Embed Size (px)

Citation preview

HOW DO WE IMPROVE SCOTLAND’S CONNECTIVITY IN A GLOBAL MARKET?

Alf Baird

Head, Maritime Research Group

Napier Transport Research Institute

Globalization

• Division of labour = globalization• Ongoing relocation of manufacturing from US and

W. Europe to China• Worldwide economic growth:

• Increase in average incomes• Reduced cycle time for innovations• Decrease in unit prices of consumer goods• State-of-the-art buying behaviour• “Throw-away & buy-new” instead of repair• China boom

• Dramatic increases in global freight volumes

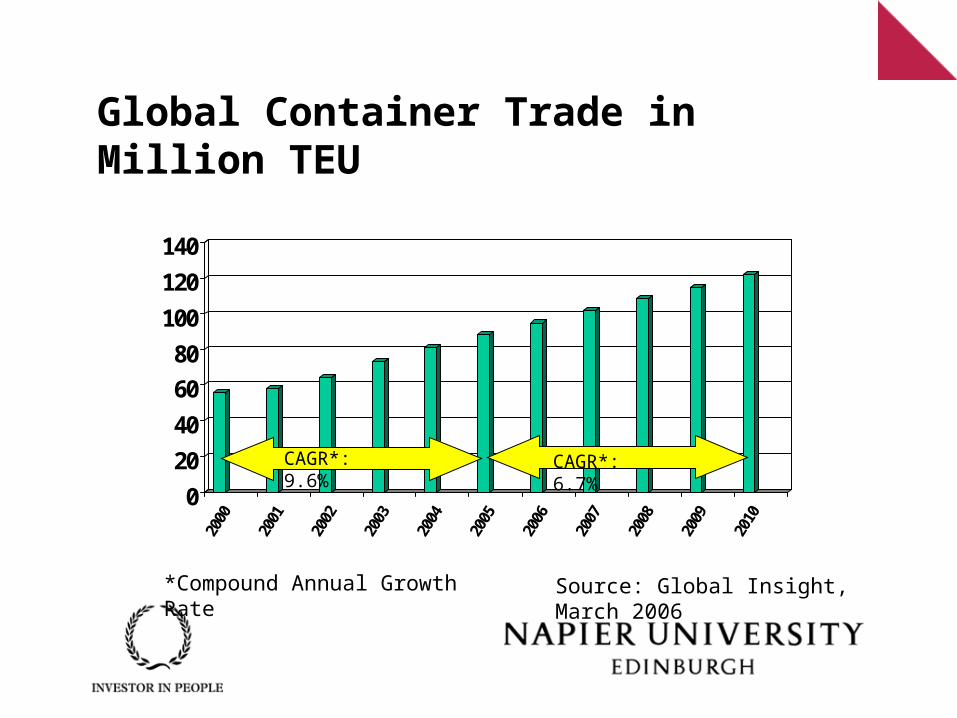

Global Container Trade in Million TEU

0

20

40

60

80

100

120

140

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

*Compound Annual Growth Rate Source: Global Insight, March 2006

CAGR*: 9.6% CAGR*: 6.7%

Critical Enablers of Globalization

• IT• Convergence of consumer tastes• Liberalisation of financial markets• Jet aviation travel• Containerisation of world trade

(Source: Cafruny, 1987)

“The scale of worldwide multinational activity today would be unthinkable without the benefits brought about by containerisation, and its impact on

world trade”(Source: Dicken, 1992)

GLOBALIZATION DEPENDS ON TWO TRANSPORT MODES!

Scotland’s Global Connectivity

• Scotland is a small economy, with limited population• On the edge of Europe• Few direct transport services• Majority of liner shipping and air services are via distant hubs• Scotland’s factor advantages are diminishing• Foreign Direct Investment (FDI) is reducing (fast)

• What is Scotland’s future competitive advantage?• What can Scotland do to compete globally?• Are there transport hub opportunities?

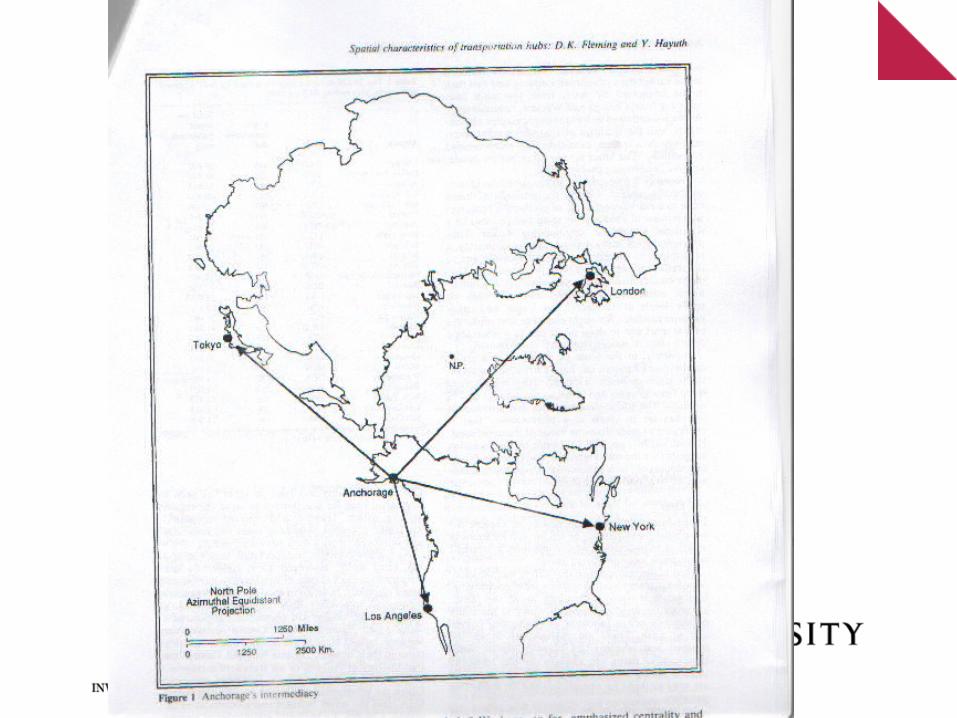

Theory of Centrality & Intermediacy(Source: Fleming & Hayuth, 1994)

• Hub Centrality– Hub capitalises on large local market– Market centre is foci of transport activity– Centrality can be induced (manufactured)

• Hub Intermediacy– Locations between important origins and destinations– Usually at a strategic intersection point– Importance of accessibility and proximity– Hub acquires spacial quality via transport function

• CAN SCOTLAND BECOME AN INTERMEDIATE HUB?

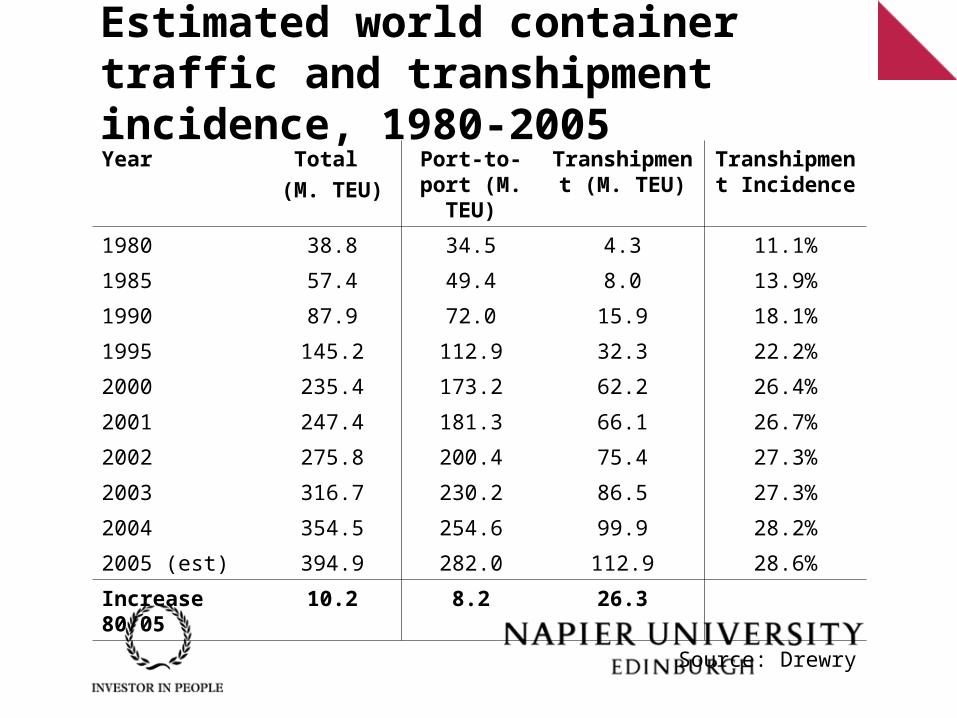

Estimated world container traffic and transhipment incidence, 1980-2005Year Total

(M. TEU)

Port-to-port (M. TEU)

Transhipment (M. TEU)

Transhipment Incidence

1980 38.8 34.5 4.3 11.1%

1985 57.4 49.4 8.0 13.9%

1990 87.9 72.0 15.9 18.1%

1995 145.2 112.9 32.3 22.2%

2000 235.4 173.2 62.2 26.4%

2001 247.4 181.3 66.1 26.7%

2002 275.8 200.4 75.4 27.3%

2003 316.7 230.2 86.5 27.3%

2004 354.5 254.6 99.9 28.2%

2005 (est) 394.9 282.0 112.9 28.6%

Increase 80/05 10.2 8.2 26.3

Source: Drewry

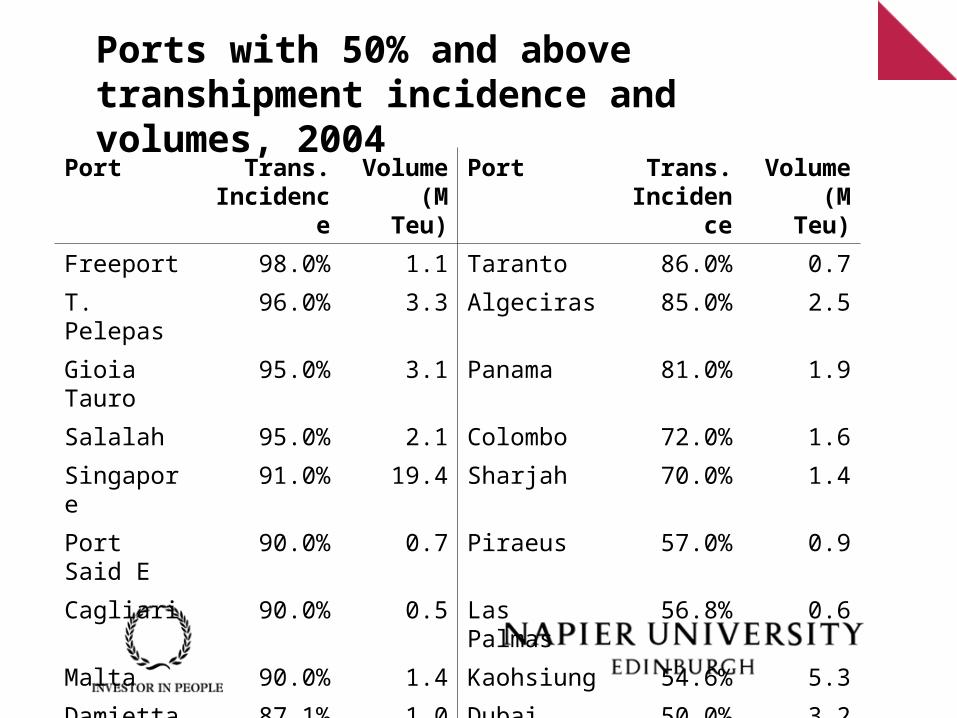

Ports with 50% and above transhipment incidence and volumes, 2004

Port Trans. Incidence

Volume (M Teu)

Port Trans. Incidence

Volume (M Teu)

Freeport 98.0% 1.1 Taranto 86.0% 0.7

T. Pelepas 96.0% 3.3 Algeciras 85.0% 2.5

Gioia Tauro 95.0% 3.1 Panama 81.0% 1.9

Salalah 95.0% 2.1 Colombo 72.0% 1.6

Singapore 91.0% 19.4 Sharjah 70.0% 1.4

Port Said E 90.0% 0.7 Piraeus 57.0% 0.9

Cagliari 90.0% 0.5 Las Palmas 56.8% 0.6

Malta 90.0% 1.4 Kaohsiung 54.6% 5.3

Damietta 87.1% 1.0 Dubai 50.0% 3.2

Kingston 86.0% 1.0 Port Klang 50.0% 2.6

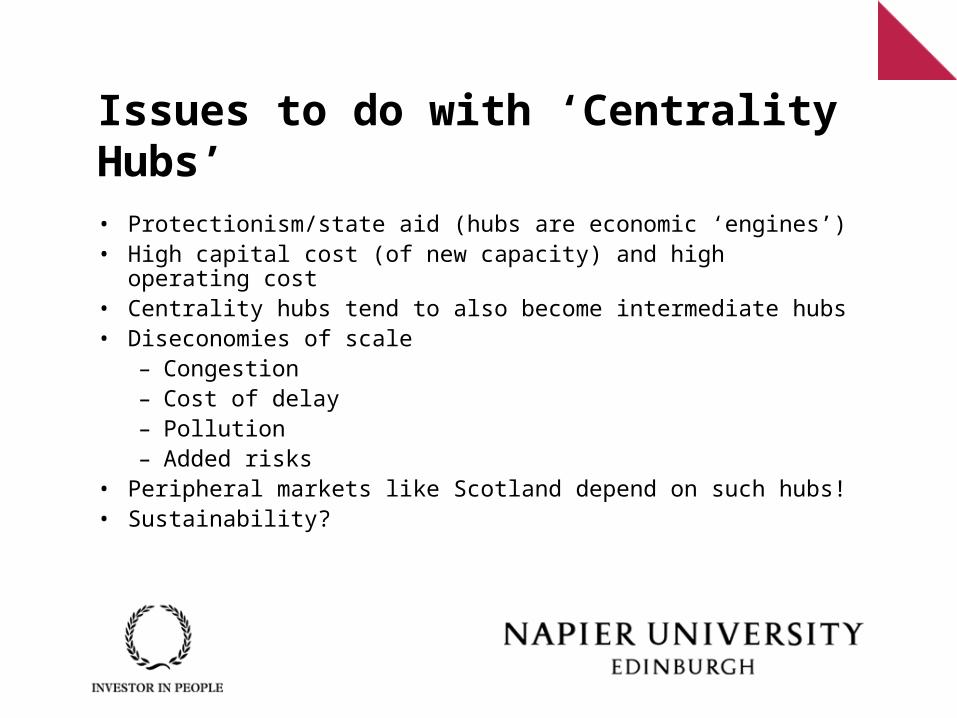

Issues to do with ‘Centrality Hubs’

• Protectionism/state aid (hubs are economic ‘engines’)• High capital cost (of new capacity) and high operating cost• Centrality hubs tend to also become intermediate hubs• Diseconomies of scale

– Congestion– Cost of delay– Pollution– Added risks

• Peripheral markets like Scotland depend on such hubs!• Sustainability?

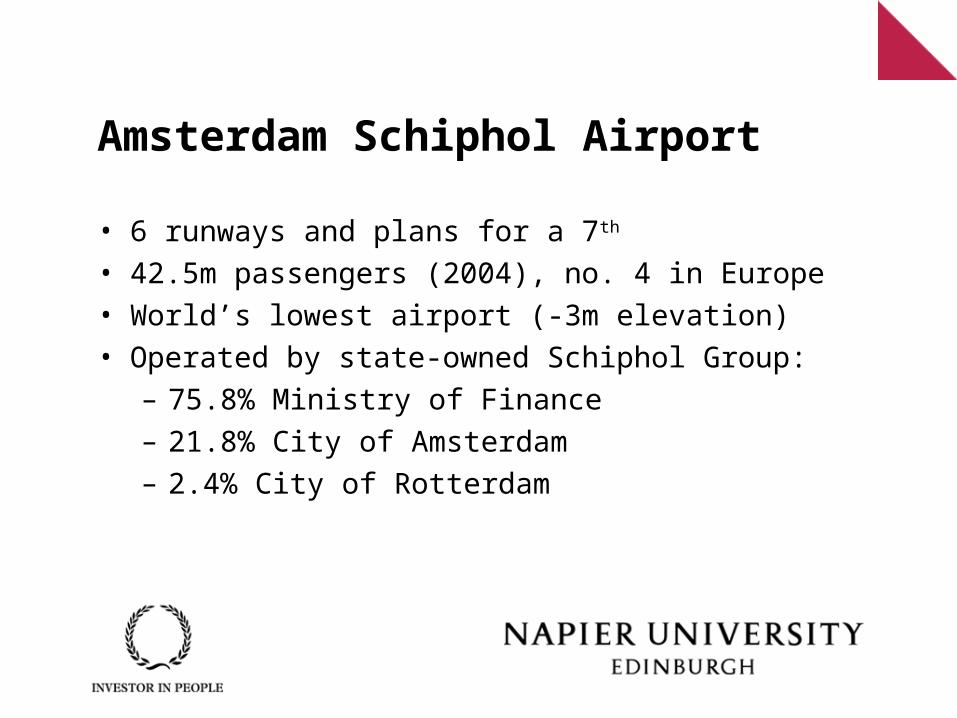

Amsterdam Schiphol Airport

• 6 runways and plans for a 7th

• 42.5m passengers (2004), no. 4 in Europe• World’s lowest airport (-3m elevation)• Operated by state-owned Schiphol Group:

– 75.8% Ministry of Finance– 21.8% City of Amsterdam– 2.4% City of Rotterdam

North European container terminal developments

JaderWeserPort

Bremerhaven

Hamburg

Zeebrugge

Antwerp

Amsterdam

Rotterdam Flushing

Felixstowe Bathside Bay

London Gateway

Southampton

Le Havre

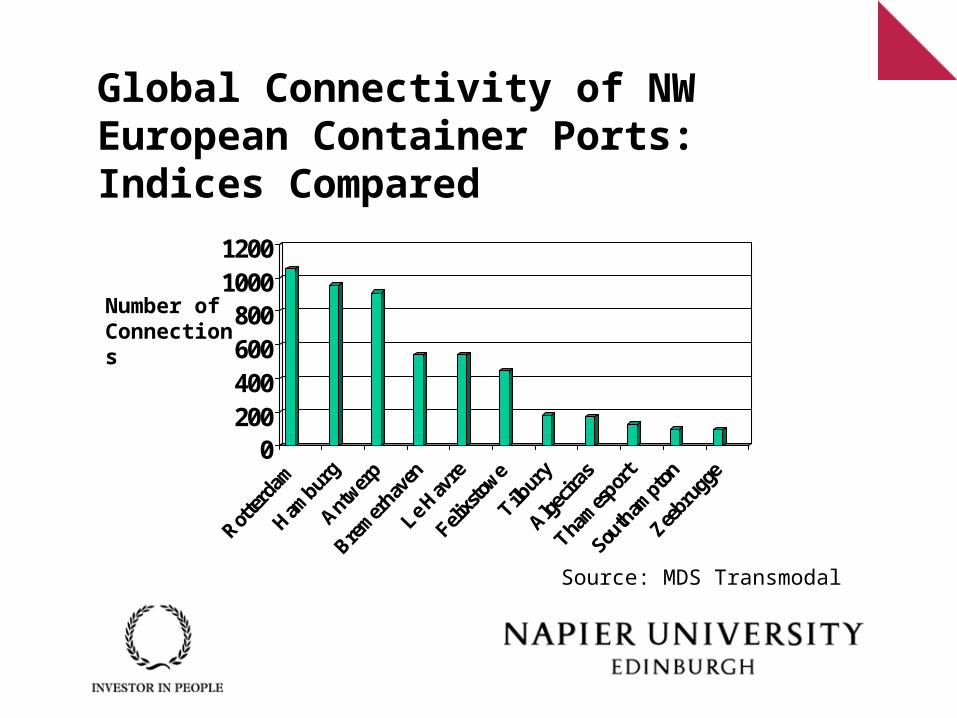

Global Connectivity of NW European Container Ports: Indices Compared

0200400600800

10001200

Source: MDS Transmodal

Number of Connections

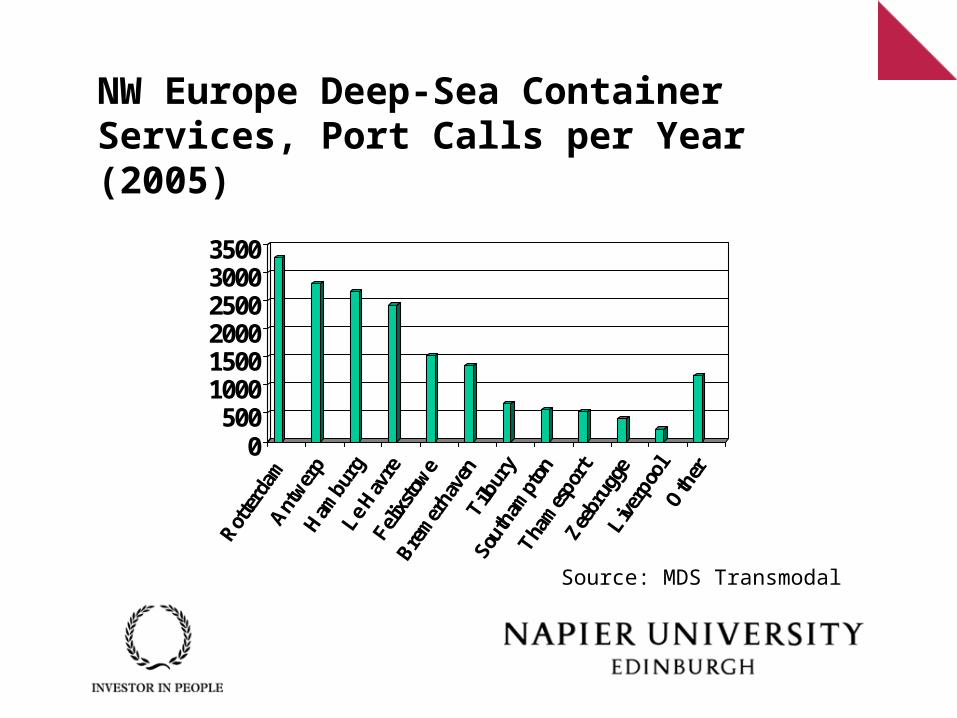

NW Europe Deep-Sea Container Services, Port Calls per Year (2005)

0500

100015002000250030003500

Source: MDS Transmodal

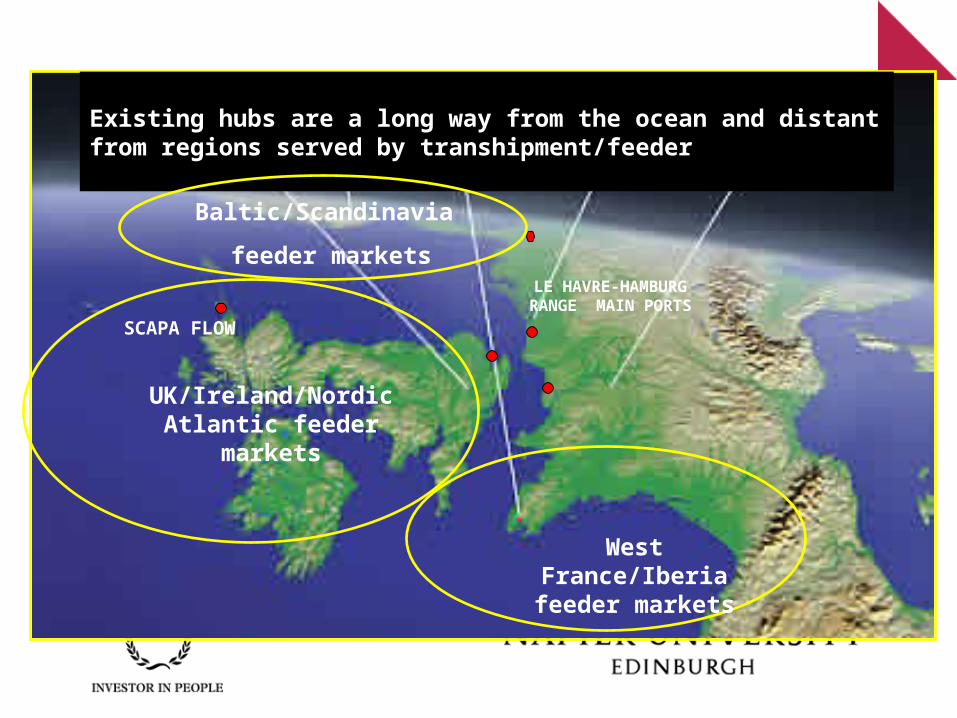

SCAPA FLOW

LE HAVRE-HAMBURG RANGE MAIN PORTS

Existing hubs are a long way from the ocean and distant from regions served by transhipment/feeder

West France/Iberia feeder markets

UK/Ireland/Nordic Atlantic feeder markets

Baltic/Scandinavia

feeder markets

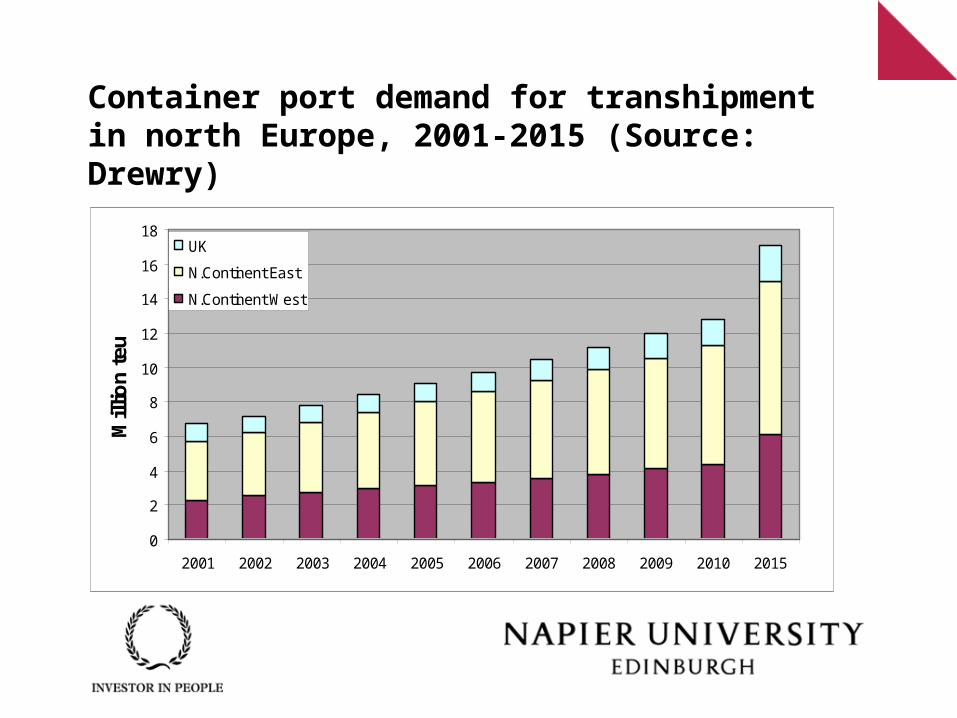

Container port demand for transhipment in north Europe, 2001-2015 (Source: Drewry)

0

2

4

6

8

10

12

14

16

18

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2015

Mill

ion

teu

UK

N.Continent East

N.Continent West

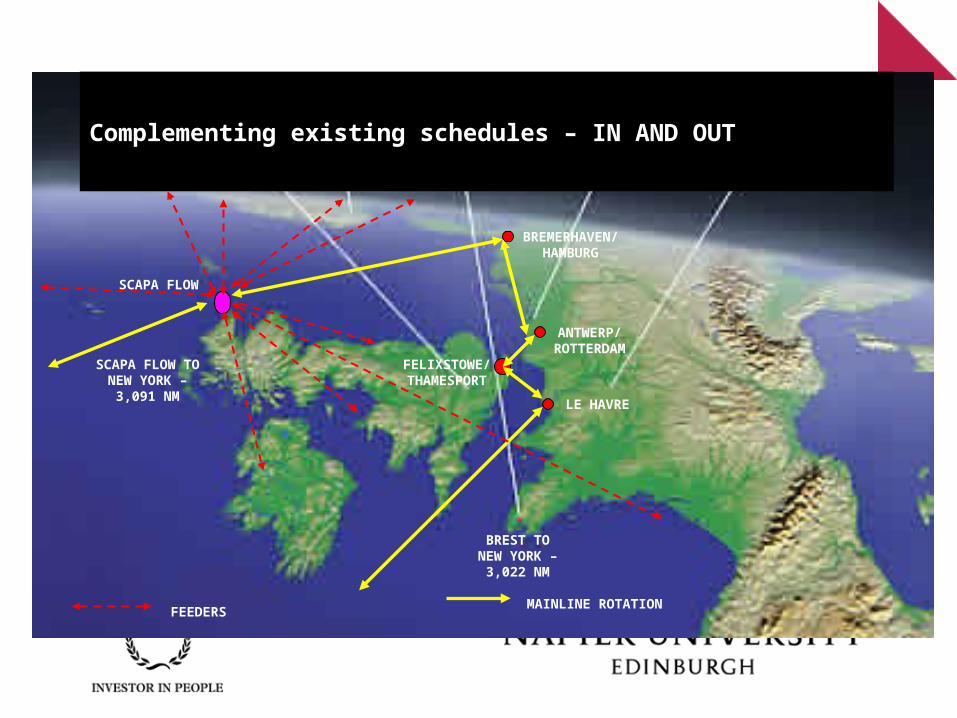

SCAPA FLOW

ANTWERP/ROTTERDAM

FELIXSTOWE/THAMESPORT

Complementing existing schedules – IN AND OUT

BREMERHAVEN/HAMBURG

LE HAVRE

FEEDERSMAINLINE ROTATION

SCAPA FLOW TO NEW YORK –

3,091 NM

BREST TO NEW YORK –

3,022 NM

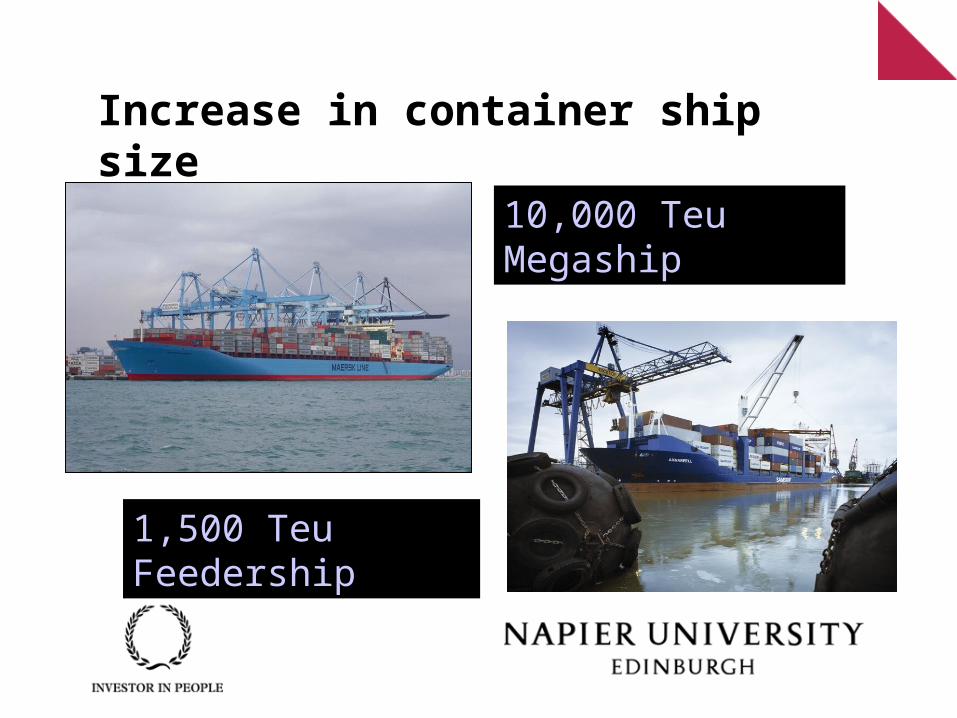

Increase in container ship size

10,000 Teu Megaship

1,500 Teu Feedership

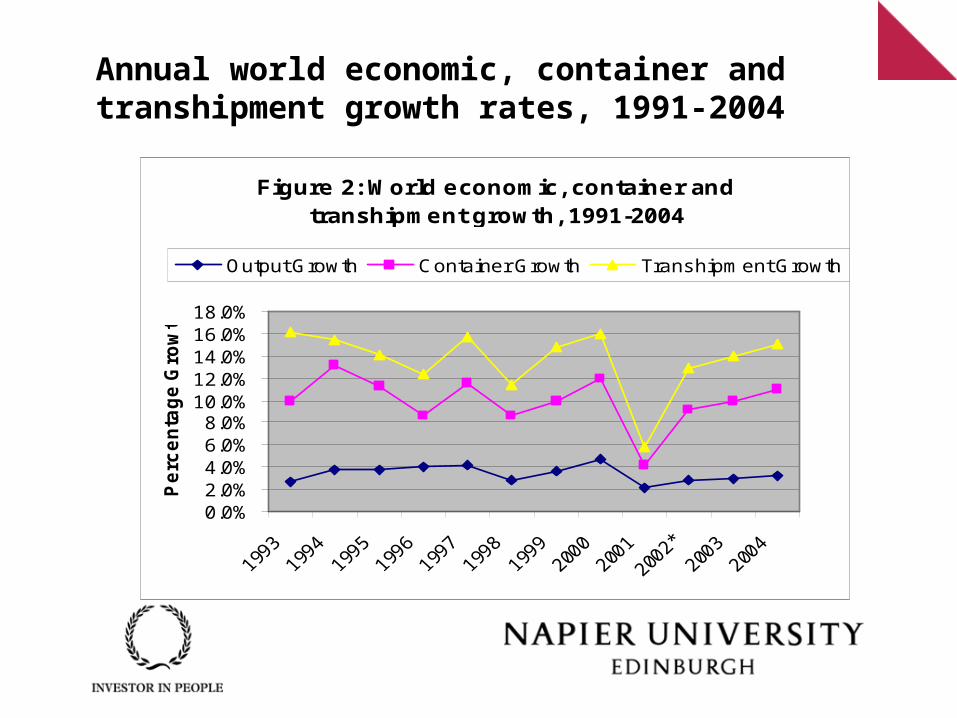

Annual world economic, container and transhipment growth rates, 1991-2004

Figure 2: World economic, container and transhipment growth, 1991-2004

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%

Pe

rce

nta

ge

Gro

wth

Output Growth Container Growth Transhipment Growth

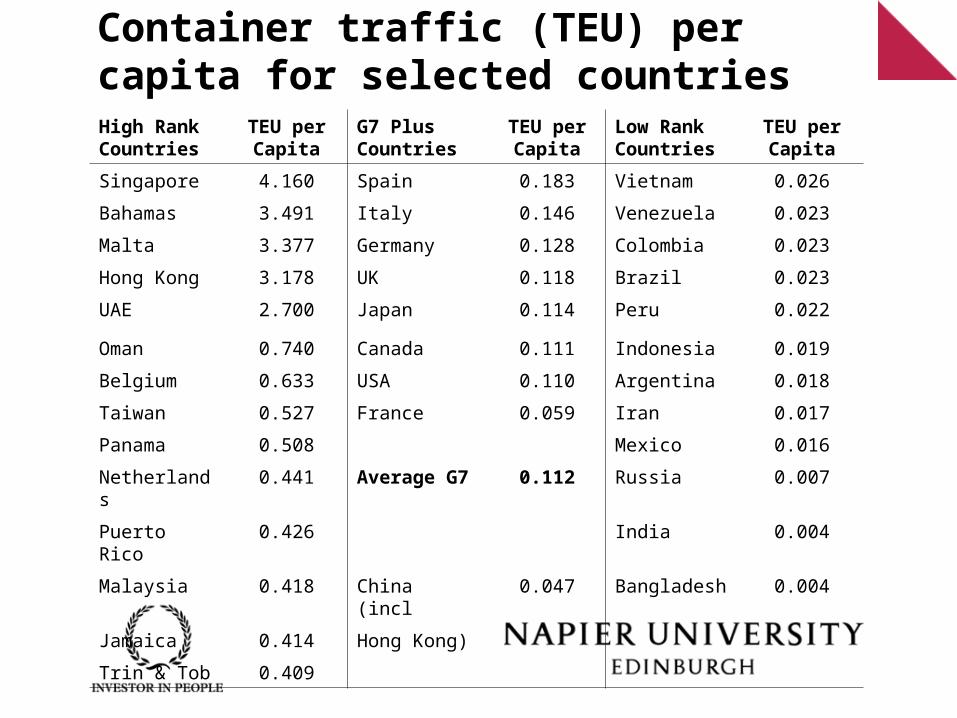

Container traffic (TEU) per capita for selected countriesHigh Rank Countries

TEU per Capita

G7 Plus Countries

TEU per Capita

Low Rank Countries

TEU per Capita

Singapore 4.160 Spain 0.183 Vietnam 0.026

Bahamas 3.491 Italy 0.146 Venezuela 0.023

Malta 3.377 Germany 0.128 Colombia 0.023

Hong Kong 3.178 UK 0.118 Brazil 0.023

UAE 2.700 Japan 0.114 Peru 0.022

Oman 0.740 Canada 0.111 Indonesia 0.019

Belgium 0.633 USA 0.110 Argentina 0.018

Taiwan 0.527 France 0.059 Iran 0.017

Panama 0.508 Mexico 0.016

Netherlands 0.441 Average G7 0.112 Russia 0.007

Puerto Rico 0.426 India 0.004

Malaysia 0.418 China (incl 0.047 Bangladesh 0.004

Jamaica 0.414 Hong Kong)

Trin & Tob 0.409

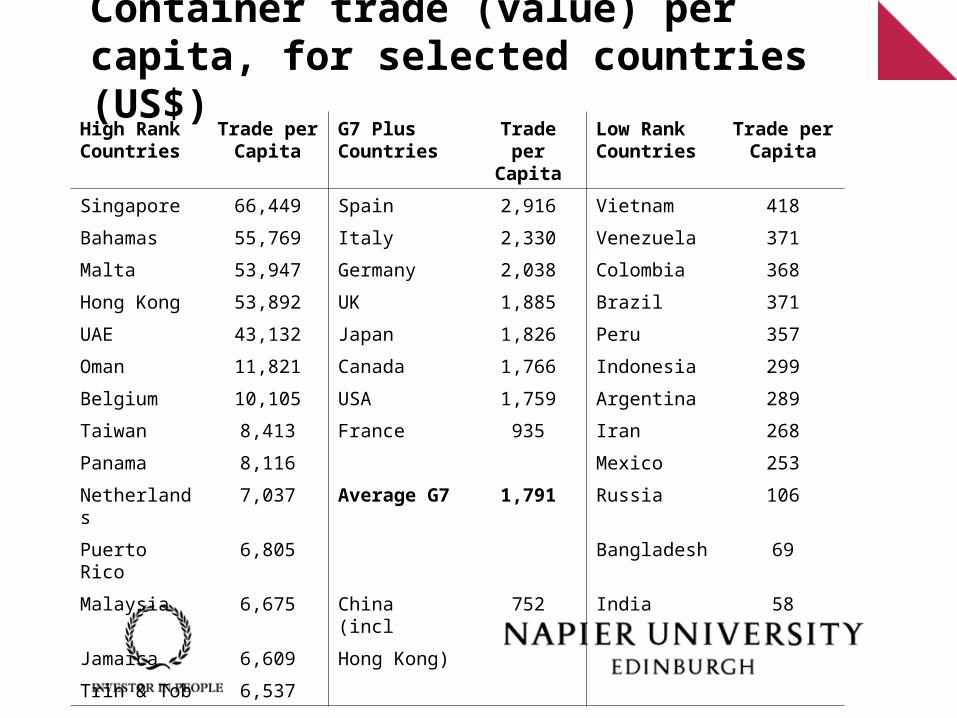

Container trade (value) per capita, for selected countries (US$)

High Rank Countries

Trade per Capita

G7 Plus Countries

Trade per Capita

Low Rank Countries

Trade per Capita

Singapore 66,449 Spain 2,916 Vietnam 418

Bahamas 55,769 Italy 2,330 Venezuela 371

Malta 53,947 Germany 2,038 Colombia 368

Hong Kong 53,892 UK 1,885 Brazil 371

UAE 43,132 Japan 1,826 Peru 357

Oman 11,821 Canada 1,766 Indonesia 299

Belgium 10,105 USA 1,759 Argentina 289

Taiwan 8,413 France 935 Iran 268

Panama 8,116 Mexico 253

Netherlands 7,037 Average G7 1,791 Russia 106

Puerto Rico 6,805 Bangladesh 69

Malaysia 6,675 China (incl 752 India 58

Jamaica 6,609 Hong Kong)

Trin & Tob 6,537

Can Scotland become a global logistics hub in Europe?

Summary

• Scotland has no real global competitive advantage• Could transhipment hubs provide that advantage?• Transhipment hubs intercept trade:

– Moderate scale hub could double Scottish trade– Creates direct services for host nation– Provides value added/logistics opportunities– Acts as lever for FDI– Strengthens indigenous industry

• Is this a strategy Scotland should pursue to improve global connectivity and competitiveness?

Thank You

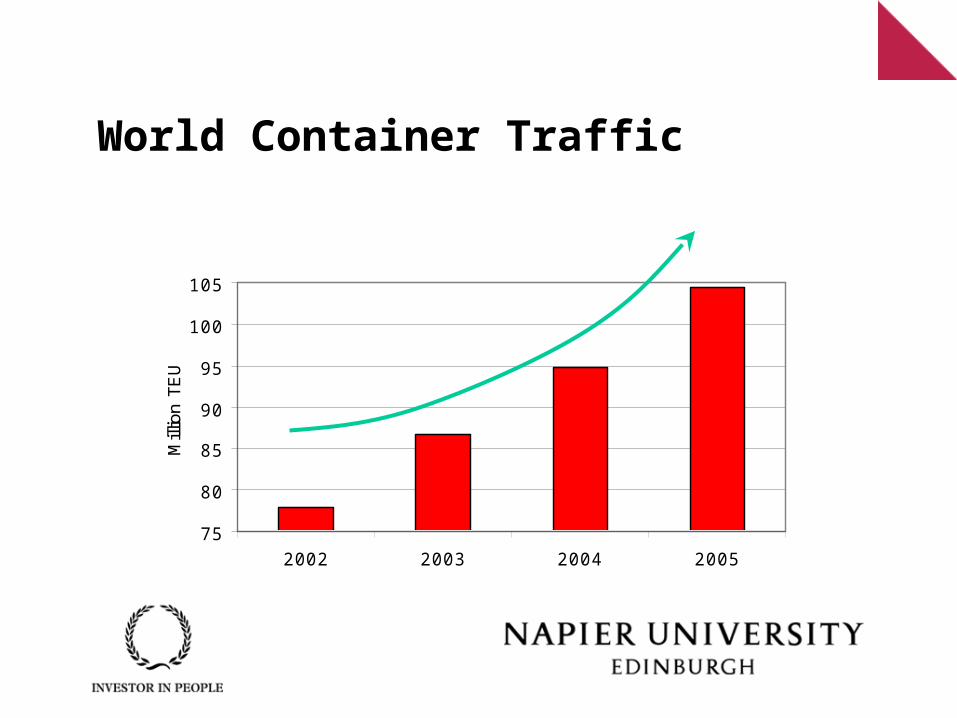

World Container Traffic

75

80

85

90

95

100

105

2002 2003 2004 2005

Mill

ion

TE

U

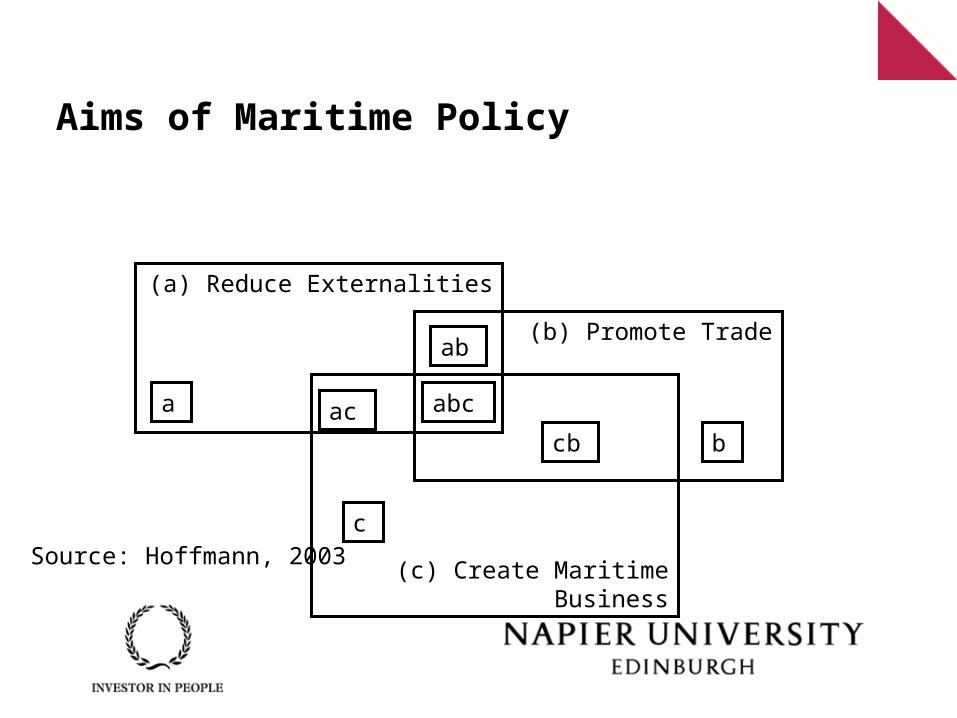

Aims of Maritime Policy

(a) Reduce Externalities

(b) Promote Trade

(c) Create Maritime Business

a ac

c

abc

cb b

ab

Source: Hoffmann, 2003

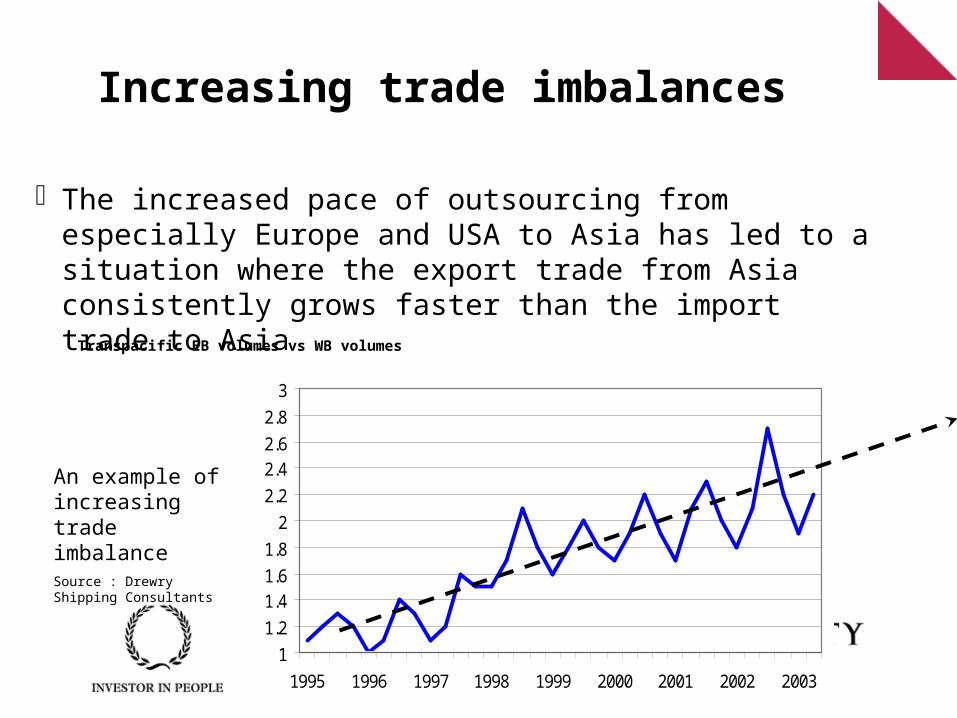

Increasing trade imbalances

The increased pace of outsourcing from especially Europe and USA to Asia has led to a situation where the export trade from Asia consistently grows faster than the import trade to Asia

Transpacific EB volumes vs WB volumes

An example of increasing trade imbalance Source : Drewry Shipping Consultants

1

1.2

1.41.6

1.8

2

2.2

2.42.6

2.8

3

1995 1996 1997 1998 1999 2000 2001 2002 2003

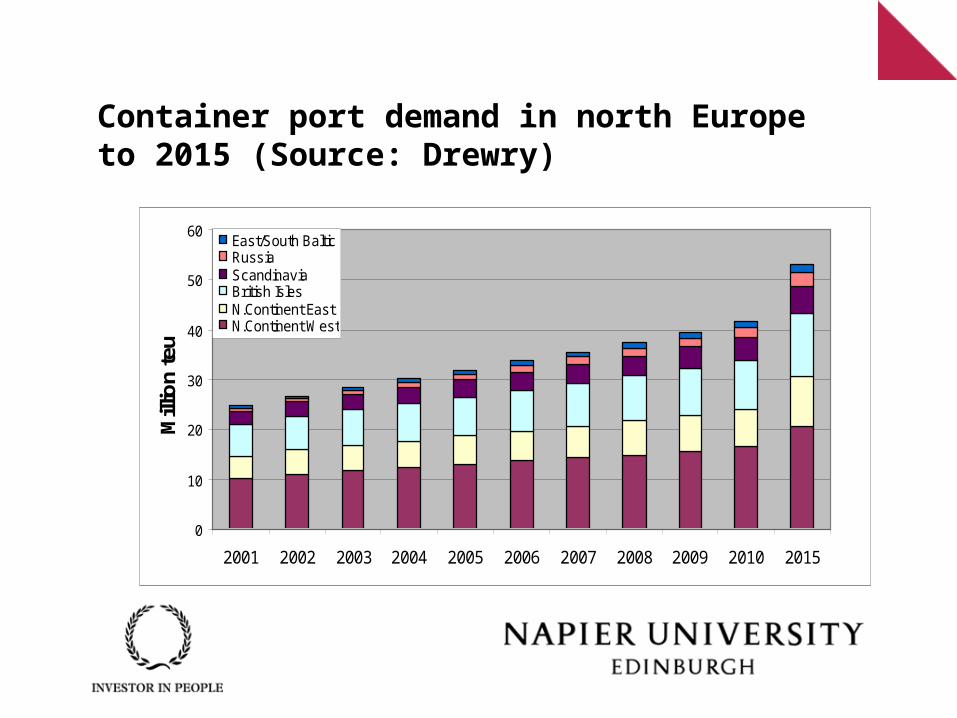

Container port demand in north Europe to 2015 (Source: Drewry)

0

10

20

30

40

50

60

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2015

Mill

ion

teu

East/South BalticRussiaScandinaviaBritish IslesN.Continent EastN.Continent West