Embed Size (px)

Citation preview

Mike Petters President and Chief Executive Officer

Barb Niland Corporate Vice President, Business Management

& Chief Financial Officer

Huntington Ingalls Industries

September 23, 2014

Citi 2014 Industrials Conference

Safe Harbor

1

Statements in this presentation, other than statements of historical fact, constitute "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve risks and uncertainties that could cause our actual results to differ materially from those expressed in these statements. Factors that may cause such differences include: changes in government and customer priorities and requirements (including government budgetary constraints, shifts in defense spending, and changes in customer short-range and long-range plans); our ability to obtain new contracts, estimate our future contract costs and perform our contracts effectively; changes in government regulations and procurement processes and our ability to comply with such requirements; our ability to realize the expected benefits from consolidation of our Ingalls facilities; natural disasters; adverse economic conditions in the United States and globally; risks related to our indebtedness and leverage; and other risk factors discussed in our filings with the U.S. Securities and Exchange Commission. There may be other risks and uncertainties that we are unable to predict at this time or that we currently do not expect to have a material adverse effect on our business, and we undertake no obligation to update any forward-looking statements. You should not place undue reliance on any forward-looking statements that we may make. This presentation also contains non-GAAP financial measures and includes a GAAP reconciliation of these financial measures. Non-GAAP financial measures should not be construed as being more important than comparable GAAP measures.

Carrier Construction

Carrier RCOH

Submarines

Fleet Support & Other

Newport NewsCoast Guard

Expeditionary Warfare

Surface Combatants

Fleet Support & Other

Ingalls

FY 2013 Revenues: $6.8 bn Employees: ~39,000

FY 2013 EBIT: $512 mn Engineers / Designers: ~7,500

FY 2013 Pension-adj. EBIT:(1) $573 mn Headquarters: Newport News, VA

Current Backlog: ~$24 bn History: 128 years

FY 2013 Revenue Breakdown

Investment Highlights

• Nation’s premier naval and principal nuclear shipbuilder

– Sole source for U.S. Navy nuclear-powered aircraft carriers and their refueling and inactivation services

– One of two builders constructing Virginia-class nuclear-powered submarines

– Builder of record for LPD, LHD and LHA-class amphibious assault ships

• Mission critical partnership with the U.S. Navy

• Significant revenue stability and visibility

• Opportunity for margin expansion and cash flow improvement

2 (1) Refer to reconciliation to reported GAAP financial data on page 26.

Company Snapshot

World-Class Facilities with Broad Scale and Scope

3

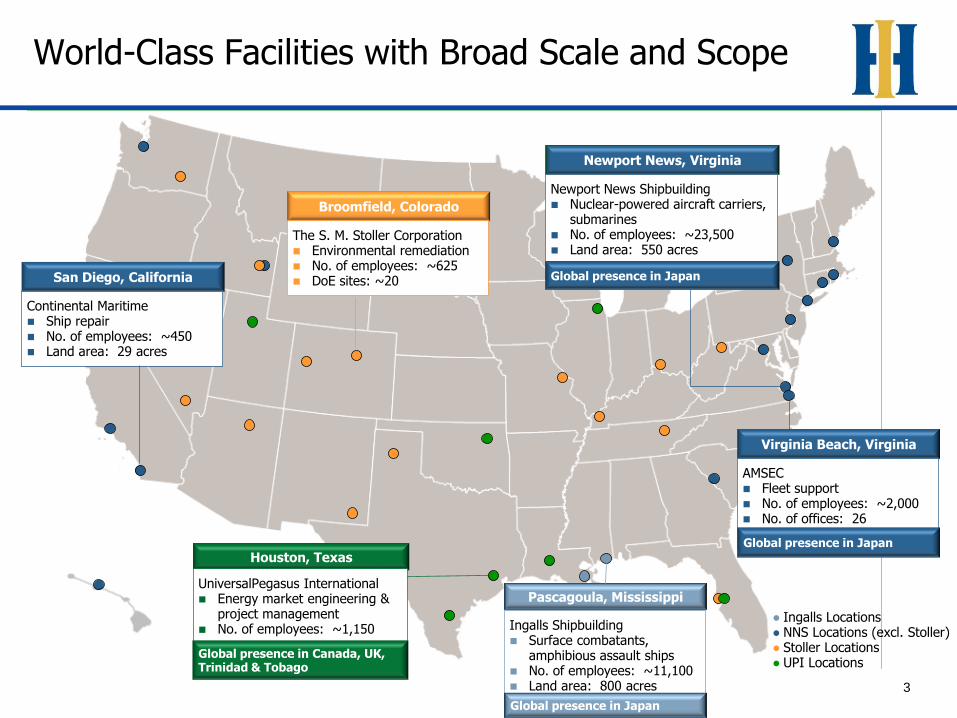

Broomfield, Colorado

The S. M. Stoller Corporation Environmental remediation No. of employees: ~625 DoE sites: ~20

Ingalls Shipbuilding Surface combatants,

amphibious assault ships No. of employees: ~11,100 Land area: 800 acres

San Diego, California

Continental Maritime Ship repair No. of employees: ~450 Land area: 29 acres

Virginia Beach, Virginia

AMSEC Fleet support No. of employees: ~2,000 No. of offices: 26

Houston, Texas

UniversalPegasus International Energy market engineering &

project management No. of employees: ~1,150

Pascagoula, Mississippi

● Ingalls Locations ● NNS Locations (excl. Stoller) ● Stoller Locations ● UPI Locations

Newport News, Virginia

Newport News Shipbuilding Nuclear-powered aircraft carriers,

submarines No. of employees: ~23,500 Land area: 550 acres

Global presence in Japan

Global presence in Japan

Global presence in Canada, UK, Trinidad & Tobago

Global presence in Japan

Nuclear Operations

Heavy Manufacturing

4

Core Competencies

Leveraging our world-class facilities, highly skilled workforce and culture of ethics and compliance

Engineering & Program Management

Mission Critical Partner Aligned with U.S. Navy

5

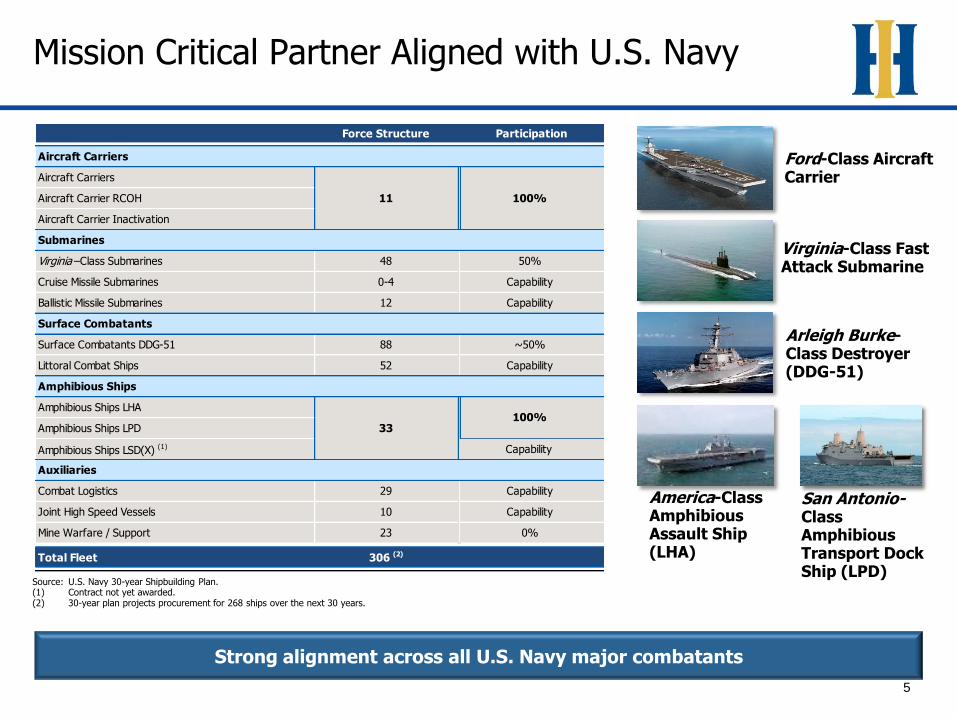

Force Structure Participation

Aircraft Carriers

Aircraft Carriers

Aircraft Carrier RCOH

Aircraft Carrier Inactivation

Submarines

Virginia –Class Submarines 48 50%

Cruise Missile Submarines 0-4 Capability

Ballistic Missile Submarines 12 Capability

Surface Combatants

Surface Combatants DDG-51 88 ~50%

Littoral Combat Ships 52 Capability

Amphibious Ships

Amphibious Ships LHA

Amphibious Ships LPD

Amphibious Ships LSD(X) (1) Capability

Auxiliaries

Combat Logistics 29 Capability

Joint High Speed Vessels 10 Capability

Mine Warfare / Support 23 0%

Total Fleet 306 (2)

11 100%

33100%

Source: U.S. Navy 30-year Shipbuilding Plan. (1) Contract not yet awarded. (2) 30-year plan projects procurement for 268 ships over the next 30 years.

Ford-Class Aircraft Carrier

Virginia-Class Fast Attack Submarine

America-Class Amphibious Assault Ship (LHA)

Arleigh Burke-Class Destroyer (DDG-51)

Strong alignment across all U.S. Navy major combatants

San Antonio-Class Amphibious Transport Dock Ship (LPD)

2-Per-Year Sub Plan

DDG-51 Re-Start

CVN-78 100% Erect

6 Key Contract

Awards

Successful Execution as an Independent Company

6

Pascagoula

Completed Spin-off

March 2011

Delivered 6 Ships

and 2 Submarines

LPD-26 and 27

DDG-113 and 114

NSC-5

SSN 786 and 787

NSC WMSL-752 USCGC Stratton

Targeted, Successful Execution

CVN-78

USS California USS Minnesota

DDG

LPD-22 – LPD-25

LHA-7

LHA-6

• Protect and Strengthen Market Position

– Continue strong execution of programs

– Selective capital investments to support current programs and new opportunities

– Maintain financial predictability, backlog and stability

• Capture New Business

– Ohio-class Replacement Program

– Energy market adjacencies

– Acquisition of The S.M. Stoller Corporation to build presence

7

Manage for Performance

Strategy: Strengthen Market Position and Execute Well for the U.S. Navy

Newport News Ingalls

Continue expanding the performance culture across the business

Capture Benefits of Serial Production

• Ingalls Operating System

− Class plans

− First time quality

− Labor resource management

− Risk & opportunity management

− Consistent recurring ship metrics

• Support Continuation of Amphibious Assault Ship Programs

• Restructuring

− $284 million in restructuring expenses recouped as allowable costs through contracts over five years starting after closure

• Potential Redeployment

− Exploring and evaluating best-use opportunities for re-developing the facility with Kinder Morgan Energy Partners

The Future of Avondale

UPI Overview

Strategic Rationale Customers and Projects

UniversalPegasus International (UPI) Overview

Deal Overview

• Fits HII’s strategy to enter adjacent markets through engineering

• Capable and experienced management team with proven engineering services track records

• Strategic adjacent market that is growing

• Provides access to a broad customer base, including many fortune 500 companies

• Creates strong engineering services growth platform for HII

Key Customers

TransCanada

Enbridge

Enterprise

Kinder Morgan

ENI U.S. Co.

• All cash transaction

• Accretive pending purchase accounting determination

• Expect EBITDA to track to industry average or slightly above

• UPI is included in the “Other” segment for financial reporting purposes

• Closed in June 2014

Projects

Keystone XL

Prince Rupert Transmission

Flanagan South Pipeline

Seaway Crude Pipeline

Trans Mountain Expansion

Longhorn Subsea Tieback

• Based in Houston, TX with ~1,500 Employees

• Global footprint with operations in Calgary, AB (Canada); London & Aberdeen (United Kingdom); Trinidad & Tobago

• Providers of engineering and project management services to the domestic and international energy markets 2014 Engineering

News Record #61

8

Submarine Construction

Aircraft Carrier Construction

Premier Nuclear Capabilities

9

CVN-78 Gerald R. Ford CVN-79 John F. Kennedy CVN-72 USS Abraham Lincoln RCOH

CVN-65 Enterprise Inactivation

Virginia-class submarine

128 years of shipbuilding experience with unique visibility and stability

• New aircraft carrier for 21st century

• Replacement for Nimitz-class

• Conducting final outfitting and test activities

• 2016 delivery

• 2nd aircraft carrier in the Ford-class

• Conducting design, engineering, material purchases and unit construction under construction preparation contract

• 2022/3 delivery

• 5th Nimitz-class carrier to be refueled

• 2013 refueling execution start

• Preparing for undocking in Q3

• 2016/7 redelivery

• First nuclear aircraft carrier inactivation

• New revenue generation for HII

• 2013 inactivation execution start

• 2016 redelivery

• Very successful teaming arrangement with Electric Boat

• Block III transitioned to 2 subs per year

• Block IV construction starting in 2014

Aircraft Carrier Inactivation

Aircraft Carrier RCOH

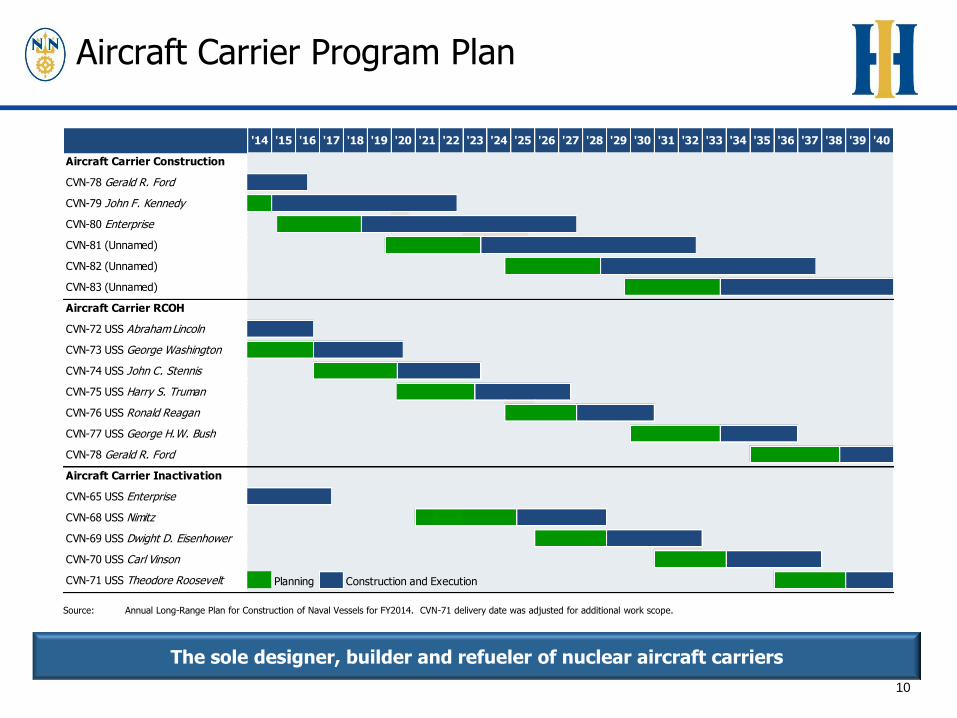

'14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25 '26 '27 '28 '29 '30 '31 '32 '33 '34 '35 '36 '37 '38 '39 '40

Aircraft Carrier Construction

CVN-78 Gerald R. Ford

CVN-79 John F. Kennedy

CVN-80 Enterprise

CVN-81 (Unnamed)

CVN-82 (Unnamed)

CVN-83 (Unnamed)

Aircraft Carrier RCOH

CVN-72 USS Abraham Lincoln

CVN-73 USS George Washington

CVN-74 USS John C. Stennis

CVN-75 USS Harry S. Truman

CVN-76 USS Ronald Reagan

CVN-77 USS George H.W. Bush

CVN-78 Gerald R. Ford

Aircraft Carrier Inactivation

CVN-65 USS Enterprise

CVN-68 USS Nimitz

CVN-69 USS Dwight D. Eisenhower

CVN-70 USS Carl Vinson

CVN-71 USS Theodore Roosevelt Planning Construction and Execution

Aircraft Carrier Program Plan

10

Source: Annual Long-Range Plan for Construction of Naval Vessels for FY2014. CVN-71 delivery date was adjusted for additional work scope.

The sole designer, builder and refueler of nuclear aircraft carriers

CVN 78 Gerald R. Ford Class

Advanced

Weapons Elevators

EMALSAdvanced

Arresting Gear

Dual Band

Radar

1100 Ton AC

Plant

Ship Shell

10.2# HSLA-65

7.65# HSLA-65

7.65# HSLA-65

7.65# HSLA-65

Hangar Side Bhd

Spon

son

Web

Spon

son

Web

Spon

son

Web

7.65# HSLA-65

7.65# HSLA-65

Proposed Sponson 02 Level

Stiffeners 8x5-1/2x7.65#/12.75#T HSLA-65

No Brackets

Plasma Arc

Waste Disposal

System

Lightweight

Materials

Reverse Osmosis

Distilling Unit JP-5 Optical

Monitoring

New

Propulsion/Electric Plant

All Electric Aux

services

Zonal Electrical

Distribution System

Increased CapabilityIncreased Flexibility Increased Affordability

Focused Investment

• Greater operational availability

• 3X electric plant capacity• Sortie Generation Rates

increased by 25%

• $5 B TOC reduction

• 500-1200 billet reduction

CVN 78 Class

More capability at a lower Total Ownership Cost Utilized 3D Product Model

Designed for Producibility

Land Based Test Facility

Schedule Fidelity, Detailed Planning

11

Investments in technology enhance capability and reduce long-term operational costs

11

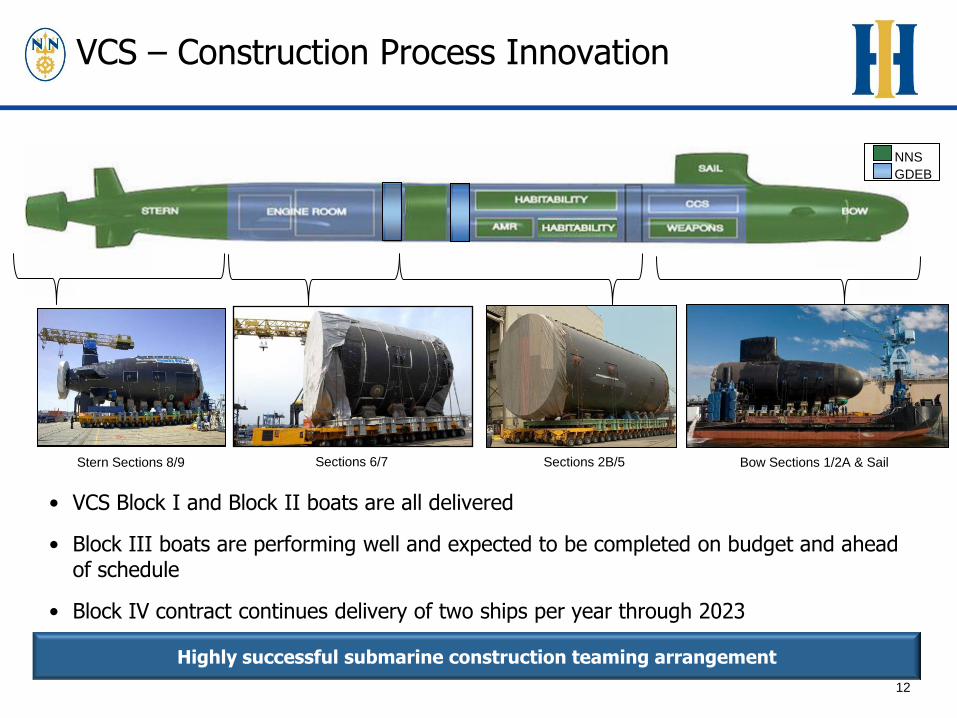

VCS – Construction Process Innovation

• VCS Block I and Block II boats are all delivered

• Block III boats are performing well and expected to be completed on budget and ahead of schedule

• Block IV contract continues delivery of two ships per year through 2023

Highly successful submarine construction teaming arrangement

12

Stern Sections 8/9 Bow Sections 1/2A & Sail Sections 6/7 Sections 2B/5

NNS

GDEB

• Twelve ballistic missile submarines over 15 years

• Electric Boat expected to lead the program

• Newport News is sharing in the design effort

• Expected 2021 construction start

• Leverages nuclear capabilities in non-Navy initiatives

• Partnerships with DoE and commercial contractors

• Build market presence through acquisition of The S.M. Stoller Corporation

• Limited capital investment in JV structures

Organic Growth Opportunities

Ohio-Class Submarine Replacement Program Energy

Leveraging unique shipbuilding, energy and marine capabilities to capture growth

13

The S.M. Stoller Corporation Overview

14

• A leading U.S.-based environmental management and remediation company.

• Provides a full suite of environmental and facility management services across the spectrum of US

government departments and agencies.

• Office and project locations throughout the DOE nuclear complex.

• Strategically positioned to support HII-Energy growth opportunities.

Sole Source Shipbuilder on Three Programs

15

LHA-6 America-Class LPD-17 San Antonio-Class

Large, flexible and newly re-capitalized shipyard with 75-year history

National Security Cutter

• LHA-6 America is 1st ship in LHA(R) program

• Next generation of amphibious ship for joint operations with enhanced aviation capabilities

– Delivered April 2014

• LHA-7 Tripoli is 2nd ship

– Contract awarded in May 2012

– 2018 delivery

• Newest ship in the U.S. Navy’s amphibious fleet used to transport 700 to 800 marines, their equipment and supplies

• Delivered LPD-22 USS San Diego in 2011, LPD-23 Anchorage in Q3 2012, LPD-24 Arlington in Q4 2012, and LPD-25 Somerset in Q4 2013

• LPD-26 Murtha and LPD-27 Portland currently under construction with delivery in 2016 and 2017, respectively.

• Largest and most capable new multi-mission cutter

• Coast Guard plans to build 7 or 8 NSCs to replace aging fleet

• NSC-4 and NSC-5 under construction

• NSC-6 contract awarded in May 2013

• NSC-7 contract awarded in March 2014

• NSC-8 long lead time materials contract awarded in June 2014

• Next generation multi-mission surface combatant class (three-ship class)

• Ingalls work-share consists of composite deckhouse/hangar and steel aft peripheral vertical launch systems

• Unique composites characteristics include light weight and increased stealth

• Co-lead on ship design (work-share products related)

• DDG-1001 delivered in August 2014 which ends the program for HII

• US Navy’s primary surface combatant class

• Designed for conducting anti-air, anti-submarine, anti-surface and strike operations

• Most advanced state-of-the-art surface combat ships

• Original 62-ship program / 28 awarded to HII previously

• Awarded construction contracts for DDG-113 and DDG-114, first two ships of the program re-start

• Awarded a $3.3 billion contract for five DDG-51s in June 2013

Surface Combatant Programs

DDG-51 Arleigh Burke-Class DDG-1000 Zumwalt-Class

Ingalls expects to capture benefits of serial production

16

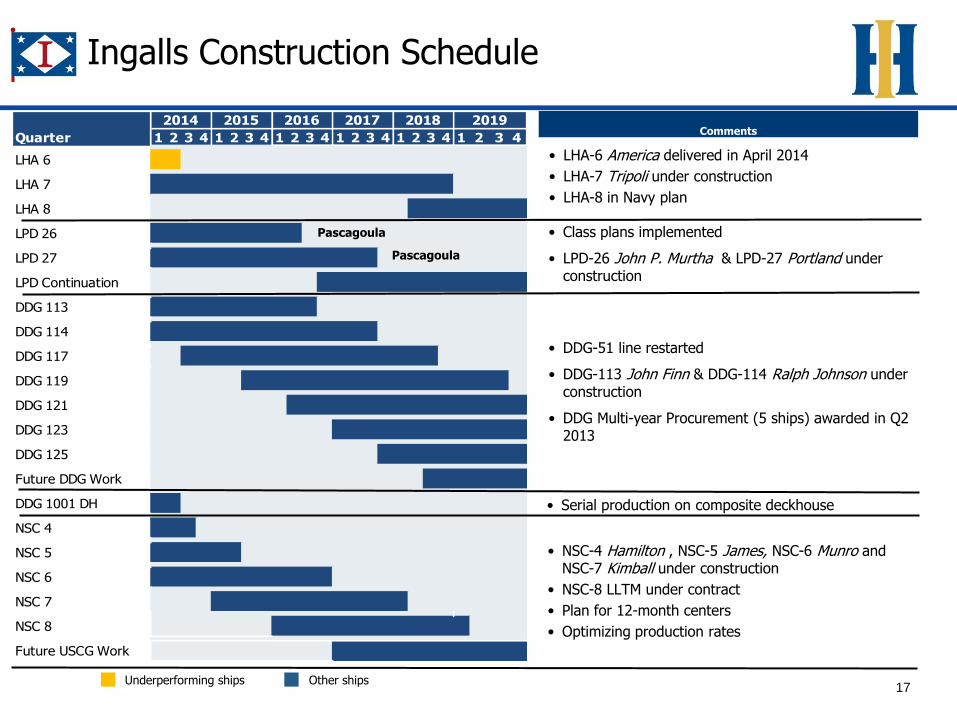

Quarter 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

LHA 6

LHA 7

LHA 8

LPD 26

LPD 27

LPD Continuation

DDG 113

DDG 114

DDG 117

DDG 119

DDG 121

DDG 123

DDG 125

Future DDG Work

DDG 1001 DH

NSC 4

NSC 5

NSC 6

NSC 7

NSC 8

Future USCG Work

20192015 20182014 2016 2017

Underperforming ships

Ingalls Construction Schedule

17 Other ships

Comments

• NSC-4 Hamilton , NSC-5 James, NSC-6 Munro and NSC-7 Kimball under construction

• NSC-8 LLTM under contract

• Plan for 12-month centers

• Optimizing production rates

• Class plans implemented

• LPD-26 John P. Murtha & LPD-27 Portland under construction

• DDG-51 line restarted

• DDG-113 John Finn & DDG-114 Ralph Johnson under construction

• DDG Multi-year Procurement (5 ships) awarded in Q2 2013

• Serial production on composite deckhouse

• LHA-6 America delivered in April 2014

• LHA-7 Tripoli under construction

• LHA-8 in Navy plan

Pascagoula

Pascagoula

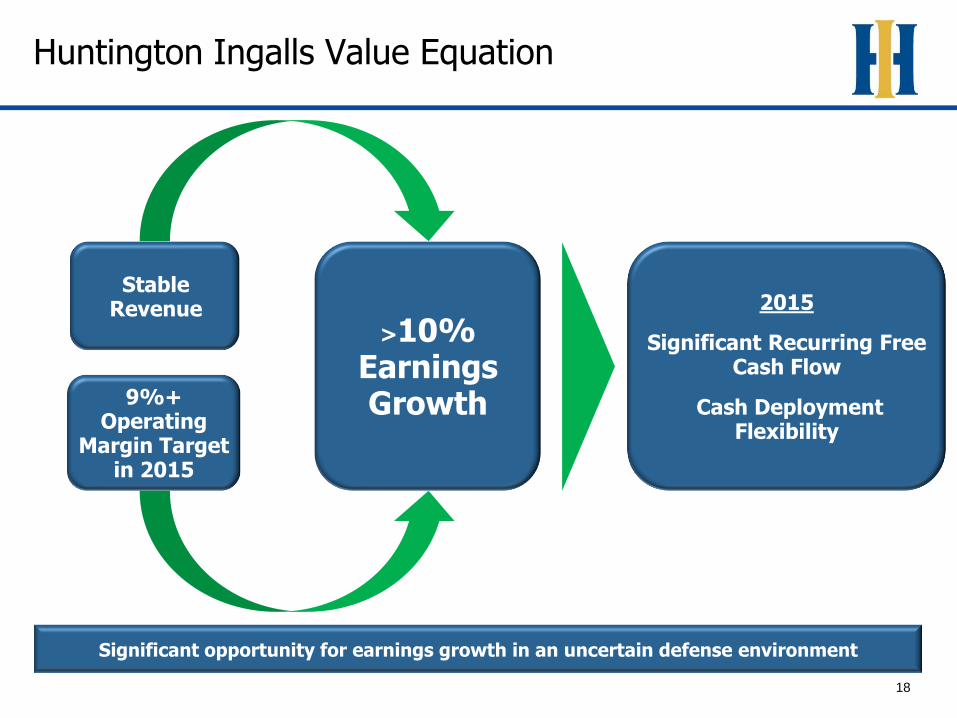

Huntington Ingalls Value Equation

18

Stable Revenue

9%+ Operating

Margin Target in 2015

Significant opportunity for earnings growth in an uncertain defense environment

>10% Earnings Growth

2015

Significant Recurring Free Cash Flow

Cash Deployment Flexibility

Unsa

ve

d D

ocu

me

nt

/ 1

2/2

9/1

0 /

10

:02

Consolidated Financial Highlights

Historical Financial Summary

20

YTD 2014 YTD 20131 FY 2013 FY 2012 FY 2011

($ in millions, except EPS)

Newport News $2,176 $2,104 $4,139 $3,840 $3,766

Ingalls 1,119 1,142 2,757 2,840 2,885

Other 20 -

Intersegment eliminations (2) (1) (76) (72) (76)

Total Revenue $3,313 $3,245 $6,820 $6,708 $6,575

Newport News 198 201 392 360 342

Ingalls 102 55 175 97 70

Total Segment Operating Income2 $300 $256 $567 $457 $412

% Margin2 9.1% 7.9% 8.3% 6.8% 6.3%

Total Operating Income2 $340 $211 $512 $358 $390

% Margin2 10.3% 6.5% 7.5% 5.3% 5.9%

Pension-adjusted Operating Income2 $297 $252 $573 $438 $413

% Margin2 9.0% 7.8% 8.4% 6.5% 6.3%

Diluted EPS $3.84 $2.00 $5.18 $2.91 ($2.05)

Pension-adjusted Diluted EPS2 $3.28 $2.53 $5.97 $3.95 $4.15

Adjusted operating margin improving, but limited by legacy underperforming contracts

1 Segment information includes realignment of AMSEC and CMSD business lines from Ingalls to Newport News segment. 2 Refer to reconciliation to reported GAAP financial data on pages 25 and 26.

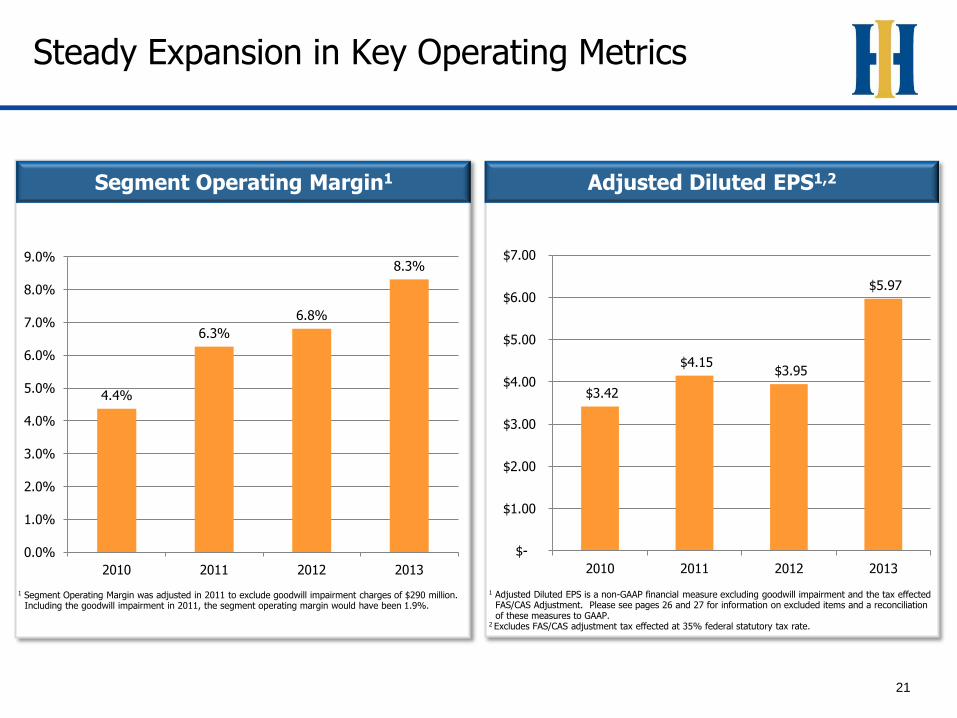

Steady Expansion in Key Operating Metrics

21

4.4%

6.3%

6.8%

8.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2010 2011 2012 2013

$3.42

$4.15 $3.95

$5.97

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

2010 2011 2012 2013

Adjusted Diluted EPS1,2 Segment Operating Margin1

1 Segment Operating Margin was adjusted in 2011 to exclude goodwill impairment charges of $290 million. Including the goodwill impairment in 2011, the segment operating margin would have been 1.9%.

1 Adjusted Diluted EPS is a non-GAAP financial measure excluding goodwill impairment and the tax effected FAS/CAS Adjustment. Please see pages 26 and 27 for information on excluded items and a reconciliation of these measures to GAAP.

2 Excludes FAS/CAS adjustment tax effected at 35% federal statutory tax rate.

22

$76

$136

$220

$266

$287

$246

$218

$181$191 $197

$162

$139

1.6%

2.5%

3.5%

4.6%

5.4%

4.3%

3.5%

2.9% 2.8% 3.0%

2.4%2.0%

$0

$100

$200

$300

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Future

Capex Capex % of Revenues

Investing for Long-term Program Stability

Capital Expenditure

($ in millions)

2007 – 2011 – Carrier Inactivation/RCOH

2009 – 2014 – VCS 2-per year (Submarines)

2003 – 2009 – Ford-class (Carriers)

2003 – 2007 – New Pier (Carriers)

Long term “Maintenance” capex =

~2.0-3.0% of sales

2003 – 2008 – Electrical System and CAD Upgrade

2005 – 2009 – Hurricane spending

Substantial investments designed to protect and strengthen market position

Unsa

ve

d D

ocu

me

nt

/ 1

2/2

9/1

0 /

10

:02

Unsa

ve

d D

ocu

me

nt

/ 1

2/2

9/1

0 /

10

:02

Non-GAAP Reconciliations

Reconciliation of Non-GAAP Measures – Segment and Pension-adjusted Operating Income and Margin

25

Year Ended Dec. 31,

YTD 2014 YTD 2013 2013 2012 2011

($ in millions)

Sales and Service Revenues $3,313 $3,245 $6,820 $6,708 $6,575

Segment Operating Income 300 256 567 457 122

Adjustment for non-cash goodwill impairment1 - - - - 290

Adjusted Segment Operating Income 300 256 567 457 412

Adjusted Segment Operating Margin 9.1% 7.9% 8.3% 6.8% 6.3%

Operating Income 340 211 512 358 100

Adjustment for non-cash goodwill impairment1 - - - - 290

FAS/CAS Adjustment (43) 41 61 80 23

Adjusted Total Operating Income 297 252 573 438 413

Adjusted Operating Margin 9.0% 7.8% 8.4% 6.5% 6.3%

1 Non-cash goodwill impairment charge recorded at the Ingalls segment as a result of adverse equity market conditions that began in the second quarter of 2011 and the resultant decline

in industry market multiples and HII's market capitalization.

Reconciliation of Non-GAAP Measures – Adjusted EPS

26

Year Ended Dec. 31,

YTD 2014 YTD 2013 2013 2012 2011

($ in millions, except per share amounts) Pension-adjusted Net Earnings

Net Earnings (Loss) $190 $101 $261 $146 ($100)

Adjustment for non-cash goodwill impairment - - - - 290

After-tax FAS/CAS Adjustment1 (28) 27 40 52 15

Pension-adjusted Net Earnings $162 $128 $301 $198 $205

Outstanding Shares

Weighted-Average Diluted Shares Outstanding 49.5 50.5 50.4 50.1 48.8

Dilutive impact excluded due to net loss position - - - - 0.6

Adjusted Weighted-Average Diluted Shares Outstanding2 49.5 50.5 50.4 50.1 49.4

Pension-adjusted Diluted EPS

Diluted earnings (loss) per share $3.84 $2.00 $5.18 $2.91 ($2.05)

Non-cash goodwill impairment per share - - - -

5.94

After-tax FAS/CAS Adjustment per share1 (0.56) 0.53 0.79 1.04 0.31

Impact of Adjusted Weighted-Average Diluted Shares Outstanding - - - - (0.05)

Pension-adjusted Diluted EPS $3.28 $2.53 $5.97 $3.95 $4.15

1 Tax effected at 35% federal statutory tax rate.

2 Adjusted weighted-average diluted common shares outstanding is a non-GAAP measure defined as weighted average common shares outstanding plus the dilutive effect of stock options

and stock awards. This measure has been provided for consistency and comparability of the 2011 results with earnings per share from 2012.