Embed Size (px)

Citation preview

Hotel Report

In Focus Provincial? Not in the slightest! The unnoticed destinations of Rostock-Warnemünde, Mainz, and Darmstadt

Edition November 2014

© INFINITY - fotolia.com

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 2

FairmasHotel Reportin cooperation with SolutionsDotWG

Index

Dear readers, 3

Oktober 2014 in comparison to the previous year 4

Fairmas Trendbarometer 8

In Focus 16

Disclaimer 29

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 3

FairmasHotel Reportin cooperation with SolutionsDotWG

Dear readers,

In this Fairmas Hotel Report, we examine the performance of German cities, on time and informatively. The

figures reveal the sensitive movements of the market - good and bad times between Hamburg and Munich.

But how do things look in those cities and towns beyond the major conurbations? Which factors are af-

fecting booking behaviour there? Our author Gabriele Kiesling, analyst at Solutions dot WG, examined the

potential of the cities of Rostock/Warnemünde, Mainz and Darmstadt. She has meticulously put together

the pieces of a puzzle made up of seasonal highlights, territorial conditions and peculiarities, school holiday

periods, trade fair events, concerts, and many other factors. It is a thoroughly exciting view of the first three

quarters of 2014 in these three cities, as well as a clear demonstration of how benchmarking helps in really

understanding the market.

A golden October? We now have the figures for October hot off the press and we look at the forecasts for

November, December and January in the Trendbarometer. Forecasts are mixed. The current Fairmas ana-

lysis figures show where hoteliers are looking forward to good times, as well as where thumbs are pointing

down.

The Fairmas Hotel Report team wishes you enjoyable reading, as well as a little time to breathe before the

end-of-the-year rush!

(Gabriele Kiessling & Nadine Kilian)

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 4

FairmasHotel Reportin cooperation with SolutionsDotWG

Oktober 2014 in comparison to the previous year1

A brief overview of hotel performances at selected German destinations:

1 All the figures (daily collected) quoted are comparisons with those for the previous year, rounded to full amounts Source: Fairmas GmbH/STR Global, Data as of 06.11.2014

Berlin

Occ: 82%, ADR: €94, RevPar: €77

Berlin can look back on a turbulent October. De-

mand for the long weekend starting on October 3

(the German national holiday) came very late. And

it almost seemed as if Berlin had overslept the IN-

TERGEO Conference. Demand only picked up in

late September but it was above average because

many events and conferences were held at the

same time. Many hoteliers had not been expecting

this and, when the demand arose, they were un-

able to achieve high-priced business for capacity

reasons. This problem seemed to continue throug-

hout the whole month, because the “belektro”

event (15 to 17 October 2014) and the 27th ECNP

Congress (18 to 21 October 2014) led to high de-

mand, although the expected ADR remained far

below the rates actually achieved. Tourist demand

during the school holidays and for the Festival of

Lights was also very healthy but with low prices. All

this meant that while occupancy indeed increased

(+ 5%), the ADR fell by 4% (RevPar: +0.4%).

Dresden

Occ: 73%, ADR: €71, RevPar: €52

A significant decline was expected in Dresden in

October. Last year, Semicon Europe took place

(7 to 10 October 2013), a trade show that provi-

des Dresden with good performance figures every

two years. Its presence was missed this year. The

school holidays in the second half of the month im-

peded conference and corporate business, so that

only two weeks were available solely for business

guests, who also provided too little exhibition and

convention business. In addition, the public holi-

days on 3 and 31 October 2013 had both been on

a Thursday, which set up excellent long weekends

and in each case the opportunity for a day’s busi-

ness at higher room rates than this year. So it is

not surprising that occupancy and room rates rose

by 0.1%, resulting in a 0.3% fall in RevPar, even

though the final figures were not quite as bad as

had previously been predicted.

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 5

FairmasHotel Reportin cooperation with SolutionsDotWG

Dusseldorf

Occ: 74%, ADR: €113, RevPar: €83

Performance in October was very poor with a col-

lapse in room rates (ADR: -26%), as well as high

losses (-2%) in occupancy. This year, far fewer

trade fairs took place in Dusseldorf than in 2013.

For instance, the “K” trade fair( held on a three-year

cycle) , as well as the Anuga in Cologne, which

last year led to very healthy overflow trade, were

absent this October. The “Aluminium” (7 to 10

September 2014) and “Glasstec” events (21 to 24

September 2014; held on a two-year cycle) that

took place this year and representing with seven

trade fair days, were unable to improve the overall

result. The Aluminium trade fair, in particular, was

far below expectations, with a 14% fall in RevPar

compared to 2012.

Hamburg

OCC: 83%, ADR: €110, RevPar: €92

The forecast for October was also positive, with

RevPar set to increase by 5%, due to a 3% rise in

ADR. The DGHO convention, which is held at rota-

ting venues, held from 10 to 14 October 2014, and

the Schmerzkongress, a specialist German medical

conference (22 to 25 October) contributed greatly

to the improved room rates. In addition, the Con-

gress of the „European Commodities Exchange“

from 16 to 17 attended and the two German soc-

cer cup matches at the end of the month (28 and

29 October 2014) assured very high demand in the

city. The “Hanseboot boat show”, this time from 25

October to 2 November, and this year’s Hamburg

“Summit” event, were also viewed positively by the

city’s hoteliers. Overall, October revealed a trend

towards major year-on-year improvements in the

MICE and Business sectors.

Frankfurt

OCC: 74%, ADR: €115, RevPar: €85

October was far worse in terms of performance

than last year. Room rates fell by 15%, which re-

sulted in a 14% drop in RevPar. This was largely

due to trade fairs being held on different dates than

before. Last year, the CPhl (a conference held at

different venues) took place from 22 to 24 October

2013. It had a particularly strong impact on room

rates and occupancy, leading to unusually good

business in an otherwise meagre autumn holiday

week in Frankfurt. As in 2013, the Frankfurt Buch-

messe (book fair) was held again this year (8 to

12 October 2014). However, competition is incre-

asing all the time due to the many new hotels that

are opening in Frankfurt, and it will no longer be

possible to achieve the same room rates. The 2%

increase in occupancy in October was influenced

positively by unexpected strikes and flight cancel-

lations, which generated additional layover busi-

ness in some hotels. As this year‘s German Day of

Unity public holiday on 3 October fell on a Friday

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 6

FairmasHotel Reportin cooperation with SolutionsDotWG

(in 2013 it had been on a Thursday), hoteliers in

Frankfurt were able to record a quite normal busi-

ness week, marked by an occupancy increase of

+14% compared to 3 October last year.

Cologne/Bonn

OCC: 73%, ADR: €104, RevPar: €76

Business in Cologne/Bonn was marked by a near-

dramatic downward trend. Occupancy fell by 4%

year-on-year. However, this was overshadowed by

the 21% decline in room rates and there was a

related 24% fall in RevPar. The main reason was

the absence of the ANUGA trade show, which only

takes place every two years, though it was not held

in 2014. No other trade event in the region can be

sold at such high prices. The “K” trade fair in Dus-

seldorf, which otherwise provides for much over-

flow business in Cologne, was not held this year,

either. The ORGATEC (21 to 25 October 2014) and

INTERMOT (1 to 5 October 2014) trade fairs did

nothing like enough to offset the losses. In addi-

tion, demand during the autumn school holidays

was significantly weaker than in recent years. De-

mand in the last week of October was still quite

strong, but did little to change the overall result.

Munich

OCC: 88%, ADR: €149, RevPar: €131

The Munich hoteliers were able to record a little

growth in October. As room rates had dropped

by 1%, a 3% increase occupancy led to a slight

(2%) growth in RevPar. Last year, there had been

one extra day of Oktoberfest in October; this time

around there was an additional day in September.

The second Oktoberfest week was slightly wor-

se than last year, particularly in the group sector.

Demand was low, resulting in a noticeable drop in

prices. In addition, there was a lack of large mee-

tings in the city in October, an absence which me-

ant that higher prices could not be achieved. The

InterAirport trade show, held every two years, was

missing this time. The autumn vacation in the last

week of October did nothing to boost rates in busi-

ness sector trade, but due to the holiday situation,

the week of school holidays still meant healthy de-

mand.

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 7

FairmasHotel Reportin cooperation with SolutionsDotWG

Overview of all destinations

2014 2013 Var. Var.% 2014 2013 Var. Var.% 2014 2013 Var. Var.%

Berlin 81,9% 78,4% 3,5 4,5% 93,9 97,7 -3,8 -3,9% 76,9 76,6 0,3 0,4%Cologne/Bonn 73,2% 76,6% -3,4 -4,4% 103,8 131,3 -27,5 -20,9% 76,0 100,6 -24,6 -24,5%Dresden 72,9% 73,0% -0,1 -0,1% 71,2 71,3 -0,1 -0,1% 51,9 52,0 -0,1 -0,3%Dusseldorf 73,6% 75,3% -1,7 -2,3% 113,4 159,7 -46,3 -29,0% 83,5 120,3 -36,8 -30,6%Frankfurt 74,2% 72,8% 1,4 1,9% 114,8 135,5 -20,7 -15,3% 85,2 98,6 -13,5 -13,6%Hamburg 83,2% 81,6% 1,6 2,0% 110,1 106,9 3,2 3,0% 91,6 87,2 4,4 5,0%Munich 88,0% 85,8% 2,2 2,6% 149,2 150,7 -1,5 -1,0% 131,3 129,3 2,0 1,5%

*Source: Fairmas GmbH / STR Global, based on data from participants with daily data entry, Data as of 03.11.2014

LegendOCC OccupancyADR Average Daily Rate (net rooms revenue)RevPar Revenue per available Room (net logistics revenue per available room)

Hotel Performance October 2014/2013*

Occupancy in % Average Daily Rate in Euro RevPar in Euro

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 8

FairmasHotel Reportin cooperation with SolutionsDotWG

Fig.1: Trendbarometer Berlin 2014 – Trend versus last year

4,4%

0,3%

3,1%

2,6%

0,0%

-1,3%

7,0%

0,3%

1,8%

November

December

January

Last Year

Occ ADR RevPAR

Source: Fairmas GmbH / Data as of 05.11.2014

Fairmas Trendbarometer

A peek into the future – in detail:

Berlin

In recent years, November has regularly been a

good month for business: hardly any public holi-

days and no school vacations, so that the month

offers the promise of four full business weeks. The

“SAP TechEd” conference (11 to 13 November

2014), the DGPPN Congress (26 to 29 November

2014), as well as even more business sector and

group travel than in recent years is boosting Berlin

hoteliers’ confidence. The advance booking situ-

ation has been very good for weeks now. A 4%

growth in occupancy is thought likely and room

rates are expected to grow by 3%, leading to a

7% rise in RevPar. Short-term individual pickup is

also expected, and even greater gains can be ex-

pected.

December promises no ma-

jor changes compared to

last year (Occ: +0.3%, ADR:

+0.0%, and RevPar: +0.3%).

Berlin hoteliers are still ex-

pecting good business sector

trade in the first two weeks

of the month. The number of

shopping and Christmas mar-

ket tourists will be around last

year‘s level. Demand for the

Advent weekends has always

been high in recent years. New Year‘s Eve and

the days before are highly promising because the

public holidays are very convenient for employees

this year; they can take the whole week off and yet

only use a few days of their vacation. Nonetheless,

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 9

FairmasHotel Reportin cooperation with SolutionsDotWG

December this year will be a classic low-season

month with little group sector trade and business

sales.

The beginning of 2015 promises to be positive. In

January, a 3% increase in occupancy is expected.

Employee-friendly long weekends at the end of the

year will ensure plenty of leisure business, but with

weaker room rates. Hoteliers have so far been cau-

tious about predicting the Green Week and Berlin

Fashion Week because both events were weaker

in 2014 than in previous years. Currently, it is esti-

mated that the average rate will fall by 1% (RevPar:

+ 2%), but advance bookings are well above last

year’s levels. It is hoped that the lower room rates

in the periods before and after the big events will

yet bring some extra leisure business in the city.

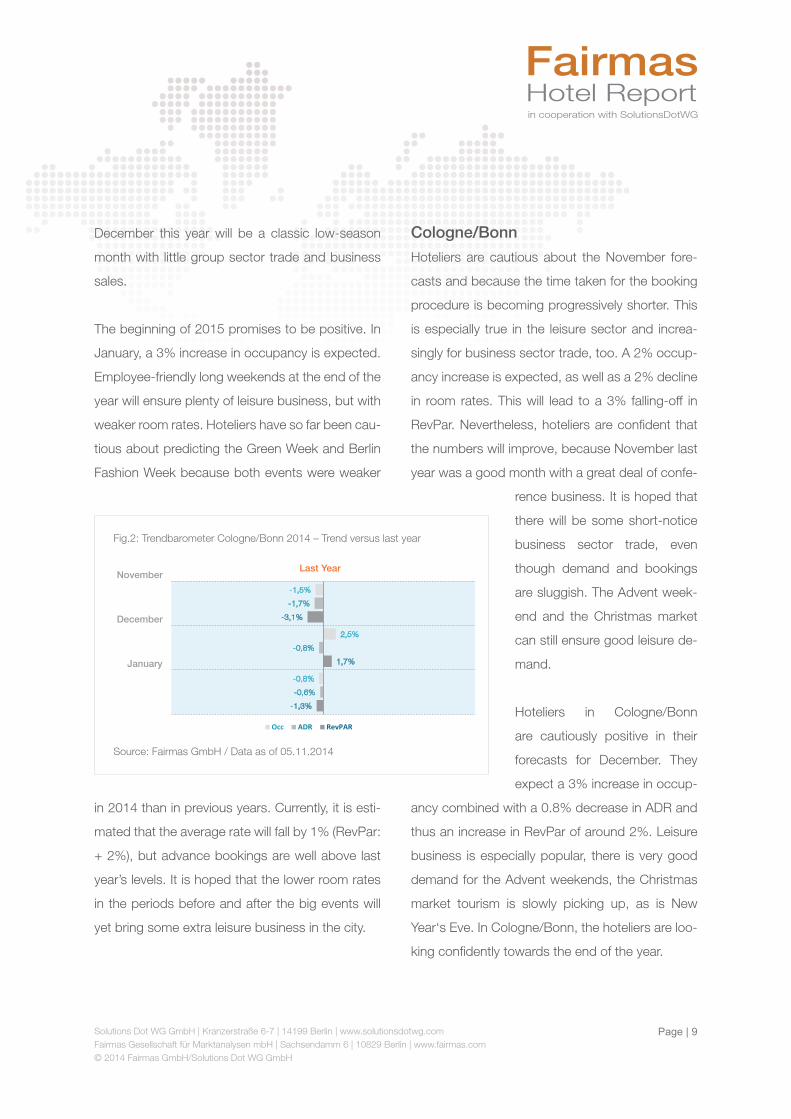

Cologne/Bonn

Hoteliers are cautious about the November fore-

casts and because the time taken for the booking

procedure is becoming progressively shorter. This

is especially true in the leisure sector and increa-

singly for business sector trade, too. A 2% occup-

ancy increase is expected, as well as a 2% decline

in room rates. This will lead to a 3% falling-off in

RevPar. Nevertheless, hoteliers are confident that

the numbers will improve, because November last

year was a good month with a great deal of confe-

rence business. It is hoped that

there will be some short-notice

business sector trade, even

though demand and bookings

are sluggish. The Advent week-

end and the Christmas market

can still ensure good leisure de-

mand.

Hoteliers in Cologne/Bonn

are cautiously positive in their

forecasts for December. They

expect a 3% increase in occup-

ancy combined with a 0.8% decrease in ADR and

thus an increase in RevPar of around 2%. Leisure

business is especially popular, there is very good

demand for the Advent weekends, the Christmas

market tourism is slowly picking up, as is New

Year‘s Eve. In Cologne/Bonn, the hoteliers are loo-

king confidently towards the end of the year.

Fig.2: Trendbarometer Cologne/Bonn 2014 – Trend versus last year

-1,5%

2,5%

-0,8%

-1,7%

-0,8%

-0,6%

-3,1%

1,7%

-1,3%

November

December

Last Year

Occ ADR RevPAR

January

Source: Fairmas GmbH / Data as of 05.11.2014

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 10

FairmasHotel Reportin cooperation with SolutionsDotWG

Cologne/Bonn expects a slow start to the New

Year. January is predicted to be slightly down. Oc-

cupancy is expected to decline by 0.8% and room

rates by 0.6%. RevPar will thus be 1% down. This

January, there was no ISM (the next one will be

held on 1 to 4 February 2015). The nights with the

greatest demand are in 2015 are in February, while

this year, the trade fair only took place in January

(26 to 29 January 2014). So far, bookings in the

first week of January are still

very poor. Many hotels are

trying to attract leisure sector

guests to the city by offering

low room rates.

Dresden

Hoteliers in Dresden expect

a very positive November.

Events include the “Jazztagen”

jazz festival, the “Unity.Dres-

den.Night”, the CYNETART

Festival, and the Striezelmarkt,

which opens its gates on 27 November 2014.

Things are happening in the city this autumn. The

Advent weekends before Christmas are generally

well booked in Dresden, and the Striezelmarkt

event is extremely well attended. The figures for

November are boosted by the fact that the first day

of Advent falls on 30 November this year. Prelimi-

nary booking levels for the first weekend of Advent

are already very promising. However, it remains to

be seen whether the positive forecasts (Occ: up

by 5%, ADR plus 0.4% and RevPar up 5%) are

justified because bookings are, as always, made

at short notice.

Still, the forecast for December is rather more cau-

tious. Occupancy is expected to fall by almost 6%,

though room rates will rise by 5%, resulting in a 1%

decline in RevPar. Since the fourth day of Advent

is so close to Christmas, it will be hard to sell it

to leisure sector guests. Nevertheless, the Advent

weekends prior to Christmas are usually times of

high demand. New Year‘s Eve is also looking good

for Dresden, as is the tradition. Hoteliers are tigh-

tening the price screw, so that room rates for the

Advent weekends are significantly higher than in

Fig.3: Trendbarometer Dresden 2014 – Trend versus last year

4,8%

-5,5%

10,0%

0,4%

4,9%

0,2%

5,2%

-0,9%

10,1%

November

December

January

Last Year

Occ ADR RevPAR

Source: Fairmas GmbH / Data as of 05.11.2014

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 11

FairmasHotel Reportin cooperation with SolutionsDotWG

recent years. However, while this is perhaps so-

mewhat at the expense of occupancy, the average

rate remains positive.

There are very positive expectations for the start of

the New Year in Dresden. Occupancy is expected

to increase by 10%, though room rates will virtually

stagnate, with a tiny increase of just 0.2%. Thus,

a RevPar increase of 10% is expected in January.

Due to the employee-friendly timing of the school

holidays at the turn of the year, and the fact that the

school holidays take up more of January than was

the case this year, hoteliers are expecting strong

leisure-sector business in January. In general, ho-

teliers in Dresden are cautiously optimistic about

the New Year.

Dusseldorf

The forecast for November predicted dismal pro-

spects for hoteliers in Dusseldorf (Occ down 5%,

ADR-5%, and RevPar-10%). There have been fe-

wer inquiries for events so far. In addition, the “A+A”

trade fair, which takes place every other year, will

be absent in 2014. Last year, it was accompanied

by high room rates. Furthermore, the important

annual “Medica” trade show (12 to 14 October

2014), with four trade fair days, will hardly be able

to counteract the overall poor

performance. It also remains to

be seen whether the result can

be improved. In November, due

to increasingly short-term boo-

king behaviour, it will also be

seen whether the results can be

corrected upwards.

There will be no trade fairs in

the city in December, as was

also the case at this time last

year. Dusseldorf Hoteliers ex-

pect a 5% decline in occupan-

cy, though a minor increase in ADR of around 4%,

and a 1% fall in RevPar. The savings by corporate

clients and reduced demands in the meeting and

conference sector due to more stringent compli-

ance measures are increasingly showing their ne-

gative effects on the Dusseldorf hotel trade.

Fig.4: Trendbarometer Dusseldorf 2014 – Trend versus last year

-5,3%

-4,7%

-2,0%

-5,3%

3,8%

0,0%

-10,4%

-1,0%

-2,0%

November

December

Last Year

Occ ADR RevPAR

January

Source: Fairmas GmbH / Data as of 05.11.2014

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 12

FairmasHotel Reportin cooperation with SolutionsDotWG

Nevertheless, the first three weeks of December

are business weeks that are easy to sell. There is

usually also good demand over the weekends in

the run-up to Christmas, so that occupancy and

room rates might well rise because leisure boo-

kings in particular are being made at very short

notice.

So far, January also looks set to be a troubled

month for hoteliers in Dusseldorf (RevPar down

2%). Thus, many Düsseldorf hotels are recording

a major fall in the volume of meeting and busi-

ness overnights. (Occ: down 2 %). A more specific

statement on the January forecast can be expec-

ted from mid-November. An improvement in occu-

pancy and room rates due to short-term corporate

bookings may yet be expected, as so far, the boo-

king situation is still very subdued and many corpo-

rate customers are simply keeping their requests

as options.

Frankfurt

As a rule, November is a good corporate and con-

ference month in Frankfurt. Nevertheless, hoteliers

are restrained in their forecasts. Occupancy is ex-

pected to rise by 0.4%, while room rates are set to

fall by 3%. A 3% decline in year-on-year RevPar is

thus expected. Many hoteliers feel that the gene-

ral deterioration in the convention business is the

main reason for the generally negative ADR fore-

cast. Currently, individual pickup is still lacking at

many hotels. However, since the EuroMold trade

fair (although not a major event) is taking place in

Frankfurt this year (24 to 28 November 2014), the

hotels around the exhibition centre will be able to

charge higher room rates, something that could

make the results seem a little more positive.

Compared to last year, fore-

casts for this December are very

negative indeed. Occupancy is

expected to fall by 6% though

room rates will rise by as much

as 0.2%. A 6% decline RevPar

is thus expected. So far, preli-

minary bookings in the leisure

and events sectors are good

but volume is still lacking in the

individual segments. Last year,

Fig.5: Trendbarometer Frankfurt 2014 – Trend versus last year

0,4%

-6,3%

-6,9%

-3,3%

0,2%

-1,0%

-2,9%

-6,2%

-7,8%

November

December

Last Year

Occ ADR RevPAR

January

Source: Fairmas GmbH / Data as of 05.11.2014

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 13

FairmasHotel Reportin cooperation with SolutionsDotWG

“EuroMold” took place in December, trade fair that

days will be missing this year. Yet even if the boo-

kings for Christmas and New Year pick up soon,

figures could clearly still be positive, because the

development of room rates not least depends on

individual pickup, which is currently very difficult to

estimate. Group business is expected along with

the Christmas market tourism. In addition, the last

three weeks before Christmas are likely to be easily

sellable business weeks.

Forecasts for January are also well below last

year’s levels, both in terms of occupancy (7% less),

and in room rates (ADR down 1%). This time, the

Christmas holidays in many federal states are up to

three days longer than in 2014, which will lead to a

decline in corporate and meeting business in 2015.

In addition, the absence of “Paperworld” in Janu-

ary means two full trade fair days less in February

2015. Last year the entire event

fell in January. The steady growth

in hotel openings in Frankfurt is

leading to a cut-throat competiti-

on among the hotels; this beco-

mes particularly noticeable in the

winter months in the lower room

rate levels compared to last year.

Hamburg

November seems set to be a po-

sitive month for Hamburg with a

4% increase in RevPar. The starter for November

is the 66th Eisbeinessen (“pork knuckle dinner”),

which will bring many tourists to the city over the

weekend. Generally, the Hamburg hotels confirm

that this November’s business will be marked by

especially good advance bookings from the corpo-

rate and conference sectors, coupled with a high

demand in the transient segment (Occ: up by 2%,

ADR: up 2%).

December also looks likely to be extremely promi-

sing. Increases in all three key indicators are ex-

pected: occupancy is set to increase by 1% and

room rates will rise by 3%, which will lead to a (4%)

growth in RevPar. In Hamburg too, there are three

full business weeks before Christmas. Demand

for the Advent weekends is high and New Year‘s

Eve is very convenient for holidaymakers this year.

The hoteliers in Hamburg are looking confidently

Fig.6: Trendbarometer Hamburg 2014 – Trend versus last year

1,7%

0,7%

-5,5%

1,8%

3,0%

2,5%

3,5%

3,7%

-3,1%

November

December

January

Last Year

Occ ADR RevPAR

Source: Fairmas GmbH / Data as of 05.11.2014

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 14

FairmasHotel Reportin cooperation with SolutionsDotWG

towards the end of the year, although here too,

bookings are made at short notice.

However, the trend for January is subdued, with

declines in occupancy of up to 6%, leading to an

overall 3% drop in RevPar, despite a positive room

rate forecast (up 3%). Many trade shows, such as

the Nortec fair (21 to 24 January 2014) and the

congresses that took place in 2014, will be ab-

sent in 2015. With regard to the room rates fore-

cast, many hoteliers are already registering a very

good advance booking level in response to various

events, as well as a significantly growing demand

in the MICE segment. In Janu-

ary 2015, Hamburger hoteliers

expect more short-term boo-

king inquiries for annual kick-off

events and tourist trips.

Munich

November means three full

business weeks for Munich ho-

teliers. Forecasts are correspon-

dingly enthusiastic. Occupancy

is expected to rise by 6% com-

pared to last year and room rates by as much as

11%, thus leading to an 18% RevPar boost. This

positive development is largely due to the “electro-

nica” trade fair (11 to 14 November 2014), which

is leading to a huge demand and high room ra-

tes. This year too, room rates are well above tho-

Fig.7: Trendbarometer Munich 2014 – Trend versus last year

6,4%

0,3%

4,3%

11,1%

-0,1%

18,2%

18,2%

0,2%

23,2%

November

Dezember

Januar

Last Year

Occ ADR RevPAR

Source: Fairmas GmbH / Data as of 05.11.2014

se charged during the “Productronica” event. The

first weekend of Advent 2014 falls in November,

and hoteliers are expecting good leisure-sector

demand.

Forecasts for December in Munich are still cau-

tious. A slight increase in occupancy of 0.3% is

expected, but a 0.1% decline in room rates is also

forecast. This means that RevPar will slide by 0.2%.

December contains three full business weeks,

which could represent many guests at high room

rates, especially because the third Advent week is

a relatively long time before Christmas. There will

be no trade fairs or other major events in Decem-

ber. Individual bookings are only being made at a

late stage; it remains to be seen whether there will

still be any room for improvement.

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 15

FairmasHotel Reportin cooperation with SolutionsDotWG

January 2015 in Munich is expected to be much

better than in 2014 (Occ: +4.3%, ADR: +18.2%,

RevPar: +23.2%). The main reason for this positi-

ve development is the BAU trade fair, which takes

place every two years (19 to 24 January 2015).

The public holiday on 6 January 2015 will have a

negative effect on occupancy and room rates in

the first week. However, even if one calculates for

the low ADR associated with leisure sector busi-

ness, this only serves to reinforce the enormous

positive impact that the BAU event has on room

rates and RevPar.

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 16

FairmasHotel Reportin cooperation with SolutionsDotWG

In Focus

Provincial? Not in the slightest!

The unnoticed destinations of Rostock-Warnemünde, Mainz, and Darmstadt

The ABC of destinations

The Fairmas Hotel Report regularly highlights Germany’s most important A and B destinations. But what

actually characterizes an A or B destination? If we look for classification criteria, we will encounter a variety

of possible interpretations, the most important points of which are very similar or even identical. Important

distinguishing features for classifying a location are, for example, its population, infrastructure, industry and

trade, culture and education, administration, as well as the location’s regional, national or even international

significance.

People travel from all over the world to cities such as Berlin, Hamburg or Munich; they are lured by tourist

attractions just as much as by business meetings or international trade fairs. The hospitality industry is

booming. We also examine some B destinations on a regular basis. There are also many other large cities

that are of great importance for their respective region, the C destinations. We have systematically exami-

ned three such cities that are typical for this group and that are of both regional and national importance:

Rostock-Warnemünde, Mainz, and Darmstadt. All three places possess similar parameters such as popu-

lation, trade fair and convention centres; additionally, they are all university cities and transportation hubs.

Here, we look at the examples of Rostock-Warnemünde, Mainz and Darmstadt.

The hotels participating use Fairmas Hotel Benchmarking to provide the basis of their data analysis.

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 17

FairmasHotel Reportin cooperation with SolutionsDotWG

BerlinDusseldorf

Frankfurt (Main)HamburgCologneMunich

Stuttgart

Bochum Bonn Bremen

Dortmund Dresden Duisburg Nuremberg

Hannover Karlsruhe Leipzig Mannheim

Munster Essen Wiesbaden

Aachen Augsburg Bielefeld

Braunschweig Darmstadt Erfurt Erlangen

Freiburg (Breisgau) Heidelberg Kiel Lübeck Magdeburg Mainz

Mönchengladbach Mülheim (Ruhr) Offenbach (Main)

Osnabrück Potsdam Regensburg Rostock

Saarbrücken Wuppertal

Albstadt Aschaffenburg Bamberg Bayreuth Bergisch

Gladbach Bottrop Brandenburg (Havel) Bremerhaven Chemnitz Coburg

Cottbus Dessau Detmold Düren Eisenach Flensburg Frankfurt (Oder) Friedrichshafen

Fulda Fürth Gelsenkirchen Gera Gießen Görlitz Göttingen Greifswald Gütersloh Hagen Halberstadt

Halle (Saale) Hamm Hanau Heilbronn Herne Hildesheim Ingolstadt Jena Kaiserslautern Kassel

Kempten (Allgäu) Koblenz Konstanz Krefeld Landshut Leverkusen Lüdenscheid Ludwigshafen Lüneburg Marburg

Minden Moers Neubrandenburg Neumünster Neuss Oberhausen Offenburg Oldenburg Paderborn Passau

Pforzheim Plauen Ratingen Ravensburg Recklinghausen Remscheid Reutlingen

Rosenheim Salzgitter Schweinfurt Schwerin Siegen Solingen Stralsund Suhl Trier

Tübingen Ulm Villingen-Schwenningen Weimar Wilhelmshaven Witten

Wolfsburg Würzburg Zwickau

B

C

D

Most important centres:Population: 500,000 and more

National and/or international significanceLarge functioning markets in all segments

Of interregional or international importance culturally

Important centres:Population: 100,000 and moreLarge cities with a major economic and cultural significance that is mainly interregional or national

Important citiesMultifunctional large cities

Of regional and limited national significanceImportant impact on the immediate surroundings

Important regional cities:Population: up to 100,000Multifunctional medium-sized and small citiesregional focussed cities with significance for the immediate surroundings Low market volume and revenue Sources:

http://www.riwis.de/http://www.mygeo.info

& Fairmas

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 18

FairmasHotel Reportin cooperation with SolutionsDotWG

Figures, trends, and developments:

the cities of Rostock-Warnemünde, Mainz, and Darmstadt

Rostock-Warnemünde

The city of Rostock (to-

gether with its most famous

district, the seaside resort

of Warnemünde), with more

than 200,000 inhabitants, is

the largest city in the state

of Mecklenburg-Western

Pomerania, as well as a tou-

rist growth region. The eco-

nomic, cultural and scientific

centre in North-eastern Ger-

many has an important Bal-

tic port that handles ferry

and cargo ships, and one of Germany’s largest cruise ship ports. Besides being a university and logistics

site, Rostock is one thing above all: a tourism city that attracts guests from every German federal state and

from abroad. In addition to the area’s natural beauty, guests appreciate above all the widespread recrea-

tional facilities, water sports, shopping and culture, the family-friendly nature of the area, as well as health

and spa opportunities. This is proven by the steadily growing visitor numbers: in 2013, more guests than

ever visited this hanseatic city.

The number of guests grew by 11% in 2013 compared to the year before. In addition to Germans’ gene-

rally growing liking for city breaks, this also shows that the wide-ranging efforts of tourism operators and

hoteliers to make the low season attractive are now bearing fruit. During this time, holiday-makers arrive

who appreciate tranquillity and quiet enjoyment, as well as spa and health services. Moreover, new and/or

distinctive event formats are being introduced, such as the “Warnemünde Wintervergnügen” (“Warnemün-

Fig.1: Arrivals Rostock/Warnemünde (2006-2013)

(Source:Statistical office Western Pomerania)

547.961 564.323 561.578 550.874594.554 607.976

637.088

706.075

3,0%

-0,5%-1,9%

7,9%

2,3%

4,8%

10,8%

-10%

-5%

0%

5%

10%

15%

20%

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

2006 2007 2008 2009 2010 2011 2012 2013

Arrivals Change (%)

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 19

FairmasHotel Reportin cooperation with SolutionsDotWG

de Winter Fun”), Leuchtturm in Flammen (“Lighthouse in Flames”), and “Kultur trifft Genuss” (“Culture Meets

Pleasure”). So is everything really OK? The downside is enormously tight cut-throat competition, with many

new hotels having to compete for guests. This is the decisive cause of the development in 2014: year-to-

date figures show a minimal change in September with a RevPar increase of 0.4%, marked by downhill

development in relation to occupancy (Occ: down 2.4%) although ADR rose by 3%.

Let us look at 2014 at the Rostock-Warnemünde destination in more detail:

The beginning of the year

was difficult in economic

terms. With demand con-

stant, more beds were

available (partly due to the

opening of the “a-ja” resort

with 233 rooms in Warne-

münde in March 2013).

Due to the different timing

of the Easter holidays this year (2014: 14 to 23 April; 2013: 25 March to 3 April) March also turned out to

be just as problematic (Occ: down 14.4%). The turnaround came in April with a very positive overall deve-

lopment in RevPar of +13%, due to a sharp increase in occupancy (Occ: +5%) and room rates (ADR: +8%).

The positive trend continued in May, with RevPar growing by 6%. The sunny weather of early summer was

a big boost in May and made June very good all-round.

The overall performance deteriorated slightly in July, the first month of the school holidays (RevPar: down

1%) despite the positive room rates (ADR: up 2%). Less leisure business could be generated (Occ: - 3%),

due to the shift of the summer holidays (they began in mid-July in Mecklenburg-Western Pomerania; in

2013 the school summer holidays took up all of July). The improvement in ADR was largely due to a stricter

price policy in some hotels. In addition, some hotels were able to register a stronger conference business,

while other events, such as the “N-JOY”, and “The Beach und Stars@ndr2” on 25 and 26 July were parti-

cularly in demand. Rostock-Warnemünde recorded a slight increase in leisure sector business due to the

Number of hotels

Change No. of available beds

Change

2009 108 - 10.349 -2010 114 5,6% 14.029 35,6%2011 113 -0,9% 13.868 -1,1%2012 109 -3,5% 13.739 -0,9%2013 110 0,9% 14.577 6,1%2014 June 109 -0,9% 14.258 -2,2%

Hotel & bed supply, Rostock-Warnemünde

Fig. 2: Hotel & bed supply, Rostock-Warnemünde (2009-2014)

(Source:Statistical office Western Pomerania)

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 20

FairmasHotel Reportin cooperation with SolutionsDotWG

shift in the school summer holidays in Mecklenburg-Western Pomerania to mid-August and to the stable

summer weather on the coast this August (Occ: up 0.1%). The “Hanse Sail Rostock” and the “DFB Beach

Soccer Cup” were especially responsible for boosting room rates (ADR: up 5.4%). Taken together, this led

to a 6% increase in RevPar. And September? The terms of overall performance, the coastal resort showed

a 3% year-on-year improvement in RevPar. However, ADR and occupancy developed very differently to last

year (Occ: down 3%, ADR: up 6%). While hoteliers on the coast were able to achieve stable room rates due

to the longer school summer holiday in many states until the first week of September (especially in Lower

Saxony), the good weather conditions, and the Warnemünde market, their colleagues in the city of Rostock

itself complained of a decline in company and corporate business.

Fig. 3: Performance changes in 2014 Rostock-Warnemünde compared to the same month last year (Source: Fairmas)

Conclusion and outlook:

The new hotels that have opened since 2013 (the aja-Resort in Warnemünde, as well as the Hotel Sports-

forum, the Markgrafenheide beach resort and the Motel One – the last three all in Rostock itself) accoun-

ted for a total of 640 new rooms. This ensured even greater more cut-throat competition, with a negative

impact on the corporate segment in particular. The question of how the autumn-winter season will shape

up remains an exciting one. In principle, the assessment for the next five months remains subdued due to

the upcoming low season with short-term pick-up business for the Christmas season in November and

December.

-3%-5%

-14%

5%2%

0,3%

-3%

0,1%

-3% -2%

0,1%

3%

-10%

8%

1%

6%

2%

5% 6%

3%

-3% -2%

-23%

13%

3%6%

-1%

6%3%

0,4%

January February March April May June July August September YTDSeptember

Occ ADR RevPar

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 21

FairmasHotel Reportin cooperation with SolutionsDotWG

Mainz

Mainz is the capital of Rhi-

neland-Palatinate and, with

more than 200,000 inha-

bitants, it is also that fede-

ral state’s largest city. This

university town with a his-

tory going back more than

2000 years is headquarters

to a number of television

and radio stations and sees

itself as a stronghold of the

Rhineland Carnival. In 2013,

the city where printer Johan-

nes Gutenberg was born set a record with almost 570,000 arrivals. The YTD figures until September show

the stability of this development, with a RevPar plus of 6%, due to a very high (6%) increase in occupancy.

Mainz is also benefitting from a strong trade fair year, because many more trade shows, congresses and

events take place here in the even numbered years than in the odd, relatively poorer trade fair years. Also

worth mentioning are the city’s plans and activities to profile and promote the attractiveness of the desti-

nation under the umbrella of “mainzplus Citymarketing GmbH” in a partnership of government, university,

hoteliers and other tourism managers. These numbers provide more than a hint that it has been successful.

This is what we will see in Mainz as a destination in 2014:

The deterioration of the overall performance by 8% in January was due to a similar sharp drop (8%) in occu-

pancy. While a number of carnival events attracted guests in January 2013, this year they were held a month

later. February benefited from this, as well as from the first-ever annual kick-off event of a large insurance

company with 700 guests (approx. 450 overnight stays). This meant a 9% rise in ADR and a similar 9% growth

447.707 448.145 460.331430.849

487.205530.394

549.381569.940

0,1%2,7%

-6,4%

13,1%

8,9%

3,6% 3,7%

-15,0%

-10,0%

-5,0%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

0

100.000

200.000

300.000

400.000

500.000

600.000

2006 2007 2008 2009 2010 2011 2012 2013

Arrivals Change (%)

Fig.4: Arrivals Mainz (2006-2013)

Source: Statistical office of Rhineland-Palatinate

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 22

FairmasHotel Reportin cooperation with SolutionsDotWG

in RevPar. The upward

trend continued throug-

hout March with a 16%

increase in occupancy. The

causes were - as so often

- a series of large confe-

rences and events: from

14 to 16 March there was

a medical congress, which

takes place on a two-year

cycle with 800 participants,

estimated overnights: 2300; from 24 to 28 March the spring meeting of the Deutsche Physikalische Gesell-

schaft at the University of Mainz, with 1400 participants, estimated overnight stays: 5000 (a similar event

last took place in 2012). The good March figures could not be maintained in April and there were poorer

results in all performance areas: Occ: -6%, ADR: -2.2%, and RevPar: -8%. This was mainly due to the

Easter holidays, which allowed far less corporate business. That which April lacked was a benefit to May:

a huge (29%) increase RevPar thanks to a growth of 22% in occupancy and a 5% improvement in room

rates. Three heavyweight congresses contributed to this fantastic result: the CIMT medical congress was

held from 6 to 8 May (900 participants, estimated overnight stays: 2500); the “JAX” IT congress took place

from 12 to 16 May (1000 attendees, estimated overnights: 4000); while the annual general meeting of the

Museumsbund (Museums Association) was held from 4 to 7 May, attracting 450 participants, and an esti-

mated 1300 overnight stays).

June was mixed. RevPar was down by 4%, mainly due to the fall in room rates (ADR down 5%). June

2013 had been a strong month for corporate business. In 2014, the two public holidays (Whit Monday

and Corpus Christi) had a negative effect on two full business weeks. Besides this, the “Techtextil” event in

Frankfurt (held every two years) had ensured healthy overflow business in Mainz in 2013. In July, the overall

performance (RevPar: up 13%) improved, mainly due to the good occupancy figures (Occ: up 13%). This

was due to both the flourishing conference business and the later start of the school holidays in Rhineland-

Palatinate (at the end of July). Another factor was the “Summer in the City” music festival, with artists such

as Elton John, Neil Young, and Unheilig. These open-air events attracted nearly 55,000 visitors and led to

Number of hotels

Change No. of available

bedsChange

2007 39 - 4.948 -2008 39 0,0% 4.933 -0,3%2009 42 7,7% 4.671 -5,3%2010 41 -2,4% 4.999 7,0%2011 43 4,9% 5.211 4,2%2012 41 -4,7% 5.200 -0,2%2013 43 4,9% 5.493 5,6%2014 April 43 0,0% 5.205 -5,2%

Hotel & bed supply, Mainz

Fig.5: Hotel & bed supply, Mainz (2006-2013)

(Source: Statistical Office of Rhineland-Palatinate)

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 23

FairmasHotel Reportin cooperation with SolutionsDotWG

many extra overnights. August was also positive: the total market grew (RevPar: up by 2%), mainly due

to a rise of more than 5% in occupancy. A major international medical conference (the 47th International

Congress of Pathology with more than 3500 overnight stays) ensured good figures, as did a corporate

event with an additional 1500 overnights. A number of major events such as “Summer in the City”, “Rhein

in Flammen” (“Rhine in Flames”) and the Sunday TV show “ZDF-Fernsehgarten” clearly boosted demand.

The “James Rizzi exhibition (the New York Atelier)” from 18 July to 14 September carried on seamlessly

where the last exhibition left off in the summer of 2008, attracting more than 30,000 guests and ensuring

further overnight stays in Mainz.

The Mainz Wine Market succeeded in attracting a record 380,000 visitors. The later start of the school

summer holidays (2013: 8 July to 18 August; 2014: 28 July to 7 September) resulted in lower room rates in

August with fewer corporate sector bookings (ADR: down 3.3%). Growth in Mainz continued in September

(RevPar: up 9%). Numerous events and congresses (the Veterinary Medical Congress with 600 partici-

pants, estimated overnight stays: 1600; the German Nature Conservation Congress with 450 participants,

estimated overnights: 2000; the Meeting of the Society of German Natural Scientists and Physicians, 700

participants, estimated nights: 1800; the EMC Forum, with 600 participants, estimated overnights: 600;

the International Electrochemistry Conference, 450 participants, estimated overnights: 1200) took place in

Mainz and provided better occupancy results (Occ: up 6%) and improved room rates (ADR: +3.3%).

-8%

-0,5%

16%

-6%

22%

1%

13%

5% 6% 6%

-0,1%

9%

-8%

-2%

5%

-5%

-0,1%-3%

3%

-0,1%

-8%

9%7%

-8%

29%

-4%

13%

2%

9%6%

January February March April May June July August September YTDSeptember

Occ ADR RevPar

Fig.6: Performance changes in 2014 Mainz compared to the same month last year (Source: Fairmas)

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 24

FairmasHotel Reportin cooperation with SolutionsDotWG

Conclusion and outlook:

The performance in the printing and media city impressed all round. The figures show well-founded and

solid progress. Such developments do not happen by chance. In Mainz, they have mainly been due to

the combined activities of all the major tourism service providers, in close cooperation with the mainzplus

CITYMARKETING GmbH company. This invigorates both the conference and congress destination, as well

as the cultural and leisure activities. In the view of many insiders, 2014 has been a particularly strong year

for hoteliers in Mainz.

The increase in the number of beds appears moderate and well-planned. Discussions are taking place in

the city about a new four-star hotel next to the palace. A feasibility study is being prepared, and it is due to

be completed by the spring of 2015.

Darmstadt:

Darmstadt in South Hes-

se, with a population of

around 150,000, has been

allowed to call itself a “Wis-

senschaftsstadt” (“Science

City”) since 1997. Here,

a technical university, two

polytechnics with appro-

ximately 41,000 students,

as well as over 30 other re-

search facilities and institu-Fig.7: Arrivals Darmstadt (2006-2013)

Source: Statistical Office of Hesse

226.164216.189

264.701 269.733290.086 295.531

310.833 317.459

-4,4%

22,4%

1,9%

7,5%

1,9%5,2%

2,1%

-20,0%

-10,0%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

-20.000

30.000

80.000

130.000

180.000

230.000

280.000

330.000

2006 2007 2008 2009 2010 2011 2012 2013

Arrivals Change (%)

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 25

FairmasHotel Reportin cooperation with SolutionsDotWG

tions are actively researching and working. They include such renowned bodies as the European Space

Agency’s European Space Operations Centre (ESA/ESOC) and the European Organisation for the Exploi-

tation of Meteorological Satellites (EUMETSAT). This affinity with education also determines the congresses

that take place. The year-to-date figures show an excellent overall performance for Darmstadt up to the

month of September.

2014 at destination Darmstadt:

Experience shows that

January is a bad month in

Darmstadt (with RevPar

decline of 5%), mainly due

to negative development

in terms of occupancy

(Occ down 9%). This time,

all the hoteliers complai-

ned about the start to the

year because not even the

Heimtex home-textile fair in

Frankfurt provided any respite, and the month only picked up speed very slowly due to the long school

Christmas holidays that carried on until 11 January. February made up for the poor start to the year with

extremely positive overall figures and a 16% increase. The later-than-usual Carnival at the end of February

and beginning of March boosted corporate bookings. The “Ambiente” trade fair in Frankfurt and the “Dt.

SQL Server” IT conference at the Darmstadtium were also important. March was excellent with a further

19% increase in RevPar, which could be attributed to an extremely high (26%) surge in occupancy. Due

to the different timing of the Easter and the Easter school holidays this year, it was a full business month

(except for the first three days of Carnival). The city’s hoteliers consistently reported hotels being booked

out from Monday until Friday almost every week. April lacked the factors that had benefited the month of

March (Occ: down 14%). The later Easter holidays also left their mark. Unlike the same month last year,

May profited from the fortunate calendar. The month was marked by a tremendous figures (Occ: +30%,

Fig.8: Hotel & bed supply Darmstadt (2006-2014)

Source: Statistical Office of Hesse

Number of hotels

Change No. of available

bedsChange

2006 - - 3.349 -2007 - - 3.335 -0,4%2008 - - 4.120 23,5%2009 40 - 4.048 -1,7%2010 41 2,5% 4.302 6,3%2011 41 0,0% 4.250 -1,2%2012 43 4,9% 4.281 0,7%2013 42 -2,3% 4.374 2,2%2014 May 41 -2,4% 4.478 2,4%

Hotel & bed supply, Darmstadt

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 26

FairmasHotel Reportin cooperation with SolutionsDotWG

ADR: +4%), as there was hardly a room to be booked in Frankfurt, either. The “Microsoft Synopsis 2014”

and “XXIV Quark Matter Conference” were held in the Darmstadtium. During the first half of the year, May

was by far the best month in Darmstadt and surrounding areas. The public holidays and the late start of the

school summer vacations had a negative effect on June, a month in which corporate business levels were

much lower than in 2013 (Occ: -8%, ADR: -10%, and RevPar: -18%). July was marked by a very strong

improvement in overall performance (RevPar: + 41%). The late start of the school summer holidays in Hesse

at the end of July ensured a full business month with plenty of corporate and meeting sector trade (Occ:

+33%) and ADR (+6%). In August, Darmstadt’s performance shone at all levels: Occ: +45%, ADR: +1.3%

and RevPar: +47.2%. The two-week-long International Summer School Courses for New Music, run by the

Darmstadt Institute of Music were responsible for these excellent results. In September, the positive trend

continued with is a 7% increase, mainly due to the 5% year-on-year growth in occupancy. The IAA trade fair

in Frankfurt had far less impact on Darmstadt than this year‘s “Automechanika” event. During these strong

top-ranking trade fairs, many visitors take advantage of Darmstadt’s closeness and first-rate transport con-

nections to avoid paying Frankfurt’s high room rates.

-9%

14%

26%

-14%

30%

-8%

33%

45%

5%11%

4% 2%

-5%-1%

4%

-10%

6%1% 1%

-1%-5%

16%19%

-14%

35%

-18%

41%47%

7%10%

January February March April May June July August September YTDSeptember

Occ ADR RevPar

Fig.9: : Performance changes in 2014 Darmstadt compared to the same month last year (Source: fairmas)

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 27

FairmasHotel Reportin cooperation with SolutionsDotWG

Conclusion and outlook:

One exciting development – hoteliers had prepared themselves mentally for an economically weak year,

because a commercial giant (Procter & Gamble/Wella) had left the city and while some large conferences

and events (e.g. Deutsche Post and Deutsche Telekom) had been cancelled. The actual figures do permit

some restrained optimism, even if the global player left a large gap that no other company is currently filling.

The Darmstadium is a big plus for the exhibition, conference and events scene. Maybe the city also neds

a five-star hotel? Opinions differ on this point. The outlook towards a solid location policy is unanimous: no

further hotel openings are planned in the near future.

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 28

FairmasHotel Reportin cooperation with SolutionsDotWG

The Fairmas Hotel Report is published by:

Fairmas Gesellschaft für Marktanalysen mbH, Sachsendamm 6, 10829 Berlin, Deutschland

Solutions Dot WG GmbH, Kranzer Strasse 6-7, 14199 Berlin, Deutschland

Fairmas Gesellschaft für Marktanalysen mbH specializes in market

analyses and the development of planning and controlling software

for the hotel industry. The company offers its international clientele a

hotel benchmarking platform, as well as various software applications

for the fields of budgeting, forecasting, controlling, management re-

porting and work process optimization.

As a strategic management consultancy, Solutions Dot WG develops

individual and customized strategies and solutions for companies in

the hotel, catering and tourism, and provides support in implementing

plans. Solutions dot also manages independent project implementa-

tion, is active in support management and interim management, as

well as in the total quality management (TQM) sector.

The Fairmas Hotel Report is edited by:

Nadine Kilian, Marketing & Communications Manager,

Fairmas Gesellschaft für Marktanalysen mbH, e-mail: [email protected]

Gabriele Kiessling, Consultant und Project Management,

Solutions Dot WG GmbH, e-mail: [email protected]

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 29

FairmasHotel Reportin cooperation with SolutionsDotWG

Disclaimer

No representation or warranty (express or implied) is given as to the accuracy or complete-ness of the

information contained in this publication, and, to the extent permitted by law, Fairmas GmbH / Solutions

Dot WG do not accept or assume any liability, responsibility or duty of care for any consequences of you

or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for

any decision based on it.