Embed Size (px)

Citation preview

While every effort has been made to ensure accuracy, the Publisher does not accept responsibility for any errors or omissions and disclaims liability

for all claims, which may arise from any person acting on the material contained within the report.

HUNTER VALLEY COAL REPORT The Hunter Valley Coal Report is published weekly by Nadine Brierley

26 Princes Avenue Charlestown NSW 2290 Australia

Ph.: +61 2 4023 8050 ABN 92 506 051 400

© Copyright Nadine Brierley All rights reserved ISSN 1036-7454

26 May 2016 Number: 21/16

Bulga residents to withdraw legal challenge against Warkworth coal mine expansion......................................... 2

Port Waratah April coal shipments to China reach four month high at 1.32 million tonnes ................................. 2

ARTC announce Hunter Valley coal chain maintenance shutdown from 31 May to 03 June 2016 ...................... 3

Hume Coal will not appeal Southern Highlands land access decision ................................................................... 3

Wesfarmers plans to write down value of Curragh coal mine by between $600 to $850 million ......................... 4

Australian Pacific Coal estimates 1.2 billion tonnes coal resource at Dartbrook .................................................. 4

Queensland Government Chain of Responsibility working group membership announced ................................. 4

Gladstone Ports Corporation Barney Point Coal Terminal ships last coal ............................................................. 5

Queensland’s Mineral and Other Legislation Amendment Bill restores farmer & community rights on mining . 5

Queensland Government and Korea Development Bank sign MoU to unlock investment potential .................... 6

Company News – Paringa Resources, CS Energy, NSW Government, Gladstone Ports Corporation, Universal

Coal, Fircroft Group, Origin Energy, AJ Lucas Group, Ausdrill, Lycopodium, Australian Competition and

Consumer Commission .......................................................................................................................................... 6

Safety ...................................................................................................................................................................... 8

Diary Dates ............................................................................................................................................................ 9

Personnel .............................................................................................................................................................. 10

HVCCC Weekly Performance Report .................................................................................................................. 11

Coal Statistics ....................................................................................................................................................... 12

Port Waratah Coal Services Monthly Report – April 2016 .................................................................................. 12

Transcoal Port Congestion Graph East Coast Australia ....................................................................................... 13

Braemar Seascope Weekly Focus ........................................................................................................................ 14

Exchange Rates .................................................................................................................................................... 16

Thermal Coal Swap Bids ...................................................................................................................................... 16

Hunter Valley Coal Report is in it’s 26th

year of publication

26 May 2016 Hunter Valley Coal Report No 21/16 2

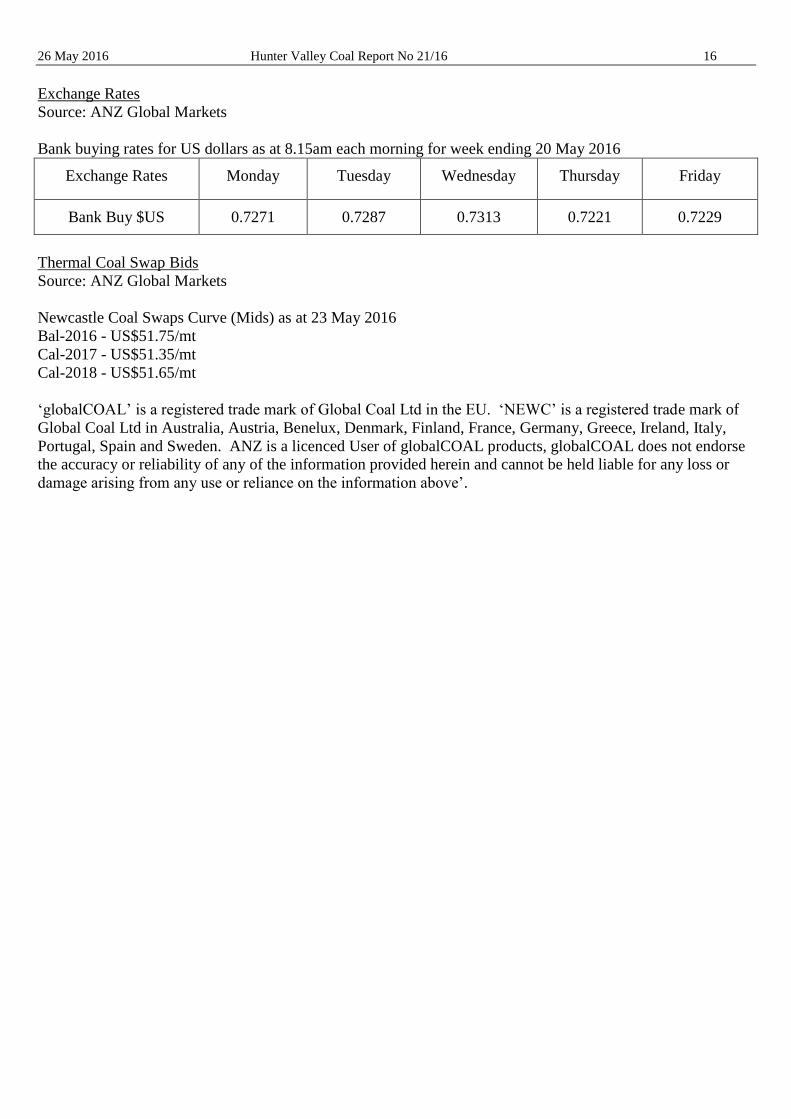

Exchange Rates Monday Tuesday Wednesday Thursday Friday

Bank Buy $US 0.7271 0.7287 0.7313 0.7221 0.7229

Bank buying rates for US dollars as at 8.15am each morning for week ending 20 May 2016

Bulga residents to withdraw legal challenge against Warkworth coal mine expansion

The Bulga Milbrodale Progress Association Inc. (BMPA) has announced that it has discontinued legal

proceedings that were challenging the November 2015 decision by the Planning Assessment Commission

(PAC) to approve Rio Tinto’s Warkworth mine expansion.

BMPA said that it’s legal team, EDO NSW has advised that after inspecting all of the documents in the

Government offices provided as part of the proceedings, it’s grounds of challenge to protect the uncertain future

of the Warkworth Sands Woodlands would not be able to succeed in the court.

EDO NSW advised that in their view, the PAC, following the advice of the NSW Department of Planning, did

all that they were required to do under the law to protect the critically endangered Warkworth Sands Woodland,

notwithstanding the strong evidence that this mine will push it to extinction.

Port Waratah April coal shipments to China reach four month high at 1.32 million tonnes

Platts has reported that China’s offtake from the Port Waratah coal terminals touched a four-month high in

April at 1.32 million mt, including 70,000 mt shipped to Hong Kong - a 43% increase on 922,000 mt in March.

Coal shipments from Port Waratah’s two coal terminals at Newcastle port to China have come off a low of

580,000 mt in January, and were 1.44 million mt in December.

For the January-April period, China has lifted 3.6 million mt of coal from the PWCS terminals, down from 5.3

million mt in the corresponding four-month period last year.

Japan maintained a steady offtake at the PWCS terminals last month at 4.44 million mt, up from 4.14 million

mt in March.

Last month’s shipments to Japan bring the Asian country’s year-to-date total to 17.1 million mt, and higher than

16.57 million mt for the year-ago period.

According to Platts, port data said that South Korean buyers took delivery of 840,000 mt of coal exports at the

PWCS terminals in April, taking their year-to-date total to 4.98 million mt, down from 5.8 million mt for

January-April 2015.

Taiwan booked 1.1 million mt of coal exports from PWCS terminals for April, down slightly on 1.24 million

mt in March.

India was a destination for only 134,000 mt of coal exports shipped from the PWCS terminals last month, up

from only 35,000 mt in March.

India’s year-to-date shipments total is 552,000 mt, compared with 175,000 mt for the January-April 2015

period, said PWCS data.

Last month, PWCS coal shipments to Mexico, Malaysia and Thailand added up to 988,000 mt, as miners seek

to diversify their customer base with China’s demand pulling back.

26 May 2016 Hunter Valley Coal Report No 21/16 3

Thermal coal accounted for 7.93 million mt of total coal exports from the PWCS terminals in April, or 86%,

and semi-soft coking coal exports were 1.3 million mt or 14%, the data showed.

In April 2015, only 10% of coal exports at the PWCS terminals were semi-soft coking coal and 90% was

thermal coal, indicating that coal shippers such as Rio Tinto and Whitehaven have increased their output of

semi-soft coal over the past year.

Source: Platts.

ARTC announce Hunter Valley coal chain maintenance shutdown from 31 May to 03 June 2016

The Australian Rail Track Corporation (ARTC) has announced a network maintenance shutdown of the Hunter

Valley coal chain between the Port and Narrabri, which commences from early morning of Tuesday 31 May to

6am Friday 3 June. Ulan line works from Muswellbrook to Ulan will run slightly longer from 6am Tuesday to

8pm on Friday.

ARTC Executive General Manager Hunter Valley, Jonathan Vandervoort said that over 100 projects to improve

throughput and reliability are scheduled to take place, furthering the Hunter Valley coal chain’s already high

level of service delivery.

“There are multiple components that intricately work together for the rail network to perform well and it

requires an in-depth check-up and regular maintenance to ensure it continues running safely for over 250 train

services a day.”

Typical rail maintenance tasks like replacing sleepers, cleaning and compacting ballast, welding rail and

technical jobs like signalling work will also take place.

The next major, network-wide maintenance shutdown is planned for 23-25 August. There will also be some

weekend maintenance trackwork around the port 11-13 June.

Hume Coal will not appeal Southern Highlands land access decision

Hume Coal has announced that it has ruled out seeking leave to appeal the recent Southern Highlands land

access decision handed down by Chief Justice Brian Preston of the NSW Land and Environment Court (“s31

Appeal Decision”).

Greig Duncan, Hume Coal Project Director, said that land access for exploration and mining companies has

been an ongoing issue in NSW for decades.

“It is now a matter of urgency and up to the State Government to take this issue seriously and implement

changes to the legislation which clarify the rights of landowners, explorers and ultimately investors in NSW,”

he said.

Mr Duncan said that an appeal of Chief Justice Preston’s ruling would be futile. The s31 Appeal Decision did

not even address an earlier decision by Sheahan J in Hume Coal Pty Limited v Alexander (No 3) [2013] NSW

LEC 58 that is clearly inconsistent with the s31 Appeal Decision, leaving the NSW mining law jurisprudence in

disarray.

Mr Duncan said that the ball is now in the State Government’s court. If Government are looking for investment

in NSW to continue, they must address the legislation with a matter of urgency.

26 May 2016 Hunter Valley Coal Report No 21/16 4

Wesfarmers plans to write down value of Curragh coal mine by between $600 to $850 million

Wesfarmers Limited has announced plans to write-down the value of it Curragh coal mine in Queensland by

between $600 million to $850 million.

The Company said that the write down mainly reflects a slower forecast recovery in long term export coal

prices and higher volatility (including in exchange rates).

The effect of this impairment charge will be to write down the depreciable and amortisable assets of Curragh.

Wesfarmers said that notwithstanding challenging market conditions, Curragh has maintained its relative low

cost position and very strong safety record, and will continue to seek to deliver further benefits in these areas.

Australian Pacific Coal estimates 1.2 billion tonnes coal resource at Dartbrook

Australian Pacific Coal Limited has announced that a report commissioned ahead of the Dartbrook Project

acquisition has identified a Total Coal Resource Estimate of 1.2 billion tonnes, comprising 446 million tonnes

of Measured, 449 million tonnes of Indicated and 249 million tonnes of Inferred Resources to a maximum

depth of 350 metres for the project.

Coal quality analysis demonstrates the ability to produce a range of thermal coal products between 10% to 18%

ash on an air dried basis.

Australian Pacific Coal , Chief Executive Officer of John Robinson Jnr said that the Coal Resource Estimate

confirms Dartbrook as one of the largest under developed coal operations in the Hunter Valley, reaffirming the

company’s belief that Dartbrook is a tier 1 mining asset that has the potential to create a significant number of

job opportunities for the local community.

“The high quality of Dartbrook’s coal will also help to meet global demand for low ash premium thermal coal.”

said Mr Robinson.

Queensland Government Chain of Responsibility working group membership announced

The Queensland Government has announced the membership of the Chain of Responsibility working group, to

assist in developing a statutory guideline to complement the Environmental Protection (Chain of

Responsibility) Amendment Act 2016.

The Chain of Responsibility laws protect the taxpayer and the environment when a major resources company

closes its doors without cleaning-up and rehabilitating its site of operations.

The working group will consist of:

Queensland Resources Council

Australian Banker’s Association

Australian Petroleum Production and Exploration Association

Queensland Law Society

Chamber of Commerce and Industry Queensland

Association of Mining and Exploration Companies Inc

Queensland Environmental Law Association

Australian Institute of Company Directors

Australian Restructuring Insolvency and Turnaround Association

Environmental Defenders Office

26 May 2016 Hunter Valley Coal Report No 21/16 5

Gladstone Ports Corporation Barney Point Coal Terminal ships last coal

Gladstone Ports Corporation (GPC) and the port community will mark a significant milestone this month with

GPC’s Barney Point Terminal receiving and exporting its final coal and the subsequent closure of coal

operations at the terminal.

Leo Zussino, Chairman of GPC, advised that the closure of coal operations at the terminal is in line with GPC’s

50 Year Strategic Plan and commitment to the communities in which it operates, and will enable operations at

Barney Point to focus on other dry bulk and possible new trade opportunities.

“In 2008, as part of GPC’s commitment to a healthier environment for the Gladstone community, Gladstone

Ports Corporation announced that coal operations at Barney Point Terminal would cease during the first year of

continuous operations at the Wiggins Island Coal Terminal. This commitment has now been fulfilled,” Mr

Zussino stated.

Mitsui Coal Holdings (then Mitsui and Co.) was an original joint venture owner of the Barney Point Terminal,

which was established to export coal from the Moura mine in which Mitsui has continued part ownership since

the commencement of operations in the early 1960s.

The Barney Point Coal Terminal was constructed in 1967 by joint venture, Thiess Peabody Mitsui.

Operations commenced at the terminal in August 1967 with 1,600 tonnes of Moura coal exported on 9 August

of that year.

GPC purchased the facility from BHP Mitsui Coal in November 1998, extending the capacity of its bulk

handling operations.

The Barney Point Terminal received its last coal train on Saturday, 7 May 2016 and exported it’s final shipment

of coal to Japan on Thursday 19 May 2016.

Acting Chief Executive Officer, Michael Galt said GPC had confirmed that the closure of coal operations at

Barney Point Terminal would not impact permanent employee numbers due to port growth, new trade

opportunities and the continued utilisation of the RG Tanna Coal Terminal.

Queensland’s Mineral and Other Legislation Amendment Bill restores farmer & community rights on mining

Queensland Parliament has passed legislation that protects farm infrastructure and restores community

objection rights, restoring balance between the rights of farmers, miners, and the community.

Queensland Minister for State Development and Natural Resources and Mines Minister Dr Anthony Lynham

told Parliament that the Mineral and Other Legislation Amendment Bill fulfilled two Palaszczuk Government

commitments to farmers and to community groups.

Landholders will retain:

a minimum 50 metre protection zone around key agricultural infrastructure such as principal stockyards,

bores and artesian wells, dams and artificial water storages connected to a water supply

the right to prevent any mining lease being granted over restricted land without the consent of the owner

the security of knowing ministers cannot extinguish restricted status for their land – a power a minister

would have had under the LNP’s proposed laws.

26 May 2016 Hunter Valley Coal Report No 21/16 6

Community members will retain rights they would have lost under the LNP laws:

to have their say on mining lease and environmental authority applications for mining projects

to be advised of any proposed mining projects through ads in newspapers.

Dr Lynham said that the resource sector would benefit from the Queensland Land Court having a new power to

strike out any frivolous or vexatious objections.

The changes take effect on September 27 2016.

Queensland Government and Korea Development Bank sign MoU to unlock investment potential

The Queensland Government has signed a Memorandum of Understanding (MoU) with the Korea

Development Bank (KDB), to help unlock significant investment opportunities across Queensland including in

infrastructure, energy and natural resources.

Queensland Deputy Premier and Minister for Trade and Investment Jackie Trad said the new partnership was a

strong vote of confidence in Queensland.

“This is the first agreement of this kind that KDB has signed with any Australian Government – State or

Federal,” Ms Trad said.

“KDB is Korea’s leading policy bank and has been a driving force behind Korea’s economic development for

more than 60 years, so this partnership is a real coup for Queensland.

“KDB has already participated in Queensland projects as one of the lenders to the senior and subordinated debt

on Wiggins Island Coal Export Terminal and through its subsidiary, KIAMCO (KDB Infrastructure Investment

Asset Management Company), as an investor in the Millmerran Power Station.

“Officiating this partnership between Queensland and KDB will not only build upon our state’s amicable

relationship with South Korea, but it will also unlock even more opportunities for engagement between Korean

investors and Queensland companies.”

“This MoU will allow us to support Korean companies exploring new projects and investment opportunities in

Queensland particularly in, but not limited to, infrastructure, energy and natural resources,” she said.

Company News – Paringa Resources, CS Energy, NSW Government, Gladstone Ports Corporation, Universal

Coal, Fircroft Group, Origin Energy, AJ Lucas Group, Ausdrill, Lycopodium, Australian Competition and

Consumer Commission

Paringa Resources Limited has amended it’s coal sales contract with Louisville Gas and Electric Company

and Kentucky Utilities Company (“LG&E and KU”) following the Company’s recent change in strategy which

will see the low capex Buck Creek No.2 mine developed first, ahead of the Buck Creek No.1 Mine’s proposed

3.8 million tons per annum (Mtpa) coal project. In October 2015, Paringa signed a coal sales agreement with

LG&E and KU to deliver coal from the No.1 Mine. In February 2016, the Company decided to develop the

No.2 Mine first following exceptional results from a Scoping Study which demonstrated the No.2 Mine to be a

high margin 1.8Mtpa mine with low capex of only US$44 million. As a result, the amended cornerstone coal

sales agreement with LG&E and KU now reflects delivery of coal from the No.2 Mine. The amended contract

is on substantially the same terms as the original contract. Most importantly, coal volumes and coal

specifications remain unchanged. Fixed sale prices have changed slightly to reflect recent sales data, and the

project development milestones and delivery schedule have been updated for the No.2 Mine. Paringa is

expected to start construction of the No.2 Mine during second quarter of 2017, begin production by mid-2018,

and reach full production of 1.8Mtpa during 2019.

26 May 2016 Hunter Valley Coal Report No 21/16 7

CS Energy has extended its contract with Golding to operate the Kogan Creek Mine near Chinchilla in South

West Queensland. The companies have agreed terms to extend the current contract to at least July 2019, with

the potential for Golding to operate the mine until 30 June 2022. The Kogan Creek Mine employs 75 people

and supplies approximately 2.5 million tonnes of coal per year to the neighbouring coal-fired Kogan Creek

Power Station. CS Energy owns both the power station and mine.

NSW Government has announced that the process to sell about 44,000 hectares of land in the State’s Central

West for agricultural use will begin in the coming months. It was announced in 2015 that the land, initially

purchased for the development of a coal mine at Cobbora, would be sold for agricultural use. The land will be

sold by competitive tender, public auction or private sale depending on the land being offered. The government

said that it intends to sell the land in parts rather than as one lot in order to both maximise value and to enable

smaller investors to bid, including existing licence and lease holders. Sale proceeds will be directed to Restart

NSW, to be invested into new infrastructure across the State. The Cobbora Holding Company will continue to

keep current licence and lease holders up to date on developments. All licence and lease holders are invited to

participate in the sale process.

Gladstone Ports Corporation funding from the 2016 Botanic to Bridge FunD Run will be directed to

Roseberry Community Services’ Branchout programme to assist disadvantaged young people in Gladstone.

The funding will be used to build a new kitchen facility that will be used in the organisation’s Branchout

programme to facilitate cooking programs and assist young people to gain skills in hospitality.

Universal Coal Plc has provided an update on the Coal of Africa Limited (CoAL) recommended offer for the

entire issued and to be issued share capital of Universal Coal. It was announced on 13 May 2016 by CoAL that

the Offer Period of the Offer had been extended, such that the Closing Date is 24 June 2016. Pursuant to a

Deed of Variation, CoAL and Universal have agreed to amend the terms of the Cooperation Agreement entered

into between the parties in connection with the Offer, such that the date by which the Effective Date must have

occurred be extended until 3 June 2016, or such other date as the parties may agree. The Independent Universal

Directors have previously recommended and continue to recommend for the reasons set out in the Offer

Document that Universal shareholders accept the Offer, as they have irrevocably done in respect of their own

Universal Shares, subject to statutory and fiduciary exceptions that relate to the discharge of their duties as

directors.

Fircroft Group has announced it’s acquisition One Key Resources. Fircroft is a global workforce solutions

provider to the technical engineering sectors and has strengthened it’s position within the mining, minerals and

natural resources as a specialist provider of labour hire and managed workforce services to the mining, oil and

gas, and infrastructure industries. One Key, established in 2011, is a market leader in the supply of workforce

solutions to the mining industry in the Asia-Pacific region.

Origin Energy Limited has entered into an Asset Sale Agreement with SEA Gas (Mortlake) Partnership (SEA

Gas Mortlake) for the sale of Mortlake Pipeline for cash consideration of $245 million. Mortlake Pipeline,

which is currently operated by a related party of SEA Gas Mortlake, supplies gas to Origin’s Mortlake Power

Station in Victoria. Origin has secured long-term gas transportation and storage services on the pipeline.

AJ Lucas Group Limited has changed its registered office and principal administrative office:

Registered office and principal administrative office is now at Suite 6.01, Level 61 Elizabeth Plaza North

Sydney NSW 2060. Postal Address Locked Bag 2113 North Ryde BC NSW 1670. Phone +61 2 9490 4000

Fax +61 2 9490 4200

26 May 2016 Hunter Valley Coal Report No 21/16 8

Ausdrill Limited has signed a Sale and Purchase Agreement to sell its Drilling Tools Australia (“DTA”)

business to Robit Plc, is a Finnish manufacturer of high quality drilling products for $66 million. Ausdrill said

that the transaction is in line with it’s strategy to refocus on its core competencies. Ausdrill Managing Director

Ron Sayers said that the sale of DTA provides Ausdrill with the opportunity to crystallise considerable value on

a portion of the Group’s earnings, generating a profit after tax in the order of $35 million and allowing the

company to further pay down debt.

Lycopodium Limited has announced that it expects to achieve an improved outcome for the full 2015/16

financial year with a forecast after tax operating profit of at least $3 million on revenue of $126 million.

The Australian Competition and Consumer Commission (ACCC) has released a Statement of Issues on the

proposed acquisition of Asciano Limited by a consortium comprising Qube Holdings Ltd., Brookfield

Infrastructure Partners LP, and a group of global private equity and pension funds. ACCC Chairman Rod Sims

said that amongst concerns raised by market participants was the vertical integration of Patrick container

terminals with the two largest landside import-export container logistics providers in Australia, Qube and

ACFS. The ACCC considers this to be a significantly greater degree of vertical integration than the current

situation where Patrick is vertically integrated with only ACFS. “The ACCC is concerned that Patrick

container terminals may provide preferential access to Qube and ACFS vehicles, and Qube regional export

trains running into Port Botany, and raise rivals’ costs. Qube and Brookfield will each own 50 per cent of

Patrick container terminals, and may have parallel incentives to favour their landside logistics operations,” Mr

Sims said. Comments are invited from interested parties regarding the Statement of Issues. The closing date

for submissions is 10 June 2016.

Safety

Source: NSW Government

Weekly Incident Summary 18 May 2016

http://www.resourcesandenergy.nsw.gov.au/__data/assets/pdf_file/0004/656347/ISR16-19-Weekly-Incident-

Summary-18-May-2016.pdf

26 May 2016 Hunter Valley Coal Report No 21/16 9

Diary Dates

26 May

2016

National Sorry Day

1-2 Jun

2016

Australian Energy Storage Conference and Exhibition

Australian Technology Park

Sydney

NSW

8 Jun 2016 Australian Coal Preparation Society Qld Technical Meeting

https://www.acps.com.au/events/technical-meetings/qld-technical-meeting-8-june-2016-

brisbane/

29-31 May

2016

22nd

Coaltrans Asia

BICC

Bali

Indonesia

09 – 10Jun

2016

Mine Managers Association of Australia 2016 CPD Seminar

Caves Beachside Hotel

Caves Beach

NSW

15 Jun

2016

Australian Coal Preparation Society NSW Technical Meeting

Novotel Wollongong Northbeach

Wollongong

NSW

https://www.acps.com.au/events/technical-meetings/nsw-technical-meeting-15-june-2016-

wollongong/

28 Jun-01

Jul 2016

Australian Coal Preparation Society International Coal Preparation Congress

St Petersburg

Russia

https://www.acps.com.au/assets/Uploads/ICPC-2016-Notice.pdf

26-28 Jul

2016

Queensland Mining and Engineering Exhibition

Mackay Showground

QLD

http://www.queenslandminingexpo.com.au/

27-28 Jul

2016

Australian Clean Energy Summit 2016

The Hilton

488 George Street

Sydney

NSW

22-24 Aug

2016

AusIMM International Mine Management 2016

Brisbane

QLD

26 May 2016 Hunter Valley Coal Report No 21/16 10

25-26 Aug

2016

Coaltrans Australia

Novotel Sydney Central

Sydney

NSW

12-16 Sept

2016

Australian Institute of Mine Surveyors

ISM 2016 – XVI International Congress for Mine Surveying Brisbane Convention & Exhibition Centre

Brisbane

QLD

9-13 Oct

2016

World Energy Council – 23rd

World Energy Congress

Istanbul

Turkey

25-26 Oct

2016

15th

Annual Longwall Conference

Crowne Plaza

Hunter Valley

NSW

http://www.longwallconference.com.au/

7-10 Nov

2016

IMARC 2016

http://imarcmelbourne.com

1–3 May

2017

Minesafe International 2017

http://www.minesafe.ausimm.com.au/

Personnel

Rio Tinto Limited has announced the appointment of Stephen McIntosh as the acting Group Executive,

Technology & Innovation. Mr McIntosh will succeed Greg Lilleyman, who will leave the company after 25

years of service.

Noble Group Limited has announced the appointment of Paul Jackaman to the position of Chiief Financial

Officer.

26 May 2016 Hunter Valley Coal Report No 21/16 11

The following positions have been advertised: Company Location Position

BHP Billiton Queensland HR Business Partner

BHP Billiton BMA Engineer A&I,

Superintendent Site

Services, Principal

Engineer Electrical

BHP Billiton NSW Manager Mine Planning

Coal Services Singleton Support Co-ordinator

Coal Services Sydney Risk Officer

Downer Blackwater

Drill and Blast

Maintenance

Superintendent, Open

Cut HV Electrician,

Maintenance Planner

Downer Gunnedah Traffic Controller,

Leading Hand Fitter

Rio Tinto Brisbane Network Engineer - 12

Month Fixed Term

Whitehaven Coal Gunnedah/Narrabri CHPP Supervisor

Whitehaven Coal Werris Creek Environmental Officer

Whitehaven Coal Gunnedah Explosives Supervisor,

External Relations

Officer

HVCCC Weekly Performance Report

Report for 16 - 22 May 2016

Source: Hunter Valley Coal Chain Co-ordinator (HVCCC).

Coal Delivery

Planned rates were 582kt below target while Actual inbound performance was 493kt below the Declared

Inbound Throughput (DIT). Total losses finished the week at 6.1% compared to the declared target of

7.4%.

May’s month-to-date throughput is currently 10,491kt (174.5Mtpa) which is 1,051kt below the DIT,

with total losses of 6.8%.

Shiploading - PWCS Only

Planned rates were 558kt below target while Actual outbound performance was 250kt below the

Declared Outbound Throughput (DOT). May’s month-to-date shiploading is currently 6,830kt

(113.6Mtpa), 912kt below the DOT.

PWCS port stocks finished the week at 1,433kt, on par with the previous week.

Coal Chain Demand

May’s nominations are currently 9.2Mt.

Based on terminal demand the PWCS queue is estimated to be two at the end of May and one at the end

of June.

At PWCS there were five vessels in the offshore queue at the end of the week.

26 May 2016 Hunter Valley Coal Report No 21/16 12

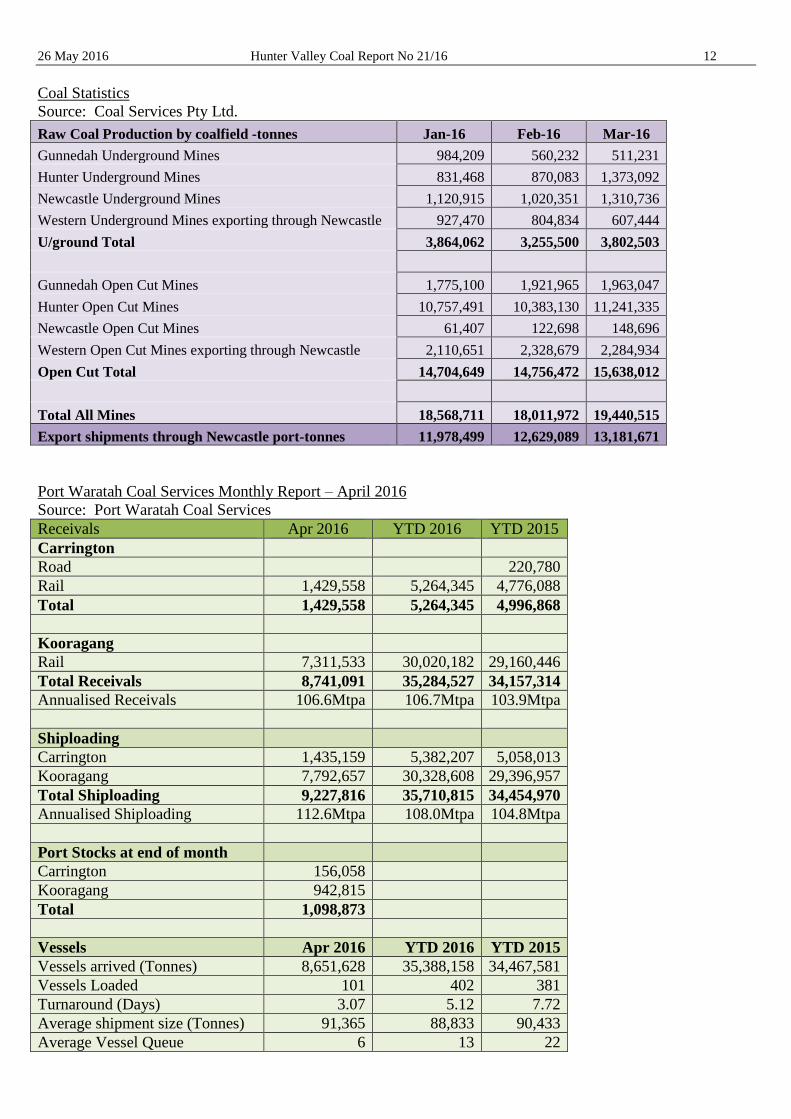

Coal Statistics

Source: Coal Services Pty Ltd.

Raw Coal Production by coalfield -tonnes Jan-16 Feb-16 Mar-16

Gunnedah Underground Mines 984,209 560,232 511,231

Hunter Underground Mines 831,468 870,083 1,373,092

Newcastle Underground Mines 1,120,915 1,020,351 1,310,736

Western Underground Mines exporting through Newcastle 927,470 804,834 607,444

U/ground Total 3,864,062 3,255,500 3,802,503

Gunnedah Open Cut Mines 1,775,100 1,921,965 1,963,047

Hunter Open Cut Mines 10,757,491 10,383,130 11,241,335

Newcastle Open Cut Mines 61,407 122,698 148,696

Western Open Cut Mines exporting through Newcastle 2,110,651 2,328,679 2,284,934

Open Cut Total 14,704,649 14,756,472 15,638,012

Total All Mines 18,568,711 18,011,972 19,440,515

Export shipments through Newcastle port-tonnes 11,978,499 12,629,089 13,181,671

Port Waratah Coal Services Monthly Report – April 2016

Source: Port Waratah Coal Services

Receivals Apr 2016 YTD 2016 YTD 2015

Carrington

Road 220,780

Rail 1,429,558 5,264,345 4,776,088

Total 1,429,558 5,264,345 4,996,868

Kooragang

Rail 7,311,533 30,020,182 29,160,446

Total Receivals 8,741,091 35,284,527 34,157,314

Annualised Receivals 106.6Mtpa 106.7Mtpa 103.9Mtpa

Shiploading

Carrington 1,435,159 5,382,207 5,058,013

Kooragang 7,792,657 30,328,608 29,396,957

Total Shiploading 9,227,816 35,710,815 34,454,970

Annualised Shiploading 112.6Mtpa 108.0Mtpa 104.8Mtpa

Port Stocks at end of month

Carrington 156,058

Kooragang 942,815

Total 1,098,873

Vessels Apr 2016 YTD 2016 YTD 2015

Vessels arrived (Tonnes) 8,651,628 35,388,158 34,467,581

Vessels Loaded 101 402 381

Turnaround (Days) 3.07 5.12 7.72

Average shipment size (Tonnes) 91,365 88,833 90,433

Average Vessel Queue 6 13 22

26 May 2016 Hunter Valley Coal Report No 21/16 13

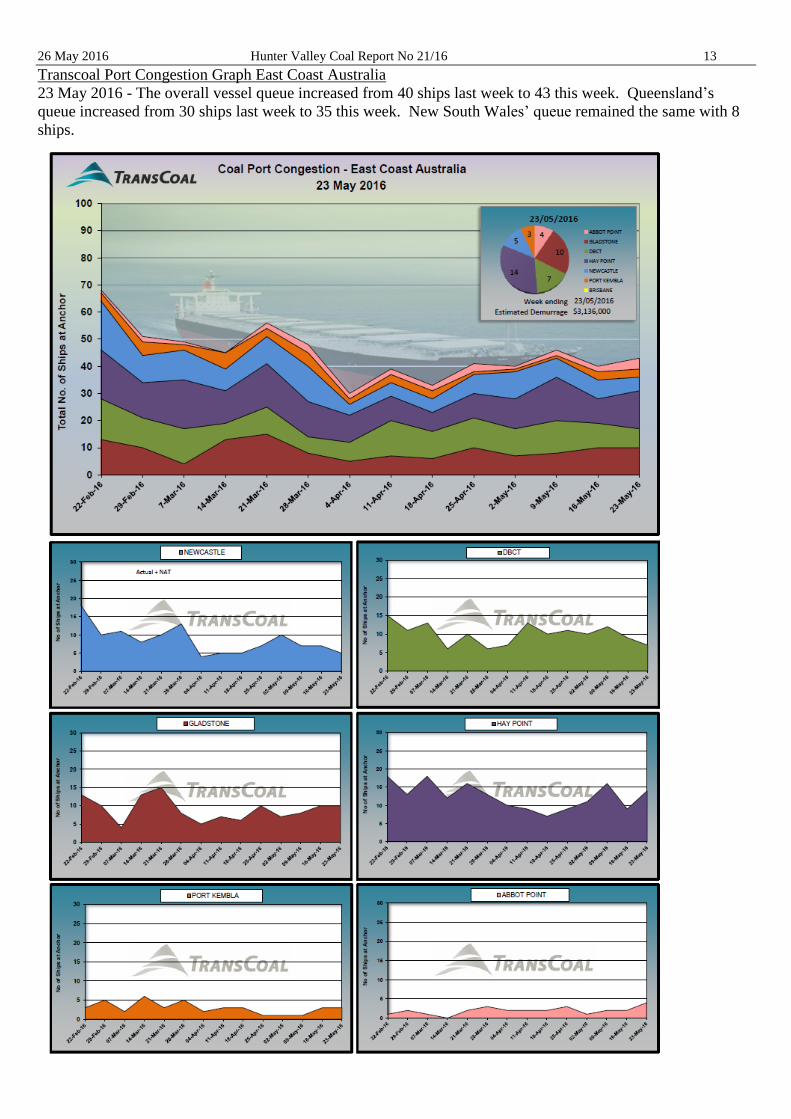

Transcoal Port Congestion Graph East Coast Australia

23 May 2016 - The overall vessel queue increased from 40 ships last week to 43 this week. Queensland’s

queue increased from 30 ships last week to 35 this week. New South Wales’ queue remained the same with 8

ships.

26 May 2016 Hunter Valley Coal Report No 21/16 14

Braemar Seascope Weekly Focus

25 May 2016

Vessel

DWT

Australian Round Voyage Far East

Mediterranean/Continent

Mediterranean/Continent – Far

East

Last

Week

This

Week

Change Last

Week-

This

Week

Change Last

Week

This

Week

Change

28,000 $3,350 $3,500 $0 $1,750 $1,750 $0

32,000 $3,850 $4,000 $0 $2,250 $2,250 $0

52,000 $4,900 $5,200 $300 $3,200 $2,900 -$300 $8,500 $8,750 $250

58,000 $5,400 $5,700 $300 $3,350 $3,200 -$150 $9,000 $9,250 $250

74,000 $4,810 $4,773 -$37 $582 $638 $56 $8,590 $8,581 -$9

180,000 $5,042 $5,596 $524 $244 $356 $112 $14,324 $15,648 $1,324

Note: NOTE: The trades 28K, 32K, 52K & 58K DWT sizes rates are assumed to be DOP South East Asia. All

other sizes are assumed DOP North Asia.

Vessel DWT 1 year period 3 years period

28,000 3,950 5,000

52,000 5,800 7,000

74,000 5,500 7,000

180,000 6,500 19000

CAPESIZE

A weak market in both basins with minimal activity and softer numbers. There was a hope towards the end of

last week that with owners in the Pacific starting to dig their heels in we might see firmer numbers.

Unfortunately the lack of activity in the Atlantic smothered any chance of a rally and rates traded down on

every route.

The Pacific started the week at $4.30/T level for early-June dates and there was a widespread belief that all

three shippers had much more cargo to move for early-June. That was decidedly not the case and all three

shippers were very quiet before pushing their dates to 6th June onwards and trading down to the low-$4.00/T

with $4.10/T fixed a couple of times on Tuesday. Some TCT fixing with a vessel delivery end-May getting

$6,000/day for a full Australian round voyage.

The Atlantic was very slow. TA RV traded quickly down with offers in the $10,000/day range with fixing

levels of $7,000/day within a few days. Voyage rates were equally few and far between with $5.80/T fixed for

Bolivar to Ashkelon and Saldanha Bay back to Rotterdam at $3.75/T and C3 at $7.50/T. With tonnage piling up

and cargoes thin on the ground it does not look like we will see anything more encouraging in the near term.

PANAMAX

A very mixed Panamax market this week, with rates done at last week numbers. The cause might be due

to the rallying of bunker prices. ECSA round voyages for early-June dates were reportedly fixed at $7,300/day

+ $240,000 ballast bonus levels. Rumoured US Gulf grains in the market were, reportedly being fixed at

$12,500/day + $280,000 BB levels. In the Pacific $5,000/day seems to be the magic number from charterers for

June date cargoes. Indonesia - India, Indonesia - China and Australian round voyage cargoes were reportedly

being done at $5,000/day levels for Panamaxes up to Post- Panamaxes. With the uncertainty in ECSA, many

owners are choosing to stay in the Pacific doing shorter round voyages to buy time and perhaps waiting for the

market to pick up before deciding whether to ballast.

Short period fixtures were stagnant with fixtures reportedly done at low-$5,000/day for 4-8 months.

26 May 2016 Hunter Valley Coal Report No 21/16 15

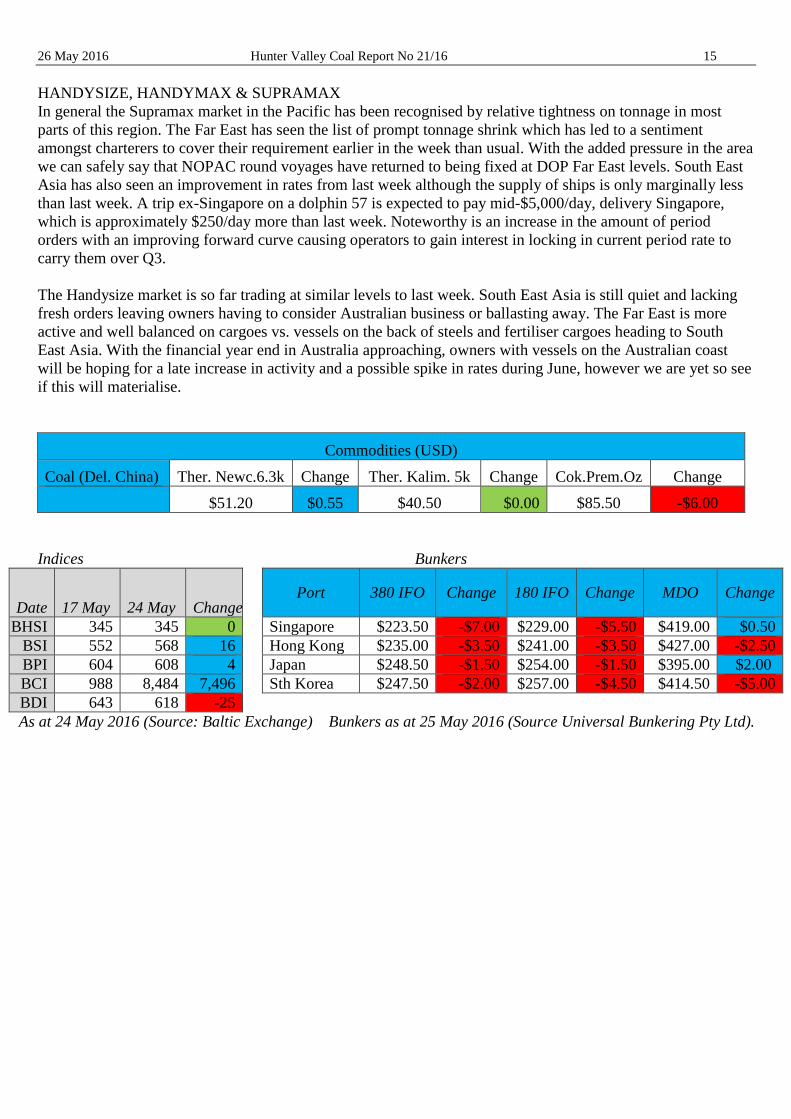

HANDYSIZE, HANDYMAX & SUPRAMAX

In general the Supramax market in the Pacific has been recognised by relative tightness on tonnage in most

parts of this region. The Far East has seen the list of prompt tonnage shrink which has led to a sentiment

amongst charterers to cover their requirement earlier in the week than usual. With the added pressure in the area

we can safely say that NOPAC round voyages have returned to being fixed at DOP Far East levels. South East

Asia has also seen an improvement in rates from last week although the supply of ships is only marginally less

than last week. A trip ex-Singapore on a dolphin 57 is expected to pay mid-$5,000/day, delivery Singapore,

which is approximately $250/day more than last week. Noteworthy is an increase in the amount of period

orders with an improving forward curve causing operators to gain interest in locking in current period rate to

carry them over Q3.

The Handysize market is so far trading at similar levels to last week. South East Asia is still quiet and lacking

fresh orders leaving owners having to consider Australian business or ballasting away. The Far East is more

active and well balanced on cargoes vs. vessels on the back of steels and fertiliser cargoes heading to South

East Asia. With the financial year end in Australia approaching, owners with vessels on the Australian coast

will be hoping for a late increase in activity and a possible spike in rates during June, however we are yet so see

if this will materialise.

Commodities (USD)

Coal (Del. China) Ther. Newc.6.3k Change Ther. Kalim. 5k Change Cok.Prem.Oz Change

$51.20 $0.55 $40.50 $0.00 $85.50 -$6.00

Indices Bunkers

Date 17 May 24 May Change Port 380 IFO Change 180 IFO Change MDO Change

BHSI 345 345 0 Singapore $223.50 -$7.00 $229.00 -$5.50 $419.00 $0.50

BSI 552 568 16 Hong Kong $235.00 -$3.50 $241.00 -$3.50 $427.00 -$2.50

BPI 604 608 4 Japan $248.50 -$1.50 $254.00 -$1.50 $395.00 $2.00

BCI 988 8,484 7,496 Sth Korea $247.50 -$2.00 $257.00 -$4.50 $414.50 -$5.00

BDI 643 618 -25

As at 24 May 2016 (Source: Baltic Exchange) Bunkers as at 25 May 2016 (Source Universal Bunkering Pty Ltd).

26 May 2016 Hunter Valley Coal Report No 21/16 16

Exchange Rates

Source: ANZ Global Markets

Bank buying rates for US dollars as at 8.15am each morning for week ending 20 May 2016

Exchange Rates Monday Tuesday Wednesday Thursday Friday

Bank Buy $US 0.7271 0.7287 0.7313 0.7221 0.7229

Thermal Coal Swap Bids

Source: ANZ Global Markets

Newcastle Coal Swaps Curve (Mids) as at 23 May 2016

Bal-2016 - US$51.75/mt

Cal-2017 - US$51.35/mt

Cal-2018 - US$51.65/mt

‘globalCOAL’ is a registered trade mark of Global Coal Ltd in the EU. ‘NEWC’ is a registered trade mark of

Global Coal Ltd in Australia, Austria, Benelux, Denmark, Finland, France, Germany, Greece, Ireland, Italy,

Portugal, Spain and Sweden. ANZ is a licenced User of globalCOAL products, globalCOAL does not endorse

the accuracy or reliability of any of the information provided herein and cannot be held liable for any loss or

damage arising from any use or reliance on the information above’.

26 May 2016 Hunter Valley Coal Report No 21/16 17

HUNTER VALLEY COAL REPORT The Hunter Valley Coal Report is published weekly by Nadine Brierley

26 Princes Avenue Charlestown NSW 2290 Australia

Ph.: +61 2 4023 8050 Mob 0423 688192 [email protected]

ABN 92 506 051 400

Subscription to HUNTER VALLEY COAL REPORT (50 copies) $1,200.00

Photomosaic of Hunter Valley Coalfields – (plus GST, postage and packaging)

All operating mines 25,000 scale or 3.11m by 1.43m (laminated add $190)

$1,000.00

All operating mines 50,000 scale or 1.72m by 0.83m (laminated add $100)

$540.00

All operating mines 75,000 scale or 1.15m by 0.58m (laminated add $60) $360.00

Your Details:

Name Title

Company

Address:

City State Postcode

Tel: Fax: Email:

Payment Method…..MasterCard/Visa/Amex Amex 4-Digit Security Code……….. Credit Card Details:

Card holders name

Card number

Expiry date

Direct deposit details:

HVCR Nadine Brierley

ANZ Bank Charlestown

A/C 298070174

BSB 012571

![Hunter Valley Coal Network Access Undertaking...Hunter Valley Coal Network Access Undertaking Dated: 23 June 2011 (as varied on 17 October 2012 and [ ] 2014) BY AUSTRALIAN RAIL TRACK](https://img.pdfslide.net/doc/110x75/5e4427669ec4780778720900/hunter-valley-coal-network-access-undertaking-hunter-valley-coal-network-access.jpg)