Embed Size (px)

Citation preview

Hyundai Merchant Marine December 2013

Table of Contents

1. Company Overview

1.1 Business Portfolio

1.2 Fleet Portfolio

1.3 Fleet Expansion Plan

2. Performance Review

3. Divisional Data

4. Financial Data

5. Appendix

1. Company Overview

Business Portfolio

HMM has three main business operations: container, wet bulk, and dry bulk shipping service.

Diversified business portfolio supports sustainable growth withstanding market volatility.

■ Historical Revenue ■ Historical Operating Income

3

15%

(Unit : KRW billion)

(Source : Non–consolidated financial statements)

3,945

5,119 4,846 4,734

5,092

8,003

6,115

8,087

7,188 7,714

6,908

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Container Wet Bulk Dry Bulk

18%

64%

16%

20%

64%

14%

23%

63%

16%

18%

66%

15%

19%

66%

13%

19%

68%

15%

14%

71%

15%

12%

73%

16%

12%

72%

15%

12%

73%

12%

16%

72%

18%

303

555 466

97

314

587

-565

602

-318

-520

-351

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Container Wet Bulk Dry Bulk Total(Unit : KRW billion, %)

1. Company Overview

Fleet Portfolio

※ Capacity Unit : Container 1,000 TEU / Wet Bulk 1,000 DWT / Dry Bulk 1,000 DWT (Chartered over one year)

(As of December 31, 2013)

4

Owned Chartered Total

No. Capacity No. Capacity No. Capacity

Container > 10,000TEU 5 65 5 65

8,000-10,000TEU 4 34 4 34 8 68

4,000-8,000TEU 14 73 19 111 33 184

< 4,000TEU 10 19 10 19

Container total 18 107 38 229 56 336

Wet Bulk Gas carrier 6 454 3 226 9 680

Crude tanker 7 1,536 7 1,810 14 3,346

Other tanker 2 98 6 284 8 382

Wet bulk total 15 2,088 16 2,320 31 4,408

Dry Bulk Capesize 11 1,855 10 1,854 21 3,709

Panamax 7 551 7 551

Supramax 2 120 21 1,159 23 1,279

Handysize 1 38 9 255 10 293

Heavy Lift 10 273 10 273

Dry bulk total 14 2,013 57 4,092 71 6,105

Total 47 111 158

1. Company Overview

Fleet Expansion Plan

2014 2015 2016 2017

Owned Chartered Owned Chartered Owned Chartered Owned Chartered

Container 13,100 TEU 5

10,000 TEU 6

Wet Bulk VLCC

Dry Bulk Capesize 1 4 1

Panamax 3

Supramax

Handysize

Heavy Lift

Total No. of New vessel 5 1 7 6 1

(As of December 31, 2013)

(Chartered over one year) (Number of delivered vessel)* 5

Table of Contents

1. Company Overview

2. Performance Review

2.1 FY2013 Annual Results

2.2 Quarterly Results

2.3 Divisional Results

2.4 Cost Structure

3. Divisional Data

4. Financial Data

5. Appendix

FY2013 Results

2. Performance Review

(Unit : KRW billion, USD million)

7

FY2013 FY2012 YoY

Revenue 6,908 7,714 -10.4%

(USD million) 6,294 6,830 -7.8%

COGS 7,096 8,064 -12.0%

SG&A 163 170 -4.1%

Operating Income -351 -520

Operating Margin -5.1% -6.7%

1. Revenue : KRW 6,908 Bn

YoY - 10.4%

Container Freight Rate YoY -7.6%

2. COGS : KRW 7,096 Bn

YoY -12.0%

Fuel Cost YoY -29.9%

Charterage YoY -11.2%

3. Operating Income : KRW -351 Bn

Quarterly Results

2. Performance Review

(Unit : KRW billion, USD million)

8

4Q 2013 3Q 2013 QoQ 4Q 2012 YoY

Revenue 1,650 1,740 -5.2% 1,842 -10.4%

(USD million) 1,557 1,564 -0.4% 1,696 -8.2%

COGS 1,717 1,743 -1.5% 1,966 -12.7%

SG&A 39 43 44

Operating Income -107 -46 -168

Operating Margin -6.5% -2.6% -9.1%

(Source : Non–consolidated financial statements)

Divisional Results

2. Performance Review

2013 4Q 2013 3Q QoQ 2012 4Q YoY

Container Revenue 1,221 1,297 -5.9% 1,324 -7.9%

Operating Income -51 4 -58

Operating Margin -4.2% 0.3% -4.4%

Wet Bulk Revenue 183 184 -0.5% 209 -12.4%

Operating Income -9 -24 -10

Operating Margin -4.9% -13.0% -4.3%

Dry Bulk Revenue 246 259 -5.0% 309 -20.4%

Operating Income -47 -26 -100

Operating Margin -19.0% -10.0% -32.5%

Total Revenue 1,650 1,740 -5.2% 1,842 -10.4%

Operating Income -107 -46 -168

Operating Margin -6.5% -2.7% -9.1%

(Unit : KRW billion)

9 (Source : HMM inside data)

Cost Structure

2. Performance Review

(Unit : KRW billion)

10

4Q 2013 3Q 2013 QoQ 4Q 2012 YoY

COGS 1,717 1,743 -1.5% 1,966 -12.7%

Cargo Handling 768 809 -5.1% 774 -0.8%

Fuel 296 332 -10.8% 480 -38.3%

Charterage 574 531 8.1% 590 -2.5%

Depreciations 40 45 -11.1% 45 -11.1%

Others 39 26 50.0% 77 -49.4%

■ COGS Structure

44%

17%

34%

2% 2%

Cargo Handling Fuel Charterage Depreciations Others

KRW 1,717 Bn

COGS decreased by 1.5% QoQ.

Cargo Handling fee decreased by 5.1% QoQ as container volume diminished.

Fuel cost fell by 10.8% QoQ due to fuel saving plans as well as lowering of bunker price.

(Source : HMM inside data)

Table of Contents

1. Company Overview

2. Performance Review

3. Divisional Data

3.1 Container Division

3.2 Wet Bulk Division

3.3 Dry Bulk Division

4. Financial Data

5. Appendix

Container Division

(Source: HMM inside data)

■ Freight Rate Trend

HMM implemented GRI(General Rate Increase) for all U.S destinations as of November 15, 2013.

$950/TEU GRI in Asia-North Europe & Med trades(W/B) in November is followed by another $800/TEU GRI as of

December 16.

3. Divisional Data

■ HMM GRI Record

12

50

75

100

125

150

Transpacific Asia-Europe Intra Asia

(Unit : percentage)

*

Service Effective

$400/FEU November 15

$200/FEU December 20

PSS $50/FEU January 6, 2014

$300/FEU January 15, 2014

$300/FEU March 15, 2014

$515/TEU September 1

$950/TEU November 1

$800/TEU December 16

$800/TEU January 13, 2014

$500/TEU March 15, 2014

Guideline

Transpacific

(E/B)

Asia Europe

(W/B)

Container Division

(Source: HMM inside data)

■ Utilization Ratio

Trade volume remains strong despite 4Q slack season.

Carriers seek to improve supply-demand imbalance by way of reorganizing their service products as well as of

expanding blank sailings.

3. Divisional Data

■ Weekly Trade Volume

13

23 24 26 23 23 26 27 25 25 26 26 27

14 14 15 14 14

14 14 13 12

13 14 13

17 19 19

19 17 19 19

20 20 21 22 22

55 57 60

56 54 59 60 58 57

60 62 61

0

20,000

40,000

60,000

80,000

Transpacific Asia-Europe Intra Asia

(Unit : 1,000 TEU/WK)

*

80

90

100

Transpacific Asia-Europe Intra Asia

*

(Unit : percentage)

Wet Bulk Division

■ World Scale(WS)

3. Divisional Data

World Scale(WS) has rallied sharply by strong seasonal demand.

3.5%

4.7%

3.5%

5.2%

2.7%

4.5%

2012 2013 2014

Supply Demand

■ Supply & Demand Growth

(Source : Drewry) (Source: Clarksons – BDTI TD3 : 260,000mt, Middle East Gulf to Japan)

14

60.25

0

20

40

60

80

100

120

Mar

-10

Jun

-10

Sep

-10

De

c-1

0

Mar

-11

Jun

-11

Sep

-11

De

c-1

1

Mar

-12

Jun

-12

Sep

-12

De

c-1

2

Mar

-13

Jun

-13

Sep

-13

De

c-1

3

Wet Bulk Division

3. Divisional Data

(Source: HMM inside data)

■ Wet Bulk Revenue Mix ■ Spot Exposure

COA 59.8%

Charter-out 4.6%

SPOT 35.6%

(Based on 4Q 2013 Wet Bulk Revenue)

KRW 183 Bn

15

48%

HMM has secured long term contract for stable earnings as bearish market continues with oversupply of vessels.

HMM is finding opportunities to increase crude oil tankers to take best advantage of the trough of industrial cycle.

48% 48% 47%

12% 12% 13%

37% 37% 38%

4% 4% 2%

FY2011 FY2012 FY2013

Crude Tanker Product Tanker LNG LPG

0

50

100

150

200

0

25

50

75

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Fixed Revenue Exposure(L) WS(R)

Wet Bulk Division

(Source: HMM inside data, Clarksons)

* Delivery includes Owned and Chartered Vessels

HMM’s VLCCs are cost competitive as they were set to be delivered ahead of the hike of new building price.

Based on accurate and extensive market forecasts, HMM has well balanced the ratio of spot and fixed revenues in

crude oil tanker service.

3. Divisional Data

2 2 2 3

5

3 4

0

5

10

0

50

100

150

200

Vessel Delivery(R) VLCC New Building Price(L)

■ VLCC Delivery vs. New Building Price ■ Historical Fixed Revenue vs. World Scale

($ million) (Percentage)

16

Dry Bulk Division

■ BDI

3. Divisional Data

Bearish market continued during the year, but the market seems to be gradually improving next year.

After sharp rally in capesize market due to increasing Brazil iron ore export in the 3Q, the market shows upward trend

while in volatile condition.

■ Supply & Demand Growth

10.3%

7.8%

6.6% 6.5%

9.3% 8.5%

2012 2013 2014

Supply Demand

17

(Source : MSI) (Source: Baltic Exchange)

1,752

2,277

0

1,000

2,000

3,000

4,000

5,000

Mar

-10

Jun

-10

Sep

-10

De

c-1

0

Mar

-11

Jun

-11

Sep

-11

De

c-1

1

Mar

-12

Jun

-12

Sep

-12

De

c-1

2

Mar

-13

Jun

-13

Sep

-13

De

c-1

3

Dry Bulk Division

3. Divisional Data

(Source: HMM inside Data)

■ Dry Bulk Revenue mix ■ Spot Exposure

COA/CVC 31.5%

Charter-out 23.1%

SPOT 45.4% KRW 246 Bn

18

HMM will continue to try long-term freight contracts for stable income flow.

HMM has been focusing on reforming cost structure for the longer-term perspective.

(Based on 4Q 2013 Dry Bulk Revenue)

23% 22% 24%

50% 50% 46%

17% 17% 18%

11% 12% 12%

FY2011 FY2012 FY2013

Dedicated Service Tramper Bulk Liner Heavy Lift

Table of Contents

1. Company Overview

2. Performance Review

3. Divisional Data

4. Financial Data

4.1 Non Consolidated

4.2 Consolidated

5. Appendix

Summary Financial Statements - Non consolidated

Category FY2012 FY2013 Category FY2012 FY2013

Total assets 7,908,884 6,854,879 Sales Revenue 7,713,825 6,908,325

Current assets 2,136,915 1,765,697 Cost of sales 8,064,005 7,096,331

(Cash and cash equivalents) 624,894 614,139 Gross profit -350,180 -188,006

Non-current assets 5,771,969 5,089,182 Operating Income -519,778 -351,392

Total liabilities 7,029,206 6,396,954 Profit before tax -987,590 -591,813

Current liabilities 1,854,801 3,773,266 Profit (Loss) -998,938 -585,881

Non-current liabilities 5,174,405 2,623,688

Total equity 879,678 457,925

Total equity and liabilities 7,908,884 6,854,879

(Unit: KRW million)

■ Statement of Financial Position ■ Statement of Comprehensive Income

Category FY2012 FY2013

Debt to Equity Ratio 799.1% 1396.9%

Net Debt to Equity Ratio 633.0% 1088.8%

Dividends FY2012 FY2013

Common Stock N/A N/A

4. Financial Data

(Unit: KRW million)

20

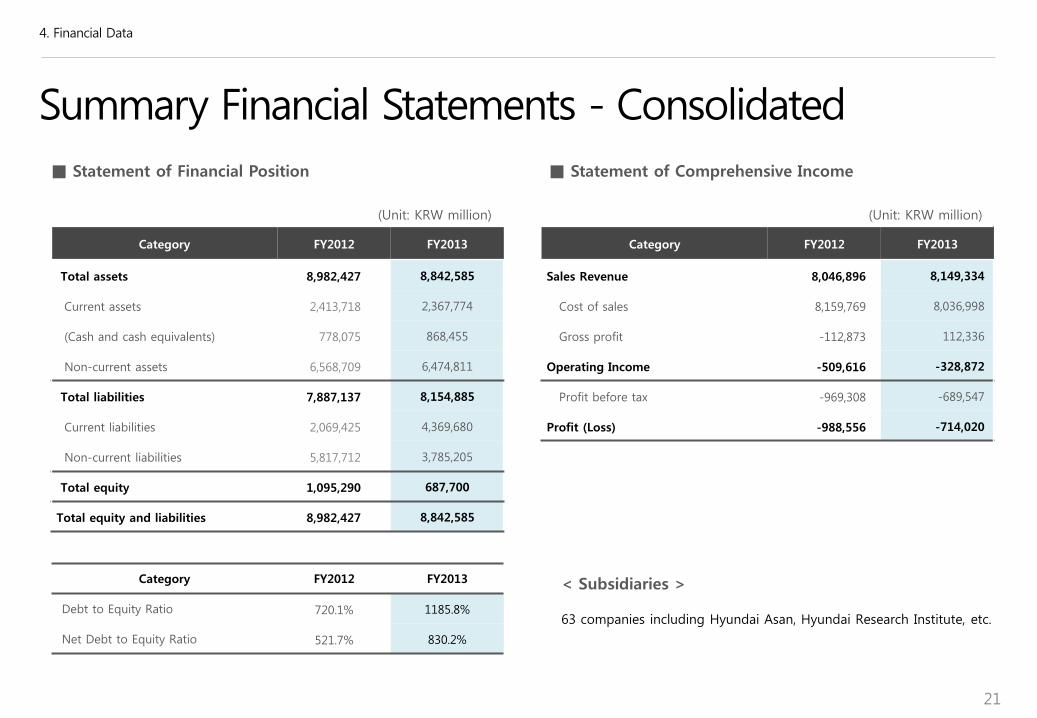

Summary Financial Statements - Consolidated

Category FY2012 FY2013 Category FY2012 FY2013

Total assets 8,982,427 8,842,585 Sales Revenue 8,046,896 8,149,334

Current assets 2,413,718 2,367,774 Cost of sales 8,159,769 8,036,998

(Cash and cash equivalents) 778,075 868,455 Gross profit -112,873 112,336

Non-current assets 6,568,709 6,474,811 Operating Income -509,616 -328,872

Total liabilities 7,887,137 8,154,885 Profit before tax -969,308 -689,547

Current liabilities 2,069,425 4,369,680 Profit (Loss) -988,556 -714,020

Non-current liabilities 5,817,712 3,785,205

Total equity 1,095,290 687,700

Total equity and liabilities 8,982,427 8,842,585

■ Statement of Financial Position ■ Statement of Comprehensive Income

Category FY2012 FY2013

Debt to Equity Ratio 720.1% 1185.8%

Net Debt to Equity Ratio 521.7% 830.2%

63 companies including Hyundai Asan, Hyundai Research Institute, etc.

< Subsidiaries >

(Unit: KRW million) (Unit: KRW million)

4. Financial Data

21

Table of Contents

1. Company Overview

2. Performance Review

3. Divisional Data

4. Financial Data

5. Appendix

5.1 Shareholder Structure

5.2 Global Networks

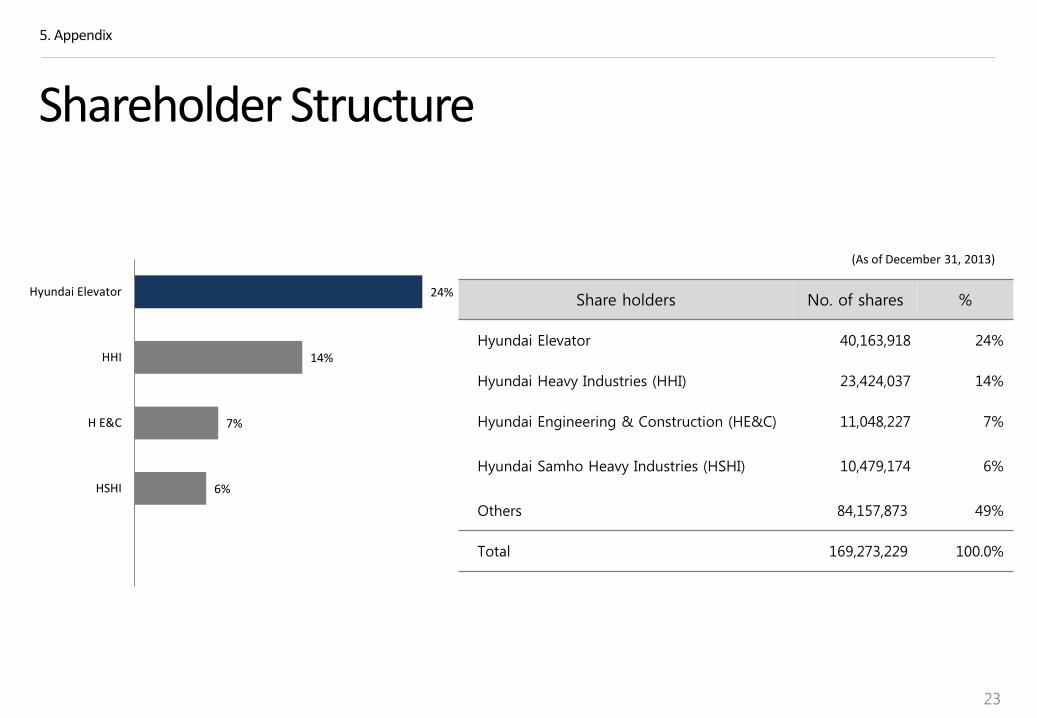

Shareholder Structure

5. Appendix

(As of December 31, 2013)

23

Share holders No. of shares %

Hyundai Elevator 40,163,918 24%

Hyundai Heavy Industries (HHI) 23,424,037 14%

Hyundai Engineering & Construction (HE&C) 11,048,227 7%

Hyundai Samho Heavy Industries (HSHI) 10,479,174 6%

Others 84,157,873 49%

Total 169,273,229 100.0%

24%

14%

7%

6%

Hyundai Elevator

HHI

H E&C

HSHI

5. Appendix

Global Networks

Hamburg

Le Harve

Gothenburg

London

Genoa

St. Petersburg

Vienna

Hong Kong Dubai Mumbai Bangkok

Singapore Klang

Ho Chi Minh

Kaohsiung

Taipei

Shanghai Tokyo

Sydney

Long Beach

Tacoma

Irving

Antwerp

Rotterdam HMM HQ

HMM CHINA

HMM America

HMM Europe

HMM South East/West Asia

Seoul

Operating Terminals

HMM HQ

Regional HQ

Operating Terminals Location Capacity /year Owned Share Remark

CUT California 1,200,000 TEU 100%

WUT Washington 1,100,000 TEU 100%

KHT Kaohsiung 800,000 TEU 100%

HPNT Busan 2,000,000 TEU 50%

RWG Rotterdam 4,000,000 TEU 20% to be opened in 2014

4 Regional HQ, 26 Subsidiaries, 74 Branches, 3 Liaison Offices, 5 Operating Terminals

24

Sau Paulo

(Others are subsidiaries)

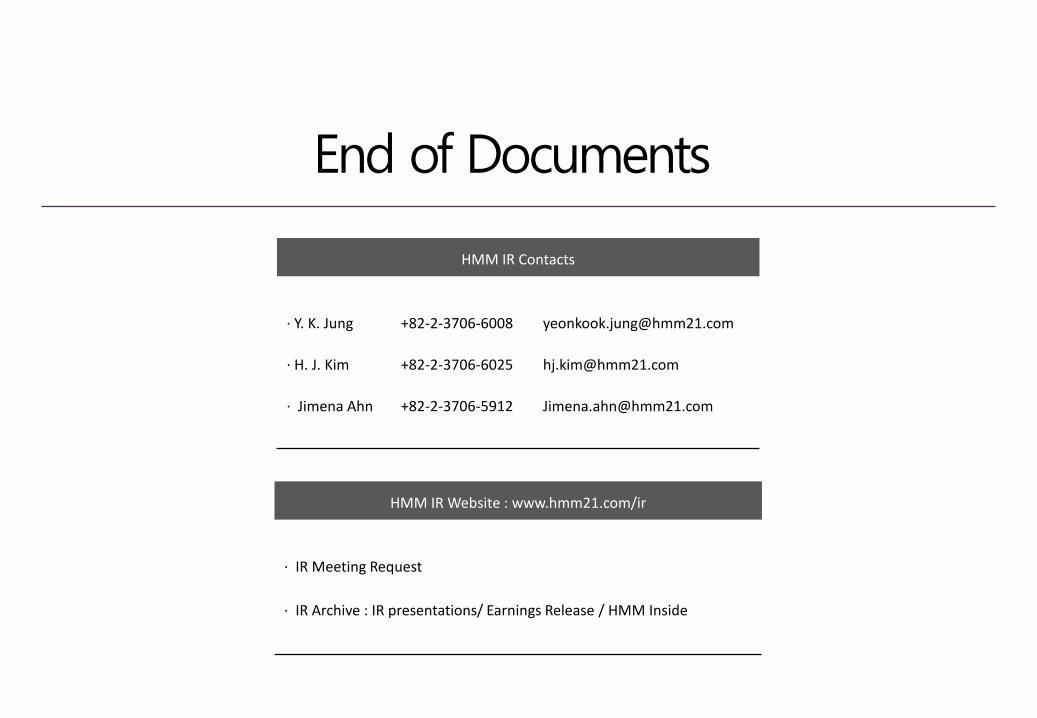

End of Documents

HMM IR Contacts

∙ Y. K. Jung +82-2-3706-6008 [email protected]

∙ H. J. Kim +82-2-3706-6025 [email protected]

∙ Jimena Ahn +82-2-3706-5912 [email protected]

HMM IR Website : www.hmm21.com/ir

∙ IR Meeting Request

∙ IR Archive : IR presentations/ Earnings Release / HMM Inside