Embed Size (px)

Citation preview

Houston, Like the Nation, is Returning to Growth

Tim Hopper

Senior Economist

Federal Reserve Bank of Dallas

June 15, 2004

External Forces that Drive Houston

• US Economy

• Global Economic Conditions

• Oil and Natural Gas Markets

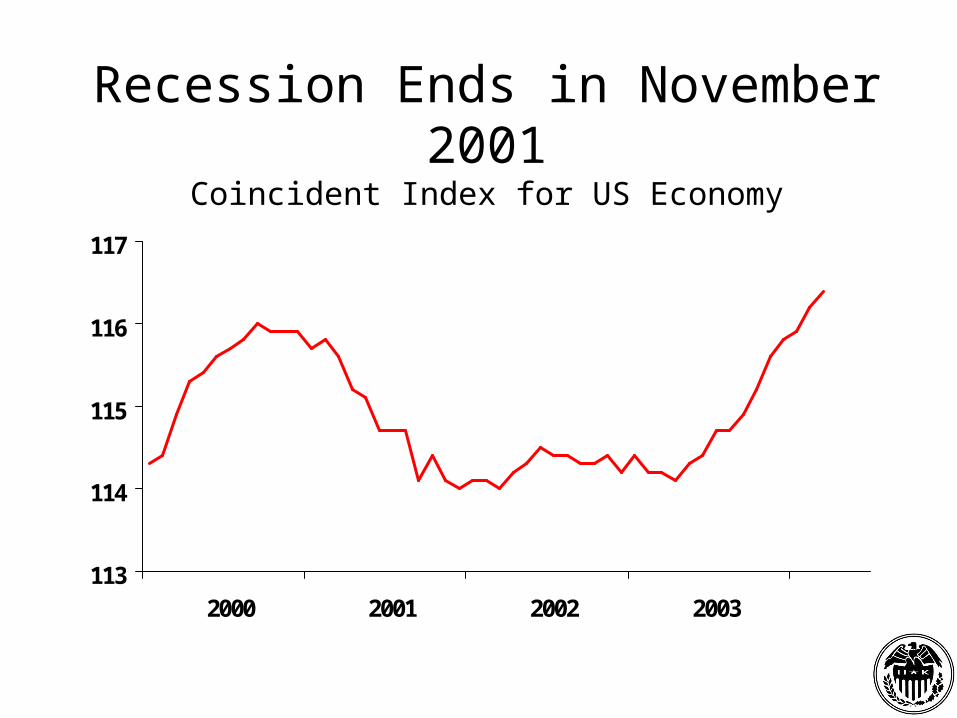

Recession Ends in November 2001Coincident Index for US Economy

113

114

115

116

117

2000 2001 2002 2003

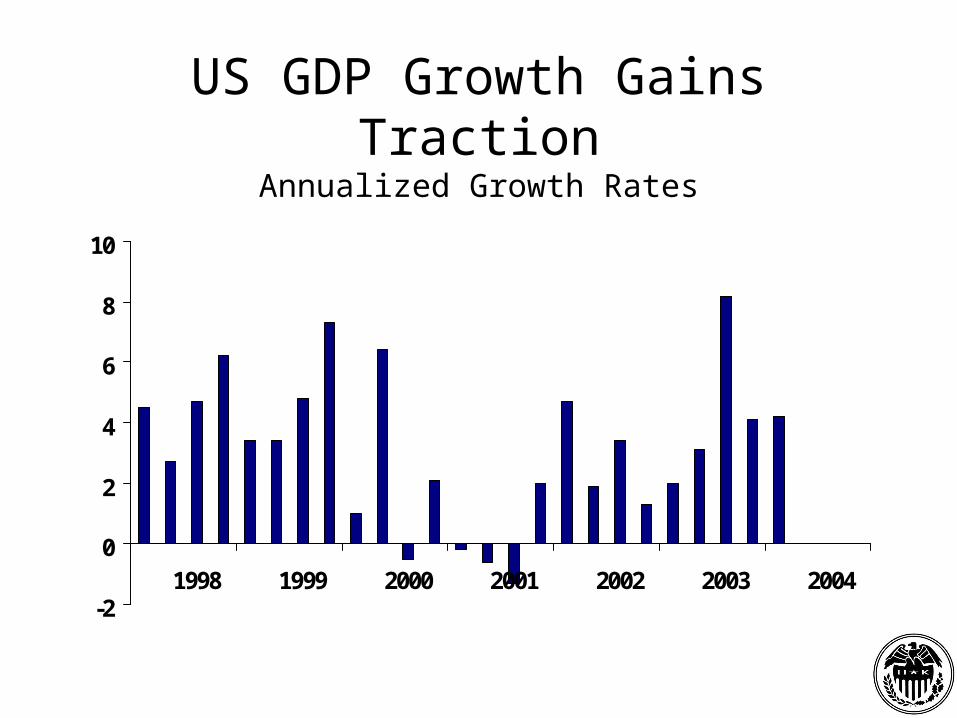

US GDP Growth Gains TractionAnnualized Growth Rates

-2

0

2

4

6

8

10

1998 1999 2000 2001 2002 2003 2004

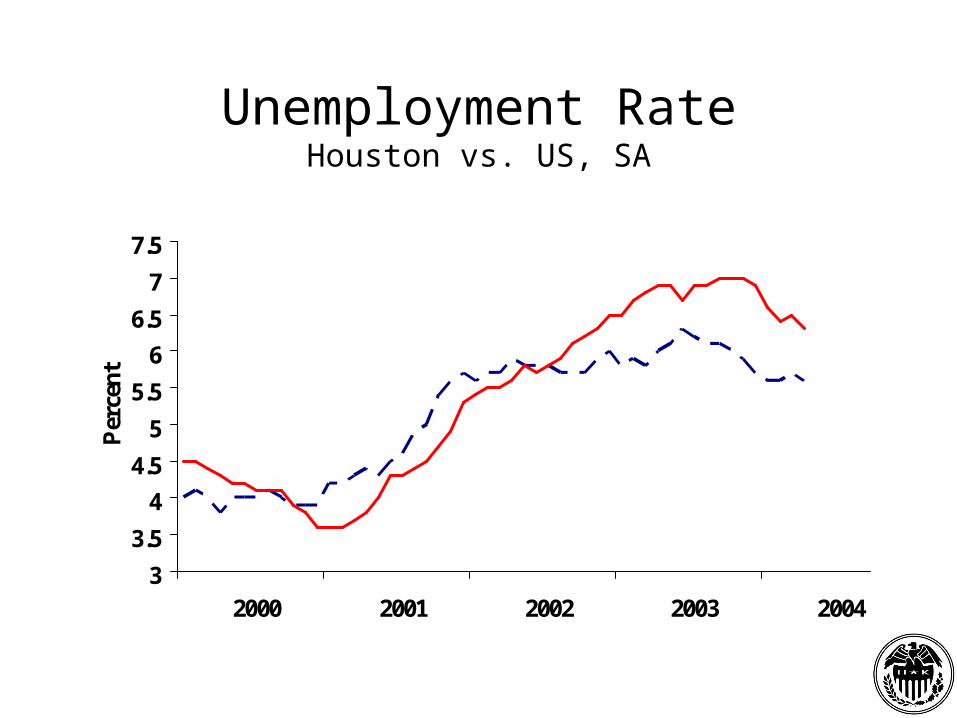

Unemployment RateHouston vs. US, SA

3

3.5

4

4.5

5

5.5

6

6.5

7

7.5

2000 2001 2002 2003 2004

Per

cent

US

Houston

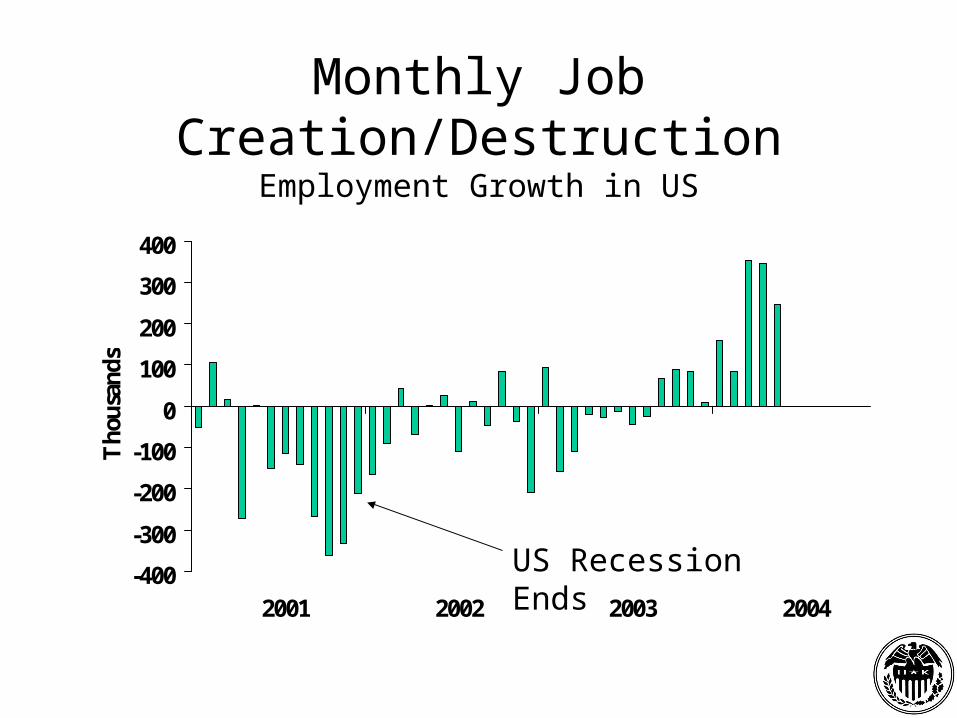

-400

-300

-200

-100

0

100

200

300

400

2001 2002 2003 2004

Tho

usan

dsMonthly Job Creation/Destruction

Employment Growth in US

US Recession Ends

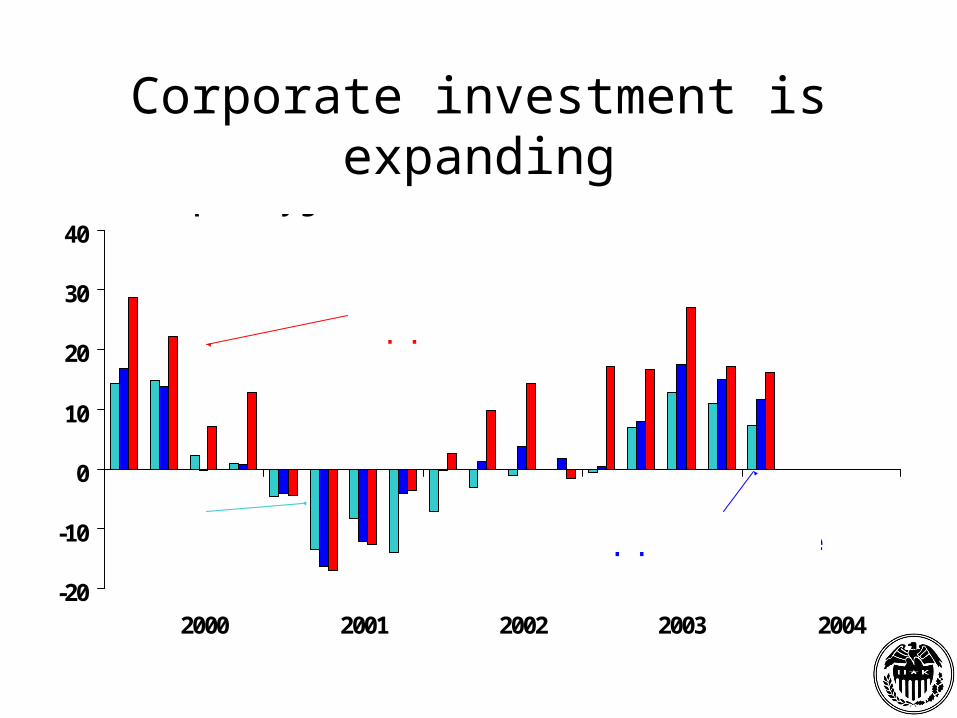

Corporate investment is expanding

-20

-10

0

10

20

30

40

2000 2001 2002 2003 2004

Annualized quarterly growth

Business fixed investment

Equipment & software

Information processingequipment & software

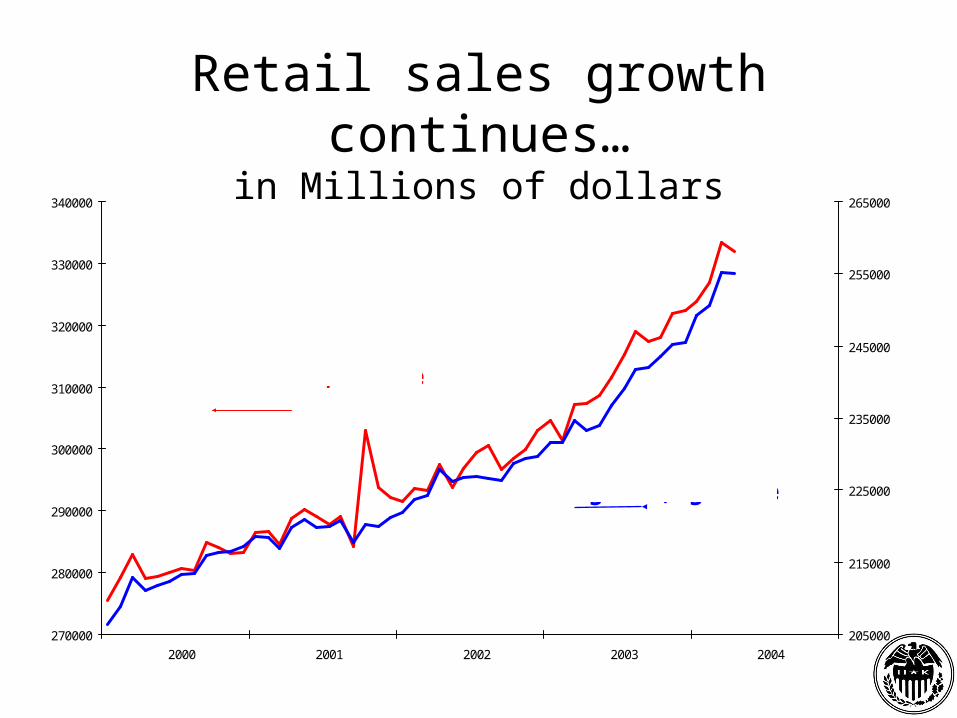

Retail sales growth continues…in Millions of dollars

270000

280000

290000

300000

310000

320000

330000

340000

2000 2001 2002 2003 2004

205000

215000

225000

235000

245000

255000

265000

Overall retail sales, left scale

Excluding autos, right scale

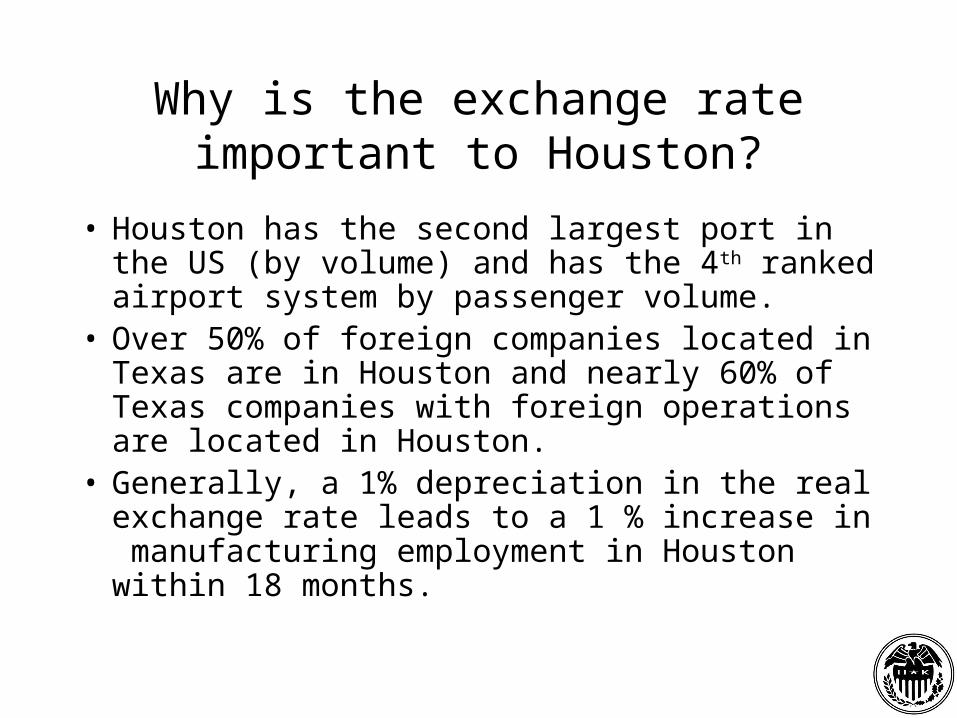

Why is the exchange rate important to Houston?

• Houston has the second largest port in the US (by volume) and has the 4th ranked airport system by passenger volume.

• Over 50% of foreign companies located in Texas are in Houston and nearly 60% of Texas companies with foreign operations are located in Houston.

• Generally, a 1% depreciation in the real exchange rate leads to a 1 % increase in manufacturing employment in Houston within 18 months.

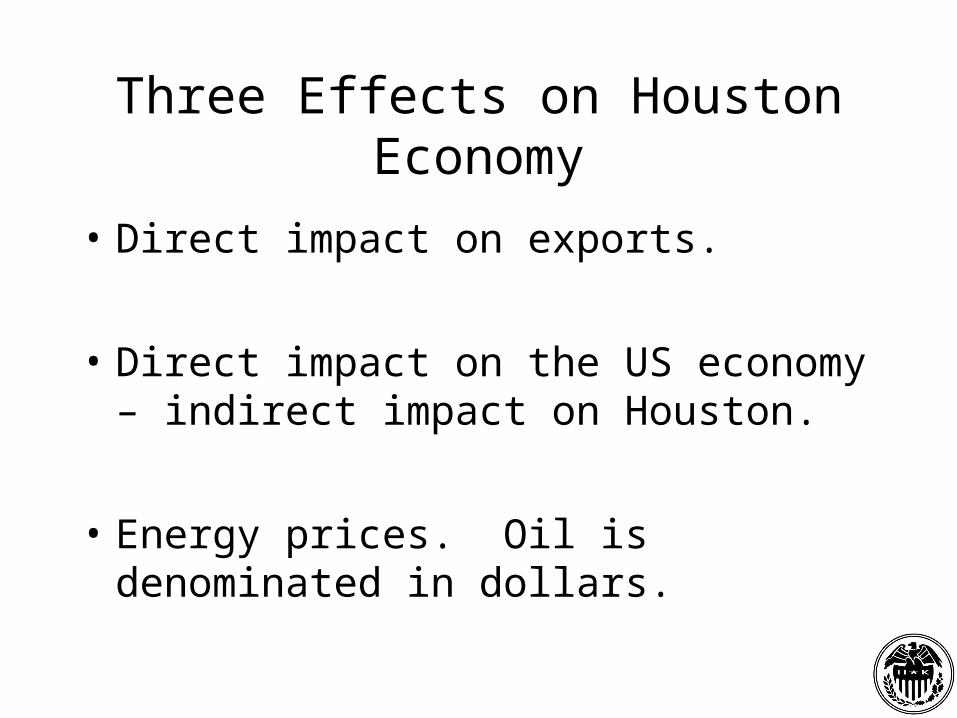

Three Effects on Houston Economy

• Direct impact on exports.

• Direct impact on the US economy – indirect impact on Houston.

• Energy prices. Oil is denominated in dollars.

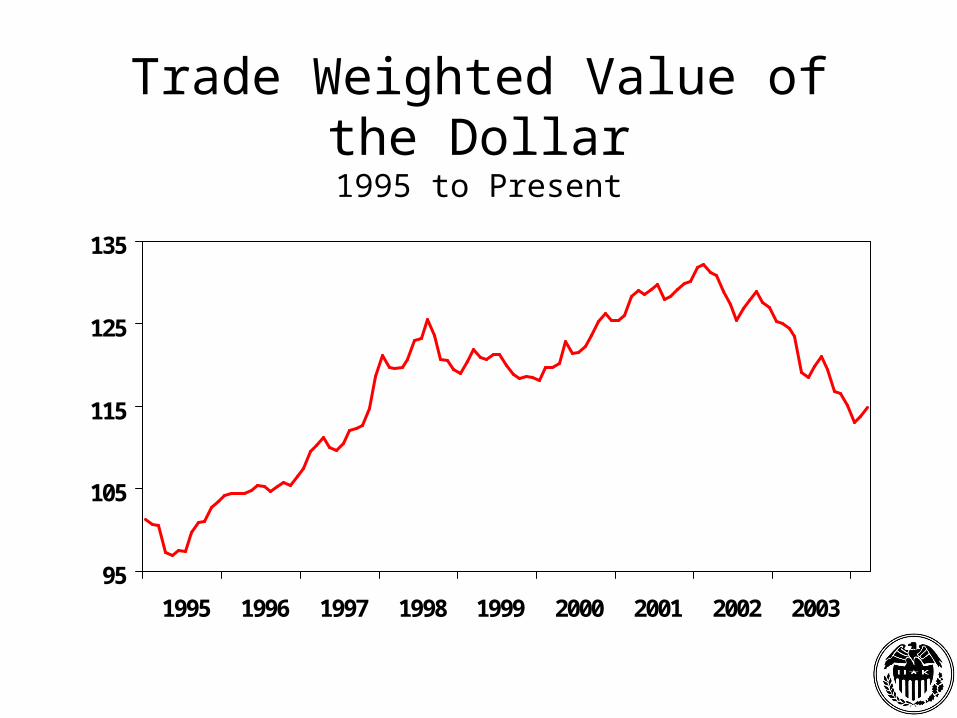

Trade Weighted Value of the Dollar1995 to Present

95

105

115

125

135

1995 1996 1997 1998 1999 2000 2001 2002 2003

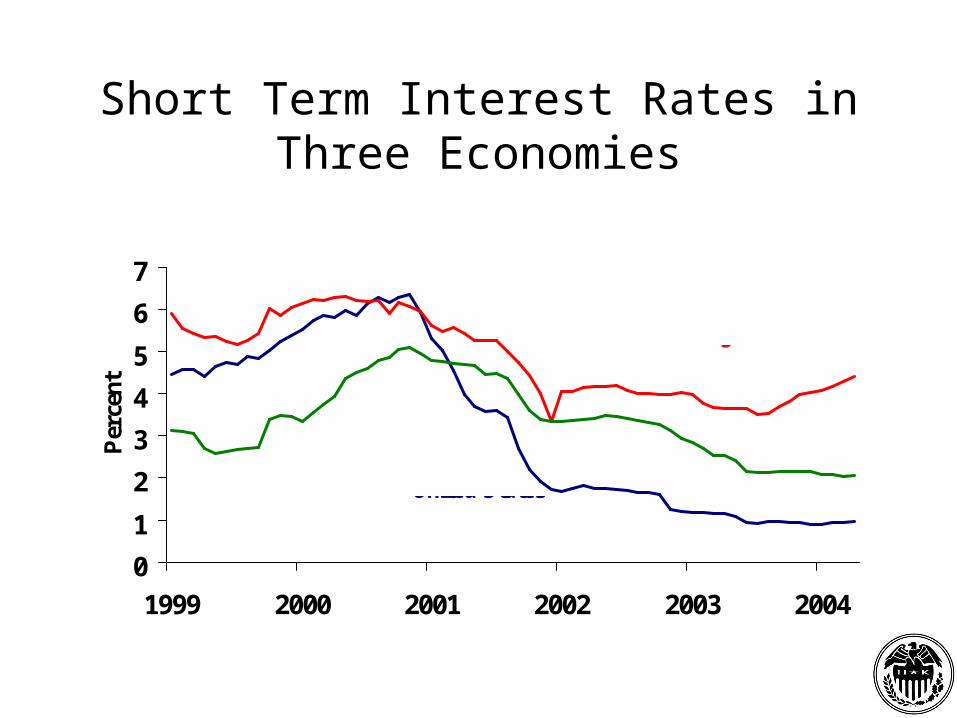

Short Term Interest Rates in Three Economies

0

1

2

3

4

5

6

7

1999 2000 2001 2002 2003 2004

Per

cent

United States

United Kingdom

EuroZone

Energy and Houston

• 50% to 60% of Houston’s economy is directly or indirectly linked to energy markets.

• Upstream Exploration.

• Downstream refining and petrochemical operations.

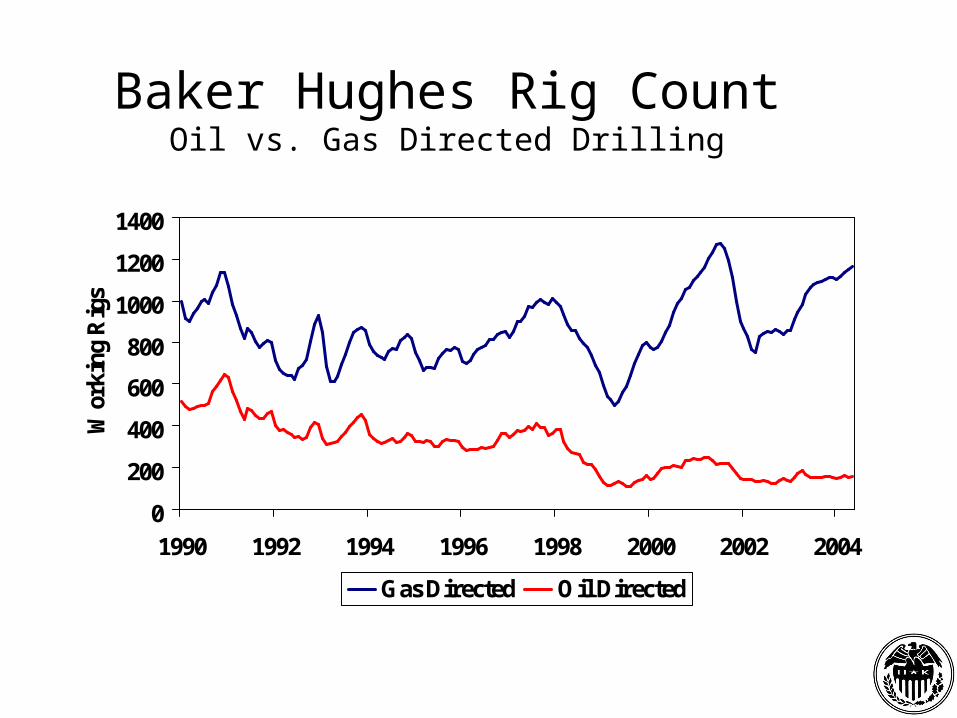

Baker Hughes Rig CountOil vs. Gas Directed Drilling

0

200

400

600

800

1000

1200

1400

1990 1992 1994 1996 1998 2000 2002 2004

Wor

king

Rig

s

Gas Directed Oil Directed

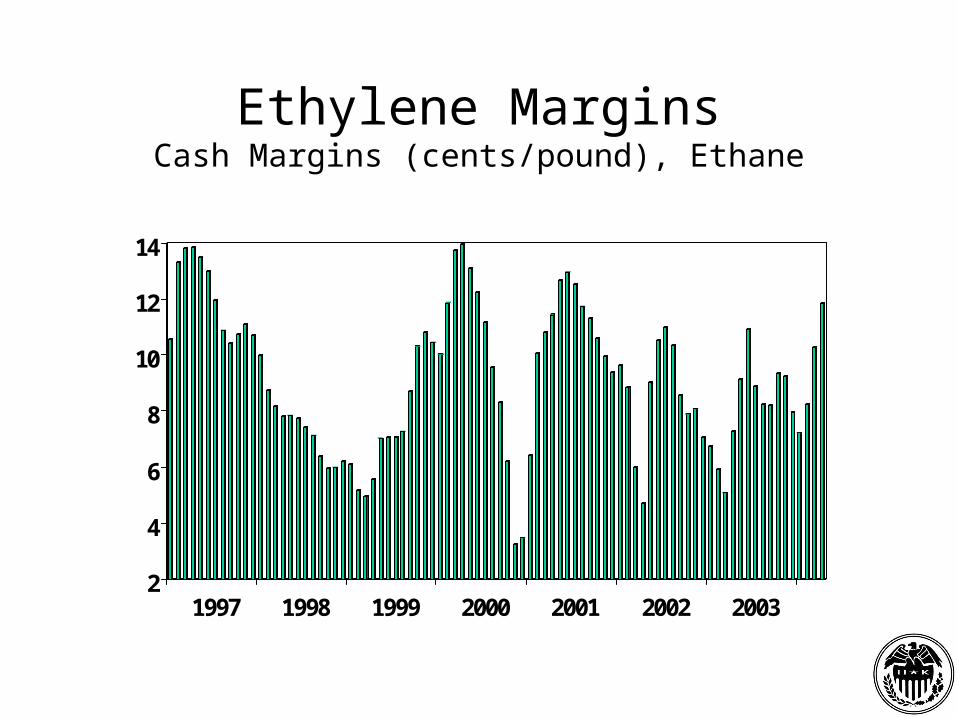

Ethylene MarginsCash Margins (cents/pound), Ethane

2

4

6

8

10

12

14

1997 1998 1999 2000 2001 2002 2003

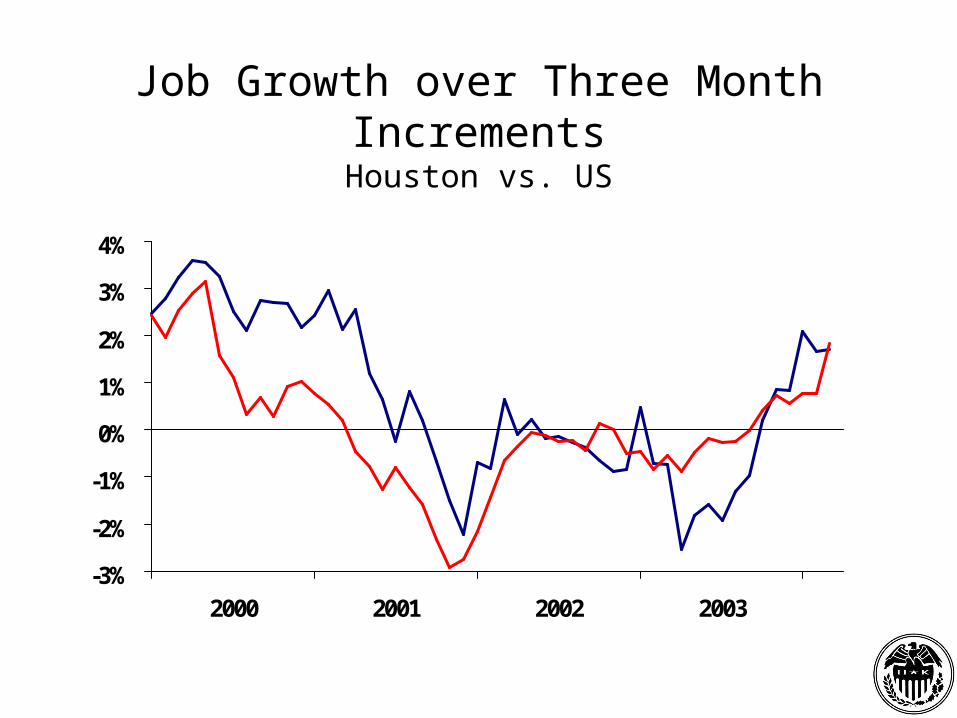

Job Growth over Three Month IncrementsHouston vs. US

-3%

-2%

-1%

0%

1%

2%

3%

4%

2000 2001 2002 2003

US

Houston

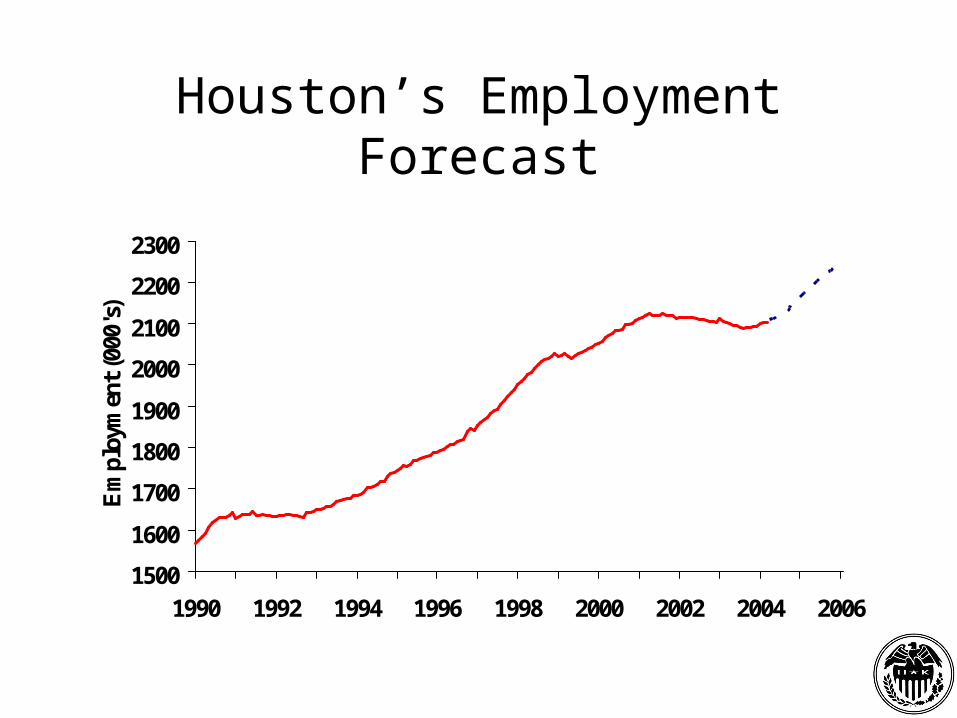

Houston’s Employment Forecast

1500

1600

1700

1800

1900

2000

2100

2200

2300

1990 1992 1994 1996 1998 2000 2002 2004 2006

Em

ploy

men

t (0

00's

)

Conclusion

• Things are finally moving in the right direction for Houston. This economy tends to lag the national economy. This period is no exception.

• A pick up in the national economy will help Houston and momentum will grow as the year progresses.

• The rig count is stable and employment is beginning to firm up with prices.

• 2004 should see 2.0 - 2.5% employment growth with 2005 possibly even stronger.

Houston, Like the Nation, is Returning to Growth

Tim Hopper

Senior Economist

Federal Reserve Bank of Dallas

June 15, 2004