Embed Size (px)

Citation preview

Brussels, March 15, 2012

Wim Boonstra

Chief Economist,Rabobank, UtrechtPresident of the Monetary Commission of ELEC, Brussels

How to stabilize EMU using conditional Eurobonds

The ELEC temporary Euro T-Bill facility

Contents

• What are Eurobonds?

• Why are Eurobonds useful?

• The ELEC T-Bill proposal

• Advantages

• Disadvantages

• Conclusions

Definitions

• Eurobonds (EMU Bonds, stability bonds) are bonds that are issuedby a newly established European agency. The proceeds are used tofinance the public deficits of the member states of EMU

• The issuing agency is called the EMU Fund

• If the countries that participate in a Eurobond scheme pay a surcharge over the funding costs of the EMU Fonds we call them ‘conditional eurobonds’.

• EMU T-Bills are eurobonds with a maximum maturity of 2 years

Why are Eurobonds useful?

• Fragmented bond markets add to vulnerability of eurozone– Member states can run into acute and severe luidity problems– Problems of even small member states can derail the eurozone

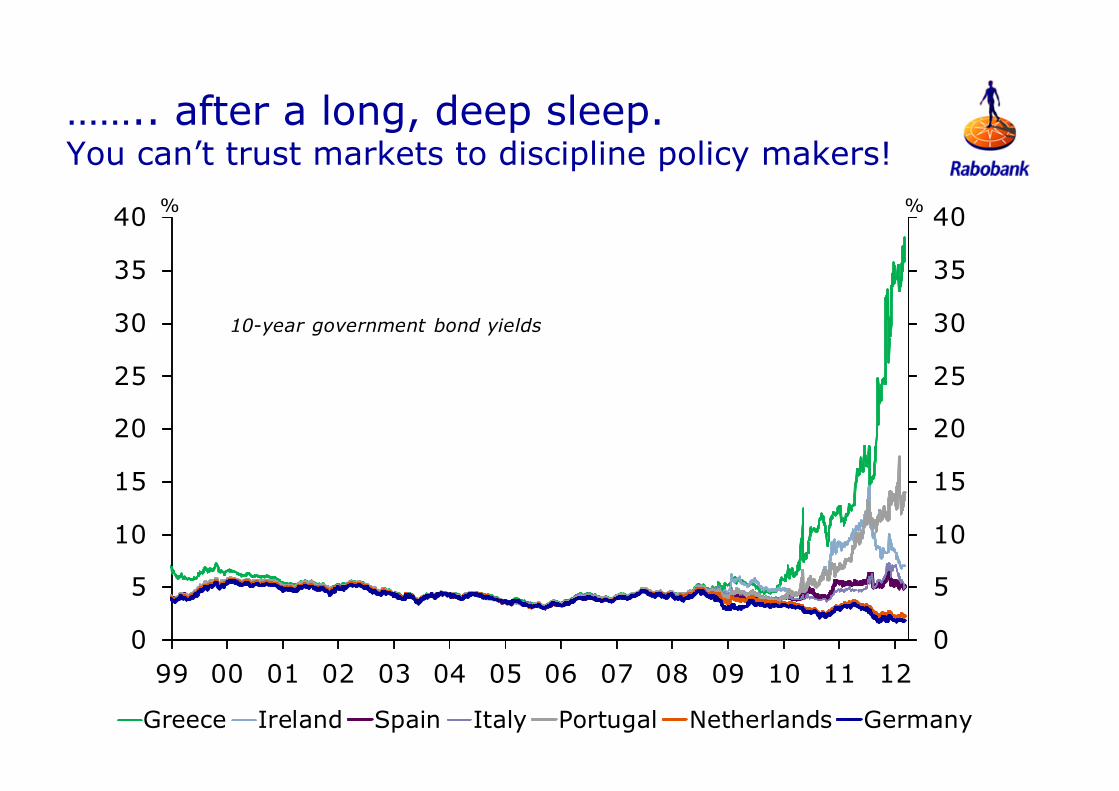

• You cannot trust that markets will discipline policymakers– Financial markets ignored fundamental disequilibria for almost a

decade– A ‘free rider’s paradise’.

• Current situation undermines market and banking stability– Bond markets risk of major instability– Banking sectors potential losses on public bonds– Banking sectors tight links between public and banking sectors

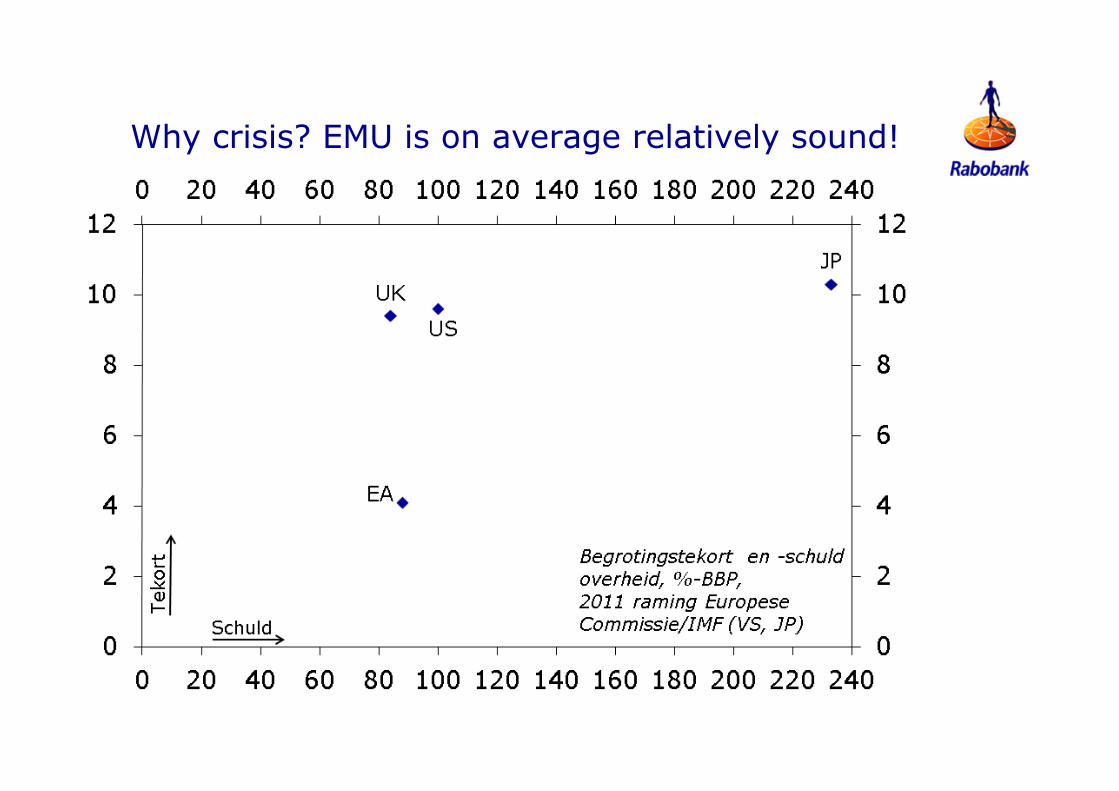

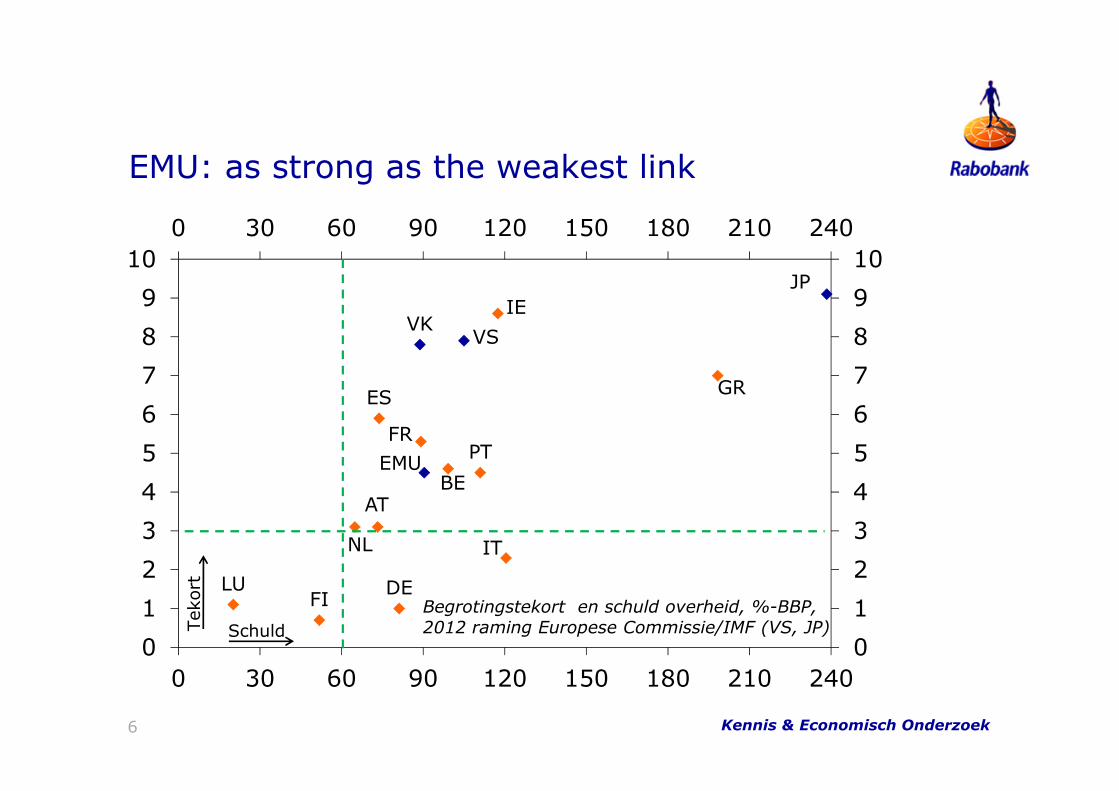

Why crisis? EMU is on average relatively sound!

EMU: as strong as the weakest link

Kennis & Economisch Onderzoek6

BE

DE

IE

GRES

FR

IT

LU

NL

AT

PT

FI

EMU

VKVS

JP

012345678910

0 30 60 90 120 150 180 210 240

0123456789

10

0 30 60 90 120 150 180 210 240

Begrotingstekort en schuld overheid, %-BBP, 2012 raming Europese Commissie/IMF (VS, JP)SchuldTe

kort

Markets started to differentiate………..

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

08 09 10 11 12

Greece Ireland Spain Italy Portugal Netherlands Germany

% %

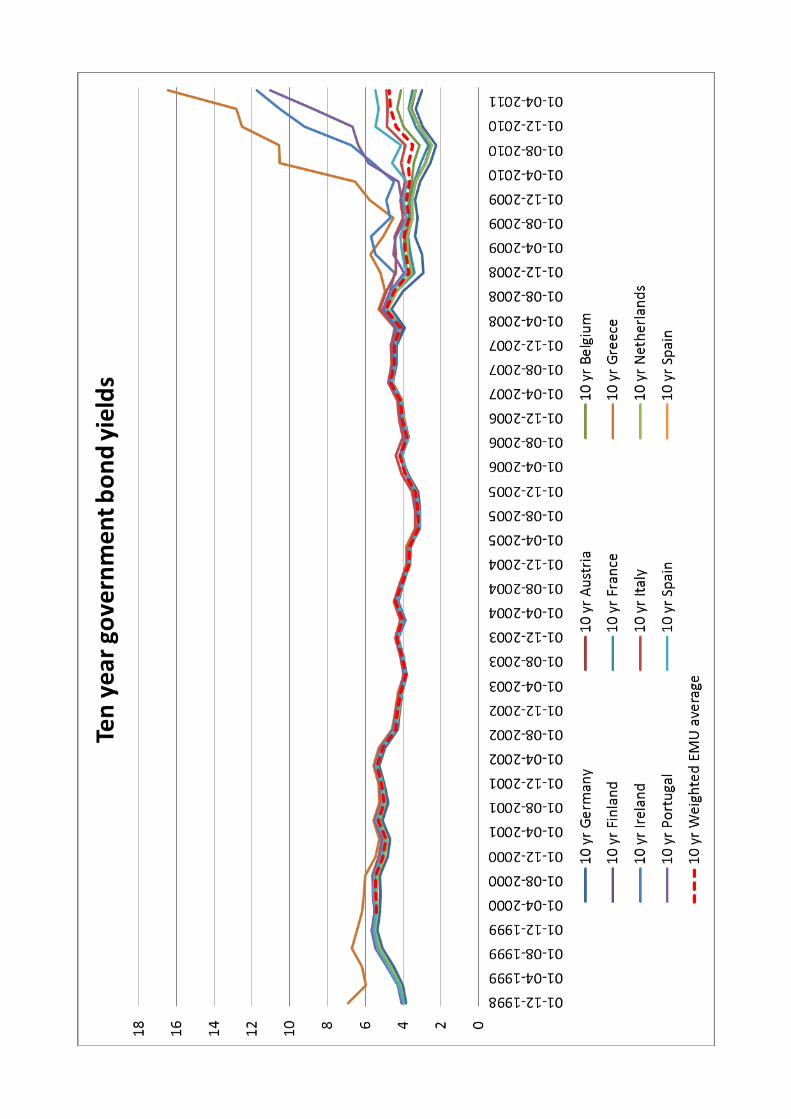

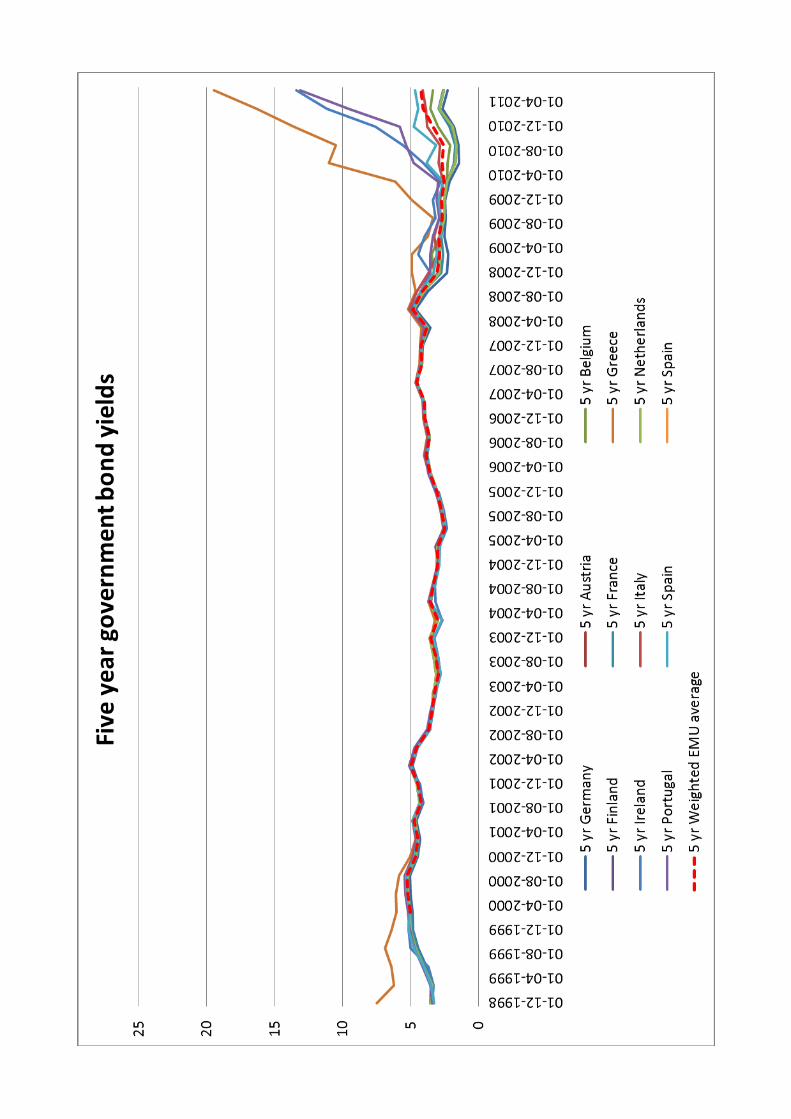

10-year government bond yields

…….. after a long, deep sleep. You can’t trust markets to discipline policy makers!

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

99 00 01 02 03 04 05 06 07 08 09 10 11 12

Greece Ireland Spain Italy Portugal Netherlands Germany

% %

10-year government bond yields

Today’s situation

• Public bond markets are fragmented

• In normal times: – Bad fiscal policies are ignored by the markets– Good fiscal policies are not rewarded

• In times of crisis: strong market reactions– Acute and large increases in interest rate differentials within EMU– Doubts about euro’s future existence– Turmoil on bond markets hurt investors– Weak governents weak banks

What should succesful Eurobonds bring?

• Stability in the financial markets

• More stable banking systems

• Access to finance against a reasonable price for all member states

• Improved fiscal discipline for policy makers

• Clear benefits for all countries (weak and strong)

• Preferably: a self-financing and pro-active crisis mechanism (create buffers via an insurance premium)

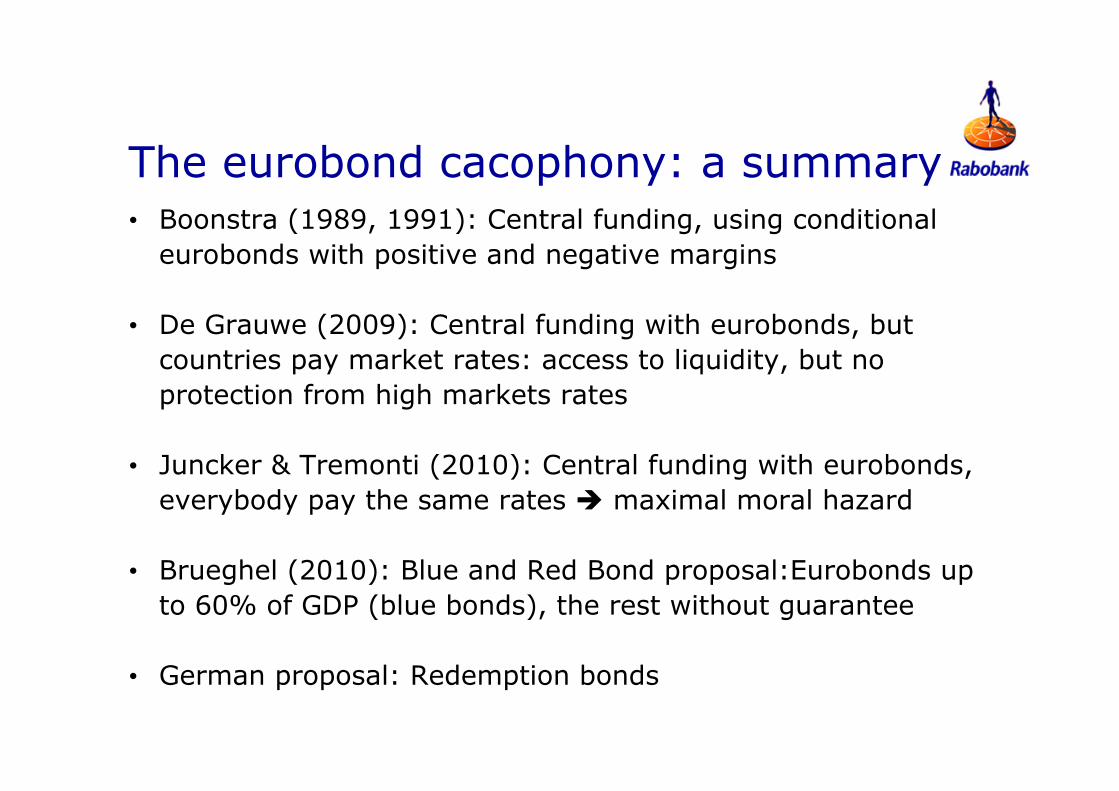

The eurobond cacophony: a summary• Boonstra (1989, 1991): Central funding, using conditional

eurobonds with positive and negative margins

• De Grauwe (2009): Central funding with eurobonds, but countries pay market rates: access to liquidity, but no protection from high markets rates

• Juncker & Tremonti (2010): Central funding with eurobonds, everybody pay the same rates maximal moral hazard

• Brueghel (2010): Blue and Red Bond proposal:Eurobonds up to 60% of GDP (blue bonds), the rest without guarantee

• German proposal: Redemption bonds

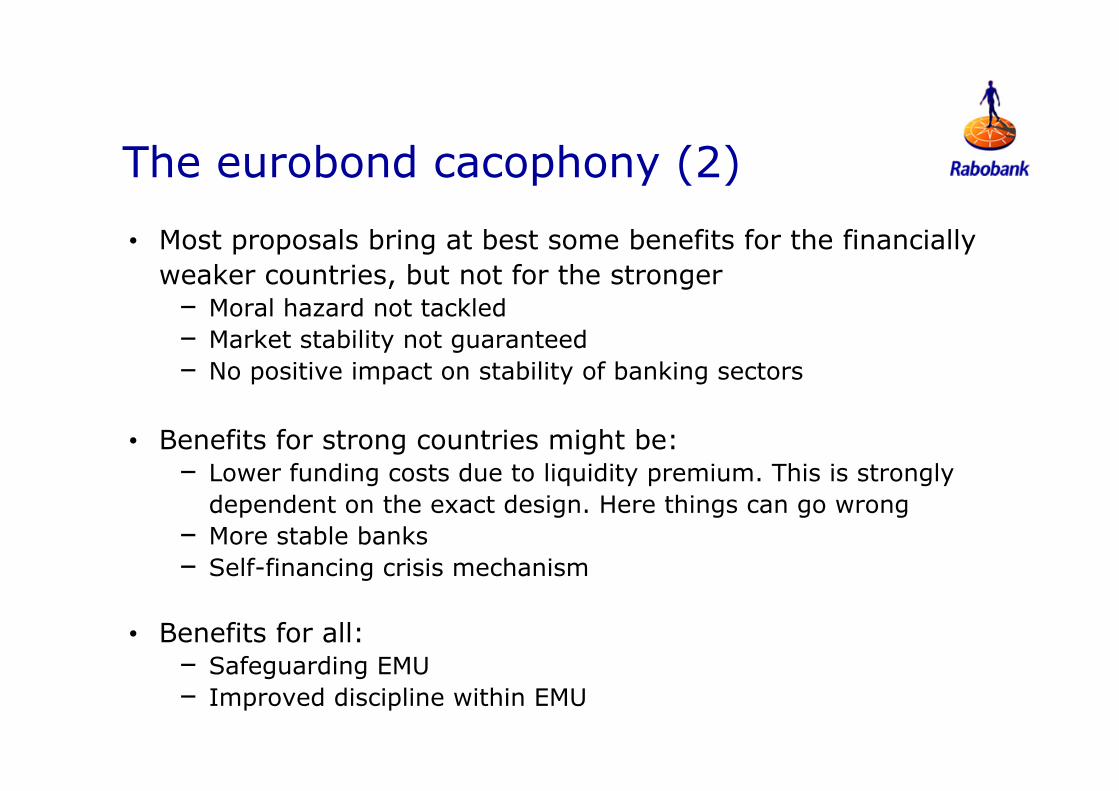

The eurobond cacophony (2)• Most proposals bring at best some benefits for the financially

weaker countries, but not for the stronger– Moral hazard not tackled– Market stability not guaranteed– No positive impact on stability of banking sectors

• Benefits for strong countries might be:– Lower funding costs due to liquidity premium. This is strongly

dependent on the exact design. Here things can go wrong– More stable banks– Self-financing crisis mechanism

• Benefits for all:– Safeguarding EMU– Improved discipline within EMU

The ELEC approach (1)• Temporary (4 years) conditional Eurobond programme

(under cross-guarantee)

• Covers all liquidity needs (debt redemption and deficit)

• Fot the time being only open for solvent countries (not for GR, IRE and PT) that fully implement new fiscal rules

• Maximum maturity of Bills: 2 years

• Conditional bonds surcharge depending on performance of public finances

The ELEC approach (2)• Temporary programme: acceptable for constitutional courts

• Big stick at the end: misbehaving countries can be removed without contamination of the system (thanks to the cross-guarantee)

• A four year facility buys time to implement adequate policies

• Cuts link between domestic banking systems and national public debt failing governments don’t contaminate domestic banks

• Creates a “risk-free asset”

The ELEC approach (3)• Common funding with a cross guarantee, open for all countries

that don’t draw on the EFSF and comply to the new budget rules

• Central funding via a new institution: the EMU Fund.

• ECB can stop its SMP. EFSF enlargement is not necessary

• Countries that participate give up their right to directly tap the financial markets in the short term maturities

• Countries that fail to meet the SGP criteria pay a spread over funding costs of the Fund, determined by public debt and deficitratios (see below)

The ELEC approach (4)• EMU Fund issues short term bonds, paying market rates

• The issued bonds are covered by a full cross-guarantee

• The money raised is distributed to the participating member states

• Participating countries pay market rates plus surcharge (see below)

• The surcharges are added to the reserves of EMU Fund, creating buffers for future mishaps

• Cross-guarantee in combination with good governance (budget rules with effective supervision and automatic and effective sanctions) will result in a very high credit rating

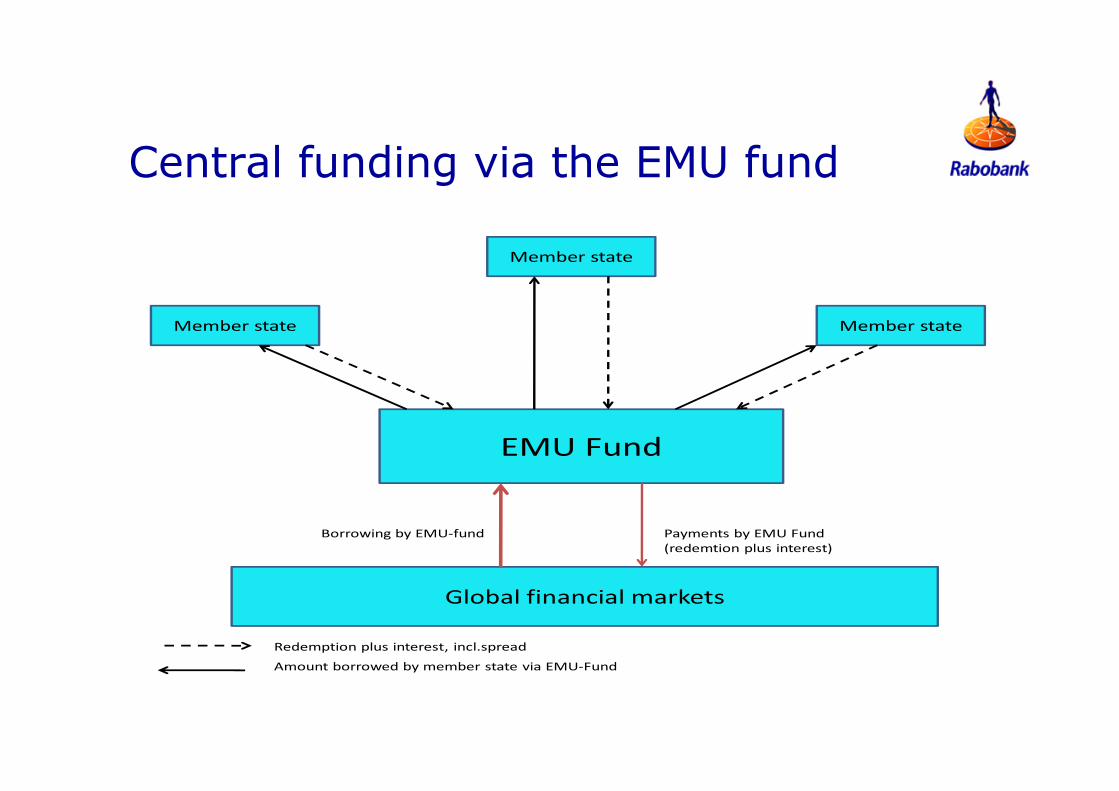

Central funding via the EMU fund

EMU Fund

Global financial markets

Member state

Member stateMember state

Redemption plus interest, incl.spread

Amount borrowed by member state via EMU-Fund

Borrowing by EMU-fund Payments by EMU Fund(redemtion plus interest)

Practical implementation

• It is essential that Germany participates

• Countries that are able to do so still have the freedom to issuelonger term debt (> 2 years) on their own behalf

• The system should be scaleable with more countries objective anchor necessary

• Participation should be on a voluntary basis, but once you’re in, you can’t go out

Advantages of this approach (1)• Better discipline as diverging fiscal policies translate into

diverging funding costs (restoration of failing market discipline)

• Countries are sheltered from sudden swings in market sentiment

• Creation of huge and liquid pan-EMU market for short-term bonds

• Weaker countries pay premium to EMU Fund, instead of higher interest rates to markets financial buffer against future problems

Advantages of this approach (2)

• Using cross-guarantee the EMU average counts, not the problem countries in the margin lower funding costs for all?

• Non-performing countries can be removed without danger of contagion

• Link between national public sector and domestic banks is cut: “risk free assets’ are covered by a cross-guarantee.

• Stability of banking sector improves because of more stable markets and cut of link between banks and governments.

Consequences for investors

• In the short maturities (< 2 year) for public debt there will be only one relevant issuer: the EMU fund

• In the longer maturities (> 2 year) there will only be public bond issues from the countries that are able to tap the markets without cross-guarantee

• The liquidity of the EMU market for public T-Bills will improve enormously and match the market for short term US Treasuries

• The competitive position of the euro as a major reserve currencywill improve enormously

• The euro will probably appreciate substantially

Possible problems of this approach

• Potential tensions with no-bail out clause we already have crossed this line

• Anchoring the system and calculation of the spread see below

• Lack of political willingness voluntary participation, but once you’re in, you cant go out (unless you are removed……)

• Uncertain impact on funding costs for stronger countries

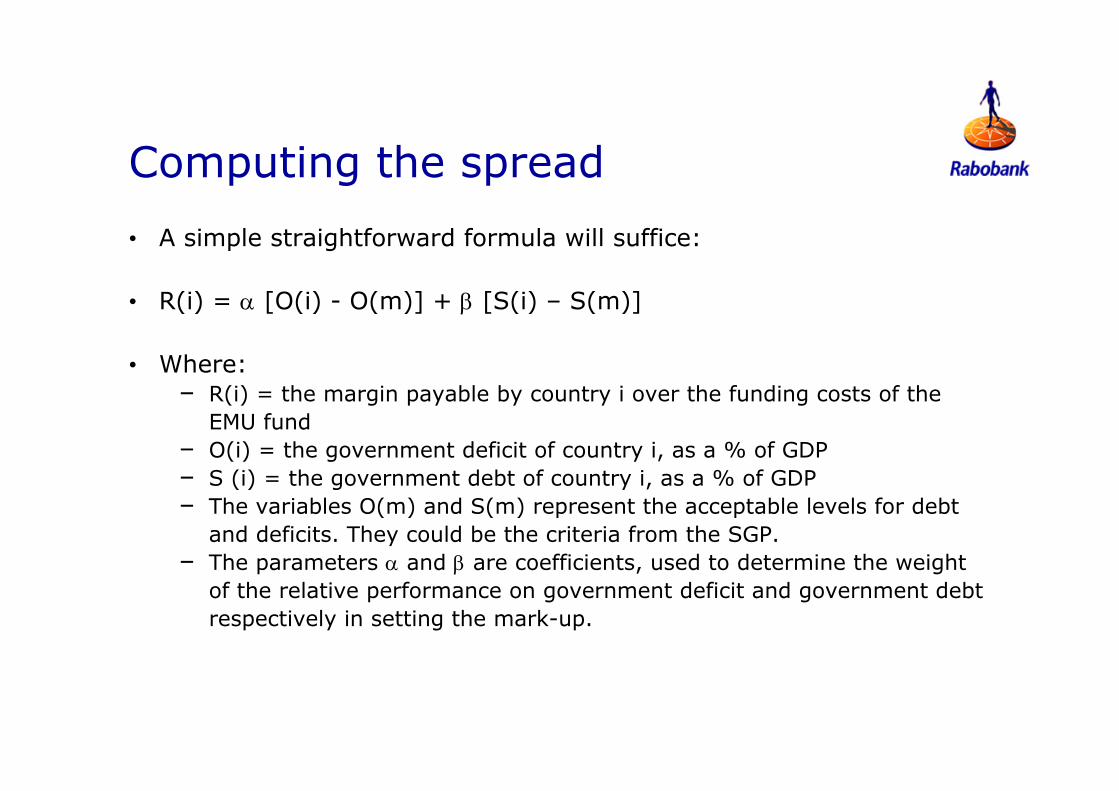

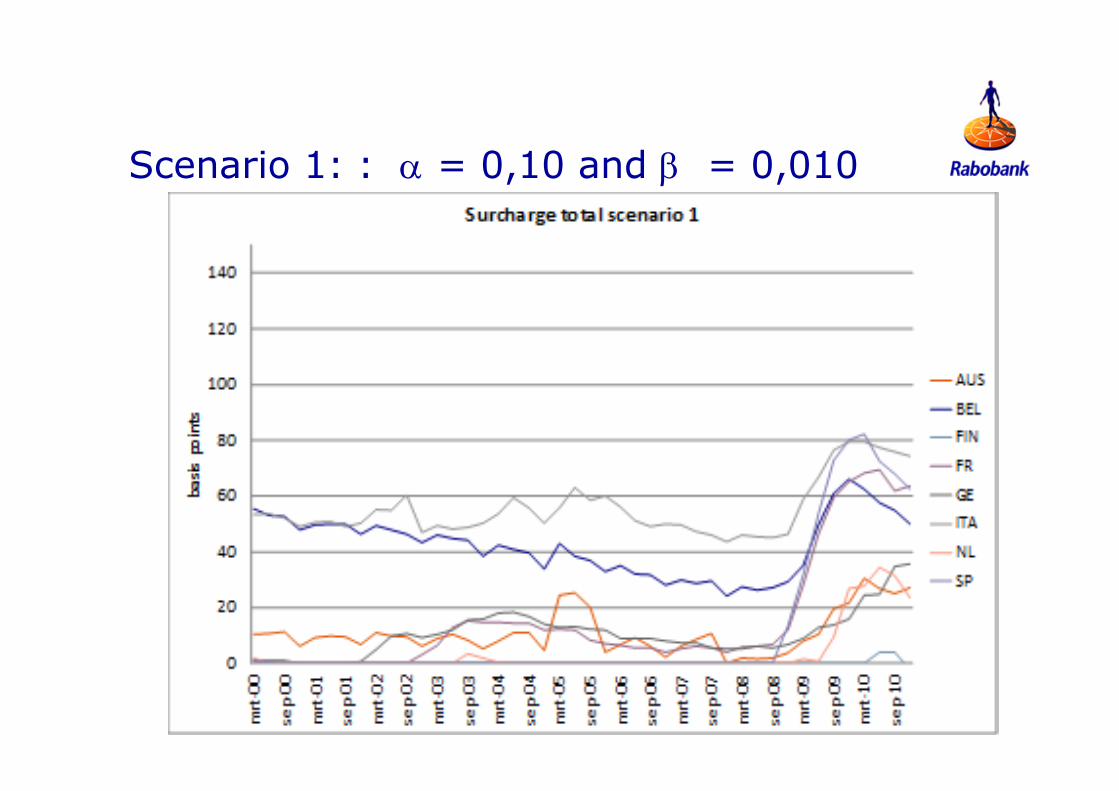

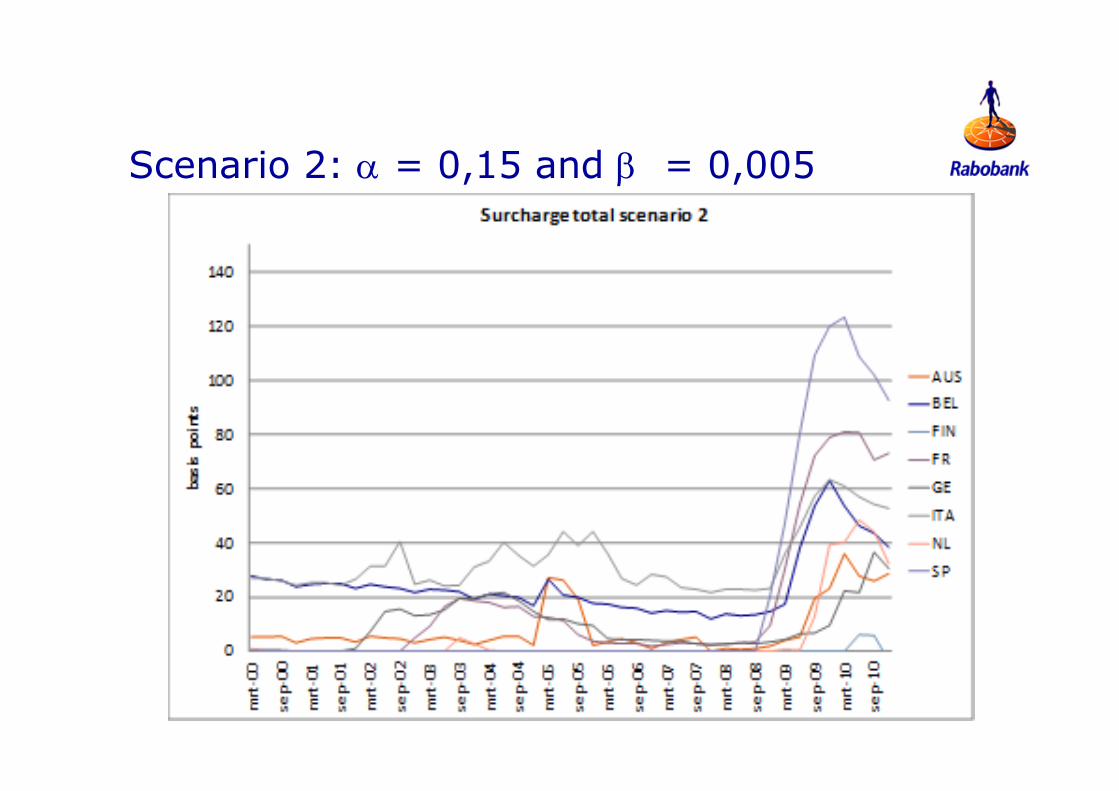

Computing the spread• A simple straightforward formula will suffice:

• R(i) = α [O(i) - O(m)] + β [S(i) – S(m)]

• Where: – R(i) = the margin payable by country i over the funding costs of the

EMU fund– O(i) = the government deficit of country i, as a % of GDP– S (i) = the government debt of country i, as a % of GDP– The variables O(m) and S(m) represent the acceptable levels for debt

and deficits. They could be the criteria from the SGP.– The parameters α and β are coefficients, used to determine the weight

of the relative performance on government deficit and government debt respectively in setting the mark-up.

Funding costs: what are the effects for the stronger countries? Two scenario’s

• Convergence torwards the best stronger (Germany) or even lower (due to improved liquidity) everybody better off

• Covergence towards a weighted average of yields of participatingcountries– German fundings costs increase with only 25 basispoints– Meaning an annual additional interest bill of € 5 billion

• These estimates are excluding liquidity effects

• Including moderate liquidity premium of 25 bp German funding costs don’t rise.

Funding costs: what are the effects for the stronger countries? Additional remarks

1. Even in a pessimistic scenario the average extra funding costs for Germany are low. Costs of crises and rescue packages are much larger

2. Funding advantage of stronger countries only exists in times of crises. In normal times non-existent.

3. Countries are always free to tap the markets in the longer maturities

4. In times of crisis huge costs of rescue packages and market volatility. EMU fund scheme is self-financing.

5. Finally: every solution of the eurocrisis will translate into increasing interest rates in Germany and the NL, dus to end of safe-haven effect

Scenario 1: : α = 0,10 and β = 0,010

Scenario 2: α = 0,15 and β = 0,005

Concluding remarks

• Only a pan-EMU federal budget or Eurobonds tackles a fundamental flaw in EMU’s design: the fragmentation of markets.

• If fragmentation of national bond markets is not eliminated, EMUwill remain vulnerable and may in the end not survive.

• A vulnerable EMU results in vulnerable banks and unstable markets

• Eurobonds will only help if they deliver advantages for both strong and weak countries

• However: Eurobonds are a fundamental redesign of EMU and need time to implement

• The ELEC temporary scheme of conditional euro T-Bills delivers most, if not all of these benefits

www.rabobank.com/kennisbank

More information?