Embed Size (px)

Citation preview

How to CreateHow to CreateA Performance BudgetA Performance Budget

and How to Use Itand How to Use It

Justine Farr RodriguezJustine Farr Rodriguez

American Association for American Association for Budget and Program AnalysisBudget and Program Analysis

May 2, 2002May 2, 2002

A Budget for Better OutcomesA Budget for Better Outcomes

• The objective of a performance budget is The objective of a performance budget is to achieve outcomes that the public wants:to achieve outcomes that the public wants:

– Children who can read,– Air that is clean,– Streets that are safe,– An economy that provides jobs,– A nation that is secure.

• The federal government can influence The federal government can influence such outcomes, but not control them.such outcomes, but not control them.

How Do We Influence Outcomes?How Do We Influence Outcomes?• The government influences outcomes by The government influences outcomes by

its outputs and activities, such as:its outputs and activities, such as:– Providing grants to certain entities for

specified purposes;– Making transfers to eligible individuals;– Making and guaranteeing loans;– Enforcing laws and regulations; and– Producing goods and services.

• The characteristics of these outputs affect The characteristics of these outputs affect their success in influencing outcomes. their success in influencing outcomes.

Tools That Affect CharacteristicsTools That Affect Characteristics

Criteria in LawCriteria in Law

EducationEducation Information Information

InterpretationsInterpretations Outreach and Outreach andin Regulationsin Regulations Screening Screening

Incentives forIncentives for Awards for Awards for AchievementAchievement Best Practices Best Practices

Technical Technical Customized Customized AssistanceAssistance Services Services

NetworkingNetworking Research Research

Budget for Outputs Budget for Outputs JustifiedJustified by by Their Influence on OutcomesTheir Influence on Outcomes

Inputs OutcomesBudget resources Net impacts

• Budget “obligations by program activity” can be aligned with an output or cluster of related outputs intended to influence a single outcome, so that cost can be “matched” with outputs produced.

• Outcomes, which have an unstable relationship with cost, can be explained using these outputs and their characteristics, other federal outputs, external factors, and time lags in analytical equations.

Outputs

Infrastructure for Infrastructure for a Performance Budgeta Performance Budget

Three steps lead to a performance budget.

• Align “program activities” with an output or Align “program activities” with an output or outputs intended to influence an outcome. As outputs intended to influence an outcome. As necessary, merge or alter budget accounts. (#3)necessary, merge or alter budget accounts. (#3)

– This can be done agency by agency or even by bureau.

• Charge accounts consistently with the full annual Charge accounts consistently with the full annual cost of the resources used. (#4)cost of the resources used. (#4)

– This requires government-wide legislation.

• Present strategic goals, outcomes, and the related Present strategic goals, outcomes, and the related outputs and costs in a performance budget. (#2)outputs and costs in a performance budget. (#2)

Align Program Activities and Align Program Activities and “Match” Cost With Outputs“Match” Cost With Outputs

• In budget accounts that finance programs, In budget accounts that finance programs, align each align each program activity with an output or related outputs and program activity with an output or related outputs and activities designed to influence a single outcomeactivities designed to influence a single outcome..

• Request budgetary resources for full annual cost of Request budgetary resources for full annual cost of producing these outputs and related activities.producing these outputs and related activities.

• Program activities should not align with inputs or partial processes. They should include direct operations, purchased support services, and all other costs required to provide outputs that influence an outcome.

Outputs Program activity

What About Budget Accounts?What About Budget Accounts?• Program activities can be aligned with outputs without Program activities can be aligned with outputs without

much change in budget accounts. much change in budget accounts.

• Accounts should be consolidated or modified when they Accounts should be consolidated or modified when they inhibit good management -- e.g., prevent matching full inhibit good management -- e.g., prevent matching full annual cost with outputs or create extra complexity.annual cost with outputs or create extra complexity.– Align accounts with bureaus to provide accountability

and stability. – Within bureaus, consider separate accounts for

mandatory versus discretionary funding or for programs with very different purposes.

• Provide federal support goods and services from Provide federal support goods and services from revolving funds that charge customers and are self-revolving funds that charge customers and are self-sustaining by line of business.sustaining by line of business.

Charge Resources to the Place Charge Resources to the Place Where They Are UsedWhere They Are Used

All resources are financed in the budget, but not All resources are financed in the budget, but not consistently where they are used.consistently where they are used.

– Some are financed centrally by the agency or Treasury, or cross-subsidized by other programs.

Budgeting and managing would be more effective if:Budgeting and managing would be more effective if: – Appropriations were made where resources are used;

– Salaries, grants, transfers, credit subsidies, and other costs were charged to programs;

– Support goods and services were finance via revolving funds;

– Pairs of accounts were used to charge the annual cost of retiree

benefits, cleanup, and capital use to programs.

Separate Mission and Separate Mission and Support AccountsSupport Accounts

Mission accountsMission accounts

Get appropriations for:

Executive direction (policy and oversight)

IG

Programs for the public:Direct operationsGrants and transfers

Credit and insuranceRegulation

-------------------------------Agency operating cost

Support accountsSupport accounts

Support revolving funds: paid by customers, self sustaining over operating cycle.

Retiree benefit funds: get accruing cost, amortization of unfunded liability.

Clean up funds: get accruing cost, appropriations for unfunded liability.

Capital acquisition funds: get borrowing authority, repay Treasury with usage charges.

Map Outputs to Outcomes, GoalsMap Outputs to Outcomes, Goals

Output 1 A a

Output 1 A b

Outcom e 1 A

Output 1 B a

Outcom e 1 B

Output 1 C a

Output 1 C b

Outcom e 1 C

Strategic Goal # 1

Strategic plan and organization:

Are aligned Not aligned

Bureau A Bureau A

Bureau A Bureau D

Bureau B Bureau C

Bureau C Bureau B

Bureau C Bureau C

How to Implement Full Cost (1)How to Implement Full Cost (1)

Executive directionIgStrategic goal I

OutcomeProgram activitiesProgram activities

OutcomeProgram activities

Strategic goal 2Outcome

Program activities----------------------Support revolving fund(s)Capital acquisition fund

(After bill enactment)

Program costsProgram costs

• Estimate the cost of grants, transfers, credit subsidies, and other program benefits that would be paid by each program activity.

• Request BA to cover these costs in “the right place” as soon as program activities are aligned.

BA

How to Implement Full Cost (2)How to Implement Full Cost (2)

Executive directionIgStrategic goal I

OutcomeProgram activitiesProgram activities

OutcomeProgram activities

Strategic goal 2Outcome

Program activities----------------------Support revolving fund(s)Capital acquisition fund

(After bill enactment)

Salaries and expensesSalaries and expenses • Estimate the cost of

salaries and expenses used for executive direction, the IG, and each program activity.

• Add the employer share of accruing retiree costs.

• Request BA to cover these costs in “the right place” when program activities are aligned.

BA

How to Implement Full Cost (3)How to Implement Full Cost (3)

Executive directionIgStrategic goal I

OutcomeProgram activitiesProgram activities

OutcomeProgram activities

Strategic goal 2Outcome

Program activities----------------------Support revolving fund(s)Capital acquisition fund

(After bill enactment)

Support goods, servicesSupport goods, services

• Estimate the cost of support goods and services used for executive direction, the IG, and each program activity.

• Allow for the cost of support goods and services used but not now charged for.

• Request BA to cover these costs in “the right place” as soon as program activities are aligned.

BA

How to Implement Full Cost (4)How to Implement Full Cost (4)

Executive directionIgStrategic goal I

OutcomeProgram activitiesProgram activities

OutcomeProgram activities

Strategic goal 2Outcome

Program activities----------------------Support revolving fund(s)Capital acquisition fund (Gets borrowing authority to implement second bill)

Capital and cleanupCapital and cleanup

• Prepare asset registers.

• Establish capital acquisition funds and levy capital asset user charges to implement second bill.

• Estimate accruing cleanup cost, establish fund.

• Request BA to cover these costs in “the right place” at implementation of second bill.

BA

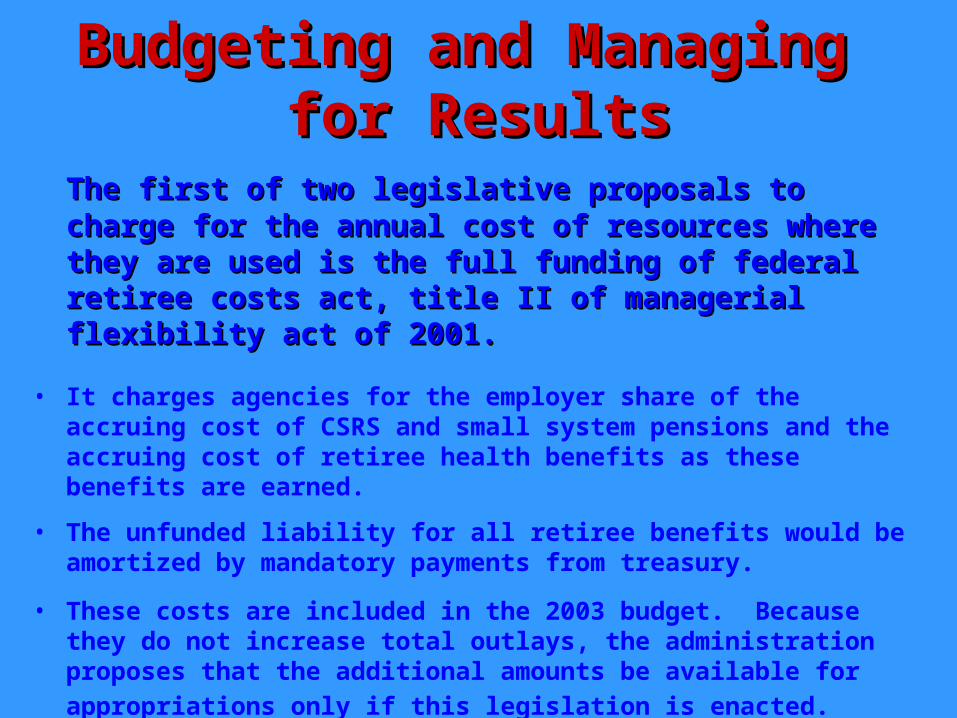

Budgeting and Managing Budgeting and Managing for Resultsfor Results

The first of two legislative proposals to charge for the The first of two legislative proposals to charge for the annual cost of resources where they are used is the full annual cost of resources where they are used is the full funding of federal retiree costs act, title II of managerial funding of federal retiree costs act, title II of managerial flexibility act of 2001.flexibility act of 2001.

• It charges agencies for the employer share of the accruing cost of CSRS and small system pensions and the accruing cost of retiree health benefits as these benefits are earned.

• The unfunded liability for all retiree benefits would be amortized by mandatory payments from treasury.

• These costs are included in the 2003 budget. Because they do not increase total outlays, the administration proposes that the additional amounts be available for appropriations only if this

legislation is enacted.

• Appropriations would be made to budget accounts that fund programs for the public and executive direction of the agency.

• Support goods and services would be in revolving funds sustained by payments from their customers.

• Accruing costs to clean up hazardous substances generated by agency operations would be paid to a cleanup fund.

• And capital acquisition funds would be created that would request up-front budget authority to acquire assets, receive that in the form of authority to borrow from Treasury, and charge asset users for their share of the “mortgage payments.”

The second legislative proposal to charge for costs where The second legislative proposal to charge for costs where they are used is The Budgetary Cost and Performance they are used is The Budgetary Cost and Performance Integration Act of 2002.Integration Act of 2002.

Budgeting and Managing Budgeting and Managing for Resultsfor Results

• A good performance budget integrates past and future A good performance budget integrates past and future performance with resources in streamlined presentation. performance with resources in streamlined presentation.

• It is organized around the agency’s strategic goals and It is organized around the agency’s strategic goals and the outcomes the agency aspires to influence.the outcomes the agency aspires to influence.

• Under each it shows which program activities (outputs Under each it shows which program activities (outputs and cost) contribute to achieving these outcomes.and cost) contribute to achieving these outcomes.

– For some agencies, presentation by goal, outcome, and outputs will find the contributing bureaus quite well aligned.

– For other agencies, bureaus contribute to so many goals that the performance budget will need a supplementary table by organization.

Creating a Performance BudgetCreating a Performance Budget

Present AccomplishmentsPresent Accomplishments• Request the agency’s budget in terms of its strategic Request the agency’s budget in terms of its strategic

goals and the outcomes it aspires to influence.goals and the outcomes it aspires to influence.

• Build on its results from prior years, analyzing Build on its results from prior years, analyzing differences in outputs, effectiveness, and external differences in outputs, effectiveness, and external factors from last year’s expectations. factors from last year’s expectations.

– Explain how effective the different outputs are in influencing the outcome, how they are balanced and coordinated to achieve the best effect, and how efficiently they are produced.

– Explain any external factors or time lags which affect the relationship between the aggregate cost of the relevant outputs and the outcome.

Allocate Resources for ResultsAllocate Resources for Results

• Allocate resources to programs that can document Allocate resources to programs that can document their effectiveness or at least that show more their effectiveness or at least that show more effectiveness than similar programs. effectiveness than similar programs.

• Propose incentives or targets to encourage programs Propose incentives or targets to encourage programs to increase their effectiveness.to increase their effectiveness.

• When programs are ineffective, explain and justify When programs are ineffective, explain and justify proposed reform in relation to the importance of the proposed reform in relation to the importance of the goal and evidence why the reform is likely to work.goal and evidence why the reform is likely to work.

• Alternatively, shift resources to more effective Alternatively, shift resources to more effective

programs or higher priority outcomes.programs or higher priority outcomes.

Support Good ManagementSupport Good Management• This is a:This is a:

– Program activity?Program activity?– Staff unit?Staff unit?– Cost center?Cost center?– All of the above?All of the above?

• This is a staff unit producing outputs to influence a single outcome, financed by a program activity sub-account in the budget, and using a cost center for financial analysis and reporting.

Manage for ResultsManage for Results

• Monitor costs, outputs, performance Monitor costs, outputs, performance measures, outcomes, and analytical ratios.measures, outcomes, and analytical ratios.

• Hold regular meetings of managers of Hold regular meetings of managers of program activities influencing each outcome.program activities influencing each outcome.

– Where these are in multiple bureaus, designate a lead manager to be accountable for coordinating the agency’s influence on that outcome.

• Quarterly, review the monitoring and Quarterly, review the monitoring and coordination of efficiency and effectiveness.coordination of efficiency and effectiveness.– Consider whether new analyses or policy options

are required to keep results on track.

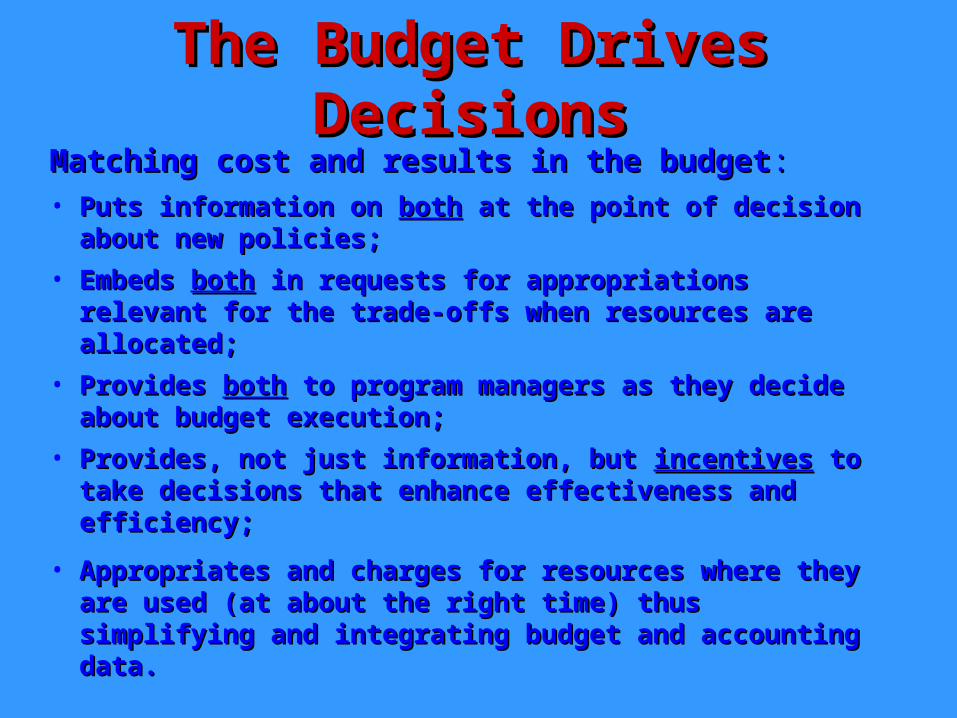

The Budget Drives DecisionsThe Budget Drives DecisionsMatching cost and results in the budgetMatching cost and results in the budget::• Puts information on Puts information on bothboth at the point of decision at the point of decision

about new policies;about new policies;

• Embeds Embeds bothboth in requests for appropriations relevant in requests for appropriations relevant for the trade-offs when resources are allocated; for the trade-offs when resources are allocated;

• Provides Provides bothboth to program managers as they decide to program managers as they decide about budget execution;about budget execution;

• Provides, not just information, but Provides, not just information, but incentivesincentives to take to take decisions that enhance effectiveness and efficiency; decisions that enhance effectiveness and efficiency;

• Appropriates and charges for resources where they Appropriates and charges for resources where they are used (at about the right time) thus simplifying are used (at about the right time) thus simplifying and integrating budget and accounting data.and integrating budget and accounting data.

Use It to Budget and Manage Use It to Budget and Manage for Resultsfor Results

• Highlight the agency’s mission and accomplishments.Highlight the agency’s mission and accomplishments.

• Shift resources to more effective programs.Shift resources to more effective programs.

• Align funding and staff to support good management.Align funding and staff to support good management.

• Coordinate activities to influence outcomes.Coordinate activities to influence outcomes.

• Integrate and use budget, performance, and accounting Integrate and use budget, performance, and accounting information to budget and manage.information to budget and manage.

• Illuminate the ways in which a performance budget can Illuminate the ways in which a performance budget can

achieve better outcomes for Americans. achieve better outcomes for Americans.