Embed Size (px)

Citation preview

H O U S I N G G O V E R N A N C E R E V I E W 2 0 1 4

Steering the way to excellence in governance

Contents

Highlights 1

The regulator’s perspective 2

Foreword 3

Compliance with adopted codes 5

Leadership 8

The role of the board 8

Board composition 10

Board committees 11

Effectiveness 14

Board evaluation 14

Board attendance 14

Gender diversity 16

Assurance 18

Internal audit 18

External audit 20

Accountability 22

The audit committee 22

Risk management 25

Understanding and managing risk 25

Principal risks and uncertainties 26

Disclosure of main risks 27

Internal control 30

Remuneration 31

Narrative reporting 34

Value for money 34

About Grant Thornton 36

Methodology

This report is based on a desktop review of the latest financial statements of the top 60 not for profit registered providers (by income) in England.

Jenny Brown would like to thank Donald Sadler, Sarah Heritage, Louise Hughes, Amanda Tilley, Fiona Baldwin, Graham Nunns, Kyla Bellingall, Dan Watson, Rachael Rickwood and Aleen Tirmzey for their help in preparing this report.

HOUSING GOVERNANCE REVIEW 2014 1

87% follow the National Housing Federation’s Excellence in governance code. 13% follow the UK Corporate Governance Code.

68% declare full compliance with their adopted code.

84% of board members are non-executives.

Only 22% of providers give details of their board evaluations.

Just 22% disclose member attendance at board or committee meetings (compared to 99% in the FTSE 350).

The top 60 providers paid £5.8 million in audit fees in 2013: the average was £98,000, the average non audit fee was £59,000.

Welfare reform is mentioned in two out of three risk registers.

83% of the largest providers pay their board members, at an average of £9,874 each.

More than one in four (28%) board members are female.

Highlights

Our findings from the top 60 providers by income in England show:

HOUSING GOVERNANCE REVIEW 2014 2

Registered providers are working in an increasingly challenging operating environment. In our Sector Risk Profile 2013 published last September we focused on the financial risks which could lead to a provider failing to comply with our economic standards, particularly in relation to expectations on financial viability. In addition to a number of operating risks we specifically highlighted four key strategic risks – welfare reform, diversification, housing market risk and finance market risks.

The sector’s heightened risk environment, together with the growing diversification of providers into a wider range of activities and complex financial arrangements, means that what has been good enough in the past in terms of governance may not be good enough now and in the future. It is essential that the skills, expertise and experience of board members are commensurate with the ambitions of the providers which they govern. Boards must challenge their executives as well as their own effectiveness, and have processes in place which will ensure that they are fit for purpose to meet the challenges ahead.

Greater risk and complexity in the sector increase the risks to the Social Housing Regulator achieving its own objectives. Our Regulation Committee is focused on the protection of social housing assets and the public value within them, and helping the sector to continue to attract the necessary finance to develop new homes. We have developed our

regulatory approach to focus on the most complex and risky providers, and we will continue to develop our approach alongside changes to the Regulatory Framework which will support the protection of social housing assets.

The Regulatory Framework is based on the principles of co-regulation and that will continue to be the case. One of those principles is that “Transparency and accountability is central to co-regulation”. The Housing Governance Review 2014 is certainly one tool which providers might use to assess how transparent they are being with their tenants, service users and other stakeholders.

The Regulatory Framework also says that “Boards and Councillors who govern providers are responsible and accountable for delivering their organisation’s social housing objectives”. Our preferred model is to work with providers and allow them to get on with running their businesses. However we will take action where we have concerns. At the time of writing, of 245 providers with regulatory judgements on the HCA’s website, nine are assessed as non-compliant in terms of our expectations on governance, and a further 31 are assessed as compliant but with work needed to maintain that compliance. If that position is to be maintained and improved, it will require boards to continue to develop at the pace of a rapidly changing market.

The regulator’s perspective

Mick Warner, Deputy Director Regulatory Operations, Homes and Communities Agency

“Boards must challenge their executives as well as their own effectiveness, and have processes in place which will ensure that they are fit for purpose to meet the challenges ahead.”

HOUSING GOVERNANCE REVIEW 2014 3

Welcome to Grant Thornton’s first annual review of governance in the social housing sector. It is based on analysis of disclosures in the financial statements of the top 60 not for profit registered providers of social housing (by income) in England.

There have been significant changes in social housing in recent years, marked for example, by reductions in grants, changes in regulation, new forms of financing, changes in bank lending, and the entry of for-profit providers. This has led to a divergence in the business models being followed by registered providers, and a need for governance that reflects the specific needs of each organisation. The principle of co-regulation with the Homes and Communities Agency (HCA) has also increased the need for registered providers to take greater responsibility for their own governance structures, as prescriptive requirements and specific guidance have reduced.

At the same time, and perhaps as a result of such changes, the stakeholder focus on governance has increased. Lenders and credit ratings agencies consider the impact of governance on the cost of finance and the regulator increasingly makes reference to the quality of governance.

Our review, which is based only on the information given in the accounts rather than actual practice, found that many aspects of good governance – such as: diverse board membership; monitoring of external audit;

and internal audit activity – are in place but that detail on these processes is often limited and doesn’t provide the insight that it could. This perhaps reflects the debate as to the role of financial statements/annual reports in good governance, with many seeing them as compliance exercises rather than opportunities for greater transparency.

Indeed, there has been a view that sparsely-written financial statements are a mark of efficiency given that, traditionally, few people read them and that more energy should be spent on resident-focused annual reviews. However, the increased scrutiny of statements by the HCA, funders and others around – board membership (including tenure and remuneration); value for money; and compliance with chosen codes of governance – suggests that sparse financial statement information is becoming more a sign of weakness than a strength.

The coming years herald further changes – and challenges – for sector reporting. The new strategic report requirements mean that for year ends post September 2013, those providers who are registered companies will need to deliver more balanced reporting. Such balance will involve acknowledging

Foreword

Jenny Brown, Head of Housing, Grant Thornton

The coming years herald further changes – and challenges – for sector reporting. The new strategic report requirements mean that for year ends post September 2013, those providers who are registered companies will need to deliver more balanced reporting.

HOUSING GOVERNANCE REVIEW 2014 4

things which have been unsuccessful, as well as those that have gone well. Organisations may be more reluctant to include additional information in the absence of specific requirements, especially given the scrutiny of potential funders. This requirement is expected to extend out to all providers with more than 1,000 units with the new SORP.

The financial statement’s narrative is attracting ever more attention. The new value for money reporting requirement, in particular, obliges providers to comment on more issues. Internal control statements, meanwhile, need to become more specific and measurable. Our analysis shows the narrative is often repeated ‘boilerplate’,

with little reference to current events or activities. The emerging trend of providers following the UK Corporate Governance Code (UK Code) will impose further demands, as it requires more detailed disclosure. While most providers continue to follow the National Housing Federation’s Excellence in governance code (NHF Code), as the sector continues to diversify, we expect more will consider alternatives. The reporting bar will, therefore, keep on rising, with all providers needing to deliver more accessible, balanced and relevant narrative.

We hope this social housing review will help providers tackle the reporting challenges ahead.

This project aims to help organisations improve their performance by learning from their peers, both within and outside their own sector. In this spirit, in many places, this report lists both NHF and UK code requirements.

1 Corporate governance review 2013 – Governance steps up a gear; Local government review 2014 – Working in tandem; NHS Governance review 2014 – Staying in the saddle; Charity governance review 2014 – Good governance gathers pace.

This report is part of a broad assessment of UK governance practice, which already includes reviews of the FTSE 350, NHS, charity and local government1. This project aims to help organisations improve their performance by learning from their peers, both within and outside their own sector. In this spirit, in many places, this report lists both NHF and UK code requirements.

We also refer to our other governance reviews, particularly the charities and FTSE 350 reports, to provide a comparison between the housing sector’s performance and that of others. In doing so, we highlight areas where the sector compares favourably, for example in gender diversity. Where it trails behind, we import best practice from the other fields, such as around board remuneration reporting.

HOUSING GOVERNANCE REVIEW 2014 5

Compliance with adopted codes

Codes of governance

“A code of governance provides boards and committees with a framework, based around principles, to help them deliver better organisational performance and discharge their duties in the best interest of the organisation. A code will set the standard, based on good practice and the law, for boards to adopt and work to using it in the best way that suits their organisation’s circumstances and complexity. It should be a live document that boards and senior managers refer to on a regular basis and can measure overall compliance with each principle, or explain and justify any areas of non-compliance to itself and key stakeholders. Whatever code you choose, it should be appropriate for your organisation and provide some challenge and ‘stretch’ to the board and management.

The National Housing Federation’s code of governance – Excellence in governance was last updated in 2010. In planning any update to the code we will be taking into consideration the content of other recognised codes such as the UK Corporate Governance Code, as well as general trends in governance. Some issues we may be considering in any review are length of service on boards, size of boards and any recent material regulatory judgements.

The social housing regulator has an expectation that a registered provider adopts a recognised code of governance and provides a statement in the public domain that shows compliance with each principle in the code or the reasons for non-compliance. The federation agrees with this stance and is confident that if an association adopts and complies with the housing-specific Excellence in governance, they will be able to demonstrate a well-governed organisation.”

Stephen Bull, Head of Governance, National Housing Federation

Primary codesThe two main codes of governance used in the social housing sector are the National Housing Federation’s Excellence in Governance Code (NHF Code) and the Financial Reporting Council (FRC) UK Corporate Governance Code 2012 (UK Code), which is usually associated with listed companies. Our review found that the vast majority (87%) of providers have adopted the NHF Code, with 13% adopting the UK Code.

The NHF Code includes nine principles (ethics, accountability, customer first, openness, diversity and inclusion, review and renewal, clarity, control and structures) that providers should follow, along with provisions against which they should assess themselves. The UK Code sets out good practice covering issues such as board composition and effectiveness, the role of board committees, risk management, remuneration and relations with shareholders.

CHOSEN CODE OF GOVERNANCE

87%NHF EXCELLENCE IN GOVERNANCE

13%UK CORPORATE

GOVERNANCE CODE

HOUSING GOVERNANCE REVIEW 2014 6

Compliance levelsThe NHF Code requires a “reasoned statement about any areas in which [a provider does] … not comply”. This ‘comply or explain’ approach is also central to the UK Code. The disclosure of the rationale for non-compliance, details of any mitigating controls put in place instead, or outlines of plans for reversing non-compliance, vary greatly between providers.

We found that 68% of providers declare full compliance with their adopted code. This compares favourably with FTSE 350 companies, where 57% claim to be in full compliance. This is perhaps not surprising in the housing sector, where the interplay between government funding, regulation and responsibility to tenants drives a high consciousness of the importance of good governance. However, one must also take into account the number of recent HCA regulatory judgements which have identified areas of non-compliance within organisations, in some cases, when full compliance has been reported in the financial statements.

Of the 32% of providers who do not comply in full, the average number of non-compliance areas is 1.6. There are clear trends in non-compliance. They generally relate to non-executive directors’ terms of office exceeding the recommended nine years and chief executive appraisal procedures not being led by committees of non-executives.

COMPLIANCE WITH THE CODE

68%FULLY COMPLIANT

32%PARTIALLY COMPLIANT

We found that 68% of providers declare full compliance with their adopted code. This compares favourably with FTSE 350 companies, where 57% claim to be in full compliance.

57% 68% Housing

FTSE 100

Where providers identify areas of non-compliance, they must outline clearly how they will resolve these issues promptly. However, only 33% of the non-compliance points listed in the accounts disclose clear actions and a timescale for resolution.

TH

E I

N S I D E T R

AC

K

HOUSING GOVERNANCE REVIEW 2014 7

PICKING UP THE PACE

• Clearlystatethechosencode of governance

• Setouttherationaleforadoption of the chosen code

• Makeclearwhetheryoucomplyfully with the code and, if not, explain why. Have a clear plan in place with timescales for full compliance

• Statethemitigatingcontrols in place

“We currently follow the NHF Code of Governance as stated in our annual financial statements with two exceptions, in relation to the limitation of shareholdings to board members and the resetting of the term of office of the chair of the board. This latter factor is important to us and how we recruit to the board – we generally recruit people in through committees rather than straight to the board and we always recruit from the board to the chair’s position. Resetting the chair’s term of office ensures continuity in the management of the governing body; without this we might have to resort to external recruitment, which does not align with custom and practice at the group.

We have been spending time considering whether to continue to follow the NHF Code or, like some other housing associations, follow the UK Code. While the NHF Code is obviously designed with the social housing sector in mind, it also aims to cover all sizes of association. As a large association, there are some aspects where we consider that the UK Code may set a better bar for us to meet and as a guide in our governance. The UK Code has higher standards in reference to transparency in reporting which may be appropriate for us to consider, such as in regard to remuneration reports and statements about external audit.

We support the comply or explain approach, whichever code is used, but currently consider that, to follow the UK Code, may involve a longer list of ‘explanations’ if we are to follow it properly, given that that code is written for profit-making entities.

We have been in discussions with various parties, including the Financial Reporting Council about authorising an amended version which is more applicable to the sector, changing references, for example, in relation to shareholders. We’re still working on this and are watching other developments across the sector and elsewhere.”

Tom Dacey, Group Chief Executive of Southern Housing Group

HOUSING GOVERNANCE REVIEW 2014 8

Leadership

The role of the board

“The board must be effective in leading and controlling the organisation and acting wholly in its best interest.”

NHF Code

“It is up to each organisation or group parent organisation to decide on the best board composition. Board members who are executive staff must normally be in a clear minority.”

NHF Code

The board’s role is key in guiding the housing provider’s strategy and in directing, controlling, scrutinising and evaluating its affairs. Boards need a mix of appropriate skills to operate effectively in this role, and disclosure of this mix on websites and in the annual financial statements demonstrates openness, in the spirit of the codes of governance.

The housing sector is facing significant challenges due to changes in government policies, lack of access to finance, reduction in grants for development, and customers wanting more for less in difficult economic times. Providers are looking to diversify into new areas of business and therefore need to ensure they have non-executive directors with the skills and experience to challenge and support the executive.

The majority (84%) of the 682 board members of the top 60 housing providers are non-executive directors. Most (70%) of boards have 20% or fewer executive director representation, thus keeping non-executive directors in the majority, in accordance with best practice. Thirteen providers (22%) have no executive directors on their boards; this in itself raises questions about how the executive and board join together in those organisations.

BOARD MEMBERS

BALANCE BETWEEN EXECUTIVE AND NON-EXECUTIVE

84%NON-EXECUTIVE

DIRECTORS

70%20% OR FEWER

EXECUTIVE DIRECTORS

16%EXECUTIVE DIRECTORS

30%MORE THAN 20%

EXECUTIVE DIRECTORS

HOUSING GOVERNANCE REVIEW 2014 9

DETAILS ON BOARD IN THE FINANCIAL STATEMENTS (%)

DETAILS ON BOARD ON WEBSITES (%)

No details of directors other than initials and surname

Only full name

Very brief (eg description of their main current job)

As above plus a description of prior jobs

Skills highlighted

Roles and other trusteeships

5218

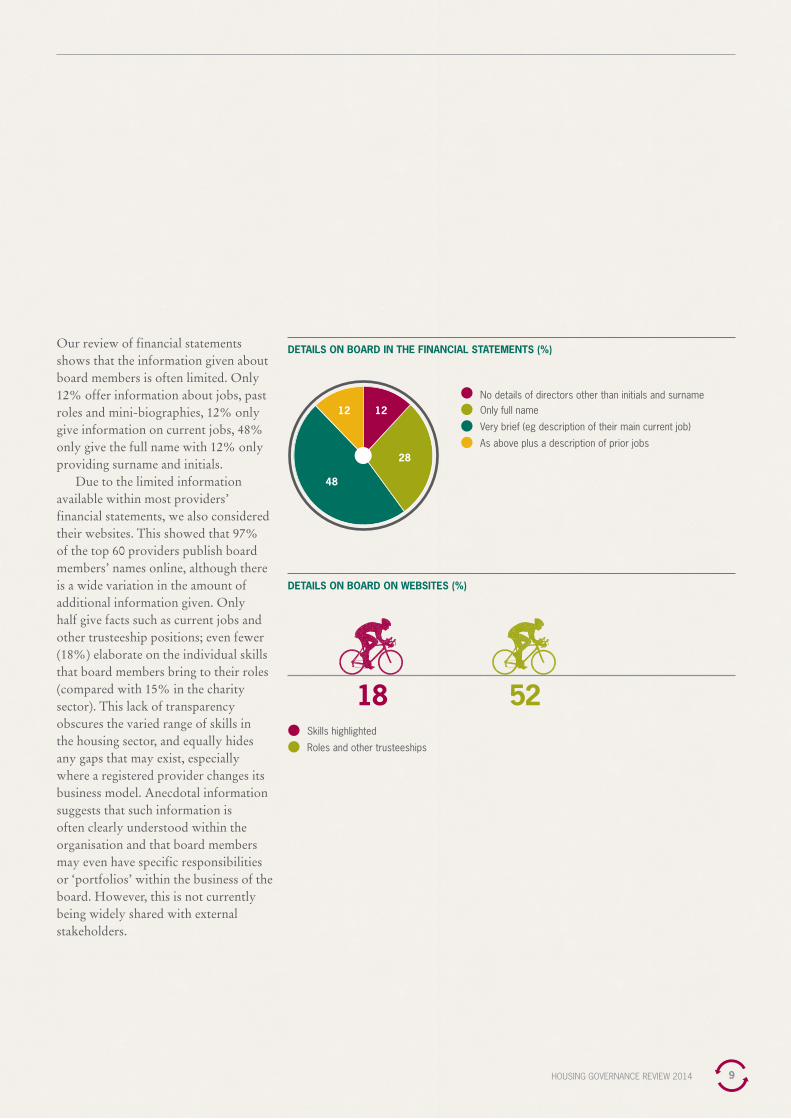

Our review of financial statements shows that the information given about board members is often limited. Only 12% offer information about jobs, past roles and mini-biographies, 12% only give information on current jobs, 48% only give the full name with 12% only providing surname and initials.

Due to the limited information available within most providers’ financial statements, we also considered their websites. This showed that 97% of the top 60 providers publish board members’ names online, although there is a wide variation in the amount of additional information given. Only half give facts such as current jobs and other trusteeship positions; even fewer (18%) elaborate on the individual skills that board members bring to their roles (compared with 15% in the charity sector). This lack of transparency obscures the varied range of skills in the housing sector, and equally hides any gaps that may exist, especially where a registered provider changes its business model. Anecdotal information suggests that such information is often clearly understood within the organisation and that board members may even have specific responsibilities or ‘portfolios’ within the business of the board. However, this is not currently being widely shared with external stakeholders.

1212

28

48

HOUSING GOVERNANCE REVIEW 2014 10

“Odgers Berndtson works extensively with registered providers across the country which are responding to the many challenges in the sector. Growth (both organic and inorganic), commercialisation and diversification are ever increasing features in the sector and this is certainly encouraging debate about what ‘good governance’ means. Without doubt, the type of individuals joining boards is shifting and appointing board and committee members who bring expertise in supporting the commercial drivers of an organisation adds immense value.

As one would expect, the need for different skill-sets on boards is driving a cultural shift at board level, both consciously and unconsciously. This is creating an inherent tension with more traditional board members, who perhaps retain a sole focus on the core social purpose of an organisation. It is important that these tensions remain healthy and productive, to ensure the balance is right and boards remain aligned to the organisation’s fundamental objectives.”

Rebecca Royle, housing lead at Odgers Berndtson

VIEW FROM THE TRACKSIDE

Board composition

“Boards should have at least five members and no more than 12, including co-optees.”

NHF Code

Boards should consider the optimum size for effective meetings. The top 60 providers’ boards have between six and 20 members listed (although this may include subsidiary board members or committee members: in some cases it is unclear), although most have from 10 to 14, with the average being 11.5. As well as the NHF recommendation above, a number of studies suggest that between seven and 10 members is the best size for effective board meetings2. This highlights that the housing sector average continues to be relatively high. In comparison, FTSE 350 company boards have 9.6 members on average, while charity boards have 12.8.

2 For example, The Eversheds Board Report: Measuring the impact of board composition on company performance, 2011.

Large boards often occur where specific groups need to be represented (such as in the standard large-scale voluntary transfer (LSVT) model); a reduction in size often accompanies a move to a single status or unitary board. Reducing the size of the board is often linked to increased effectiveness; at a practical level it allows better co-ordination of meetings (and higher attendance) as it enables increased contributions from each member without meetings becoming unwieldy.

11.5

9.6

12.8

FTSE350

HOUSING

CHARITIES

BOARD SIZE

HOUSING GOVERNANCE REVIEW 2014 11

NOMINATION

REMUNERATION

AUDIT & RISK

DEVELOPMENT

CUSTOMER SERVICES

FINANCE

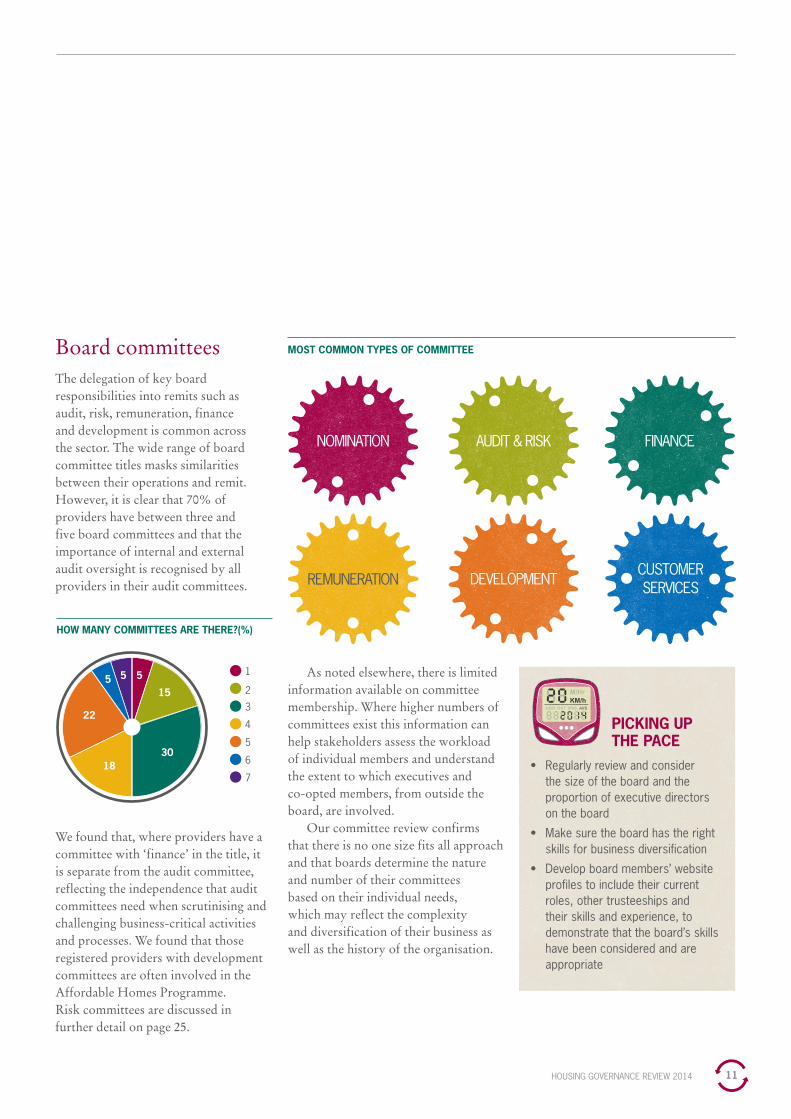

MOST COMMON TYPES OF COMMITTEEBoard committeesThe delegation of key board responsibilities into remits such as audit, risk, remuneration, finance and development is common across the sector. The wide range of board committee titles masks similarities between their operations and remit. However, it is clear that 70% of providers have between three and five board committees and that the importance of internal and external audit oversight is recognised by all providers in their audit committees.

We found that, where providers have a committee with ‘finance’ in the title, it is separate from the audit committee, reflecting the independence that audit committees need when scrutinising and challenging business-critical activities and processes. We found that those registered providers with development committees are often involved in the Affordable Homes Programme. Risk committees are discussed in further detail on page 25.

As noted elsewhere, there is limited information available on committee membership. Where higher numbers of committees exist this information can help stakeholders assess the workload of individual members and understand the extent to which executives and co-opted members, from outside the board, are involved.

Our committee review confirms that there is no one size fits all approach and that boards determine the nature and number of their committees based on their individual needs, which may reflect the complexity and diversification of their business as well as the history of the organisation.

PICKING UP THE PACE

• Regularlyreviewandconsiderthe size of the board and the proportion of executive directors on the board

• Makesuretheboardhastherightskills for business diversification

• Developboardmembers’websiteprofiles to include their current roles, other trusteeships and their skills and experience, to demonstrate that the board’s skills have been considered and are appropriate

1

2

3

4

5

6

7

HOW MANY COMMITTEES ARE THERE?(%)

3018

22

55515

HOUSING GOVERNANCE REVIEW 2014 12

TH

E I

N S I D E T R

AC

K

Gordon Perry, Chief Executive of Accent Group

“We have made some significant changes to the group over the last five years since I joined Accent as chief executive.

The starting point was expressing the desire to change the focus of the group. At that point we had 54 companies with business priorities and strategies that were not aligned which meant that getting everyone to pull together was difficult, leading to dysfunctional behaviour.

First, we determined that our focus was housing which led to us to divest ourselves of businesses we no longer wanted to pursue, such as the private finance initiative (PFI) and the Local Improvement Finance Trust (LIFT). We also combined entities doing similar activities. This reduced the number of legal entities to 13, which started to clarify our legal framework. The new structure consists of a holding entity with three main registered providers controlling over 20,000 homes nationally, and some smaller companies doing niche activities.

The other main area was governance of the group. While legally the group board exercised full control, in practice making group-wide decisions was lengthy and complex. We really operated as a federation. Also, the group board and the boards of each registered provider were made up of different directors with no links between. A key decision was to bring the chairs of each registered provider onto the main board to enable better communication across the group and to reinforce the message that Accent was again focused on housing.

We set up an annual board members conference bringing all these individuals from across the country to enable geographical boundaries to be broken down. Two years ago, the conference had the theme of ‘Where are we going?’. This enabled us to have really radical conversations which concluded that staying together as a group was the best idea and most likely to leave us fit for the

future. Having made that decision it was agreed that we should adopt a virtual governance arrangement with completely co-terminus boards for the group board and the registered providers. This is much less complex and a quicker way of bringing things together than deciding to legally consolidate the group.

Each registered provider in the group had a different history and characteristics and we needed to keep all this in mind in our negotiations. This included resolving council nominations to a large-scale voluntary transfer (LSVT) and legacy shareholdings in a registered provider.

All through the process communication was critical. We were transparent and honest about the changes we were making and ensured that the individual entities and directors felt ownership of decisions. There was an understanding that we were stronger together.

We took our time with the process so no one was railroaded but, once changes started to go through, their impact was immense, with decision making across the group simpler and quicker. It has changed our culture and brought us together so we now operate as one housing organisation able to focus on the things which are important. For example, we now can spend much more time on performance at our board meetings and getting scrutiny right and at the right levels. We have introduced five local customer service committees improving our links to local communities.

Since Gail Teasdale arrived as finance director, the value for money agenda has been integral to this change. It has delivered £1.75 million of annualised savings by removing duplication and has driven up performance to our customers.”

HOUSING GOVERNANCE REVIEW 2014 13

“The last year has seen a continued emphasis on the roles of boards in the social housing sector. This has been reinforced by the regulator through the governance standard and by checking compliance with providers’ adopted governance code, with a particular eye on risk management and value for money. This reflects an operating environment where registered providers are exposed to new and increasing risks.

To provide effective leadership and control it is essential that boards have the necessary skills to understand the businesses that they are responsible for and the risks they face. We are seeing a significant number of organisations reviewing their board structures and skills. In particular, where boards have held a number of posts for ‘representatives’, questions are being asked as to whether their role continues to be appropriate, the impact on the balance of the board as a whole, and whether boards can have the breadth of skills now required without being excessively large.

For other organisations with complex group structures and related governance, we are seeing a continued drive for simplification. Such groups, which are only as strong as their weakest link, create complexity which can hide risks or underperformance and create an excessive workload for board members and officers. In the worst cases, such structures create inertia where unpopular or difficult decisions cannot be made quickly or at all. Where achievable at a reasonable cost, we are seeing the simplification of the legal entities. Where that is not possible, people are at least simplifying their governance arrangements.”

Ian Davis, Partner at Trowers & Hamlins

VIEW FROM THE TRACKSIDE

HOUSING GOVERNANCE REVIEW 2014 14

Effectiveness

Board evaluation

“The board must carry out an annual appraisal of its own performance and an annual appraisal of individual board members including the chair and, if appropriate, the vice chair and any executive who sits on the board.”

NHF Code

“The board should state in the annual report how performance evaluation of the board, its committees and its individual directors has been conducted.”

UK Code, B.6.1

“Evaluation of the board of FTSE 350 companies should be externally facilitated at least every three years. The external facilitator should be identified in the annual report and a statement made as to whether they have any other connection with the company.”

UK Code, B.6.2

Only 22% of providers give details of their board evaluation which makes it difficult to assess whether the NHF Code has been complied with. Just a quarter of those who mention evaluation say their evaluation was carried out externally. This means that only 7% of the top 60 providers confirm they had an external review (FTSE 350: 34%). It is unclear whether the other three quarters who note evaluations performed them with external independent support or otherwise (in accordance with the Code) as no mention is made of it. In our review of the FTSE 100, 80% provide details about their evaluation process, with 63% doing so from the FTSE 350.

IS THERE A BOARD EVALUATION MENTIONED?

22%YES

78%NO

Board appraisal and transparency may be considered even more important by stakeholders where board members are being remunerated for their roles, although quality and transparency are always vital even with remuneration.

Board attendanceOnly 22% of accounts disclose statistics on attendance at board or committee meetings (compared with 99% in the FTSE 350). Providers often monitor this information internally, therefore reference in the accounts would be an appropriate disclosure of the effort non-executives invest. Equally, it could encourage fuller attendance by board members.

TH

E I

N S I D E T R

AC

K

HOUSING GOVERNANCE REVIEW 2014 15

“In an ever-changing risk environment, at B3Living, we have been investing time in ensuring the board is well equipped to meet the many challenges and to take advantage of opportunities. The expectations of boards of housing associations are high and many associations are considering changes to the board structures, to adapt to the changing environment, but this can itself bring risks.

To further develop our board effectiveness we are focusing on how we need to work as a team, on whole organisation training and development and on creating a level of understanding that disagreement can be healthy if it creates challenge and is within the right environment.

We’ve been working with external support on the concept of collaborative leadership and have been considering the concept of the ‘Boardroom not the board’, that is, to consider the executives and non-executives as a partnership where space is created for strategic thinking and decisions are made in the right place based on roles and responsibilities. We want to balance this aspect with the board ‘in control’ and have been working with other advisers to further develop the board and its relationship with the executive.

Although more associations are now remunerating board members it is appropriate for balance that many members have ‘day jobs’ and this has to be taken into account in the commitment expected.

We are conscious of the number of organisations now looking at moving away from stipulated constituencies and towards single status boards. The world is a very different place now from when many of these arrangements were set up; however, there are risks to changing and there needs to be a clear plan as to what the board should look like and why change is necessary.

We have also heard that some boards are considering having a senior non-executive director. We have not yet agreed whether to introduce that role at this time but, to ensure those risks are still managed, we have now ensured that our chair has access to our legal advisers without the need for it flowing through the executive, which we have seen as best practice elsewhere.”

John Giesen, Chief Executive of B3Living

HOUSING GOVERNANCE REVIEW 2014 16

Gender diversity

“Boards must demonstrate leadership and commitment to equality, diversity and inclusion as outlined in the Equality Act 2010, across all the organisation’s activities.”

NHF Code

“The search for board candidates should be conducted and appointments made, on merit, against objective criteria and with due regard for benefits of diversity on the board, including gender.”

UK Code, supporting principle B.2

“[It should also] include a description of the board’s policy on diversity including gender, any measurable objectives that it has set for implementing the policy and progress on achieving the objectives.”

UK Code, supporting principle B.2.4

15

19

28

29

MID 250

FTSE 100

HOUSING

CHARITIES

3 http://www.som.cranfield.ac.uk/som/dynamic-content/research/documents/WomenonBoards2012Code.pdf

Gender diversity remains a key issue for all entities. As housing providers and not for profit entities have generally out-performed corporates in this area, it is worth demonstrating that they have a much higher ratio of females than most companies.

Registered providers appear to be significantly more accessible to women than FTSE 350 companies. Research published by Cranfield School of Management, in November 2013, shows that 19% of FTSE 100 board members and 15% of those in the Mid 250 are now women3. There is a higher representation on the top 60 registered providers’ boards, at 28% (where gender is identifiable from available information), but this is still topped by charity boards, where female representation is 29%.

WOMEN ON THE BOARD (%)

HOUSING GOVERNANCE REVIEW 2014 17

FEMALE CHAIRS OF THE BOARD (%) FTSE350 Charities Housing

1.5 2220

PICKING UP THE PACE

• Includeastatementontheboardevaluation process, including whether it was internal or externally supported and the key outcome/conclusion

• Detailboardmemberattendance at board and committee meetings

• Includemoredetailsontheintended recruitment and diversity of the board, so readers of the accounts can be clear on the intended mix

• Setgoalsforfuturechanges and measure performance against them

The 2011 Davies report ‘Women on Boards’, which recommended that 25% of board members be female by 2015, has encouraged 78% of FTSE 100 companies to disclose their gender diversity policies in their annual reports. However, this trend has not extended to the not for profit sector, with limited discussion of gender or other diversity aspirations apparent in our assessment of providers (as we also noted in our review of charities).

Eighty per cent of board chairs of the top 60 registered providers are male and 22% female. This is comparable

to the gender balance of the top 100 charities’ boards, where 22% are women, and is considerably better than the FTSE 350, where only 1.5% – or three chairs – are women.

Housing provider accounts disclose little about other areas of diversity. Such omissions, along with the limited information on board evaluation and attendance, give stakeholders little basis on which to assess the board. Age was another area of diversity documented in our FTSE 350 review, which found that the average age of a non-executive director (NED) is 59.

HOUSING GOVERNANCE REVIEW 2014 18

Assurance

Internal audit

“Effective audit is essential to good governance. This goes beyond traditional financial audit into all areas of an organisation’s work and should be integrated into business management. Standards of performance, service delivery and compliance should all be subject to some form of audit if they are to remain effective. Larger and more complex organisations will need to devote substantial time and resources to audit matters, including an internal audit function.”

NHF Code

Internal audit continues to play a significant role in internal control by providing assurance to management and the audit committee (or equivalent) that key business risks are being effectively managed and policies and procedures adhered to. Internal audit’s role can also include fraud investigations, consultancy activities, systems design and implementation advice, value for money studies and helping to embed good practice risk management procedures.

Despite this, a recent survey of heads of internal audit by the Chartered Institute of Internal Auditors (IAA) in its inaugural Governance and Risk

Report 2013 found that 18% of public sector organisations are cutting their internal audit budgets, whereas 25% of private sector bodies are increasing them. This is not surprising given the current squeeze on the public purse, with cuts in funding and changes in the welfare system, and the turmoil and control failings which have infected the corporate world.

Internal audit is mentioned in 97% of providers’ annual reports, compared to 89% of FTSE 350 companies. However, there is a lack of transparency and clarity about the provision of the service.

DETAILS OF INTERNAL AUDIT ARRANGEMENTS GIVEN IN FINANCIAL STATEMENTS (WHERE INTERNAL AUDIT IS MENTIONED) (%)

INTERNAL AUDIT MENTIONED (%)

Housing

FTSE350

Named external provider

Unclear whether in-house or out/co-sourced

97

29

89

71

HOUSING GOVERNANCE REVIEW 2014 19

Seventy-one per cent of registered providers do not state clearly whether their internal audit service is in-house, outsourced or co-sourced (in-house plus external support), making it difficult to identify any trend or emerging pattern in the delivery of these services. Of those where the internal audit service appears to be outsourced and information is provided (29%), the results show that providers use several audit practices.

We know, anecdotally, that larger registered providers favour co-sourcing arrangements, with audit firms providing support in specialist areas such as IT, treasury and forensics. In contrast, small or medium-sized providers have fewer in-house staff and tend to favour full outsourcing.

Internal audit effectivenessHousing providers formerly required their internal audit service to conform to the Government Internal Audit Standards (GIAS), which broadly reflected the IAA standards. GIAS has now been replaced by the Public Sector Internal Audit Standards (PSIAS), which came into effect from April 2013, following consultation between the IIA, the Chartered Institute of Public Finance and Accountancy, HM Treasury, the Department of Health, the Scottish and Welsh Governments, and the Department for Finance and Personnel.

One of the fundamental requirements of the new standards, under the Attribute Standards, 1312 – External Assessments clause, is that “external assessments must be

conducted at least once every five years by a qualified, independent assessor or assessment team from outside the organisation” and that “external assessments can be in the form of a full external assessment, or a self-assessment with independent external validation”.

Reviewing the effectiveness of the internal audit function is critical to its development, profile and positioning within the business, as is identifying and understanding the contribution it makes to a robust system of internal control. In our study, no registered providers disclosed clearly whether a review has taken place.

“The audit committee … should monitor and review the effectiveness of the internal audit activities.”

UK Code, C.3.2

HOUSING GOVERNANCE REVIEW 2014 20

External audit

“Every federation member should ensure that it observes the following principles:

1. Its external auditors must be independent and effective. External auditors cannot usually be judged to be independent if they also provide significant non-audit services

2. There should be a proper and transparent procedure for the selection and periodic review of the appointment of external auditors.”

NHF Code, Section L1 (1)

Auditor independence and objectivityThe debate about whether auditors should undertake non-statutory services is gaining momentum, driven by the UK and the EU regulators about choice in the listed company audit market. Perspectives range, on one side, from audit committees being able to set appropriate parameters to, on the other, auditors being barred from undertaking such services and the creation of audit-only firms. The spectre of the 2012 FRC Guidance on Audit Committees suggests that the external auditor’s independence and objectivity and the effectiveness of the external audit should be monitored. Disclosure of this information in the board’s report would give account users a sense of how long the auditors have been engaged, other services provided and, ultimately, whether auditor independence is in danger of being compromised.

A new provision in the 2012 edition of the UK Code states that FTSE 350 companies should put the external audit contract out to tender at least once per decade. In our experience, registered providers tender their external audit between every three and seven years, often in an attempt to demonstrate value for money.

The majority of annual reports and financial statements for providers do not state how the external auditor’s independence and objectivity is preserved, the auditor’s term of office, the last time the service was tendered, or the frequency of tendering. This compares to the 90% of FTSE 350 companies which also do not state when they next plan to put audit services out to tender. Ninety-eight per cent of FTSE 350 companies do, however, explain why they recommended the appointment, reappointment or removal of auditors. Such detail would help readers of registered providers’ accounts judge whether proper governance arrangements exist for appointing and working with external auditors.

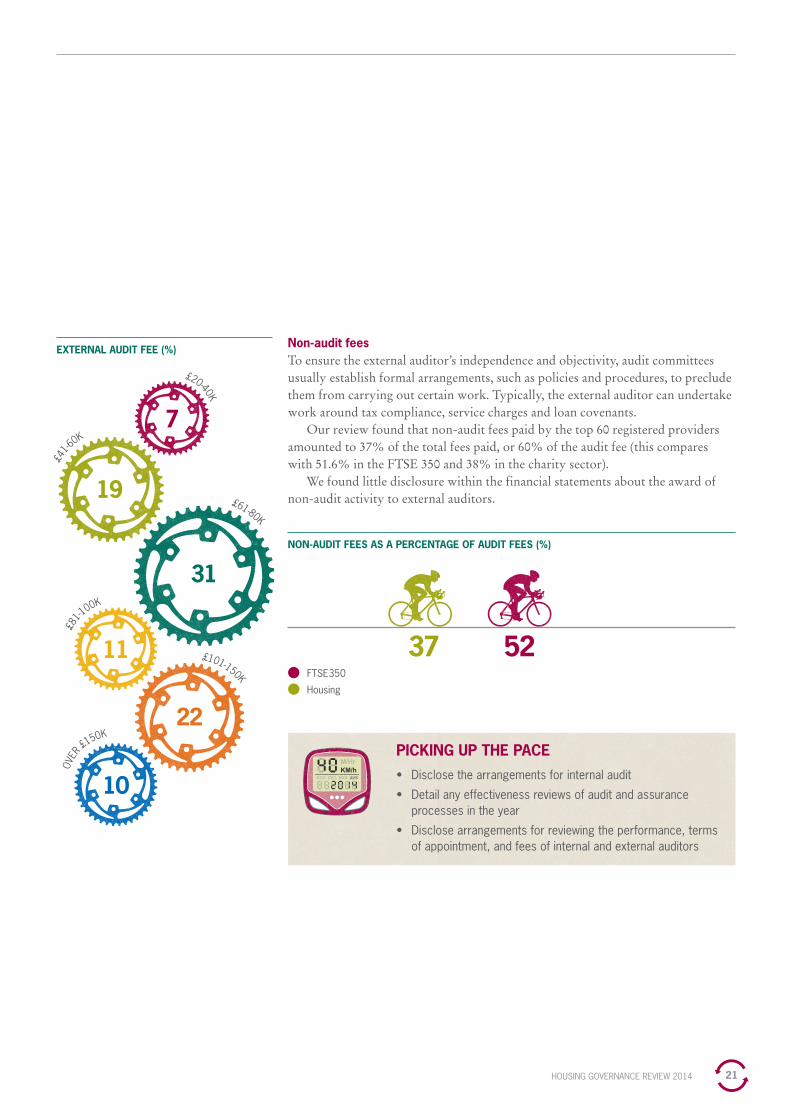

Audit feesOur review of the total external audit and non-audit fees for the top 60 providers found that more than £9.3 million was paid for such services the year-ended 31 March 2013. This was split between audit fees of £5.8 million and non-audit fees of £3.5 million. The average audit fee was £98,000, within a wide range of £23,000 to £400,000; the average non-audit fee was £59,000.

The accounts indicate that 50% of the top 60 registered providers paid audit fees within the ranges of £41,000 to £80,000. Only 7% paid less than £40,000, with 10% paying more than £150,000.

HOUSING GOVERNANCE REVIEW 2014 21

7

11

10

19

31

22

£20-40K

£41-6

0K

£81-1

00K

OVER

£150K

£61-80K

£101-150K

EXTERNAL AUDIT FEE (%) Non-audit feesTo ensure the external auditor’s independence and objectivity, audit committees usually establish formal arrangements, such as policies and procedures, to preclude them from carrying out certain work. Typically, the external auditor can undertake work around tax compliance, service charges and loan covenants.

Our review found that non-audit fees paid by the top 60 registered providers amounted to 37% of the total fees paid, or 60% of the audit fee (this compares with 51.6% in the FTSE 350 and 38% in the charity sector).

We found little disclosure within the financial statements about the award of non-audit activity to external auditors.

NON-AUDIT FEES AS A PERCENTAGE OF AUDIT FEES (%)

FTSE350

Housing

37 52

PICKING UP THE PACE• Disclosethearrangementsforinternalaudit

• Detailanyeffectivenessreviewsofauditandassuranceprocesses in the year

• Disclosearrangementsforreviewingtheperformance,termsof appointment, and fees of internal and external auditors

HOUSING GOVERNANCE REVIEW 2014 22

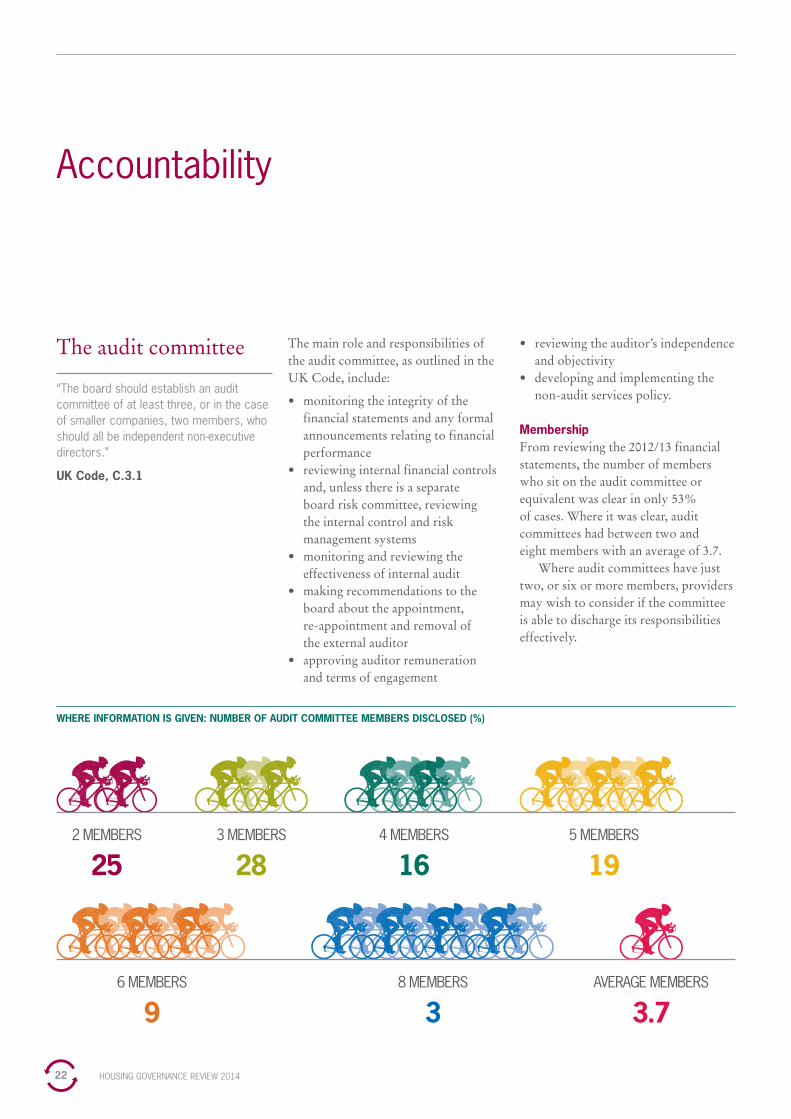

Accountability

The audit committee

“The board should establish an audit committee of at least three, or in the case of smaller companies, two members, who should all be independent non-executive directors.”

UK Code, C.3.1

The main role and responsibilities of the audit committee, as outlined in the UK Code, include:

• monitoringtheintegrityofthefinancial statements and any formal announcements relating to financial performance

• reviewinginternalfinancialcontrolsand, unless there is a separate board risk committee, reviewing the internal control and risk management systems

• monitoringandreviewingtheeffectiveness of internal audit

• makingrecommendationstotheboard about the appointment, re-appointment and removal of the external auditor

• approvingauditorremuneration and terms of engagement

• reviewingtheauditor’sindependenceand objectivity

• developingandimplementingthenon-audit services policy.

MembershipFrom reviewing the 2012/13 financial statements, the number of members who sit on the audit committee or equivalent was clear in only 53% of cases. Where it was clear, audit committees had between two and eight members with an average of 3.7.

Where audit committees have just two, or six or more members, providers may wish to consider if the committee is able to discharge its responsibilities effectively.

2 MEMBERS

25

6 MEMBERS

9

8 MEMBERS

3

AVERAGE MEMBERS

3.7

3 MEMBERS

28

4 MEMBERS

16

5 MEMBERS

19

WHERE INFORMATION IS GIVEN: NUMBER OF AUDIT COMMITTEE MEMBERS DISCLOSED (%)

HOUSING GOVERNANCE REVIEW 2014 23

Committee members’ names and attendanceAs well as the number of audit committee members, we also sought to identify their names and attendance records.

We found that 58% of providers do not provide any details about their audit committee members. Forty per cent do include the names of members but only 15% give attendance levels.

Such information would enable readers to better understand the additional responsibilities of board members who serve on committees.

None

Number of members only

Names only

Names and attendance

AUDIT COMMITTEE MEMBER DETAILS (%)

58

2

25

15

Describing the audit committee’s workThe board approves the terms of reference for the audit committee, setting out its role and remit. Eighty-eight per cent of registered providers repeat aspects of the audit committee’s responsibilities within their financial statements, rather than setting out what the committee did during the year. This does not suggest that audit committees are not discharging their responsibilities, rather that they are not publicising their work.

The UK Code 2012 introduced new revisions for audit committee reporting. These include reporting on:

• significantjudgementsandestimatesinrelationtothefinancial statements

• thebasisonwhichitdeterminestheannualreportisfair,balanced and understandable

• theprocessbywhichthecommitteehasassessedtheeffectiveness of the audit process.

Housing sector providers are not required to produce an audit committee report, although those who follow the UK Code should do so. Our FTSE 350 Corporate Governance Review 2013 highlights that 44% of company reports include an audit committee chair’s report, which provides a personal commentary on the work of the committee during the year. By contrast, in the registered provider accounts surveyed, very little information is given on the structure and activity of the audit committee.

PICKING UP THE PACE• Disclosureshouldinclude:

– the name of each committee– its key responsibilities– matters considered during the year– meeting frequency– details of how the committee reports to the main board– the names of the board members (and outside

members) sitting on each committee– why committee members are selected (for example,

audit committees normally include a member with relevant financial and/or audit experience)

– the attendance rates for each committee member

• Considerincludingareportbytheauditcommitteechair setting out how the committee has discharged its responsibilities and conformed to best practice

HOUSING GOVERNANCE REVIEW 2014 24

“The role of the audit committee has been written about in detail by the good and the great – there are books and papers dedicated to the topic, so what can I tell you that is different? This is a ‘pocket-size’ reflection on the good and effective audit committees that I see operating within the housing sector today.

‘Risk awareness, management and change’ is the mantra we need to heed. This is the environment that currently exists and we have to operate within. So, does that put additional pressure on the audit committee? The role of providing assurance has always been the task of an audit committee within a benign or ever changing environment, and does not change whatever the environment.

So, how do good and effective audit committees operate in organisations that are becoming more diverse? Ten points I’ve noted in really good committees are that:

1. All members take time to really understand the business, its operating environment and its future strategy, linking risk to all aspects

2. They ensure the committee does what it is meant to do – focusing on financial reporting (where there’s no separate finance committee) and internal controls

3. The committee gains assurance on business risk and compliance, considering especially the views of regulators

4. Where there’s no separate finance committee, a good audit committee ensures the accounts ‘tell the story’ – challenging whether they are consistent with the information received throughout the year

5. The membership is diverse – not all members have to have a financial background as a wider perspective is very important

6. A good training programme is in place and there is an awareness and understanding of any impending accounting changes

7. They ensure auditor independence and that a healthy (not cosy) relationship exists between the auditor and the finance team, reviewing their performance annually

8. The audit committee does not work in isolation – knowledge and understanding is shared, especially of risk, with the board and executive

9. Time is spent measuring their own effectiveness – challenging themselves on their added value

10. Finally, they do not just tick the boxes. They debate and challenge to seek the assurance and listen to ‘the lone voice in the wilderness’ – understanding that they may be saying something important.”

VIEW FROM THE TRACKSIDE

Dr Fiona Underwood, Partner of Altair, and Chair of the assurance and audit committee of Bromford Housing Group

HOUSING GOVERNANCE REVIEW 2014 25

Risk management

“It is the board’s responsibility for ‘establishing and overseeing a risk management framework in order to safeguard the assets of the organisation’.”

NHF Code, C.3.1

“The board should, at least annually, conduct a review of the effectiveness of the company’s risk management and internal control systems and should report to shareholders that they have done so. The review should cover all material controls, including financial, operational and compliance controls.”

UK Code, C.2.1

Understanding and managing riskFrom 2012, all financial services companies were required to have separate risk and audit committees. Only 38% of FTSE 350 companies outside this arena have discrete risk committees. Although ultimate responsibility for risk must stay with the board, sub-committees help the board to focus on key risk issues and risk review findings and give strategic direction on risk, rather than spending its limited time on detailed risk reviews.

Within housing, there is no requirement for a separate risk committee. Arrangements are similar to those in the charity sector, that is responsibility is shared between the audit committee and the board. We found that 53% of registered providers state that they have an audit committee with the word ‘risk’ in its title, but that none say they have a separate risk committee (although 3% mention a risk panel). The remaining 47% have an ‘audit committee’ which we assume takes responsibility for approving and monitoring the risk register for approval by the board, as per good practice in the NHF Code.

TITLES OF COMMITTEES WHOSE REMIT INCLUDES AUDIT AND RISK

53%AUDIT AND RISK

COMMITTEE

47%AUDIT COMMITTEE

HOUSING GOVERNANCE REVIEW 2014 26

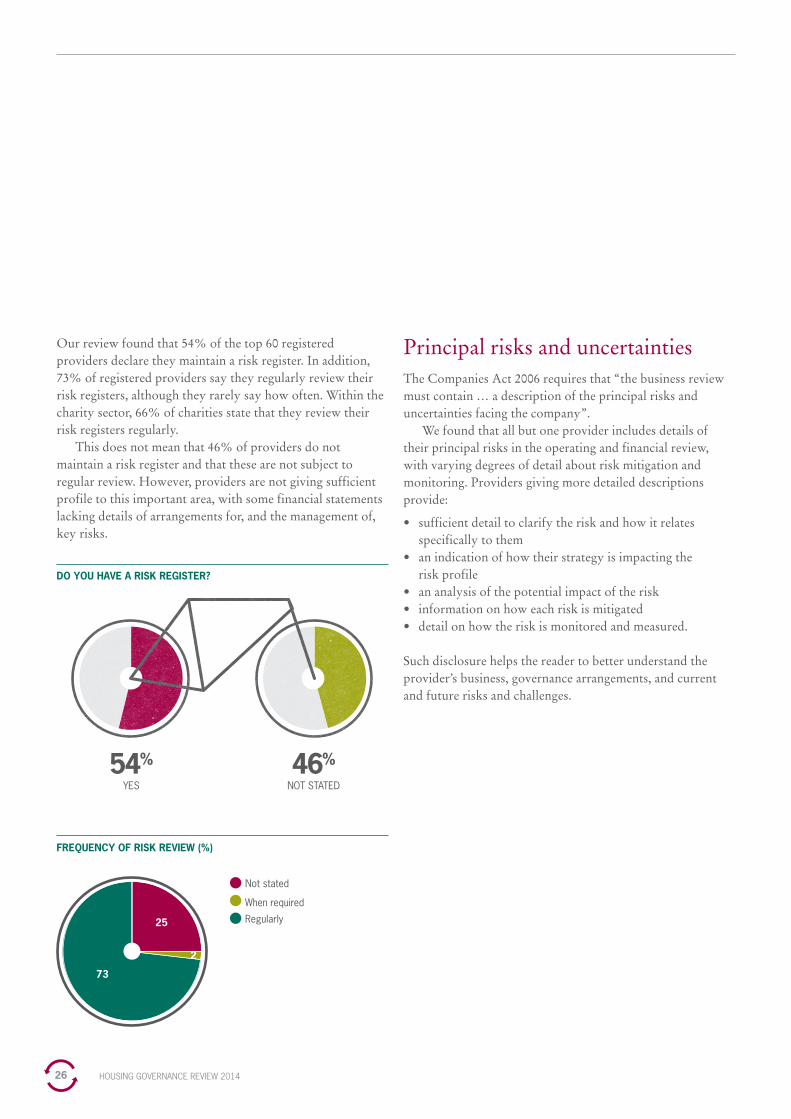

Our review found that 54% of the top 60 registered providers declare they maintain a risk register. In addition, 73% of registered providers say they regularly review their risk registers, although they rarely say how often. Within the charity sector, 66% of charities state that they review their risk registers regularly.

This does not mean that 46% of providers do not maintain a risk register and that these are not subject to regular review. However, providers are not giving sufficient profile to this important area, with some financial statements lacking details of arrangements for, and the management of, key risks.

DO YOU HAVE A RISK REGISTER?

54%YES

46%NOT STATED

Not stated

When required

Regularly

FREQUENCY OF RISK REVIEW (%)

2

25

73

Principal risks and uncertaintiesThe Companies Act 2006 requires that “the business review must contain … a description of the principal risks and uncertainties facing the company”.

We found that all but one provider includes details of their principal risks in the operating and financial review, with varying degrees of detail about risk mitigation and monitoring. Providers giving more detailed descriptions provide:

• sufficientdetailtoclarifytheriskandhowitrelatesspecifically to them

• anindicationofhowtheirstrategyisimpactingthe risk profile

• ananalysisofthepotentialimpactoftherisk• informationonhoweachriskismitigated• detailonhowtheriskismonitoredandmeasured.

Such disclosure helps the reader to better understand the provider’s business, governance arrangements, and current and future risks and challenges.

HOUSING GOVERNANCE REVIEW 2014 27

Disclosure of main risksIn a sector where the core business is providing social housing, it is unsurprising that the main risks disclosed by the top 60 registered providers in their financial statements are broadly similar. The main risks named are shown in the table below, along with the number of providers disclosing them:

67

50

40

35

32 32 32

28 2826

23

2018 18

15 15

5 53

0

Welfare

refor

m

Acce

ss to

finan

ce

Econ

omic

climate

Govern

ment p

olicie

s

Strate

gy de

livery

Develo

pmen

t

Housin

g mark

et

Govern

ance

Delive

ring s

ervice

s

Regu

lation

Pens

ion co

sts

Repu

tation

Intere

st rat

es

Prope

rty sa

les

Asse

t man

agem

ent

Health

and s

afety

Procu

remen

t

Value

for m

oney

FRS1

02

5

10

20

25

30

35

40

45

50

55

60

65

70

15

FREQUENCY OF SPECIFIC RISKS (%)

HOUSING GOVERNANCE REVIEW 2014 28

The three most-cited risks are welfare reform, accessing finance and the economic climate. In addition, on the right, we list the risks most frequently identified in other sectors.

Not surprisingly, irrespective of sector, the main risks are around finance, funding cuts, quality, operational performance and regulation.

In housing, welfare reform is mentioned by 67% of registered providers. This is to be expected, given that the Welfare Reform Act 2012 came into force at the time (April 2013). Like welfare reform, many of the other risks, such as, access to finance, the economic climate and government policies, are out of a registered provider’s control. Given the recent regulatory judgements and letters from the HCA to a number of providers, it is interesting that only 5% list value for money as a risk. The real challenge as encouraged by the new strategic reporting requirements is to leave out the ‘Business as Usual’ notes and just report the strategic risks – are registered providers up for it?

Our study also found that the number of risks mentioned in the reports varies from one to 15, with the average being 5.7. This is not dissimilar to the NHS, but is half the average of the corporate sector, which is 11. A focus on increased transparency would suggest that discussion of a wider range of risks would be appropriate.

No./Sector HousingLocal

government Healthcare Charities Corporates

1 Welfare reform Finance Finance RecessionOperational

performance

2Access to

financeWelfare reform Quality

Loss of key contracts

Finance

3Economic climate

DemographyOperational

performanceDelivery of

serviceRegulatory/ compliance

Number of organisations

0

0 2 4 6 8 10 12 14 16

12345

6789

10

5.7

1112131415

AverageNum

ber

of r

isks

HOW MANY RISKS ARE MENTIONED?

PICKING UP THE PACE• Beclearaboutwhetherthereisariskregisterandhowoften

it is reviewed and by who

• Considerhowyourriskscomparetosimilarorganisations

• Beclearonrisksandmitigation

HOUSING GOVERNANCE REVIEW 2014 29

“Four years ago as a housing provider a critical Audit Commission inspection told us we’d lost our way. From being a market leader we had lost touch with residents, our services were no longer fit for purpose. My challenge was to develop a risk management approach to provide on-going assurance on service delivery – this couldn’t happen again.

To get a consistent view on ‘what is risk’ we held ‘risk’ days with managers so we could show the wider impact of issues and risks and increase learning and thinking about our reputation as an organisation. Alongside this we held risk workshops and consolidated our 140 risks down to 8 operational and 5 strategic risks. Put simply, our strategic risks are those which might lead to the failure to deliver the Corporate Plan and operational risks are those which might lead to failure in service quality. These are reviewed monthly by management teams and ‘emerging issues’ reported into the Executive Management Team who report overall risk scores and our ‘risk map’ to the various committees which audit our work. Whilst we share the detail, we ensure their focus is on the bigger picture.

At the same time, we also looked at our ‘lines of defence’ and focused on keeping it simple – we set ourselves a goal of capturing our ‘assurance framework’ on one page. We also changed how we involve residents in monitoring our service delivery. A team of trained residents now carry out inspections of the service experience – this provides valuable insight and assurance on our services alongside the scrutiny of performance KPIs which is undertaken by our local Resident Assurance Committee’s.

This approach to risk management is underpinned in our reporting on KPIs. Performance is rated red/amber/green which allows for exception reporting and trend analysis. This helps the Resident Assurance Committee’s to focus on service improvement plans and it means that the board can focus on the potential impact on strategic issues.

Underpinning this we present a monthly PESTLE report to the board which allows us to look further ahead. We’ve split our board meetings too, we have four covering the business, one on the year end accounts and 5 which are less structured meetings, focusing on discussions around the corporate strategy and the bigger picture. This means we get into a really good space when we need to focus on matters of the here and now whilst still having space to think about more longer term, strategic issues. Where we have very specific areas of interest, we set up smaller, sub groups to consider them but with clear lines of alignment to the Group Board.

To ensure a holistic, joined up approach, we report internal audit headlines to Committees and the Chairs of the various boards and meet with the Group Audit Chair every 6 months to consider risk and issues emerging from assurance work.

As a result of these changes, the board are now in a much better position to understand risks as they emerge and to understand how the organisation as a whole considers risk. Similarly, across the organisation, there is a much clearer link between operations and risk assessment and management.”

Tracy Allison, Group Director of Corporate Services at The Hyde Group

TH

E I

N S I D E T R

AC

K

HOUSING GOVERNANCE REVIEW 2014 30

Internal control

“It is the board’s responsibility ‘for establishing, overseeing and reviewing annually a framework of delegation and systems of internal control’.”

NHF Code

“The board should, at least annually, conduct a review of the effectiveness of the company’s risk management and internal control systems and should report to shareholders that they have done so.”

UK Code, C.2.1

All boards of social landlords are required to conduct an annual review of the effectiveness of their system of internal control. Social landlords must ensure that they consider the regulatory requirements relevant to them and include in their financial statements the disclosures and statements required by legislation and/or relevant accounting direction, determination or order.

A statement of internal control no longer needs to feature in the annual report, although its inclusion is still considered best practice. Our review found that all providers followed this convention.

Internal control is the process, effected by the board, management, and other personnel, providing reasonable assurance in achieving objectives in the following three categories:

1. Reliability of financial reporting2. Effectiveness and efficiency of

operations3. Compliance with applicable laws

and regulations

Risk management and internal control and assurance processes must be seen within the overall organisational context. Among other things, good governance requires that a registered provider is led by an effective board, organisational and management structures reflect the provider’s business objectives, and the provider operates a framework that effectively identifies and manages the risks to achieving such objectives. Consequently, risk management and control processes should be continuous and embedded across an organisation’s activities.

In today’s complex economic environment, the housing sector faces some of its biggest challenges for decades, with a shortage of homes, reduced access to development grants,

diversification into non-core business and, of course, welfare reform. The HCA is looking to apply greater focus on risk management and contingency planning, as well as to seek assurances around the controls designed to protect social housing assets.

The board should use the internal control statement to communicate with stakeholders, and other interested parties, about the risk and internal controls it faces. The statement should include the main features of the risk management process and the systems of internal control. From year-to-year, as plans are implemented and strategies evolve, boards should record changes in their patterns of risk and control.

However, our review identified many similarities between this year’s statements on internal control and previous ones. This could lead a reader to question the robustness of the annual review process and whether the provider has taken proper steps to satisfy itself that its internal control system remains sound and appropriate in the changing landscape.

PICKING UP THE PACE• Makeyourinternalcontrolstatementspecificto

the organisation

• Commentonareasaddressedintheyear

• Highlightareaswherechangeswillbemade

• Bespecific

HOUSING GOVERNANCE REVIEW 2014 31

The debate among housing board members as to whether they should be paid has strong opinions on both sides.

Non-executive directors in the corporate world have received payment for many years. In the charity sector, on the other hand, despite trustees’ significant responsibilities, most go unpaid. Those who argue for trustee remuneration believe it allows charities to recruit those who could not afford to give their time unpaid, encouraging diversity of income on a board.

In the housing sector, if payment to board members is considered appropriate, the NHF Code states that boards should ensure that:

• thereisaclearbusinesscase• thereisamechanismforestablishingpaymentlevelsthatis

independent of the board• agreedpaymentlevelsareproportionatetothe

organisation’s size and resources• paymentlevelsmeetindustrynorms• paymentislinkedtospecifieddutiesagainstwhich

performance will be reviewed• paymentfornon-executivesisfullydisclosedona

named basis.

To pay or not to payArguably, the board member’s role is getting harder and more challenging, as they make increasingly commercial decisions around their respective strategies. We found that 83% of the top 60 pay their board members, a ratio which we believe is growing in direct response to the increasing complexity of the role.

Remuneration

AVERAGE REMUNERATION FOR NEDs (£)

9,874

7,120

11,805HOUSING

NHS TRUST (2012)

NHS

FO

UNDATION TRUST (2012)

Average payment for a board memberThe average pay of £9,874 per board member is more than non-executive directors received in 2012 in NHS trusts (£7,120), but less than they received in foundation trusts (£11,805). Where charities pay their trustees, we found the average pay in 2013 was £10,180*.

Average chair’s payThe NHF Code states that the chair’s responsibilities include, but are not limited to:

• ensuringtheefficientconductoftheboard’sbusinessandof the organisation’s general meetings

• makingsuretheorganisationprovidesroleprofilesandcompetency frameworks for all board members

• ensuringallboardmembershavetheopportunitytoexpress their views

• establishingaconstructiveworkingrelationshipwith,andproviding support for, the chief executive and ensuring the board acts in partnership with executive staff

• makingsuretheboarddelegatessufficientauthorityto its committees

• ensuringtheboardreceivesprofessionaladvicewhenneeded

• representingtheorganisationasappropriate• takingdecisionsdelegatedtothechair.

*This refers to the charity governance review 2013 as similar statistics were not collected for 2014.

HOUSING GOVERNANCE REVIEW 2014 32

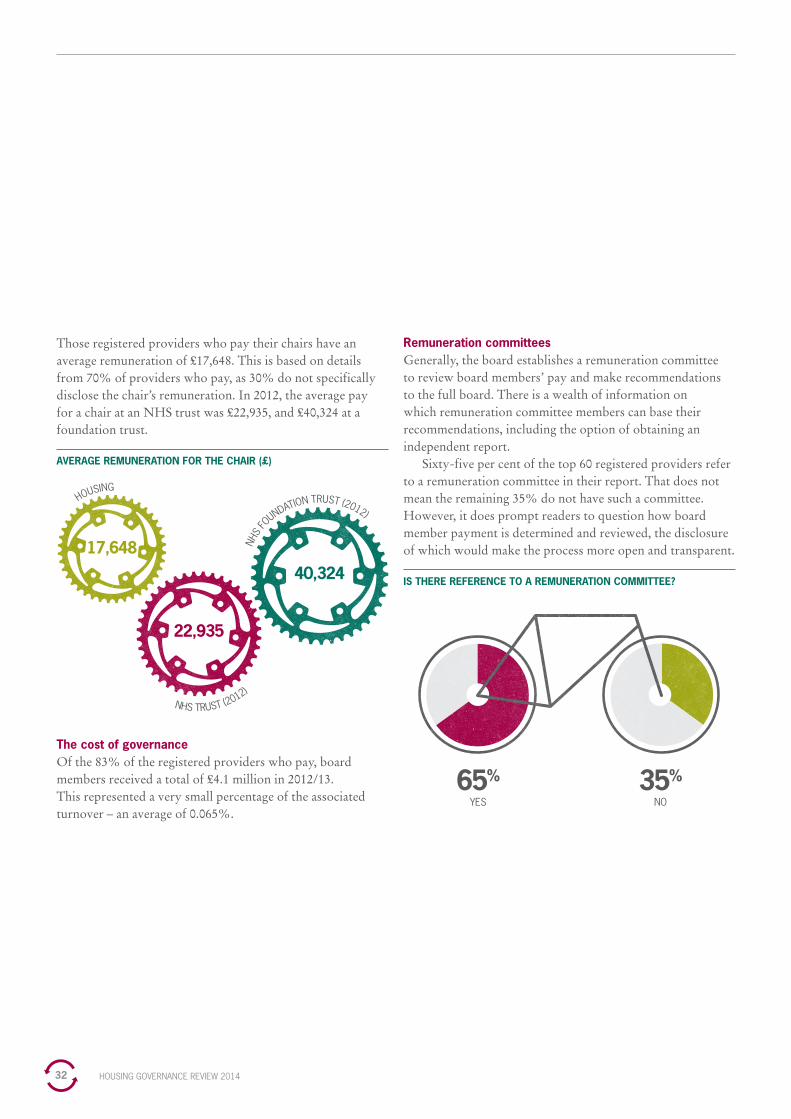

Those registered providers who pay their chairs have an average remuneration of £17,648. This is based on details from 70% of providers who pay, as 30% do not specifically disclose the chair’s remuneration. In 2012, the average pay for a chair at an NHS trust was £22,935, and £40,324 at a foundation trust.

AVERAGE REMUNERATION FOR THE CHAIR (£)

22,935

17,64840,324

HOUSING

NHS TRUST (2012)

NHS

FOUNDATION TRUST (2012)

The cost of governanceOf the 83% of the registered providers who pay, board members received a total of £4.1 million in 2012/13. This represented a very small percentage of the associated turnover – an average of 0.065%.

Remuneration committeesGenerally, the board establishes a remuneration committee to review board members’ pay and make recommendations to the full board. There is a wealth of information on which remuneration committee members can base their recommendations, including the option of obtaining an independent report.

Sixty-five per cent of the top 60 registered providers refer to a remuneration committee in their report. That does not mean the remaining 35% do not have such a committee. However, it does prompt readers to question how board member payment is determined and reviewed, the disclosure of which would make the process more open and transparent.

IS THERE REFERENCE TO A REMUNERATION COMMITTEE?

65%YES

35%NO

HOUSING GOVERNANCE REVIEW 2014 33

Remuneration reportFollowing high profile debate and challenge about executive and non-executive directors’ pay in the corporate world, in 2012 the Department for Business, Innovation and Skills published a consultation document to increase transparency in the way that remuneration is set and paid. This led to new requirements for quoted company remuneration reports.

Under the regulations and related changes to the Companies Act 2006:

• Theremunerationreportmustbesplitintoapolicyreport (not subject to audit) and an annual report on remuneration (some elements of which are subject to audit)

• Thepolicyreportwillbesubjecttoabindingshareholdervote which must take place in the first financial year beginning on or after 1 October 2013

• Theannualreportonremunerationmustprovidedetailson remuneration in the period and some information for the following year. It will be subject to an annual advisory shareholder vote

• Therequiredcontentsoftheannualreportonremuneration are substantially different from before. They include the ‘single figure’ for the total remuneration of each director and a number of other new requirements

The Financial Reporting Council is now consulting on aspects of remuneration reporting.

The housing sector is not required to produce a remuneration report although, if providers do, the resulting transparency may address many stakeholders concerns.

An additional area of great discussion in FTSE organisations is the payment of bonuses to board members with linkage to KPIs with possible clawback if issues arise. Bonuses are less typical in the sector, but a greater linkage to performance may be worthy of consideration.

PICKING UP THE PACE• Includearemunerationstatementor

report setting out the governance process in determining pay levels and linkage to performance

Our findings indicate that, in their value for money statement, only 23% of the top 60 providers refer to their KPIs and how they performed against targets.

HOUSING GOVERNANCE REVIEW 2014 34

Narrative reporting

“The board must publish an annual report of the organisation’s activities and performance.”

NHF Code

Registered providers include information about their activities and performance in the operating and financial review which usually details their vision, value and principal activities, performance against strategic objectives and a financial review. For the first time, in 2013, they had to include a value for money statement.

In early 2014, the HCA highlighted the findings from their review of the previous year’s statements which resulted in several downgrades in governance ratings for housing associations deemed not to have met the requirements and letters to a number of providers highlighting areas for improvement. Given the importance of these disclosures we focus our review of narrative reporting on them.

Value for moneyThe change in requirement came from the HCA’s value for money standard and the subsequent accounting direction.

As this was the first year of the new requirement, which did not include guidance on content, perhaps inevitably the length of the value for money statements varied considerably, from one to 10 pages.

One expectation was for information to be specific, which can be measured to some extent through KPIs. Our findings indicate that, in their value for money statement, only 23% of the top 60 providers refer to their KPIs and how they performed against targets. Fifty per cent either make no reference to their KPIs, or do not list them, making it challenging for readers to put the statements into perspective.

No mention of KPIs

KPIs mentioned but not listed

KPIs listed but performance not included

KPIs listed and performance included

HOW ARE KPIs INCLUDED IN THE VALUE FOR MONEY STATEMENT (%)

12

38

27

23

HOUSING GOVERNANCE REVIEW 2014 35

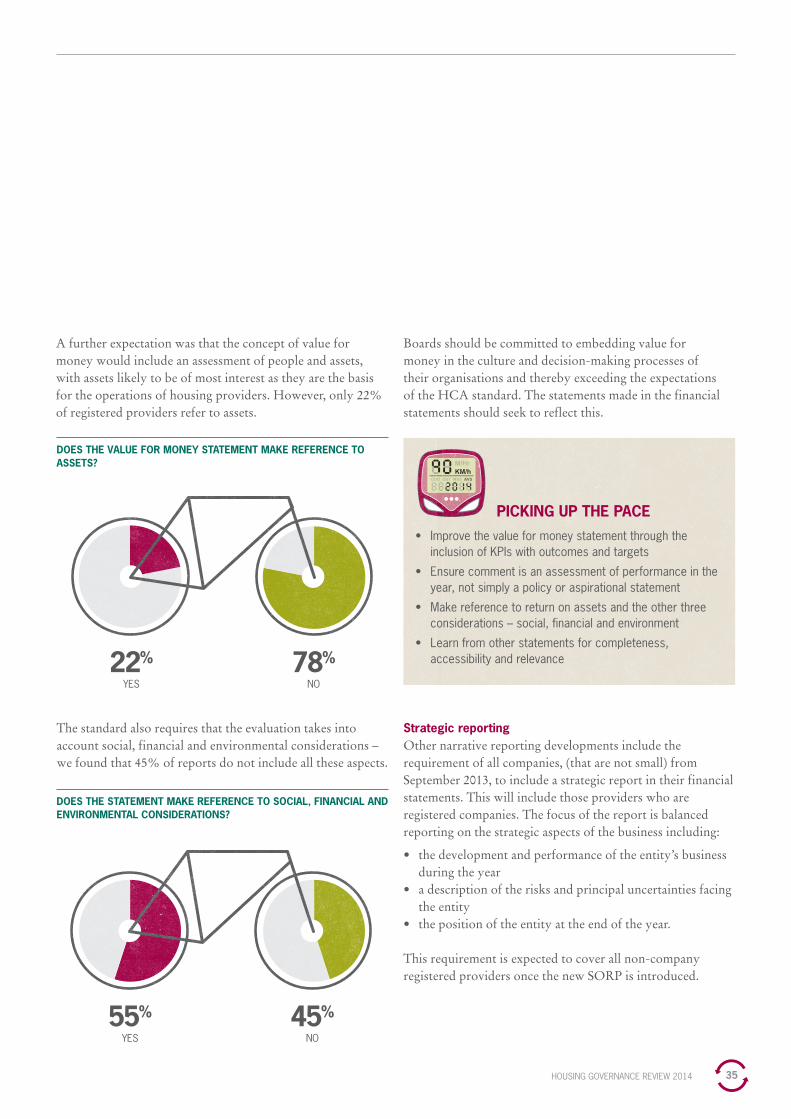

A further expectation was that the concept of value for money would include an assessment of people and assets, with assets likely to be of most interest as they are the basis for the operations of housing providers. However, only 22% of registered providers refer to assets.

22%YES

55%YES

78%NO

45%NO

DOES THE VALUE FOR MONEY STATEMENT MAKE REFERENCE TO ASSETS?

The standard also requires that the evaluation takes into account social, financial and environmental considerations – we found that 45% of reports do not include all these aspects.

DOES THE STATEMENT MAKE REFERENCE TO SOCIAL, FINANCIAL AND ENVIRONMENTAL CONSIDERATIONS?

Boards should be committed to embedding value for money in the culture and decision-making processes of their organisations and thereby exceeding the expectations of the HCA standard. The statements made in the financial statements should seek to reflect this.

PICKING UP THE PACE• Improvethevalueformoneystatementthroughthe

inclusion of KPIs with outcomes and targets

• Ensurecommentisanassessmentofperformanceintheyear, not simply a policy or aspirational statement

• Makereferencetoreturnonassetsandtheotherthreeconsiderations – social, financial and environment

• Learnfromotherstatementsforcompleteness,accessibility and relevance

Strategic reportingOther narrative reporting developments include the requirement of all companies, (that are not small) from September 2013, to include a strategic report in their financial statements. This will include those providers who are registered companies. The focus of the report is balanced reporting on the strategic aspects of the business including:

• thedevelopmentandperformanceoftheentity’sbusinessduring the year

• adescriptionoftherisksandprincipaluncertaintiesfacingthe entity

• thepositionoftheentityattheendoftheyear.

This requirement is expected to cover all non-company registered providers once the new SORP is introduced.

HOUSING GOVERNANCE REVIEW 2014 36

About Grant Thornton

We are Grant Thornton UK LLPDynamic organisations know they need to apply both reason and instinct to decision making. At Grant Thornton, this is how we advise our clients every day. We combine award-winning technical expertise with the intuition, insight and confidence gained from our extensive sector experience and a deep understanding of our clients.