Embed Size (px)

Citation preview

High Value Residential Properties – The New Rules

STEP – City of London

November 2012

www.blplaw.com Page 2 © Berwin Leighton Paisner

Speakers

Paul WhiteheadDDI: 020 3400 2332

Email: [email protected]

Damian BloomDDI: 020 3400 2262

Email: [email protected]

www.blplaw.com Page 3 © Berwin Leighton Paisner

Overview

1. What prompted the changes?

2. What were the changes?

3. Impact of the consultation document

4. New purchases

5. Existing structures

www.blplaw.com Page 4 © Berwin Leighton Paisner

What’s the policy point?

• 4 policies…

• SDLT avoidance

• targeted anti-avoidance (e.g. sub-sale relief)

• new rules for properties > £2m

• credibility of SDLT regime

• encourage de-enveloping

• equalise taxation of residents and non-residents?

• …

or 5?

• tackle IHT avoidance?

www.blplaw.com Page 5 © Berwin Leighton Paisner

Four FIVE new charges for £2m+ residential property

Now:

• 7% SDLT on purchases by individuals

• 15% SDLT on purchases by ‘non-natural persons’

From April 2013:

• annual charge for non-natural persons (UK and non-UK)

• CGT extended for non-resident non-natural persons

• ? CGT on disposals of indirect interests in property

www.blplaw.com Page 6 © Berwin Leighton Paisner

Who are ‘non-natural persons’?

• Companies (UK & non-UK) - so REITs, pension funds, banks

• Collective investment schemes (UK & non-UK) - so JPUTs, unittrusts, funds

• Partnerships with any of above as a partner - but partnershipscomprising people only are OK

CGT only

• Trustees / foundations (not bare trusts / nominees)

• Personal representatives

• Other property holding foreign entities

www.blplaw.com Page 7 © Berwin Leighton Paisner

Annual charge

• Valuations every 5 years, with self certification & prior agreement

• Revaluations on change of ownership

• Costs - to increase annually in line with CPI

• Tax collection:

• joint and several liability: investors, beneficial owners,shareholders, occupiers?

• impact on tenancy agreements?

• impact on beneficiaries in occupation?

• Multiple interests = multiple charges – freehold and leasehold

£2m to £5m £15,000

£5m to £10m £35,000

£10m to £20m £70,000

£20m+ £140,000

www.blplaw.com Page 8 © Berwin Leighton Paisner

Developers and investors

• Developer company excluded if:

• acquires land in course of “bona fide” property developmentbusiness;

• for sole purpose of developing and reselling land; and

• the company has carried on that business for two years beforepurchase

• Care homes, hotels, student accommodation excluded

• Possible extension of exclusions to widely held property(e.g. collective investment schemes, unit trusts)

www.blplaw.com Page 9 © Berwin Leighton Paisner

Annual charge: consultation document

• “Government aims to target the annual charge atthose circumstances where tax avoidance may be asignificant factor”

• Intended to encourage de-enveloping “therebyensuring that the onward sale of the property issubject to SDLT”

• “To what extent do you think the impact of the 15per cent SDLT charge will differ from the annualcharge? Should the Government continue with bothmeasures once the annual charge is in place?”

www.blplaw.com Page 10 © Berwin Leighton Paisner

Capital gains tax

• > £2m only

• No rebasing: “one year” to plan instead (!)

• Applies to all property regardless of use – employers

• Gain pro-rated where change of use

• Rates: CT or CGT, but unlikely to be a new rate

www.blplaw.com Page 11 © Berwin Leighton Paisner

CGT: consultation document

• “The aim of the CGT extension is to support theannual charge by creating a further deterrent toenveloping and to create more equal tax treatmentbetween UK residents and non-residents.”

• “where [non-UK resident non-natural persons]choose to de-envelope a property, a non-residentdoes not have a clear financial advantage over a UKresident”

www.blplaw.com Page 12 © Berwin Leighton Paisner

The Fifth Element: CGT on indirect property holding

• New CGT on disposal of assets where > 50% of thevalue derives from UK residential property

• Shares, interests in securities, options

• Applies to disposals of interests of any value?

• Intentional, not aspirational, unless impossible

• Why CGT on indirect interests, rather than SDLT?

www.blplaw.com Page 13 © Berwin Leighton Paisner

Reliefs and double taxation

• Principal Private Residence relief – should still beavailable, e.g. for disposals by non-resident trustees

• Interaction with existing provisions

“will be considered with the aim of avoidingunnecessary complexity and to ensure a sensibleprioritisation of charging provisions”

• Wide range of potential double charges

www.blplaw.com Page 14 © Berwin Leighton Paisner

Double taxation

OffshoreCo

Section 13TCGA

Section 13TCGA

OffshoreCo

OffshoreTrust

SETTLOR

Section 86TCGA

BENEFICIARYSection 87 TCGA

www.blplaw.com Page 15 © Berwin Leighton Paisner

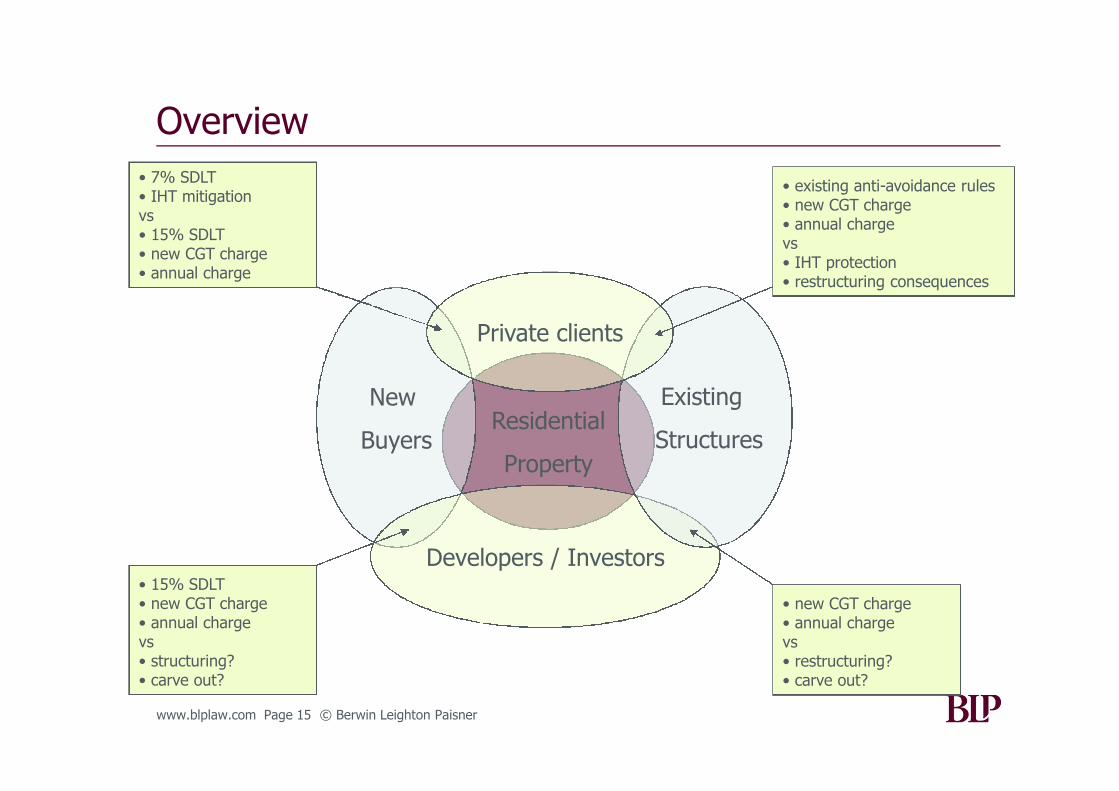

Overview

Residential

Property

New

Buyers

Developers / Investors

Existing

Structures

Private clients

• existing anti-avoidance rules• new CGT charge• annual chargevs• IHT protection• restructuring consequences

• new CGT charge• annual chargevs• restructuring?• carve out?

• 7% SDLT• IHT mitigationvs• 15% SDLT• new CGT charge• annual charge

• 15% SDLT• new CGT charge• annual chargevs• structuring?• carve out?

www.blplaw.com Page 16 © Berwin Leighton Paisner

Corporate ownership: old and new

Offshore company: old rules Offshore company: new rules

• 5% SDLT • 15% SDLT

• No CGT on disposal • CGT on disposal

• No annual charge • Annual charge

• no IHT (for non-doms) No change

• 20% tax on rental income

• confidentiality

• limited liability/asset protection

• succession

www.blplaw.com Page 17 © Berwin Leighton Paisner

Target?

OffshoreCo

Sell company

No stamp duty

www.blplaw.com Page 18 © Berwin Leighton Paisner

So what does that mean?

OffshoreCo

OffshoreTrust

OffshoreCo

OffshoreTrust

www.blplaw.com Page 19 © Berwin Leighton Paisner

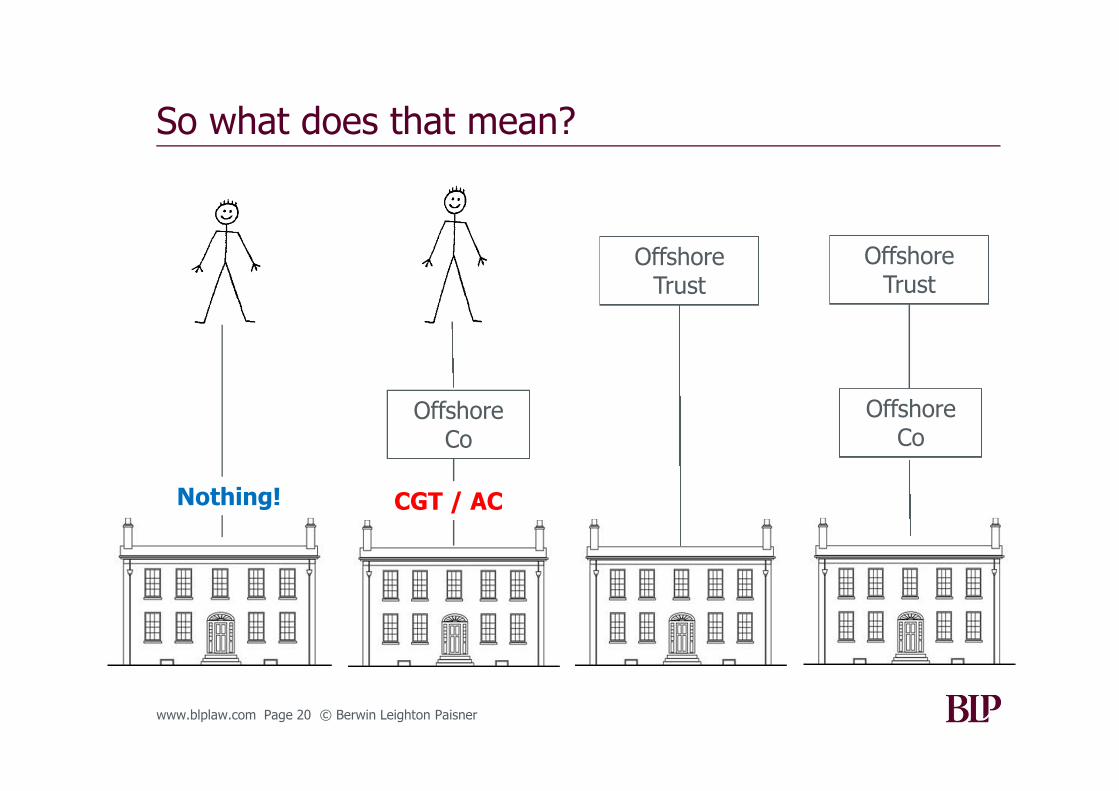

So what does that mean?

OffshoreCo

OffshoreTrust

OffshoreCo

OffshoreTrust

Nothing!

www.blplaw.com Page 20 © Berwin Leighton Paisner

So what does that mean?

OffshoreCo

OffshoreTrust

OffshoreCo

OffshoreTrust

Nothing! CGT / AC

www.blplaw.com Page 21 © Berwin Leighton Paisner

So what does that mean?

OffshoreCo

OffshoreTrust

OffshoreCo

OffshoreTrust

Nothing! CGT / AC CGT

www.blplaw.com Page 22 © Berwin Leighton Paisner

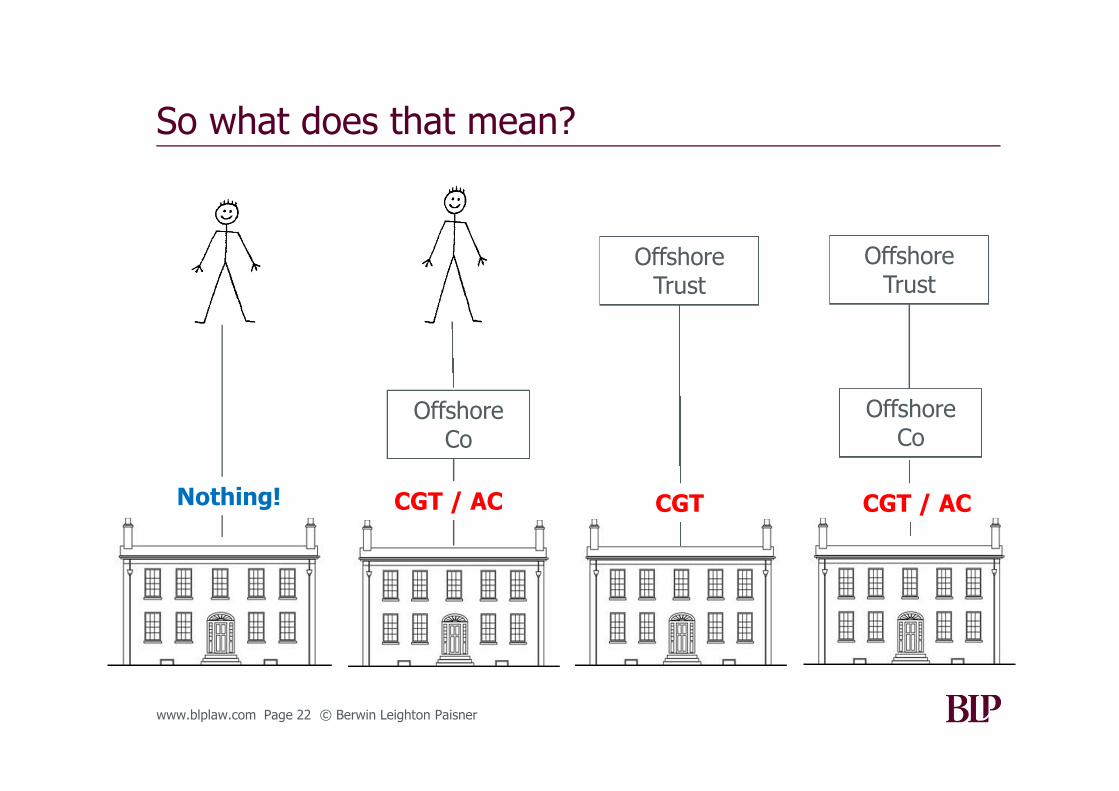

So what does that mean?

OffshoreCo

OffshoreTrust

OffshoreCo

OffshoreTrust

Nothing! CGT / AC CGT CGT / AC

www.blplaw.com Page 23 © Berwin Leighton Paisner

So what does that mean?

OffshoreCo

OffshoreTrust

OffshoreCo

OffshoreTrust

Nothing! CGT / AC CGT CGT / AC

IHT No IHT IHT No IHT

www.blplaw.com Page 24 © Berwin Leighton Paisner

The Good, the Bad & the UglyPersonal ownership (no impact)

Direct trust ownership: PPR available

Direct non-UK trust ownership: no PPR

Non-U

Kco

ow

nersh

ip

NR/ND shareholder

NR/UKD shareholder

UKR/ND shareholder

UKR/UKD shareholder

Trust

and

com

pany

ow

nersh

ip

NR/ND / dead settlor; NRND beneficiaries

NR/UKD / dead settlor; NR/UKD beneficiaries

NR/ND / dead settlor; UKR beneficiary – NR beneficiaries

NR/ND / dead settlor; UKR beneficiary – no NR beneficiaries

www.blplaw.com Page 25 © Berwin Leighton Paisner

What are the variables?

• Structural variable

• Legislative variables

• Planning variables

www.blplaw.com Page 26 © Berwin Leighton Paisner

Structural variables

high gain

low gain

single

married

young

old / ill emigratingliquid

confidentiality

no capital

accepts future tax

governance

debt

local issues

PPR

domicile

succession

residence

rental income

www.blplaw.com Page 27 © Berwin Leighton Paisner

Structural variables

high gain

low gain

single

married

young

old / ill emigratingliquid

confidentiality

no capital

accepts future tax

governance

debt

local issues

PPR

domicile

succession

residence

rental income

www.blplaw.com Page 28 © Berwin Leighton Paisner

Structural variables

high gain

low gain

single

married

young

old / ill emigratingliquid

confidentiality

no capital

accepts future tax

governance

debt

local issues

PPR

domicile

succession

residence

rental income

www.blplaw.com Page 29 © Berwin Leighton Paisner

Structural variables

high gain

low gain

single

married

young

old / ill emigratingliquid

confidentiality

no capital

accepts future tax

governance

debt

local issues

PPR

domicile

succession

residence

rental income

www.blplaw.com Page 30 © Berwin Leighton Paisner

Legislative variables

Exclude investors

Tax on disposals

of shares in property

holding companies

Effective set off

Exclude fundsCheck the box

7% SDLT

Annual charge

taxation of

non-residents

15% SDLT

Rebasing /

hold – over

New CGT provision –

defer or drop?

Restrospective

PPR

www.blplaw.com Page 31 © Berwin Leighton Paisner

Legislative variables

Exclude investors

Tax on disposals

of shares in property

holding companies

Effective set off

Exclude fundsCheck the box

7% SDLT

Annual charge

taxation of

non-residents

15% SDLT

Rebasing /

hold – over

New CGT provision –

defer or drop?

Restrospective

PPR

Planning variables

• Do nothing

• Liquidation for non-res shareholders

• Clear out gains to non-res beneficiary

• Rebase

• No magic bullet for res beneficiary occupiers

• Debt / insurance

• Partnerships

www.blplaw.com Page 32 © Berwin Leighton Paisner

www.blplaw.com Page 33 © Berwin Leighton Paisner

Existing structure: corporate ownership(UK RND shareholder)

Tax Issue

CGT CGT on disposal of property (> £2m) bycompany (post April 2013)

Corporate gain attributed to shareholder (preand post April 2013, potential double charge)

28% on disposal of shares by shareholder(subject to remittance basis)

IHT Nil

Income tax If let 20% on company and income tax onshareholder either through anti-avoidance, ordividend, with credit for 20% paid by company

Corporationtax

N/A (see 20% income tax charge above if let)

Annualcharge

£15,000 to £140,000 if property value > £2m

OffshoreCo

www.blplaw.com Page 34 © Berwin Leighton Paisner

Keep or Kill?

Non-UK Co

UK-res

Non-dom

Low (?) gain

single

old / ill

liquid (AC)

www.blplaw.com Page 35 © Berwin Leighton Paisner

Keep or Kill?

Non-UK Co

Non-res

Non-dom

high gain

married

young

limited cash

www.blplaw.com Page 36 © Berwin Leighton Paisner

Keep or Kill?

Non-UK Co

Non-res

Non-dom

low gain

single

old / ill

liquid (AC)

acceptsfuture CGT

www.blplaw.com Page 37 © Berwin Leighton Paisner

Existing structure: trust ownership (PPR available)

OffshoreTrust

Tax Issue

CGT CGT on disposal of property (> £2m) bytrustees (post April 2013)

Beneficiaries potentially chargeable to tax ontrust gains, but should be set off by PPR relief

IHT Discretionary trust: 10 yearly charge on valueof trust assets and charge on distribution

Qualifying interest in possession: charge ondeath of life tenant

In estate of settlor if settlor / spouse interested

Income tax 50% (45% from April 2013) if let

Corporationtax

N/A

AnnualCharge

N/A

www.blplaw.com Page 38 © Berwin Leighton Paisner

Existing structure: trust and corporate ownership

Tax Issue

CGT CGT on disposal of property (> £2m) bycompany (post April 2013)

On a disposal pre-April 2013, corporate gainattributed to trust and potentially chargeable onbeneficiaries / settlor

IHT Non-domiciled settlor: nil UK domiciled settlor: depends on trust

Income tax If let: 20% on company; and 50% (45% from April 2013) potentially on

settlor if UK ordinarily resident (anti-avoidance)but credit for 20% paid by company

Corporationtax

N/A (see 20% income tax charge above if let)

Annualcharge

£15,000 to £140,000 if property value > £2m

OffshoreCo

OffshoreTrust

www.blplaw.com Page 39 © Berwin Leighton Paisner

Keep or Kill?

Non-UK Co

Non-UK Trust

(non dom/dead settlor)

high gain

young / married

limited cash

non-resbeneficiaryoccupying

www.blplaw.com Page 40 © Berwin Leighton Paisner

Keep or Kill?

Non-UK Co

Non-UK Trust

(non dom/dead settlor)

high gain

Old / single

Cash resources

non-resbeneficiaryoccupying

www.blplaw.com Page 41 © Berwin Leighton Paisner

Keep or Kill?

Non-UK Co

Non-UK Trust

(non dom/dead settlor)

PPR available

young / married

UK resbeneficiaryoccupying

low gain

www.blplaw.com Page 42 © Berwin Leighton Paisner

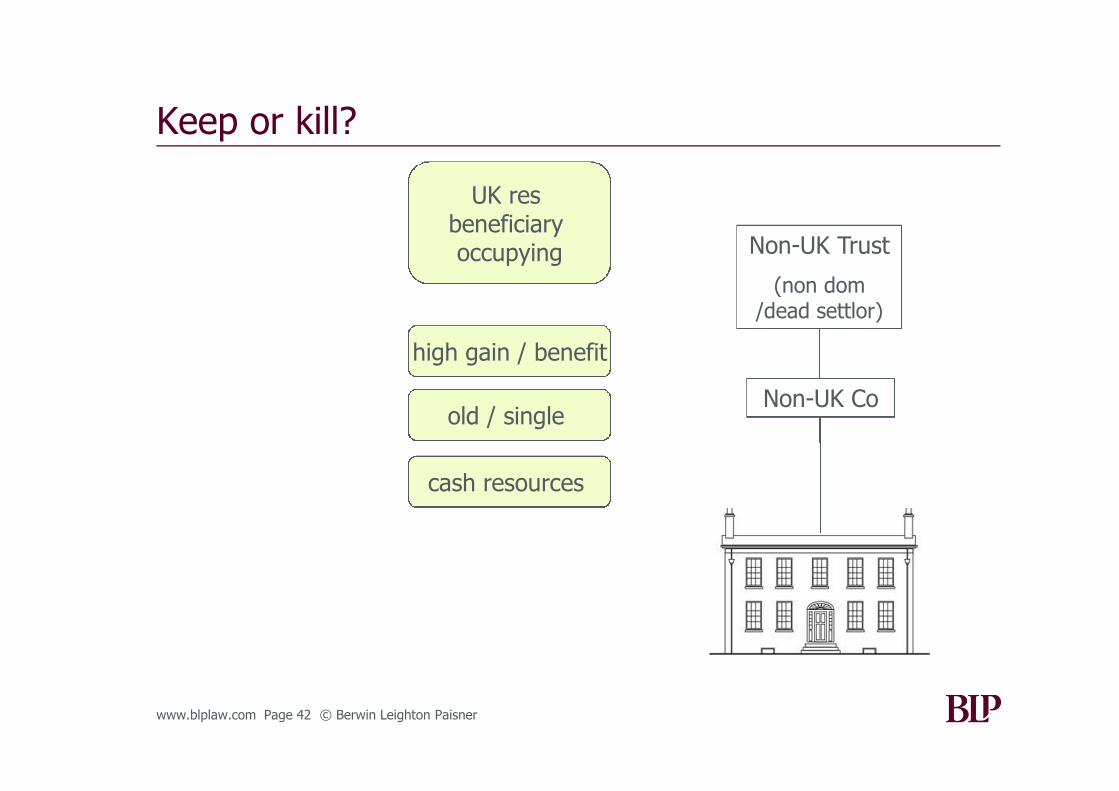

Keep or kill?

Non-UK Co

Non-UK Trust

(non dom/dead settlor)

old / single

cash resources

UK resbeneficiaryoccupying

high gain / benefit

www.blplaw.com Page 43 © Berwin Leighton Paisner

Personal ownership

Nominee

life insurance(joint life

second death)

non-resnon-dom

Bank90%

borrowing

Offshore

UK

rent

www.blplaw.com Page 44 © Berwin Leighton Paisner

Trust ownership (direct)

Nominee

life insurance(joint life

second death)Bank

90%

borrowing

Offshore

UK

Non-UK Trust

(non dom/dead settlor)

www.blplaw.com Page 45 © Berwin Leighton Paisner

Partnership solutions

Insurance?

Nominee

non-resnon-dom

LLP

non-resnon-dom

Bank?

Offshore

UKrent

www.blplaw.com Page 46 © Berwin Leighton Paisner

Success?

• Stamp out SDLT avoidance

• Restore credibility of SDLT regime

• Encourage de-enveloping

• Equalise taxation of residents and non-residents

• Tackle IHT avoidance

This document provides a general summary only and is not intended to be comprehensive. Specific legal advice should always be soughtin relation to the particular facts of a given situation.

PW/27412474

High Value Residential Properties – The New Rules

STEP – City of London

November 2012