Embed Size (px)

Citation preview

Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S.

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Hero Supermarket

(HERO IJ)

A new chapter for HERO

PT Hero Supermarket Tbk (HERO) is a modern retail company focusing on four types of

business: supermarket, health & beauty, hypermart, and home furnishing. Based on our

ground check at Hero Supermarket and IKEA (HERO’s home furnishing business) located

at Alam Sutera and Sarinah shopping centers, we predict that HERO’s earnings are to

improve going forward. This is on the back of 1) the improvement in shopping

experience and quality of Alam Sutera Hero Supermarket, 2) IKEA’s leading edge over its

competitors, and 3) HERO’s efficiency strategy of closing a great number of Starmart

stores.

A new story from a new supermarket

We have conducted a ground check at Hero Supermarket at Alam Sutera and Sarinah

shopping centers. We came to the conclusion that the Alam Sutera Hero Supermarket is

to be HERO’s earnings growth driver over the longer term. This is on the back of its new

renovation, which has improved the shopping experience for its customers, compared to

the Sarinah Hero Supermarket. Despite the supermarket’s premium pricing strategy, we

believe that the business is less price-sensitive predicated on the upper-middle class

customer target.

IKEA is to be a key driver for HERO

Given the higher contribution of non-food segment revenue to HERO’s 9M16 total

revenue, we also visited the IKEA outlet in Alam Sutera for mystery shopping. We believe

that the success of a retail company can be seen by the number of customers and the

products they buy. As the time struck 9.00 p.m. in the day of our ground check, we

observed long queues of customers at IKEA’s cashiers, which we believe demonstrated

the customers’ enthusiasm towards IKEA’s products. All in all, we predict IKEA to be the

growth engine for HERO’s earnings over the longer term.

As per IKEA Indonesia press release in 2015, the company successfully grabbed 2.5mn

visitors in the first year of its establishment in Indonesia. IKEA offers one-stop solution

furniture, meaning that it sells all kinds of home furniture. The fact that IKEA also

displays furniture layout designs for various rooms belonging to 25m2 - 55m2 houses in

its stores serves as IKEA’s edge over its competitors.

Efficiency strategy by closing Starmart

Starmart is HERO’s convenience store business. After 81 of its stores being closed during

the course of January-September 2016, now Starmart only has 4 stores left. Given that

12% of HERO’s 9M16 total operating expenses were comprised of rent expenses, we

consider the closing of Starmart to be a good efficiency strategy to reduce the

company’s large rent expenses. Furthermore, the competition among convenience stores

in Indonesia proves to be very tight, with the mushrooming of Alfamart and Indomaret,

their strong brand image as convenience stores, and their large number of customers.

Trade & services

Company Report

December 27, 2016

Recommendation Not rated

Target Price (12M, IDR) N/A

Share Price (12/23/16, IDR) 1,255

Expected Return N/A

Consensus OP (16F, IDRtr) N/A

EPS Growth (16F, %) N/A

P/E (16F, x) N/A

Industry P/E (16F, x) N/A

Benchmark P/E (16F, x) 16.5

Market Cap (IDRbn) 5,250.5

Shares Outstanding (mn) 4,183.6

Free Float (mn) 562.0

Institutional Ownership (%) 27.1

Beta (Adjusted, 24M) 0.9

52-Week Low (IDR) 960

52-Week High (IDR) 1,400

(%) 1M 6M 12M

Absolute 0.4 11.1 9.1

Relative 3.9 7.9 -2.0

PT. Daewoo Securities Indonesia

Andy Wibowo Gunawan

+62-21-515-1140

FY (Dec) 12/10 12/11 12/12 12/13 12/14 12/15

Revenue (IDRbn) 7,667.3 8,952.1 10,510.4 11,900.4 12,769.0 14,352.7

OP (IDRbn) 355.3 426.6 487.1 144.5 -173.5 -246.4

OP Margin (%) 4.6 4.8 4.6 1.2 -1.4 -1.7

Net Profit (IDRbn) 221.9 273.6 302.7 671.1 43.8 -144.1

EPS (IDR) 65.1 80.2 88.8 177.8 10.0 -34.0

ROE (%) 21.4 21.3 19.7 19.1 0.8 -2.7

P/E (x) 6.4 13.2 47.0 13.6 156.4 -

P/B (x) 1.2 2.6 8.6 1.9 1.8 0.9

Note: All figures are based on consolidated data; OP refers to operating profit

Source: Bloomberg, Daewoo Securities Indonesia

80

90

100

110

120

12

/15

1/1

6

2/1

6

3/1

6

4/1

6

5/1

6

6/1

6

7/1

6

8/1

6

9/1

6

10

/16

11

/16

JCI HERO(D-1yr=100)

Hero Supermarket

2

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

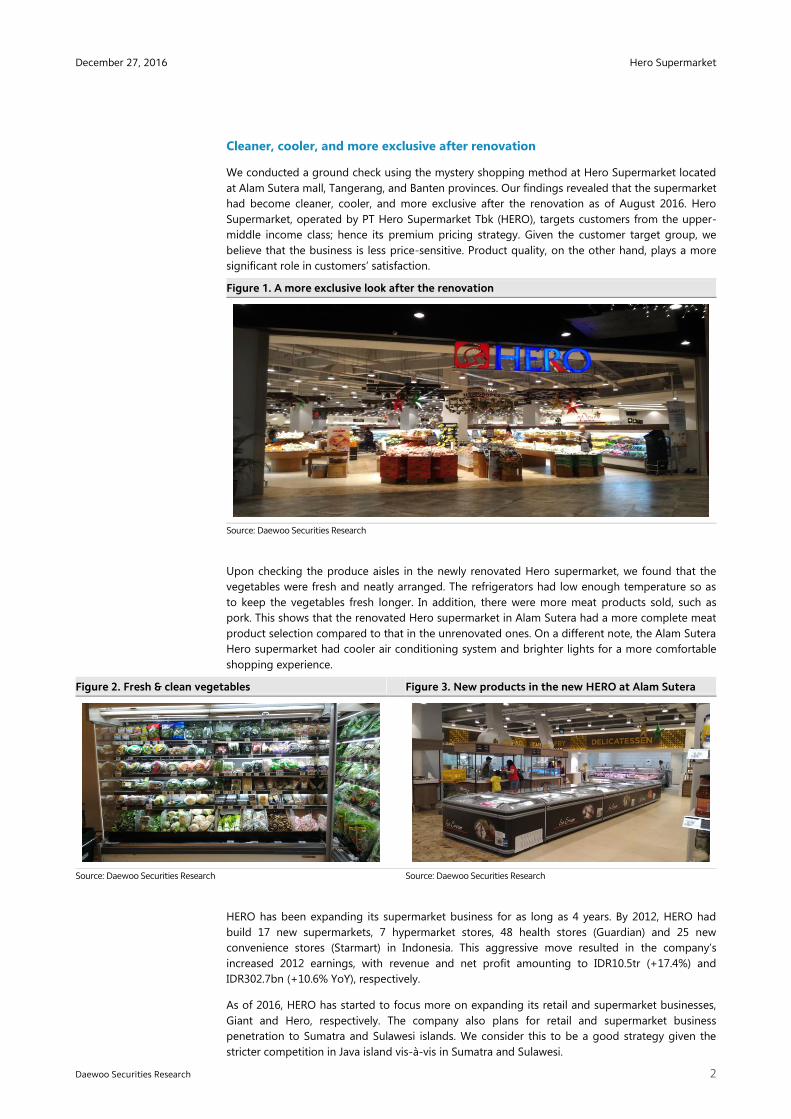

Cleaner, cooler, and more exclusive after renovation

We conducted a ground check using the mystery shopping method at Hero Supermarket located

at Alam Sutera mall, Tangerang, and Banten provinces. Our findings revealed that the supermarket

had become cleaner, cooler, and more exclusive after the renovation as of August 2016. Hero

Supermarket, operated by PT Hero Supermarket Tbk (HERO), targets customers from the upper-

middle income class; hence its premium pricing strategy. Given the customer target group, we

believe that the business is less price-sensitive. Product quality, on the other hand, plays a more

significant role in customers’ satisfaction.

Figure 1. A more exclusive look after the renovation

Source: Daewoo Securities Research

Upon checking the produce aisles in the newly renovated Hero supermarket, we found that the

vegetables were fresh and neatly arranged. The refrigerators had low enough temperature so as

to keep the vegetables fresh longer. In addition, there were more meat products sold, such as

pork. This shows that the renovated Hero supermarket in Alam Sutera had a more complete meat

product selection compared to that in the unrenovated ones. On a different note, the Alam Sutera

Hero supermarket had cooler air conditioning system and brighter lights for a more comfortable

shopping experience.

Figure 2. Fresh & clean vegetables Figure 3. New products in the new HERO at Alam Sutera

Source: Daewoo Securities Research

Source: Daewoo Securities Research

HERO has been expanding its supermarket business for as long as 4 years. By 2012, HERO had

build 17 new supermarkets, 7 hypermarket stores, 48 health stores (Guardian) and 25 new

convenience stores (Starmart) in Indonesia. This aggressive move resulted in the company’s

increased 2012 earnings, with revenue and net profit amounting to IDR10.5tr (+17.4%) and

IDR302.7bn (+10.6% YoY), respectively.

As of 2016, HERO has started to focus more on expanding its retail and supermarket businesses,

Giant and Hero, respectively. The company also plans for retail and supermarket business

penetration to Sumatra and Sulawesi islands. We consider this to be a good strategy given the

stricter competition in Java island vis-à-vis in Sumatra and Sulawesi.

Hero Supermarket

3

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

Figure 4. Revenue increased 17.4% YoY in 2012 Figure 5. also net profit increased 10.6% YoY in 2012

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

Sarinah Hero Supermarket as a comparison

As a comparison, we also conducted a ground check in the unrenovated Hero Supermarket at

Sarinah shopping center, Central Jakarta, and found several findings. Firstly, the supermarket’s

location on the lower ground floor of Sarinah shopping center is less strategic compared to the

one on the ground floor at Alam Sutera mall. Also, as we arrived at the Sarinah Hero Supermarket,

we did not see many customers at the cashiers. In addition, its store design was not as attractive

as the one in the newly renovated Hero supermarket. As per our discussion with the staff, it is still

unclear whether the supermarket at Sarinah will see a renovation in the future.

Figure 6. Less strategic location at Sarinah Figure 7. Not many shoppers in sight

Source: Daewoo Securities Research

Source: Daewoo Securities Research

As we continued our trip inside the Hero Supermarket at Sarinah, we noticed that the air

conditioning system was less cool compared to the one at Alam Sutera. The layout was also

arranged in a less neat way and packed with too many products (see Figure 9). In the fruit and

meat shelves, we saw that the fruits were less fresh (see Figure 10) and the meat product

selection was not as complete as the one at Alam Sutera Hero Supermarket (see Figure 11).

Figure 8. Air conditioner not working well Figure 9. Layout not neatly arranged

Source: Daewoo Securities Research

Source: Daewoo Securities Research

9.0

10.5

11.9

12.8

14.4

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

2011 2012 2013 2014 2015

(IDR tr)

273.6302.7

365.3

79.7

-96.6

-200.0

-100.0

0.0

100.0

200.0

300.0

400.0

2011 2012 2013 2014 2015

(IDR bn)

Hero Supermarket

4

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

Figure 10. The fruit is less fresh Figure 11. Less complete meat products

Source: Daewoo Securities Research

Source: Daewoo Securities Research

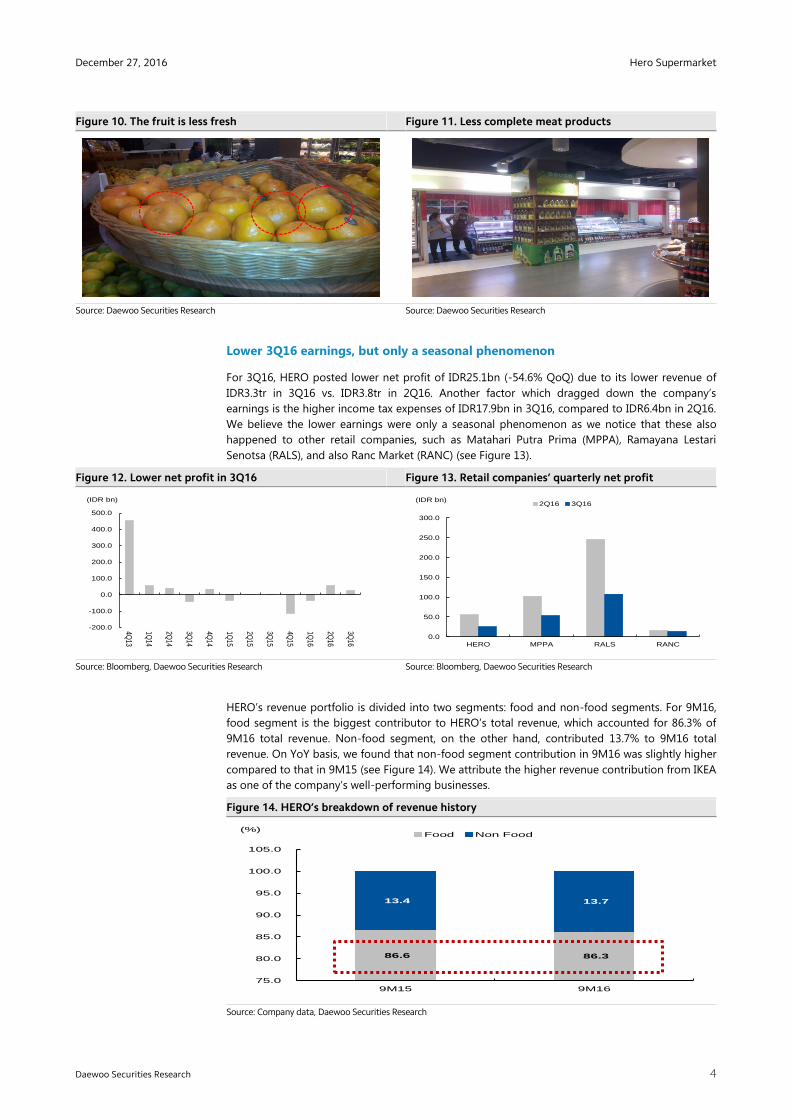

Lower 3Q16 earnings, but only a seasonal phenomenon

For 3Q16, HERO posted lower net profit of IDR25.1bn (-54.6% QoQ) due to its lower revenue of

IDR3.3tr in 3Q16 vs. IDR3.8tr in 2Q16. Another factor which dragged down the company’s

earnings is the higher income tax expenses of IDR17.9bn in 3Q16, compared to IDR6.4bn in 2Q16.

We believe the lower earnings were only a seasonal phenomenon as we notice that these also

happened to other retail companies, such as Matahari Putra Prima (MPPA), Ramayana Lestari

Senotsa (RALS), and also Ranc Market (RANC) (see Figure 13).

Figure 12. Lower net profit in 3Q16 Figure 13. Retail companies’ quarterly net profit

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

HERO’s revenue portfolio is divided into two segments: food and non-food segments. For 9M16,

food segment is the biggest contributor to HERO’s total revenue, which accounted for 86.3% of

9M16 total revenue. Non-food segment, on the other hand, contributed 13.7% to 9M16 total

revenue. On YoY basis, we found that non-food segment contribution in 9M16 was slightly higher

compared to that in 9M15 (see Figure 14). We attribute the higher revenue contribution from IKEA

as one of the company’s well-performing businesses.

Figure 14. HERO’s breakdown of revenue history

Source: Company data, Daewoo Securities Research

-200.0

-100.0

0.0

100.0

200.0

300.0

400.0

500.0

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

(IDR bn)

0.0

50.0

100.0

150.0

200.0

250.0

300.0

HERO MPPA RALS RANC

(IDR bn)2Q16 3Q16

86.6 86.3

13.4 13.7

75.0

80.0

85.0

90.0

95.0

100.0

105.0

9M15 9M16

(%)Food Non Food

Hero Supermarket

5

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

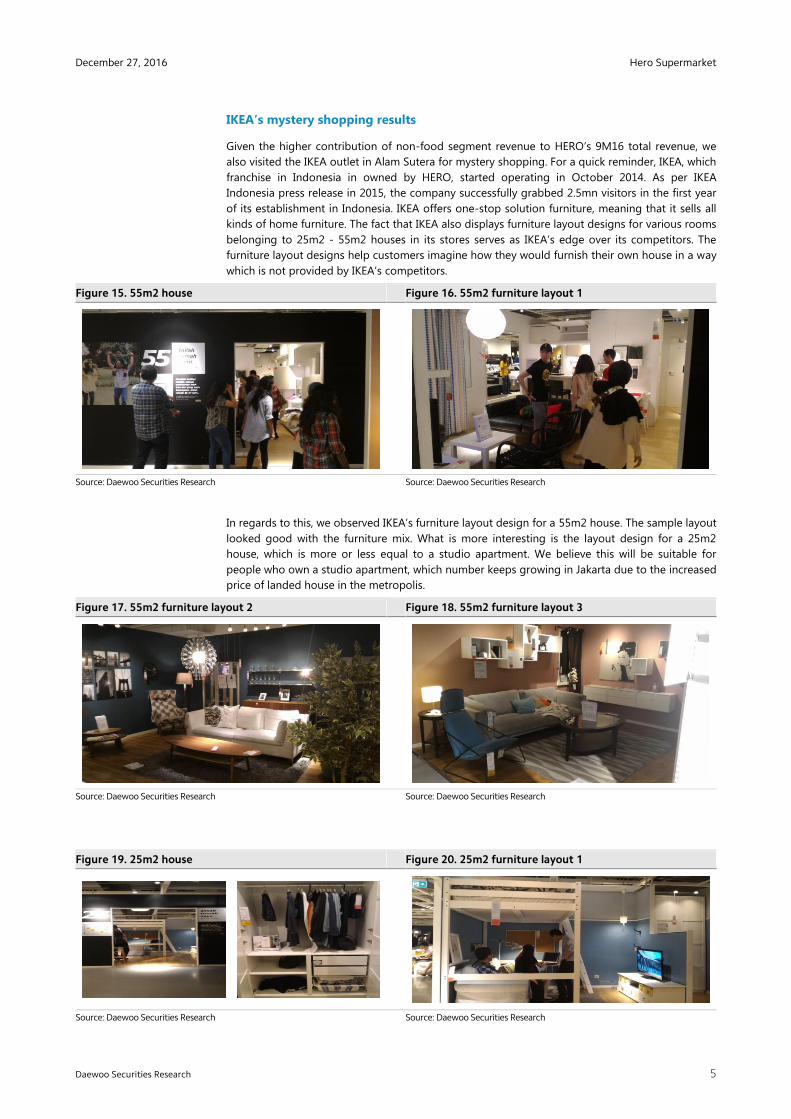

IKEA’s mystery shopping results

Given the higher contribution of non-food segment revenue to HERO’s 9M16 total revenue, we

also visited the IKEA outlet in Alam Sutera for mystery shopping. For a quick reminder, IKEA, which

franchise in Indonesia in owned by HERO, started operating in October 2014. As per IKEA

Indonesia press release in 2015, the company successfully grabbed 2.5mn visitors in the first year

of its establishment in Indonesia. IKEA offers one-stop solution furniture, meaning that it sells all

kinds of home furniture. The fact that IKEA also displays furniture layout designs for various rooms

belonging to 25m2 - 55m2 houses in its stores serves as IKEA’s edge over its competitors. The

furniture layout designs help customers imagine how they would furnish their own house in a way

which is not provided by IKEA’s competitors.

Figure 15. 55m2 house Figure 16. 55m2 furniture layout 1

Source: Daewoo Securities Research

Source: Daewoo Securities Research

In regards to this, we observed IKEA’s furniture layout design for a 55m2 house. The sample layout

looked good with the furniture mix. What is more interesting is the layout design for a 25m2

house, which is more or less equal to a studio apartment. We believe this will be suitable for

people who own a studio apartment, which number keeps growing in Jakarta due to the increased

price of landed house in the metropolis.

Figure 17. 55m2 furniture layout 2 Figure 18. 55m2 furniture layout 3

Source: Daewoo Securities Research

Source: Daewoo Securities Research

Figure 19. 25m2 house Figure 20. 25m2 furniture layout 1

Source: Daewoo Securities Research

Source: Daewoo Securities Research

Hero Supermarket

6

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

Figure 21. 25m2 layout 2 Figure 22. 25m2 layout 3

Source: Daewoo Securities Research

Source: Daewoo Securities Research

We believe that the success of a retail company can be seen by the number of customers and the

products they buy. As the time struck 9.00 p.m. in the day of our ground check, we observed long

queues at IKEA’s cashiers, which we believe demonstrated the customers’ enthusiasm towards

IKEA’s products. All in all, we predict IKEA to be the growth engine for HERO’s earnings over the

longer term.

Figure 23. Long queue at the cashier Figure 24. IKEA’s storage

Source: Daewoo Securities Research

Source: Daewoo Securities Research

Before we went to the cashier, we found several helpful kitchen appliances, such as manual mixer

which works only by turning the handle instead of using power (see Figure 25). We also saw IKEA’s

foodcourt crowded with customers having a meal after their shopping time, which can also

indicate a strong demand for IKEA’s products.

Figure 25. A helpful kithchen appliances Figure 26. IKEA’s foodcourt

Source: Daewoo Securities Research

Source: Daewoo Securities Research

All in all, we have been able to observe HERO’s performance by ground checking using

mystery shopping method, which we believe to be the best way to see a retail company’s

level of success. Based on our observation, we expect IKEA to be HERO’s success key driver over

the longer term.

Hero Supermarket

7

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

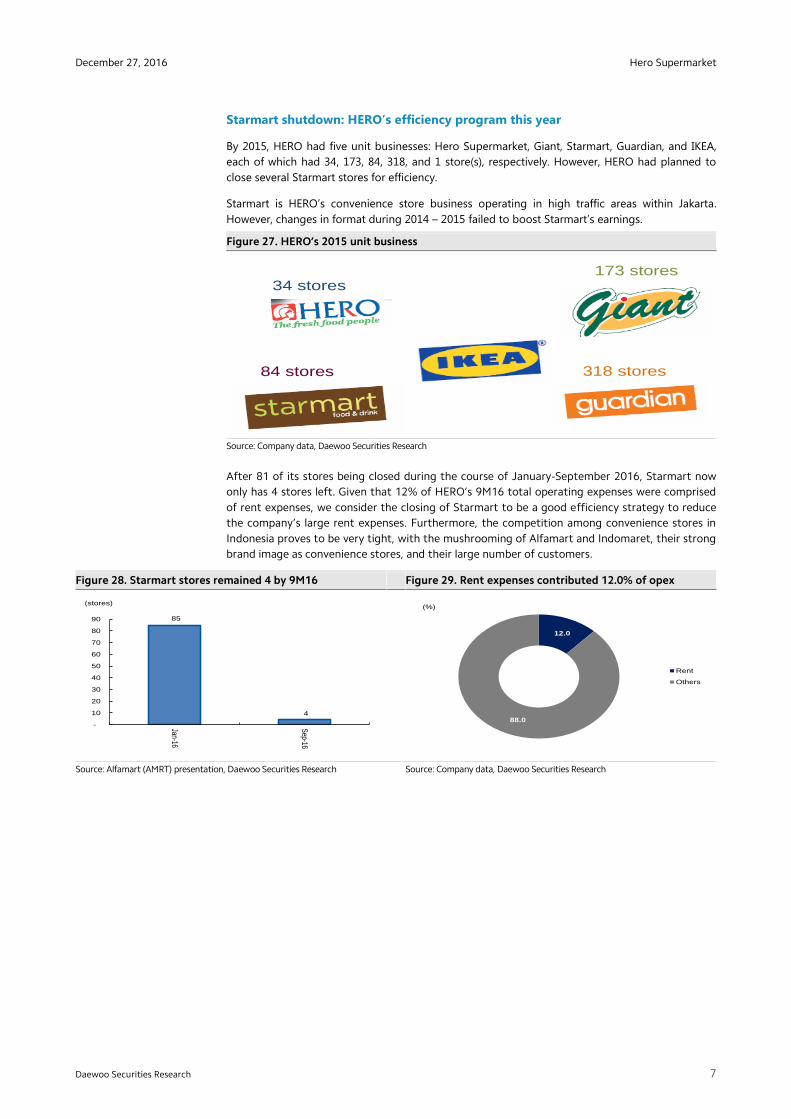

Starmart shutdown: HERO’s efficiency program this year

By 2015, HERO had five unit businesses: Hero Supermarket, Giant, Starmart, Guardian, and IKEA,

each of which had 34, 173, 84, 318, and 1 store(s), respectively. However, HERO had planned to

close several Starmart stores for efficiency.

Starmart is HERO’s convenience store business operating in high traffic areas within Jakarta.

However, changes in format during 2014 – 2015 failed to boost Starmart’s earnings.

Figure 27. HERO’s 2015 unit business

Source: Company data, Daewoo Securities Research

After 81 of its stores being closed during the course of January-September 2016, Starmart now

only has 4 stores left. Given that 12% of HERO’s 9M16 total operating expenses were comprised

of rent expenses, we consider the closing of Starmart to be a good efficiency strategy to reduce

the company’s large rent expenses. Furthermore, the competition among convenience stores in

Indonesia proves to be very tight, with the mushrooming of Alfamart and Indomaret, their strong

brand image as convenience stores, and their large number of customers.

Figure 28. Starmart stores remained 4 by 9M16 Figure 29. Rent expenses contributed 12.0% of opex

Source: Alfamart (AMRT) presentation, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

34 stores173 stores

84 stores 318 stores

85

4

-

10

20

30

40

50

60

70

80

90Jan-16

Sep-16

(stores)

12.0

88.0

Rent

Others

(%)

Hero Supermarket

8

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

APPENDIX 1

Important Disclosures & Disclaimers

Stock Ratings Industry Ratings

Buy Relative performance of 20% or greater Overweight Fundamentals are favorable or improving

Trading Buy Relative performance of 10% or greater, but with volatility Neutral Fundamentals are steady without any material changes

Hold Relative performance of -10% and 10% Underweight Fundamentals are unfavorable or worsening

Sell Relative performance of -10%

* Ratings and Target Price History (Share price (----), Target price (----), Not covered (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆))

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months.

* Although it is not part of the official ratings at Daewoo Securities, we may call a trading opportunity in case there is a technical or short-term material

development.

* The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of

future earnings.

The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic

conditions.

Analyst Certification

The research analysts who prepared this report (the “Analysts”) are registered with the Indonesian jurisdiction and are subject to Indonesian securities

regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws and regulations thereof. Opinions expressed in

this publication about the subject securities and companies accurately reflect the personal views of the Analysts primarily responsible for this report. Except

as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject companies in the past 12 months and

have not been promised the same in connection with this report. No part of the compensation of the Analysts was, is, or will be directly or indirectly related

to the specific recommendations or views contained in this report but, like all employees of PT Daewoo Securities Indonesia, the Analysts receive

compensation that is impacted by overall firm profitability, which includes revenues from, among other business units, the institutional equities, investment

banking, proprietary trading and private client division. At the time of publication of this report, the Analysts do not know or have reason to know of any

actual, material conflict of interest of the Analyst or PT Daewoo Securities Indonesia except as otherwise stated herein.

Disclaimers

This report is published by PT Daewoo Securities Indonesia (“Daewoo”), a broker-dealer registered in the Republic of Indonesia and a member of the

Indonesia Exchange. Information and opinions contained herein have been compiled from sources believed to be reliable and in good faith, but such

information has not been independently verified and Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness,

accuracy, completeness or correctness of the information and opinions contained herein or of any translation into English from the Bahasa Indonesia. If this

report is an English translation of a report prepared in the Indonesian language, the original Indonesian language report may have been made available to

investors in advance of this report. Daewoo, its affiliates and their directors, officers, employees and agents do not accept any liability for any loss arising

from the use hereof. This report is for general information purposes only and it is not and should not be construed as an offer or a solicitation of an offer to

effect transactions in any securities or other financial instruments. The intended recipients of this report are sophisticated institutional investors who have

substantial knowledge of the local business environment, its common practices, laws and accounting principles and no person whose receipt or use of this

report would violate any laws and regulations or subject Daewoo and its affiliates to registration or licensing requirements in any jurisdiction should receive

or make any use hereof. Information and opinions contained herein are subject to change without notice and no part of this document may be copied or

reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Daewoo. Daewoo, its affiliates and

their directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may make a purchase or sale,

or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or otherwise, in each case

either as principals or agents. Daewoo and its affiliates may have had, or may be expecting to enter into, business relationships with the subject companies to

provide investment banking, market-making or other financial services as are permitted under applicable laws and regulations. The price and value of the

investments referred to in this report and the income from them may go down as well as up, and investors may realize losses on any investments. Past

performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur.

Disclosures

As of the publication date, PT Daewoo Securities Indonesia, and/or its affiliates do not have any special interest with the subject company and do not own

1% or more of the subject company's shares outstanding.

Hero Supermarket

9

December 27, 2016

Daewoo Securities Research

KDB Daewoo Securities Research

Distribution

United Kingdom: This report is being distributed by Daewoo Securities (Europe) Ltd. in the United Kingdom only to (i) investment professionals falling within

Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other

persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as “Relevant

Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its

contents.

United States: This report is distributed in the U.S. by Daewoo Securities (America) Inc., a member of FINRA/SIPC, and is only intended for major institutional

investors as defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by their acceptance

thereof represent and warrant that they are a major institutional investor and have not received this report under any express or implied understanding that

they will direct commission income to Daewoo or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed

herein should contact and place orders with Daewoo Securities (America) Inc., which accepts responsibility for the contents of this report in the U.S. The

securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered or

sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements.

Hong Kong: This document has been approved for distribution in Hong Kong by Daewoo Securities (Hong Kong) Ltd., which is regulated by the Hong Kong

Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for

distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws

of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person.

All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Daewoo or

its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Daewoo and its

affiliates to any registration or licensing requirement within such jurisdiction.

Daewoo Securities International Network

PT. Daewoo Securities Indonesia Daewoo Securities Co. Ltd. (Seoul) Daewoo Securities (Hong Kong) Ltd.

Equity Tower 50th Floor

Jl.Jend Sudirman, SCBD Lot 9

Jakarta 12190

Head Office

14, Eunhaeng-ro, Yeongdeungpo-gu

Seoul 150-973

Korea

Suites 2005-2012

Two International Finance Centre

8 Finance Street, Central

Hong Kong

Tel: 62-21-515-1140 Tel: 82-2-768-3026 Tel: 85-2-2514-1304

Daewoo Securities (America) Inc. Daewoo Securities (Europe) Ltd. Daewoo Securities (Singapore) Pte. Ltd.

320 Park Avenue, 31st Floor.

New York, NY 10022

United States

41st Floor, Tower 42

25 Old Broad Street

London EC2N 1HQ

United Kingdom

Six Battery Road #11-01

Singapore, 049909

Tel: 1-212-407-1000 Tel: 44-20-7982-8000 Tel: 65-6671-9845

Tokyo Representative Office Beijing Representative Office Shanghai Representative Office

7F, Yusen Building, 2-3-2

Marunouchi, Chiyoda-ku

Tokyo 100-0005

Japan

2401A, 24th Floor. East Tower

Twin Tower, B-12 Jianguomenwai Avenue

Chaoyang District, Beijing 100022

China

Room 38T31, 38F SWFC

100 Century Avenue, Pudong New Area,

Shanghai, 200120

China

Tel: 81-3- 3211-5511 Tel: 86-10-6567-9699 Tel: 86-21-5013-6392

Ho Chi Minh Representative Office Daewoo Investment Advisory (Beijing) Co., Ltd Daewoo Securities (Mongolia) LLC

Suites 901B. Centec Tower

72-74 Nguyen Thi Minh Khai St, Ward 6

District 3, HCMC

2401B,24th Floor. East Tower

Twin Tower, B-12 Jianguomenwai Avenue

Chaoyang District, Beijing 100022

China

#406, Blue Sky Tower, Peace Avenue 17

1 Khoroo, Sukhbaatar District

Ulaanbaatar 14240

Mongolia

Tel: 84-8-3910-6000 Tel: 86-10-6567-9699 Tel: 976-7011-0807