Embed Size (px)

DESCRIPTION

Horizon Risk and Interest Rate Risk. Chapter 21. Background. This chapter analyzes default-free bonds Evaluates prices relative to changing interest rates and maturity Horizon risk increases with the time remaining until a bond matures - PowerPoint PPT Presentation

Citation preview

Francis & Ibbotson Chapter 21: Interest Rate Risk and Horizon Risk 11

Slides by:

Pamela L. Hall, Western Washington University

Horizon Risk and Interest Rate Horizon Risk and Interest Rate Risk Risk

Chapter 21

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 22

BackgroundBackground

This chapter analyzes default-free bonds– Evaluates prices relative to changing

interest rates and maturity

Horizon risk increases with the time remaining until a bond matures

Interest rate risk increases with the size of a bond’s price fluctuation when its YTM changes

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 33

Present Value of a BondPresent Value of a Bond

The present value of a bond is determined by the following equation:

1 2 T

1 2 T

ParCoupon Coupon CouponPV

1 discount rate 1 discount rate 1 discount rate

Even though a bond’s par, maturity and coupon rate may be fixed The bond’s price varies over time

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 44

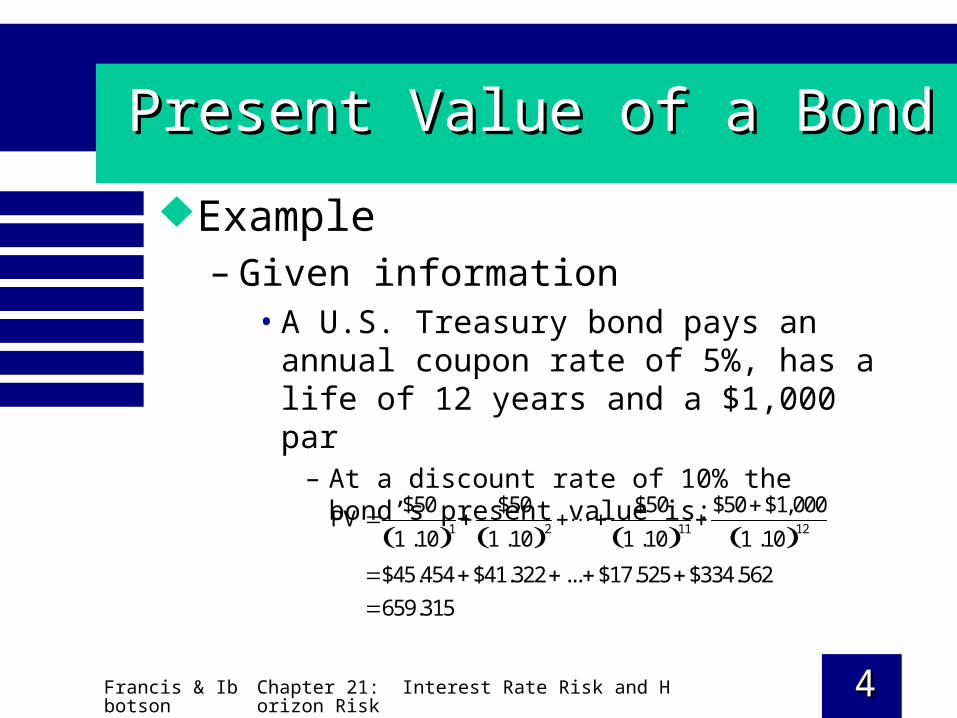

Present Value of a BondPresent Value of a Bond

Example– Given information

• A U.S. Treasury bond pays an annual coupon rate of 5%, has a life of 12 years and a $1,000 par

– At a discount rate of 10% the bond’s present value is:

1 2 11 12

$50 $50 $50 $50 $1,000PV

1 .10 1 .10 1 .10 1 .10

$45.454 $41.322 ... $17.525 $334.562

659.315

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 55

Present Value of a BondPresent Value of a Bond

Bond prices vary due to fluctuating market interest rates– As a bond’s YTM increases its price

decreases• The size of the fluctuations depends on the

bond’s time horizon and coupon rate

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 66

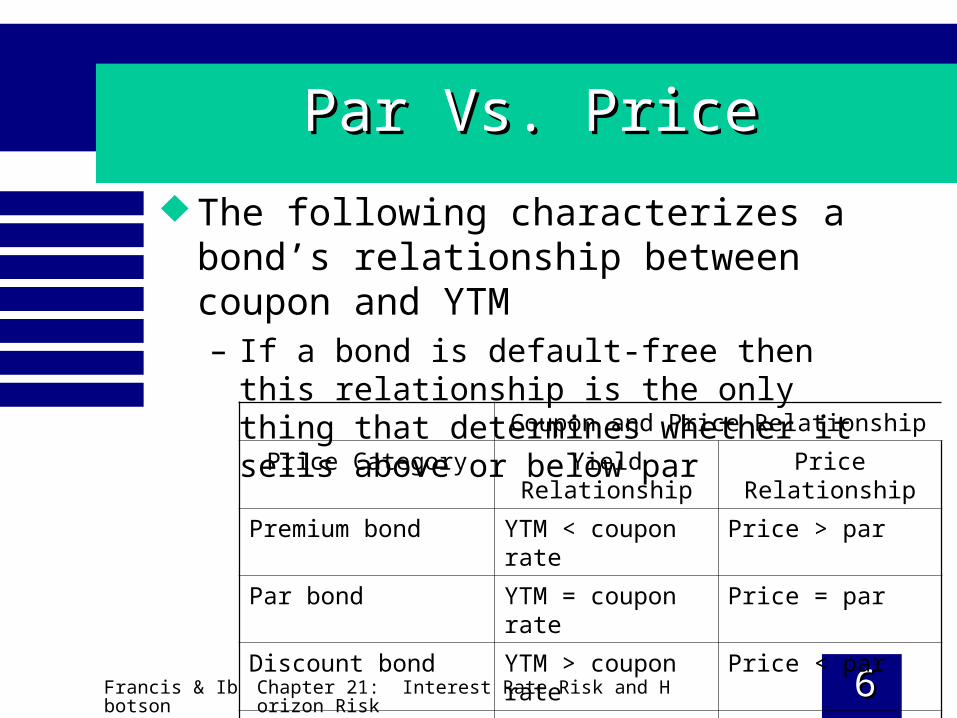

Par Vs. PricePar Vs. Price

The following characterizes a bond’s relationship between coupon and YTM– If a bond is default-free then this relationship is

the only thing that determines whether it sells above or below par

Coupon and Price Relationship

Price Category Yield Relationship Price Relationship

Premium bond YTM < coupon rate Price > par

Par bond YTM = coupon rate Price = par

Discount bond YTM > coupon rate Price < par

Zero coupon bond Zero coupons Price < par

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 77

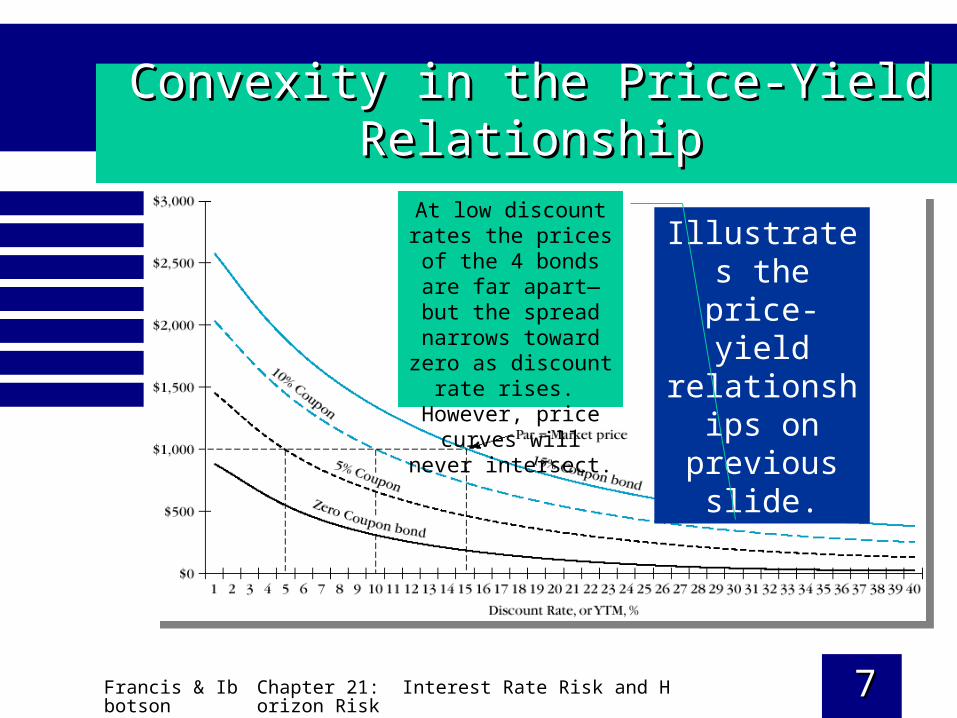

Convexity in the Price-Yield RelationshipConvexity in the Price-Yield Relationship

Illustrates the price-yield

relationships on previous

slide.

At low discount rates the prices of the 4

bonds are far apart—but the spread narrows toward zero as discount

rate rises. However, price curves will never

intersect.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 88

Convexity in the Price-Yield RelationshipConvexity in the Price-Yield Relationship

The shape of a bond’s price-yield relationship offers information about bond’s interest rate risk– Interest rate risk—variability in a bond’s

price due to fluctuating interest rates

Price-yield relationship is more convex for – Longer maturities– Lower coupons

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 99

The Coupon EffectThe Coupon Effect

A bond’s coupon rate impacts its YTM YTM depends on:

– Term structure of interest rates

– Size and timing of coupons

– Bond’s time horizon

Bonds with low coupons receive more of their value from its principal payments– Involve more interest rate risk

• Thus have more convexity

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1010

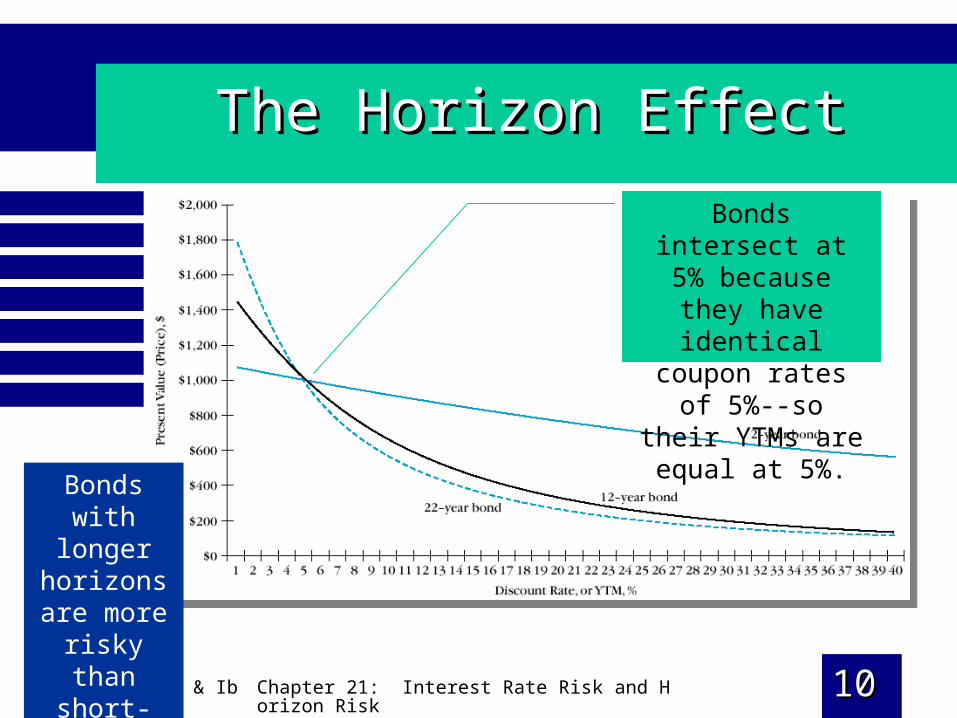

The Horizon EffectThe Horizon Effect

Bonds with longer

horizons are more risky than short-term bonds.

Bonds intersect at 5% because they have

identical coupon rates of 5%--so their YTMs

are equal at 5%.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1111

Hedging Fixed Income InstrumentsHedging Fixed Income Instruments

Even someone who invests in default-free fixed-income securities face risk– Reinvestment risk– Price fluctuation risk

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1212

Reinvestment RiskReinvestment Risk

Variability of return resulting from reinvestment of a bond’s coupon at fluctuating interest rates– Can be avoided by investing in zero

coupon bonds

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1313

Hedging Bond Price Fluctuation RiskHedging Bond Price Fluctuation Risk

Rational bond investors may wish to hedge price fluctuation risk– Hedge—a combination of investments

designed to reduce or avoid risk• Hedged portfolios usually earn lower rates of

return than unhedged portfolios– Perfect hedges result when returns from long and

short positions of equal value exactly offset each other

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1414

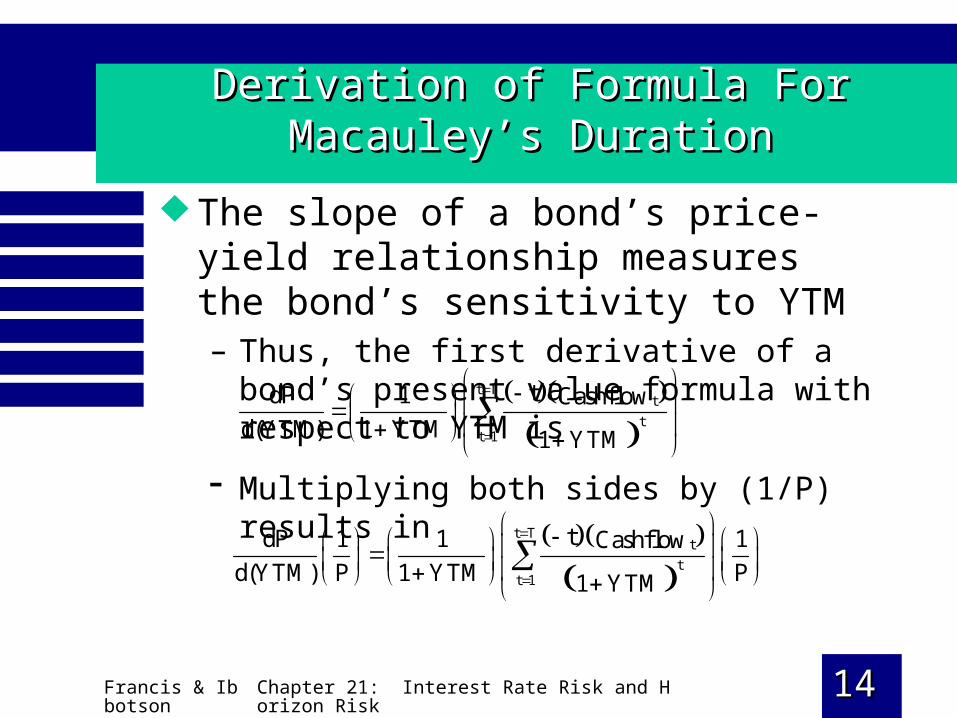

Derivation of Formula For Macauley’s DurationDerivation of Formula For Macauley’s Duration

The slope of a bond’s price-yield relationship measures the bond’s sensitivity to YTM– Thus, the first derivative of a bond’s present

value formula with respect to YTM is

t Tt

tt 1

tdP 1 Cashflowd(YTM) 1 YTM 1 YTM

Multiplying both sides by (1/P) results in

t Tt

tt 1

tdP 1 1 1Cashflowd(YTM) P 1 YTM P1 YTM

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1515

Derivation of Formula For Macauley’s DurationDerivation of Formula For Macauley’s Duration

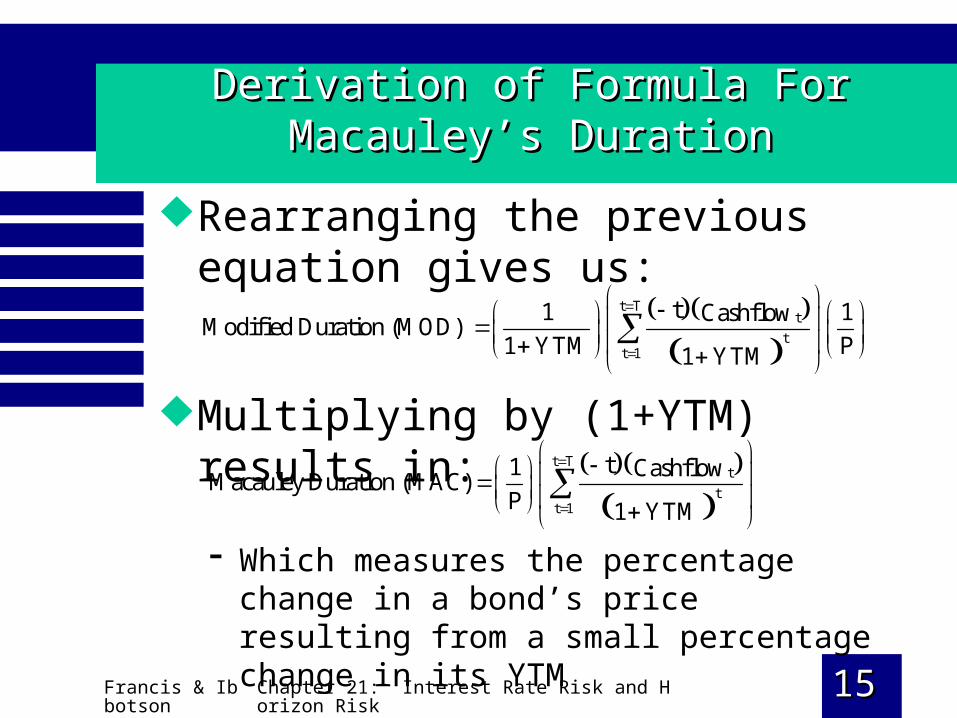

Rearranging the previous equation gives us:

t Tt

tt 1

t1 1CashflowModified Duration (MOD)

1 YTM P1 YTM

Multiplying by (1+YTM) results in:

t Tt

tt 1

t1 CashflowMacauley Duration (MAC)

P 1 YTM

Which measures the percentage change in a bond’s price resulting from a small percentage change in its YTM

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1616

Derivation of Formula For Macauley’s DurationDerivation of Formula For Macauley’s Duration

MAC and MOD are similar measures of a bond’s time structure– MAC: average number of years the

investor’s money is invested in the bond– MOD: average number of modified years

the investor’s money is invested in the bond

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1717

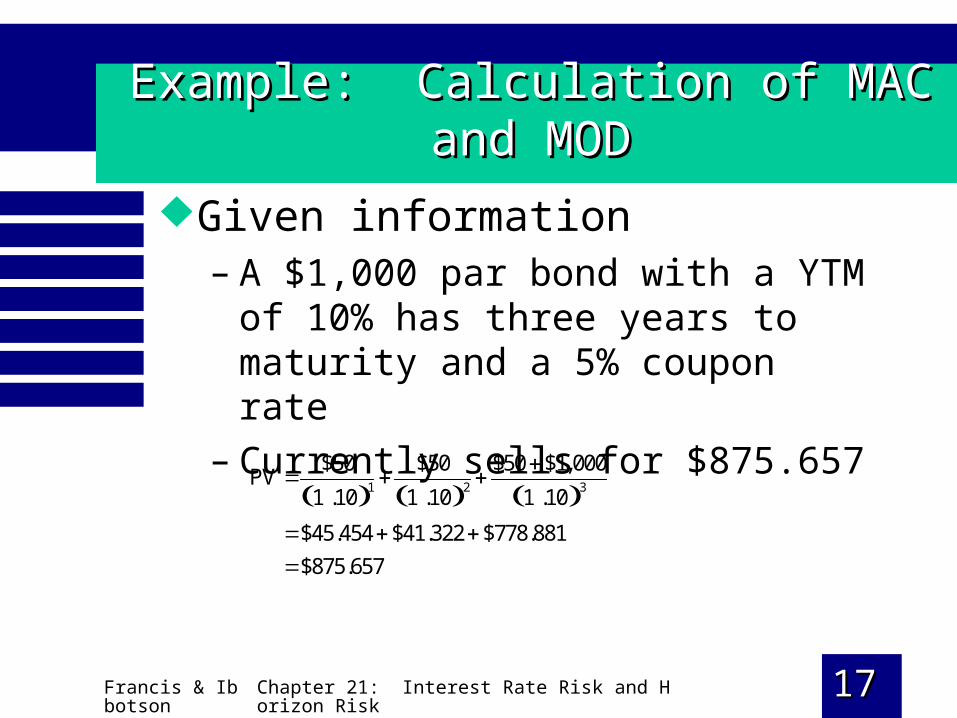

Example: Calculation of MAC and MODExample: Calculation of MAC and MOD

Given information– A $1,000 par bond with a YTM of 10%

has three years to maturity and a 5% coupon rate

– Currently sells for $875.657

1 2 3

$50 $50 $50 $1,000PV

1 .10 1 .10 1 .10

$45.454 $41.322 $778.881

$875.657

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1818

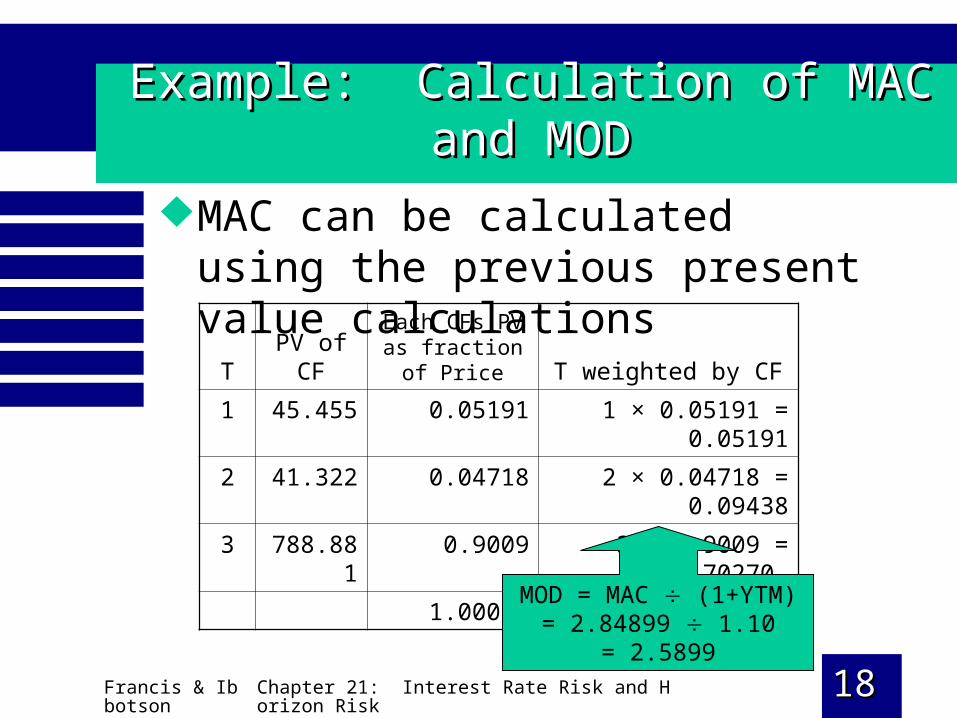

Example: Calculation of MAC and MODExample: Calculation of MAC and MOD

MAC can be calculated using the previous present value calculations

T PV of CFEach CFs PV as fraction of Price T weighted by CF

1 45.455 0.05191 1 × 0.05191 = 0.05191

2 41.322 0.04718 2 × 0.04718 = 0.09438

3 788.881 0.9009 3 × 0.9009 = 2.70270

1.00000 MAC = 2.84899

MOD = MAC (1+YTM)= 2.84899 1.10

= 2.5899

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 1919

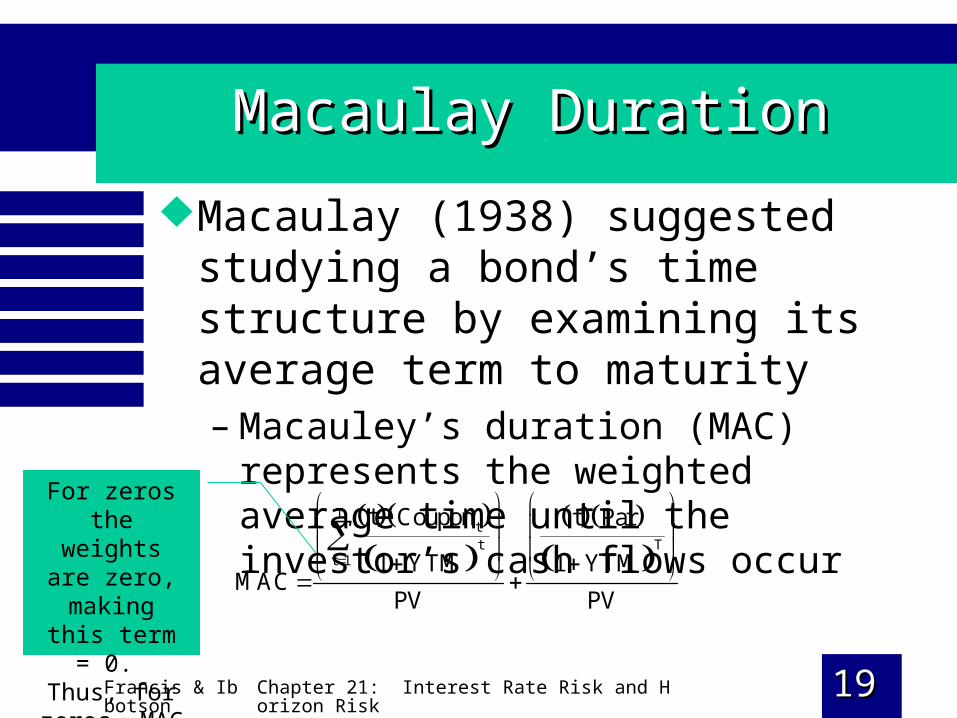

Macaulay DurationMacaulay Duration

Macaulay (1938) suggested studying a bond’s time structure by examining its average term to maturity– Macauley’s duration (MAC) represents

the weighted average time until the investor’s cash flows occur

Ttt T

t 1

t Coupon t Par

1 YTM 1 YTMMAC

PV PV

For zeros the weights are

zero, making this term = 0.

Thus, for zeros, MAC = t.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2020

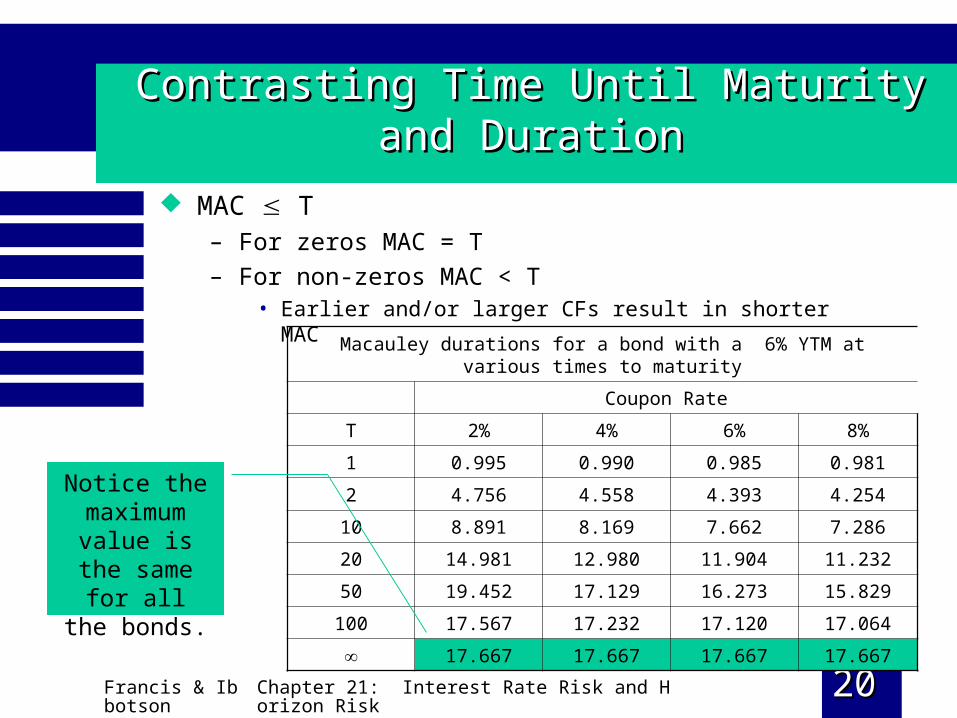

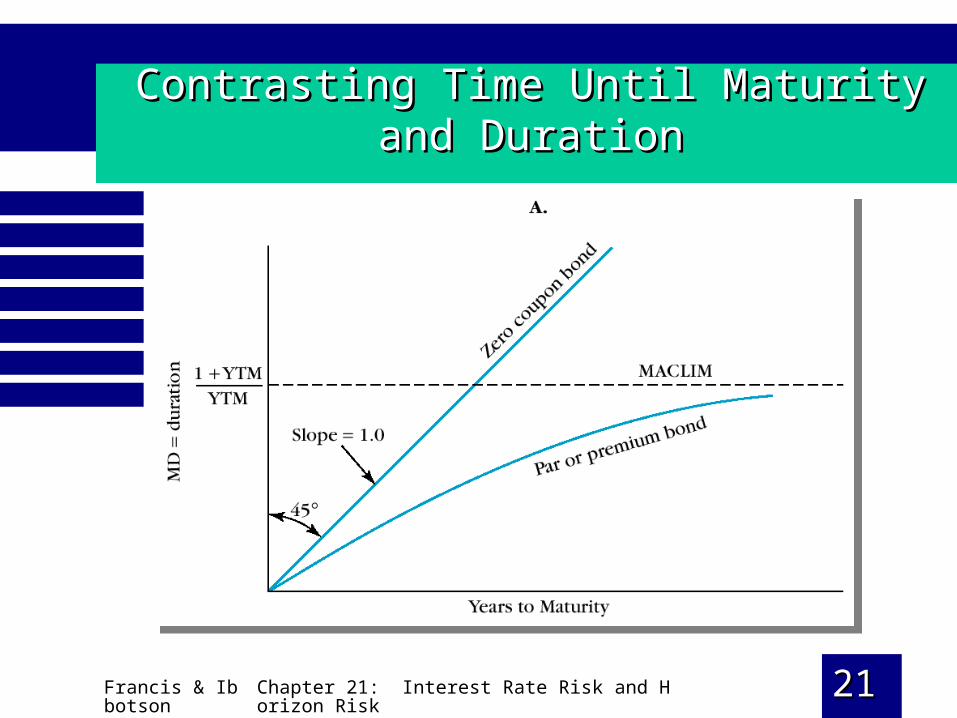

Contrasting Time Until Maturity and DurationContrasting Time Until Maturity and Duration

MAC T– For zeros MAC = T

– For non-zeros MAC < T• Earlier and/or larger CFs result in shorter MAC

Macauley durations for a bond with a 6% YTM at various times to maturity

Coupon Rate

T 2% 4% 6% 8%

1 0.995 0.990 0.985 0.981

2 4.756 4.558 4.393 4.254

10 8.891 8.169 7.662 7.286

20 14.981 12.980 11.904 11.232

50 19.452 17.129 16.273 15.829

100 17.567 17.232 17.120 17.064

17.667 17.667 17.667 17.667

Notice the maximum value is the same for all the bonds.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2121

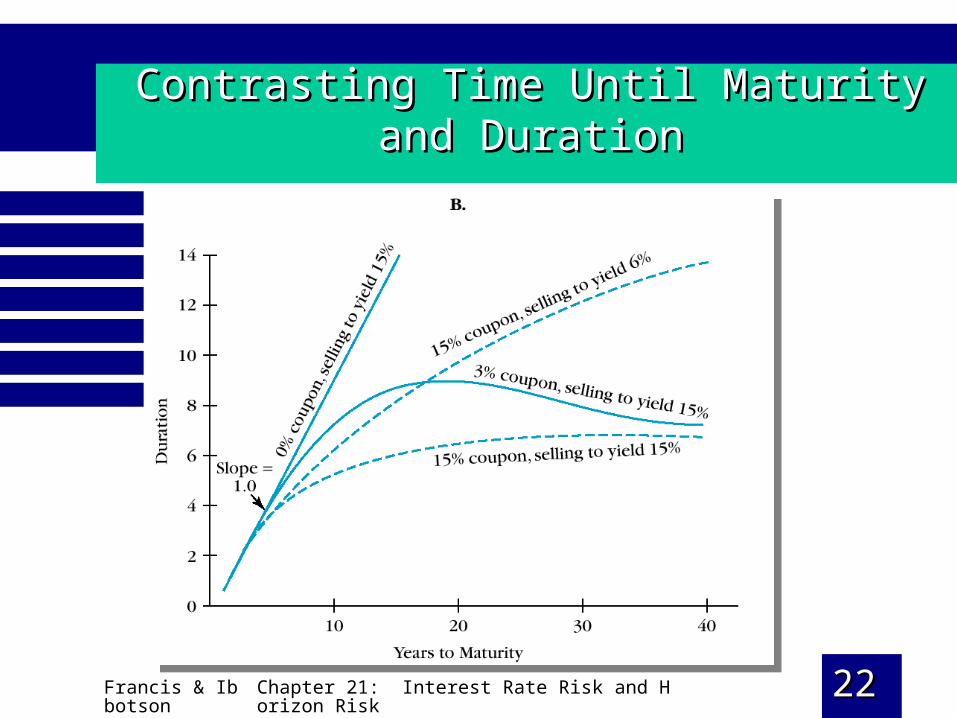

Contrasting Time Until Maturity and DurationContrasting Time Until Maturity and Duration

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2222

Contrasting Time Until Maturity and DurationContrasting Time Until Maturity and Duration

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2323

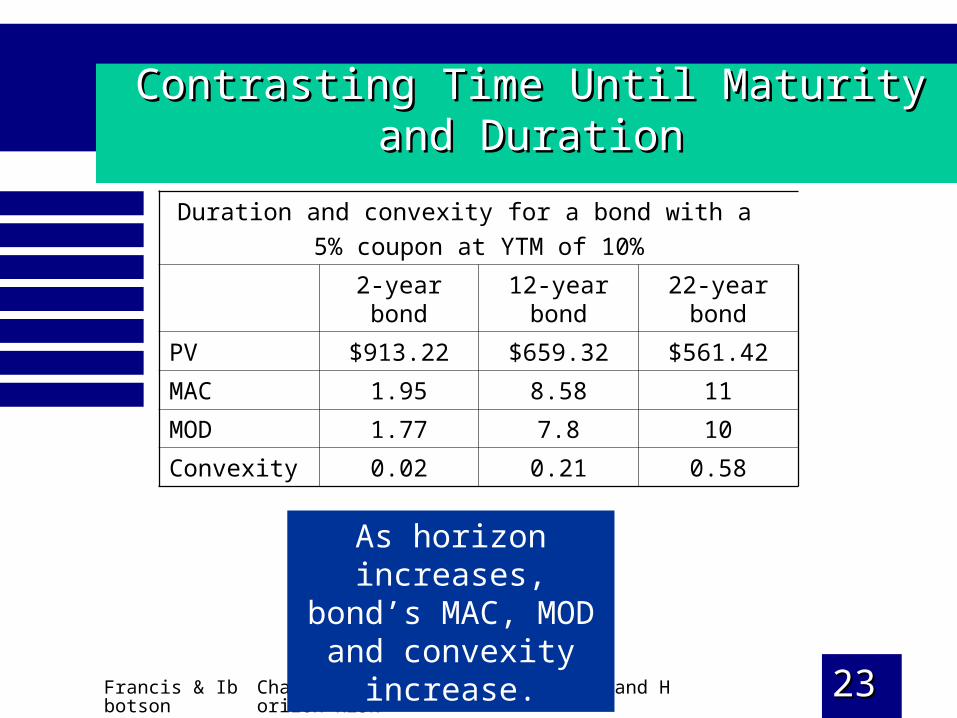

Contrasting Time Until Maturity and DurationContrasting Time Until Maturity and Duration

Duration and convexity for a bond with a

5% coupon at YTM of 10%

2-year bond 12-year bond 22-year bond

PV $913.22 $659.32 $561.42

MAC 1.95 8.58 11

MOD 1.77 7.8 10

Convexity 0.02 0.21 0.58

As horizon increases, bond’s MAC, MOD

and convexity increase.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2424

Contrasting Time Until Maturity and DurationContrasting Time Until Maturity and Duration

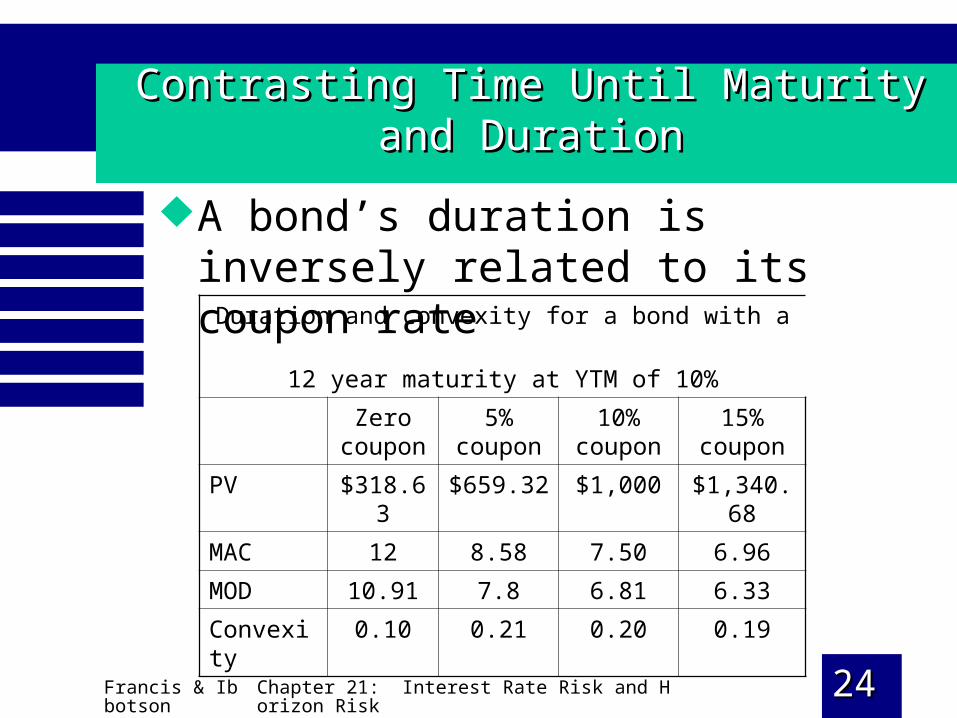

A bond’s duration is inversely related to its coupon rate

Duration and convexity for a bond with a

12 year maturity at YTM of 10%

Zero coupon

5% coupon

10% coupon

15% coupon

PV $318.63 $659.32 $1,000 $1,340.68

MAC 12 8.58 7.50 6.96

MOD 10.91 7.8 6.81 6.33

Convexity 0.10 0.21 0.20 0.19

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2525

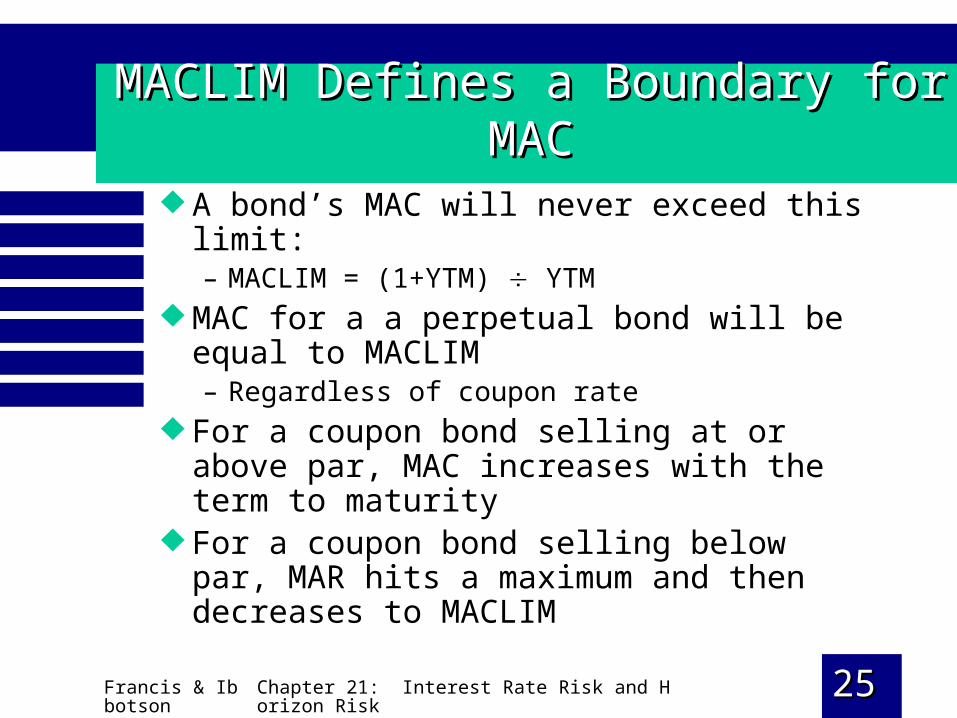

MACLIM Defines a Boundary for MACMACLIM Defines a Boundary for MAC

A bond’s MAC will never exceed this limit:– MACLIM = (1+YTM) YTM

MAC for a a perpetual bond will be equal to MACLIM– Regardless of coupon rate

For a coupon bond selling at or above par, MAC increases with the term to maturity

For a coupon bond selling below par, MAR hits a maximum and then decreases to MACLIM

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2626

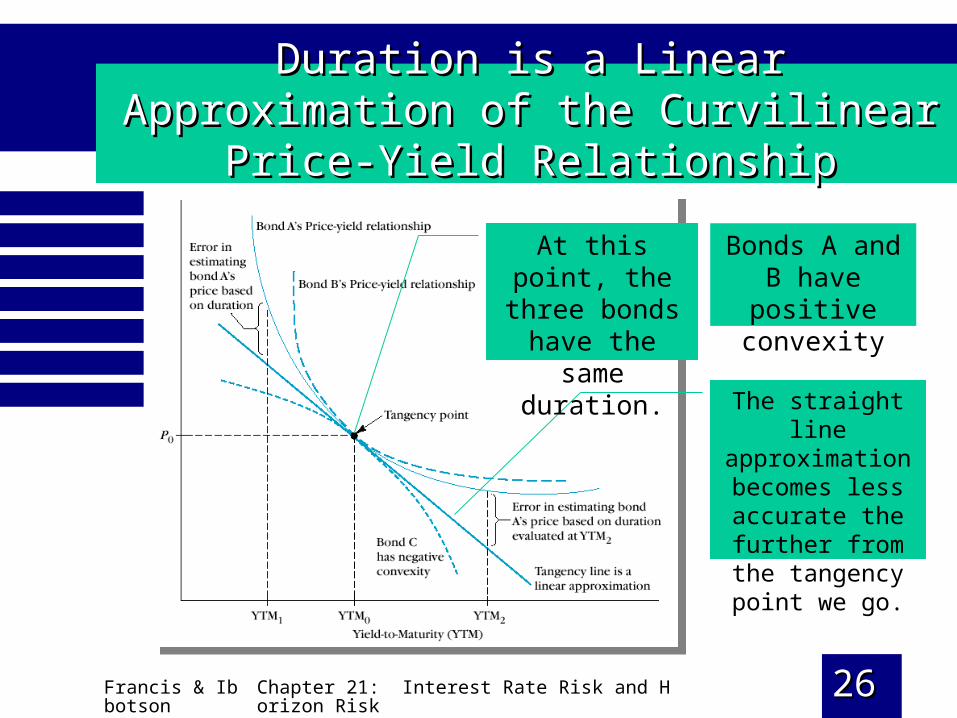

Duration is a Linear Approximation of the Duration is a Linear Approximation of the Curvilinear Price-Yield RelationshipCurvilinear Price-Yield Relationship

Bonds A and B have positive

convexity

The straight line approximation becomes less

accurate the further from the tangency

point we go.

At this point, the three bonds have

the same duration.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2727

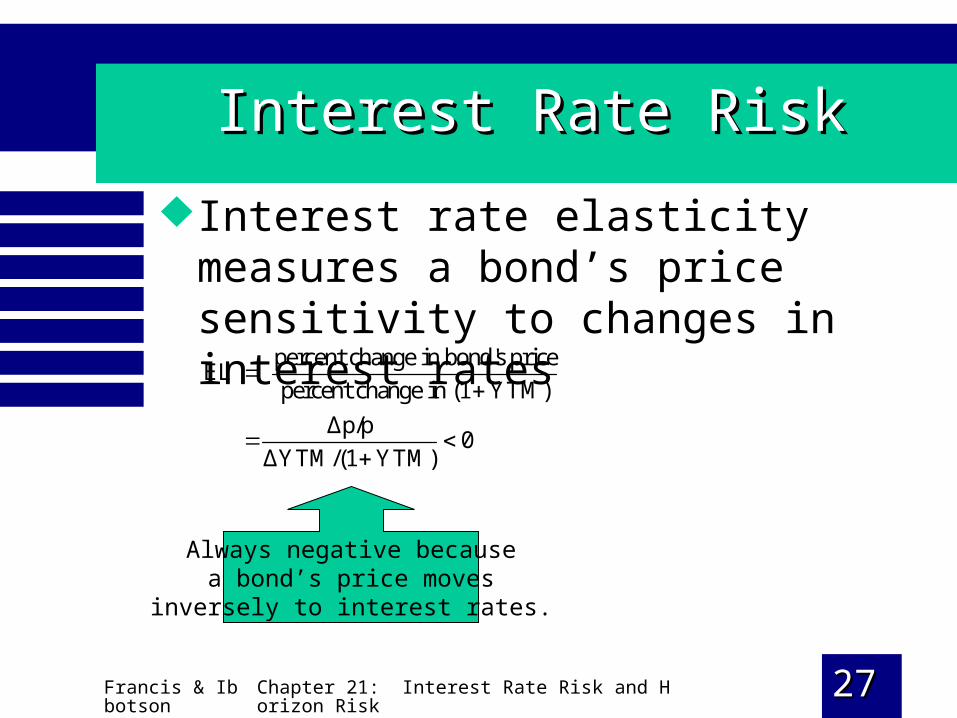

Interest Rate RiskInterest Rate Risk

Interest rate elasticity measures a bond’s price sensitivity to changes in interest rates

percent change in bond's priceEL

percent change in (1 YTM)

Δp/p0

ΔYTM/(1 YTM)

Always negative becausea bond’s price moves

inversely to interest rates.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2828

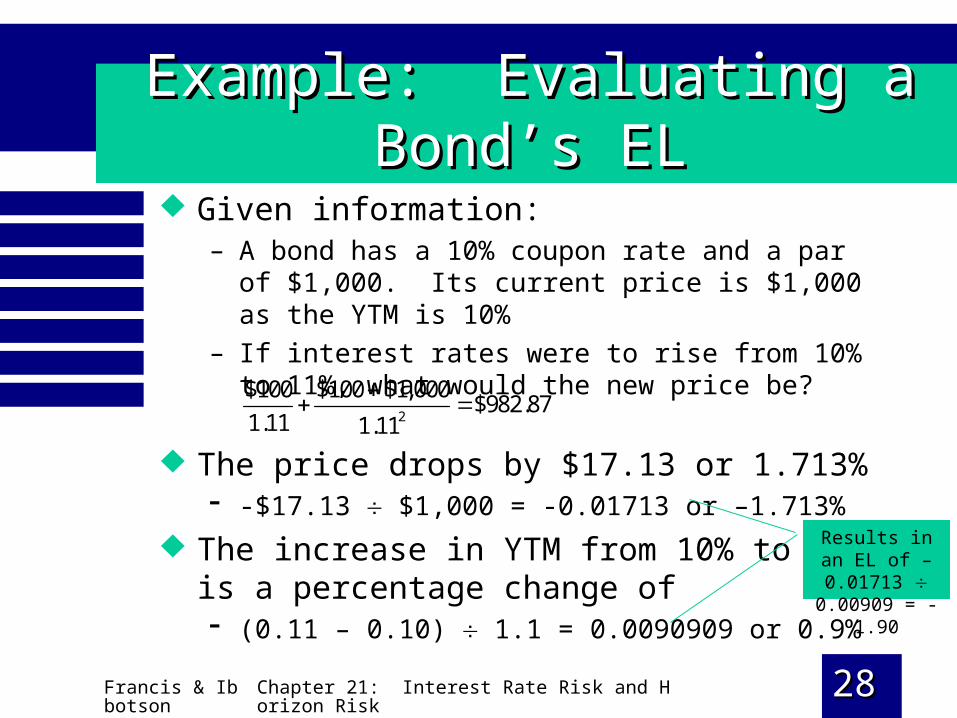

Example: Evaluating a Bond’s ELExample: Evaluating a Bond’s EL

Given information:– A bond has a 10% coupon rate and a par of $1,000. Its

current price is $1,000 as the YTM is 10%

– If interest rates were to rise from 10% to 11%, what would the new price be?

2

$100 $100 $1,000$982.87

1.11 1.11

The price drops by $17.13 or 1.713% -$17.13 $1,000 = -0.01713 or –1.713%

The increase in YTM from 10% to 11% is a percentage change of (0.11 – 0.10) 1.1 = 0.0090909 or 0.9%

Results in an EL of –0.01713

0.00909 = -1.90

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 2929

Interest Rate RiskInterest Rate Risk

MAC can also be used to calculate a bond’s elasticity– MAC = [(t=1)($90.909 $1,000] + [(t=2)

($909.091) $1,000] = 1.90 years

Interest rate elasticity and MAC are equally good measures of interest rate risk

Also good measures of total risk– Because all bonds are impacted by systematic

fluctuations in interest rates

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3030

Immunizing Interest Rate RiskImmunizing Interest Rate Risk

Immunization—procedure designed to reduce or eliminate interest rate risk– Purchase an offsetting asset or liability

with the same duration and present value• Creates a portfolio that will earn the same rate

of return expected prior to immunization, regardless of interest rate fluctuations

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3131

Example: Immunizing the Example: Immunizing the Palmer Corporation’s $1,000 LiabilityPalmer Corporation’s $1,000 Liability

Given information– Palmer Corporation has a $1,000 liability due in

6.79 years

If Palmer purchased a default-free bond with a 9% coupon rate, par of $1,000 and maturity of 10 years for $1,000 [has a duration of 6.79 years] to repay the liability due in 6.79 years– Would have to deal with reinvestment risk—if

interest rates drop below the original YTM of 9% this is a problem

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3232

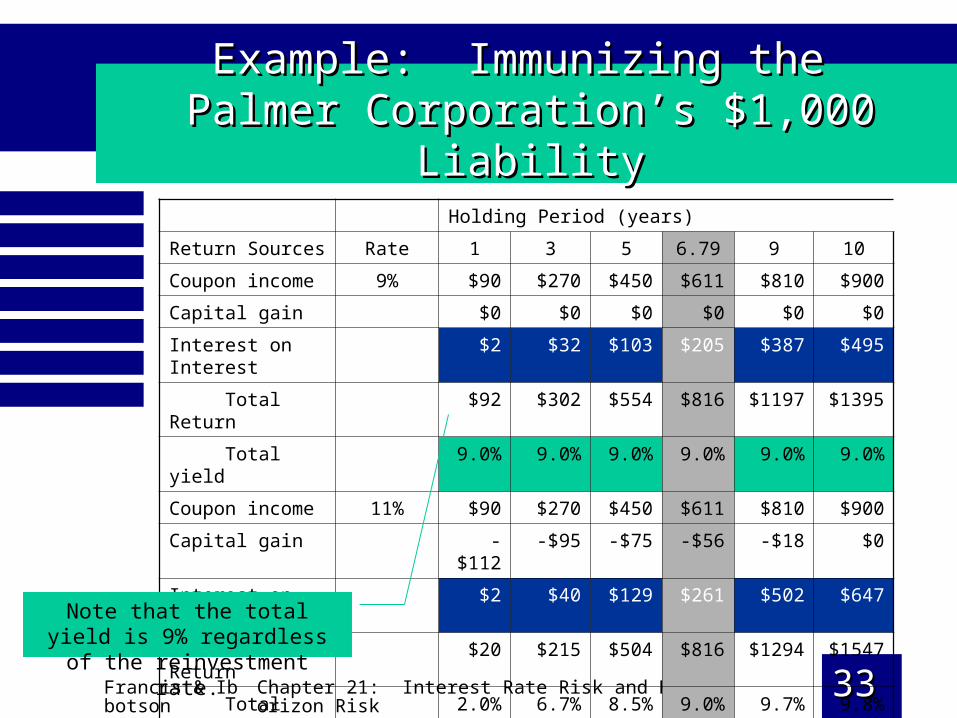

Example: Immunizing the Example: Immunizing the Palmer Corporation’s $1,000 LiabilityPalmer Corporation’s $1,000 Liability

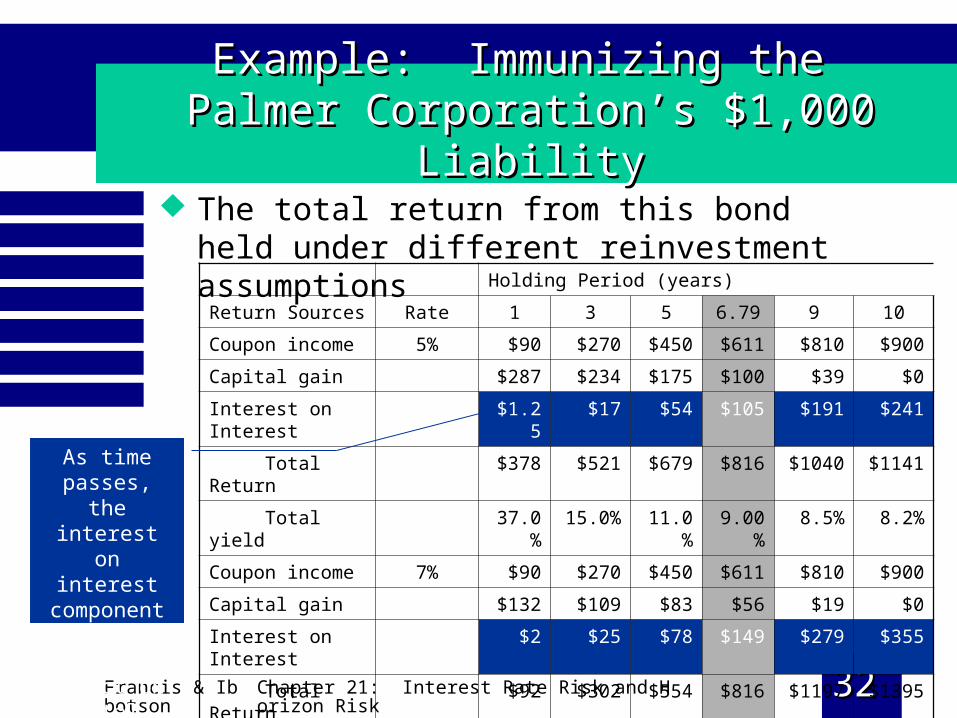

The total return from this bond held under different reinvestment assumptions

Holding Period (years)

Return Sources Rate 1 3 5 6.79 9 10

Coupon income 5% $90 $270 $450 $611 $810 $900

Capital gain $287 $234 $175 $100 $39 $0

Interest on Interest $1.25 $17 $54 $105 $191 $241

Total Return $378 $521 $679 $816 $1040 $1141

Total yield 37.0% 15.0% 11.0% 9.00% 8.5% 8.2%

Coupon income 7% $90 $270 $450 $611 $810 $900

Capital gain $132 $109 $83 $56 $19 $0

Interest on Interest $2 $25 $78 $149 $279 $355

Total Return $92 $302 $554 $816 $1197 $1395

Total yield 22.0% 12.0% 10.0% 9.0% 8.6% 8.5%

As time passes, the interest on

interest component has

a greater impact on total

return.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3333

Example: Immunizing the Example: Immunizing the Palmer Corporation’s $1,000 LiabilityPalmer Corporation’s $1,000 Liability

Holding Period (years)

Return Sources Rate 1 3 5 6.79 9 10

Coupon income 9% $90 $270 $450 $611 $810 $900

Capital gain $0 $0 $0 $0 $0 $0

Interest on Interest $2 $32 $103 $205 $387 $495

Total Return $92 $302 $554 $816 $1197 $1395

Total yield 9.0% 9.0% 9.0% 9.0% 9.0% 9.0%

Coupon income 11% $90 $270 $450 $611 $810 $900

Capital gain -$112 -$95 -$75 -$56 -$18 $0

Interest on Interest $2 $40 $129 $261 $502 $647

Total Return $20 $215 $504 $816 $1294 $1547

Total yield 2.0% 6.7% 8.5% 9.0% 9.7% 9.8%

Note that the total yield is 9% regardless of the reinvestment rate.

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3434

Example: Immunizing the Example: Immunizing the Palmer Corporation’s $1,000 LiabilityPalmer Corporation’s $1,000 Liability

A bond’s total return is impacted by– Its interest income and interest-on-interest – Its price fluctuations

These two forces work in the opposite direction– Is there some point where they exactly

offset each other?• Yes, when the bond has been held for the

length of the bond’s duration

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3535

Maturity MatchingMaturity Matching

Palmer Corporation could purchase a bond with a maturity exactly equal to the maturity of its liability, 6.79 years– However, ignores the coupon and interest on invested coupons

What if Palmer bought a zero-coupon bond?– There would be no need to worry about coupons and reinvestment

These methods are impractical– Extremely difficult to find zeros with needed maturity date

– Extremely difficult (impossible) to find fixed-income securities with needed maturity date

• Also difficult to match a single bond’s duration with the liability’s duration

Due to these problems the more practical duration-matching strategy was developed

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3636

Duration MatchingDuration Matching

Can immunize against interest rate risk by matching the weighted average MAC of a portfolio’s assets and liabilities– The MAC of a portfolio is equal to a

weighted average of the individual MACs 1 2

p 1 21 2 1 2

Value ValueMAC MAC MAC

Value Value Value Value

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3737

Duration MatchingDuration Matching

Financial institutions routinely perform duration matching strategies– Called asset-liability management (ALM)

Duration matching is necessary but not sufficient to achieve immunization– If CFs are spread over a wide range of times

must meet all of these conditions to effectively immunize

• DurationAssets = DurationLiabilities

• PVAssets = PVLiabilities

• DispersionAssets = DispersionLiabilities

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3838

Duration Wandering and Portfolio RebalancingDuration Wandering and Portfolio Rebalancing

A bond’s duration does not decrease on a one-to-one basis with time

Market interest rates impact durations– For these reasons portfolios must be

rebalanced to maintain a duration that will eliminate interest rate risk

• Annual or semi-annual rebalancing may be sufficient for certain assets/liability characteristics

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 3939

Duration Wandering and Portfolio RebalancingDuration Wandering and Portfolio Rebalancing

For example:– Palmer Corporation originally wanted to

match a liability with a life of 6.79 years• So perhaps it bought a bond with a duration of

6.79– After 1 year the maturity of its liability has

decreased to 5.79 years

» However the duration of the matched bond has declined by a smaller amount

» Portfolio needs to be rebalanced to maintain the duration-matching strategy

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4040

Problems with DurationProblems with Duration

Changes in term structure of interest rates cause stochastic process risk– Alternative duration measures have been

developed to deal with this• Macaulay Duration (MAC)—simplest and

most popular measure of duration– Implicit assumptions

» Yield curve is horizontal at the level of the bond’s YTM

» Yield curve only experiences horizontal shifts

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4141

Problems with DurationProblems with Duration• Fisher-Weil Duration (FWD)

– Produces similar value as MAC but is superior because» Considers each time period’s forward interest rate

• Modified Duration (MOD)– Different from MAC because MAC measures the

percentage change in a bond’s price resulting from a percentage change in the market interest rate

» MOD’s denominator is d(YTM) (1+YTM)

• Cox, Ingersoll & Ross Duration (CIR)– More difficult to calculate than MAC and never been as

popular

Results of tests indicate that MAC works about as well as the other measures– Is also cost effective, because of its simplicity

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4242

Problems with DurationProblems with Duration

MAC, FWD & CIR are one-factor models– Based on fluctuations in a single interest

rate

Other researchers are developing two-factor interest rate risk models– Use a short-term and a long-term interest

rate• None of these models are popular

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4343

Horizon AnalysisHorizon Analysis

A bond buyer’s investment horizon is often different from a bond’s maturity horizon– Investor should perform a horizon

analysis for every potential bond investment

• Horizon return—a bond’s total return including CFs and price changes over relevant investment horizon

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4444

Horizon AnalysisHorizon Analysis

Some investors rely only upon a bond’s YTM– Don’t calculate horizon return because it requires

estimates about future interest rates• Horizon analysis is important—need to analyze

different interest rate scenarios

Contingent immunization– Combines active management and immunization

• Portfolio manager may actively manage a portfolio so long as it earns a minimum safety net return

– If safety net return is not earned manager is terminated and remaining assets are immunized

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4545

The Bottom LineThe Bottom Line

Behavior of bond prices– Bond prices move inversely to YTM– A bond’s interest rate risk usually increases with

the time to maturity (horizon risk)• However, risk increases at a decreasing rate

– Price changes resulting from an equal-size change in a bond’s YTM are asymmetrical

• A decrease in YTM increases prices by more than an equal increase in YTM decreases prices

– Coupon-paying bonds are influenced by the size of their coupon rates

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4646

The Bottom LineThe Bottom Line Duration Axioms

– Duration measures the average length of time funds are tied up in an investment

– MAC is less than maturity for a coupon-paying bond and equals maturity for a zero

• MOD is less than MAC

– Duration always varies directly with a bond’s maturity for zeros and bonds selling above or at par, and usually for bonds selling at a discount

– All other factors equal, duration varies inversely with YTM for a non-zero

– MAC equals a bond’s interest rate elasticity– Duration is a linear forecast of a bond’s price movement relative

to YTM changes• Only accurate for small changes in YTM

– MAC has a limiting value

Francis & Ibbotson

Chapter 21: Interest Rate Risk and Horizon Risk 4747

The Bottom LineThe Bottom Line

Interest rate risk axioms– Interest rate risk usually increases directly with MAC,

MOD, elasticity and term to maturity

– Immunization is used to reduce or eliminate interest rate risk

– Asset-liability management may also be used to manage interest rate risk as well as market and/or credit risk

– Positive convexity exists for option-free bonds but some embedded bonds may have negative convexity

– If a bond will not be held to its maturity a horizon analysis should be performed