Embed Size (px)

Citation preview

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

HOT TOPICS

Asia Region Tax

ITR Asia Tax Executives Forum

Singapore, May 8, 2013

Presented By

Eric N. Roose Morrison & Foerster (Moderator)

Amit Gupta, Dell Global BV (Singapore Branch)

Miaw Hui Goh, United Technologies

Peter Ni, Zhong Lun

Pieter de Ridder, Loyens & Loeff

This is MoFo. 2

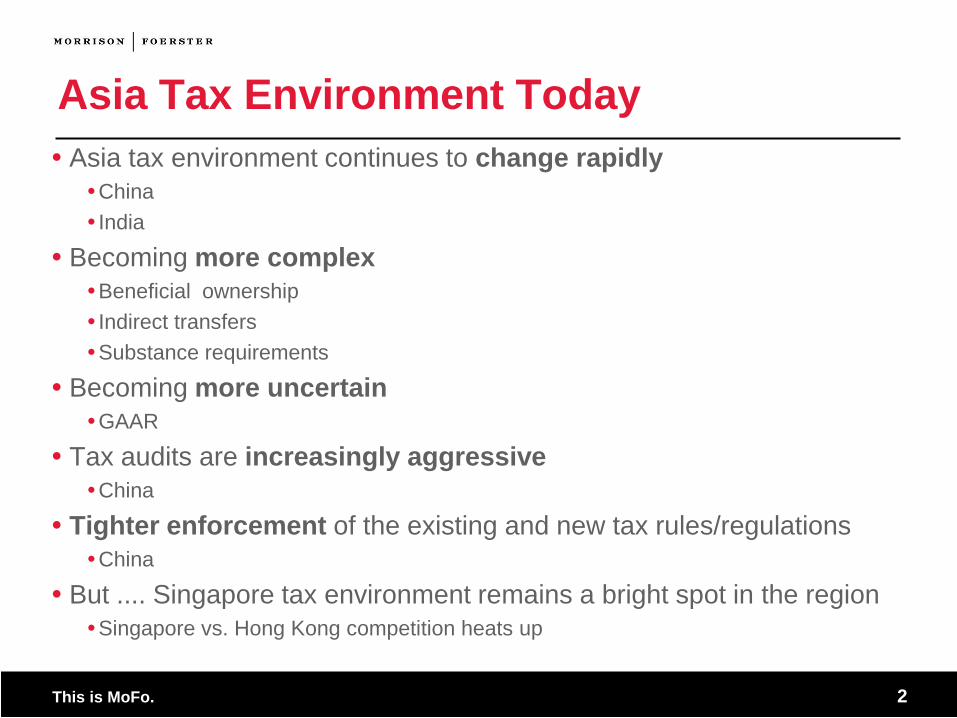

Asia Tax Environment Today

Asia tax environment continues to change rapidly

China

India

Becoming more complex

Beneficial ownership

Indirect transfers

Substance requirements

Becoming more uncertain

GAAR

Tax audits are increasingly aggressive

China

Tighter enforcement of the existing and new tax rules/regulations

China

But .... Singapore tax environment remains a bright spot in the region

Singapore vs. Hong Kong competition heats up

This is MoFo. 3

Hot Topics Beneficial ownership

Anti-abuse legislation to limit treaty benefits

Indirect equity/share transfers

Aggresive tax audits

M&A – Divestiture issues

Myanmar – Taxation Primer

Hong Kong versus Singapore – the competition heats up

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

Beneficial Ownership

Developments

This is MoFo. 5

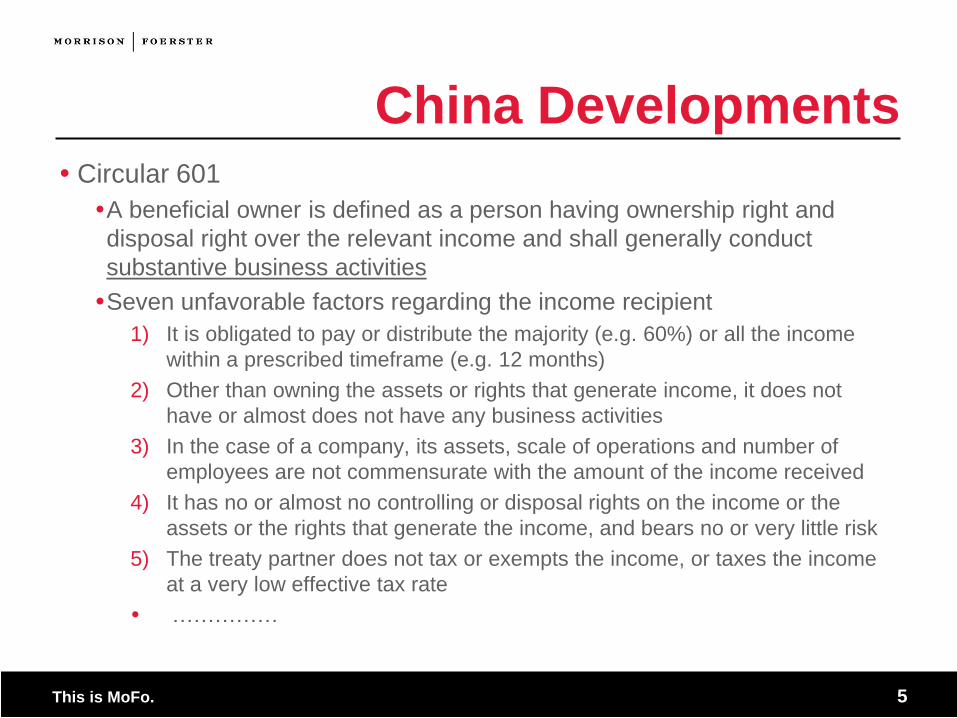

China Developments Circular 601

A beneficial owner is defined as a person having ownership right and

disposal right over the relevant income and shall generally conduct

substantive business activities

Seven unfavorable factors regarding the income recipient

1) It is obligated to pay or distribute the majority (e.g. 60%) or all the income

within a prescribed timeframe (e.g. 12 months)

2) Other than owning the assets or rights that generate income, it does not

have or almost does not have any business activities

3) In the case of a company, its assets, scale of operations and number of

employees are not commensurate with the amount of the income received

4) It has no or almost no controlling or disposal rights on the income or the

assets or the rights that generate the income, and bears no or very little risk

5) The treaty partner does not tax or exempts the income, or taxes the income

at a very low effective tax rate

……………

This is MoFo. 6

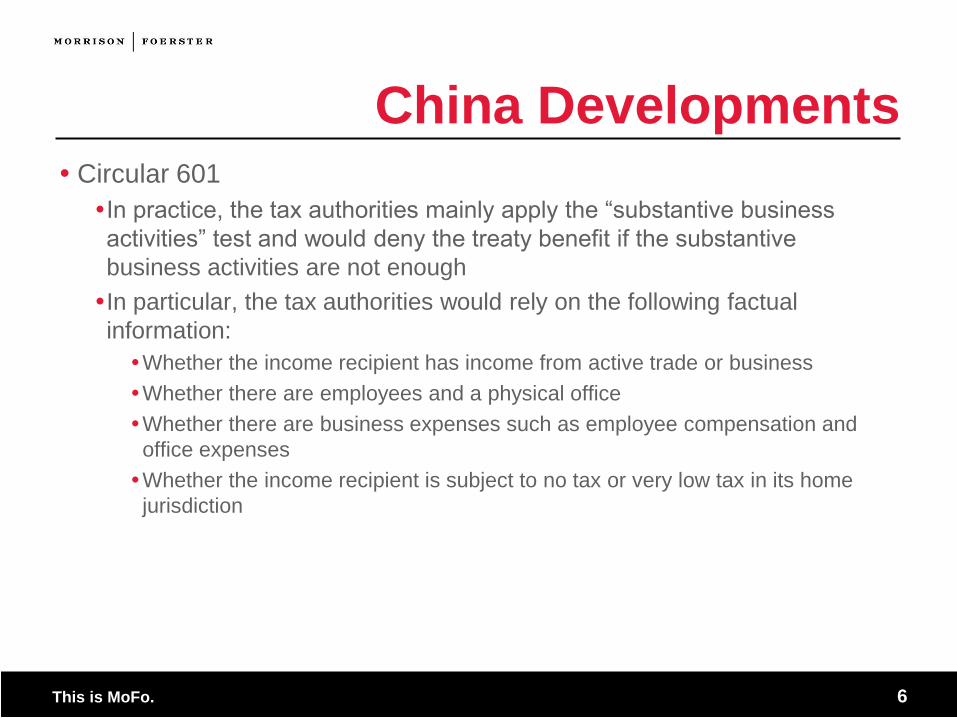

China Developments Circular 601

In practice, the tax authorities mainly apply the “substantive business

activities” test and would deny the treaty benefit if the substantive

business activities are not enough

In particular, the tax authorities would rely on the following factual

information:

Whether the income recipient has income from active trade or business

Whether there are employees and a physical office

Whether there are business expenses such as employee compensation and

office expenses

Whether the income recipient is subject to no tax or very low tax in its home

jurisdiction

This is MoFo. 7

China Developments Circular 30

The determination cannot be just based on the existence of one single

unfavorable factor in Circular 601. Rather, a comprehensive analysis of all

the factors is required

The tax authorities shall review the following information before making a

determination:

Articles of association, financial statements, cash flow records, board meeting

minutes, board resolutions, HR and material resources status, expenditure

information, function and risk assumption status, etc.

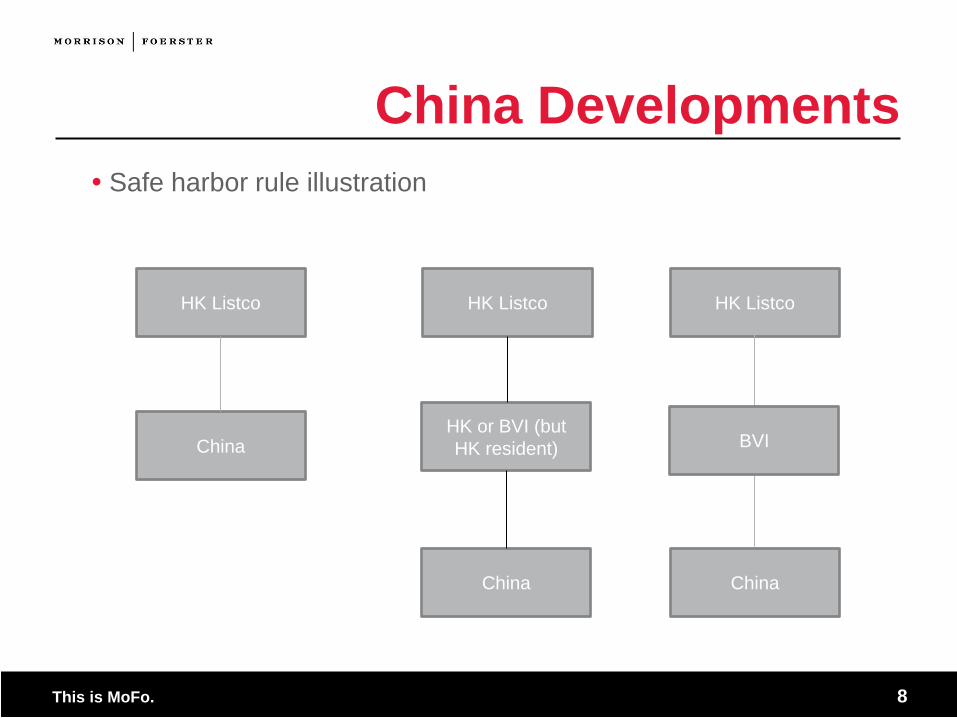

Circular 30 also provides a safe harbor rule

Dividends paid to a non-resident that is publicly listed in the relevant treaty

country and is a tax resident of that country

Dividends paid to a non-resident that is 100% owned (directly or indirectly) by

the above mentioned listed company and is also a tax resident of that country

This is MoFo. 8

China Developments

Safe harbor rule illustration

HK Listco

China

HK Listco

HK or BVI (but

HK resident)

China

76

HK Listco

BVI

China

This is MoFo. 9

China Developments Circular 30

More clarification under Circular 30

The use of payment receipt agent does not t impact the determination of

beneficial ownership, as long as the agent makes an agency declaration

To get the money out quickly, a taxpayer can pay the withholding tax at the

standard rate (10%) and apply for the treaty benefit and a refund later on

If a taxpayer needs to apply with multiple tax authorities (e.g. it has multiple

Chinese subsidiaries) which make different determinations, the taxpayer can

take the applications to the upper level tax authorities for a final decision

Circular is helpful but still too general regarding how to determine the

beneficial ownership

This is MoFo. 10

China Developments Circular 165 (Brand New)

Issued on April 12 but still not made public as of May 3

Good news to taxpayers

If a HK applicant doesn’t distribute dividends to its non-HK shareholders, it is

out of the first unfavorable factor stipulated in Circular 601

Investments in subsidiaries (e.g. holding companies) are considered

“substantive business activities”

A holding company formed purely for holding one subsidiary shall still be

respected if other factors support the determination

Assets don’t equal registered capital. Also, one cannot just rely on the number

of the employees or labor costs when making a determination. Rather, the

focus should be on their job responsibilities and substance

As to whether the HK applicant has enough controlling or disposal rights on the

income or the assets/rights generating the income, and bears enough risk, the

answer should be yes if the articles of association confirm that and the relevant

decisions are made by its own decision making authority, e.g. the board

The fact that HK doesn’t tax non-HK sourced income is not considered a key

unfavorable factor

This is MoFo. 11

China Beneficial Ownership Local tax bureau asking more detailed questions/information

- background of the foreign shareholder

- why the shareholder is established in that country e.g. Hong Kong

- why business income is small, compared to investment income

- copies of Board minutes , financial statements of Shareholder (in Chinese)

- why the 601 unfavorable factors do not apply

Trend is likely to continue and process may become increasingly difficult

Delay in processing and approving the reduced WHT application

Maintain good relationship and close communications with local tax bureau

Educate/train the local finance team to respond to the tax bureau’s queries

Work towards obtaining the 5% WHT and avoid creating a bad precedent

This is MoFo. 12

India – Beneficial Ownership

Requirement of Tax Residency Certificate (TRC) in specified format

scrapped as per amended Finance Bill 2013 dated 30 April 2013;

TRC is a valid proof of residence; Assessee shall be required to

provide such other documents and information, as may be

prescribed along with the TRC

‘Beneficial Ownership’ under GAAR will be questioned specifically in

the context of capital gains (for royalties, etc. BO is already required):

Corporate structure maybe disregarded

Treaty benefits denied

Place of residence and/or situs of an asset can be reassigned

Article 13 of Mauritius India tax treaty doesn’t mention “beneficial

owner”, it just mentions “resident” of a contracting state

GAAR WILL SHIFT THE FOCUS TO SUBSTANCE OVER FORM

This is MoFo. 13

Indonesia Developments

Beneficial ownership victories for the taxpayer in the Tax Court

concerning pre-2010 cross border payments

Also victories for the taxpayer on the ‘mode of application’ stance of

the Tax Office as per their 2005 tax circular

Tax treaty Indonesia/Hong Kong took effect on 1 January 2013

5% dividend WHT rate if > 25% interest

Income tax exemption on sale of shares of Indonesian company

10% interest WHT

Beneficial ownership requirement, business purpose test, Indonesian domestic

anti avoidance tax provisions may be applied

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

Anti Abuse Rules

Developments

This is MoFo. 15

China Developments

Chinese GAAR

Targeted arrangements of the Chinese GAAR

Abuse of tax incentives

Abuse of tax treaties (Circular 601)

Abuse of corporate vehicle (Circular 698)

Use of tax havens to avoid taxes

Other arrangements that lack business purposes

The current focus is on cross-border transactions (as opposed to

domestic transactions)

The Chinese tax authorities are enforcing such rules diligently and

aggressively

China joined the Joint International Tax Shelter Information Centre

(JITSIC) in 2011

The enforcement of the Chinese GAAR is a new focus of the Chinese tax

authorities

This is MoFo. 16

India Developments

GAAR in India will be effective from April 1, 2015 (FY2015-16)

Any arrangement “main purpose of which is to obtain a tax benefit”

can be regarded as “impermissible avoidance arrangement”

“Tax benefit” includes a reduction or avoidance or deferral of Indian

tax, as a result of a tax treaty

Burden of proof that an arrangement is not entered into for the

purpose of obtaining a tax benefit is on the assessee (tax payer)

No grandfathering for investments already in place before August,

2010

No monetary threshold of the tax benefit for invoking GAAR

prescribed

This is MoFo. 17

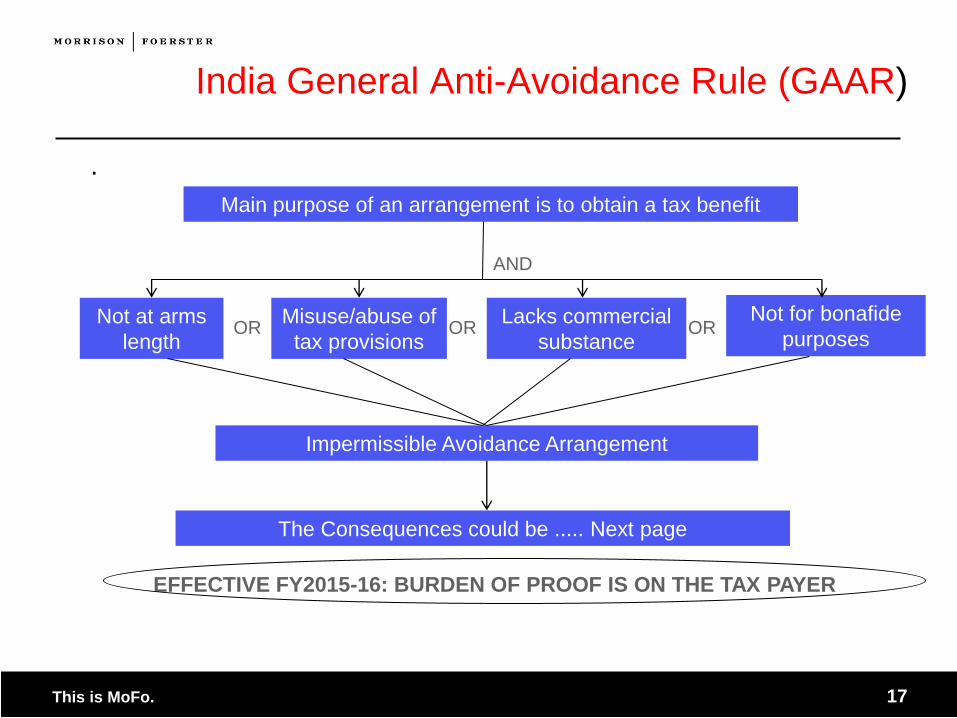

India General Anti-Avoidance Rule (GAAR)

.

Main purpose of an arrangement is to obtain a tax benefit

AND

Not at arms

length

Misuse/abuse of

tax provisions OR

Lacks commercial

substance OR

Not for bonafide

purposes OR

Impermissible Avoidance Arrangement

The Consequences could be ..... Next page

EFFECTIVE FY2015-16: BURDEN OF PROOF IS ON THE TAX PAYER

This is MoFo. 18

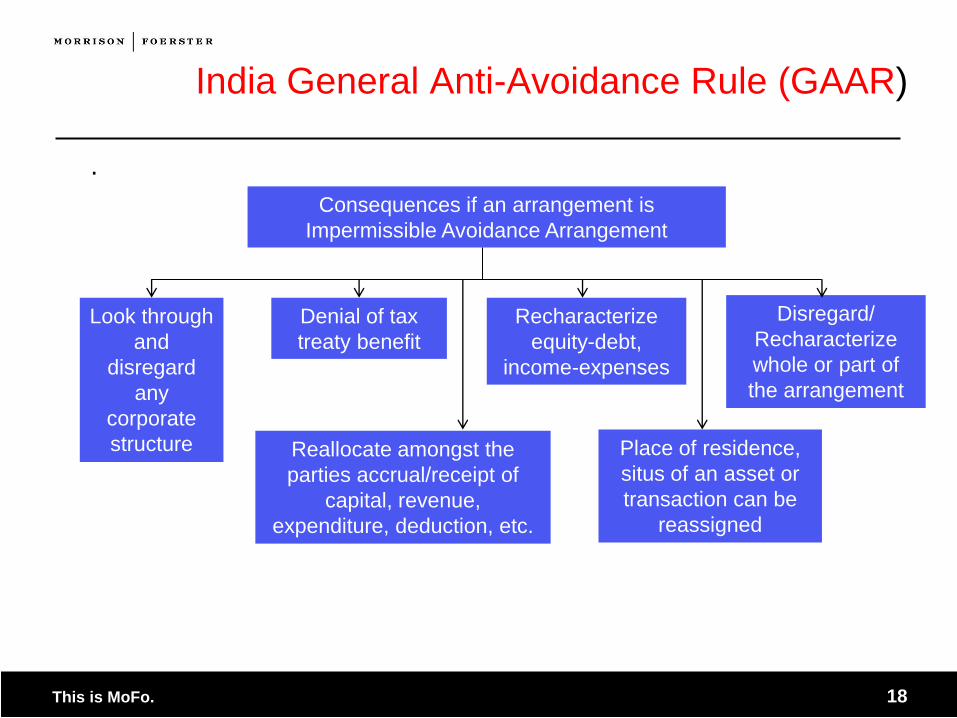

India General Anti-Avoidance Rule (GAAR)

.

Consequences if an arrangement is

Impermissible Avoidance Arrangement

Look through

and

disregard

any

corporate

structure

Denial of tax

treaty benefit

Recharacterize

equity-debt,

income-expenses

Disregard/

Recharacterize

whole or part of

the arrangement

Reallocate amongst the

parties accrual/receipt of

capital, revenue,

expenditure, deduction, etc.

Place of residence,

situs of an asset or

transaction can be

reassigned

This is MoFo. 19

Indonesia Developments

Much focus on cross border transfer pricing matters by the Tax

Office

Purchasing

Sales

Royalties

Intra-group services

Both income tax and VAT

Fake invoices

This is MoFo. 20

Singapore Developments

The High Court on 18 December 2012 handed down its decision on

an appeal by AQQ against the decision of Board of Review regarding

the application of the general anti avoidance provision of s.33 ITA

AQQ v CIT [2012] SGHC 249

This is MoFo. 21

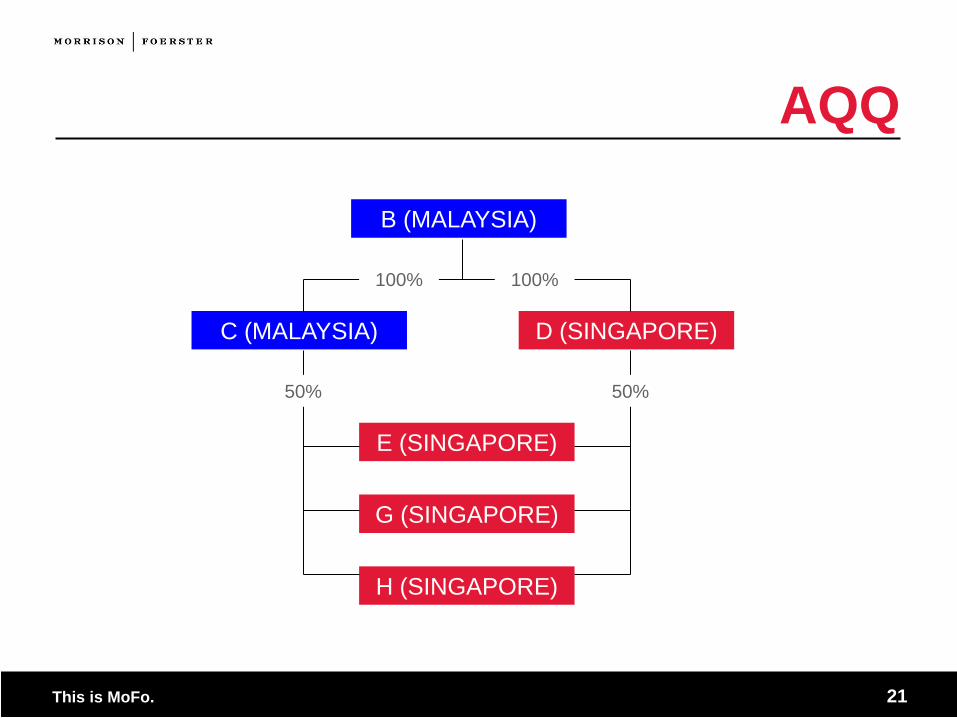

AQQ

B (MALAYSIA)

C (MALAYSIA) D (SINGAPORE)

E (SINGAPORE)

G (SINGAPORE)

H (SINGAPORE)

100% 100%

50% 50%

This is MoFo. 22

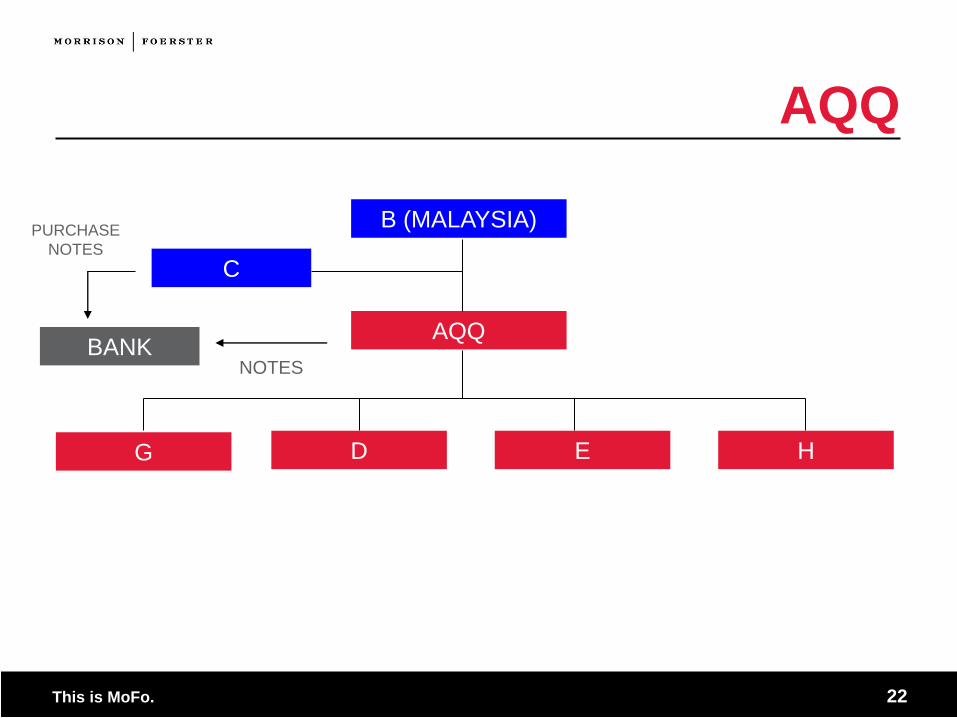

AQQ

B (MALAYSIA)

AQQ

G D E H

BANK NOTES

C

PURCHASE

NOTES

This is MoFo. 23

AQQ

s.33(1) Predication principle: to objectively determine whether the

purpose or effect of an arrangement is to reduce or avoid tax, with

reference to the terms of the arrangement and the manner in which it

was implemented

Two part structure: the Restructuring and the Financing Arrangement

High Court agreed with BOR that the Financing Arrangement fell

within s.33 ITA:

Interest expenses reduced the chargeable dividend income and

no withholding tax on the interest due to interposing a bank and

stripping coupons from principal of financing

This is MoFo. 24

AQQ

s.33(3) – Subjective motive test: Was the arrangement carried out

for bona fide commercial reasons and had not as one of its main

purposes the avoidance or reduction of tax?

The Restructuring: yes

The Financing Arrangement: no, based on the relevant evidence: it

was done to monetize s.44 credits of the SPO subsidiaries

The Comptroller’s counteraction powers were not exercised in a fair

and reasonable manner as he should not have disregarded the

dividend income and certain of the interest expenses

Therefore AQQ won the case

AQQ highlights that the Comptroller is vulnerable to his

counteraction being invalidated unless he gets it absolutely right

This is MoFo. 25

Dealing with GAAR Ensure underlying tax processes are strong

Ensure activities are understood, properly analyzed and documented

e.g. business purpose and substance for the transaction

Watch out for published tax cases where tax authorities have challenged

transactions and are overly aggressive

Monitor legislative developments especially tax rules that have retroactive

application to prior years

Manage relationships with the relevant tax authorities

Increase awareness of key stakeholders on GAAR rules, and

on the importance of documentation and communications through email

E.g. Be careful about documenting tax risks, especially via email

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

Indirect Transfer

Developments

This is MoFo. 27

China Developments

Unanswered questions under Circular 698

What kind of business purpose is considered a reasonable business

purpose for setting up the offshore holding company

Whether there shall be a safe harbor rule under which an indirect minority

shareholder can be exempt from the Circular 698 reporting requirement

Whether the transfer of red chip company shares should be exempt from

the Circular 698 reporting requirement

Whether and how the offshore holding company being transferred can get

a tax basis step-up in its Chinese subsidiary to avoid potential double

taxation

Whether a group transfer relief will be available anytime soon

What is the penalty for non-compliance

This is MoFo. 28

India Developments

Indirect transfers now liable to tax - Supreme Court decision in

Vodafone overturned:

Retroactive amendment made (wef FY1961-62)

Typically intended to apply where shares derive value “substantially” from assets in

India

“Substantially” not defined

Validation Clause inserted in Finance Act 2012 - Notwithstanding

anything contained in any judgment, decree or order of any Court or

Tribunal or any authority, all notices sent or purporting to have been

sent, or taxes levied, demanded, assessed, imposed, collected or

recovered or purporting to have been levied, demanded, assessed,

imposed based on the retroactive amendments shall be valid

This is MoFo. 29

Indonesia Developments

Art 18 enables the Tax Office to disregard the immediate foreign

holding company if there is a special relationship and either the

transaction was not at arm’s length or if the foreign holding company

is located in a tax haven jurisdiction

No statutory definition of ‘tax haven’ but based on notes to the

Corporate Income Tax return, the term tax haven is a country with a

CIT return of less than half of Indonesia’s or if it has a bank secrecy

or limited exchange of information legislation

Singapore a tax haven?

Thus far relatively few cases reported where Tax Office is taking

action

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

Aggressive Tax Audits

This is MoFo. 31

The Environment in China Tax authorities are strengthening their tax collection and nationwide tax

inspections

Tax authorities are also increasingly more aggressive and enforcing the

rules more tightly

Jurisdictions behind their local tax revenue target could be driven to being

very “creative” in interpreting certain tax rules

Once tax audit is launched, tax officers may be very impatient and want to

close the case and collect the tax as soon as possible

Instead of being reasonable, they may take an overly creative position and

disregard the technical analysis of the tax issues

This is MoFo. 32

Tax Audits in China The recent focus of the Chinese tax authorities during tax audits:

- Intercompany charges such as service fee, royalty fee, etc

- Reversal of provisions/accruals that have been adjusted in prior years

- Legitimate supporting documents for tax deduction/credit

- Cross border restructuring

- Mergers/Acquisitions

- HNTE status qualification

(HNTE = High New Technology Enterprise)

- Transfer Pricing

This is MoFo. 33

India

Shell, Vodafone challenged on valuation of shares from transfer

pricing perspective:

Shell India issued shares to its parent

TPO/Tax office challenged that shares have been undervalued

Treating it as “income foregone” and levying interest on short receipt

(characterized as loan)

Tolerance band amended for Transfer Pricing:

1% in case of wholesale traders

3% in all other cases

TP Circulars issued on conditions for identifying development

centers engaged as contract research and development (R&D)

service providers with insignificant risk and on application of profit

split method in case of controlled transactions involving R&D activity

This is MoFo. 34

Indonesia

Tax audit procedures implemented in late 2011

Income tax and VAT on cross border transactions between related

parties

Tax Office has almost finished the first MAP case and is said to be

prepared to take on many MAP and APAs

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

M&A - Divestitures

This is MoFo. 36

M&A – Divestitures (China) 1/2

Managing the Capital Gains Tax (“CGT”) payable arising from the direct sale of a

Chinese entity, from Non Resident Enterprise (“NRE”) to NRE in China can be costly & tedious:

A Valuation Report of the divested entity is likely to be required by tax authorities, even

when the target entity is sold to unrelated Buyer or when Sales Proceeds>Investment Cost

It may be practically difficult for the non Resident Seller to:

- file the Capital Gains Tax Return without a Valuation Report;

- determine the cost base for calculating the capital gain (with supporting documentation);

- compute the right amount of CGT Payable (which exchange rates will apply etc?); and

- remit the monies to pay the CGT, Stamp Duty timely and to avoid any late payment

surcharges, which process is complicated by:

- currency fluctuations, enough buffer to cover CGT amount

- unexpected requirement from tax bureau to move up or push out the tax payment,

- Bank’s local practice for handling the exchange rate,

- balance refund to the NRE Seller,

- procedures and formalities both external and internal, etc

This is MoFo. 37

M&A – Divestitures (China) 2/2

If the Chinese entity is part of a Global Divestiture, would require the following:

- Separate Equity Transfer Agreement for each of the Chinese entity;

(each with an acceptable equity transfer price)

- Basis and allocation of the Global Purchase Price to the Chinese entity,

preferably followed by an external Valuation Report

Nil CGT filing may be rejected by tax bureau yet requested by the Buyer as evidence

that the tax filing obligation has been met

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

Myanmar

This is MoFo. 39

Myanmar

New Foreign Investment Law on 3 November 2012 and Foreign Investment

Rules issued on 31 Jan 2013

No 100% foreign ownership for investments in public health, natural

resources, environment, agriculture, livestock farming, fisheries,

manufacturing, services done by Myanmar citizens

Minimum investment of USD 500K for industrial projects and USD 300K for

service related activities

Local staff must be trained to increasingly fill skilled positions over time

5 Years Corporate Income Tax holidays can be enjoyed

Companies (FIL and non-FIL) and branches registered under the FIL are

subject to 25% CIT

Branches (non FIL) 35% CIT

Individual income tax rate is maximum 20% for residents – BIK planning may

reduce the tax burden

This is MoFo. 40

Myanmar

No VAT but Commercial Tax on prescribed goods and services with

rates mostly at 5% or 8% or up to 100% on certain luxurious or what

the government considers to be undesirable products

Customs duties range between 5-40%

No dividend withholding tax

15% interest withholding tax on cross border payments

20% royalty withholding tax on cross border payments

Non Resident Capital Gains Tax is 40% on disposal of shares of a

Myanmar company

Myanmar has 10 tax treaties which are currently in force: India,

Korea, Malaysia, Singapore, Thailand, UK, Vietnam

And tax treaties with Bangladesh, Indonesia and Laos which are

signed but not yet in force

© 2

011 M

orr

ison &

Foers

ter

LLP

| A

ll R

ights

Reserv

ed | m

ofo

.com

Hong Kong versus

Singapore

This is MoFo. 42

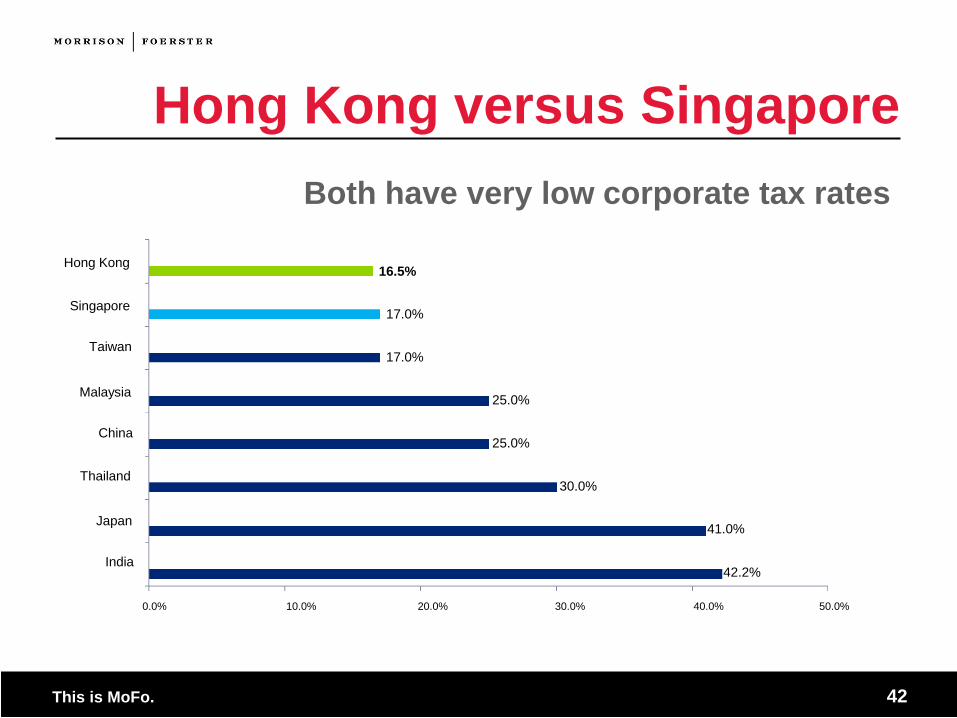

Hong Kong versus Singapore

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Hong Kong

Singapore

Taiwan

Malaysia

China

Thailand

Japan

India

16.5%

17.0%

17.0%

25.0%

25.0%

30.0%

41.0%

42.2%

Both have very low corporate tax rates

This is MoFo. 43

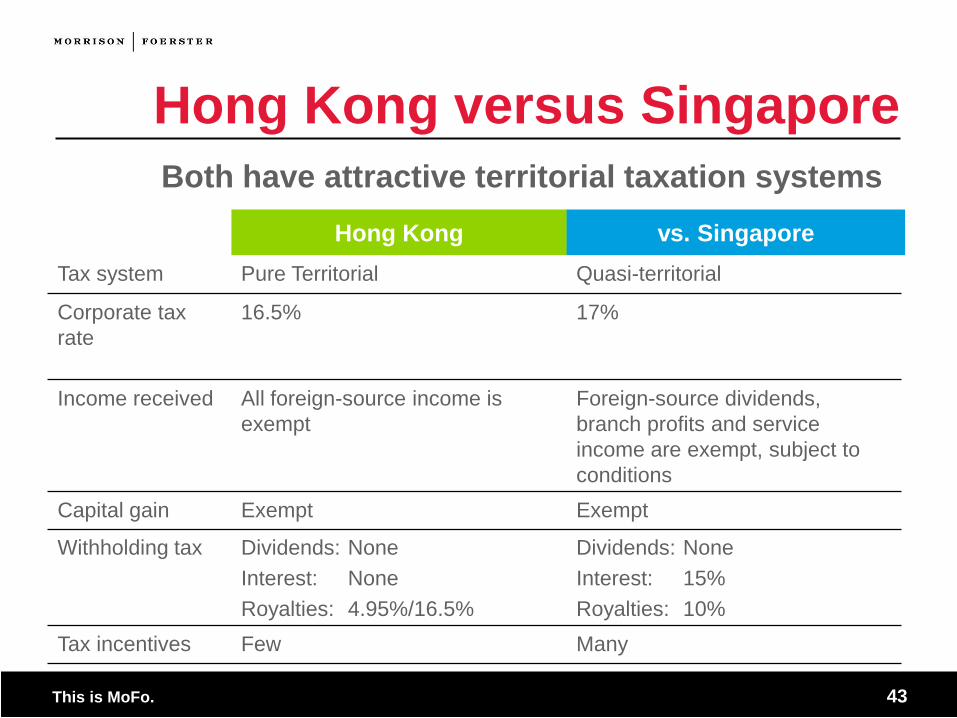

Hong Kong versus Singapore

Hong Kong vs. Singapore

Tax system Pure Territorial Quasi-territorial

Corporate tax

rate

16.5% 17%

Income received All foreign-source income is

exempt

Foreign-source dividends,

branch profits and service

income are exempt, subject to

conditions

Capital gain Exempt Exempt

Withholding tax Dividends: None

Interest: None

Royalties: 4.95%/16.5%

Dividends: None

Interest: 15%

Royalties: 10%

Tax incentives Few Many

Both have attractive territorial taxation systems

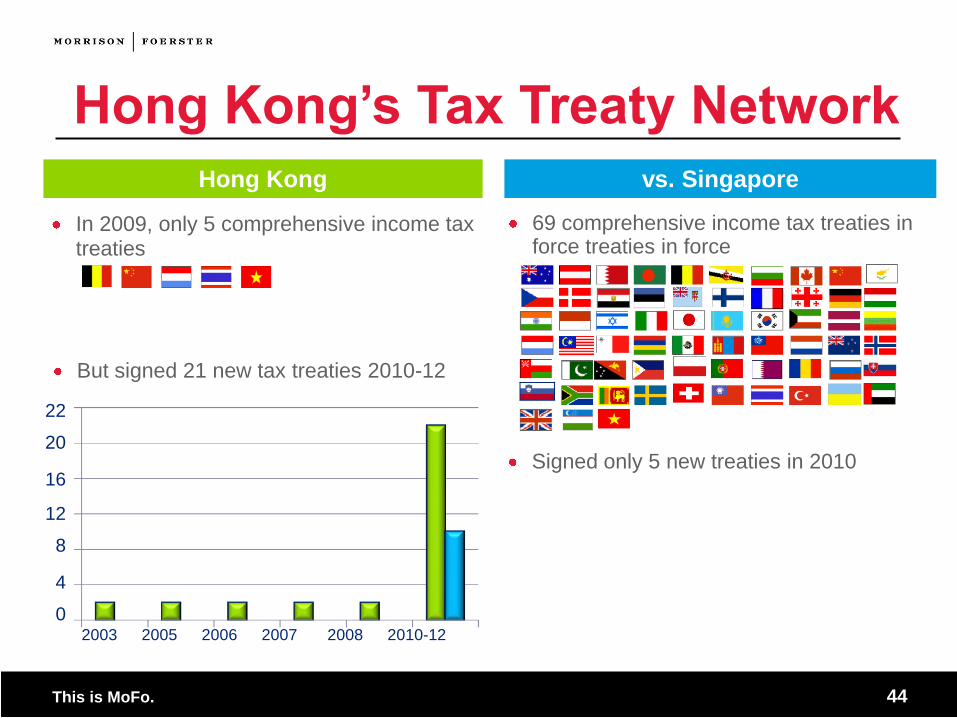

This is MoFo. 44

Hong Kong

vs. Singapore

In 2009, only 5 comprehensive income tax treaties

But signed 21 new tax treaties 2010-12

2003 2005 2006 2007 2008 2010-12

22

20

16

12

8

4

0

Signed only 5 new treaties in 2010

69 comprehensive income tax treaties in force treaties in force

Hong Kong’s Tax Treaty Network

This is MoFo. 45

Regional Holding Company

HONG KONG

Foreign dividends offshore sourced and non taxable

Gains on disposal of securities either non-taxable (capital gains)

or taxable (revenue gains) unless offshore sourced

No dividend withholding tax in Hong Kong

Growing tax treaty network (21 DTA’s in effect)

Good treaties with PRC, Indonesia

This is MoFo. 46

Regional Holding Company

Singapore Foreign dividends either offshore sourced and non taxable

(unless remitted to Singapore) or tax exempt

Headline tax rate at least 15%

Foreign income taxed (income tax or dividend withholding tax)

Gains on disposal of securities non taxable if either capital gain or if Singapore company holds an interest of at least 20% of ordinary shares and has held these shares for at least 24 months

No dividend withholding tax in Singapore

Wide tax treaty network (69 DTA’s in effect)

Good treaties with PRC, India, Vietnam and Japan

This is MoFo. 47

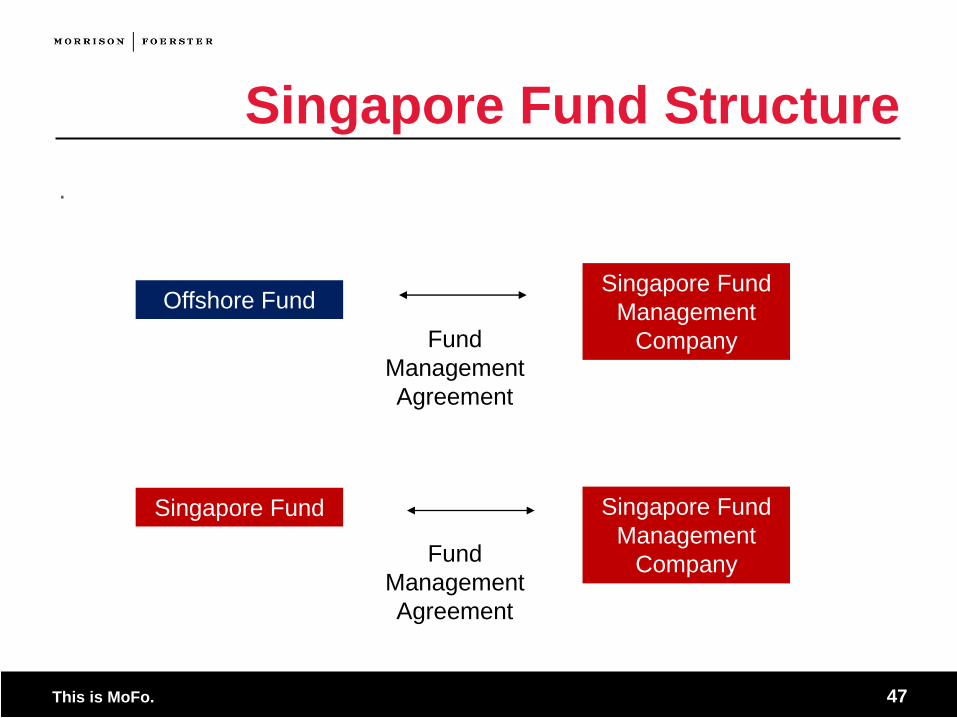

Singapore Fund Structure

.

Offshore Fund Singapore Fund

Management

Company Fund

Management

Agreement

Singapore Fund

Management

Company Fund

Management

Agreement

Singapore Fund

This is MoFo. 48

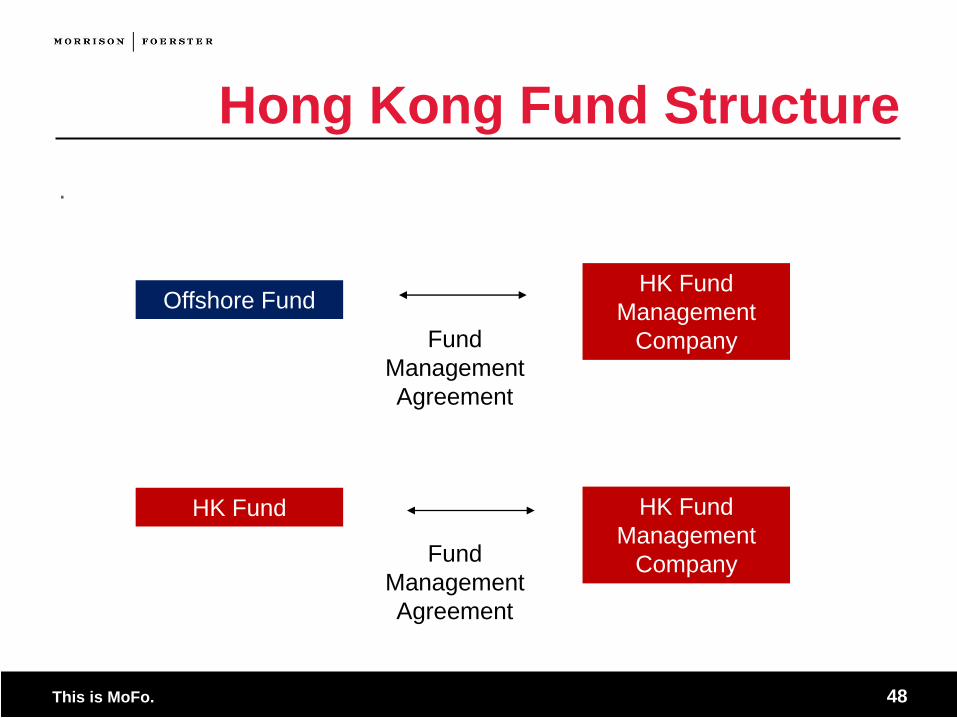

Hong Kong Fund Structure

.

Offshore Fund HK Fund

Management

Company Fund

Management

Agreement

HK Fund

Management

Company Fund

Management

Agreement

HK Fund

This is MoFo. 49

Q & A

.

![INTEREST PAYABLE BY THE TAXPAYER UNDER …As amended by Finance Act, 2018] INTEREST PAYABLE BY THE TAXPAYER UNDER THE INCOME-TAX ACT Introduction Under the Income-tax Act, different](https://img.pdfslide.net/doc/110x75/5b0ae0877f8b9a45518cf93c/interest-payable-by-the-taxpayer-under-as-amended-by-finance-act-2018-interest.jpg)