Embed Size (px)

Citation preview

D J Carmichael Pty Limited ABN 26 003 058 857 AFSL 232571 Market Participant of ASX Limited Telephone: 08 9263 5200 Facsimile: 08 9263 5283 Email: [email protected] Webpage: http://www.djcarmichael.com.au

CARMICHAEL RESEARCH

RESOURCES

Hot Chili Ltd (HCH)

First Resource at Productora HCH has announced their maiden resource for the Productora Project in Chile. The resource tonnage and grade will provide a very good foundation stone for the continued addition of resources through an aggressive 55,000m definition and exploration drilling campaign over the course of the next year. HCH s maiden resource came in 13% ahead of our expectations with 85.1Mt against our expected 75Mt, at a copper grade of 0.6% meeting our expectations. Gold and molybdenum credits provide a copper equivalent grade of 0.8% with further credits from cobalt and uranium not taken into account in the resource estimate at this stage. We move to a Buy recommendation on the existing resource and a high likelihood of additional material being added over the course of the next 12 months.

Key Points

The maiden resources estimate of 85.1Mt grading 0.6% Cu, 0.1g/t gold and 146g/t

molybdenum, contains 483,000 tonnes of copper metal, 290,000 ounces of gold and 12,418 tonnes of molybdenum metal with 37% of the resource in the Indicated category and 63% in

the inferred category. The resource starts from surface requiring no pre-strip prior to mining.

HCH have now embarked on major 55,000m RC drilling program, augmented with 8,000m

of diamond drilling, to expand the initial resource adjacent to, along strike and at depth. The

diamond drilling will be employed to lift the grade category for the mineralisation encountered in the deeper parts of the system. RC drilling beyond the central lease, which

has a strike length of just 1.4km, has already intersected broad zones of mineralisation

similar in style and grade to that already defined in the central lease resource with a breccia-hosted zone already seen over a 3.7km strike length.

HCH have released a revised exploration target for Productora taking into account the maiden resource and the indications of the extent of the mineralised system. HCH estimate

a total tonnage of between 280Mt and 320Mt containing between 1.4Mt and 2.2Mt of

contained copper. On this metric, Productora would rank as one of the larger IOCG deposits in the Chilean Coastal Cordillera and would have an approximately equivalent size to Teck s

Andacolla porphyry deposit (400Mt at 0.38% Cu for 1.5Mt of contained copper) currently in

production adjacent to HCH s Los Mantos Project, further south.

Our forward valuation for HCH is determined by our assumptions with respect to the size of

the combined Productora and Los Mantos resources in nine to 12 months time. We have assumed an additional 54.9Mt at Productora by Q3 2012 to bring the total to 140Mt, an

increase of 64.5%. We believe that this is a conservative estimate given the prospectivity of

their ground and the aggressive drill program, but we are comfortable with this target prior to further indications from HCH on the progress of the drilling and the release of further results.

We have also assumed a maiden 15mt resource estimate for Los Mantos late 1H 2012 for a

total combined tonnage of 155Mt and a total contained copper of 1.35Mt.

20 September 2011

RECOMMENDATION

Buy

12 Month Price Target

$1.33 per share

12 month volume 108.5m 12 month share low A$0.18 12 month share high A$0.85

Market Risk High Liquidity Risk Med Infrastructure Risk Med Country Risk Low

IRESS & DJC Research

ISSUED CAPITAL ASX HCH Share price $0.52 Mkt cap1 $84.5m Ordinary shares on issue 162.4m Options (Nov 2013, 20c) 40.6m Diluted for restricted shares Source: IRESS

DIRECTORS Murray Black Chairman Christian Easterday Managing Director Dr Alan Trench Executive Director

MAJOR SHAREHOLDERS Kalgoorlie Auto Services Pty Ltd 24.7% Rex Harbour (consolidated) 5.0% Panoramic Resources Ltd 4.1% Taurus Funds Management 4.1% CAP S.A. (Port Finance) 3.8%

12 MONTH PERFORMANCE

0.00

0.25

0.50

0.75

1.00

Sep-10 Dec-10 Mar-11 Jun-11 Sep-11

Source: IRESS

Paul Adams Head of Research +61 8 9263 5200 [email protected]

2 20 September 2011

CARMICHAEL RESEARCH

RESOURCES

Productora maiden resource

HCH have released details of their maiden resource estimate for the Productora copper-gold-

molybdenum Project in Chile. Productora is the company flagship project and will continue to receive the majority of exploration and definition drilling funds for the remainder of 2011 and into

2012.

The resource estimate is confined to the 1.4km long Central Lease, within a main mineralised

trend that extends for a strike length of 12.5km. The Central Lease contains the existing small

scale Productora underground copper mine which has been excised from the resource estimate at this stage.

The milestone of the maiden resource estimate for Productora has been achieved within 15 months of the HCH listing. We believe this is an extraordinary achievement and demonstrates

the commitment that the Board and management team have shown to their projects. The

production of the resource now allows HCH to start to put together a development team to commence the scoping phase of their development studies.

Figure 1. Productora Central Area Resource Table Source: HCH

The maiden resources estimate of 85.1Mt grading 0.6% Cu, 0.1g/t gold and 146g/t molybdenum,

contains 483,000 tonnes of copper metal, 290,000 ounces of gold and 12,418 tonnes of molybdenum metal with 37% of the resource in the Indicated category and 63% in the inferred

category. The resource starts from surface, requiring no pre-strip prior to mining. However, the

gold and molybdenum credits have only been estimated where they co-exist with copper and HCH note that significant quantities of molybdenum lie outside the current resource model.

Figure 2. Grade-Tonnage curves from Productora Source: HCH

20 September, 2011 3

CARMICHAEL RESEARCH

RESOURCES

As can be seen from Figure 2 above, the tonnage of the resource is effectively constant at grades below 0.3% indicating that 0.3% provides a natural geological cut-off to the mineralisation

and there is little mineralisation in the resource below this grade. The average depth to the base

of the resource is about 400m from surface, mostly confined by the drilling.

Figure 3. Isometric view with cross section and long section through resource model Source:HCH

The mineralisation is associated with a series of vertical lodes (Figure 3) with some minor

horizontal mantos horizons within a felsic volcanic country rock, extensively intruded by a

tourmaline breccia along the main mineralised north-east trend.

The sulphide mineralisation is contained in an assemblage of pyrite, chalcopyrite, bornite and

molybdenite as breccia, vein and cavity fill as well as disseminations within the breccia host rocks. In the oxidised zone, down to an average depth of 70m below surface, the mineralisation

is dominated by malachite.

Figure 4. Distribution of tonnes and grade along strike Source:HCH

4 20 September 2011

CARMICHAEL RESEARCH

RESOURCES

Further Potential and Exploration Target

HCH have now embarked on major 55,000m RC drilling program, augmented with 8,000m of

diamond drilling, to expand the initial resource adjacent to, along strike and at depth. The diamond drilling will be employed to lift the grade category for the mineralisation encountered in

the deeper parts of the system (see Figure 5 below).

Figure 5. Distribution of mineralisation with depth Source: HCH

The geophysical surveys, geochemical sampling and mapping conducted in the 15 months since

listing have enabled HCH to determine the mineralised footprint of the Productora project. The

copper-gold-molybdenum breccia zone in the central lease is located on the eastern flank of a consistent magnetic anomaly seen over a strike length of some 12.5km. Coincident with this

magnetic anomaly are several induced polarisation (IP) anomalies up to 4.0km in length which

could be associated with sulphide mineralisation. The combined length of the IP anomalies is 9.5km.

RC drilling beyond the Central Lease has intersected broad zones of mineralisation similar in style and grade to that already defined in the resource with a breccia-hosted zone already seen

over a 3.7km strike length.

Previous drilling by Teck in an area just south of the Central Lease, in-which the mineral rights

are held by the Chilean Nuclear Commission (CCHEN), had intersections of 112m at 0.65%Cu

and 0.1g/t gold and 20m at 0.77% Cu and 0.34g/t gold. To the north, Teck drilling intersected 149m at 0.6% Cu eq.

In their first drilling campaign, to the north of the Central Lease, HCH clipped the mineralised breccia zone in the very eastern hole (12m at 0.6% Cu eq. open to end of hole). These holes

targeted the magnetic anomaly prior to the understanding that the mineralised zone was actually

located on its eastern margin. In the current campaign HCH intend to extend the lines to the east thereby intersecting the target zone properly.

We take the view that additional mineralisation is likely to be added in subsequent resource estimates, with the potential to grow the resource substantially.

20 September, 2011 5

CARMICHAEL RESEARCH

RESOURCES

Figure 6. IP anomalies, previous and future drill hole locations Source: HCH

Combining the existing drilling in the central lease and that of previous workers, HCH now

estimate they have successful drill results over a strike length of 3.7km, extending the known mineralisation an additional strike length of 2.3km beyond the current resource envelope.

Larger exploration target

HCH have released a revised exploration target for Productora taking into account the maiden

resource and the indications of the extent of the mineralised footprint. HCH estimate a total tonnage of between 280Mt and 320Mt containing between 1.4Mt and 2.2Mt of contained copper.

Figure 7. Exploration target table for Productora, September 2011 Source: HCH

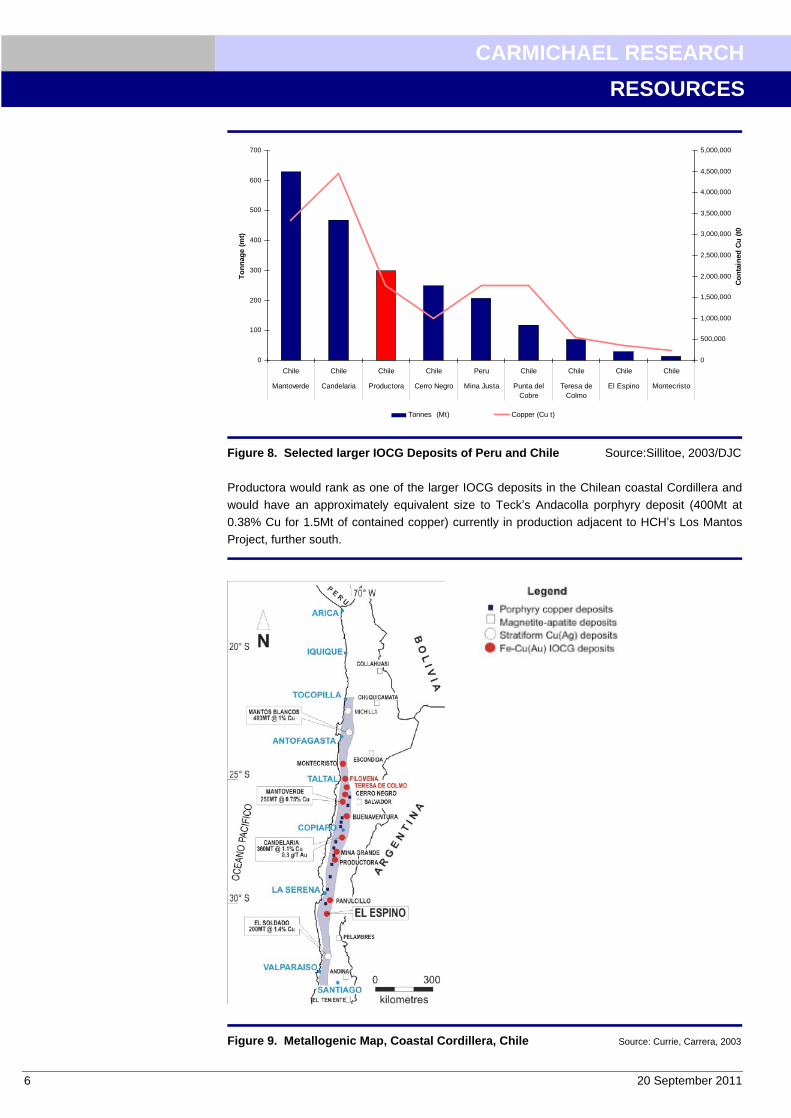

A deposit of this size at Productora compares favourably with well known IOCG deposits in the

Chilean Cordillera, where Candelaria stands out as the type IOCG deposit in the region. The graph below (Figure 8) illustrates where Productora would be placed among its peers should

HCH realise the mid-point of their exploration target i.e. 300Mt at 0.6% Cu (without minor metal

credits).

6 20 September 2011

CARMICHAEL RESEARCH

RESOURCES

0

100

200

300

400

500

600

700

Chile Chile Chile Chile Peru Chile Chile Chile Chile

Mantoverde Candelaria Productora Cerro Negro Mina Justa Punta delCobre

Teresa deColmo

El Espino Montecristo

To

nn

age

(mt)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

Co

nta

ined

Cu

(t0

Tonnes (Mt) Copper (Cu t)

Figure 8. Selected larger IOCG Deposits of Peru and Chile Source:Sillitoe, 2003/DJC

Productora would rank as one of the larger IOCG deposits in the Chilean coastal Cordillera and

would have an approximately equivalent size to Teck s Andacolla porphyry deposit (400Mt at 0.38% Cu for 1.5Mt of contained copper) currently in production adjacent to HCH s Los Mantos

Project, further south.

Figure 9. Metallogenic Map, Coastal Cordillera, Chile Source: Currie, Carrera, 2003

20 September, 2011 7

CARMICHAEL RESEARCH

RESOURCES

Corporate

In early August HCH completed two separate private placements of $4m each to add $8m in

cash to fund the on-going drilling campaigns at Productora and Los Mantos. One placement has been made to Panoramic Resources Limited (ASX:PAN) for 6.66m shares at A$0.60 per share

(A$4m) which results in PAN becoming a corner-stone investor in HCH with 4.1%. The second

placement has been made to Taurus Funds Management Pty Limited ( Taurus ), under the same terms, also providing it with a cornerstone 4.1% holding. HCH has approximately $11.5m in cash

and two strategic partners on the share register.

HCH have stated their intension to exercise their 100% purchase option over the Productora

Mine for a total of US$7.0m whilst at the same time allowing mining to continue under a capped

mining rate to maintain the underground infrastructure. This will be used later by HCH to obtain a bulk metallurgical sample for further processing route studies and potentially as a drilling site

for definition drilling in the immediate mine environs.

With regard to the purchase option HCH have a number of funding opportunities available from

paying for the purchase option out of existing cash; utilising option conversions of approximately

$8.1m; or utilising further funding from strategic partners.

Development Strategy

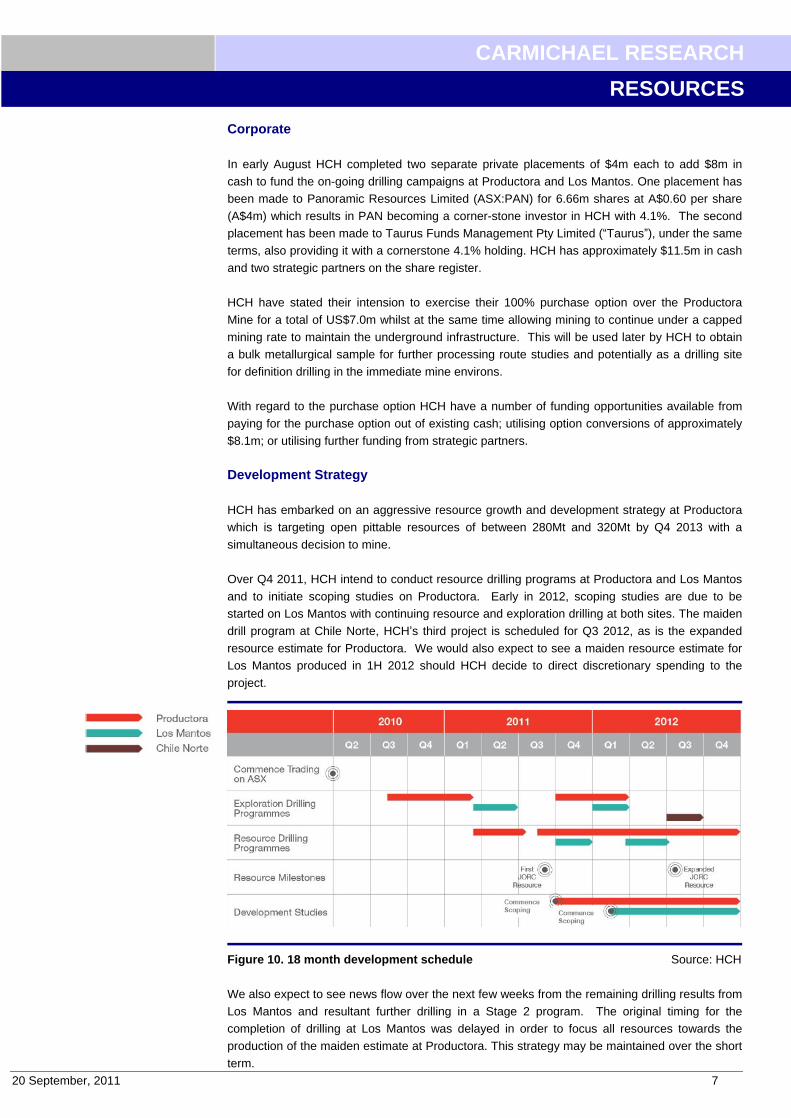

HCH has embarked on an aggressive resource growth and development strategy at Productora

which is targeting open pittable resources of between 280Mt and 320Mt by Q4 2013 with a

simultaneous decision to mine.

Over Q4 2011, HCH intend to conduct resource drilling programs at Productora and Los Mantos

and to initiate scoping studies on Productora. Early in 2012, scoping studies are due to be started on Los Mantos with continuing resource and exploration drilling at both sites. The maiden

drill program at Chile Norte, HCH s third project is scheduled for Q3 2012, as is the expanded

resource estimate for Productora. We would also expect to see a maiden resource estimate for Los Mantos produced in 1H 2012 should HCH decide to direct discretionary spending to the

project.

Figure 10. 18 month development schedule Source: HCH

We also expect to see news flow over the next few weeks from the remaining drilling results from

Los Mantos and resultant further drilling in a Stage 2 program. The original timing for the completion of drilling at Los Mantos was delayed in order to focus all resources towards the

production of the maiden estimate at Productora. This strategy may be maintained over the short

term.

8 20 September 2011

CARMICHAEL RESEARCH

RESOURCES

Valuation and Recommendation

Our forward valuation for HCH is determined by our assumptions with respect to the size of the

combined Productora and Los Mantos resources in nine to 12 months time. The maiden resource at Productora provides the foundation for transparent valuation and the basis for further

resource additions.

The drilling program at Productora throughout the remainder of FY2012 is aggressive and we

anticipate significant additions to the resource base by early Q3 2012. We also assume a

maiden resource for Los Mantos during 1H2012, but this may be deferred towards Productora.

Current Resource Grade Contained t Assumed Resource 2012 Grade Contained t(Mt) (cu eq) % (Cu metal equiv.) (Mt) (cu eq) % (Cu metal equiv.)

Productora 85.1 0.8 680,800 140 0.8 1,120,000

Los Mantos - - - 15 1.5 225,000

Chile Norte - - - - - -

Total 85.1 680,800 155 1,345,000

Project

Figure 11. Future resource tonnage and grade assumptions Source: DJC estimates

We have assumed an additional 54.9Mt at Productora by Q3 2012 to bring to total to 140Mt, an

increase of 64.5%. We believe that this is a conservative estimate given the prospectivity of their

ground and the aggressive drill program, but we are comfortable with this target prior to further indications from HCH on the progress of the drilling program and release of further results.

We have also assumed a maiden resource at Los Mantos of around 15Mt but at a grade of 1.5% Cu equivalent, given the slightly different tenor of the mineralisation so far seen in early drilling

and samples from the Los Mantos underground mine. Los Mantos is characterised by several

shallowly dipping mantos horizons with intersection widths typically around 5m to 15m.

Productora Los Mantos

Tonnes 140,000,000 15,000,000

(Grade Cu eq %) 0.8% 1.5%

Contained Cu eq 1,120,000 225,000

Value at $200/t 224,000,000$ 45,000,000$

Shs on issue 203,017,222 203,017,222

Value per share 1.10 0.22

Total value per share 1.33$

Figure 12. Project valuation on new forward assumptions Source: DJC

Using an unchanged peer group median EV / t Cu of US$200/t, which at current copper prices represents 2.3% of the value of copper in-situ, and the expanded capital structure after the

recent capital raise, our project value for the current 85.1Mt resource is $136.1M, or $0.67 per

share, a 10% reduction from $0.74 per share due to the withdrawal of cobalt and uranium credits. Using our 12 month forward assumptions however our project valuation increases to $181.2m, or

$1.33, per share, an increase of 98%.

Whilst HCH has cash reserves of $11.5m, we assume that all the cash will be used in defining

the expanded resources and therefore do not include a cash component in our valuation. We

have therefore derived a project valuation only and derive our price target accordingly. We upgrade to a Buy rating, from Speculative Buy, and move our 12 month price target from $0.93 to

$1.33 per share, an increase of 43%.

20 September, 2011 9

CARMICHAEL RESEARCH

RESOURCES

Investment Thesis

We believe HCH provides an opportunity for investors to obtain exposure in an up and coming mineral exploration and now potential development company with a growing Tier 2 asset in one

of the world s premier copper belts.

Very competent technical team: HCH, through their associations with various embedded

consultants and through the considerable experience of the Board, have an exceptionally

competent technical team. The depth of their knowledge of their chosen model and the geology on the ground, has been instrumental in HCH gaining a very early understanding of their projects

and importantly for the future, the ability to very quickly assess new opportunities. This provides

them with the ability to act quickly if need be.

Important Joint Venture Partners: HCH have been very successful in negotiating with, and

entering into a number of JV s, with the large Chilean mining companies, Codelco and CMP. The value of these relationships can not be understated. They have been established over a

considerable period of time and it is not easy for new companies to enter Chile and establish

these types of relationships.

First Resource Estimate provides basis for valuation: HCH have released their maiden

resource at Productora of 85.1Mt at 0.6% Cu (0.8% Cu equiv. after gold and molybdenum credits). This forms the basis of a valuation of $0.67 per share.

Continuing exploration results: The exploration results up to this point show a large

mineralised system is present at Productora and this could grow significantly over the course of

the next 9 months. Any deal with CCHEN to get access to the lease surrounding the Central

Lease will add significant tonnage potential beyond this. Further exploration results from Los Mantos are yet to be received and we expect a maiden resource for Los Mantos late 1H 2012.

Recommendation

Buy: We move our Speculative Buy recommendation on HCH to a Buy.

We anticipate more results to be announced over the course of the next few months. We believe

HCH will continue to get re-rated as successful drill results give more indications of

mineralisation at Productora, new mineralisation discovered through drilling at Los Mantos, a resource update at Productora and a maiden resource at Los Mantos. Economic studies will

continue throughout 2012.

10 20 September 2011

CARMICHAEL RESEARCH

RESOURCES

Risks

Exploration Risk: The exploration risk at Productora has lessened considerably since our

previous note with the publishing of the maiden resource. Investors can now see that mineralisation continues to the north and south of the central lease area and is likely to add

resource tonnes in the mid-2012 estimate. Exploration risk is higher at Los Mantos, drill results

still need to be compiled and a resource has not yet been produced.

Sovereign Risk: Whilst we believe Chile to be one of the most stable countries in South

America, changes in the political landscape can never be ruled out. Chile has an enviable track record in providing a stable political environment in which to attract and retain interest in its

mineral resource industry. Changes to taxation laws, royalties, repatriation of profits for foreign

companies and labour relations can all effect the operations of mineral resource companies.

Commodity Price Risk: Commodities pricing is affected by the outlook for the world s economy

and growth rates. The volatile nature of the commodities markets reflects the uncertain nature of the current world growth outlook in the aftermath of the global financial crisis, and more recently

as a result of the sovereign debt crisis in Europe and the anticipated slowdown in western

economies. Fluctuations in the price of copper could exert an influence on the price of HCH shares.

Exchange Rate Risk: Fluctuations in the exchange rate will affect the exploration expenditure

programs. Exchange rate fluctuations between the Chilean Peso, US Dollar and the Australian

Dollar will be taken into account by HCH in the application of its exploration funds.

Metallurgical Risk: Given the early stage in exploration of their polymetallic deposits, the

process route of any potential operation has not yet been considered and will only be considered

in our view, as part of the scoping study exercise. Metallurgical testwork will be required to find out how much of the copper and additional metals will be potentially recoverable.

20 September, 2011 11

CARMICHAEL RESEARCH

RESOURCES

Disclosure Disclaimer RCAN0981

This Research report, accurately expresses the personal view of the Author.

DJ Carmichael Pty Limited, members of the Research Team; including authors of this report, its directors and employees advise that they may hold securities, may have an interest in and/or earn brokerage and other benefits or advantages, either directly or indirectly from client transactions in stocks mentioned in this report. DJ Carmichael Pty Limited acted for Hot Chili Limited as Lead Manager for the Initial Public Offering and Lead Manager in a capital raise and was paid a fee for this service. DJ Carmichael Pty Ltd are retained by Hot Chili Limited as corporate advisors and is paid a fee for this service. DJ Carmichael Pty Limited holds securities in Hot Chili Limited.

DJ Carmichael Pty Ltd is a wholly owned subsidiary of DJ Carmichael Group Pty Ltd ACN 114 921 247.

In accordance with Section 949A of the Corporations Act 2001 D J Carmichael Pty Limited advise this email contains general financial advice only. In preparing this document D J Carmichael Pty Limited did not take into account the investment objectives, financial situation and particular needs ( financial circumstances ) of any particular person. Accordingly, before acting on any advice contained in this document, you should assess whether the advice is appropriate in light of your own financial circumstances or contact your D J Carmichael Pty Limited adviser. D J Carmichael Pty Limited, its Directors employees and advisers may earn brokerage or commission from any transactions undertaken on your behalf as a result of acting upon this information. D J Carmichael Pty Limited, its directors and employees advise that they may hold securities, may have an interest in and/or earn brokerage and other benefits or advantages, either directly or indirectly, from client transactions. D J Carmichael Pty Limited believe that the advice herein is accurate however no warranty of accuracy or reliability is given in relation to any advice or information contained in this publication and no responsibility for any loss or damage whatsoever arising in any way for any representation, act or omission, whether express or implied (including responsibility to any persons by reason of negligence), is accepted by DJ Carmichael Pty Limited or any officer, agent or employee of D J Carmichael Pty Limited. This message is intended only for the use of the individual or entity to which it is addressed and may contain information that is privileged, confidential and exempt from disclosure under applicable law. If you are not the intended recipient or employee or agent responsible for delivering the message to the intended recipient, you are hereby notified that any dissemination, distribution or copying of this communication and its attachments is strictly prohibited.

The Author of this report made contact with the Hot Chili Limited for assistance with verification of facts, admittance to business sites, access to industry/company information. No inducements have been offered or accepted by the company.

The Author of this report holds securities in Hot Chili Limited.

The recommendation made in this report is valid for four weeks from the stated date of issue. If in the event another report has been constructed and released on Hot Chili Limited, the new recommendation supersedes this and therefore the recommendation in this report will become null and void.

Recommendation Definitions

SPECULATIVE BUY 10% or more outperformance, high risk BUY 10% or more outperformance HOLD 10% underperformance to 10% over performance SELL 10% or more underperformance Period: During the forthcoming 12 months, at any time during that period and not necessarily just at the end of those 12 months.

Stocks included in this report have their expected performance measured relative to the ASX All Ordinaries index. DJ Carmichael Pty Limited s recommendation is made on the basis of absolute performance. Recommendations are adjusted accordingly as and when the index changes.

To elect not to receive any further direct marketing communications from us, please reply to this email and type 'opt out ' in the subject line. Please allow two weeks for request to be processed. © 2011 No part of this report may be reproduced or distributed in any manner without permission of DJ Carmichael Pty Limited.