Embed Size (px)

Citation preview

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 1/106

Edelweiss Securities LimitedManoj Bahety, CFA+91 22 6623 [email protected]

Manav Vijay+91 22 4063 [email protected]

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 2/106

Executive Summary

Demand-supply economics favourable in India

World Travel & Tourism Council (WTTC) expects travel and tourism (T&T) demand in

India to grow at 8.2% annually till 2019, the highest growth after China in the bigcountries league. Owing to various supply bottlenecks, the 13% CAGR growth till FY12E

in demand of premium category rooms is expected to outpace the 10% CAGR growth in

supply; HVS estimates ongoing construction work on only 60% of the 1,00,000

announced rooms. Demand is expected to remain robust as the Indian economy gathers

pace and with many sporting events lined up in the next 12-18 months.

ARRs to rise and ORs to stay firm till FY12

Owing to the increasing demand across many categories/locations, we expect occupancy

rates (ORs) to firm up to 65% and further to 70% in FY11E and FY12E, respectively.

After a difficult H1FY10, when average room rates (ARRs) declined as much as 35-40%

in many locations, marked improvement witnessed by hotel companies in Q3FY10 instills

confidence to estimate an increase of 10% each in FY11E and FY12E. By 2012, we

estimate addition of 9,000-10,000 rooms in the five star and above category. We expect

above 85% of the incremental capacity to be utilised due to better demand.

International hotel chains eye Indian hospitality

According to WTTC, India’s T&T market is expected to grow more than 100% by 2018 to

USD 61 bn against USD 28 bn in 2008. To tap this opportunity, ~25 major international

hotel companies like Accor, Marriott, Claridges, Shangri-la, and Carlson Hospitality are

looking to enter India, either independently or in collaboration with a local party. Also,

GoI’s conscious efforts towards promoting India as a leading leisure destination are likely

to increase the country’s share in the foreign tourist arrivals (FTAs).

Outlook: Good long-term opportunity

Considering that the US offers 40x and China 10x hotel rooms as compared to the

110,000 hotel rooms in India, the Indian hospitality industry has huge potential to grow

structurally. However, high land prices, low FSI, plethora of taxes, and low incentive

from government are some key hurdles for hotel companies in India.

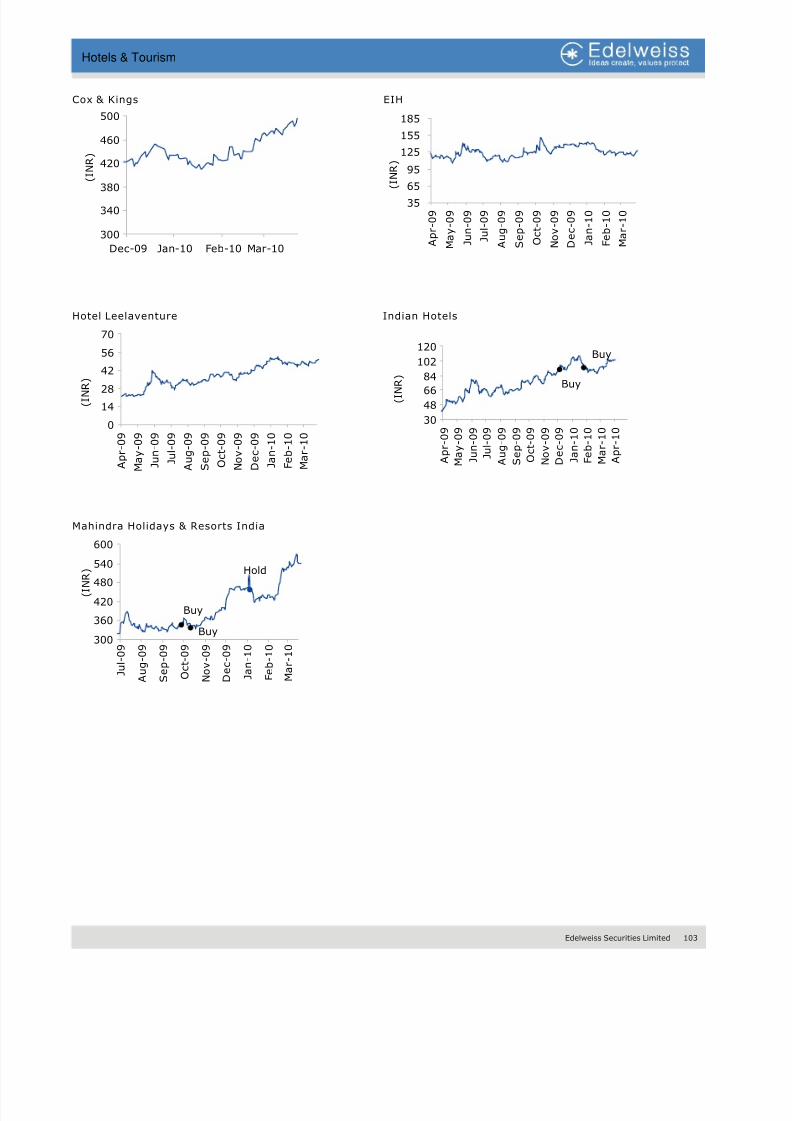

In this report, we have discussed listed hospitality companies. We initiate coverage on

Cox & Kings and EIH with ‘HOLD’ recommendations, and on Hotel Leela with ‘REDUCE’

recommendation. Also featured in this report are Indian Hotels (BUY), Mahindra

Holidays & Resorts India (REDUCE), Asian Hotels (NOT RATED), and TAJ GVK (NOT

RATED).

Edelweiss Research is also available on www.edelresearch.com, Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset. Edelweiss Securities Limited

Hotels & Tourism

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 3/106

2 Edelweiss Securities Limited

Hotels & Tourism

Contents

At a glance ................................................................................................................. 3

Indian Travel & Tourism Industry: Overview ................................................................... 4

Demand-Supply Economics Favourable .......................................................................... 5

Improving ARRs and ORs during 2010-12..................................................................... 20

Global Player’s Indian Venture .................................................................................... 22

Vacation Ownership ................................................................................................... 23

Global Travel & Tourism ............................................................................................. 26

Key Trends ............................................................................................................... 28

Business Analysis ...................................................................................................... 30

Valuation Methodology ............................................................................................... 33

Key Risks ................................................................................................................. 35

Challenges ............................................................................................................... 36

Annexure I ............................................................................................................... 37

Annexure II .............................................................................................................. 38

Annexure III ............................................................................................................. 39

Companies

Cox & Kings ............................................................................................................ 41

EIH .......................................................................................................................... 53

Hotel Leelaventure .................................................................................................... 67

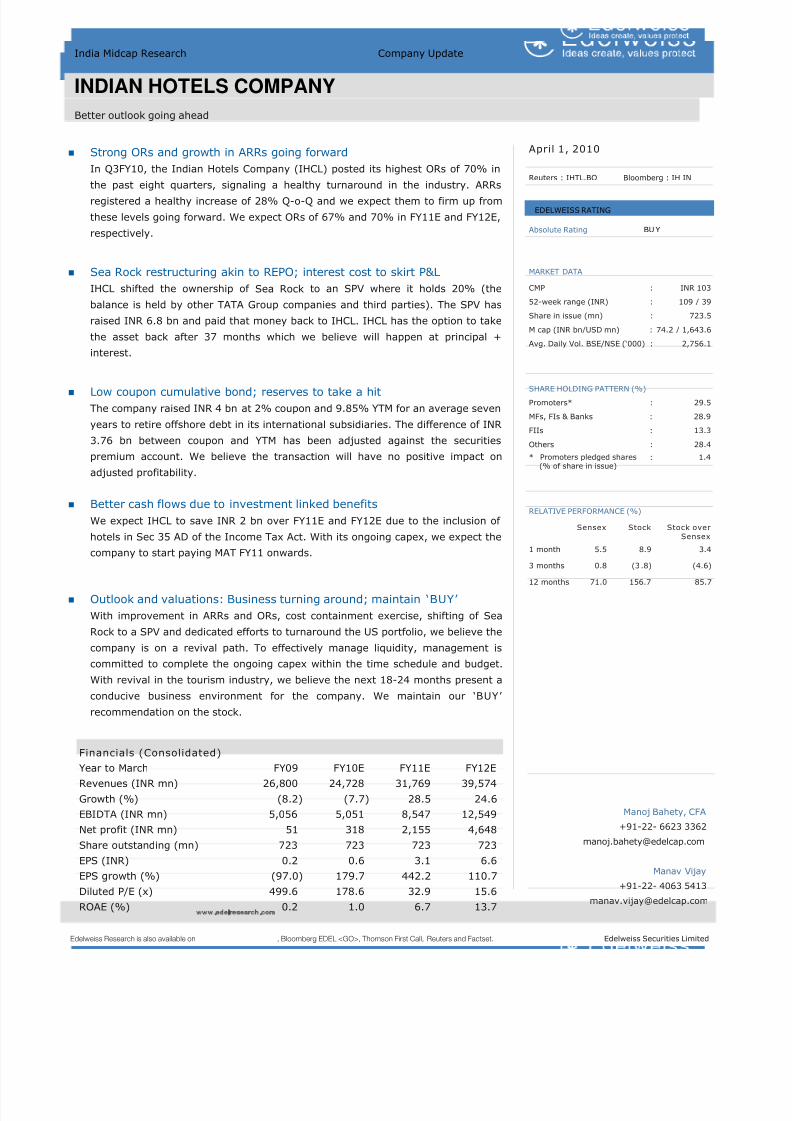

Indian Hotels Company .............................................................................................. 81

Mahindra Holidays & Resorts India............................................................................... 87

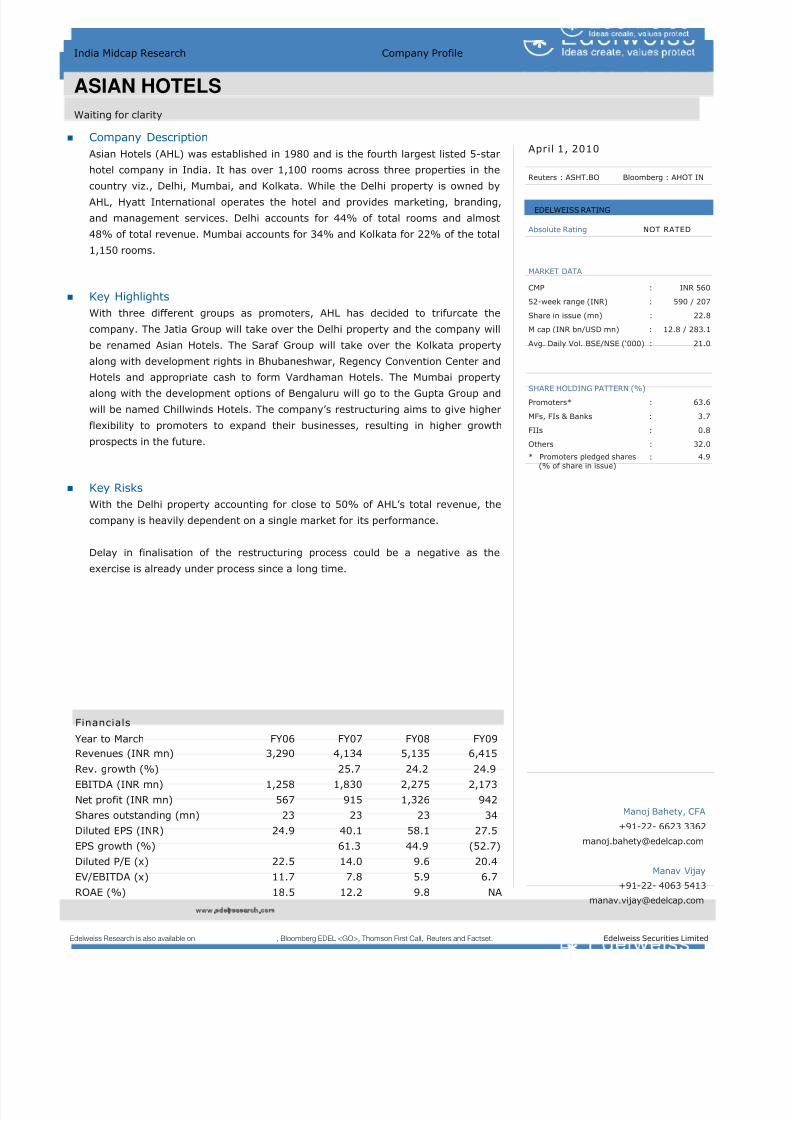

Asian Hotels ............................................................................................................. 95

Taj GVK Hotels & Resorts ........................................................................................... 99

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 4/106

Edelweiss Securities Limited 3

Hotels & Tourism

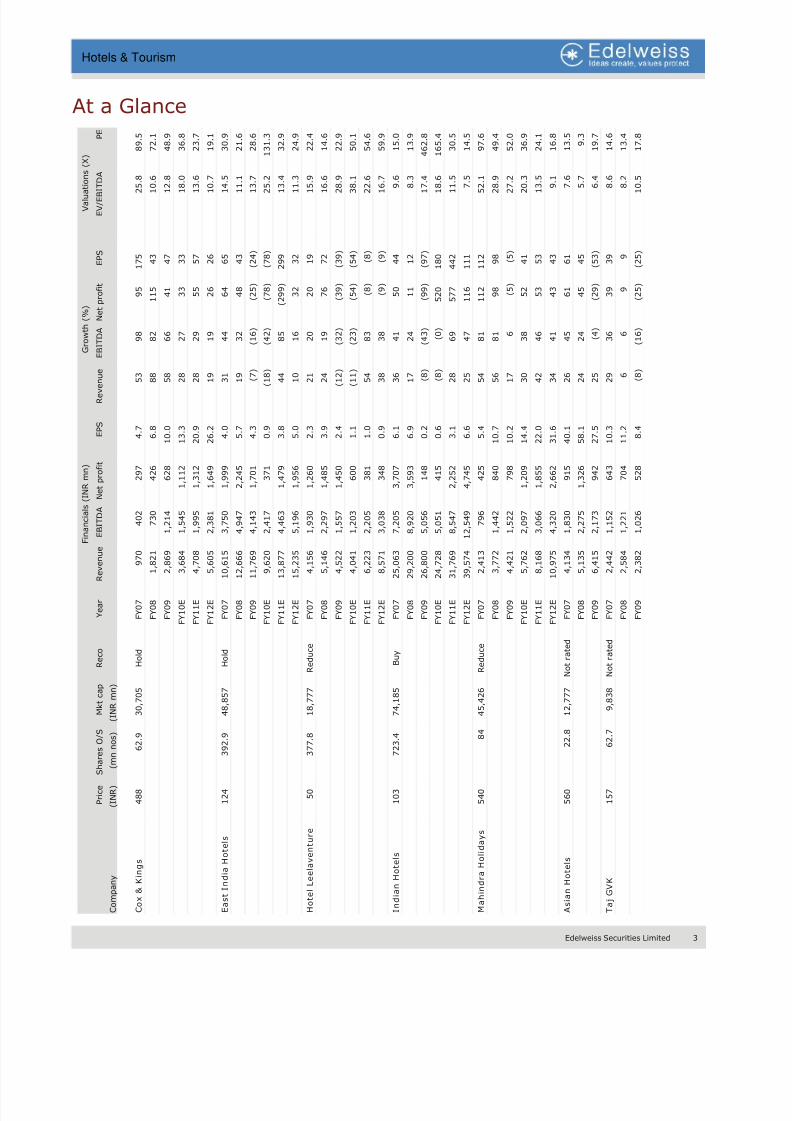

At a Glance

P r i c e

S h a r e

s O / S

M k t c a p

R e c o

Y e a r

R e v e

n u e

E B I T D A

N e t p r o f i t

E P S

R e v e n u

e

E B I T D A

N e t p r o f i t

E P S

E V / E B I T D A

P E

C o m p a n y

( I N R )

( m n

n o s )

( I N R m n )

C o x

& K i n g s

4 8 8

6 2 . 9

3 0 , 7

0 5

H o l d

F Y 0 7

9

7 0

4 0 2

2 9 7

4 . 7

5 3

9 8

9 5

1 7 5

2 5 . 8

8 9 . 5

F Y 0 8

1 , 8

2 1

7 3 0

4 2 6

6 . 8

8 8

8 2

1 1 5

4 3

1 0 . 6

7 2 . 1

F Y 0 9

2 , 8

6 9

1 , 2

1 4

6 2 8

1 0 . 0

5 8

6 6

4 1

4 7

1 2 . 8

4 8 . 9

F Y 1 0 E

3 , 6

8 4

1 , 5

4 5

1 , 1

1 2

1 3 . 3

2 8

2 7

3 3

3 3

1 8 . 0

3 6 . 8

F Y 1 1 E

4 , 7

0 8

1 , 9

9 5

1 , 3

1 2

2 0 . 9

2 8

2 9

5 5

5 7

1 3 . 6

2 3 . 7

F Y 1 2 E

5 , 6

0 5

2 , 3

8 1

1 , 6

4 9

2 6 . 2

1 9

1 9

2 6

2 6

1 0 . 7

1 9 . 1

E a s t I n d i a

H o t e l s

1 2 4

3

9 2 . 9

4 8 , 8

5 7

H o l d

F Y 0 7

1 0 , 6

1 5

3 , 7

5 0

1 , 9

9 9

4 . 0

3 1

4 4

6 4

6 5

1 4 . 5

3 0 . 9

F Y 0 8

1 2 , 6

6 6

4 , 9

4 7

2 , 2

4 5

5 . 7

1 9

3 2

4 8

4 3

1 1 . 1

2 1 . 6

F Y 0 9

1 1 , 7

6 9

4 , 1

4 3

1 , 7

0 1

4 . 3

( 7

)

( 1 6 )

( 2 5 )

( 2 4 )

1 3 . 7

2 8 . 6

F Y 1 0 E

9 , 6

2 0

2 , 4

1 7

3 7 1

0 . 9

( 1 8

)

( 4 2 )

( 7 8 )

( 7 8 )

2 5 . 2

1 3 1 . 3

F Y 1 1 E

1 3 , 8

7 7

4 , 4

6 3

1 , 4

7 9

3 . 8

4 4

8 5

( 2 9 9 )

2 9 9

1 3 . 4

3 2 . 9

F Y 1 2 E

1 5 , 2

3 5

5 , 1

9 6

1 , 9

5 6

5 . 0

1 0

1 6

3 2

3 2

1 1 . 3

2 4 . 9

H o t e l L e e l a v e n t u r e

5 0

3

7 7 . 8

1 8 , 7

7 7

R e d u c e

F Y 0 7

4 , 1

5 6

1 , 9

3 0

1 , 2

6 0

2 . 3

2 1

2 0

2 0

1 9

1 5 . 9

2 2 . 4

F Y 0 8

5 , 1

4 6

2 , 2

9 7

1 , 4

8 5

3 . 9

2 4

1 9

7 6

7 2

1 6 . 6

1 4 . 6

F Y 0 9

4 , 5

2 2

1 , 5

5 7

1 , 4

5 0

2 . 4

( 1 2

)

( 3 2 )

( 3 9 )

( 3 9 )

2 8 . 9

2 2 . 9

F Y 1 0 E

4 , 0

4 1

1 , 2

0 3

6 0 0

1 . 1

( 1 1

)

( 2 3 )

( 5 4 )

( 5 4 )

3 8 . 1

5 0 . 1

F Y 1 1 E

6 , 2

2 3

2 , 2

0 5

3 8 1

1 . 0

5 4

8 3

( 8 )

( 8 )

2 2 . 6

5 4 . 6

F Y 1 2 E

8 , 5

7 1

3 , 0

3 8

3 4 8

0 . 9

3 8

3 8

( 9 )

( 9 )

1 6 . 7

5 9 . 9

I n d i a n

H o t e l s

1 0 3

7

2 3 . 4

7 4 , 1

8 5

B u y

F Y 0 7

2 5 , 0

6 3

7 , 2

0 5

3 , 7

0 7

6 . 1

3 6

4 1

5 0

4 4

9 . 6

1 5 . 0

F Y 0 8

2 9 , 2

0 0

8 , 9

2 0

3 , 5

9 3

6 . 9

1 7

2 4

1 1

1 2

8 . 3

1 3 . 9

F Y 0 9

2 6 , 8

0 0

5 , 0

5 6

1 4 8

0 . 2

( 8

)

( 4 3 )

( 9 9 )

( 9 7 )

1 7 . 4

4 6 2 . 8

F Y 1 0 E

2 4 , 7

2 8

5 , 0

5 1

4 1 5

0 . 6

( 8

)

( 0 )

5 2 0

1 8 0

1 8 . 6

1 6 5 . 4

F Y 1 1 E

3 1 , 7

6 9

8 , 5

4 7

2 , 2

5 2

3 . 1

2 8

6 9

5 7 7

4 4 2

1 1 . 5

3 0 . 5

F Y 1 2 E

3 9 , 5

7 4

1 2 , 5

4 9

4 , 7

4 5

6 . 6

2 5

4 7

1 1 6

1 1 1

7 . 5

1 4 . 5

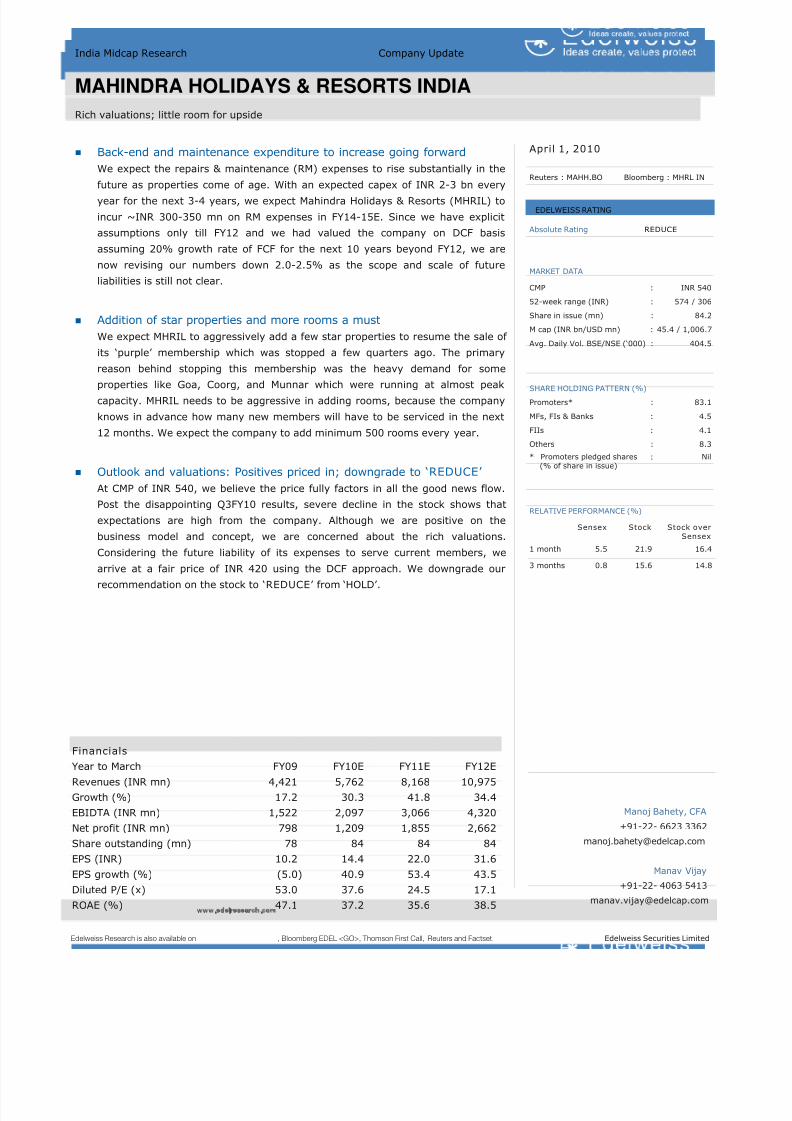

M a h i n d r a

H o l i d a y s

5 4 0

8 4

4 5 , 4

2 6

R e d u c e

F Y 0 7

2 , 4

1 3

7 9 6

4 2 5

5 . 4

5 4

8 1

1 1 2

1 1 2

5 2 . 1

9 7 . 6

F Y 0 8

3 , 7

7 2

1 , 4

4 2

8 4 0

1 0 . 7

5 6

8 1

9 8

9 8

2 8 . 9

4 9 . 4

F Y 0 9

4 , 4

2 1

1 , 5

2 2

7 9 8

1 0 . 2

1 7

6

( 5 )

( 5 )

2 7 . 2

5 2 . 0

F Y 1 0 E

5 , 7

6 2

2 , 0

9 7

1 , 2

0 9

1 4 . 4

3 0

3 8

5 2

4 1

2 0 . 3

3 6 . 9

F Y 1 1 E

8 , 1

6 8

3 , 0

6 6

1 , 8

5 5

2 2 . 0

4 2

4 6

5 3

5 3

1 3 . 5

2 4 . 1

F Y 1 2 E

1 0 , 9

7 5

4 , 3

2 0

2 , 6

6 2

3 1 . 6

3 4

4 1

4 3

4 3

9 . 1

1 6 . 8

A s i a n

H o t e l s

5 6 0

2 2 . 8

1 2 , 7

7 7

N o t r a t e d

F Y 0 7

4 , 1

3 4

1 , 8

3 0

9 1 5

4 0 . 1

2 6

4 5

6 1

6 1

7 . 6

1 3 . 5

F Y 0 8

5 , 1

3 5

2 , 2

7 5

1 , 3

2 6

5 8 . 1

2 4

2 4

4 5

4 5

5 . 7

9 . 3

F Y 0 9

6 , 4

1 5

2 , 1

7 3

9 4 2

2 7 . 5

2 5

( 4 )

( 2 9 )

( 5 3 )

6 . 4

1 9 . 7

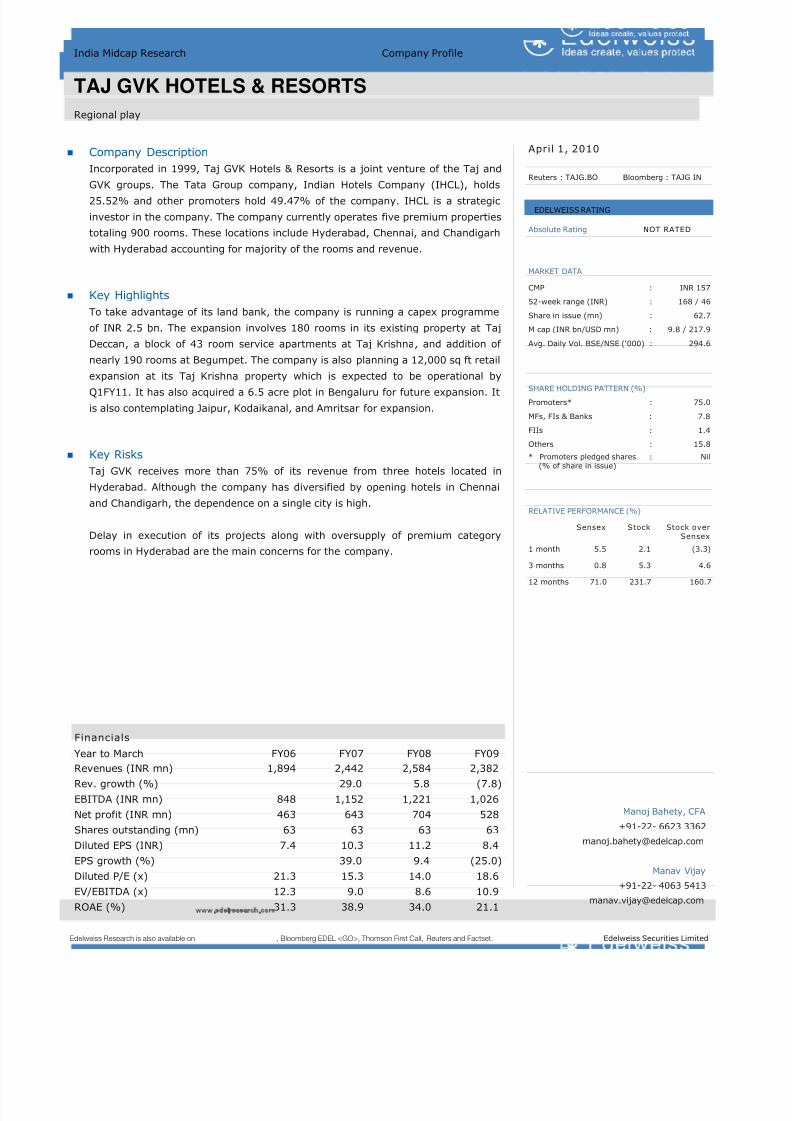

T a j G V K

1 5 7

6 2 . 7

9 , 8

3 8

N o t r a t e d

F Y 0 7

2 , 4

4 2

1 , 1

5 2

6 4 3

1 0 . 3

2 9

3 6

3 9

3 9

8 . 6

1 4 . 6

F Y 0 8

2 , 5

8 4

1 , 2

2 1

7 0 4

1 1 . 2

6

6

9

9

8 . 2

1 3 . 4

F Y 0 9

2 , 3

8 2

1 , 0

2 6

5 2 8

8 . 4

( 8

)

( 1 6 )

( 2 5 )

( 2 5 )

1 0 . 5

1 7 . 8

F i n a n c i a l s ( I N R m n )

G r o w t h ( % )

V a l u a t i o n s ( X )

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 5/106

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 6/106

Edelweiss Securities Limited 5

Hotels & Tourism

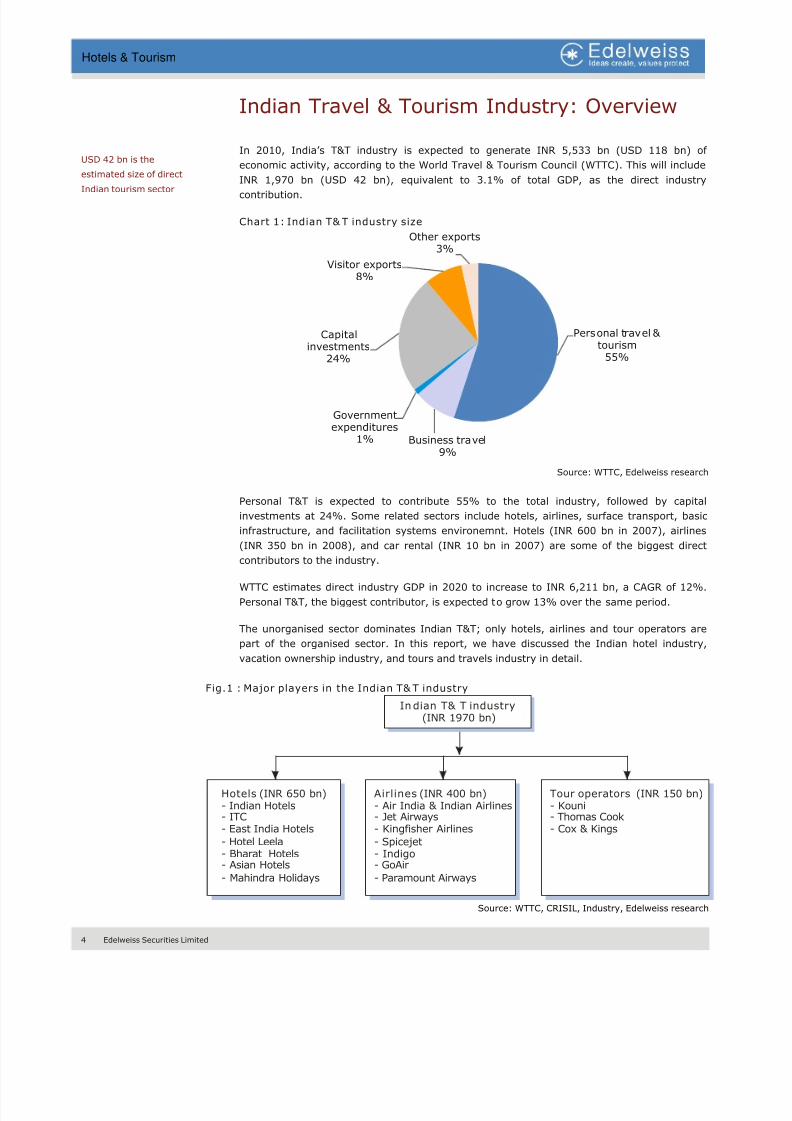

Demand-Supply Economics Favourable

Tourism demand on the rise in India

Till 2019, WTTC estimates India’s T&T demand to post 8.2% CAGR, one of the highest in

the world. The Ministry of Tourism (MoT) aims to achieve 10 mn (versus 5.1 mn in 2009)

foreign tourist arrivals (FTAs) and 675 mn (versus 563 mn in 2008) domestic tourists in

2010. Provisional estimates of December 2009 for FTA is 0.65 mn, the highest in the

past three years, guides to above 6 mn FTAs in 2010. We estimate India’s contribution to

the worldwide T&T growth to rise to 1.9% in 2018 (1.27% in 2009) when global T&T is

projected to grow at 4% according to WTCC. Continuous tourist growth in India is

attributable to factors like media campaigns ‘Incredible India’ organised by GoI, high

level of service standards in the country and great regional diversity. Foreign exchange

earning from T&T has posted 13% CAGR in 1996-2008. Robust GDP growth will aid the

business and leisure travel, implying a positive outlook for the Indian hospitality

industry. Recent jump in ORs across major cities, followed by increased ARRs, gives us

confidence that the industry is set for a major business upturn.

Chart 2: Rise in FTAs to aid growth in organised hospitality

(8.0)

0.0

8.0

16.0

24.0

32.0

0

240

480

720

960

1200

1 9 9 9 - 0 0

2 0 0 0 - 0 1

2 0 0 1 - 0 2

2 0 0 2 - 0 3

2 0 0 3 - 0 4

2 0 0 4 - 0 5

2 0 0 5 - 0 6

2 0 0 6 - 0 7

2 0 0 7 - 0 8

2 0 0 8 - 0 9

2 0 0 9 - 1 0 E

2 0 1 0 - 1 1 E

2 0 1 1 - 1 2 E

( % )

R e v e n u e ( I N R b n )

Hospitality sector size FTAs growth

Source: CRISIL, Ministry of Tourism, Edelweiss research

Within T&T, the hotels segment is likely to grow the fastest. With an expected 10% jump

in ARRs in FY11 and FY12, we expect the share of hotel industry to increase to 22% in

FY12 against 19% in FY09. Limited supply of rooms, along with healthy demand, is

expected to help hotels to post better performance. Healthy growth in both international

and domestic tourists, along with India’s emergence as one of the fastest economies, is

likely to drive its business tourist traffic substantially.

Indian tourism set for

major growth

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 7/106

6 Edelweiss Securities Limited

Hotels & Tourism

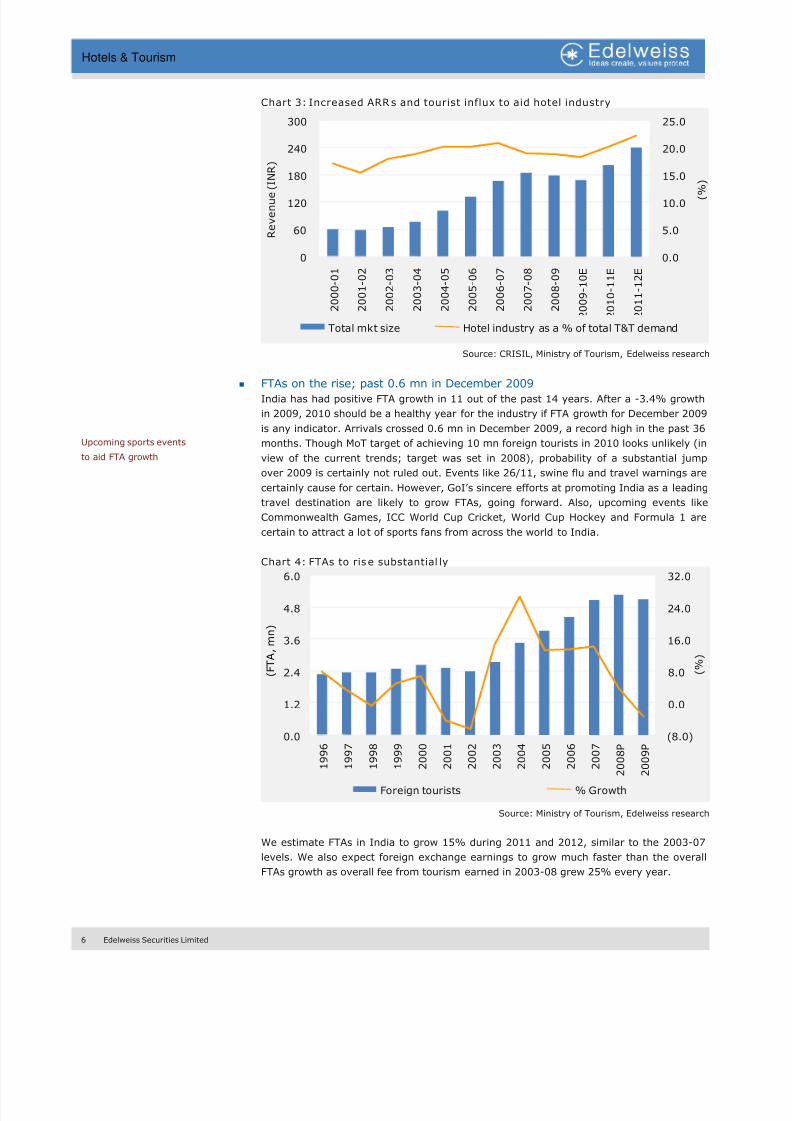

Chart 3: Increased ARRs and tourist influx to aid hotel industry

0.0

5.0

10.0

15.0

20.0

25.0

0

60

120

180

240

300

2 0 0 0 - 0 1

2 0 0 1 - 0 2

2 0 0 2 - 0 3

2 0 0 3 - 0 4

2 0 0 4 - 0 5

2 0 0 5 - 0 6

2 0 0 6 - 0 7

2 0 0 7 - 0 8

2 0 0 8 - 0 9

2 0 0 9 - 1 0 E

2 0 1 0 - 1 1 E

2 0 1 1 - 1 2 E

( %

)

R e v e n u e (

I N R )

Total mkt size Hotel industry as a % of total T&T demand

Source: CRISIL, Ministry of Tourism, Edelweiss research

FTAs on the rise; past 0.6 mn in December 2009

India has had positive FTA growth in 11 out of the past 14 years. After a -3.4% growth

in 2009, 2010 should be a healthy year for the industry if FTA growth for December 2009

is any indicator. Arrivals crossed 0.6 mn in December 2009, a record high in the past 36

months. Though MoT target of achieving 10 mn foreign tourists in 2010 looks unlikely (in

view of the current trends; target was set in 2008), probability of a substantial jump

over 2009 is certainly not ruled out. Events like 26/11, swine flu and travel warnings are

certainly cause for certain. However, GoI’s sincere efforts at promoting India as a leading

travel destination are likely to grow FTAs, going forward. Also, upcoming events like

Commonwealth Games, ICC World Cup Cricket, World Cup Hockey and Formula 1 are

certain to attract a lot of sports fans from across the world to India.

Chart 4: FTAs to rise substantial ly

(8.0)

0.0

8.0

16.0

24.0

32.0

0.0

1.2

2.4

3.6

4.8

6.0

1 9 9

6

1 9 9

7

1 9 9

8

1 9 9

9

2 0 0

0

2 0 0

1

2 0 0

2

2 0 0

3

2 0 0

4

2 0 0

5

2 0 0

6

2 0 0

7

2 0 0 8

P

2 0 0 9

P

( % )

( F T A , m n )

Foreign tourists % Growth

Source: Ministry of Tourism, Edelweiss research

We estimate FTAs in India to grow 15% during 2011 and 2012, similar to the 2003-07

levels. We also expect foreign exchange earnings to grow much faster than the overall

FTAs growth as overall fee from tourism earned in 2003-08 grew 25% every year.

Upcoming sports events

to aid FTA growth

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 8/106

Edelweiss Securities Limited 7

Hotels & Tourism

Moreover, what has helped improve India’s image on the world tourism map is its

improving infrastructure that has connected the remotest of the places within the

country. Further, low-cost airlines, highway development and better power situation

have buoyed India’s tourism prospects.

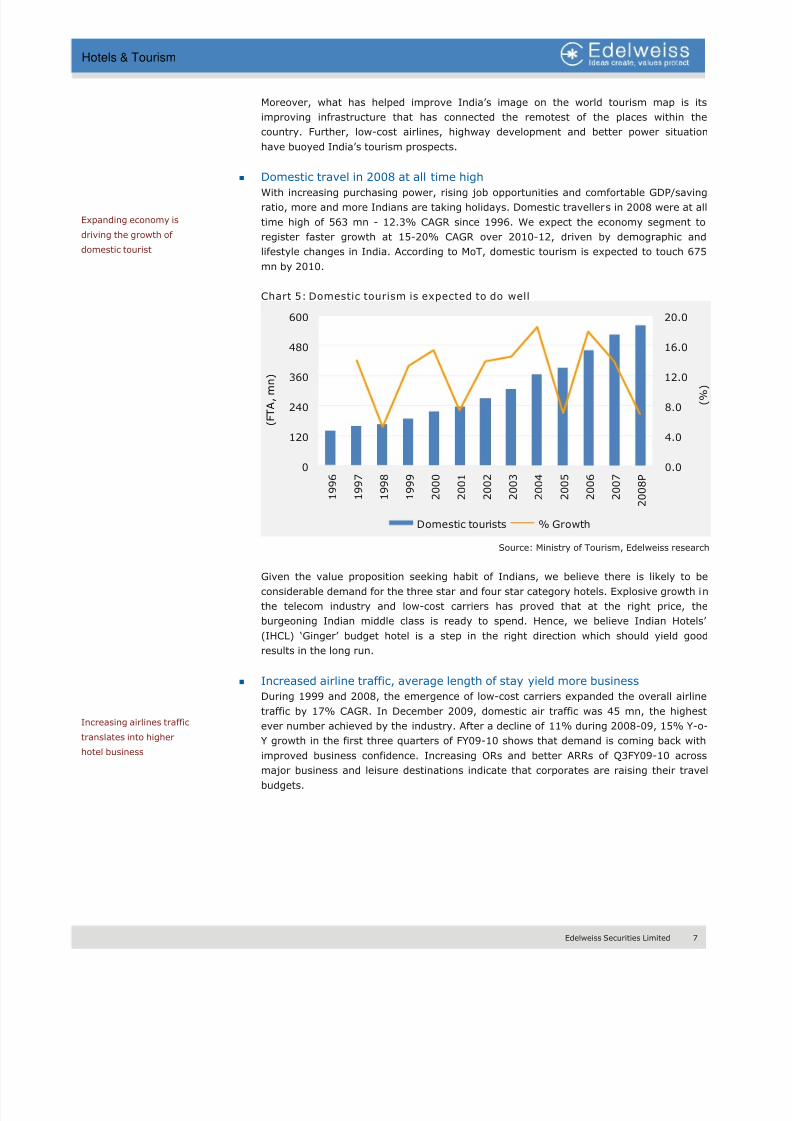

Domestic travel in 2008 at all time high

With increasing purchasing power, rising job opportunities and comfortable GDP/saving

ratio, more and more Indians are taking holidays. Domestic travellers in 2008 were at all

time high of 563 mn - 12.3% CAGR since 1996. We expect the economy segment to

register faster growth at 15-20% CAGR over 2010-12, driven by demographic and

lifestyle changes in India. According to MoT, domestic tourism is expected to touch 675

mn by 2010.

Chart 5: Domestic tourism is expected to do well

0.0

4.0

8.0

12.0

16.0

20.0

0

120

240

360

480

600

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8 P

( % )

( F T A , m n )

Domestic tourists % Growth

Source: Ministry of Tourism, Edelweiss research

Given the value proposition seeking habit of Indians, we believe there is likely to be

considerable demand for the three star and four star category hotels. Explosive growth in

the telecom industry and low-cost carriers has proved that at the right price, the

burgeoning Indian middle class is ready to spend. Hence, we believe Indian Hotels’

(IHCL) ‘Ginger’ budget hotel is a step in the right direction which should yield good

results in the long run.

Increased airline traffic, average length of stay yield more business

During 1999 and 2008, the emergence of low-cost carriers expanded the overall airline

traffic by 17% CAGR. In December 2009, domestic air traffic was 45 mn, the highest

ever number achieved by the industry. After a decline of 11% during 2008-09, 15% Y-o-

Y growth in the first three quarters of FY09-10 shows that demand is coming back with

improved business confidence. Increasing ORs and better ARRs of Q3FY09-10 acrossmajor business and leisure destinations indicate that corporates are raising their travel

budgets.

Expanding economy is

driving the growth of

domestic tourist

Increasing airlines traffic

translates into higher

hotel business

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 9/106

8 Edelweiss Securities Limited

Hotels & Tourism

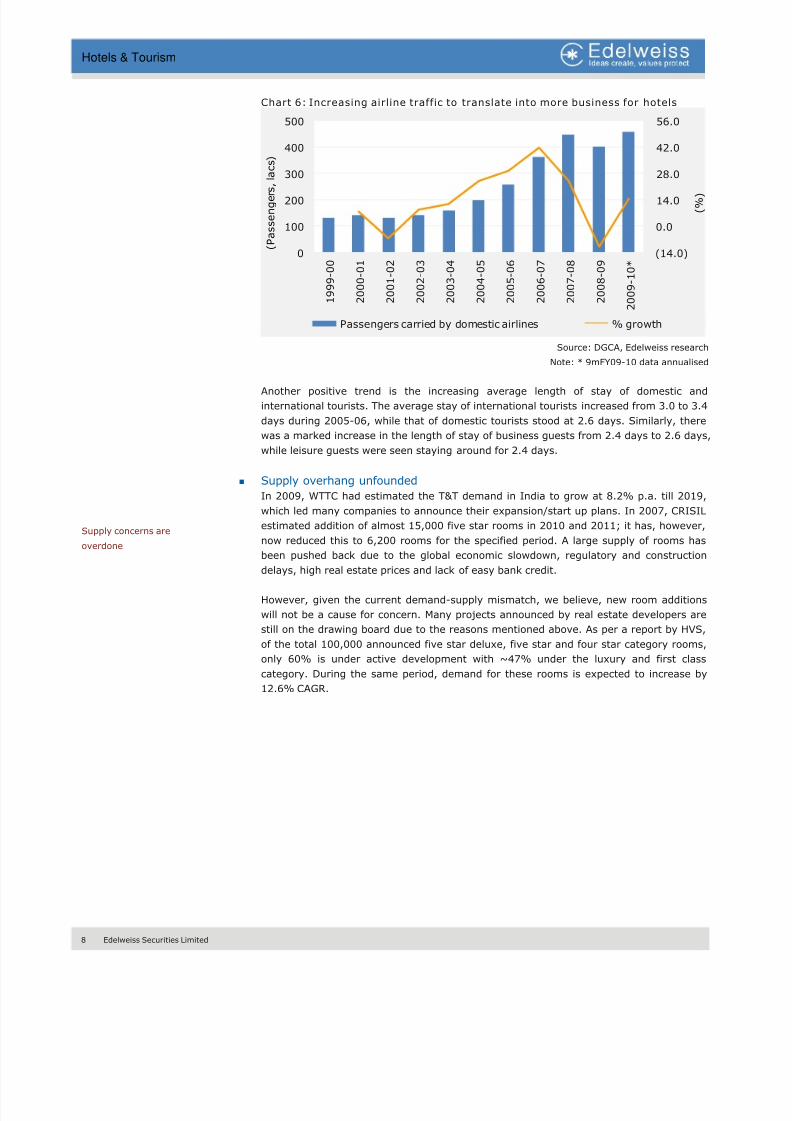

Chart 6: Increasing airline traffic to translate into more business for hotels

(14.0)

0.0

14.0

28.0

42.0

56.0

0

100

200

300

400

500

1 9 9 9 - 0 0

2 0 0 0 - 0 1

2 0 0 1 - 0 2

2 0 0 2 - 0 3

2 0 0 3 - 0 4

2 0 0 4 - 0 5

2 0 0 5 - 0 6

2 0 0 6 - 0 7

2 0 0 7 - 0 8

2 0 0 8 - 0 9

2 0 0 9 - 1 0 *

( % )

( P a s s e n g e r s , l a c s )

Passengers carried by domestic airlines % growth

Source: DGCA, Edelweiss research

Note: * 9mFY09-10 data annualised

Another positive trend is the increasing average length of stay of domestic and

international tourists. The average stay of international tourists increased from 3.0 to 3.4

days during 2005-06, while that of domestic tourists stood at 2.6 days. Similarly, there

was a marked increase in the length of stay of business guests from 2.4 days to 2.6 days,

while leisure guests were seen staying around for 2.4 days.

Supply overhang unfounded

In 2009, WTTC had estimated the T&T demand in India to grow at 8.2% p.a. till 2019,

which led many companies to announce their expansion/start up plans. In 2007, CRISIL

estimated addition of almost 15,000 five star rooms in 2010 and 2011; it has, however,

now reduced this to 6,200 rooms for the specified period. A large supply of rooms has

been pushed back due to the global economic slowdown, regulatory and construction

delays, high real estate prices and lack of easy bank credit.

However, given the current demand-supply mismatch, we believe, new room additions

will not be a cause for concern. Many projects announced by real estate developers are

still on the drawing board due to the reasons mentioned above. As per a report by HVS,

of the total 100,000 announced five star deluxe, five star and four star category rooms,

only 60% is under active development with ~47% under the luxury and first class

category. During the same period, demand for these rooms is expected to increase by

12.6% CAGR.

Supply concerns are

overdone

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 10/106

Edelweiss Securities Limited 9

Hotels & Tourism

Table 1: Distribution of existing and proposed branded hotels by major cities

Existing

supply

Proposed

supply

Increase

over five

years (%)

Active

development of

supply (%)

Luxury

(%)

First

class (%)

Mid-

market

(%)

Budget

(%)

Extended

stay (%)

Agra 1,419 400 28.2 75.0 25.0 - 75.0 - -

Ahmedabad 800 3,058 382.3 71.0 8.2 39 35.2 10.3 7.2 Bengaluru 3,889 10,784 277.3 58.0 23.8 29 16.0 22.7 8.4

Chandigarh 351 1,459 415.7 55.0 11.3 34 25.1 29.2 -

Chennai 3,307 4,945 149.5 67.0 36.7 32 12.4 11.8 7.0

Delhi (NCR) 8,625 16,560 192.0 53.0 18.2 30 33.7 16.3 1.5

Goa 2,795 2,178 77.9 31.0 14.0 42 30.8 13.4 -

Hyderabad 2,761 5,884 213.1 73.0 42.1 21 17.8 19.1 -

Jaipur 1,683 3,357 199.5 53.0 16.1 27 40.5 16.1 -

Kolkata 1,373 4,025 293.2 62.0 24.2 28 36.3 11.1 -

Mumbai 7,948 13,386 168.4 73.0 29.9 26 24.8 15.2 4.4

Pune 1,518 8,054 530.6 52.0 22.3 29 29.6 19.2 -

Other cities 12,006 20,025 166.8 60.0 2.5 21 48.0 28.1 0.6

Total 48,475 94,115 194.2 60.0 20.2 27 31.2 19.0 2.9

Proposed supply

Source: HVS, Edelweiss research

Mumbai (9,771 rooms), Delhi (8,776 rooms) and Bengaluru (6,254 rooms) are expected

to witness the largest absolute addition, whereas Pune (276%), Ahmadabad (271%) and

Chandigarh (229%) could see the largest increase in percentage terms. CRISIL expects

addition of ~32,000 rooms in the next five years.

Limited supply of premium category rooms during FY04-08 had led to ~50% rise in ARRs

during the period. ORs also improved during the period to ~70% from 63%. For business

hotels, occupancies in excess of 70% are considered to be above normal as only five

business days are used for calculations.

Of the expected addition of almost 10,000 five star hotel rooms in FY10-12, more than

85% is likely to get filled which will push ORs to 65% in FY11E and 70% in FY12E. ORs

of more than 70% witnessed by the hotel industry during FY05-08 is indicative of an

even better number for the next few years as business activity in India is rising.

Chart 7: Increased demand w ith limited supply to push ORs higher till FY12E

0.0

16.0

32.0

48.0

64.0

80.0

0

9,000

18,000

27,000

36,000

45,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( %

)

( R o o

m s )

Room availability Room demand ORs

Source: CRISIL, Edelweiss research

Mumbai, Delhi and

Bengaluru to witness the

largest addition of rooms

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 11/106

10 Edelweiss Securities Limited

Hotels & Tourism

Supply scenario in major markets

NCR: Commonwealth Games and ICC Cricket World Cup key triggers

To serve the anticipated demand of hotel rooms due to the upcoming Commonwealth

Games in October 2010 and ICC World Cup in Q4FY11, during FY10-11, supply in the

premium category is expected to rise 20% in the National Capital Region (NCR); we

expect the existing room count to rise 60%, from 7,000 to ~11,000 rooms in the nextfive years. Including four star rooms, we expect total addition of 7000-8000 rooms in the

period.

We expect ORs to remain strong at 75% in FY11E and decline to 70% in FY12E post the

Commonwealth Games. In our view, considering the supply of hotels in FY11E and FY12E,

we believe the new supply post FY12E to come down for a while as the market will take

time to expand.

Chart 8: Strong ORs till FY12E – Limited supply and robust demand

0.0

20.0

40.0

60.0

80.0

100.0

0

2,000

4,000

6,000

8,000

10,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( R o o m s )

Supply Demand ORs

Source: CRISIL, Edelweiss research

ARRs, after rising at 22% CAGR during FY04-09, are expected to fall 15% in FY10.

Considering the expected demand, we anticipate a conservative 15% increase in ARRs

during FY11 and FY12, though we believe the actual rise could be much higher.

Chart 9: Strong ARRs till FY 12

0.0

20.0

40.0

60.0

80.0

100.0

0

2,800

5,600

8,400

11,200

14,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( %

)

( I N R )

ARRs RevPAR ORs

Source: CRISIL, Edelweiss research

Upcoming international

sports events to hold the

demand high

ARRs to remain firm in

anticipation of high

demand

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 12/106

Edelweiss Securities Limited 11

Hotels & Tourism

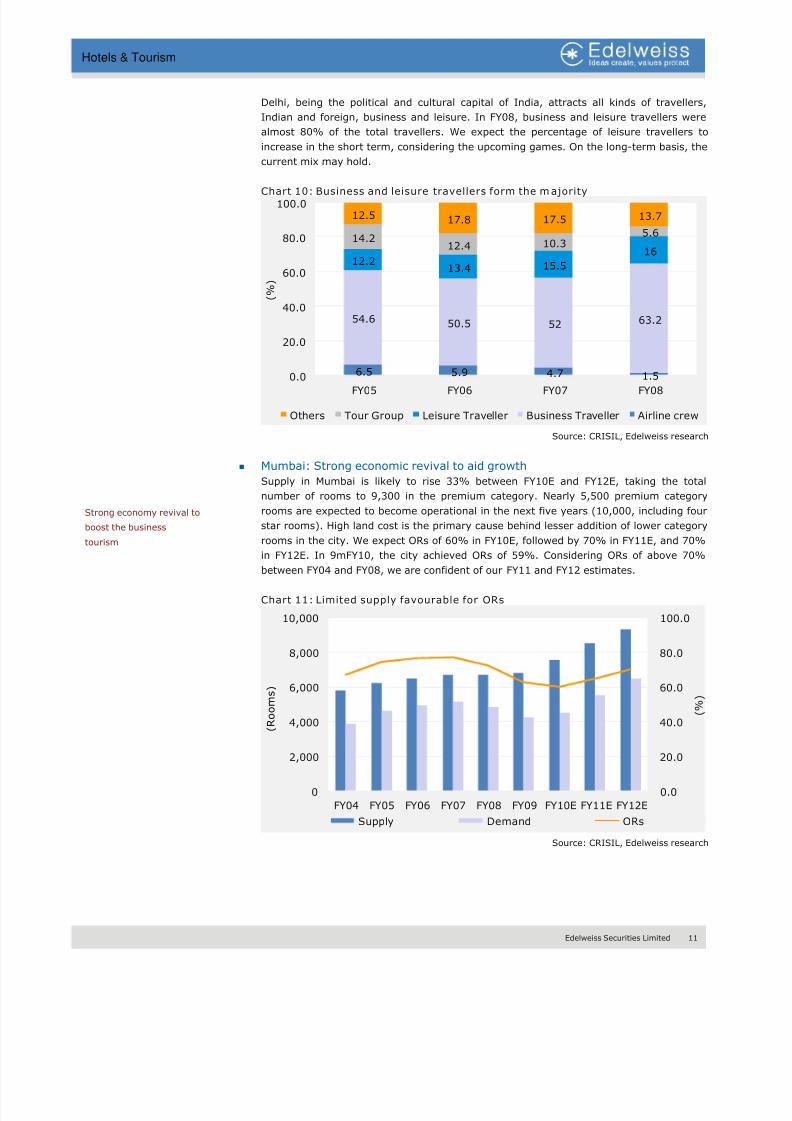

Delhi, being the political and cultural capital of India, attracts all kinds of travellers,

Indian and foreign, business and leisure. In FY08, business and leisure travellers were

almost 80% of the total travellers. We expect the percentage of leisure travellers to

increase in the short term, considering the upcoming games. On the long-term basis, the

current mix may hold.

Chart 10: Business and leisure travellers form the majority

6.5 5.9 4.7 1.5

54.6 50.5 52 63.2

12.213.4 15.5

16

14.212.4 10.3

5.6

12.5 17.8 17.5 13.7

0.0

20.0

40.0

60.0

80.0

100.0

FY05 FY06 FY07 FY08

( % )

Others Tour Group Leisure Traveller Business Traveller Airline crew

Source: CRISIL, Edelweiss research

Mumbai: Strong economic revival to aid growth

Supply in Mumbai is likely to rise 33% between FY10E and FY12E, taking the total

number of rooms to 9,300 in the premium category. Nearly 5,500 premium category

rooms are expected to become operational in the next five years (10,000, including four

star rooms). High land cost is the primary cause behind lesser addition of lower category

rooms in the city. We expect ORs of 60% in FY10E, followed by 70% in FY11E, and 70%

in FY12E. In 9mFY10, the city achieved ORs of 59%. Considering ORs of above 70%

between FY04 and FY08, we are confident of our FY11 and FY12 estimates.

Chart 11: Limited supply favourable for ORs

0.0

20.0

40.0

60.0

80.0

100.0

0

2,000

4,000

6,000

8,000

10,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( R o o m s )

Supply Demand ORs

Source: CRISIL, Edelweiss research

Strong economy revival to

boost the business

tourism

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 13/106

12 Edelweiss Securities Limited

Hotels & Tourism

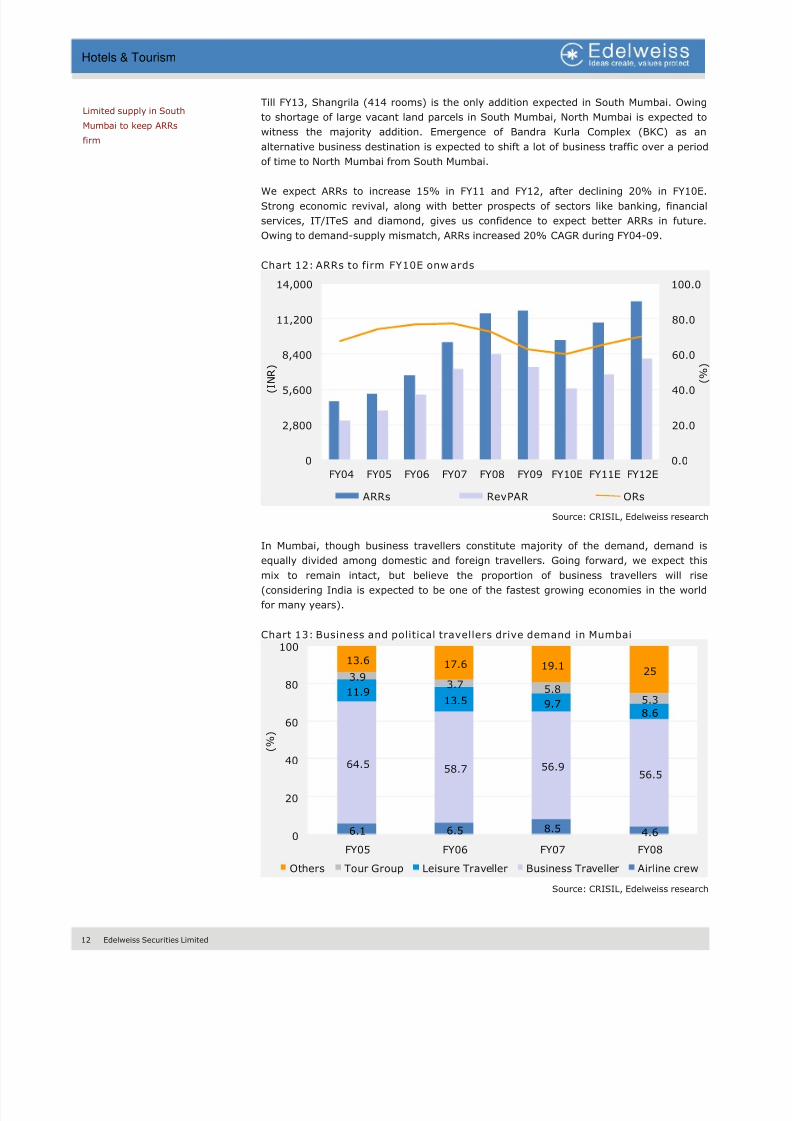

Till FY13, Shangrila (414 rooms) is the only addition expected in South Mumbai. Owing

to shortage of large vacant land parcels in South Mumbai, North Mumbai is expected to

witness the majority addition. Emergence of Bandra Kurla Complex (BKC) as an

alternative business destination is expected to shift a lot of business traffic over a period

of time to North Mumbai from South Mumbai.

We expect ARRs to increase 15% in FY11 and FY12, after declining 20% in FY10E.

Strong economic revival, along with better prospects of sectors like banking, financial

services, IT/ITeS and diamond, gives us confidence to expect better ARRs in future.

Owing to demand-supply mismatch, ARRs increased 20% CAGR during FY04-09.

Chart 12: ARRs to firm FY10E onw ards

0.0

20.0

40.0

60.0

80.0

100.0

0

2,800

5,600

8,400

11,200

14,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( %

)

( I N R )

ARRs RevPAR ORs

Source: CRISIL, Edelweiss research

In Mumbai, though business travellers constitute majority of the demand, demand is

equally divided among domestic and foreign travellers. Going forward, we expect thismix to remain intact, but believe the proportion of business travellers will rise

(considering India is expected to be one of the fastest growing economies in the world

for many years).

Chart 13: Business and political travellers drive demand in Mumbai

6.1 6.5 8.5 4.6

64.5 58.7 56.956.5

11.913.5 9.7

8.6

3.93.7 5.8

5.3

13.6 17.6 19.125

0

20

40

60

80

100

FY05 FY06 FY07 FY08

( % )

Others Tour Group Leisure Traveller Business Traveller Airline crew

Source: CRISIL, Edelweiss research

Limited supply in South

Mumbai to keep ARRs

firm

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 14/106

Edelweiss Securities Limited 13

Hotels & Tourism

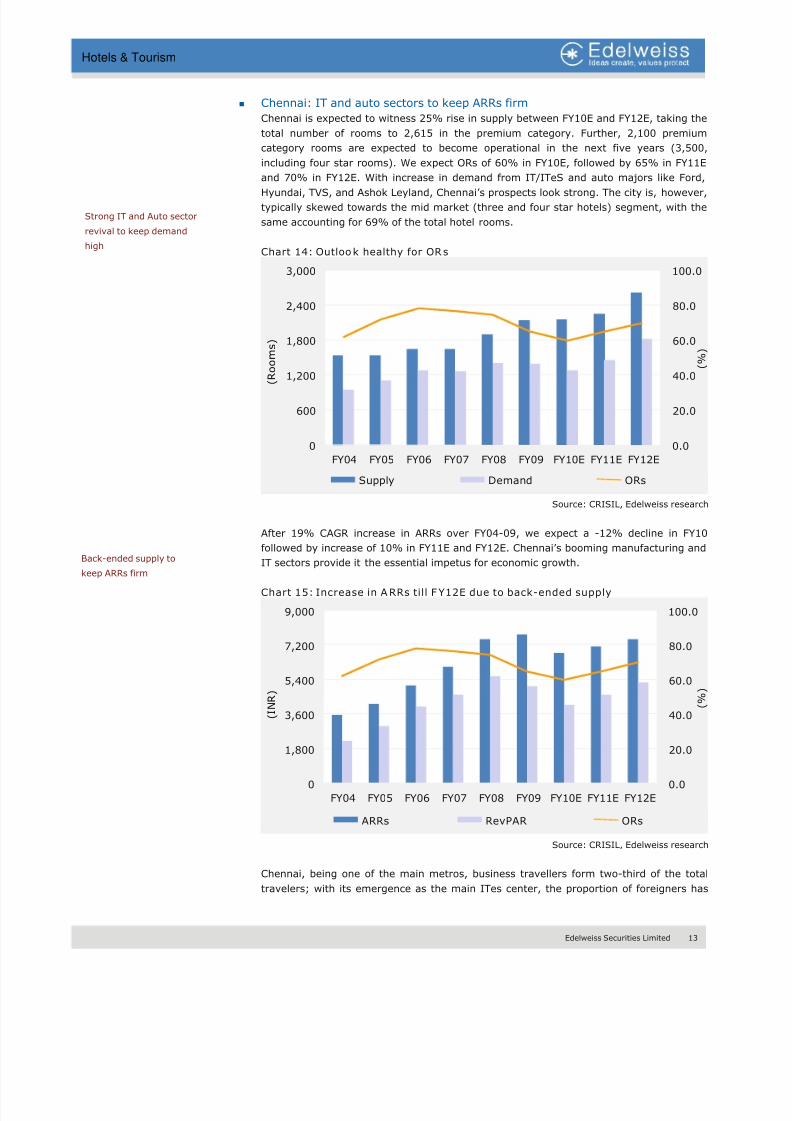

Chennai: IT and auto sectors to keep ARRs firm

Chennai is expected to witness 25% rise in supply between FY10E and FY12E, taking the

total number of rooms to 2,615 in the premium category. Further, 2,100 premium

category rooms are expected to become operational in the next five years (3,500,

including four star rooms). We expect ORs of 60% in FY10E, followed by 65% in FY11E

and 70% in FY12E. With increase in demand from IT/ITeS and auto majors like Ford,

Hyundai, TVS, and Ashok Leyland, Chennai’s prospects look strong. The city is, however,

typically skewed towards the mid market (three and four star hotels) segment, with the

same accounting for 69% of the total hotel rooms.

Chart 14: Outlook healthy for ORs

0.0

20.0

40.0

60.0

80.0

100.0

0

600

1,200

1,800

2,400

3,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( R

o o m s )

Supply Demand ORs

Source: CRISIL, Edelweiss research

After 19% CAGR increase in ARRs over FY04-09, we expect a -12% decline in FY10

followed by increase of 10% in FY11E and FY12E. Chennai’s booming manufacturing and

IT sectors provide it the essential impetus for economic growth.

Chart 15: Increase in ARRs till F Y12E due to back-ended supply

0.0

20.0

40.0

60.0

80.0

100.0

0

1,800

3,600

5,400

7,200

9,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( I N R )

ARRs RevPAR ORs

Source: CRISIL, Edelweiss research

Chennai, being one of the main metros, business travellers form two-third of the total

travelers; with its emergence as the main ITes center, the proportion of foreigners has

Strong IT and Auto sector

revival to keep demand

high

Back-ended supply to

keep ARRs firm

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 15/106

14 Edelweiss Securities Limited

Hotels & Tourism

been rising consistently. As Chennai is also emerging as a hub for almost all auto majors,

we expect this trend to continue, going forward.

Chart 16: Business travellers to continue to form the majority

8.3 7.1 10.1 9.5

65.7 67.1 59.1 62.1

11.6 7.49.3

10.5

7.05.0 9.3 8.7

7.413.4 12.2 9.2

0.0

20.0

40.0

60.0

80.0

100.0

FY05 FY06 FY07 FY08

( % )

Others Tour Group Leisure Traveller Business Traveller A irline crew

Source: CRISIL, Edelweiss research

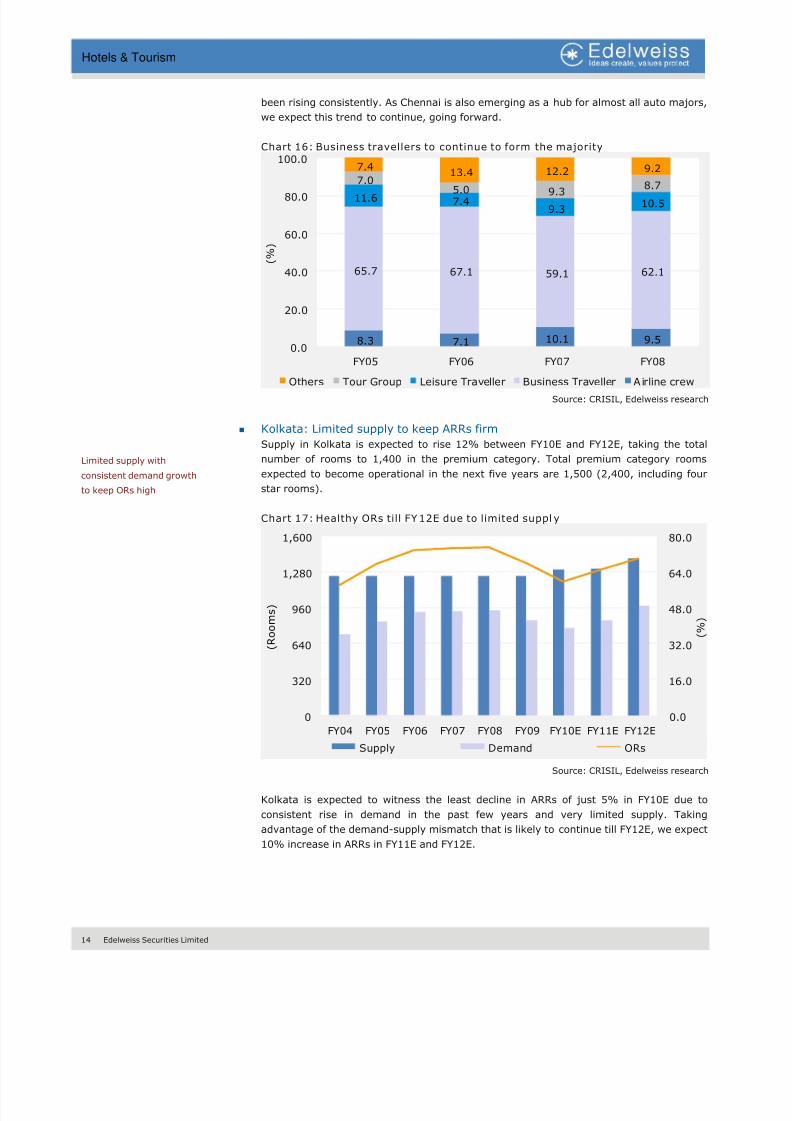

Kolkata: Limited supply to keep ARRs firm

Supply in Kolkata is expected to rise 12% between FY10E and FY12E, taking the total

number of rooms to 1,400 in the premium category. Total premium category rooms

expected to become operational in the next five years are 1,500 (2,400, including four

star rooms).

Chart 17: Healthy ORs till FY12E due to limited suppl y

0.0

16.0

32.0

48.0

64.0

80.0

0

320

640

960

1,280

1,600

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( R o o m s )

Supply Demand ORs

Source: CRISIL, Edelweiss research

Kolkata is expected to witness the least decline in ARRs of just 5% in FY10E due to

consistent rise in demand in the past few years and very limited supply. Taking

advantage of the demand-supply mismatch that is likely to continue till FY12E, we expect

10% increase in ARRs in FY11E and FY12E.

Limited supply with

consistent demand growth

to keep ORs high

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 16/106

Edelweiss Securities Limited 15

Hotels & Tourism

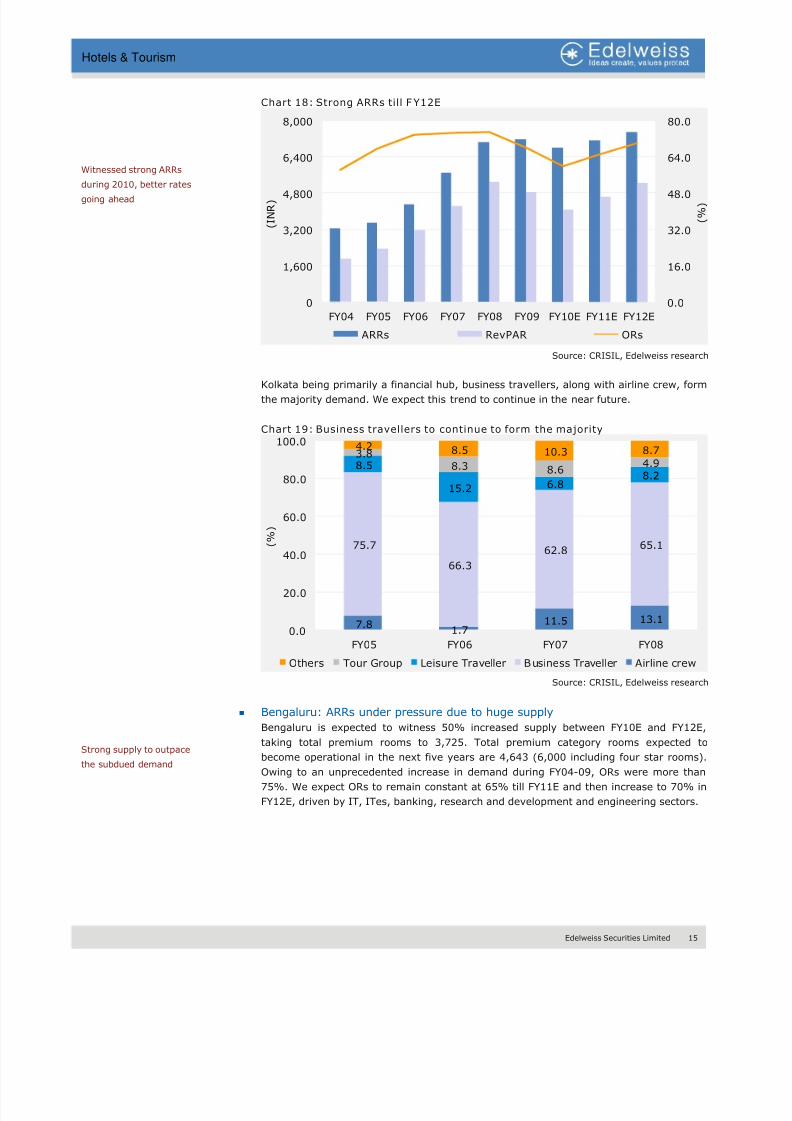

Chart 18: Strong ARRs till F Y12E

0.0

16.0

32.0

48.0

64.0

80.0

0

1,600

3,200

4,800

6,400

8,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( I N R )

ARRs RevPAR ORs

Source: CRISIL, Edelweiss research

Kolkata being primarily a financial hub, business travellers, along with airline crew, form

the majority demand. We expect this trend to continue in the near future.

Chart 19: Business travellers to continue to form the majority

7.81.7

11.5 13.1

75.7

66.3

62.865.1

8.5

15.2 6.88.2

3.88.3 8.6

4.9

4.2 8.5 10.3 8.7

0.0

20.0

40.0

60.0

80.0

100.0

FY05 FY06 FY07 FY08

( % )

Others Tour Group Leisure Traveller Business Traveller Airline crew

Source: CRISIL, Edelweiss research

Bengaluru: ARRs under pressure due to huge supply

Bengaluru is expected to witness 50% increased supply between FY10E and FY12E,

taking total premium rooms to 3,725. Total premium category rooms expected to

become operational in the next five years are 4,643 (6,000 including four star rooms).

Owing to an unprecedented increase in demand during FY04-09, ORs were more than

75%. We expect ORs to remain constant at 65% till FY11E and then increase to 70% in

FY12E, driven by IT, ITes, banking, research and development and engineering sectors.

Strong supply to outpacethe subdued demand

Witnessed strong ARRs

during 2010, better ratesgoing ahead

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 17/106

16 Edelweiss Securities Limited

Hotels & Tourism

Chart 20: ORs to firm post FY12E

0.0

18.0

36.0

54.0

72.0

90.0

0

800

1,600

2,400

3,200

4,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( R o o m s )

Supply Demand ORs

Source: CRISIL, Edelweiss research

We expect ARRs to rise 5% in FY11E and FY12E, after declining ~28% in FY10E (decline

due to the IT slowdown and new supply of rooms).

Chart 21: ARRs to firm FY11E onw ards

0.0

18.0

36.0

54.0

72.0

90.0

0

3,200

6,400

9,600

12,800

16,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( I N R )

ARRs RevPAR ORs

Source: CRISIL, Edelweiss research

With the emergence of Bengaluru as India’s Silicon Valley, business and foreign

travellers constitute more than three-fourth of the total demand. We expect this trend to

continue in future.

ARRs to witness growth

only post FY11

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 18/106

Edelweiss Securities Limited 17

Hotels & Tourism

Chart 22: IT/ ITes business travellers to continue to form the majority

4.5 8.3 5.4 6.7

69.1

7676.1 78.5

10.5

9.44.6

5.92.5

1.2

2.51.913.4

5.111.4 7

0.0

20.0

40.0

60.0

80.0

100.0

FY05 FY06 FY07 FY08

( % )

Others Tour Group Leisure Traveller Business Traveller Airline crew

Source: CRISIL, Edelweiss research

Hyderabad: Conferencing the next big trend

Hyderabad is expected to witness 45% increased room supply between FY10E and FY12E,

taking the total number of rooms to 2,800 in the premium category. Number of premium

category rooms expected to become operational in next five years is 2,500 (4,200

including four star rooms). We expect ORs to improve FY11E onwards, after hitting 55%

in FY10E.

Chart 23: Demand to catch up with supply post FY10E

0.0

18.0

36.0

54.0

72.0

90.0

0

600

1,200

1,800

2,400

3,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( R o o m s )

Supply Demand ORs

Source: CRISIL, Edelweiss research

We believe, going forward, the Hyderabad hotel industry will shape up with the number

of conferences happening there. Improved infrastructure already shows the efforts put in

by the state government to make Hyderabad a leading business city in India.

We expect slight improvement in ARRs FY11E onwards. With likelihood of Hyderabad

becoming a major conference city in the South and much better connectivity to the new

airport, ORs and ARRs are poised to improve, albeit gradually.

Conferencing facilities to

drive the growth in

demand

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 19/106

18 Edelweiss Securities Limited

Hotels & Tourism

Chart 24: Gradual improvement in ARRs FY10E onw ards

0.0

18.0

36.0

54.0

72.0

90.0

0

1,800

3,600

5,400

7,200

9,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( I N R )

ARRs RevPAR ORs

Source: CRISIL, Edelweiss research

Proportion of business travellers and airline crew has been going up consistently. We

expect this trend to continue in future, considering the way Hyderabad has come up on

the world IT map.

Chart 25: Proportion of business travellers to rise

1.5 0.4 6 5.5

60.6 68.4 58.7 62

6

10.4 15.8 13.53.5

8 7.2 828.4

12.8 12.3 11

0.0

20.0

40.0

60.0

80.0

100.0

FY05 FY06 FY07 FY08

( % )

Others Tour Group Leisure Traveller Business Traveller Airline crew

Source: CRISIL, Edelweiss research

Strong demand to help

ARRs to improve post

FY10

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 20/106

Edelweiss Securities Limited 19

Hotels & Tourism

Outlook on other major cities

Pune: We expect Pune to add 4,000 rooms over the next five years, growing more than

250%. In the premium category, ~1,000 rooms are expected to come up in the next five

years. Owing to IT slowdown and the swine flu scare, ARRs are expected to fall 25% in

FY10E and ORs to sub 50% levels. Likelihood of excess supply in the city is certain to

keep the pressure on ORs and ARRs in FY11E and FY12E.

Pune has become highly popular because of its biotechnology, pharmaceutical, IT, ITeS

and BPO industries, which will eventually drive growth in its hospitality industry.

Goa: The city is expected to register 30% jump in supply till FY12E, taking the total

supply close to 3,900 rooms. Tough real estate laws are to be blamed for the slow

development of hotels across the city. Including four star hotels, the total supply

expected in the next five years is 2,178 rooms. We expect Goa to witness continuous

rise in ARRs during FY11-12E, as we expect domestic travellers to replace the gap left by

foreign travellers to some extent. Recent trends show increased demand for hotel rooms

in Goa all year round, reducing the impact of seasonality on the local hotel market. This

is also evident from the fact that ORs, FY04 onwards, have been moving up consistently.

Long-term positive

outlook on demand-supply and ARRs on many

Indian cities

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 21/106

20 Edelweiss Securities Limited

Hotels & Tourism

Improving ARRs and ORs During 2010-12

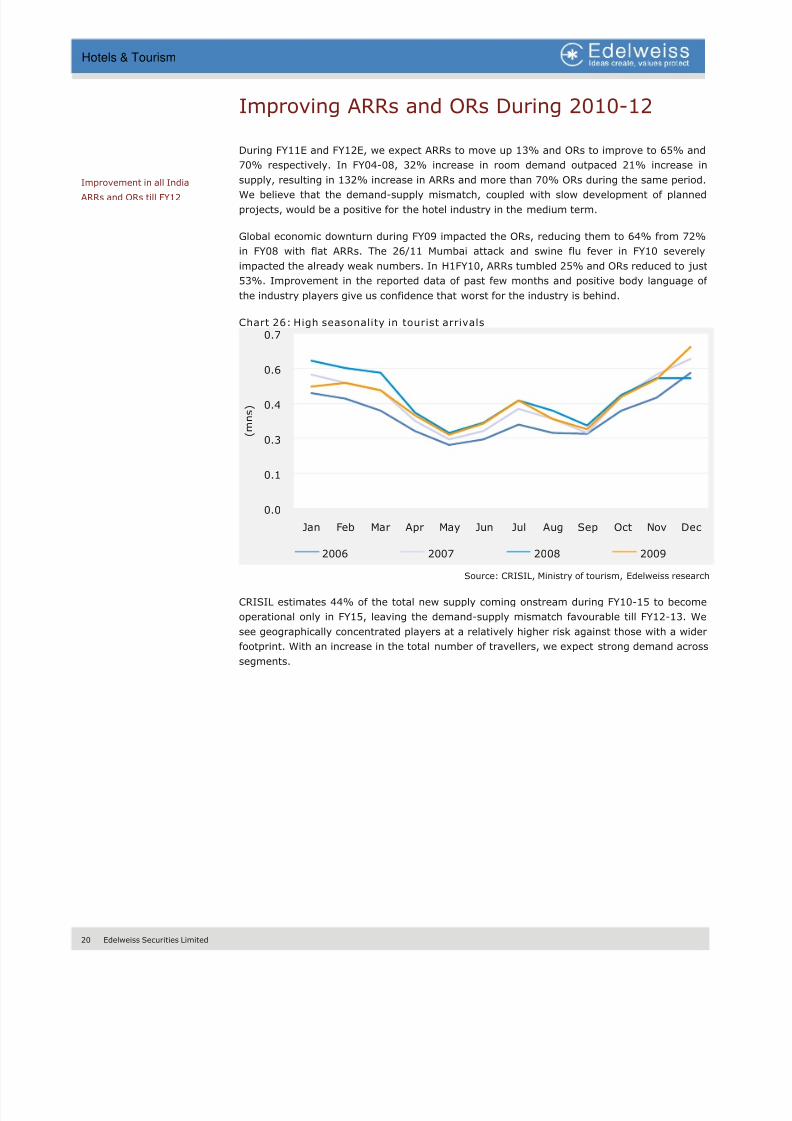

During FY11E and FY12E, we expect ARRs to move up 13% and ORs to improve to 65% and

70% respectively. In FY04-08, 32% increase in room demand outpaced 21% increase in

supply, resulting in 132% increase in ARRs and more than 70% ORs during the same period.

We believe that the demand-supply mismatch, coupled with slow development of planned

projects, would be a positive for the hotel industry in the medium term.

Global economic downturn during FY09 impacted the ORs, reducing them to 64% from 72%

in FY08 with flat ARRs. The 26/11 Mumbai attack and swine flu fever in FY10 severely

impacted the already weak numbers. In H1FY10, ARRs tumbled 25% and ORs reduced to just

53%. Improvement in the reported data of past few months and positive body language of

the industry players give us confidence that worst for the industry is behind.

Chart 26: High seasonality in tourist arrivals

0.0

0.1

0.3

0.4

0.6

0.7

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

( m n s )

2006 2007 2008 2009

Source: CRISIL, Ministry of tourism, Edelweiss research

CRISIL estimates 44% of the total new supply coming onstream during FY10-15 to become

operational only in FY15, leaving the demand-supply mismatch favourable till FY12-13. We

see geographically concentrated players at a relatively higher risk against those with a wider

footprint. With an increase in the total number of travellers, we expect strong demand across

segments.

Improvement in all India

ARRs and ORs till FY12

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 22/106

Edelweiss Securities Limited 21

Hotels & Tourism

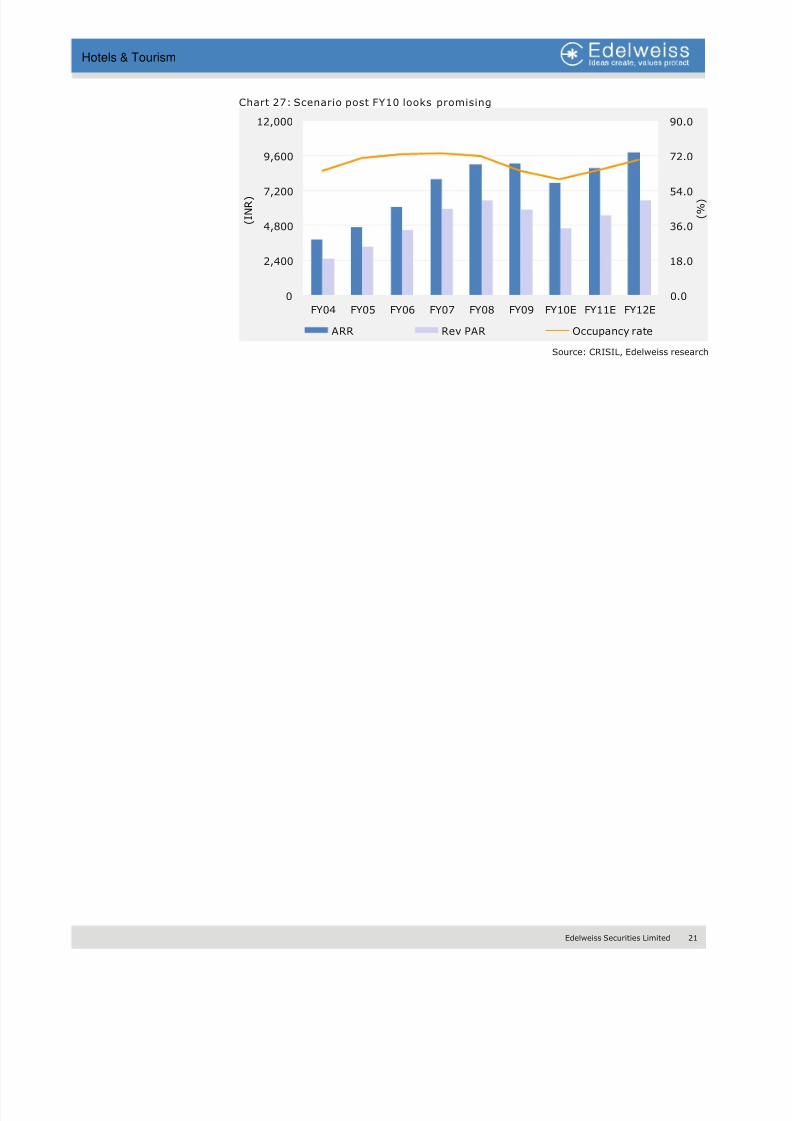

Chart 27: Scenario post FY10 looks promising

0.0

18.0

36.0

54.0

72.0

90.0

0

2,400

4,800

7,200

9,600

12,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

( % )

( I N R )

ARR Rev PAR Occupancy rate

Source: CRISIL, Edelweiss research

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 23/106

22 Edelweiss Securities Limited

Hotels & Tourism

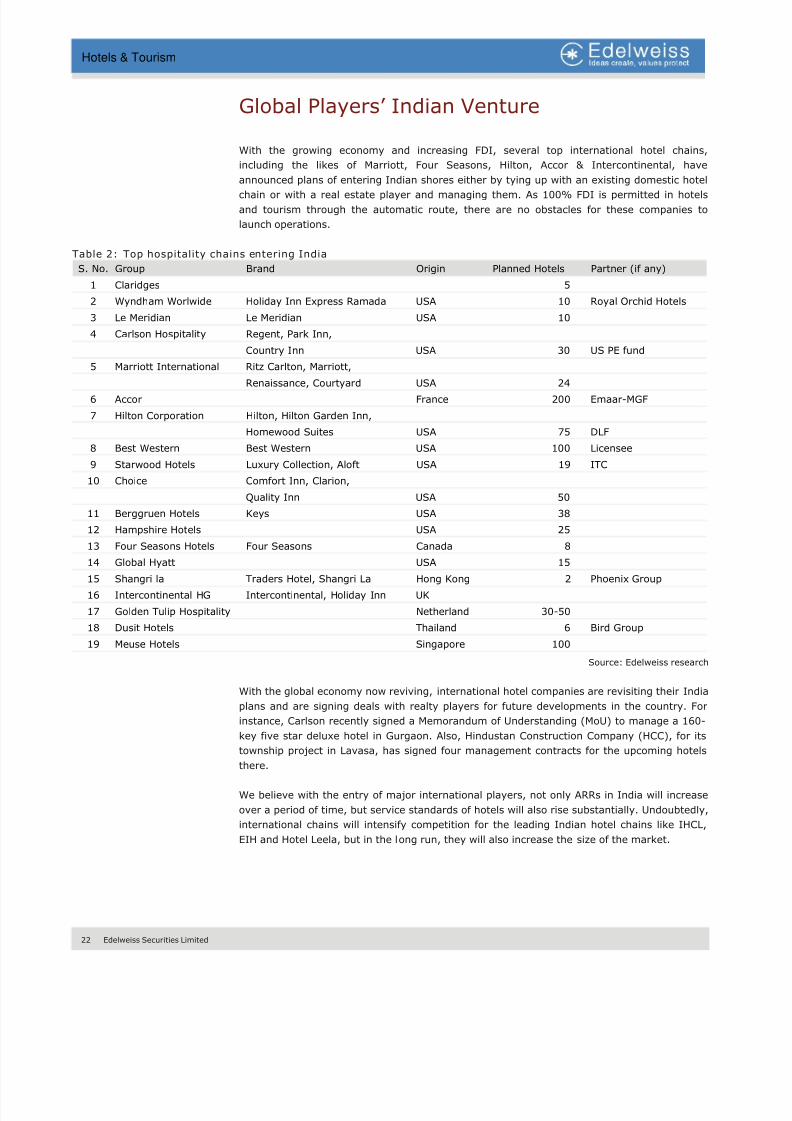

Global Players’ Indian Venture

With the growing economy and increasing FDI, several top international hotel chains,

including the likes of Marriott, Four Seasons, Hilton, Accor & Intercontinental, have

announced plans of entering Indian shores either by tying up with an existing domestic hotel

chain or with a real estate player and managing them. As 100% FDI is permitted in hotels

and tourism through the automatic route, there are no obstacles for these companies to

launch operations.

Table 2: Top hospitality chains entering India

S. No. Group Brand Origin Planned Hotels Partner (if any)

1 Claridges 5

2 Wyndham Worlwide Holiday Inn Express Ramada USA 10 Royal Orchid Hotels

3 Le Meridian Le Meridian USA 10

4 Carlson Hospitality Regent, Park Inn,

Country Inn USA 30 US PE fund

5 Marriott International Ritz Carlton, Marriott,

Renaissance, Courtyard USA 24

6 Accor France 200 Emaar-MGF

7 Hilton Corporation Hilton, Hilton Garden Inn,

Homewood Suites USA 75 DLF

8 Best Western Best Western USA 100 Licensee

9 Starwood Hotels Luxury Collection, Aloft USA 19 ITC

10 Choice Comfort Inn, Clarion,

Quality Inn USA 50

11 Berggruen Hotels Keys USA 38

12 Hampshire Hotels USA 25

13 Four Seasons Hotels Four Seasons Canada 8

14 Global Hyatt USA 15 15 Shangri la Traders Hotel, Shangri La Hong Kong 2 Phoenix Group

16 Intercontinental HG Intercontinental, Holiday Inn UK

17 Golden Tulip Hospitality Netherland 30-50

18 Dusit Hotels Thailand 6 Bird Group

19 Meuse Hotels Singapore 100

Source: Edelweiss research

With the global economy now reviving, international hotel companies are revisiting their India

plans and are signing deals with realty players for future developments in the country. For

instance, Carlson recently signed a Memorandum of Understanding (MoU) to manage a 160-

key five star deluxe hotel in Gurgaon. Also, Hindustan Construction Company (HCC), for its

township project in Lavasa, has signed four management contracts for the upcoming hotelsthere.

We believe with the entry of major international players, not only ARRs in India will increase

over a period of time, but service standards of hotels will also rise substantially. Undoubtedly,

international chains will intensify competition for the leading Indian hotel chains like IHCL,

EIH and Hotel Leela, but in the long run, they will also increase the size of the market.

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 24/106

Edelweiss Securities Limited 23

Hotels & Tourism

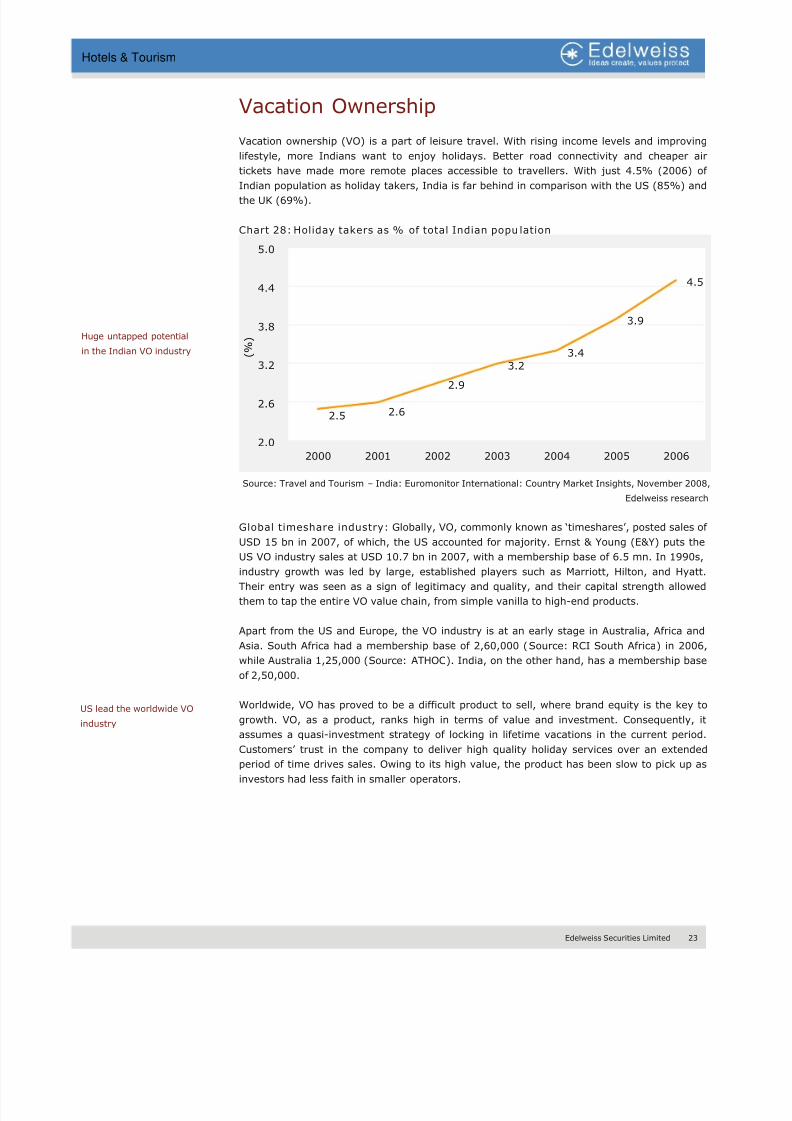

Vacation Ownership

Vacation ownership (VO) is a part of leisure travel. With rising income levels and improving

lifestyle, more Indians want to enjoy holidays. Better road connectivity and cheaper air

tickets have made more remote places accessible to travellers. With just 4.5% (2006) of

Indian population as holiday takers, India is far behind in comparison with the US (85%) andthe UK (69%).

Chart 28: Holiday takers as % of total Indian popu lation

2.5 2.6

2.9

3.2

3.4

3.9

4.5

2.0

2.6

3.2

3.8

4.4

5.0

2000 2001 2002 2003 2004 2005 2006

( % )

Source: Travel and Tourism – India: Euromonitor International: Country Market Insights, November 2008,

Edelweiss research

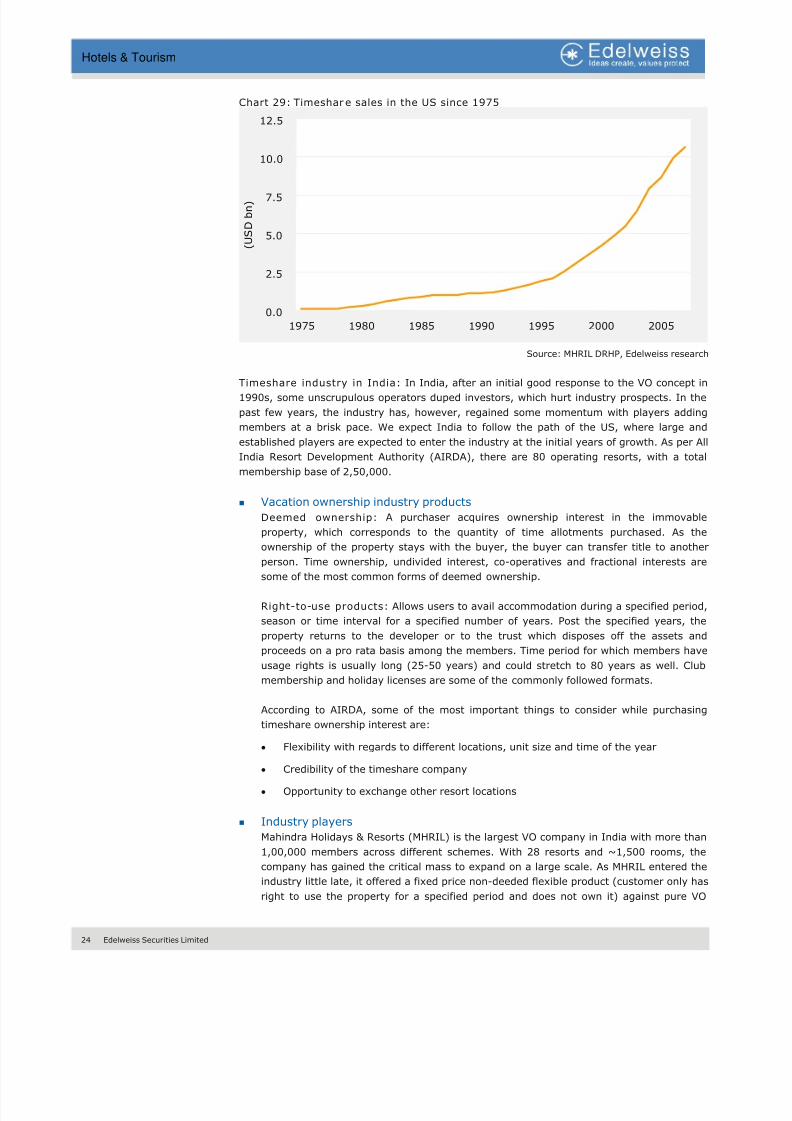

Global timeshare industry: Globally, VO, commonly known as ‘timeshares’, posted sales of

USD 15 bn in 2007, of which, the US accounted for majority. Ernst & Young (E&Y) puts the

US VO industry sales at USD 10.7 bn in 2007, with a membership base of 6.5 mn. In 1990s,

industry growth was led by large, established players such as Marriott, Hilton, and Hyatt.

Their entry was seen as a sign of legitimacy and quality, and their capital strength allowed

them to tap the entire VO value chain, from simple vanilla to high-end products.

Apart from the US and Europe, the VO industry is at an early stage in Australia, Africa and

Asia. South Africa had a membership base of 2,60,000 (Source: RCI South Africa) in 2006,

while Australia 1,25,000 (Source: ATHOC). India, on the other hand, has a membership base

of 2,50,000.

Worldwide, VO has proved to be a difficult product to sell, where brand equity is the key to

growth. VO, as a product, ranks high in terms of value and investment. Consequently, it

assumes a quasi-investment strategy of locking in lifetime vacations in the current period.

Customers’ trust in the company to deliver high quality holiday services over an extendedperiod of time drives sales. Owing to its high value, the product has been slow to pick up as

investors had less faith in smaller operators.

Huge untapped potential

in the Indian VO industry

US lead the worldwide VO

industry

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 25/106

24 Edelweiss Securities Limited

Hotels & Tourism

Chart 29: Timeshare sales in the US since 1975

0.0

2.5

5.0

7.5

10.0

12.5

1975 1980 1985 1990 1995 2000 2005

( U S D b n )

Source: MHRIL DRHP, Edelweiss research

Timeshare industry in India: In India, after an initial good response to the VO concept in

1990s, some unscrupulous operators duped investors, which hurt industry prospects. In the

past few years, the industry has, however, regained some momentum with players adding

members at a brisk pace. We expect India to follow the path of the US, where large and

established players are expected to enter the industry at the initial years of growth. As per All

India Resort Development Authority (AIRDA), there are 80 operating resorts, with a total

membership base of 2,50,000.

Vacation ownership industry products

Deemed ownership: A purchaser acquires ownership interest in the immovable

property, which corresponds to the quantity of time allotments purchased. As the

ownership of the property stays with the buyer, the buyer can transfer title to another

person. Time ownership, undivided interest, co-operatives and fractional interests aresome of the most common forms of deemed ownership.

Right-to-use products: Allows users to avail accommodation during a specified period,

season or time interval for a specified number of years. Post the specified years, the

property returns to the developer or to the trust which disposes off the assets and

proceeds on a pro rata basis among the members. Time period for which members have

usage rights is usually long (25-50 years) and could stretch to 80 years as well. Club

membership and holiday licenses are some of the commonly followed formats.

According to AIRDA, some of the most important things to consider while purchasing

timeshare ownership interest are:

• Flexibility with regards to different locations, unit size and time of the year

• Credibility of the timeshare company

• Opportunity to exchange other resort locations

Industry players

Mahindra Holidays & Resorts (MHRIL) is the largest VO company in India with more than

1,00,000 members across different schemes. With 28 resorts and ~1,500 rooms, the

company has gained the critical mass to expand on a large scale. As MHRIL entered the

industry little late, it offered a fixed price non-deeded flexible product (customer only has

right to use the property for a specified period and does not own it) against pure VO

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 26/106

Edelweiss Securities Limited 25

Hotels & Tourism

product (customer owns a share of the unit, and can use it for the designated holiday

period).

MHRIL offers 25-year 7 nights holidays to its members where membership rates range

from INR 0.15 to INR 1.00 mn. It offers purple, red, white and blue seasons as per the

membership rates. MHRIL charges its members upfront and uses that cash to build its

fixed assets inventory. The company also offers Zest (targeting young urban consumers

seeking short breaks), Club Mahindra Fundays (targeting corporate customers) and

Mahindra Homestays (targeting vacation travellers who prefer to stay with an Indian

family). Further, the company plans to launch more schemes like Mahindra Heritage (for

senior citizens), Gypsy (targeting teenagers) and fractional ownership property products

(for high-end customers seeking a holiday home).

MHRIL derives its revenues from membership fee, annual subscription fee, resort income,

securitization income and interest income. As MHRIL charges customers upfront to build

its resorts. The company gains as ownership of the property stays with it and the

member gains over a period of time as the value of membership increases which is

transferable.

Country Club and Sterling Holiday Resorts are some of the competitors in the listed

space, but their scale and operations are no comparison for MHRIL.

Mahindra Holidays

dominates the Indian VO

industry

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 27/106

26 Edelweiss Securities Limited

Hotels & Tourism

Global Travel & Tourism

T&T is currently one of the world’s largest economic activities. It is the leading industry in

many countries as well as the fastest growing economic sector worldwide in terms of job

creation, according to the World Tourism Organization (UNWTO). Encompassing all

components of T&T consumption, investment, government spending and exports, T&T isestimated to have generated ~USD 7,892 bn of economic activity worldwide in 2008. In 2008,

global T&T is expected to have accounted for USD 5,890 bn of economic activity, equivalent

to 9.9% of total GDP. In the same year, there were 230.5 mn jobs in the industry, making up

8.2% of the total employment worldwide. Rising economic importance of the industry has

been fuelled by the large and growing number of international travellers. According to

UNWTO, the number of international arrivals grew from 25 mn in 1950 to an estimated 763

mn in 2004, corresponding to an average annual growth rate of 6.5%.

T&T is divided into inbound and outbound tourism, where inbound refers to countries

attracting the largest number of tourists and outbound refers to countries from where the

largest number of tourist originate.

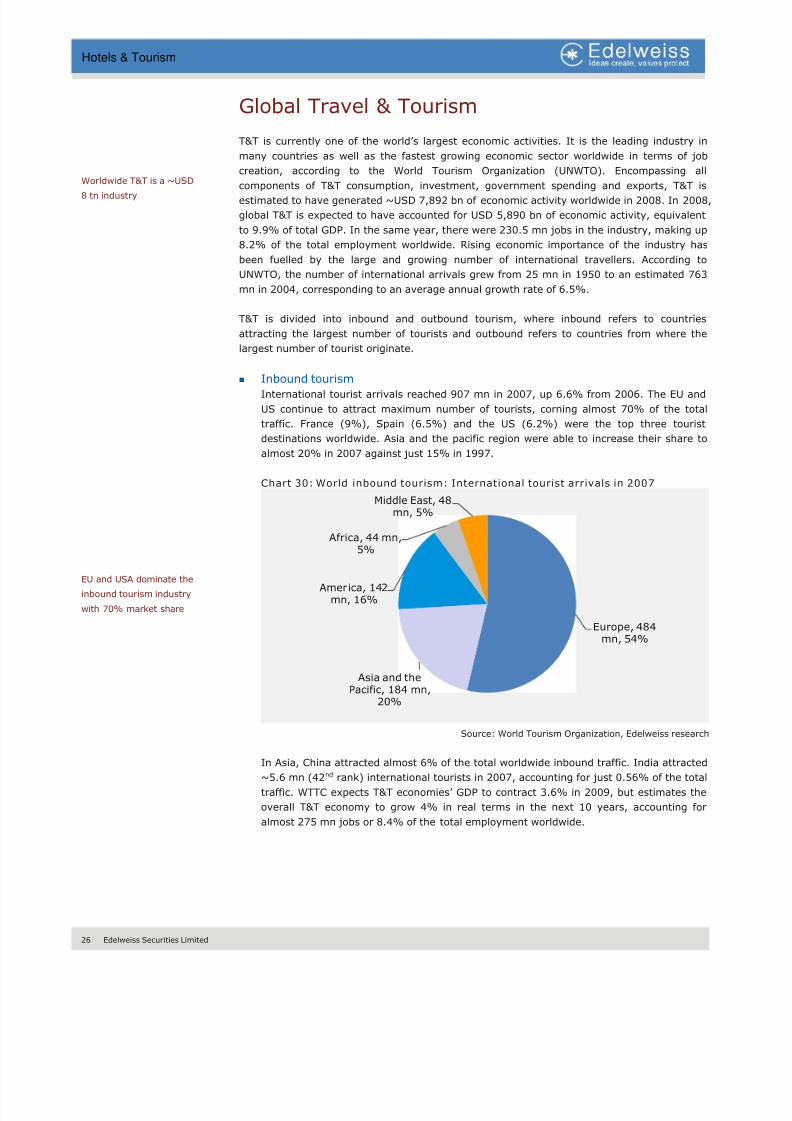

Inbound tourismInternational tourist arrivals reached 907 mn in 2007, up 6.6% from 2006. The EU and

US continue to attract maximum number of tourists, corning almost 70% of the total

traffic. France (9%), Spain (6.5%) and the US (6.2%) were the top three tourist

destinations worldwide. Asia and the pacific region were able to increase their share to

almost 20% in 2007 against just 15% in 1997.

Chart 30: World inbound tourism: International tourist arrivals in 2007

Europe, 484mn, 54%

Asia and thePacific, 184 mn,

20%

America, 142mn, 16%

Africa, 44 mn,5%

Middle East, 48mn, 5%

Source: World Tourism Organization, Edelweiss research

In Asia, China attracted almost 6% of the total worldwide inbound traffic. India attracted

~5.6 mn (42nd rank) international tourists in 2007, accounting for just 0.56% of the total

traffic. WTTC expects T&T economies’ GDP to contract 3.6% in 2009, but estimates the

overall T&T economy to grow 4% in real terms in the next 10 years, accounting for

almost 275 mn jobs or 8.4% of the total employment worldwide.

Worldwide T&T is a ~USD

8 tn industry

EU and USA dominate the

inbound tourism industry

with 70% market share

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 28/106

Edelweiss Securities Limited 27

Hotels & Tourism

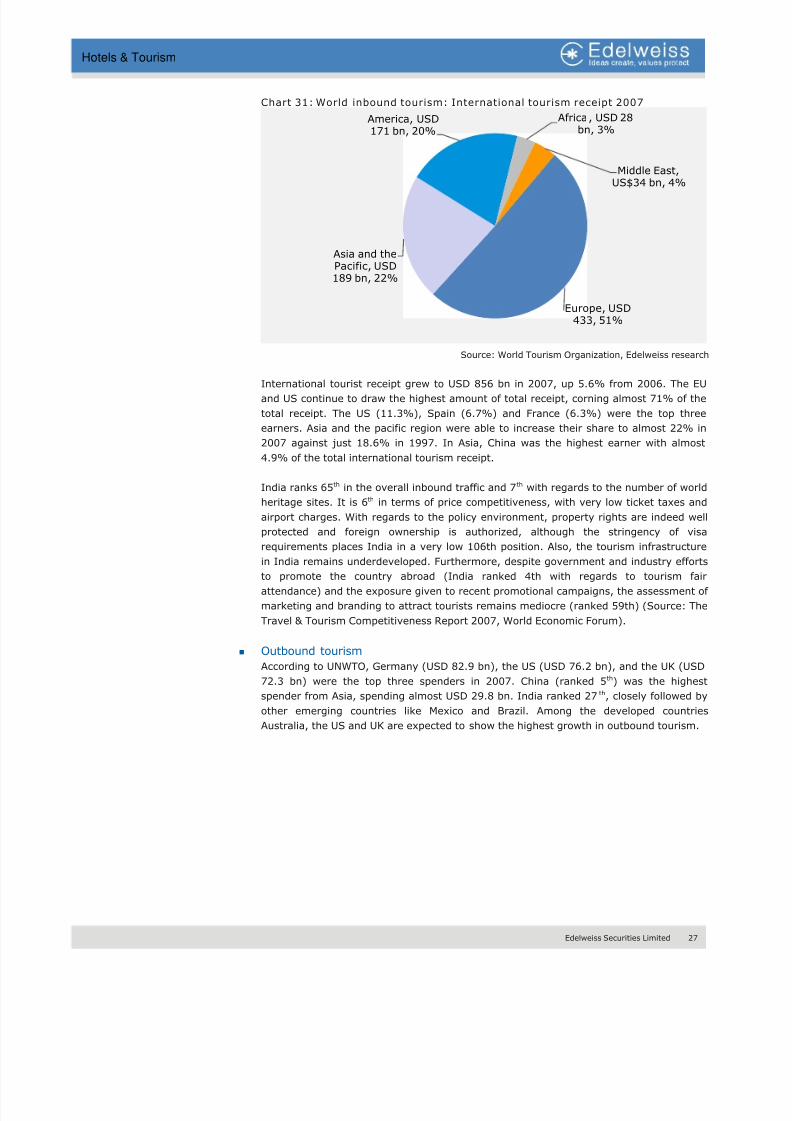

Chart 31: World inbound tourism: International tourism receipt 2007

Europe, USD433, 51%

Asia and thePacific, USD189 bn, 22%

America, USD171 bn, 20%

Africa, USD 28bn, 3%

Middle East,US$34 bn, 4%

Source: World Tourism Organization, Edelweiss research

International tourist receipt grew to USD 856 bn in 2007, up 5.6% from 2006. The EU

and US continue to draw the highest amount of total receipt, corning almost 71% of the

total receipt. The US (11.3%), Spain (6.7%) and France (6.3%) were the top three

earners. Asia and the pacific region were able to increase their share to almost 22% in

2007 against just 18.6% in 1997. In Asia, China was the highest earner with almost

4.9% of the total international tourism receipt.

India ranks 65th in the overall inbound traffic and 7th with regards to the number of world

heritage sites. It is 6th in terms of price competitiveness, with very low ticket taxes and

airport charges. With regards to the policy environment, property rights are indeed well

protected and foreign ownership is authorized, although the stringency of visa

requirements places India in a very low 106th position. Also, the tourism infrastructure

in India remains underdeveloped. Furthermore, despite government and industry effortsto promote the country abroad (India ranked 4th with regards to tourism fair

attendance) and the exposure given to recent promotional campaigns, the assessment of

marketing and branding to attract tourists remains mediocre (ranked 59th) (Source: The

Travel & Tourism Competitiveness Report 2007, World Economic Forum).

Outbound tourism

According to UNWTO, Germany (USD 82.9 bn), the US (USD 76.2 bn), and the UK (USD

72.3 bn) were the top three spenders in 2007. China (ranked 5th) was the highest

spender from Asia, spending almost USD 29.8 bn. India ranked 27 th, closely followed by

other emerging countries like Mexico and Brazil. Among the developed countries

Australia, the US and UK are expected to show the highest growth in outbound tourism.

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 29/106

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 30/106

Edelweiss Securities Limited 29

Hotels & Tourism

5. Hotel brand growth in India: With the emergence of India as one of the leading T&T

destinations worldwide, more than 25 leading international hotel names are lined up to

have a presence in one of the fastest growing economies. This is a far cry from 2000

when IHCL, EIH, ITC, and ITDC (government owned) used to dominate the hospitality

sector in India. Growth of Indian middle class offers a large consumer base for hotel

chains ranging from luxury to budget. With the lower end of the market still in the hands

of unorganized players, we expect huge scope for the organised sector.

6. Emerging MICE business opportunity: Convention or meetings tourism accounts for

over 20% of all international arrivals worldwide. The US and Europe dominate this space,

although several Asian countries have successfully captured a growing portion of MICE

business in recent years. The Hyderabad International Convention Centre (HICC) is

India's only branded (Novotel), large scale convention facility with a capacity of 5,000

which has been able to attract some business. IHCL is also planning to have a world-

class convention center in Mumbai. We believe with the growth of science and technology

related industries like biotechnology and pharmaceuticals (wherein companies host large

conferences), India needs to successfully replicate the model of HICC to tap the

emerging MICE business opportunity.

7. Food & beverage (F&B) concepts: With the emergence of standalone eating joints

selling their own USPs, five star hotels are expected to face a tough competition going

ahead. As diners are always ready to test different concepts with fine dining experience,

restaurants like Indigo, Tote, Olives, Tetsuma, Trishna, Zest and Smoke House Grill are

making marks in small pockets. We believe over a period of time, many more individual

restaurants with different concepts and superior interiors will come into India and expand

the market exponentially.

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 31/106

30 Edelweiss Securities Limited

Hotels & Tourism

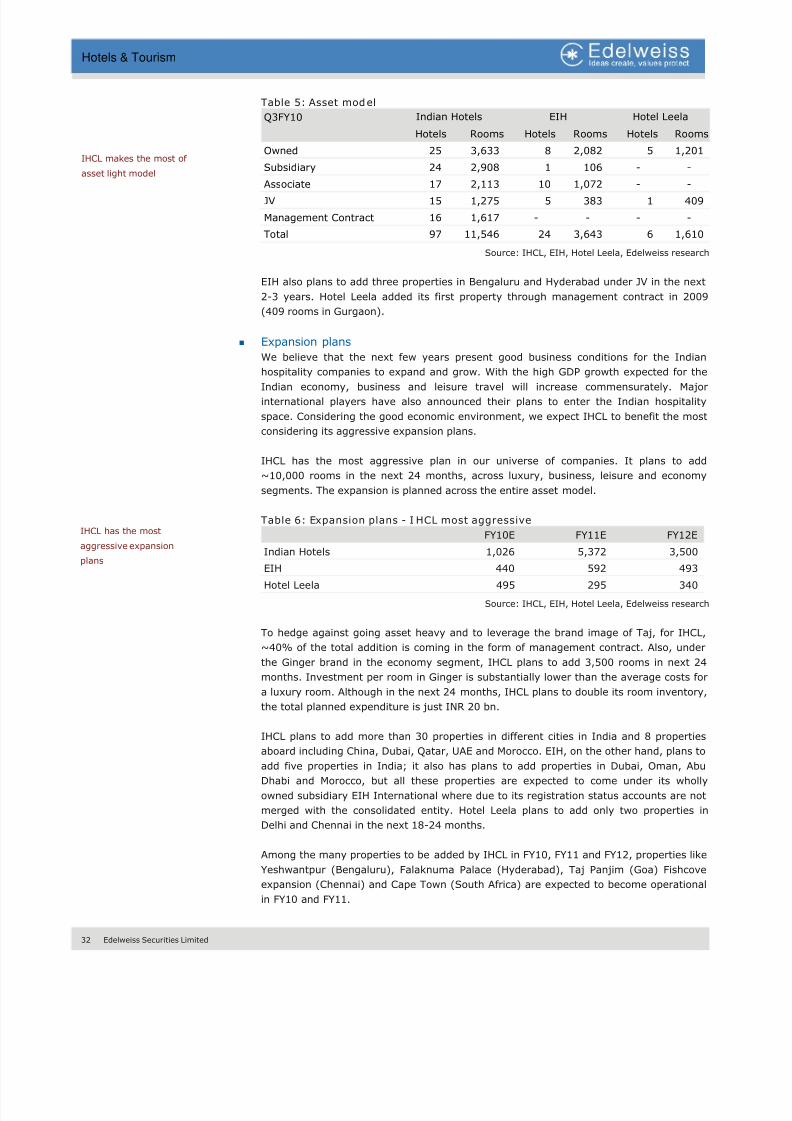

Business Analysis

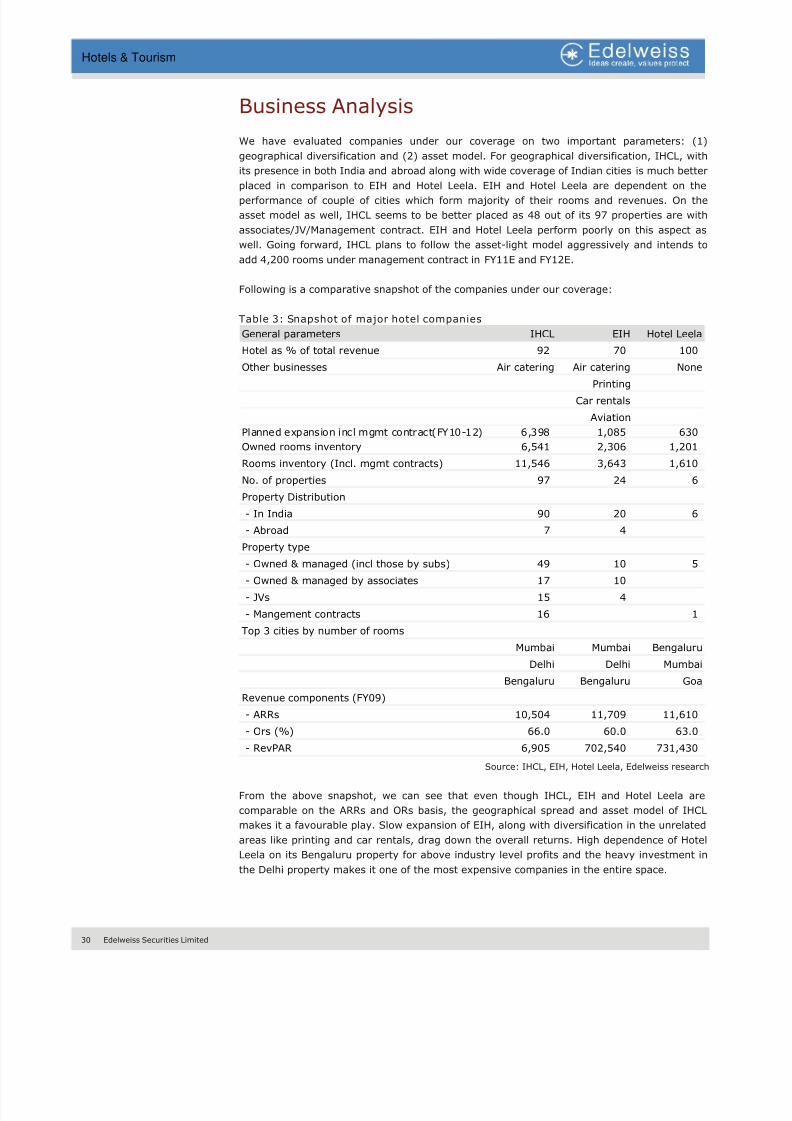

We have evaluated companies under our coverage on two important parameters: (1)

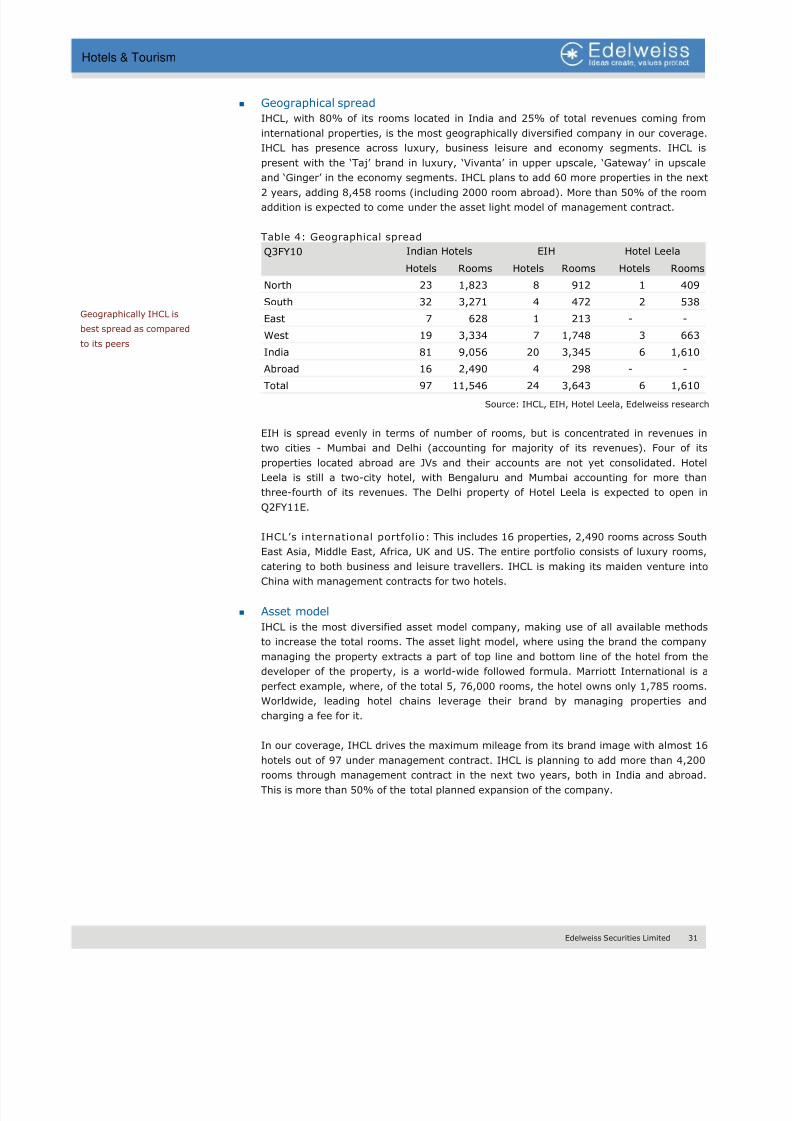

geographical diversification and (2) asset model. For geographical diversification, IHCL, with

its presence in both India and abroad along with wide coverage of Indian cities is much better

placed in comparison to EIH and Hotel Leela. EIH and Hotel Leela are dependent on theperformance of couple of cities which form majority of their rooms and revenues. On the

asset model as well, IHCL seems to be better placed as 48 out of its 97 properties are with

associates/JV/Management contract. EIH and Hotel Leela perform poorly on this aspect as

well. Going forward, IHCL plans to follow the asset-light model aggressively and intends to

add 4,200 rooms under management contract in FY11E and FY12E.

Following is a comparative snapshot of the companies under our coverage:

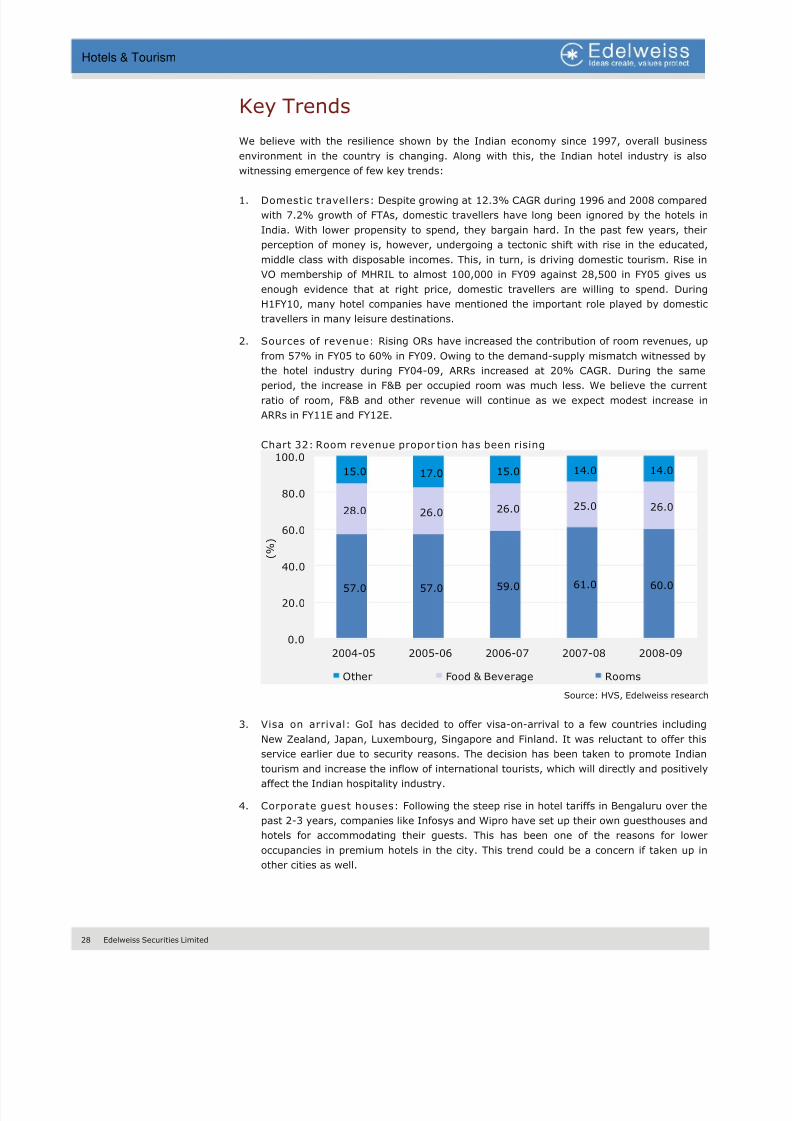

Table 3: Snapshot of major hotel companies

General parameters IHCL EIH Hotel Leela

Hotel as % of total revenue 92 70 100

Other businesses Air catering Air catering None

Printing

Car rentals

Aviation

Planned expansion incl mgmt contract(FY10-12) 6,398 1,085 630

Owned rooms inventory 6,541 2,306 1,201

Rooms inventory (Incl. mgmt contracts) 11,546 3,643 1,610

No. of properties 97 24 6

Property Distribution

- In India 90 20 6

- Abroad 7 4

Property type

- Owned & managed (incl those by subs) 49 10 5 - Owned & managed by associates 17 10

- JVs 15 4

- Mangement contracts 16 1

Top 3 cities by number of rooms

Mumbai Mumbai Bengaluru

Delhi Delhi Mumbai

Bengaluru Bengaluru Goa

Revenue components (FY09)

- ARRs 10,504 11,709 11,610

- Ors (%) 66.0 60.0 63.0

- RevPAR 6,905 702,540 731,430

Source: IHCL, EIH, Hotel Leela, Edelweiss research

From the above snapshot, we can see that even though IHCL, EIH and Hotel Leela are

comparable on the ARRs and ORs basis, the geographical spread and asset model of IHCL

makes it a favourable play. Slow expansion of EIH, along with diversification in the unrelated

areas like printing and car rentals, drag down the overall returns. High dependence of Hotel

Leela on its Bengaluru property for above industry level profits and the heavy investment in

the Delhi property makes it one of the most expensive companies in the entire space.

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 32/106

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 33/106

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 34/106

Edelweiss Securities Limited 33

Hotels & Tourism

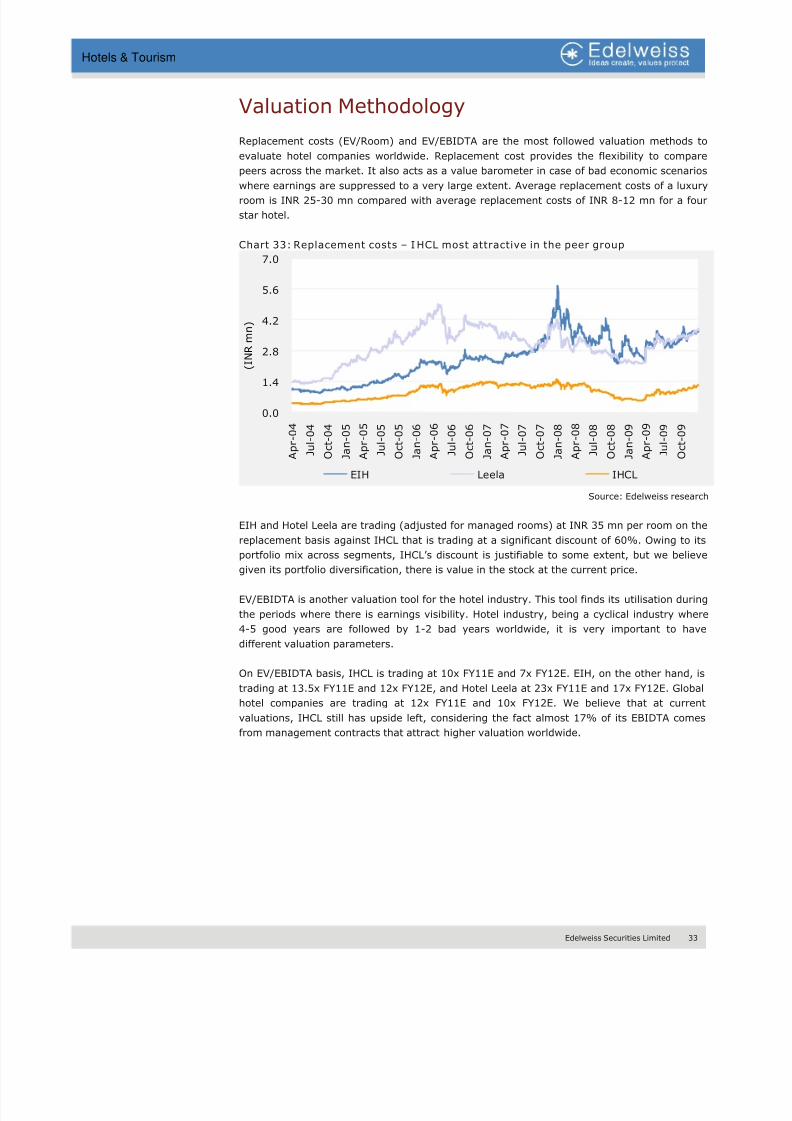

Valuation Methodology

Replacement costs (EV/Room) and EV/EBIDTA are the most followed valuation methods to

evaluate hotel companies worldwide. Replacement cost provides the flexibility to compare

peers across the market. It also acts as a value barometer in case of bad economic scenarios

where earnings are suppressed to a very large extent. Average replacement costs of a luxuryroom is INR 25-30 mn compared with average replacement costs of INR 8-12 mn for a four

star hotel.

Chart 33: Replacement costs – IHCL most attractive in the peer group

0.0

1.4

2.8

4.2

5.6

7.0

A p r - 0 4

J u l - 0 4

O c t - 0 4

J a n - 0 5

A p r - 0 5

J u l - 0 5

O c t - 0 5

J a n - 0 6

A p r - 0 6

J u l - 0 6

O c t - 0 6

J a n - 0 7

A p r - 0 7

J u l - 0 7

O c t - 0 7

J a n - 0 8

A p r - 0 8

J u l - 0 8

O c t - 0 8

J a n - 0 9

A p r - 0 9

J u l - 0 9

O c t - 0 9

( I N R m n )

EIH Leela IHCL

Source: Edelweiss research

EIH and Hotel Leela are trading (adjusted for managed rooms) at INR 35 mn per room on the

replacement basis against IHCL that is trading at a significant discount of 60%. Owing to its

portfolio mix across segments, IHCL’s discount is justifiable to some extent, but we believe

given its portfolio diversification, there is value in the stock at the current price.

EV/EBIDTA is another valuation tool for the hotel industry. This tool finds its utilisation during

the periods where there is earnings visibility. Hotel industry, being a cyclical industry where

4-5 good years are followed by 1-2 bad years worldwide, it is very important to have

different valuation parameters.

On EV/EBIDTA basis, IHCL is trading at 10x FY11E and 7x FY12E. EIH, on the other hand, is

trading at 13.5x FY11E and 12x FY12E, and Hotel Leela at 23x FY11E and 17x FY12E. Global

hotel companies are trading at 12x FY11E and 10x FY12E. We believe that at current

valuations, IHCL still has upside left, considering the fact almost 17% of its EBIDTA comes

from management contracts that attract higher valuation worldwide.

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 35/106

34 Edelweiss Securities Limited

Hotels & Tourism

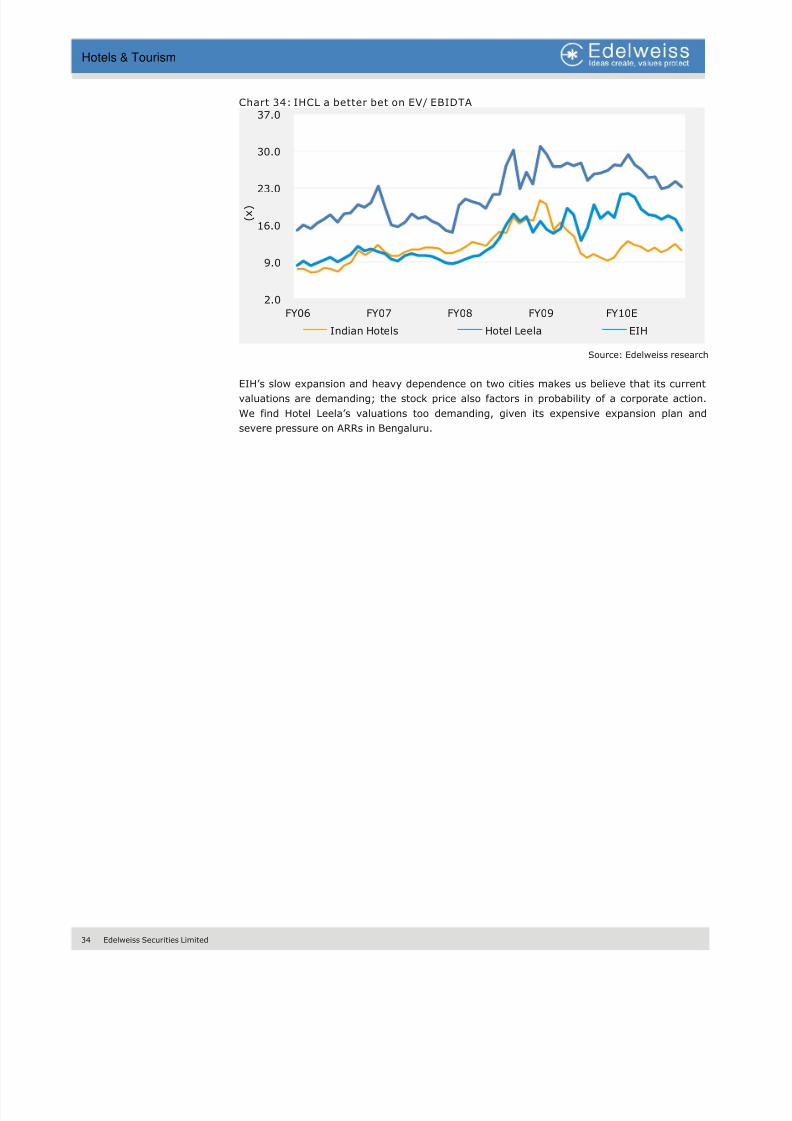

Chart 34: IHCL a better bet on EV/ EBIDTA

2.0

9.0

16.0

23.0

30.0

37.0

FY06 FY07 FY08 FY09 FY10E

( x )

Indian Hotels Hotel Leela EIH

Source: Edelweiss research

EIH’s slow expansion and heavy dependence on two cities makes us believe that its current

valuations are demanding; the stock price also factors in probability of a corporate action.

We find Hotel Leela’s valuations too demanding, given its expensive expansion plan and

severe pressure on ARRs in Bengaluru.

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 36/106

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 37/106

36 Edelweiss Securities Limited

Hotels & Tourism

Challenges

Scores of agencies and licenses major hurdle

As per ICRA, to start a new hotel in India, clearances from roughly 40 agencies and 110

licenses are required. Considering the state of bureaucracy in India, the time and costs

involved in getting the required approvals is quite high. We believe that the country

needs a single window clearance system, so that the industry can focus on getting the

operational issues right, then doing the paperwork.

Low FSI + high land costs: A dangerous combination

Considering the high costs of prime land in India, the current permissible FSI for hotels is

woefully inadequate. Manhattan allows FSI of 15 for hotels; whereas, in Mumbai it is

3.45 at Nariman Point, 2.66 in the city and 1 in suburbs. Higher FSI will allow hotels to

construct higher number of rooms, in turn, increasing the profitability of the property.

We realise that higher FSI will increase the already heavy pressure on the existing

inadequate infrastructure facilities. However, considering the importance of hotel

industry to the overall economy and the fact that it doesn’t receive any kind of benefit

from the government, we believe higher FSI is very much needed in India. In one of therecent development, Mumbai Metropolitan Region Development Authority (MMRDA)

recently sanctioned an FSI of 9.34 in G block of BKC, Mumbai. The higher FSI was

redistributed by MMRDA as the FSI in the area was underutilized.

Taxes: A complex issue

1. Section 80 I A (infrastructure status for the hotel industry): The Indian hotel

industry was asking for the infrastructure status under Section 80 IA of the IT Act.

In 2010 budget, the government has included hotels under section 35 AD where any

capex (excl. land, goodwill and financial instruments) incurred post 1.4.2010 is

eligible for 100% deduction as investment linked tax incentive in the year of

expenditure. We believe the benefit to help the industry in the long-term, even

though the land costs forms a major part of total capex.

In fact, under Section 10 (23) g of the IT Act, hotels were added to the

infrastructure list so that the interest received by financial institutions and banks for

loans extended to hotels were tax exempted. However, the section itself was

discontinued from April 1, 2007.

2. Luxury tax: Luxury tax, which is a state level tax, is levied on the published rates

without taking into consideration the discount given on the rack rates and

commission paid to agents. Luxury tax in India varies from 5% to 15%. The industry

has been asking for the tax to be reduced to a maximum of 5%.

3. VAT, sales tax, excise duty, custom duty and service taxes are some of the other

issues which the industry has been grappling with.

Infrastructure bottlenecks

Woefully inadequate infrastructure has been one of the biggest problems for India to

emerge as the topmost travel and tourism destination. In comparison to some of the

leading tourist destinations of South East Asia, the infrastructure in India scores poorly.

Inadequate infrastructure is one of the main reasons why many Indian cities with great

potential remain untapped on the world tourism map.

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 38/106

Edelweiss Securities Limited 37

Hotels & Tourism

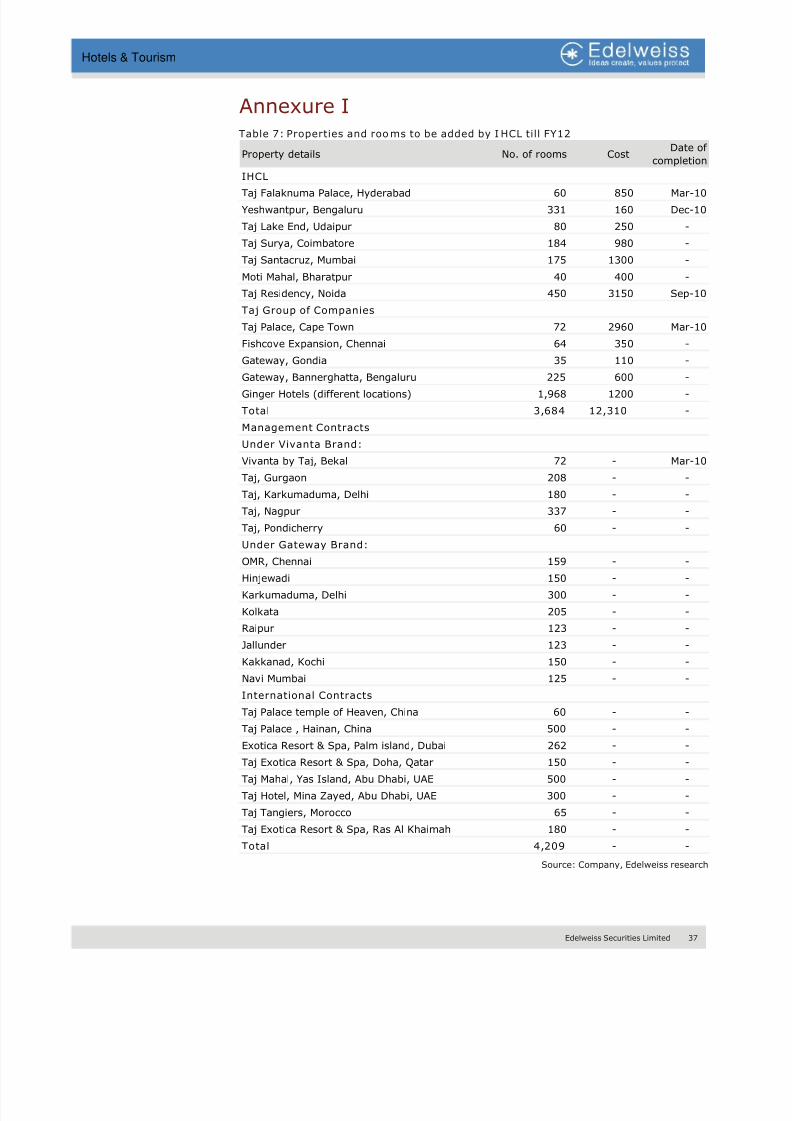

Annexure ITable 7: Properties and rooms to be added by I HCL till FY12

Property details No. of rooms CostDate of

completion

IHCL

Taj Falaknuma Palace, Hyderabad 60 850 Mar-10

Yeshwantpur, Bengaluru 331 160 Dec-10

Taj Lake End, Udaipur 80 250 -

Taj Surya, Coimbatore 184 980 -

Taj Santacruz, Mumbai 175 1300 -

Moti Mahal, Bharatpur 40 400 -

Taj Residency, Noida 450 3150 Sep-10

Taj Group of Companies

Taj Palace, Cape Town 72 2960 Mar-10

Fishcove Expansion, Chennai 64 350 -

Gateway, Gondia 35 110 -

Gateway, Bannerghatta, Bengaluru 225 600 -

Ginger Hotels (different locations) 1,968 1200 -

Total 3,684 12,310 -

Management Contracts

Under Vivanta Brand:

Vivanta by Taj, Bekal 72 - Mar-10

Taj, Gurgaon 208 - -

Taj, Karkumaduma, Delhi 180 - -

Taj, Nagpur 337 - -

Taj, Pondicherry 60 - -

Under Gateway Brand:

OMR, Chennai 159 - - Hinjewadi 150 - -

Karkumaduma, Delhi 300 - -

Kolkata 205 - -

Raipur 123 - -

Jallunder 123 - -

Kakkanad, Kochi 150 - -

Navi Mumbai 125 - -

International Contracts

Taj Palace temple of Heaven, China 60 - -

Taj Palace , Hainan, China 500 - -

Exotica Resort & Spa, Palm island, Dubai 262 - -

Taj Exotica Resort & Spa, Doha, Qatar 150 - -

Taj Mahal, Yas Island, Abu Dhabi, UAE 500 - -

Taj Hotel, Mina Zayed, Abu Dhabi, UAE 300 - -

Taj Tangiers, Morocco 65 - -

Taj Exotica Resort & Spa, Ras Al Khaimah 180 - -

Total 4,209 - -

Source: Company, Edelweiss research

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 39/106

38 Edelweiss Securities Limited

Hotels & Tourism

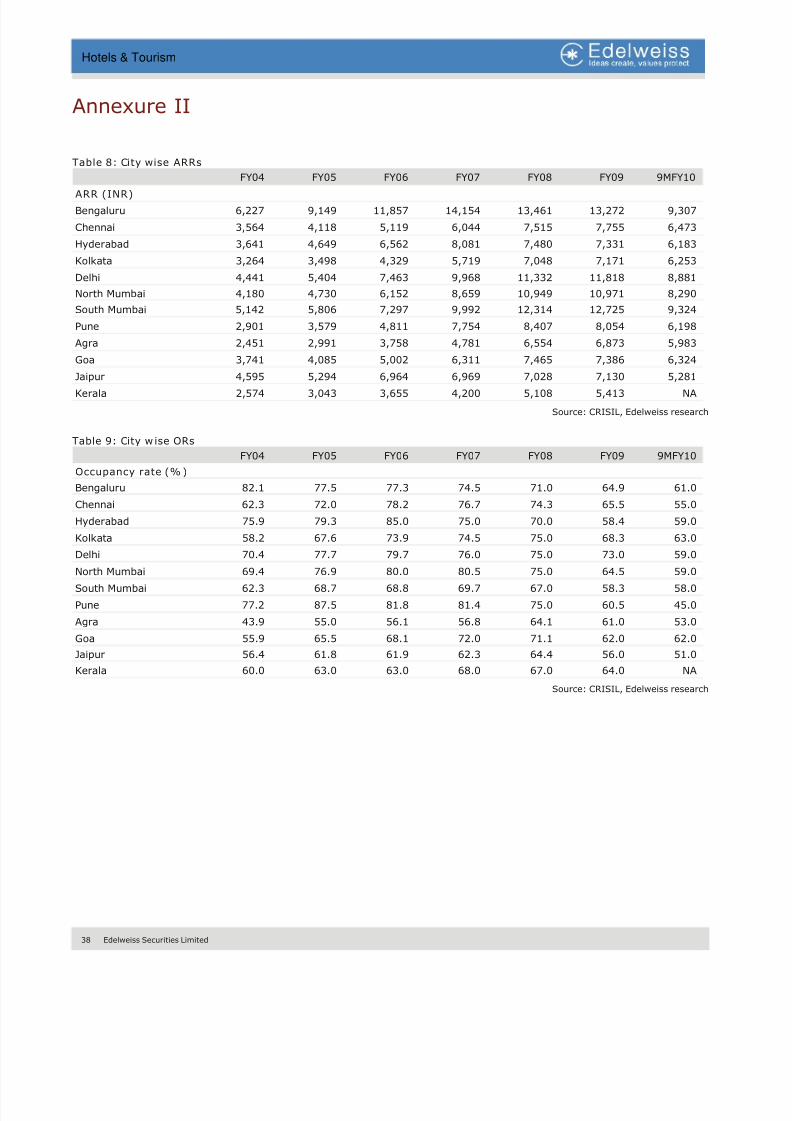

Annexure II

Table 8: City wise ARRs

FY04 FY05 FY06 FY07 FY08 FY09 9MFY10

ARR (INR)

Bengaluru 6,227 9,149 11,857 14,154 13,461 13,272 9,307

Chennai 3,564 4,118 5,119 6,044 7,515 7,755 6,473

Hyderabad 3,641 4,649 6,562 8,081 7,480 7,331 6,183

Kolkata 3,264 3,498 4,329 5,719 7,048 7,171 6,253

Delhi 4,441 5,404 7,463 9,968 11,332 11,818 8,881

North Mumbai 4,180 4,730 6,152 8,659 10,949 10,971 8,290

South Mumbai 5,142 5,806 7,297 9,992 12,314 12,725 9,324

Pune 2,901 3,579 4,811 7,754 8,407 8,054 6,198

Agra 2,451 2,991 3,758 4,781 6,554 6,873 5,983

Goa 3,741 4,085 5,002 6,311 7,465 7,386 6,324

Jaipur 4,595 5,294 6,964 6,969 7,028 7,130 5,281

Kerala 2,574 3,043 3,655 4,200 5,108 5,413 NA

Source: CRISIL, Edelweiss research

Table 9: City w ise ORs

FY04 FY05 FY06 FY07 FY08 FY09 9MFY10

Occupancy rate (% )

Bengaluru 82.1 77.5 77.3 74.5 71.0 64.9 61.0

Chennai 62.3 72.0 78.2 76.7 74.3 65.5 55.0

Hyderabad 75.9 79.3 85.0 75.0 70.0 58.4 59.0

Kolkata 58.2 67.6 73.9 74.5 75.0 68.3 63.0

Delhi 70.4 77.7 79.7 76.0 75.0 73.0 59.0

North Mumbai 69.4 76.9 80.0 80.5 75.0 64.5 59.0

South Mumbai 62.3 68.7 68.8 69.7 67.0 58.3 58.0

Pune 77.2 87.5 81.8 81.4 75.0 60.5 45.0

Agra 43.9 55.0 56.1 56.8 64.1 61.0 53.0

Goa 55.9 65.5 68.1 72.0 71.1 62.0 62.0

Jaipur 56.4 61.8 61.9 62.3 64.4 56.0 51.0

Kerala 60.0 63.0 63.0 68.0 67.0 64.0 NA

Source: CRISIL, Edelweiss research

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 40/106

Edelweiss Securities Limited 39

Hotels & Tourism

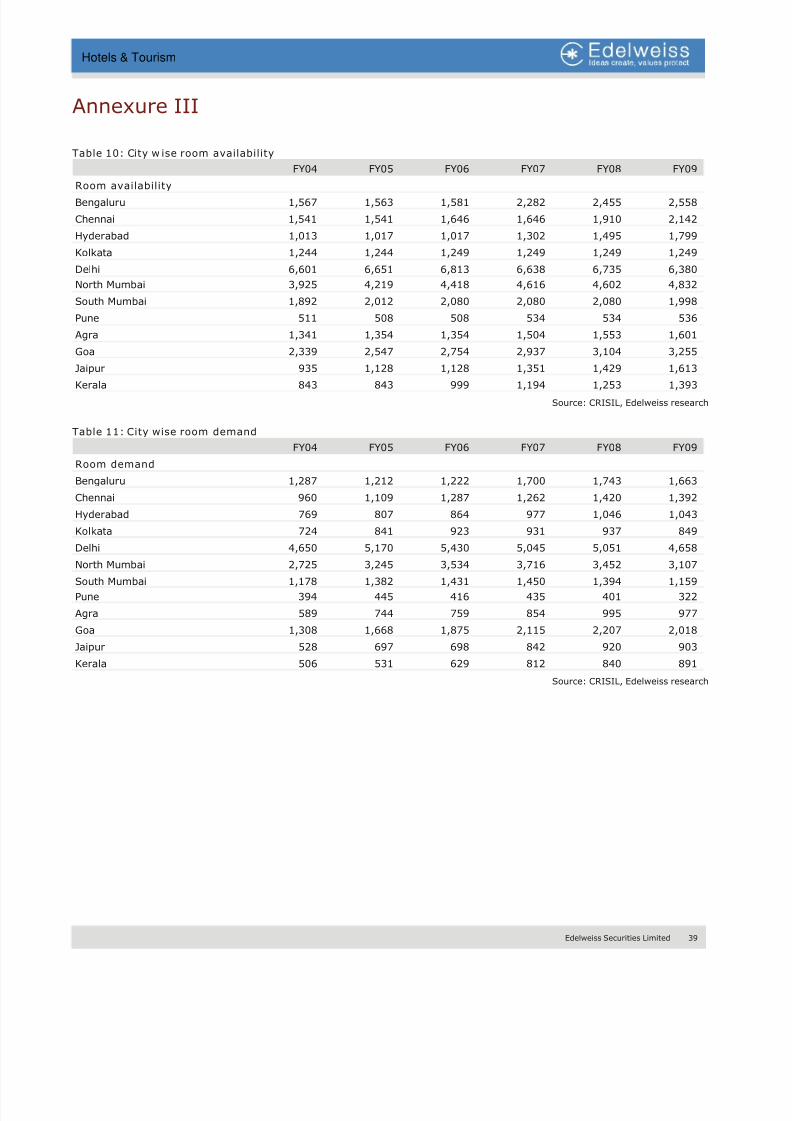

Annexure III

Table 10: City w ise room availability

FY04 FY05 FY06 FY07 FY08 FY09

Room availabilityBengaluru 1,567 1,563 1,581 2,282 2,455 2,558

Chennai 1,541 1,541 1,646 1,646 1,910 2,142

Hyderabad 1,013 1,017 1,017 1,302 1,495 1,799

Kolkata 1,244 1,244 1,249 1,249 1,249 1,249

Delhi 6,601 6,651 6,813 6,638 6,735 6,380

North Mumbai 3,925 4,219 4,418 4,616 4,602 4,832

South Mumbai 1,892 2,012 2,080 2,080 2,080 1,998

Pune 511 508 508 534 534 536

Agra 1,341 1,354 1,354 1,504 1,553 1,601

Goa 2,339 2,547 2,754 2,937 3,104 3,255

Jaipur 935 1,128 1,128 1,351 1,429 1,613

Kerala 843 843 999 1,194 1,253 1,393

Source: CRISIL, Edelweiss research

Table 11: City wise room demand

FY04 FY05 FY06 FY07 FY08 FY09

Room demand

Bengaluru 1,287 1,212 1,222 1,700 1,743 1,663

Chennai 960 1,109 1,287 1,262 1,420 1,392

Hyderabad 769 807 864 977 1,046 1,043

Kolkata 724 841 923 931 937 849

Delhi 4,650 5,170 5,430 5,045 5,051 4,658

North Mumbai 2,725 3,245 3,534 3,716 3,452 3,107 South Mumbai 1,178 1,382 1,431 1,450 1,394 1,159

Pune 394 445 416 435 401 322

Agra 589 744 759 854 995 977

Goa 1,308 1,668 1,875 2,115 2,207 2,018

Jaipur 528 697 698 842 920 903

Kerala 506 531 629 812 840 891

Source: CRISIL, Edelweiss research

8/8/2019 Hotel and Tourism

http://slidepdf.com/reader/full/hotel-and-tourism 41/106

40 Edelweiss Securities Limited

Hotels & Tourism

THIS PAGE IS INTENTIONALLY LEFT BLANK