Embed Size (px)

Citation preview

ICOrating

Inchain Project Review (http://ico.inchain.io/)

ICO dates (26.10.2016 – 23.11.2016)

Web: icorating.com Email: [email protected] Twitter: @IcoRating

Overview of Contents 1. PROJECT DESCRIPTION 4

Features of Inchain’s Platform 4

2. BUSINESS MODEL 6 Introduction 6 Inchain 6 Risk Assessment Model 7 Model for formation of the insurance premiums cost 9 The insurance fund formation model 9

Investing on the part of the insurance fund 11 DAO Project Management Structure 12 Development plans 13 Conclusion 14

3. THE TECHNICAL ASPECTS OF THE PLATFORM 16 Insurance 17 Notes 18 GitHub 19

ICO 19 Inchain bounty campaigns 19 Escrow 20

4. TEAM 21 Proof of developer 21 Experience 21

Founders 21 Tech 21 PR 22 Business advisors 23 elCoin 23 Conclusion 24

Activity 24

5. LEGAL 25 Risk of legal prosecution 25 Guarantees to investors 25 Legal team 25

6. SOCIAL MEDIA 26 Feedback 26

The Crypto-community 26

1

Marketing 26 Media 26 Announcement 27

Bitcointalk 27 Website 27

7. SUMMARIES 28 Advantages: 28 Disadvantages: 28 Rating assessment 29

Rationale 29

2

1. PROJECT DESCRIPTION

Inchain is a project that insures investors against loss risks from crypto-shares, caused by security breaches on exchanges and e-wallets (at first it works only with Bitcoin and Ethereum). At launch, the service, according to its founders, will give users insurance from hacking exclusively occurring on exchanges or crypto-shares storage platforms, with the nature of the hack not important. Inchain does not insure against the hacking and theft of user accounts and/or passwords. Insurance will be valid for one year. The process is implemented by a p2p (peer-to-peer) insurance model. In other words, to cover the amount of insurance for damages to each insured individual (either a natural or legal person that insures their values) bonds are issued. These bonds then are sold on the market and anyone can purchase them. Thus coverage for the damages in case of an insured event is carried out at the expense of investors who buy bonds and receive a coupon income. This coupon income is generated from premiums for the insurance and investment activities alongside a portion of the insurance fund. The fund is formed within the limits of the insurance company, and at the expense of insurance premiums used for insurance claims purposes).

Features of Inchain’s Platform

The Platform’s founders highlight the following: - All operations are carried out solely in cryptocurrency; - An Inchain insurance policy is a smart contract; - For each insurance statement, Inchain releases insurance bonds for for which an investor receives will receive a coupon and at the same time, accepts the insurance risks. In other words, i.e., if an insurance claim is made, the investor can not get a coupon, or even lose a part of their investment in bonds, depending on how many insurance payments were carried out for the reporting period and in what amount; - Inchain is managed by a DAO. As such, all key decisions are in the hands of the owners of Inchain tokens: this entails investment management of insurance funds and the distribution of income from investments, updating the platform, smart contracts etc.

3

2. BUSINESS MODEL

Introduction

Inchain’s founders took the concept of their project from the traditional insurance business model. At the same time, they added an element of p2p (peer-to-peer, a decentralized or peer network), which allows them to raise money to reimburse insurance claims from third-party investors, rather than organize their own insurance fund. This concept, which is trending in Fintech today, looks very logical and effective. The same method was used by other online lending tech platforms like Lending Club, Prosper, Ondeck, Funding Circle and others. If you look at Fintech’s trends, we see that young innovative players have already entered almost all the spheres of the traditional economy (banking, lending, brokerage, consulting), except for insurance. Most experts agree that this is due to the industry’s high level of regulation and high financial requirements for companies who want to enter this market. The main aspect in question, besides the strict requirements for this sector on the part of the regulators, is the high social importance of insurance, designed to maintain a level of welfare for the population. It’s not surprising that in the cryptocurrency industry we see new players emerging in the insurance sector. It’s also worth noting the clear need for such services in the cryptocurrency industry, which is characterized by high levels of instability and frequent hacker attacks on crypto-services.

Inchain

We have seen the creation of the crypto-insurance service, whose developers provide an entire infrastructure for customers and investors. They also plan to give platform management to the electoral DAO Committee.

4

In a traditional insurance business, a major role is played by mathematical models regarding the risk assessment of insured objects, including investment models of the part of the insurance reserve for getting additional profits. A for-profit commercial insurance business consists of insurance premiums paid by the Insured to transfer their risks to a third party, and investment activities. This is intended to increase the reserve fund capital. The main item of expenditure are insurance payments as a result of an insurance claim. In other words, it’s vital for the insurance company to know the rate of occurrence of certain events in the area in which they operate. For example, if the company is engaged in car insurance, it must know all the statistics on hijackings of particular brands and model, and based on such data, cars are ranked according to their risk of theft level. In accordance with this information, the size of insurance premiums change accordingly and are given a strictly defined part of an insurance company’s portfolio. Part of the insurance reserves, which the company will invest in various assets, is always strictly regulated. The volume of insurance reserves directly affects the performance of the insurance company's financial stability, as well as its ability to fulfill its obligations to customers. This is why investments from traditional insurance businesses are carried out with the most secure assets, most often: bonds from the corporate and municipal sectors, shares from the most reliable companies that are traded on world stock exchanges. In that particular case, shares constitute a relatively small part of the insurance reserves’ investment, due to their speculative nature and high volatility rate. Above, we described, in general terms, the main points on which an insurance business is based. Now let’s look at how all this is implemented in Inchain’s case.

Risk Assessment Model

Inchain is a project that insures against the risk of loss of crypto-shares resulting from exchange and e-wallet breaches. In this case, it’s logical that the object of insurance is a cryptocurrency (ex. Bitcoin, ethereum) within the user’s account. Therefore, the service should have a full risk assessment model for the platforms, to whose users they plan to provide insurance services.

5

We have not found a description of the risk assessment model, so we asked this question in a personal letter to the founders of the project: ICOrating’s question: "Is the risk assessment model ready?" Inchain’s answer: "No. The model will be developed after the ICO." Attempting to clarify at least the outline of the parameters of this model, we received a response similar one of the founders gave on the Russian-speaking branch of Bitcointalk’s forum: "Whether the site was hacked in the past; whether there were losses due to hacking and what’s the amount; how long is the service presented on the market; Does it use two factor authentication; Does it multisignature; Is the company officially registered, etc." At the same time, there is an item in their Whitepaper which states that Inchain offers different templates for smart contracts which are designed for the most common insurance claims: duration, risks, bonuses and so on. We asked the following question: ICOrating’s question: "What kind of templates have been developed and what kind of new templates do you plan to create and when?". Inchain’s answer: "At the moment there is no designed templates. All development according to the Roadmap will begin after the ICO. For each insured risk there will be a insurance policy pattern. This includes a smart contract template for bond management for different risks, oracle template(s) and so on." The financial model, which is officially represented by the developers to illustrate that their platform is stable in financial matters, and that all platforms have the same weight in the portfolio - 8.33%. Logically this indicates that all areas have absolutely the same level of risk. Although this is impossible by definition. We asked a few questions on this: ICOrating’s question: "In your financial model, interest for all platforms is distributed in equal shares - 8.33%. We understand that you equate all of them to the same level of risk?"

6

Inchain’s answer: "No. This is the percentage of the share of the risk for the each service, the risks of which are insured, made in the structure of Inchain insurance bonds. In other words, the insurance bond includes, in equal shares, risks for each service, the accounts of which are insured. " ICOrating’s question: "Are you planning to launch with the same proportions, or will there be an analysis of the areas according to their risk level, and will there be some amendments made based on that?" Inchain’s answer: "There be an analysis. All of the potential services to be rated by the insurance risk, and the high-risk ones will not be insured. Each of the insured services will have its own risk rating. The higher the risk, the more expensive the insurance, and vice versa." At the same time, we learned that so far there is no risk assessment model, it will be created later. This raises a legitimate question: why build a financial modeling to demonstrate the stress resistance of a project on what are obviously unrealistic figures? As a result, we can say that, at the moment, there is no model to assess the risk level of the platforms, whose users the service plans to insure. According to the team, they will begin to develop it after the ICO.

Model for formation of the insurance premiums cost

There is no information about an insurance premiums formation model at present. At the same time, on the forums and in the financial model, the founders provide the 3% figure, which would prevail as an average premium. Regarding the question about the model of the insurance premiums calculation we got the following answer from the founders: this model has not been developed so far. It is not clear why it is precisely 3% used in the financial model currently presented to the community.

The insurance fund formation model

The risks of the policyholder will be covered by issued bonds (the principle of these bonds is borrowed from a catastrophe bond), which will be issued and sold in the market for the sum that is equivalent to an insurance payment. Thus, insurance risks are passed on to investors, the purchasers of bonds.

7

Annotation: A catastrophe bond (CAT) is a high-yield debt instrument that is usually insurance-linked and meant to raise money in case of a catastrophe such as a hurricane or earthquake. It has a special condition that states if the issuer, such as the insurance or reinsurance company, suffers a loss from a particular predefined catastrophe, then its obligation to pay interest and/or repay the principal is either deferred or completely forgiven. - Investopedia Bond turnover will be carried out on Inchain’s trading platform. The coupon yield will be paid onto them. According to the founders’ concept, the bond includes a pool of the entire insurance portfolio, rather than a separate platform. This minimizes the risk of bonds holders should a hacker attack one platform and cause significant losses. Thus, risks are, even in nature and in the case of bankruptcy of one platform, investors do not lose their entire investment, but only part of it according to the proportional distribution of platforms’ shares in the insurance portfolio. In the calculations of the financial plan and in the discussion on bitcointalk.com the team declares the return on the bond insurance at a level of about 10% per year. The insurance bond’s profitability will be formed at the cost of the insurance premiums and the investment part of the insurance fund. There is no answer anywhere in official sources regarding this next question: where did the 10% figure came from, except in response to a poll for the community about what numbers would be the most comfortable for them. So, we asked the founders: ICOrating’s question: "Where did the 10% figure came from, just the poll? Based on what parameters were the evaluations carried out? What was taken into account? Is there a formula?" Inchain’s answer: "The figures are taken from a survey and from assessments by expert business advisors and team members. Also, they come from an analysis of similar products in real insurance." We did not see any specifics in that response. From what we can conclude, this figure was created without a real assessment of the project’s capacity to generate income, which carries serious risks for the entire business model.

8

Investing on the part of the insurance fund Managing the investment part of the insurance fund is a key aspect of the insurance company’s operations. In this type of environment, investment structure is very important. It will allow the company to generate profits while minimizing risks for the fund because they directly affect the company's financial position and ability to fulfill service obligations. As a rule, the investment portfolio of insurance companies is managed very conservatively, as mentioned above. Inchain did not release any official information on this subject. Again we asked for clarification from the founders: ICOrating’s question: "The figure of 10% rate of return on bonds is mentioned in your financial plan. You write the following "In addition, we expect that the average cost of insurance will be around 3% ", i.e, the profitability is above three percent you expect to receive from investments. If we keep in mind that those investments should be reliable, where you are planning to invest the insurance fund? What are the options? Do they exist?" Inchain’s answer: "The development of the investment strategy is not an easy task. To solve it, we asked business advisors. The initial strategy will be offered by the developers. After that, the Inchain DAO can change it. Right now we consider cryptocurrency trading and investing in new projects as investment possibilities. We’ll be more specific after the advisors finish their work after the ICO." ICOrating’s question: "Do you not think that cryptocurrency trading is a too risky an option for investing your insurance fund? What do you mean by "new projects?" Inchain’s answer: "I personally do, but as I wrote, the development of the investment strategy is not my strong point, so we'll attract and engage business consultants. New projects here means crypto economy-based projects" ICOrating’s question: "Why do you expect that insurance will be an average of around 3%? What is your insurance premiums matrix? Why 3%?" Inchain’s answer: "The figures are taken from polls and assessments by expert business advisors and team members."

9

In addition, the right balance between the number of insurance contracts and bonds actually sold is very important. This protects the insurance fund that covers the insurance liabilities. Therefore, there can be a situation when there will be significantly more insurance liabilities than sold bonds, which should protect them. Or vice versa, the demand for bonds will grow faster than the inflow of new customers for insurance. In order to understand the details of the calculation of these financial nuances described, we turned to the founders: ICOrating’s question: "What are the limits of a balance between the necessary insurance sum in the fund and the amount of bonds sold? At what point will this imbalance affect you?" Inchain’s answer: "Since the insurance model is not developed yet, I can not answer your question." It’s worth noting that according to the developers, they’re planning to use about 80% of the insurance fund for investment purposes. This is a very significant figure, and without a clearly defined investment strategy, even partial loss of this capital can greatly undermine the financial sustainability of the project.

DAO Project Management Structure

According to the founders’ idea, the project should be developed further under the control of an elected committee: 5-20 people that are voted on by all DAO participants. The DAO’s functions: 1) The investment strategy of the insurance fund; 2) Distribution of investment returns including paying dividends to Inchain token holders; 3) Selecting the Insurance Committee; 4) Selecting the Investment Committee; 5) Updating Smart contracts; 6) Confirmation of an insurance claim; 7) Insurance fund management (transfers from one account to another for example); 8) Management of oracles - smart contracts; 9) Managing the parameters of the insurance / investment model; 10) Managing the rating model;

10

There is no information on how exactly the process of insurance and selecting the investment committee will be held.

At the same time the DAO Committee will make the final decision about the insurance payments. The very purpose of the Insurance Committee is to ensure that, when negotiating key decisions on insurance cases, there won’t be a requirement to hold a vote among all the DAO’s members since it is too slow and expensive; voting should be limited only to the Insurance Committee. Smart contracts (Oracles) must monitor insurance claims, and the insurance committee approves the amount of compensation transfer. The mechanism of insurance claims monitoring by the Oracles is also described in very general terms, without specific details.

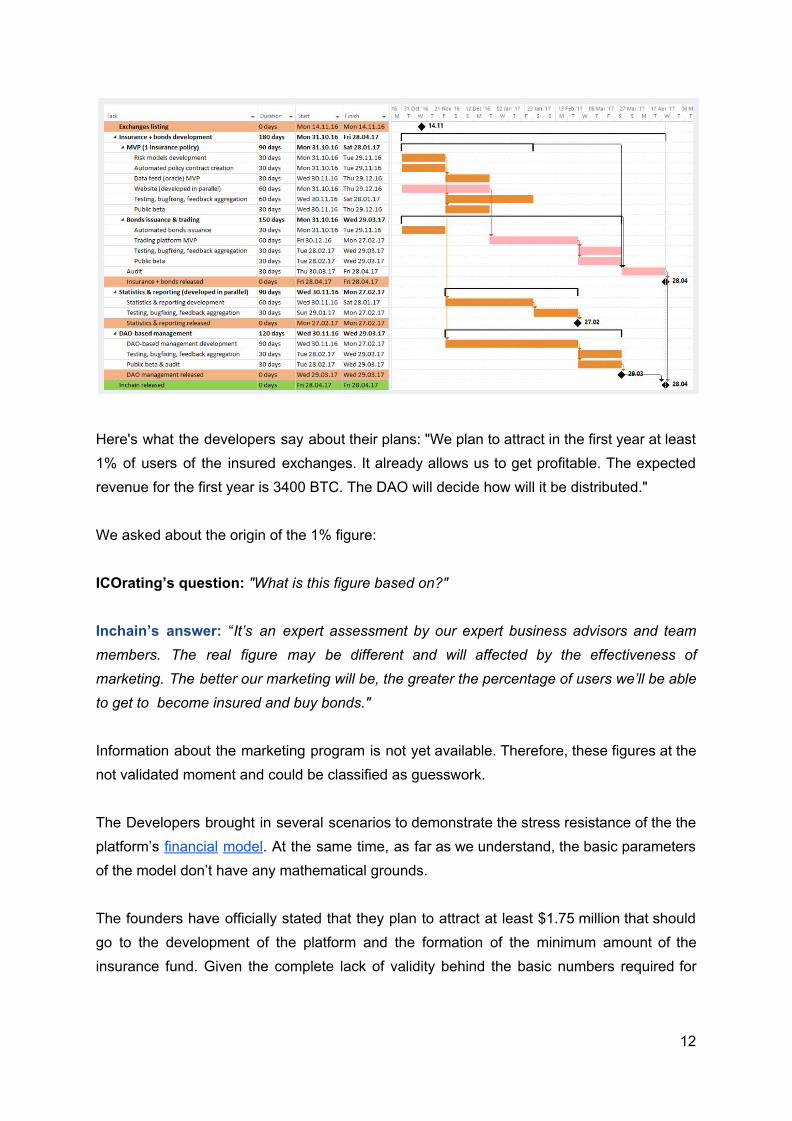

Development plans

The project’s roadmap is limited to only a few platform launch details, which is scheduled for the end of April 2017. There is no specific information on the next steps of the service. The founders of the platform on the forums mention only their plans to work with European exchanges and web wallets to expand the number of platforms on which insurance will be offered to users, but without any specific steps.

11

Here's what the developers say about their plans: "We plan to attract in the first year at least 1% of users of the insured exchanges. It already allows us to get profitable. The expected revenue for the first year is 3400 BTC. The DAO will decide how will it be distributed." We asked about the origin of the 1% figure: ICOrating’s question: "What is this figure based on?" Inchain’s answer: “It’s an expert assessment by our expert business advisors and team members. The real figure may be different and will affected by the effectiveness of marketing. The better our marketing will be, the greater the percentage of users we’ll be able to get to become insured and buy bonds." Information about the marketing program is not yet available. Therefore, these figures at the not validated moment and could be classified as guesswork. The Developers brought in several scenarios to demonstrate the stress resistance of the the platform’s financial model. At the same time, as far as we understand, the basic parameters of the model don’t have any mathematical grounds. The founders have officially stated that they plan to attract at least $1.75 million that should go to the development of the platform and the formation of the minimum amount of the insurance fund. Given the complete lack of validity behind the basic numbers required for

12

understanding the development of the insurance project, we have asked the following question to the developers: ICOrating’s question: "How was the cost of the minimally required insurance fund calculated, based on what formula and what data?" Inchain’s answer: "I won’t tell you the formula. It’s an expert assessment by our expert business advisors and team members."

Conclusion

A lack of grounded mathematical and statistical models to confirm the potential profitability of the project poses serious risks for investors. The founders developed a theoretical aspect of the project’s launch by taking the basic principles of an insurance business. An entire insurance business is based solely on mathematical and statistical models that accurately control the stability of the business and its ability to fulfill obligations. For Inchain, such calculations will only be created after collecting funds, which looks unprofessional on the part of the project's management team. Like trying to drive a car when all you have is a frame, a seat, and no motor: very difficult.

13

3. THE TECHNICAL ASPECTS OF THE PLATFORM

Inchain is a decentralised insurance platform based on Ethereum smart contracts. Inchain tokens are a type of DAO token which does allow you to take some ownership and control of Inchain. Token holders will be eligible to receive dividends, vote and take part in Inchain’s management. Developers started with Ethereum because they know it works. But, as they already discussed with Sasha Ivanov from Waves, a platform’s concept can be realised on others blockchains as well. However, most of them still do not have enough tools to realise Inchain’s concept. They have also some suggestions from the ETC community to realise Inchain, based on Ethereum classic. The most important features of Inchain are:

● Decentralisation and Ethereum smart contracts ● Decentralised insurance to mitigate crypto-economy risks ● Insurance-based bonds (tokens) as investment instruments ● DAO-like principles for managing investment portfolios their approach

Ethereum smart contracts are accountable for:

● Insurance policies and premiums ● Managing insurance-based bonds ● Maintaining a balance in the interests of stakeholders

14

● Monitoring insurance claims through specific oracles ● Coupon repayment ● Insurance claim payouts

Having a DAO as an investment management vehicle lines up with the decentralised nature of the blockchain. This approach provides both transparency and full control over Insurance funds by Inchain token holders. Of course, insurance terms such as duration and risks may vary and the smart contracts would be adjustable for different cases. Inchain proposes offering different templates for smart contracts designed for the most widespread cases. The templates will also be open sourced and their number will increase. The policyholder receives an Ethereum smart contract, which contains all the terms and conditions of the policy. In order to define coupon rates, every bond will be ranked. Inchain develops an adjustable risk-scoring system for wallets and exchanges.

Insurance

A client decides to obtain an insurance policy to mitigate his risks. He registers an account with Inchain, He provides the characteristics he desires in the policy, such as coverage duration, amount and the exchange’s name. Based on this data and the ranking model, the platform creates an offer for client. Once he accepts the offer, the platform generates an Ethereum smart contract. Because the contract is visible to client, he can check the code. The contract is activating by the receipt of payment for the insurance policy. The insurance premium transfers to the insurance fund. For now, the developers’ plan does not check the address and balance of insured before insure them. This is because registration of BTC/ETH addresses and balances is not an easy task. Imagine you hold some BTC in Coinbase. Do you know what address they have exactly? And if you are a trader, your balance can change very often so it can be very different at the end of the insurance policy from when you insure it. Every contract is integrated with its own oracle—a specific smart contract-based application— that monitors whether the insured risks have materialised. Every oracle automatically notifies associated smart contracts if it identifies the occurrence of an insurance claim. An Oracle is a smart contract that contains information about the state of “external reality” (e.g. non-blockchain events). Oracle contract associate with some trusted party, by delegating private key to that party (can be several participants for backup purposes). It's

15

more similar to how SSL certificates work: as soon as the originator of the data have announced his public key, anyone can verify the validity of the submitted data. In this case, the contract initiates a transfer from the insurance fund to the contract’s address, which then makes a transfer to the policyholder and deactivates itself when the processes are complete. Once the trader has obtained the insurance policy as described above, Inchain issues bonds linked to the policy. The bonds have specific coupon rates, face values, ratings and durations. The bonds become available at the trading section immediately after issuing. The face value of the bonds are paid:

● To the policyholder if the risks have materialised. Smart contract initiates a payment out of the insurance fund. Investors holding bonds linked to such insurance policies cease to receive coupons immediately after the case happens that carries risk of losing their investments.

● To the investor if the bonds are expired. Investors receive all coupon payments and the bond’s face value.

Such an insurance system has a few drawbacks. For example hacker/exchange (or anyone aware of the hack before announcement) could easily drain all of Inchain's capital:

1. They know about hack before anyone else does 2. They buy Inchain insurance 3. A breach is announced to the public 4. They get paid the compensation from insurance

The developers promise to take a number of measures to mitigate such risks:

● Every exchange has a total limit of the risks insured ● The policy will be a time lag between the issuance of the policy and the date the

coverage starts ● Use some KYC service to stop insurance spamming (It is a good tool to prevent

some types of fraud. But, it also may scare a lot of crypto-economy members who care about their anonymity. Therefore KYC is a discussion in progress)

● Restrict max insured balance to minimize a potential damage if some of the policies are abused

● Stop issuing insurance policies after the first minimal signal about a hack is received Developers intend to rate every exchange and depends on their risk rating they can or can not be insured by Inchain. This info will be public. Some criteria for rating:

16

● How long the service is operational ● If it was compromised previously ● Security audit results ● Multi-Sig & Hot Wallets/ 2Factor

Notes

The Developers will make the platform only after the ICO. There are other criticisms on the quality of implementing development ideas that are not possible, stemming from the inability to determine the team’s level of professionalism. Theoretically it has claimed broad functionality, but this isn’t technically supported by anything.

GitHub

The Developers are working on deploying the code to github. Today you can only find a few samples of smart contracts (ICO). Technical documentation: White Paper Ambisafe will participate in the development of smart contracts for the platform.

ICO The ICO will last for 4 weeks. The start was set for 12 October, but was eventually postponed to 26 October. The developers commented on this via Bitcointalk: “The situation with Ethereum is very poor. We are waiting when the problems with ddos & next hardfork will be resolved. We need this stability to launch.” On October 25 the developers published a new statement: “Our ICO is postponed for 24 hours, which is October 27 2016 00:00 GMT. We know that many of you have been waiting a long time to start investing. We apologize for any inconvenience this may cause. The delays have occurred due to a legal entity registration and appointments of new escrows, who will be responsible for investments made in ETH. The BTC escrows remain unchanged.”

Some information about ICO below.

17

Inchain bounty campaigns FB & Twitter Translation Signature

On using the investment fund: - firstly, developers pay for development and each investment part will be released by escrow after we achieve next milestone.

18

- development cost is about $850-950 K - all remaining funds after development will be directed to the Inchain insurance fund under escrow control The Developers plan to list the Inchain token on some exchanges directly after the ICO ends. One fact: https://www.livecoin.net/en/news/view/186

Escrow Inchain has two forms of escrow:

BTC Escrow: ● TwinWinNer Paul Klanschek is the Founder/CEO of Austrian Coinimal GmbH, a

Bitcoin company that is focused on providing the most convenient conversion from fiat money to digital currency and vice-versa. In this role, he is responsible for all major areas: operations, strategy, finance, compliance, sales, marketing

● SebastianJu is an escrow for the Bitcointalk community since May 2013, and a

member since June 2011. He has already escrowed more than 8150 BTC since may 2013.

ETH Escrow (added 25 october) “We are proud to announce the ETH escrows. We have partnered with Johann Barbie and Daniel Nagy. They are well known Ethereum experts. This allows us to ensure that escrow contracts are handled and reviewed by the best security experts.”

● Johann Barbie - CEO of http://www.ocolin.com/ and http://www.cosign.io/ One of the first bitcoin evangelists. Founder of 37coins, the world’s first SMS bitcoin wallet (now defunct). Johann has participated in multiple innovative Ethereum projects including Provenance, Chronicled and Ambisafe.

● Daniel Nagy is one of Ethereum’s core developers, currently working on the Geth

node Swarm system.

19

4. TEAM

Proof of developer

The team is not anonymous and active on few social media channels.

Experience

All the information is given according to the description of the official website and team members’ LinkedIn profiles.

Founders

Dmitry Lazarichev (LinkedIn) ● He founded Wirex (ex E-Coin) - personal finance platform that works with the

blockchain tech and traditional finance. According to the Inchain website, it has almost 200K accounts. Also co-founded biomass supplier Peltrade Ltd.

● He also has an extensive experience in finance, working as a managing partner in Solid Finance House and in the company valuation, working as a Head of Valuation Department at IFC Solid and Senior Consultant at Regional Agency of Business Valuation

Has business experience. Has blockchain experience. Sergey Primatchik (LinkedIn)

● Worked as CIO at LLC Registratura.ru, Information systems development manager at OJSC VimpelCom and as a Project manager for elCoin, a crypto-currency project

● According the the official website, he’s “actively involved in blockchain technology since 2015” and “has participated as a consultant in several blockchain based projects”.

Has technical and business experience. No recorded blockchain experience apart from the elCoin project.

Tech

Andrey Zamovskiy (LinkedIn) - Blockchain architect ● He has worked as a software engineer and project manager in various companies

(RussianDesigners, TechnoPark, Krendls LTD, DIMALEX, Matvil Corp, Skykillers and oDesk). According to his linkedin he was involved in the Tether project.

20

● He was a founder and CTO at NoveltyLab, where he was involved in crypto-projects HolyTransaction, Bitmerch and BTC dealer (the latter two are now defunct)

● Currently Andrey is a founder at Ambisafe - a blockchain technology company that specializes in blockchain-based shared ledgers for financial instruments. Ambisafe has been chosen as a platform for Inchain. He’s also a Chief Blockchain Evangelist at Propy Inc. - company that allows users to look for the information on available apartments and houses for sale.

He has a technical background and blockchain experience. Oleksii Matiiasevych (LinkedIn) - Smart contracts engineer

● According to the CV posted on his LinkedIn profile he has an experience in blockchain technologies, Ethereum and smart contracts.

● Has a extensive experience in Quality Assurance, having worked as a QA Automation Lead, QA Engineer and QA Specialist.

● At the moment he’s an Engineering Project Manager at Ambisafe. According to the official Inchain website “during his engagement with Ambisafe, he has developed five DAOlike tokens with the most advanced features you can find on these kinds of contracts.”

● According to the interview with the founders of Inchain he was involved in the development of the Bitfinex exchange, which is confirmed by his CV.

He has a technical background and blockchain experience. Aleksei Shakhov (LinkedIn) - Frontend developer.

● According to the official Inchain website “ He has 7+ years experience in professional web development and has spent more than three years designing full stack applications.” There is no information on his LinkedIn about any other projects except for Inchain.

He has no recorded blockchain experience.

PR

Richard Kastelein (LinkedIn) - PR /marketing partner ● He is a director at media company Agora Media Ltd, an external assessor at Innovate

UK and an expert at the European Commission, where he gives advice on companies looking for EU funding.

● He’s also a founder of The Hackitarians and Blockchain News, where he’s also a publisher and editor in chief.

He has media and blockchain experience.

21

Business advisors

Martin Galas (LinkedIn) ● Leads the Finance team for Chubb Insurance in Germany & Austria. Previously he

worked as an Analyst in the Financial Planning & Analysis team and Head of Financial Planning & Analysis in Zurich Insurance Group and AIG.

He has experience in insurance. Serge Umansky (LinkedIn)

● He’s a Co-founder of the Signet Group - an independent investment solutions provider. Also, according to the official Inchain website “he is a Head of portfolio management at Whiteridge Investment Funds and a co-founder of the Signet Research & Advisory SA based in Lausanne, Switzerland. He has served as a Managing Director at Morgan Creek Capital (Europe) and has been a principal of ICG Consulting LLC in Washington DC.”

He has business experience.

elCoin

According to the comments of some Bitcointalk users, key members of the Inchain team participated in the creation and development of the elCoin project:

● Sergey Primachik - elCoin Project Manager ● Andrew Zamovsky - founder and CEO of Ambisafe, company that was involved in the

development of elCoin wallet, as stated in the white-paper. ● Dmitry Lazarichev is a founder of Wirex Limited, which worked on a joint card project

for deposit/withdrawal of fiat through debit, real and virtual Visa cards. elCoin is a part of Elephant project and is connected to the Elevrus, considered by many to be a fraudulent pyramid scheme, in which almost all participants lost their money. According to the comments of Sergey Primachik, he agreed to participate in the project, attracted by the possibility to create big infrastructure platform for the crypto-economy with different crypto-services. After the first Elephant's product, elCoin, was launched, project owners decided to use elCoin as debt obligations to its investors, however, these obligations have not been fulfilled. According to his comments, he was a contract employee and had no stake in the project.

22

He also mentioned that neither Wirex nor Dmitry Lazarichev never had any relations with elCoin, however the fact of cooperation between Elephant and Wirex is confirmed in the elCoin blog.

Conclusion Both founders have blockchain experience. Tech team has strong technical background and blockchain experience (however confirmed by CV for only ⅔). 2 of tech specialists have recorded blockchain experience. Head of PR has experience in both media and blockchain industry. However, core part of the team was involved in a development of a pyramid scheme. That doesn’t mean that they necessarily had criminal intentions, and Sergey Primatchik presented his take on the story, according to which they didn’t. But his statement about the involvement of Wirex and Dmitry Lazarichev into the project turned out to no match the facts.

Activity

The team (apparently mostly Sergey Primatchik) is active on Slack, Facebook, and Bitcointalk, answering most users’ questions. We were able to talk to Inchain’s founders over email and they give answers to our questions. The team gave two interviews to ForkLog and Cryptosource. They also had a Q&A over Google Hangouts at 10.10.2016. The fragment of the video was uploaded on YouTube, but the video is unlisted and currently has only 36 views. They also have an active blog on Medium. There is no information about the team participating in a any big crypto-events and conferences or meetups.

23

5. LEGAL

According to the developers, the ICO was postponed because team is working out the legal questions.

Apparently, the company is not registered at the moment. Founders don’t yet know if it will be registered before or after the ICO.

Risk of legal prosecution According to the founders, they “presume that blockchain-economy is not regulated”, therefore they don’t have any special permissions to provide the insurance service even though “they are working on legal challenges in order to protect themselves and investors from regulation much as possible”. It should me mentioned that insurance business is in some way regulated by the government in most of the countries, although there was no precedent in the blockchain industry.

Guarantees to investors The only guarantee to that the investors will receive their tokens and that the project will continue to develop according to the roadmap is that all funds are in the escrow.

Legal team According to the founders, they work with Adam Vaziri, director of DIACLE, company that provides licensing and compliance support to fintech operators including blockchain start ups. They’re also establishing contact with lawyers from the United States and Russia, but they didn’t provide us with any names.

24

6. SOCIAL MEDIA

Feedback

The Crypto-community

The project has received considerable attention on bitcointalk.org, getting 837 replies throughout 27 days (Oct, 18 2016). It also have few threads in other languages, including French, Russian and Filipino. There is a lot of neutral questions and positive feedback, however, a significant part of comments (especially in the Russian thread) is made up of concerns about the business model and ties of developers with the Elephant project. The Inchain team answers most of these complaints. Inchain didn’t receive any noticeable attention from the influencers in fintech and blockchain industry (apart from those who are involved in the project).

Marketing

Richard Kastelein is in charge of Inchain marketing. Inchain plans to spend 1 million INC (1% of the total amount) on bounty campaign that includes promotion over Facebook and Twitter, Bitcointalk and translation. They’re also using the crowd-speaking platform, Thunderclap, to spread a message about the company. The site uses an "all-or-nothing" model, in that if the campaign does not meet its desired number of supporters in the given time frame, the organizer receives none of the donations, so it’s not known yet if this is going to promote Inchain.

Media

The company has a social media presence on a few social platforms ● Facebook ● Twitter ● Medium

25

Community. The Crypto-Community does not have a majority opinion at the moment: users on Bitcointalk are expressing polarizing views. Media attention. Inchain has received attention from a few crypto and financial media outlets such as ForkLog, Coremedia, All Insurance, CoinFox, Bitroad, CoinCheck, Viral Alert and CryptoCoin Home.

Announcement

Bitcointalk

● Account Type - Member ● Not Self-Moderated Announcement Thread

Website ● Has a detailed website. ● There is a whitepaper and a roadmap. ● There is a financial plan, although it is rather generic and not detailed at the moment.

26

7. SUMMARIES

Advantages:

● Given the high risks of crypto-market due to lack of regulatory and supervisory institutions, insurance sphere can be in high demand among users to reduce the risks of loss of crypto-actives.

● The absence of competition among blockchain projects creates a large market advantage for the first player that comes into this market.

● Due to the nature of frauds in the insurance industry, which is not always noticeable by algorithms, the fact that the final decision on the payment of insurance sums is made by the DAO Committee, and not smart contracts, looks sensible.

● Escrow with reliable signees. ● Most members of the team have noticeable blockchain experience.

Disadvantages:

● Project founders are starting to raise funds for the development of the project with only a theoretical, abstract model, with no real justification and modeling of their plans (model of platforms risk assessment, payment of insurance premiums, payment of return on bonds, the insurance fund investment).

● Rationale of the business model stress resistance is based on the unsubstantiated figures.

● The lack of a plan for the period after the ICO. ● An uninformative Whitepaper. ● Almost a complete lack of code on GitHub except for a few examples of smart

contracts. ● The core part of the team was involved in the development of a pyramid scheme. ● The company has no registration, no permissions to provide the insurance service

and doesn’t present any guarantees to the investors apart from the escrow. ● Lack of a demo or prototype of the service.

27

Rating assessment

Our evaluation for Inchain is “Risky”. If the company will do the following, we may assign a higher rating for the project:

● Present mathematical and statistical models, which will illustrate the model of platforms risk assessment, the formation of insurance premiums, the insurance fund investment plan, the returns on the bonds;

● Disclose more technical aspects (code, smart contracts); ● Release a demo or prototype of the service.

Rationale As a result, the idea of creating an insurance platform for the crypto-currency industry, which at the moment is basically the Wild West, an industry without regulation and control, is interesting and promising. If we consider that today there is no similar service, the first player with proper implementation could become really successful. At the same time, the fact that the founders of the project start to to raise funds for the development of the project with only a theoretical, abstract model, with no real justification and modeling of their plans is rather worrying. The lack of evidence for managing the business model’s stress resistance is also a negative factor. Another disadvantage is the lack of a Roadmap. On the one hand, this can be attributed to the DAO format of the model management platform, but still, a lack of strategic vision for the development of the project complicates matters. In any business model, the most important element is not the general business idea, but the way it’s implemented and how this is justified. This is especially important for financial sectors such as insurance, where the main success factors are determined by clear statistical models. In this case, they don’t not exist at all. Also, Inchain’s model is hardly decentralized. Blockchain-based smart contracts control all the key processes typical for the insurance business, but the final decision about the insurance claim is made by the DAO Committee.

28

People often try to cheat insurance companies for insurance payments, and often do it in very sophisticated ways, so it probably would be wrong to trust decision-making on insurance payments to the algorithms only. The fact that a final decision regarding insurance payments is made by the DAO Committee looks sensible, although, this spoils the concept of decentralization somewhat. Large gaps in the technical backgrounds of the project do not allow us to estimate the quality of the project’s implementation.

The information contained in the document is for informational purposes only. The views expressed in this document are solely personal stance of the ICOrating team, based on data from open access and information that developers provided to the team through Skype, email or other means of communication. Our goal is to increase the transparency and reliability of the young ICO market and to minimize the risk of fraud. We appreciate feedback with constructive comments, suggestions and ideas on how to make the analysis more comprehensive and informative.

29