Embed Size (px)

Citation preview

i Company No. 256516-W I 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS

AND KEY MANAGEMENT

8.1 Promoters and substantial shareholders

8.1.1 Shareholdings

Sindora

Dato' Hak

Datin Hamidah

Kulim

Other substantial shareholder

• JCorp

The direct and indirect interest of our Promoters and substantial shareholders in our Company before our IPO and after our IPO is set out below:-

Malaysia

Malaysian

Malaysian

Malaysia

Malaysia

Notes:-

255,000 65.4 - 255,000 50.6

96,000 24.6 (1)39,000 10.0 90,900 18.0 (1)29,100 5.8

39,000 10.0 (2)96.000 24.6 29,100 5.8 (2)90,900 18.0

- (3)255,000 65.4 - (3)255,000 50.6

- (4)255,000 65.4 - (4)255,000 50.6

(1) Deemed interested by virtue of his spouse's shareholdings in our Company pursuant to Section 6A of the Act.

(2) Deemed Interested by virtue of her spouse's shareholdings in our Company pursuant to Section 6A of the Act.

(3) Deemed interested by virtue of its interest in Sindora pursuant to Section 6A of the Act. (4) Deemed interested by virtue of its interest In Kulim pursuant to Section 6A of the Act.

Save as disclosed above, our Directors are not aware of any person who. directly or indirectly, jointly or severally, exercises control over our Company.

8.1.2 Profiles of Promoters

Kulim, Sindora, Dato' Hak and Datin Hamidah are the Promoters as well as the substantial shareholders of our Company.

Kulim was incorporated as a private limited company in Malaysia under the Act on 3 July 1975 as Kulim (Malaysia) Sdn Bhd and converted to a public company as Kulim (Malaysia) Berhad on 18 August 1975. Kulim was listed on the Main Board of Bursa Securities (presently known as Main Market of Bursa Securities) on 14 November 1975.

Kulim is principally engaged in oil palm plantation, investment holdings and property investment. The principal activities of its subsidiaries consist mainly of oil palm planting, crude palm oil processing, plantation management services and consultancy, sea transportation. sales of wood based products, as well as property investment.

150

r.nnnn~'''I\1 No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

As at the LPO, the authorised share capital of Kulim is RM500,000,000 comprising 2,000,000,000 ordinary shares of RMO.25 each. The issued and paid-up share capital of Kulim as at the LPO is approximately RM323,642,408 comprising 1,294,569,631 ordinary shares of RMO.25 each ("Kulim Share(s)") excluding 15,322,000 Kulim Shares which are held as treasury shares. As at the LPO, there are 124,153,940 of warrants ("Warrant(s)") and 54,106,250 employees' share option scheme options ("ESOS Option(s)") that have yet to be exercised into Kulim Shares.

The directors of Kulim and their respective holdings in Kulim Shares, Warrants and ESOS Option as at the LPO are set out below:-

Dato' Kamaruzzaman bin Malaysian - I - I - I - I - I - I - I - 1 1,000 I 1.85 Abu Kassim (M)

Ahamad bin Mohamad (M) Malaysian 963 0.08 500 0.92

Wong Seng Lee (M) Malaysian 301 0.02 56 0.05 200 0.37

Abdul Rahman bin Malaysian 250 0.46 Sulaiman (M)

Jamaludin bin Md Ali (M) Malaysian 50 (5) 200 0.37

Rozan bin Mohd Sa'at (M) Malaysian 9 (5) (6) (5) 150 0.28

Datin Paduka Siti Sa'diah Malaysian 278 0.02 35 0.03 150 0.28 binti Sheikh Bakir (F

Zulkifli bin Ibrahim (M) Malaysian

2,47; I 0.1~ I {4J4.90; I 0.3~ I ~ I ~ I (4)25~ I 0.2~ I 150 I 0.28

Tan Sri Dato' Seri Utama Malaysian 150 0.28 Arshad bin Ayub

Datuk Haron bin Siraj (M) Malaysian

~ I ~ I ~ I ~ I ~ I ~ I ~ I ~ I 150 I 0.28

Dr. Radzuan bin A. Malaysian 150 0.28 Rahman (M)

Kok Keong (M) Malaysian - I - I - I - I - I - I - I - I 150 I 0.28

151

I Company No. 256516-\1\111

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cant'd)

Notes:-

(1) Based on 1,279,247,631 Kulim Shares in issue, which does not include 15,322,000 treasury shares held by Kulim as at the LPD. (2) Based on 124,153,940 outstanding Wa"ants as at the LPD. (3) Based on 54,106,250 outstanding ESOS Options as at the LPD. (4) Deemed interested through his interest in Zalaraz Sdn Bhd pursuant to Section 6A of the Act. (5) Negligible (6) Represents 100 units ofWa"ants.

The substantial shareholders of Kulim and their respective shareholdings and warrantholdings in Kulim as at the LPD are set out below:-

JCorp

Kumpulan Wang Persaraan (Diperbadankan)

Notes:-

Malaysia

Malaysia

679,785 I 53.14 I (3)94,563 I 7.39 15,176 I 12.22 107,330 8.39

(1) Based on 1,279,247,631 Kulim Shares in issue, which does not include 15,322,000 treasury shares held by Kulim as at the LPD. (2) Basedon 124, 153,940 outstanding Wa"ants as at the LPD.

(4)50,332 I 40.54

(3) Deemed interest through its interests in JCorp Capital Solutions Sdn Bhd (formerly known as Jedcon Engineering Survey Sdn Bhd), Johor Ventures Sdn Bhd, Intrapreneur Development Sdn Bhd, Tenaga Utama (J) Berhad and Waqaf An-Nur Corporation Berhad pursuant to Section 6A of the Act.

(4) Deemed interest through its interests in JCorp Capital Solutions Sdn Bhd (formerly known as Jedcon Engineering Survey Sdn Bhd), Johor Ventures Sdn Bhd, Tenaga Utama (J) Berhad and Waqaf An-Nur Corporation Berhad pursuant to Section 6A of the Act.

THE REST OF THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK

152

I Company No. 256516-W I 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS

AND KEY MANAGEMENT ,P_._.' .... ,

Sindora was incorporated as a public company in Malaysia under the Act on 30 December 1972. Sindora commenced its business operations in 1974 and was subsequently listed on the Main Board of Bursa Securities (presently known as the Main Market of Bursa Securities) on 7 December 1995. The entire issued and paid-up share capital of Sindora was removed from the Official List of Bursa Securities on 30 November 2011 following the completion of the take-over offer made by Kulim. The notice of the take-over was served on 16 August 2011 and wholly satisfied in cash. Kulim had at the close of acceptances received acceptances of more than 90.0% of the offer shares not held by Kulim and persons acting in concert, and had invoked compulsory acquisition proceedings to successfully complete the privatisation of Sindora. Sindora is principally involved in intrapreneur ventures business and operation of oil palm plantations, palm oil milling and rubber estate.

As at the LPD, Sindora has an authorised share capital of RM200,OOO,OOO comprising 200,000,000 ordinary shares of RM1.00 each, of which RM96,OOO,000 comprising 96,000,000 ordinary shares of RM1.00 each have been issued and fully paid-up.

As at the LPD, the Directors of Sindora are Ahamad bin Mohamad, Abdul Rahman bin Sulaiman, Jamaludin bin Md Ali and Nasharuddin bin Shukor. As at the LPD, Sindora is a wholly-owned subsidiary of Kulim.

Dato' Hak, a Malaysian aged 60, is our Managing Director. He was appointed to our Board on 1 February 2002. He is responsible for the day-tO-day operations and business activities of our Group.

He graduated with a Bachelor of Science in Marine Engineering from Merchant Marine Academy, Jakarta in 1976. He also holds a Master of Science in Project Engineering from the University of Lancaster, United Kingdom, a Diploma in Ship Survey from Det Norske Veritas, Oslo, Norway, and the Certificate of Competency as a Foreign Going Marine Engineer. He is currently registered as a Professional Engineer with the Board of Engineers, Malaysia. He began his career as a marine engineer onboard ocean going vessels owned by Malaysian International Shipping Corporation Sdn Bhd in 1976 prior to becoming a project manager with Malaysian Fisheries Development Authority in 1981. I n mid of 1981, he worked as a mill engineer at Sime Darby Plantation Berhad for approximately two (2) years and later became the project engineer at Bank Pembangunan Malaysia Berhad in mid-1983 until end of 1983. Subsequent to his departure, he joined Det Norske Veritas (Singapore) Pte Ltd as a ship and engineering surveyor. His job scope involved surveying ships in service/in operation, surveying ships under construction, surveying of offshore structures under construction, approval of ship designs, conducting trainings to newly recruited Ship and Engineering Surveyors, and giving feedback/contributing to the development of "Det Norske Veritas' Steel Ship Rules". During his tenure with Det Norske Veritas (Singapore) Pte Ltd, he was posted to various countries and was subsequently promoted to be a principal surveyor in 1990. In the same year, he also became the managing director of Det Norske Veritas Sdn Bhd, of which he held the position until 2002.

153

Company No. 25

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Confd)

In 2002, he joined our Company as the Managing Director, focusing on our Company's business strategy and has overseen the growth of our Company from chartering of vessels from third party owners to vessel owning and also shipbuilding. Currently, he is actively involved in the local maritime fraternity and holds many positions in various shipping related non-governmental organisations. He was formerly the President of Institut Kelautan Malaysia (IKMAL). Presently, he is the Vice Chairman of Malaysian Shipowners Association (MASA), Member of Australia Asia Committee for Bureau Veritas, Member for Nippon Kaiji Kyokai Malaysia Committee, and Chancellor of Ranaco Education and Training Institute (RETI) Terengganu. He is also the industry advisor to University Kuala Lumpur, Malaysian Institute of Marine Engineering Technology (UNIKL MIMET) and University Technology Malaysia (UTM) for maritime studies. Since 2010, he has been part of the Malaysian delegation at International Maritime Organisation (iMO),s Marine Environment Protection Committee (MEPC) meetings in London.

Datin Hamidah, a Malaysian aged 53, is our Promoter and substantial shareholder. She graduated with a Certificate of Accounting from Goon College, Kuala Lumpur in 1979. She began her career as an accounts clerk in Hilton Hotel, Kuala Lumpur. A year later, she joined the Malaysian Fisheries Development Authority (LKIM) as an assistant auditor until 1983. After she resigned in 1983, she became a housewife until 1993, when she established EA Technique with the initial business of cargo braking. Later on in 1995, with the assistance of Ir. Zulklifi Mohd Amin, they ventured into new businesses such as marine consultancy services and ship chartering. During her tenure in our Company, she managed all the financial aspects of our Company on a day-to-day basis. She retired in 2007 but currently holds substantial shares in our Company.

8.1.3 Profile of other substantial shareholder

The profile of our other substantial shareholder apart from Kulim, Sindora, Dato' Hak and Datin Hamidah is as follows:-

JCorp was incorporated under the Johor Corporation Enactment No. 4 of 1968 (as amended by Enactment No. 5 of 1995). JCorp is principally engaged in palm oil business, property development and management and investment holding. The principal activities of the JCorp Group consist mainly of palm oil business, healthcare services, property development and management, intrapreneur ventures, quick service restaurants and investment holding.

As at the LPD, the Directors of JCorp are Dato' Seri Mohamed Khaled bin Nordin, Tan Sri Or Ali bin Hamsa, Dato' Kamaruzzaman bin Abu Kassim, Dato' Haji Ismail bin Karim, Data' Ishak bin Sahari, Tuan Ha]i Marsan bin Kassim, Tuan Haji Md Jais bin Haji Sarday, Dato' Hafsah binti Hashim. Data' Siti Zauyah binti Mohd Desa and Encik Izaddeen bin Daud.

154

ompany No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Confd)

8.1.4 Changes in shareholdings

The table below sets forth our Promoters' and sUbstantial shareholders' direct and indirect interests in our Company for the past three financial years up to the LPD:-

Shareholdings in our Company as at 31 December 2011 Shareholdings in our Company as at 31 December 2012 Promoters Direct Indirect Direct Indirect Direct Indirect Direct Indirect and No. of No. of No. of No. of substantial No. of No. of RCCP RCCP No. of No. of RCCP RCCP shareholders Shares ~Io Shares ~Io Shares % Shares % Shares #% Shares #% Shares % Shares %

('000) ('000) ('000) ('000) ('000) ('000) ('000) ('000)

Sindara 22,461 51.0 6,578 73.1 22,461 51.0 6,578 73.1

Data' Hak 14,974 34.0 (1)6,606 15.0 1,679 18.7 (1) 741 8.2 14,974 34.0 (1)6,606 15.0 1,679 18.7 (1) 741 8.2

Datin 6,606 15.0 (2)14,974 34.0 741 8.2 (2) 1,679 18.7 6,606 15.0 (2)14,974 34.0 741 8.2 (2) 1,679 18.7 Hamidah

Kulim (3)22,461 51.0 (3) 6,578 73.1 (3)22,461 51.0 - (3) 6,578 73.1

Other substantial shareholder

JCarp (4)22,461 51.0 (4) 6,578 73.1 (4)22,461 51.0 - (4) 6,578 73.1

155

Company No. 256516

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Promoters and substantial shareholders

Sindora

Dato' Hak

Datin Hamidah

Kulim

Other substantial shareholder

JCorp

Shareholdingsin our Company as at 31 December 2013 Shareholdings in our Company as at the LPD Direct Indirect Direct Indirect Direct Indirect Direct Indirect

No. of No. of No. of No. of No. of No. of RCCP RCCP No. of No. of RCCP RCCP

Shares % Shares % Shares % Shares % Shares (1)% Shares (1)% Shares % Shares % ('000) ('000) ('000) ('000) ('000) ('000) ('000) ('000)

198,900 51.0 255,000 65.4

132,600 34.0 (1)58,500 15.0 96,000 24.6 (1) 39,000 10.0

58,500 15.0 (2)132,600 34.0 39,000 10.0 (2)96,000 24.6

(3)198,900 51.0 (3)255,000 65.4

(4)198,900 51.0 (4)255,000 65.4

Notes:# Ordinary shares of RM1.00 each in our Company. Prior to a share split involving the subdivision of evel}' one (1) existing ordinary share of RM1.00 each held our

Company into four (4) Shares which was completed on 30 December 2013. (1) (2) (3) (4) (5)

Deemed interested by virtue of his spouse's shareholdings in our Company pursuant to Section 6A of the Act. Deemed interested by virtue of her spouse's shareholdings in our Company pursuant to Section 6A of the Act. Deemed interested by virtue of its interest in Sindora pursuant to Section 6A of the Act. Deemed interested by virtue of its interest in Kulim pursuant to Section 6A of the Act. On 30 December 2013, all outstanding RCCP Shares had been converted to Shares.

156

ompany No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

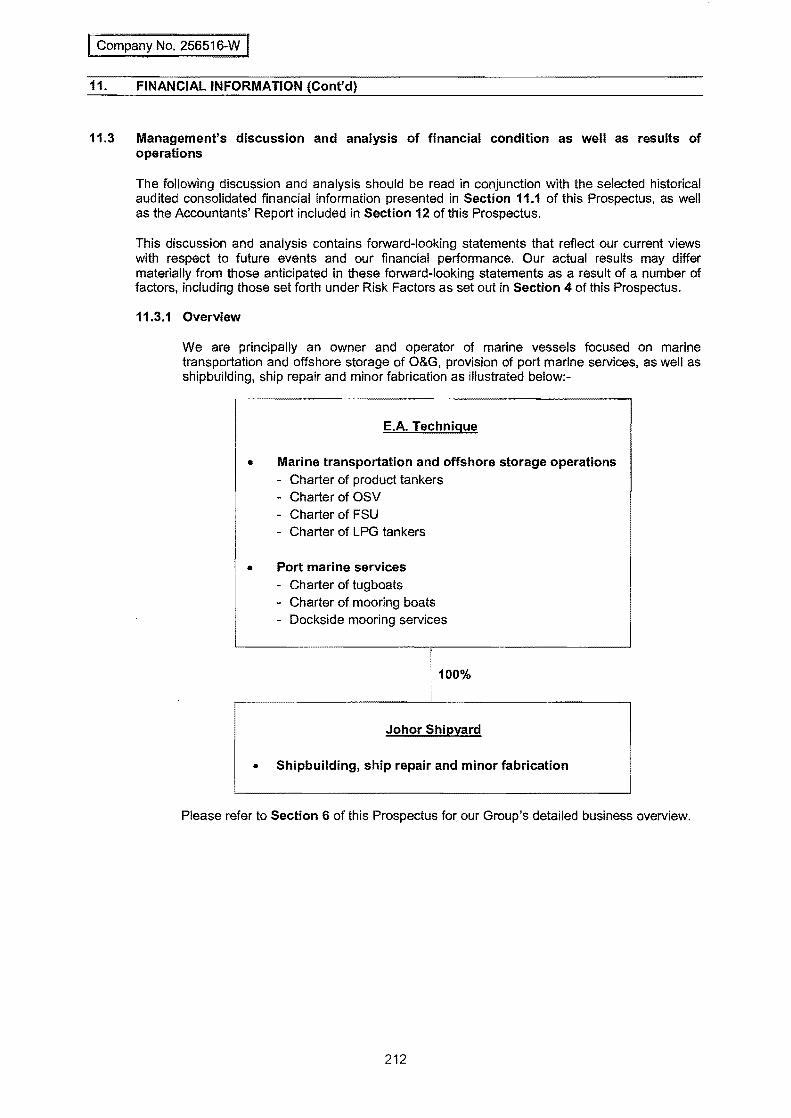

8.2 Directors

8.2.1 Shareholdings

The following table sets forth the direct and indirect shareholdings of each of our Directors before and after the IPO, assuming our Directors will subscribe for their respective pink form allocation as set out in Section 3.4.1 (iii) of this Prospectus:-

Before IPO After IPO Direct Indirect Direct Indirect No. of No. of No. of No. of

Shares Shares Shares Shares Director Designation Nationality ('000) % ('000) % ('000) % ('000) %

Ahamad bin Mohamad Non-Independent Non- Malaysian 500 0.1 Executive Chairman

Dato' Hak Managing Director Malaysian 96,000 24.6 (1)39,000 10.0 90,900 18.0 (1)29,100 5.8

Rozan bin Mohd Sa'at Non-Independent Non- Malaysian 328 0.1 Executive Director

Azli bin Mohamed Non-Independent Non- Malaysian 328 0.1 Executive Director

Datuk Anuar bin Ahmad Senior Independent Non- Malaysian 328 0.1 Executive Director

Datuk Mohd Nasir bin AIi Independent Non-Executive Malaysian 328 0.1 Director

Md Tamyes bin Hj A.Rahim Independent Non-Executive Malaysian 328 0.1 Director

Abdul Azmin bin Abdul Halim Independent Non-Executive Malaysian 328 0.1 Director

Note:

(1) Deemed interested by virtue of his spouse's shareholding in our Company pursuant to Section 6A of the Act.

Notwithstanding the pink form allocation reserved for our Directors, our Directors may subscribe for the Issue Shares under the Public Offer.

157

pany No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT

8.2.2 Profiles of Directors

Save for the profile of Dato' Hak which is set out in Section 8.1.2 of this Prospectus, the profiles of our other Directors are as follows:-

Ahamad bin Mohamad, a Malaysian aged 60, is our Non-Independent NonExecutive Chairman. He was appointed to our Board on 12 October 2009. He is also the Chairman of our Nomination and Remuneration Committee.

He graduated in 1976 with a Bachelor of Economics (Honours) degree from the University of Malaya. He joined JCorp in June 1979 as a company secretary for various companies within the JCorp Group. He was involved in many of JCorp's projects, among others, the Johor Specialist Hospital and the Kotaraya Complex in Johor Bahru. Presently, he is the managing director of Kulim which he held this position since 30 June 1994 and is also a member of the board of directors of KPJ Healthcare Berhad and New Britain Palm Oil Limited (Papua New Guinea). He is also the chairman and director of several other companies within the JCorp Group and a director of Waqaf An-Nur Corporation Berhad, an Islamic endowment institution that spearheads JCorp Group's Corporate Responsibility programmes, namely the Corporate Waqaf Concept initiated by JCorp.

Rozan bin Mohd Sa'at, a Malaysian aged 55, is our Non-Independent NonExecutive Director. He was appointed to our Board on 1 January 2007.

He graduated with a Bachelor of Economics (Honours) majoring in Statistics from Universiti Kebangsaan Malaysia in 1982. He started his career in 1983 as an administrative officer in Planning & Research Department of JCorp before being seconded as an operations manager in Sergam Berhad, a subsidiary of JCorp in 1986. From 1987 to 1988, he served in the Corporate Communications Department of JCorp as an administrative officer. From 1988 to 1993, he was appointed as the executive director of several other subsidiaries in JCorp Group. In 1994, he was appointed as the general manager of JCorp's Tourism Division before assuming the post as chief executive of the same Division on 15 June 1996, a post which he held until his appointment as the general manager, Business Development, JCorp, in early 1999. Prior to his appointment as the managing director of Sindora on 1 September 2002, he served as the senior general manager, Business Development of JCorp from 2000 until August 2002. In March 2014, he resigned as the managing director of Sindora to assume his new position as the managing director of PIJ Holdings Sdn Bhd, a subsidiary company of Johor State Government Linked Company, Perbadanan Islam Johor.

Azli bin Mohamed, a Malaysian aged 46, is our Non-Independent Non-Executive Director. He was appointed to our Board on 15 April 2014. He is a graduate of the Association of Chartered Certified Accountants, United Kingdom and also a member of the Malaysian Institute of Accountants.

He began his career as an audit assistant in PricewaterhouseCoopers in 1992 and promoted as a manager which he stayed on until 2001. He left the firm and joined KPJ Healthcare Berhad in 2001 until 2007 as the group accountant. He then served JCorp in 2007 as a general manager, Finance Division until he assumed the current position as the vice presidenUchief financial officer of Kulim since 2011. Currently, he also sits on the board of other companies within the JCorp Group and Kulim group. Given his extensive training and experience in corporate accounting and reporting practices within the JCorp Group, he has been appointed as a member of our Audit Committee.

158

Company No. 256516-

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT IC·~.~."'"

Datuk Anuar bin Ahmad, a Malaysian aged 60, is our Senior Independent NonExecutive Director. He was appointed to our Board on 15 April 2014. He is the Chairman of our Audit Committee and a member of our Remuneration Committee. He graduated in 1977 with a Bachelor of Economics (Honours) from the London School of Economics and. Political Science University of London.

He started his career in 1977 with PETRONAS. During his 36 years of service with the PETRONAS Group, he held various senior managerial and leadership positions in marketing, trading, corporate planning and human resource management until his

. retirement in April 2014 where his last position held was the executive vice president of Gas and Power Business. During his stint with PETRONAS Group, he was appointed as the managing director and chief executive officer in PETRONAS Dagangan from 1998 to 2002. He was also a member of PETRONAS Management Committee and member of PETRONAS board from 2002 to April 2014 .. He also sat· on the board of various companies within PETRONAS Group. In 1997, between his years of service with the PETRONAS Group, he underwent a three (3) months business management course under the Advanced Management Program at Harvard Business School.

Presently, he is a non-independent non-executive director of PETRONAS Dagangan· and is an ind~pendent non-executive.director of PDZ Holdings Berhad, both of which are companies listed on Bursa Securities. He also holds directorships in a few private companies.

Datuk Mohd Nasir bin Ali, a Malaysian aged 56, is our Independent Non-Executive Director. He was appointed to our Board on 17 October 2014. He graduated in 1980 with a Bachelor of Economics (Honours) degree from the University of Malaya. He also obtained a Master of Science (Finance) from the University of Strathclyde, United Kingdom in 1988.

He was with Permodalan Nasional Berhad as a senior financial and marketing analyst in 1982 prior to joining BBMB Unit Trust Management Berhad as an investment manager in 1988. He later joined Mayban Securities Sdn Bhd as a general manager of Dealing & Research Department from 1991 to 1995. Following that, he was appointed as the chief executive officer of Kuala Lumpur City Securities Sdn Bhd until

. 2000. He then became the· group executive director of Utusan Melayu(Malaysia) Berhad in 2000 until his retirement on 5 June 2014.

Presently, he is the chairman and independent non-executive director of The Nomad Group Bhd, a company listed on Bursa Securities and the chairman of ICB Islamic Bank Limited, a company listed in Bangladesh. He also holds directorships ina few private companies.

Md Tamyes bin Hj A.Rahim, a Malaysian aged 63, is our Independent NonExecutive Director. He was appOinted to our Board on 15 April 2014. He is also a member of our Remuneration and Nomination Committee. He obtained a Bachelor of Arts degree majoring in Economics in 1974 from Universiti Malaya.

He commenced his career in JCorp in 1974 and has held various positions in subsidiary companies and. divisions within the JCorp Group. He was the Senior General Manager, Human Resource Development and Administration, JCorp prior to his retirement in year 2008. Previously, he sat on the board of various companies within the JCorp Group during his tenure of service with JCorp.

159

Company No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'~d},--____ _

He was appointed as our Independent Non-Executive Director after taking into consideration his wealth of knowledge and experience in human resource and administrative related matters. He left the JCorp Group more than five (5) years ago and since then has not had any business dealings nor holds any directorship in our company or any of the companies within the JCorp Group following his retirement at the end of year 2008. He is not accustomed to act nor obliged formally or informally to act under the instructions of any other party. We conduded that his length of service in the JCorp Group previously does not interfere with the exercise of independent judgement and ability to act in the best interests of our Company. In addition, we believes that his past experience in the JCorp Group's business and his proven commitment, experience and competence will greatly benefit our Company.

Abdul Azmin bin Abdul Halim, a Malaysian aged 61, is our Independent NonExecutive Director. He was appointed to our Board on 15 April 2014. He is also a member of our Audit and Nomination Committee. He obtained a Diploma in Banking Studies from Mara Institute of Technology in 1974. He also obtained a Bachelor of SCience degree from Syracuse University, United States in 1976 and Master of Business Administration from Central Michigan University in 1978.

He commenced his career in Esso Production Malaysia Inc. in 1978 to 1981 as a management executive in the Accounts Department. In 1981, he joined Motorola Malaysia for eight (8) months as a cost accountant prior to joining PETRONAS until his retirement in 2008. During his tenure with PETRONAS, he was a management executive in 1981 to 1989 and was subsequently promoted to a manager, where he was posted to the Commercial Department at the gas processing plant in Kertih, Terengganu in 1989 to 1994 under PETRONAS Gas Sdn Bhd. He later served PETRONAS Carigali in 1994 to 2002 as senior manager in the Contracts and Procurement Department and was subsequently transferred to PETRONAS headquarters in 2002 to 2008 as senior manager in Tenders and Contracts Division being in charge of companies' tenders and overall licencing and registration.

THE REST OF THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK

160

[e;ompany No. 256516-W J

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

8.2.3 Principal business performed outside our Group

The following table sets out the principal directorships of our Directors as at the LPD and that which were held within the past five (5) years up to the LPD, and the principal business activities performed by our Directors outside of our Group as at the LPD:-

Name Companies Principal activities ~. _Date...Qf apPC!i"tment D..,.te of resignation

Involvement in business activities performed outside our Group other than director

Dato' Hak Present directorships:

Berkat Global Sdn Bhd ("Berkat,,)(l)

Notes;(1)

(2)

Marginal Reld(2)

Core Laboratories (Malaysia) Sdn Bhd

Previous directorships:

Sindora# (Kulim)

Orkim

Delmar Marine Ventures Sdn Bhd

Orkim Energy Sdn Bhd

Provides consultancy and 15 January 2002 project management services in the maritime and O&G industries Principally engaged in 12 February 2014 provision of marginal oilfield solutions, focusing on light weight platform system and FEED Analysis on the reservoir fluid, 1 March 2014 surveyor

Principally involved in intrapreneur ventures and plantations .

1 January 2008

Principally involved in provision 22 February 2009 of sea transportation and related services

Principally involved in provision 6 October 2009 of sea transportation and related services Principally involved in provision 6 October 2009 of sea transportation and related services

N/A Shareholder (direct: 90.0%)

N/A Shareholder (direct: 51.0%)

N/A Shareholder (direct: 31.0%)

16 January 2012 N/A

23 April 2013 N/A

23 April 2013 N/A

23 April 2013 N/A

There is no situation of conflict of interest that exists or is likely to exist in relation to Dato' Hak's directorship and shareholdings in Berkat as Berkat is a separate and distinct business from our Group which is run by a pool of engineers providing very speCialised engineering services comprising, amongst others, ship deSign, ship survey, third party inspection for ship construction and on hire/off hire survey services. As the nature of our business is different from Berkat, our employees does not possess the above skills (except for Dato' Hak and Ir. Zulkifli bin Mohd Amin) nor do we provide such services to our customers. We only engage Berkat as and when the need arises and such transactions moving forward will require the approval of our Audit Committee to ensure that such transactions entered between our Group and Berkat will be on arm's length basis and normal commercial terms. There is no Situation of conflict of interest that exists or is likely to exist in relation to Dato' Hak's diractorship and shareholdings in Marginal Fieid as he is merely a passive investor and is not involved in the day-ta-day activities and operations of Marginal Field. Marginal Field is managed by an experienced and well qualified management team In addition, the business of Marginal Field is relatively smaller in term of the scale of operation, revenue and asset as compared to our Group.

161

No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name

Dato' Hak

Companies

Previous directorships (Cont'd):

Principal activities

Orkim Ship Management Sdn Management company Bhd

Tanjung Langsat Port Sdn Bhd Principally involved in port operations

Date of appointment

6 October 2009

6 October 2009

Ahamad bin Mohamad Present directorships;

Kulim@

EPA Management Sdn Bhd# (Kulim)

Panquest Ventures Ltd (British Virgin Island)

Principally involved in oil palm 24 January 1991 plantation, investment holdings and property investment

Investment holding, provision 1 January 1993 of management services and conSUltancy, and mechanical equipment assembler Investment holding 28 October 1994

Pembinaan Prefab Sdn Bhd Construction 1 January 1997 19 May 1997 New Britain Palm Oil Limited Principally involved in the

(Papua New Guinea)@#(Kulim) production and sale of palm oil

Kulim Plantations (Malaysia) Sdn Bhd#(Kulim)

KPJ Healthcare Berhad ("KPJ")@

Kumpulan Bertam Plantations Berhad# (Kulim)

and palm based products

Oil palm plantation 1 January 2003

Investment holding and 1 January 2005 provision of management services to subsidiaries mainly the operation of specialist hospitals Oil palm plantation 1 January 2005

162

Date of resignation

23 April 2013

16 January 2012

N/A

N/A

N/A

NIA N/A

N/A

N/A

N/A

Involvement in business activities performed outside our Group other than director

N/A

N/A

Shareholder (direct: 0.08%)

N/A

N/A

N/A N/A

N/A

Shareholder (direct: 11)

N/A

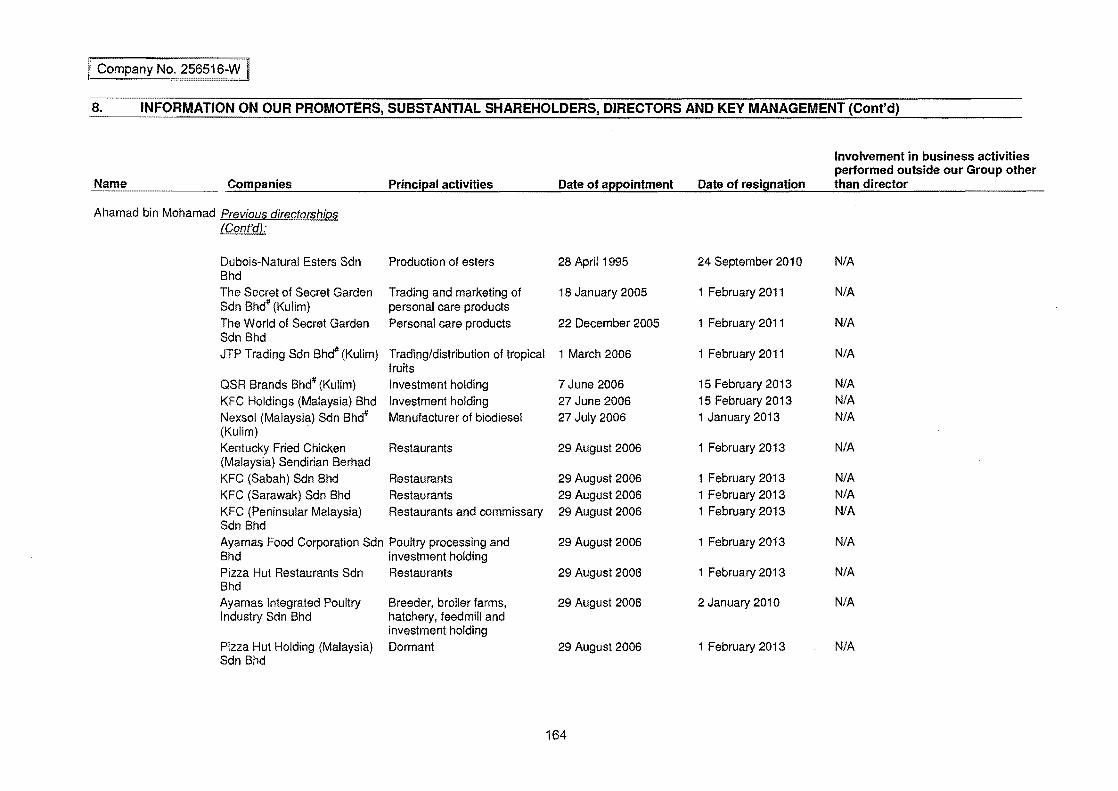

[cOrl1pany No. 256516-W I 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name Companies Principal activities Date of appointment

Ahamad bin Mohamad Present directorships (Cont'd):

Waqaf An-Nur Corporation Trustees and manager of 7 December 2005 Berhad Waqaf Kulim Energy Sdn Bhd# (Kulim) Investment holding and oil 2 August 2006

palm Mahamumi Plantations Sdn Oil palm plantation 1 February 2011 Bhd#(Kulim) Sindora# (Kulim) Principally involved in 16 January 2012

intrapreneur ventures and plantations

Rentak Alam Sdn Bhd Agriculture 1 October 2012 Kulim Topplant Sdn Bhd# Production of oil palm clones 1 January 2013 (Kulim) Yayasan Ansar Manage and administer of 3 April 2013

foundation for corporate social responsibility activities of Kulim group staff & family

QSR Brands (M) Holdings Sdn Investment holding and 1 June 2013 Bhd provision of management

services Massive Equity Sdn Bhd Investment holding 1 June 2013

Previous directorshiIl§;.

Skellerup Polymer Products Dissolved on 31 July 1995 1 January 1994 Sdn Bhd Natural Oleochemicals Sdn Production of fatty acids and 20 July 1994 Bhd glycerine hydro triglycerides

163

Date of resignation

N/A

N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A

N/A

24 September 2010

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A

N/A

N/A

No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cant'd)

Name Companies Principal activities Date of appointment Date of resignation

Ahamad bin Mohamad Previous directorships (Cont'd):

Dubois-Natural Esters Sdn Production of esters 28 April 1995 24 September 2010 Bhd The Secret of Secret Garden Trading and marketing of 18 January 2005 1 February 2011 Sdn Bhd# (Kulim) personal care products

The World of Secret Garden Personal care products 22 December 2005 1 February 2011 Sdn Bhd

JTP Trading Sdn Bhd# (Kulim) Trading/distribution of tropical 1 March 2006 1 February 2011 fruits

QSR Brands Bhd# (Kulim) Investment holding 7 June 2006 15 February 2013

KFC Holdings (Malaysia) Bhd Investment holding 27 June 2006 15 February 2013

Nexsol (Malaysia) Sdn Bhd# Manufacturer of biodiesel 27 July 2006 1 January 2013 (Kulim)

Kentucky Fried Chicken Restaurants 29 August 2006 1 February 2013 (Malaysia) Sendirian Berhad KFC (Sabah) Sdn Bhd Restaurants 29 August 2006 1 February 2013

KFC (Sarawak) Sdn Bhd Restaurants 29 August 2006 1 February 2013

KFC (Peninsular Malaysia) Restaurants and commissary 29 August 2006 1 February 2013 Sdn Bhd

Ayamas Food Corporation Sdn Poultry processing and 29 August 2006 1 February 2013 Bhd investment holding

Pizza Hut Restaurants Sdn Restaurants 29 August 2006 1 February 2013 Bhd Ayamas Integrated Poultry Breeder, broiler farms, 29 August 2006 2 January 2010 Industry Sdn Bhd hatchery, feed mill and

investment holding Pizza Hut Holding (Malaysia) Dormant 29 August 2006 1 February 2013 Sdn Bhd

164

Involvement in business activities pertormed outside our Group other than director

N/A

N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A

N/A

N/A

No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name Companies Principal activities Date of appointment

Ahamad bin Mohamad Previous directorships (Cont'd):

WQSR Holdings CS) Pte Ltd Investment holding 29 September 2006 (Singapore)

Kentucky Fried Chicken Kentucky Fried Chicken 29 September 2006 Management Pte Ltd restaurants in Singapore (Singapore)

WQSR Holdings (S) Pte Ltd Investment holding 29 September 2006 (Singapore) Kentucky Fried Chicken Kentucky Fried Chicken 29 September 2006 Management Pte Ltd restaurants in Singapore (Singapore) Pizza Hut Singapore Pte Ltd Restaurants 29 September 2006 (Singapore) Multibrand QSR Holdings Pte Investment holding 29 September 2006 Ltd (Singapore) KFC (B) Sdn Bhd (Brunei) Restaurants 1 November 2006 Renown Value Sdn Bhd# Cultivation of pineapples and 7 May 2007 (Kulim) other agricultural produce Akli Resources Sdn Bhd# Provider of in-house and 1 January 2008 (Kulim) external training programmes Cita Tani Sdn Bhd#{Kulim) Cultivation of sugar cane 15 February 2008 Kulim Civilworks Sdn Bhd# Facilities maintenance 15 February 2008 (Kulim) SIM Manufacturing Sdn Bhd# Manufacturers and dealers in 15 February 2008 (Kulim) rubber products of all kinds

and articles made from rubber Kampuchea Food Corporation Restaurants 29 February 2008 Co limited (Cambodia) Kulim livestock Sdn Bhd# Breeding and sal,as of cattle 14 August 2008 (Kulim)

165

Date of resignation

1 February 2013

1 February 2013

1 February 2013

1 February 2013

1 February 2013

1 February 2013

1 February 2013 1 February 2011

1 February 2011

1 February 2011 1 February 2011

1 February 2011

1 February 2013

1 February 2011

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A

N/A

N/A

N/A

N/A N/A

N/A

N/A N/A

NlA

N/A

N/A

No. 256516-

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name Companies Principal activities Date of aPPClintrnent .. pate of resignation

Ahamad bin Mohamad Previous directorships (Cont'd):

Special Appearance Sdn Bhd# Production house and event 19 January 2009 1 February 2011 (Kulim) management Superior Harbour Sdn Bhd# Aquaculture Operations for 19 January 2009 1 February 2011 (Kulim) food consumption JTP Montel Sdn Bhd# (Kulim) Cultivations of bananas 22 January 2009 1 February 2011

Kulim Nursery Sdn Bhd# Operator of strategic business 22 January 2009 1 February 2011

KFC India Holding Sdn Bhd Investment holding 13 May 2009 1 February 2013

Mauritius Food Corporation Investment holding 1 3 August 2009 1 February 2013 Pvt Ltd (Mauritius) DPIM Consult Sdn Bhd Operator of strategic business 1 January 2010 1 July 2011

Extreme Edge Sdn Bhd# Computer equipment supplier 1 January 2010 1 February 2011 (Kulim) and services

Akademi JCorp Sdn Bhd Operator of strategic business 14 January 2010 16 January 2012 school and corporate training programmes

Grating Solar Sdn Bhd Dormant 29 January 2010 1 February 2013

KFCIC Assets Sdn Bhd Property holding 29 January 2010 1 February 2013

KFCH Education (M) Sdn Bhd Management of 29 January 2010 1 February 2013 collegellearning institution

Exquisite Livestock Sdn Bhd Commercial cattle farming 1 February 2010 1 February 2011

Pizza (Kampuchea) Private Dormant 1 April 2010 1 February 2013 Limited KFCH Restaurants Private Restaurants 19 May 2010 11 March 2013 Limited (India) PHD Delivery Sdn Bhd Pizza delivery 9 July 2010 1 February 2013

Kulim Safety Training and Occupational Safety and 22 July 2010 1 February 2011 Services Sdn Bhd# (Kulim) Health Administration Training

and services

166

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A N/A

N/A N/A

N/A N/A

N/A

N/A N/A N/A

N/A N/A

N/A

N/A N/A

LC~rTlpany No. 256516-W i 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name Companies

Ahamad bin Mohamad Previous directorships (Cont'd):

Pinnacle Platform Sdn Bhd# (Kulim) KCW Electrical Sdn Bhd# (Kulim) KCW Kulim Marine Services Sdn Bhd# (Kulim) Perfect Synergy Trading Sdn Bhd#(Kulim) Optimum Status Sdn Bhd# (Kulim) KCW Hardware Sdn Bhd# (Kulim) Yayasan Amal Bistari Cemerlang Sinergi Sdn Bhd Orkim

Ihsan Permata Sdn Bhd

Principal activities Date of appointment

Software maintenance and 22 July 2010 supplier Electrical installation services 22 July 2010

Marine maintenance 22 July 2010

Fertiliser supplier 22 July 2010

Mill maintenance and 22 July 2010 fabrication Hardware supplier 22 July 2010

Dormant 1 September 2010 Strike off on 28 March 2014 1 February 2011 Principally involved in provision 15 May 2011 of sea transportation and related services Providing consultancy and 1 March 2012 management services for cattle breeding

Super Heritage Brand Sdn Bhd Importer and trader of poultry 7 March 2012 business and other related activities

Felda Ayamas Ventures Sdn Dormant 30 November 2012 Bhd

167

Date of resignation

1 February 2011

1 March 2011

1 February 2011

1 February 2011

1 February 2011

1 February 2011

22 March 2013 1 February 2013 23 April 2013

15 March 2014

6 April 2014

1 February 2013

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A

N/A

N/A

N/A

N/A N/A N/A

N/A

N/A

N/A

I Company N~. 256516~W ]

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name Companies Principal activities Date of appointment Date of resignation

Rozan bin Mohd Sa'at Present directorships:

Kulim@ Principally involved in oil palm 1 January 2008 plantation. investment holdings and property investmeQt

Johor Land Berhad Property management 1 January 2011 JCorp Hotels and Resort Sdn Hotel 1 February 2011 Bhd PIJ Holdings Sdn Bhd Holding company PIJ Property Development Sdn Property Bhd PIJ Plantation & Agriculture Sdn Bhd PIJ Manufacturing Sdn Bhd Isdecor Bina Sdn Bhd Pandan Baru Sdn Bhd Jismil Plantation Sdn Bhd Perisind Samudra Sdn Bhd Perisind Venture Sdn Bhd Koridor Utiliti (Johor) Sdn Bhd Isedecor Infra Sdn Bhd Sutera Samudra Sdn Bhd

Previous directorships:

Sindora# (Kulim)

Tiram Travel Sdn Bhd

Plantation

Manufacturing Construction Developer Plantation Property management Ducting provider Ducting provider Civil engineering Project management

Principally involved in intrapreneur ventures and plantations Sale of flight tickets and package for umrah, haj and tourism

15 March 2014 15 March 2014

15 March 2014

15 March 2014 15 March 2014 15 March 2014 15 March 2014 15 March 2014 15 March 2014 8 April 2014 8 April 2004 27 May 2014

1 September 2002

15 October 2003

168

NlA

NlA N/A

N/A N/A

N/A

N/A N/A N/A N/A N/A N/A N/A N/A N/A

15 March 2014

1 October 2014

Involvement in business activities performed outside our Group other than director

Shareholder (direct: A)

N/A N/A

N/A N/A

N/A

N/A N/A N/A N/A N/A N/A N/A N/A Shareholder (Direct: 50.0%)

N/A

N/A

ompany No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Involvement in business activities perfonned outside our Group other

Name Companies Principal activities Date of appointment Date of resignation than director

Rozan bin Mohd Sa'at Previous directorships (Cont'd):

Metro Parking (M) Sdn Bhd# Parking operations and the 1 July 2004 15 December 2012 N/A (Damansara Realty Berhad) provision of related

consultancy services Willis (Malaysia) Sdn Bhd Insurance brokers 12 July 2004 14 December 2009 N/A DPIM Korporat Sdn Bhd Management consultant 31 July 2004 1 July 2011 N/A Sindora limber Sdn Bhd# Timber products 1 January 2005 1 January 2011 N/A (Kulim) EPASA Shipping Agency Sdn Shipping and forwarding agent 1 April 2005 15 July 2012 N/A Bhd# (Kulim) services MM Vitaoils Sdn Bhd#{Kulim) Producer and wholesale of 1 July 2005 11 October 2011 N/A

palm oil and other edible oil and fats

Puteri Hotels Sdn Bhd Hotel operations 1 September 2005 6 April 2014 N/A Waqaf An-Nur Corporation Trustees and manager of 7 Decem ber 2005 1 October 2014 N/A Berhad waqaf GranuLab (M) Sdn Bhd# Trading granular synthetic 17 May 2007 15 July 2012 N/A (Kulim) bone graft Bistari Young Entrepreneur Producing, promoting and 22 October 2007 16 January 2012 N/A Sdn Bhd marketing Catur Bistari and

Service related Amazing Cuisine Sdn Bhd Cold-cuts and sausages 10 July 2008 16 January 2012 N/A

production KPJ@ Investment holding and 1 January 2009 1 January 2014 Shareholder (direct: 1\)

provision of management services to subsidiaries mainly the operation of specialist hospitals

169

ILC~rTl~~~Y No. 256516-W ! 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Confd)

Name Companies Principal activities Date of appointment

Rozan bin Mohd Sa'at Previous directorships (Cont'd):

EPA Management Sdn Bhd# Investment holding, provision 1 January 2009 (Kulim) of management services and

consultancy, and mechanical equipment assembler

T eraju Fokus Sdn Bhd Security services 1 January 2009

Orkim Principally involved in provision 22 June 2009 of sea transportation and related services

DPIM Consult Sdn Bhd Management consultant 1 January 2010 Akademi JCorp Sdn Bhd Operator of Strategic BUsiness 14 January 2010

School and Corporate Training Programmes

Microwell Bio Solutions Sdn Business in agriculture and 23 April 201 0 Bhd#(Kulim) natural products, water

treatment, biotechnology research and development

Microwell Trading Sdn Bhd# Trading in Biochemical 23 April 2010 (Kulim) Fertiliser Healthcare Technical Services Project management and Sdn Bhd# (Damansara Realty engineering maintenance

7 May 2010

Berhad) services JKing Sdn Bhd Producer of sports attire 20 July 2010 MIT Insurance Brokers Sdn Insurance 1 December 2010 Bhd#(Kulim)

Kumpulan Perbadanan Johor Sdn Bhd#(Kulim)

Management services 1 January 2011

Mahamurni Plantations Sdn Bhd#(Kulim)

Oil palm plantation 1 February 2011

Hotel Selesa (JB) Sdn Bhd Hotel operations 1 February 2011

Sibu Island Resorts Sdn Bhd Island resorts operator 1 February 2011

170

Date of resignation

15 March 2014

1 January 2011

23 April 2013

16 January 2012 15 July 2012

15 July 2012

15 July 2012

15 February 2011

16 January 2012 1 October 2014

1 January 2013

15 March 2014

6 April 2014 6 April 2014

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A N/A

rC~rl1pany No. 256516-W ! 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name Companies Principal activities

Rozan bin Mohd Sa'at Previous directorships (Cant 'd):

Tanjung TUan Hotel Sdn Bhd Hotel operations Hotel Selesa Sdn Bhd Investment holding

Metro E:1uipment Systems (M) Trading of parking and other Sdn Bhd (Damansara Realty related equipment Berhad)

Smart Parking Management Trading of parking and other Systems Sdn Bhd# related services (Damansara Realty Berhad)

Pusat Pakar Kluang Utama Sdn Bhd# (KPJ)

Specialist hospital

Pasir Gudang Specialist Hospital Sdn Bhd# (KPJ)

Specialist hospital

Kulim Civilworks Sdn Bhd# Facilities maintenance (Kulim) Akademi Mutawwif Sdn Bhd Training of Mutawwif

Selasih Catering Services Sdn Sale and purchase and cater Bhd (Formerly known as Johor food and drinks Land Property Management Sdn Bhd)

KCW Roadworks Sdn Bhd# Dormant

Golden Clay Industries Sdn Roofing tiles Bhd GCI Marketing Sdn Bhd Roofing tiles Kukup Garden Sdn Bhd Chalet Operator Johor Plant Tech Sdn Bhd Tissue culture Karisma Astaka Sdn Bhd Quarry Isedecor Batu Bata Sdn Bhd Construction PPL Plantation Sdn Bhd Management of Ladang

Terosot

Date of appointment

1 February 2011 1 September 2011

15 Septem ber 2011

15 September 2011

1 January 2012

1 January 2012

6 January 2012

2 September 2013 1 January 2014

1 January 2014

15 March 2014

15 March 2014 15 March 2014 15 March 2014 15 March 2014 15 March 2014 15 March 2014

171

Date of resignation

6 April 2014 6 April 2014

15 December 2012

15 December 2012

1 January 2014

1 January 2014

15 July 2012

15 March 2014

15 April 2014

15 March 2014

8 April 2014

8 April 2014

8 April 2014 8 April 2014 8 April 2014 8 April 2014 24 June 2014

Involvement in business activities performed outside our Group other than director

N/A N/A

N/A

N/A

N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A N/A N/A N/A N/A N/A

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Involvement in business activities performed outside our Group other

Name Companies Principal activities Date of appointment Date of resignation than director

Rozan bin Mohd Sa'at Previous directorships (Cont'd):

Isedecor Pengangkutan & Dormant 15 March 2014 16 October 2014 N/A Pelancungan Sdn Bhd

Azli bin Mohamed Present directorships:

EPA Management Sdn Bhd# Investment holding, provision 1 July 2009 N/A N/A (Kulim) of management services and

consultancy. and mechanical equipment assembler

Permodalan Teras Sdn Bhd Investment holding 26 April 2010 NlA N/A Mahamurni Plantations Sdn Oil palm plantation 1 February 2011 NlA N/A Bhd# (Kulim)

KCW Roadworks Sdn Bhd# Dormant 1 July 2011 N/A N/A (Kulim) Kulim Plantations (Malaysia) Oil palm plantation 1 July 2011 N/A NlA Sdn Bhd# (Kulim)

Kumpulan Bertam Plantations Oil palm plantation 1 July 2011 N/A N/A Berhad# (Kulim)

Nexsol (Malaysia) Sdn Bhd# Manufacturer of bio diesel 1 July 2011 N/A N/A (Kulim) Superior Harbour Sdn Bhd# Aquaculture operations 1 July 2011 NlA N/A (Kulim) Pristine Bay Sdn Bhd# (Kulim) Investment holding 1 November 2011 N/A N/A Pinnacle Platform Sdn Bhd# Software maintenance and 2 July 2012 NlA N/A (Kulim) supplier EPASA Shipping Agency Sdn Shipping and forwarding agent 1 January 2013 N/A N/A Bhd# (Kulim) services

172

Company No. 256516-

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name Companies Principal activities Date of appointment Date ()f resignation

Azli bin Mohamed Present directorships (Cont'd):

KCW Electrical Sdn Bhd# Electrical installation services 1 January 2013 N/A (Kulim) KCW Kulim Marine Services Marine maintenance 1 January 2013 N/A Sdn Bhd# (Kulim) Kulim Civilworks Sdn Bhd# Facilities maintenance 1 January 2014 N/A (Kulim)

Previous directorships:

TMR Urusharta (M) Sdn Bhd# Principally engaged in the 1 January 2009 1 July 2011 (Damansara Realty Berhad) business of real estate

services, involved in general services, facility management, project consultant and project management

Johor Ventures Sdn Bhd Investment holding 1 July 2009 1 January 2014 Rajaudang Sdn Bhd Rental of marine livestock 1 July 2009 1 July 2011

pond and engaging business in aquaculture

Rajaudang Aquaculture Sdn Engaging in business of 1 July 2009 1 July 2011 Bhd fishing, sourcing, breeding,

hatching and growing of water plants

Aquapreneur Sdn Bhd Rental of marine livestock 1 July 2009 1 July 2011 pond and engaging business in aquaculture

Rajaudang Trading Sdn Bhd Tradingl Supplier agent 1 July 2009 1 July 2011 Sindora Ventures Sdn Bhd Investment Holding 1 July 2009 1 July 2011

Laut Resort Sdn Bhd Dormant 1 July 2009 1 July 2011 East Asian Marine Foods Sdn Processing and marketing of 1 July 2009 1 July 2011 Bhd tiger prawns and seafood Intrapreneur Development Investment holding 1 July 2009 2 September 2013 Capital Sdn Bhd

173

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A

N/A

N/A N/A

N/A

N/A

N/A N/A N1A N/A

N/A

No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name

Azli bin Mohamed

Companies

Previous directorships . (Cont'd):

Principal activities Date of appointment

Johor Franchise Development Investment holding and estate 1 July 2009 Sdn Bhd management

Aquabuilt Sdn Bhd Aquaculture management 1 July 2009 services

Intrapreneur Development Sdn Investment 15 July 2009 Bhd

Johor Foods Sdn Bhd Investment holding and oil 1 August 2009 palm plantation

Johor Tea Sdn Bhd Tea plantation 1 August 2009 Tanjung Tuan Hotel Sdn Bhd Hotelier 16 November 2009

Effective Corporate Resources Accounting services 1 January 2010 Sdn Bhd JCorp Hotels & Resorts Sdn Investment holding 5 May 2010 Bhd JCorp Capital Solutions Sdn Investment holding 1 February 2011 Bhd (Formerly known as Jedcon Engineering Survey Sdn Bhd)

TPM Technopark Sdn Bhd Development and sale of 1 February 2011 industrial land

Puteri Hotels Sdn Bhd Hotel operations 1 April 2011 Skellerup Industries (Malaysia) Production of rubber products Sdn Bhd# (Kulim)

1 July 2011

Kulim Safety Training And Occupational Safety and 1 January 2013 Services Sdn Bhd# (Kulim) Health Administration Training

and services Optimum Status Sdn Bhd# Mill maintenance and 1 January 2013 (Kulim) fabrication Ara Offshore Engineering & Dormant 30 December 2013 Services Sdn Bhd

174

Date of resignation

1 January 2012

1 July 2011

2 September 2013

1 January 2013

16 January 2012 1 January 2014 1 July 2011

1 Julv 2011

15 August 2011

15 August 2011

16 January 2012 2 July 2012

1 January 2014

1 January 2014

24 April 2014

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A

N/A

N/A N/A N/A

N/A

N/A

N/A

N/A N/A

N/A

NlA

N/A

Company No. 2S6S16-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name

Datuk Anuar bin Ahmad

Companies Principal activities Date of appointment pate of resignation

Present directorships:

Concrete Acres Sdn Bhd Investment 29 December 2011 N/A Angeles Foods Sdn Bhd Food/Cafe 8 April 2013 N/A

Syarikat Wandeerfull Sdn Bhd Property development 1 July 2014 N/A Mampan Esa (Melaka) Sdn Property development 4 July 2014 N/A Bhd

PETRONAS Dagangan@ Retailing & marketing of 1 August 2014 N/A petroleum product

PDZ Holdings Berhad@ Investment holding 4 September 2014 NlA

TNB Fuels Services Sdn Bhd Business of supplying fuel and 10 October 2014 N/A coal for power generation

Previous directorshiJ2§;.

PETRONAS O&G 1 October 2002 16 April 2014

Prince Court Medical Centre Healthcare 24 September 2004 1 September 2011 Sdn Bhd Institute of Technology Education 1 August 2005 16 April 2014 PETRONAS Sdn Bhd PETRONAS Carigali O&G exploration and 1 September 2005 20 July 2010

production PETRONAS Carigali Overseas O&G exploration and 1 September 2005 20 July 2010 Sdn Bhd production PETRONAS Lubricants Marketing & manufacturing of 12 September 2007 15 July 2010 International Sdn Bhd lubricants PETRONAS Chemicals Group Manufacturing and marketing 22 June 2010 15 September 2011 Berhad of petrochemicals Malaysia LNG Sdn Bhd Natural gas liquidation 16 July 2010 16 April 2014

175

Involvement in business activities performed outside our Group other than director

Shareholder (direct: 50.0%)

N/A

N/A Shareholder (indirect interest held through Concrete Acres Sdn Bhd: 20.0%)

N/A

N/A N/A

N/A N/A

N/A

N/A

N/A

N/A

N/A

N/A

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Name

Datuk Anuar bin Ahmad

Companies

Previous directorships (Cont'd):

Malaysia LNG Dua Sdn Bhd

Malaysia LNG liga Sdn Bhd

Trans Thai-Malaysia (Malaysia) Sdn Bhd International CoRference and Exhibition ProfeSsionals PETRONAS Gas Berhad@

PETRONAS LNG Sdn Bhd PETRONAS Power Sdn Bhd PETRONAS LNG 9 Sdn Bhd

Principal activities Date of appointment

Manage and operate second 16 July 2010 LNG plant Manage and operate third LNG 16 July 2010 plant Transmission of natural gas 23 August 2010

Conference & exhibition 23 September 2010 management Natural gas processing & 17 October 2010 transmission

Marketing of LNG 21 March 2011

Electricity generation 11 November 2011 Natural gas liquefaction 13 January 2012

Datuk Mohd Nasir bin Present directorships: Ali

Langkah Bahagia Sdn Bhd The Nomad Group Berhad ("Nomad")@

Investment holding Investment holding

Vertical Theme Sdn Bhd Investment holding

The Nomad Hotel Penang Sdn Hotelier and hotel related Bhd# (Nomad) . services

15 October 1996 5 August 1998

9 March 2005

18 June 2013

ICB Islamic Bank Umited@ Banking and financial business 10 June 2014 activities

Yayasan Kelana Ehsan Financial assistance, donation, 11 Septem ber 2014 gifts, sponsorship and scholarship

176

Date of resignation

16 April 2014

16 April 2014

11 August 2011

11 April 2013

15 May 2014

16 April 2014

16 April 2014 10 September 2012

N/A N/A

N/A

NlA

N/A

N/A

Involvement in business activities performed outside our Group other than director

N/A

N/A

N/A

N/A

N/A

N/A

NlA N/A

Shareholder (direct: 1.0%) Shareholder (direct: A)

N/A

N/A

N/A

N/A

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cant'd)

Name Companies Principal activities Date Of appointment

Datuk Mohd Nasir bin. Previous directorships: AIi

Md Tamyes bin Hj A.Rahim

Utusan Melayu (Malaysia) . Publication, printing and Berhad ("Utusan")@ distribution of newspapers Utusan Publications and Publication and distribution of Distributors Sdn Bhd# (Utusan) reading materials Utusan Media Sales Sdn Bhd# Advertising agents (Utusan) Swan Malaysia Sdn Bhd# (Utusan)

Manufacturing and trading educational aids; and writing instruments and related products

2 October 2000

26 January 2001

26 January2oo1

26 January 2001

Utusan Karya Sdn Bhd# (Utusan)

Publication of magazines and 4 June 2003

Perfisio Solutions Sdn Bhd# (Utusan)

advertiSing Information technology, multimedia and online advertising

14 September 2006

Swan Solar Sdn Bhd# (Utusan) Installation of non-electric solar 17 July 2013 energy collectors

Present directorships:

N/A N/A N/A

Previous directorships:

N/A N/A N/A

177

Date of resignation

5 June 2014

5 June 2014

5 June 2014

5 June 2014

5 June 2014

15 December 2013

5 August 2013

N/A

NlA

Involvement in business activities performed outside our Group other than director

Shareholder (direct: 11)

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

Company No. 256

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Confd)

Name Companies Principal activities Date of appointment

Abdul Azmin bin Abdul Present directorships: Halim

Ashera Jaya Sdn Bhd Dormant 8 August 2008 Star Technic Engineering Sdn Supply installation of highway 21 June 2013 Bhd guardrails and accessories

Previous directorships:

Global Marine & Offshore Sdn Dormant Bhd

6 July 2009

Piezzoe Sdn Bhd Manufacturing of heat 15 October 2009 ventilating and air conditioning systems

Notes:-

# 1\

@

NIA

: SubSidiary company of a listed company as at the LPD. : Negligible : Listed company : Not applicable

Date of resignation

N/A N/A

19 September 2012

13 June 2012

THE REST OF THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK

178

Involvement in business activities performed outside our Group other than director

Shareholder (direct: 40.0%) Shareholder (direct: 50.0%)

N/A

N/A

ompany No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

8.2.4 Directors' remuneration, fees and material benefits~in-kind

The aggregate remuneration and material benefits-in-kind paid and proposed to be paid to our Directors for services rendered in all capacities to our Group for the FYE 31 December 2013 and FYE 31 December 2014 are as follows:-

Remuneration band

Directors

Ahamad bin Mohamad

Data' Hak

Rozan bin Mohd Sa'at

Azli bin Mohamed

Datuk Anuar bin Ahmad

Datuk Mohd Nasir bin Ali

Md Tamyes bin Hj A. Rahim

Abdul Azmin bin Abdul Halim

Notes:-

FYE 31 December 2013

50,001 -100,000

800,001 - 850,000

o 50,000

"N/A

"N/A

"N/A

"N/A

"N/A

A

NIA Appointed subsequent to FYE 31 December 2013 Not applicable

Proposed for FYE 31 December 2014

50,001 -100,000

850,001 - 900,000

0-50,000

o 50,000

0-50,000

0-50,000

0-50,000

0-50,000

The remuneration of our Directors which includes salaries, bonuses, fees and allowances as well as other benefits, is approved by our Board, following recommendations made by our Remuneration Committee and subject to our Articles of Association. Any change in Directors' fees as set out in our Articles of Association must be approved by shareholders of our Company pursuant to an ordinary resolution passed at a general meeting where appropriate notice of any proposed increase should be given. Please refer to Section 8.3.3 of this Prospectus for further details.

8.3 Board practice

8.3.1 Directorship

In accordance with our Articles of Association, the Directors shall have the power at any time and from time to time to appoint any person to be a Director either to fill a casual vacancy or as an additional Director, but so that the total number of Directors shall not at any time exceed the maximum number fixed by or in accordance with our Articles of Association which is fifteen (15) directors. At the first annual general meeting of our Company, all our Directors shall retire from office, and at the annual general meeting in every subsequent year, one third (1/3) of our Directors must retire at each annual general meeting of shareholders but are eligible for re-election. Our Directors must submit themselves for re-election at least once in three (3) years.

179

I Company No. 256516-W I:

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT

As at the LPD, the details of the date of expiration of the current term of office for each of our Directors and the period that each of our Directors has served in office are as follows:-

Name

Ahamad bin Mohamad

Data' Hak

Rozan bin Mohd Sa'at

Azli bin Mohamed

Datuk Anuar bin Ahmad

Datuk Mohd Nasir bin AIi

Md Tamyes bin Hj ARahim

Abdul Azmin bin Abdul Halim

8.3.2 Audit committee

Date of appointment as

Director

12 October 2009

1 February 2002

1 January 2007

15 April 2014

15 April 2014

17 October 2014

15 April 2014

15 April 2014

Date of expiration of the current term of

office

Subject to retirement at the

AGM 2014

Subject to retirement at the

AGM 2015

Subject to retirement at the

AGM 2016

Subject to retirement at the

AGM 2017

Subject to retirement at the

AGM 2017

Subject to retirement at the

AGM 2017

Subject to retirement at the

AGM 2017

Subject to retirement at the

AGM 2017

The composition of our Audit Committee is set out below:-

Approximate no. of years in office

5

12

7

Name Designation DirectorstliCJ.:p __________ _

Datuk Anuar bin Ahmad Chairman Senior Independent Non-Executive Director

Abdul Azmin bin Abdul Halim Member Independent Non-Executive Director

Azli bin Mohamed Member Non-Independent Non-Executive Director

The terms of reference of our Audit Committee, amongst others, indude the· following:-

(i) To ensure openness, integrity and accountability in our Group's activities so as to safeguard the rights and interests to our shareholders;

180

Company No. 256

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

(ii) To provide assistance to our Board in fulfilling its fiduciary responsibilities relating to corporate accounting and reporting practices;

(iii) To improve our Group's business efficiency, the quality of accounting and audit function and strengthening of public's confidence in our Group's reported results;

(iv) To maintain a direct line of communication between our Board and the external and internal auditors;

(v) To enhance the independence of the external and internal auditors;

(vi) To create a climate of discipline and control, this will reduce the opportunity for fraud;

(vii) To assess the financial risks and matters relating to related party transactions and conflict of interests;

(viii) To recommend our Board regarding the appointment of the external auditors; and

(ix) Obtain advice from independent parties and other professionals, where necessary, in discharging their duties.

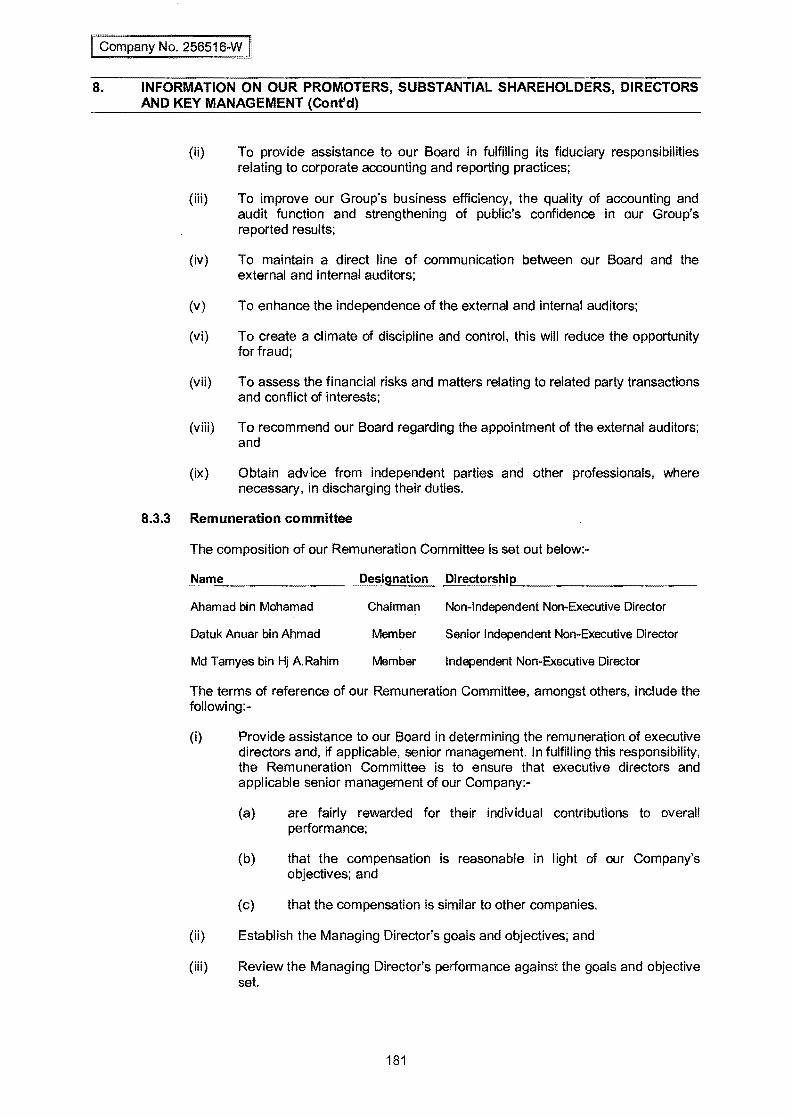

8.3.3 Remuneration committee

The composition of our Remuneration Committee is set out below:-

Designation ..=D:..::ir:...:::e=ct.::.::o:.::.r.=.:sh:.:::iJ:..p __________ _

Ahamad bin Mohamad Chairman Non-Independent Non-Executive Director

Datuk Anuar bin Ahmad Member Senior Independent Non-Executive Director

Md Tamyes bin Hj A.Rahim Member Independent Non-Executive Director

The terms of reference of our Remuneration Committee, amongst others, include the following:-

(i) Provide assistance to our Board in determining the remuneration of executive directors and, if applicable, senior management. In fulfilling this responsibility, the Remuneration Committee is to ensure that executive directors and applicable senior management of our Company:-

(a) are fairly rewarded for their individual contributions to overall performance;

(b) that the compensation is reasonable in light of our Company's objectives; and

(c) that the compensation is similar to other companies.

(ii) Establish the Managing Director's goals and objectives; and

(iii) Review the Managing Director's performance against the goals and objective set.

181

Company No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

8.3.4 Nomination committee

The composition of our Nomination Committee is set out below:-

Name Designation ,.;;;;D..:..;ir'-=e-=.ct::.,:o:..;..rs;;;..:h.;..:.iJ.:-p ________ _

Ahamad bin Mohamad Chairman Non-Independent Non-Executive Director

Md Tamyes bin Hj A.Rahim Member Independent Non-Executive Director

Abdul Azmin bin Abdul Halim Member Independent Non-Executive Director

The terms of reference of our Nomination Committee, amongst others, include the following:-

(i) Identify and recommend to our Board, candidates for board directorships of our Company;

. (ii) Recommend to our Board, directors to fill the seats on Board committees;

(Hi) Evaluate the effectiveness of our Board and Board committees (including its size and composition) and contributions of each individual director; and

(iv) Ensure an appropriate framework and plan for Board succession for our Company.

In relation to the above, our Board is aware of and supports the Malaysian Code of Corporate Governance 2012 ("MCCG 2012") as a basis for practices on corporate governance. Recommendation 3.5 of the MCCG 2012 states that where the position of chairman of the board is not an independent director, the board must comprise of a majority of independent directors,

Although our Company has yet to be in line with the above recommendation, where our current Board comprise, one (1) Non-Independent Non-Executive Chairman, and only four (4) out of the remaining seven (7) Directors are Independent Non-Executive Directors, it is pertinent to note the following:-

(i) Our Board believes that the interest of shareholders is best served by a Chairman who is sanctioned by the shareholders and who will act in the best interests of the shareholders as a whole. The Chairman exercises independent and broad judgement as well as provides constructive views on proposals put forth by the Managing Director. As the Chairman representing Kulim who is the controlling shareholder of our Company, he is well placed to act on behalf of shareholders and in their best interest. Similarly, there are two (2) other Non-Independent Non-Executive Directors on our Board who represent Kulim and have been appointed to ensure that Kulim's interest in our Company is safeguarded;

(H) There is only one (1) executive director on our Board who is the Managing Director and involved in the day-to-day operations of our Group. The Managing Director is hence responsible for reporting our Group's overall business and financial performance to both our Chairman and the remaining six (6) Non-Executive directors of our Company. The high number of NonExecutive directors provide sufficient checks and balances in the functioning of our Board whilst ensuring a high standard of reporting and corporate governance; and

182

i Company No. 256516-W I 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS

AND KEY MANAGEMENT (Cont'd)

(iii) The four (4) Independent Non-Executive Directors are qualified professionals in their respective fields and bring with them a wealth of knowledge and experience as highlighted under Section 8.2.2 of this Prospectus.

Notwithstanding the above, the present position on the current board composition may change over time as our Company grows further in terms of size and scale. Our Board undertakes to re-assess and review its position on the independence of our Board on an annual basis and in its deliberations, will take into consideration, amongst others, its performance and conduct during the period under review (in terms of effectiveness, integrity, fairness and independence) and the recommendations prescribed under the MCCG 2012.

As at the LPD, save for recommendations 3.5 of the MCCG 2012, our Board confirms compliance with the other recommendations in MCCG 2012.

THE REST OF THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK

183

[C?ompa~y No. 2565w:w]

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Confd)

8.4 Key management

8.4.1 Shareholdings

The following table sets forth the direct and indirect shareholdings of each of our key management before and after the IPO, assuming each of our key management will subscribe for their respective pink form allocation:-

Before IPO After IPO

Direct Indirect Direct Indirect No. of No. of No. of No. of

Shares held Shares held Shares held Shares held Name Designation Nationality ('000) % ('000) % ('000) % ('000) %

Dato' Hak Managing Director Malaysian 96,000 24.6 (1139,000 10.0 90,900 18.0 (1129,100 5.8

Ir. Zulkifli bin Mohd Amin General Manager Malaysian 340 0.1

Zuraimi bin Basri Chief Financial Officer Malaysian 280 0.1

Tajul Asikin bin Sallehudin Manager. Technical Malaysian 215 *

Captain Nasruddin bin Abdul Manager, Safety. Quality Malaysian 245 * Mutalib and Security

Che Zal Azilah bte Che Omar Manager, Account Malaysian 250 *

Captain Mohd Yusni bin Manager, Fleet Operation Malaysian 215 * Razali

Farrah Radziah Binti Dato' Ir Manager, Commercial Malaysian 195 * Abdul Hak

New Kok Ho General Manager, Johor Malaysian 325 0.1 Shipyard

Notes:-Negligible Deemed interested by virtue of his spouse's shareholdings in our Company pursuant to Section 6A of the Act. (1)

Notwithstanding the pink form allocation reserved for our key management, our key management may subscribe for the Issue Shares under the Public Offer.

184

11 Company No. 256?16-W I 8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS

AND KEY MANAGEMENT

8.4.2 Key management profiles

Save for the profile of Dato' Hak which is set out in Section 8.1.2 of this Prospectus, the profiles of the others key management of our Group are as follows:-

Ir. Zulkifli bin Mohd Amin, a Malaysian aged 46, is our General Manager. He graduated in 1992 with a Bachelor of Science in Naval Architecture & Marine Engineering from University of New Orleans, United States. He started his career in 1992 as a naval architect at Penang Shipbuilding Corporation Sdn Bhd. In 1993, he joined GEC (M) Sdn Bhd as sales engineer/naval architect. In 1994, he joined our Company as a technical manager. In 2008, he was promoted to General Manager and is currently responsible for overall fleet operations and commercial operations for our marine transportation and offshore storage operations as well as port marine services. He is also a director of Johor Shipyard.

Zuraimi bin Basri, a Malaysian aged 45, is our Chief Financial Officer. He graduated in 1993 with a Bachelor of Accounting (Honours) from University Utara Malaysia. He started his career in 1994 as a finance executive in Sindora. In 1996, he was promoted as the head of internal audit unit in Sindora. In 2003, he was seconded to a joint venture company of Sindora, PT Andalas Lumber Products in Padang, West Sumatera as a finance director. In 2004, he served as deputy finance manager of Sindora until 2006 before he joined our Group in early 2007 as the Senior Manager of Finance & Administration. On 1 September 2014, he was re-designated to Chief Financial Officer and is currently responsible for overall financial, accounting, compliance and reporting, administration and internal control functions of our Group. He has been a member of Malaysian Institute of Accountants since 2002.

Che Zal Azilah bte Che Omar, a Malaysian aged 45, is our Accounts Manager. She graduated in 1991 with a Diploma in Statistics from Mara Institute of Technology, Shah Alam, Selangor. She started her career in 1991 as an assistant statistician at Lembaga Kemajuan Terengganu Tengah. In 1993, she joined our Group as an account officer. In 1995, she left our Group and joined Sempati Air Pte ltd as a senior account officer. In 1998, she re-joined our Group as an accounts officer. In 2006, she was promoted to Accounts Manager and is currenijy responsible for the overall accounting functions of our Group, such as payables, receivables, cash flow monitoring and preparation of accounts for financial reporting purposes.

Tajul Asikin bin Sallehudin, a Malaysian aged 50, is our Technical Manager. He graduated in 1984 with a Bachelor of Engineering (Marine) from Indonesian Merchant Marine Academy Jakarta, Indonesi.a. He started his career in 1984 at Malaysian International Shipping Corporation Berhad ("MISC") as cadet engineer before he was promoted as a marine junior engineer from 1985 to 1986. From 1986 to 1995, he moved up his rank from a marine fourth engineer to a marine chief engineer. The last post he held in MISC is as an auditor in Ship Management Audit Department before he left the company to join Pan Pacific Hotel in 1996 which he served as building chief engineer until 1997. From 1997 to 1998, he served as a field service manager in Sapura Petroleum Services. In 1998, he joined Sapura Maritime Engineering Sdn Bhd as a base/business development manager. From 1999 to 2001, he was the managing director in Profile Budi Sdn Bhd before he left the company to join Rusli Offshore Corporation Sdn Bhdas a vice president of operations. In 2002, he re-joined MISC and served as senior superintendent liner for four (4) years. From 2007 to 2010, he served as a head of fleet in Global Carriers Berhad before he joined JRI Resources Sdn Bhd as a general manager of Operations Department from 2011 until 2012. In early 2013, he joined our Group as a Technical Manager and is mainly responsible for the entire technical operations of our vessels including deck, equipment and machinery.

185

Company No. 256516-W

8. INFORMATION ON OUR PROMOTERS, SUBSTANTIAL SHAREHOLDERS, DIRECTORS AND KEY MANAGEMENT (Cont'd)

Captain Nasruddin bin Abdul Mutalib, a Malaysian aged 61, is our Safety, Quality and Security Manager. He graduated in 1982 with Master Class 1 Certificate of Competency, Foreign Going in Mualim Pelayaran Besar. He started his career in 1971 at Indonesian Maritime Academy before he was promoted as a cadet on IVIISC vessels in 1973. From 1975 to 1984, he moved up his rank as a third officer to a senior chief officer with a Master's Certificate. From 1985 to 1988 he was appointed as a master in MISC vessels and commanded 13 MISC's ships. From 1988 to 1990 he became an operations superintendent of Liner Division which is in charge of operations and ship planning for Far East Australia services and Japan Taiwan services. From 1990 to 1995, he was in charge of the operations for Far East Europe Service Sector, Australia Service Sector and Japan Taiwan Service Sector for eleven (11) of MISC's vessels and 16 partners' vessels. From 1995 to 2000 he was promoted as an operation manager of Liner Division. Soon after that, he was again promoted as a manager action team where he is responsible for cost reduction measures of Liner Division from 2000 to 2001. From 2001 to 2002 he was appointed as a marine superintendent of the Fleet Management Division. Then, from 2002 to 2004 he was responsible for Technical Operations for three (3) Liner vessels in MISC. In 2004, he left and joined our Company as a senior manager of our Fleet Operation where he is responsible for Technical Operations of our Company's four (4) tanker vessels and LPG vessel, and thereafter in 2005 he was appointed as a company security officer as per the requirement of The International Ship and Port Security (ISPS). In 2006, he was promoted as a Safety, Quality and Security Manager and is currently responsible to carry out shipboard and safety management audits on the vessels in accordance to statutory bodies' requirements.