Embed Size (px)

Citation preview

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

Your Guide to Completing a Short Sale

Under the Federal Government’s HAFA Program

03-10-2011

Home Affordable Foreclosure

Alternatives (HAFA)

Short Sale Program

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE PROGRAM

Guide Revisions

Updates to the HAFA guide are made on a regular basis, so visit the Real

Estate Agent Resource Center (bankofamerica.com/realestateagent) to

download the most recent version.

Guide updates

• Version 2 – released March 10, 2011

– Policy updates (Supplemental Directive 10-18)

– Milestone chart on ARASS (HAFA process with offer already in hand)

– Key actions for agents

2

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA DEFINED

3

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE PROGRAM

• This federal government program

helps homeowners who:

– Can’t afford their first mortgage.

– Want to avoid foreclosure.

– Have exhausted all modification

attempts and can’t keep their

home.

• The program:

– Allows homeowners to sell their

home through a short sale and

settle mortgage debt.

– Offers financial incentives to

borrowers who successfully

complete a HAFA short sale or

deed in lieu of foreclosure.

• The federal government specifies

aspects of the program, including:

– Customer qualification

requirements.

– The process used by the servicer.

– Decision timeframes.

• Investor participation:

– Fannie Mae and Freddie Mac

implemented their own versions

of HAFA in 2010.

– FHA, VA and Ginnie Mae loans

are not yet covered by a HAFA-

type program.

4

Home Affordable Foreclosure Alternatives (HAFA)

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE PROGRAM

Homeowner Benefits of HAFA Program

Compared to traditional short sale process:

• Quickest option for a short sale decision when there is no offer.– Faster decisions: in 10 days once an offer is submitted.

– A lender-recommended list price is provided before listing the home.

• Deficiency is waived.– The mortgage debt will be settled through the program.

– No legal action can be taken on/against the outstanding mortgage debt.

• $3,000 at closing for relocation assistance.

• No cash contribution or promissory note required to release any lien.

• Foreclosure process put on hold.

When should homeowners consider the HAFA program?

• During initial discussions of alternative foreclosure options.

• Even after a short sale offer is received.

5

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE PROGRAM

Requirements for HAFA Eligibility*

• The homeowner has:

– Exhausted all modification options, and/or

– Decided to pursue a short sale or deed in lieu of foreclosure.

• The property is the homeowner’s primary residence.

• The mortgage:

– Originated on or before Jan. 1, 2009 (for the 1st lien).

– Is delinquent or default is reasonably foreseeable.

• The homeowner must contact us to determine the likelihood of default.

– Has an unpaid principal balance less than $729,750 for 1-unit properties.

• Higher balances are available for 2-4 unit properties.

• No properties with more than 4 units allowed.

6

* HAFA eligibility doesn’t represent being qualified as investor determines.

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

ENHANCEMENTS – 10-18 UPDATES

7

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE PROGRAM

HAFA 10-18 Enhancements

• Supplemental Directive 10-18 has reduced eligibility requirements so more borrowers may qualify.

• Major eligibility improvements include:– Eliminated the requirement to verify borrower’s financial information,

including debt-to-income (DTI) ratio.

– Property can be vacant or rented up to 12 months prior to the Short Sale Agreement (SSA), as long as the borrower can prove the property was the primary residence and has not purchased another home in the last 12 months prior to SSA.

• Relocation no longer has to be work-related, nor is there a minimum distance requirement.

– Payment to 2nd lien holders up to $6,000 remains, but the 6% requirement is eliminated.

– Agent commissions:• Are not deducted from 3rd party vendor fees.

• Will be stated in the Short Sale Agreement.

• Download Supplemental Directive 10-18 for more details.

8

For more information about policy updates,

see: HAFA 10-18 Enhancements

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

INVESTOR PARTICIPATION

9

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE PROGRAM

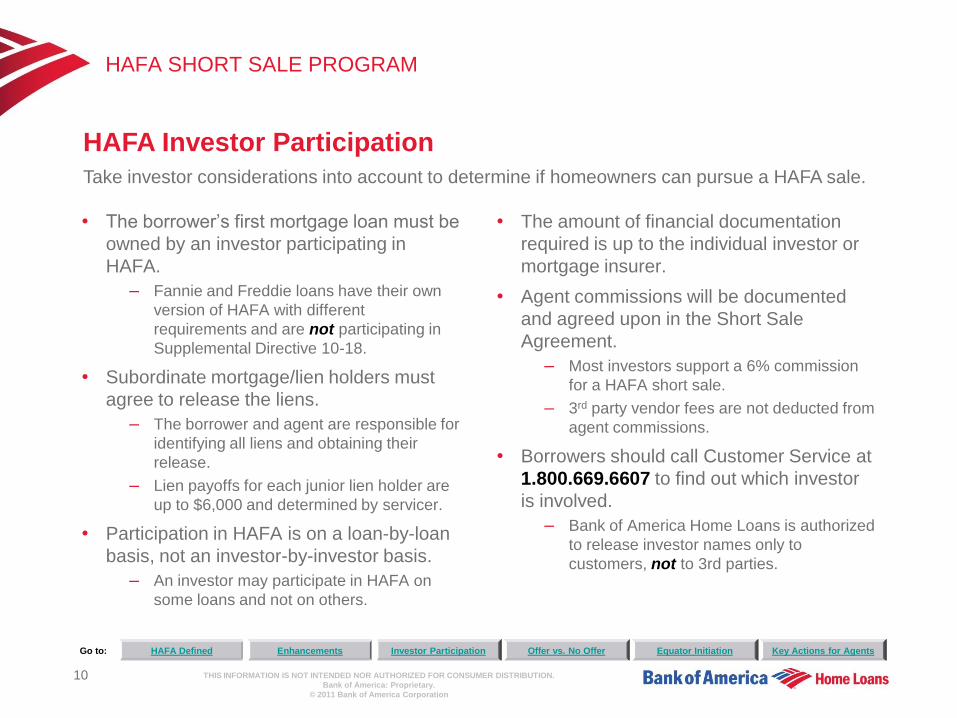

• The borrower’s first mortgage loan must be

owned by an investor participating in

HAFA.

– Fannie and Freddie loans have their own

version of HAFA with different

requirements and are not participating in

Supplemental Directive 10-18.

• Subordinate mortgage/lien holders must

agree to release the liens.

– The borrower and agent are responsible for

identifying all liens and obtaining their

release.

– Lien payoffs for each junior lien holder are

up to $6,000 and determined by servicer.

• Participation in HAFA is on a loan-by-loan

basis, not an investor-by-investor basis.

– An investor may participate in HAFA on

some loans and not on others.

• The amount of financial documentation

required is up to the individual investor or

mortgage insurer.

• Agent commissions will be documented

and agreed upon in the Short Sale

Agreement.

– Most investors support a 6% commission

for a HAFA short sale.

– 3rd party vendor fees are not deducted from

agent commissions.

• Borrowers should call Customer Service at

1.800.669.6607 to find out which investor

is involved.

– Bank of America Home Loans is authorized

to release investor names only to

customers, not to 3rd parties.

10

HAFA Investor Participation

Take investor considerations into account to determine if homeowners can pursue a HAFA sale.

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

OFFER VS. NO OFFER

11

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

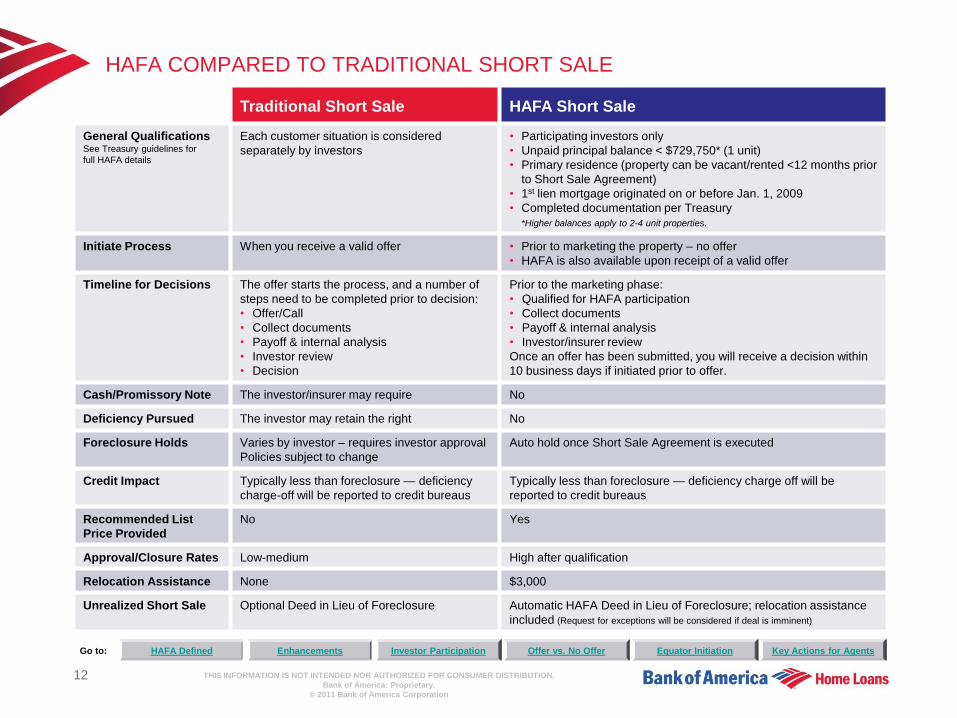

HAFA COMPARED TO TRADITIONAL SHORT SALE

12

Traditional Short Sale HAFA Short Sale

General QualificationsSee Treasury guidelines for

full HAFA details

Each customer situation is considered

separately by investors

• Participating investors only

• Unpaid principal balance < $729,750* (1 unit)

• Primary residence (property can be vacant/rented <12 months prior

to Short Sale Agreement)

• 1st lien mortgage originated on or before Jan. 1, 2009

• Completed documentation per Treasury

*Higher balances apply to 2-4 unit properties.

Initiate Process When you receive a valid offer • Prior to marketing the property – no offer

• HAFA is also available upon receipt of a valid offer

Timeline for Decisions The offer starts the process, and a number of

steps need to be completed prior to decision:

• Offer/Call

• Collect documents

• Payoff & internal analysis

• Investor review

• Decision

Prior to the marketing phase:

• Qualified for HAFA participation

• Collect documents

• Payoff & internal analysis

• Investor/insurer review

Once an offer has been submitted, you will receive a decision within

10 business days if initiated prior to offer.

Cash/Promissory Note The investor/insurer may require No

Deficiency Pursued The investor may retain the right No

Foreclosure Holds Varies by investor – requires investor approval

Policies subject to change

Auto hold once Short Sale Agreement is executed

Credit Impact Typically less than foreclosure — deficiency

charge-off will be reported to credit bureaus

Typically less than foreclosure — deficiency charge off will be

reported to credit bureaus

Recommended List

Price Provided

No Yes

Approval/Closure Rates Low-medium High after qualification

Relocation Assistance None $3,000

Unrealized Short Sale Optional Deed in Lieu of Foreclosure Automatic HAFA Deed in Lieu of Foreclosure; relocation assistance

included (Request for exceptions will be considered if deal is imminent)

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

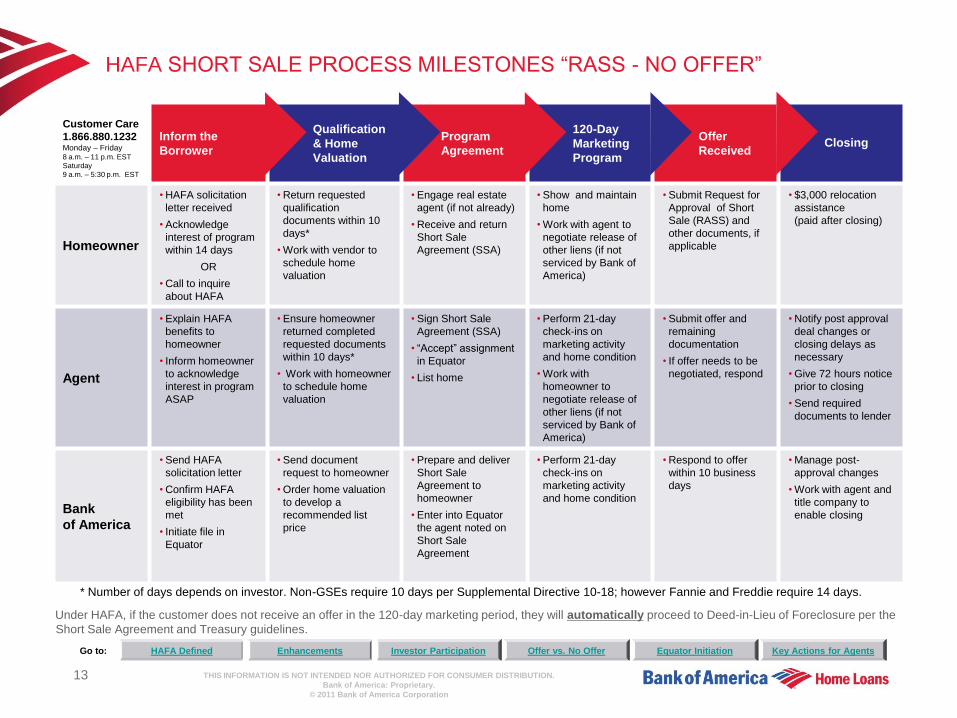

HAFA SHORT SALE PROCESS MILESTONES ―RASS - NO OFFER‖

13

Customer Care

1.866.880.1232 Monday – Friday8 a.m. – 11 p.m. EST

Saturday

9 a.m. – 5:30 p.m. EST

Inform the

Borrower

Qualification

& Home

Valuation

Program

Agreement

120-Day

Marketing

Program

Offer

ReceivedClosing

Homeowner

• HAFA solicitation

letter received

• Acknowledge

interest of program

within 14 days

OR

• Call to inquire

about HAFA

• Return requested

qualification

documents within 10

days*

• Work with vendor to

schedule home

valuation

• Engage real estate

agent (if not already)

• Receive and return

Short Sale

Agreement (SSA)

• Show and maintain

home

• Work with agent to

negotiate release of

other liens (if not

serviced by Bank of

America)

• Submit Request for

Approval of Short

Sale (RASS) and

other documents, if

applicable

• $3,000 relocation

assistance

(paid after closing)

Agent

• Explain HAFA

benefits to

homeowner

• Inform homeowner

to acknowledge

interest in program

ASAP

• Ensure homeowner

returned completed

requested documents

within 10 days*

• Work with homeowner

to schedule home

valuation

• Sign Short Sale

Agreement (SSA)

• ―Accept‖ assignment

in Equator

• List home

• Perform 21-day

check-ins on

marketing activity

and home condition

• Work with

homeowner to

negotiate release of

other liens (if not

serviced by Bank of

America)

• Submit offer and

remaining

documentation

• If offer needs to be

negotiated, respond

• Notify post approval

deal changes or

closing delays as

necessary

• Give 72 hours notice

prior to closing

• Send required

documents to lender

Bank

of America

• Send HAFA

solicitation letter

• Confirm HAFA

eligibility has been

met

• Initiate file in

Equator

• Send document

request to homeowner

• Order home valuation

to develop a

recommended list

price

• Prepare and deliver

Short Sale

Agreement to

homeowner

• Enter into Equator

the agent noted on

Short Sale

Agreement

• Perform 21-day

check-ins on

marketing activity

and home condition

• Respond to offer

within 10 business

days

• Manage post-

approval changes

• Work with agent and

title company to

enable closing

* Number of days depends on investor. Non-GSEs require 10 days per Supplemental Directive 10-18; however Fannie and Freddie require 14 days.

Under HAFA, if the customer does not receive an offer in the 120-day marketing period, they will automatically proceed to Deed-in-Lieu of Foreclosure per the

Short Sale Agreement and Treasury guidelines.

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

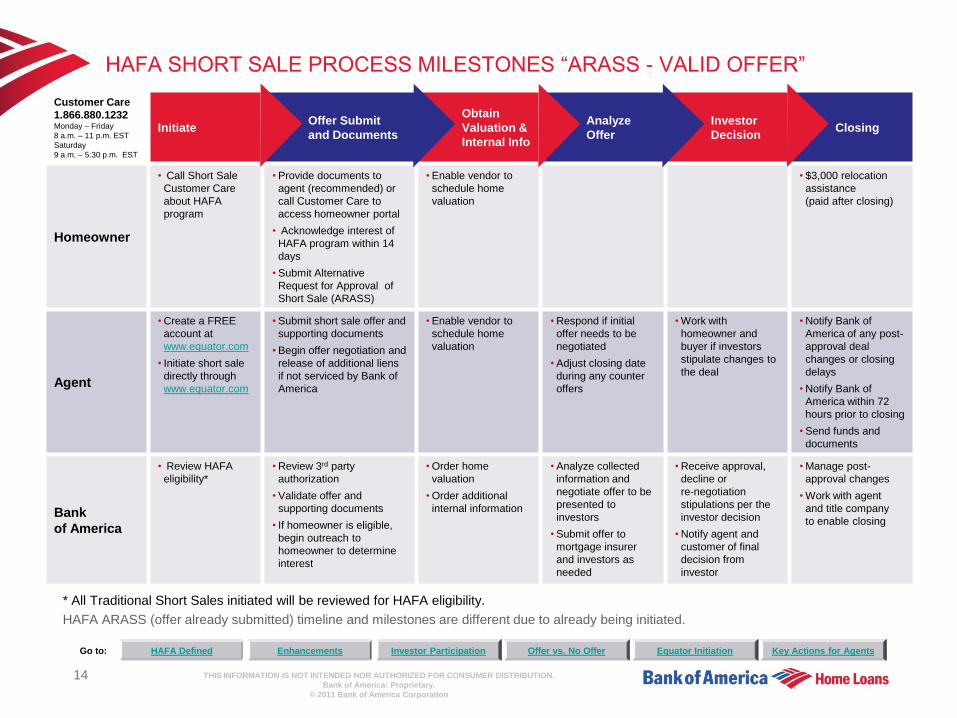

HAFA SHORT SALE PROCESS MILESTONES ―ARASS - VALID OFFER‖

* All Traditional Short Sales initiated will be reviewed for HAFA eligibility.

HAFA ARASS (offer already submitted) timeline and milestones are different due to already being initiated.

14

Customer Care

1.866.880.1232 Monday – Friday

8 a.m. – 11 p.m. EST

Saturday

9 a.m. – 5:30 p.m. EST

InitiateOffer Submit

and Documents

Obtain

Valuation &

Internal Info

Analyze

Offer

Investor

DecisionClosing

Homeowner

• Call Short Sale

Customer Care

about HAFA

program

• Provide documents to

agent (recommended) or

call Customer Care to

access homeowner portal

• Acknowledge interest of

HAFA program within 14

days

• Submit Alternative

Request for Approval of

Short Sale (ARASS)

• Enable vendor to

schedule home

valuation

• $3,000 relocation

assistance

(paid after closing)

Agent

• Create a FREE

account at

www.equator.com

• Initiate short sale

directly through

www.equator.com

• Submit short sale offer and

supporting documents

• Begin offer negotiation and

release of additional liens

if not serviced by Bank of

America

• Enable vendor to

schedule home

valuation

• Respond if initial

offer needs to be

negotiated

• Adjust closing date

during any counter

offers

• Work with

homeowner and

buyer if investors

stipulate changes to

the deal

• Notify Bank of

America of any post-

approval deal

changes or closing

delays

• Notify Bank of

America within 72

hours prior to closing

• Send funds and

documents

Bank

of America

• Review HAFA

eligibility*

• Review 3rd party

authorization

• Validate offer and

supporting documents

• If homeowner is eligible,

begin outreach to

homeowner to determine

interest

• Order home

valuation

• Order additional

internal information

• Analyze collected

information and

negotiate offer to be

presented to

investors

• Submit offer to

mortgage insurer

and investors as

needed

• Receive approval,

decline or

re-negotiation

stipulations per the

investor decision

• Notify agent and

customer of final

decision from

investor

• Manage post-

approval changes

• Work with agent

and title company

to enable closing

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

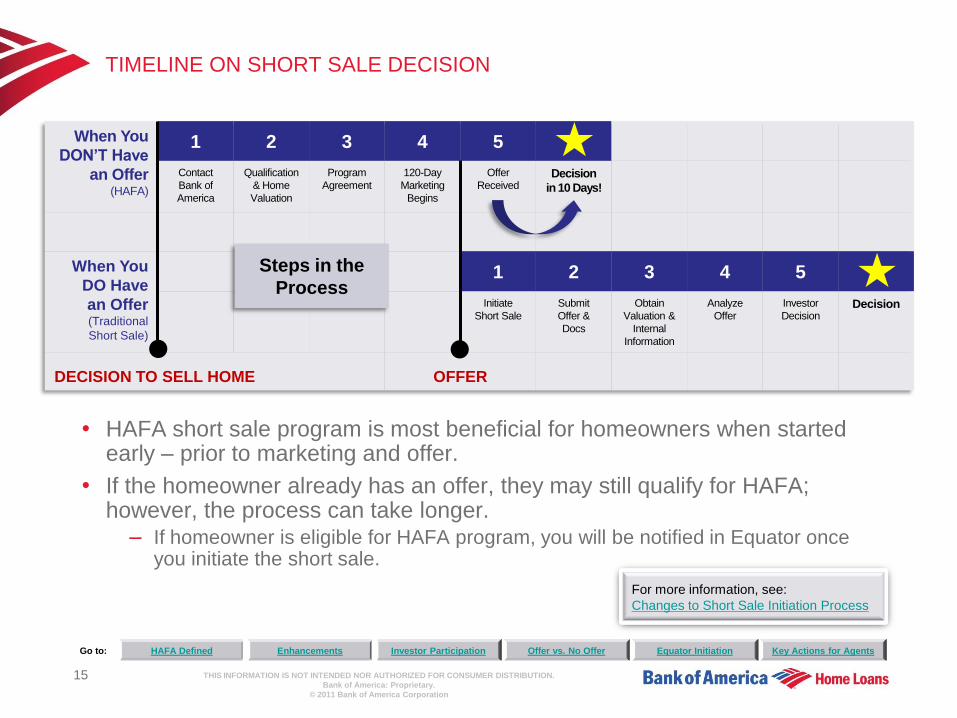

TIMELINE ON SHORT SALE DECISION

• HAFA short sale program is most beneficial for homeowners when started early – prior to marketing and offer.

• If the homeowner already has an offer, they may still qualify for HAFA; however, the process can take longer.

– If homeowner is eligible for HAFA program, you will be notified in Equator once you initiate the short sale.

15

When You

DON’T Have

an Offer (HAFA)

1 2 3 4 5

Contact

Bank of

America

Qualification

& Home

Valuation

Program

Agreement

120-Day

Marketing

Begins

Offer

ReceivedDecision

in 10 Days!

When You

DO Have

an Offer (Traditional

Short Sale)

1 2 3 4 5

Initiate

Short Sale

Submit

Offer &

Docs

Obtain

Valuation &

Internal

Information

Analyze

Offer

Investor

DecisionDecision

DECISION TO SELL HOME OFFER

Steps in the

Process

For more information, see:

Changes to Short Sale Initiation Process

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

EQUATOR INITIATION – NO OFFER

16

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE EQUATOR

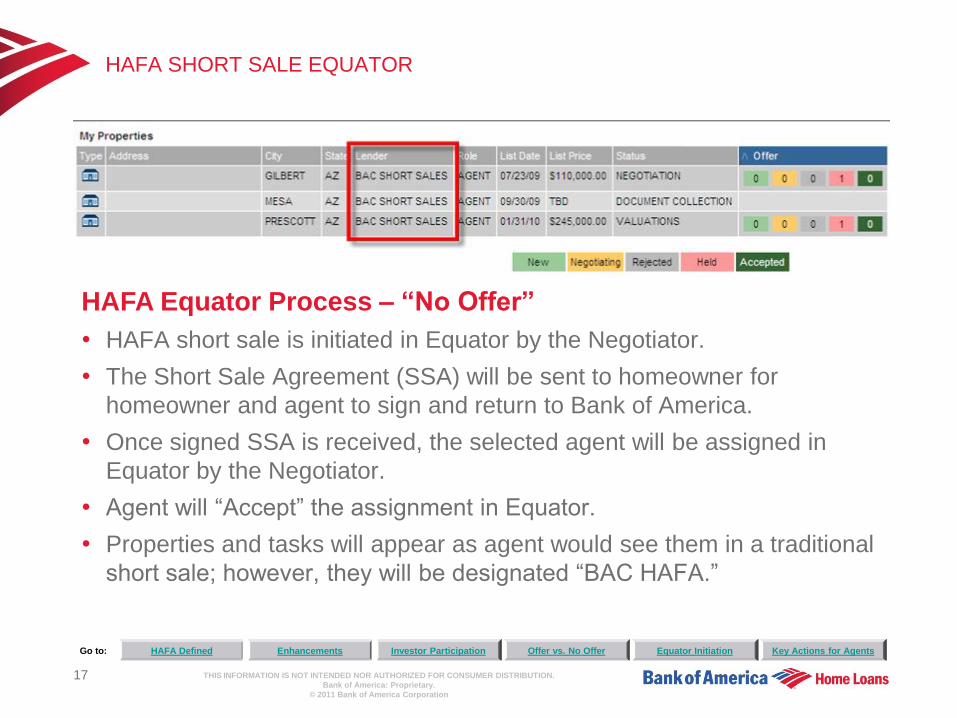

HAFA Equator Process – “No Offer”

• HAFA short sale is initiated in Equator by the Negotiator.

• The Short Sale Agreement (SSA) will be sent to homeowner for

homeowner and agent to sign and return to Bank of America.

• Once signed SSA is received, the selected agent will be assigned in

Equator by the Negotiator.

• Agent will ―Accept‖ the assignment in Equator.

• Properties and tasks will appear as agent would see them in a traditional

short sale; however, they will be designated ―BAC HAFA.‖

17

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

HAFA SHORT SALE EQUATOR

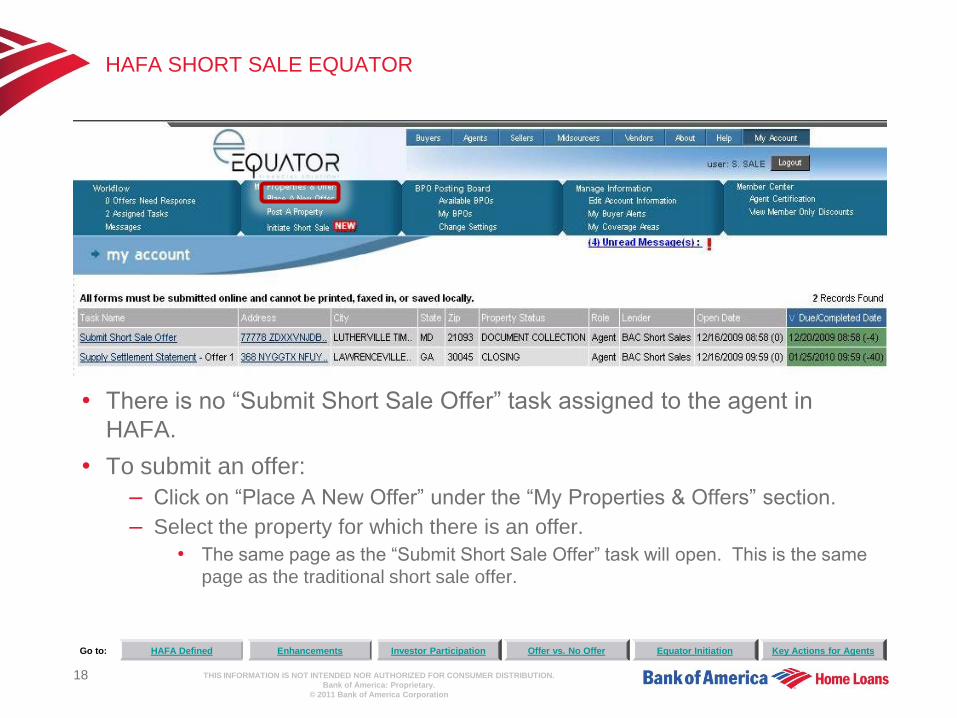

• There is no ―Submit Short Sale Offer‖ task assigned to the agent in

HAFA.

• To submit an offer:

– Click on ―Place A New Offer‖ under the ―My Properties & Offers‖ section.

– Select the property for which there is an offer.

• The same page as the ―Submit Short Sale Offer‖ task will open. This is the same

page as the traditional short sale offer.

18

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

3 KEY ACTIONS FOR AGENTS

19

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

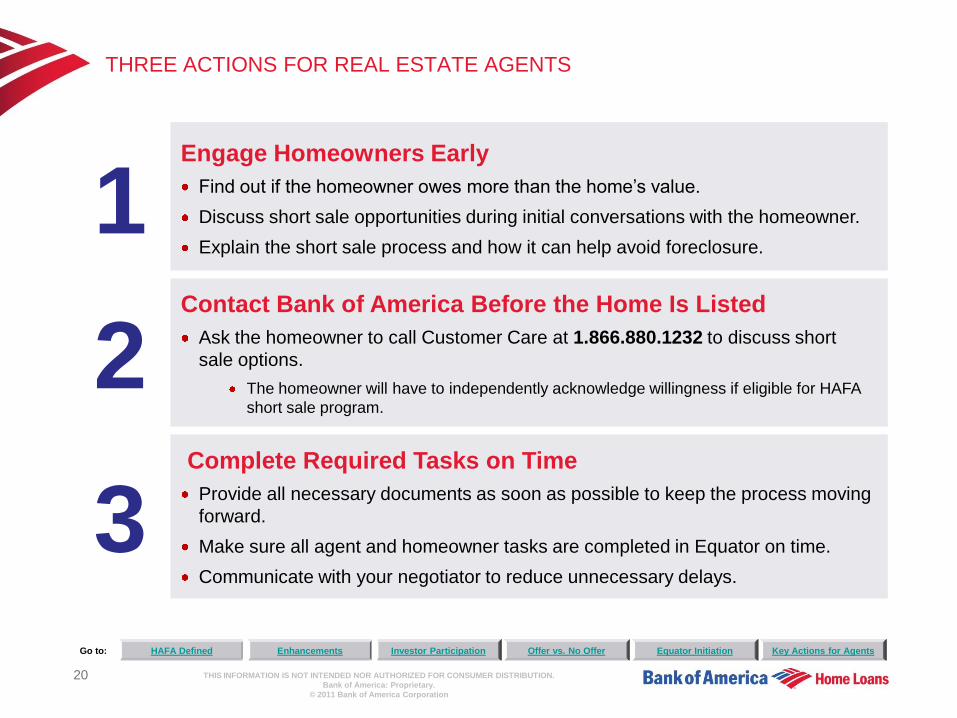

THREE ACTIONS FOR REAL ESTATE AGENTS

20

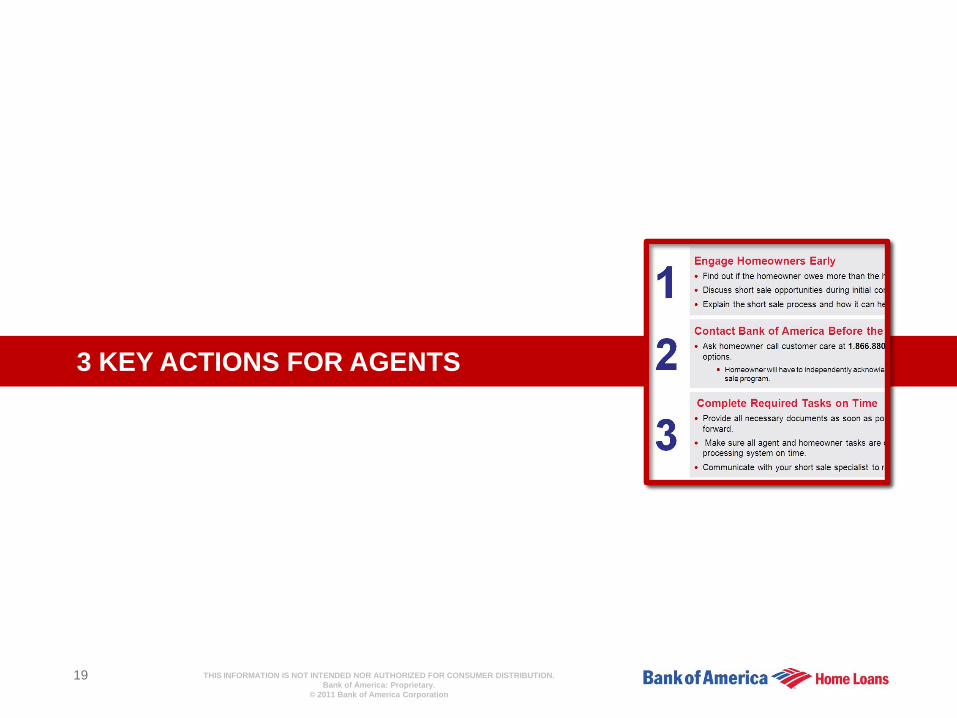

1Engage Homeowners Early

Find out if the homeowner owes more than the home’s value.

Discuss short sale opportunities during initial conversations with the homeowner.

Explain the short sale process and how it can help avoid foreclosure.

2Contact Bank of America Before the Home Is Listed

Ask the homeowner to call Customer Care at 1.866.880.1232 to discuss short

sale options.

The homeowner will have to independently acknowledge willingness if eligible for HAFA

short sale program.

3Complete Required Tasks on Time

Provide all necessary documents as soon as possible to keep the process moving

forward.

Make sure all agent and homeowner tasks are completed in Equator on time.

Communicate with your negotiator to reduce unnecessary delays.

THIS INFORMATION IS NOT INTENDED NOR AUTHORIZED FOR CONSUMER DISTRIBUTION.

Bank of America: Proprietary.

© 2011 Bank of America Corporation

Go to: HAFA Defined Enhancements Investor Participation Offer vs. No Offer Equator Initiation Key Actions for Agents

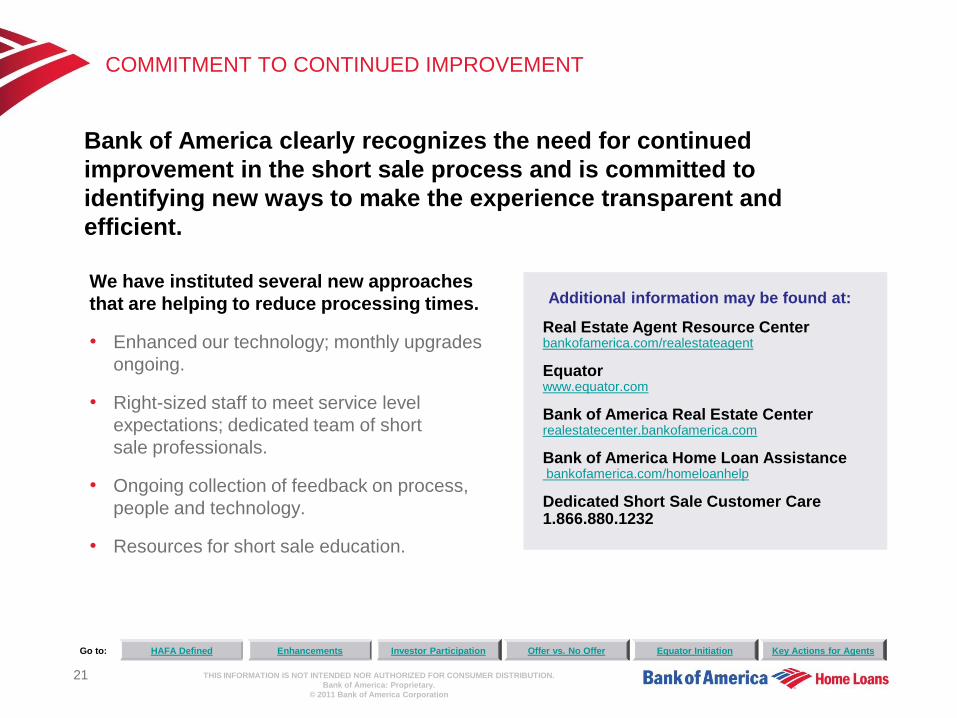

Additional information may be found at:

Real Estate Agent Resource Centerbankofamerica.com/realestateagent

Equatorwww.equator.com

Bank of America Real Estate Centerrealestatecenter.bankofamerica.com

Bank of America Home Loan Assistancebankofamerica.com/homeloanhelp

Dedicated Short Sale Customer Care 1.866.880.1232

COMMITMENT TO CONTINUED IMPROVEMENT

21

Bank of America clearly recognizes the need for continued

improvement in the short sale process and is committed to

identifying new ways to make the experience transparent and

efficient.

We have instituted several new approaches

that are helping to reduce processing times.

• Enhanced our technology; monthly upgrades

ongoing.

• Right-sized staff to meet service level

expectations; dedicated team of short

sale professionals.

• Ongoing collection of feedback on process,

people and technology.

• Resources for short sale education.