Embed Size (px)

Citation preview

Housing Authority of the CITY OF OPELOUSAS

Opelousas, Louisiana

Annual Financial Report As of and for the Year Ended June 30, 2014

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Basic Financial Statements As of and for the Year Ended June 30, 2014 With Supplemental Information Schedules

CONTENTS

Exhibit Page Independent Auditor's Report 3

Required Supplementary Information

Management's Discussion and Analysis 6

Basic Financial Statements: Statement of Net Position A 11 Statement of Revenues, Expenses and Changes in Net Position B 13 Statement of Cash Flows C 14 Notes to the Financial Statements 15

Supplementary Information Financial Data Schedule 25

Other Reports Required by Government Auditing Standards; 0MB Circular A-133, Audits of States, Locai Govemments, and Non-Profit Organizations; and the Singie Audit Act Amendments of 1996:

Independent Auditor's Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards 30

Independent Auditor's Report on Compliance For Each Major Federal Program and on Internal Control Over Compliance Required by OMB Circular A-133 32

Schedule of Expenditures of Federal Awards 35

Schedule of Current Year Findings and Questioned Costs 37

Other Information

Schedule of Prior Audit Findings 39

Schedule of Compensation Paid Board Members 40

William Daniel McCaskill, CPA A Professional Accounting Corporation

415 Magnolia Lane Mandeville, Louisiana 70471

Telephone 866-829-0993 Member of Fax 225-665-1225 Louisiana Society of CPA's E-mail [email protected] American Institute of CPA's

INDEPENDENT AUDITOR'S REPORT

Board of Commissioners Housing Authority of the City of Opeiousas Opelousas, Louisiana

Report on the Financial Statements

I have audited the accompanying financial statements of the Housing Authority of the City of Opelousas (the authority) as of and for the year ended June 30, 2014, and the related notes to the financial statements, which comprise the Authority's basic financial statements as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

My responsibility is to express opinions on these financial statements based on my audit. I conducted my audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that I plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, I express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Independent Auditor's Report, 2014 Page Two

I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis for my audit opinions.

Opinions

In my opinion, the financial statements referred to above present fairly in all material respects, the respective financial position of the Housing Authority of the City of Opelousas as of June 30, 2014, and the respective changes in net financial position and cash flows, thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the Management's discussion and analysis as listed in the table of contents be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. I have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management's responses to my inquiries, the basic financial statements, and other knowledge I obtained during my audit of the basic financial statements. I do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

My audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the authority's basic financial statements. The Financial Data Schedule is presented for purposes of additional analysis and is not a required part of the basic financial statements. The Schedule of Expenditures of Federal Awards is presented for purposes of additional analysis as required by the U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is also not a required part of the basic financial statements.

The Financial Data Schedule and the Schedule of Expenditures of Federal Awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In my opinion, the information is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Independent Auditor's Report, 2014 Page Three

The Schedule of Compensation of Board Members has not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, I do not express an opinion or provide any assurance on it.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, I have also issued my report dated November 12, 2014 on my consideration of the authority's internal control over financial reporting and on my tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of my testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the authority's internal control over financial reporting and compliance.

'WiCCiam (DanieCMCQCLS^C

William Daniel McCaskill, CPA A Professional Accounting Corporation

November 12, 2014

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS. LOUISIANA MANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30, 2014

Introduction

The Management's Discussion and Analysis is a narrative overview and analysis of the financial activities of the Housing Authority of the City of Opeiousas, Louisiana (The Authority) for the fiscal year ended June 30, 2014. Management's Discussion and Analysis (MD&A) is a look at the overall financial performance of the Housing Authority of the City of Opeiousas, Louisiana using an objective, easily readable analysis of the Authority's financial activities. We encourage readers to consider the information presented herein in conjunction with additional information that we have furnished in the Notes to Financial Statements. Please reference the Table of Contents for the exact location of those items.

Financial Highlights

• The assets of the Authority exceeded its liabilities as of June 30, 2014 by $14,458,680 (net position)

• The Authority's cash balance as of June 30, 2014 was $4,402,189 representing an increase of $832,409 from the prior year.

• The Authority had $1,392,644 in Dwelling Rental, $2,535,543 in HUD Operating Grants, and $563,696 in Capital Grants for the year ended June 30, 2014.

• Overall the Authority continues to maintain a good financial position and operates without the need for debt borrowing.

Overview of the Financial Statements

The financial statements included in this annual report are those of a special-purpose government engaged in a business-type activity. The following statements are included:

• Statement of Net Position - reports the Authority's current financial resources (short-term spendable resources) with capital assets and long-term debt obligations.

• Statement of Revenues, Expenses, and Changes in Net Position - reports the Authority's operating and non-operating revenues, by major source along with operating and non-operating expenses and capital contributions.

• Statement of Cash Flows - reports the Authority's cash flows from operating, investing, capital and non-capital activities.

Reporting on the Housing Authoritv as a Whole

The analysis of the Authority as a whole is discussed below. The MD&A should answer the question "Is the Authority as a whole better off or worse as a result of the year's activities?"

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS. LOUISIANA MANAGEMENT'S DISCUSSION AND ANALYSIS (CONTINUED)

JUNE 30, 2014

The attached analysis of entity wide net position, revenues, and expenses are provided to assist with answering the above question. This analysis includes all assets and liabilities using the accrual basis of accounting, which is similar to the accounting used by most private sector companies. Accrual of the current year's revenues and expenses are taken into account regardless of when cash is received or paid. This analysis also reflects the Authority's net position and changes in them. The Authority's net position is the differences between what the Authority owns (i.e., assets) and what the Authority owes (i.e., liabilities), as one way to measure the Authority's financial health.

The Notes to Financial Statements provide additional information that is essential to a full understanding of the data provided in the basic financial statements. The Notes to Financial Statements can be found in this report after the financial statements referred to above.

Over time, changes in the Authority's net position are an indicator of whether its financial health is improving or deteriorating. Readers need to consider other non-financial factors such as changes in family composition, fluctuations in the local economy, HUD mandated program administrative changes, and the physical condition of the Authority's capital assets to assess the overall health of the Authority.

Analysis of Entity Wide Net Assets fStatement of Net Assets)

Total Assets for FYE 2014 was $14,828,048 and for FYE 2013 the amount was $14,463,496. This represents a net increase of $364,552 over the prior year.

Cash increased by $832,409 from the prior year. Dwelling rental revenue increased by $145,636, the operating grants decreased by $120,135, and capital grants decreased by $531,230. General and administrative expense decreased by $173,340, repairs and maintenance expense decreased by $193,185, and utilities expense increased by $105,636.

Total Liabilities decreased from $379,431 in FYE 2013 to $369,368 in FYE 2014. This represents a decrease of $10,063.

Non-Current Liabilities decreased by $14,656. This decrease represents an adjustment to properly record compensated absences.

The following table illustrates our analysis:

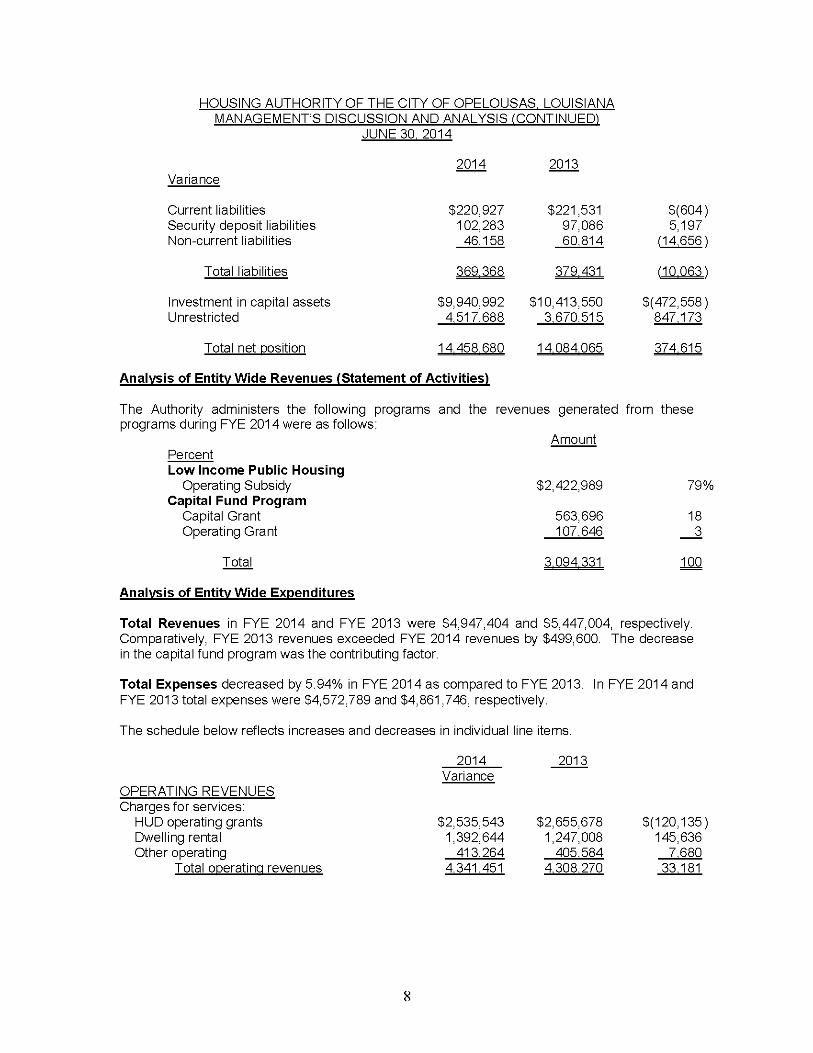

2014 2013 Variance

Cash $4,402,189 $3,569,780 $832,409 Other current assets 382,584 383,080 (496) Restricted cash 102,283 97,086 5,197 Capital assets 9.940.992 10.413.550 (472.5581

Total assets 14.828.048 14.463.496 364.552

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS. LOUISIANA MANAGEMENT'S DISCUSSION AND ANALYSIS (CONTINUED)

JUNE 30. 2014

2014 2013 Variance

Current liabilities Security deposit liabilities Non-current liabilities

$220,927 102,283

46.158

$221,531 97,086 60.814

$(604) 5,197

n4.6561

Total liabilities 369 368 379 431 no 0631

investment in capital assets Unrestricted

$9,940,992 4.517.688

$10,413,550 3.670.515

$(472,558) 847.173

Total net position 14 458 680 14 084 065 374 615

Analysis of Entity Wide Revenues fStatement of Activities)

The Authority administers the following programs and the revenues generated from these programs during FYE 2014 were as follows:

Amount Percent Low Income Public Housing

Operating Subsidy $2,422,989 79% Capital Fund Program

Capital Grant 563,696 18 Operating Grant 107,646 3

Total 3.094.331 100

Analysis of Entity Wide Expenditures

Total Revenues in FYE 2014 and FYE 2013 were $4,947,404 and $5,447,004, respectively. Comparatively, FYE 2013 revenues exceeded FYE 2014 revenues by $499,600. The decrease in the capital fund program was the contributing factor.

Total Expenses decreased by 5.94% in FYE 2014 as compared to FYE 2013. In FYE 2014 and FYE 2013 total expenses were $4,572,789 and $4,861,746, respectively.

The schedule below reflects increases and decreases in individual line items.

2014 2013 Variance

OPERATING REVENUES Charges for services:

HUD operating grants $2,535,543 $2,655,678 $(120,135) Dwelling rental 1,392,644 1,247,008 145,636 aher operating 413.264 405.584 7.680

Total ooeratina revenues 4.341.451 4.308.270 33.181

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS, LOUISIANA

JUNE 30. 2014

2014 2013 Variance

OPERATING EXPENSES Administrative salaries $345,618 $305,430 $40,188 Employee benefit contr. - admin. 112,200 102,466 9,734 Other operating 346,588 546,662 (200,074) Utilities 1,070,796 965,163 105,633 Ordinary maint. - labor 526,854 569,311 (42,457) Ordinary maint. - materials 244,976 272,933 (27,957) Ordinary maint. - contract costs 162,086 257,006 (94,920) Ordinary maint. -emp. ben. contr. 229,577 257,429 (27,852) Protective services - labor 51,341 67,595 (16,254) Protective services - emp. ben. contr. 19,851 19,989 (138) Protective services - other 45 (45) insurance premiums 289,242 322,409 (33,167) Payments in lieu of taxes 76,080 72,176 3,904 Bad debts - tenants 27,051 20,973 6,078 Depreciation 1.070.529 1.082.159 n 1.630)

Total coeratino expenses 4,572,789 4,861,746 f288,957)

Ooeratino loss f231,3381 f553,4761 322,138

NON-OPERATING REVENUES fEXPENSES) Capital grants 563,696 1,094,926 (531,230) interest revenue 14,184 6,040 8,144 Misceiianeous revenue 28.073 37.768 f9.695)

Total non-ooeratina revenues 605,953 1,138,734 f532,781 )

Chance in net oosition 374 615 585 258 f210 643)

Budaetary SummarY

Budgetary Highlights are as follows:

The final operating budget for fiscal year ended June 30, 2014 showed budgeted revenues exceeding budgeted expenses by $685,214.

The revenue budget was $5,132,548 (excluding OFF grants) for fiscal year 2014. The budgeted revenues exceeded the actual revenues by $228,261.

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS. LOUISIANA MANAGEMENT'S DISCUSSION AND ANALYSIS (CONTINUED)

JUNE 30, 2014

Budgetary Summary - Continued

The expense budget was $4,447,334 for fiscal year 2014. The budgeted expenses exceeded the actual expenses (excluding depreciation) by $316,851.

Capital Asset

The Authority's total investment in capital assets at June 30, 2014 was $36,627,336, with accumulated depreciation of $26,686,344. This results in capital assets, net of accumulated depreciaticn, of $9,940,992.

Future Budget and Economic Outlook

The Authority is primarily dependent upon HUD for the funding of operations; therefore, the Authority is affected by federal budget and HUD mandates. The capital fund program for 2013 is currently being drawn and no major changes are expected.

The capital fund programs are multiple year budgets and have remained relatively stable. Capital funds are used for the modernization of public housing properties including administrative fees involved in the modernization.

Reguests for Information

This report is intended to provide interested parties with a general overview of the finances of the Housing Authority of the City of Opeiousas, Louisiana. Questions or requests for further information should be addressed to the Authority at P.O. Box 689, Opeiousas 70571-0689

10

Housing Authority of the City of Opelousas Opelousas, Louisiana

Statement of Net Position As of June 30, 2014

Exhibit A

ASSETS Current assets Cash and cash equivalents Receivables:

HUD Tenant rents, net of allowance

Prepaid expenses Inventory, net of allowance Restricted assets - cash and cash equivalents

Total current assets

4,402,189

2,330 13,466

237,854 128,934 102,283

4,887,056

Noncurrent assets Capital assets:

Nondepreciable capital assets: Land Total nondepreciable capital assets

Depreciable capital assets: Buildings and improvements Furniture and equipment Less accumulated depreciation

Total depreciable capital assets, net of accumulated depreciation

Total capital assets, net of accumulated depreciation

Total assets

TOTAL ASSETS

1,327,350 1,327,350

33,954,409 1,345,577

(26,686,344) 8,613,642

9,940,992

14,828,048

14,828,048

(continued)

11

Housing Authority of the City of Opelousas Opelousas, Louisiana

Statement of Net Position As of June 30, 2014

Exhibit A

LIABILITIES AND NET POSITION Current Liabilities

Accounts payable Payable to other governments Accrued wages payable Accrued compensated absences Unearned revenue Security deposit liability

81,990 76,080 19,832 33,024 10,001

102,283

Total current liabilities 323,210

Noncurrent liabilities Accrued compensated absences 46,158

Total noncurrent liabilities 46,158

TOTAL LIABILITIES 369,368

NET POSITION Net Investments in Capital Assets Restricted Unrestricted

9,940,992

4,517,688

TOTAL NET POSITION $ 14,458,680

The accompanying notes are an integral part of these financial statements.

12

Housing Authority of the City of Opeiousas

Opelousas, Louisiana

Statement of Revenues, Expenses, and Changes In Net Position

For the Year ended June 30, 2014

Exhibit B

Operating Revenues HUD Operating Grants Dwelling Rental Other Operating

Totai operating revenues

Operating Expenses General and administrative Repairs and maintenance Utilities Protection seivices Depreciation and amortization

Totai operating expenses

Operating income (ioss)

Nonoperating Revenues (Expenses): Interest revenue Miscellaneous revenues

Totai nonoperating revenues (expenses)

income (ioss) before other revenues, expenses, gains, iosses and transfers

Oapital contributions (grants)

increase (decrease) in net position

Net position, beginning of year

Net position, end of year

The accompanying notes are an integral part of these financial statements.

2,535,543 1,392,644 413,264

4,341,451

1,196,776 1,163,494 1,070,799

71,192 1,070,528

4,572,789

(231,338)

14,184 28,073

42,257

(189,081)

563,696

374,615

14,084,065

$ 14,458,680

13

Housing Authority of the City of Opelousas Statement of Cash Flows

For the Year ended June 30, 2014

Exhibit C

CASH FLOWS FROM OPERATiNG ACTiViTiES

Receipts from federal subsidies Receipts from tenants Payments to suppliers Payments to employees

Net cash provided by operating activities

CASH FLOWS FROM NONCAPiTAL FiNANCiNG ACTiViTiES

Miscellaneous revenues

Net cash provided by noncapitai financing activities

CASH FLOWS FROM CAPiTALAND RELATED FiNANCiNG ACTiViTiES

Proceeds from capital grants Purchase and construction of capital assets

Net cash (used in) capitai and reiated financing activities

CASH FLOWS FROM iNVESTiNG ACTiViTiES interest received

Net cash provided by investing activities

Net increase (decrease) in cash and cash equivalents

Cash and cash equivalents - beginning of year

Cash and Cash equivalents - unrestricted

Cash and Cash equivalents - restricted

Totai Cash and Cash Equivalents - end of year

2,533,213 1,803,808

(2,589,195) (923,8121

824,014

28,073

28,073

563,696 (592,361)

(28,665)

14,184 14,184

837,606

3,666,866

4,402,189

102,283

4,504,472

Reconciiiation of operating income (loss) to net cash provided by operating activities:

Operating (loss)

Adjustments to reconcile operating (loss) to net cash provided by operating activities:

Depreciation and amortization

Changes in assets and iiabiiities:

HUD receivable Tenant rents, net of allowance Prepaid insurance inventories Accounts payable Accrued wages payable PILOT Payable Accrued compensated absences Unearned revenue Security deposit iiabiiity

Net cash provided by operating activities

$ (231,338)

1,070,528

(2,330) (7,297)

(15,822) 25,945 (8,807) (1,644) 3,904

(15,459) 1,137 5,197

824,014

The accompanying notes are an integral part of the financial statements

14

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Notes to the Basic Financial Statements June 30, 2014

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The accompanying basic financial statements of the authority have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financial reporting principles.

(1) Reporting Entitv

The Housing Authority of The City of Opelousas (the authority) was chartered as a public corporation under the laws of the State of Louisiana for the purpose of providing safe and sanitary dwelling accommodations for the residents of the City of Opelousas, Louisiana. This formation was contingent upon the approval of the city.

The authority is governed by a Board of Commissioners (Board), which is composed of five members appointed by the city and serve five-year staggered terms. The Board of the authority exercises all powers granted to the authority.

GASB Statement No. 14 established criteria for determining the governmental reporting entity. Under provisions of this statement, the authority is considered a primary government, since it is a special purpose government that has a separately elected governing body, is legally separate, and is fiscally independent of other state and local governments. As used in GASB 14, fiscally independent means that the authority may, without the approval or consent of another governmental entity, determine or modify its own budget, control collection and disbursements of funds, maintain responsibility for funding deficits and operating deficiencies, and issue bonded debt. The authority has no component units, defined by GASB 14 as other legally separate organizations for which the elected authority members are financially accountable.

15

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

The authority is a related organization of the City of Opelousas, Louisiana since the city appoints a voting majority of the authority's governing board. The city is not financially accountable for the authority as it cannot impose its will on the authority and there is no potential for the authority to provide financial benefit to, or impose financial burdens on, the city. Accordingly, the authority is not a component unit of the financial reporting entity of the city.

(2) Funds

The accounts of the authority are organized and operated on the basis of funds. A fund is an independent fiscal and accounting entity with a self-balancing set of accounts. Fund accounting segregates funds according to their intended purpose and is used to aid management in demonstrating compliance with finance-related legal and contractual provisions. The minimum number of funds is maintained consistent with legal and managerial requirements.

All funds of the authority are classified as proprietary. The general fund accounts for transactions of all of the authority's programs.

Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with a proprietary fund's principal ongoing operations. The principal operating revenues of the authority's enterprise fund are HUD operating grants and subsidies and tenant dwelling rents. Operating expenses include General and Administrative expenses, repairs and maintenance expenses, utilities and depreciation and amortization on capital assets. All revenues and expenses not meeting this definition are reported as nonoperating revenues and expenses.

The accompanying basic financial statements of the authority have been prepared in conformity with governmental accounting principles generally accepted in the Unites States of America. The GASB is the accepted standard setting body for establishing governmental accounting and financial reporting principles. The accompanying basic financial statements have been prepared in conformity with GASB statement No. 34. Basic Financial Statements and Managements discussion and Analysis—for State and Local Governments, which was unanimously approved in June 1999 by the GASB.

16

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

(3) Measurement focus and basis of accounting

Proprietary finds are accounted for on the flow of economic resources measurement focus and the accrual basis of accounting. Under this method, revenues are recorded when earned and expenses are recorded at the time the liabilities are incurred. With this management focus all assets and all liabilities associated with the operation of these funds are included on the statement of net positions.

(4) Assets, liabilities, and net Position

(a) Deposits

The authority's cash and cash equivalents are considered to be cash on hand, demand deposits, and short-term investments with original maturities of three months or less from the date of acquisition. HUD regulations, state law and the authority's investment policy allow the housing authority to invest in collateralized certificates of deposit and securities backed by the federal government.

(b) Inventory and prepaid items

All inventories are valued at cost on a first-in first-out (FIFO) basis. Inventories consist of expendable building materials and supplies held for consumption in the course of the authority's operations.

Certain payments to vendors reflect costs applicable to future accounting periods and are recorded as prepaid items.

(c) Restricted Assets

Gash equal to the amount of tenant security deposits is reflected as restricted.

(d) Capital assets

Capital assets of the authority are included in the statement of net positions and are recorded at actual cost. The capitalization threshold is $500. Depreciation of all exhaustible fixed assets is charged as an expense against operations.

Property, plant, and equipment of the Authority is depreciated using the straight line method over the following estimated useful lives:

17

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

Buildings 35 years Modernization and improvements 15 years Furniture and equipment 3-7 years

(e) Due from/to other governments or agencies

Amounts due from/to the authority to/by other governments or agencies are generally for grants or programs under which the services have been provided by the authority. The authority also records an amount due to the various taxing districts within the region for payments in lieu of taxes.

(f) Allowance for doubtful accounts

The authority provides an allowance for doubtful accounts, as needed, for accounts deemed not collectible. At June 30, 2014, the management of the authority established an allowance for doubtful accounts of approximately $242.

(g) Compensated absences

It is the authority's policy to permit employees to accumulate earned but unused vacation pay benefits. In accordance with the provisions of GASB Statement No. 16, "Accoi;/?f/7?sffo/'Co/T7pe/?safedAbse/?ces," vacation pay is accrued when incurred and reported as a liability. Employees may accumulate an unlimited number of annual leave hours. Depending on their length of service, employees receive payment for up to 300 annual leave hours upon termination or retirement at their then current rate of pay. The cost of current leave privileges, computed in accordance with GASB Codification Section C60 is recognized as a current year expense when leave is earned.

(h) Restricted net Position

Net positions are reported as restricted when constraints placed on net positions use are either:

Externally imposed by creditors (such as debt covenants), grantors, contributors or laws or regulations of other governments or imposed by law through constitutional provisions or enabling legislation.

Restricted resources are used first when an expense is incurred for purposes for which both restricted and unrestricted resources are available.

18

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

(i) Use of estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the government-wide financial statements and reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

NOTE B-DEPOSITS

Deposits are stated at cost, which approximates fair value. Under state law and/or federal regulation, these deposits, or the resulting bank balances, must be in Federal Securities, secured by federal deposit insurance or the pledge of federal securities. The fair value of the pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent.

As of June 30, 2014, the authority's carrying amount of deposits was $4,504,472, which includes the following:

Cash and cash equivalents-unrestricted $4,402,189 Cash and cash equivalents- restricted 102,283 Total $4,504,472

Interest Rate Risk—The authority's policy does not address interest rate risk.

Credit Rate Risk—Since all of the authority's deposits are federally insured and/or backed by federal securities, the authority does not have credit rate risk.

Custodial Credit Risk—This is the risk that in the event of a bank failure, the authority's deposits may not be returned to it. The authority does not have a policy for custodial credit risk. $616,599 of the authority's total deposits were covered by federal depository insurance, and do not have custodial credit risk. The remaining $3,955,316 of deposits have custodial credit risk, but were collateralized with securities held by the pledging financial institution trust department or agent. The bank balances at June 30, 2014 totaled $4,571,915.

19

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

NOTE 0 - CAPITAL ASSETS

Capital assets activity for the year ended June 30, 2014 was as follows:

6 30 2013 Additions Deletions 6 30 2014 Nondepreciable Assets:

Land Construction in Progress Depreciable Assets: Building and improvements Furniture and equipment

1,327,350

33,423,669

1,439,074

530,741

82,326 175,824

1,327,350

33,954,410

1,345,576

Total 36,190,093 613,067 175,824 36,627,336

Less accumulated depreciation Building and improvements Furniture and equipment

24,873,326

903,218

952,124

118,403 160,727

25,825,450

860,894 Total accumulated depreciation 25,776,544 1,070,527 160,727 26,686,344

Net Capital Assets 10,413,549 (457,460) 15,097 9,940,992

NOTE D - CONSTRUCTION COMMITMENTS

The authority is engaged in a modernization program and has entered into construction type contracts with approximately $1,714,264 remaining until completion.

NOTE E-LEASES

During the year ended June 30, 2011, the authority entered into a capital lease for copier systems. The lease is considered immaterial and has been presented as an operating lease.

The lease requires monthly payments of $552 for 63 months beginning September 2010. Rent expense for the fiscal year ended totaled $6,624 and is included in administrative expenses in the accompanying financial statements. The minimum annual commitments under the non-cancelable lease is as follows:

20

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

Fiscal Year Ending Amount 2015 6,624 2016 3,060

Total $9,684

NOTE F - COMPENSATED ABSENCES

At June 30, 2014, employees of the authority have aooumulated and vested $79,182 of employee leave benefits, which was computed in accordance with GASB Codification Section 060. The leave payable is recorded in the accompanying financial statements. $46,158 is reported in long-term debt.

NOTE G - LONG TERM OBLIGATIONS

As of June 30, 2014, long term obligations consisted of compensated absences in the amount of $46158. The following is a summary of the changes in the long term obligations for the year ended June 30, 2014.

Compensated Absences

Balance as of July 1, 2013 $94,641 Additions 51,897 Deductions (67,356)

Balance as of June 30, 2014 79,182

Long term portion 46,158 Amount due in one year (Short term) $33,024

NOTE H - POST EMPLOYMENT RETIREMENT BENEFITS

The authority does not provide any post employment retirement benefits. Therefore the authority does not include any entries for unfunded actuarial accrued liability, net OPEB expense, or annual contribution required.

21

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

NOTE I- RETIREMENT PLAN

The authority participates in the Louisiana Housing Council Group Retirement Plan, administered by Broussard, Bush and Hurst, which is a defined contribution plan. The plan consists of employees of various local and regional housing authorities which are members of the Louisiana Housing Council. Through this plan, the authority provides pension benefits for all of its full-time employees. All full-time employees who have attained age 18 are eligible to participate in the plan on the first day of the month after completing three months of continuous and uninterrupted employment.

Under a defined contribution plan, benefits depend solely on amounts contributed to the plan plus investment earnings. The employer is required to make monthly contributions equal to seven percent of each participant's basic (excludes overtime) compensation. Employees are required to contribute five percent of their annual covered salary.

The authority's contribution for each employee and income allocated to the employee's account are fully vested after five years of continuous service. The authority's contributions and interest forfeited by employees who leave employment before five years of service are used to offset future contributions of the authority.

Normal retirement date shall be the first day of the month following the employee's sixty-fifth birthday. Early retirement may be elected on the first day of any month within 10 years of the employee's normal retirement date, provided the employee has completed five years of service with the authority. With the authority's consent, employees may defer retirement to the first day of any month beyond normal retirement date.

The authority's total payroll for the year ended June 30, 2014, was $923,812. The authority's contributions were calculated using the base salary amount of $669,637. The authority made the required contributions of $46,875 for the year ended June 30, 2014.

NOTE J- RISK MANAGEMENT

The authority is exposed to various risks of loss related to torts; theft of, damage to, and destruction of assets; errors and omissions, injuries to employees; and natural disasters. The authority's risk management program encompasses obtaining property and liability insurance.

22

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

The authority transfers risk of loss by participating in a public entity risk pool and contracting with a commercial insurance carrier for all major categories of exposed risk.

This includes coverage of property, general liability, public liability, and workers compensation. The risk pool and insurance contracted are obligated to meet settlements up to the maximum coverage, after the authority's deductions are met.

There has been no significant reduction in insurance coverages from coverages in the prior year. In addition, there have been no significant claims that have exceeded commercial insurance coverages in any of the past three fiscal years.

NOTE K - LITIGATION AND CLAIMS

At June 30, 2014, the authority is involved in litigation. Management and the authority's attorneys believe that the authority's insurance coverage would cover any potential losses due to adverse litigation. The authority may be responsible for the amount of insurance deductible, which is not a material amount. The financial statements do not include recordation of any litigation contingency.

NOTE L - FEDERAL COMPLIANCE CONTINGENCIES

The authority is subject to possible examinations by federal regulators who determine compliance with terms, conditions, laws and regulations governing grants given to the entity in the current and prior years. These examinations may result in required refund by the entity to federal grantors and/or program beneficiaries. The authority is subject to HDD's consideration of reducing grants in order to have the authority utilize authority Equity to fund expenses.

NOTE M - SUBSEQUENT EVENTS

Subsequent to the FYE, the authority entered into an agreement with another local housing authority whereby OHA will manage the operations of the other housing authority. OHA should benefit financially from the agreement with little liability incurred. HUD encouraged and pre-approved the management agreement.

23

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana Notes to the Financial Statements, 2014 - continued

NOTE N- ECONOMIC DEPENDENCE

Statement of Financial Accounting Standard (SFAS) No. 14 requires disclosure in financial statements of a situation where one entity provides more than 10% of the audited entity's revenues. The Department of Housing and Urban Development provided $3,094,331 to the authority, which represents approximately 63% of the authority's total revenue for the year.

24

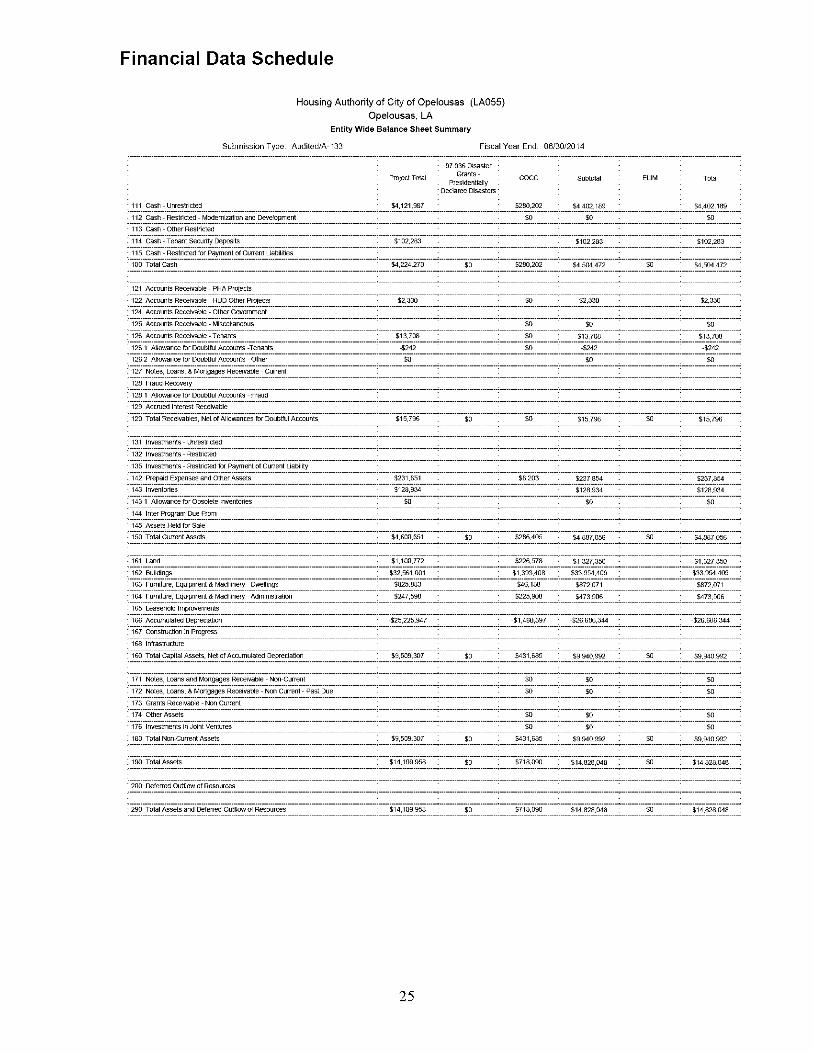

Financial Data Schedule

Housing Authority of City of Opelousas (LA055) Opelousas, LA

Entity Wide Balance Sheet Summary

Submission Type: Audite<l/A-133 Fiscal Year End: 06/30/2014

Project Totd

97.036 Disaster Grants-

Presldentl^ Declared Disasters

COCC Subtotal ELIM Total

111 Cash - Unrestricted $4,121,987 $280,202 K402,189 $4,402,189

112 Cash - Restricted - Modernization and Oevelc^imeht $0 $0 $0

113 Cash - Other Restricted

114 Cash - Tenant Secifflty Oeposrts $102,283 $102,283 $102,283

115 Cash - Restricted lor Paymoit of Current Liaillltles

100 Total Cash $4^24,270 $0 $280,202 $4,504,472 $0 $4,504,472

121 Accounts Recelwajle - PHA Projects

122 Accounts Recelvatile-HUO Other Projects $2,330 $0 $2,330 $2,330

124 Accounts Recelvatile - Ottier Government

125 Accounts Recelvatile - MIscellaheous $0 $0 $0

126 Accounts Recelvatile-Tenants $13,708 $0 $13,708 $13,708

126.1 Allowance for Doubtful Accounts -Tenants -$242 $0 -$242 -$242

126.2 Allowance for Doubtful Accounts - Other SO $0 $0

127 Notes, Loans, S Mortgages Receivable - Current

128 Fraud Recovery

128.1 Allowance for Doubtful Accounts - Fraud

129 Accnjed Interest Receivable

120 Total Receivables, Net of Allowancesfor Doubtful Accounts $15,796 $0 SO $15,796 $0 $15,796

131 Investments-Unrestrcted

132 Investments - Restricted

135 Investments - Restricted tor Payment of Cunent Uablllty

142 Prepaid Expenses and Ottier Assets $231,651 $6,203 $237,854 $237,854

143 Inventories $128,934 $128,934 $128,934

143.1 Allowance for Obscaete Inventones $0 $0 $0

144 Inter Program Due From

145 Assets Held for Sale

ISO Total Current Assets $4,600,651 $0 $286,405 $4,887,056 $0 $4,887,056

161 Land $1,100,772 $226,578 $1,327,350 $1,327,350

162 Biildlngs $32,561,001 $1,393,408 $33,954,409 $33,954,409

163 Furniture, Equipment 8 ti4actweiy - Dwellihgs $825,883 $46,188 $872,071 $872,071

164 Furniture, Equipment 8 Mact&ieiy - AdrrinlstraUon $247,598 $225,908 $473,506 $473,506

165 Leasehold Improvements

166 Accumulated Depreciation -$25225,947 -$1,460,397 -$26,686,344 -$26,686,344

167 Construction In Progress

168 Irrtrastnjcture

160 Total Coital Assets, Net of Accumiiated Depreciation $9,509,307 $0 $431,685 $9,940,992 $0 $9,940,992

171 Notes, Loans and Mortgages Receivat^ - N(Bi-C4irrent $0 $0 $0

172 Notes, Loans, 8 tvloitgages Receivable - Non Cunent - Past Due $0 $0 $0

173 Grants Receivable - Non Current

174 Otfier Assets $0 $0 $0

176 Investments in Joinf Veitures $0 $0 $0

180 Total Non-Cunent Assets $9,509,307 $0 $431,685 $9,940,992 $0 $9,940,992

190 Total Assets $14,109,958 $0 $718,090 $14,828,048 $0 $14,828,048

200 Defered Outflow of Resources

290 Total Assets and Deferred Outflow of Resources $14,109,958 $0 $718,090 $14,828,048 $0 $14,828,048

25

Financial Data Schedule

Housing Authority of City of Opelousas (1_A055) Opelousas, LA

Entity Wide Balance Sheet Summary

Submission Type: AiJdited/A-133 Fiscai Year End: 06/30/2014

; 97.036 Disaster ;

\ i Projed Total : Grants - : ; Presldentl^ < ; Declared Disasters;

COCC SiAtolal EUM Total i

311 BankOvenSatI

312 Accounts Payatile <= 90 Days $78,142 $3,848 $81,990 $81,990

313 Accounts Payatile >90 Days Past Due

321 Accnjed Wage/Payroll Taxes Pay^e $13,919 $5,913 $19,832 $19,832

322 Accfued Compensated Atis^ces - Current Poftlon $19,291 $13,733 $33,024 $33,024

324 Accrued Contingency Liability

325 Accrued Interest Payable

331 Accounts Payable - HUD PHA Programs

332 Account Payable - PHA Projects

333 Accounts Payable - Other Government $76,080 $76,080 $76,000

341 Tenant Securty Deposits $102^83 $102,283 $102,283

342 Unearned Revenue $10,001 $10,001 $10,001

343 Current Portion ol Long-term Detit - Capital Projects/Mortgage ftevenue

344 Current Portion ol Long-term Detit - C^iwatmg Borrowings

346 OttierCunent Uabllltles

346 Accrued Uabllltles - oma-

347 Inter Program - Due To

348 LoanUabHity-Carent

310 Total Current Liabilities $299,716 $23,494 $323,210 $323,210

351 Long-temi Debt, Net of Cunent - Capital Projects/Mortgage Revenue

352 Long-temi Debt, Net of Cunent - Operating Borrowings

353 Non-current Liabilities - Ottier

354 Accroed Compensated Atisences - Non Ciarent $24,665 $21,493 $46,158 $46,158

355 Loan Uabllity - Non Current

356 FASB 5 Uabilites

357 Acoued Pension and OPEB Liabilities

350 Total Non-Cunent Liabilities $24,665 $0 $21,493 $46,158 $46,158

300 Total Ijabillties $324,381 $0 $44,987 $369,368 $369,368

400 Deterred Inflow Of ITesajrces

508.4 Net investmerfl In Capital Assets $9,509,307 $431,685 $9,940,992 $9,940,992

511.4 Restncted Net Posltlrxi

512.4 Unrestricted Net Position $4,276,270 $241,418 $4,517,688 $4,517,688

513 Total Equity-Na Assets/Po^on $13,785,577 $673,103 $14,458,680 $14,458,680

600 TotalUab.Def.lntlowofRes.,andEqulty-NdAssets/Poation $14,109,958 $718,090 $14,828,048 $14,828,048

26

Financial Data Schedule

Housing Authority of City of Opelousas (LA055) Opeiousas, LA

Entity Wide Revenue and Expense Summary

Submission Type: Audited/A-133 Fiscal Year End: 06/30/2014

Prcjed Total

97.036 Disaster Grants-

Presidentiaiiy Declared DBasters

COCC Sriilolai EUM Total

7Q300 Net Tenant Rentd Revenue $1,392,644 $0 $1,392,644 $1,392,644

70400 Tenant Revenue - Ottier $413,264 $413,264 $413,264

70500 Tola Tenant Revenue $1,805,908 $0 $0 $1,805,908 $0 $1,805,908

70600 HUD PHA Operating Grants $2,530,635 $0 $2,530,635 $2,530,635

70610 Capital Grants $563,696 $0 $563,696 $563,696

70710 Management Fee $483,948 $483,948 -$483,948 $0

70720 Asset Management Fee $82,800 $82,800 -$82,800 $0

70730 BOOK Keeping Fee $61,479 $61,479 -$61,479 $0

70740 Front Line Senrice Fee

70750 other Fees $0 $0 $0

70700 Total Fee Revenue $628,227 $628,227 -$628227 $0

70800 other Government Grants $4,908 $4,908 $4,908

71100 investment Income-Unrestrided $5,436 $8,748 $14,184 $14,184

71200 Mortgage interest income

71300 Proceeds from Disposrtion of Assets Fieid tor Sale

71310 Cost of Sale of Assets

71400 Fraud Recovery

71500 other Revenue $28,073 $28,073 $28,073

71600 Gain or Loss on Sale of Captai Assets

72000 investment Income - Restrided

70000 Total Revenue $4,905,675 $4,908 $665,048 $5,575,631 -$628,227 $4,947,404

91100 Adnmistrative Sdartes $147,944 $197,673 $345,617 $345,617

91200 Auditing Fees $14,190 $4,730 $18,920 $18,920

91300 Management Fee $483,948 $483,948 -$483,948 $0

91310 BooK-keepng Fee $61,479 $61,479 -$61,479 $0

91400 Advertsing and Martteting

91500 Empoyee Benetit contnbutions - Atthinisiralive $50,498 $61,703 $112,201 $112,201

91600 Office Expenses $29,263 $40,899 $70,162 $70,162

91700 Legal Expense $17,686 $17,686 $17,686

91800 Travel $37,830 $29,996 $67,826 $67,826

91810 Allocated Overhead

91900 Other $56,946 $32202 $89,148 $89,148

91000 Total Operating - Admxristrative $882,098 $0 $384,889 $1,266,987 -$545,427 $721,560

92000 Asset Management Fee $82,800 $82,800 -$82,800 $0

92100 Tenant Senrices - Salanes

92200 Relocation Costs

92300 Employee Benetit ContnbiRions - Tenant Services

92400 Tenant Senrices - Ottier

92500 Total Tenant Serwces $0 $0 $0 $0 $0 $0

93100 Water $303,357 $2,517 $305,874 $305,874

93200 Etedhdty $718,471 $21,499 $739,970 $739,970

93300 Gas $23,289 $1,666 $24,955 $24,955

93400 Fuel

93500 Labor

93600 Seiner

93700 Employee BenetilContnbulions-Utiiities

93800 Other Utilities Expense

93000 Total Uhiities $1,045,117 $0 $25,682 $1,070,799 $0 $1,070,799

27

Financial Data Schedule

Housing Authority of City of Opelousas (LA055)

Opeiousas, LA Entity Wide Revenue and Expense Summary

Submission Type: Audited/A-133 Fiscal Year End: 06/30/2014

FYoject Total

; 97.036 Disastef : : Grants- : I Presidentlaily • • Declared Disasters •

94100 Ordinary tulalntenance and Operations - Latxir $473,786 $53,068 $526,854 $526,854

94200 Ordinary ti/laintenance and Operations - Materlais and Ottier $239,926 $5,050 $244,976 $244,976

94300 Ordinary tvlaintenance and Operations Contracts $160,317 $1,770 $162,087 $162,087

94500 Empoyee Benetit Contributions - Ordinary tilaintenance $221,784 $7,793 $229,577 $229,577

94000 Total I4aintenance $1,095,813 $0 $67,681 $1,163,494 $0 $1,163,494

95100 Protective Services - LatKT $51,341 $51,341 $51,341

95200 Protective Services - Otfier Ccntract Costs

95300 Protectve Services - Other

95500 Empoyee Benetit Ccntnbutions - Protective Savices $19,851 $19,851 $19,851

95000 Total Protective Services $71,192 $0 $0 $71,192 $0 $71,192

96110 Property insurance $248,254 $11,792 $260,046 $260,046

96120 Liabiiity insurance $453 $151 $604 $604

96130 Workmen's Compaisation $21,444 $7,148 $28,592 $28,592

96140 All Oilier insurance

96100 Total insurance pyemiuns $270,151 $0 $19,091 $289,242 $0 $289,242

96200 Oilier Generai Expenses $62,291 $20,551 $82,842 $82,842

96210 Crvnpensated Absences

96300 Payments in Lieu of Taxes $76,000 $76,080 $76,080

96400 Bad debt - Tenant Rents $27,052 $0 $27,052 $0 $27,052

96500 Bad detit - ivlortgages

96600 Bad debt - Other

96800 Severance Expense

96000 Total Ottier General Expenses $165,423 $0 $20,551 $185,974 $0 $185,974

96710 interest ot Mortgage (or Bonds) Payatte

96720 interest on Notes Payable (Short and Long Term)

96730 Amortization ofBond issue Costs

96700 Total interest Ei^iense and Amortization Cost $0 $0 $0 $0 $0 $0

96900 T(^ Operating Expenses $3,612,594 $0 $517,894 $4,130,488 -$628,227 $3,502,261

97000 Excess of Operating Revenue Operating Expenses $1^93,081 $4,908 $147,154 $1,445,143 $0 $1,445,143

97100 Extraordinary Maintenance

97200 Casualty Losses - Non-capitailzed

97300 Housing Assistance Parents

97350 HAP Portabiilty-in

97400 Depreciation Expense $1,003,808 $66,720 $1,070,528 $1,070,528

97500 Fraud Losses

97600 Capital Outlays - Governmental Funds

97700 Debt Pnncipai Paymeit - Governmental Funds

97800 Dvreiilng Urxts Rent Expense

90000 TcXal Expenses $4,616,402 $0 $584,614 $5,201,016 -$628,227 $4,572,789

28

Financial Data Schedule

Housing Authority of City of Opelousas (LA055) Opelousas, LA

Entity Wide Revenue and Expense Summary

Submission Type: Audited/A-133 Fiscal Year End: 06/30/2014

• 97.036 Disasta ;

: Project Totai • Grants- • • Presidentiaiiy • ; Decided Cfeaslers;

COCC I SiXitotai I BUM Total 1

1 10010 Operating Transfer in $0 $4,908 $4,908 $4,908

i 10020 Operating transfer Out $0 -$4,908 -$4,908 -$4,908

i 10030 Operating Transfers frDrrtfto Pilmay Government $0 $0 $0

i 10040 Operating Transfers frorrVto Component LSiil $0 $0 $0 $0

i 10050 Proceeds from Notes, Loans and Bonds

i 10060 Proceeds from Property Saies

{ 10070 Extraordinary items. Net GainiLoss $0 $0 $0 $0

1 10080 Spedai items (Net GainTLoss) $0 $0 $0 $0

i 10091 inter Prefect Excess Cash Transfer in 1 $0 1 SO | $0 1

110092 inter Prqect Excess Cash Transfer Out ! $0 i SO | SO !

! 10093 Transfers between Program and Project - in $0 $0 $0 $0

i 10094 Transfers between Project and Program - Out $0 $0 $0 $0

1 10100 Totaotherlinancing Sources (Uses) $0 -$4,908 $4,908 $0 $0 $0

i 10000 Excess (Deficiency) ol Totai Reveiue Over (Under) Totai Ei^nses $289,273 $0 $85,342 $374,615 $0 $374,615

i 11020 Required Annual Debt Phncipai Payments $0 $0 $0 $0 $0

i 11030 Beginning Equity $13,496,304 $0 $587,761 $14,084,065 $14,084,065

! 11040 Prior Period Adjustments, Equity Transfers and Conedion of Errors $0 $0 $0 $0

j 11050 ChangesinCompensated/UrsenceBaiance

1 11060 ChangesinContingentLiaOiiityBaiance

i 11070 ChangesinUnrecognizedPensionTransitionLiability

1 11080 ChangesmSpecialTerm/SeNeranceBenefitsLiabiiity

1 11090 ChangesinAiiowanceforDoubtluiAccounts-OweiiingRents

M1100 Changes in Allowance for Doubtlui Accounts-OOier

i 11170 Administrative Fee Equity

j 11180 HousingAssistancePa^ditsEquity

! 11190 Umt Months Avaiiabie 8280 8280 8280

1 11210 Nixnber of LXiit Months Leased 8198 8198 8198

i 11270 Excess Cash $3,648,273 $3,648,273 $3,648,273

i 11610 Land Purchases $0 $0 $0 SO

1 11620 Buiiding Purcnases $530,741 $0 $530,741 $530,741

1 11630 Furniture & Equipment - Dweiiing Pirchases $32,955 $0 $32,955 $32,955

; 11640 Furniture & Equipment - Administrafive Pirchases $0 $0 $0 $0

I 11650 Leasefiold improvements Purcfiases $0 $0 $0 $0

i 11660 infrastructure Purcnases $0 $0 $0 $0

i 13510 CFFP Debt Senrice Payments $0 $0 $0 $0

113901 Replacement Housing Factor Fmds $0 $0 $0 $0

29

William Daniel McCaskill, CPA A Professional Accounting Corporation

415 Magnolia Lane Mandeville, Louisiana 70471

Telephone 866-829-0993 Member of Fax 225-665-1225 Louisiana Society of CPA's E-mail [email protected] American Institute of CPA's

Independent Auditor's Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial

Statements Performed in Accordance With Government Auditing Standards

Board of Commissioners Housing Authority of the City of Opelousas Opeiousas, Louisiana

I have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the Housing Authority of the City of Opelousas, as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the authority's basic financial statements, and have issued my report thereon dated November 12, 2014.

Internal Control Over Financial Reporting

In planning and performing my audit of the financial statements, I considered the authority's internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing my opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the authority's internal control. Accordingly, I do not express an opinion on the effectiveness of the authority's internal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material v\/eakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

30

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Report on Internal Control... Goue/7?/T7e/?Mi;c//f/7?sf Standards, 2014 Page Two

My consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during my audit I did not identify any deficiencies in internal control that I consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the authority's financial statements are free from material misstatement, I performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of my audit, and accordingly, I do not express such an opinion. The results of my tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of my testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity's internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity's internal control and compliance. Accordingly, this communication is not suitable for any other purpose. Under Louisiana Revised Statute 24:513, this report is distributed by the Legislative Auditor as a public document.

'WilEam (DanieC ̂ McCas^H

William Daniel McCaskill, CPA A Professional Accounting Corporation

November 12, 2014

31

William Daniel McCaskill, CPA A Professional Accounting Corporation

415 Magnolia Lane Mandeville, Louisiana 70471

Telephone 866-829-0993 Member of Fax 225-665-1225 Louisiana Society of CPA's E-mail [email protected] American Institute of CPA's

independent Auditor's Report on Compiiance For Each Major Federal Program and on internal Control Over Compiiance Required by 0MB Circular A-133

Board of Commissioners Housing Authority of the City of Opeiousas Opelousas, Louisiana

Report on Compiiance for Each Major Federal Program

I have audited the Housing Authority of the City of Opelousas's compliance with the types of compliance requirements described in the 0MB Circular A-133 Compliance Supplement that could have a direct and material effect on each of the authority's major federal programs for the year ended June 30, 2014. The authority's major federal programs are identified in the summary of auditor's results section of the accompanying schedule of findings and questioned costs.

Managements Responsibility

Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to its federal programs.

Auditor's Responsibility

My responsibility is to express an opinion on compliance for each of the authority's major federal programs based on my audit of the types of compliance requirements referred to above. I conducted my audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and OMBCircular A-133, Audits of States, Local Governments, and Non-ProfIt Organizations. Those

32

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Report on Compliance...A-133, 2014 Page Two

standards and OMB Circular A-133 require that I plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about the authority's compliance with those requirements and performing such other procedures as I considered necessary in the circumstances.

I believe that my audit provides a reasonable basis for my opinion on compliance for each major federal program. However, my audit does not provide a legal determination of the authority's compliance.

Opinion on Each Major Federai Program

In my opinion, the authority complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended June 30, 2014.

Report on Internal Control Over Compliance

Management of the authority is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing my audit of compliance, I considered the authority's internal control over compliance with the types of requirements that could have a direct and material effect on each major federal program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and to test and report on internal control over compliance in accordance with OMB Circular A-133, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, I do not express an opinion on the effectiveness of the authority's internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material v\/eakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in Internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance.

33

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Report on Compliance...A-133, 2014 Page Three

My consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. I did not identify any deficiencies in internal control over compliance that I consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

The purpose of this report on internal control over compliance is solely to describe the scope of my testing of internal control over compliance and the results of that testing based on the requirements of OMB Circular A-133. Accordingly, this report is not suitable for any other purpose. Under Louisiana Revised Statute 24:513, this report is distributed by the Legislative Auditor as a public document.

'WilEam (DanieC ̂ McCas^CC

William Daniel McCaskill, CPA A Professional Accounting Corporation

November 12, 2014

34

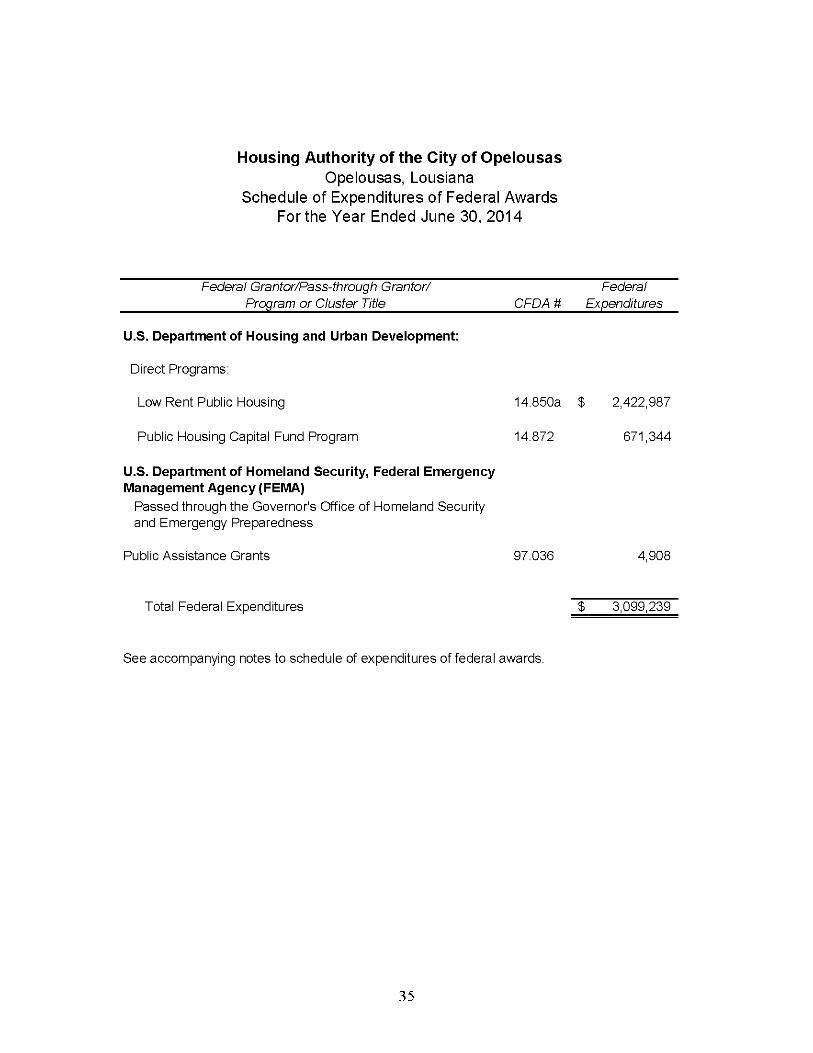

Housing Authority of the City of Opelousas Opelousas, Lousiana

Schedule of Expenditures of Federal Awards Forthe Year Ended June 30, 2014

Federal Grantor/Pass-through Grantor/ Federal Program or Cluster Title CFDA # Expenditures

U.S. Department of Housing and Urban Development:

Direct Programs:

Low Rent Public Housing 14.850a $ 2,422,987

Public Housing Capital Fund Program 14.872 671,344

U.S. Department of Homeland Security, Federal Emergency Management Agency (FEMA)

Passed through the Governor's Office of Homeland Security and Emergengy Preparedness

Public Assistance Grants 97.036 4,908

Total Federal Expenditures $ 3,099,239

See accompanying notes to schedule of expenditures of federal awards.

35

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Notes to the Schedule of Expenditures of Federal Awards For the Year Ended June 30, 2014

NOTE A - General

The accompanying Schedule of Expenditures of Federal Awards presents all of the Federal awards programs of the Authority. The authority reporting entity is defined in Note 1 to the basic financial statements. Federal awards received directly from federal agencies, as well as federal awards passed through other governmental agencies are included in this schedule.

NOTE B - Basis of accounting

The accompanying Schedule of Expenditures of Federal Awards Programs is presented using the accrual basis of accounting, which is described in Note 1 to the authority's basic financial statements.

NOTE C - Relationship to Basic Financial Statements

Federal awards revenues are reported in the authority's basic financial statements as follows:

Low Rent Public Housing $2,422,987 Public Housing Capital Fund Program $ 671,344 Public Assistance Grants $ 4,908

NOTE D - Relationship to Federal Financial Reports

Amounts reported in the accompanying schedule agree with the amounts reported in the related federal financial reports except for changes made to reflect amounts in accordance with GAAP.

NOTE E- FEDERAL AWARDS

For those funds that have matching revenues and state funding, federal expenditures were determined by deducting matching revenues from total expenditures. In accordance with HUD Notice PIH 9814, "federal awards" do not include the authority's operating income from rents or investments (or other Non-federal sources). In addition, the entire amount of operating subsidy received and/or accrued during the fiscal year is considered to be expended during the fiscal year.

36

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Schedule of Findings and Questioned Costs Fiscal Year Ended June 30, 2014

Section I—Summary of Auditor's Results

Financial Statements Type of auditor's report issued

Internal control over financial reporting:

Material weakness(es) identified?

Significant deficiency(ies) identified?

Noncompliance material to financial statements noted?

Federal Awards

Internal control over major programs:

Material weakness(es) identified?

Significant deficiency(ies) identified?

Unmodified

_yes

_yes

_yes

_yes

X no

_X none reported

X no

X no

_yes _X none reported

Type of auditor's report issued on compliance for major programs: Unmodified

Any audit findings disclosed that are required to be reported in accordance with section510(a) of OMB Circular A-133? _yes X no

Identification of major programs:

14.850 Public and Indian Housing - Low Rent Program

37

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Schedule of Findings and Questioned Costs (Continued) Fiscal Year Ended June 30, 2014

The threshold used for distinguishing between Type A and B programs was $300,000.

Auditee qualified as a low-risk auditee? ^yes X no

SECTION II - FINDINGS - FINANCIAL STATEMENTS AUDIT

None

SECTION III - FEDERAL AWARDS FINDINGS AND QUESTIONED COST

None

38

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Schedule of Prior Year Audit Findings Fiscal Year Ended June 30, 2014

There were no findings in the prior audit.

39

HOUSING AUTHORITY OF THE CITY OF OPELOUSAS Opelousas, Louisiana

Schedule of Compensation Paid to Board Members Fiscal Year Ended June 30, 2014

Board members serve without compensation.

40

![The Opelousas courier (Opelousas, La.) 1889-05-04 [p ]chroniclingamerica.loc.gov/lccn/sn83026389/1889-05-04/ed-1/seq-1.pdf · qtdlished 1852.t itablisihed 1852. official journal of](https://img.pdfslide.net/doc/110x75/5d30a8c988c9937b5d8cc6f5/the-opelousas-courier-opelousas-la-1889-05-04-p-qtdlished-1852t-itablisihed.jpg)

![The Opelousas courier (Opelousas, La.) 1855-02-03 [p ]chroniclingamerica.loc.gov/lccn/sn83026389/1855-02-03/ed-1/seq-1.pdf · ce nom, estua compos d'ides htrognes qaijreiit de se](https://img.pdfslide.net/doc/110x75/5b98bb9a09d3f2fd558c8bbd/the-opelousas-courier-opelousas-la-1855-02-03-p-ce-nom-estua-compos.jpg)

![The Opelousas courier (Opelousas, La.) 1854-04-29 [p ] · 2017. 12. 14. · pMr.t have been uent . more e frequenthtio amusna, whenat all the of Ito •olEti • ae mtlritles aod](https://img.pdfslide.net/doc/110x75/60953d0a380c404bc467682b/the-opelousas-courier-opelousas-la-1854-04-29-p-2017-12-14-pmrt-have.jpg)

![The Opelousas courier (Opelousas, La.) 1896-10-17 [p ] · 2017. 12. 15. · exceptionally tile mantler, as wvas sh0own by tihe appreciation of the audience. Prof. Mayer and Miss Alice](https://img.pdfslide.net/doc/110x75/60e4c894e37a3971142d2a5b/the-opelousas-courier-opelousas-la-1896-10-17-p-2017-12-15-exceptionally.jpg)

![The Opelousas courier (Opelousas, La.) 1854-01-21 [p ] · 2017. 12. 14. · Paroisse t. Landry, le Jeudi, 16 Fvrier prochain, 1854, les proprits suivantes, appartenant la suc-cession](https://img.pdfslide.net/doc/110x75/60b33bdafbadb23854289823/the-opelousas-courier-opelousas-la-1854-01-21-p-2017-12-14-paroisse.jpg)

![The Opelousas courier (Opelousas, La.) 1859-04-09 [p ] · 2017-12-14 · II eatjuste'de reconilaitre cependant que cette ar-deur pour la pair se trouve aussi dans certaines re-gions](https://img.pdfslide.net/doc/110x75/5ed0672aec773d44031be850/the-opelousas-courier-opelousas-la-1859-04-09-p-2017-12-14-ii-eatjustede.jpg)

![The Opelousas courier (Opelousas, La.) 1877-03-03 [p ]€¦ · Opelousas Courier OPELOUSAS. . LOUISIANA. LONGFELLOW'S LAST POEM1. Mtr. Tongfellowj a poen, in the current Atlantic](https://img.pdfslide.net/doc/110x75/5f160f6605977d65981b2702/the-opelousas-courier-opelousas-la-1877-03-03-p-opelousas-courier-opelousas.jpg)

![The Opelousas courier (Opelousas, La.) 1854-08-26 [p ] · of the New Orleans, Opelousas and Great Western Rail Road, except on that portion lying between the Lafourche and. Algiers](https://img.pdfslide.net/doc/110x75/5f3d628a7ce4ac52d904b224/the-opelousas-courier-opelousas-la-1854-08-26-p-of-the-new-orleans-opelousas.jpg)

![The Opelousas courier (Opelousas, La.) 1862-01-11 [p ]- Gen. McClellan is quite unwell, and Gen. Marcy, Chief of Staff, too ill toattend to duty. Senator Chandler, of Michigau, advocates](https://img.pdfslide.net/doc/110x75/5e9e1df5bbdecc13af15610a/the-opelousas-courier-opelousas-la-1862-01-11-p-gen-mcclellan-is-quite.jpg)

![The Opelousas courier (Opelousas, La.) 1868-11-21 [p ]](https://img.pdfslide.net/doc/110x75/62ab6606052f1a516f4e8cb5/the-opelousas-courier-opelousas-la-1868-11-21-p-.jpg)

![The Opelousas courier (Opelousas, La.) 1853-11-26 [p ]](https://img.pdfslide.net/doc/110x75/6187117758a27c160d4fe10e/the-opelousas-courier-opelousas-la-1853-11-26-p-.jpg)

![The Opelousas courier (Opelousas, La.) 1853-04-30 [p ]...abetdhis btha'aeidcoitit, what he was before at-EB $ s iM crd• prineie.-If our neighbori, b 'write sine more mechrticles](https://img.pdfslide.net/doc/110x75/6068a5a49c96e0586b2f5460/the-opelousas-courier-opelousas-la-1853-04-30-p-abetdhis-bthaaeidcoitit.jpg)