Embed Size (px)

Citation preview

Elham Bolooki and Conrad Sokolnicki

FINN901

Hotel Feasibility Project Hilton Niagara Falls Fallsview Hotel and Suites

Executive Summary

The following report is a financial feasibility study on acquiring the Hilton Niagara Falls

Fallsview Hotel and Suites. Niagara Falls, Ontario, Canada is a popular tourist destination

with many entertainment and natural attractions that welcomes around 12 million visitors

annually. The Hilton Niagara Falls located in the destination is a 965 room property with 6

food and beverage outlets and meeting spaces located conveniently close to many attractions

in the city. Three competitors of the hotel include the Four Points by Sheraton Niagara Falls

Fallsview, Fallsview Casino Hotel, and the Crowne Plaza Niagara Falls Fallsview. Valuation

of the hotel was based on a three year average city wide ADR of USD 109.20 and occupancy

of 57.4%. A national debt to equity ratio of 60:40 was identified with a 4% interest rate and

17% ROE resulting in a cap rate of 10.71%. These figures valued the property at USD

103,015,000. Upon further investigation it was identified that an owner operated management

structure would produce the highest EBITDA during the stabilized year of around USD

11,139,000. Ten year cash flow, amortization, and depreciation are calculated for the

property. Using these figures NPV of the cash flow is calculated along with discounted

payback. The results showed a negative NPV and payback periods of longer than 10 years

(i.e. the holding period) under cash flow from property and cash flow to equity. As such it is

deemed that under current and forecasted market conditions, acquiring the Hilton Niagara

Falls Fallsview Hotel and Suites would not be feasible and therefore it is not recommended to

proceed with the investment. Should the investor proceed to go ahead with the project, great

efforts need to be made to increase revenues or decrease costs and in particular increase

occupancy rates to encourage the feasibility of the project.

Table of Content

i

sIntroduction................................................................................................................................1

Background – About Niagara Falls........................................................................................1Description of Chosen Property.............................................................................................3

Reason for Choosing this Location and Hotel...........................................................................6Justifications...............................................................................................................................8

Average Daily Rate................................................................................................................8Occupancy Rates....................................................................................................................8Food and Beverage Revenue..................................................................................................8Other Revenue........................................................................................................................8Departmental Expenses..........................................................................................................9Undistributed Expenses..........................................................................................................9Fixed Charges.........................................................................................................................9

Valuation..................................................................................................................................11Forecasted EBITDA at Purchase.........................................................................................11Capital Requirements...........................................................................................................12Valuation Using Income Method.........................................................................................13

Operational Structures..............................................................................................................14Descriptions of Operational Structures................................................................................14Operational Structures - Stable Year EBITDA....................................................................17Stable Year EBITDA Summary...........................................................................................21

11 Year EBITDA Forecast.......................................................................................................22Estimated Amortization...........................................................................................................23Depreciation of the Property....................................................................................................24Cash Flow of the Property........................................................................................................25Feasibility of Property..............................................................................................................26

Net Present Value (NPV) of Cash Flows.............................................................................26Average Accounting Return (ARR).....................................................................................26Payback Period.....................................................................................................................27

Discussion................................................................................................................................28References................................................................................................................................30

ii

Introduction

The chosen city for the feasibility study is Niagara Falls, Ontario, Canada.

Background – About Niagara Falls

Niagara Falls City is an enormously popular tourist destination in the southeastern part of

Ontario Canada that welcomes around 12 million visitors each year (City of Niagara Falls,

2015). The city which boasts all four seasons overlooks both the Canadian Horseshoe falls

and American falls which combined have 750,000 US Gallons of water per second flow over

them making it the largest waterfalls by volume in the world (Niagara Falls Live, 2015).

Niagara Falls View from the Canadian Side

Source: Niagara Falls Live, 2015

Niagara Falls has an extensive multimodal transportation network of roads, rail, air and

water. The city is situated within the international travel corridor between Canada and the

US. In fact, it is located directly along the border of the US, and has direct cross border

connections through a series of road and rail bridges including the Rainbow Bridge,

Whirlpool Bridge and Queenston-Lewiston Bridge. These road and rail links connect all

major 400 series national highways in Canada to the US state highway system. Niagara Falls

is also located within an hour’s drive from three international airports while private charter

flights can make it even closer to the city at the Niagara District Airport located minutes from

the downtown area (City of Niagara Falls, 2015).

The city offers visitors a wide portfolio of attractions which include Queen Victoria Park

offering pristine views of the falls; The Maid of the Mist, a boat trip that takes adventurous

travelers a chance to float up to the foot of the falls; the neighborhoods of Lundy’s Lane and

Clifton Hill which offer a variety of entertainment, dining, shopping, and nightlight venues;

the 775 foot Skylon Tower and Pavilion, containing a revolving restaurant and observation

1

deck overlooking the falls; the Butterfly Conservatory at Niagara Parks Botanical Gardens;

Marineland, a themed amusement and marine animal exhibition park; and several pristine

golf courses (City of Niagara Falls, 2015 ).

Niagara Falls at Night

Source: Niagara Falls Tourism, 2015

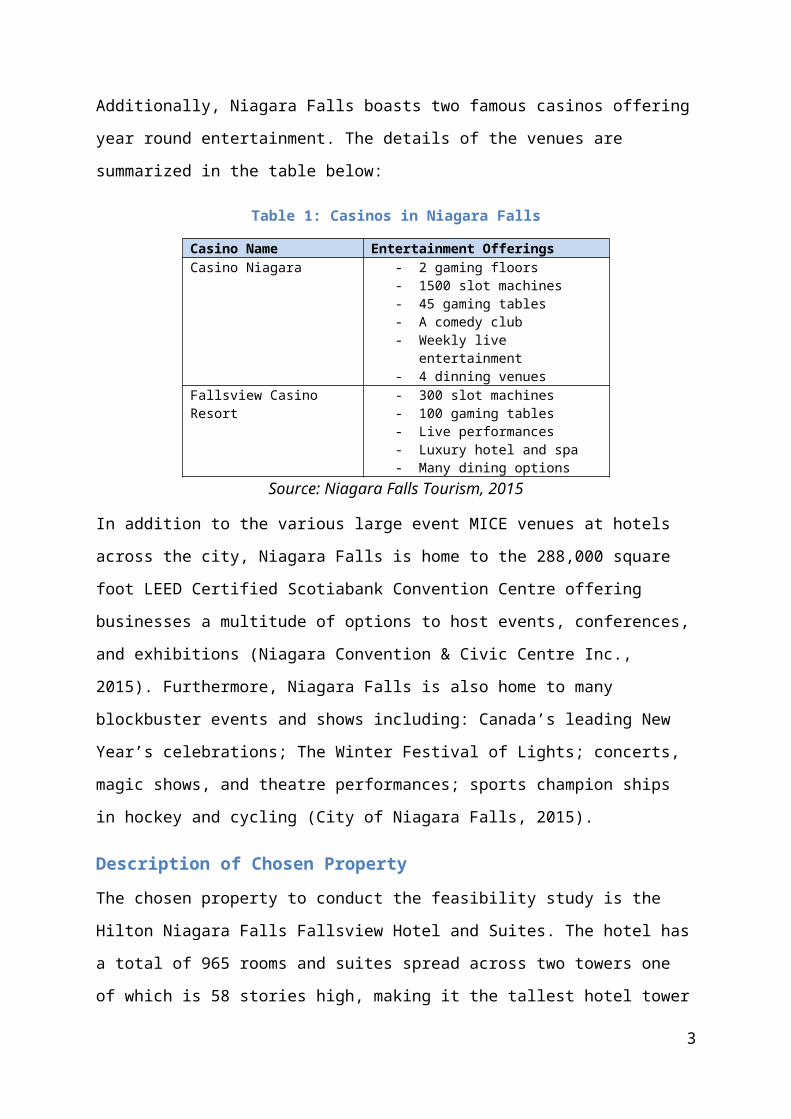

Additionally, Niagara Falls boasts two famous casinos offering year round entertainment.

The details of the venues are summarized in the table below:

Table 1: Casinos in Niagara Falls

Casino Name Entertainment OfferingsCasino Niagara - 2 gaming floors

- 1500 slot machines- 45 gaming tables- A comedy club- Weekly live entertainment- 4 dinning venues

Fallsview Casino Resort - 300 slot machines- 100 gaming tables- Live performances- Luxury hotel and spa- Many dining options

Source: Niagara Falls Tourism, 2015

In addition to the various large event MICE venues at hotels across the city, Niagara Falls is

home to the 288,000 square foot LEED Certified Scotiabank Convention Centre offering

businesses a multitude of options to host events, conferences, and exhibitions (Niagara

Convention & Civic Centre Inc., 2015). Furthermore, Niagara Falls is also home to many

blockbuster events and shows including: Canada’s leading New Year’s celebrations; The

Winter Festival of Lights; concerts, magic shows, and theatre performances; sports champion

ships in hockey and cycling (City of Niagara Falls, 2015).

2

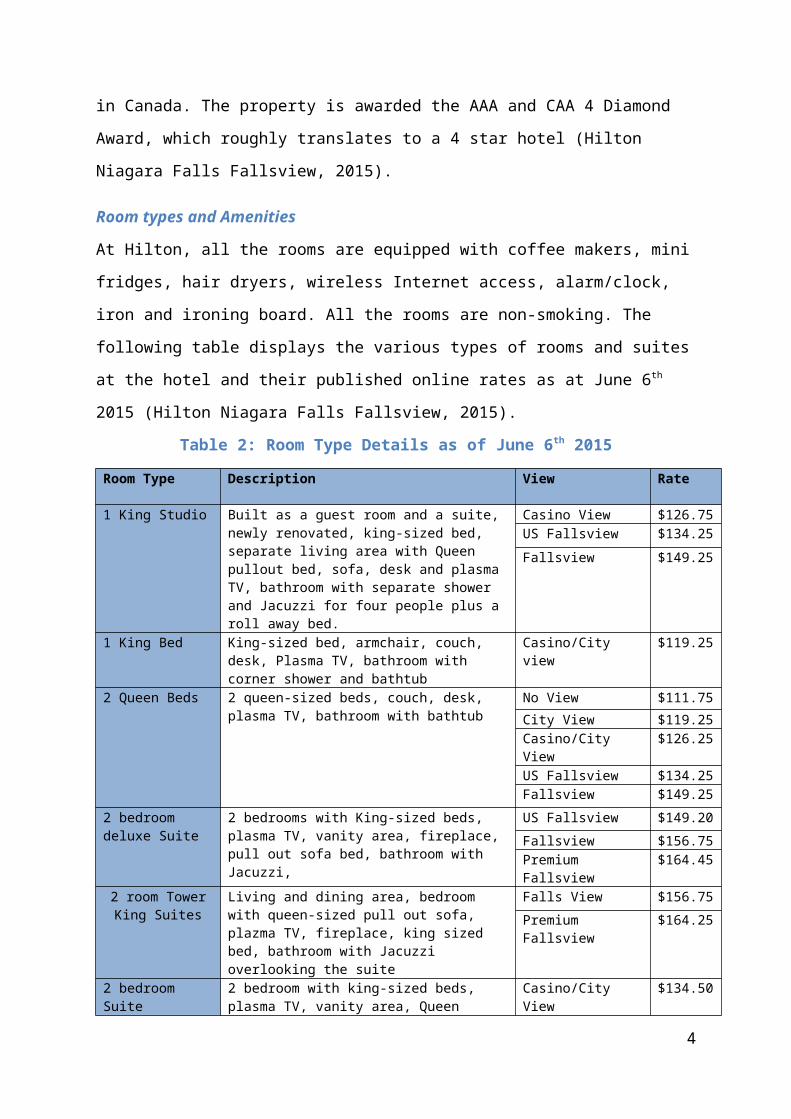

Description of Chosen Property

The chosen property to conduct the feasibility study is the Hilton Niagara Falls Fallsview

Hotel and Suites. The hotel has a total of 965 rooms and suites spread across two towers one

of which is 58 stories high, making it the tallest hotel tower in Canada. The property is

awarded the AAA and CAA 4 Diamond Award, which roughly translates to a 4 star hotel

(Hilton Niagara Falls Fallsview, 2015).

Room types and Amenities

At Hilton, all the rooms are equipped with coffee makers, mini fridges, hair dryers, wireless

Internet access, alarm/clock, iron and ironing board. All the rooms are non-smoking. The

following table displays the various types of rooms and suites at the hotel and their published

online rates as at June 6th 2015 (Hilton Niagara Falls Fallsview, 2015).

Table 2: Room Type Details as of June 6th 2015

Room Type Description View Rate

1 King Studio Built as a guest room and a suite, newly renovated, king-sized bed, separate living area with Queen pullout bed, sofa, desk and plasma TV, bathroom with separate shower and Jacuzzi for four people plus a roll away bed.

Casino View $126.75US Fallsview $134.25

Fallsview $149.25

1 King Bed King-sized bed, armchair, couch, desk, Plasma TV, bathroom with corner shower and bathtub

Casino/City view $119.25

2 Queen Beds 2 queen-sized beds, couch, desk, plasma TV, bathroom with bathtub

No View $111.75

City View $119.25Casino/City View $126.25US Fallsview $134.25Fallsview $149.25

2 bedroom deluxe Suite

2 bedrooms with King-sized beds, plasma TV, vanity area, fireplace, pull out sofa bed, bathroom with Jacuzzi,

US Fallsview $149.20

Fallsview $156.75Premium Fallsview $164.45

2 room Tower King Suites

Living and dining area, bedroom with queen-sized pull out sofa, plazma TV, fireplace, king sized bed, bathroom with Jacuzzi overlooking the suite

Falls View $156.75

Premium Fallsview $164.25

2 bedroom Suite 2 bedroom with king-sized beds, plasma TV, vanity area, Queen pullout sofa and bathroom with Jacuzzi

Casino/City View $134.50

Source: Hilton Niagara Falls Fallsview, 2015

3

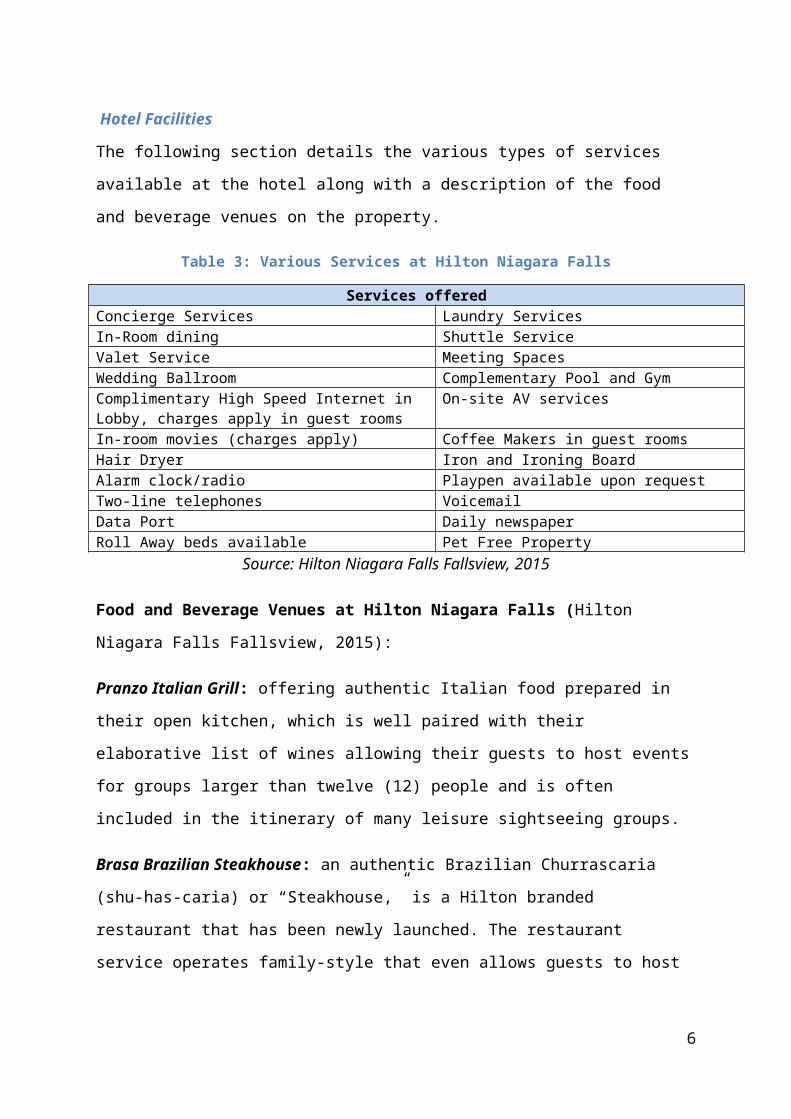

Hotel Facilities

The following section details the various types of services available at the hotel along with a

description of the food and beverage venues on the property.

Table 3: Various Services at Hilton Niagara Falls

Services offeredConcierge Services Laundry ServicesIn-Room dining Shuttle ServiceValet Service Meeting SpacesWedding Ballroom Complementary Pool and GymComplimentary High Speed Internet in Lobby, charges apply in guest rooms

On-site AV services

In-room movies (charges apply) Coffee Makers in guest roomsHair Dryer Iron and Ironing BoardAlarm clock/radio Playpen available upon requestTwo-line telephones VoicemailData Port Daily newspaperRoll Away beds available Pet Free Property

Source: Hilton Niagara Falls Fallsview, 2015

Food and Beverage Venues at Hilton Niagara Falls (Hilton Niagara Falls Fallsview,

2015):

Pranzo Italian Grill: offering authentic Italian food prepared in their open kitchen, which is

well paired with their elaborative list of wines allowing their guests to host events for groups

larger than twelve (12) people and is often included in the itinerary of many leisure

sightseeing groups.

Brasa Brazilian Steakhouse: an authentic Brazilian Churrascaria (shu-has-caria) or

“Steakhouse,” is a Hilton branded restaurant that has been newly launched. The restaurant

service operates family-style that even allows guests to host events for groups larger than

twelve (12) people and is often included in the itinerary of many leisure sightseeing groups.

Watermark Rooftop Restaurant: This restaurant is located on the 33rd level of the property

allowing guests to experience a unique cuisine with an elaborative wine list. This restaurant

also allows guests to host events for groups larger than twelve (12) people and is often

included in the itinerary of many leisure sightseeing groups.

Spyce Lounge: a special restaurant located on street level right in the heart of the Niagara

Falls’ entertainment district.

4

Grand Cafe Breakfast Buffet: a spacious breakfast buffet offering European cuisines that

incorporates numerous live cooking stations as well.

Mercato Market Café: a small café brewing Starbucks coffee and offering Yogurty’s frozen

yogurt. The restaurant also offers many different food items from pizzas to muffins.

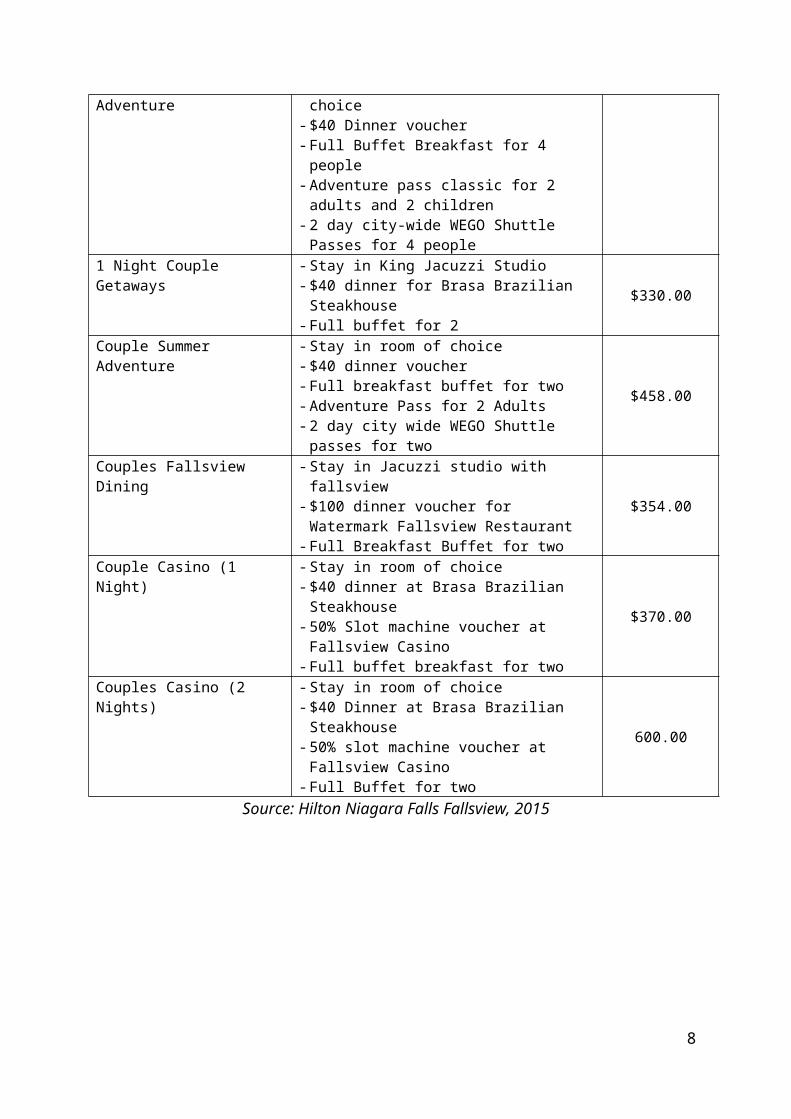

Packages Offered

The following at the special packages offered on the hotel’s website as of June 6th 2015.

Table 4: Special offers at Hilton Niagara Falls

Packages Description Average RatesFamily - Two bedroom deluxe suite for 6 people

- $24 Dinner at Pranzo Italian- Full Buffet for 4 people- Two day city wide WEGO Shuttle passes for 4

people

$329.00

Family Summer Adventure - Stay in room of your guests choice- $40 Dinner voucher- Full Buffet Breakfast for 4 people- Adventure pass classic for 2 adults and 2

children- 2 day city-wide WEGO Shuttle Passes for 4

people

$499.00

1 Night Couple Getaways - Stay in King Jacuzzi Studio- $40 dinner for Brasa Brazilian Steakhouse- Full buffet for 2

$330.00

Couple Summer Adventure - Stay in room of choice- $40 dinner voucher- Full breakfast buffet for two- Adventure Pass for 2 Adults- 2 day city wide WEGO Shuttle passes for two

$458.00

Couples Fallsview Dining - Stay in Jacuzzi studio with fallsview- $100 dinner voucher for Watermark Fallsview

Restaurant- Full Breakfast Buffet for two

$354.00

Couple Casino (1 Night) - Stay in room of choice- $40 dinner at Brasa Brazilian Steakhouse- 50% Slot machine voucher at Fallsview Casino- Full buffet breakfast for two

$370.00

Couples Casino (2 Nights) - Stay in room of choice- $40 Dinner at Brasa Brazilian Steakhouse- 50% slot machine voucher at Fallsview Casino- Full Buffet for two

600.00

Source: Hilton Niagara Falls Fallsview, 2015

5

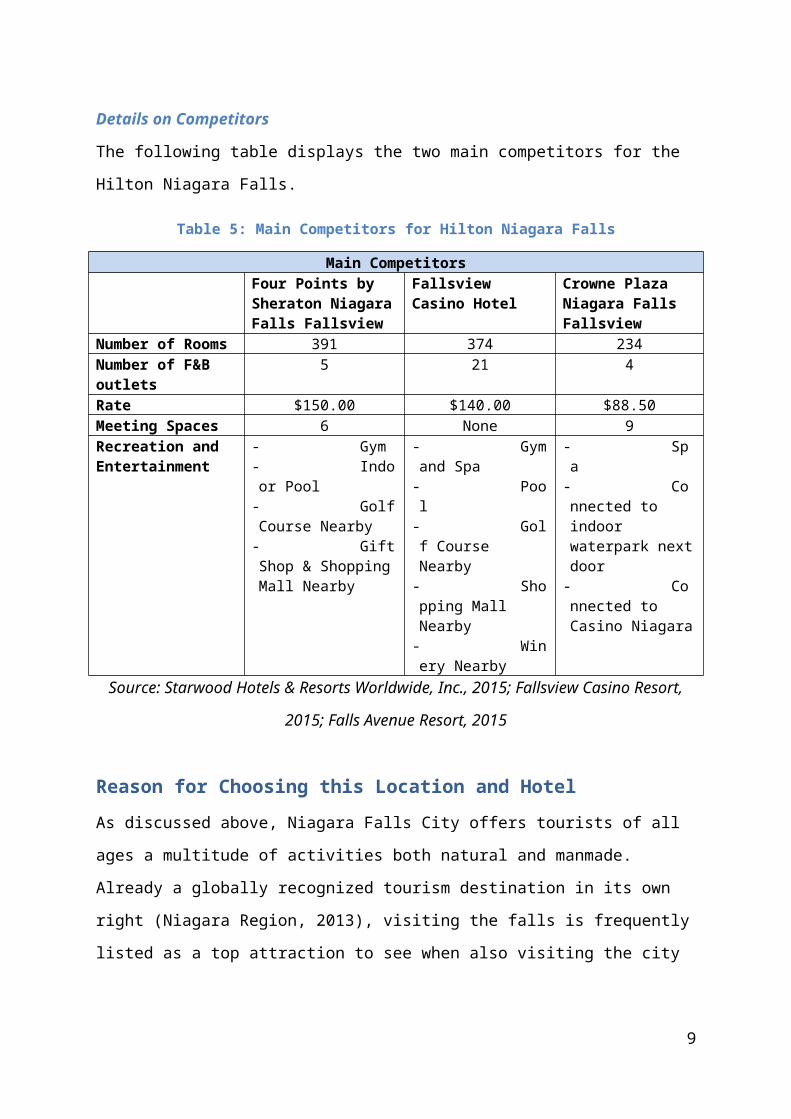

Details on Competitors

The following table displays the two main competitors for the Hilton Niagara Falls.

Table 5: Main Competitors for Hilton Niagara Falls

Main CompetitorsFour Points by Sheraton Niagara Falls Fallsview

Fallsview Casino Hotel

Crowne Plaza Niagara Falls Fallsview

Number of Rooms 391 374 234Number of F&B outlets

5 21 4

Rate $150.00 $140.00 $88.50Meeting Spaces 6 None 9Recreation and Entertainment

- Gym- Indoor Pool- Golf Course Nearby- Gift Shop & Shopping Mall Nearby

- Gym and Spa- Pool- Golf Course Nearby- Shopping Mall Nearby

- Winery Nearby

- Spa- Connected to indoor waterpark next door

- Connected to Casino Niagara

Source: Starwood Hotels & Resorts Worldwide, Inc., 2015; Fallsview Casino Resort, 2015;

Falls Avenue Resort, 2015

Reason for Choosing this Location and Hotel

As discussed above, Niagara Falls City offers tourists of all ages a multitude of activities both

natural and manmade. Already a globally recognized tourism destination in its own right

(Niagara Region, 2013), visiting the falls is frequently listed as a top attraction to see when

also visiting the city of Toronto, a major tourism destination for Canada as well, located only

a 2 hour journey away.

The city already welcomes 12 million tourists annually (Niagara Falls Tourism, 2015) 42% of

which are international visitors (Niagara Region, 2013). Visitors to the city bring in CAD 1.5

billion in annual receipts accounting for 10% of the province of Ontario’s annual tourism

receipts (Niagara Region, 2013). Over one-third of all visitors to Niagara Falls stay overnight

with 50% of overnight visitors staying in a hotel, motel or B&B (Niagara Falls Tourism,

2015). In addition to Niagara Falls already having a vibrant and diverse tourism industry,

choosing Niagara to invest in is strongly supported by the economic development plans of the

city. Tourism is listing among the 4 key areas that the Niagara Region will focus on for

continual development over the coming years (Niagara Region, 2013).

6

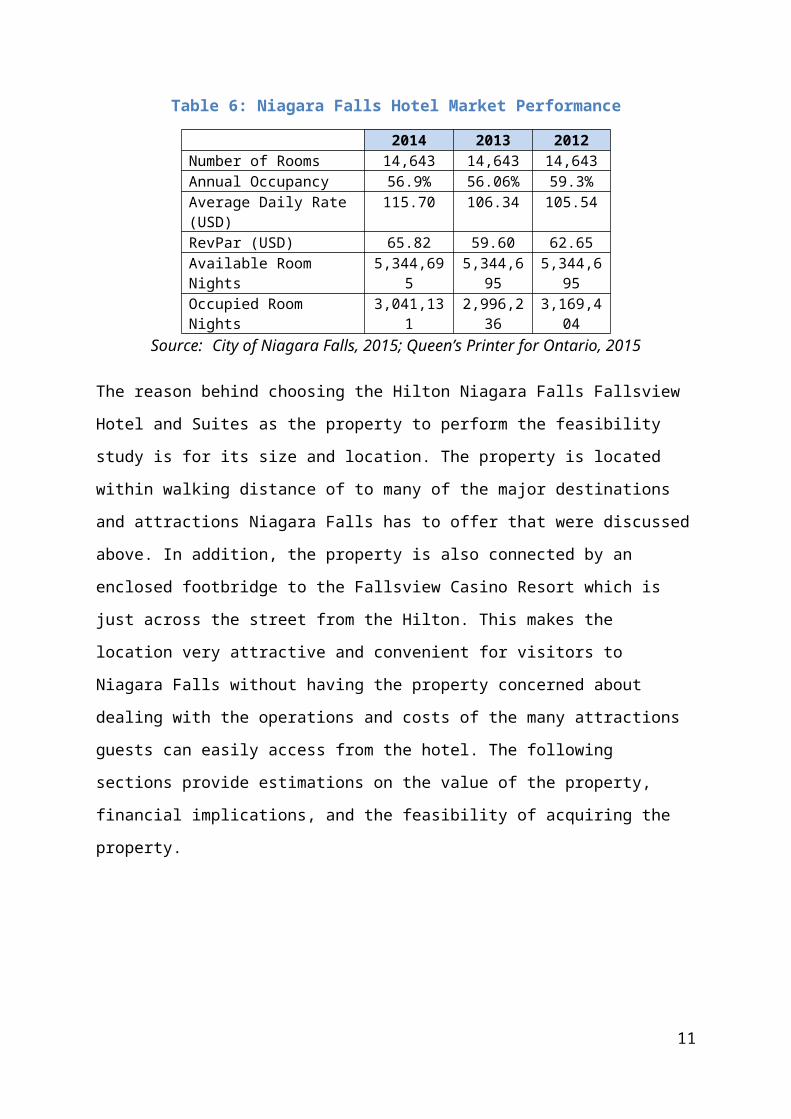

That being said however, no new construction of any hotel properties was seen in 2013 and

2014 in the Niagara Falls region (Colliers International, 2015). 2015 is also not expected to

see any new hotel opening, so the room count for the city will remain stable. Nationwide

there was a growth in RevPAR of 6.2% in 2014, which is anticipated to be a peaking point,

meaning that there will be a dampened gain in 2015. Taking this into account, average

growth in ADR in the property is expected to be around 0.5% over the coming years. The

following table gives a snapshot of the hotel market performance in Niagara Falls.

Table 6: Niagara Falls Hotel Market Performance

2014 2013 2012Number of Rooms 14,643 14,643 14,643Annual Occupancy 56.9% 56.06% 59.3%Average Daily Rate (USD) 115.70 106.34 105.54RevPar (USD) 65.82 59.60 62.65Available Room Nights 5,344,695 5,344,695 5,344,695Occupied Room Nights 3,041,131 2,996,236 3,169,404

Source: City of Niagara Falls, 2015; Queen’s Printer for Ontario, 2015

The reason behind choosing the Hilton Niagara Falls Fallsview Hotel and Suites as the

property to perform the feasibility study is for its size and location. The property is located

within walking distance of to many of the major destinations and attractions Niagara Falls has

to offer that were discussed above. In addition, the property is also connected by an enclosed

footbridge to the Fallsview Casino Resort which is just across the street from the Hilton. This

makes the location very attractive and convenient for visitors to Niagara Falls without having

the property concerned about dealing with the operations and costs of the many attractions

guests can easily access from the hotel. The following sections provide estimations on the

value of the property, financial implications, and the feasibility of acquiring the property.

7

Justifications

The following section provides justifications for the values used in conducting the feasibility

study. A table summarizing all the performance details can be found at the end of the section.

Average Daily Rate

The average daily rate in the Niagara Falls region was found to be USD 105.54 in 2012,

106.34 in 2013 and USD 115.70 in 2014 (City of Niagara Falls, 2015; Queen’s Printer for

Ontario, 2015). An average of these three rates was taken to estimate the ADR for Niagara

Falls in 2015, which calculates to USD 109.20. This will be the estimated probably ADR

used for the valuation of this property. USD 20 will be added and subtracted for the

optimistic and pessimistic scenarios respectively.

Occupancy Rates

Occupancy rates in Niagara Falls region were found to be 59.3% in 2012, 56.1% in 2013 and

56.9% in 2014 (City of Niagara Falls, 2015; Queen’s Printer for Ontario, 2015). As with the

ADR, an average of these three values was taken to estimate the occupancy for Niagara Falls

in 2015, which calculates to an occupancy percentage of 57.4%. This will be the estimated

probable occupancy percentage for the valuation of this property. 7% will be added and

subtracted for the optimistic and pessimistic scenarios respectively.

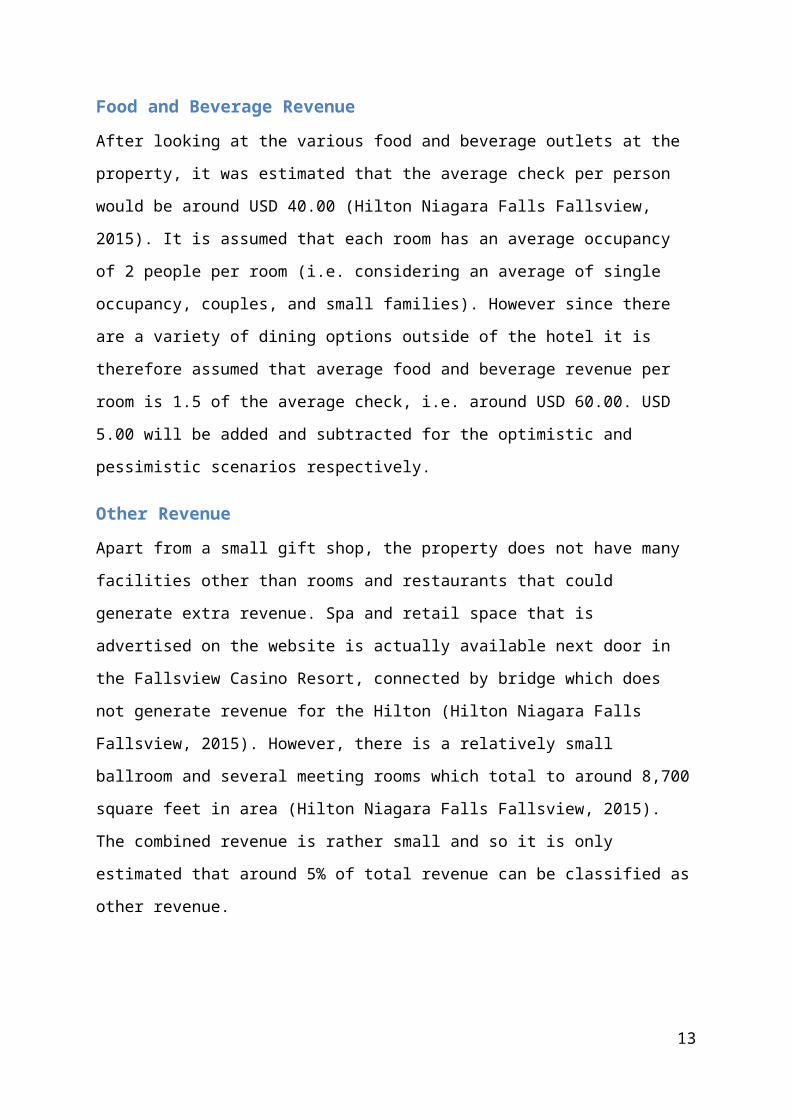

Food and Beverage Revenue

After looking at the various food and beverage outlets at the property, it was estimated that

the average check per person would be around USD 40.00 (Hilton Niagara Falls Fallsview,

2015). It is assumed that each room has an average occupancy of 2 people per room (i.e.

considering an average of single occupancy, couples, and small families). However since

there are a variety of dining options outside of the hotel it is therefore assumed that average

food and beverage revenue per room is 1.5 of the average check, i.e. around USD 60.00. USD

5.00 will be added and subtracted for the optimistic and pessimistic scenarios respectively.

Other Revenue

Apart from a small gift shop, the property does not have many facilities other than rooms and

restaurants that could generate extra revenue. Spa and retail space that is advertised on the

website is actually available next door in the Fallsview Casino Resort, connected by bridge

which does not generate revenue for the Hilton (Hilton Niagara Falls Fallsview, 2015).

8

However, there is a relatively small ballroom and several meeting rooms which total to

around 8,700 square feet in area (Hilton Niagara Falls Fallsview, 2015). The combined

revenue is rather small and so it is only estimated that around 5% of total revenue can be

classified as other revenue.

Departmental Expenses

Due to the similarities in culture, business processes, and economic ties, some calculations

and figures will be based on US or North American figures.

Rooms: according to Rushmore (2011) expenses for rooms varies across the globe. In India

they are quite low while in Europe they are quite high because of various regulations and

high labor costs. In North America and South America rooms department expenses are said

to be around 22%. For the valuation of this property, 22% rooms department expense will be

used.

Food and Beverage: as well according to Rushmore (2011) expenses for food and beverage

varies around the world. As with rooms, in India the costs are lower at around 45.5%. In the

United States the rate is around 68%. This same rate will be used for the valuation of this

property.

Other: according to an HVS report (Rushmore, 2011), other departmental expenses were at

around 29% of other revenue in the US. Therefore this same rate will be used for the

valuation of this property.

Undistributed Expenses

Undistributed operating expenses include expenses related to administrative and general

operations, sales and marketing, utilities (i.e. water and electricity), and final repairs and

maintenance. Findings from an HVS report based on a hotel in the US will be used to

calculate the percent total of the undistributed expenses as follows (Rushmore, 2011):

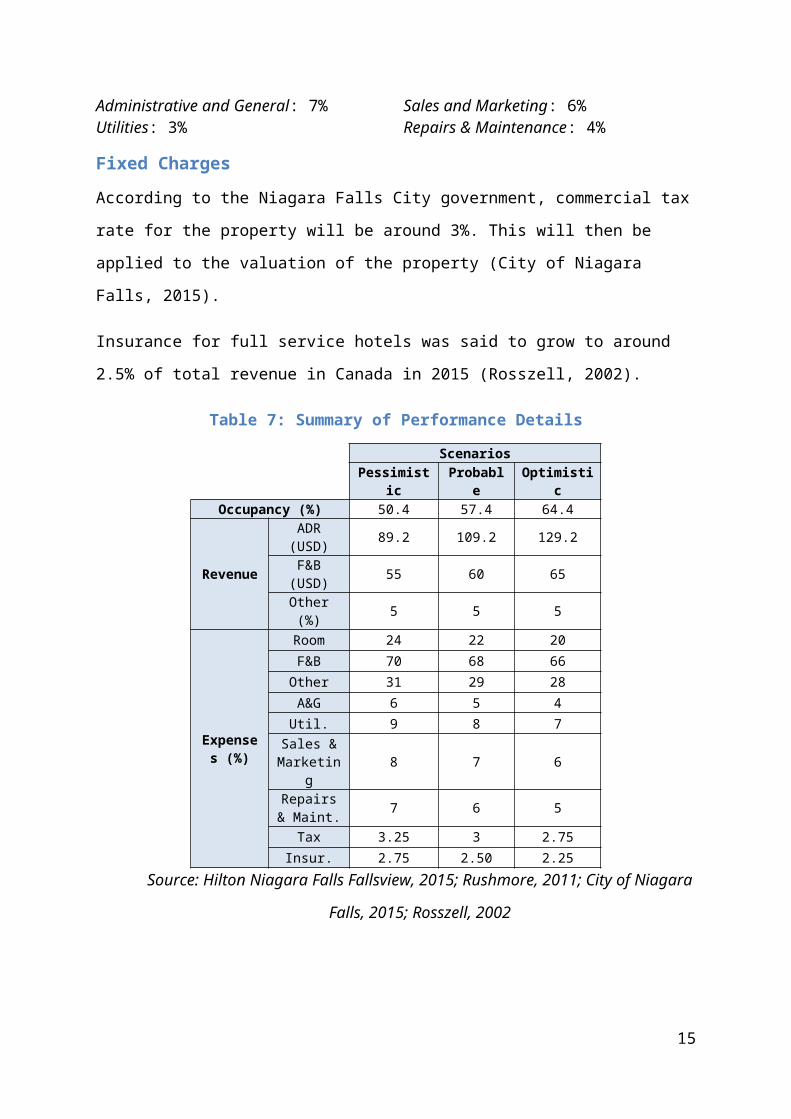

Administrative and General: 7% Sales and Marketing: 6%Utilities: 3% Repairs & Maintenance: 4%

Fixed Charges

According to the Niagara Falls City government, commercial tax rate for the property will be

around 3%. This will then be applied to the valuation of the property (City of Niagara Falls,

2015).

9

Insurance for full service hotels was said to grow to around 2.5% of total revenue in Canada

in 2015 (Rosszell, 2002).

Table 7: Summary of Performance Details

ScenariosPessimistic Probable Optimistic

Occupancy (%) 50.4 57.4 64.4

Revenue

ADR (USD) 89.2 109.2 129.2

F&B (USD) 55 60 65Other (%) 5 5 5

Expenses (%)

Room 24 22 20F&B 70 68 66Other 31 29 28A&G 6 5 4Util. 9 8 7

Sales & Marketing 8 7 6

Repairs & Maint. 7 6 5

Tax 3.25 3 2.75Insur. 2.75 2.50 2.25

Source: Hilton Niagara Falls Fallsview, 2015; Rushmore, 2011; City of Niagara

Falls, 2015; Rosszell, 2002

10

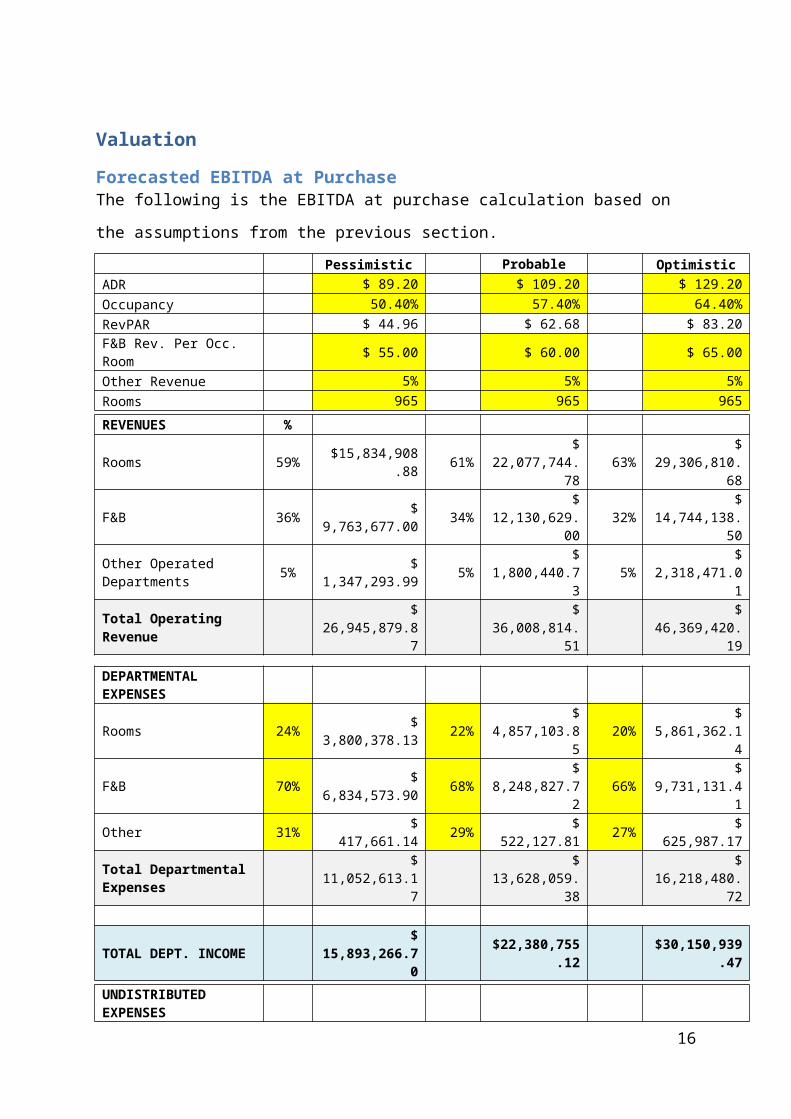

Valuation

Forecasted EBITDA at PurchaseThe following is the EBITDA at purchase calculation based on the assumptions from the

previous section.

Pessimistic Probable OptimisticADR $ 89.20 $ 109.20 $ 129.20

Occupancy 50.40% 57.40% 64.40%

RevPAR $ 44.96 $ 62.68 $ 83.20

F&B Rev. Per Occ. Room $ 55.00 $ 60.00 $ 65.00

Other Revenue 5% 5% 5%

Rooms 965 965 965

REVENUES %Rooms 59% $15,834,908.88 61% $ 22,077,744.78 63% $ 29,306,810.68F&B 36% $ 9,763,677.00 34% $ 12,130,629.00 32% $ 14,744,138.50Other Operated Departments 5% $ 1,347,293.99 5% $ 1,800,440.73 5% $ 2,318,471.01Total Operating Revenue $ 26,945,879.87 $ 36,008,814.51 $ 46,369,420.19

DEPARTMENTAL EXPENSESRooms 24% $ 3,800,378.13 22% $ 4,857,103.85 20% $ 5,861,362.14F&B 70% $ 6,834,573.90 68% $ 8,248,827.72 66% $ 9,731,131.41Other 31% $ 417,661.14 29% $ 522,127.81 27% $ 625,987.17Total Departmental Expenses $ 11,052,613.17 $ 13,628,059.38 $ 16,218,480.72

TOTAL DEPT. INCOME $ 15,893,266.70 $22,380,755.12 $30,150,939.47

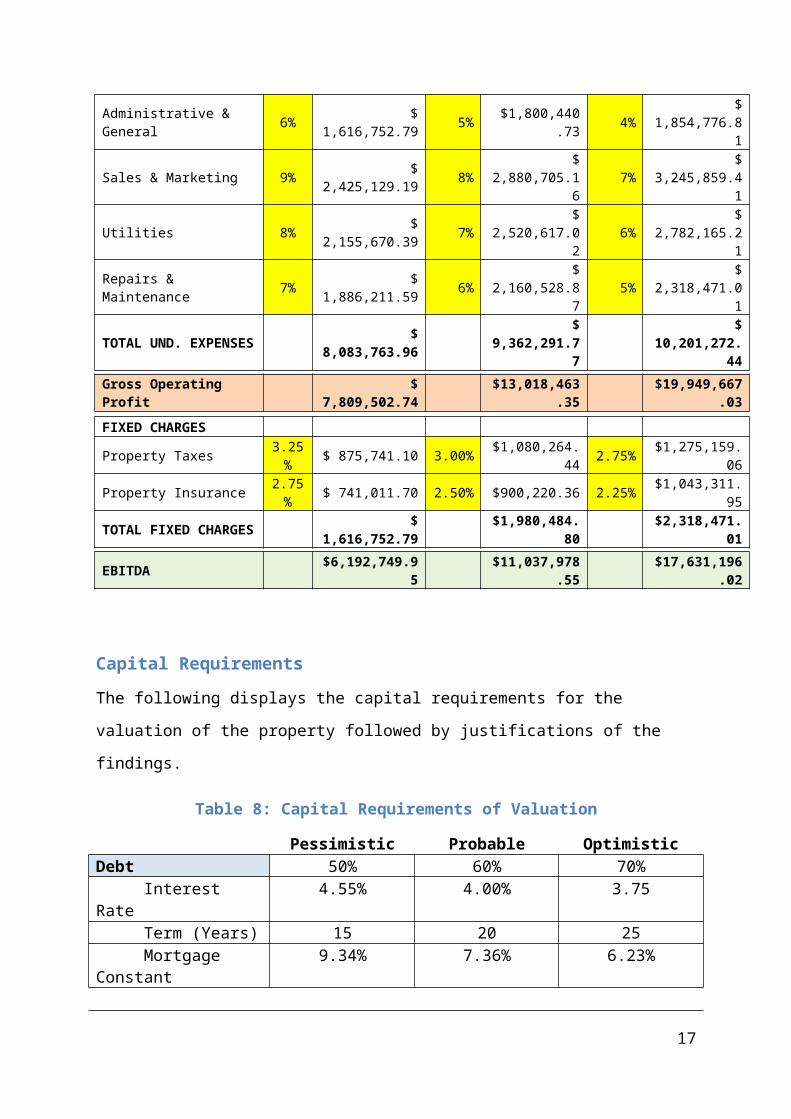

UNDISTRIBUTED EXPENSESAdministrative & General 6% $ 1,616,752.79 5% $1,800,440.73 4% $ 1,854,776.81Sales & Marketing 9% $ 2,425,129.19 8% $ 2,880,705.16 7% $ 3,245,859.41Utilities 8% $ 2,155,670.39 7% $ 2,520,617.02 6% $ 2,782,165.21Repairs & Maintenance 7% $ 1,886,211.59 6% $ 2,160,528.87 5% $ 2,318,471.01TOTAL UND. EXPENSES $ 8,083,763.96 $ 9,362,291.77 $ 10,201,272.44

Gross Operating Profit $ 7,809,502.74 $13,018,463.35 $19,949,667.03

FIXED CHARGESProperty Taxes 3.25% $ 875,741.10 3.00% $1,080,264.44 2.75% $1,275,159.06Property Insurance 2.75% $ 741,011.70 2.50% $900,220.36 2.25% $1,043,311.95TOTAL FIXED CHARGES $ 1,616,752.79 $1,980,484.80 $2,318,471.01

EBITDA $6,192,749.95 $11,037,978.55 $17,631,196.02

11

Capital Requirements

The following displays the capital requirements for the valuation of the property followed by

justifications of the findings.

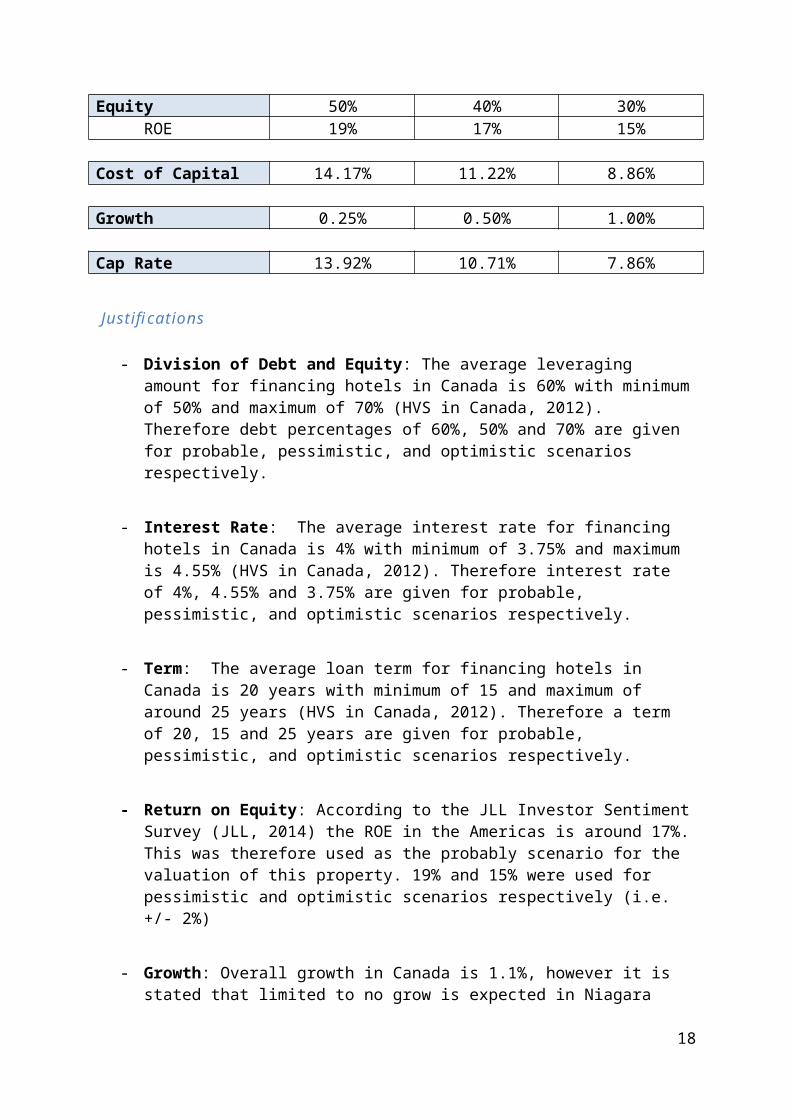

Table 8: Capital Requirements of Valuation

Pessimistic Probable OptimisticDebt 50% 60% 70%

Interest Rate 4.55% 4.00% 3.75Term (Years) 15 20 25Mortgage

Constant9.34% 7.36% 6.23%

Equity 50% 40% 30%ROE 19% 17% 15%

Cost of Capital 14.17% 11.22% 8.86%

Growth 0.25% 0.50% 1.00%

Cap Rate 13.92% 10.71% 7.86%

Justifications

- Division of Debt and Equity: The average leveraging amount for financing hotels in Canada is 60% with minimum of 50% and maximum of 70% (HVS in Canada, 2012). Therefore debt percentages of 60%, 50% and 70% are given for probable, pessimistic, and optimistic scenarios respectively.

- Interest Rate: The average interest rate for financing hotels in Canada is 4% with minimum of 3.75% and maximum is 4.55% (HVS in Canada, 2012). Therefore interest rate of 4%, 4.55% and 3.75% are given for probable, pessimistic, and optimistic scenarios respectively.

- Term: The average loan term for financing hotels in Canada is 20 years with minimum of 15 and maximum of around 25 years (HVS in Canada, 2012). Therefore a term of 20, 15 and 25 years are given for probable, pessimistic, and optimistic scenarios respectively.

- Return on Equity: According to the JLL Investor Sentiment Survey (JLL, 2014) the ROE in the Americas is around 17%. This was therefore used as the probably scenario for the valuation of this property. 19% and 15% were used for pessimistic and optimistic scenarios respectively (i.e. +/- 2%)

12

- Growth: Overall growth in Canada is 1.1%, however it is stated that limited to no grow is expected in Niagara Falls so the value of growth has been estimated as 0.50%, 0.25% and 1.00% for probable, pessimistic and optimistic scenarios (Colliers International, 2014).

Valuation Using Income Method

The following table shows the valuation of the property using the Direct Capitalization

Method of valuation with the data presented and justified from above. The rounded number

under the probable scenario will be used as the valuation of the hotel. The property is

therefore valued at USD 103,015,00.00 at a per room value of USD 106,751.30. The average

per room value in Niagara Falls (which includes properties of all ranges) was USD 63,117

(HVS in Canada, 2014). It is therefore assumed that the valuation for the property is

appropriate as the property is in the upper category range.

Table 9: Valuation of Property

Pessimistic Probable OptimisticEBITDA $ 6,192,749.95 $ 11,037,978.55 $ 17,631,196.02Cap Rate 13.92% 10.71% 7.86%

Value $ 44,482,687.86 $ 103,015,178.71 $ 224,223,663.92Rounded $ 44,483,000.00 $ 103,015,000.00 $ 224,224,000.00

Per Room $ 46,096.37 $ 106,751.30 $ 232,356.48

Chosen Value Probable (Rounded) $ 103,015,000.00

Debt 60% $ 61,809,000.00Equity 40% $ 41,206,000.00

13

Operational Structures

The following section looks at the EBITDA at the stabilized year with probable, pessimistic,

optimistic scenarios under four different management structures: owner-operated,

management contract, franchise, and management contract with franchise. Descriptions of the

four operational structures are provided followed by the EBITDA calculations for each

structure under the three scenarios. All details on ADR, occupancy, expenses and fees for

each structure is highlighted in the table after at the end of the descriptions.

The stabilized year is predicted to be at year 3 after purchase. As already stated, the growth

in the region is assumed to be around 0.5%. This will make an ADR in the stabilized year to

be USD 110.29 under and F&B revenue per room in the stabilized year USD 60.60 in the

probable scenario. Occupancy is expected to drop slightly upon acquisition, however will

then return to at EBITDA purchase amount of 57.4% for probable.

Descriptions of Operational Structures

Owner-Operated

This is when the hotel is owned and operated by the owner themselves and having full control

over the operation and keeps all the profit. However, the owner would then have to manage

the operations, which could be more efficiently done by somebody else and one would not be

able to access the market like an already established brand would. There are no fees in this

structure; however expected ADR and occupancy levels will also not be as high as they

potentially could. In addition, expenses will be the highest out of all three structures

(Rushmore, O’Neill & Rushmore, 2012).

As such ADR and occupancy at the stabilized year will be set at area averages with the

expected growth and expenses will be kept the same as with the EBITDA at purchase.

Management Contract

A management contract is between an operator or a management company and an owner.

This is when the operator takes complete responsibility of the hotel operations and can reduce

costs and improve revenues. However, they may not take control over the policies and

procedures and is financially responsible of the property. In this situation, the income less the

management fee, goes directly to the owner (Rushmore et al., 2012).

14

Fees with this structure include a basic fee (% of total operating revenue) and an incentive fee

(% of gross operating profit). Basic fee is set at 2.9% and incentive fee is set at 10% based on

HVS statistics for upper upscale properties (Detlefsen & Glodz, 2013). ADR and occupancy

at the stabilized year will be set at area averages with the expected growth. However, since

the hotel would be run more efficiently, departmental expenses will be reduced by 2%.

Franchise

This happens when a contract is signed between a hotel company and an owner that is

looking to take the name, trademarks and some or all services offered by the hotel company.

This is a good way to go about purchasing a property because it gives the owner instant

reputation and identity in the market, dependent on the property one would also have the rates

already decided due to the classification of the hotel, one would get access to the central

reservation, advertisements, manuals, purchasing and loyalty programs. However, should, at

any point in time, the property fail, the hotel company can withdraw the franchise and the

owner assumes all liabilities (Rushmore et al., 2012).

Fees with this structure include a franchise fee (% of total operating revenue). Franchise fee

is set at 12% based on HVS report specifying the royalty, loyalty, marketing, reservation and

miscellaneous fees (Rushmore & Bagley, 2014). ADR and occupancy at the stabilized year

will be set higher than at area averages with the expected growth as the brand recognition and

reservation system will improve the figures. However expenses will be kept the same as with

the EBITDA at purchase.

Management Contract with Franchise (Manchise)

In this structure the elements of a management contract and a franchise are combined. By

matching the goals, objectives, property, location and standards. One would use the name of

the company brand as that is better for lenders and to reach the targeted market. However,

they are a financial risk to owners due to the dual fees and the franchisor would decide on the

operating standards (Rushmore et al., 2012).

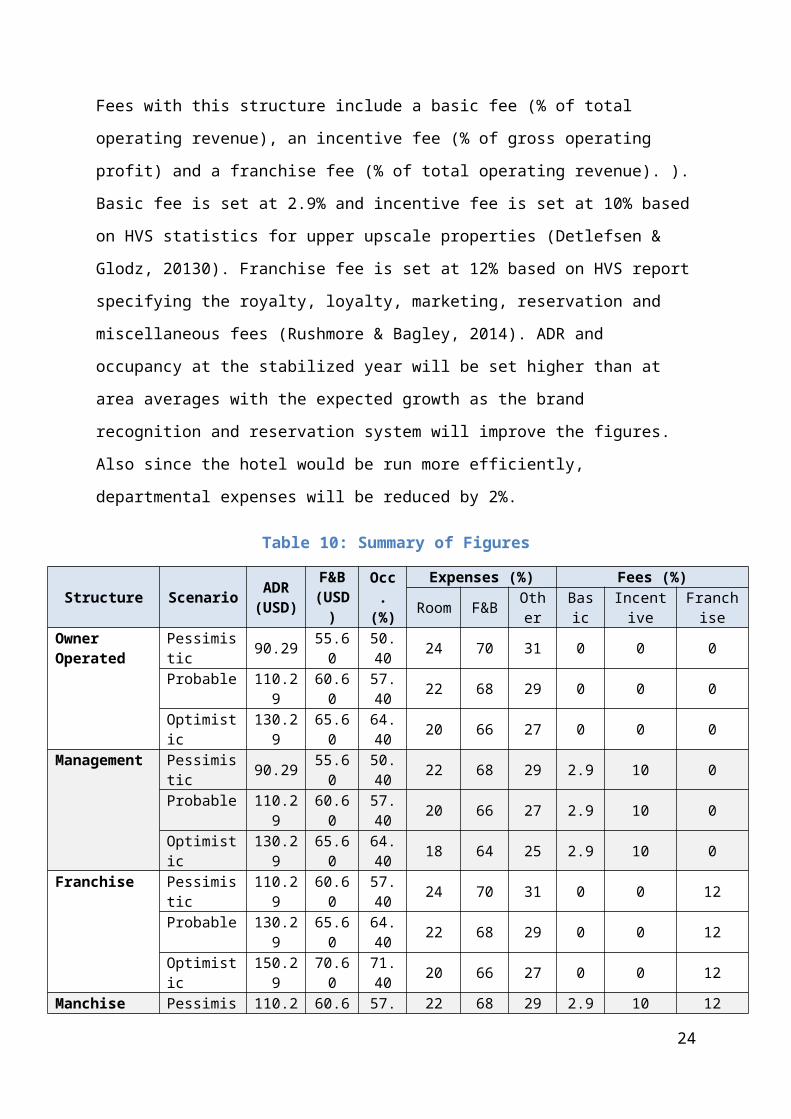

Fees with this structure include a basic fee (% of total operating revenue), an incentive fee (%

of gross operating profit) and a franchise fee (% of total operating revenue). ). Basic fee is set

at 2.9% and incentive fee is set at 10% based on HVS statistics for upper upscale properties

(Detlefsen & Glodz, 20130). Franchise fee is set at 12% based on HVS report specifying the

royalty, loyalty, marketing, reservation and miscellaneous fees (Rushmore & Bagley, 2014).

ADR and occupancy at the stabilized year will be set higher than at area averages with the

15

expected growth as the brand recognition and reservation system will improve the figures.

Also since the hotel would be run more efficiently, departmental expenses will be reduced by

2%.

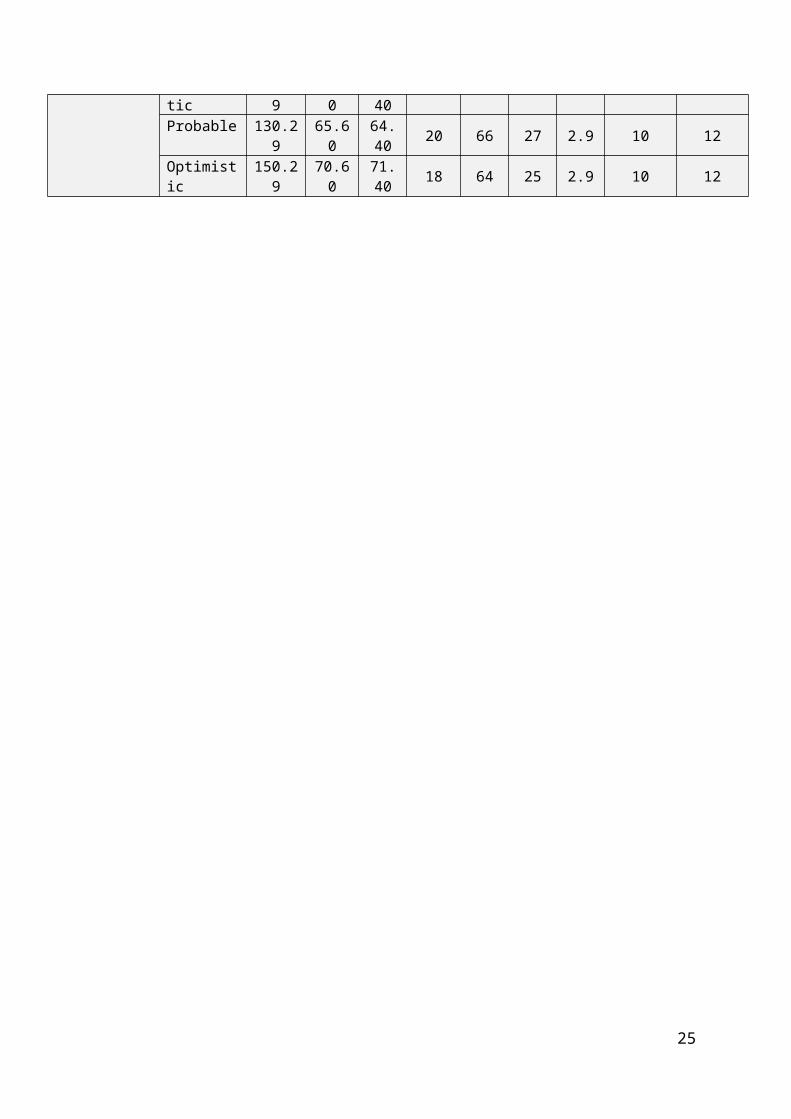

Table 10: Summary of Figures

Structure Scenario ADR (USD)

F&B (USD)

Occ. (%)

Expenses (%) Fees (%)Room F&B Other Basic Incentive Franchise

Owner Operated

Pessimistic 90.29 55.60 50.40 24 70 31 0 0 0Probable 110.29 60.60 57.40 22 68 29 0 0 0Optimistic 130.29 65.60 64.40 20 66 27 0 0 0

Management Pessimistic 90.29 55.60 50.40 22 68 29 2.9 10 0Probable 110.29 60.60 57.40 20 66 27 2.9 10 0Optimistic 130.29 65.60 64.40 18 64 25 2.9 10 0

Franchise Pessimistic 110.29 60.60 57.40 24 70 31 0 0 12Probable 130.29 65.60 64.40 22 68 29 0 0 12Optimistic 150.29 70.60 71.40 20 66 27 0 0 12

Manchise Pessimistic 110.29 60.60 57.40 22 68 29 2.9 10 12Probable 130.29 65.60 64.40 20 66 27 2.9 10 12Optimistic 150.29 70.60 71.40 18 64 25 2.9 10 12

16

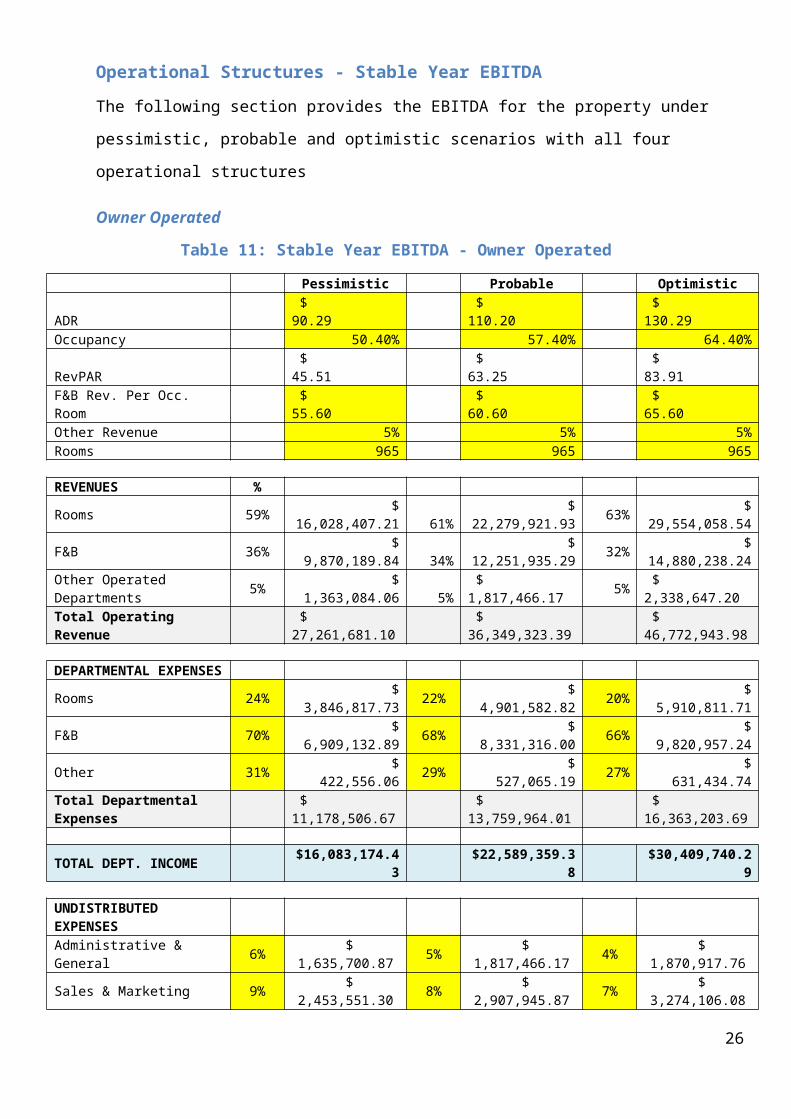

Operational Structures - Stable Year EBITDA

The following section provides the EBITDA for the property under pessimistic, probable and

optimistic scenarios with all four operational structures

Owner Operated

Table 11: Stable Year EBITDA - Owner Operated

Pessimistic Probable OptimisticADR $ 90.29 $ 110.20 $ 130.29Occupancy 50.40% 57.40% 64.40%RevPAR $ 45.51 $ 63.25 $ 83.91F&B Rev. Per Occ. Room $ 55.60 $ 60.60 $ 65.60Other Revenue 5% 5% 5%Rooms 965 965 965

REVENUES %Rooms 59% $ 16,028,407.21 61% $ 22,279,921.93 63% $ 29,554,058.54F&B 36% $ 9,870,189.84 34% $ 12,251,935.29 32% $ 14,880,238.24Other Operated Departments 5% $ 1,363,084.06 5% $ 1,817,466.17 5% $ 2,338,647.20Total Operating Revenue $ 27,261,681.10 $ 36,349,323.39 $ 46,772,943.98

DEPARTMENTAL EXPENSESRooms 24% $ 3,846,817.73 22% $ 4,901,582.82 20% $ 5,910,811.71F&B 70% $ 6,909,132.89 68% $ 8,331,316.00 66% $ 9,820,957.24Other 31% $ 422,556.06 29% $ 527,065.19 27% $ 631,434.74Total Departmental Expenses $ 11,178,506.67 $ 13,759,964.01 $ 16,363,203.69

TOTAL DEPT. INCOME $16,083,174.43 $22,589,359.38 $30,409,740.29

UNDISTRIBUTED EXPENSESAdministrative & General 6% $ 1,635,700.87 5% $ 1,817,466.17 4% $ 1,870,917.76Sales & Marketing 9% $ 2,453,551.30 8% $ 2,907,945.87 7% $ 3,274,106.08Utilities 8% $ 2,180,934.49 7% $ 2,544,452.64 6% $ 2,806,376.64Repairs & Maintenance 7% $ 1,908,317.68 6% $ 2,180,959.40 5% $ 2,338,647.20TOTAL UND. EXPENSES $ 8,178,504.33 $ 9,450,824.08 $ 10,290,047.68

Gross Operating Profit $7,904,670.10 $13,138,535.30 $20,119,692.61

FeesBasic Fee 0% $ - $ - $ -Incentive Fee 0% $ - $ - $ -Franchise Fee 0% $ - $ - $ -Total Fees $ - $ - $ -

FIXED CHARGESProperty Taxes 3.25% $886,004.64 3.00% $1,090,479.70 2.75% $1,286,255.96Property Insurance 2.75% $749,696.23 2.50% $908,733.08 2.25% $1,052,391.24TOTAL FIXED CHARGES $1,635,700.87 $1,999,212.79 $2,338,647.20

EBITDA $6,268,969.23 $11,139,322.51 $17,781,045.42

17

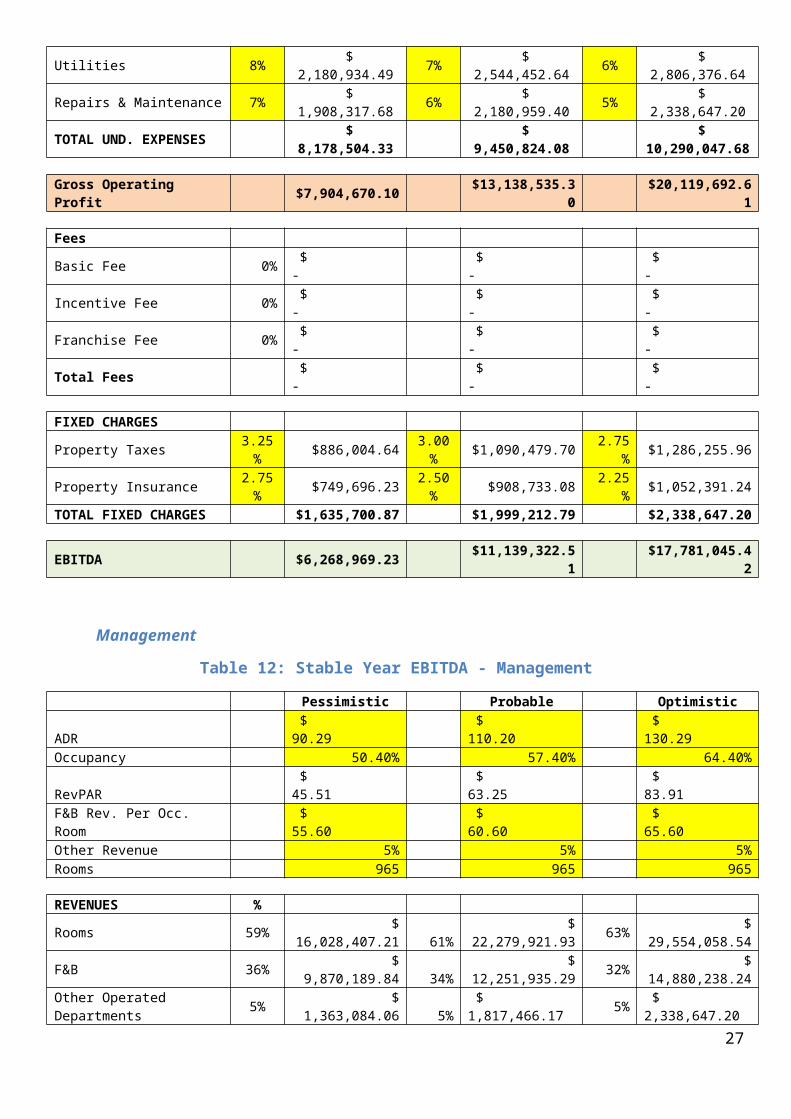

Management

Table 12: Stable Year EBITDA - Management

Pessimistic Probable OptimisticADR $ 90.29 $ 110.20 $ 130.29Occupancy 50.40% 57.40% 64.40%RevPAR $ 45.51 $ 63.25 $ 83.91F&B Rev. Per Occ. Room $ 55.60 $ 60.60 $ 65.60Other Revenue 5% 5% 5%Rooms 965 965 965

REVENUES %Rooms 59% $ 16,028,407.21 61% $ 22,279,921.93 63% $ 29,554,058.54F&B 36% $ 9,870,189.84 34% $ 12,251,935.29 32% $ 14,880,238.24Other Operated Departments 5% $ 1,363,084.06 5% $ 1,817,466.17 5% $ 2,338,647.20Total Operating Revenue $ 27,261,681.10 $ 36,349,323.39 $ 46,772,943.98

DEPARTMENTAL EXPENSESRooms 22% $ 3,526,249.59 20% $ 4,455,984.39 29% $ 8,570,676.98F&B 68% $ 6,711,729.09 66% $ 8,086,277.29 64% $ 9,523,352.47Other 29% $ 395,294.38 27% $ 490,715.87 25% $ 584,661.80Total Departmental Expenses $ 10,633,273.05 $ 13,032,977.54 $ 18,678,691.25

TOTAL DEPT. INCOME $16,628,408.05 $23,316,345.85 $28,094,252.73

UNDISTRIBUTED EXPENSESAdministrative & General 6% $ 1,635,700.87 5% $ 1,817,466.17 4% $ 1,870,917.76Sales & Marketing 9% $ 2,453,551.30 8% $ 2,907,945.87 7% $ 3,274,106.08Utilities 8% $ 2,180,934.49 7% $ 2,544,452.64 6% $ 2,806,376.64Repairs & Maintenance 7% $ 1,908,317.68 6% $ 2,180,959.40 5% $ 2,338,647.20TOTAL UND. EXPENSES $ 8,178,504.33 $ 9,450,824.08 $ 10,290,047.68

Gross Operating Profit $8,449,903.72 $13,865,521.77 $17,804,205.05

FeesBasic Fee 3% $ 790,588.75 $ 1,054,130.38 $ 1,356,415.38Incentive Fee 10% $ 844,990.37 $ 1,386,552.18 $ 1,780,420.51Franchise Fee 0% $ - $ - $ -Total Fees $ 1,635,579.12 $ 2,440,682.55 $ 3,136,835.88

FIXED CHARGESProperty Taxes 3.25% $886,004.64 3.00% $1,090,479.70 2.75% $1,286,255.96Property Insurance 2.75% $749,696.23 2.50% $908,733.08 2.25% $1,052,391.24TOTAL FIXED CHARGES $1,635,700.87 $1,999,212.79 $2,338,647.20

EBITDA $5,178,623.73 $9,425,626.42 $12,328,721.97

18

Franchise

Table 13: Stable Year EBITDA - Franchise

Pessimistic Probable OptimisticADR $ 110.29 $ 130.29 $ 150.29Occupancy 57.4% 64.40% 71.40%RevPAR $ 63.31 $ 83.91 $ 107.31F&B Rev. Per Occ. Room $ 60.60 $ 65.60 $ 70.60Other Revenue 5% 5% 5%Rooms 965 965 965

REVENUES %Rooms 61% $ 22,298,117.87 63% $ 29,554,058.54 65% $ 37,796,229.21F&B 34% $ 12,251,935.29 32% $ 14,880,238.24 30% $ 17,755,098.69Other Operated Departments 5% $ 1,818,423.85 5% $ 2,338,647.20 5% $ 2,923,754.10Total Operating Revenue $ 36,368,477.01 $ 46,772,943.98 $ 58,475,082.00

DEPARTMENTAL EXPENSESRooms 24% $ 5,351,548.29 22% $ 6,501,892.88 20% $ 7,559,245.84F&B 70% $ 8,576,354.70 68% $ 10,118,562.00 66% $ 11,718,365.14Other 31% $ 563,711.39 29% $ 678,207.69 27% $ 789,413.61Total Departmental Expenses $ 14,491,614.39 $ 17,298,662.57 $ 20,067,024.58

TOTAL DEPT. INCOME $21,876,862.63 $29,474,281.41 $38,408,057.41

UNDISTRIBUTED EXPENSESAdministrative & General 6% $ 2,182,108.62 5% $ 2,338,647.20 4% $ 2,339,003.28Sales & Marketing 9% $ 3,273,162.93 8% $ 3,741,835.52 7% $ 4,093,255.74Utilities 8% $ 2,909,478.16 7% $ 3,274,106.08 6% $ 3,508,504.92Repairs & Maintenance 7% $ 2,545,793.39 6% $ 2,806,376.64 5% $ 2,923,754.10TOTAL UND. EXPENSES $ 10,910,543.10 $ 12,160,965.43 $ 12,864,518.04

Gross Operating Profit $10,966,319.52 $17,313,315.98 $25,543,539.37

FeesBasic Fee 0% $ - $ - $ -Incentive Fee 0% $ - $ - $ -Franchise Fee 12% $ 4,364,217.24 $ 5,612,753.28 $ 7,017,009.84Total Fees $ 4,364,217.24 $ 5,612,753.28 $ 7,017,009.84

FIXED CHARGESProperty Taxes 3.25% $1,181,975.50 3.00% $1,403,188.32 2.75% $1,608,064.75Property Insurance 2.75% $1,000,133.12 2.50% $1,169,323.60 2.25% $1,315,689.34TOTAL FIXED CHARGES $2,182,108.62 $2,572,511.92 $2,923,754.10

EBITDA $4,419,993.66 $9,128,050.78 $15,602,775.43

19

Manchise

Table 14: Stable Year EBITDA - Manchise

Pessimistic Probable OptimisticADR $ 110.29 $ 130.29 $ 150.29Occupancy 57.4% 64.40% 71.40%RevPAR $ 63.31 $ 83.91 $ 107.31F&B Rev. Per Occ. Room $ 60.60 $ 65.60 $ 70.60Other Revenue 5% 5% 5%Rooms 965 965 965

REVENUES %Rooms 61% $ 22,298,117.87 63% $ 29,554,058.54 65% $ 37,796,229.21F&B 34% $ 12,251,935.29 32% $ 14,880,238.24 30% $ 17,755,098.69Other Operated Departments 5% $ 1,818,423.85 5% $ 2,338,647.20 5% $ 2,923,754.10Total Operating Revenue $ 36,368,477.01 $ 46,772,943.98 $ 58,475,082.00

DEPARTMENTAL EXPENSESRooms 22% $ 4,905,585.93 20% $ 5,910,811.71 29% $ 10,960,906.47F&B 68% $ 8,331,316.00 66% $ 9,820,957.24 64% $ 11,363,263.16Other 29% $ 527,342.92 27% $ 631,434.74 25% $ 730,938.52Total Departmental Expenses $ 13,764,244.85 $ 16,363,203.69 $ 23,055,108.16

TOTAL DEPT. INCOME $22,604,232.17 $30,409,740.29 $35,419,973.84

UNDISTRIBUTED EXPENSESAdministrative & General 6% $ 2,182,108.62 5% $ 2,338,647.20 4% $ 2,339,003.28Sales & Marketing 9% $ 3,273,162.93 8% $ 3,741,835.52 7% $ 4,093,255.74Utilities 8% $ 2,909,478.16 7% $ 3,274,106.08 6% $ 3,508,504.92Repairs & Maintenance 7% $ 2,545,793.39 6% $ 2,806,376.64 5% $ 2,923,754.10TOTAL UND. EXPENSES $ 10,910,543.10 $ 12,160,965.43 $ 12,864,518.04

Gross Operating Profit $11,693,689.06 $18,248,774.85 $22,555,455.80

FeesBasic Fee 3% $ 1,054,685.83 $ 1,356,415.38 $ 1,695,777.38Incentive Fee 10% $ 1,169,368.91 $ 1,824,877.49 $ 2,255,545.58Franchise Fee 12% $ 4,364,217.24 $ 5,612,753.28 $ 7,017,009.84Total Fees $ 6,588,271.98 $ 8,794,046.14 $ 10,968,332.80

FIXED CHARGESProperty Taxes 3.25% $1,181,975.50 3.00% $1,403,188.32 2.75% $1,608,064.75Property Insurance 2.75% $1,000,133.12 2.50% $1,169,323.60 2.25% $1,315,689.34TOTAL FIXED CHARGES $2,182,108.62 $2,572,511.92 $2,923,754.10

EBITDA $2,923,308.46 $6,882,216.80 $8,663,368.90

20

Stable Year EBITDA Summary

The following table displays the EBITDA at the stable year for all four management

structures under each scenario. From the table it is evident that under the probable scenario,

the owner operated structure has produced the greatest EBIDTA. This management structure

will therefore be used for further analysis.

Table 15: Summary of EBITDA

EBITDA Pessimistic Probable OptimisticOwner Operated $ 6,268,969.23 $ 11,139,322.51 $ 17,781,045.42Management $ 5,178,623.73 $ 9,425,626.42 $ 12,328,721.97Franchise $ 4,419,993.66 $ 9,128,050.78 $ 8,663,368.90Branded $ 2,923,308.46 $ 6,882,216.80 $ 8,663,368.90

21

11 Year EBITDA Forecast

The following table displays the 11 year EBITDA calculation with an owner operated structure based on the details provided earlier in the report.

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Year 11ADR $ 109.20 $ 109.75 $ 110.29 $ 110.85 $ 111.40 $ 111.96 $ 112.52 $ 13.08 $ 13.65 $ 114.21 $ 114.78Occupancy 55.4% 56.4% 57.4% 57.4% 57.4% 57.4% 57.4% 57.4% 57.4% 57.4% 57.4%RevPAR $ 60.50 $ 61.90 $ 63.31 $ 63.63 $ 63.94 $ 64.26 $ 64.58 $ 64.91 $ 65.23 $ 65.56 $ 65.89F&B Rev. Per Occ. Room $ 60.00 $ 60.30 $ 60.60 $ 60.90 $ 61.21 $ 61.52 $ 61.82 $ 62.13 $ 62.44 $ 62.75 $ 63.07Other Revenue 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5%Rooms 965 965 965 965 965 965 965 965 965 965 965

Revenue Growth 0.50%

REVENUESRooms 61% $ 21,308,485.38 $ 21,801,580.66 $ 22,299,074.17 $ 22,410,569.54 $ 22,522,622.39 $ 22,635,235.50 $ 22,748,411.68 $ 22,862,153.74 $ 22,976,464.51 $ 23,091,346.83 $ 23,206,803.56F&B 34% $ 11,707,959.00 $ 11,978,890.47 $ 12,252,238.56 $ 12,313,499.75 $ 12,375,067.25 $ 12,436,942.58 $ 12,499,127.30 $ 12,561,622.93 $ 12,624,431.05 $ 12,687,553.20 12,750,990.97Other Operated Departments 5% $ 1,737,707.60 $ 1,777,919.53 $ 1,818,490.14 $ 1,827,582.59 $ 1,836,720.51 $ 1,845,904.11 $ 1,855,133.63 $ 1,864,409.30 $ 1,873,731.34 $ ,883,100.00 $ 1,892,515.50Total Operating Revenue $ 34,754,151.98 $ 5,558,390.66 $ 36,369,802.87 $ 36,551,651.89 $ 36,734,410.14 $ 36,918,082.20 $ 37,102,672.61 $ 37,288,185.97 $ 37,474,626.90 $ 7,662,000.03 $ 37,850,310.03

DEPARTMENTAL EXPENSESRooms 22% $ 4,687,866.78 $ 4,796,347.74 $ 4,905,796.32 $ 4,930,325.30 $ 4,954,976.93 $ 4,979,751.81 $ 5,004,650.57 $ 5,029,673.82 $ 5,054,822.19 $ 5,080,096.30 $ 5,105,496.78F&B 68% $ 7,961,412.12 $ 8,145,645.52 $ 8,331,522.22 $ 8,373,179.83 $ 8,415,045.73 $ 8,457,120.96 $ 8,499,406.56 $ 8,541,903.59 $ 8,584,613.11 $ 8,627,536.18 $ 8,670,673.86Other 29% $ 503,935.20 $ 515,596.66 $ 527,362.14 $ 529,998.95 $ 532,648.95 $ 535,312.19 $ 537,988.75 $ 540,678.70 $ 543,382.09 $ 546,099.00 $ 548,829.50Total Departmental Expenses $ 13,153,214.11 $ 13,457,589.93 $ 13,764,680.68 $ 13,833,504.08 $ 13,902,671.60 $ 13,972,184.96 $ 14,042,045.88 $ 14,112,256.11 $ 14,182,817.39 $ 14,253,731.48 $ 14,325,000.14

TOTAL DEPT. INCOME $21,600,937.87 $22,100,800.73 $22,605,122.19 $22,718,147.80 $22,831,738.54 $22,945,897.24 $23,060,626.72 $23,175,929.86 $23,291,809.51 $23,408,268.55 $23,525,309.90

UNDISTRIBUTED EXPENSESAdministrative & General 5% $ 1,737,707.60 $ 1,777,919.53 $ 1,818,490.14 $ 1,827,582.59 $ 1,836,720.51 $ 1,845,904.11 $ 1,855,133.63 $ 1,864,409.30 $ 1,873,731.34 $ 1,883,100.00 $ 1,892,515.50Sales & Marketing 8% $ 2,780,332.16 $ 2,844,671.25 $ 2,909,584.23 $ 2,924,132.15 $ 2,938,752.81 $ 2,953,446.58 $ 2,968,213.81 $ 2,983,054.88 $ 2,997,970.15 $ 3,012,960.00 $ 3,028,024.80Utilities 7% $ 2,432,790.64 $ 2,489,087.35 $ 2,545,886.20 $ 2,558,615.63 $ 2,571,408.71 $ 2,584,265.75 $ 2,597,187.08 $ 2,610,173.02 $ 2,623,223.88 $ 2,636,340.00 $ 2,649,521.70Repairs & Maintenance 6% $ 2,085,249.12 $ 2,133,503.44 $ 2,182,188.17 $ 2,193,099.11 $ 2,204,064.61 $ 2,215,084.93 $ 2,226,160.36 $ 2,237,291.16 $ 2,248,477.61 $ 2,259,720.00 $ 2,271,018.60TOTAL UND. EXPENSES $ 9,036,079.51 $ 9,245,181.57 $ 9,456,148.75 $ 9,503,429.49 $ 9,550,946.64 $ 9,598,701.37 $ 9,646,694.88 $ 9,694,928.35 $ 9,743,402.99 $ 9,792,120.01 $ 9,841,080.61

Gross Operating Profit $12,564,858.36 $12,855,619.16 $13,148,973.45 $13,214,718.31 $13,280,791.91 $13,347,195.87 $13,413,931.84 $13,481,001.50 $13,548,406.51 $13,616,148.54 $13,684,229.29

FIXED CHARGESProperty Taxes 3.00% $1,042,624.56 $1,066,751.72 $1,091,094.09 $1,096,549.56 $1,102,032.30 $1,107,542.47 $1,113,080.18 $1,118,645.58 $1,124,238.81 $1,129,860.00 $1,135,509.30Property Insurance 2.50% $868,853.80 $888,959.77 $909,245.07 $913,791.30 $918,360.25 $922,952.05 $927,566.82 $932,204.65 $936,865.67 $941,550.00 $946,257.75TOTAL FIXED CHARGES $1,911,478.36 $1,955,711.49 $2,000,339.16 $2,010,340.85 $2,020,392.56 $2,030,494.52 $2,040,646.99 $2,050,850.23 $2,061,104.48 $2,071,410.00 $2,081,767.05

EBITDA $10,653,380.00 $10,899,907.67 $11,148,634.29 $11,204,377.46 $11,260,399.35 $11,316,701.34 $11,373,284.85 $11,430,151.28 $11,487,302.03 $11,544,738.54 $11,602,462.23

22

Reversion Value

The reversion value for the property (i.e. the value at which you can sell it) is calculated by

taking the year 11 EBITDA after purchase and the terminal cap rate (i.e. initial cap rate + 2%

using the Rushmore method). As such, the reversion value after the 10 year holding period is

USD 91,251,000 (rounded). This means that the year 10 EBITDA would actually be USD

102,796,000 (rounded). The below table summarizes the findings.

Table 16: Reversion Value and Actual Year 10 EBITDA

Initial Cap Rate 10.71%Terminal Cap Rate 12.71%Reversion Value $91,250,876.17Year 10 EBITDA $102,795,614.71

Estimated Amortization

Based on the findings in the previous sections, the following tables display the estimated

amortization details with a 10 year holding period.

Table 17: Amortization Details

Debt Amount $ 61,809,000.00Rate 4.00%Term 20Payment $ 4,548,014Holding Period 10Mortgage Balance $ 36,888,471

Table 18: Amortization Schedule

Period Payment Interest Principal Paid Ending Balance1 $4,548,014 $ 2,472,360 $2,075,654 $ 59,733,3462 $4,548,014 $ 2,389,334 $2,158,681 $ 57,574,6653 $4,548,014 $ 2,302,987 $2,245,028 $ 55,329,6374 $4,548,014 $ 2,213,185 $2,334,829 $ 52,994,8085 $4,548,014 $ 2,119,792 $2,428,222 $ 50,566,5866 $4,548,014 $ 2,022,663 $2,525,351 $ 48,041,2357 $4,548,014 $ 1,921,649 $2,626,365 $ 45,414,8708 $4,548,014 $ 1,816,595 $2,731,420 $ 42,683,4519 $4,548,014 $ 1,707,338 $2,840,676 $ 39,842,77410 $4,548,014 $ 1,593,711 $2,954,303 $ 36,888,471

23

Depreciation of the Property

For this property the building, FF&E and land is estimated to be worth 70%, 20%, and 10%

respectively of the total value. Straight line depreciation will be completed with a useful life

of 39 years and 10 years for the building and FF&E respectively. Based on the valuation of

the property done in the previous section and the above details, the total annual depreciation

for the property is USD 3,909,287.18. The table below shows the details of the depreciation

for the property.

Table 19: Depreciation of the Property

Value $ 103,015,000.00 Useful Life Annual DepreciationBuilding 70% $ 72,110,500.00 39 $ 1,848,987.18FF&E 20% $ 20,603,000.00 10 $ 2,060,300.00Land 10%

Total $ 3,909,287.18

24

Cash Flow of the Property

The following table displays the estimated cash flow of the property within the 10 year holding period. It is followed by a table that then looks at

the total year 10 cash flow based on the remaining mortgage balance.

Table 20: 10 Year Cash Flow

Year 1 2 3 4 5 6 7 8 9 10EBITDA $ 10,653,380 $ 10,899,908 $ 11,148,634 $ 11,204,377 $ 11,260,399 $ 11,316,701 $ 11,373,285 $ 11,430,151 $ 11,487,302 $ 11,544,739Depreciation $ (3,909,287) $ (3,909,287) $ (3,909,287) $ (3,909,287) $ (3,909,287) $ (3,909,287) $ (3,909,287) $ (3,909,287) $ (3,909,287) $ (3,909,287)Interest $ (2,472,360) $ (2,389,334) $ (2,302,987) $ (2,213,185) $ (2,119,792) $ (2,022,663) $ (1,921,649) $ (1,816,595) $ (1,707,338) $ (1,593,711)EBT $ 4,271,733 $ 4,601,287 $ 4,936,361 $ 5,081,905 $ 5,231,320 $ 5,384,751 $ 5,542,348 $ 5,704,269 $ 5,870,677 $ 6,041,740Tax (30%) $ 1,281,520 $ 1,380,386 $ 1,480,908 $ 1,524,571 $ 1,569,396 $ 1,615,425 $ 1,662,704 $ 1,711,281 $ 1,761,203 $ 1,812,522NET INCOME $ 2,990,213 $ 3,220,901 $ 3,455,452 $ 3,557,333 $ 3,661,924 $ 3,769,326 $ 3,879,644 $ 3,992,989 $ 4,109,474 $ 4,229,218Depreciation $ 3,909,287 $ 3,909,287 $ 3,909,287 $ 3,909,287 $ 3,909,287 $ 3,909,287 $ 3,909,287 $ 3,909,287 $ 3,909,287 $ 3,909,287Principal Payment $ (2,075,654) $ (2,158,681) $ (2,245,028) $ (2,334,829) $ (2,428,222) $ (2,525,351) $ (2,626,365) $ (2,731,420) $ (2,840,676) $ (2,954,303)CASH FLOW $ 4,823,846 $ 4,971,507 $ 5,119,712 $ 5,131,792 $ 5,142,989 $ 5,153,262 $ 5,162,566 $ 5,170,856 $ 5,178,085 $ 5,184,202

Table 21: Actual Cash Flow Year 10

Reversion Value $ 91,250,876.17Mortgage Balance $ 36,888,470.85Proceeds to Equity $ 54,362,405.32

Year 10 Cash Flow $ 59,546,607.34

25

Feasibility of Property

Net Present Value (NPV) of Cash Flows

The following table displays the NPV of cash flow from property and cash flow to equity.

Table 22: NPV of Cash Flows

Year Cash Flow from Property Year Cash Flow to Equity0 $ (103,015,000.00) 0 $ (41,206,000.00)1 $ 10,653,380.00 1 $ 4,823,845.752 $ 10,899,907.67 2 $ 4,971,507.273 $ 11,148,634.29 3 $ 5,119,711.734 $ 11,204,377.46 4 $ 5,131,791.625 $ 11,260,399.35 5 $ 5,142,988.996 $ 11,316,701.34 6 $ 5,153,261.727 $ 11,373,284.85 7 $ 5,162,565.978 $ 11,430,151.28 8 $ 5,170,856.089 $ 11,487,302.03 9 $ 5,178,084.5810 $ 102,795,614.71 10 $ 59,546,607.34

Discount Rate 11.21% Discount Rate 17.00%NPV $ (6,385,562.28) NPV $ (6,320,411.15)IRR 10.12% IRR 13.95%

From the calculations under both conditions, we can see that NPV is negative with an IRR

lower than the discount rate.

Average Accounting Return (ARR)

The following table displays the ARR for the property

Table 23: ARR for Property

Total Net Income $ 36,866,473Average Net Income $ 3,686,647Total Investment $ 103,015,000

ARR 3.58%

26

Payback Period

The following tables display the payback period for overall property and equity cash flows as

well as at discounted cash flows. Cash flow from property is set at a discount rate of 11.21%

while cash flow to equity is set at 17%.

Table 24: Payback for Property

Year Cash Flow from Property Discounted Rates Accumulated Payback Payback Tipping Point0 $ (103,015,000.00)

1 $ 10,653,380.00 $9,579,093.73 $9,579,093.73 ($93,435,906.27)

2 $ 10,899,907.67 $8,812,453.30 $18,391,547.04 ($84,623,452.96)

3 $ 11,148,634.29 $8,104,620.50 $26,496,167.53 ($76,518,832.47)

4 $ 11,204,377.46 $7,323,787.76 $33,819,955.29 ($69,195,044.71)

5 $ 11,260,399.35 $6,618,183.68 $40,438,138.98 ($62,576,861.02)

6 $ 11,316,701.34 $5,980,560.43 $46,418,699.41 ($56,596,300.59)

7 $ 11,373,284.85 $5,404,368.44 $51,823,067.85 ($51,191,932.15)

8 $ 11,430,151.28 $4,883,689.18 $56,706,757.03 ($46,308,242.97)

9 $ 11,487,302.03 $4,413,174.32 $61,119,931.35 ($41,895,068.65)

10 $ 102,795,614.71 $35,509,506.37 $96,629,437.72 ($6,385,562.28)

Table 25: Payback from Equity

Year Cash Flow to Equity Discounted Rates Accumulated Pay Back Pay Back Tipping Point0 $ (41,206,000.00)

1 $ 4,823,845.75 $4,122,945.08 $4,122,945.08 ($37,083,054.92)

2 $ 4,971,507.27 $3,631,753.43 $7,754,698.51 ($33,451,301.49)

3 $ 5,119,711.73 $3,196,597.26 $10,951,295.77 ($30,254,704.23)

4 $ 5,131,791.62 $2,738,580.84 $13,689,876.61 ($27,516,123.39)

5 $ 5,142,988.99 $2,345,774.64 $16,035,651.25 ($25,170,348.75)

6 $ 5,153,261.72 $2,008,940.29 $18,044,591.54 ($23,161,408.46)

7 $ 5,162,565.97 $1,720,143.12 $19,764,734.66 ($21,441,265.34)

8 $ 5,170,856.08 $1,472,568.67 $21,237,303.33 ($19,968,696.67)

9 $ 5,178,084.58 $1,260,365.14 $22,497,668.47 ($18,708,331.53)

10 $ 59,546,607.34 $12,387,920.37 $34,885,588.85 ($6,320,411.15)

From the calculations it is evident that under both cash flow from property and cash flow to

equity, the payback period is longer than the 10 year holding period with discounted values.

There is a balance of over six million dollars in both cases.

27

Discussion

Niagara Falls City, Ontario, Canada is a very popular tourist destination that makes up around

10% of the province of Ontario’s annual tourism receipts. Located along the USA-Canada

border, the city has an extensive transportation network leading in and out connecting

Niagara Falls to the rest of Canada, the US and the globe. In addition, Niagara Falls has a

wide portfolio of entertainment, dining options, and natural beauty not the mention the falls

themselves. With the city focused on developing the tourism industry, one would think that

Niagara Falls would be an ideal location to invest in a property.

The chosen hotel to perform the feasibility study, Hilton Niagara Falls Fallsview Hotel and

Suites, also seems like an ideal property to invest in as it is located near the falls and near

many attractions as well as being directly connected to the Fallsview Casino by an enclosed

foot bridge. This allows the property to benefit from being a convenient location for guests to

stay at without the need to be concerned about the operational requirements of these

attractions.

Upon reviewing current market conditions of Niagara Falls, it was estimated that the property

is worth USD 103,015,000. With further investigations, it was identified that under an owner

operated management structure, the property would generate the highest EBITDA out of all

four structures. Continued analysis revealed the anticipated cash flows from the property

based on a 0.50% growth rate and a stabilized occupancy rate of 57.4%. According to the net

present value calculations, it was revealed that the cash flow from the property and the cash

flow to equity at a discounted rate of 11.21% and 17.00% respectively would result in a

negative (-) NPV. Additionally, it was found that payback periods again for both cash flow

from property and cash flow to equity would be longer than the 10 year holding period of the

property.

These two findings indicate that under the current and forecasted market conditions,

acquiring the Hilton Niagara Falls Fallsview Hotel and Suites would not be feasible and

therefore it is not recommended to proceed with the investment.

Encouraging Project Feasibility

Should the investor proceed with the acquisition, there is a possibility to make the project a

feasible investment. Efforts to improve overall ADR in the property should be made as well

28

as an attempt to improve cost percentages for example by improving operational efficiency or

leasing out all food and beverage outlets and collecting rent from each unit. Additionally, the

revenues coming from other operated departments (i.e. the meeting and ballroom space)

could be improved.

However, even at the same market and operational conditions in this report, the project can

be made feasible overall by significantly improving occupancy levels. It is estimated that by

increasing occupancy to around 66% at the stabilized year, the project could become feasible.

However further investigation and analysis would need to be performed to support this

estimation.

Improving occupancy in the city can in fact be a collective effort by all business,

organizations, and municipal entities involved with tourism. Working together would indeed

improve the overall financial performance of the city as well as benefitting the economy,

creating more jobs, and various other economic and social factors. Overnight visitors were

found to be at one-third of total visitors to the city, which could be a result of the city having

a very well connected transportation network. As such, special campaigns to encourage more

overnight stays could be implemented. As well, special deals for hotel guests with various

attractions and entertainment destinations could be launched to encourage day visitors to stay

the night. As said, the increase in overnight visitors would surely not only benefit Niagara

Falls City but indeed potentially make the acquisition of the Hilton Niagara Falls Fallsview

Hotel and Suites a feasible project.

29

References

City of Niagara Falls. (2015). Niagara Falls Canada. Retrieved from

https://www.niagarafalls.ca/

Colliers International. (2014). 2014 Canadian hotel investment report. Toronto, CA: Author.

Retrieved from http://www.colliershotels.com/2014/CHIR/Colliers-2014CHIR.pdf

Colliers International. (2015). 2015 Canadian hotel investment report. Toronto, CA: Author.

Retrieved from http://www.colliershotels.com/reports/2015-canadian-hotel-

investment-report

Detlefsen, H. & Glodz, M. (2013, January). Historical trends hotel management contracts.

Chicago, US: HVS. Retrieved from EAHM Moodle Open-source learning platform

Falls Avenue Resort. (2015). Crowne Plaza Niagara Falls – Fallsview. Retrieved from

http://www.niagarafallscrowneplazahotel.com/

Fallsview Casino Resort. (2015). Retrieved from http://www.fallsviewcasinoresort.com/

Hilton Niagara Falls Fallsview. (2015). Retrieved from

https://www.niagarafallshilton.com/index.php

HVS in Canada. (2012, November). Canadian monthly lodging outlook – November 2012.

Toronto, CA: Author. Retrieved from http://www.hvs.com/article/6152/canadian-

monthly-lodging-outlook-november-2012/

HVS in Canada. (2014, October). 2014 Canadian hotel valuation index. Toronto, CA: Author.

Retrieved from http://www.hvs.com/article/7088/2014-canadian-hotel-valuation-

index/

JLL. (2014, June). Hotel investor sentiment survey. Chicago, US: Author. Retrieved from

EAHM Moodle Open-source learning platform

Niagara Convention & Civic Centre Inc. (2015). Scotia Bank Convention Centre. Retrieved

from http://www.fallsconventions.com/facility.html

Niagara Falls Live. (2015). Facts about Niagara Falls. Retrieved from

https://www.niagarafallslive.com/facts_about_niagara_falls.htm

30

Niagara Falls Tourism. (2015). Retrieved from http://www.niagarafallstourism.com/

Niagara Region. (2013). Economic growth strategy 2013-2015: Report to the public. ON,

Canada: Author. Retrieved from http://www.niagaraknowledgeexchange.com/wp-

content/uploads/sites/2/2014/05/Economic_Growth_Strategy_2013_2015.pdf

Queen’s Printer for Ontario. (2015). Historical statistics. Retrieved from

http://www.mtc.gov.on.ca/en/research/historicalstats/historical_statistics_tables.shtml

Rosszell, M. (2002). Hotel insurance premiums on the rise?. Retrieved from

http://www.hotel-online.com/News/PR2002_2nd/May02_CanadianLodgingOutlook.h

tml

Rushmore S. Jr. & Bagley, E. (2014). 2014 United States hotel franchise fee guide. NY,

USA: HVS. Retrieved from EAHM Moodle Open-source learning platform

Rushmore, S. (2011, November 2). Comparing same hotels across five regions. HVS Lodging

Hospitality. Retrieved from http://www.hvs.com/article/5529/comparing-same-hotel-

across-five-regions/

Rushmore, S., O’Neill, J.W. & Rushmore S. Jr. (2012). Hotel market analysis and valuation.

Chicago, US: Appraisal Institute

Starwood Hotels & Resorts Worldwide, Inc. (2015). Four Points by Sheraton Niagara Falls

Fallsview. Retrieved from

http://www.starwoodhotels.com/fourpoints/property/overview/index.html?

propertyID=3315

31