritage assets: some practical difficulties

Incomparable nature: Some heritage assets (such as theRosetta Stone) simply cannot be valued as there are nocomparable assets from which to determine a value.The provenance of a heritage asset (for example, thespear that killed Captain Cook) may determine itscultural (as well as monetary) value which cannot beascertained properly from like-for-like comparisons orfrom its reproduction cost as the heritage provenancecannot be recreated.

Lack of active market: Heritage assets tend to be heldindefinitely and may be rarely sold. Consequently theremay be no market reference from which to identify acurrent value. And where markets do exist they may be

Section 4: Some practical considerations

33

specialised and the volumes of transactions small, sothat prices fluctuate making it impossible to determinemeaningful trends.

Insurance values may not be available or relevant: Theincomparable nature of heritage assets which, beingunique, cannot be replaced also brings into questionthe appropriateness of insurance values. For this reasonmany entities do not generally insure heritage assets,although they may insure against accidental damagewhere items are loaned to another institution.

Large collections to be valued: Museums and galleries mayhold thousands of heritage assets. The sheer volume ofobjects precludes their valuation on cost-benefitgrounds alone. Sampling techniques may have someapplication where large collections of similar objectsare held. However, a museum collection may well notbe homogeneous in nature and the incomparablenature of heritage assets might preclude widerapplication of sample-based valuations.

Non-capitalisation approach

4.14 Under this approach it is proposed that entities are notpermitted to capitalise values for heritage assets acquired inthe past or during the current reporting period. Acquisitionsand disposals of heritage assets in the current reportingperiod should be reported separately outside of the incomeand expenditure account to distinguish them clearly fromthe financial performance of the entity.

Statement of change in recognised net assets

4.15 In order to achieve this it is proposed that a separatestatement – a statement of change in recognised net assets –is developed to present heritage asset transactions. Thestatement would reconcile reported financial performance to

Accounting Standards Board january 2006 discussion paper

34

the movement in recognised net assets by including heritageasset acquisitions and disposals.

4.16 Acquisitions would be reported in aggregate referenced tomore detailed information in the notes to the accounts. Insome circumstances heritage assets may be disposed ofthrough sale and it would be appropriate to report thesedisposal proceeds, separately from other gains, in thestatement as well. For example:

Statement of change in recognised net

assets

£000s £000s

Recognised gains/(losses) for the financial year 1,000)

Heritage asset transactions:

Proceeds from disposal of heritage assets 25

Acquisition of heritage assets (250)

Net heritage asset transactions (225)

Change in recognised net assets 775)

4.17 Charities in the UK already use a single accountingstatement (the Statement of Financial Activity or SOFA)which presents income and expenditure together with otherrecognised gains and losses and reconciles the opening andclosing net asset position. It would seem desirable, inprinciple, to distinguish heritage asset acquisitions anddisposals from other charitable activities and the format ofthe SOFA should be flexible enough to accommodate this.

Reporting related transactions

4.18 In addition to acquisitions and disposals, other transactionsare associated specifically with heritage assets includingdonations of heritage assets, cash donations and grants toacquire heritage assets and the costs of major restoration.Appendix 3 considers whether these transactions might alsobe reported in the statement of change in recognised netassets.

Section 4: Some practical considerations

35

First time adoption of proposed accounting treatments

Capitalisation approach

4.19 It is anticipated that those entities which currently capitalisevalues for their heritage assets would continue to do soproviding the approach is applied consistently to all heritageassets and the assets are capitalised at a current value.

4.20 Where heritage assets are reported at historical cost, and thecapitalisation approach is to be applied, all heritage assets willneed to be remeasured at a current value. This should bepresented as a prior period adjustment in accordance withFRS 3 ‘Reporting financial performance’.

Non-capitalisation approach

4.21 Those entities that determine that it is not practicable toapply a full capitalisation approach consistently to theirheritage assets will adopt the non-capitalisation approach.This may require the restatement of recently capitalisedacquisitions of heritage assets which should be presented asprior period adjustment in accordance with FRS 3.

Conclusion

4.22 This Section has considered some practical implications ofapplying a capitalisation and non-capitalisation approach toaccounting for heritage assets. While there are clearlydifficulties in valuing heritage assets, simplifications toexisting valuation requirements and other pragmatictreatments are proposed to support implementation of acapitalisation approach. Where valuation of heritage assets isnot practicable, an entity should have regard to specific teststo justify adoption of a non-capitalisation approach. Heritageasset acquisitions and disposals under a non-capitalisationapproach would be reported in a separate statementreconciling gains and losses to total recognised net assets.

Accounting Standards Board january 2006 discussion paper

36

S E C T I O N 5 :D I S C L O S U R E R E Q U I R E M E N T S

5.1 In considering what accounting should try to do, thedesirable requirements for the financial reporting of heritageassets identified in Section 2 were, briefly:

(a) the provision of relevant and reliable financialinformation which is readily understandable to users,prepared on a consistent basis that facilitates comparisonbetween accounting periods and between similarentities; and

(b) information that helps an assessment of the entity’sstewardship and discloses the resources ‘invested’ inheritage assets through their acquisition, maintenanceand restoration.

5.2 A feature of the proposals developed in Section 3 of theDiscussion Paper is that the capitalisation and non-capitalisation accounting approaches should besupplemented with appropriate disclosures to provideuseful and relevant information about the heritage assetsheld.

5.3 This Section proposes disclosure requirements in light ofthese considerations and the practical issues identified inSection 4 of the Discussion Paper.

Existing disclosure requirements

5.4 FRS 15 currently requires that where alternative approachesto those given in that standard are applied to the valuation ofinalienable and historic assets, adequate disclosures should begiven of the reasons for the different treatment, and of theage, scale and nature of the assets held14. The CharitiesSORP15 requires further disclosures on the use made ofheritage assets together with financial information on

Section 5: Disclosure requirements

37

acquisitions and disposals during the reporting period andaccounting policy notes explaining the charity’scapitalisation policy and measurement bases. It is generallyagreed that these requirements can be widely interpreted andcommentators within the UK sector have noted that underthese existing requirements disclosures could be improved.

5.5 The disclosure requirements for heritage assets contained inthe pronouncements of other jurisdictions are summarised inAppendix 2.

Proposals for disclosures

5.6 Unless indicated, it is proposed that the following disclosuresshould be regarded as the minimum to be provided by areporting entity irrespective of whether the capitalisation ornon-capitalisation approach has been adopted.

5.7 Some entities may provide detailed information for some ofthese disclosures in the Operating and Financial Review$ or,for charitable entities, the Trustees’ Annual Report. It maytherefore be appropriate to refer, in the notes to the financialstatements, to this more detailed accompanying information.

The nature and scale of heritage assets held

5.8 The reporting entity should provide a description of itsheritage assets and an indication of the numbers held. Thisinformation should indicate the extent to which the entityprovides access to the heritage assets. Where heritage assetsare held in collections, this information should be given inaggregate for each collection.

$

An OFR is a narrative explanation, provided in or accompanying the annual report, of the main trends

and factors underlying the development, performance and position of an entity during the period covered by

the financial statements, and those which are likely to affect the entity’s future development, performance

and position.

Accounting Standards Board january 2006 discussion paper

38

Accounting policies

5.9 The accounting policy notes should including cogentreasoning to support the classification of heritage assets assuch and state unambiguously the accounting approachapplied. If, under the capitalisation approach, valuationshave been obtained for some but not all groups of heritageassets so that most of the total value is capitalised, this shouldbe clearly stated. The valuation methodology and the policyfor depreciation should be disclosed.

5.10 Where a capitalisation approach has not been applied thisshould be clearly explained with reference to why it is notpracticable to provide an assessment of the value of heritageassets through obtaining valuations and making appropriatedisclosures.

Preservation and management policy

5.11 The reporting entity should disclose its policies for thepreservation of the heritage assets it holds. This disclosureshould include references to the aims of conservation (eg toimprove the condition of the assets or to maintain a steadystate of repair), planned programmes for major restorationand maintenance (description and estimate of expenditure)and the extent to which existing programmes have beencompleted, together with the expenditure on restorationprogrammes for the reporting period.

Acquisitions and disposals

5.12 Under either accounting approach an entity will bereporting, in summary for the current accounting period,the acquisition and disposal of heritage assets. It is proposedthat an entity should disclose details of the significant$ assetsacquired in the current reporting period and their cost orestimated value, if donated, which should reconcile to the

$

Significance might be assessed with regard to value or cultural importance.

Section 5: Disclosure requirements

39

additions figure presented in the statement of change inrecognised net assets or the relevant note to the balancesheet. An entity will need to have regard to materialityconsiderations in determining which items are separatelydisclosed. A similar approach should be adopted for heritageassets disposed of during the current reporting period. Themethod of acquisition and disposal should be brieflydescribed.

Funding sources for acquisitions

5.13 Many entities acquire heritage assets as a result of specificfunding received through grant or donation. The fundingsources for acquisitions should be disclosed in a note to theaccounts. This should reconcile to the additions figurepresented in the note to the balance sheet or the statement ofchange in recognised net assets. Funding sources may beidentified, for example, to distinguish between governmentgrants, cash donations, donated assets and utilisation ofexisting cash resources.

Five year financial summary of activity

5.14 Entities can only acquire heritage assets when they becomeavailable; entities may also be constrained by the availabilityof external funding for acquisitions. Activity in the currentreporting period may vary significantly from that in theprevious period. Some commentators have noted that insuch cases comparative information is more useful if it coversthe medium term. It is proposed that the notes to theaccounts should disclose the following financial informationfor the current reporting period and comparativeinformation for the four previous reporting periods:

(a) Acquisitions: purchases and donations of heritage assets;

(b) Proceeds from the disposal of heritage assets;

(c) Funding: grants, cash donations and other incomereceived for the acquisition of heritage assets; and

Accounting Standards Board january 2006 discussion paper

40

(d) Major restoration costs.

The five year financial summary should be supplemented byquantitative and qualitative information where this is useful,for example to interpret trends.

5.15 In this way an entity adopting a non-capitalisation approachwill disclose financial information more relevant and usefulthan that currently reported under FRS 15 which is limitedto the cumulative cost of acquisitions since 2001.

Groups of heritage assets

5.16 Where an entity manages its heritage assets in discrete groups(such as collections), the aggregate asset values for eachgroup should be disclosed in a note to the accounts. Thisshould also provide, for each group, information on balancesheet movements during the reporting period.

5.17 Where the current value of a group of heritage assets isknown, but that value is not capitalised because reliablevaluations cannot be obtained for the majority by value ofheritage assets held this value should be disclosed in a note tothe accounts.

Other useful information

5.18 Many public-benefit entities holding heritage assets,particularly those in the government sector, are requiredto report on aspects of stewardship including keyperformance indicators in their annual reports. Otherentities will have regard to any requirements orrecommendations for preparing an Operating andFinancial Review or Trustees’ Annual Report. In light ofthis, disclosures to be made specifically in accompanyinginformation are not proposed in this Discussion Paper.

Section 5: Disclosure requirements

41

Illustrative examples of disclosures

5.19 The following examples illustrate how the disclosurerequirements proposed in paragraphs 5.8 to 5.17 might beapplied in practice.

Illustrative disclosures under the capitalisation approach

The Vintage Car Museum: the museum holds a collection of vintagecars and a collection of motoring ephemera. The vintage carcollection is capitalised at market value and was acquired throughdonations and purchases. The collection of motoring ephemeraincludes manuals, brochures and advertising material. Most ofthese items were acquired over 5 years ago at nominal cost orthrough donations and there were no transactions for 2004-05. Inthese circumstances, the museum has not made extensivedisclosures about the collection of motoring ephemera.

Note 1 Accounting policies

Tangible fixed assets and depreciation

Heritage assets capitalised in the balance sheet

The Museum maintains a collection of 250 vintage andclassic cars which reflect the history of the British sports carfrom 1900-1960. Approximately 240 of these are on displaywhile the remainder are held in the Museum’s maintenancedepot undergoing or awaiting repair.

Valuation

The cars are reported in the balance sheet at current marketvalue to the extent practicable. Valuations are undertakenperiodically by professional valuers (Parker, Glass and Co).Gains and losses on revaluation are recognised in thestatement of total recognised gains and losses.

Accounting Standards Board january 2006 discussion paper

42

Acquisitions and disposals

Acquisitions are made by purchase or donation. Purchasesare funded from the Museum’s cash resources or specificappeals. The Museum occasionally disposes of objects fromthe collection in order to fund new acquisitions where theTrustees determine this does not detract from the integrity ofthe collection. Individual vehicles are occasionally donatedto the Museum and are valued by reference to the marketvalue as advised by the Museum’s valuers. Furtherinformation is given in Note 7 to the accounts.

Preservation policy

It is the Museum’s policy to maintain vehicles in thecollection in full working order and maintenance costs arecharged to the income and expenditure account whenincurred. The vehicles are deemed to have indeterminatelives and the Trustees do not therefore consider itappropriate to charge depreciation in respect of thecollection.

Heritage assets not capitalised in the balance sheet

The Museum also holds a collection of motoring ephemeraassociated with the history of the British Sports car consistingof manuals, brochures and advertising material. Thecollection is not capitalised in the balance sheet as theTrustees consider the benefit of valuing the collection doesnot justify the costs that would be incurred. Furtherinformation on the collection is given in Note 8 to theaccounts.

Section 5: Disclosure requirements

43

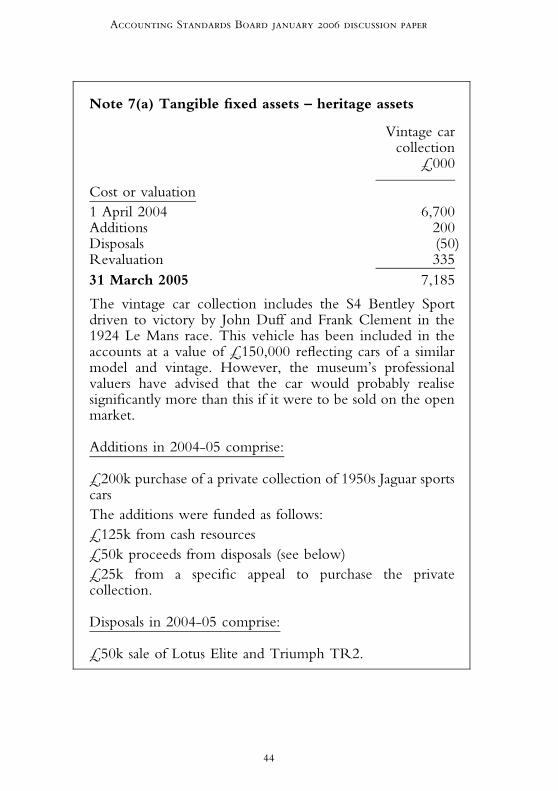

Note 7(a) Tangible fixed assets – heritage assets

Vintage carcollection

£000

Cost or valuation

1 April 2004 6,700Additions 200Disposals (50)Revaluation 335

31 March 2005 7,185

The vintage car collection includes the S4 Bentley Sportdriven to victory by John Duff and Frank Clement in the1924 Le Mans race. This vehicle has been included in theaccounts at a value of £150,000 reflecting cars of a similarmodel and vintage. However, the museum’s professionalvaluers have advised that the car would probably realisesignificantly more than this if it were to be sold on the openmarket.

Additions in 2004-05 comprise:

£200k purchase of a private collection of 1950s Jaguar sportscars

The additions were funded as follows:

£125k from cash resources

£50k proceeds from disposals (see below)

£25k from a specific appeal to purchase the privatecollection.

Disposals in 2004-05 comprise:

£50k sale of Lotus Elite and Triumph TR2.

Accounting Standards Board january 2006 discussion paper

44

Note 7(b) Five year summary of purchases and sales of

vehicles

2004-05 2003-04 2002-03 2001-02 2000-01

Additions: £000 £000 £000 £000 £000

Purchases 200 130 100 160 50Donations - 25 - - -

Total additions 200 155 100 160 50

Disposal proceeds 50 - 30 50 -

Purchases funded by:

Cash resources 125 100 100 110 30Specific appeals 25 - - - 20Disposal proceeds 50 30 - 50 -

Sub-total 200 130 100 160 50

NotesSince 2001-02 it has been the Trustees’ policy to acquire vehicles in orderto increase the diversity of the collection.

Note 8 Heritage Assets not capitalised in the balancesheet

The museum holds a collection of motoring ephemeraassociated with the history of the British Sports car. Thecollection comprises some 2,000 objects including manuals,brochures and advertising material. Objects have beenacquired in the past by purchase or through directdonation. There were no major acquisitions or disposalsduring 2004-05 (nil 2003-04).

Section 5: Disclosure requirements

45

Illustrative disclosures under the non-capitalisation approach

The Barsetshire Museum: the Museum holds a collection of heritageassets relating to the natural and man-made history of the localarea. The collection comprises three discrete classes of objects:fossils, artefacts and documents. Much of the collection wasacquired over the last 120 years through donation or purchase. It isimpractical for the Museum to value most of its objects owing tothe lack of comparable market values, the diverse nature of theobjects and the volume of items held.

Heritage asset transactions would be presented in the statement ofchange in recognised net assets as follows$:

Statement of change in recognised netassets

£000s £000s

Recognised gains/(losses) for the financial year 1,000Heritage asset transactions (Note 8):

Grants for acquisition of heritage assets 250Cash donations for acquisition of heritage assets 50

Donations of heritage assets 55Proceeds from disposal of heritage assets 10

Acquisition of heritage assets (375)Major restoration costs (50)

Net heritage asset transactions (60)

Change in recognised net assets 940

The following note disclosures would be provided in the financialstatements.

$

The illustration assumes that all heritage asset related transactions are presented in the statement of change

in recognised net assets – see Appendix 3 for discussion.

Accounting Standards Board january 2006 discussion paper

46

Note 1 Accounting policies

Heritage assets not capitalised in the balance sheet

The Museum holds collections of fossils, artefacts anddocuments of historical and scientific importance insupport of the Museum’s objective to increase knowledge,understanding and appreciation of the Barsetshire landscape.The Trustees consider that owing to the diverse nature of theassets held and the lack of market based valuationinformation for most of these as well as the size of thecollections it is not practicable to obtain valuations toprovide sufficient information to make an assessment of thevalue of the collections and so the Museum does notcapitalise the collections in the Balance Sheet.

Acquisitions

Acquisitions are presented in the Statement of Change inRecognised Net Assets as reductions in net assets when legaltitle passes to the Museum. Acquisitions are made bypurchase or donation. Purchases are recorded at cost anddonations are recorded at market value ascertained by theMuseum’s curators with reference, where possible, tocommercial markets using recent transaction informationfrom auctions.

Disposals

In exceptional circumstances, and with the approval of theTrustees, collection items may be disposed of. Proceeds fromdisposals are presented in the Statement of Change inRecognised Net Assets as increases in net assets.

Income restricted to the acquisition of heritage assets

Income from grants and cash donations received specificallyto acquire heritage assets is presented in the Statement ofChange in Recognised Net Assets when it is received.

Section 5: Disclosure requirements

47

Occasionally the Museum receives bequests which includeobjects already represented in the Museum’s collections. TheMuseum’s Trustees permit disposal of these objects throughsale to acquire objects to be added to the collections. Saleproceeds are reported in the Statement of Change inRecognised Net Assets as increases in net assets.

Unrestricted income from whatever source that issubsequently used to purchase collection items isrecognised in the income and expenditure account when itis received.

Preservation policy