Embed Size (px)

Citation preview

HUMAIRA KAYANI

RABIA ZAMEER

AYESHA SHAUKAT

ANSA JAVED

ZAHIDA PARVEEN

Presented by

VALUATION OF DEBT SECURITIES BY MUTUAL FUNDS

SEBI Circular Dated

October 18, 2008

Topics to be Covered

Introduction Circular dated September 18, 2000 Clause 1 Clause 2 Circular dated February 20, 2002 Clause 4 Proposed amendments in SEBI circular dated

October 18, 2008

Introduction to Circular

This is in partial modification of SEBI Circular September 18, 2000 and February 20, 2002 which, inter-alia, specified the discount adjustments for debt securities rated by external agencies for

Ill-liquidity Risk Promoter Background Finance Company Risk Issuer Class Risk

Introduction (contd…)

It has been brought to the notice of SEBI by AMFI and CRISIL that the current valuation methodology which allows the discretion of -50 basis points (bps) to 100 bps to account for the aforesaid risks is inadequate as debt securities of similar maturity and credit rating are being traded over wide range of yields.

With a view to ensure that the value of debt securities reflects the current market scenario in calculation of net asset value, it has been decided to increase the discretion permitted.

Circular - September 18, 2000 (Clause 1)

GUIDELINES FOR VALUATION OF SECURITIES FOR MUTUAL

FUNDS

Types of Securities:

Traded Securities

Thinly Traded Securities

Non Traded Securities

Methodology:

Construction of Risk Free Benchmark

Building a Matrix of Spreads for Marking-up the Benchmark Yield

Mark-up/Mark-down Yield

Circular - September 18, 2000 (Clause 2)

Guidelines For Identification and

Provisioning for Non Performing Assets

(Debt Securities) For Mutual Funds

Definition of a Non Performing Asset (NPA):

An ‘asset’ shall be classified as non performing, if the interest and/or principal amount have not been received or remained outstanding for one quarter from the day such income / installment has fallen due.

Effective date for classification of NPAs:

The definition of NPA may be applied after a quarter past due date of the interest. e.g. if the due date for interest is 30.06.2000, it will be classified as NPA from 01.10.2000.

Provision for NPAs – Debt Securities.

After the expiry of the 1st quarter from the date the income has fallen due, there will be no further interest accrual on the asset.

e.g. if the due date for interest falls on 30.06.2000 and if the interest is not received, accrual will continue till 30.09.2000 after which there will be no further accrual of income.

Provision for NPAs – Debt Securities:

Duration Asset declared

3 months OAEM(other asset especially mentioned)

6 months SS(sub standard)

9 months Doubtful

12 months Loss

15 months Loss

Provision for NPAs – Debt Securities (contd…)

Effective day for provisioning

Minimum provision as % of book value

(outstanding principal amount)

Cumulative provisions

6 months 10% 10%

9 months 20% 30%

12 months 20% 50%

15 months 25% 75%

18 months 25% 100%

Circular - February 20, 2002(Clause 4)

Mark up/ Mark down Yield:

The discount adjustments provided for securities rated by external rating agencies and internally rated securities on page 5 [Clauses C(I) & C(II)] of the circular dated September 18, 2000, shall be revised as follows:

Mark up/ Mark down Yield

Category Discretionary discount over benchmark yield in basis points

Rated Instruments with duration up to 2 years

Discretionary Discount of up to +100

Rated Instruments with duration over 2 years

Discretionary Discount of up to +75

Unrated Instruments with duration up to 2 years

Discretionary Discount of up to +50 over and above the mandatory

Discount of +50

Unrated Instruments with duration over 2 years

Discretionary Discount up to +50 over and above the mandatory Discount of

+25

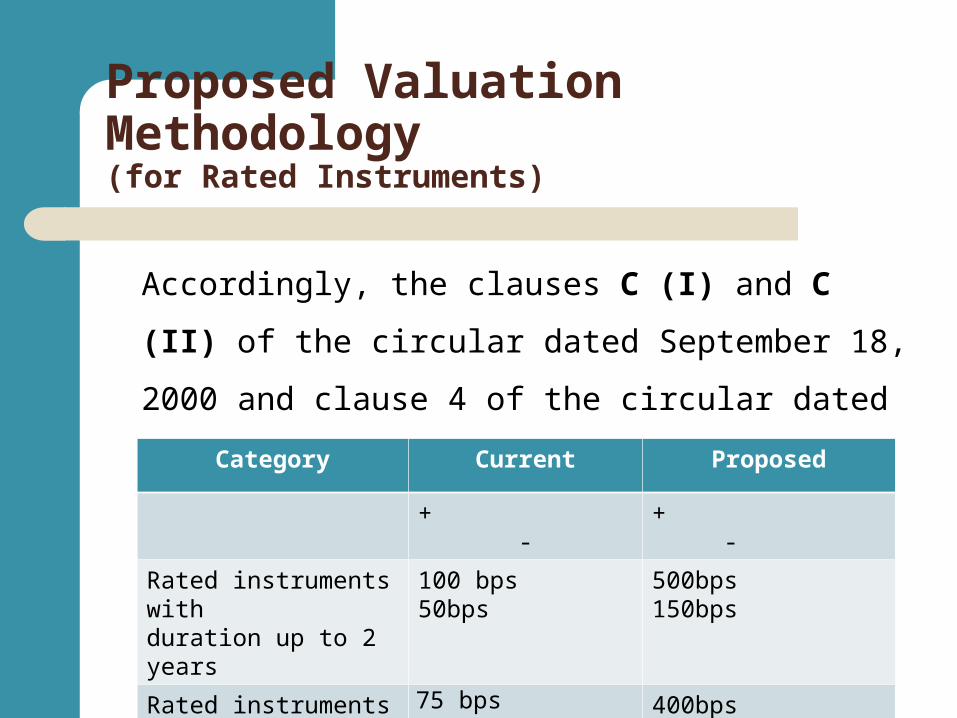

Proposed Valuation Methodology(for Rated Instruments)

Accordingly, the clauses C (I) and C (II) of the circular

dated September 18, 2000 and clause 4 of the circular

dated February 20, 2002 shall be revised as follows:

Category Current Proposed

+ - + -

Rated instruments withduration up to 2 years

100 bps 50bps 500bps 150bps

Rated instruments withduration over 2 years

75 bps 25bps 400bps 100bps

Proposed Valuation Methodology(for Unrated Instruments)

Category Current Proposed

+ - + -

Unrated instruments withduration up to 2 years

Discretionary discount ofUp to +50 bps over andabove mandatorydiscount of +50 bps

Discretionarydiscount of up to +450 bps over and above mandatory discountof +50 bps

Unrated instruments withduration over 2 years

Discretionary discount ofUp to +50 bps over andabove mandatorydiscount of +25 bps

Discretionarydiscount of up to +375bps over and abovemandatory discountof +25 bps

References

This circular is issued in exercise of powers conferred under Section 11 (1) of the Securities and Exchange Board of India Act, 1992.with the provisions of Regulation 77 of SEBI (Mutual Funds) Regulations, 1996,

To protect the interests of investors in securities To promote the development of and to regulate the

securities market Other contents of the aforesaid circulars remain the

same.