Embed Size (px)

Citation preview

From information, knowledge

Paragon Economics, Inc.

Steve R. Meyer, Ph.D.Paragon Economics, Inc.

PPIC/RAC - - September 2009

Hog and Pork Market Outlook

From information, knowledge

Paragon Economics, Inc.

Thought for the day

If a man is in a desert and speaks

And no woman is around

Is he still wrong?

From information, knowledge

Paragon Economics, Inc.

To paraphrase the Clinton campaign:

“IT‟S COSTS, STUPID!”

From information, knowledge

Paragon Economics, Inc.

The cause of losses is still COSTS!!!!!

. . . +22% from historical levels through 2010ACTUAL & PREDICTED HOG

PRODUCTION COSTS*

40

45

50

55

60

65

70

75

80

85

90

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

$/cwt carcass

Actual Costs per ISU

Predicted/Forecast Costs - Carcass

*Based on relationsip between ISU Estimated Costs & Returns data and historic Omaha corn and Decatur soybean meal prices

9/28/09

Average Cost, 1999-2006:

$52.76/cwt

Average Cost, 9/09 - 12/10:

$64.44/cwt

From information, knowledge

Paragon Economics, Inc.

September would be our first losses . . .

. . . under the historical cost scenario ACTUAL & PREDICTED HOG

PRODUCTION COSTS* AND PRICES

10

20

30

40

50

60

70

80

90

100

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

$/cwt carcassActual Costs per ISU

Predicted/Forecast Costs - Carcass

Cash Hog Price

Futures-Implied IA-MN Price

*Based on relationsip between ISU Estimated Costs & Returns data and historic Omaha corn and Decatur soybean meal prices

9/28/09

From information, knowledge

Paragon Economics, Inc.

Near-record corn crop will help!

U S ANNUAL CORN PRODUCTIONCrop Year

2

4

6

8

10

12

14

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Bil. Bushels

From information, knowledge

Paragon Economics, Inc.

Record-high availability, price down 19% . . .

U S TOTAL CORN SUPPLY AND PRICECrop Year

6

7

8

9

10

11

12

13

14

15

1985 1988 1991 1994 1997 2000 2003 2006 2009

Bil. Bushels

1.20

1.60

2.00

2.40

2.80

3.20

3.60

4.00

4.40

4.80

$ Per Bushel

Supply

Price

. . . but still around $3/bu

From information, knowledge

Paragon Economics, Inc.

Cash corn is still in its new “normal” range . . .

. . . at least in Omaha CASH CORN PRICE, OMAHA, WEEKLY

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

$/bu.

Source: USDA, Agricultural Marketing Service

From information, knowledge

Paragon Economics, Inc.

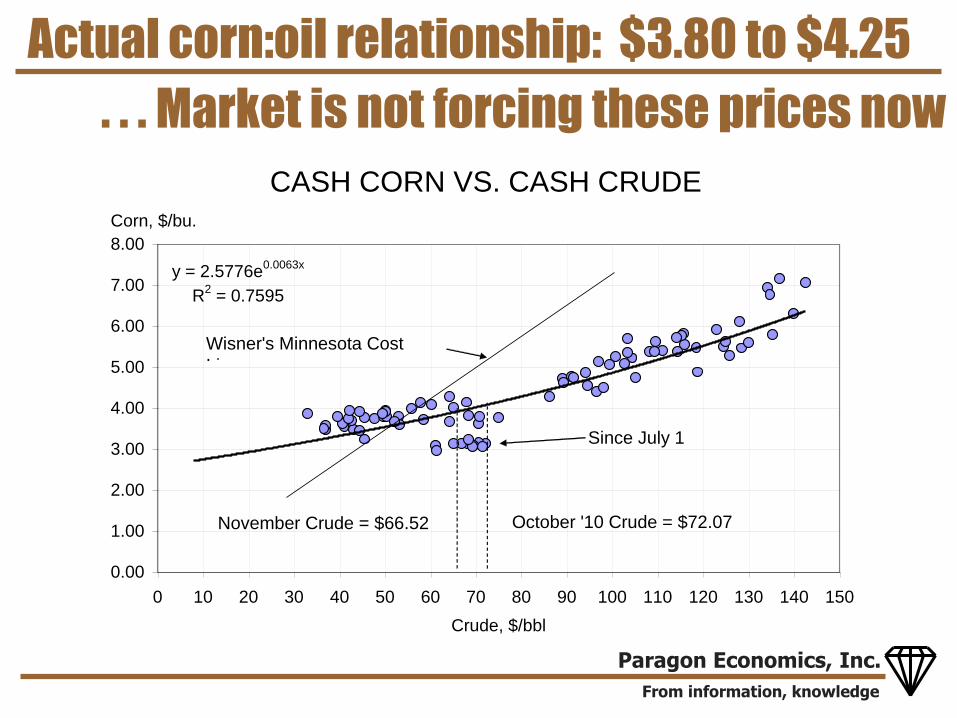

Actual corn:oil relationship: $3.80 to $4.25

. . . Market is not forcing these prices now

CASH CORN VS. CASH CRUDE

y = 2.5776e0.0063x

R2 = 0.7595

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

Crude, $/bbl

Corn, $/bu.

Wisner's Minnesota Cost

Line

November Crude = $66.52 October '10 Crude = $72.07

Since July 1

From information, knowledge

Paragon Economics, Inc.

Corn usage for ethanol up to 4.2 bil. bu. . . .

. . . +14.3% vs. ‟08; 280 mil. bu. more in „10U.S. CORN PRODUCTION & USAGE BY

CATEGORY

0

1000

2000

3000

4000

5000

6000

7000

1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

Usage - Mil. bu.

Ethanol

FSI-Non Ethanol

Feed & Residual

Exports

USDA Forecast, 9/11

From information, knowledge

Paragon Economics, Inc.

Positive ethanol margins will drive corn bids

From information, knowledge

Paragon Economics, Inc.

Dec corn was trending down . . .

. . . but can it do much more with oil at $70?

From information, knowledge

Paragon Economics, Inc.

Cash meal has been near record high . . .

. . . Poor SA crop, VERY tight bean stocks CASH SBM PRICE, DECATUR

150.00

200.00

250.00

300.00

350.00

400.00

450.00

500.00

J F M A M J J A S O N D

$/bu.

2009

2008

2007

Avg. '03-'07

From information, knowledge

Paragon Economics, Inc.

Futures market is +/-$275 and falling . . .

. . . Tech: Sit tight, watch for a breakout

From information, knowledge

Paragon Economics, Inc.

Feed costs have fallen 25% since June. . .

. . . still 2X historical, but at a BUYING level CORN-SOY COST, 16% CR. PROTEIN DIET

50

100

150

200

250

300

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

$/Ton

Actual

Predicted July 1, 2008

Predicted December 8, 2008

Predicted June 11, 2009

Predicted September 28, 2009

From information, knowledge

Paragon Economics, Inc.

We can‟t “unring” the ethanol bell

The plants are in place – they will be operated by someone

From information, knowledge

Paragon Economics, Inc.

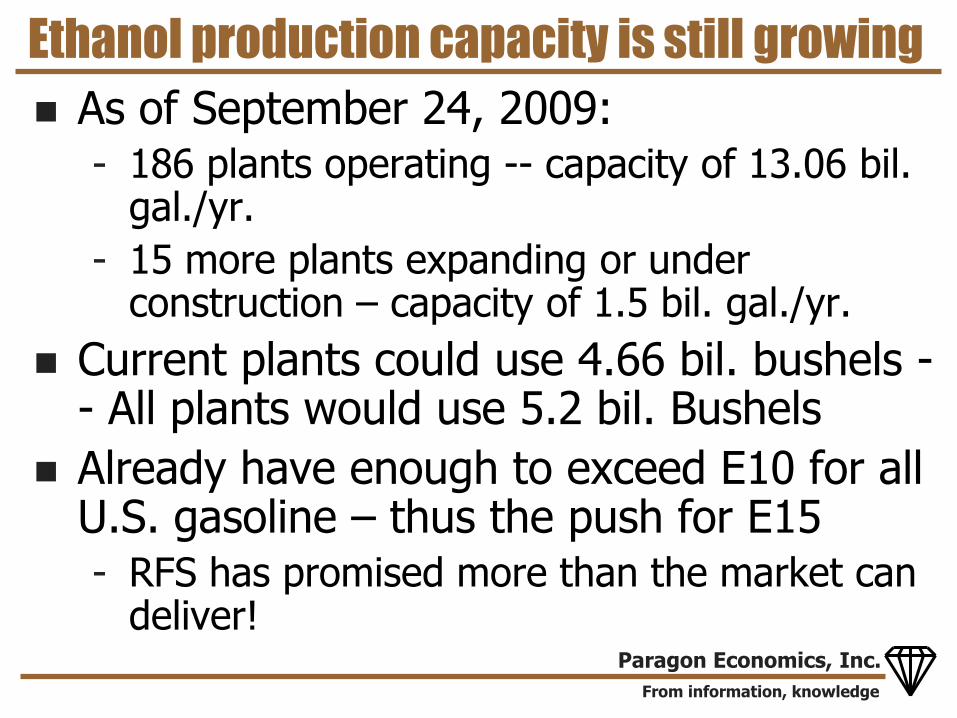

Ethanol production capacity is still growing

As of September 24, 2009:- 186 plants operating -- capacity of 13.06 bil.

gal./yr.

- 15 more plants expanding or under construction – capacity of 1.5 bil. gal./yr.

Current plants could use 4.66 bil. bushels -- All plants would use 5.2 bil. Bushels

Already have enough to exceed E10 for all U.S. gasoline – thus the push for E15- RFS has promised more than the market can

deliver!

From information, knowledge

Paragon Economics, Inc.

We can‟t “unring” the ethanol bell

The plants are in place – they will be operated by someone

FAPRI/TAMU study – looked at 2011-2018- Removing the BTC lowers corn price 0.6%

- Removing the tariff lowers corn price 2.8%

- Removing the RFS lowers corn price 4.6%

- Removing all three lowers corn price 13.1%

- NONE OF THESE WILL HAPPEN -- Politics

NEED – an automatic trigger for situation where oil is cheap and we have a drought

From information, knowledge

Paragon Economics, Inc.

If an input price rises – SLR & SSR shift . . .

P

Q

SLR

SSRDH

PE

QE

SS’SR

C’

. . . But S cannot shift immediately

Revenue =

PE * QE

Costs = QE * C’

Losses = QE *

(C’ – PE)

From information, knowledge

Paragon Economics, Inc.

ONLY TWO WAYS TO RESTORE PROFITS

Increase demand

P

Q

SLR

SSRDH

PE

QE

S

S’LR

S’SR

C’=P’

D’H

From information, knowledge

Paragon Economics, Inc.

Increasing demand is a SLOW process!

Population growth – 0.8 to 0.9% per year

New markets – most of the big ones are open – most of the time!

Reduce tariffs in existing markets

- NAFTA did this but total reduction took 10 yrs

- Korean FTA and others would help now

Promotion – small budget vs. market size

Product development – the driver of chicken demand since 1980s

From information, knowledge

Paragon Economics, Inc.

Second, more likely, solution . . .

Reduce supply

P

Q

SLR

SSRDH

PE

QE

S’

S’LR

S’SR

Q’

P’

From information, knowledge

Paragon Economics, Inc.

ALL PROTEINS ARE IN THE SAME PICKLE!!!!

Chicken production is down 4.7% YTD

Turkey production is down 5.4% YTD

Pork production is down 2.2% YTD

Beef production is down 3.9% YTD

Chicken and turkey reductions will slow –they could react more quickly

Pork reduction will get larger

Beef reduction may not get larger but will last MUCH longer

From information, knowledge

Paragon Economics, Inc.

Consider the impact in the pork industry:

For each 1 million head fewer market hogs produced in the U.S., there will be

- 331 fewer jobs in pork production

- 681 fewer jobs in pork processing

- 1,142 fewer jobs in the rest of agriculture

- 2,154 fewer jobs – mostly rural!

And we are in the process of reducing output by 10 million head

- 21,540 fewer jobs – mainly in rural areas

From information, knowledge

Paragon Economics, Inc.

Other impacts

Financial requirements and risk

- It now takes $130-$170 to produce a market hog vs. $110 pre-2007

- Raising a fed steer now takes $1200-$1500 vs. $1100-$1300 pre-2007

Many banks are bowing out of ag lending in general and livestock in particular

At best, owner equity requirements are higher

From information, knowledge

Paragon Economics, Inc.

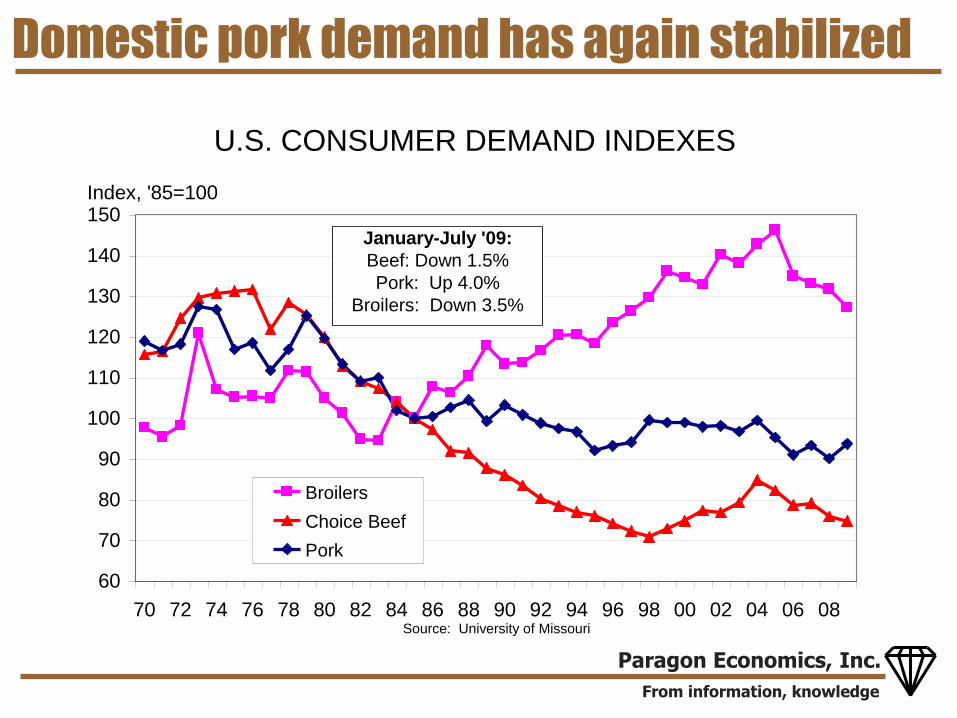

Domestic pork demand has again stabilized

U.S. CONSUMER DEMAND INDEXES

60

70

80

90

100

110

120

130

140

150

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

Index, '85=100

Broilers

Choice Beef

Pork

Source: University of Missouri

January-July '09:

Beef: Down 1.5%

Pork: Up 4.0%

Broilers: Down 3.5%

From information, knowledge

Paragon Economics, Inc.

Monthly expenditures – higher demand . . .

MONTHLY REAL PER CAPITA PORK

CONSUMPTION VALUE

6.00

7.00

8.00

9.00

10.00

11.00

12.00

J F M A M J J A S O N D

$/month

2007

2008

2009

Average,'03-'07

From information, knowledge

Paragon Economics, Inc.

Retail prices show VERY LITTLE decline ???

RETAIL MEAT PRICES, USDA

0

50

100

150

200

250

300

350

400

450

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Cents/lb.

All-Fresh Beef

Pork

Composite Broiler

Turkey

From information, knowledge

Paragon Economics, Inc.

Very good disappearance/consumption . . .

DOMESTIC PORK CONSUMPTION

1200

1300

1400

1500

1600

1700

1800

1900

2000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Bil. lbs. carc. wt.

Disappearance

Dissappearance, 6-mo. Avg.

. . . Largest July ever, 2nd largest June ever

From information, knowledge

Paragon Economics, Inc.

Pork exports grew rapidly in 2008 . . .

U.S. PORK EXPORTS

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1955 1959 1963 1967 1971 1975 1979 1983 1987 1991 1995 1999 2003 2007

Mil. lbs. carcass

The NAFTA signed in 1994

2008: Exports UP 48%!

. . . Permanent or transient?

From information, knowledge

Paragon Economics, Inc.

2008 exports: A happy confluence . . .

Record-low U.S. dollar made U.S. product relatively cheap

China/Hong Kong was the driver

- Booming economy and rising middle class

- Death losses in 2006-07 due to disease, earthquake, harsh winters = pork shortage

- Olympic games

Economic growth in other countries

Strong Canadian dollar

From information, knowledge

Paragon Economics, Inc.

YTD: Export Q and V are lower . . .

YTD PORK EXPORTS - PRODUCT WT.

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

2003 2004 2005 2006 2007 2008 2009

Mil

. lb

s.

-- W

orl

d

0

50

100

150

200

250

300

350

400

450

500

550

600

Mil

. lb

s.

-- I

nd

iv.

Co

un

trie

s

WORLD TOTAL AUSTRALIA

CANADA JAPAN

KOREA MEXICO

RUSSIA TAIWAN

CHINA/HONG KONG

JANUARY - JULY

-16.9%

-69.9%

-2.6%

33.0%

YTD PORK EXPORT VALUE

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

2400

2003 2004 2005 2006 2007 2008 2009

Mil.

$$

--

Wo

rld

0

100

200

300

400

500

600

700

800

900

1000

Mi. $

$ -

- In

div

. C

ou

ntr

ies

WORLD TOTAL AUSTRALIA

CANADA JAPAN

KOREA MEXICO

RUSSIA TAIWAN

CHINA/HONG KONG

-12.9%

JANUARY - JULY

25.5%

-69.6%

10.2%

13.8%

Mexico: +33% Q, +14% V

Japan: -2.6% Q, +10.2% V

Ch/HK: -70% Q & V

From information, knowledge

Paragon Economics, Inc.

Variety meat exports have been GOOD . . . YTD PORK VARIETY MEAT EXPORTS -

PRODUCT WT.

0

50

100

150

200

250

300

350

400

450

500

550

600

650

2003 2004 2005 2006 2007 2008 2009

Mil

. lb

s.

-- W

orl

d

0

25

50

75

100

125

150

175

200

225

250

Mil

. lb

s.

-- I

nd

iv.

Co

un

trie

s

WORLD TOTAL AUSTRALIA

CANADA JAPAN

KOREA MEXICO

RUSSIA TAIWAN

CHINA + HONG KONG

JANUARY - JULY

21.3%

7.1%

-48.1%

62.5%

81.8%

YTD PORK VARIETY MEAT EXPORT

VALUE

0

50

100

150

200

250

300

350

2003 2004 2005 2006 2007 2008 2009

Mil.

$$

--

Wo

rld

0

30

60

90

120

150

Mi. $

$ -

- In

div

. C

ou

ntr

ies

WORLD TOTALAUSTRALIACANADAJAPANKOREAMEXICORUSSIATAIWANCHINA + HONG KONG

17.9%

JANUARY - JULY

208.8%

12.3%

-46.0%

47.2%

47.3%

Quantity: +21% YTD

Mexico: +63%!

Ch/HK: +7%

Value: +18% YTD

Mexico: +47%

Ch/HK: +12.3%

From information, knowledge

Paragon Economics, Inc.

2009 exports have been remarkably strong .

. . . Given the obstacles we have faced!!!

MONTHLY U.S. PORK EXPORTS &

TRENDS

0

100

200

300

400

500

600

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Mil. lbs. carcass

U.S. Pork Exports

Polynomial, '90-'08

Trend '04-'07 2008 Export Surge

July ’09:

Down13.2% vs. ’08

UP 61% vs. ‘07

From information, knowledge

Paragon Economics, Inc.

Slaughter exploded in ‟07 -- +7.8% in Q4-‟07

FI HOG SLAUGHTER, WEEKLY

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

Thous. Hd.

Record: 2.478 mil. hd., 12/22/2007

Circovirus vaccines

introduced -- July 2007

. . . circovirus vaccines were main cause

From information, knowledge

Paragon Economics, Inc.

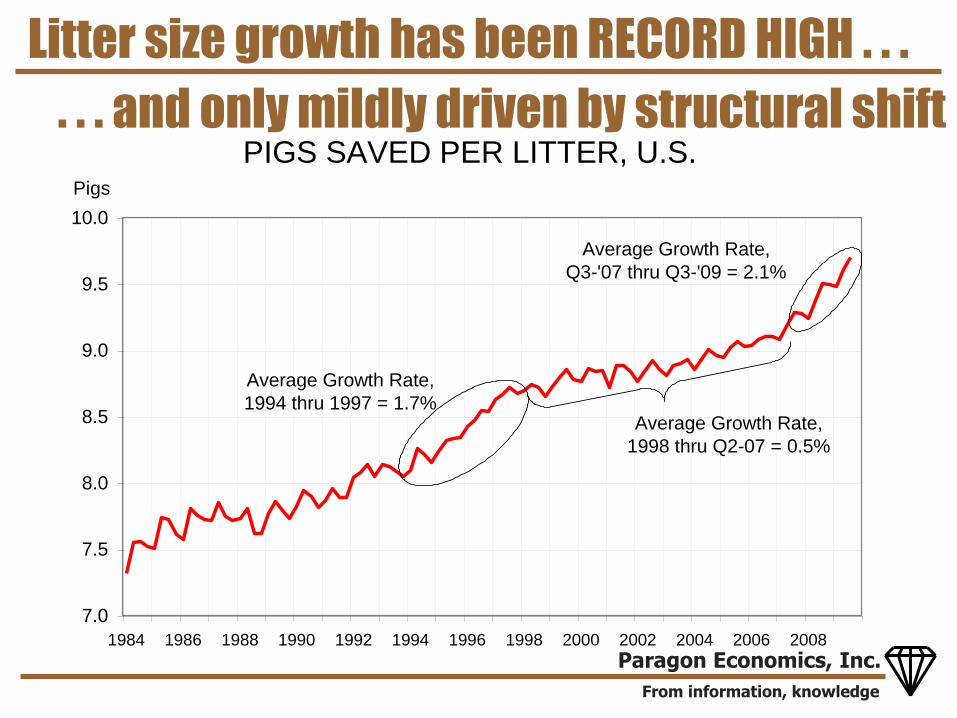

Litter size growth has been RECORD HIGH . . .

PIGS SAVED PER LITTER, U.S.

7.0

7.5

8.0

8.5

9.0

9.5

10.0

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Pigs

Average Growth Rate,

1994 thru 1997 = 1.7%

Average Growth Rate,

Q3-'07 thru Q3-'09 = 2.1%

Average Growth Rate,

1998 thru Q2-07 = 0.5%

. . . and only mildly driven by structural shift

From information, knowledge

Paragon Economics, Inc.

FI HOG SLAUGHTER, WEEKLY

1600

1700

1800

1900

2000

2100

2200

2300

2400

2500

2600

J F M A M J J A S O N D

Thous. Hd.

Actual 08

Actual 09

Pred '09

Pred '10

Based on USDA Hogs & Pigs Report, June '09 w/ Adjustments

Last 8 wks -- +3.0% from June H&P level . . .

. . . hogs backed up or pulled ahead?

-196+501

From information, knowledge

Paragon Economics, Inc.

High weights have added 2-3% to prod . . .

FI CARCASS WEIGHTS, HOGS

192

194

196

198

200

202

204

206

208

J F M A M J J A S O N D

Pounds

2009

2008

Avg '03-'07

From information, knowledge

Paragon Economics, Inc.

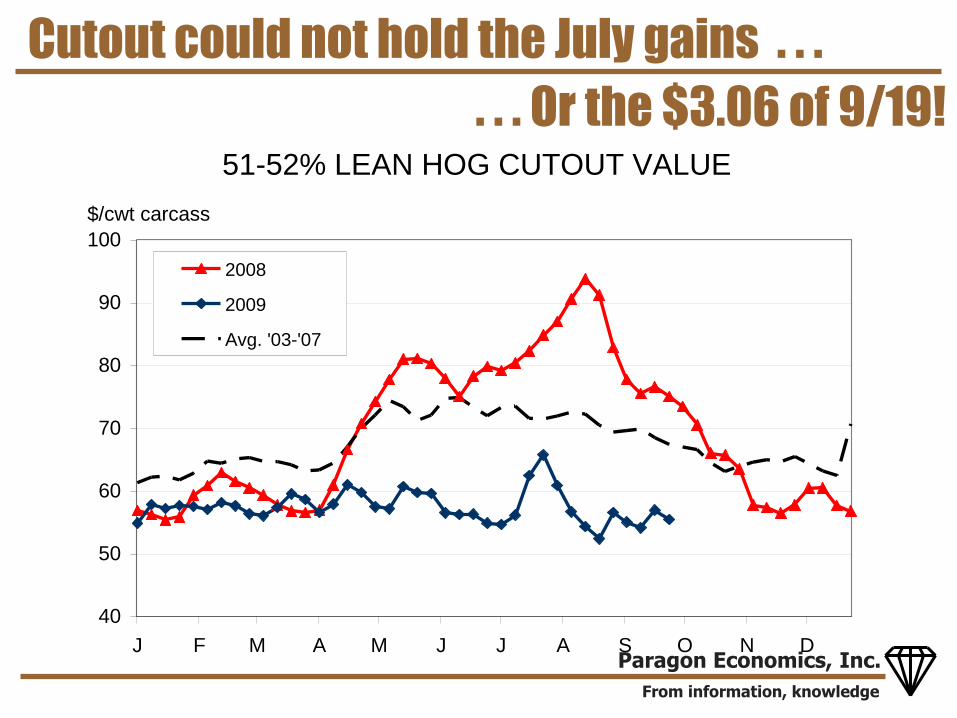

Cutout could not hold the July gains . . .

. . . Or the $3.06 of 9/19!51-52% LEAN HOG CUTOUT VALUE

40

50

60

70

80

90

100

J F M A M J J A S O N D

$/cwt carcass

2008

2009

Avg. '03-'07

From information, knowledge

Paragon Economics, Inc.

Packers finally healed up margins in July . . .

PORK PACKERS' EST'D GROSS MARGIN

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

J F M A M J J A S O N D

$/hd.

2008

2009

Average '03-'07

Highest gross margin since Feb 1999

Lowest gross margin on record

From information, knowledge

Paragon Economics, Inc.

By-products have helped since May . . .

PORK PACKER MARGIN COMPONENTS

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Dollars/Head

By-Product Value, $/hd.

Meat Margin, $/Hd

. . . But the July jump was meat margin

From information, knowledge

Paragon Economics, Inc.

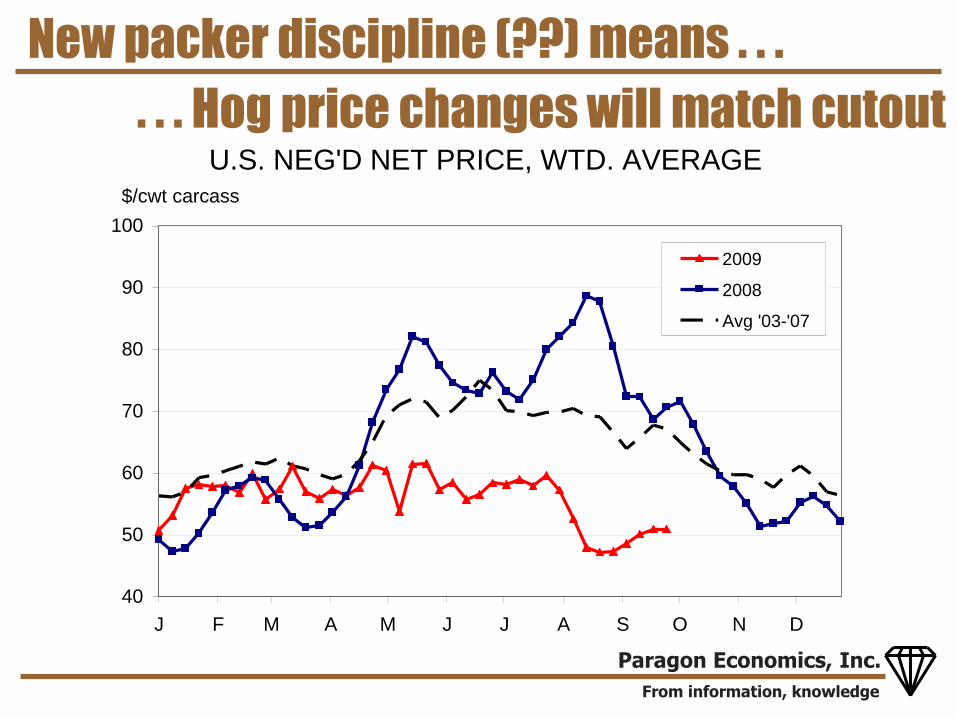

New packer discipline (??) means . . .

. . . Hog price changes will match cutoutU.S. NEG'D NET PRICE, WTD. AVERAGE

40

50

60

70

80

90

100

J F M A M J J A S O N D

$/cwt carcass

2009

2008

Avg '03-'07

From information, knowledge

Paragon Economics, Inc.

Average price actually received . . .

. . . still about $5/cwt higher than spot priceNATIONAL WTD. AVG. NET PRICE

ALL PURCHASE METHODS

40

45

50

55

60

65

70

75

80

85

90

J F M A M J J A S O N D

$/cwt carcass

2009

2008

Avg '03-'07

From information, knowledge

Paragon Economics, Inc.

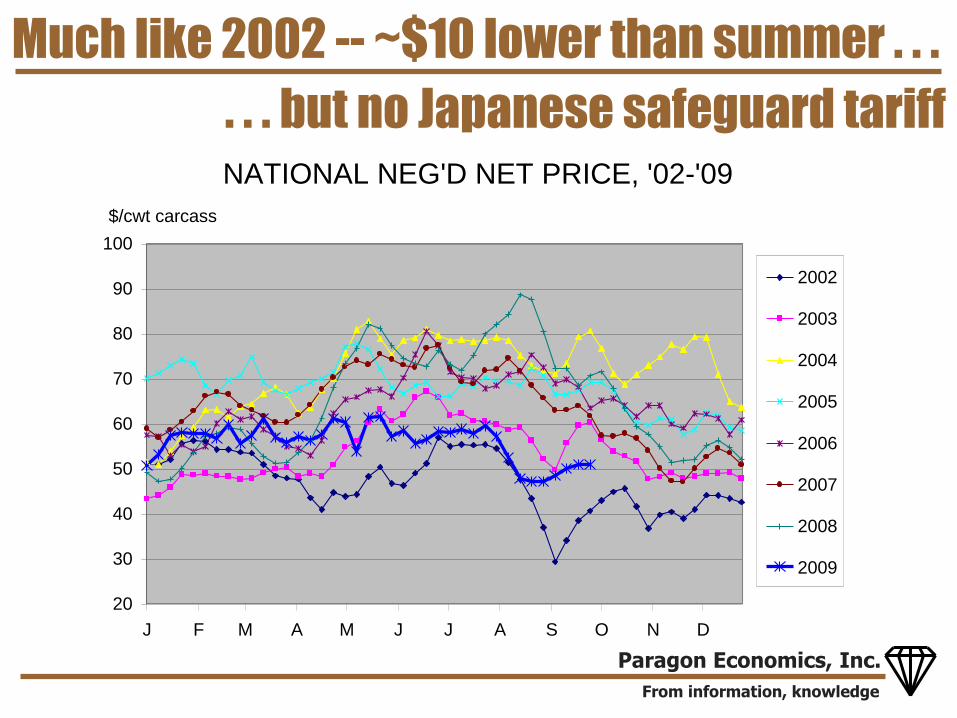

Much like 2002 -- ~$10 lower than summer . . .

. . . but no Japanese safeguard tariffNATIONAL NEG'D NET PRICE, '02-'09

20

30

40

50

60

70

80

90

100

J F M A M J J A S O N D

$/cwt carcass

2002

2003

2004

2005

2006

2007

2008

2009

From information, knowledge

Paragon Economics, Inc.

September Hogs & Pigs: About as expected . .

. . . with some reduction of the pig crop

Category 2008 2009

2009 as Pct

of 2008

Pre-Report

Estimates

Actual -

Estimate

Inventories on September 11

All hogs and pigs 68,196 66,626 97.7 98.2 -0.5

Kept for breeding 6,061 5,874 96.9 97.4 -0.5

Kept for market 62,135 60,752 97.8 98.3 -0.5

Under 60 lbs. 22,683 21,837 96.3 98.3 -2.0

60-119 lbs. 15,397 15,078 97.9 98.3 -0.4

120-179 lbs. 12,855 12,674 98.6 98.8 -0.2

180 lbs. and over 11,201 11,163 99.7 99.0 0.7

Farrowings2

June-Aug sows farrowed 3,075 2,966 96.5 96.8 -0.3

Sep-Nov Intentions 3,028 2,935 96.9 97.3 -0.4

Dec-Feb Intentions 3,024 2,930 96.9 96.9 0.0

June-Aug Pig Crop1 29,240 28,772 98.4 98.1 0.3

June-Aug pigs saved per litter 9.51 9.70 102.0 101.4 0.61Thousand head

2Thousand litters

USDA Quarterly Hogs and Pigs Report

September 25, 2009

From information, knowledge

Paragon Economics, Inc.

Slaughter declining, yr/yr, through 2010 . . .

FI HOG SLAUGHTER, WEEKLY

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

2,600

J F M A M J J A S O N D

Thous. Head

Actual 08

Actual 09

Pred '09

Pred '10

Based on USDA Hogs & Pigs Report, September '09

Adjustmets have been made for

fewer market hogs from

Canada through Jan '10 and

fewer feeder pigs through

September '10

. . . But with largest drop – so far – in Q2

From information, knowledge

Paragon Economics, Inc.

FP and MH imports are down sharply . . .

LIVE HOG IMPORTS FROM CANADA

-

50,000

100,000

150,000

200,000

250,000

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Head

Feeder Pigs

Slght Barr's & Gilts

Slght Sows & Boars

Incorrect data from

APHIS

MH: -71%

FP: -27%

SB: +3%

All: -33%

. . . But are equal to the levels I expected

From information, knowledge

Paragon Economics, Inc.

Quarterly slaughter forecasts . . .

Mil. Hd % Chnge Mil. Hd % Chnge Mil. Hd % Chnge Mil. Hd % Chnge

2008 Q1 29.601 11.1%

Q2 27.941 9.5%

Q3 28.696 8.1%

Q4 30.214 -0.05%

Year 116.452 6.7%

2009 Q1 28.488 -3.8% 28.488 -3.8% 28.488 -3.8% 28.488 -3.8%

Q2 27.063 -3.1% 27.063 -3.1% 27.063 -3.1% 27.063 -3.1%

Q3 28.400 -1.0% 28.553 -0.5% 28.208 -1.7% 28.380 -1.1%

Q4 29.670 -1.8% 29.912 -1.0% 29.607 -2.0% 29.489 -2.4%

Year 113.621 -2.4% 114.015 -2.1% 113.366 -2.7% 113.420 -2.6%

2010 Q1 27.435 -3.7% 28.061 -1.5% 28.357 -0.5% 27.405 -3.8%

Q2 26.200 -3.2% 26.657 -1.5% 27.036 -0.1% 27.804 -2.4%

Q3 27.500 -3.2% 27.981 -2.0% 27.908 -1.1% 27.699 -2.4%

Green figures are actual data from USDA. Red figures are based on partial USDA data. 9/28/2009

September 2009 Commercial Slaughter ForecastsMizzou LMIC MeyerISU

ACTUAL DATA FOR 2008

From information, knowledge

Paragon Economics, Inc.

Sow herd reduction has sped up and . . .

SWINE BREEDING HERDS -- US & Canada

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Pct Chnge, Yr-Yr

Canada

U.S.

Can-Am

Canada July 2009 -- Down 4.6%

U.S. September 2009 -- Down 3.1%

%

y

. . . Canada‟s October report will say the same

From information, knowledge

Paragon Economics, Inc.

MPR sow purchases: Continued high slghtr

TOTAL SOW PURCHASES, MPR DATA

10

15

20

25

30

35

40

45

50

55

60

J F M A M J J A S O N D

Thous. Head

Avg. '03-'07

2008

2009

MPR Coverage

Expanded by

Farm Bill

Changes

From information, knowledge

Paragon Economics, Inc.

Sow slaughter finally went above 70k/wk. . . .

. . . Will it stay this high? Canadian buyout?FI SOW SLAUGHTER, U.S.

40

45

50

55

60

65

70

75

80

J F M A M J J A S O N D

Thous. Head

Avg. '03-'07

2008

2009

Forecast

From information, knowledge

Paragon Economics, Inc.

Sow slaughter as a % of BH is just now . . .

. . . large enough to make a real differenceFI SOW SLAUGHTER

As a Percent of Previous Quarter's Breeding Herd

0.60%

0.70%

0.80%

0.90%

1.00%

1.10%

1.20%

1.30%

1.40%

J F M A M J J A S O N D

2009

2008

Avg. '03-'07

From information, knowledge

Paragon Economics, Inc.

Why such a slow reaction?

Producers WANT to be in this business – it has been good to them!

2008 exports provided false security and hope – Producers believed 2008 was the new reality???

From information, knowledge

Paragon Economics, Inc.

Producer equity was record high in ‟07 . . .

ACCUMULATED PROFITS

IOWA FARROW-TO-FINISH OPERATIONS(Sum of the profit from selling one pig per month since January 1991)

$(200)

$(100)

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Took 8 years to get

back to Nov 1997 level

Peak in Sept '07 = $786.87

Thru August 2009

Have lost $517.52

66% of peak amount

Source: Paragon Economics, Inc. using data from Estimated Costs and Returns, Dr. John Lawrence, Department of Economics, Iowa State

University

Aug '09 = $269.35

. . . but is now down by two-thirds!

From information, knowledge

Paragon Economics, Inc.

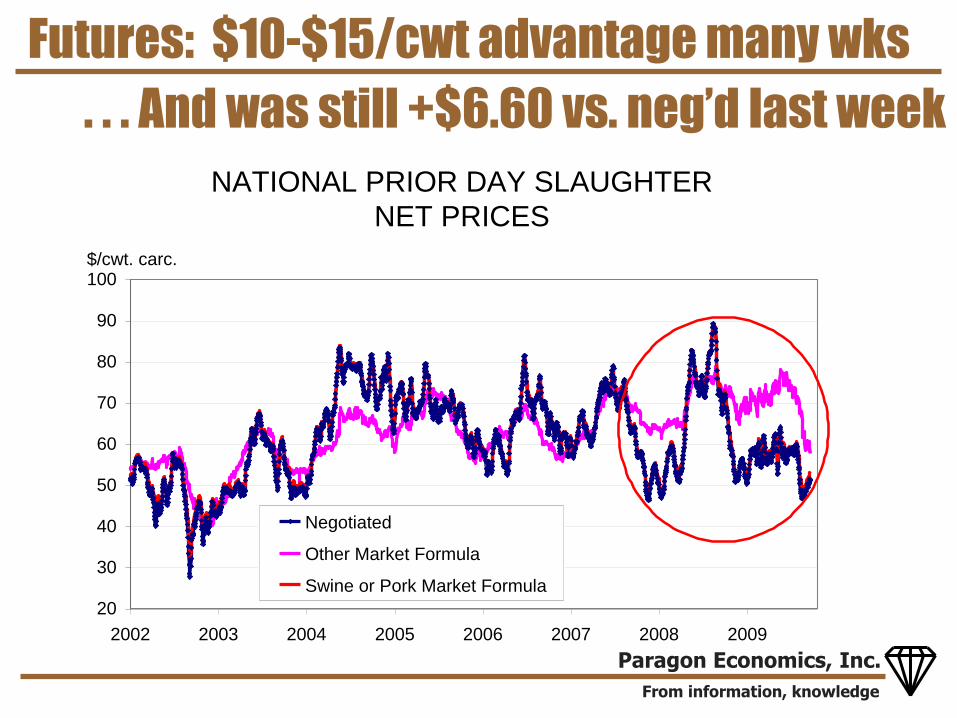

Futures: $10-$15/cwt advantage many wks

NATIONAL PRIOR DAY SLAUGHTER

NET PRICES

20

30

40

50

60

70

80

90

100

2002 2003 2004 2005 2006 2007 2008 2009

$/cwt. carc.

Negotiated

Other Market Formula

Swine or Pork Market Formula

. . . And was still +$6.60 vs. neg‟d last week

From information, knowledge

Paragon Economics, Inc.

What to expect

Incentives to cut back are now VERY strong – actually for the first time in this cycle!

Though the pace is quickening – liquida-tion will be slow by historical standards

THERE WILL BE A U.S. PORK INDUSTRY

- Exceptional operational efficiencies

- Adept financial management

- Successful RISK MANAGEMENT – a BIG one!

From information, knowledge

Paragon Economics, Inc.

How much of a reduction do we need?

We have to make up for:

- ~7-8% productivity increase of circo vac‟s

- 20-30% higher costs.

Need a 12% reduction of US/Canada herd from 10/07 peak of 7.752 mil. = 6.82 mil.

- Canada is already at 1.38 million and will cut farther – to 1.25 mil. or so

- U.S. needs to go to between 5.5 and 5.6 million

Sept 1: 5.874 million, down 3.1% vs. „08

From information, knowledge

Paragon Economics, Inc.

Price forecasts – but futures are higher!

Missouri ISU LMIC Meyer CME

51-52% Lean,

Live1

Ia-S. Mn. Live

Price1

National Wtd

Avg. Base Price

National Net

Neg'd Price,

Wtd. Avg.

CME Lean

Hog Futures

9/28/09

2008 Q1 $52.85 $53.05 $55.27 $53.40 $54.26**

Q2 $70.01 $73.80 $69.92 $71.66 $71.66**

Q3 $76.36 $80.02 $75.60 $77.48 $78.45**

Q4 $55.89 $57.25 $59.00 $56.70 $58.51**

Year $63.78 $66.03 $64.95 $64.81 $65.72**

2009 Q1 56.15 56.80 58.11 57.22 $58.14**

Q2 57.67 58.48 59.45 58.18 $59.03**

Q3 52.13* 52.79* 54.14* 52.72* $54.18**

Q4 43 - 47 45 - 48 51 - 54 50 - 53 $49.81

Year 52 - 54 53 - 54 56 - 57 54 - 56 $55.29

2010 Q1 47 - 51 53 - 56 56 - 59 54 - 56 $56.60

Q2 53 - 57 64 - 67 61 - 64 62 - 66 $66.97

Q3 52 - 56 57 - 61 65 - 68 64 - 68 $70.051Converted to carcass using a yield of 75% *Partial USDA data **Average of CME Lean Hog Index

September 2009 Hogs & Pigs Price Forecasts

From information, knowledge

Paragon Economics, Inc.

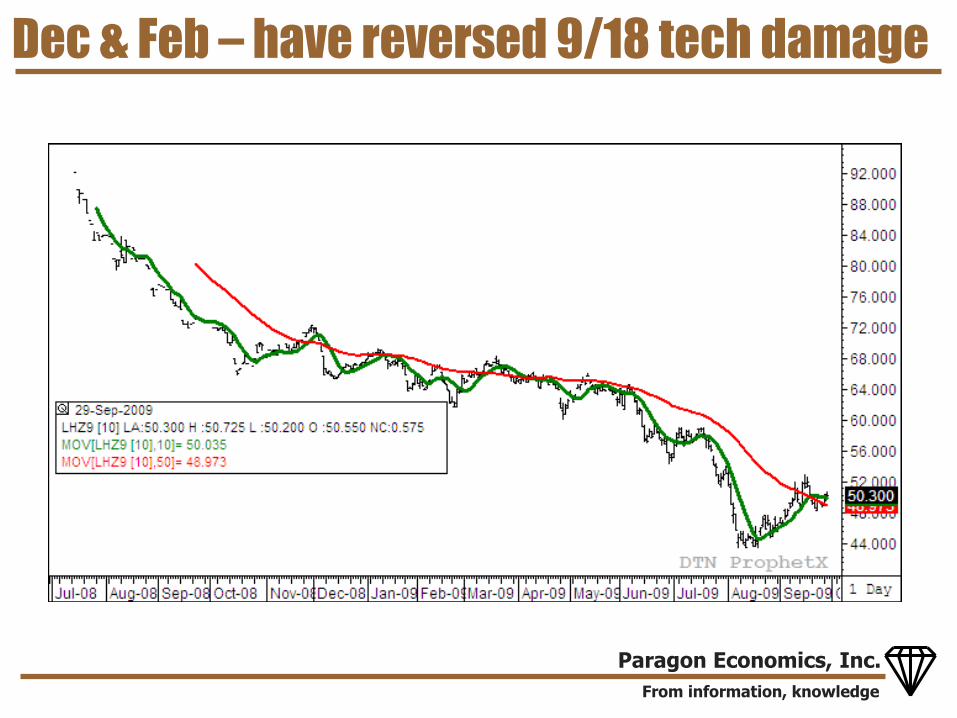

Dec & Feb – have reversed 9/18 tech damage

From information, knowledge

Paragon Economics, Inc.

April and beyond: Big top side breakout

From information, knowledge

Paragon Economics, Inc.

H1N1 hurt prices in May & June . . .

. . . hard to blame it now – exc. export PROJECTED & ACTUAL HOG PRICES, PRE

AND POST H1N1 -- AS OF 9/28

35

45

55

65

75

4/24

5/22

6/19

7/17

8/14

9/11

10/9

11/6

12/4 1/

11/

292/

263/

264/

23

$/cwt.Futures-Implied, 4/24

Neg&Swine/Pork Formula

Futures-Implied, 9/28

$1.125 Bil.

Through April 2010: $2.74 Billion

From information, knowledge

Paragon Economics, Inc.

“Why are you in this shape?”

“20% higher production costs driven by higher corn and soybean meal prices.”

NOT due to overexpansion – only 3.1% more sows during 44 months of profits!

Productivity has played a big role:

- Circo vaccines – economic and humane treatment AND concern for workers

- Improved genetics, management, etc.

H1N1 and associated disruptions

From information, knowledge

Paragon Economics, Inc.

“Why should I be worried about this?”

Pork producers have lost $4.9 billion since September 2007

Since April 24 (H1N1), revenues have fallen by $1.1 billion and will fall by $2.02 billion for all of 2009.

1500-sow producer has lost $1 million since 9/07 and faces $400k more by 12/31

Each 1 million fewer market hogs mean:

- 311 fewer production jobs

- 681 fewer pork processing jobs

- 1,142 fewer jobs in the rest of agriculture

From information, knowledge

Paragon Economics, Inc.

QUESTIONS AND DISCUSSION?