Embed Size (px)

Citation preview

Sustainable financing and investing survey 2021US reportSustainability comes of age as companies, investors and government embrace change

Key Findings & OverviewThe pandemic, rapid shifts in public opinion and a change of political climate have helped to transform the outlook for sustainability in the US in the past year.

¡ Buyside to the fore – US institutional investors have embraced the sustainability agenda more emphatically than their company peers – some 67% of asset allocators and owners we surveyed say their focus on sustainability has strongly increased and will continue to increase compared to 21% of issuers who say the same. What’s more, a fifth of investors say sustainability has become their most important priority.

¡ Investment constraints – While 63% of investors say they see no obstacles to investing in the green and sustainable economy, of the 36% who do see obstacles, most of them (47%) say insufficient company disclosure is the one of the main challenges.

¡ Regulatory call – US companies and investors are united in making a strong call for increased regulatory involvement in the green and sustainable economy; 84% of them believe regulators such as the SEC (which is currently considering a new climate risk disclosure rule) should require companies to disclose more information on the environmental effects of their activities. Opinions are split on the social side – 50% of respondents (though more investors than companies) believe there should be greater disclosure on the social effects.

¡ Regulatory call – Most companies (61%) and investors (69%) say they believe investment firms should also be required by regulators such as the SEC to disclose more about how they invest sustainably.

¡ Disclosure impact – More than half of companies believe that if regulators required them to increase their disclosure on environmental and social issues it would not only help them become more sustainable, but help their investors understand their sustainability activities better. For investors, about 46% of them say the effect of this would be to help them choose between more and less sustainable companies and make it easier to invest sustainably.

¡ Sustainability-linked debt – Firm interest from US companies in sustainability-linked bonds and loans; 33% say they would consider issuing such bonds, and about 56% say the same for loans. Investors are also very supportive of this type of financing – 90% say these bonds and loans are of interest to them, largely due to them helping to encourage companies to improve their sustainability.

¡ Strategy impact – 61% of companies and investors say the Biden administration’s green economic recovery and transition plan (which includes the drive to cut emissions by 2030 and achieve net zero by 2050) will substantially change how they invest and prioritise opportunities. Less than 25% of them expect no change at all to their investment strategy.

¡ Backing the plan – Although an emphatic 85% of companies and investors believe the administration’s green recovery plan is a good plan, 36% of them – and particularly companies – say they do not believe it is ambitious enough.

¡ Environmental areas of interest – Top five most attractive environmental investment opportunities for companies and investors over the next five years are: Sustainable plastic and alternatives; recycling and circular economy; carbon capture technology; sustainable waste; and sustainable water management.

¡ Social areas of interest – The top five most attractive social investment opportunities for companies over the next five years are socioeconomic advancement and empowerment, access to education and vocational training, and access to financing and financial services. For investors, their top three also includes access to financial services, but they also see greater opportunity than companies around the provision of access to healthcare and food security.

of investors we surveyed say their focus on sustainability has strongly increased and will continue to increase

67%

Although sustainability has gained steadily increased prominence across the country over the past decade, a tipping point may now have been reached: even those sceptical about some aspects of sustainability believe change is inevitable and are therefore preparing for it.

This sense of change is evident in the responses of 200 US companies – that are active in the capital markets – and institutional investors, who we surveyed on the topic of sustainable financing and investing. Some of the key findings from the survey, discussed later in the report, are:

“US companies and investors are united in making a strong call for increased regulatory involvement in the green and sustainable economy.”

2 | Sustainable financing and investing survey 2021: US report

Our focus on sustainability has not changed much in

the past 12 months

We have increased our focus on sustainability in

the past 12 months

We have made a decision in the past 12 months to significantly increase our

focus on sustainability

Our focus on sustainability has increased strongly and will

continue to increase

Sustainability has become our most important priority

of US companies and investors, say their focus on sustainability has increased or has increased strongly (and they expect it to continue to increase) in the past 12 months

44%Figure 1: Investors drive greater focus in environmental and social issues Is your organisation increasing its focus on sustainability (including social impact)?

Investor Issuer Overall

70%60%50%40%30%20%0% 10%

IntroductionGreater sustainability focus for investors

“A confluence of factors is driving change for Companies and investors. These range from the impact of the pandemic on attitudes to sustainability, to greater awareness of the needs of society.”

As perhaps the world’s largest and most advanced economy, the importance of the US embracing environmental, social and sustainability issues is paramount in the drive to bring about profound and lasting change across the global economy.

For many years, these issues have been important to US companies and increasingly to institutional investors. But in the past year, amid political change, the pandemic and its unprecedented economic impact, sustainability has risen in strategic importance, coming into greater focus than ever before.

This is one of the key findings of our US survey, which, for the first time, forms part of our annual global research study on sustainable financing and investing.

Indeed, in the past year, some 60% of US companies (Fig 1) and investors say their focus on sustainability has increased or has increased strongly and they expect it to continue to increase.

A confluence of factors is driving change for companies and investors. These range from the impact of the pandemic on attitudes to sustainability, to greater awareness of the needs of society, of the urgency of climate change and the rising danger that the natural environment is in. Other factors include government policy support and development, pressure from investors to change, and recognition among companies and investors that focusing on sustainability is good for business.

While many of these drivers appear unaligned – public appetite for action has grown partly as a result of the Covid-19-inspired appreciation for the inter-connectedness of humans and nature – they are nevertheless significant.

Similarly, the election of President Biden has resulted in a sea change in government policy on climate change and sustainability. The symbolism of the US re-joining the Paris Agreement on climate change is powerful, and Biden’s plans for a greater role for renewable energy could result in a major shift in the US energy market.

3 | Sustainable financing and investing survey 2021: US report

Without question change is underway, and companies and investors are pivoting accordingly. What’s interesting is where they are in relation to each other on sustainability.

Some 67% of investors, for instance, say their focus has increased strongly compared to only 21% of issuers. Notably, about a fifth of US investors say sustainability has become their most important priority, however, by comparison, US companies are more measured, with most of them (31%) saying they have only increased their focus in the past 12 months.

This divergence of views between issuers and investors is also reflected in the reasons why each group is – and isn’t – increasing its focus on sustainability.

For companies (Fig 2)., the top reasons are: Greater availability of advice and information (69%) to help them become sustainable; the pandemic has changed their attitude to sustainability (60%); recognition that the natural environment is in danger (54%); and supportive government policy (54%). Interestingly, almost no companies say that they are increasing their focus on

sustainability in response to investor pressure, while only about a fifth said that it is good for their business.

In contrast, the main reasons driving investors’ sustainability efforts is their greater awareness of the needs of society (43%), greater information and advice (36%), and recognition of the urgency of climate change (33%). Most revealingly, 31% of the capital providers we surveyed said their end investors want them to consider sustainability – public opinion is driving change.

The divergence in views between companies and investors may reflect the potential ease with which investors are able to shift their business models relative to companies; it is easier to amend investment policies than reconfigure supply chains, for instance.

Moreover, companies, which operate in a variety of sectors following different sustainability trajectories, are necessarily more diverse than investors.

“The divergence in views between companies and investors may reflect the potential ease with which investors are able to shift their business models relative to companies; it is easier to amend investment policies than reconfigure supply chains..”

Figure 2: Multiple reasons why respondents have increased their focus Why are you increasing/have you increased your focus on sustainability?

Issuer Investor

4%

43%

We have become more aware of the needs of society

69%

36%

More advice and information is available to help us become sustainable

24%

33%

We have become more aware that climate change is an urgent problem

1%

31%

Our investors want us to

22%

28%

It is good for our business

54%

22%

The natural environment is in danger

54%

20%

Government policy supports this

60%

19%

The Covid-19 pandemic has changed our attitude to sustainability

Other organisations in our industry are doing this

4%

12%

of companies say one of the main reasons why they have incresed their focus on these issues is because they recognize that the natural environment is in danger

54%

Change UnderwayCompany and investor divergence

4 | Sustainable financing and investing survey 2021: US report

221

122

5264

Clean coal

One of the greatest challenges the US and the world faces in accelerating a more sustainable agenda is finding solutions to the ubiquitous use of plastic and developing effective ways of recycling.

Plastic is everywhere, with in excess of 8.3 billion tons of it in the world, some three quarters of which has ended up as waste, according to research by the American Association for the Advancement of Science. Substantial investment is needed to address this challenge, a need that is in turn creating an attractive investment opportunity, especially for the US companies and investors we surveyed.

When asked to choose the most attractive environmental investment opportunities (Fig 3) in the green and sustainable economy over the next five years, notably more respondents said the opportunity to develop more sustainable plastics and alternatives over the next five years, followed by recycling and the circular economy (which aims to eliminate waste).

This is an important response, one that not only indicates the corporate sectors’ awareness of the billions of dollars lost in packaging material waste each year, but also the huge potential to claw back some of that lost value by adopting a more sustainable approach to the use of plastic across operations and product lines.

The other most popular investment opportunities included the exciting, though relatively new area of carbon capture technology, as well as sustainable waste and water management. Carbon capture technology is still a long way from becoming widespread, but there are now a number of plants operational in the US associated with natural gas or coal-fired power plants or industrial facilities manufacturing iron, for example.

Interestingly, some of these investment opportunities are also among the top five opportunities seen by respondents in our China and UK deep dive surveys. For instance, US and China respondents see opportunities in sustainable waste management, and recycling and the circular economy. In addition, US and UK respondents see opportunities in sustainable water management and carbon capture technology.

What unites these environmental investment opportunities is the need for advanced technologies to support them. Some of the technology is established, but some are emerging, such as carbon capture, perhaps representing the next big thing to companies and investors.

While renewable energy technologies – specifically solar, wind and tidal – are still seen as opportunities, they are less popular, which perhaps indicates they are seen as part of the status quo – the potential for sizeable returns therefore may now be limited.

Figure 3: Investors and companies see attractive environmental investment opportunitiesWhich of the following environmental investment opportunities do you think will be the most attractive in the US in the next five years?

Note: Issuers and investors were asked to rank the investment opportunities they thought would be most attractive. From these rankings each option was given a blended score indicating its popularity. These scores are displayed in the graph.

367

Sustainable agriculture and forestry

376

Wind power generation

77Recycling and the circular economy

7579

Biofuels

5287Energy-efficient commercial and

public buildings

139102

Sustainable water management

8Solar power generation

146125

Sustainable waste management

150135Carbon capture technology (i.e.

to be used in carbon-intensive industries)

185185

205More sustainable plastics and alternatives to them

0 250200 225175150125100755025

Electric cars54

28

031Tidal and wave power

3031

Hydrogen energy

533

Improved electricity grids

10037

Nuclear energy

443

Energy-efficient housing

1551

Sustainable public transport

3353

Electric commercial vehicles

8854

Energy efficiency in industry

Investor Issuer

“What unites these environmental investment opportunities is the need for advanced technologies to support them. Some of the technology is established, but some are emerging.”

Environmental and social investmentOpportunities evolve and grow

5 | Sustainable financing and investing survey 2021: US report

4

234

136

45

141

168

163

20

167

63

181

18

49

110

66

145

101

242

106

39

110

146

161

119

Figure 4: Investors and companies see attractive social investment opportunitiesWhich of the following social investment opportunities do you think will be the most attractive in the US in the next five years?

150 200 25022517512575 10050250

Environmental investment opportunities like these attract attention and are important, but so too are opportunities on the social side. We similarly asked respondents to choose the most attractive social investment opportunities (Fig 4) over the next five years.

Interestingly, the responses from companies and investors show they are not as aligned as they are on environmental opportunities. Both groups give access to finance and financial services as one of their top three opportunities.

However, the other most popular social opportunities for investors are access to healthcare and food security. In contrast, companies give socioeconomic advancement and empowerment, and access to education and vocational training, as their top two most attractive opportunities.

Multiple reasons may explain this difference in view. Access to healthcare may involve higher cost implications for companies, for instance. What’s perhaps most important, however, is that companies and investors are together seeing compelling social investment opportunities at a time when there is a need to increase the financial support provided to certain areas of society.

What’s more, companies and investors are not seemingly being held back from being able to provide some of that that investment support – an emphatic 81% of our respondents say that they see no obstacles to investing in the green and sustainable economy.

Note: Issuers and investors were asked to rank the investment opportunities they thought would be most attractive. From these rankings each option was given a blended score indicating its popularity. These scores are displayed in the graph.

Socioeconomic advancement and

empowerment

Urban and rural regeneration

schemes

Access to financing and financial services

Food security

Access to affordable basic infrastructure

(e.g. sanitation, transport)

Access to healthcare

Access to the internet and technology (e.g.

laptops, smartphones)

Supporting businesses

owned by women

Supporting businesses

owned by minorities

Access to education and vocational training

Access to affordable housing

Access to affordable energy

Investor Issuer

Changing viewsSocial investments come into focus

“Companies and investors are together seeing compelling social investment opportunities at a time when there is a need to increase the financial support provided to certain areas of society.”

of our respondents say that they see no obstacles to investing in the green and sustainable economy

81%

6 | Sustainable financing and investing survey 2021: US report

Issuer Investor

say the recovery plan will substantially change how they invest and prioritise opportunities

62%

The plan is good, but is not ambitious enough

The plan is too ambitious on green

issues

I am concerned that aspects of the plan may not work well

It is a good plan for the US and the climate

Figure 6: The plan will impact how respondents investHow will the US’s green economic recovery and transition plan influence your investment strategy?

19%

60%

21%

0%

It will not require much change

It will substantially change how we invest and prioritise opportunities

No change

We will have to develop a new investment strategy

Figure 5: Respondents back the green recovery planWhat do you think of the US’s green economic recovery plan and drive to cut emissions by about 50% by 2030?

70%60%50%40%30%20%10%0%

8%

62%

24%

6%

Issuer Investor

One of the most notable developments in the sustainability debate in the past year has been the election of President Biden, a proponent of measures to tackle climate change and other sustainability challenges.

It is important to note that while the optics have been transformed by the election of President Biden, for many US corporates it’s business as usual. Companies and many US states committed to sustainability and climate change mitigation measures during President Trump’s term of office.

Nevertheless, the groundswell of support among survey respondents for President Biden’s green economic recovery plan and commitment to net zero emissions by 2050 is striking (Fig 5).

Some 85% of respondents think it is a good plan for the US and the climate, with investors especially bullish. Companies are a bit more circumspect about it – 42% think the plan is good but not ambitious enough compared to 30% of investors who say the same – and about a quarter of them say they have concerns that certain aspects may not work well.

To be sure, many details of the plan have not yet been clarified: haggling in Congress is ongoing. Moreover, while there is broad support for President Biden’s plan, among corporates in particular there remains a divide as to how sustainability issues should be tackled; a sizeable contingent continues to believe that technology (and the market) can address many sustainability challenges without government compulsion.

Such reservations will not diminish the impact of the plan. Most companies (60%) and investors (62%) say the plan will substantially change how they invest and prioritise opportunities (Fig 6).

“The groundswell of support among survey respondents for President Biden’s green economic recovery plan and commitment to net zero emissions by 2050 is striking.”

Accelerating changeGreen economic plan and emissions targets

7 | Sustainable financing and investing survey 2021: US report

Lending more advanced While the SLB market in the US is still in its infancy, sustainability-linked lending is more established, with some banks now including sustainability as a standard part of loan documentation.

Overall, there is a greater support for this type of financing from the companies we surveyed – some 56% of them said these loans would be useful to them, with most of them (45%) saying so because they see value in being able to demonstrate their efforts to connect financing with sustainability (Fig 9).

Some 11% said these loans would be of use because they see value in knowing that their cost of capital would be lower if they achieve our sustainability targets. However, that still leaves 42% who believe the benefits don’t currently outweigh the additional work involved.

Powerfully, 89% of investors say they see value in companies adopting these facilities (Fig 10), with most (65%) of them saying so because they see value in companies having to set annual sustainability targets and communicate them to their banks. Some 24% of investors say they see value in companies connecting their cost of capital with their sustainability performance.

Sustainability-linked debt financing, where the company can use the funds for any purpose but commits to hit sustainability targets (and paying a higher interest rate if it fails), is well established in Europe but still a relatively new financing arrangement in the US. (Fig 7).

For companies, a key attraction of such financing is that it enables them to demonstrate how their sustainability and financing strategy are integrated, which can potentially lower their borrowing costs.

In addition, such financing also demonstrates their sustainability commitment to stakeholders. For investors, sustainability-linked products can deliver good returns, provide further information on an issuer’s progress toward sustainability goals, and may come with lower risk than traditional instruments. Such benefits are attractive, but not to all.

A third of US companies we surveyed said sustainability-linked bonds (SLBs) are potentially useful to them and they would consider issuing them (Fig 7) – some 37% of UK companies who we asked in our related UK deep dive survey said the same – while 53% said they would not be useful. One likely stumbling block is third party verification, which is costly.

Somewhat expectedly there is greater appetite among the largest companies (some 58% say SLBs would be useful and would consider issuing them) we surveyed compared the smallest companies (only 13% said the same), which perhaps reflects the larger size of their funding needs.

In addition, while companies appreciate the benefits of SLBs in terms of stakeholder engagement, they want to be compensated for the increased cost and effort associated with such bonds. Naturally, there will always be a trade-off between what companies and investors want.

For investors, they are emphatically supportive of these bonds – some 90% say they are of interest to them, with most (64%) of them saying so because they could encourage companies to improve their sustainability (Fig 8). A quarter of investors say the bonds are of interest because they would be compensated if the company fails to hit its sustainability targets.

Interestingly, over half the investors say they would invest in SLBs within the same fund that invests in green bonds (which are linked to specific projects). This may reflect relatively loose mandates at green bond funds or the growing ESG-focus of mainstream bond funds.

Yes, these bonds sound interesting and

we would consider issuing them

Yes, these bonds sound interesting because

they could compensate us if a company fails to

improve its sustainability

Yes, we see value in knowing that our

cost of capital will be lower if we achieve our

sustainability targets

Yes, we see value in companies connecting

their cost of capital with their sustainability

performance

Yes, we see value in being able to

demonstrate how we are connecting our financing

with sustainability

Yes, we see value in companies having to

set annual sustainability targets and communicate

them to their banks

No, we have loans, but benefits don’t seem to outweigh the additional work

No, companies rarely draw on their loans

which means any interest rate adjustment

has little to no effect

No, we do not have any loans or rarely draw on facilities

No, as targets are not public and/or margin

adjustment is not material we do not

assign high value for this

No, we issue bonds but these bonds

do not sound interesting for us

Yes, these bonds sound interesting because

they could encourage companies to improve

their sustainability

No, we do not issue bonds

No, we buy corporate bonds but these

bonds do not sound interesting for us

Figure 7: Companies show interest in sustainability-linked bondsSome companies are beginning to issue ‘sustainability-linked bonds’.Would these bonds be useful to you? (Issuers only)

Figure 8: Investors show interest and see value in sustainability-linked bondsSome companies are beginning to issue ‘sustainability-linked bonds’. Would these bonds be of interest to you? (Investors only)

Figure 9: Companies show interest in sustainability-linked loansSome companies are beginning to issue ‘sustainability-linked loans’. Would a loan like this be useful to you? (Issuers only)

Figure 10: Investors show interest and see value in sustainability-linked loansSome companies are beginning to issue ‘sustainability-linked loans’. TDo you see value in companies adopting these facilities? (Investors only)

60% 70%60%

50%

50% 50%40% 40%

40%

30% 30%

30%

20% 20%

20%

10% 10%

10%

0% 0%

0% 70%60%50%40%30%20%10%0%

Evolving needsGrowing appetite for sustainability-linked finance

8 | Sustainable financing and investing survey 2021: US report

While most investors (63%) see no obstacles to investing in the green and sustainable economy, 36% do, and for most of them insufficient disclosure is the biggest challenge (Fig 11, 12).

Disclosure has been a perennial problem for sustainability. There are myriad voluntary or partial standards around carbon emissions for example, but there is no objective benchmark by which all companies are measured (as there are with financial accounts).

The issue is so intractable that more than 80% of company and investor respondents (Fig 13) want regulators such as the SEC to require companies to disclose more information on the environmental effects of their activities – a striking response not least because it’s a rare example of market participants essentially calling for greater regulatory involvement.

This call is, however, strongest on the environmental side. This sentiment does not apply to the disclosure of companies’ efforts regarding social issues.

While the tragic death of George Floyd and increased public concern about racial discrimination in the US has prompted many companies to increase their focus on diversity and inequality issues, change necessarily takes time. At this stage, companies are seemingly not ready yet to be scrutinised on social issues – just over half say regulators such as the SEC should not require them to disclose more on the social effects of their activities. Even so, some 46% of companies do think this should happen, and importantly, some 54% of investors think so, too (Fig 14).

Given that measuring the social effects of company activity is tougher than for environmental issues – and it is even more politically controversial – it remains to be seen whether SEC regulation will ever be seen as appropriate in this area.

The SEC, however, appears eager to consider a broad range of ESG issues, including both greenhouse gas emissions and (potentially) workforce turnover and diversity. A number of public consultations have been launched in 2021.

Companies’ enthusiasm for regulation (of environmental issues at least) is driven by a belief that it will help them internally in their efforts to become more sustainable (95% of respondents agree), while 56% say it would help investors understand their sustainability activities better (Fig 15). Companies will be keen to see that any liability risk relating to differences between climate change disclosures in their 10-K report and sustainability report is minimised.

Figure 11: Investors see some obstaclesDo you see obstacles to investing in the green and sustainable economy in the US?

TOP 5

Figure 12: Insufficient disclosure one of the main obstacles for investorsIf you see obstacles to investing in the green and sustainable economy in the US, which are the main ones?

47%

Insufficient disclosure

28%

These investments are not accessible to us because of regulatory or legal barriers

28%

Investment opportunities are not clearly communicated

25%

The technologies are not available at the necessary scale or cost

17%

The technologies are not useful for my business

It would help us internally to become

more sustainable

It would help us internally to become

more sustainable

It would help investors understand our

sustainability activities better

It would help investors understand our

sustainability activities better

We already disclose more than other

companies so this would be fairer

We already disclose more than other

companies so this would be fairer

It would be helpful for us to have clear guidance on

disclosure

It would be helpful for us to have clear guidance on

disclosure

Figure 15: Companies see greater disclosure as a force for good in their sustainability driveIf regulators required companies to disclose more information on environmental issues, how would this affect you? (Issuers only)

Companies see greater disclosure as a force for good in their sustainability driveIf regulators required companies to disclose more information on social issues, how would this affect you?(Issuers only)

70% 70%80% 80%100% 100%90% 90%60% 60%50% 50%40% 40%30% 30%20% 20%10% 10%0% 0%

No

Don’t knowYes

36%

63%

1%Issuer

Issuer

Figure 13: Respondents back greater disclosure by companies on environmental effects of their activitiesDo you think regulators such as the SEC should require companies to disclose more information on the environmental effects of their activities?

0%

0%

90%

90%

80%

80%

100%

100%

70%

70%

60%

60%

50%

50%

40%

40%

30%

30%

20%

20%

10%

10%

Investor

Investor

Yes No

Figure 14: Respondents split on whether companies should disclose more on the social effects of their activitiesDo you think regulators such as the SEC should require companies to disclose more information on the social effects of their activities?

The Market speaksNeed for greater regulatory involvement

9 | Sustainable financing and investing survey 2021: US report

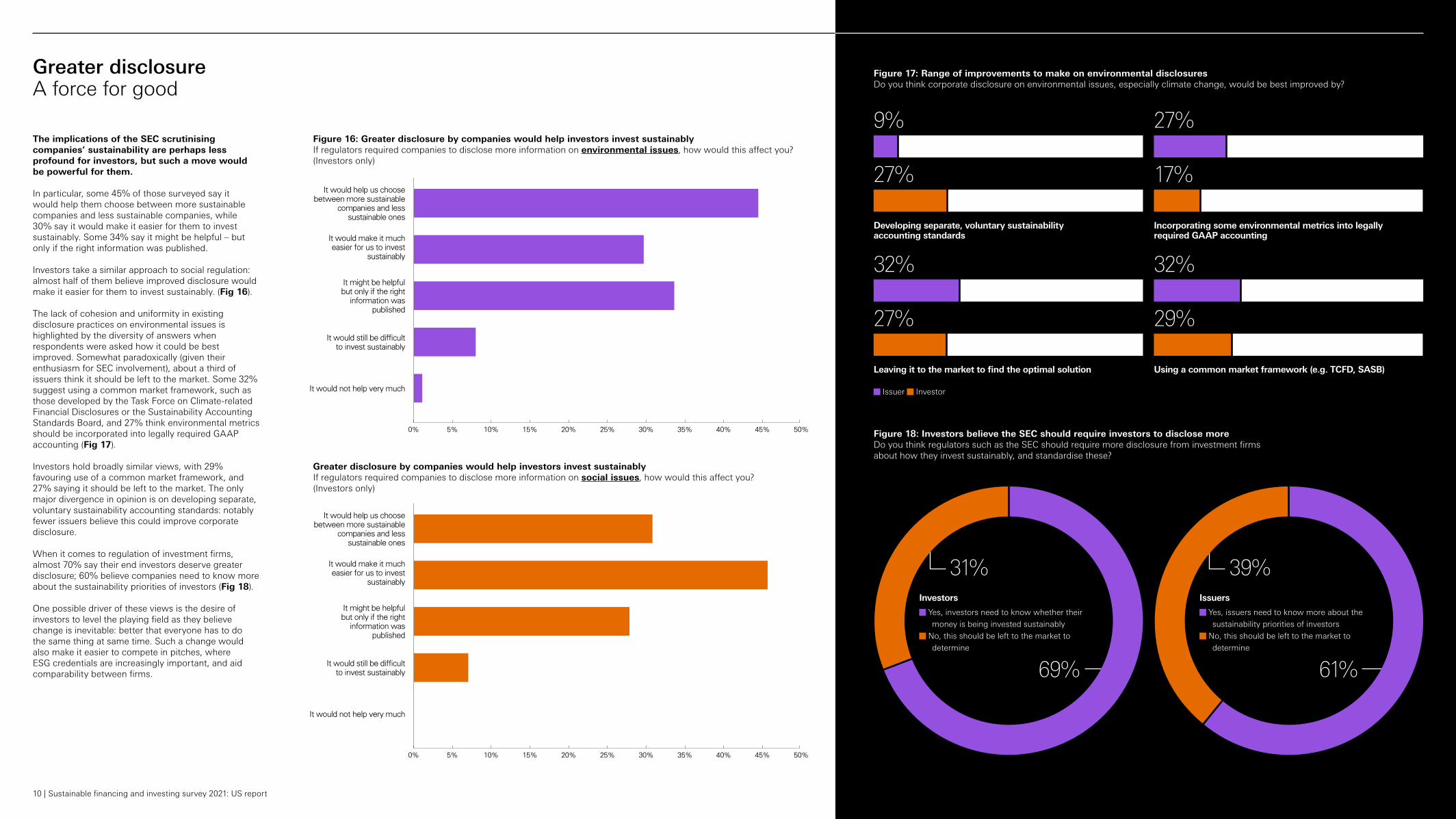

The implications of the SEC scrutinising companies’ sustainability are perhaps less profound for investors, but such a move would be powerful for them.

In particular, some 45% of those surveyed say it would help them choose between more sustainable companies and less sustainable companies, while 30% say it would make it easier for them to invest sustainably. Some 34% say it might be helpful – but only if the right information was published.

Investors take a similar approach to social regulation: almost half of them believe improved disclosure would make it easier for them to invest sustainably. (Fig 16).

The lack of cohesion and uniformity in existing disclosure practices on environmental issues is highlighted by the diversity of answers when respondents were asked how it could be best improved. Somewhat paradoxically (given their enthusiasm for SEC involvement), about a third of issuers think it should be left to the market. Some 32% suggest using a common market framework, such as those developed by the Task Force on Climate-related Financial Disclosures or the Sustainability Accounting Standards Board, and 27% think environmental metrics should be incorporated into legally required GAAP accounting (Fig 17).

Investors hold broadly similar views, with 29% favouring use of a common market framework, and 27% saying it should be left to the market. The only major divergence in opinion is on developing separate, voluntary sustainability accounting standards: notably fewer issuers believe this could improve corporate disclosure.

When it comes to regulation of investment firms, almost 70% say their end investors deserve greater disclosure; 60% believe companies need to know more about the sustainability priorities of investors (Fig 18).

One possible driver of these views is the desire of investors to level the playing field as they believe change is inevitable: better that everyone has to do the same thing at same time. Such a change would also make it easier to compete in pitches, where ESG credentials are increasingly important, and aid comparability between firms.

39%

Figure 18: Investors believe the SEC should require investors to disclose moreDo you think regulators such as the SEC should require more disclosure from investment firms about how they invest sustainably, and standardise these?

Yes, investors need to know whether their money is being invested sustainably

No, this should be left to the market to determine

Yes, issuers need to know more about the sustainability priorities of investors

No, this should be left to the market to determine

Figure 17: Range of improvements to make on environmental disclosuresDo you think corporate disclosure on environmental issues, especially climate change, would be best improved by?

9% 27%

27% 17%

Developing separate, voluntary sustainability accounting standards

Investors Issuers

Incorporating some environmental metrics into legally required GAAP accounting

32%

31%

69% 61%

32%

27% 29%

Leaving it to the market to find the optimal solution Using a common market framework (e.g. TCFD, SASB)

It would still be difficult to invest sustainably

It would still be difficult to invest sustainably

It would not help very much

It would not help very much

It might be helpful but only if the right

information was published

It might be helpful but only if the right

information was published

It would make it much easier for us to invest

sustainably

It would make it much easier for us to invest

sustainably

It would help us choose between more sustainable

companies and less sustainable ones

It would help us choose between more sustainable

companies and less sustainable ones

Figure 16: Greater disclosure by companies would help investors invest sustainably If regulators required companies to disclose more information on environmental issues, how would this affect you? (Investors only)

Greater disclosure by companies would help investors invest sustainably If regulators required companies to disclose more information on social issues, how would this affect you? (Investors only)

40%

40%35%

35% 50%

50%45%

45%30%

30%25%

25%20%

20%15%

15%10%

10%5%

5%0%

0%

Issuer Investor

Greater disclosure A force for good

10 | Sustainable financing and investing survey 2021: US report

By any interpretation, the responses from our survey of US companies and institutional investors confirms the growing centrality and priority of sustainability to the private sector.

Even before 2021, the pace of change had clearly accelerated, with a number of high-profile companies making vocal commitments to cutting greenhouse gas emissions and ESG funds under management outpacing broader market growth.

However, while the previous administration may have arguably held back ESG’s advancement into the mainstream, even as companies and investors in other regions – most notably Europe – embraced the opportunities available. That barrier, slight though it might have been in reality, has now been lifted.

It is wrong to see the results of this survey as demonstrating unconditional support and unalloyed enthusiasm for sustainability as a goal in itself. But even among those companies and investors indifferent to the sustainability agenda, there is an acceptance of the inevitability of change.

This – combined with the increased prominence given to these issues by President Biden’s green plan and emissions targets and broader public support (partly as a result of the pandemic) – will generate greater momentum.

In five years’ time, it seems certain that financing and investment in the US will look very different, and decidedly more sustainable in character.

The US survey is related to the HSBC Sustainable Financing and Investing Survey, which is an annual global survey of 2,000 capital markets issuers and institutional investors. This year is the fifth year the global survey has been run.

Euromoney Institutional Investor PLC designed and executed the US and global surveys.

The 200 respondents to the US survey – which was run between May and June 2021 – were split evenly between 100 issuers, from across industries, and 100 institutional investors, including asset allocators and asset owners.

Company respondents held senior positions in the CFO office and finance function.

Investor respondents held senior positions in the CIO and CFO office, in portfolio and fund management and investment.

100%

100%

90%

90%

80%

80%

70%

70%

60%

60%

50%

50%

40%

40%

30%

30%

20%

20%

10%

10%

0%

0%

$10bn+

$1bn to $10bn

$500m to $1bn

$250m to $500m

$25bn+

$5bn to $25bn

$1bn to $5bn

Up to $1bn

Issuers by annual revenues (US$)

Investors by AUM

Methodology

Banking 3%

Consumer goods 9%

Healthcare 9%

Information technology 8%

Insurance 9%

Metals and mining 9%

Oil, gas, coal and chemicals 12%

Real estate 11%

Retail and consumer services 8%

Telecoms 11%

Transport 11%

BASE SIZE 100

Issuers by industry/sector

Endowment and foundation 20%

Pension fund 17%

Family office 16%

Insurer 14%

Hedge fund 13%

Sovereign wealth fund 10%

Asset manager 8%

Advisor to Multi Family offices/co-investor 1%

Non-financial corporate treasury 1%

BASE SIZE 100

Investors by institution type

ConclusionSustainability agenda in the US gathers powerful momentum

11 | Sustainable financing and investing survey 2021: US report

Published: September 2021For Professional clients and Eligible Counterparties only.All information is subject to local regulations.

© Copyright HSBC Bank plc. All rights reserved. No part of this document may be reproduced, stored, distributed or transmitted in any form without the prior written permission.

The information presented is not meant to be comprehensive and does not constitute financial, legal, tax or other professional advice. You should not act upon the information contained in this document without first obtaining specific professional advice. While reasonable care has been taken in preparing this document, HSBC does not make any guarantee, representation or warranty (express or implied) as to its accuracy or completeness. The information presented in this document is subject to change without notice. Certain of the products and services offered by HSBC and its subsidiaries and affiliates are subject to credit adjudication and approval. This document does not constitute an offer to provide the services and products described and the provision of such services and products remains subject to contract.

Issued by the following HSBC entitiesIssued in the United States by HSBC Bank USA, N.A. 2020. All Rights Reserved. Member FDIC.

Opinions expressed in the report may differ from those of the HSBC Group, its officers, or employees.

![BNEF Green Investing 2011 Reducing the Cost of Financing[1]](https://img.pdfslide.net/doc/110x75/54fab6c04a79590b398b4d30/bnef-green-investing-2011-reducing-the-cost-of-financing1.jpg)