Embed Size (px)

Citation preview

1

HYDERABAD

REAL ESTATE OVERVIEW

MAY 2016

2

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY 3

2. CITY FACT FILE 5

3. MAJOR INFRASTRUCTURE DEVELOPMENTS 7

4. REAL ESTATE OVERVIEW 10

5. WEST HYDERABAD METROPOLITAN REGION 15

6. NORTH-WEST HYDERABAD METROPOLITAN REGION 17

7. NORTH HYDERABAD METROPOLITAN REGION 19

8. EAST HYDERABAD METROPOLITAN REGION 21

9. CENTRAL HYDERABAD METROPOLITAN REGION 22

10. SOUTH HYDERABAD METROPOLITAN REGION 24

11. LOCATION ATTRACTIVENESS INDEX 25

12. DISCLAIMER 26

3

The ‘Hyderabad Residential Real Estate Overview – May 2016’ provides a comprehensive insight

into the key trends that have emerged in residential markets of Hyderabad. The report is an

outcome of a rigorous survey conducted by ICICI Home Finance Company across different regions

of Hyderabad. Some of the key findings are as follows:

Political stability and government initiatives have infused a positive sentiment into the

Hyderabad real estate market. Residential markets across Hyderabad witnessed a gradual

phase of recovery after a long drawn political unrest which culminated into the creation of

Telangana state with Hyderabad as its capital. Weak sentiments had dented the markets for

over three years till the bifurcation of the state, leading to an over-supply situation across the

city as buyers stayed away during this time of uncertainty.

Hyderabad residential real estate is driven by a mix of both investors and end users.

However, end-users comprise of the majority share of the total pie of buyers. With the

increase in off-take of the office supply space, organized players have been firming up the

residential supply in Hyderabad market.

There has been a marked preference for apartments in multi-storeyed buildings in a variety

of price ranges depending on the purchasing power of the buyer. Many areas on the west of

Hyderabad like Gachibowli, HITEC City, Kukatpally, Madhapur and Chandanagar have

witnessed increased demand due to their proximity to the IT hub, along with other factors

such as excellent connectivity, developed infrastructure, and availability of good residential

development in Hyderabad at affordable prices in these locations.

The development of Metro with its proposed commencement in a year’s time and other

infrastructure projects such as radial roads, inner ring road, outer ring road and availability of

Grade-A offices at comparatively lower prices than those in Bangalore and Pune is a

benefitting factor for residential real estate in Hyderabad.

Since Hyderabad has a sizable population of migrants, particularly IT/ITes professionals, the

rental housing market is very prominent in the city.

Our survey of the market indicates a stable off-take in residential stock during CY2015, with

ready-to-move inventory witnessing buyers. There has been a rise in consumption of

apartments in multi-storeyed buildings by buyers moving into Hyderabad from other cities

and is expected to add impetus to the real estate market of Hyderabad.

Our analysis indicates that maximum supply and absorption in Hyderabad residential market

falls in the price bracket of INR 2,000 per sq. ft. to 3,000 per sq. ft. primarily comprising of

units developed by local developers. The most active configuration in terms of both new

launches and absorption for residential units has been the 3-BHK segment.

Gachibowli, Kukatpally, HITEC City and Madhapur have been witnessing a lot of activity with

majority of new project launches lying in the price range of INR 40 to 60 lakhs.

EXECUTIVE SUMMARY

4

The report has been divided into following six distinct regions – North, East, West, South,

Central and North-West, based on the geographical location and real-estate activity. We have

analyzed the key trends in the markets and have provided a perspective of the prevailing

market scenario.

Further, the report tracks the city absorption and supply trends along with property price

trends for each of these micro-markets through weighted average prices of the available

supply of units.

The report concludes with a Location Attractiveness Index, which grades each micro-market

on the basis of certain key parameters such as the current state of Infrastructure, Residential

Cost, Proximity to Retail Establishments, Future Employment Generation Capacity, etc.

EXECUTIVE SUMMARY

5

Hyderabad is the capital of Telangana and one of the most populous cities of India. Telangana

acquired its identity as the Telugu-speaking region of the princely state of Hyderabad, ruled by the

Nizam of Hyderabad, joining the Union of India in 1948. In 1956, Hyderabad state was dissolved as

part of the linguistic re-organisation of the states and Telangana was merged with former Andhra

State to form Andhra Pradesh.

However, after a long-drawn agitation for bifurcation of the states, the Andhra Pradesh

Reorganisation Act, 2014 (an Act of the Indian Parliament) bifurcated the state of Andhra Pradesh

into Telangana and the residuary Andhra Pradesh state. The Act defined the boundaries of the two

states, determined how the assets and liabilities were to be divided, and laid out the status of

Hyderabad as the permanent capital of Telangana and temporary capital of the new Andhra

Pradesh state. Hyderabad will continue to serve as the joint capital city for Andhra Pradesh and

Telangana for a period of not more than ten years.

An earlier version of the bill, Andhra Pradesh Reorganisation Act, 2013, was rejected by the Andhra

Pradesh Legislative Assembly on 30th

January 2014. The 2014 bill was passed in the Lok Sabha on

18th

February 2014 and in the Rajya Sabha on 20th

February 2014. The bill was attested by the

President of India, Pranab Mukherjee on 1st

March 2014 and published in the official Gazette which

was followed by the creation of the new states on 2nd

June 2014.

Hyderabad’s urban agglomeration, known as Hyderabad Metropolitan Region (HMR), is spread over

7,100 sq. km. The population of the city is 6.8 million and that of its metropolitan area is 7.75 million

making it the fourth most populous city and sixth most populous urban agglomeration in India.

Hyderabad city is located on the banks of Musi River on the Deccan Plateau. At an average altitude

of 542 meters, most parts of Hyderabad are situated on hilly terrain and are surrounded by artificial

lakes including Hussain Sagar, which lies towards the north of the city center.

History

Hyderabad was established in 1591 by Muhammad Quli Qutb Shah. It remained under the rule of

Qutb Shahi dynasty until 1687, when Mughal emperor Aurangzeb conquered the region and the city

became part of the Deccan province of the Mughal Empire. In 1724 Asif Jah I, a Mughal viceroy,

declared his sovereignty and formed Asif Jahi dynasty, also known as Nizams of Hyderabad.

Nizams ruled the princely state of Hyderabad for more than two centuries, in a subsidiary alliance

with the British Raj. The city remained the princely state's capital from 1769 to 1948, when the

Nizam signed an Instrument of Accession with the Indian Union at the conclusion of Operation Polo.

The 1956 States Reorganisation Act created the modern state of Andhra Pradesh, with Hyderabad

as its capital.

Administrative Framework

The Hyderabad Metropolitan Development Authority (HMDA) was formed by an Act of Andhra

Pradesh Legislature in the year 2008, with an area of 7,100 sq. km. under its purview. It is one of the

largest urban development areas in India. HMDA was formed by merging the following erstwhile

entities: Hyderabad Urban Development Authority (HUDA), Hyderabad Airport Development

Authority (HADA), Cyber Abad Development Authority (CDA) and Buddha Poornima Project

Authority (BPPA).

CITY FACT FILE

6

HMDA was set up for the purposes of planning, co-ordination, supervising, promoting and securing

planned development of Hyderabad Metropolitan Region. It coordinates the development activities

of the municipal corporations, municipalities and other local authorities like Hyderabad Metropolitan

Water Supply & Sewerage Board, Andhra Pradesh Transmission Corporation, Andhra Pradesh

Industrial Infrastructure Corporation, Andhra Pradesh State Road Transport Corporation, and other

such bodies.

HMDA also maintains and manages the Hyderabad Management Development Fund, allocating

finances based on the plans and programs of local bodies to undertake development of amenities

and infrastructure facilities.

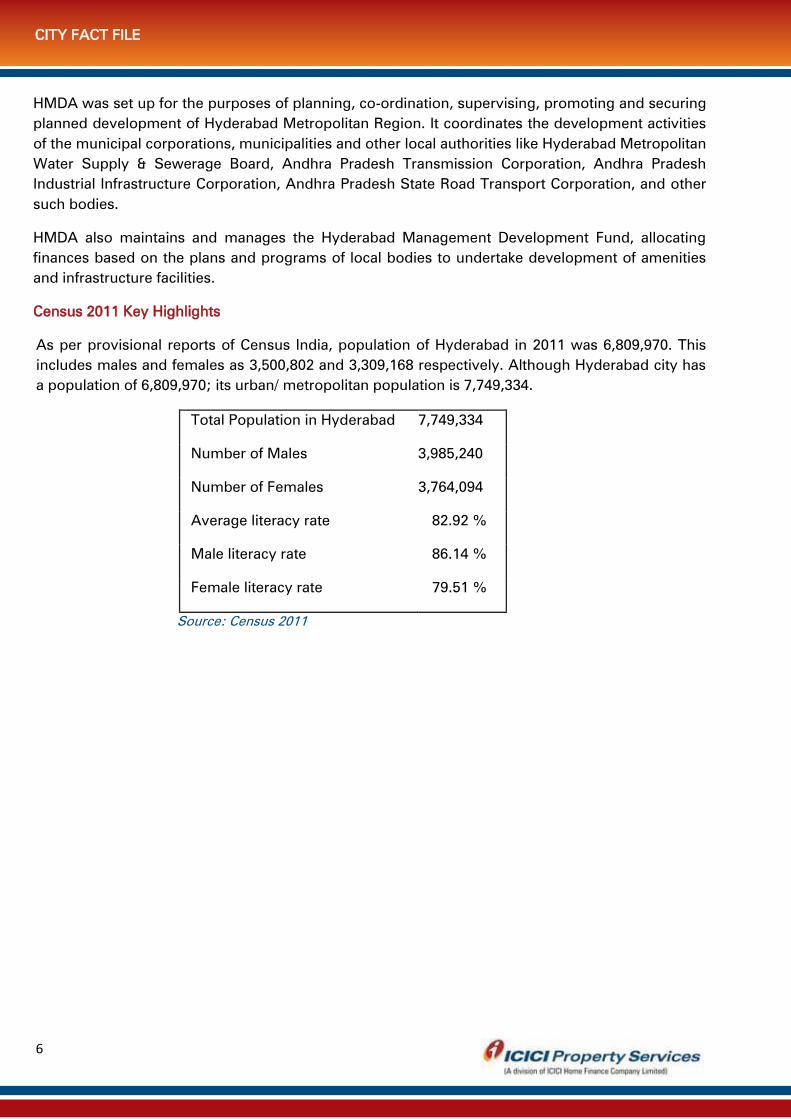

Census 2011 Key Highlights

As per provisional reports of Census India, population of Hyderabad in 2011 was 6,809,970. This

includes males and females as 3,500,802 and 3,309,168 respectively. Although Hyderabad city has

a population of 6,809,970; its urban/ metropolitan population is 7,749,334.

Total Population in Hyderabad 7,749,334

Number of Males 3,985,240

Number of Females 3,764,094

Average literacy rate 82.92 %

Male literacy rate 86.14 %

Female literacy rate 79.51 %

Source: Census 2011

CITY FACT FILE

7

Outer Ring Road (ORR)

Nehru Outer Ring Road or ORR is a 158 kilometer, 8-lane ring road expressway encircling the city of

Hyderabad. It is being built by HMDA at an estimated cost of INR 6,696 crores with an assistance of

INR 3,123 crores from Japan International Cooperation Agency. A large part, 124 kms of the 158

kms was opened in December 2012 covering the areas of HITEC City, Financial District, Hyderabad

International Airport etc. It provides an easy connectivity between NH 9, NH 7, NH 4 and state

highways leading to Vikarabad, Srisailam and Nagarjunasagar.

The road aims to improve connectivity and decongest traffic flow on existing major arterial roads

between the outer suburbs of Greater Hyderabad. The expressway is fenced and 33 radial roads

connect it with the Inner Ring Road, and the upcoming Regional Ring Road. The current status of

ORR is as given below:

Completed segments

Gachibowli to Shamshabad (22 km) was completed in November 2008

Shamshabad to Pedda Amberpet (38 km) was completed in July 2010

Narsingi to Patancheru (23.7 km) was completed in August 2011

Patancheru - Gowdavalli, and Kandlakoya - Shamirpet (38 km) was completed in December

2012

Pedda Amberpet - Ghatkesar (14 km) was completed in March 2015

Under Construction

Ghatkesar to Keesara (11 km) (Delayed due to Rail Over Bridge construction)

Keesara to Shamirpet (10.5 km)

Source: HMDA official website, media sources

Puppalguda and Narsingi micro-markets are expected to witness a significant positive impact in the

residential real estate landscape as both these micro-markets run on both sides of ORR and lie in

close proximity to the IT Hub. Kompally and Medchal will also be positively impacted by ORR as the

connectivity of these areas with central Hyderabad will improve.

Inner Ring Road (IRR)

The Inner Ring Road or IRR is a 50 kilometer city arterial road in Hyderabad, Telangana, India with

the objective to de-congest city roads and give way for trucks and other commercial vehicles.

IRR's master plan called as Intelligent Transport System was done by Nippon Koei of Japan. The

project, which includes the Outer Ring Road, is being implemented with assistance from Japanese

International Cooperation Agency (JICA).

The road passes through Mehdipatnam including Masab Tank, Banjara Hills, Punjagutta, Begumpet,

Mettuguda, Tarnaka, Nagole, L B Nagar, Attapur, Rethi Bowli etc. The road joins P V Narsimha Rao

Elevated Expressway at Aramgarh. Thus, these areas will be positively affected in terms of real

estate development due to the enhanced connectivity.

MAJOR INFRASTRUCTURE DEVELOPMENTS

8

Multi-Modal Transport System (MMTS)

The Multi-Modal Transport System (MMTS) is a suburban rail system in Hyderabad which is a joint

partnership of Government of Telangana and South Central Railway. It is operated by the South

Central Railway. This project is expected to complement and support the fast growth of the city.

The first phase was completed at a cost of INR 178 crore (USD 26 million), and started its operations

on August 9, 2003. It spans a distance of 43 km, covering 27 stations and connects Secunderabad,

Nampally, Dabirpura, Malakpet, Falaknuma, HITEC city and Lingampally. The Diesel Multiple Units

(green local trains) complement the MMTS (white-blue trains) along few other routes like Bolarum

(up to Manoharabad), Umdanagar etc.

The second phase work on Multi Modal Transportation System (MMTS) is progressing

simultaneously in all five stretches of Greater Hyderabad. This second phase covers a length of 103

km at an estimated cost of INR 819 crore. Eleven of the 16 major bridges, electrification of the

existing Secunderabad-Bolarum double line and track doubling of Bolarum-Medchal stretch are

under progress in the MMTS Phase-II project. Construction is also underway on Falaknuma-

Umdanagar section.

Multi-level flyovers

As a part of the Telangana government’s initiative for redesigning the entire road network in

Hyderabad, Hyderabad is estimated to witness the construction of 20 multi-level flyovers very soon.

The Municipal Administration and Urban Development (MA&UD) Department has approved

construction of these flyovers and development of junctions as part of the Strategic Road

Development Plan (SRDP). SRDP was prepared to meet the growing requirements of the city, which

has a population of over one crore. Under the plan, multi-level flyovers, skywalks and signal-less

junctions will be developed at 54 places in the city.

The Greater Hyderabad Municipal Corporation (GHMC) will soon commence work on construction

of 20 multi-level flyovers and development of junctions to ease traffic congestion in the city. These

will be taken up under the design-build-maintain and transfer mode.

Consolidating the Water Infrastructure

Telangana’s flagship developmental programs – ‘Mission Kakatiya’ (reviving the water bodies) and

‘Mission Bhagiratha’ (also known as Telangana Water Grid Scheme, for enhancing the water

supply), are aimed at consolidating the water infrastructure in the state. It is estimated that INR

15,000 crore will be required for Mission Kakatiya to revive the water bodies and INR 28,000 crore

for Mission Bhagiratha which is envisaged to supply drinking water to all households by 2019.

Mission Bhagiratha will be providing water from Krishna and Godavari to the towns and villages of

Telangana and reduce water supply woes. Nizampet, Kondapur, Narsingi and Kukatpally are

expected to witness a positive impact as a consequence of this improved water supply since a

significant number of residential projects are coming up in these micro-markets.

Hyderabad Metro

Hyderabad Metro Rail (HMR) is a rapid transit system, currently under construction, for the city of

Hyderabad. It is being implemented entirely on public-private partnership (PPP) basis, with the state

government holding a minority equity stake.

MAJOR INFRASTRUCTURE DEVELOPMENTS

9

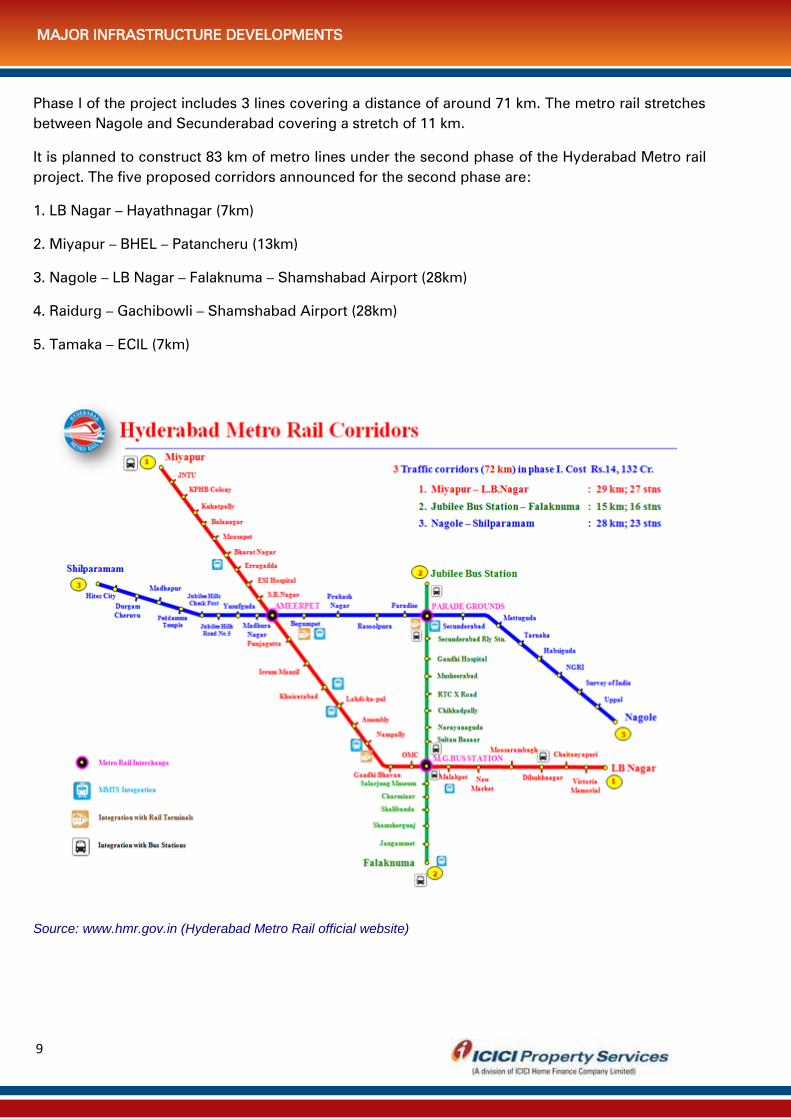

Phase I of the project includes 3 lines covering a distance of around 71 km. The metro rail stretches

between Nagole and Secunderabad covering a stretch of 11 km.

It is planned to construct 83 km of metro lines under the second phase of the Hyderabad Metro rail

project. The five proposed corridors announced for the second phase are:

1. LB Nagar – Hayathnagar (7km)

2. Miyapur – BHEL – Patancheru (13km)

3. Nagole – LB Nagar – Falaknuma – Shamshabad Airport (28km)

4. Raidurg – Gachibowli – Shamshabad Airport (28km)

5. Tamaka – ECIL (7km)

Source: www.hmr.gov.in (Hyderabad Metro Rail official website)

MAJOR INFRASTRUCTURE DEVELOPMENTS

10

A. Market Summary

Residential markets across Hyderabad witnessed a gradual phase of recovery after a long drawn

political unrest which culminated with the creation of Telangana state with Hyderabad as its capital

on 2nd June, 2014. Weak sentiments had dented the markets for over three years till the bifurcation

of the state, leading to an over-supply situation across the region. Our survey of the markets

indicates a stable off-take in residential stock during CY2015, with ready-to-move inventory finding

takers. New launches by prominent developers along the IT/ITeS corridor indicate a cautious

optimism prevailing in the markets. However, new launches across the micro-markets decreased by

about 10% in CY2015 Y-o-Y indicating a cautious stance being maintained by the developers. The

new government is trying to instill a positive sentiment in the market with a slew of infrastructure

initiatives and policies. It is expected that the market will remain stable with a positive bias, with

existing stock witnessing a stable off-take across the micro-markets.

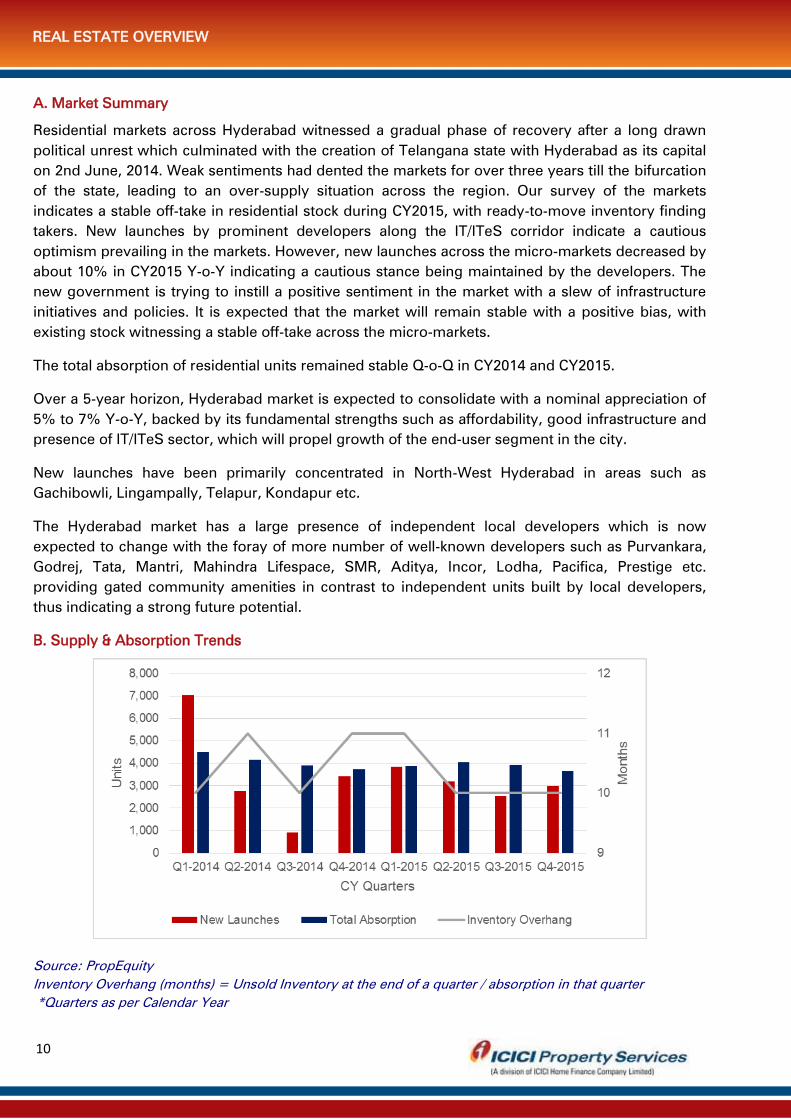

The total absorption of residential units remained stable Q-o-Q in CY2014 and CY2015.

Over a 5-year horizon, Hyderabad market is expected to consolidate with a nominal appreciation of

5% to 7% Y-o-Y, backed by its fundamental strengths such as affordability, good infrastructure and

presence of IT/ITeS sector, which will propel growth of the end-user segment in the city.

New launches have been primarily concentrated in North-West Hyderabad in areas such as

Gachibowli, Lingampally, Telapur, Kondapur etc.

The Hyderabad market has a large presence of independent local developers which is now

expected to change with the foray of more number of well-known developers such as Purvankara,

Godrej, Tata, Mantri, Mahindra Lifespace, SMR, Aditya, Incor, Lodha, Pacifica, Prestige etc.

providing gated community amenities in contrast to independent units built by local developers,

thus indicating a strong future potential.

B. Supply & Absorption Trends

Source: PropEquity

Inventory Overhang (months) = Unsold Inventory at the end of a quarter / absorption in that quarter

*Quarters as per Calendar Year

REAL ESTATE OVERVIEW

11

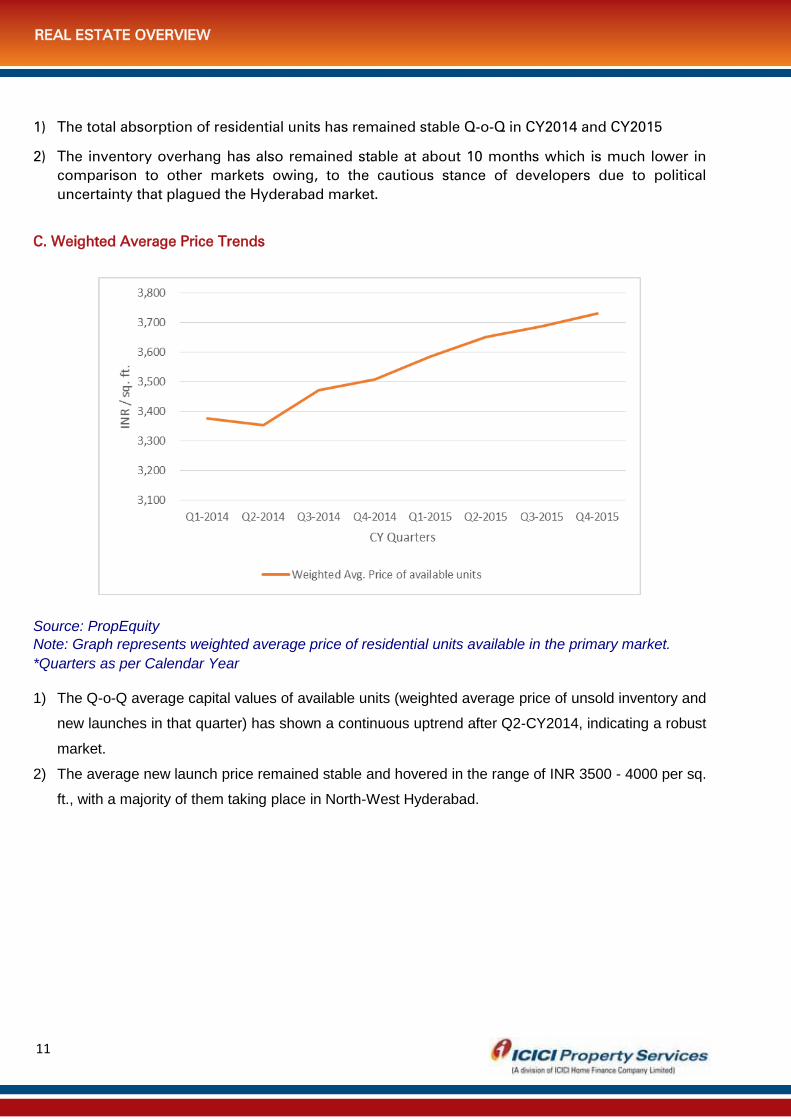

1) The total absorption of residential units has remained stable Q-o-Q in CY2014 and CY2015

2) The inventory overhang has also remained stable at about 10 months which is much lower in

comparison to other markets owing, to the cautious stance of developers due to political

uncertainty that plagued the Hyderabad market.

C. Weighted Average Price Trends

Source: PropEquity

Note: Graph represents weighted average price of residential units available in the primary market.

*Quarters as per Calendar Year

1) The Q-o-Q average capital values of available units (weighted average price of unsold inventory and

new launches in that quarter) has shown a continuous uptrend after Q2-CY2014, indicating a robust

market.

2) The average new launch price remained stable and hovered in the range of INR 3500 - 4000 per sq.

ft., with a majority of them taking place in North-West Hyderabad.

REAL ESTATE OVERVIEW

12

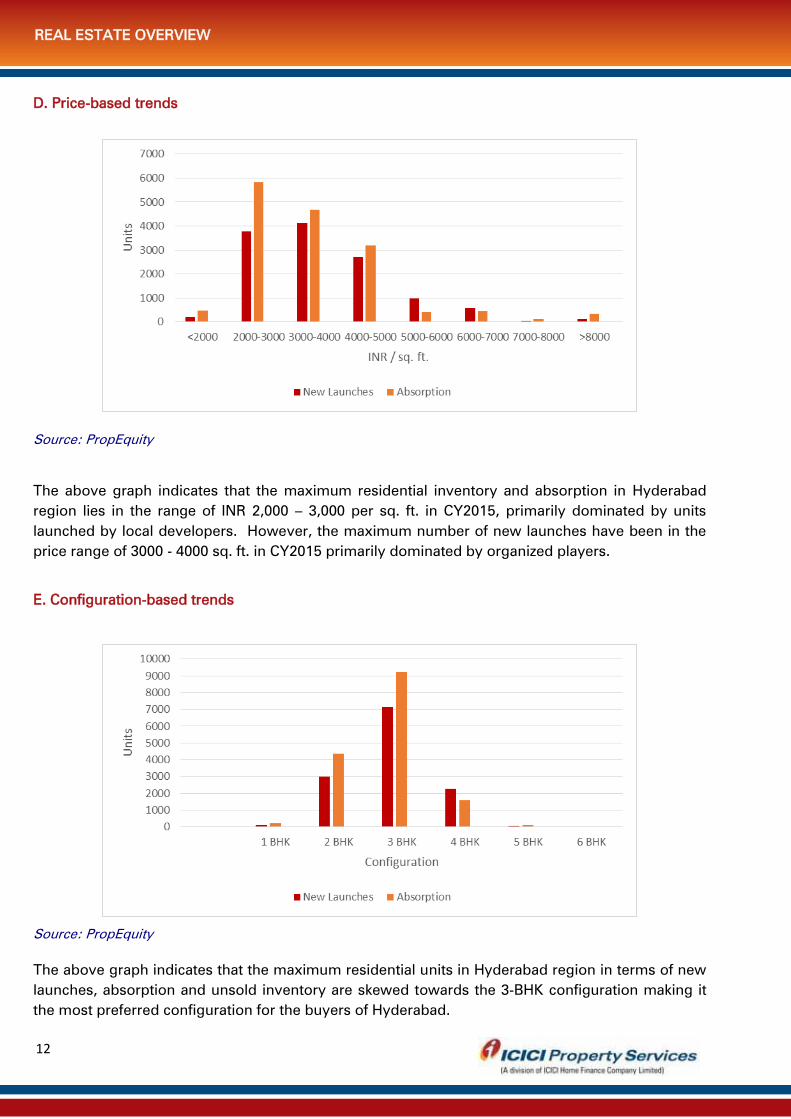

D. Price-based trends

Source: PropEquity

The above graph indicates that the maximum residential inventory and absorption in Hyderabad

region lies in the range of INR 2,000 – 3,000 per sq. ft. in CY2015, primarily dominated by units

launched by local developers. However, the maximum number of new launches have been in the

price range of 3000 - 4000 sq. ft. in CY2015 primarily dominated by organized players.

E. Configuration-based trends

Source: PropEquity

The above graph indicates that the maximum residential units in Hyderabad region in terms of new

launches, absorption and unsold inventory are skewed towards the 3-BHK configuration making it

the most preferred configuration for the buyers of Hyderabad.

REAL ESTATE OVERVIEW

13

Short Term 10-12 months Stagnation in capital value.

Long Term 50-60 months

5 - 7% Y-o-Y appreciation in capital value with an

upward bias on a conservative note.

The realty markets in Hyderabad which took a strong beating due to prolonged uncertainty over the

state bifurcation issue during 2010-2014, is today in a gradual phase of recovery. The period saw

buyers holding back their buying plans and remained on the sidelines due to lack of clarity. Weak

sentiments dented the markets for over three years and to kickstart demand during the lull phase

(2010-14), developers offered discounts on unsold units, and others postponed launches as the

market price was not attractive.

Our survey of the market indicates a stable off-take in residential stock during CY 2015, with ready-

to-move inventory witnessing buyers. New launches by prominent developers in North-West

Hyderabad have received a good response, indicating a cautious optimism prevailing in the

markets. It is expected that the market will remain stable, with existing stock witnessing an

improved off-take across micro-markets as compared to previous years.

Over a 5-year horizon, markets are expected to consolidate with a nominal appreciation of 5% - 7%

Y-o-Y, backed by its fundamental strengths such as affordability, good infrastructure and presence

of IT/ITeS sector, which will propel the growth of end-user buying in the city. Also driving the

positive sentiment among developers is the upcoming launch of the metro rail project, and the

political stability post the bifurcation. The buoyant office market activity has also helped regain the

market momentum.

Affordable Real estate Prices compared to Other Major Cities

Residential real estate prices in Hyderabad are yet to regain their peak values. It is currently in a

consolidation phase, with properties available at attractive valuations. Buyers are increasingly

focusing on acquiring properties in the western part of the city (in the proximity of financial district

and the IT Hub).

It is expected that demand will be higher in the INR 3,000 - 4,000 per sq. ft. segment as majority of

them lie along the metro rail corridor and enquiries have been significantly higher for such

locations.

REAL ESTATE OVERVIEW

14

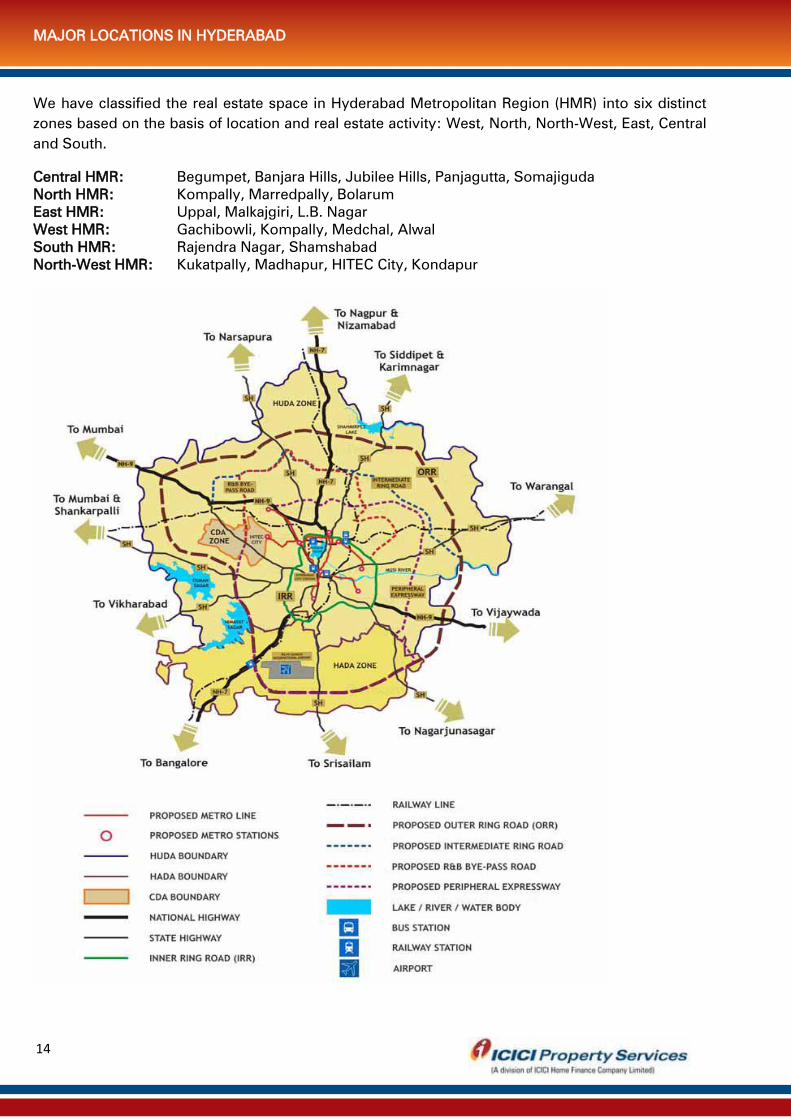

We have classified the real estate space in Hyderabad Metropolitan Region (HMR) into six distinct

zones based on the basis of location and real estate activity: West, North, North-West, East, Central

and South.

Central HMR: Begumpet, Banjara Hills, Jubilee Hills, Panjagutta, Somajiguda

North HMR: Kompally, Marredpally, Bolarum

East HMR: Uppal, Malkajgiri, L.B. Nagar

West HMR: Gachibowli, Kompally, Medchal, Alwal

South HMR: Rajendra Nagar, Shamshabad

North-West HMR: Kukatpally, Madhapur, HITEC City, Kondapur

MAJOR LOCATIONS IN HYDERABAD

15

Major Locations: Gachibowli, Nanakramguda, Narsingi, Manikonda, Khajaguda, Kismatpur,

Hyderguda, Gopanpalli, Tellapur, Nallagandla, Kokapet, Gandipet.

Key Highlights:

Gachibowli is witnessing development of projects in the price-band of INR 4,000 per sq. ft. to

INR 5,000 per sq. ft., depending on location, developer and specifications. Demand in this region

is end user-driven, majority of which caters to IT/ITeS employees. It is expected that this micro-

market will firm up in the coming quarters because of its proximity to HITEC City, Kondapur,

Manikonda, Chandanagar, among other areas falling under the western IT belt which are close

to the upcoming office supply. It has a high supply of under-construction projects and primarily

offers residential apartments. The saturation of residential areas in Central Hyderabad has

encouraged real estate development towards the west of the city. Ample social infrastructure in

terms of organised retail and multiple entertainment options have made this area one of the

most desirable locations in Hyderabad.

The region surrounding Nanakramguda is witnessing development in mid-segment residential

units. Projects are in the price-band of INR 3,500 per sq. ft. to INR 4,500 per sq. ft., depending on

location, developer and specifications. It is expected that there will be a gradual absorption of

inventory in projects nearing completion due to an increase in demand from the expanding IT

corridor in HITEC City and Financial District in Gachibowli.

Narsingi is emerging as an alternate residential destination along the western corridor. Its

proximity to ORR and IT/ITeS hub has led to a spurt of residential development in these

locations. Mid-segment properties at Narsingi are in the price-band of INR 3,000 per sq. ft. to

INR 4,000 per sq. ft.

The micro-market of Manikonda is witnessing development of integrated townships. A rapidly

growing commercial-cum-residential area, it shares neighborhood with Gachibowli, Shaikpet,

Jubilee Hills and Kondapur. One of the major advantages of Manikonda is its connectivity via

Outer Ring Road and Old Mumbai Highway; the former connects it to the Airport, the latter

connects it to IT hubs. Manikonda is witnessing development of mid-segment properties in the

price range of INR 3,000 per sq. ft. to INR 3,700 per sq. ft., depending on location, developer and

specifications. A gradual off-take of existing stock is expected in coming months due to its

relative affordability, thus emerging as an alternative rental destination.

Tellapur is witnessing development of mid-segment and villa projects. Sale of mid-segment

projects is expected to remain sluggish due to presence of sufficient supply in surrounding

micro-markets, closer to the IT/ITeS hub of Gachibowli. Villa projects in this micro-market are

expected to witness a relatively better off-take with increasing influx of people into Hyderabad

because of its positive future growth potential and its proximity to Gachibowli.

Kokapet and Gandipet are predominantly witnessing development of gated communities and

villa projects. With an increase in residential demand due to the increasing office supply around

these micro-markets coupled with good connectivity to other parts of Hyderabad (through ORR),

these micro-markets are expected to witness stability in terms of demand.

Some of the major developers in this region are Aditya, Aparna, Incor, Lodha, Mahindra

Lifespace, Manjira, Mantri, Pacifica, Prestige and SMR.

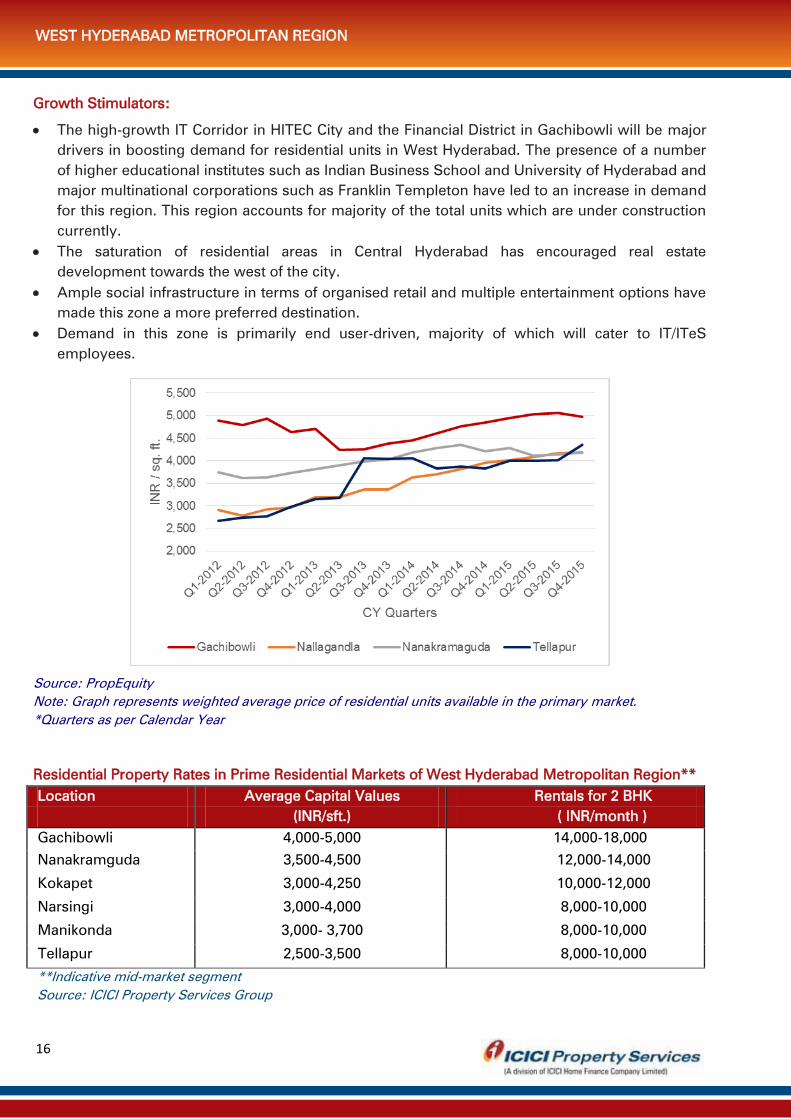

WEST HYDERABAD METROPOLITAN REGION

16

Growth Stimulators:

The high-growth IT Corridor in HITEC City and the Financial District in Gachibowli will be major

drivers in boosting demand for residential units in West Hyderabad. The presence of a number

of higher educational institutes such as Indian Business School and University of Hyderabad and

major multinational corporations such as Franklin Templeton have led to an increase in demand

for this region. This region accounts for majority of the total units which are under construction

currently.

The saturation of residential areas in Central Hyderabad has encouraged real estate

development towards the west of the city.

Ample social infrastructure in terms of organised retail and multiple entertainment options have

made this zone a more preferred destination.

Demand in this zone is primarily end user-driven, majority of which will cater to IT/ITeS

employees.

Source: PropEquity

Note: Graph represents weighted average price of residential units available in the primary market.

*Quarters as per Calendar Year

Residential Property Rates in Prime Residential Markets of West Hyderabad Metropolitan Region**

Location Average Capital Values Rentals for 2 BHK

(INR/sft.) ( INR/month )

Gachibowli 4,000-5,000 14,000-18,000

Nanakramguda 3,500-4,500 12,000-14,000

Kokapet 3,000-4,250 10,000-12,000

Narsingi 3,000-4,000 8,000-10,000

Manikonda 3,000- 3,700 8,000-10,000

Tellapur 2,500-3,500 8,000-10,000

**Indicative mid-market segment

Source: ICICI Property Services Group

WEST HYDERABAD METROPOLITAN REGION

17

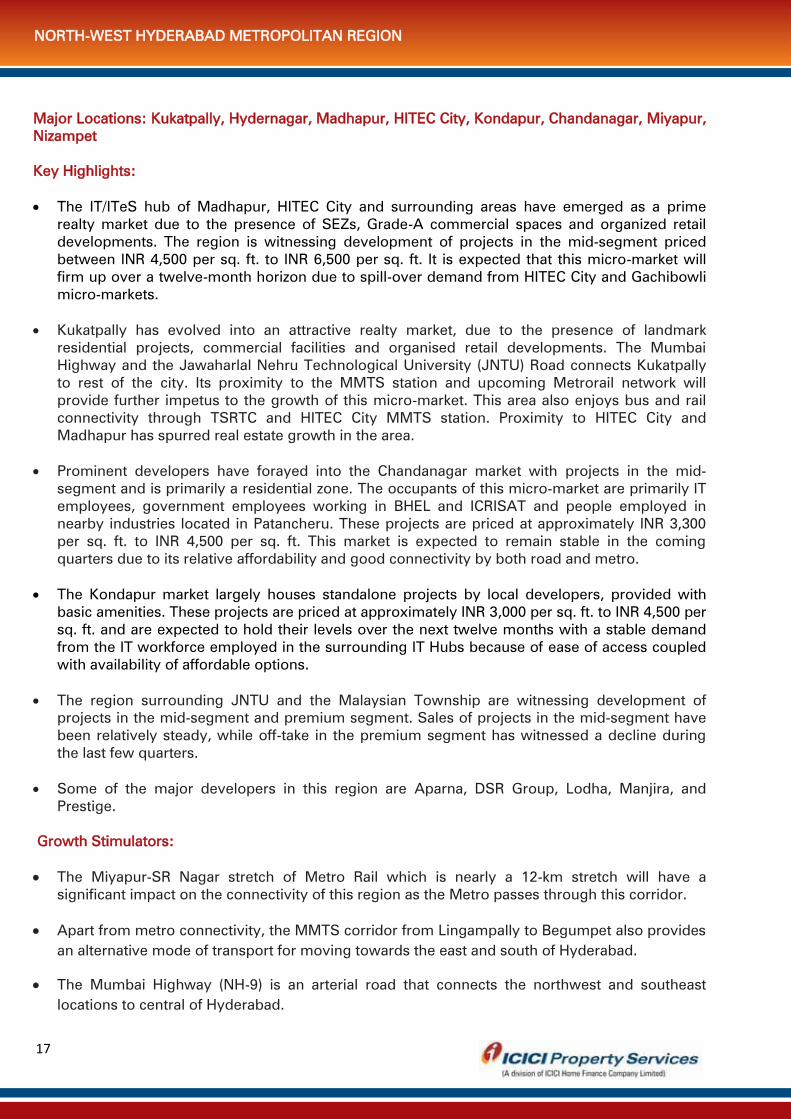

Major Locations: Kukatpally, Hydernagar, Madhapur, HITEC City, Kondapur, Chandanagar, Miyapur,

Nizampet

Key Highlights:

The IT/ITeS hub of Madhapur, HITEC City and surrounding areas have emerged as a prime

realty market due to the presence of SEZs, Grade-A commercial spaces and organized retail

developments. The region is witnessing development of projects in the mid-segment priced

between INR 4,500 per sq. ft. to INR 6,500 per sq. ft. It is expected that this micro-market will

firm up over a twelve-month horizon due to spill-over demand from HITEC City and Gachibowli

micro-markets.

Kukatpally has evolved into an attractive realty market, due to the presence of landmark

residential projects, commercial facilities and organised retail developments. The Mumbai

Highway and the Jawaharlal Nehru Technological University (JNTU) Road connects Kukatpally

to rest of the city. Its proximity to the MMTS station and upcoming Metrorail network will

provide further impetus to the growth of this micro-market. This area also enjoys bus and rail

connectivity through TSRTC and HITEC City MMTS station. Proximity to HITEC City and

Madhapur has spurred real estate growth in the area.

Prominent developers have forayed into the Chandanagar market with projects in the mid-

segment and is primarily a residential zone. The occupants of this micro-market are primarily IT

employees, government employees working in BHEL and ICRISAT and people employed in

nearby industries located in Patancheru. These projects are priced at approximately INR 3,300

per sq. ft. to INR 4,500 per sq. ft. This market is expected to remain stable in the coming

quarters due to its relative affordability and good connectivity by both road and metro.

The Kondapur market largely houses standalone projects by local developers, provided with

basic amenities. These projects are priced at approximately INR 3,000 per sq. ft. to INR 4,500 per

sq. ft. and are expected to hold their levels over the next twelve months with a stable demand

from the IT workforce employed in the surrounding IT Hubs because of ease of access coupled

with availability of affordable options.

The region surrounding JNTU and the Malaysian Township are witnessing development of

projects in the mid-segment and premium segment. Sales of projects in the mid-segment have

been relatively steady, while off-take in the premium segment has witnessed a decline during

the last few quarters.

Some of the major developers in this region are Aparna, DSR Group, Lodha, Manjira, and

Prestige.

Growth Stimulators:

The Miyapur-SR Nagar stretch of Metro Rail which is nearly a 12-km stretch will have a

significant impact on the connectivity of this region as the Metro passes through this corridor.

Apart from metro connectivity, the MMTS corridor from Lingampally to Begumpet also provides

an alternative mode of transport for moving towards the east and south of Hyderabad.

The Mumbai Highway (NH-9) is an arterial road that connects the northwest and southeast

locations to central of Hyderabad.

NORTH-WEST HYDERABAD METROPOLITAN REGION

18

This zone is well-connected to all other parts of the city through well-planned roads.

Close proximity to the IT Corridor in HITEC City and the Financial District in Gachibowli will be

major drivers in boosting demand.

Source: PropEquity

Note: Graph represents weighted average price of residential units available in the primary market.

*Quarters as per Calendar Year

Residential Property Rates in Prime Residential Markets of North-West Hyderabad Metropolitan

Region**

Location Average Capital Values Rentals for 2 BHK

(INR/sft.) (INR/month)

Madhapur 4,500-6,500 14,000-18,000

Kukatpally 4,000-5,000 12,000-14,000

Chandanagar 3,300-4,500 8,000-12,000

Miyapur 3,000-4,500 8,000-12,000

Kondapur 3,000-4,500 10,000-12,000

Nizampet 1,800-2,800 8,000-10,000

**Indicative mid-market segment

Source: ICICI Property Services Group

NORTH-WEST HYDERABAD METROPOLITAN REGION

19

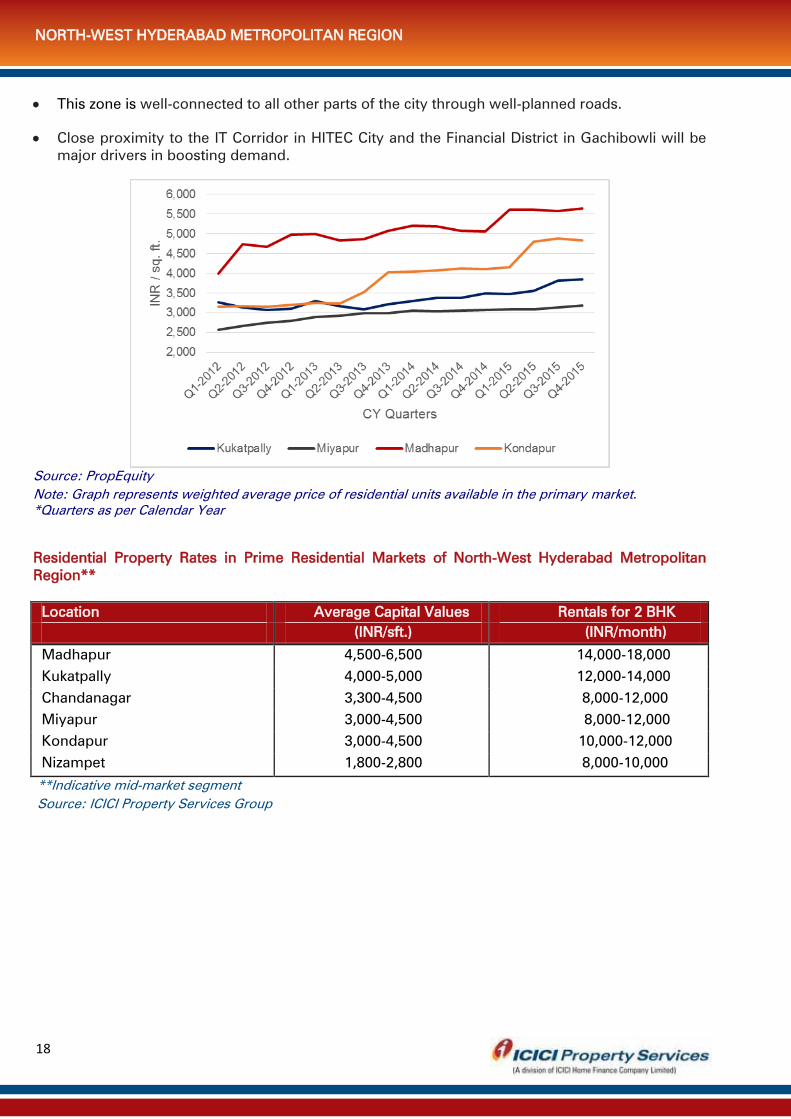

Major Locations: Kompally, Alwal, Sainikpuri, A.S. Rao Nagar, Bolarum, Marredpalli, Himayath

Nagar

Key Highlights:

Marredpalli has an inherent presence of the end-user segment due to its proximity to the CBD

and existing trader community coupled with limited upcoming supply in surrounding areas. This

micro-market is a premium locality. There is no significant availability of land but standalone

apartments are coming up through redevelopment. This region enjoys a strategic location

situated near the Secunderabad station and also ample social infrastructure in terms of schools,

hospitals etc.

A.S. Rao Nagar, in close proximity to Sainikpuri, is witnessing development of affordable

housing and primarily has the presence of local developers. Projects in affordable segment are

priced at approximately INR 3,000 per sq. ft. to INR 3,500 per sq. ft. This is a developed micro-

market with low number of new launches.

Kompally is witnessing development of projects which are primarily expected to cater to the

population working in pharmaceutical companies present in Jeedimetla. It is expected that this

area will firm up over the next twelve months due to good social infrastructure, educational

institutes and industries.

Some of the major developers in this region are Aparna, Janpriya, Modi Builders and NCL

Homes.

Growth Stimulators:

National Highway 7 passes through this region, crossing the areas of Medchal, Kompally,

Secunderabad, and Shivarampally. It is an arterial road that connects this region with locations

in southern and central Hyderabad.

Demand for industrial and warehouse development along with the region’s proximity to

cantonment area will be driving factors for the real estate activity in this region.

Source: PropEquity

Note: Graph represents weighted average price of residential units available in the primary market.

*Quarters as per Calendar Year

NORTH HYDERABAD METROPOLITAN REGION

20

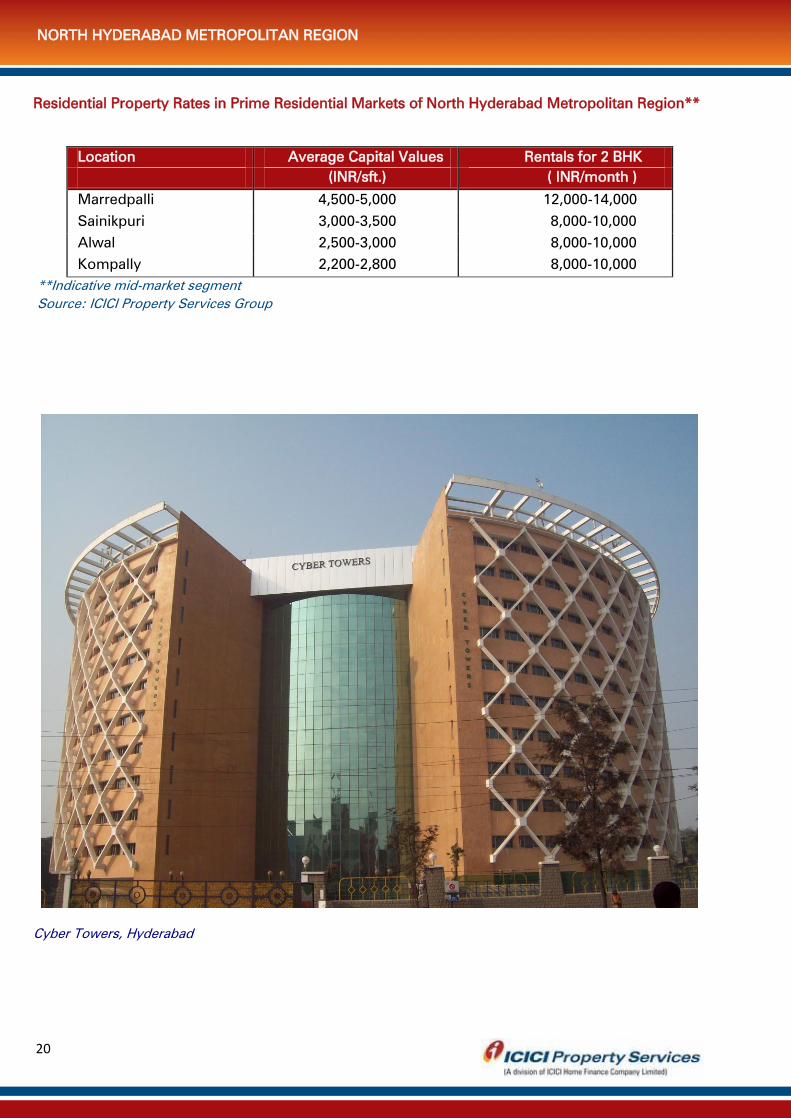

Residential Property Rates in Prime Residential Markets of North Hyderabad Metropolitan Region**

Location Average Capital Values Rentals for 2 BHK

(INR/sft.) ( INR/month )

Marredpalli 4,500-5,000 12,000-14,000

Sainikpuri 3,000-3,500 8,000-10,000

Alwal 2,500-3,000 8,000-10,000

Kompally 2,200-2,800 8,000-10,000

**Indicative mid-market segment

Source: ICICI Property Services Group

Cyber Towers, Hyderabad

NORTH HYDERABAD METROPOLITAN REGION

21

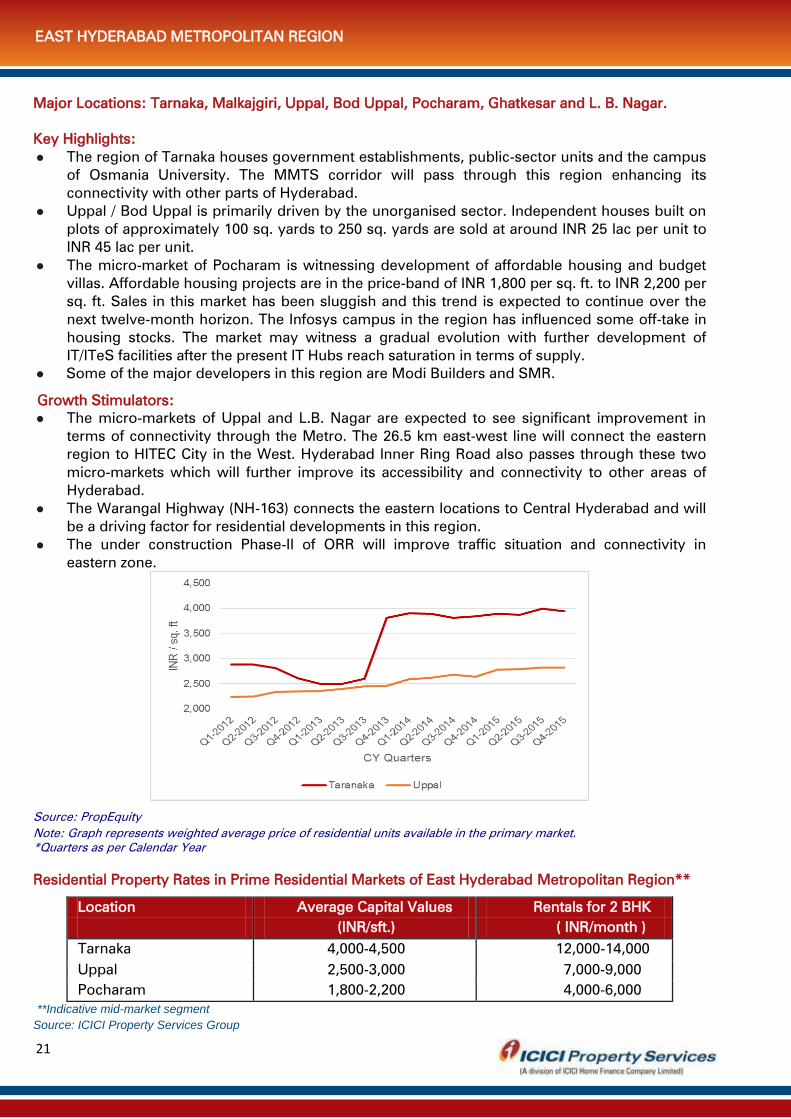

Major Locations: Tarnaka, Malkajgiri, Uppal, Bod Uppal, Pocharam, Ghatkesar and L. B. Nagar.

Key Highlights:

The region of Tarnaka houses government establishments, public-sector units and the campus

of Osmania University. The MMTS corridor will pass through this region enhancing its

connectivity with other parts of Hyderabad.

Uppal / Bod Uppal is primarily driven by the unorganised sector. Independent houses built on

plots of approximately 100 sq. yards to 250 sq. yards are sold at around INR 25 lac per unit to

INR 45 lac per unit.

The micro-market of Pocharam is witnessing development of affordable housing and budget

villas. Affordable housing projects are in the price-band of INR 1,800 per sq. ft. to INR 2,200 per

sq. ft. Sales in this market has been sluggish and this trend is expected to continue over the

next twelve-month horizon. The Infosys campus in the region has influenced some off-take in

housing stocks. The market may witness a gradual evolution with further development of

IT/ITeS facilities after the present IT Hubs reach saturation in terms of supply.

Some of the major developers in this region are Modi Builders and SMR.

Growth Stimulators:

The micro-markets of Uppal and L.B. Nagar are expected to see significant improvement in

terms of connectivity through the Metro. The 26.5 km east-west line will connect the eastern

region to HITEC City in the West. Hyderabad Inner Ring Road also passes through these two

micro-markets which will further improve its accessibility and connectivity to other areas of

Hyderabad.

The Warangal Highway (NH-163) connects the eastern locations to Central Hyderabad and will

be a driving factor for residential developments in this region.

The under construction Phase-II of ORR will improve traffic situation and connectivity in

eastern zone.

Source: PropEquity

Note: Graph represents weighted average price of residential units available in the primary market.

*Quarters as per Calendar Year

Residential Property Rates in Prime Residential Markets of East Hyderabad Metropolitan Region**

Location Average Capital Values Rentals for 2 BHK

(INR/sft.) ( INR/month )

Tarnaka 4,000-4,500 12,000-14,000

Uppal 2,500-3,000 7,000-9,000

Pocharam 1,800-2,200 4,000-6,000

**Indicative mid-market segment

Source: ICICI Property Services Group

EAST HYDERABAD METROPOLITAN REGION

22

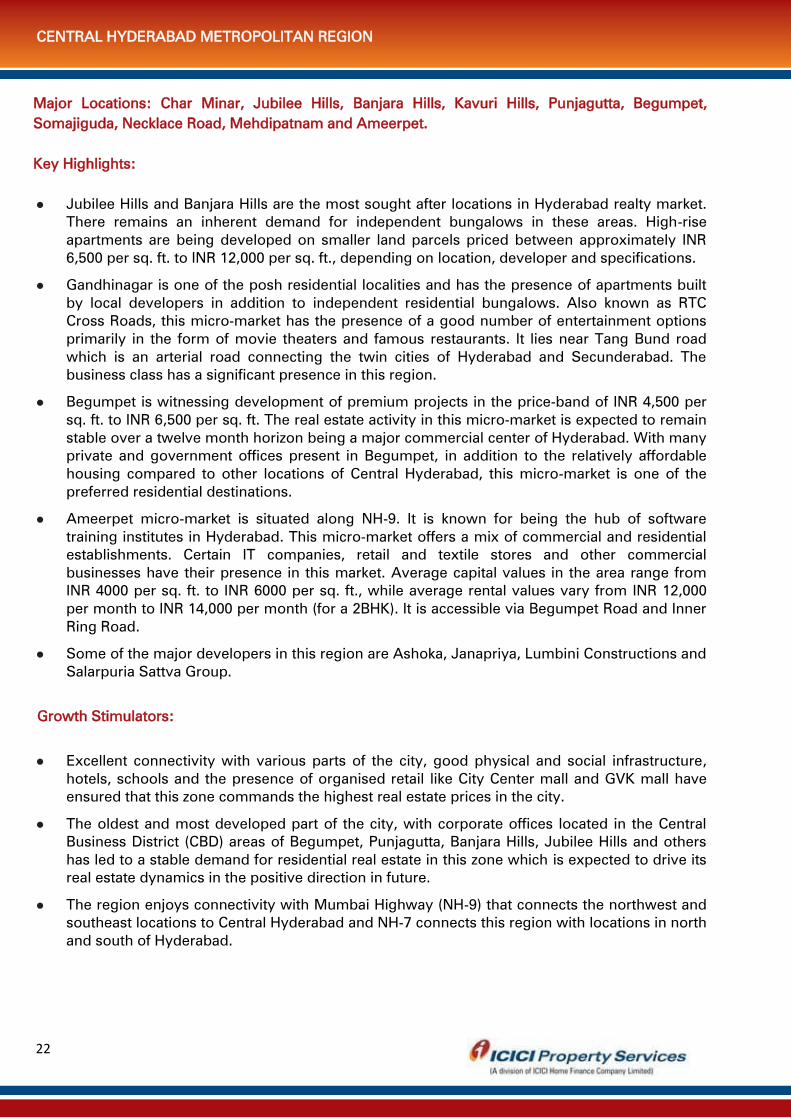

Major Locations: Char Minar, Jubilee Hills, Banjara Hills, Kavuri Hills, Punjagutta, Begumpet,

Somajiguda, Necklace Road, Mehdipatnam and Ameerpet.

Key Highlights:

Jubilee Hills and Banjara Hills are the most sought after locations in Hyderabad realty market.

There remains an inherent demand for independent bungalows in these areas. High-rise

apartments are being developed on smaller land parcels priced between approximately INR

6,500 per sq. ft. to INR 12,000 per sq. ft., depending on location, developer and specifications.

Gandhinagar is one of the posh residential localities and has the presence of apartments built

by local developers in addition to independent residential bungalows. Also known as RTC

Cross Roads, this micro-market has the presence of a good number of entertainment options

primarily in the form of movie theaters and famous restaurants. It lies near Tang Bund road

which is an arterial road connecting the twin cities of Hyderabad and Secunderabad. The

business class has a significant presence in this region.

Begumpet is witnessing development of premium projects in the price-band of INR 4,500 per

sq. ft. to INR 6,500 per sq. ft. The real estate activity in this micro-market is expected to remain

stable over a twelve month horizon being a major commercial center of Hyderabad. With many

private and government offices present in Begumpet, in addition to the relatively affordable

housing compared to other locations of Central Hyderabad, this micro-market is one of the

preferred residential destinations.

Ameerpet micro-market is situated along NH-9. It is known for being the hub of software

training institutes in Hyderabad. This micro-market offers a mix of commercial and residential

establishments. Certain IT companies, retail and textile stores and other commercial

businesses have their presence in this market. Average capital values in the area range from

INR 4000 per sq. ft. to INR 6000 per sq. ft., while average rental values vary from INR 12,000

per month to INR 14,000 per month (for a 2BHK). It is accessible via Begumpet Road and Inner

Ring Road.

Some of the major developers in this region are Ashoka, Janapriya, Lumbini Constructions and

Salarpuria Sattva Group.

Growth Stimulators:

Excellent connectivity with various parts of the city, good physical and social infrastructure,

hotels, schools and the presence of organised retail like City Center mall and GVK mall have

ensured that this zone commands the highest real estate prices in the city.

The oldest and most developed part of the city, with corporate offices located in the Central

Business District (CBD) areas of Begumpet, Punjagutta, Banjara Hills, Jubilee Hills and others

has led to a stable demand for residential real estate in this zone which is expected to drive its

real estate dynamics in the positive direction in future.

The region enjoys connectivity with Mumbai Highway (NH-9) that connects the northwest and

southeast locations to Central Hyderabad and NH-7 connects this region with locations in north

and south of Hyderabad.

CENTRAL HYDERABAD METROPOLITAN REGION

23

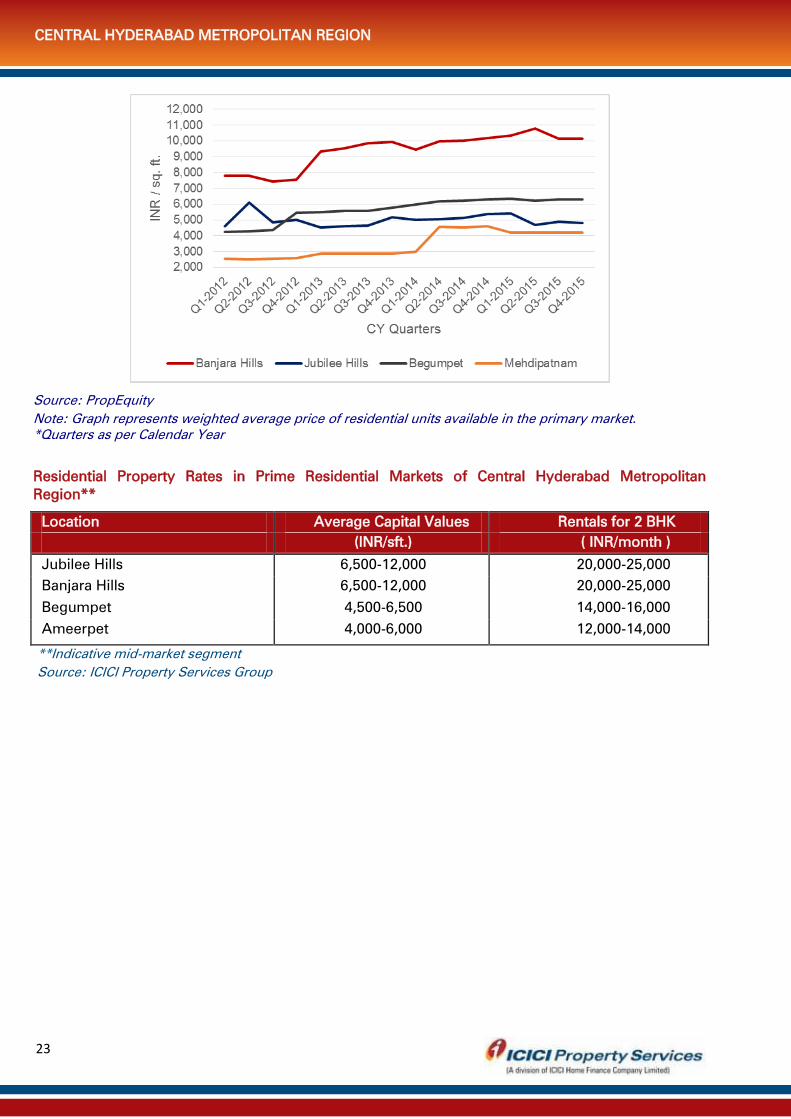

Source: PropEquity

Note: Graph represents weighted average price of residential units available in the primary market.

*Quarters as per Calendar Year

Residential Property Rates in Prime Residential Markets of Central Hyderabad Metropolitan

Region**

Location Average Capital Values Rentals for 2 BHK

(INR/sft.) ( INR/month )

Jubilee Hills 6,500-12,000 20,000-25,000

Banjara Hills 6,500-12,000 20,000-25,000

Begumpet 4,500-6,500 14,000-16,000

Ameerpet 4,000-6,000 12,000-14,000

**Indicative mid-market segment

Source: ICICI Property Services Group

CENTRAL HYDERABAD METROPOLITAN REGION

24

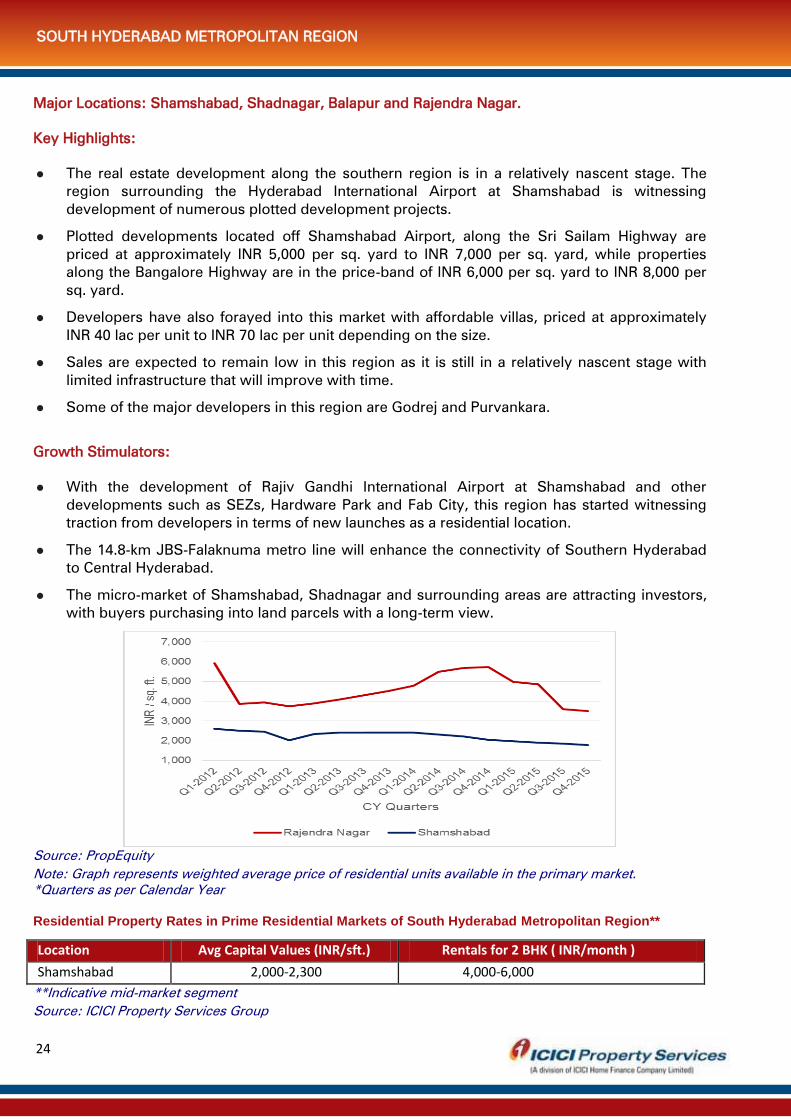

Major Locations: Shamshabad, Shadnagar, Balapur and Rajendra Nagar.

Key Highlights:

The real estate development along the southern region is in a relatively nascent stage. The

region surrounding the Hyderabad International Airport at Shamshabad is witnessing

development of numerous plotted development projects.

Plotted developments located off Shamshabad Airport, along the Sri Sailam Highway are

priced at approximately INR 5,000 per sq. yard to INR 7,000 per sq. yard, while properties

along the Bangalore Highway are in the price-band of INR 6,000 per sq. yard to INR 8,000 per

sq. yard.

Developers have also forayed into this market with affordable villas, priced at approximately

INR 40 lac per unit to INR 70 lac per unit depending on the size.

Sales are expected to remain low in this region as it is still in a relatively nascent stage with

limited infrastructure that will improve with time.

Some of the major developers in this region are Godrej and Purvankara.

Growth Stimulators:

With the development of Rajiv Gandhi International Airport at Shamshabad and other

developments such as SEZs, Hardware Park and Fab City, this region has started witnessing

traction from developers in terms of new launches as a residential location.

The 14.8-km JBS-Falaknuma metro line will enhance the connectivity of Southern Hyderabad

to Central Hyderabad.

The micro-market of Shamshabad, Shadnagar and surrounding areas are attracting investors,

with buyers purchasing into land parcels with a long-term view.

Source: PropEquity

Note: Graph represents weighted average price of residential units available in the primary market.

*Quarters as per Calendar Year

Residential Property Rates in Prime Residential Markets of South Hyderabad Metropolitan Region**

Location Avg Capital Values (INR/sft.) Rentals for 2 BHK ( INR/month )

Shamshabad 2,000-2,300 4,000-6,000

**Indicative mid-market segment

Source: ICICI Property Services Group

SOUTH HYDERABAD METROPOLITAN REGION

25

Good / low cost

Above Average / below average cost

Average / Medium Cost

Below Average / above average cost

Bad / High Cost

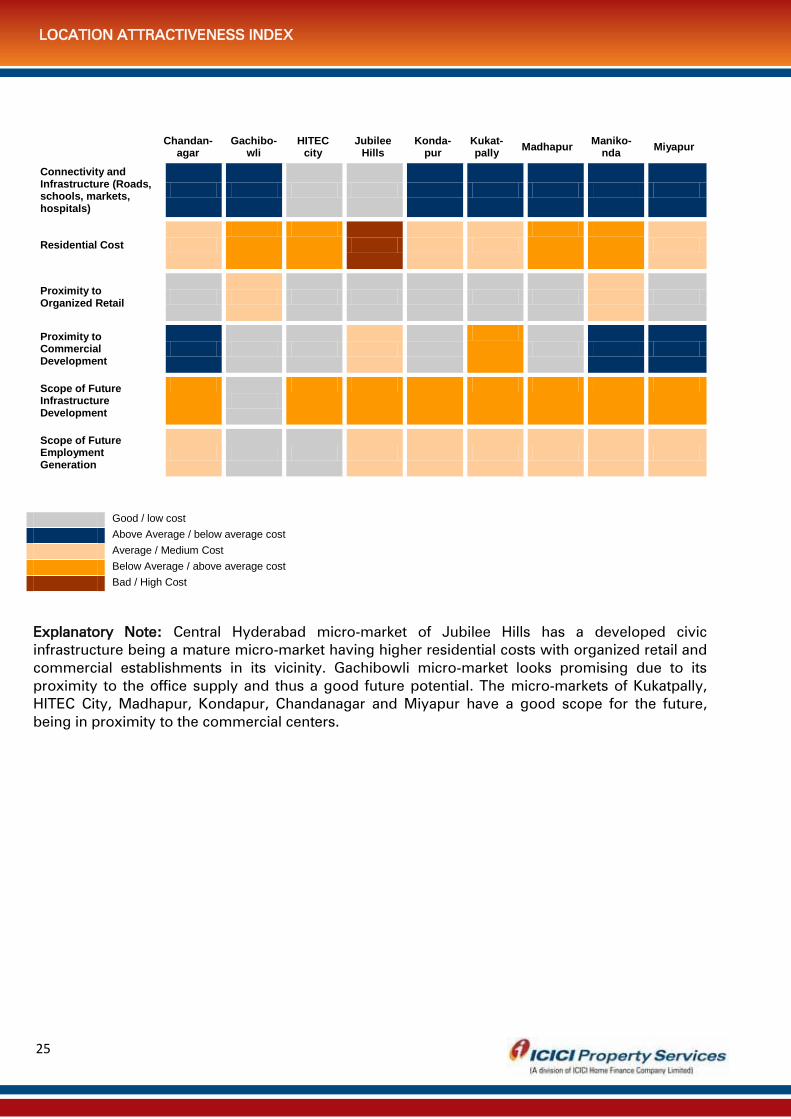

Explanatory Note: Central Hyderabad micro-market of Jubilee Hills has a developed civic

infrastructure being a mature micro-market having higher residential costs with organized retail and

commercial establishments in its vicinity. Gachibowli micro-market looks promising due to its

proximity to the office supply and thus a good future potential. The micro-markets of Kukatpally,

HITEC City, Madhapur, Kondapur, Chandanagar and Miyapur have a good scope for the future,

being in proximity to the commercial centers.

Chandan-agar

Gachibo-wli

HITEC city

Jubilee Hills

Konda-pur

Kukat-pally

Madhapur Maniko-

nda Miyapur

Connectivity and Infrastructure (Roads, schools, markets, hospitals)

Residential Cost

Proximity to Organized Retail

Proximity to Commercial Development

Scope of Future Infrastructure Development

Scope of Future Employment Generation

GHAZIABAD

LOCATION ATTRACTIVENESS INDEX

26

ANALYST

TANAY AGARWAL

Deputy Manager – Research

ICICI Home Finance Co. Ltd.

For any further queries, please e–mail us at [email protected]

or

For more on our research reports & periodicals please log on to

www.icicihfc.com / www.icicihomesearch.com

ICICI HFC DISCLAIMERS & DISCLOSURES

The information set out in this document has been prepared by ICICI HFC Ltd. based upon projections which

have been determined in good faith by ICICI HFC Ltd. There can be no assurance that such projections will

prove to be accurate. Past performance cannot be a guide to future performance.

The information in this document reflects prevailing conditions and our views as of this date, all of which are

subject to change. In preparing this document we have relied upon and assumed, without independent

verification, the accuracy and completeness of all information available from public sources or which was

provided to us or which was otherwise reviewed by us. ICICI HFC Ltd. does not accept any responsibility for

any errors whether caused by negligence or otherwise or for any loss or damage incurred by anyone in

reliance on anything set out in this document. No reliance may be placed for any purpose whatsoever on the

information contained in this document or on its completeness

The product(s)/service(s)/offer(s) as contained herein are provided /offered by third party and are subject to

their respective terms and conditions and not intended to create any rights or obligations.

The information set out in this document may be subject to change and such information may change

materially.

This document is being communicated to you solely for the purposes of providing our views on current market

trends on a confidential basis and does not carry any right of publication or disclosure to any third party. By

accepting delivery of this document each recipient undertakes not to reproduce or distribute this presentation in

whole or in part, nor to disclose any of its contents (except to its professional advisers) without the prior written

consent of ICICI HFC Ltd., who the recipient agrees has the benefit of this undertaking. The recipient and its

professional advisers will keep permanently confidential information contained herein and not already in the public

domain.

This document is not an offer, invitation or solicitation of any kind to buy or sell any product/ service and is not

intended to create any rights or obligations. Nothing in this document is intended to constitute legal, tax,

securities or investment advice, or opinion regarding the appropriateness of any investment, or a solicitation

for any product or service. The use of any information set out in this document is entirely at the recipient's own

risk. Recipients of this Information should exercise appropriate due diligence, including legal and tax diligence,

prior to taking of any decision.