Embed Size (px)

Citation preview

NCBJ Retail Panel

Hot Topics in Recent Retail Cases National Conference of Bankruptcy Judges October 31, 2019

KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Panelists Agenda

James H. M. Sprayregen Overview

Kenneth H. Eckstein Retail Today: The View From The Trenches

Bob Duffy Wholesale Model vs DTC Model

Mo Meghji IP and Distressed Retailers

How to Save a Distressed Retailer

Leases and Landlords

Financing Retailers in Bankruptcy

2 KIRKLAND & ELLIS LLP

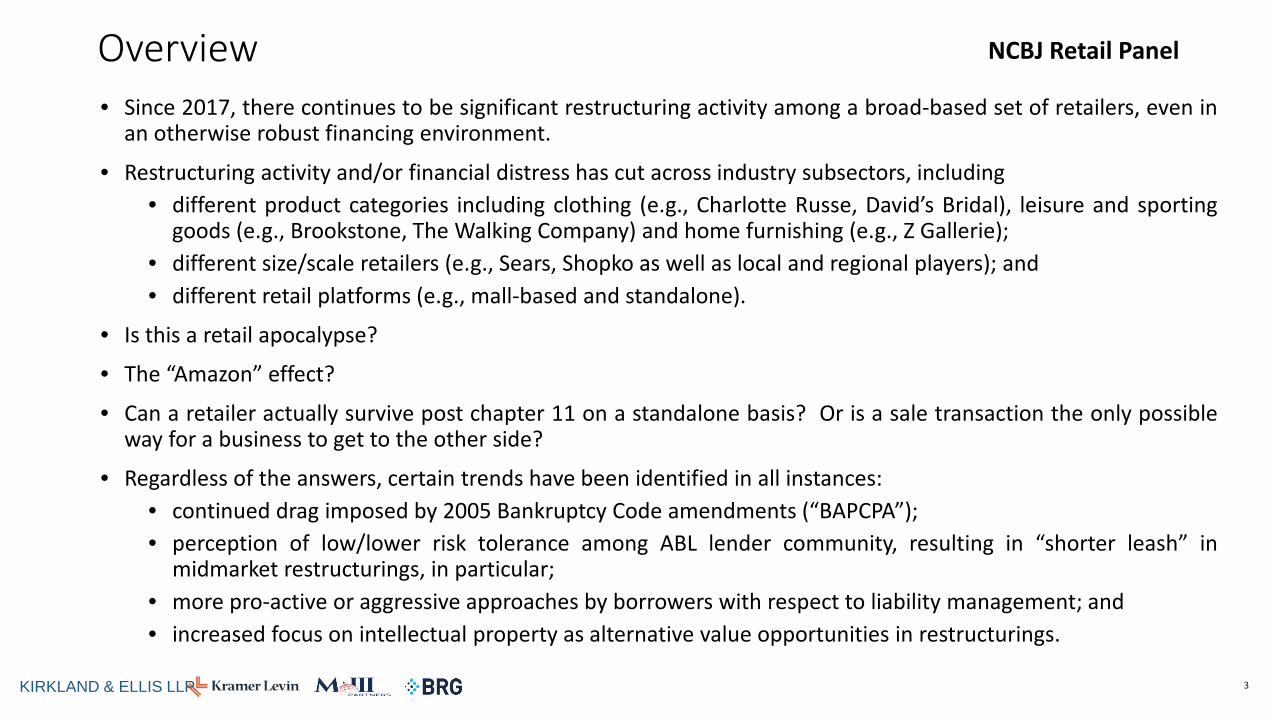

NCBJ Retail Panel Overview • Since 2017, there continues to be significant restructuring activity among a broad-based set of retailers, even in

an otherwise robust financing environment.

• Restructuring activity and/or financial distress has cut across industry subsectors, including • different product categories including clothing (e.g., Charlotte Russe, David’s Bridal), leisure and sporting

goods (e.g., Brookstone, The Walking Company) and home furnishing (e.g., Z Gallerie); • different size/scale retailers (e.g., Sears, Shopko as well as local and regional players); and • different retail platforms (e.g., mall-based and standalone).

• Is this a retail apocalypse?

• The “Amazon” effect?

• Can a retailer actually survive post chapter 11 on a standalone basis? Or is a sale transaction the only possible way for a business to get to the other side?

• Regardless of the answers, certain trends have been identified in all instances: • continued drag imposed by 2005 Bankruptcy Code amendments (“BAPCPA”); • perception of low/lower risk tolerance among ABL lender community, resulting in “shorter leash” in

midmarket restructurings, in particular; • more pro-active or aggressive approaches by borrowers with respect to liability management; and • increased focus on intellectual property as alternative value opportunities in restructurings.

3 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Retail Today: The View From The Trenches

KIRKLAND & ELLIS LLP 4

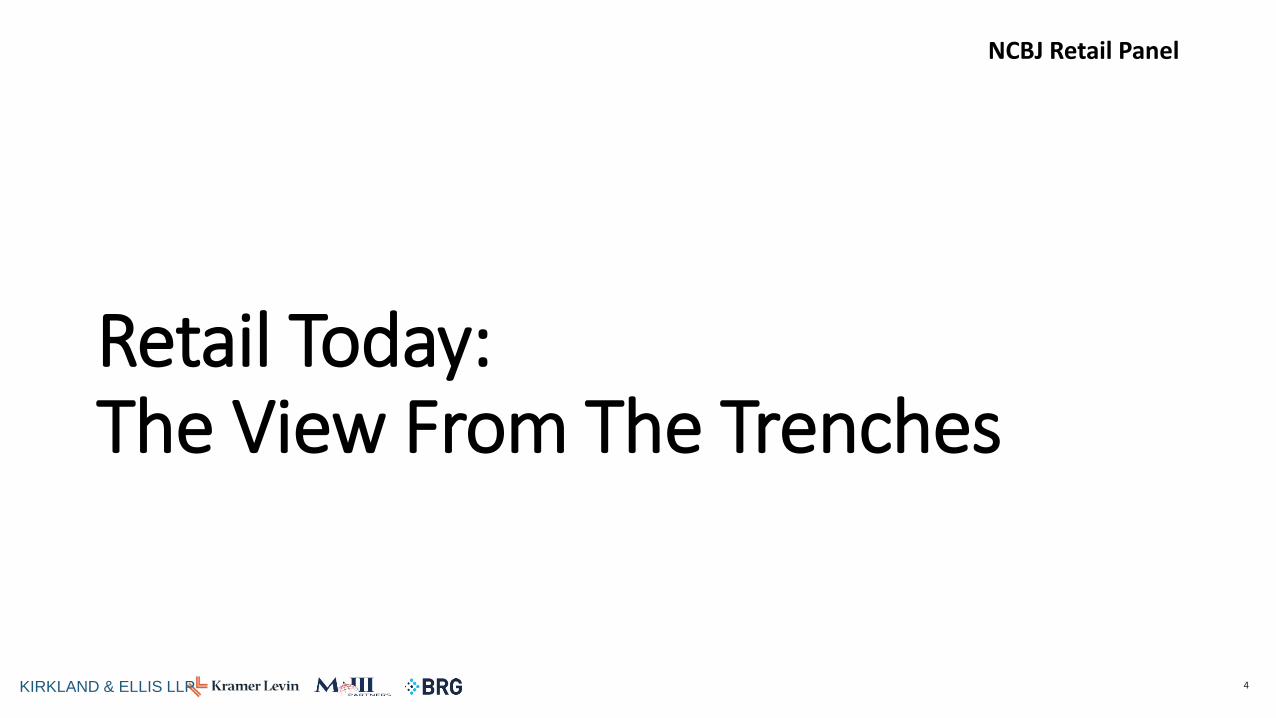

The retail apocalypse is shutting down flagship stores. Associated Press

5

I N D U S T R Y W I D E C O N C E R N

…that [retail] bubble has now burst. We are seeing the results, doors shuttering and rents retreating. This trend will continue for the foreseeable future, and may even accelerate…

Richard Hayne , CEO Urban Outfitters

We’ve not seen this number of distressed retailers since 2009 in the Great Recession.

Brian Cornell, CEO Target

Retail graveyard: More than 8,900 U.S. stores have closed this year.

Moneywatch

Retailers are building themselves into trouble

Supermarket

News

The disruption in the industry is driving concern with investors, creditors, industry analysts and – most of all – the companies themselves.

There is a retail bubble— and it’s bursting

CNN Money

Rise of Amazon leaves even more retailers in intensive care.

CNN Wire

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

6

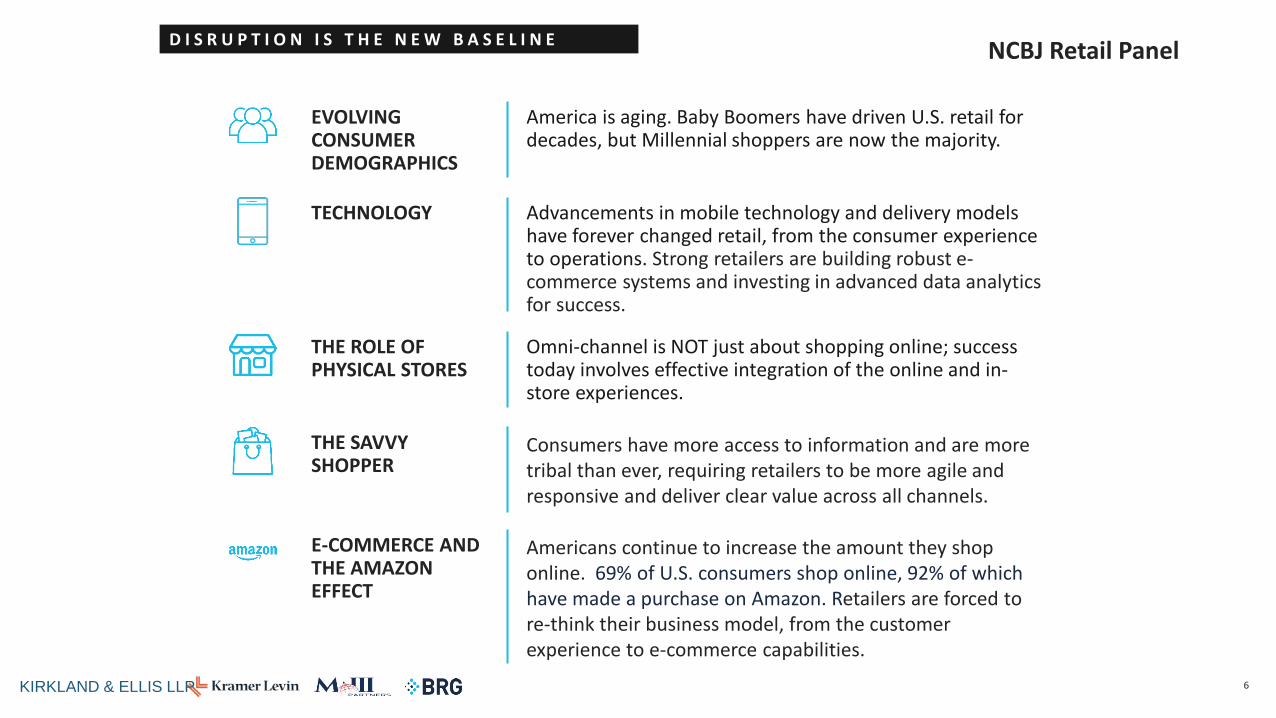

D I S R U P T I O N I S T H E N E W B A S E L I N E

America is aging. Baby Boomers have driven U.S. retail for decades, but Millennial shoppers are now the majority.

Omni-channel is NOT just about shopping online; success today involves effective integration of the online and in-store experiences.

EVOLVING CONSUMER DEMOGRAPHICS

Advancements in mobile technology and delivery models have forever changed retail, from the consumer experience to operations. Strong retailers are building robust e-commerce systems and investing in advanced data analytics for success.

TECHNOLOGY

THE ROLE OF PHYSICAL STORES

Consumers have more access to information and are more tribal than ever, requiring retailers to be more agile and responsive and deliver clear value across all channels.

THE SAVVY SHOPPER

E-COMMERCE AND THE AMAZON EFFECT

Americans continue to increase the amount they shop online. 69% of U.S. consumers shop online, 92% of which have made a purchase on Amazon. Retailers are forced to re-think their business model, from the customer experience to e-commerce capabilities.

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

7

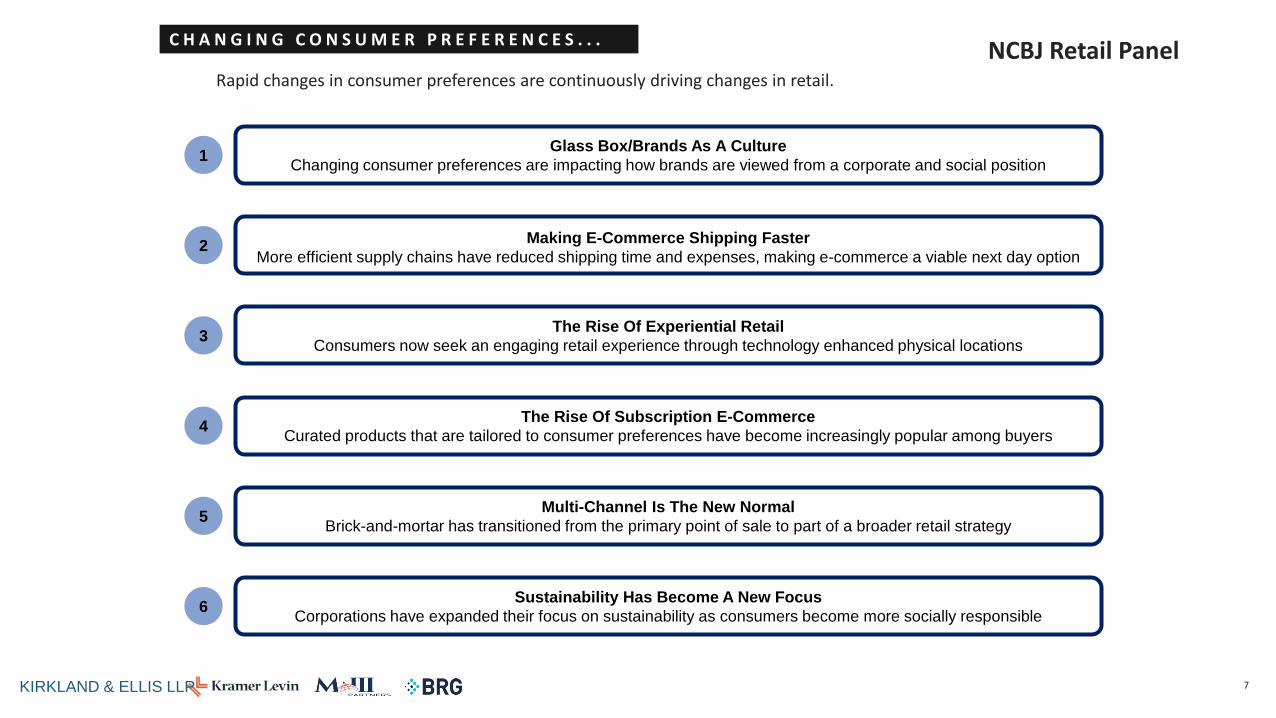

C H A N G I N G C O N S U M E R P R E F E R E N C E S . . .

Rapid changes in consumer preferences are continuously driving changes in retail. NCBJ Retail Panel

Glass Box/Brands As A Culture Changing consumer preferences are impacting how brands are viewed from a corporate and social position 1

Making E-Commerce Shipping Faster More efficient supply chains have reduced shipping time and expenses, making e-commerce a viable next day option

2

The Rise Of Experiential Retail Consumers now seek an engaging retail experience through technology enhanced physical locations 3

The Rise Of Subscription E-Commerce Curated products that are tailored to consumer preferences have become increasingly popular among buyers 4

Multi-Channel Is The New Normal Brick-and-mortar has transitioned from the primary point of sale to part of a broader retail strategy 5

Sustainability Has Become A New Focus Corporations have expanded their focus on sustainability as consumers become more socially responsible 6

KIRKLAND & ELLIS LLP

8

. . . I S I N F L U E N C I N G T H E T R A N S I T I O N I N R E T A I L

Retail isn’t going away. In fact, it’s growing. It just doesn’t look like it did 10 years ago and will continue to evolve.

YESTERDAY / TODAY TODAY / TOMORROW

GENERAL MERCHANDISE

APPAREL/ FOOTWEAR/ ACCESSORIES

SPECIALTY

ELECTRONICS/ TOYS

FOOD/ HEALTH & BEAUTY/Rx

RadioShack Gander Mountain Borders The Sports

Authority MC Sports Hibbet Guitar Center Advanced Auto

AutoZone Pep Boys O’Reilly Office Depot

The Limited Payless American Apparel Crocs

Wet Seal Bebe Stores J Crew Forever 21 David's Bridal

Claire’s Foot Locker Chico’s BCBG

Sears Kmart JC Penney

Macys Dillard's Stage Stores

Stein Mart Bon Ton

Circuit City hhGregg

Toys R Us GameStop

A&P BI-LO Winn Dixie

GNC Hello Fresh Vitamin Shoppe

Blue Apron

Amazon Dollar General Dollar Tree

Five Below Walmart Target

Nordstrom Neiman Marcus

Amazon TJX H&M

Bonobos Old Navy Urban Outfitters

Uniqlo Coach Tiffany

Amazon Walmart Ross Dick’s

Staples Tractor Supply Victoria Secret

Restoration Hardware

Apple Amazon

Walmart Costco

Sam’s Club Best Buy

Amazon Aldi Lidl

Trader Joes Walgreens Ulta

Sephora

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

9

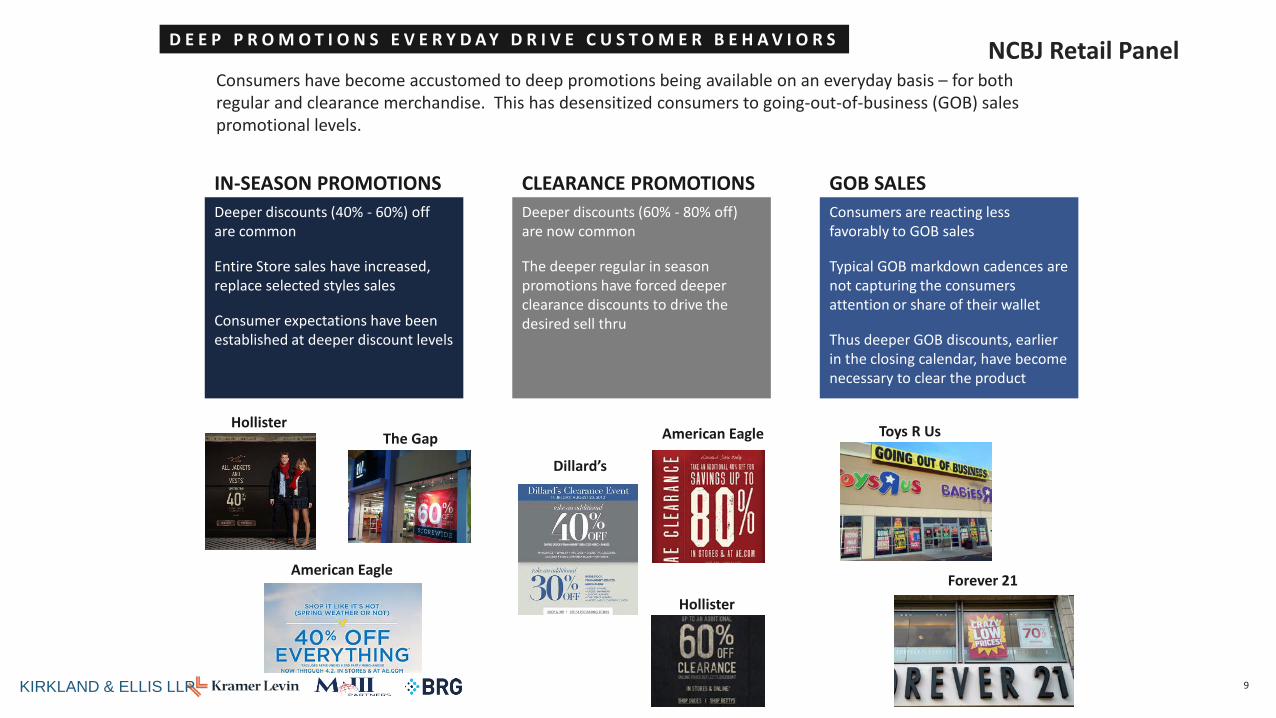

D E E P P R O M O T I O N S E V E R Y D A Y D R I V E C U S T O M E R B E H A V I O R S

Consumers have become accustomed to deep promotions being available on an everyday basis – for both regular and clearance merchandise. This has desensitized consumers to going-out-of-business (GOB) sales promotional levels.

IN-SEASON PROMOTIONS CLEARANCE PROMOTIONS Deeper discounts (40% - 60%) off are common

Entire Store sales have increased, replace selected styles sales

Consumer expectations have been established at deeper discount levels

Deeper discounts (60% - 80% off) are now common

The deeper regular in season promotions have forced deeper clearance discounts to drive the desired sell thru

Hollister The Gap

American Eagle

Dillard’s

American Eagle

Hollister

GOB SALES Consumers are reacting less favorably to GOB sales

Typical GOB markdown cadences are not capturing the consumers attention or share of their wallet

Thus deeper GOB discounts, earlier in the closing calendar, have become necessary to clear the product

Forever 21

Toys R Us

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

6.4% 5.6% 5.5%

4.3% 4.0% 3.4% 3.3%

2.8%

1.7% 1.3%

0.2%

-1.9% -2.4% -2.7%

-3.2% -3.7%

-6.3% -6.7%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

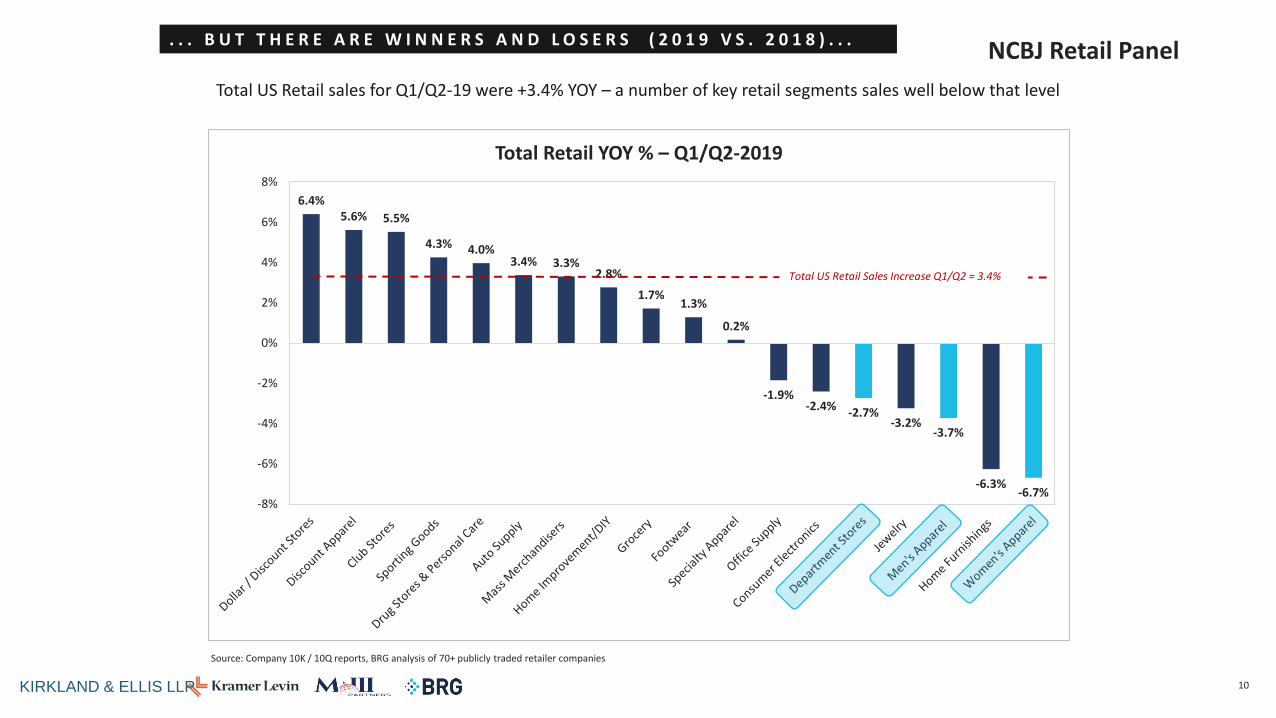

Total Retail YOY % – Q1/Q2-2019

Total US Retail sales for Q1/Q2-19 were +3.4% YOY – a number of key retail segments sales well below that level

10

. . . B U T T H E R E A R E W I N N E R S A N D L O S E R S ( 2 0 1 9 V S . 2 0 1 8 ) . . .

Total US Retail Sales Increase Q1/Q2 = 3.4%

Source: Company 10K / 10Q reports, BRG analysis of 70+ publicly traded retailer companies

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

Hardlines continue to outperfom in the retail sector while Softlines remain impacted most by e-commerce growth

11

. . . W I T H H A R D L I N E S v s S O F T L I N E S H I G H L I G H T I N G B I G D I F F E R E N C E S NCBJ Retail Panel

KIRKLAND & ELLIS LLP

Changing consumer habits have resulted in an emergence of e-commerce retailers, driving lackluster growth in traditional retail amid US retail bankruptcies and store closures

• Despite secular headwinds, Hardlines continue to be the strongest performing category in retail

‒ Furniture and home furnishings are currently in the strongest 3 month growth period the sector has seen since 2018, growing 1.1% YoY in September

‒ Building supplies continue to post strong growth numbers, growing 2.5% YoY in September

‒ Appliance and consumer electronics continue to struggle, declining 1.7% YoY in September

‒ Office supply trends continue to remain in a secular decline and have declined YoY in 87 of the last 90 months

• Softlines continue to be the weakest performing sector of retail, driven by store closings in the mall / brick-and-mortar retail space

‒ Over 8,000 US retail stores have closed in 2019, with ~75% of these being Softline retailers in malls

‒ Consumer behavior has shifted, driving major changes in purchasing habits, with luxury-good consignment shops and clothing rental providers becoming popular among “digital friendly” millennials

• E-commerce continues to take share from brick-and-mortar retailers

‒ E-commerce and mail-order retailers continue to post mid-teen growth YoY, largely driven by increased market share versus brick-and-mortar retailers

‒ September 2019 grew 15.6% YoY, extending the growth streak to 119 consecutive months

Source: KeyBanc Equity Research and other industry research

Total US Retail sales for Q1/Q2-19 were +3.4% YOY – a number of key retail segments sales well below that level

12

E - C O M M E R C E I S T A K I N G A L A R G E R S H A R E O F T O T A L R E T A I L . . . NCBJ Retail Panel

KIRKLAND & ELLIS LLP

YoY Quarterly Sales Growth

E-Commerce as a % of Total Retail Revenue

The retail landscape has changed drastically over the last several years – and the pressure on weak retailers continues to mount

13

B U T S T O R E C L O S U R E S D R I V I N G R E T A I L B A N K R U P T C I E S A N D . . .

Source: Coresight Research, https://coresight.com/research/ Source: The Deal, Chapter 7 and 11 filings, deal size $25M+

3,239 3,780 5,864

8,993

2,625

5,213

0

2,000

4,000

6,000

8,000

10,000

2018 Full Year 2019 YTD(as of 10/25/19)

Retailer Announced Store Openings & Closures Openings Closings Net Closings

Significant retail bankruptcies since 2016 2016 2017 2018 2019

19 23 23

35 30

21 24

0

10

20

30

40

2014 2015 2016 2017 2018 2019YTD

PriorYTD

Retail Bankruptcies Chapter 7 & 11, Deal Size $25M+

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

Retail bankruptcies continue apace in 2019.

14

. . . R E S U L T I N G I N L I A B I L I T I E S G R O W I N G B Y T H E B I L L I O N S NCBJ Retail Panel

KIRKLAND & ELLIS LLP

Source: Industry research 1) UBS 2) Reorg Research, as of October 24, 2019

Barneys

Retail bankruptcy activity has continued to be robust in 2019 as YTD aggregate liabilities for filing companies approach $5bn

Reorganizations within the retail industry have been focused on shifting to e-commerce business models that leverage a smaller go-forward store footprint

Over 8,000 retail stores have closed in 2019 and analysts expect another 75,000 could close by 2026(1)

Landlords have continued to be some of the most highly impacted unsecured creditors, especially within malls, as debtors seek to reject or renegotiate leases

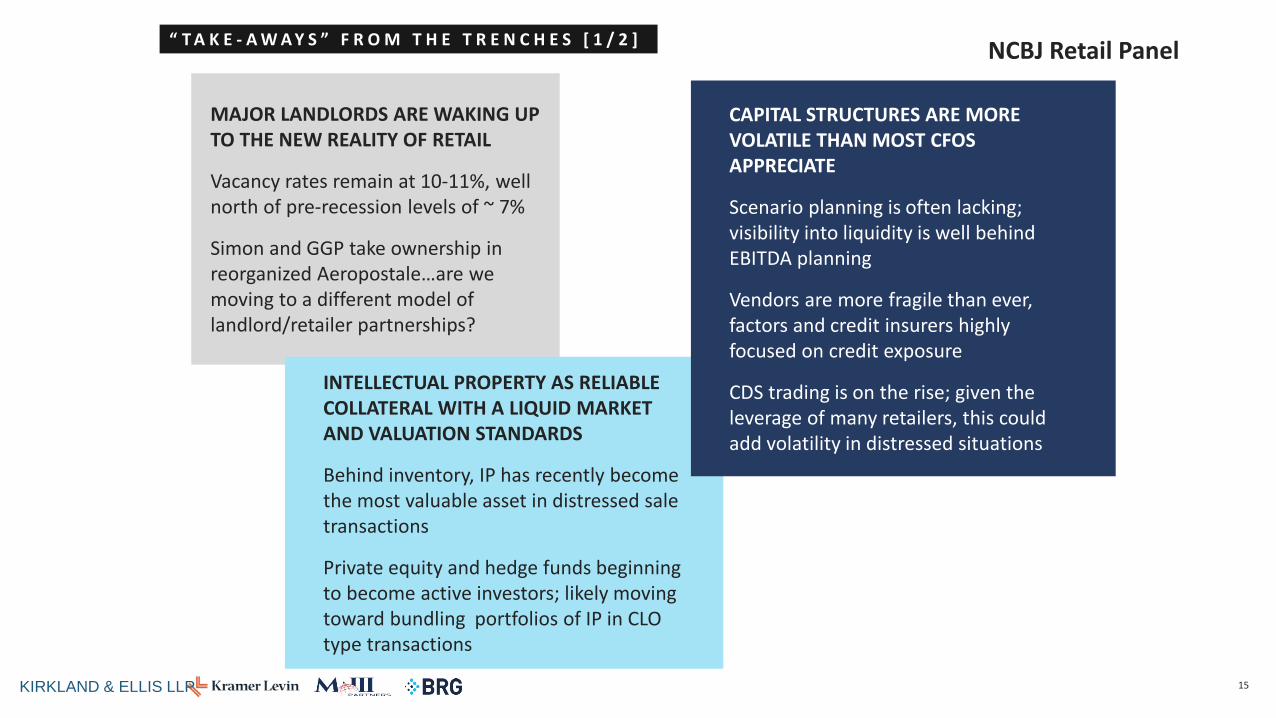

MAJOR LANDLORDS ARE WAKING UP TO THE NEW REALITY OF RETAIL

Vacancy rates remain at 10-11%, well north of pre-recession levels of ~ 7%

Simon and GGP take ownership in reorganized Aeropostale…are we moving to a different model of landlord/retailer partnerships?

INTELLECTUAL PROPERTY AS RELIABLE COLLATERAL WITH A LIQUID MARKET AND VALUATION STANDARDS

Behind inventory, IP has recently become the most valuable asset in distressed sale transactions

Private equity and hedge funds beginning to become active investors; likely moving toward bundling portfolios of IP in CLO type transactions

“ T A K E - A W A Y S ” F R O M T H E T R E N C H E S [ 1 / 2 ]

15

CAPITAL STRUCTURES ARE MORE VOLATILE THAN MOST CFOS APPRECIATE

Scenario planning is often lacking; visibility into liquidity is well behind EBITDA planning

Vendors are more fragile than ever, factors and credit insurers highly focused on credit exposure

CDS trading is on the rise; given the leverage of many retailers, this could add volatility in distressed situations

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

“ T A K E - A W A Y S ” F R O M T H E T R E N C H E S [ 2 / 2 ]

Store closures still outpace store openings and real estate owners face rent pressure

Retailers are focusing on private labels to offer value and differentiation

Sporting Goods appears to be near end of wave of distress

Continued disruption in specialty apparel, footwear and accessories

Areas of significant risk from amazon (see: auto parts and pharmacy)

CURRENT PROFILE OF DISTRESSED RETAIL…

Recovery on inventory sales is less predictable

Other collateral recoveries are speculative

A/P stretch prior to bankruptcy may create unintended surprises

MGMT/BODs/Counsel may be unpredictable from deal to deal and have competing priorities

…CREATES ELEVATED RISK FOR COMPANIES AND LENDERS…

Embrace the evolving consumer demographic

Prioritize the omni-channel challenge / initiatives

Create the right store experience

Do your own “internal restructuring”

Manage capital structure judiciously

...WHO MUST FOCUS ON BEST PRACTICE TO INCREASE

PROBABILITY OF SUCCESS.

16

NCBJ Retail Panel

KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Wholesale Model vs DTC Model

17 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Wholesale Model vs DTC Model

• It is commonly accepted that one of the contributing factors to the decline of the retail industry stems from the industry’s reliance on the wholesale model.

• Those retailers that have best weathered the most recent wave of retail bankruptcies are those that transitioned early to a business model that valued direct-sales strategies.

• The rise of the DTC model is attributable to: • consumers placing greater weight on their shopping experience; • retailers wanting to take advantage of the opportunity to build relationships with their

customers; • new technologies; and • the growth of the consumer data market.

18 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

IP and Distressed Retailers

19 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

IP in Retail Bankruptcies

• But the name lives on: IP / brand value is an increasingly popular alternative asset class in the retail space, but the acquisition of intellectual property in bankruptcy can pose unique opportunities and challenges.

• Patent, copyright subject to specific exceptions from broad assignment rights typically afforded under the Bankruptcy Code.

• Caselaw on trademark assignment was recently settled. See, e.g., Mission Prod. Holdings, Inc. v. Tempnology, LLC, No. 17-1657, 2019 WL 2166392 (U.S. May 20, 2019) (holding that that a licensor’s rejection of a trademark license in bankruptcy does not revoke or terminate the trademark license.)

• The Court ruled that a debtor-licensor’s rejection of a trademark license agreement does not in and of itself deprive a licensee of its right to use the trademark on a go-forward basis.

• Justice Sotomayor issued a concurring opinion to point out that (1) the baseline inquiry remains whether the licensee’s rights “would survive the licensor’s breach under applicable non-bankruptcy law,” and (2) trademark licensees’ post-rejection rights and remedies are in some respects broader than those of licensees of the types of intellectual property that fall under Section 365(n) of the Bankruptcy Code, upon whom certain duties are also imposed.

20 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

J. Crew

• As of December 2016, J. Crew’s capital structure included, among other things, $500 million of PIK debt issued by a “HoldCo” and approximately $1.2 billion of term loan debt (the “Term Loan”) issued or guaranteed by various subsidiaries.

• The Term Loan was secured by, among other things, various J. Crew trademarks. • In December 2016, J. Crew caused certain intellectual property to be contributed to a newly

formed and newly designated unrestricted, non-obligor subsidiary (“BrandCo”). • J. Crew argued such a transfer constituted a “Permitted Investment” and related party

investment provisions under its credit documents. • This transaction was allegedly undertaken as part of a refinancing of J. Crew’s HoldCo PIK debt, by

which • BrandCo or certain subsidiaries new debt secured by the transferred IP; and • new debt would be exchanged for HoldCo PIK (at a steep discount).

21 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

J. Crew (cont’d)

• In February 2017, J. Crew commenced a declaratory action seeking a determination that its transfer is proper.

• J. Crew’s Term Loan Agent has counterclaimed, alleging breach of the relevant credit documents and fraudulent conveyance (including actual fraud).

22 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

J. Crew (cont’d)

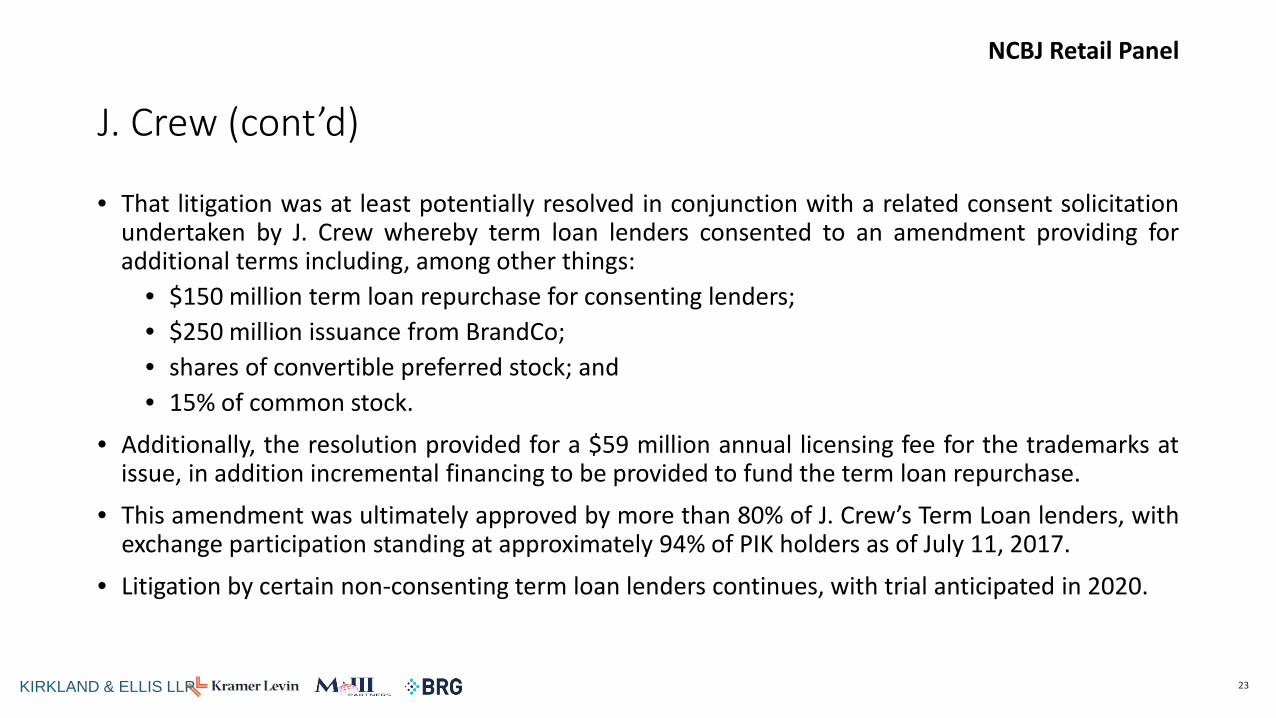

• That litigation was at least potentially resolved in conjunction with a related consent solicitation undertaken by J. Crew whereby term loan lenders consented to an amendment providing for additional terms including, among other things:

• $150 million term loan repurchase for consenting lenders; • $250 million issuance from BrandCo; • shares of convertible preferred stock; and • 15% of common stock.

• Additionally, the resolution provided for a $59 million annual licensing fee for the trademarks at issue, in addition incremental financing to be provided to fund the term loan repurchase.

• This amendment was ultimately approved by more than 80% of J. Crew’s Term Loan lenders, with exchange participation standing at approximately 94% of PIK holders as of July 11, 2017.

• Litigation by certain non-consenting term loan lenders continues, with trial anticipated in 2020.

23 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

How to Save a Distressed Retailer

24 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

How to Save a Distressed Retailer

• The (New) Standard Playbook: • Combination of falling comp store sales / fixed costs / shifting demographics trips covenant

or results in an unfavorable appraisal. • ABL lenders reduce exposure and require company to market itself. • Timing accelerated upon a “run on the bank” in trade terms. • If unsuccessful, chapter 11 filed with limited marketed window stapled to global “GOB”

process. • However, liquidation is not inevitable where prospective engagement can result in a going

concern process—even with a modified footprint.

25 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Leases and Landlords

26 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Leases and Landlords

• SOS: Save our stores. • Continued focus among labor, suppliers, real estate players and others (see, e.g., PBGC) on

preserving going concerns. • However, ability to negotiate / renegotiate concessions often has a limited clock. • Prospect for conflict with senior capital structure focused on minimizing risk.

• They aren’t making it anymore: Decreased emphasis on real estate values. • Increased skepticism on real estate footprint as value. • Lease auction now pro forma exercise. • Potential distress among commercial real estate players?

• “Double whammy” on declining rent rolls in a rising rate environment.

27 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Leases and Landlords

• A retailer’s lease portfolio should be reviewed on a location-by-location basis and defined as candidates for:

i. closure—e.g., stores with no reasonable prospect of profitability; ii. revised terms—e.g., unprofitable stores that could turn profitable; and iii. opportunistic enhancements—e.g., profitable stores that can leverage the ongoing

restructuring process. • Landlord outreach should occur in parallel with a retailer’s other restructuring initiatives.

• Where resources and/or runway are limited, the retailer should focus efforts on closures and revised terms.

• Consistent messaging is key. Sophisticated landlords will be coordinated and universally insist on “most favored nations” provisions no matter lip service to the contrary (i.e., on earning calls or otherwise).

28 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Leases and Landlords (cont’d)

• A retailer’s financial distress is a potential opportunity to extract concessions and can be utilized to incent landlords to improve terms rather than facing the downside case.

• In an out-of-court scenario, a retailer has several levers it can utilize when engaging landlords to improve terms or exit leases.

29 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Leases and Landlords (cont’d)

• Incentives a retailer may offer in exchange for concessions include: • Revenue Sharing. Landlords would be entitled to an agreed percentage of store revenues. Such

an arrangement may help align the retailer’s and the landlord’s incentives. • Debt or Equity. A retailer may decide to issue debt or equity to a supportive landlord. Such

non-cash consideration may help liquidity and defer payment obligations. • “Lease Trading”. Where a landlord is party to multiple leases—e.g., some profitable and some

unprofitable for the retailer—there may be an opportunity for the retailer to improve the lease terms governing the unprofitable locations by agreeing to concessions in lease terms at profitable locations.

• “Most Favored Nation” Protection. Provides landlords, particularly those willing to cut a deal early, with some backside assurances that they will not disproportionately fund a retailer’s lease rationalization efforts. Consent fees can still be used to incentivize early agreements.

• Joint Venture. One or more landlords may partner with other interested parties and form a joint venture to purchase certain of the retailer’s assets as in Aéropostale.

30 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Leases and Landlords (cont’d)

• On the other hand, a retailer can highlight certain downside contingencies to facilitate a negotiated outcome, including: • Vacate Premises. Empty spaces adversely impact landlords in relation to their other leased

space nearby. A retailer can highlight how vacating a store may be the least worst alternative available.

• Chapter 11. A retailer can reject unfavorable leases and limit / impair landlords’ recoveries inside of chapter 11. A credible threat of chapter 11 can be useful vis-à-vis landlords even without a court filing.

• Competition among Landlords. An auction-type process could be used to facilitate competition among landlords. E.g., the retailer may announce that it intends to continue operating 6 of 10 stores, and the landlords for those 10 stores would have an opportunity to “bid” confidentially to persuade the retailer to include such lease among the 6 stores.

• New Money Conditionality. Providers of new money may condition incremental investment on landlords also agreeing to a TBD amount of concessions. This conditionality would put pressure on landlords to provide such concessions or risk the consequences of the retailer losing access to new money.

31 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Aéropostale

• Mall-based retailer filed chapter 11 in May 2016 with $225 million of funded debt. At that time Aéropostale operated approx. 800 stores in the US.

• Filing driven by combination of factors, with Aéropostale also claiming that its largest supplier wrongly drove it into chapter 11 in a disguised “loan to own” scheme.

• Following unsuccessful litigation against its prepetition term lenders, who were affiliated with that large supplier, Aéropostale undertook an auction process in chapter 11, discussed below.

• In September 2016, a “Buyer Consortium” submitted winning bid valued at approximately $240 million.

• Consortium consisted of: Authentic Brands, GGP, Simon, Gordon Brothers, and Hilco. • Under its bid the Buyer Consortium agreed to take “up to” 229 U.S. store locations plus

Aéropostale’s e-commerce business. • Consortium reflected different roles/motivations, including liquidators (to dispose of close-

out locations), landlords, and an operator (Authentic Brands).

32 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Aéropostale (cont’d)

• In its initial stages, the Aéropostale bankruptcy also featured an aggressive ‘litigation-first’ strategy undertaken by the debtor.

• Following its May 2016 chapter 11 filing, Aéropostale commenced litigation seeking to (i) cap credit bid rights arising under a loan from its largest supplier a Fisker-like theory, (ii) equitably subordinate that term loan, and (iii) recharacterize a $50 million tranche of that loan.

• At core, Aéropostale’s theory was premised on the notion that the lender, who was also affiliated with one of its largest suppliers, exercised unreasonable control by contracting trade terms as part of a hidden ‘loan-to-own’ scheme.

• This theory was flatly rejected by the bankruptcy court. See In re Aéropostale, Inc., 555 B.R. 369 (Bankr. S.D.N.Y. 2016). Among other things, the court found:

• Aéropostale had in fact “systematically overstated its liquidity” pre-bankruptcy; • the supplier in question appropriately exercised its contractual discretion to contract trade

terms; and • allegations of a hidden ‘loan-to-own’ were “not credible.”

33 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Financing Retailers in Bankruptcy

34 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Retail Bankruptcy Cases – Key Considerations re: DIP Financings

• From a creditor/investor perspective, it is essential from the outset of the case and in conjunction with the DIP financing to focus on certain key provisions of DIP orders, including provisions regarding surcharges under Section 506(c), Section 552(b) and marshalling.

• DIP lenders often negotiate for waivers by the Debtors and their estates of all rights to surcharge collateral under Section 506(c), the ability to assert the “equities of the case” exception of Section 552(b), or the application of marshalling.

• The Committee and/or other unsecured creditors must therefore focus on negotiating modifications to preserve these rights.

• Such protections (and carveouts to the Debtors’ waivers) become potentially critical for Chapter 11 retail cases at risk of becoming administratively insolvent.

• These rights therefore may be particularly appropriate to seek to preserve in retail cases. • Postpetition trade vendors provide the inventory upon which the lender asserts its lien, and

landlords enable the inventory to be sold in their stores (and thereby generates the proceeds subject to the lien).

35 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Section 506(c) – Surcharge of Collateral

• In general, the expenses related to administering a Debtor’s estate are not chargeable to the secured creditor’s collateral, but are paid from the unencumbered assets of the estate.

• Section 506(c) of the Bankruptcy Code, however, provides an exception permitting the surcharge of collateral in certain circumstances, provided the expenses at issue:

• (i) are “necessary” to preserve or dispose of the collateral, • (ii) are “reasonable,” and • (iii) provided a “benefit” to the secured creditor.

36 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Section 552(b) – Equities of the Case

• The general rule is that postpetition property is not subject to a pre-petition lien. • However, Section 552(b) provides for certain exceptions to this general rule, namely that

a prepetition lien continues to be valid with respect to postpetition proceeds, products, offspring, or profits from the pre-petition collateral.

• But, these exceptions are subject to a further exception: • Specifically, the validity of a security interest in postpetition proceeds, products, offspring or

profits of prepetition collateral under section 552(b)(1) can be limited or eliminated by the court “based on the equities of the case.”

37 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Equitable Doctrine of Marshalling

• The common law right to marshalling can be utilized to protect junior creditors by requiring a secured creditor with recourse to multiple pieces of collateral to recover first from one source, in an attempt to avoid or limit the harm to junior creditors with access to fewer sources of collateral.

• Thus, the doctrine of marshalling seeks to satisfy the claims of both creditors in a more equitable manner.

• For example, if the lender has a prepetition lien against inventory and obtains a postpetition lien against previously unencumbered real estate, marshalling could require the lender to look to the inventory first to allow for the opportunity of junior (including unsecured) creditors to benefit from the value of the real estate if the lender is repaid from the inventory.

• If marshaling is waived, however, secured lenders are free to collect on any collateral to satisfy their secured claims (even if previously unencumbered).

• To the extent marshalling is not waived, there is often a negotiated resolution for how it would apply or the manner in which remedies can be exercised by the lenders.

38 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Key Considerations re: DIP Financings (Toys R Us Example)

• In Toys “R” Us, the Debtors obtained over $3 billion of DIP financing comprised of three parts. Among other things, the DIP financing provided liens on previously unencumbered assets in favor of the DIP lenders and prepetition secured lenders.

• Although the original DIP orders in Toys “R” Us contemplated complete waivers of estate rights under section 506(c), 552(b) and the equitable doctrine of marshalling, the Committee obtained the right to assert certain section 506(c) and 552(b) claims for unpaid administrative claims of trade vendors and landlords.

• Essentially, section 506(c) and 552(b) rights could be asserted to the extent that the aggregate net exposure of trade vendors and landlords was adversely impacted during the bankruptcy (as measured by the outstanding administrative exposure of such creditors after taking into account the benefit to such creditors from receiving critical vendor or foreign vendor payments for their prepetition claims); see language on following slide.

• The Committee also obtained concessions from the secured lenders that they would proceed first against certain collateral.

• After the wind-down of Toys’ domestic operations was announced in March 2018, these surcharge-related modifications and marshalling provisions, among other things, helped to pave a path towards a global settlement with the lenders, among others.

39 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Key Considerations re: DIP Financings (Toys R Us Example)

Toys R Us – Excerpts from North American DIP Order (Dkt. 711 at ¶¶ 13(d), 14)

“Notwithstanding the foregoing, this paragraph shall not operate to waive the right of the Creditors’ Committee (and only the Creditors’ Committee) (on behalf of the Debtors), in the event of an administrative insolvency of the Debtors but in all events only after the ABL/FILO DIP Obligations shall have been indefeasibly paid in full in cash and all related Commitments have been terminated, to seek to charge against or recover from the remaining Collateral (including Cash Collateral) pursuant to section 506(c) of the Bankruptcy Code in an amount equal to, as of any date, the positive difference, if any, of (a) the outstanding administrative expense claims of trade vendors and landlords as of such date, including without limitation in respect of payables in respect of goods and unpaid post-Petition Date amounts due under real property leases but not including fees and expenses of Professional Persons, less (b) the aggregate amount of payments made by the Debtors following the Petition Date and through such date in respect of pre-petition unsecured claims (including section 503(b)(9) and other applicable priority claims) of trade vendors and landlords, including without limitation pursuant to “Critical Vendor,” “Foreign Vendors” and similar orders (the “Net Unsecured Claimant Increase”) (provided nothing contained in this Final Order shall be deemed to be a consent by the DIP Agent, the DIP Lenders or the Prepetition Secured Parties to any charge, lien, assessment or claim against the Collateral pursuant to this sentence under section 506(c) of the Bankruptcy Code or otherwise); provided for the avoidance of doubt that the Creditors’ Committee (and only the Creditors’ Committee) shall have standing to assert such arguments.”

“In no event, whether in a liquidation, under a plan of reorganization or otherwise, shall the Senior DIP Parties or the Prepetition Secured Parties be subject to the doctrine of “marshaling” or any similar doctrine with respect to the Collateral; provided that (i) the Term DIP Lenders will seek to collect the Term DIP Obligations, first, from the ABL/FILO DIP Collateral and the proceeds thereof that are not used to satisfy the ABL/FILO DIP Obligations or other obligations (including Contingent Prepetition ABL/FILO Debt) with senior liens on such Collateral and that are not otherwise made available to the Debtors for administrative expenses, including, if applicable, liquidation expenses following an event of default with respect to the Term DIP Financing, and second, from other Collateral that is not property of the estate of Wayne (the “Non-Wayne Term Loan Collateral”), and only after the ABL/FILO DIP Collateral (following provision for senior liens, including with respect to the ABL/FILO DIP obligations, and administrative expenses, as set forth above) and Non-Wayne Term Loan Collateral have been substantially exhausted will the Term DIP Lenders seek to collect the Term DIP Obligations from their other Collateral; (ii) that the property of Wayne’s estate shall not be distributed to any other stakeholders of Wayne or otherwise unless and until the DIP Term Lenders are repaid in full, and (iii) solely to the extent reasonably practicable without any material delay in the payment in full of the ABL/FILO DIP Obligations, such obligations shall be satisfied first from Collateral (other than Collateral of Wayne) other than Avoidance Proceeds and only after such other Collateral (other than Collateral of Wayne) shall have been exhausted, from Avoidance Proceeds. The agreements set forth in this paragraph regarding application of ABL/FILO DIP Collateral and Non-Wayne Term Loan Collateral shall not apply to the adequate protection liens and claims of the Prepetition Term Loan Lenders, however solely to the extent reasonably practicable without material delay in the payment in full of any Adequate Protection Obligations, such obligations shall be satisfied first from Collateral (other than Collateral of Wayne) other than Avoidance Proceeds.”

40 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Section 503(b)(9) – Goods Received Within 20 Days of Petition • The Bankruptcy Code provides administrative priority for the value of goods sold and delivered to

the Debtor within the 20 days prior to the bankruptcy filing. • Given that sufficient inventory is critical for retailers, the volume of goods delivered within

the 20 days prior to bankruptcy can be substantial. • The 2005 amendments provided this newly-created administrative priority claim to vendors,

which has become of critical importance in retail bankruptcy cases. • Section 503(b)(9) provides for allowed administrative expenses for “the value of any goods

received by the debtor within 20 days before the date of commencement of a case under this title in which the goods have been sold to the debtor in the ordinary course of such debtor’s business.”

41 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Section 503(b)(9) (cont’d) • To qualify for an administrative claim under section 503(b)(9), the supplier must demonstrate,

among other things: • that it sold “goods” to the debtor (services provided not covered)

• If both goods and services are provided, some courts determine the value of the goods themselves and exclude services; other courts apply “predominant purpose test” to see if vendor was predominantly providing services or goods (see, e.g., Circuit City)

• such goods were “received by the debtor” within 20 days prior to the bankruptcy filing. • Often disputes about when goods “received”, particularly with overseas supply chain. • Drop-shipments (delivered directly to third-party, and thus not “received” by the Debtor)

have been denied 503(b)(9) status.

• Section 503(b)(9) does not specify time when payment must be made; courts generally find claimants not entitled to immediate payment, and payments can be made in connection with Effective Date.

42 KIRKLAND & ELLIS LLP

NCBJ Retail Panel

Critical Vendors

• Retail trade creditors are in the unique position of providing postpetition financing, in the form of goods or services that enable the retailer to operate in bankruptcy, often on an unsecured basis.

• Since retailers’ business is premised on selling merchandise to their customers, a steady and timely supply of goods from the retailer’s suppliers and vendors is critical.

• If the retailer cannot induce its primary suppliers to continue to deliver merchandise and products following the petition date, there would likely be a substantial negative impact on operations.

• Thus, in an effort to induce potentially reluctant key vendors to continue to supply goods and services, debtors have requested court authority to pay all or a portion of certain prepetition claims of “critical vendors” in exchange for the vendor’s commitment to sell goods on credit terms to the debtor during the bankruptcy case.

• To be a “critical vendor,” a creditor must supply a good or service which would be difficult for the debtor to obtain elsewhere.

• Postpetition creditors in retail cases carefully assess whether to extend credit – even with the incentive of critical vendor dollars.

43 KIRKLAND & ELLIS LLP