Embed Size (px)

Citation preview

May 2016 ©2016, Greater Houston Partnership Page 1

A Different Sort Glut — Houston’s multifamily market continues to soften. Total occu-

pancy stood at 90.1 percent in April. Conventional wisdom holds that once occupancy

falls below 90 percent, Houston becomes a renter’s market. Given the incentives now

available to renters at many Class A properties, Houston is already there.

Overall occupancy will continue falling, likely to the mid-80s, as developers deliver an-

other 21,000 apartments this year and 4,000 next. Even in a booming economy, 25,000

units would be difficult to absorb. Recent history helps one to understand why.

From January ’10 through December ’14, the region created an average of 95,000 jobs per

year. During the same period, the market absorbed an average of 15,000 apartment units

per year. Those facts suggest a multifamily rule of thumb—for every six jobs Houston

creates, one apartment unit is absorbed. Apply that 6:1 ratio to the number of units coming

online in ’16, and the region needs an additional 150,000 jobs over the next two years to

hold occupancy at its current level. Given the weak job growth expected in the near term,

Houston’s apartment market will likely be oversupplied well into the future.

Challenges Ahead for Class A — Overbuilding is hitting the Class A apartment market

the hardest. “Stable” Class A, those properties in operation 13 months or more, enjoy a

90.8 percent occupancy rate. Class A in “lease-up,” however, those properties operating

less than 13 months, have a 23.2 percent occupancy rate. While it’s normal for lease-up

to fall well below the stable rate, the glut of units hitting the market has pulled overall

Class A occupancy down to 79.5 percent. In August ’14, the peak of the recent multifamily

cycle, the overall rate for Class A space was 84.0 percent.

To attract tenants, many

Class A properties in

“lease-up” now offer a

host of incentives—gift

cards, Apple watches, flat

screen televisions, seven-

day cruises, and move-in

allowances, in addition to

several months free rent.

To remain competitive,

Class A “stable” properties

may soon be forced to do

A publication of the Greater Houston Partnership Volume 25 Number 5 — May 2016

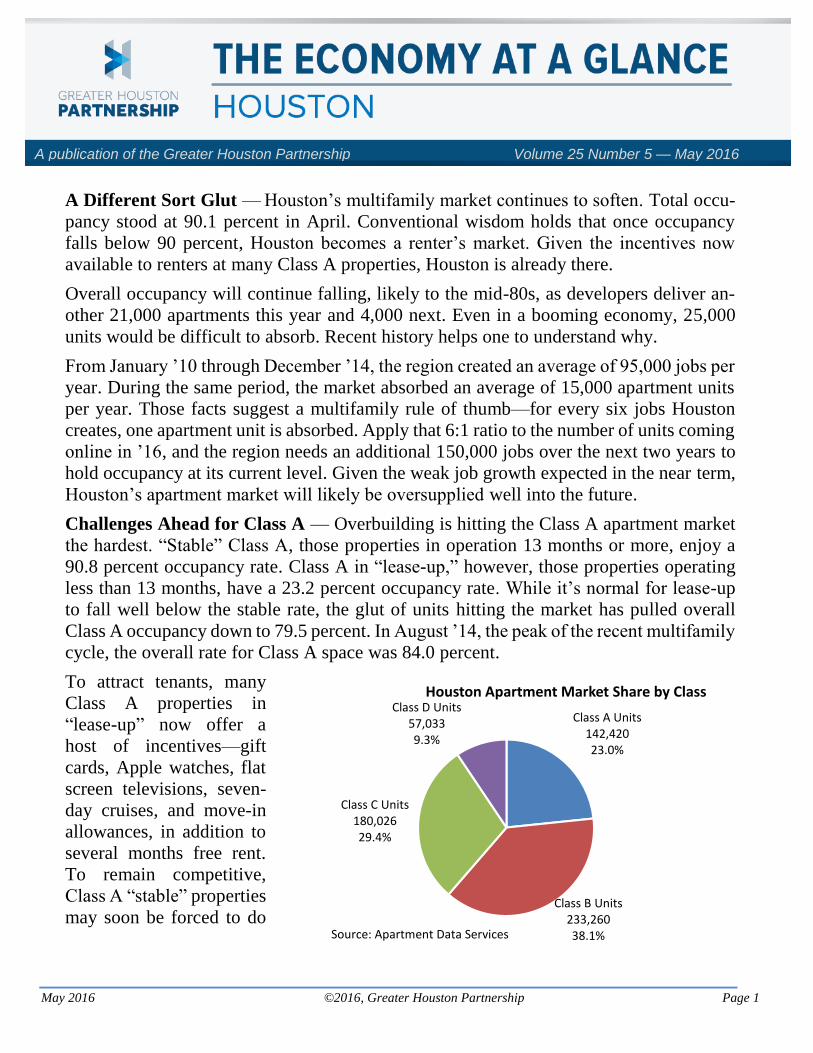

Class A Units142,42023.0%

Class B Units233,26038.1%

Class C Units180,02629.4%

Class D Units57,0339.3%

Houston Apartment Market Share by Class

Source: Apartment Data Services

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 2

the same. Evidence suggests this is already happening. On a square foot basis, overall

Class A rents have slipped 2.5 percent since June ’15.

Class B and C Faring Better — The

impact of Class A overbuilding has

been minimal on Class B and C proper-

ties. Occupancy rates have ticked

down, but their rents have grown over

the past two years. Houston is unlikely

to see a wave of Class B and C proper-

ties hit the market. With a few excep-

tions, developers don’t build Class B

units. Of the 24,000-plus units cur-

rently in “lease-up,” only 500 are Class B. Sub-A inventory tends to expand as properties

age, floor plans become dated, and structures deteriorate. Only if owners neglect their

investments during the downturn will we see a large number of Class A units slide into

the Class B market.

Nor is Houston likely to see a wave of renters upgrade from Class B to Class A, leaving a

glut of empty units in their wake. Class A rents averaged $1,459 per month in April. With

two months free rent, a fairly standard incentive these days, that works out to $14,590 per

year to live in a Class A apartment. Class B rents averaged $948 per month in April.

Without free rent, that works out to

$11,376 per year to live in a Class B

apartment. That $3,214 gap may be

too wide for many Class B households

to bridge. There’s also the question of

whether Class B renters would have

the FICO scores and income histories

to qualify for the higher-priced leases.

All these considerations put the Class

B and C submarkets in much better

position to weather the downturn. Re-

cent history suggests that’s the case.

Once-hot markets such as The

Heights, Montrose, and the Galleria

have seen effective rents decline over

the past six months. Meanwhile, less

trendy submarkets heavily weighted

with Class B and C properties–Alief,

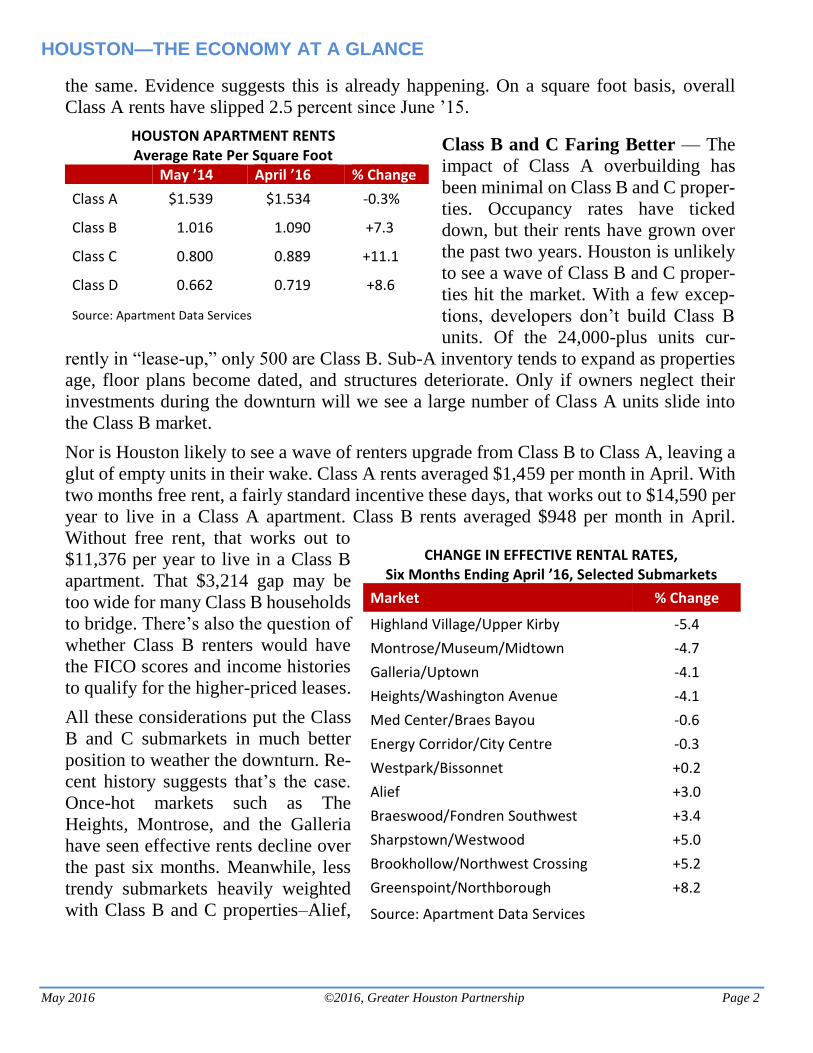

HOUSTON APARTMENT RENTS Average Rate Per Square Foot

May ’14 April ’16 % Change

Class A $1.539 $1.534 -0.3%

Class B 1.016 1.090 +7.3

Class C 0.800 0.889 +11.1

Class D 0.662 0.719 +8.6

Source: Apartment Data Services

CHANGE IN EFFECTIVE RENTAL RATES, Six Months Ending April ’16, Selected Submarkets

Market % Change

Highland Village/Upper Kirby -5.4

Montrose/Museum/Midtown -4.7

Galleria/Uptown -4.1

Heights/Washington Avenue -4.1

Med Center/Braes Bayou -0.6

Energy Corridor/City Centre -0.3

Westpark/Bissonnet +0.2

Alief +3.0

Braeswood/Fondren Southwest +3.4

Sharpstown/Westwood +5.0

Brookhollow/Northwest Crossing +5.2

Greenspoint/Northborough +8.2

Source: Apartment Data Services

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 3

Sharpstown and Westwood, for example–have seen their rental rates grow over the same

period. The investment community has taken note of this trend, too. Of the 34 apartment

transactions Transwestern tracked in its Q1 market report, 26 involved properties 25 years

old and older, ages typical of Class B and C properties.

Signs of Hope — Deliveries should taper off to 4,000 units next year, notes CBRE, and

only 1,400 units were permitted in Q1. The concern remains, however, that developers

will believe their project is unique, convince lenders of the same, and break ground on

more high-rises inside the loop and garden-style apartments in the suburbs. The stark truth

is that Houston doesn’t need any more Class A apartment communities, not until the mar-

ket absorbs the 45,000 vacant Class A units on the ground and in the pipeline. Apartment

owners and developers are more likely to see crude oil hit $70 a barrel before Houston

returns to a landlord’s market.

Industrial’s Status Quo — Houston absorbed between 1.4 and 2.1 million square feet of

industrial space in the first quarter, up from the 0.3 to 1.4 million square feet absorbed in

the fourth quarter of ’15.1 Retail distributors and third-party logistics firms—sectors tied

to population growth and port activity—drove demand for industrial space. Only four of

Houston’s 14 submarkets reported negative absorption, and with one exception, the

amount of space thrown back on the market represents less than 0.1 percent of their re-

spective inventories.

Sublease space has begun to creep into the industrial market, but not to the same extent it

has in office. Sublease inventory totaled 3.5 million square feet at the end of Q1, well

above the five-year average of 2.4 million square feet, according to CBRE. Industrial’s

direct vacancy rate is 4.9 to 5.6 per-

cent. Factor in sublease space and

the rate inches up to 5.6 to 5.8 per-

cent.

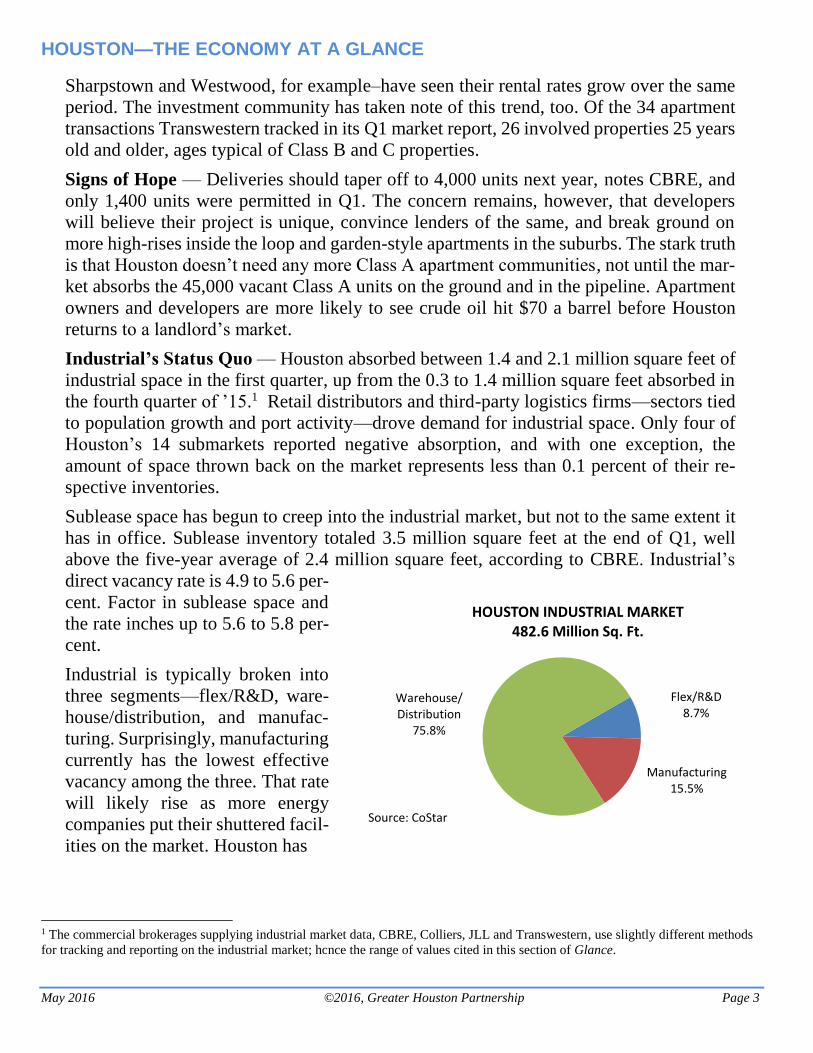

Industrial is typically broken into

three segments—flex/R&D, ware-

house/distribution, and manufac-

turing. Surprisingly, manufacturing

currently has the lowest effective

vacancy among the three. That rate

will likely rise as more energy

companies put their shuttered facil-

ities on the market. Houston has

1 The commercial brokerages supplying industrial market data, CBRE, Colliers, JLL and Transwestern, use slightly different methods

for tracking and reporting on the industrial market; hcnce the range of values cited in this section of Glance.

Flex/R&D 8.7%

Manufacturing 15.5%

Warehouse/Distribution

75.8%

HOUSTON INDUSTRIAL MARKET482.6 Million Sq. Ft.

Source: CoStar

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 4

lost nearly 30,000 manufacturing

jobs–one in nine–in the downturn,

and equipment suppliers simply

don’t need as much space.

The increase in manufacturing

sublease space won’t impact the

industrial market to the same ex-

tent it has affected office. Manu-

facturing represents a small share

of the industrial market. An addi-

tional six to 10 million square feet of empty space would have to hit the market to raise

the industrial vacancy rate by two percentage points.

At the end of Q1, 11.6 million square feet of industrial space was under construction,

according to CBRE, up from 9.5 million at year’s end. Colliers notes the space under

construction equals less than two percent of total existing space, and since 78 percent is

preleased, it should have a negligible impact on vacancy rates.

Low oil prices and weak job growth will continue to reduce demand for industrial space.

Net absorption will likely remain positive, rates will remain flat, and landlords will offer

concessions to lure tenants into their spaces. Fewer investors will be interested in Hou-

ston’s manufacturing space, but deals for flex/R&D and warehouse/distribution space

should continue. Though the industrial market faces challenges, it should perform much

better than office and multifamily over the next 12 to 24 months.

Sales Tax Update — The plunge in the rig count and oil prices has caught up to city sales

tax collections. The City of Houston collected $212.1 million in sales taxes through the

first four months of the year, a 5.2 percent decrease from the $223.7 million collected the

same period in ’15. The decline is attributed to a fall in business purchases.

Taxable sales fall in either of two categories: consumer sectors that typically pay general

sales taxes and business sectors that usually generate use taxes.2 According to analysis

conducted by the University of Houston’s Institute for Regional Forecasting, consumer

sales in the city of Houston recorded a small increase of 1.4 percent from Q1/14 to Q3/15,

but business sales fell 15.9 percent. As rig counts continue to decline, sales of machinery

and fabricated metals suffer, and the effects trickle down to a lower amount of use taxes

collected by the city.

2 Consumer sectors include retail, accommodation, food service, arts, and entertainment. Business sectors include mining, utilities,

manufacturing, wholesale trade, and all other. The most recent data that show the split between consumer and business sales for the

city of Houston is through Q3/15.

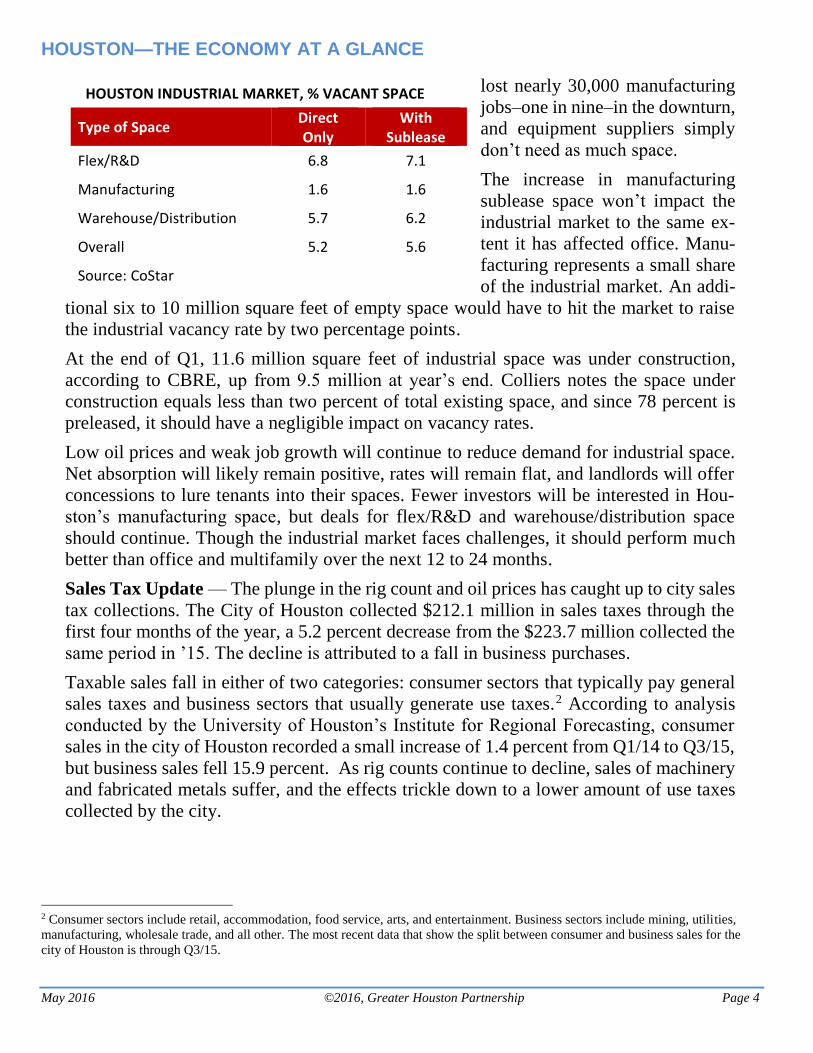

HOUSTON INDUSTRIAL MARKET, % VACANT SPACE

Type of Space Direct Only

With Sublease

Flex/R&D 6.8 7.1

Manufacturing 1.6 1.6

Warehouse/Distribution 5.7 6.2

Overall 5.2 5.6

Source: CoStar

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 5

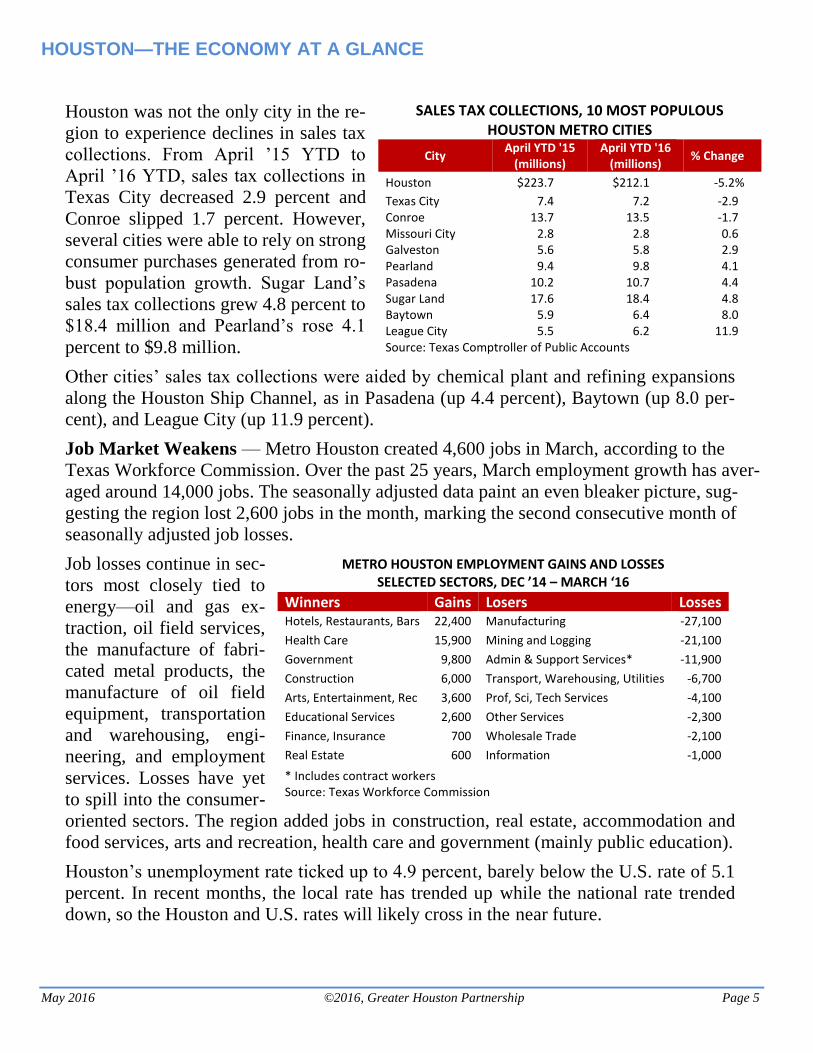

Houston was not the only city in the re-

gion to experience declines in sales tax

collections. From April ’15 YTD to

April ’16 YTD, sales tax collections in

Texas City decreased 2.9 percent and

Conroe slipped 1.7 percent. However,

several cities were able to rely on strong

consumer purchases generated from ro-

bust population growth. Sugar Land’s

sales tax collections grew 4.8 percent to

$18.4 million and Pearland’s rose 4.1

percent to $9.8 million.

Other cities’ sales tax collections were aided by chemical plant and refining expansions

along the Houston Ship Channel, as in Pasadena (up 4.4 percent), Baytown (up 8.0 per-

cent), and League City (up 11.9 percent).

Job Market Weakens — Metro Houston created 4,600 jobs in March, according to the

Texas Workforce Commission. Over the past 25 years, March employment growth has aver-

aged around 14,000 jobs. The seasonally adjusted data paint an even bleaker picture, sug-

gesting the region lost 2,600 jobs in the month, marking the second consecutive month of

seasonally adjusted job losses.

Job losses continue in sec-

tors most closely tied to

energy—oil and gas ex-

traction, oil field services,

the manufacture of fabri-

cated metal products, the

manufacture of oil field

equipment, transportation

and warehousing, engi-

neering, and employment

services. Losses have yet

to spill into the consumer-

oriented sectors. The region added jobs in construction, real estate, accommodation and

food services, arts and recreation, health care and government (mainly public education).

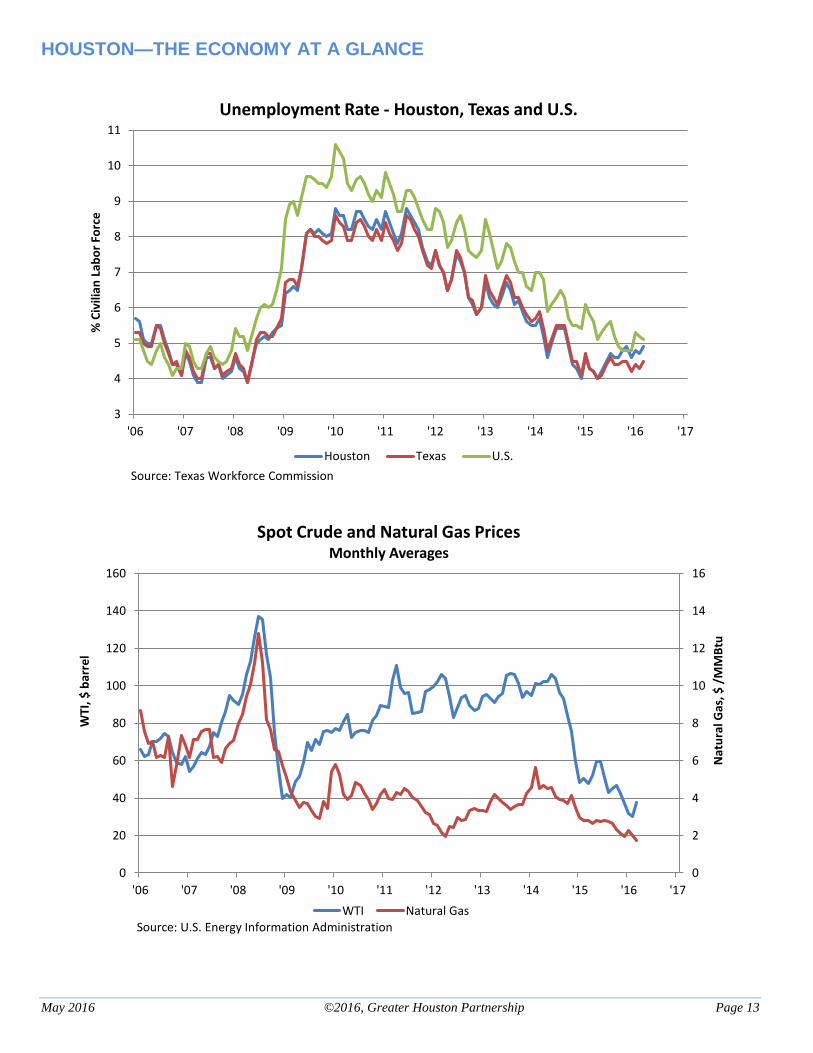

Houston’s unemployment rate ticked up to 4.9 percent, barely below the U.S. rate of 5.1

percent. In recent months, the local rate has trended up while the national rate trended

down, so the Houston and U.S. rates will likely cross in the near future.

SALES TAX COLLECTIONS, 10 MOST POPULOUS HOUSTON METRO CITIES

City April YTD '15

(millions) April YTD '16

(millions) % Change

Houston $223.7 $212.1 -5.2%

Texas City 7.4 7.2 -2.9 Conroe 13.7 13.5 -1.7 Missouri City 2.8 2.8 0.6 Galveston 5.6 5.8 2.9 Pearland 9.4 9.8 4.1 Pasadena 10.2 10.7 4.4 Sugar Land 17.6 18.4 4.8 Baytown 5.9 6.4 8.0 League City 5.5 6.2 11.9 Source: Texas Comptroller of Public Accounts

METRO HOUSTON EMPLOYMENT GAINS AND LOSSES SELECTED SECTORS, DEC ’14 – MARCH ‘16

Winners Gains Losers Losses Hotels, Restaurants, Bars 22,400 Manufacturing -27,100

Health Care 15,900 Mining and Logging -21,100

Government 9,800 Admin & Support Services* -11,900

Construction 6,000 Transport, Warehousing, Utilities -6,700

Arts, Entertainment, Rec 3,600 Prof, Sci, Tech Services -4,100

Educational Services 2,600 Other Services -2,300

Finance, Insurance 700 Wholesale Trade -2,100

Real Estate 600 Information -1,000

* Includes contract workers Source: Texas Workforce Commission

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 6

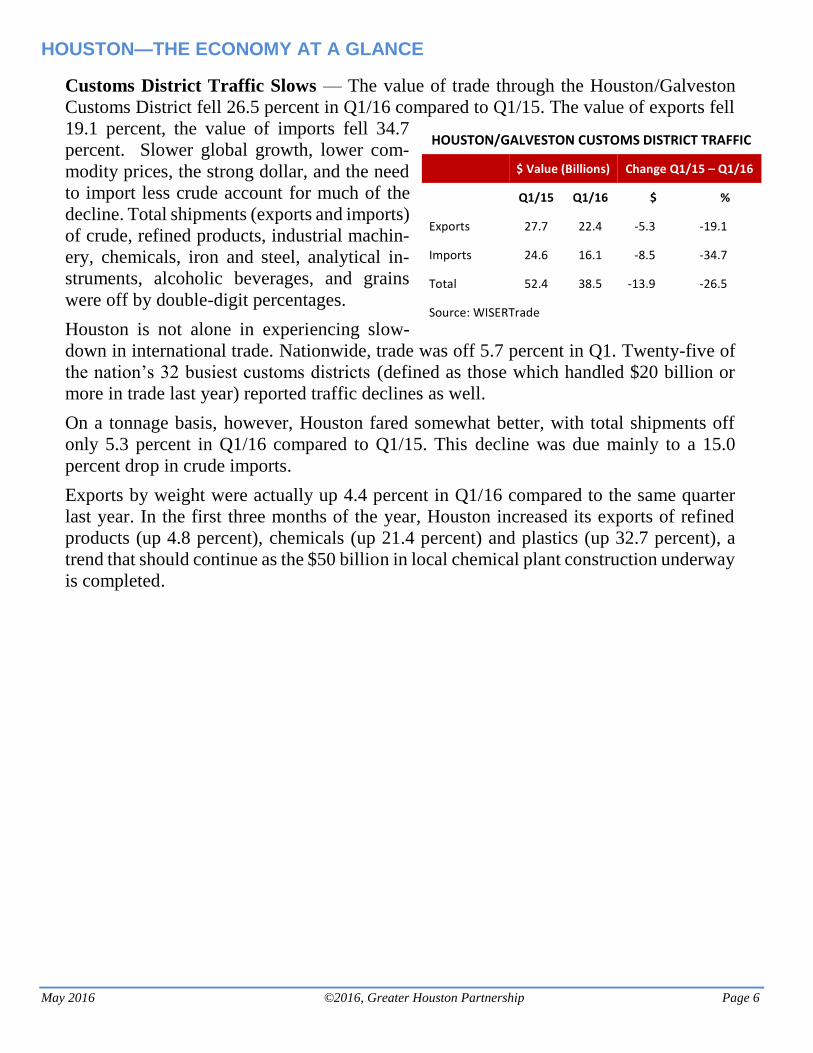

Customs District Traffic Slows — The value of trade through the Houston/Galveston

Customs District fell 26.5 percent in Q1/16 compared to Q1/15. The value of exports fell

19.1 percent, the value of imports fell 34.7

percent. Slower global growth, lower com-

modity prices, the strong dollar, and the need

to import less crude account for much of the

decline. Total shipments (exports and imports)

of crude, refined products, industrial machin-

ery, chemicals, iron and steel, analytical in-

struments, alcoholic beverages, and grains

were off by double-digit percentages.

Houston is not alone in experiencing slow-

down in international trade. Nationwide, trade was off 5.7 percent in Q1. Twenty-five of

the nation’s 32 busiest customs districts (defined as those which handled $20 billion or

more in trade last year) reported traffic declines as well.

On a tonnage basis, however, Houston fared somewhat better, with total shipments off

only 5.3 percent in Q1/16 compared to Q1/15. This decline was due mainly to a 15.0

percent drop in crude imports.

Exports by weight were actually up 4.4 percent in Q1/16 compared to the same quarter

last year. In the first three months of the year, Houston increased its exports of refined

products (up 4.8 percent), chemicals (up 21.4 percent) and plastics (up 32.7 percent), a

trend that should continue as the $50 billion in local chemical plant construction underway

is completed.

HOUSTON/GALVESTON CUSTOMS DISTRICT TRAFFIC

$ Value (Billions) Change Q1/15 – Q1/16

Q1/15 Q1/16 $ %

Exports 27.7 22.4 -5.3 -19.1

Imports 24.6 16.1 -8.5 -34.7

Total 52.4 38.5 -13.9 -26.5

Source: WISERTrade

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 7

SNAPSHOT — HOUSTON’S KEY ECONOMIC INDICATORS

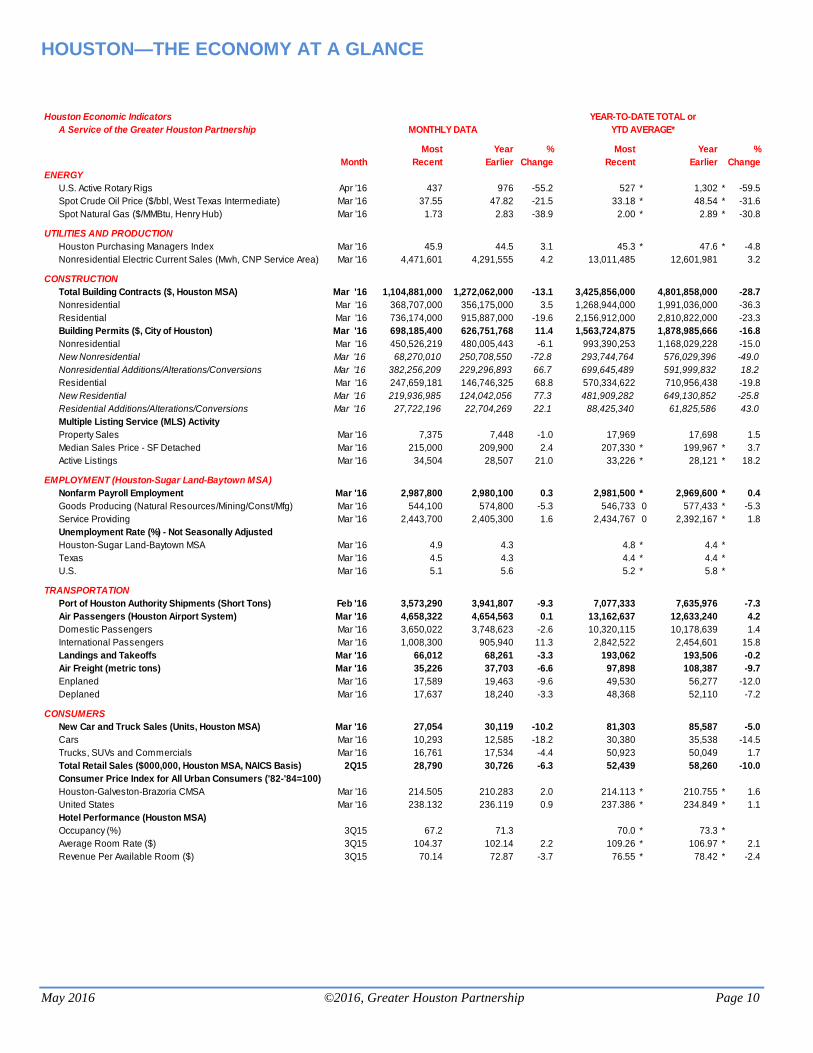

Building Permits — City of Houston building permits totaled $698.2 million in March

’16, up 11.4 percent from $626.8 million in March ’15, according to the City’s Department

of Public Works & Engineering Planning & Development Services. Year-to-date, city

building permits total $1.6 billion, down 16.8 percent from $1.9 billion over the same pe-

riod in ’15.

Inflation — The cost of consumer goods and services as measured by the Consumer Price

Index for All Urban Consumers (CPI-U) rose 0.9 percent nationwide from March ’15 to

March ’16, the smallest annual increase in prices since December ’15, according to the

U.S. Bureau of Labor Statistics. Core inflation (all items less the volatile food and energy

categories) increased 2.2 percent since March ’15. The 12-month change in core inflation

has hovered between 2.0 percent and 2.3 percent since November ’15.

Home Sales — Local realtors sold 7,375 homes in March, a 1.0 percent drop from the

7,448 sold in March of last year. Year-to-date home sales total 17,969, a 1.5 percent in-

crease from the 17,698 sold over the same period last year. The average sales price for

homes sold for in March was $272,658, down 1.6 percent from the average of $277,064 in

the same month last year. Single-family inventory is now 3.6 months, up from 2.8 months

in March the year before.

Purchasing Managers Index — The Houston Purchasing Managers Index (PMI), a short-

term leading indicator for regional production, registered 45.9 in March, up from 44.5 in

February, according to the Institute for Supply Management-Houston (ISM-Houston).

With the March reading, the PMI has signaled economic contraction in Houston for 15

consecutive months.

Vehicle Sales — Houston-area auto dealers sold 27,054 vehicles in March ’16, a 10.2 per-

cent decrease from the 30,119 sold in March last year, according to TexAuto Facts, pub-

lished by InfoNation, Inc. of Sugar Land. Through the first three months of ’16, local deal-

ers sold 81,303 vehicles, down 5.0 percent from the 85,587 sold over the comparable period

in ’15. For the 12 months ending March ’16, Houston sold 372,197 vehicles, a 1.0 percent

increase from the 363,876 sold in the 12 months ending March ’15.

Patrick Jankowski and Jenny Philip

contributed to this issue of Houston: The Economy at a Glance

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 8

STAY UP TO DATE!

To access past issues of Economy at a Glance, please click here.

If you are a not a member of the Greater Houston Partnership and would like to subscribe to

Economy at a Glance, please click here and enter your email address. For information about

joining the Greater Houston Partnership, call Member Services at 713-844-3683.

The Key Economic Indicators table is updated whenever any data change — typically, 11 or so

times per month. If you would like to receive these updates by e-mail, usually accompanied by

commentary, please email your request for Key Economic Indicators to [email protected] with

your name, title and phone number and your company’s name and address.

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 9

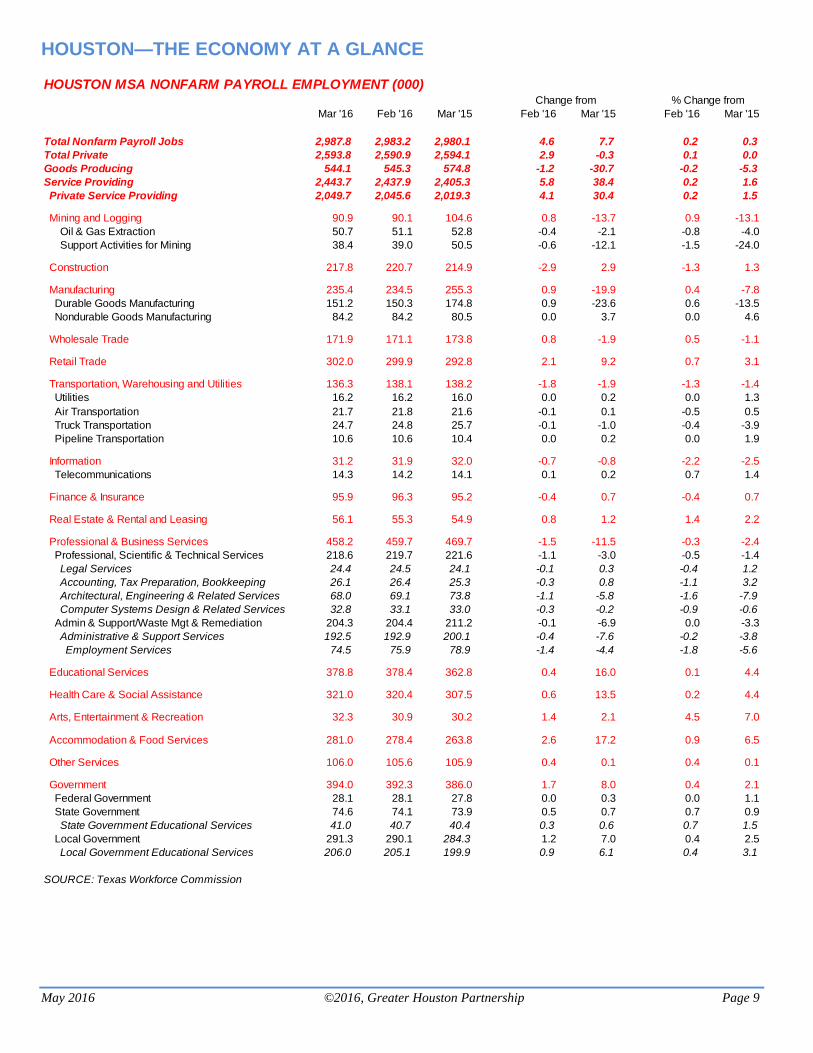

HOUSTON MSA NONFARM PAYROLL EMPLOYMENT (000) Change from % Change from

Mar '16 Feb '16 Mar '15 Feb '16 Mar '15 Feb '16 Mar '15

Total Nonfarm Payroll Jobs 2,987.8 2,983.2 2,980.1 4.6 7.7 0.2 0.3

Total Private 2,593.8 2,590.9 2,594.1 2.9 -0.3 0.1 0.0

Goods Producing 544.1 545.3 574.8 -1.2 -30.7 -0.2 -5.3

Service Providing 2,443.7 2,437.9 2,405.3 5.8 38.4 0.2 1.6

Private Service Providing 2,049.7 2,045.6 2,019.3 4.1 30.4 0.2 1.5

Mining and Logging 90.9 90.1 104.6 0.8 -13.7 0.9 -13.1

Oil & Gas Extraction 50.7 51.1 52.8 -0.4 -2.1 -0.8 -4.0

Support Activities for Mining 38.4 39.0 50.5 -0.6 -12.1 -1.5 -24.0

Construction 217.8 220.7 214.9 -2.9 2.9 -1.3 1.3

Manufacturing 235.4 234.5 255.3 0.9 -19.9 0.4 -7.8

Durable Goods Manufacturing 151.2 150.3 174.8 0.9 -23.6 0.6 -13.5

Nondurable Goods Manufacturing 84.2 84.2 80.5 0.0 3.7 0.0 4.6

Wholesale Trade 171.9 171.1 173.8 0.8 -1.9 0.5 -1.1

Retail Trade 302.0 299.9 292.8 2.1 9.2 0.7 3.1

Transportation, Warehousing and Utilities 136.3 138.1 138.2 -1.8 -1.9 -1.3 -1.4

Utilities 16.2 16.2 16.0 0.0 0.2 0.0 1.3

Air Transportation 21.7 21.8 21.6 -0.1 0.1 -0.5 0.5

Truck Transportation 24.7 24.8 25.7 -0.1 -1.0 -0.4 -3.9

Pipeline Transportation 10.6 10.6 10.4 0.0 0.2 0.0 1.9

Information 31.2 31.9 32.0 -0.7 -0.8 -2.2 -2.5

Telecommunications 14.3 14.2 14.1 0.1 0.2 0.7 1.4

Finance & Insurance 95.9 96.3 95.2 -0.4 0.7 -0.4 0.7

Real Estate & Rental and Leasing 56.1 55.3 54.9 0.8 1.2 1.4 2.2

Professional & Business Services 458.2 459.7 469.7 -1.5 -11.5 -0.3 -2.4

Professional, Scientific & Technical Services 218.6 219.7 221.6 -1.1 -3.0 -0.5 -1.4

Legal Services 24.4 24.5 24.1 -0.1 0.3 -0.4 1.2

Accounting, Tax Preparation, Bookkeeping 26.1 26.4 25.3 -0.3 0.8 -1.1 3.2

Architectural, Engineering & Related Services 68.0 69.1 73.8 -1.1 -5.8 -1.6 -7.9

Computer Systems Design & Related Services 32.8 33.1 33.0 -0.3 -0.2 -0.9 -0.6

Admin & Support/Waste Mgt & Remediation 204.3 204.4 211.2 -0.1 -6.9 0.0 -3.3

Administrative & Support Services 192.5 192.9 200.1 -0.4 -7.6 -0.2 -3.8

Employment Services 74.5 75.9 78.9 -1.4 -4.4 -1.8 -5.6

Educational Services 378.8 378.4 362.8 0.4 16.0 0.1 4.4

Health Care & Social Assistance 321.0 320.4 307.5 0.6 13.5 0.2 4.4

Arts, Entertainment & Recreation 32.3 30.9 30.2 1.4 2.1 4.5 7.0

Accommodation & Food Services 281.0 278.4 263.8 2.6 17.2 0.9 6.5

Other Services 106.0 105.6 105.9 0.4 0.1 0.4 0.1

Government 394.0 392.3 386.0 1.7 8.0 0.4 2.1

Federal Government 28.1 28.1 27.8 0.0 0.3 0.0 1.1

State Government 74.6 74.1 73.9 0.5 0.7 0.7 0.9

State Government Educational Services 41.0 40.7 40.4 0.3 0.6 0.7 1.5

Local Government 291.3 290.1 284.3 1.2 7.0 0.4 2.5

Local Government Educational Services 206.0 205.1 199.9 0.9 6.1 0.4 3.1

SOURCE: Texas Workforce Commission

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 10

Houston Economic Indicators

A Service of the Greater Houston Partnership

Most Year % Most Year %

Month Recent Earlier Change Recent Earlier Change

ENERGY

U.S. Active Rotary Rigs Apr '16 437 976 -55.2 527 * 1,302 * -59.5

Spot Crude Oil Price ($/bbl, West Texas Intermediate) Mar '16 37.55 47.82 -21.5 33.18 * 48.54 * -31.6

Spot Natural Gas ($/MMBtu, Henry Hub) Mar '16 1.73 2.83 -38.9 2.00 * 2.89 * -30.8

UTILITIES AND PRODUCTION

Houston Purchasing Managers Index Mar '16 45.9 44.5 3.1 45.3 * 47.6 * -4.8

Nonresidential Electric Current Sales (Mwh, CNP Service Area) Mar '16 4,471,601 4,291,555 4.2 13,011,485 12,601,981 3.2

CONSTRUCTION

Total Building Contracts ($, Houston MSA) Mar '16 1,104,881,000 1,272,062,000 -13.1 3,425,856,000 4,801,858,000 -28.7

Nonresidential Mar '16 368,707,000 356,175,000 3.5 1,268,944,000 1,991,036,000 -36.3

Residential Mar '16 736,174,000 915,887,000 -19.6 2,156,912,000 2,810,822,000 -23.3

Building Permits ($, City of Houston) Mar '16 698,185,400 626,751,768 11.4 1,563,724,875 1,878,985,666 -16.8

Nonresidential Mar '16 450,526,219 480,005,443 -6.1 993,390,253 1,168,029,228 -15.0

New Nonresidential Mar '16 68,270,010 250,708,550 -72.8 293,744,764 576,029,396 -49.0

Nonresidential Additions/Alterations/Conversions Mar '16 382,256,209 229,296,893 66.7 699,645,489 591,999,832 18.2

Residential Mar '16 247,659,181 146,746,325 68.8 570,334,622 710,956,438 -19.8

New Residential Mar '16 219,936,985 124,042,056 77.3 481,909,282 649,130,852 -25.8

Residential Additions/Alterations/Conversions Mar '16 27,722,196 22,704,269 22.1 88,425,340 61,825,586 43.0

Multiple Listing Service (MLS) Activity

Property Sales Mar '16 7,375 7,448 -1.0 17,969 17,698 1.5

Median Sales Price - SF Detached Mar '16 215,000 209,900 2.4 207,330 * 199,967 * 3.7

Active Listings Mar '16 34,504 28,507 21.0 33,226 * 28,121 * 18.2

EMPLOYMENT (Houston-Sugar Land-Baytown MSA)

Nonfarm Payroll Employment Mar '16 2,987,800 2,980,100 0.3 2,981,500 * 2,969,600 * 0.4

Goods Producing (Natural Resources/Mining/Const/Mfg) Mar '16 544,100 574,800 -5.3 546,733 0 577,433 * -5.3

Service Providing Mar '16 2,443,700 2,405,300 1.6 2,434,767 0 2,392,167 * 1.8

Unemployment Rate (%) - Not Seasonally Adjusted

Houston-Sugar Land-Baytown MSA Mar '16 4.9 4.3 4.8 * 4.4 *

Texas Mar '16 4.5 4.3 4.4 * 4.4 *

U.S. Mar '16 5.1 5.6 5.2 * 5.8 *

TRANSPORTATION

Port of Houston Authority Shipments (Short Tons) Feb '16 3,573,290 3,941,807 -9.3 7,077,333 7,635,976 -7.3

Air Passengers (Houston Airport System) Mar '16 4,658,322 4,654,563 0.1 13,162,637 12,633,240 4.2

Domestic Passengers Mar '16 3,650,022 3,748,623 -2.6 10,320,115 10,178,639 1.4

International Passengers Mar '16 1,008,300 905,940 11.3 2,842,522 2,454,601 15.8

Landings and Takeoffs Mar '16 66,012 68,261 -3.3 193,062 193,506 -0.2

Air Freight (metric tons) Mar '16 35,226 37,703 -6.6 97,898 108,387 -9.7

Enplaned Mar '16 17,589 19,463 -9.6 49,530 56,277 -12.0

Deplaned Mar '16 17,637 18,240 -3.3 48,368 52,110 -7.2

CONSUMERS

New Car and Truck Sales (Units, Houston MSA) Mar '16 27,054 30,119 -10.2 81,303 85,587 -5.0

Cars Mar '16 10,293 12,585 -18.2 30,380 35,538 -14.5

Trucks, SUVs and Commercials Mar '16 16,761 17,534 -4.4 50,923 50,049 1.7

Total Retail Sales ($000,000, Houston MSA, NAICS Basis) 2Q15 28,790 30,726 -6.3 52,439 58,260 -10.0

Consumer Price Index for All Urban Consumers ('82-'84=100)

Houston-Galveston-Brazoria CMSA Mar '16 214.505 210.283 2.0 214.113 * 210.755 * 1.6

United States Mar '16 238.132 236.119 0.9 237.386 * 234.849 * 1.1

Hotel Performance (Houston MSA)

Occupancy (%) 3Q15 67.2 71.3 70.0 * 73.3 *

Average Room Rate ($) 3Q15 104.37 102.14 2.2 109.26 * 106.97 * 2.1

Revenue Per Available Room ($) 3Q15 70.14 72.87 -3.7 76.55 * 78.42 * -2.4

YEAR-TO-DATE TOTAL or

YTD AVERAGE*MONTHLY DATA

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 11

Sources Rig Count Baker Hughes Incorporated Spot WTI, Spot Natural Gas U.S. Energy Information Admin. Houston Purchasing Managers National Association of Index Purchasing Management – Houston, Inc. Electricity CenterPoint Energy Building Construction Contracts McGraw-Hill Construction City of Houston Building Permits Building Permit Department, City of Houston

MLS Data Houston Association of Realtors Employment, Unemployment Texas Workforce Commission

Port Shipments Port of Houston Authority Aviation Aviation Department, City of Houston Car and Truck Sales TexAuto Facts Report, InfoNation, Inc.,

Sugar Land TX Retail Sales Texas Comptroller’s Office Consumer Price Index U.S. Bureau of Labor Statistics Hotels PKF Consulting/HospitalityAsset Advisors International Postings, Foreclosures Foreclosure Information &Listing Service

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 12

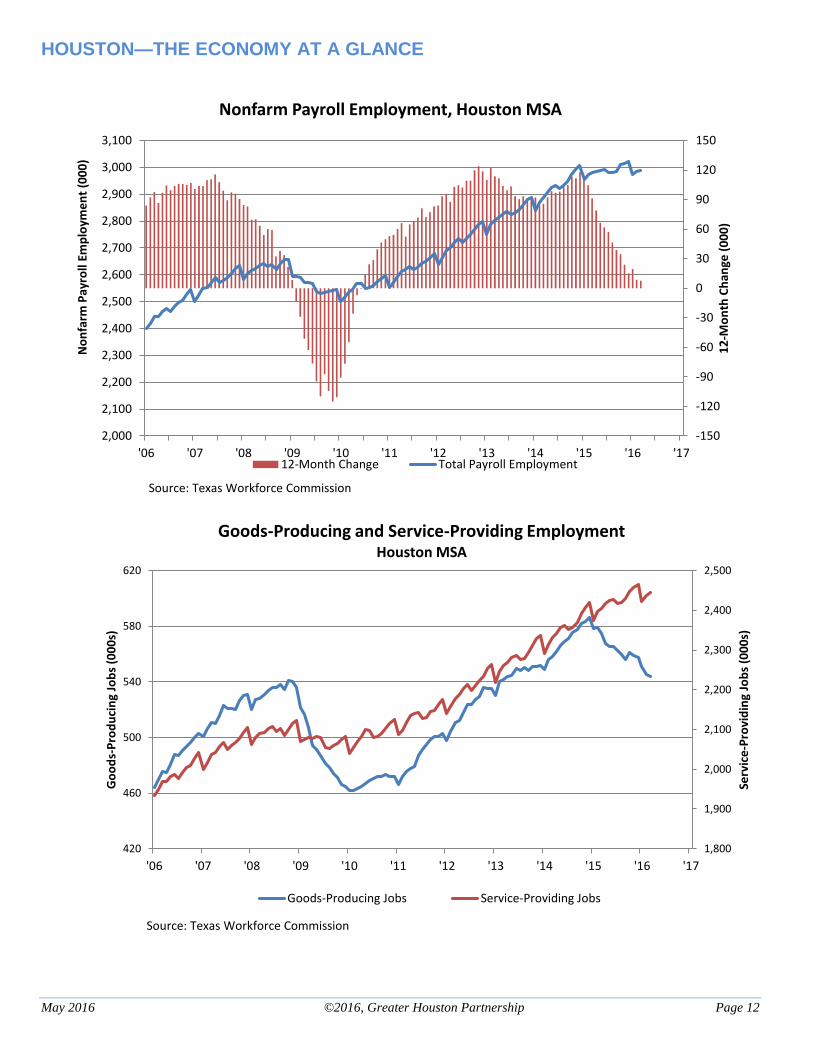

-150

-120

-90

-60

-30

0

30

60

90

120

150

2,000

2,100

2,200

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

3,100

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

12

-Mo

nth

Ch

ange

(0

00

)

No

nfa

rm P

ayro

ll Em

plo

yme

nt

(00

0)

Source: Texas Workforce Commission

Nonfarm Payroll Employment, Houston MSA

12-Month Change Total Payroll Employment

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

420

460

500

540

580

620

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Serv

ice

-Pro

vid

ing

Job

s (0

00

s)

Go

od

s-P

rod

uci

ng

Job

s (0

00

s)

Source: Texas Workforce Commission

Goods-Producing and Service-Providing EmploymentHouston MSA

Goods-Producing Jobs Service-Providing Jobs

HOUSTON—THE ECONOMY AT A GLANCE

May 2016 ©2016, Greater Houston Partnership Page 13

3

4

5

6

7

8

9

10

11

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

% C

ivili

an L

abo

r Fo

rce

Source: Texas Workforce Commission

Unemployment Rate - Houston, Texas and U.S.

Houston Texas U.S.

0

2

4

6

8

10

12

14

16

0

20

40

60

80

100

120

140

160

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Nat

ura

l Gas

, $ /

MM

Btu

WTI

, $ b

arre

l

Source: U.S. Energy Information Administration

Spot Crude and Natural Gas PricesMonthly Averages

WTI Natural Gas