Embed Size (px)

Citation preview

Water Disposal – An Assessment of Disposal Wells and Facilities Eric Peterson

Strategic Planning & Market AnalysisMay 2014

• Confidential & Proprietary• Confidential & Proprietary

Retail Propane

15%

Crude Logis-tics48%

Water Solu-tions23%

NGL14%

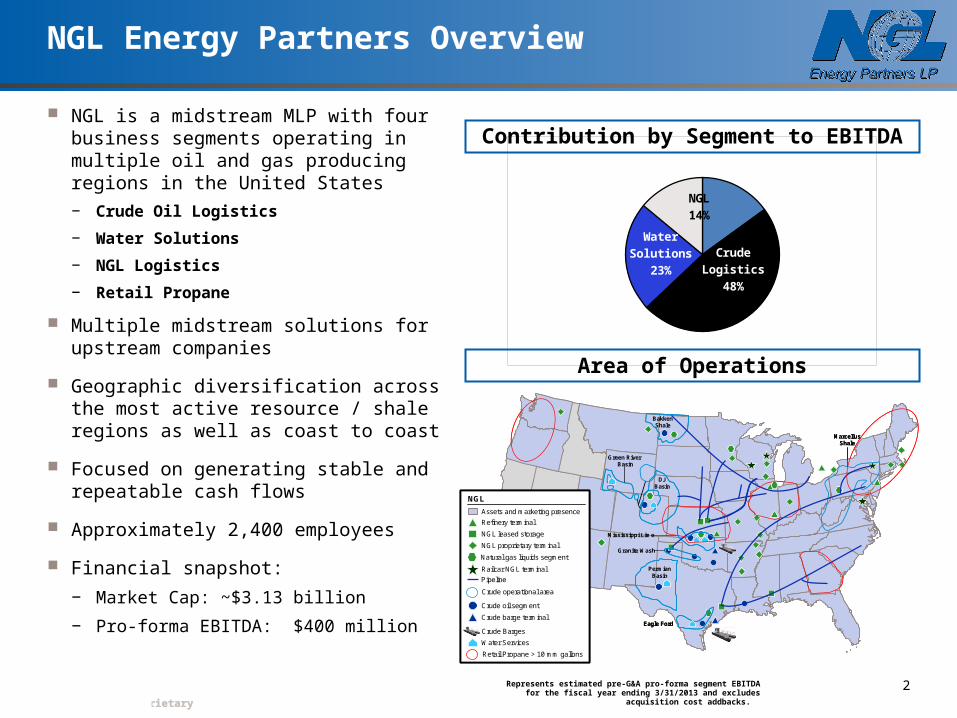

NGL Energy Partners Overview

NGL is a midstream MLP with four business segments operating in multiple oil and gas producing regions in the United States

− Crude Oil Logistics

− Water Solutions

− NGL Logistics

− Retail Propane

Multiple midstream solutions for upstream companies

Geographic diversification across the most active resource / shale regions as well as coast to coast

Focused on generating stable and repeatable cash flows

Approximately 2,400 employees

Financial snapshot:

− Market Cap: ~$3.13 billion

− Pro-forma EBITDA: $400 million

(1) Represents estimated pre-G&A pro-forma segment EBITDA for the fiscal year ending 3/31/2013 and excludes acquisition cost addbacks.

Area of Operations

Contribution by Segment to EBITDA

Eagle Ford

MarcellusShale

DJBasin

Green River Basin

BakkenShale

Mississippi Lime

Granite Wash

PermianBasin

Eagle Ford

MarcellusShale

DJBasin

Green River Basin

BakkenShale

Mississippi Lime

Granite Wash

PermianBasin

Crude Barges

Water Services

Railcar NGL terminal

Refinery terminal

NGL proprietary terminal

Natural gas liquids segment

NGL leased storage

Assets and marketing presence

Pipeline

Crude oil segment

Crude barge terminal

NGL

Retail Propane > 10 mm gallons

Crude operational area

Crude Barges

Water Services

Railcar NGL terminal

Refinery terminal

NGL proprietary terminal

Natural gas liquids segment

NGL leased storage

Assets and marketing presence

Pipeline

Crude oil segment

Crude barge terminal

NGL

Retail Propane > 10 mm gallons

Crude operational area

2

• Confidential & Proprietary• Confidential & Proprietary

Retail Propane

15%

Crude Logis-tics48%

Water Solu-tions23%

NGL14%

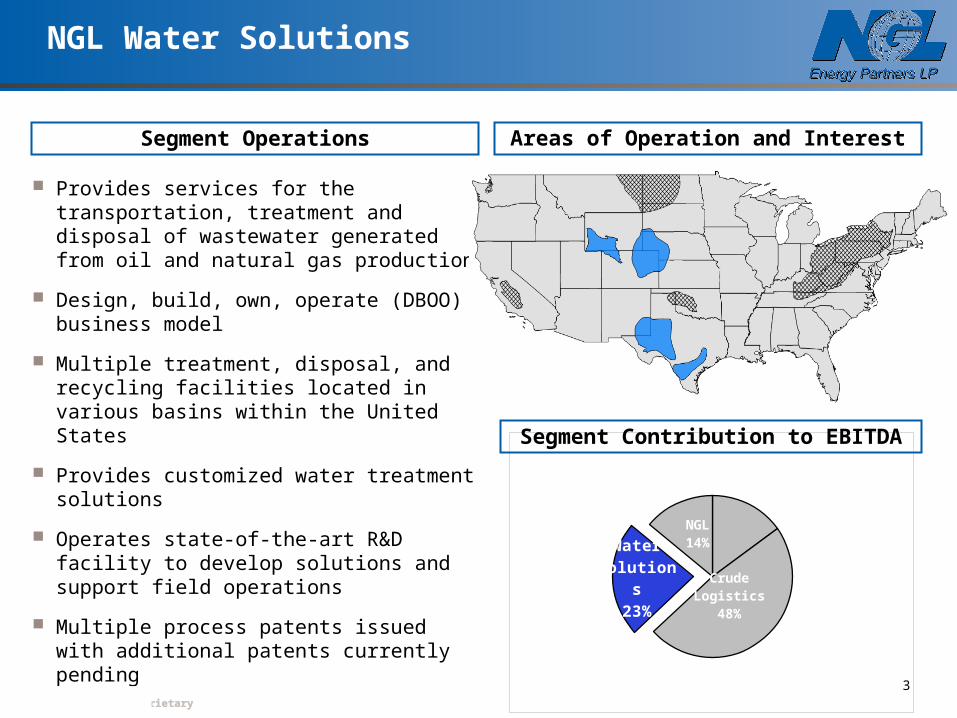

Segment Contribution to EBITDA

Areas of Operation and InterestSegment Operations

NGL Water Solutions

Provides services for the transportation, treatment and disposal of wastewater generated from oil and natural gas production

Design, build, own, operate (DBOO) business model

Multiple treatment, disposal, and recycling facilities located in various basins within the United States

Provides customized water treatment solutions

Operates state-of-the-art R&D facility to develop solutions and support field operations

Multiple process patents issued with additional patents currently pending

3

• Confidential & Proprietary• Confidential & Proprietary

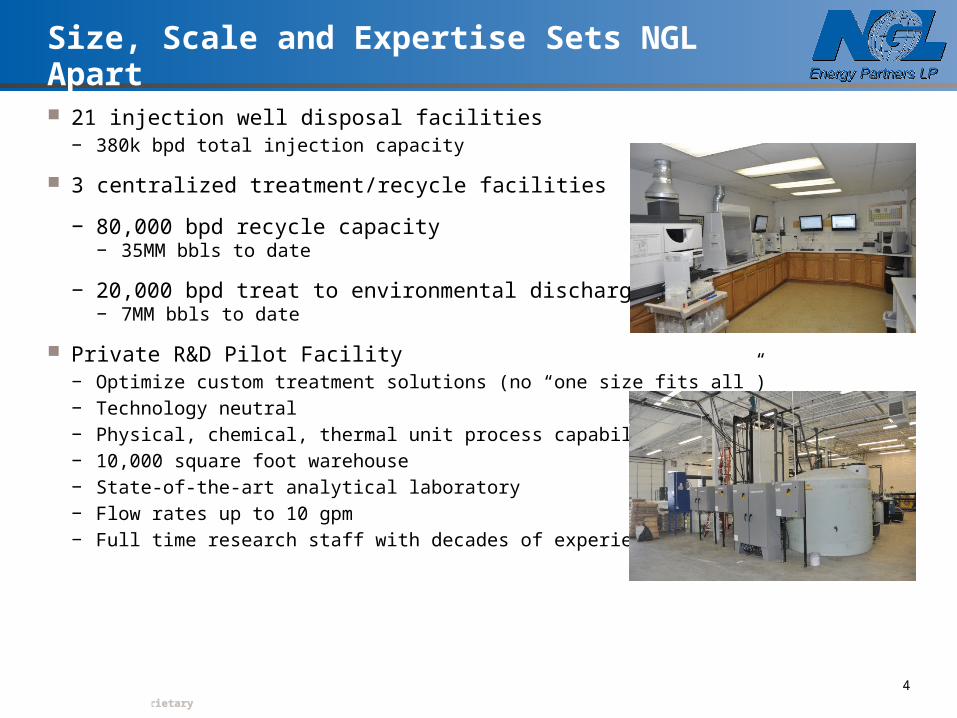

Size, Scale and Expertise Sets NGL Apart

21 injection well disposal facilities− 380k bpd total injection capacity

3 centralized treatment/recycle facilities

− 80,000 bpd recycle capacity− 35MM bbls to date

− 20,000 bpd treat to environmental discharge standard− 7MM bbls to date

Private R&D Pilot Facility− Optimize custom treatment solutions (no “one size fits all”)− Technology neutral− Physical, chemical, thermal unit process capabilities− 10,000 square foot warehouse− State-of-the-art analytical laboratory− Flow rates up to 10 gpm− Full time research staff with decades of experience

4

• Confidential & Proprietary• Confidential & Proprietary

Market Overview

5

• Confidential & Proprietary• Confidential & Proprietary

Observations

6

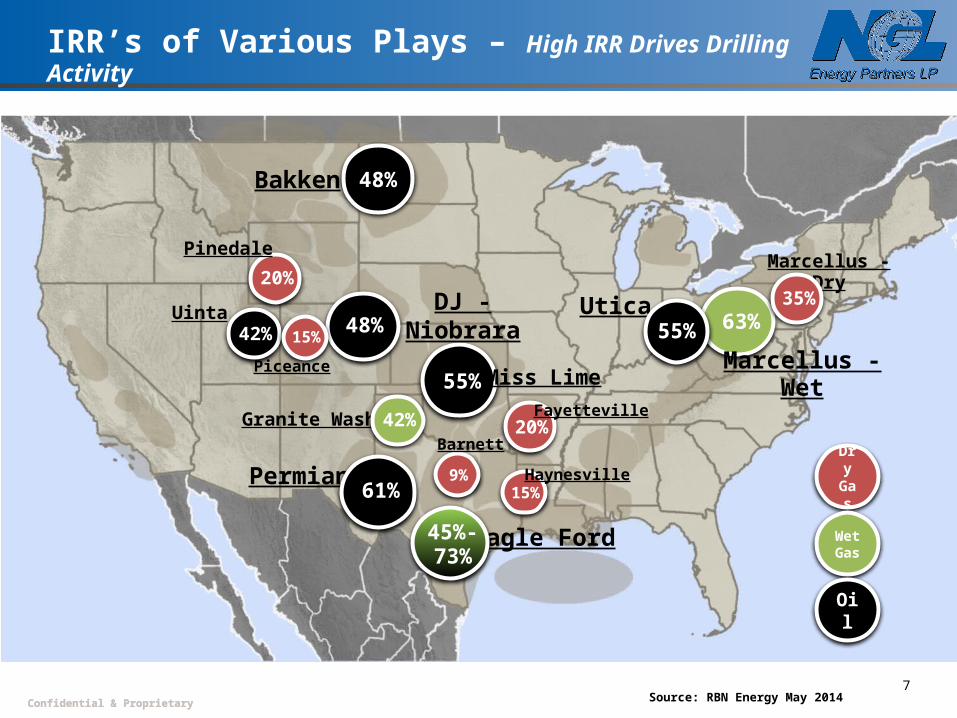

• High IRR plays incentivize drilling activity

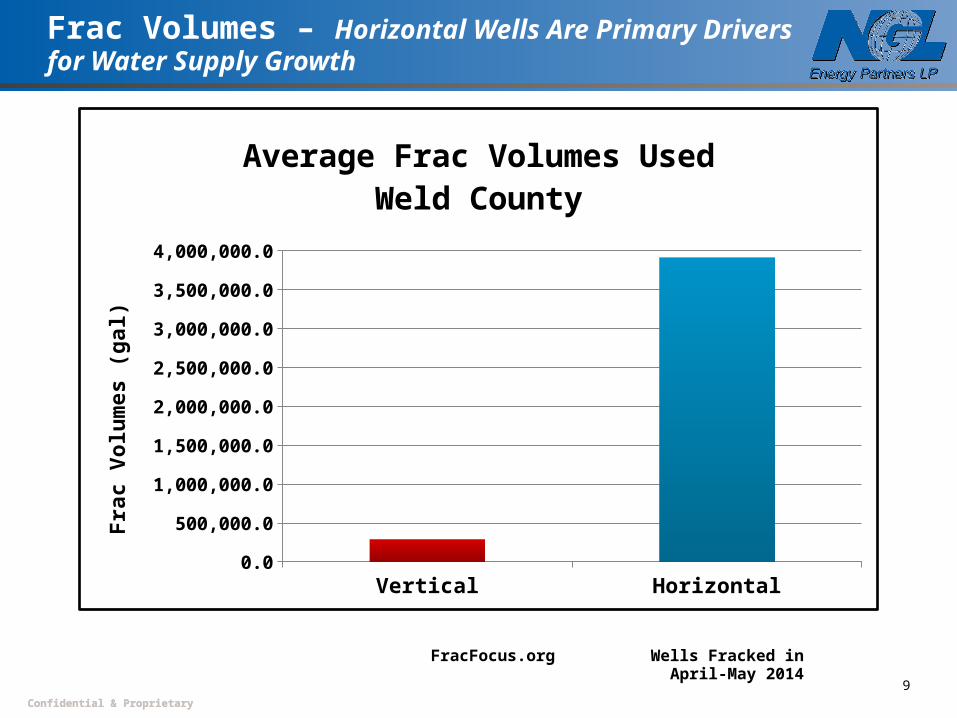

• Horizontal drilling activity is the largest driver of waste water production

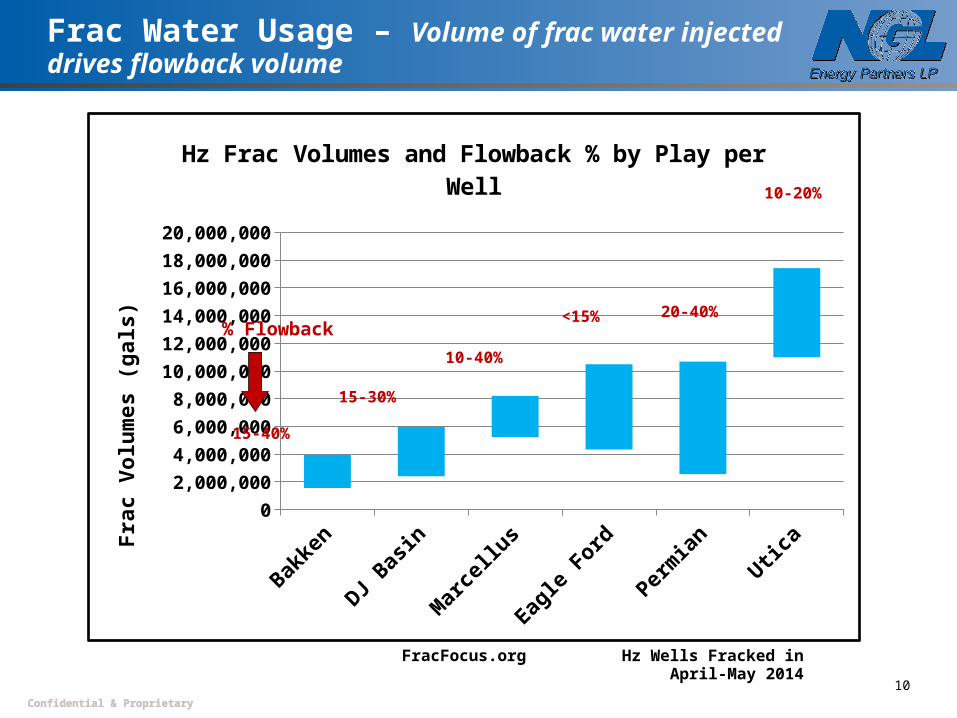

• Frac volumes and geology determine flowback volumes

• Treatment, recycle, reuse and/or disposal used for wastewater management, but typically disposal wells are the most cost effective when viable

• Disposal well viability hinges on geology, water quality, water quantity and economics

• Confidential & Proprietary• Confidential & Proprietary7

Source: RBN Energy May 2014

Utica

Marcellus - Dry

Uinta

Dry Gas

Wet Gas

Oil

20%

Piceance

Permian

Bakken

DJ -Niobrara

Eagle Ford

48%

Granite Wash

Miss Lime55%

42%

42%

Pinedale

IRR’s of Various Plays – High IRR Drives Drilling Activity

9%15%

15%

20%

48%35%

63%55%

45%-73%

61%Haynesville

Fayetteville

Barnett

Marcellus - Wet

• Confidential & Proprietary• Confidential & Proprietary

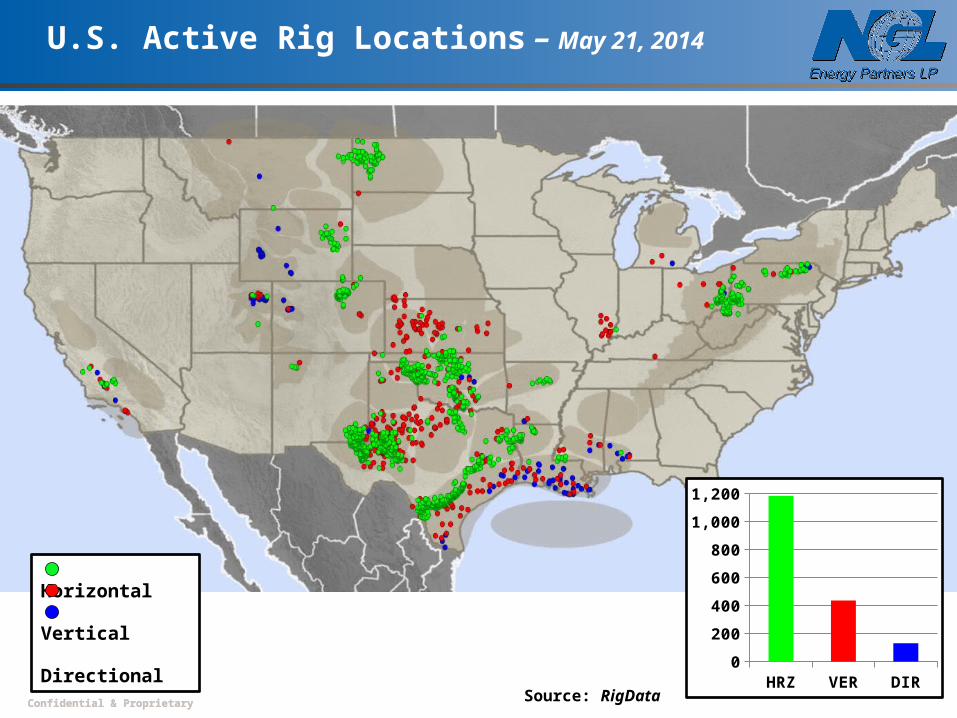

U.S. Active Rig Locations – May 21, 2014

Source: RigData

Horizontal Vertical Directional

HRZ VER DIR0

200

400

600

800

1,000

1,200

• Confidential & Proprietary• Confidential & Proprietary

Frac Volumes – Horizontal Wells Are Primary Drivers for Water Supply Growth

9

FracFocus.org Wells Fracked in April-May 2014

Vertical Horizontal0.0

500,000.0

1,000,000.0

1,500,000.0

2,000,000.0

2,500,000.0

3,000,000.0

3,500,000.0

4,000,000.0

Average Frac Volumes UsedWeld County

Frac

Vol

umes

(gal

)

• Confidential & Proprietary• Confidential & Proprietary

Frac Water Usage – Volume of frac water injected drives flowback volume

10

FracFocus.org Hz Wells Fracked in April-May 2014

Bakke

n

DJ Bas

in

Mar

cellu

s

Eagle

Ford

Perm

ian

Utica

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

Hz Frac Volumes and Flowback % by Play per WellF

rac

Vo

lum

es

(g

als

)

15-4

0%15

-30%

10-4

0%<1

5%20

-40%

10-2

0%

% Flowback

• Confidential & Proprietary• Confidential & Proprietary

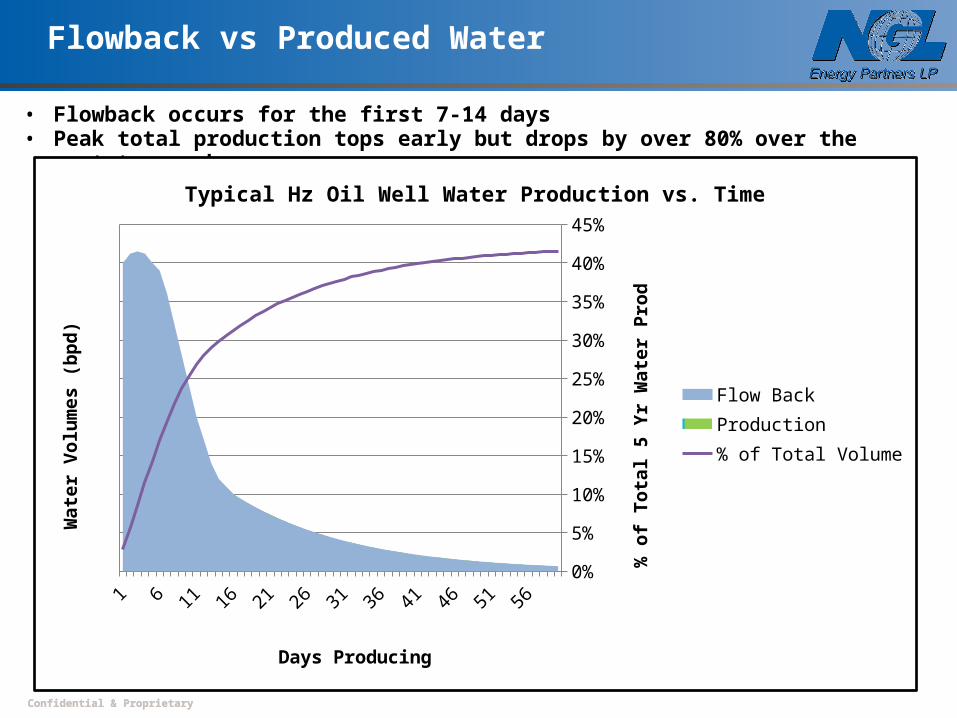

Flowback vs Produced Water

11

• Flowback occurs for the first 7-14 days• Peak total production tops early but drops by over 80% over the next two weeks

1 5 9 13 17 21 25 29 33 37 41 45 49 53 570%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Typical Hz Oil Well Water Production vs. Time

Flow BackProduction% of Total Volume

Days Producing

Wa

ter

Vo

lum

es

(b

pd

)

% o

f T

ota

l 5 Y

r W

ate

r P

rod

• Confidential & Proprietary• Confidential & Proprietary

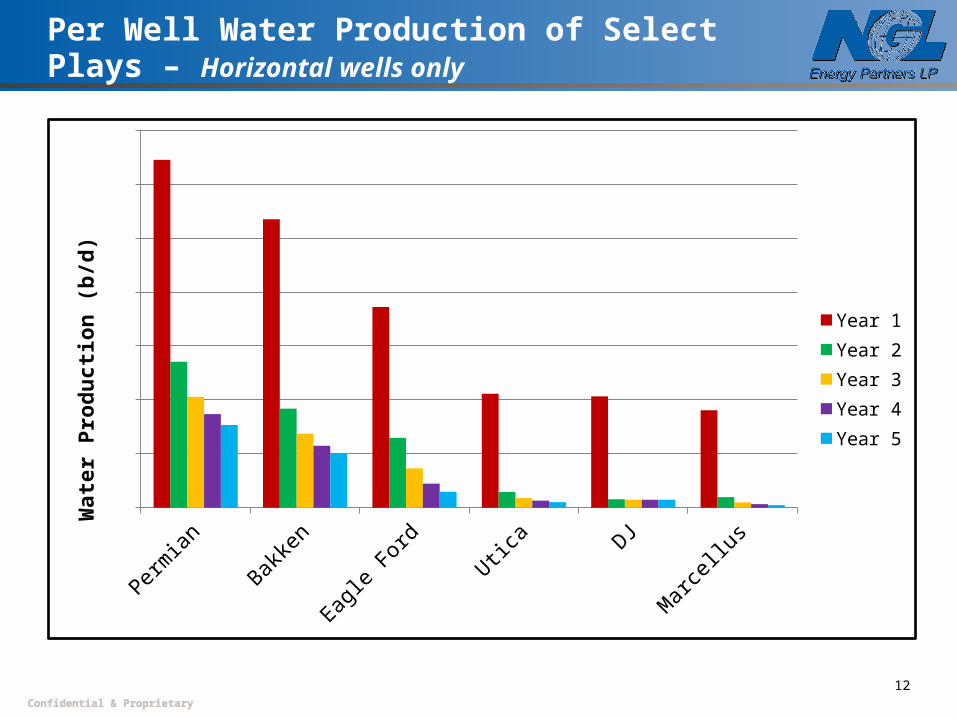

Per Well Water Production of Select Plays – Horizontal wells only

Year 1Year 2Year 3Year 4Year 5

Wa

ter

Pro

du

cti

on

(b

/d)

12

• Confidential & Proprietary• Confidential & Proprietary

Produced Water Generation in Shale Plays: Dependent on Geology of Shale Formation

High “Long Term” Produced Water Generating PlayPermian:

− Formation characteristics result in high produced water generation− Higher volumes of natural formation water present in / near shale

Moderate “Long Term” Produced Water Generating PlaysEagle Ford Shale

Bakken− Formation characteristics allow less fluid production per MMCF/bbl− Relatively dry formation

Low “Long Term” Produced Water Generating PlaysDJ, Utica, Marcellus Shale

Higher water production in South (West Virginia), lower in North (Pennsylvania)− Shale formation characteristics tend to “trap” fluids− Very dry formation− Water is “bound to formation”

Source: CHK13

• Confidential & Proprietary• Confidential & Proprietary

Disposal Wells vs Alternative Methods

Disposal− Provide producers affordable well-disposal of wastewater − Water treatment separates solids and hydrocarbons from water prior to

disposal− Certain facilities are pipeline connected, providing stronger customer

relationship with the producers

Treatment for Re-Use− Clean water can be re-used by producers for fracking, well drilling and

completion projects− Offers producers an alternative to fresh water that minimizes the impact on

aquifers, particularly in arid regions of the U.S.

Treatment for Discharge − Cleans water to environmental discharge water quality

Resource Recovery− Create high purity brine from oilfield waste water− Apply crystallization or chlor-alkali process− Yields valuable chemical products in lieu of waste stream

14

Low Tech$

High Tech$$$$

• Confidential & Proprietary• Confidential & Proprietary

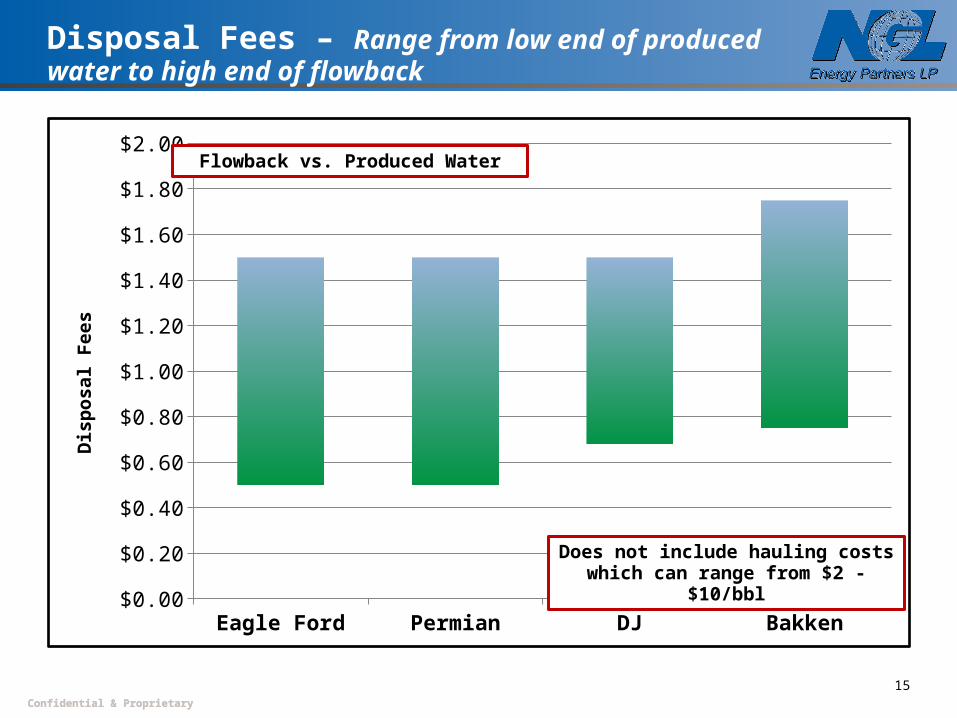

Disposal Fees – Range from low end of produced water to high end of flowback

15

Eagle Ford Permian DJ Bakken$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

Dis

po

sa

l Fe

es

Does not include hauling costs which can range from $2 - $10/bbl

Flowback vs. Produced Water

• Confidential & Proprietary• Confidential & Proprietary

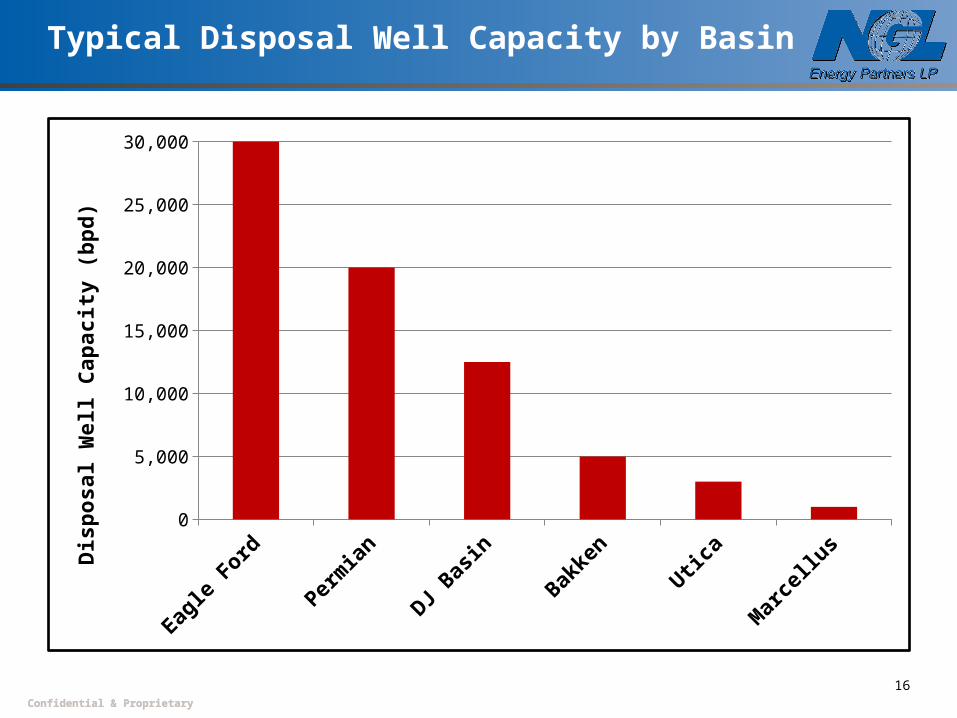

Typical Disposal Well Capacity by Basin

16

0

5,000

10,000

15,000

20,000

25,000

30,000

Dis

po

sa

l W

ell

Ca

pa

cit

y (

bp

d)

• Confidential & Proprietary• Confidential & Proprietary17

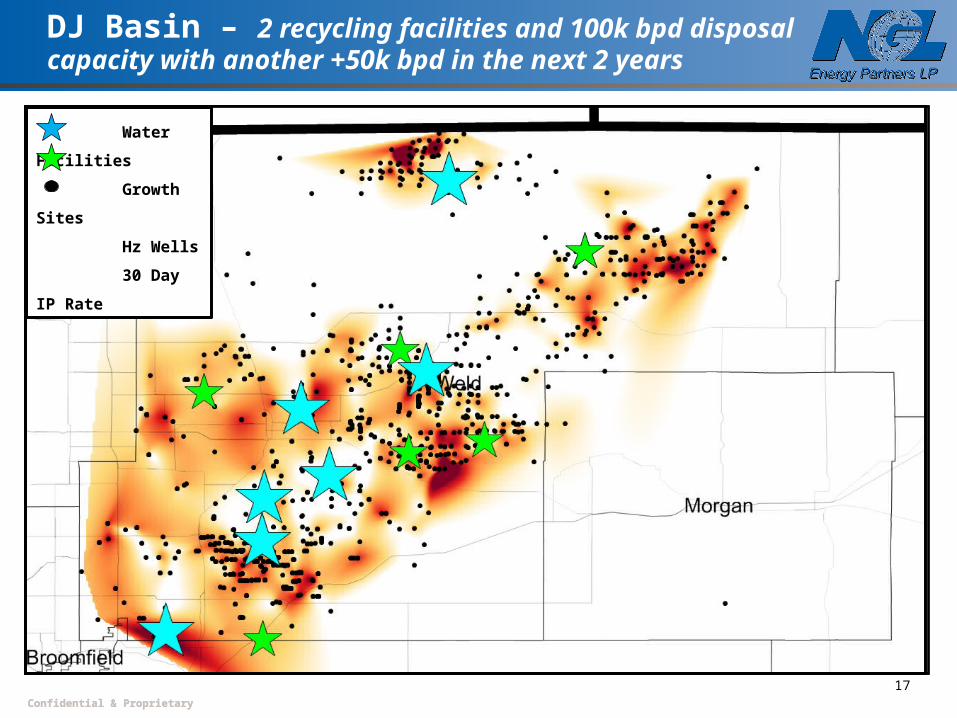

DJ Basin – 2 recycling facilities and 100k bpd disposal capacity with another +50k bpd in the next 2 years

Water Facilities

Growth Sites

Hz Wells

30 Day IP Rate

• Confidential & Proprietary• Confidential & Proprietary

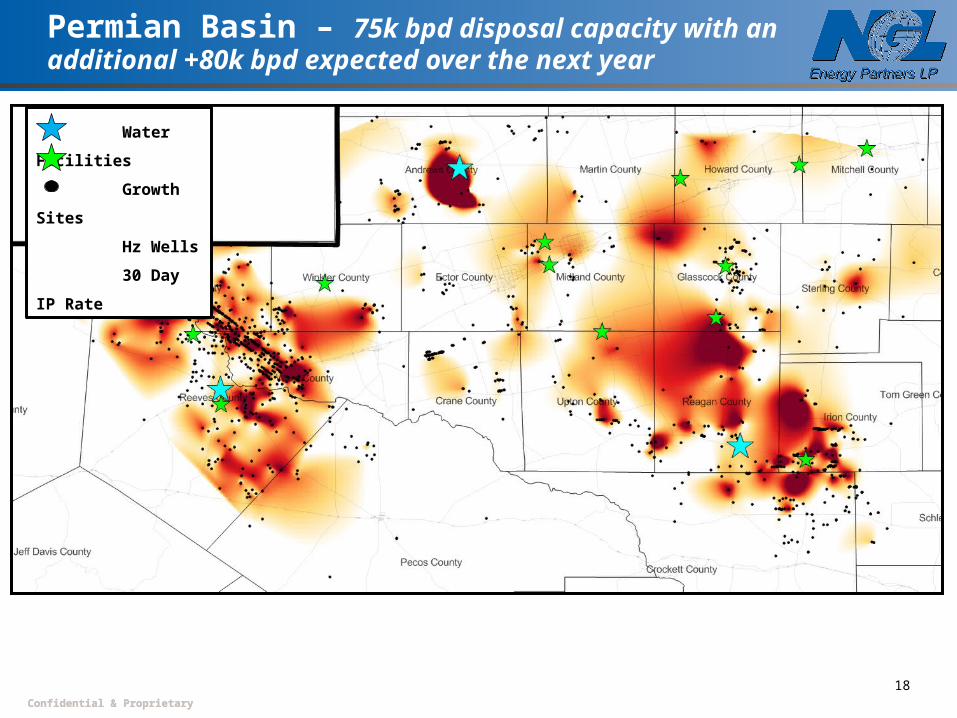

Permian Basin – 75k bpd disposal capacity with an additional +80k bpd expected over the next year

18

Water Facilities

Growth Sites

Hz Wells

30 Day IP Rate

• Confidential & Proprietary• Confidential & Proprietary

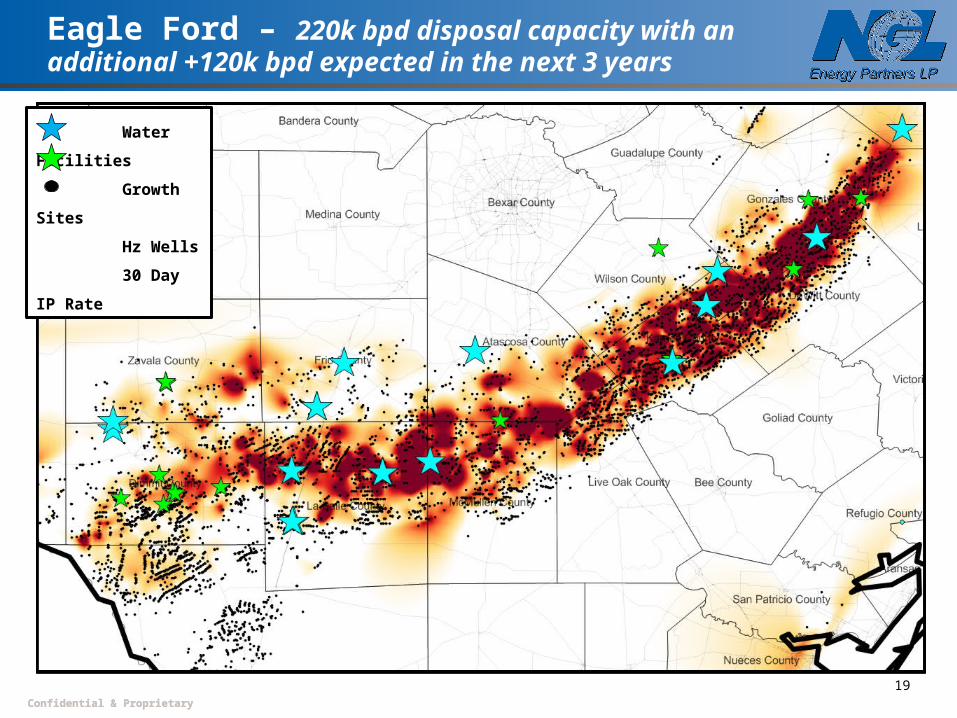

Eagle Ford – 220k bpd disposal capacity with an additional +120k bpd expected in the next 3 years

19

Water Facilities

Growth Sites

Hz Wells

30 Day IP Rate

• Confidential & Proprietary• Confidential & Proprietary

Conclusions

20

• High IRR plays incentivize drilling activity

• Horizontal drilling activity is the largest driver of waste water production

• Frac volumes and geology determine flowback volumes

• Treatment, recycle, reuse and/or disposal used for wastewater management, but typically disposal wells are the most cost effective when viable

• Disposal well viability hinges on geology, water quality, water quantity and economics

• NGL Water Solutions has a DBOO business model that provides customized wastewater management solutions

• Confidential & Proprietary• Confidential & Proprietary

Eric PetersonStrategic Planning & Market [email protected]

21

Contact Information

Greg BlaisVP – Business [email protected]