Embed Size (px)

Citation preview

David A. [email protected] www.affordablehousinginstitute.org

38 Chauncy Street, Suite 600 Boston, MA 02111 +1 (617) 502‐5913Copyright © 2015 Affordable Housing Institute

Housing’s value chains

© 2015 Affordable Housing Institute: all rights reserved

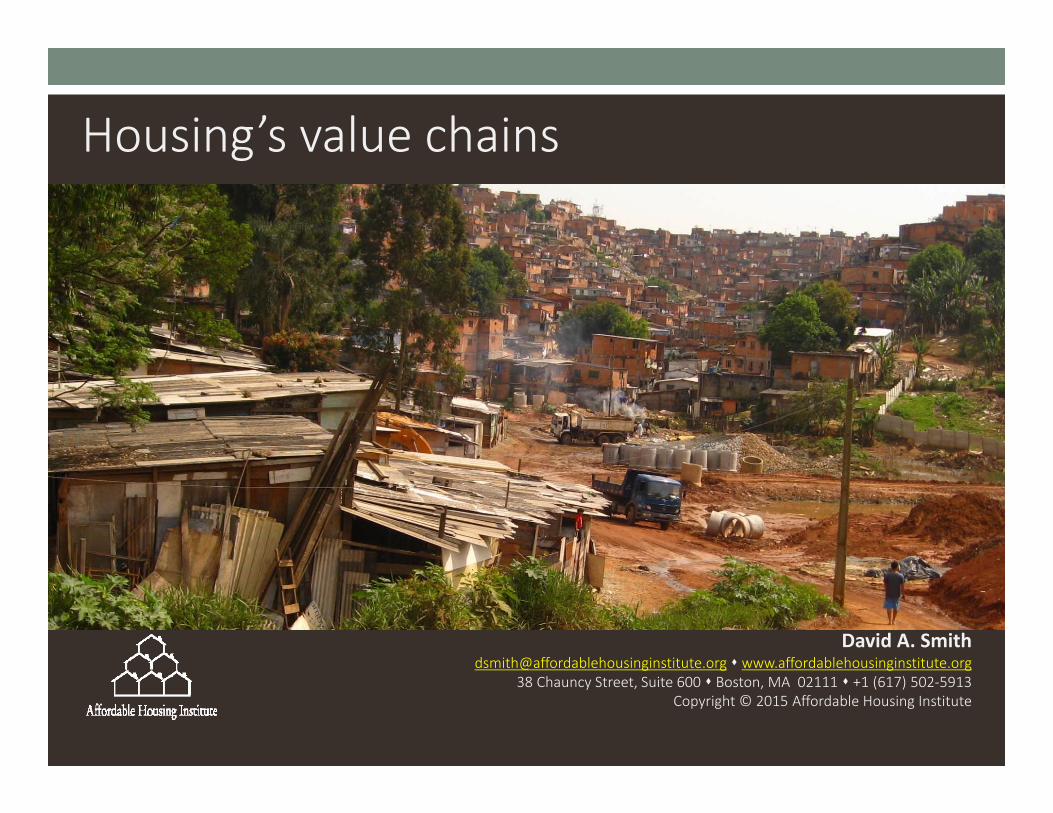

Housing is both social good and business Social good Created for public purpose Business Must be financeable, sustainable

Housing always requires capital finance Cost is 3x‐6x annual income To buy, you must borrow (long)

Longer loan term better housing options

Housing is a manufactured product And increasingly complex, technological, customized

A housing loan is also a manufactured product Complex features

Rate adjustment, incentives, penalties

Accompanying products (e.g. insurance)

Housing policy is a “strategic plan to create business”Whereby government creates business opportunity to shape and grow the market

27‐Dec‐15 2

RDP housingDurban, South Africa

© 2015 Affordable Housing Institute: all rights reserved

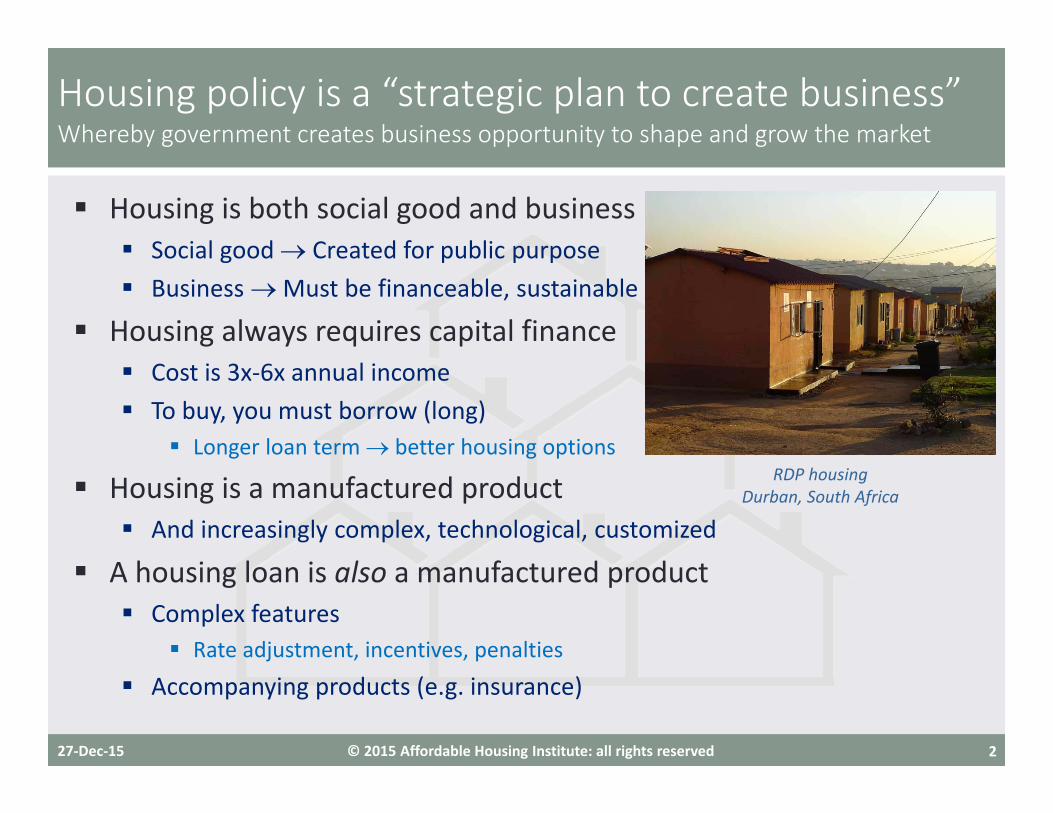

Housing markets work only when value chains workAnd when the value chains work, they’re invisible

27‐Dec‐15 3

• Households want quality housing

• May be “effective demand”• Need financing• Need down payments

• Homes are developed• Built, ready for move in• Designed to meet need• Priced to match market

• Household• Loan• Home• At same time

© 2015 Affordable Housing Institute: all rights reserved

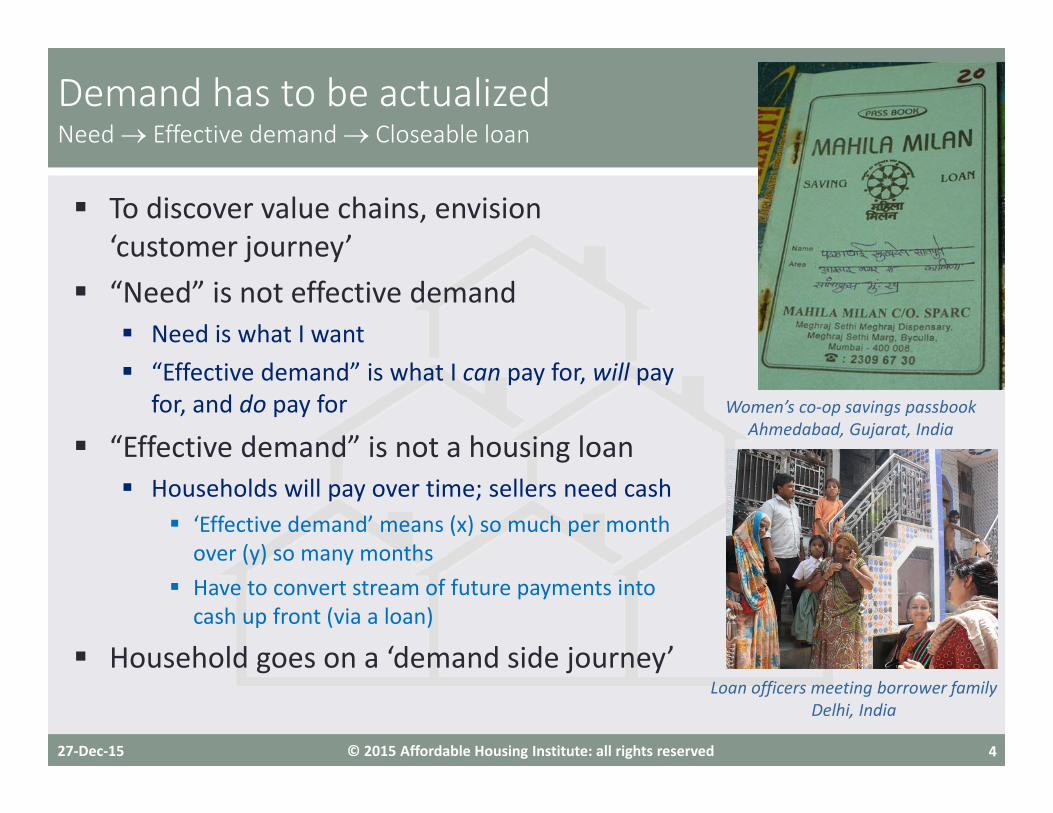

To discover value chains, envision ‘customer journey’

“Need” is not effective demand Need is what I want “Effective demand” is what I can pay for, will pay

for, and do pay for

“Effective demand” is not a housing loan Households will pay over time; sellers need cash

‘Effective demand’ means (x) so much per month over (y) so many months

Have to convert stream of future payments into cash up front (via a loan)

Household goes on a ‘demand side journey’

Demand has to be actualizedNeed Effective demand Closeable loan

27‐Dec‐15 4

Women’s co‐op savings passbookAhmedabad, Gujarat, India

Loan officers meeting borrower familyDelhi, India

© 2015 Affordable Housing Institute: all rights reserved

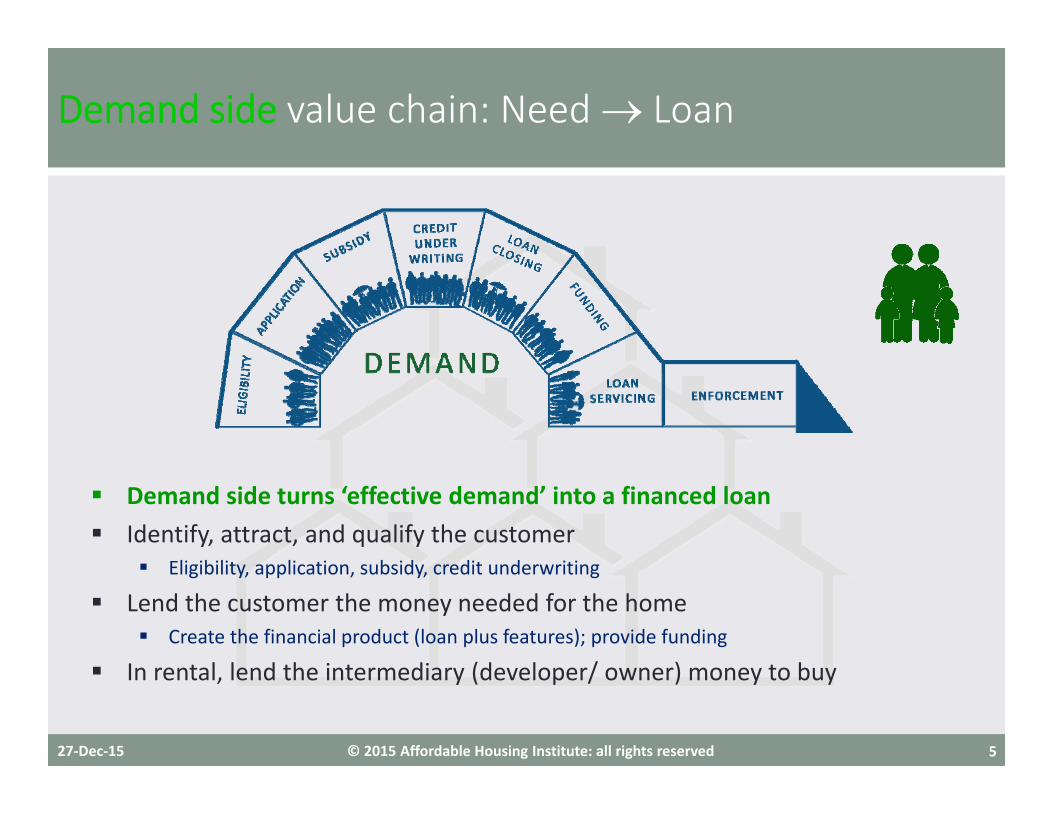

Demand side turns ‘effective demand’ into a financed loan Identify, attract, and qualify the customer

Eligibility, application, subsidy, credit underwriting

Lend the customer the money needed for the home Create the financial product (loan plus features); provide funding

In rental, lend the intermediary (developer/ owner) money to buy

Demand side value chain: Need Loan

27‐Dec‐15 5

© 2015 Affordable Housing Institute: all rights reserved

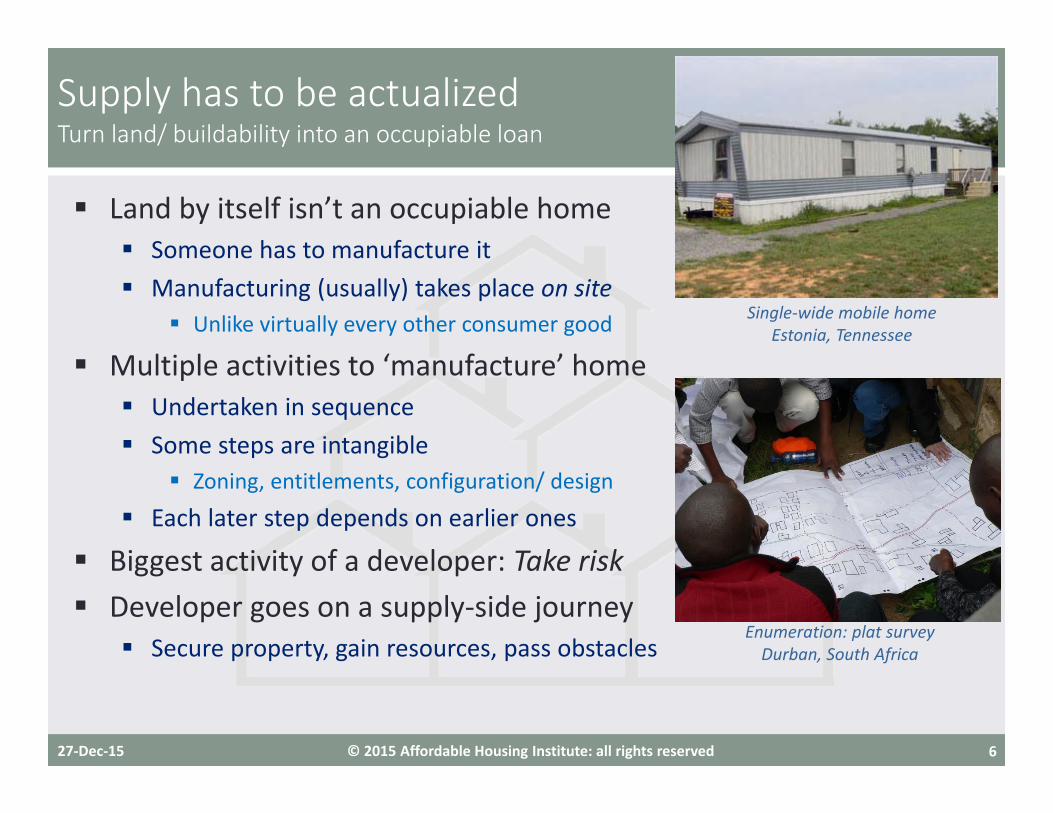

Land by itself isn’t an occupiable home Someone has to manufacture it Manufacturing (usually) takes place on site

Unlike virtually every other consumer good

Multiple activities to ‘manufacture’ home Undertaken in sequence Some steps are intangible

Zoning, entitlements, configuration/ design

Each later step depends on earlier ones

Biggest activity of a developer: Take risk Developer goes on a supply‐side journey

Secure property, gain resources, pass obstacles

Supply has to be actualizedTurn land/ buildability into an occupiable loan

27‐Dec‐15 6

Single‐wide mobile homeEstonia, Tennessee

Enumeration: plat surveyDurban, South Africa

© 2015 Affordable Housing Institute: all rights reserved

Supply‐side value chain: Land Home

27‐Dec‐15 7

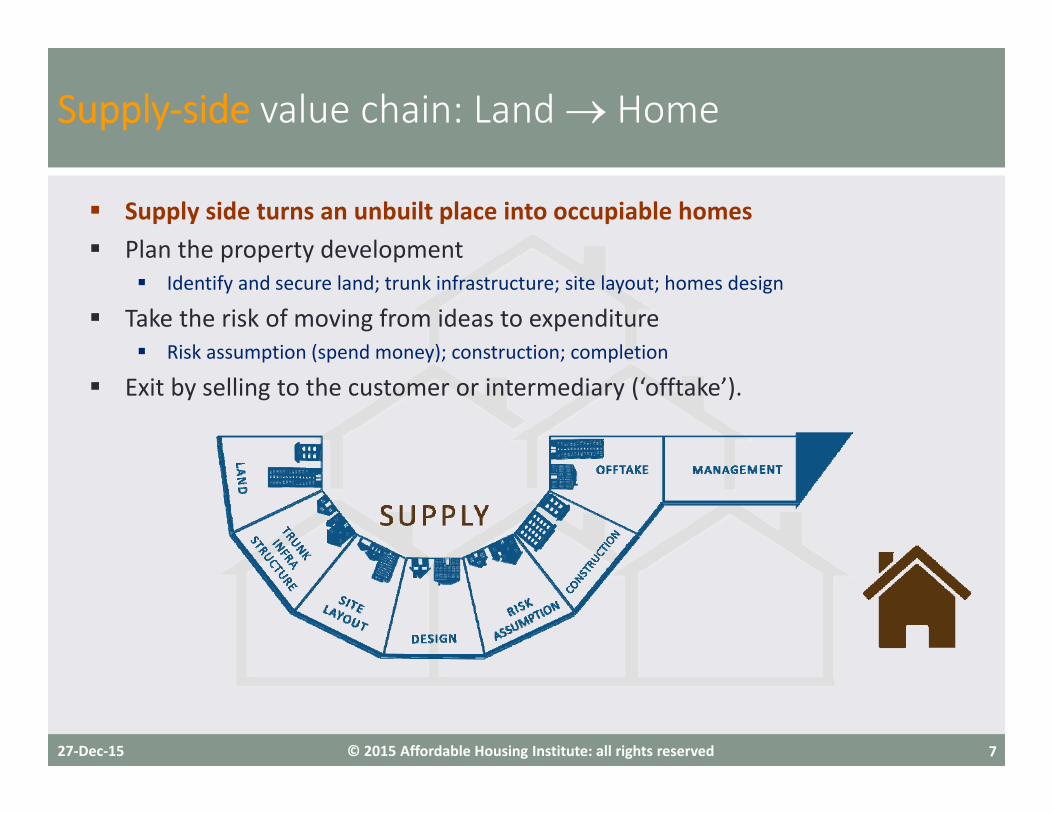

Supply side turns an unbuilt place into occupiable homes Plan the property development

Identify and secure land; trunk infrastructure; site layout; homes design

Take the risk of moving from ideas to expenditure Risk assumption (spend money); construction; completion

Exit by selling to the customer or intermediary (‘offtake’).

© 2015 Affordable Housing Institute: all rights reserved

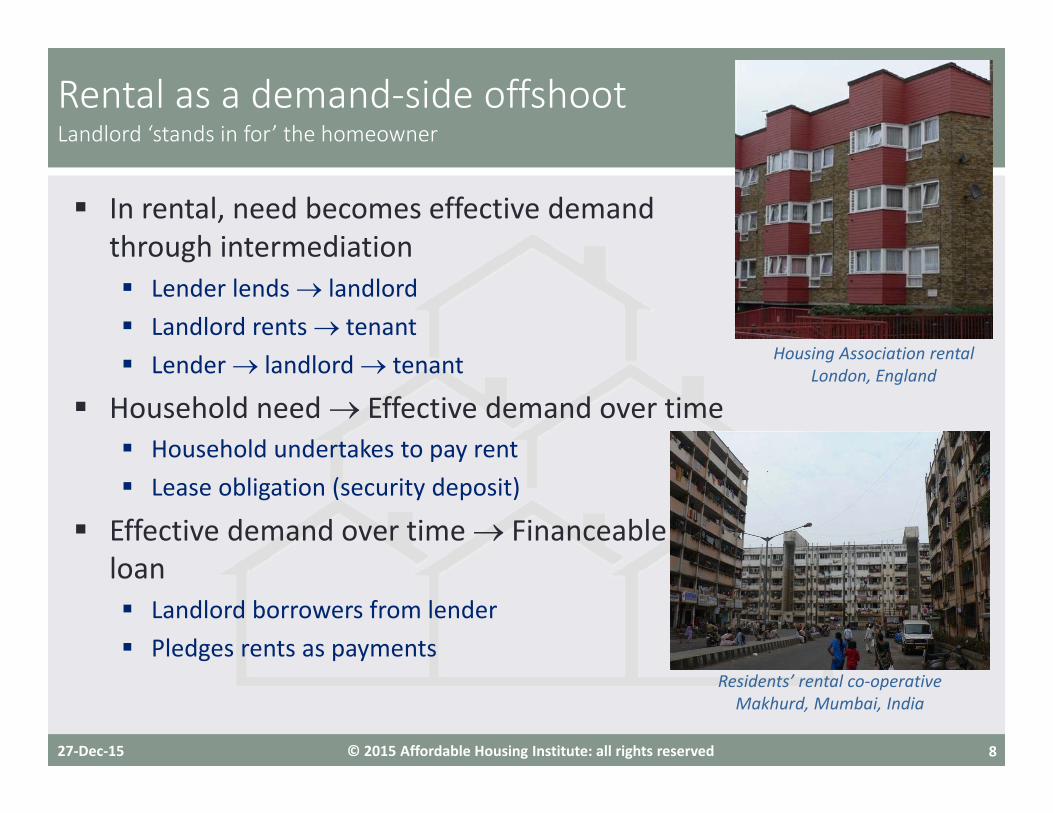

In rental, need becomes effective demand through intermediation Lender lends landlord Landlord rents tenant Lender landlord tenant

Household need Effective demand over time Household undertakes to pay rent Lease obligation (security deposit)

Effective demand over time Financeable loan Landlord borrowers from lender Pledges rents as payments

Rental as a demand‐side offshootLandlord ‘stands in for’ the homeowner

27‐Dec‐15 8

Residents’ rental co‐operativeMakhurd, Mumbai, India

Housing Association rentalLondon, England

© 2015 Affordable Housing Institute: all rights reserved

Development is a function all on its own Not construction, not design Not any of the technical functions

Development means taking all risks Everything from defective land title to

post‐occupancy latent defects/ liability Developers seek to lay off risk

Each risk laid off has a cost Turns inherent risk into counterparty risk

Developers ‘cannot’ build 100% with own cash Too much capital to maintain Too expensive to use own money

Risk assumption requires development finance Entails guarantees to the development financiers

Risk assumption = development financeDevelopers use Other People’s Money … but take everybody’s risks

27‐Dec‐15 9

Groundbreaking ceremonyVietnamese affordable housing

Boston, Massachusetts

© 2015 Affordable Housing Institute: all rights reserved

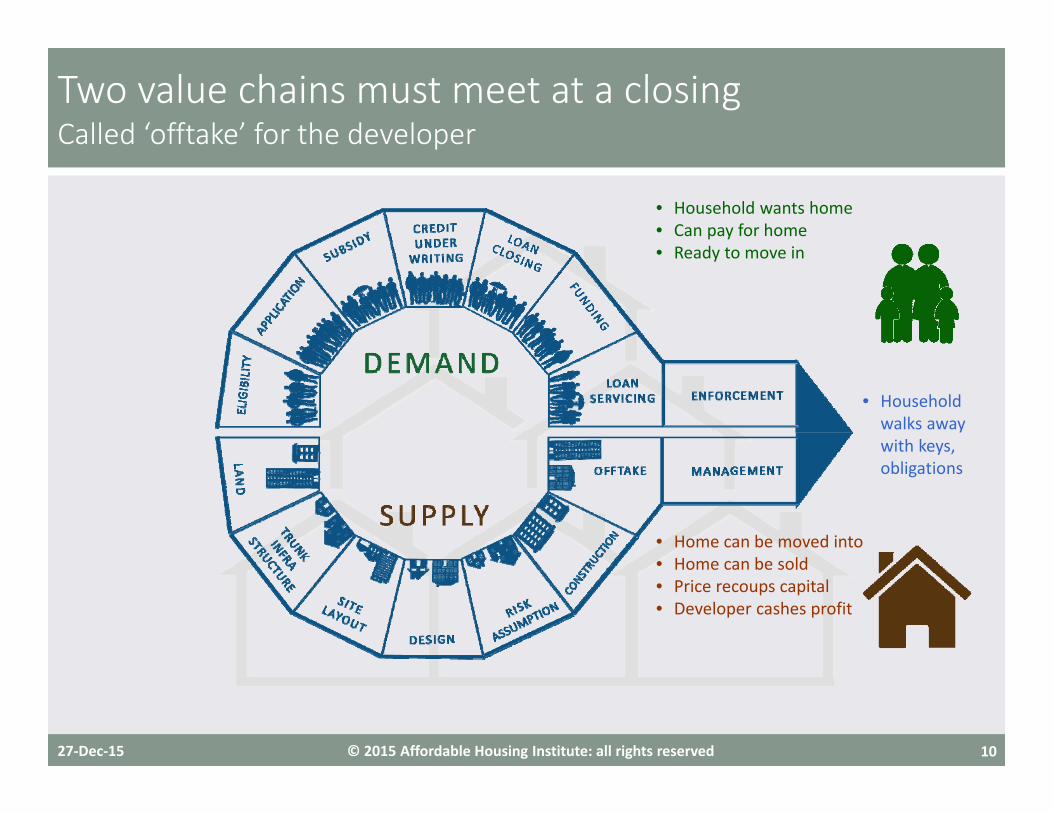

Two value chains must meet at a closingCalled ‘offtake’ for the developer

27‐Dec‐15 10

• Household wants home• Can pay for home• Ready to move in

• Home can be moved into• Home can be sold• Price recoups capital• Developer cashes profit

• Household walks away with keys, obligations

© 2015 Affordable Housing Institute: all rights reserved

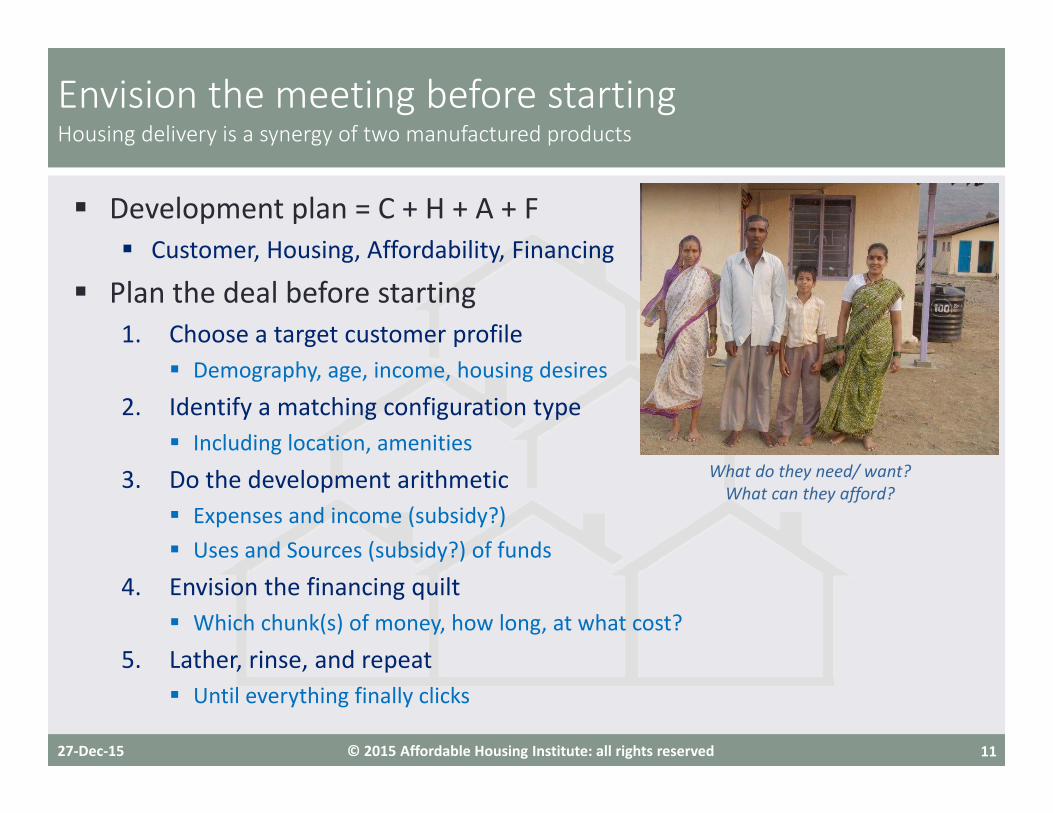

Development plan = C + H + A + F Customer, Housing, Affordability, Financing

Plan the deal before starting1. Choose a target customer profile

Demography, age, income, housing desires

2. Identify a matching configuration type Including location, amenities

3. Do the development arithmetic Expenses and income (subsidy?) Uses and Sources (subsidy?) of funds

4. Envision the financing quilt Which chunk(s) of money, how long, at what cost?

5. Lather, rinse, and repeat Until everything finally clicks

Envision the meeting before startingHousing delivery is a synergy of two manufactured products

27‐Dec‐15 11

What do they need/ want?What can they afford?

© 2015 Affordable Housing Institute: all rights reserved

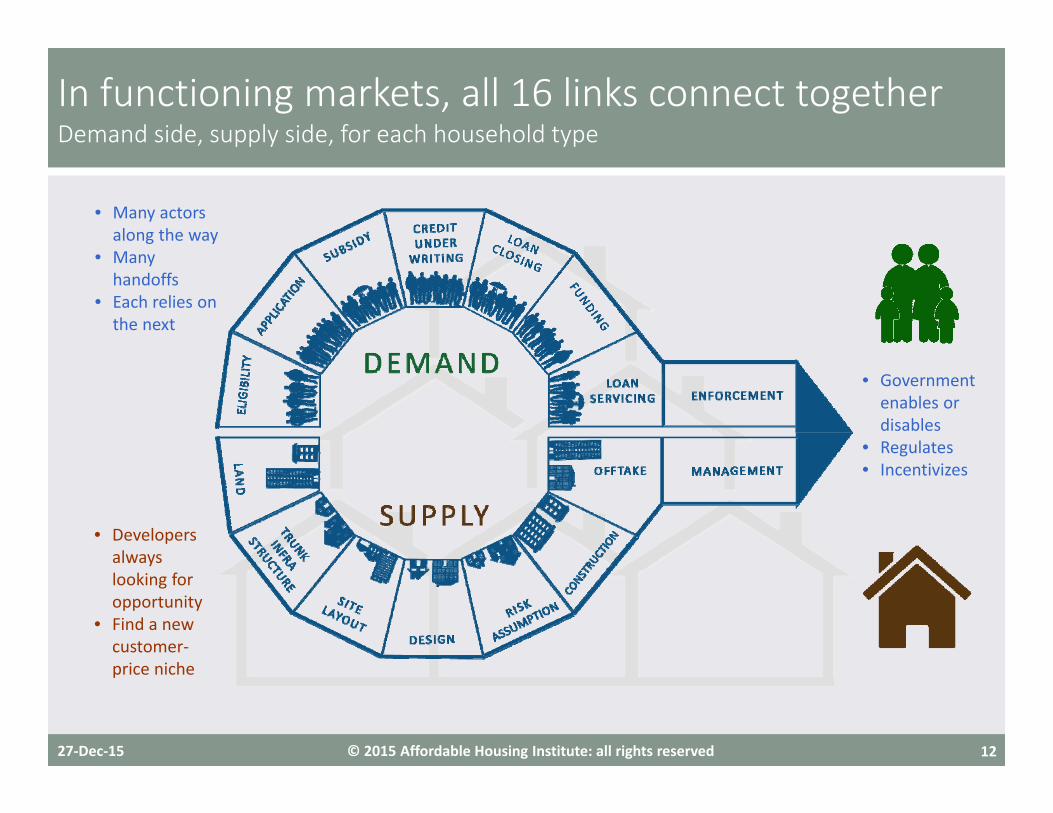

In functioning markets, all 16 links connect togetherDemand side, supply side, for each household type

27‐Dec‐15 12

• Many actors along the way

• Many handoffs

• Each relies on the next

• Developers always looking for opportunity

• Find a new customer‐price niche

• Government enables or disables

• Regulates• Incentivizes

© 2015 Affordable Housing Institute: all rights reserved

Private actors drive housing and housing finance Enlightened self‐interest: maximize results under rules

as they perceive them

Government runs in parallel at each link Authorize, regulate, enforce against ‘Steer, don’t row’

Change links, handoffs, subsidies Divert market

Government touches housing at all 16 links Supply side is heavily regulated

Title registration, zoning, environmental Building codes, occupancy limits, RESPA

Demand side is heavily regulated Usury laws, consumer protection, HMDA Foreclosure laws

Government influences every link in both chainsEnable, incentivize, enable, regulate, discourage, disable

27‐Dec‐15 13

Zoning board of appeals (ZBA)Amherst, Massachusetts

© 2015 Affordable Housing Institute: all rights reserved

Affordable housing always ‘costs money’ Does not exist in economic nature Inexorable laws of land‐use economics

Median rent/ price median income Housing standards always rising Below‐market people will never afford market housing

Affordability Subsidy (visible or invisible) Can be supply side (cost of homes) or demand side

(cost of money provided to consumer) “How much affordability can you afford?”

Money at scale comes from government Philanthropies, charities act at the margins

125 years of affordable housing pioneering

Government influences every link in both chainsEnable, incentivize, enable, regulate, discourage, disable

27‐Dec‐15 14

© 2015 Affordable Housing Institute: all rights reserved

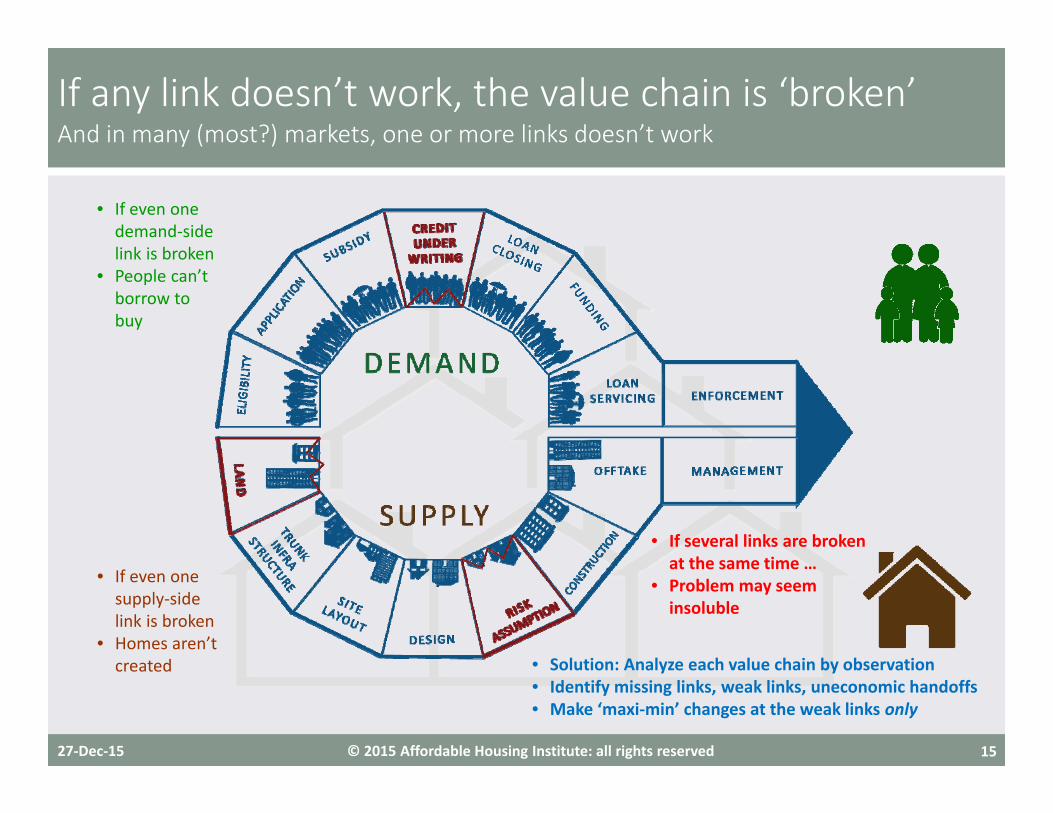

If any link doesn’t work, the value chain is ‘broken’And in many (most?) markets, one or more links doesn’t work

27‐Dec‐15 15

• If even one supply‐side link is broken

• Homes aren’t created

• If even one demand‐side link is broken

• People can’t borrow to buy

• If several links are broken at the same time …

• Problem may seem insoluble

• Solution: Analyze each value chain by observation• Identify missing links, weak links, uneconomic handoffs• Make ‘maxi‐min’ changes at the weak links only

© 2015 Affordable Housing Institute: all rights reserved

1. Collect facts Ask anyone anything; document it

2. Categorize facts by value‐chain link3. Organize links into a graphic display4. Analyze links that could be improved

Missing links, obstructions, blockages Land irresolution, entitlements, NIMBY

Weak link connections (process handoffs) Private‐private, private‐public, public‐public

Economic curbstones Costs > customer journey can afford

5. Identify ‘maxi‐min’ interventions System benefit / political cost = Maxi‐min solution

Need new solutions? Solve value‐chain problemsPart 1: Map the value chain, find its pain points

27‐Dec‐15 16

© 2015 Affordable Housing Institute: all rights reserved

1. Choose urgent unmet household type Strong political/ policy need Housing not delivered by current system

Chronic homeless, workforce, veterans

2. Envision the campus typology Residences Common areas/ amenities Services (provided by whom?)

3. Walk the future customer journeys Household type Effective demand Housing typology Viable build strategy

4. Identify and tap maxi‐min subsidy5. Convert to contract term sheets

Private‐public, public‐public

Need new solutions? Invent new ‘customer journeys’Part 2: Pick a needy customer type and a missing typology

27‐Dec‐15 17

Design review: housing co‐opMumbai, India

© 2015 Affordable Housing Institute: all rights reserved

1. Urban housing output of two value chains Demand side Housing loans Supply side Affordable homes

2. Private actors maximize their results Improving ecosystem is government’s job

3. Government influences each link Positively or negatively Smooth handoffs of dropped handoffs

4. Change starts with understanding Map the value chains as they work today Identify links/ handoffs to improve

5. Build new value chains Cross government silos/ funding streams

Points to remember

27‐Dec‐15 18

Government‐built housingMumbai, India

Home‐based seamstressDelhi, India

David A. [email protected] www.affordablehousinginstitute.org

38 Chauncy Street, Suite 600 Boston, MA 02111 +1 (617) 502‐5913Copyright © 2015 Affordable Housing Institute

Questions?

Questions?

David A. [email protected] www.affordablehousinginstitute.org

38 Chauncy Street, Suite 600 Boston, MA 02111 +1 (617) 502‐5913Copyright © 2015 Affordable Housing Institute

Housing’s value chains