Embed Size (px)

Citation preview

Housing Finance Policy Center Lunchtime Data Talk Credit Scoring: Going Beyond the Usual Sarah Davies, VantageScore Solutions Michael Turner, PERC Kenneth Brevoort, Consumer Financial Protection Bureau Laurie Goodman, Urban Institute

March 12, 2015

Alternative Data & Credit Scoring Sarah F. Davies

Senior Vice President, Analytics & Product Management

203-363-2162 VantageScore Solutions, LLC

VantageScore Solutions, LLC © 2014 2

Topics….

• Who can be scored using traditional credit file

data? • The scoreable universe • Criteria for scoring – three gating factors • How good is the score?

• Leveraging alternative data • Rent and utility data • Full-file or positive-only data

VantageScore Solutions, LLC © 2014 3

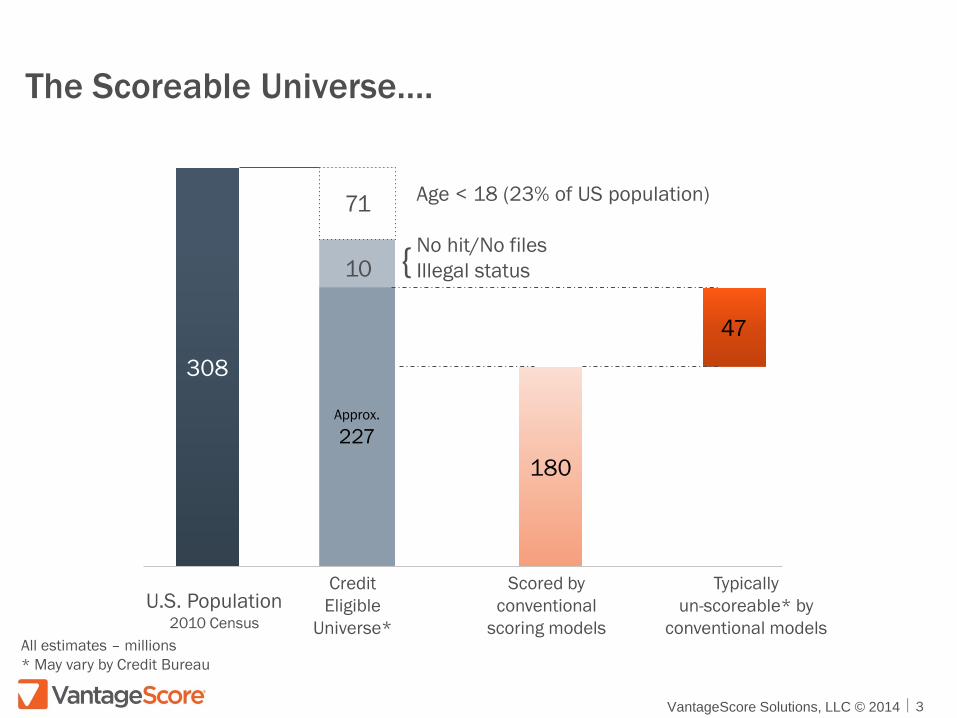

The Scoreable Universe….

308

Approx.

227 180

47

Scored by conventional

scoring models

Typically un-scoreable* by

conventional models U.S. Population

2010 Census

Credit Eligible

Universe*

Age < 18 (23% of US population)

No hit/No files Illegal status

All estimates – millions * May vary by Credit Bureau

{ 10

71

VantageScore Solutions, LLC © 2014 4

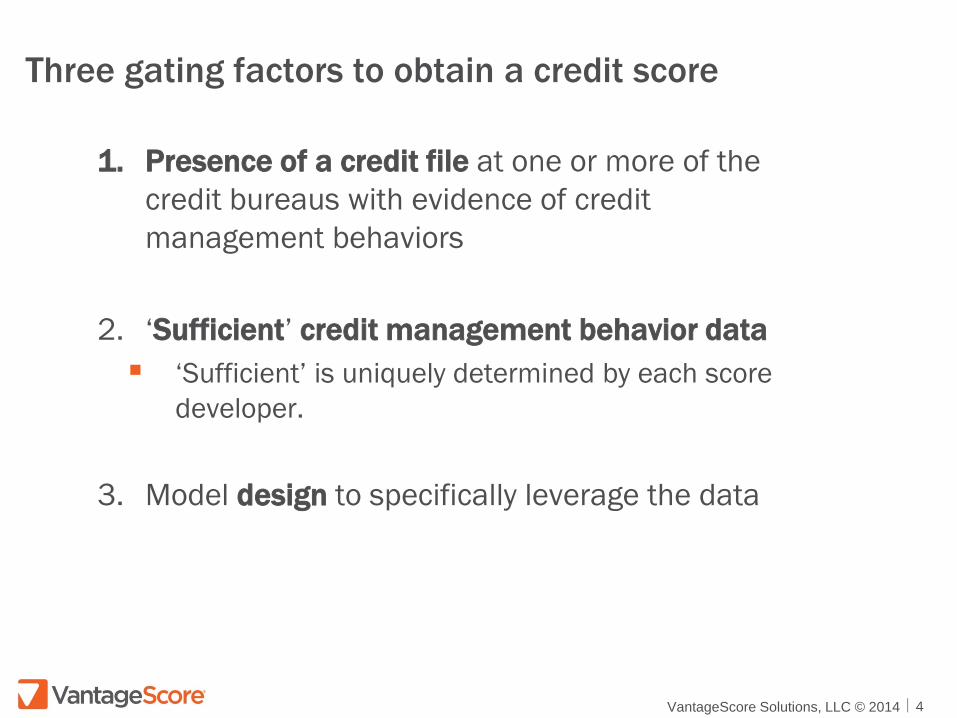

Three gating factors to obtain a credit score

1. Presence of a credit file at one or more of the credit bureaus with evidence of credit management behaviors

2. ‘Sufficient’ credit management behavior data ‘Sufficient’ is uniquely determined by each score

developer.

3. Model design to specifically leverage the data

VantageScore Solutions, LLC © 2014 5

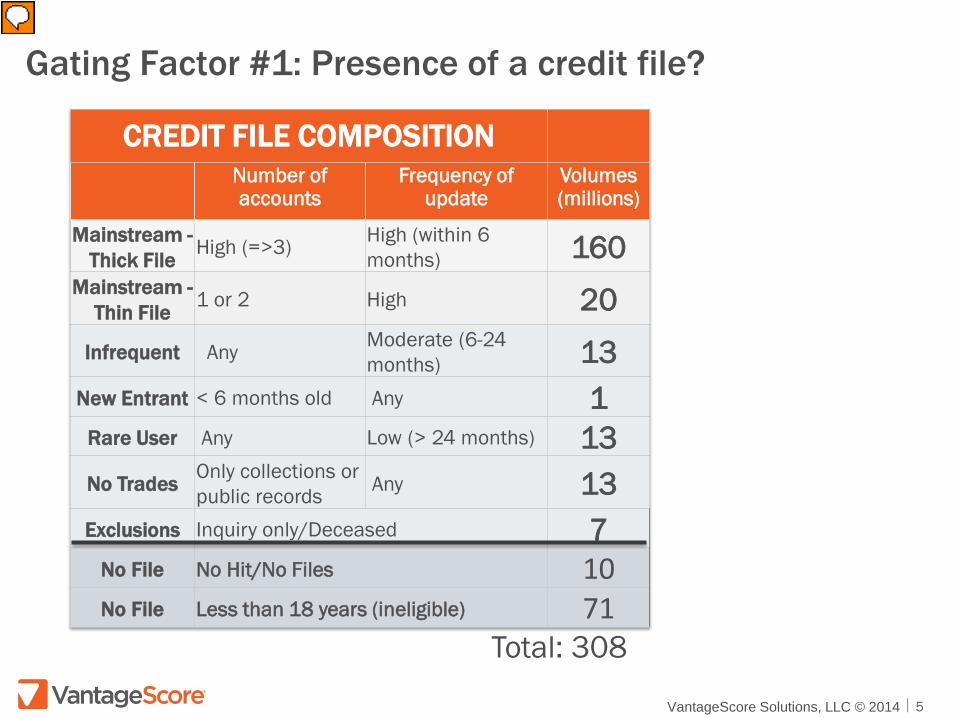

Gating Factor #1: Presence of a credit file?

CREDIT FILE COMPOSITION Number of accounts

Frequency of update

Volumes (millions)

Mainstream - Thick File High (=>3) High (within 6

months) 160 Mainstream -

Thin File 1 or 2 High 20 Infrequent Any Moderate (6-24

months) 13 New Entrant < 6 months old Any 1

Rare User Any Low (> 24 months) 13 No Trades Only collections or

public records Any 13 Exclusions Inquiry only/Deceased 7

No File No Hit/No Files 10 No File Less than 18 years (ineligible) 71

Total: 308

VantageScore Solutions, LLC © 2014 6

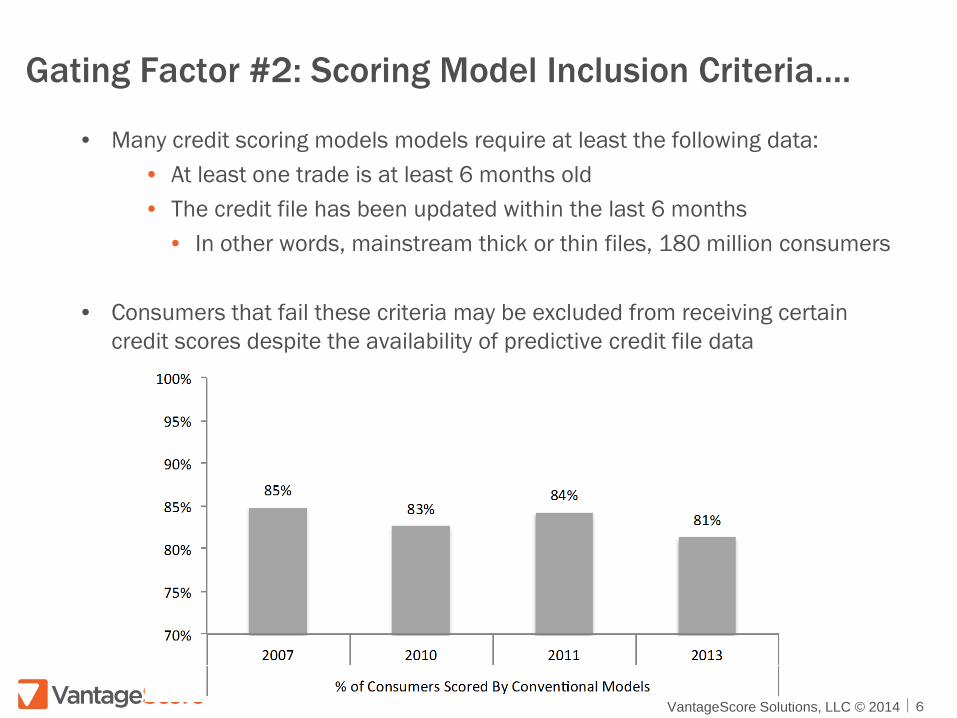

Gating Factor #2: Scoring Model Inclusion Criteria….

• Many credit scoring models models require at least the following data: • At least one trade is at least 6 months old • The credit file has been updated within the last 6 months

• In other words, mainstream thick or thin files, 180 million consumers

• Consumers that fail these criteria may be excluded from receiving certain credit scores despite the availability of predictive credit file data

VantageScore Solutions, LLC © 2014 7

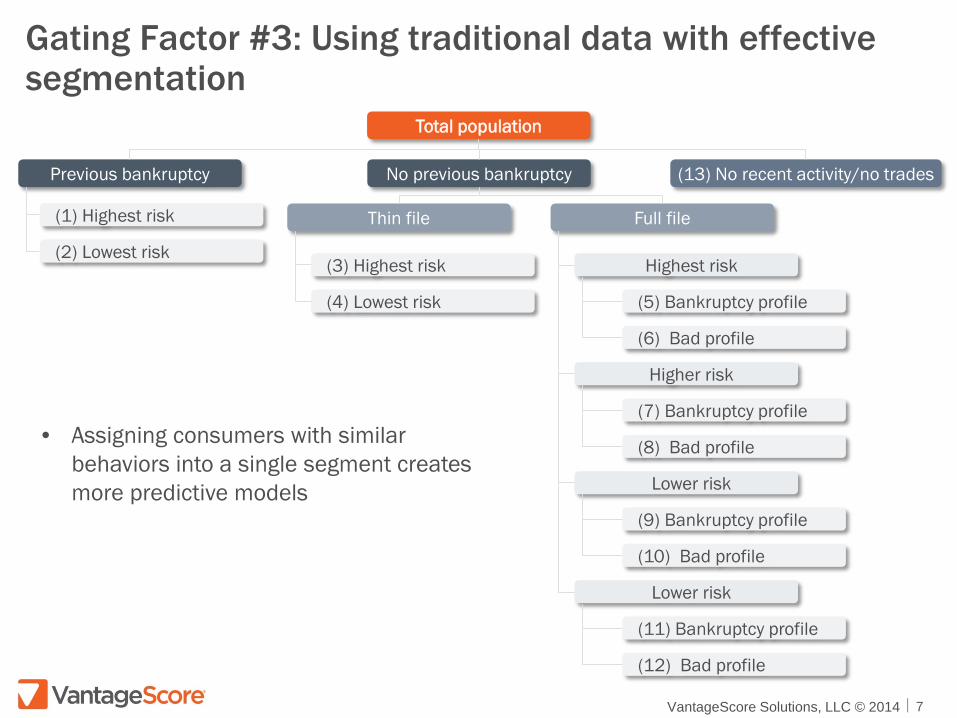

Gating Factor #3: Using traditional data with effective segmentation

Previous bankruptcy No previous bankruptcy

Thin file

Total population

(13) No recent activity/no trades

Full file (1) Highest risk

(2) Lowest risk (3) Highest risk

(4) Lowest risk

Highest risk

Higher risk

(5) Bankruptcy profile

(6) Bad profile

(7) Bankruptcy profile

(8) Bad profile

Lower risk

(9) Bankruptcy profile

(10) Bad profile

Lower risk

(11) Bankruptcy profile

(12) Bad profile

• Assigning consumers with similar behaviors into a single segment creates more predictive models

VantageScore Solutions, LLC © 2014 8

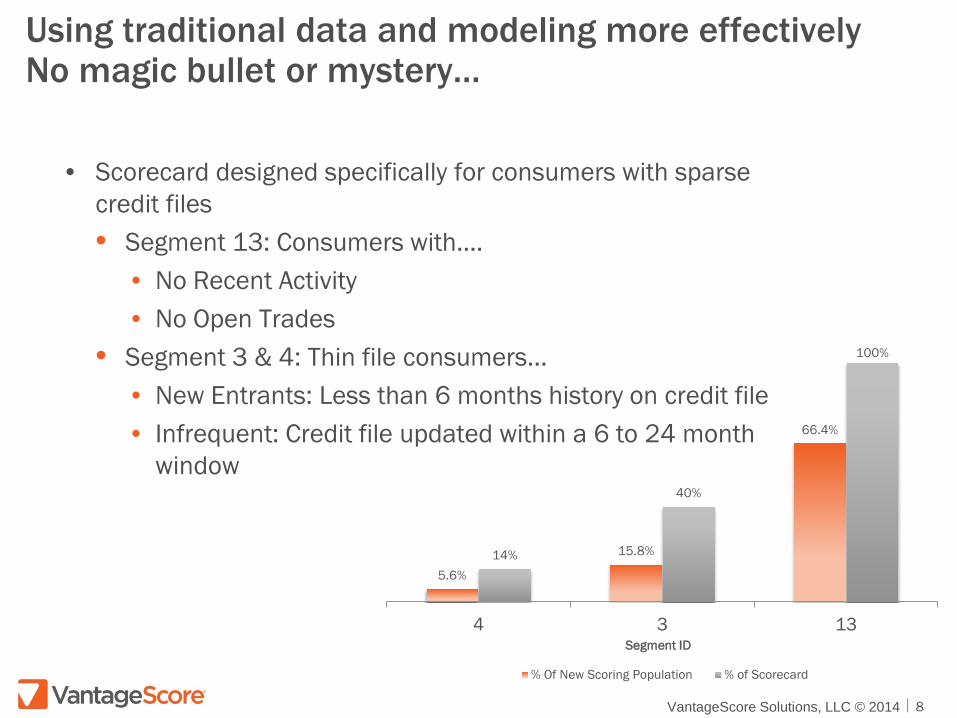

Using traditional data and modeling more effectively No magic bullet or mystery…

• Scorecard designed specifically for consumers with sparse

credit files • Segment 13: Consumers with….

• No Recent Activity • No Open Trades

• Segment 3 & 4: Thin file consumers... • New Entrants: Less than 6 months history on credit file • Infrequent: Credit file updated within a 6 to 24 month

window

5.6%

15.8%

66.4%

14%

40%

100%

4 3 13Segment ID

% Of New Scoring Population % of Scorecard

VantageScore Solutions, LLC © 2014 9

Segment 13 – Strongest predictive variable

• Number of unpaid external collections with balances greater than $250 • Provides meaningful predictive insight when included in

the appropriate segments

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Def

ault

Rate

VantageScore Solutions, LLC © 2014 10

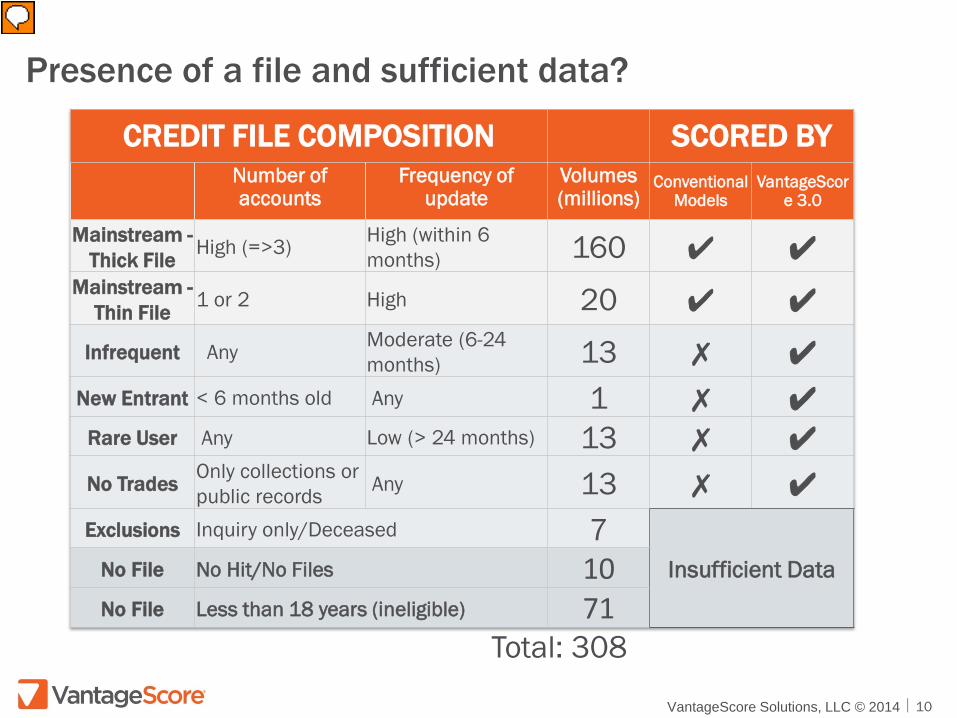

Presence of a file and sufficient data?

CREDIT FILE COMPOSITION SCORED BY Number of accounts

Frequency of update

Volumes (millions)

Conventional Models

VantageScore 3.0

Mainstream - Thick File High (=>3) High (within 6

months) 160 ✔ ✔ Mainstream -

Thin File 1 or 2 High 20 ✔ ✔ Infrequent Any Moderate (6-24

months) 13 ✗ ✔ New Entrant < 6 months old Any 1 ✗ ✔

Rare User Any Low (> 24 months) 13 ✗ ✔ No Trades Only collections or

public records Any 13 ✗ ✔ Exclusions Inquiry only/Deceased 7

Insufficient Data No File No Hit/No Files 10 No File Less than 18 years (ineligible) 71

Total: 308

VantageScore Solutions, LLC © 2014 11

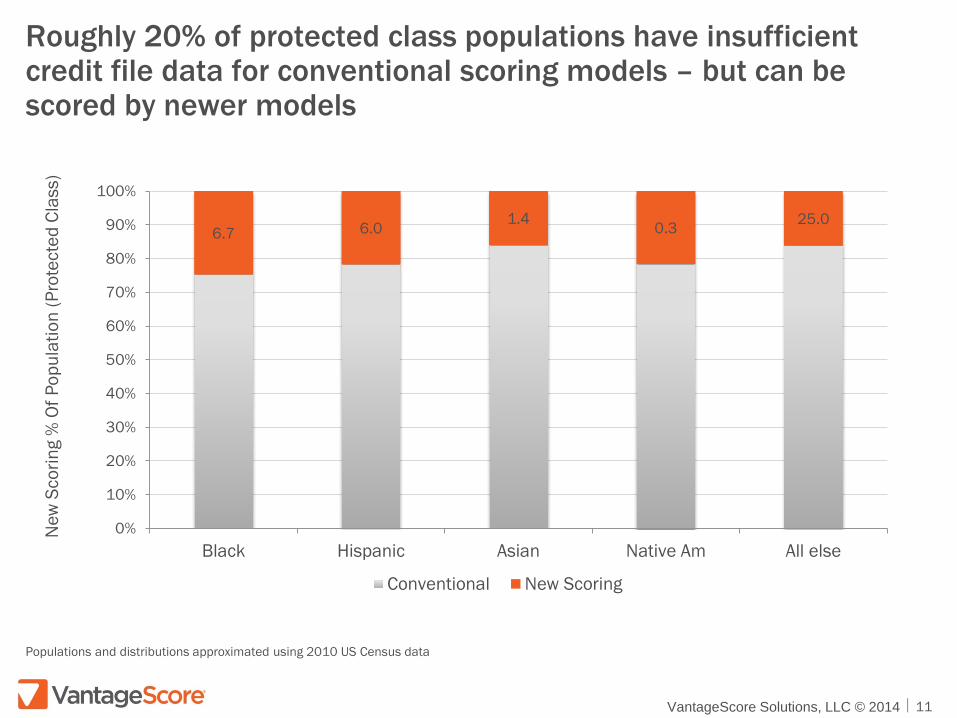

Roughly 20% of protected class populations have insufficient credit file data for conventional scoring models – but can be scored by newer models

6.7 6.0 1.4 0.3 25.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Black Hispanic Asian Native Am All else

Conventional New Scoring

New

Sco

ring

% O

f Pop

ulat

ion

(Pro

tect

ed C

lass

)

Populations and distributions approximated using 2010 US Census data

VantageScore Solutions, LLC © 2014 12

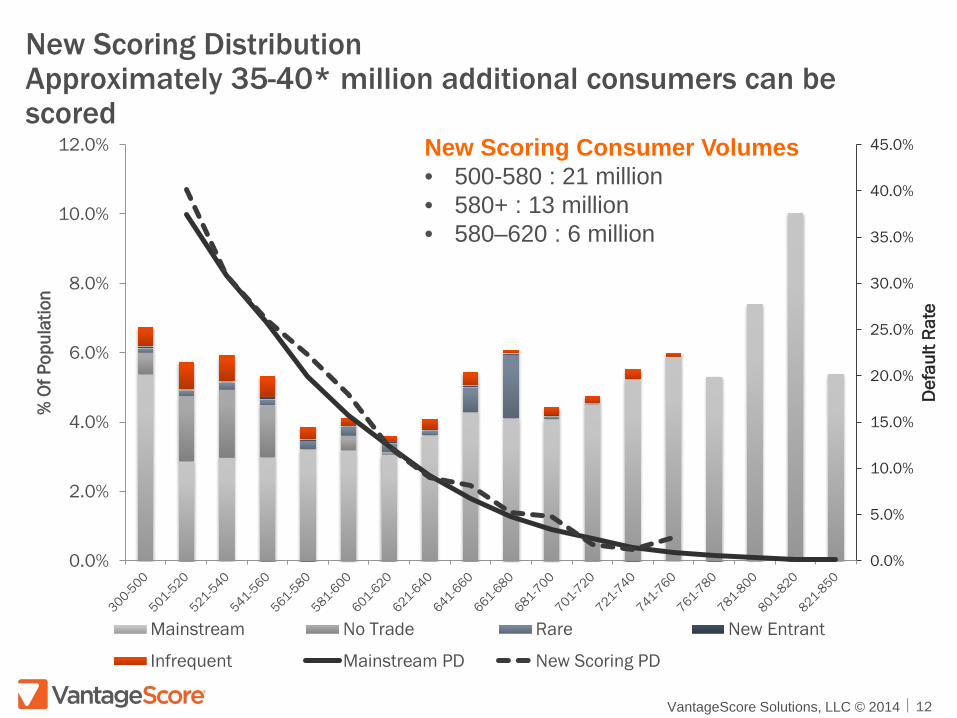

New Scoring Distribution Approximately 35-40* million additional consumers can be scored

New Scoring Consumer Volumes • 500-580 : 21 million • 580+ : 13 million • 580–620 : 6 million

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Def

ault

Rate

% O

f Pop

ulat

ion

Mainstream No Trade Rare New Entrant

Infrequent Mainstream PD New Scoring PD

VantageScore Solutions, LLC © 2014 13

• Up to 93% (~220 million consumers) of the credit eligible population can be scored using traditional credit data

• Leveraging alternative data to score the remainder

VantageScore Solutions, LLC © 2014 14

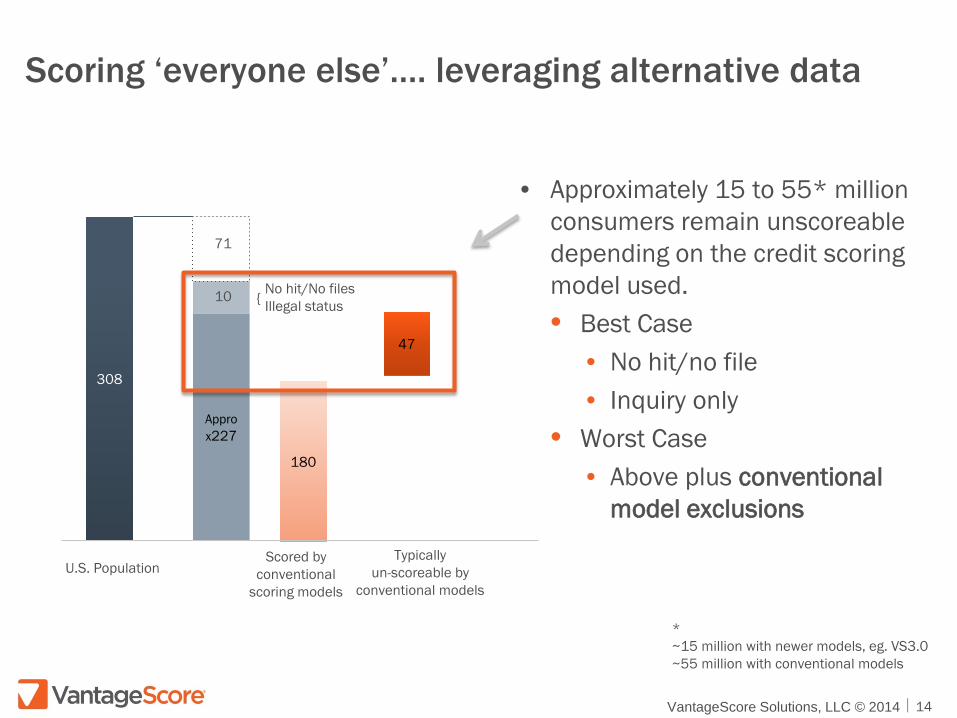

Scoring ‘everyone else’…. leveraging alternative data

• Approximately 15 to 55* million consumers remain unscoreable depending on the credit scoring model used. • Best Case

• No hit/no file • Inquiry only

• Worst Case • Above plus conventional

model exclusions

308

Approx227

180

47

Scored by conventional

scoring models

Typically un-scoreable by

conventional models U.S. Population

No hit/No files Illegal status { 10

71

* ~15 million with newer models, eg. VS3.0 ~55 million with conventional models

VantageScore Solutions, LLC © 2014 15

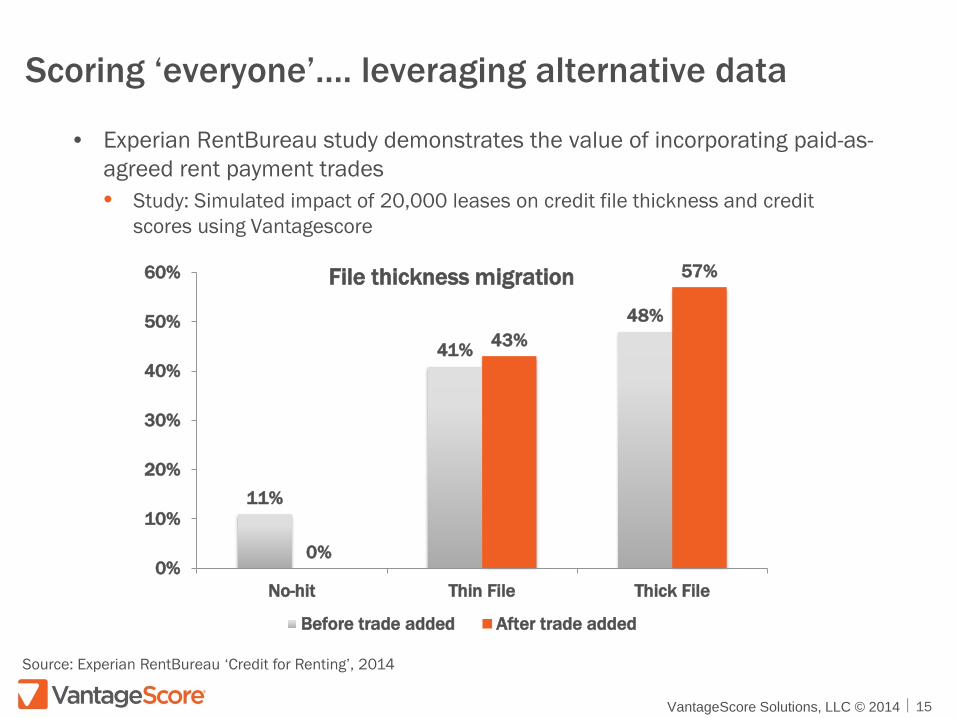

Scoring ‘everyone’…. leveraging alternative data

• Experian RentBureau study demonstrates the value of incorporating paid-as-agreed rent payment trades • Study: Simulated impact of 20,000 leases on credit file thickness and credit

scores using Vantagescore

11%

41%

48%

0%

43%

57%

0%

10%

20%

30%

40%

50%

60%

No-hit Thin File Thick File

Before trade added After trade added

Source: Experian RentBureau ‘Credit for Renting’, 2014

File thickness migration

VantageScore Solutions, LLC © 2014 16

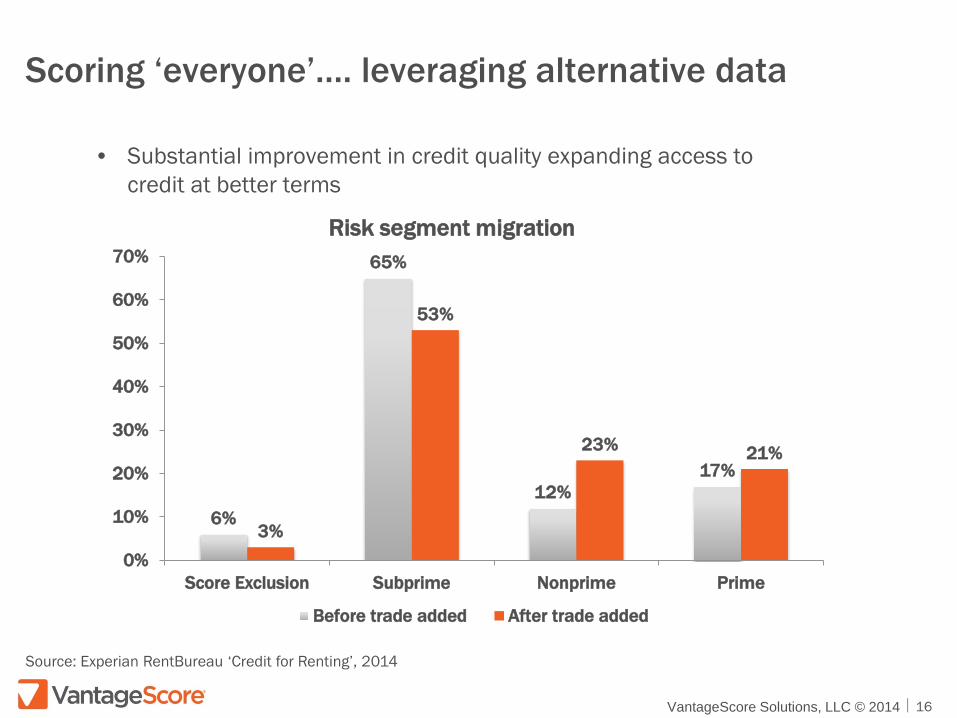

Scoring ‘everyone’…. leveraging alternative data

• Substantial improvement in credit quality expanding access to credit at better terms

6%

65%

12% 17%

3%

53%

23% 21%

0%

10%

20%

30%

40%

50%

60%

70%

Score Exclusion Subprime Nonprime Prime

Before trade added After trade added

Source: Experian RentBureau ‘Credit for Renting’, 2014

Risk segment migration

VantageScore Solutions, LLC © 2014 17

Scoring ‘everyone’…. leveraging alternative data

• Similar results are observed when incorporating positive energy-utility data (Experian ‘Let There Be Light’, 2015) • 20% of thin file consumers migrated to thick file • Subprime population reduced by 47%

• Several challenges remain with these data

• Data quality and accuracy • Universal reporting • Impact of consumer utility laws

• However, it’s a positive sign that major credit scores now

incorporate rental payments when available on the consumer’s primary credit file

VantageScore Solutions, LLC © 2014 18

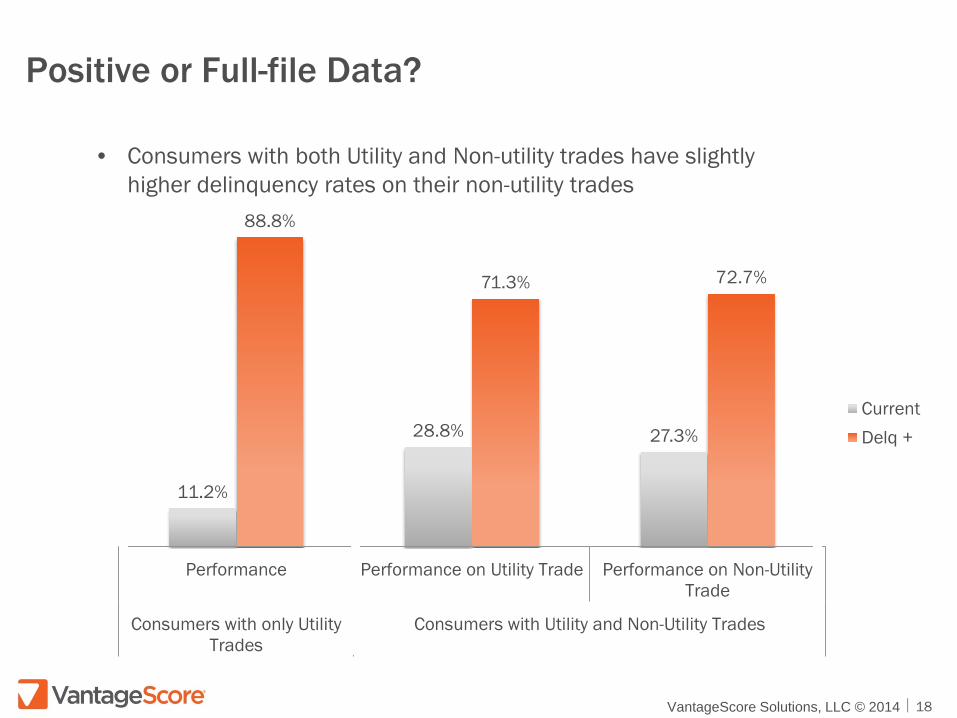

Positive or Full-file Data?

• Consumers with both Utility and Non-utility trades have slightly higher delinquency rates on their non-utility trades

11.2%

28.8% 27.3%

88.8%

71.3% 72.7%

Performance Performance on Utility Trade Performance on Non-UtilityTrade

Consumers with only UtilityTrades

Consumers with Utility and Non-Utility Trades

CurrentDelq +

Credit Scoring:

19

Going Beyond the

Usual

PERC Presentation: March 12th, 2015 Urban Institute—Washington, DC

Select PERC Supporters Include…

Foundations & Nonprofits

Government & Multilaterals

Trade Associations

Private Organizations

20

Our Footprint

Africa Cameroon Kenya South Africa Tanzania

North America/ Caribbean Canada Mexico Trinidad & Tobago United States of America

Asia Brunei China Hong Kong India Indonesia Japan Malaysia Philippines Singapore Sri Lanka Thailand

Australia/Oceania Australia New Zealand Europe France

Central/South America Bolivia Brazil Chile Colombia Guatemala Honduras 21

PERC’s Alternative

Data Initiative

(ADI) PERC advocates the inclusion of alternative data for use in credit granting

alternative = regular bill payment data from telecoms, energy utilities, rental payments and other such non-financial services that are valuable inputs for credit decisions

Q: Who benefits from ADI? A: The credit-underserved population The credit-underserved population is estimated to include the estimated 54 to 70 million Credit Invisible:

Immigrants

Students and young adults

Elderly Americans

Consumers operating on a cash basis

Minorities

Consumers trying to establish a good credit rating without new debt

23

PERC’s ADI Research

Select ADI Publications 2004 Giving Underserved Consumers Better Access to Credit Systems 2006 Give Credit where Credit is Due (w/Brookings Institution) 2008 You Score You Win 2009 New to Credit from Alternative Data 2009 Credit Reporting Customer Payment Data 2012 A New Pathway to Financial Inclusion 2012 The Credit Impacts on Low-Income Americans from Reporting Moderately Late Payment Data

24

25

A New Pathway to Financial Inclusion:

26

ALTERNATIVE DATA, CREDIT BUILDING, AND RESPONSIBLE LENDING IN THE WAKE OF THE GREAT RECESSION

June 2012

27

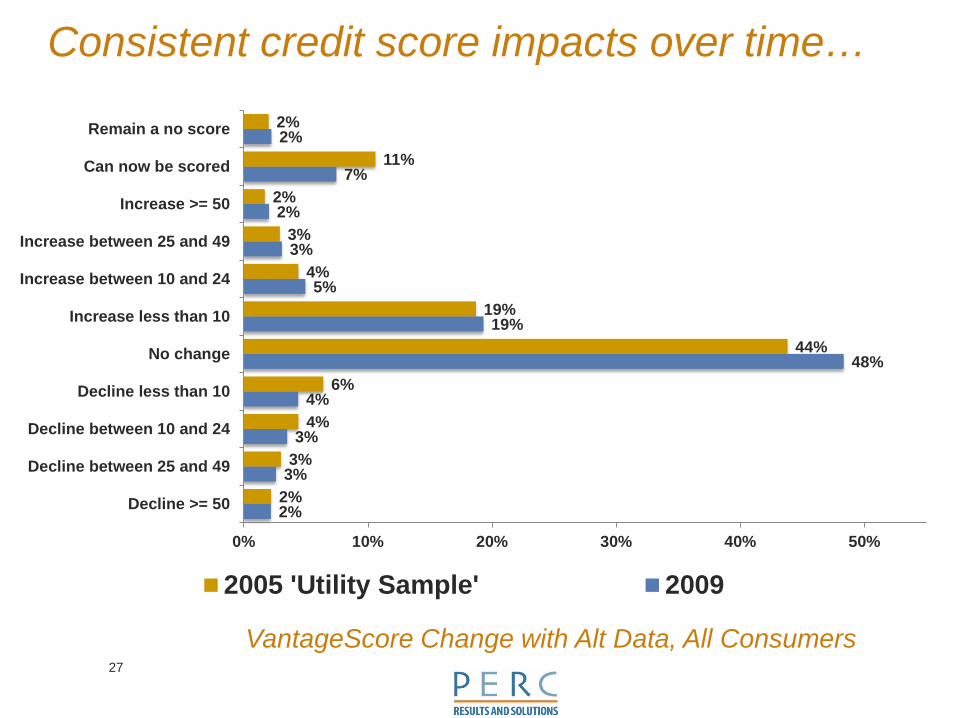

2%

3%

3%

4%

48%

19%

5%

3%

2%

7%

2%

2%

3%

4%

6%

44%

19%

4%

3%

2%

11%

2%

0% 10% 20% 30% 40% 50%

Decline >= 50

Decline between 25 and 49

Decline between 10 and 24

Decline less than 10

No change

Increase less than 10

Increase between 10 and 24

Increase between 25 and 49

Increase >= 50

Can now be scored

Remain a no score

2005 'Utility Sample' 2009

Consistent credit score impacts over time…

VantageScore Change with Alt Data, All Consumers

28

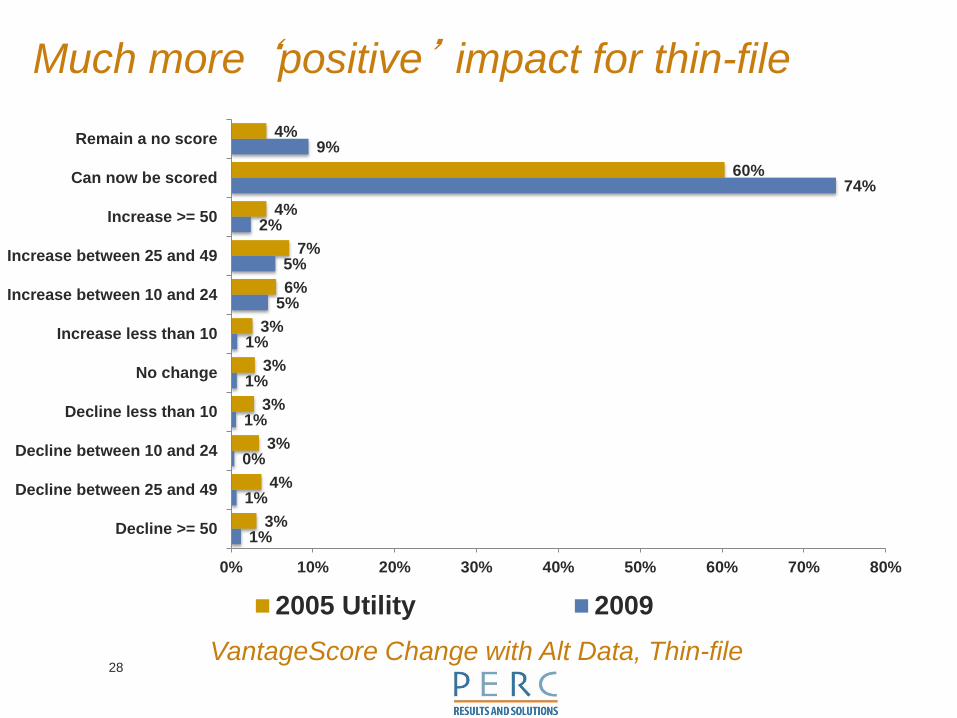

Much more ‘positive’ impact for thin-file

1%

1%

0%

1%

1%

1%

5%

5%

2%

74%

9%

3%

4%

3%

3%

3%

3%

6%

7%

4%

60%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Decline >= 50

Decline between 25 and 49

Decline between 10 and 24

Decline less than 10

No change

Increase less than 10

Increase between 10 and 24

Increase between 25 and 49

Increase >= 50

Can now be scored

Remain a no score

2005 Utility 2009VantageScore Change with Alt Data, Thin-file

29

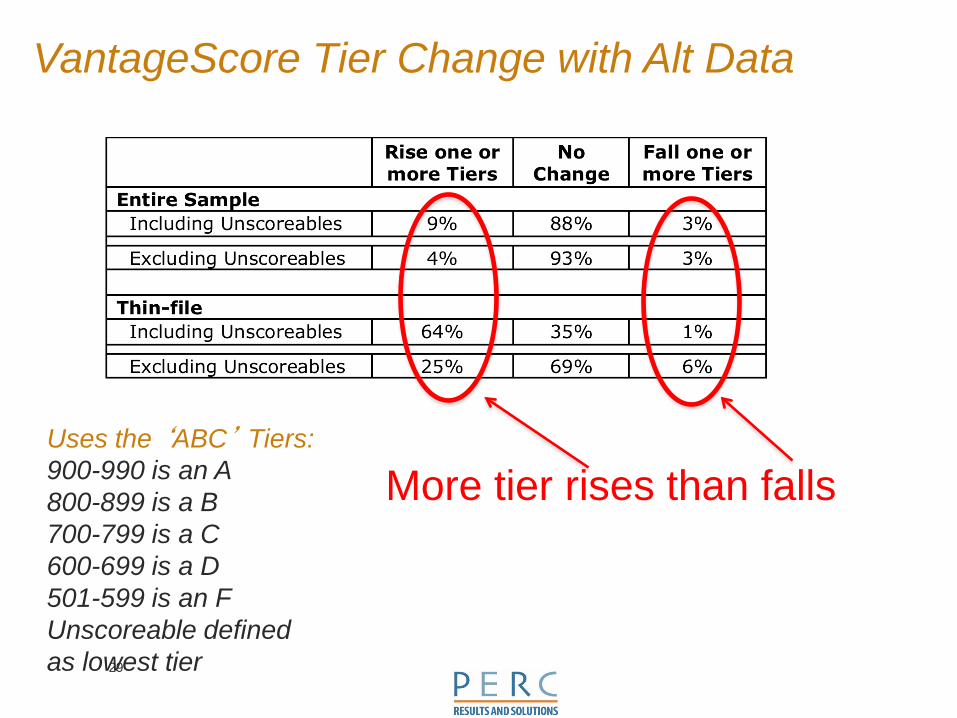

VantageScore Tier Change with Alt Data

Uses the ‘ABC’ Tiers: 900-990 is an A 800-899 is a B 700-799 is a C 600-699 is a D 501-599 is an F Unscoreable defined as lowest tier

More tier rises than falls

30

0%

5%

10%

15%

20%

25%

30%

< $20K $20-$29K $30-$49 $50-$99 $100K+2009/2010 2005/2006

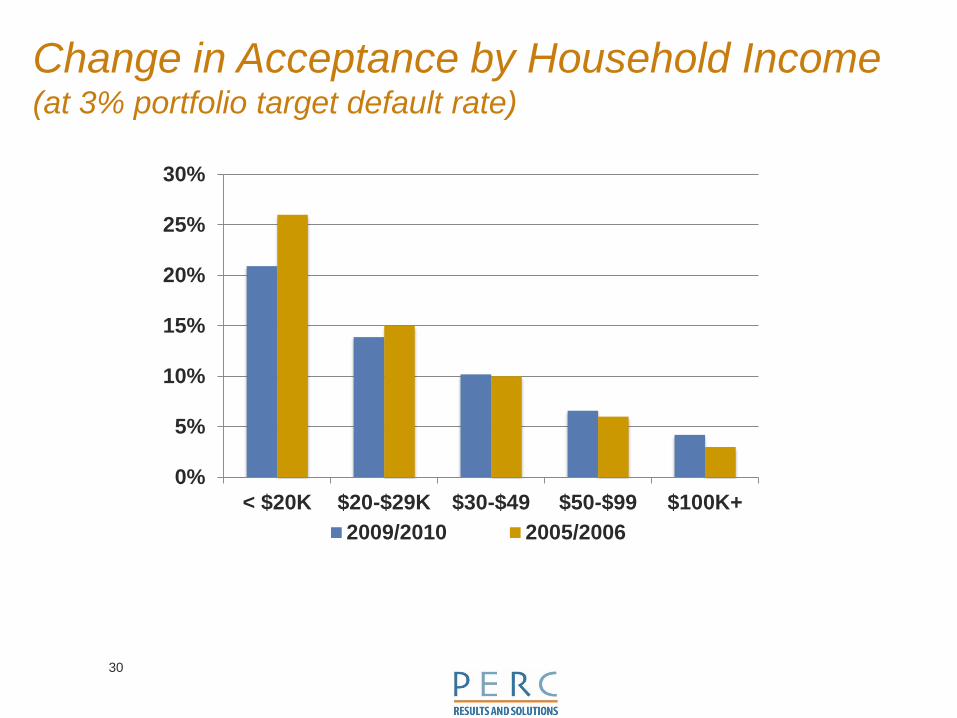

Change in Acceptance by Household Income (at 3% portfolio target default rate)

31

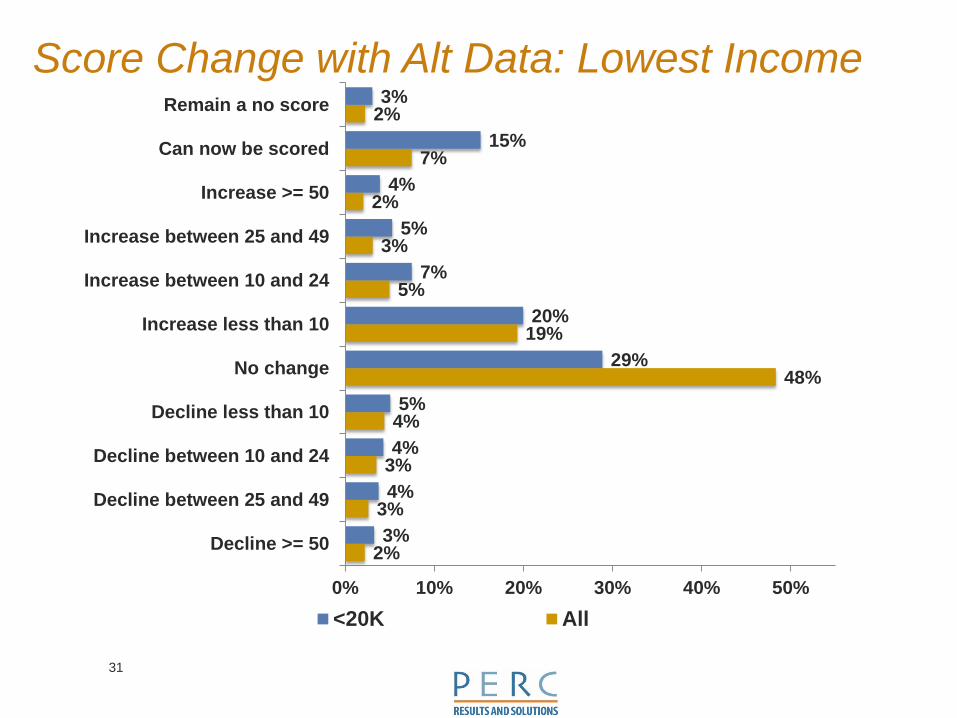

Score Change with Alt Data: Lowest Income

2%

3%

3%

4%

48%

19%

5%

3%

2%

7%

2%

3%

4%

4%

5%

29%

20%

7%

5%

4%

15%

3%

0% 10% 20% 30% 40% 50%

Decline >= 50

Decline between 25 and 49

Decline between 10 and 24

Decline less than 10

No change

Increase less than 10

Increase between 10 and 24

Increase between 25 and 49

Increase >= 50

Can now be scored

Remain a no score

<20K All

32

0%

5%

10%

15%

20%

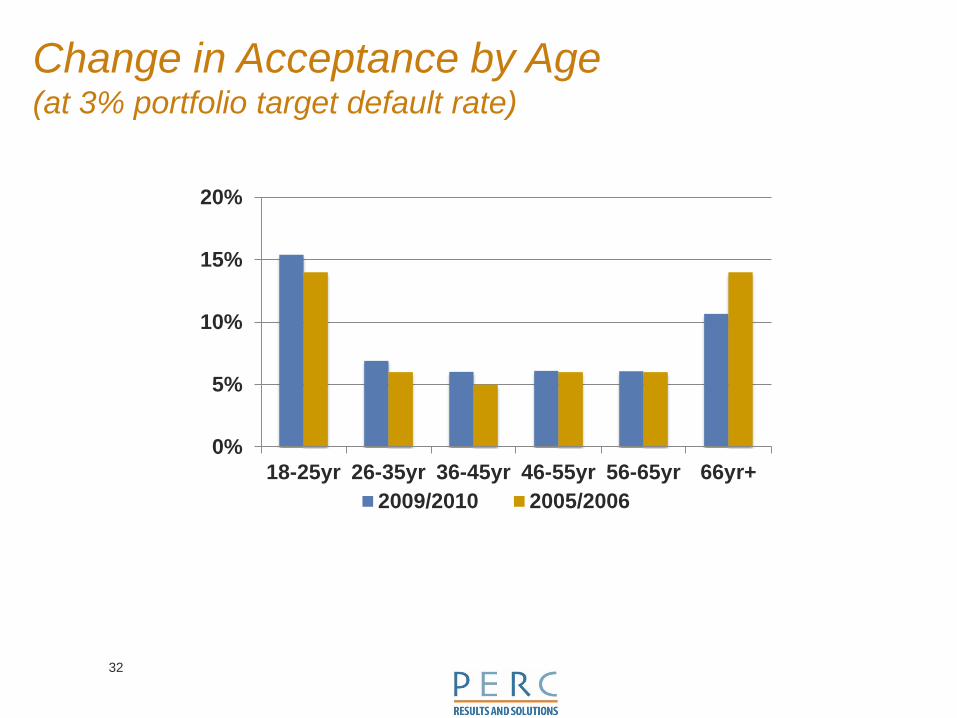

18-25yr 26-35yr 36-45yr 46-55yr 56-65yr 66yr+2009/2010 2005/2006

Change in Acceptance by Age (at 3% portfolio target default rate)

33

VantageScore Score Change with Alt Data, Helps those with damaged credit (PR & 90+ dpd)

0%

5%

10%

15%

20%

25%

30%

35%

40%

≥ 50 pt 25-49 pt 10-24 pt < 10 pt No Change Can Now beScored

Remain a"No Score"

Decrease Increase

55.8% see score increases, 30.2% see decreases

Research Consensus Confirms Benefits of Alternative Data

34

March 2015

Many Organizations Examined Alternative Data

• PERC • CFSI • Brookings Institution • Boston Fed • World Bank • IFC • PBOC CRC • Privacy Commission (AUS, NZ, EU)

• Equifax • Experian • VantageScore • FICO • Lexis-Nexis • MicroBilt • SAS Institute

Types of Data Examined: Utility payments, Rent Payments, Telecom Payments, Pay TV, Cable, and Underutilized Public Records

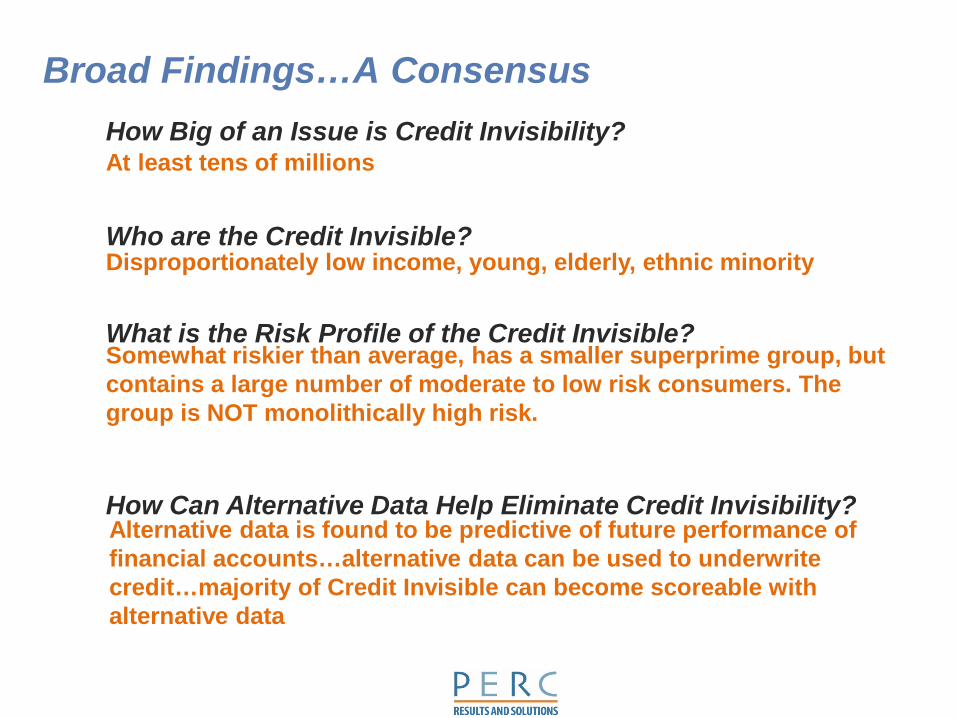

Broad Findings…A Consensus How Big of an Issue is Credit Invisibility?

Who are the Credit Invisible?

At least tens of millions

Disproportionately low income, young, elderly, ethnic minority

What is the Risk Profile of the Credit Invisible? Somewhat riskier than average, has a smaller superprime group, but contains a large number of moderate to low risk consumers. The group is NOT monolithically high risk.

How Can Alternative Data Help Eliminate Credit Invisibility? Alternative data is found to be predictive of future performance of financial accounts…alternative data can be used to underwrite credit…majority of Credit Invisible can become scoreable with alternative data

Predicting Financial Account Delinquencies with Utility and Telecom Payment Data

37

March / April 2015

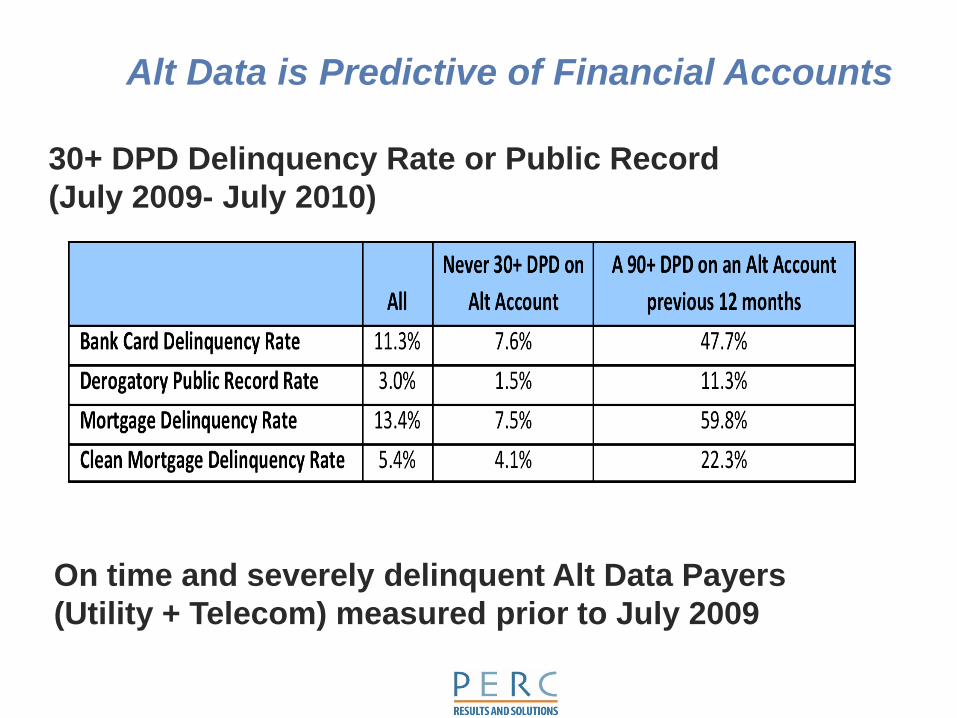

Alt Data is Predictive of Financial Accounts

30+ DPD Delinquency Rate or Public Record (July 2009- July 2010)

On time and severely delinquent Alt Data Payers (Utility + Telecom) measured prior to July 2009

7.50% 10.20% 13.40%

59.80%

70.00%

0%10%20%30%40%50%60%70%80%

Never 30+DPD on AltTradeline

No 90+ DPDever on AltTradeline

All 1 90+ DPD onan Alt

tradelineprevious 12

months

>1 90+ DPDon Alt

tradelinesprevious 12

months

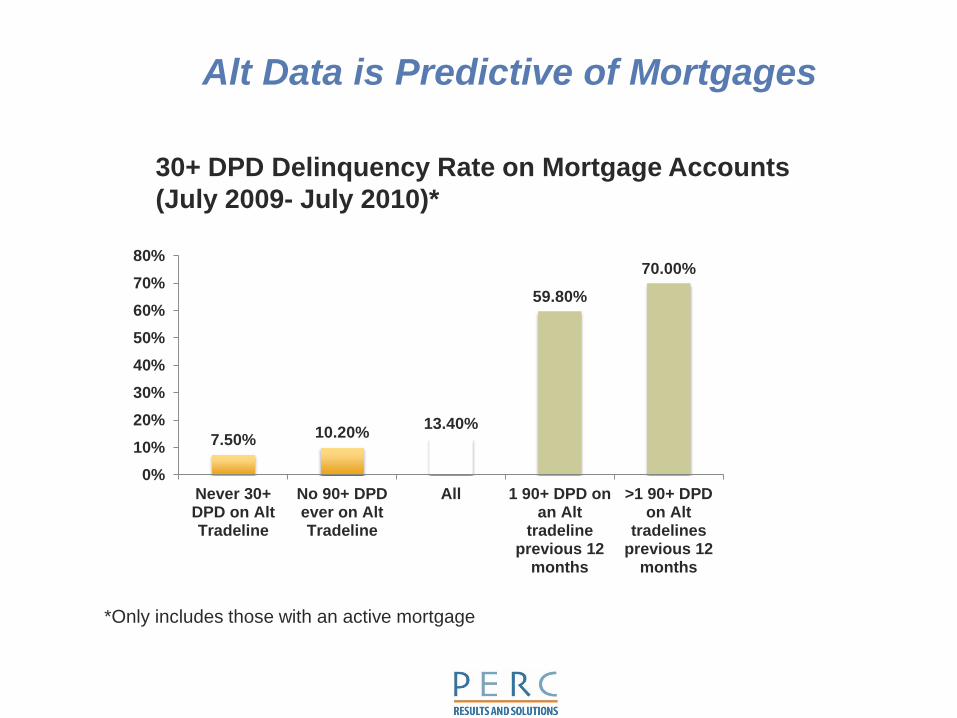

30+ DPD Delinquency Rate on Mortgage Accounts (July 2009- July 2010)*

Alt Data is Predictive of Mortgages

*Only includes those with an active mortgage

4.10% 4.90% 5.40%

22.30%

26.20%

0%

5%

10%

15%

20%

25%

30%

Never 30+ DPDon Alt

Tradeline

No 90+ DPDever on AltTradeline

All 1 90+ DPD onan Alt tradeline

previous 12months

>1 90+ DPD onAlt tradelinesprevious 12

months

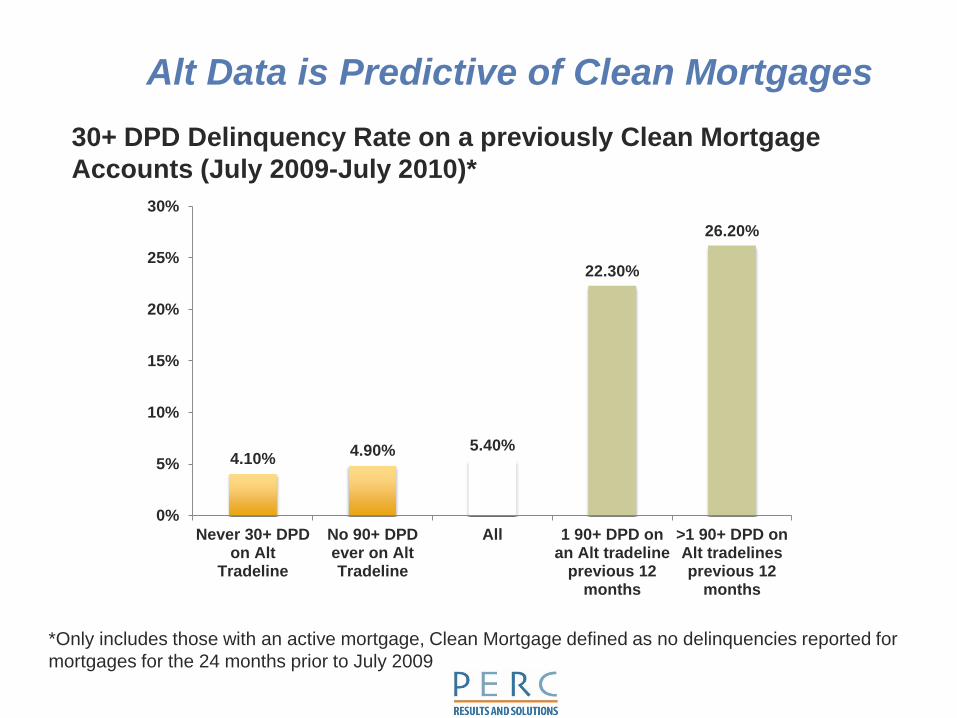

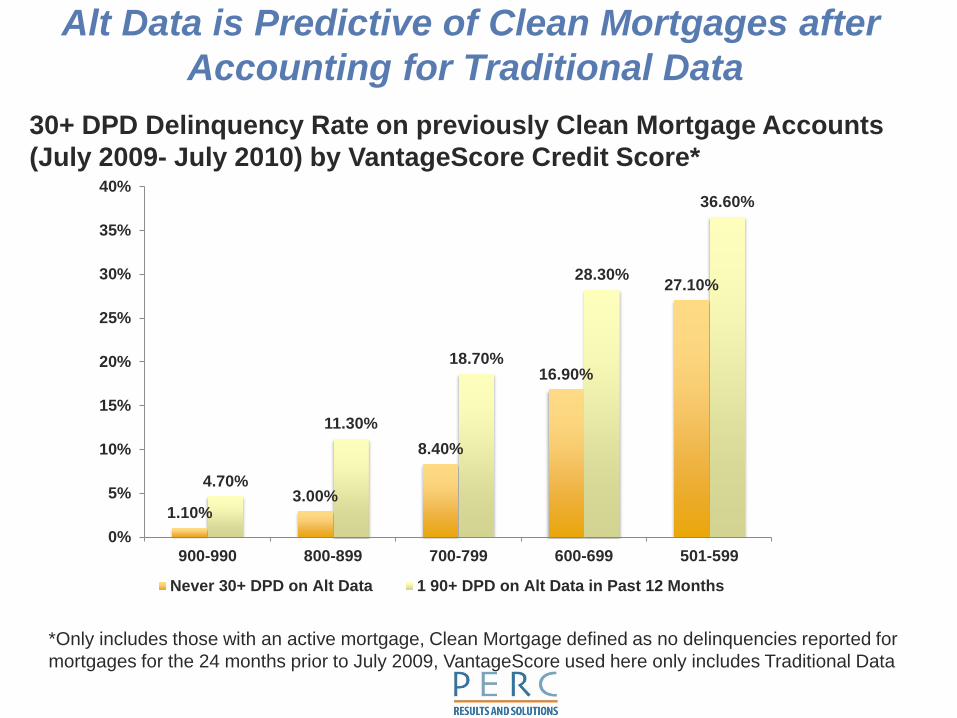

30+ DPD Delinquency Rate on a previously Clean Mortgage Accounts (July 2009-July 2010)*

Alt Data is Predictive of Clean Mortgages

*Only includes those with an active mortgage, Clean Mortgage defined as no delinquencies reported for mortgages for the 24 months prior to July 2009

1.10% 3.00%

8.40%

16.90%

27.10%

4.70%

11.30%

18.70%

28.30%

36.60%

0%

5%

10%

15%

20%

25%

30%

35%

40%

900-990 800-899 700-799 600-699 501-599

Never 30+ DPD on Alt Data 1 90+ DPD on Alt Data in Past 12 Months

30+ DPD Delinquency Rate on previously Clean Mortgage Accounts (July 2009- July 2010) by VantageScore Credit Score*

*Only includes those with an active mortgage, Clean Mortgage defined as no delinquencies reported for mortgages for the 24 months prior to July 2009, VantageScore used here only includes Traditional Data

Alt Data is Predictive of Clean Mortgages after Accounting for Traditional Data

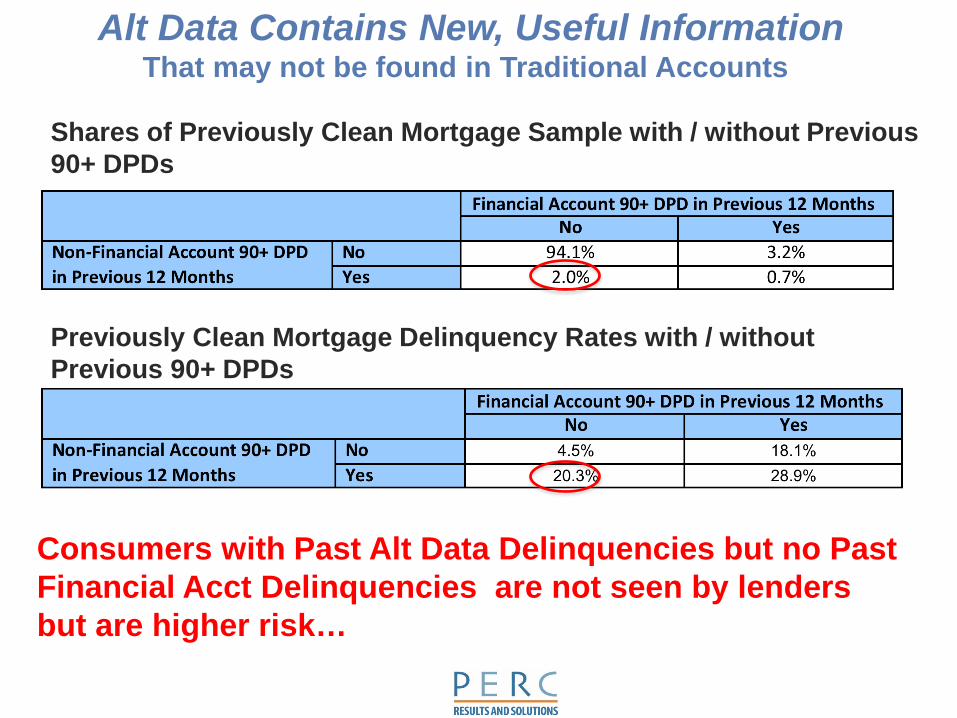

Shares of Previously Clean Mortgage Sample with / without Previous 90+ DPDs

Previously Clean Mortgage Delinquency Rates with / without Previous 90+ DPDs

Alt Data Contains New, Useful Information That may not be found in Traditional Accounts

Consumers with Past Alt Data Delinquencies but no Past Financial Acct Delinquencies are not seen by lenders but are higher risk…

43

‘Consumer Friendly’ Reporting For instance: • Use restriction (not for employment screening or insurance underwriting) • Exclude all negatives less than 90 days • Report assistance as “paid as agreed” or exclude (e.g. LIHEAP) • Exclude unpaid balances on closed accounts (e.g. <$100)

44

Other Alternative Data Being Used

Rental data United States (certain locations) Colombia (in Bogota area) South Africa (Johannesburg area) Trade supply (not trade credit) for FMCG Agricultural supply data (for rural lending) Some fit into credit bureau model, others do not

45

Digital Data Being Tested/Used

Promise of improving credit access for urban and rural poor in emerging economies:

Mobile microfinance Development of mobile based interface for financial services offers

new opportunities for risk assessment Unified platform for application and distribution Data

o Payment and prepayment patterns o Social collateral from call log data

Smart (Philippines), M-Shwari (Kenya), Cignifi (Brazil) Mobile data in bank lending First Access (Tanzania)

Hurdles to Reporting (US)

46

Technological barriers to reporting: Complex billing cycles (footprint dependent) Legacy IT systems

Regulatory barriers: Some states have statutory prohibitions Regulatory uncertainty Jurisdictional issues—FCC, state PUCs/PSCs, CFPB

Economic barriers: Compliance costs—FCRA data furnisher obligations Customer service costs from lenders scaring

customers substantial Incentives, what do you get for sharing data?

47

How Should We Approach Alt Data

For traditional providers, Incentives are different. Banks are users of the data, so they get something

for what they give.

Confidentiality concerns are different—banks are backed by regulation, by safety and soundness concerns, and by a post-paid relationship. Not so with alt data furnishers.

Fairness: why should these sources give a bureau data for free, so that a bureau can make money off of it?

Here’s where regulators can help, in pushing financial inclusion mission, and in helping the system develop trust.

48

Big Data and Data Fiefdoms Some observations from the field:

McKinsey effect

› Growing belief that every firm is sitting on a gold mine. › Seeking to monetize data assets.

Data Fiefdoms › Data becoming more fragmented (MNOs, banks on SME credit, banks) › All want to be CRA/info service provider

Muddy Waters › “Traditional” alternative data vs. “Fringe” alternative data (Robinson+Yu) › Sensing increased uncertainty among regulators/policymakers

Here’s where regulators can help—in pushing financial inclusion

mission, and in helping the system develop trust.

302 East Pettigrew Street Suite 130 Durham, NC 27701 www.perc.net (919) 338-2798 x803

Credit Scoring: Going Beyond the Usual Housing Finance Policy Center Lunchtime Data Talk

Ken Brevoort Section Chief, Credit Information & Policy Office of Research Consumer Financial Protection Bureau March 12, 2015

The opinions in this presentation are those of the author and do not necessarily reflect the views of the Consumer Financial Protection Bureau or the United States.

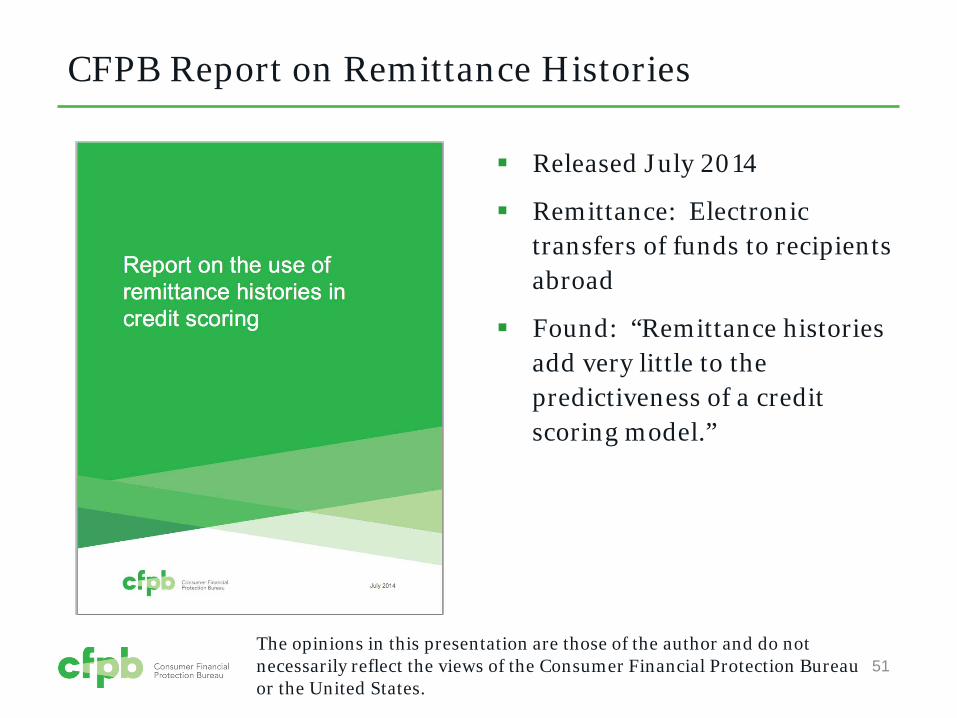

Released July 2014

Remittance: Electronic transfers of funds to recipients abroad

Found: “Remittance histories add very little to the predictiveness of a credit scoring model.”

CFPB Report on Remittance Histories

51 The opinions in this presentation are those of the author and do not necessarily reflect the views of the Consumer Financial Protection Bureau or the United States.

My Office

52 The opinions in this presentation are those of the author and do not necessarily reflect the views of the Consumer Financial Protection Bureau or the United States.

Why Are Some Records Unscorable?

Model builders are unable to predict which consumers will repay their loans

Reasons why:

A lack of information about the consumer

• Alternative data can help here, but

– How many thin files have this information? – Is alternative data really predictive?

Building a model requires both left- and right-hand-side variables, so we need observable performance

• Alternative data unlikely to help here

53 The opinions in this presentation are those of the author and do not necessarily reflect the views of the Consumer Financial Protection Bureau or the United States.

Why is this Important? An Example

Utility payment information for random sample of 1 million consumers with unscorable records

Credit Record data from end of 2012 and end of 2014

Credit Characteristics from 2012

Credit Performance in 2013 and 2014 from 2014 data

Thin files are less likely to have performance that is observable in the data

If only 10 percent have observable performance, the model

• Will be estimated using only 100,000 observations

• May prove unreliable when extrapolated to the other 90 percent of consumers with unscorable records

54 The opinions in this presentation are those of the author and do not necessarily reflect the views of the Consumer Financial Protection Bureau or the United States.

Conclusions

Sarah Davies and Michael Turner are doing important and interesting work!

There are a lot of reasons to be enthusiastic about alternative data’s potential

But until the predictive power of these data are reliably demonstrated, we should be cautious in advocating the use of such data

55 The opinions in this presentation are those of the author and do not necessarily reflect the views of the Consumer Financial Protection Bureau or the United States.