Embed Size (px)

Citation preview

How Do Retirees Value Life Annuities?Evidence from Public Employees

John ChalmersLundquist College of Business, University of Oregon

Jonathan ReuterCarroll School of Management, Boston College, and the National Bureau ofEconomic Research

Becauselife annuities can increase the level and decrease the volatility of lifetimeconsumption, economists have long been puzzled by the low demand for life annuities. Onepotential rational explanation is that adverse selection drives up life annuity prices, whichdrives down demand. We study the choice between life annuities and lump sums madeby 32,000 retiring public employees. These unique data allow us to extend the existingliterature by exploiting economically significant cross-sectional and time-series variation inlife annuity pricing. We find little evidence that retiree demand for life annuities rises whenlife annuity prices fall. We find strong evidence that demand responds to salient variationin individual characteristics, such as health, and to measures of investor sentiment, such asrecent equity returns. (JELH55, D14, G11, G22)

Sincethe publication ofYaari’s(1965) seminal article, economists have arguedthat retirees should allocate a substantial portion of their assets to life annuities.Because life annuities continue making payments until death, they insureretirees against outliving their accumulated financial assets. In a standard life-cycle model, this insurance is quite valuable. It is puzzling, therefore, that

We thank Pierluigi Balduzzi, Daniel Bergstresser, Jeffrey Brown (AFA discussant), John Campbell, DavidChapman, Daniel Cooper, Cliff Holderness, Edie Hotchkiss, Alexander Ljungqvist (editor), Alan Marcus, RobinMcKnight, Bertrand Melenberg, Ali Ozdagli, Joshua Rauh, Antoinette Schoar, Phil Strahan, Peter Tufano, EricZitzewitz, and an anonymous referee, as well as the participants at the 2010 Netspar Pension Workshop, 2010Boston Area Consumer Finance Working Group, and 2011 American Finance Association Meetings for helpfuldiscussions related to this project. We thank Benjamin Goodman for providing data on how TIAA priced lifeannuities over our sample period, and we thank employees from the Oregon Public Employees RetirementSystem who provided invaluable assistance by compiling and helping us interpret their data. Because PERSwas subject to major legislative changes in late 2003, our description of the system only applies to the periodfor which we possess data. This research was supported by a U.S. Social Security Administration grant (#10-M-98363-1-01 to the National Bureau of Economic Research (NBER) as part of the SSA Retirement ResearchConsortium). The findings and conclusions expressed in this article are solely those of the authors and do notrepresent the views of the SSA, any agency of the federal government, PERS, the State of Oregon, or the NBER.Send correspondence to Jonathan Reuter, Carroll School of Management, Boston College, 140 CommonwealthAve., Chestnut Hill, MA 02467; telephone: 617-552-2863. E-mail: [email protected].

c© The Author 2012. Published by Oxford University Press on behalf of The Society for Financial Studies.All rights reserved. For Permissions, please e-mail: [email protected]:10.1093/rfs/hhs057

RFS Advance Access published April 6, 2012 at A

cquisition Dept Serials on A

pril 10, 2012http://rfs.oxfordjournals.org/

Dow

nloaded from

TheReview of Financial Studies / v 00 n 0 2012

theprivate market for life annuities is small.1 The traditional explanation forthis inconsistency between economic models and economic behavior is thatadverse selection drives up annuity prices, which drives down demand. Thispresupposes that retirees are rationally comparing the price of a life annuityto the expected benefit of smoother lifetime consumption.2 Alternatively, asdelineated inBrown (2009) andBenartzi, Previtero, and Thaler(2011), thedearth of annuitization may reflect poor financial decision-making, resultingfrom financial illiteracy or behavioral biases. Distinguishing between rationaland behavioral explanations for “under-annuitization” is important becausetheir welfare and policy implications are quite different.

Life-cycle models predict that demand for life annuities will be higher whenthe life annuity payments available to retirees are more valuable. Variation inthe value of these payments can arise from differences in retiree characteristicsor from differences in life annuity pricing. However, due to the lack ofplausibly exogenous variation in life annuity pricing, the existing literaturefocuses on variation in retiree characteristics (e.g.,Brown 2001;Finkelsteinand Poterba 2004; Butler and Teppa 2007;Previtero 2010;Inkmann, Lopes,and Michaelides 2011). Though informative, these articles offer an incompletepicture of retiree behavior. The fact that demand for life annuities respondsto variation in retiree health, e.g., need not imply that it responds to variationin life annuity pricing, which may not be salient, even when economicallysignificant.

To offer a fuller picture of how retirees value life annuities, we study theactual payout decisions of retirees covered by the Oregon Public EmployeesRetirement System (PERS).3 Oursample includes 32,060 retirements betweenJanuary 1990 and June 2002. It has two notable features. First, each retireemust choose whether to receive higher life annuity payments and no lump sumpayment (the “total life annuity” option) or lower life annuity payments and alump sum payment (the “lump sum” option). The choice between additionallife annuity payments and cash is analogous to the choice that retirees facein the private market. Second, our empirical setting provides us with a uniqueopportunity to study the impact of plausibly exogenous variation in life annuitypricing on retiree demand for life annuities.

Variation in life annuity pricing arises from the unusual way in which PERScalculates retirement benefits. Employees contribute a fixed percentage of their

1 Accordingto Beacon Research, life annuity sales (outside of employer-sponsored retirement plans) totaled eightbillion dollars in 2010, which is small relative to the annual sales of other financial products, such as mutualfunds.

2 Even whenYogo(2009) extends existing life-cycle models to include endogenous investments in health, he findsthat the expected utility gains from access to life annuities vary from 13% to 18%, with smaller gains for retireesin poorer health. Although these gains are approximately half of those estimated inMitchell et al.(1999), theyare economically significant.

3 PERSis the state agency that administers retirement plans for approximately 95% of the state and local publicemployees in Oregon. Our data exclude judges, politicians, or university employees. In 2009, PERS held nearly$53 billion in assets, making it the twenty-first largest public or private pension fund in the United States.

2

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

salaryto an account with two investment options. Under the lump sum option,retirees are offered their accumulated retirement account balance as the lumpsum payment. Under the total life annuity and lump sum options, life annuitypayments are calculated using as many as three formulas, and retirees areautomatically offered the maximum payments for which they are eligible. Forsome retirees, the maximum payment is based on the retiree’s years of serviceand salary history. For other retirees, the maximum payment is obtained whenthe retirement account balance is multiplied by a conversion factor, referredto as the actuarial equivalency factor, which depends only on the retiree’s age.Whereas the conversion factors used in the private market offer retirees a risk-free rate of return based on the yield of the ten-year U.S. Treasury note, theconversion factors used by PERS offer retirees a risk-free rate of return ofapproximately 10%, regardless of current market conditions.4

Thesefeatures cause the pricing of PERS life annuities to deviate from thepricing of life annuities in the private market in three significant ways. First,PERS life annuity payments are significantly larger than those that could bepurchased with the lump sum in the private market. This reflects the fact thatthe yield on the ten-year Treasury note is below 10% during our entire sampleperiod. For the median retiree, the total life annuity option has a “money’sworth” of $1.45, meaning that the incremental life annuity payments have anexpected present value of $1.45 per $1.00 in forgone lump sum payment. Byway of comparison,Mitchell et al. (1999) show that the money’s worth oflife annuities offered by life insurance companies is between $0.80 and $0.90.Second, the fact that different retirees’ maximum life annuity payments arecalculated using different formulas generates cross-sectional variation in thevalue of PERS life annuity payments. Consider a retiree whose maximum lifeannuity payment is based on her years of service and salary. Because she is alsoeligible for life annuity payments offering a 10% rate of return, the paymentsbased on her years of service and salary history must offer an even higher rateof return. This is one example of how retiree characteristics that would notimpact the level of life annuity payments in the private market can impact thelevel of PERS life annuity payments. Another example is that retirees who firstcontributed to PERS after August 1981 are eligible to have their (maximum)total life annuity payments calculated using one fewer formula than are retireeswho contributed to PERS before that date. Finally, because PERS conversionfactors are not adjusted to reflect market conditions, time-series variation inthe risk-free rate generates time-series variation in the value of the PERS lifeannuities relative to those in the private market. Everything else equal, whenthe yield on the ten-year Treasury note is lower, the total life annuity option ismore valuable.

4 ThePERS conversion factors are used to determine the initial life annuity payment. Because they were set wellbefore our sample period begins, when interest rates were routinely near 8%, they assume that the risk-free rateof return is 8%. Because of the cost-of-living adjustment, payments then increase by 2% per year.

3

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

If retirees understand that PERS life annuities are better than actuariallyfair, we should observe lower demand for lump sum payments in our settingthan in other settings. Indeed, only 15% of PERS retirees choose the lumpsum option. This fraction is significantly lower than one might surmise from areading of the literature on the under-annuitization puzzle. Given that there isno default payout option and Oregon public employees are eligible to receivelife annuity payments from Social Security, the high demand for life annuitiesis all the more striking.5 An interpretation of our finding is that the averageretiree recognizes that PERS life annuities are a “good deal.” However, thisbegs the question of whether retirees respond to variation in the generosity ofthe life annuities available from PERS.

The fraction of retirees choosing the lump sum option ranges from 6.9% in1992 to 21.7% in 2000. To explain variation in retiree choices, we estimateboth time-series regressions using the fraction of retirees choosing the lumpsum option each month and logit regressions using individuals’ choices. Thelogit regressions allow us to exploit the cross-sectional and time-series varia-tion in the value of life annuity payments described above. They also allowus to control for differences in retiree characteristics, which we conjectureare the most salient source of variation. For example, not only should a lifeannuity be less valuable to a (single) retiree in poor health, but also the impactof poor health on the value of the life annuity should be easily understood.Indeed, we find strong evidence that retirees understand how differences inhealth, risk aversion, and the level of already-annuitized income impact thevalue of the incremental life annuity income. These findings are consistentwith the predictions of life-cycle models and withBrown (2001),Finkelsteinand Poterba(2004), andInkmann, Lopes, and Michaelides(2011).

In contrast, when we focus on plausibly exogenous variation in life annuitypricing, our findings are difficult to reconcile with the predictions of life-cycle models. Although we observe significant cross-sectional variation in thevalue of life annuity payments due to the use of multiple benefit formulas,the evidence that retirees respond to this variation is weak. This suggeststhat cross-sectional variation in annuity pricing is not salient. And, althoughdemand for the lump sum option should decrease when the gap between the lifeannuity payments available from PERS and insurance companies like TIAAincreases, we find no evidence that it does. In fact, we find some evidencethat demand for the lump sum is higher when interest rates are lower. Oneexplanation for this puzzling relation is that retirees are confused about therole that interest rates play in life annuity valuation, which is consistent withthe evidence in, e.g.,Campbell(2006) andLusardi and Mitchell(2007), whofind that financial illiteracy leads to financial mistakes.

5 BecauseMadrianand Shea(2001) show that default options can have a dramatic impact on financial choices,it is fortuitous that PERS retirees are not assigned to either payout option by default. Retirees must activelychoose. We should only observe a retiree choosing the total life annuity option when the value she attaches tothe incremental life annuity payments exceeds the value she attaches to the lump sum payment.

4

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

An alternative explanation is that falling interest rates are correlated withdeclining economic conditions, which increase the relative value of the lumpsum payment. Similarly, because our sample period includes the NASDAQbubble, changes in interest rates may be correlated with changes in investorsentiment. To limit the impact of omitted-variables bias, we control for thereturn on the S&P 500 index over the prior twelve months, the inflation-adjusted level of the NASDAQ index, and the level of the CBOE VolatilityIndex (VIX). Doing so reduces the size of the puzzling relation betweendemand for lump sums and the level of interest rates. However, it alsoreveals that the one-time, irreversible choice between incremental life annuitypayments and the lump sum is influenced by contemporaneous measures ofinvestor sentiment. Specifically, we find robust evidence that demand for thelump sum option is higher when equity market returns are higher, even aftercontrolling for returns posted to retirees’ PERS retirement accounts. Althoughwe do not observe if retirees invest the lump sum payment in risky assets,this finding is consistent with retirees using the lump sum to chase pastreturns.6

The extent to which demand for incremental life annuities should respondto measures of investor sentiment, like the level of the NASDAQ index, isan open question. However, because the life annuities available from PERSoffer a risk-free rate of return of at least 10%, there is a significant opportunitycost associated with choosing the lump sum option. To put this opportunitycost in perspective, consider the 453 retirees who chose the lump sum optionin 2000. The average retiree traded life annuity payments with an expectedpresent value of $225,421 for an immediate lump sum of $151,367.7

In Section1, we discuss the existing empirical literature. In Section2, wemotivate our empirical predictions and discuss identification. In Section3, wedescribe our data. In Section4, we study how demand for lump sum paymentsvaries with retiree characteristics, the relative value of the incremental lifeannuity payments, and recent equity market returns. In Section5, we conclude.The Appendix provides a detailed description of the PERS benefit calculations.

1. Related Empirical Literature

Our findings complement existing studies of the choice between incrementallife annuities and lump sums.Finkelstein and Poterba(2004) find evidenceof adverse selection using data on life annuities purchased from a large U.K.annuity company. Similarly, we find that ex post mortality is associated with

6 Benartzi(2001)provides evidence that employees allocate more of their 401(k) contributions to company stockwhen the company’s stock return over the prior decade is higher. Similarly,Chevalier and Ellison(1997) andSirri and Tufano(1998) provide evidence of return chasing behavior by mutual fund investors. However,Berkand Green(2004) argue that return chasing is not necessarily irrational when choosing mutual funds.

7 Thiscalculation ignores the fact that retirees with shorter-than-average life expectancy are more likely to choosethe lump sum option, but it also ignores the insurance value that risk-averse retirees derive from life annuities.

5

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

lower demand for incremental life annuities, especially among retirees who aremore likely to be single.Inkmann, Lopes, and Michaelides(2011) use cross-sectional data from the 2002–2003 English Longitudinal Study of Ageing tostudy household demand for voluntary life annuities. They find that demandresponds to differences in life expectancy, the level of already-annuitizedincome, and other household characteristics. Then, they argue that a life-cyclemodel that incorporates demand for life annuities, life insurance, savings, andportfolio choice can rationalize the fact that only 5.9% of the households intheir sample purchase incremental life annuities. Interestingly, although PERSretirees’ characteristics have a qualitatively similar impact on the demand forincremental life annuities, we find that 85% of the retirees in our sample chooseincremental life annuities.

Butler and Teppa(2007) study payout choices for ten Swiss pension funds.Consistent with our findings, they find that the majority of retirees choose lifeannuities over lump sums. Therefore, the low demand for life annuities in theprivate market may reflect the fact that retirees have access to sufficient lifeannuity income through their pensions, or it may signal that the search costsassociated with shopping for a life annuity are high.Previtero(2010) studiesthe choice between life annuity and lump sum payments by private employeesusing data from defined benefit plans. Consistent with our findings, he findsthat the demand for life annuities is negatively correlated with recent stockmarket returns. However, because the money’s worth of the life annuities thatPrevitero studies match those available in the private market, the welfare costof any return chasing behavior is lower in his setting than in our setting, wherelife annuities are better than actuarially fair.

2. Empirical Predictions

In a standard life-cycle model, life annuities increase expected utility bymaking the individual’s consumption between retirement and death both higherand less uncertain.8 In our setting, incremental life annuity payments increaseexpected utility by increasing the level of risk-free income, and thereforepotential consumption, during retirement. The lump sum option, on the otherhand, trades incremental life annuity payments for a cash payment, whichcan be invested in risky liquid assets, invested in safe liquid assets, or usedto purchase goods and services.9 Therefore,the choice between the total lifeannuity and lump sum options should depend on the expected present value

8 Yaari (1965) derives conditions under which a retiree with an unknown date of death should convert all ofher liquid retirement assets into life annuities.Davidoff, Brown, and Diamond(2005) extend this analysis byshowing that retirees would benefit from converting a significant fraction of their assets into life annuities undermuch less restrictive conditions. Life annuities in the private market are able to offer higher rates of return thanare other risk-free investments, because they transfer assets from those who die to those who survive.

9 Bequestmotives typically reduce demand for life annuities. However, because the incremental life annuities thatwe study are better than actuarially fair, PERS retirees with bequest motives should choose the total life annuityoption and use the monthly payments to purchase life insurance.

6

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

of incremental life annuity payments relative to the level of the lump sumpayment, plus any option value associated with holding liquid assets. We usethis trade-off to motivate our empirical predictions.

Note that because the vast majority of PERS incremental life annuities arebetter than actuarially fair, an implicit assumption throughout our article isthat market frictions limit the ability of retirees to convert life annuities intolump sums in the private market. A natural and likely source of friction isasymmetric information about retiree life expectancy. In the absence of thesefrictions, all retirees with a normal life expectancy should choose the total lifeannuity option, and those who prefer a lump sum should convert some portionof their life annuity payments into a (larger) lump sum.

2.1 Variation in retiree characteristicsOur first set of predictions is based on the fact that differences in retireecharacteristics can generate cross-sectional differences in the expected utilityassociated with life annuity payments. BecauseBrown (2001), Finkelsteinand Poterba(2004), Butler and Teppa(2007), andInkmann, Lopes, andMichaelides(2011) find support for related predictions, we are primarilyinterested in exploring whether PERS retirees behave like the retirees studiedin other settings.

We consider seven retiree characteristics. First, because PERS does notadjust life annuity payments for differences in retiree health, we predict thatthe lump sum option will be more valuable to single retirees in poor health,who should expect to receive fewer payments. Second, because PERS doesnot adjust life annuity payments for the different life expectancies of malesand females, we predict that the lump sum option will be more valuable tosingle male retirees, who should expect to receive fewer payments than singlefemale retirees. Third, like other forms of insurance, life annuities should beless valuable to a retiree who is less risk averse. We predict that a retiree whoallocates more of her retirement account allocations to the riskier of the twoinvestment options will be more likely to choose the lump sum option. Fourth,to the extent that police and fire officers’ greater tolerance for occupational risktranslates into greater tolerance for financial risk, police and fire officers will bemore likely to choose the lump sum option. Fifth, because the marginal value ofinsurance declines with the level of insurance, the value that a retiree attachesto the incremental life annuity should fall with the level of already-annuitizedincome. We predict that demand for the lump sum option will rise with the levelof the life annuity payments under the lump sum option. Sixth, we predict thata retiree who is more reliant on PERS retirement benefits because she spenta larger fraction of her career working for PERS employers is less likely tochoose the lump sum option. Seventh, to the extent that financial literacy ispositively correlated with income (Campbell 2006), we predict that a retireewith a higher preretirement salary will be less likely to choose the lump sumpayment over a better-than-actuarially-fair life annuity.

7

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

Note that because all retirees receive some life annuity payments, retireesmust also choose between single life annuities, which stop making paymentswhen the retiree dies, and joint life annuities, which stop making paymentsonly after the retiree and their beneficiary have died. Because joint lifeannuities are more likely to be chosen by married retirees, who must alsoconsider the financial needs of their spouses, we expect the characteristicsof retirees choosing joint life annuities to explain less variation in demandfor lump sums (which is found byBrown 2001). Finally, Brown and Poterba(2000) argue that access to joint life annuities should make married retireesless likely to fully annuitize their retirement assets than might single retirees.The complication with testing this prediction in our setting is that, although welack the data needed to systematically compare the money’s worth of singleand joint life annuities, calculations based on the actual payout options of amarried retiree suggest that joint life annuities are significantly more generousthan are single life annuities.

2.2 Cross-sectional variation in life annuity pricingOur second set of predictions focuses on plausibly exogenous cross-sectionalvariation in life annuity pricing arising from how PERS calculates retirementbenefits. To understand how we exploit this variation, it is necessary to provideadditional details on how retirement benefits are determined under the totallife annuity and lump sum options. PERS employees contribute 6% of theirsalary to a defined contribution-style retirement account with two investmentoptions. They have the option to invest 25%, 50%, or 75% of their contributionto the riskier “variable” account; the remainder is invested in the safer “regular”account. The contributions and returns posted to these two accounts determinethe accumulated account balance at retirement, which is the size of the lumpsum payment under the lump sum option.

The level of the life annuity payment under the total life annuity option isautomatically calculated as the maximum of three possible benefit formulas.DC is a traditional defined contribution retirement benefit that depends on theactuarial equivalency factor that PERS uses to annuitize the retirement accountbalance.DB is a traditional defined benefit retirement benefit that depends onyears of service, salary history, whether the retiree is a police or fire officer, andan adjustment for early retirement.DCDB is a hybrid benefit that equals half ofDC plus slightly more than half ofDBand which is only available to employeeswho first contributed to PERS in or before August 1981.10 Thelevel of the lifeannuity payments under the lump sum option is automatically calculated as themaximum of two benefits: half of the total life annuity payment underDC orslightly more than half of the total life annuity payment underDB. Eligibility

10 PERSrefers to theDC, DB,andDCDBoptions as “Money Match,” “Full Formula,” and “Formula plus Annuity.”We state the various total life annuity and partial life annuity formulas in the Appendix.

8

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

for DCDB only impacts the level of the life annuity payments under the totallife annuity option.

When comparing the total life annuity option to the lump sum option, life-cycle models predict that retirees will compare the expected present value ofthe incremental life annuity payments under the total life annuity option tothe lump sum payment they must forgo. Dividing the incremental life annuitypayment by the lump sum payment yields an annuity price that is analogousto the actuarial equivalency factor quoted in the private market. The fact thatPERS uses multiple formulas to calculate life annuity payments under the totallife annuity and lump sum options generates cross-sectional variation in thisannuity price. Depending on the combination of formulas used to calculatethe maximum life annuity payments, the dollar value of the incremental lifeannuity payments can range from 32.5% to 50% of the total life annuitypayment. If this variation in annuity pricing is salient to retirees, we predictthat demand for the lump sum option will be lower when the relative value ofthe incremental life annuity payments is higher.

Because the total life annuity payments of retirees who first contributedinto PERS after August 1981 are calculated using two formulas instead ofthree, there are circumstances under which these retirees are eligible forsmaller incremental life annuity payments than retirees who first contributedinto PERS in or before August 1981 (holding retiree characteristics andthe retirement account balance constant). If this particular source of cross-sectional variation is salient, we predict that it will increase demand for thelump sum option.

Though variation due to the choice of retirement benefit formulas wouldnormally raise concerns about strategic behavior, PERS retirees automaticallyreceive the maximum life annuity payments for which they are eligible.Retirees can expect to increase their future retirement benefits by workinganother year, or by allocating a larger fraction of their retirement contributionsto the risky investment, but they have no influence over which formulas PERSuses to calculate their life annuity payments under the total life annuity andlump sum options; hence, retirees have no influence over the level of theincremental life annuity payments.

2.3 Time-series variation in life annuity pricingThe final prediction concerns variation in PERS life annuity pricing dueto time-series variation in the risk-free rate. In the market for private lifeannuities, insurance companies use the prevailing risk-free rate to set theactuarial equivalency factor, which determines the level of life annuity pay-ment per dollar invested. When interest rates fall, the actuarial equivalencyfactors available from TIAA and other insurance companies fall. In contrast,the actuarial equivalency factors that PERS uses in its retirement benefitcalculations rarely change. Because of this inertia, when the risk-free rate falls,life annuity payments available from PERS become relatively more generous

9

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

thanthe life annuity payments available from TIAA. To be clear, lower interestrates do not change the dollar value of the PERS incremental life annuitypayments. Instead, they increase the cost of buying the same incremental lifeannuity payments in the private market. Or, put differently, they increase thegap between the rate of return that retirees can earn on their retirement accountbalance by choosing the total life annuity option and the risk-free rate of returnavailable in the market. For this reason, we predict that demand for the lumpsum option will be lower when interest rates are lower.

There are several caveats. The prediction that lower interest rates makelife annuities more valuable is unique to our setting.Milevsky and Young(2002) argue that retirees in the private market should delay annuitizationwhen interest rates are low, rather than lock in permanently low life annuitypayments.11 Thefacts that PERS life annuity payments become relatively morevaluable when the risk-free rate falls, and that they are only available at the timeof retirement, imply that PERS retirees are unlikely to benefit from delayingannuitization.

More importantly, our prediction holds the value of the lump sum paymentconstant. To identify retirees’ choices as mistakes, we must rule out thepossibility that lower interest rates rationally increase demand for risky liquidassets, safe liquid assets, or consumption. Although we are limited by thefact that we do not observe whether the lump sum is invested or consumed,we are able to explicitly test two alternatives. The first is that lower interestrates increase the value of already-annuitized income and that the resultingincome effect increases demand for the lump sum option. The second is thatlower interest rates proxy for greater economic uncertainty, which increasesthe value of the lump sum option by even more than it increases the value ofthe incremental life annuity payments. To control for variation in economicuncertainty, we control for the level of the CBEO Volatility Index (VIX) atthe end of the month before the payout choice.12 If larger values of VIX,which is also known as the “fear index,” increase demand for liquid savings,the coefficient on the control variable will be positive.13

Finally, demand for the lump sum option may respond, for rational or be-havioral reasons, to time-series variation in investor sentiment. If fluctuationsin interest rates and investor sentiment are correlated and we do not control forfluctuations in investor sentiment, the coefficient on our measure of relative

11 Also see Tergesen, Anne, and Leslie Scism, “Are Annuities Being Overhyped as a Retirement Cure-All?”WallStreet Journal, February 13, 2010.

12 VIX measures the expected volatility on U.S. equity over the next thirty days. It has been shown to be negativelycorrelated with mutual fund flows and other measures of investor sentiment. See, e.g.,Ben-Rephael, Kandel, andWohl (2012).

13 On the other hand,Sundaresan(2001, p. 208) provides evidence that interest rate volatility is positivelycorrelated with the level of interest rates. Given the 2% annual cap on cost-of-living adjustments, it seems justas likely that higher interest rate volatility could generate more demand for lump sum payments, which couldbe invested in assets offering even better inflationary hedges. This argument suggests that lower interest ratesshould decrease demand for the lump sum option.

10

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

generositywill suffer from omitted-variables bias. To distinguish the impactof interest rates from the impact of the NASDAQ bubble, which burst towardthe end of our sample period, we control for the inflation-adjusted level of theNASDAQ index, which has a correlation of 0.4638 with our measure of PERSgenerosity. We also control for the return on the S&P 500 index over the priortwelve months. To the extent that retirees forgo better-than-actuarially-fair lifeannuity payments in response to recent equity market conditions, they may bemaking costly mistakes.

2.4 Measuring variation in life annuity pricingAs introduced earlier, the money’s worth of the incremental life annuity is theexpected present value of the future life annuity payments per dollar of initialoutlay. The money’s worth of the incremental life annuity payments availableto retireek is defined as

MWkMax =

[Ak]

×[

1

Pk

]× EPVk

g , (1)

whereAk is the initial level of the incremental life annuity payment to retireek, Pk is the level of the forgone lump sum payment (i.e., the price of theincremental life annuity payments), andEPV k

g denotesthe expected presentvalue of retireek receiving $1.00 in month 1, $1.00 (1+g) in month 2, etc.,until death, which depends on the probability that retireek is alive to receiveeach payment.14 When incremental life annuity payments are priced to beactuarially fair, money’s worth equals $1.00.

Life annuity payments are quoted in terms of actuarial equivalency factors,which state the (fixed and nominal) number of dollars paid out each monthuntil death, per $1,000 in initial outlay. When the maximal total life annuityand partial life annuity payments for retireek are both calculated underDC,the money’s worth of the incremental life annuity payments is

MWkDC =

[AEFk

PERS × AccountBalance

$1,000

]

×[

1

AccountBalance

]× E PVk

g ,

(2)whereAEFPERSincreaseswith retiree age to reflect declining life expectanciesbut does not vary with gender.15 BecausePERS life annuities include a cost-of-living adjustment that is capped at 2.0% per year, and because that cap isbinding throughout our sample period, we setg equal to 0.17% per month.

14 Whenestimating the expected present value of life annuity payments for retireek in montht , we use the yield onten-year Treasury notes on the last trading day of montht − 1, and we use the mortality tables published by theSocial Security Administration for 2004. The second assumption leads us to slightly overestimate the estimatedpresent value in 1990 relative to 2002.

15 Finkelstein, Poterba, and Rothschild(2009) study the transfer from males to females that results from notallowing actuarial equivalency factors to vary with gender. These restrictions apply to the market for pensionannuities in the United Kingdom, Oregon’s Public Employees Retirement System, and TIAA, among others.

11

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

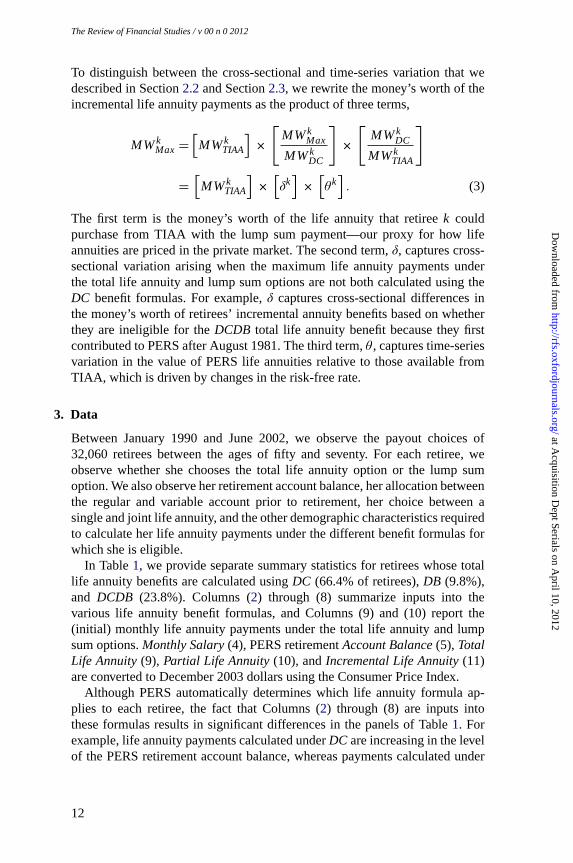

To distinguish between the cross-sectional and time-series variation that wedescribed in Section2.2and Section2.3, we rewrite the money’s worth of theincremental life annuity payments as the product of three terms,

MWkMax =

[MWk

TIAA

]×

[MWk

Max

MWkDC

]

×

[MWk

DC

MWkTIAA

]

=[MWk

TIAA

]×[δk]

×[θk]. (3)

The first term is the money’s worth of the life annuity that retireek couldpurchase from TIAA with the lump sum payment—our proxy for how lifeannuities are priced in the private market. The second term,δ, captures cross-sectional variation arising when the maximum life annuity payments underthe total life annuity and lump sum options are not both calculated using theDC benefit formulas. For example,δ captures cross-sectional differences inthe money’s worth of retirees’ incremental annuity benefits based on whetherthey are ineligible for theDCDB total life annuity benefit because they firstcontributed to PERS after August 1981. The third term,θ , captures time-seriesvariation in the value of PERS life annuities relative to those available fromTIAA, which is driven by changes in the risk-free rate.

3. Data

Between January 1990 and June 2002, we observe the payout choices of32,060 retirees between the ages of fifty and seventy. For each retiree, weobserve whether she chooses the total life annuity option or the lump sumoption. We also observe her retirement account balance, her allocation betweenthe regular and variable account prior to retirement, her choice between asingle and joint life annuity, and the other demographic characteristics requiredto calculate her life annuity payments under the different benefit formulas forwhich she is eligible.

In Table1, we provide separate summary statistics for retirees whose totallife annuity benefits are calculated usingDC (66.4% of retirees),DB (9.8%),and DCDB (23.8%). Columns (2) through (8) summarize inputs into thevarious life annuity benefit formulas, and Columns (9) and (10) report the(initial) monthly life annuity payments under the total life annuity and lumpsum options.Monthly Salary(4), PERS retirementAccount Balance(5), TotalLife Annuity(9), Partial Life Annuity(10), andIncremental Life Annuity(11)are converted to December 2003 dollars using the Consumer Price Index.

Although PERS automatically determines which life annuity formula ap-plies to each retiree, the fact that Columns (2) through (8) are inputs intothese formulas results in significant differences in the panels of Table1. Forexample, life annuity payments calculated underDC are increasing in the levelof the PERS retirement account balance, whereas payments calculated under

12

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

Tabl

e1

Ore

gon

PE

RS

retir

ees’

char

acte

ristic

s,19

90–2

002

Yea

rsof

Mon

thly

PE

RS

Acc

ount

%P

olic

eor

%E

arly

Tota

lLife

Par

tialL

ifeIn

crem

enta

lN

o.R

etire

esA

geS

ervi

ceS

alar

yB

alan

ceF

ire%

Fem

ale

Ret

iree

Ann

uity

Ann

uity

Ann

uity

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

Pane

lA:R

etire

esfo

rW

hom

Max

imal

Tota

lLife

Ann

uity

Pay

men

tDet

erm

ined

byD

C

1990

336

60.6

17.5

$4,5

55$1

10,5

383.

335

.730

.4$1

,921

$961

$960

1991

882

60.9

19.2

$4,3

09$1

23,3

132.

440

.023

.4$2

,153

$1,0

78$1

,075

1992

544

61.0

19.7

$4,4

52$1

19,4

224.

235

.127

.6$2

,093

$1,0

48$1

,046

1993

924

60.6

20.8

$4,5

19$1

33,8

682.

836

.627

.6$2

,317

$1,1

61$1

,157

1994

1,10

460

.521

.4$4

,574

$136

,170

3.0

41.6

28.5

$2,3

54$1

,180

$1,1

7519

951,

138

60.3

20.9

$4,2

65$1

41,6

623.

049

.025

.3$2

,434

$1,2

19$1

,215

1996

1,22

060

.221

.9$4

,315

$142

,426

2.8

47.5

23.2

$2,4

43$1

,225

$1,2

1719

971,

785

59.8

21.7

$4,3

59$1

55,7

814.

352

.823

.9$2

,667

$1,3

37$1

,330

1998

3,63

559

.122

.2$4

,469

$174

,448

4.4

53.6

33.6

$2,9

41$1

,473

$1,4

6719

993,

614

58.5

21.7

$4,5

28$1

81,6

136.

054

.838

.0$3

,020

$1,5

13$1

,507

2000

1,69

158

.320

.8$4

,484

$178

,727

8.4

55.5

38.6

$2,9

54$1

,482

$1,4

7220

012,

311

58.4

22.2

$4,6

03$1

88,5

867.

455

.632

.2$3

,126

$1,5

67$1

,558

2002

2,08

958

.323

.2$4

,726

$197

,325

6.8

57.1

34.3

$3,2

68$1

,641

$1,6

27

Pan

elB

:Ret

irees

for

Who

mM

axim

alTo

talL

ifeA

nnui

tyP

aym

entD

eter

min

edby

DB

1990

299

58.8

22.6

$4,4

13$7

3,32

917

.144

.14.

0$1

,829

$1,1

36$6

9319

9118

059

.519

.1$4

,203

$56,

450

20.0

45.0

7.2

$1,5

31$9

56$5

7519

9227

259

.917

.7$4

,397

$57,

921

19.1

46.7

7.0

$1,4

68$9

18$5

5119

9327

661

.214

.8$4

,080

$41,

867

19.6

43.5

5.8

$1,1

49$7

25$4

2319

9449

660

.516

.0$4

,242

$51,

231

16.1

48.2

7.3

$1,3

03$8

16$4

8719

9518

661

.111

.4$3

,507

$27,

484

10.8

52.7

11.3

$643

$392

$251

1996

316

60.8

12.1

$4,0

04$3

7,21

813

.952

.25.

1$8

91$5

53$3

3819

9724

860

.212

.8$4

,063

$40,

179

16.9

57.3

11.7

$915

$566

$349

1998

197

60.1

13.4

$4,1

29$4

1,02

219

.360

.917

.8$9

77$6

04$3

7319

9918

260

.012

.9$3

,766

$35,

421

22.5

54.4

15.9

$829

$514

$315

2000

106

60.1

11.2

$4,2

35$3

6,80

320

.837

.714

.2$8

42$5

21$3

2220

0119

860

.212

.6$4

,303

$42,

585

15.7

48.5

13.6

$973

$599

$374

2002

198

60.5

11.5

$4,1

79$3

6,48

015

.260

.614

.6$8

27$5

08$3

19

(co

ntin

ue

d)

13

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

Tabl

e1

Con

tinue

d

Yea

rsof

Mon

thly

PE

RS

Acc

ount

%P

olic

eor

%E

arly

Tota

lLife

Par

tialL

ifeIn

crem

enta

lN

o.R

etire

esA

geS

ervi

ceS

alar

yB

alan

ceF

ire%

Fem

ale

Ret

iree

Ann

uity

Ann

uity

Ann

uity

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

Pane

lC:R

etire

esfo

rW

hom

Max

imal

Tota

lLife

Ann

uity

Pay

men

tDet

erm

ined

byD

CD

B

1990

986

60.5

20.3

$3,9

32$7

8,88

86.

352

.813

.2$1

,523

$844

$679

1991

814

59.4

22.0

$4,0

07$9

4,57

414

.154

.19.

5$1

,773

$984

$789

1992

1,05

959

.722

.4$4

,262

$97,

160

13.4

49.1

12.5

$1,8

55$1

,034

$822

1993

973

59.5

22.7

$4,2

84$1

02,5

2114

.057

.810

.6$1

,928

$1,0

65$8

6319

941,

575

58.9

23.5

$4,4

69$1

10,1

6415

.656

.611

.1$2

,066

$1,1

50$9

1619

9531

358

.521

.2$4

,247

$102

,851

23.3

65.2

9.9

$1,8

64$1

,025

$839

1996

537

57.9

23.0

$4,6

09$1

20,3

2324

.658

.78.

8$2

,187

$1,2

14$9

7319

9742

456

.523

.6$5

,205

$149

,493

46.0

46.5

11.1

$2,7

07$1

,515

$1,1

9219

9833

855

.823

.9$5

,496

$174

,017

59.5

42.3

16.9

$3,0

39$1

,667

$1,3

7219

9926

955

.524

.6$6

,078

$206

,041

65.8

33.1

11.5

$3,5

44$1

,923

$1,6

2120

0086

54.6

24.9

$6,4

13$2

28,5

0074

.429

.18.

1$3

,905

$2,1

28$1

,777

2001

135

54.9

24.9

$6,3

85$2

20,3

4863

.038

.511

.1$3

,736

$2,0

19$1

,717

2002

124

55.9

24.6

$6,1

32$2

04,7

0955

.647

.616

.9$3

,514

$1,8

97$1

,617

Thi

sta

ble

repo

rts

sum

mar

yst

atis

tics

for

indi

vidu

als

betw

een

the

ages

offif

tyan

dse

vent

yw

hore

tire

from

the

Ore

gon

Pub

licE

mpl

oyee

sR

etire

men

tS

yste

m(P

ER

S)

and

begi

nco

llect

ing

retir

emen

tben

efits

imm

edia

tely

afte

rle

avin

gem

ploy

men

t.P

anel

sA

,B,a

ndC

focu

son

retir

ees

who

seto

tall

ifean

nuity

bene

fits

are

calc

ulat

edun

der

DC

,DB

,and

DC

DB

,res

pect

ivel

y.A

gere

port

sth

eav

erag

em

embe

rs’a

gein

the

mon

thof

retir

emen

t;Y

ears

ofS

ervi

cere

port

sth

eav

erag

enu

mbe

rof

year

sth

atth

em

embe

rco

ntrib

uted

into

PE

RS

;Mon

thly

Sal

ary

isth

eav

erag

eof

the

mem

ber’s

PE

RS

sala

ryov

erth

epr

ior

thirt

y-si

xm

onth

s;A

ccou

ntB

alan

ceis

the

aver

age

valu

eof

the

mem

ber’s

PE

RS

retir

emen

tac

coun

tba

lanc

esat

the

time

ofre

tirem

ent,

whi

chde

term

ines

the

size

ofth

elu

mp

sum

payo

ut;%

Fem

ale

mea

sure

sth

efr

actio

nof

retir

ees

who

are

fem

ale;

%P

olic

eor

Fire

mea

sure

sth

efr

actio

nof

retir

ees

who

prev

ious

lyw

orke

das

polic

eor

fire

offic

ers;

and

%R

etiri

ngE

arly

mea

sure

sth

efr

actio

nof

mem

bers

who

retir

ebe

fore

reac

hing

the

norm

alre

tirem

enta

ge.T

otal

Life

Ann

uity

isth

eav

erag

ele

velo

fthe

initi

alm

onth

lypa

ymen

tund

erth

eto

tall

ifean

nuity

optio

n,w

here

asP

artia

lLife

Ann

uity

isth

eav

erag

ele

velo

fthe

initi

alm

onth

lypa

ymen

tund

erth

elu

mp

sum

optio

n.M

onth

lyS

alar

y,A

ccou

ntB

alan

ce,

Tota

lLife

Ann

uity

,and

Par

tialL

ifeA

nnui

tyar

eco

nver

ted

into

Dec

embe

r20

03do

llars

usin

gth

eC

onsu

mer

Pric

eIn

dex.

14

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

DB arenot. Consequently, the averageAccount Balanceranges from $110,538to $197,325 underDC but from $27,484 to $73,329 underDB.

Table1 highlights the variation in annuity pricing faced by retirees whosemaximal total life annuity payments are calculated underDC, DB, andDCDB. Consider retirees in 1995. In Panel A, the average retiree forgoesapproximately 50% of the total life annuity monthly payment of $2,434 toreceive an immediate lump sum payment of $141,662. On the other hand,in Panel B, the retiree forgoes approximately 40% of the total life annuitymonthly payment of $643 to receive an immediate lump sum payment of$27,484.

In Table 2, we illustrate how the relative value of PERS life annuitypayments varies with the risk-free rate of return. Specifically, we calculate themoney’s worth of PERS incremental life annuity payments underDC for maleretirees who turn sixty-five in January 1990, January 1991, . . . , January 2002.We also calculate the money’s worth of the life annuity payments that retireescould purchase from TIAA using the lump sum payment. For these retirees,the PERS life annuity is always better than actuarially fair, with money’s worthranging from $1.14 in January 1990 to $1.50 in January 2002.

Within our sample of 32,060 retirees, the money’s worth of the incrementallife annuity is better than actuarially fair for all but 112 retirees. In contrast,the money’s worth of the life annuities offered by TIAA is less volatile andnever more than $0.92. In Table2, for a 65-year-old male,θ ranges from 1.30to 1.77. Within our full sample of retirees,θ ranges from 1.17 to 1.82, withan average value of 1.60. The main source of time-series variation inθ is thefact that TIAA adjusts its actuarial equivalency factors each January, based onchanges in annuitant life expectancy and the risk-free rate, whereas PERS doesnot.16 In the bottom row of Table2, we show that the correlation between theyield on ten-year U.S. Treasury notes and TIAA’s actuarial equivalency factors(Column (4)) is 0.935. We also show that the correlation between the Treasuryyield andθ (Column (9)) is−0.955.

4. How Do PERS Retirees Value Incremental Life Annuities?

Table3 reports the fraction of PERS retirees choosing the lump sum optioneach year. Notably, only 15% choose the lump sum option; the remaining 85%choose to receive all of their retirement benefits in the form of life annuitypayments. The high demand for incremental life annuities in our setting isstriking and is consistent with the fact that PERS incremental life annuitieshave much higher money’s worth than life annuities available in the privatemarket.

16 PERSadjusts its actuarial equivalency factor tables once during our sample period. On January 1, 1997, PERSswitches from actuarial equivalency factors that increase annually, in the retiree’s birth month, to factors thatincrease monthly. At the same time, PERS increases actuarial equivalency factors for those retiring below theage of fifty-five. However, the increases are small, ranging from 2.2% at age fifty to 0.1% at age fifty-four.

15

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

Tabl

e2

Com

parin

gm

oney

’sw

orth

oflif

ean

nuiti

esav

aila

ble

from

PE

RS

and

TIA

A,1

990–

2002

PE

RS

TIA

AP

ER

SR

elat

ive

toT

IAA

Yie

ldTe

n-Ye

arY

ear

AE

FE

PV

MW

AE

FE

PV

MW

AE

FE

PV

θT

reas

ury(

%)

(1)

(2)

(3)

(4)

(5)

(6)

(7)=

(1)/

(4)

(8)=

(2)/

(5)

(9)=

(3)/

(6)

(10)

1990

9.79

115.

941.

148.

8299

.39

0.88

1.11

1.17

1.30

8.43

1991

9.79

119.

511.

178.

7510

2.19

0.89

1.12

1.17

1.31

8.03

1992

9.79

126.

221.

248.

5210

7.41

0.92

1.15

1.18

1.35

7.31

1993

9.79

135.

811.

337.

7211

4.84

0.89

1.27

1.18

1.50

6.39

1994

9.79

145.

371.

427.

1012

2.20

0.87

1.38

1.19

1.64

5.64

1995

9.79

123.

271.

217.

7210

5.12

0.81

1.27

1.17

1.49

7.59

1996

9.79

145.

371.

427.

1012

2.20

0.87

1.38

1.19

1.64

5.58

1997

9.79

134.

681.

327.

3411

3.97

0.84

1.33

1.18

1.58

6.50

1998

9.79

146.

641.

447.

0312

3.18

0.87

1.39

1.19

1.66

5.51

1999

9.79

157.

501.

546.

6113

1.47

0.87

1.48

1.20

1.77

4.65

2000

9.79

132.

481.

307.

3911

2.27

0.83

1.33

1.18

1.56

6.67

2001

9.79

150.

571.

477.

0812

6.18

0.89

1.38

1.19

1.65

5.18

2002

9.79

153.

281.

506.

7712

8.25

0.87

1.45

1.20

1.73

5.03

Cor

rel.

0.00

0−

0.99

8−

0.99

80.

935

−0.

998

−0.

028

−0.

945

−0.

999

−0.

955

—

We

com

pare

the

mon

ey’s

wor

thof

life

annu

ities

base

don

PE

RS

’D

Cbe

nefit

toth

em

oney

’sw

orth

ofT

IAA’

slif

ean

nuiti

es.W

eas

sum

eth

atth

ere

tiree

issi

xty-

five

year

san

dze

rom

onth

sol

dan

dm

ale.

The

actu

aria

lequ

ival

ency

fact

or,A

EF,

dete

rmin

esth

ein

itial

mon

thly

life

annu

itypa

ymen

tper

$1,0

00sp

entt

opu

rcha

seth

elif

ean

nuity

.Dur

ing

our

sam

ple

perio

d,P

ER

Sra

rely

adju

sts

itsA

EF

s(s

eefo

otno

te16

)w

here

asT

IAA

adju

sts

itsA

EF

sin

Janu

ary

ofea

chca

lend

arye

arto

refle

ctch

ange

sin

mem

ber

life

expe

ctan

cies

orth

eris

k-fr

eera

te.E

PV

isth

eex

pect

edpr

esen

tval

ueof

rece

ivin

gan

initi

alm

onth

lylif

ean

nuity

paym

ento

f$1.

00be

ginn

ing

next

mon

th.T

heno

min

alva

lue

ofth

elif

ean

nuity

paym

ents

tobe

rece

ived

from

PE

RS

isas

sum

edto

grow

at2.

0%pe

rye

ar,w

here

asth

eno

min

alva

lue

oflif

ean

nuity

paym

ents

tobe

rece

ived

from

TIA

Ais

assu

med

tobe

cons

tant

.To

calc

ulat

eth

epr

obab

ility

that

the

retir

eere

ceiv

esth

elif

ean

nuity

paym

enttm

onth

sfro

mto

day,

we

use

life

tabl

espu

blis

hed

byth

eU

.S.S

ocia

lSec

urity

Adm

inis

trat

ion

for

2004

.To

calc

ulat

eth

epr

esen

tval

ueof

the

expe

cted

paym

ents

,we

use

the

yiel

don

the

ten-

year

U.S

.Tre

asur

yno

teat

the

end

ofth

epr

ior

mon

th.T

heav

erag

ean

nual

yiel

dis

repo

rted

inC

olum

n(1

0).W

eca

lcul

ate

mon

ey’s

wor

thof

each

life

annu

ityas

the

expe

cted

pres

entv

alue

ofits

life

annu

itypa

ymen

tsre

lativ

eto

itspr

ice

(i.e.

,as

AE

Ftim

esE

PV

divi

ded

by$1

,000

).In

Col

umn

(9),

we

calc

ulat

eth

em

oney

’sw

orth

ofth

eP

ER

Slif

ean

nuity

rela

tive

toth

em

oney

’sw

orth

ofth

eT

IAA

life

annu

ity(i.

e.,θeq

uals

AE

F PE

RS

times

EP

V 2%

divi

ded

byA

EF T

IAA

times

EP

V 0%

.Whe

nθ

equa

lson

e,P

ER

San

dT

IAA

allo

wre

tiree

sto

purc

hase

the

sam

eex

pect

edpr

esen

tval

ueof

life

annu

itybe

nefit

spe

rdo

llar

ofin

itial

outla

y.Va

lues

grea

ter

than

one,

asob

serv

edin

this

tabl

e,im

ply

that

PE

RS

sells

mor

eva

luab

lelif

ean

nuity

bene

fits

than

TIA

A.T

hebo

ttom

row

repo

rts

the

pairw

ise

corr

elat

ion

betw

een

the

yiel

don

the

ten-

year

U.S

.Tre

asur

yno

tean

dA

EF,

EP

V,an

dM

W.

16

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

Tabl

e3

Per

cent

ofP

ER

Sre

tiree

sch

oosi

nglu

mp

sum

optio

n,by

retir

emen

tcal

cula

tion

met

hod,

1990

–200

2

All

Re

tire

es

DC

DB

DC

DB

Yea

rN

o.R

etire

es%

Lum

pM

WN

o.R

etire

es%

Lum

pM

WN

o.R

etire

es%

Lum

pM

WN

o.R

etire

es%

Lum

p MW

1990

1,62

18.

6$1

.16

336

7.1

$1.1

229

99.

4$1

.24

986

8.8

$1.1

519

911,

876

8.6

$1.2

188

27.

9$1

.20

180

15.0

$1.2

981

47.

9$1

.21

1992

1,87

56.

9$1

.30

544

7.2

$1.2

827

211

.0$1

.38

1,05

95.

7$1

.31

1993

2,17

39.

7$1

.47

924

9.2

$1.4

227

618

.8$1

.54

973

7.6

$1.5

219

943,

175

10.4

$1.2

61,

104

11.4

$1.2

449

614

.3$1

.31

1,57

58.

5$1

.27

1995

1,63

716

.4$1

.40

1,13

816

.8$1

.40

186

22.6

$1.3

031

311

.2$1

.47

1996

2,07

318

.1$1

.39

1,22

018

.2$1

.37

316

20.6

$1.3

253

716

.4$1

.40

1997

2,45

717

.9$1

.43

1,78

518

.8$1

.43

248

22.2

$1.2

842

411

.6$1

.45

1998

4,17

020

.5$1

.59

3,63

521

.0$1

.59

197

23.9

$1.4

833

812

.7$1

.60

1999

4,06

520

.4$1

.51

3,61

420

.5$1

.51

182

22.0

$1.3

526

918

.2$1

.51

2000

1,88

321

.7$1

.48

1,69

121

.4$1

.50

106

28.3

$1.2

986

19.8

$1.4

720

012,

644

15.9

$1.6

32,

311

15.7

$1.6

319

818

.7$1

.48

135

15.6

$1.6

420

022,

411

10.6

$1.6

72,

089

10.4

$1.6

719

811

.6$1

.58

124

12.1

$1.6

8To

tal

32,0

6015

.0$1

.45

21,2

7316

.6$1

.49

3,15

417

.3$1

.36

7,63

39.

6$1

.33

Thi

sta

ble

sum

mar

izes

the

dem

and

for

lum

psu

mop

tions

acro

ssye

ars

and

acro

ssre

tiree

sfo

rw

hom

the

tota

llife

annu

itybe

nefit

isca

lcul

ated

usin

gD

C,

DB

,or

DC

DB

.T

hesa

mpl

eis

the

sam

eth

atw

esu

mm

ariz

ein

Tabl

e1.%

Lum

pre

flect

sth

efr

actio

nof

retir

ees

choo

sing

the

lum

psu

mop

tion.

MW

isth

em

oney

’sw

orth

ofth

eto

tall

ifean

nuity

optio

nre

lativ

eto

the

lum

psu

mop

tion.

Itis

defin

edas

the

expe

cted

pres

ent

valu

eof

the

life

annu

itypa

ymen

tsun

der

the

tota

llife

annu

ityop

tion

min

usth

ose

unde

rth

elu

mp

sum

optio

n,di

vide

dby

the

lum

psu

mpa

yout

.We

repo

rtth

em

edia

nva

lue

ofM

Wea

chye

ar.

17

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

The Review of Financial Studies / v 00 n 0 2012

The low demand for lump sum payments is also consistent with alternativeexplanations. It may reflect the fact that individuals with greater demand forannuitized retirement benefits are more likely to become public employees. Itmay reflect the fact that it is easier for employees to choose the total life annuitypayout option over the lump sum option than it is for other retirees to researchand purchase incremental life annuities in the private market. Or, becausePERS reports the monthly payment associated with each payout option ratherthan the implied rate of return, it may reflect the framing effect described inBrown et al.(2008). We cannot measure the impact of these explanations onthe average demand for lump sum payments. However, because they are time-invariant, they are unlikely to explain time-series variation in the fraction ofretirees choosing the lump sum option.

4.1 Time-series regressionsFigure 1 reveals significant time-series variation in the fraction of retireeschoosing the lump sum option, and Table3 shows that this variation existsregardless of how the total life annuity benefit is calculated. In Table4, we seekto explain this time-series variation in the demand for the lump sum option. Thedependent variable in each time-series regression is the fraction of retirees whochoose the lump sum option in montht . Because the number of retirementsvaries significantly across months (from a low of six in January 1990 to ahigh of 2,999 in February 1998), this fraction is a noisier estimate of retireepreferences in some months than others. To account for this heteroscedasticity,

Figure 1Fraction of PERS employees choosing lump sum option and lagged stock return, 1990–2002Monthly time-series plot of the fraction of retirees in each month who choose the lump sum option (scale on theleft axis) and the return on the S&P 500 index over the prior twelve months (scale on the right axis). Our sampleperiod is January 1990 to June 2002.

18

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees

Table 4Predicting average monthly demand for lump sum option, 1990–2002

Estimation: Levels Levels Levels Levels 1st Differences

(1) (2) (3) (4) (5)

Relative Generosity of PERS Life Annuity 0.268∗∗∗ 0.265∗∗∗ 0.206∗∗∗ 0.111∗∗∗ 0.322∗

(0.069) (0.038) (0.048) (0.039) (0.185)Returnon S&P 500 Index over prior 12 months 0.160∗∗∗ 0.174∗∗∗ 0.144∗∗∗ 0.071∗

(0.042) (0.036) (0.028) (0.041)Level of VIX index at end of prior month 0.289∗∗ 0.100 0.119

(0.131) (0.092) (0.124)Inflation-adjustedlevel of NASDAQ index 0.005∗∗∗ 0.001

atend of prior month (0.001) (0.002)Constant −0.182 −0.195∗∗∗ −0.180∗∗∗ −0.073 −0.009∗∗

(0.080) (0.049) (0.057) (0.048) (0.004)Numberof monthly observations 150 150 150 150 149F-statistic 15.07∗∗∗ 37.55∗∗∗ 23.39∗∗∗ 31.64∗∗∗ 2.67∗∗

We report coefficients from time-series regressions estimated via weighted least squares. The sample consists ofthe 150 months between January 1990 and June 2002. The dependent variable is the fraction of PERS retireeswho choose the lump sum option in montht . The weight in montht is the number of retiree choices used tocalculate this fraction. Independent variables include the ratio of the actuarial equivalency factor available fromPERS (under the DC formula) to the life annuity payment available from TIAA (i.e., Column (7) of Table2),the return on the S&P 500 index over the prior twelve months, the implied volatility on the S&P 500 indexoption over montht as measured by the CBOE Volatility Index (VIX) at the end of montht − 1, and theinflation-adjusted level of NASDAQ measured at the end of montht−1. Variables in Columns (1) through (4)are measured as levels. Variables in Column (5) are measured as first differences, which results in the loss of oneobservation. Standard errors are reported in parentheses and calculated as inNewey and West(1987), with a lagof twenty-four months. Significance at the 10%, 5%, and 1% levels is denoted by *, **, and ***.

we weight each observation by the number of retirements in that month.Standard errors are estimated using theNewey and West(1987) estimator,allowing autocorrelation to persist for twenty-four months.

Our basic prediction is that demand for the lump sum option will fall whenincremental life annuities are more valuable. Yet, in Column (1), we find thatdemand for the lump sum option rises when PERS life annuities are relativelymore generous than those available from TIAA. The coefficient is statisticallysignificant at the 1% level. It is also economically significant. A one-standard-deviation increase in the relative generosity of PERS is associated with a3.2 percentage point increase in the demand for the lump sum option. Inother words, demand for lump sums is increasing precisely when the relativevalue of the incremental life annuities available from PERS is increasing. Oneinterpretation is that retirees are confused about the impact of interest rates onthe value of PERS life annuity payments. For example, they may be followingadvice—like that inMilevsky and Young(2002)—to delay annuitization whenthe risk-free rate is low, despite the fact that this advice does not apply in oursetting. However, as we discuss in Section2.3, it is important to control forvariation in economic conditions and investor sentiment that may lead retireesto prefer a lump sum, despite the lower interest rates.

We learn three things when we control for the return on the S&P 500 indexover the prior twelve months, the level of VIX in the prior month, and theinflation-adjusted level of NASDAQ in the prior month. First, the coefficient

19

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

TheReview of Financial Studies / v 00 n 0 2012

on our measure of PERS generosity falls by approximately 60% betweenColumns (1) and (4), highlighting the need to control for variation in economicconditions and investor sentiment. Second, the coefficient nevertheless remainspositive and statistically significant at the 1% level in Columns (2) through(4) and at the 10% level when we switch from levels to first differences inColumn (5). It also remains positive and statistically significant at the 1%level in an unreported regression that ends the sample in December 1998 toexclude the NASDAQ crash. In other words, regardless of how we control foreconomic conditions and investor sentiment, we find no evidence that retireesunderstand that lower interest rates increase the value of PERS life annuitypayments.17

Thethird insight is that economic conditions and investor sentiment help toexplain demand for the lump sum option. We find some evidence that demandfor the lump sum option is increasing in both the level of VIX and the inflation-adjusted level of NASDAQ in the month immediately before the payout choice.However, the estimated coefficient on VIX is not statistically significant whenwe control for the level of NASDAQ. Our most robust finding is that demandfor the lump sum option rises with recent equity market returns (p-value of.001). In terms of economic significance, a one-standard-deviation increasein the lagged return on the S&P 500 index is associated with a 2.2 to 2.6percentage point increase in the demand for the lump sum option. The mostprovocative interpretation of this correlation is that retirees are extrapolatingfuture equity market returns from recent equity market returns and then usingthe lump sum payment to chase recent equity market returns.18

4.2 Predicting individual demand for the lump sum optionWe now turn our attention to individual-level retirement payout choices. InTable5, we report marginal effects from five logit models, where the dependentvariable equals one if retireek chooses the lump sum option and zero ifshe chooses the total life annuity option. We use three sets of independentvariables to explain the individual payout choices of 31,809 retirees.19 Thefirst set measures differences in retiree characteristics, including differences inlife expectancy, risk aversion, and the level of life annuity income under thelump sum option. The second set measures variation in the money’s worth of

17 In an unreported specification, we include the fraction of retirees who chose the lump sum payment in theprevious month, as a control for the impact of economic conditions and investor sentiment in the prior month,as well as the P/E ratio on the S&P 500 index in the prior quarter. The coefficient on our measure of PERSgenerosity increases from 0.111, in Column (4), to 0.137 and remains statistically significant from zero at the1% level.

18 The return chasing interpretation is consistent with behavior thatChevalier and Ellison(1997) andSirri andTufano (1998) observe in the mutual fund industry and thatBenartzi (2001) observes when studying howinvestors allocate 401(k) plan assets to company stock.

19 In Table5, we exclude 251 retirees, because we lack data on the location of their most recent employer. Withoutthese data, we are unable to control for the local unemployment rate. Our inferences are unchanged when weinclude these retirees and drop our control for the local unemployment rate.

20

at Acquisition D

ept Serials on April 10, 2012

http://rfs.oxfordjournals.org/D

ownloaded from

HowDo Retirees Value Life Annuities? Evidence from Public Employees