Embed Size (px)

Citation preview

22 irishfunds.ie

Hong Kong Exchanges and Clearing Limited

Kevin Rideout

Welcome Address

33 irishfunds.ie

Irish Funds

Kieran Fox

Welcome Address

44 irishfunds.ie

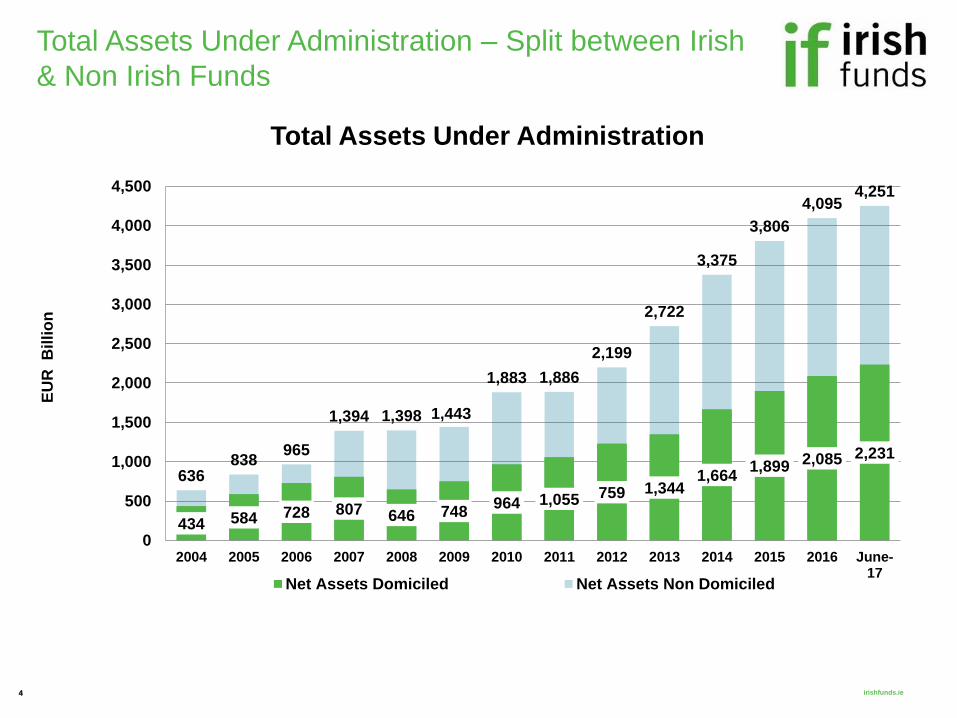

Total Assets Under Administration – Split between Irish

& Non Irish Funds

434 584 728 807 646 748964 1,055 759 1,344

1,6641,899 2,085 2,231

636838

965

1,394 1,398 1,443

1,883 1,886

2,199

2,722

3,375

3,806

4,0954,251

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 June-17

EU

R

Billi

on

Total Assets Under Administration

Net Assets Domiciled Net Assets Non Domiciled

55 irishfunds.ie

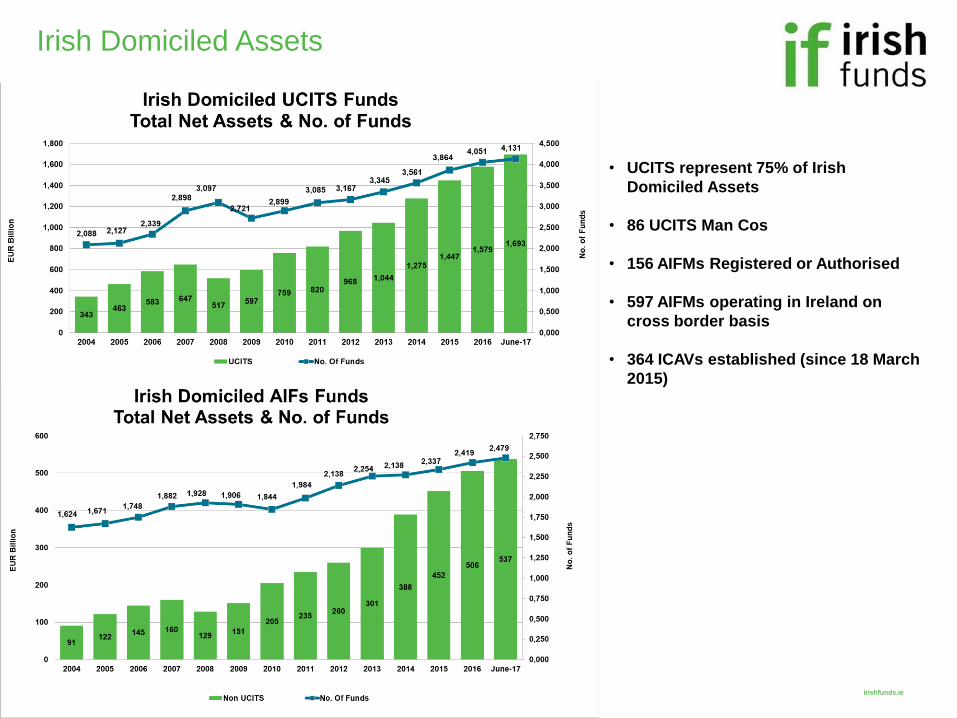

Irish Domiciled Assets

• UCITS represent 75% of Irish

Domiciled Assets

• 86 UCITS Man Cos

• 156 AIFMs Registered or Authorised

• 597 AIFMs operating in Ireland on

cross border basis

• 364 ICAVs established (since 18 March

2015)

66 irishfunds.ie

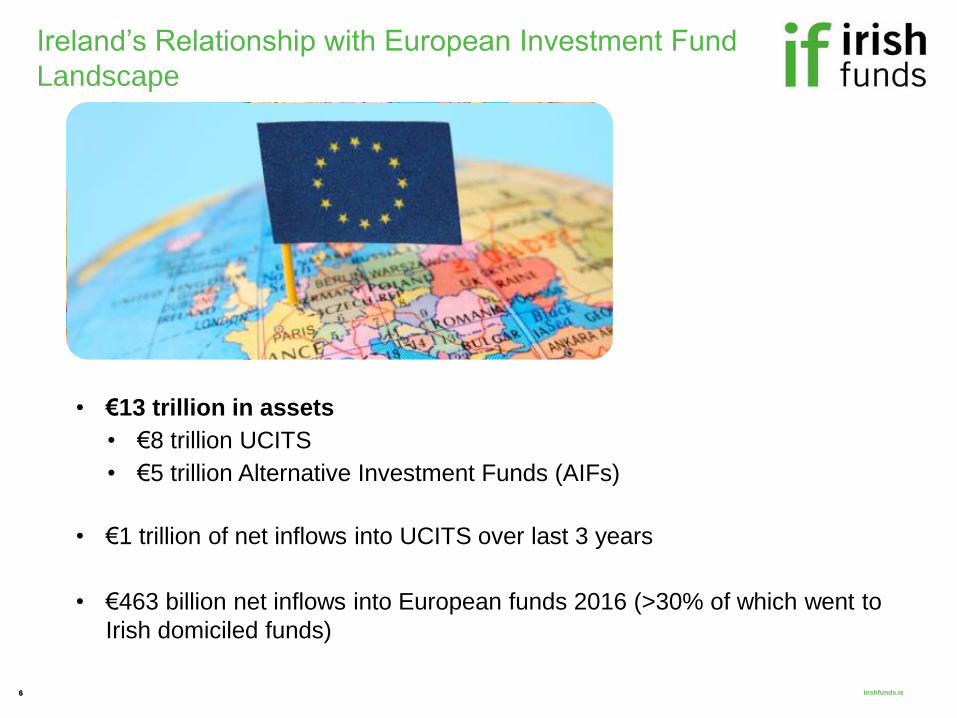

Ireland’s Relationship with European Investment Fund

Landscape

• €13 trillion in assets

• €8 trillion UCITS

• €5 trillion Alternative Investment Funds (AIFs)

• €1 trillion of net inflows into UCITS over last 3 years

• €463 billion net inflows into European funds 2016 (>30% of which went to

Irish domiciled funds)

77 irishfunds.ie

Growth of Largest European Fund Domiciles

2012 2013 2014 2015 2016

Europe 113 123 142 158 178

Luxembourg 114 125 148 167 177

Ireland 116 127 157 180 198

France 109 110 114 121 129

Germany 113 124 140 153 166

UK 117 135 159 179 177

-

50

100

150

200

250

% G

row

th

116 127157

180198

Source: EFAMA Statistics

88 irishfunds.ie

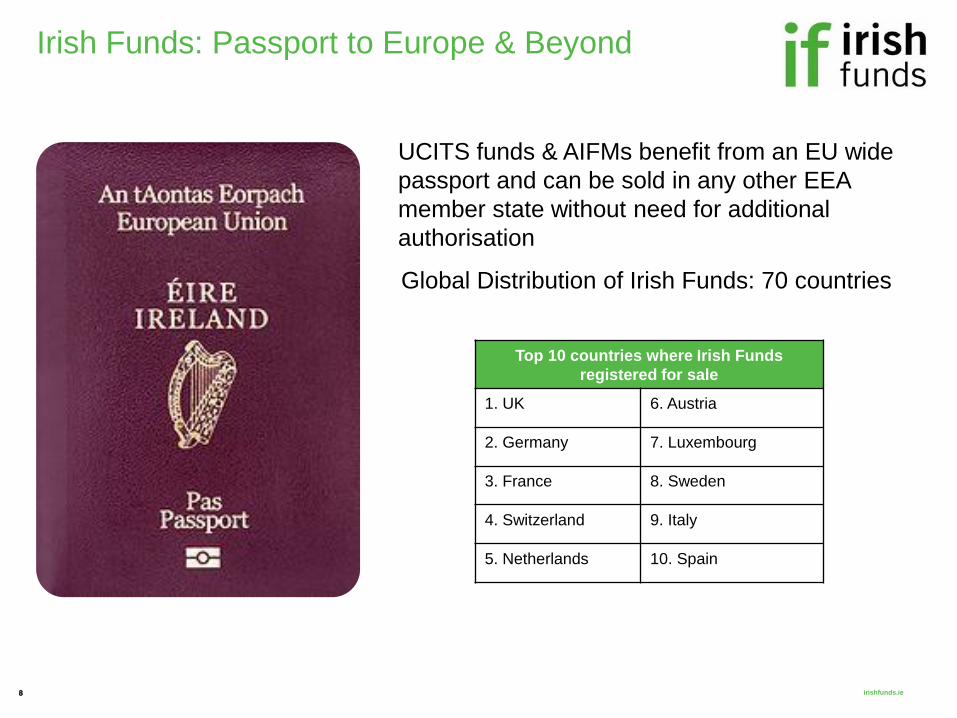

Irish Funds: Passport to Europe & Beyond

UCITS funds & AIFMs benefit from an EU wide

passport and can be sold in any other EEA

member state without need for additional

authorisation

Top 10 countries where Irish Funds

registered for sale

1. UK 6. Austria

2. Germany 7. Luxembourg

3. France 8. Sweden

4. Switzerland 9. Italy

5. Netherlands 10. Spain

Global Distribution of Irish Funds: 70 countries

99 irishfunds.ie

Irish Funds – Maximising Distribution

1010 irishfunds.ie

Irish Domiciled Funds – Net Sales

-30.0

20.0

70.0

120.0

170.0

Dec-13 Dec-14 Dec-15 Dec-16 YTD June2017

Net Sales into Irish funds by type € Bn

Equity Funds

Bond Funds

Balanced Funds

Money MarketFunds

AIF

Net sales for

YTD June 2017

have already

surpassed the

total for 2016 –

which itself was

a record year

98,46385,465

135,668114,706

139,416161,500

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2012 2013 2014 2015 2016 YTD June2017

EU

R M

n

Net Sales - Total Domiciled Funds

Net Sales - Total Domiciled Funds

1111 irishfunds.ie

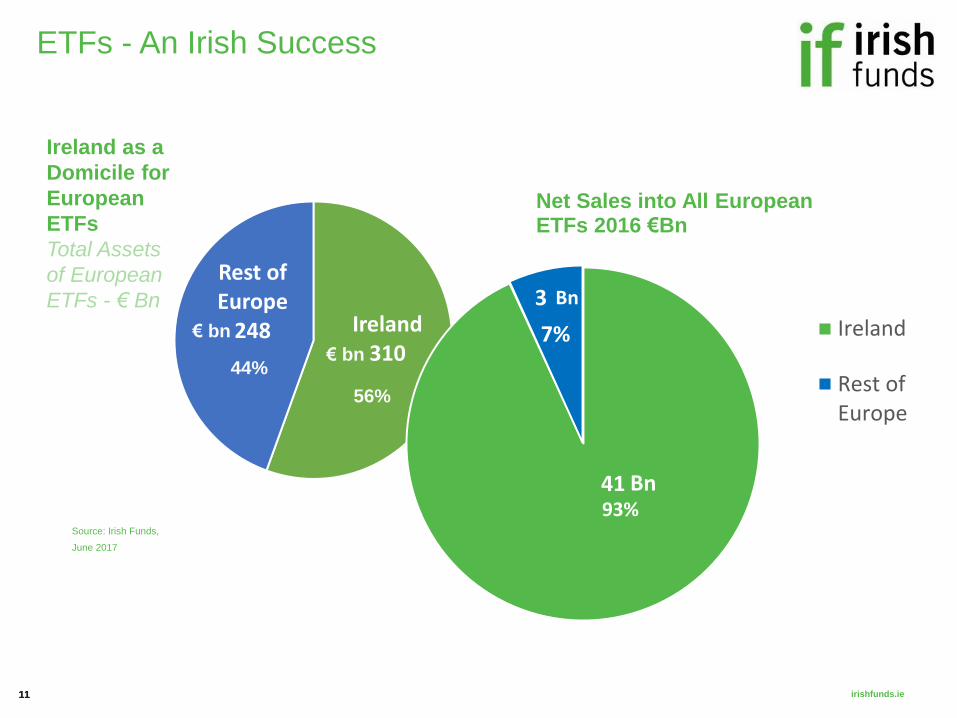

ETFs - An Irish Success

Ireland as a

Domicile for

European

ETFs

Total Assets

of European

ETFs - € Bn

Source: Irish Funds,

June 2017

Ireland310

Rest of Europe

248€ bn

56%

44%

€ bn

41

3

Net Sales into All European ETFs 2016 €Bn

Ireland

Rest ofEurope

Bn93%

7%

Bn

1212 irishfunds.ie

Looking Ahead - Technology

1313 irishfunds.ie

Looking Ahead – Brexit

Three interdependent themes

Distribution

Management

Models

(‘Delegation’)

Growth

OVER 2,000 IRISH

FUNDS SOLD TO UK

INVESTORS1

€613 bn2 IN IRISH FUND

ASSETS MANAGED BY

170+ UK FIRMS IN

IRELAND2

Continuity in UK investor

access to EU/Irish funds

Continuity in

UK firm

management

of Irish funds

Increase Ireland’s growth

trajectory as an

international asset

management centre

SOURCE: 1-Lipper IM Dec 2015

2-Monterrey Ireland Fund Report 2016

Current context Target outcome

1414 irishfunds.ie

International asset management centre

Growth

‘The Basics’

•Predictability / efficiency of regulatory process

•12.5% corporate tax rate

•Common law system

•Only English-speaking country in the Eurozone

•Less expensive than Zurich, Paris & Luxembourg1

Asset Manager Activity

Infra-structure

Re-affirm Ireland’s attractiveness as an

international asset management centreOpportunity

Benefits

SolutionProvide UK managers with options to support the

establishment of a physical presence in Ireland

NOTES:

1. Source PwC

2. http://www.iaim.ie/why-ireland (STEM = Science, Technology, Engineering &

Mathematics) & http://www.hea.ie/sites/default/files/awards_-

_all_undergraduate_by_level_and_field.xlsx

3. IFS 2020 Action Plan 2017 (http://finance.gov.ie) & IDA Ireland

4. MiFID firms, UCITS ManCos, Irish AIFMs & Non-Irish AIFMs

• Space for 100K new employees by 2020, 100K new houses3

• Leading global tech centre & fintech location

• London-Dublin: Most flight options in Europe

• 35K+ employed in international financial services in Ireland, 14K in funds industry

• 130K degree-level graduates across business, law and STEM w/ 20K new grads p.a.2

• 800+ investment firms active in Ireland4

• Increased presence of front office activities

• 18 of the top 20 global AMs have Irish funds

• €4trn total AuA, €300bn managed from Ireland2

• AM counterparties already in transit from UK

1515

Moderator:

Panellists:

irishfunds.ie

Hong Kong Equity Capital Market Update

Panel One

Tae Yoo, HKEX

Conor O’Mara, Jefferies

Patrick Wong, HSBC

Michelle Lloyd, Maples and Calder

Panellists

Moderator

1616 irishfunds.ie

Barnaby Nelson, Standard Chartered

Julien Martin, Bond Connect Company & HKEX

Bond Connect Update

Fireside Chat

1717 irishfunds.ie

Northern Trust

Ian Headon

Are Alternatives Becoming Mainstream? How to get ahead by leveraging the Evolving Product & Regulatory Environment

1818 irishfunds.ie

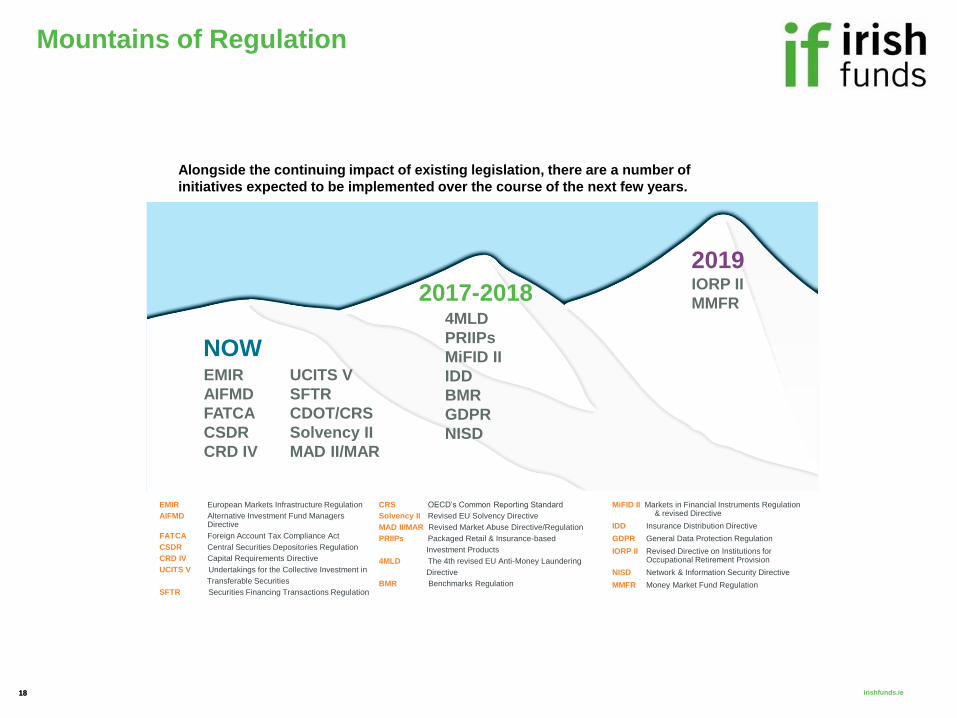

Mountains of Regulation

Alongside the continuing impact of existing legislation, there are a number of

initiatives expected to be implemented over the course of the next few years.

EMIR European Markets Infrastructure Regulation

AIFMD Alternative Investment Fund Managers Directive

FATCA Foreign Account Tax Compliance Act

CSDR Central Securities Depositories Regulation

CRD IV Capital Requirements Directive

UCITS V Undertakings for the Collective Investment in

Transferable Securities

SFTR Securities Financing Transactions Regulation

CRS OECD’s Common Reporting Standard

Solvency II Revised EU Solvency Directive

MAD II/MAR Revised Market Abuse Directive/Regulation

PRIIPs Packaged Retail & Insurance-based

Investment Products

4MLD The 4th revised EU Anti-Money Laundering

Directive

BMR Benchmarks Regulation

MiFID II Markets in Financial Instruments Regulation & revised Directive

IDD Insurance Distribution Directive

GDPR General Data Protection Regulation

IORP II Revised Directive on Institutions for Occupational Retirement Provision

NISD Network & Information Security Directive

MMFR Money Market Fund Regulation

4MLD

PRIIPs

MiFID II

IDD

BMR

GDPR

NISD

2017-2018IORP II

MMFR

2019

EMIR

AIFMD

FATCA

CSDR

CRD IV

NOWUCITS V

SFTR

CDOT/CRS

Solvency II

MAD II/MAR

1919 irishfunds.ie

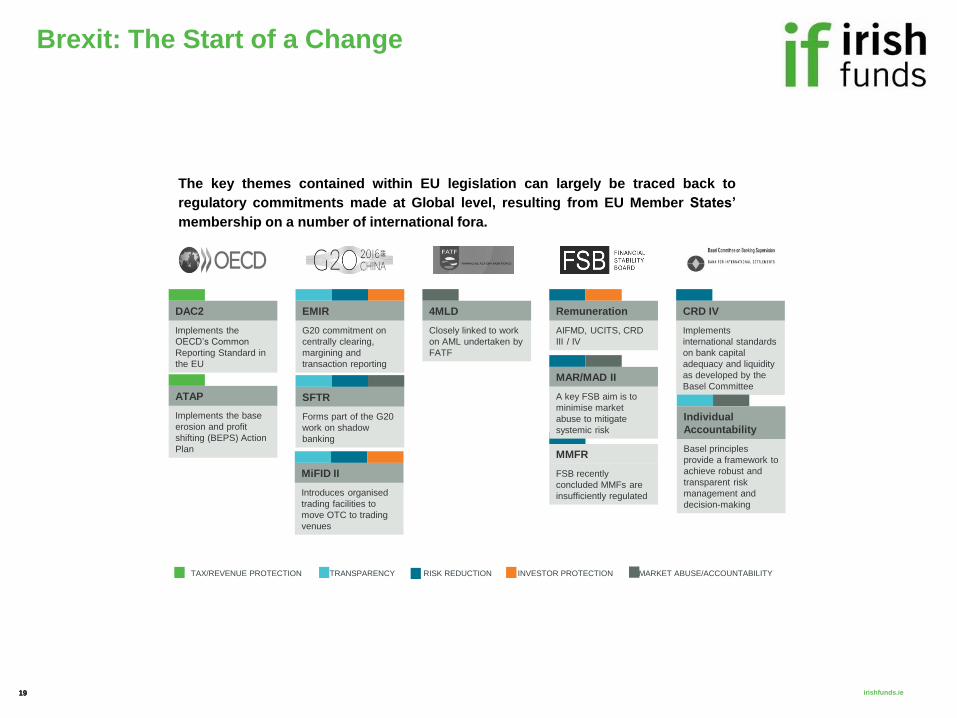

Brexit: The Start of a Change

The key themes contained within EU legislation can largely be traced back to

regulatory commitments made at Global level, resulting from EU Member States’

membership on a number of international fora.

TAX/REVENUE PROTECTION TRANSPARENCY RISK REDUCTION INVESTOR PROTECTION MARKET ABUSE/ACCOUNTABILITY

DAC2

Implements the

OECD’s Common

Reporting Standard in

the EU

EMIR

G20 commitment on

centrally clearing,

margining and

transaction reporting

4MLD

Closely linked to work

on AML undertaken by

FATF

CRD IV

Implements

international standards

on bank capital

adequacy and liquidity

as developed by the

Basel CommitteeATAP

Implements the base

erosion and profit

shifting (BEPS) Action

Plan

SFTR

Forms part of the G20

work on shadow

banking

Remuneration

AIFMD, UCITS, CRD

III / IV

MMFR

FSB recently

concluded MMFs are

insufficiently regulated

MAR/MAD II

A key FSB aim is to

minimise market

abuse to mitigate

systemic risk

Individual

Accountability

Basel principles

provide a framework to

achieve robust and

transparent risk

management and

decision-making

MiFID II

Introduces organised

trading facilities to

move OTC to trading

venues

2020 irishfunds.ie

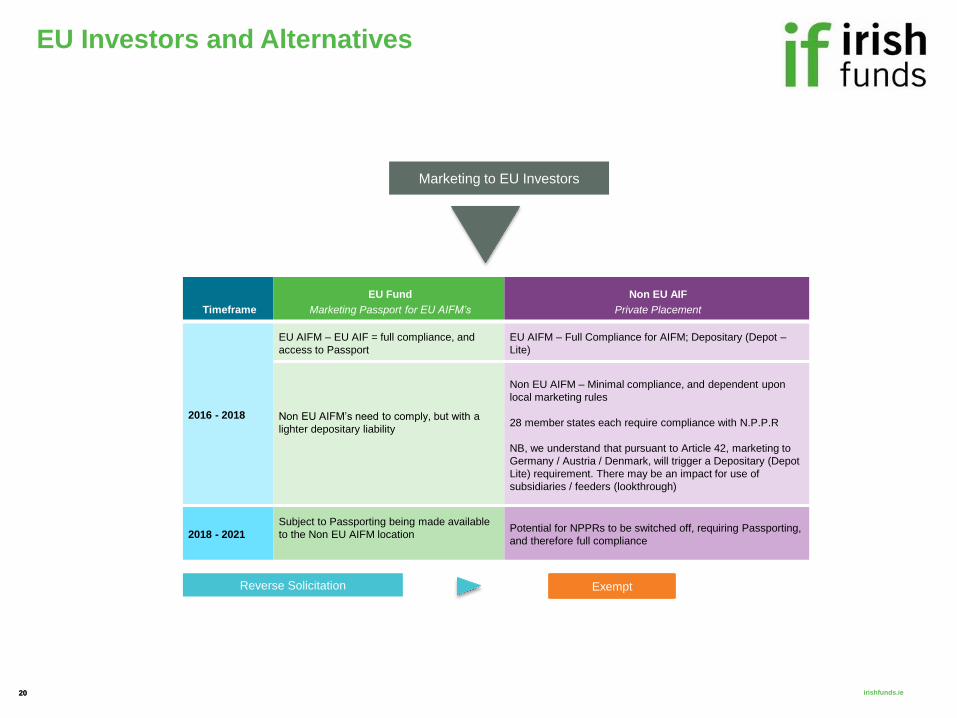

EU Investors and Alternatives

Marketing to EU Investors

Reverse Solicitation Exempt

Timeframe

EU Fund

Marketing Passport for EU AIFM’s

Non EU AIF

Private Placement

2016 - 2018

EU AIFM – EU AIF = full compliance, and

access to Passport

EU AIFM – Full Compliance for AIFM; Depositary (Depot –

Lite)

Non EU AIFM’s need to comply, but with a

lighter depositary liability

Non EU AIFM – Minimal compliance, and dependent upon

local marketing rules

28 member states each require compliance with N.P.P.R

NB, we understand that pursuant to Article 42, marketing to

Germany / Austria / Denmark, will trigger a Depositary (Depot

Lite) requirement. There may be an impact for use of

subsidiaries / feeders (lookthrough)

2018 - 2021

Subject to Passporting being made available

to the Non EU AIFM locationPotential for NPPRs to be switched off, requiring Passporting,

and therefore full compliance

2121 irishfunds.ie

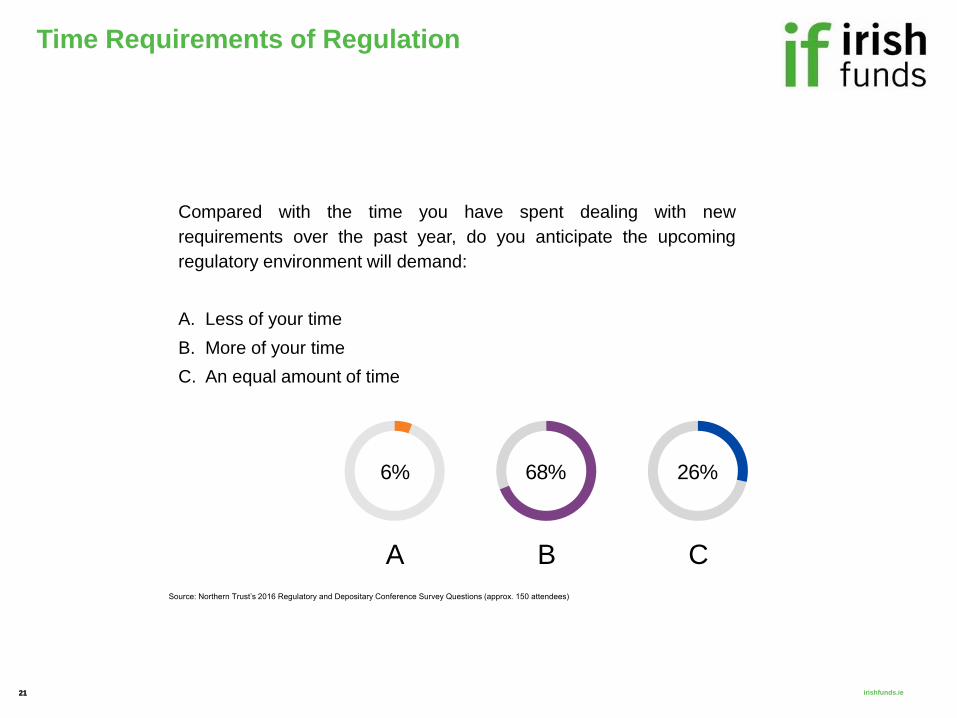

Time Requirements of Regulation

Compared with the time you have spent dealing with new

requirements over the past year, do you anticipate the upcoming

regulatory environment will demand:

A. Less of your time

B. More of your time

C. An equal amount of time

Source: Northern Trust’s 2016 Regulatory and Depositary Conference Survey Questions (approx. 150 attendees)

A B C

6% 68% 26%

2222 irishfunds.ie

Marketing Passport Extension

Do you think that the potential extension of a marketing passport to

third country funds and managers:

A. Presents a significant opportunity

for your distribution network

B. Is irrelevant to your asset

gathering strategy

C. Depends on the outcome of

Brexit discussions

Source: Northern Trust’s 2016 Regulatory and Depositary Conference Survey Questions (approx. 150 attendees)

C

B

A 16%

21%

64%

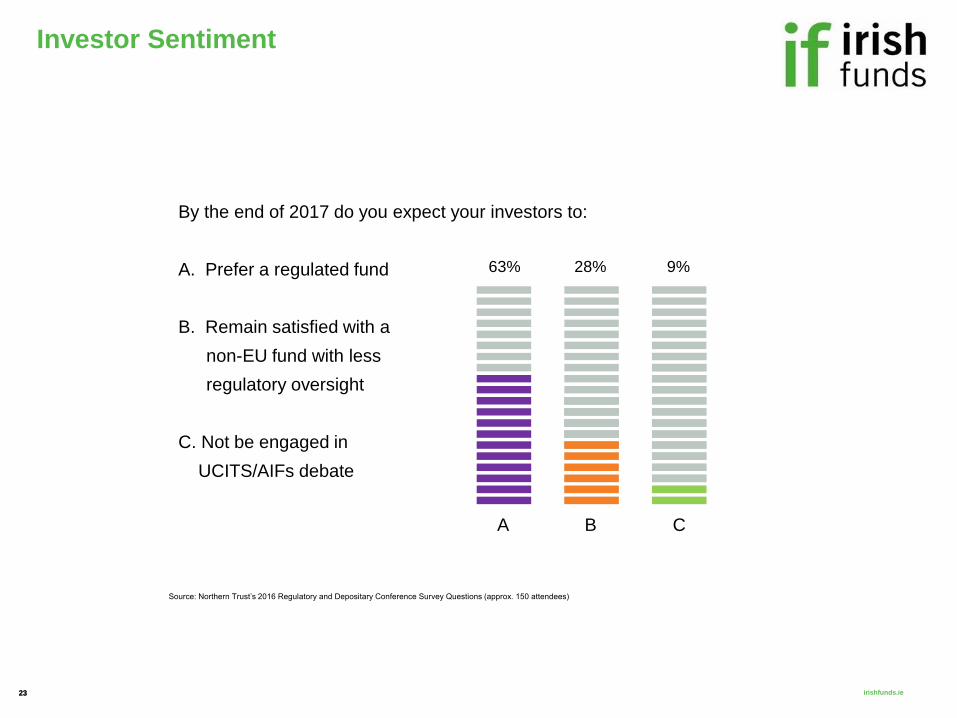

2323 irishfunds.ie

By the end of 2017 do you expect your investors to:

A. Prefer a regulated fund

B. Remain satisfied with a

non-EU fund with less

regulatory oversight

C. Not be engaged in

UCITS/AIFs debate

Investor Sentiment

Source: Northern Trust’s 2016 Regulatory and Depositary Conference Survey Questions (approx. 150 attendees)

63% 28% 9%

A B C

2424 irishfunds.ie

Fund Structure Preference

15 28 32 63

31

3527

28

54

3741

9

0

10

20

30

40

50

60

70

80

90

100

2013 2014 2015 2016

% InvestorEngagement

Not engaged in debate Offshore non EU fund (eg Cayman)

Source: Northern Trust’s 2016 Regulatory and Depositary Conference Survey Questions (approx. 150 attendees)

2525 irishfunds.ie

Conclusions

2626 irishfunds.ie

Thank You

2727

Moderator:

Panellists:

irishfunds.ie

Are Alternatives Becoming Mainstream?

Panel Two

Paul Moloney, Eversheds

Paul Martin, PwC

Patrick Robinson, Bridge Consulting

Clive Bellows, Northern Trust

Panellists

Moderator

2828 irishfunds.ie

Irish Consul General to Hong Kong and Macau

Peter Ryan

Closing Remarks

2929 irishfunds.ie

Drinks Reception

Kindly Sponsored by Northern Trust