Embed Size (px)

Citation preview

1

July 28th 2017 Derek Cedar, FCAS, CERA

IABA - Enterprise Risk Management – P&C Perspective

DC Trivia: How many bathrooms are in the White House?

2

2 # of bathrooms

Average Household

0

Copyright © 2017 The Travelers Indemnity Company. All rights reserved.

DC Trivia: How many bathrooms are in the White House?

3

2 35!

AverageHousehold

0

• There are also 132 rooms, 412 doors, 147 windows, 28 fireplaces, 8 staircases, and 3 elevators.

-https://www.whitehouse.gov/about/inside-white-house

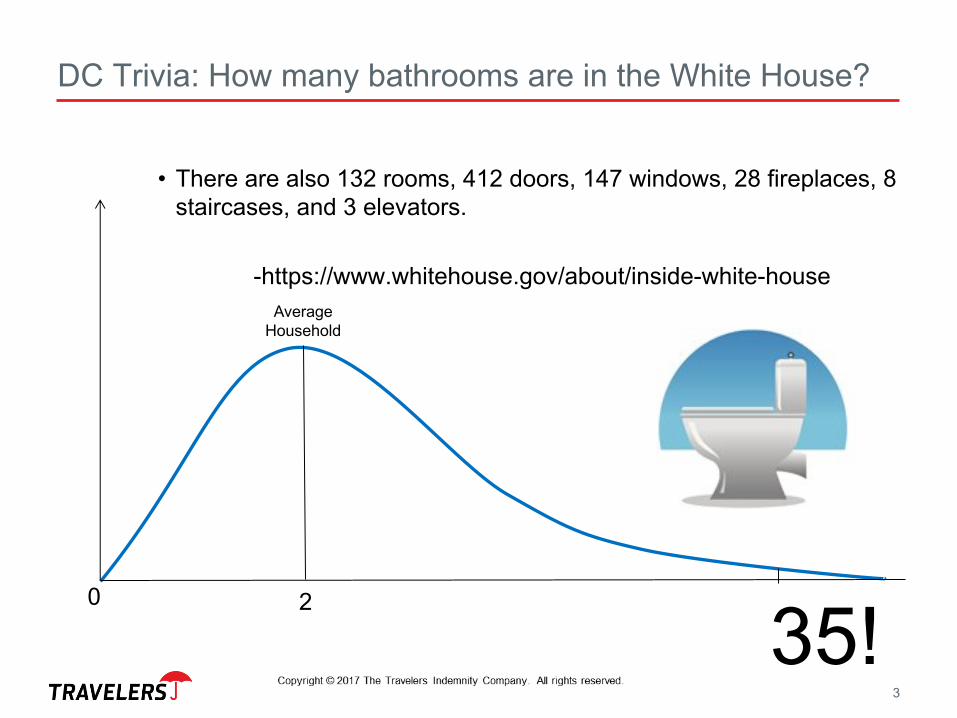

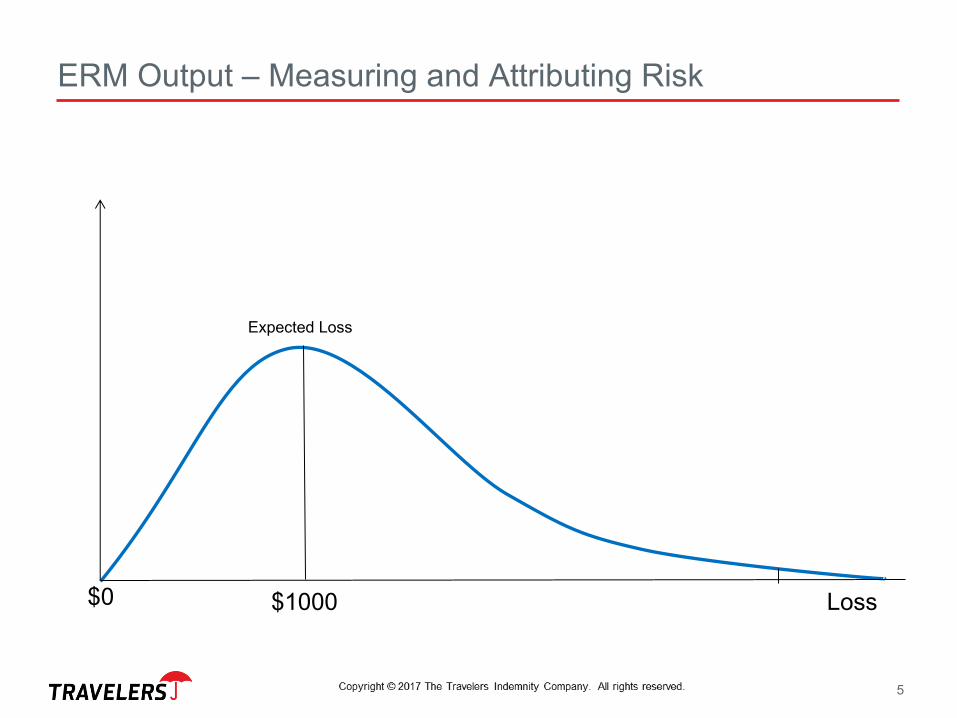

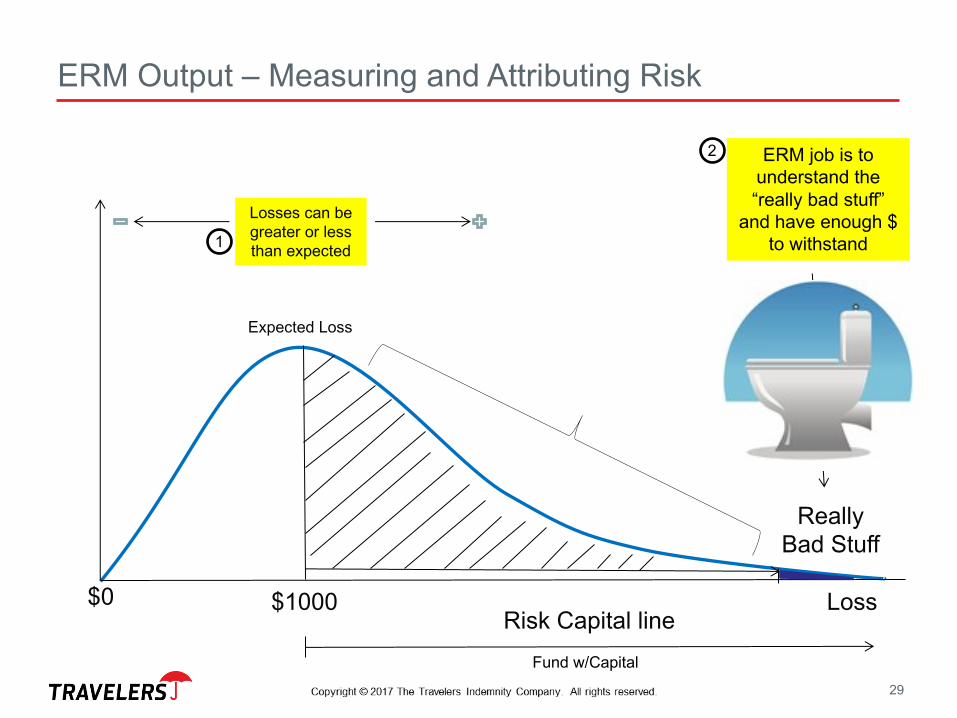

ERM Output – Measuring and Attributing Risk

4

$1000 Loss

Expected Loss

$0

Copyright © 2017 The Travelers Indemnity Company. All rights reserved.

ERM Output – Measuring and Attributing Risk

5

$1000 Loss

Expected Loss

$0

ERM Output – Measuring and Attributing Risk

ReallyBad Stuff

Risk Capital line$1000 Loss

Expected Loss

$0

6

Fund w/Capital

ERM job is to understand the “really bad stuff”

and have enough $ to withstand

Losses can be greater or less than expected1

2

Outline / Learning Objectives

• My Journey• Quick History of ERM• Capital Modeling – Why and How

• Including shameless CAS plug

• Types of P&C Risk• Puzzle• Q&A

7

MyJourney(insixpicturesorless)

8

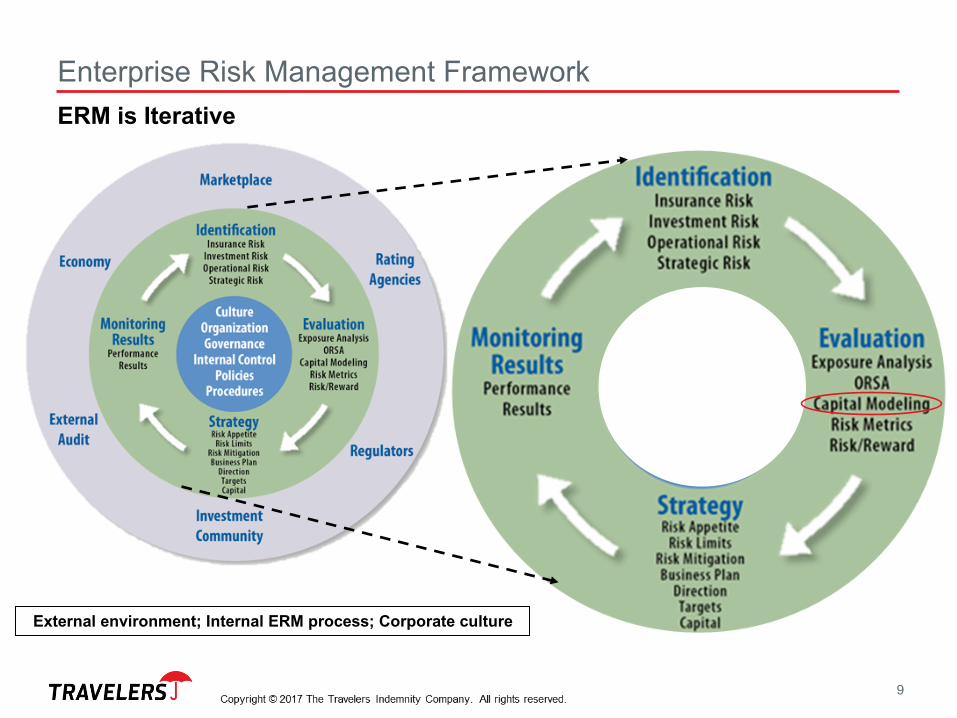

Enterprise Risk Management FrameworkERM is Iterative

External environment; Internal ERM process; Corporate culture

9

Types of Economic Capital Models

1. Regulatory – Risk Based Capital (RBC)• Protect Policyholders

2. Rating Agency – AM Best Standard & Poor’s• Inform Lenders

3. Company Internal Models• Various Stakeholders

10

Travelers Cyber Experience…

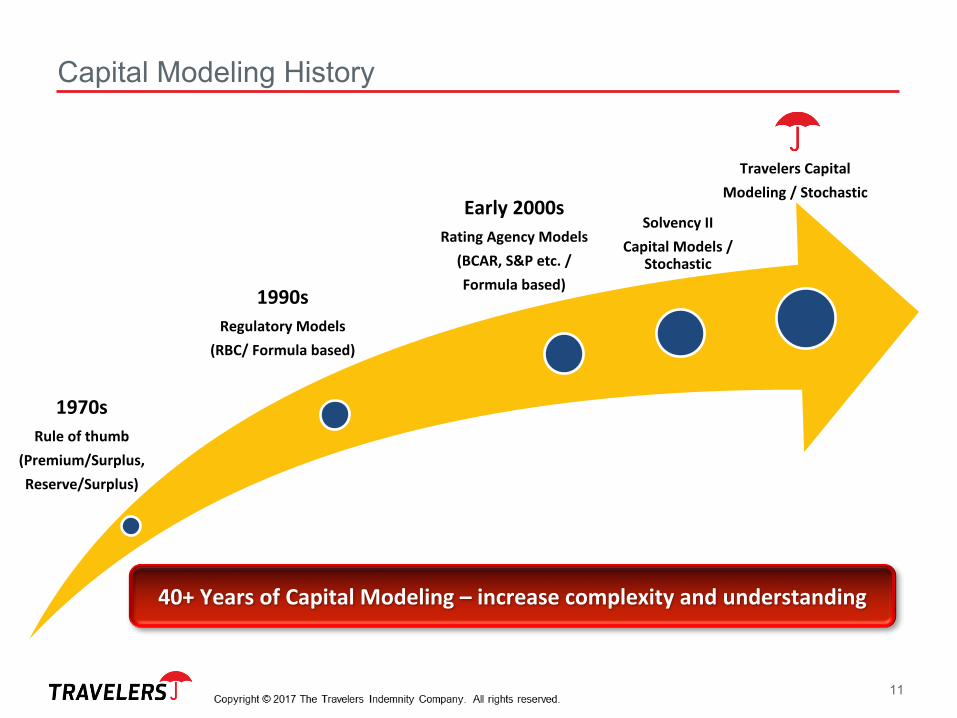

40+YearsofCapitalModeling– increasecomplexityandunderstanding

1970sRuleofthumb

(Premium/Surplus,Reserve/Surplus)

1990sRegulatoryModels

(RBC/Formulabased)

SolvencyIICapitalModels/

Stochastic

Capital Modeling History

Early2000sRatingAgencyModels

(BCAR,S&Petc./Formulabased)

TravelersCapitalModeling/Stochastic

11

Economic Capital Models

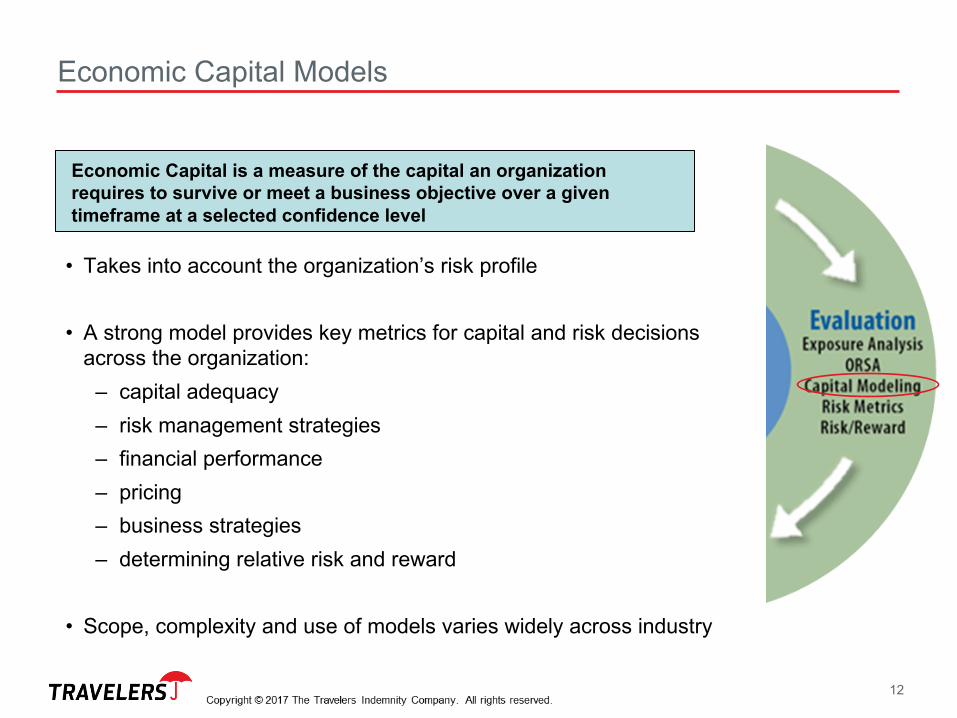

• Takes into account the organization’s risk profile

• A strong model provides key metrics for capital and risk decisions across the organization:

– capital adequacy– risk management strategies– financial performance– pricing– business strategies– determining relative risk and reward

• Scope, complexity and use of models varies widely across industry

Economic Capital is a measure of the capital an organization requires to survive or meet a business objective over a given timeframe at a selected confidence level

12

Enterprise Risk Management Framework

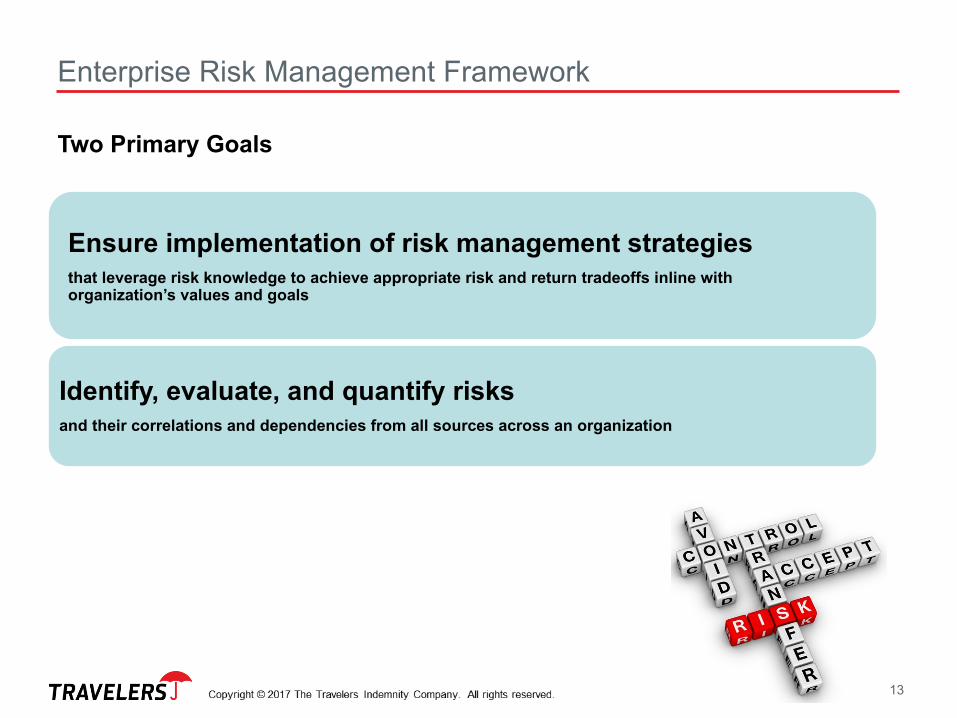

Identify, evaluate, and quantify risks and their correlations and dependencies from all sources across an organization

Ensure implementation of risk management strategies that leverage risk knowledge to achieve appropriate risk and return tradeoffs inline with organization’s values and goals

Two Primary Goals

13

CapitalModelingWhyisitImportant?

14

15

Long-Term Financial Strategy

Create Shareholder ValueBy delivering return on equity shares Over Time

RETURNEQUITY

The Return / or Income has 3 Components:

1. Underwriting Profit = Premium - Loss – Expense2. Investment Income on Premium3. Investment Income on Equity

Back to the Basics

16

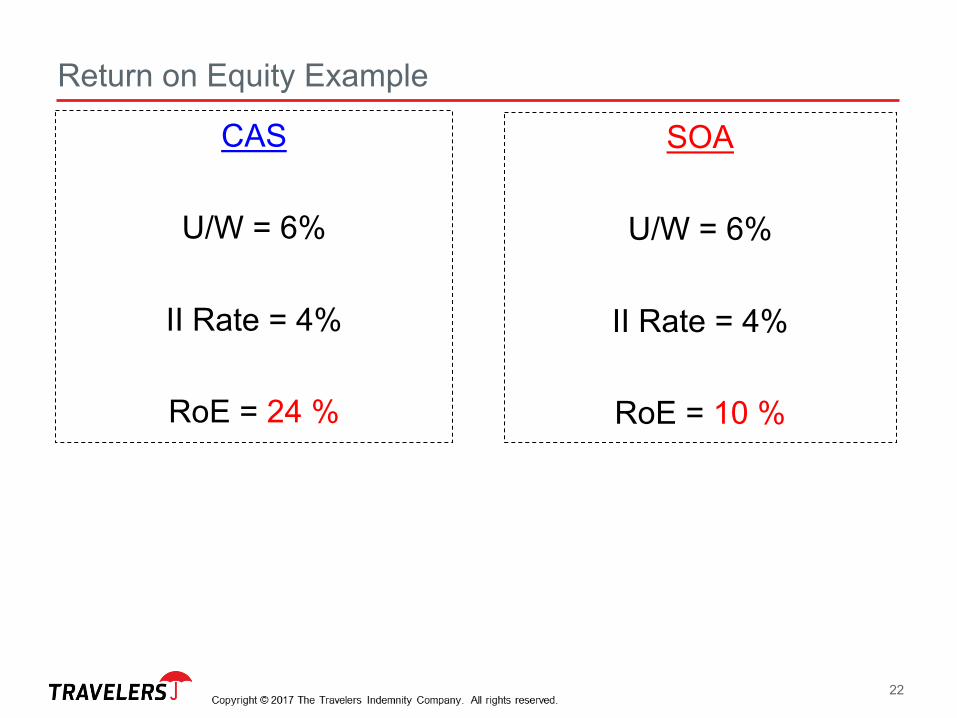

CAS SOAReturn on Equity Example

DIFFERENT ROE?!?!?

SAME RESULTS!?!?

17

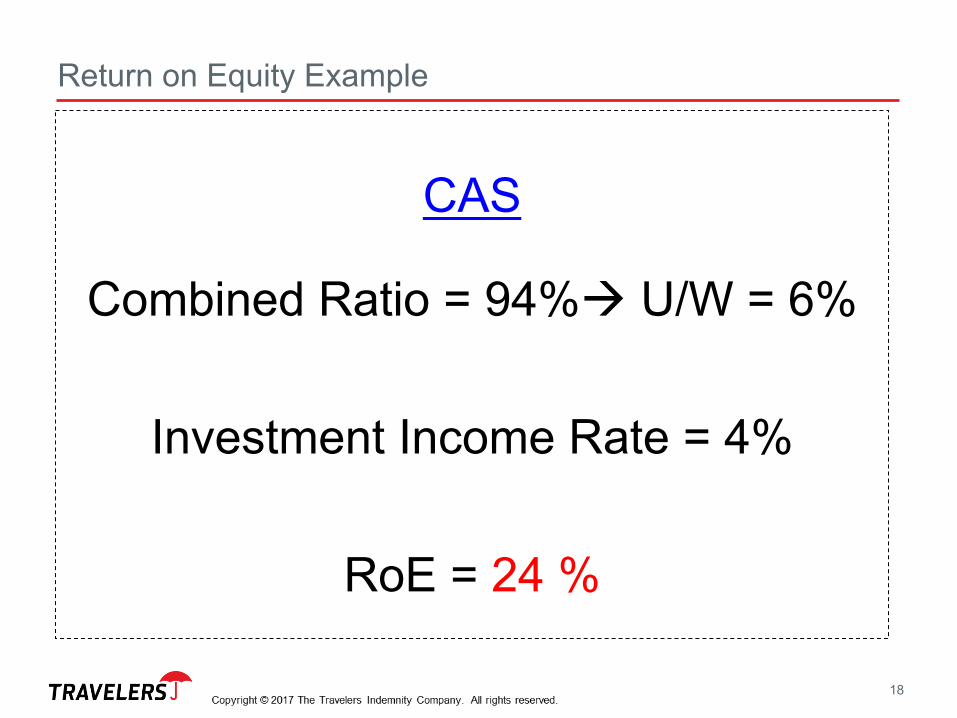

CAS

Combined Ratio = 94%à U/W = 6%

Investment Income Rate = 4%

RoE = 24 %

Return on Equity Example

18

Oh Yeaahhhhh!!! CAS IS GREAT!

19

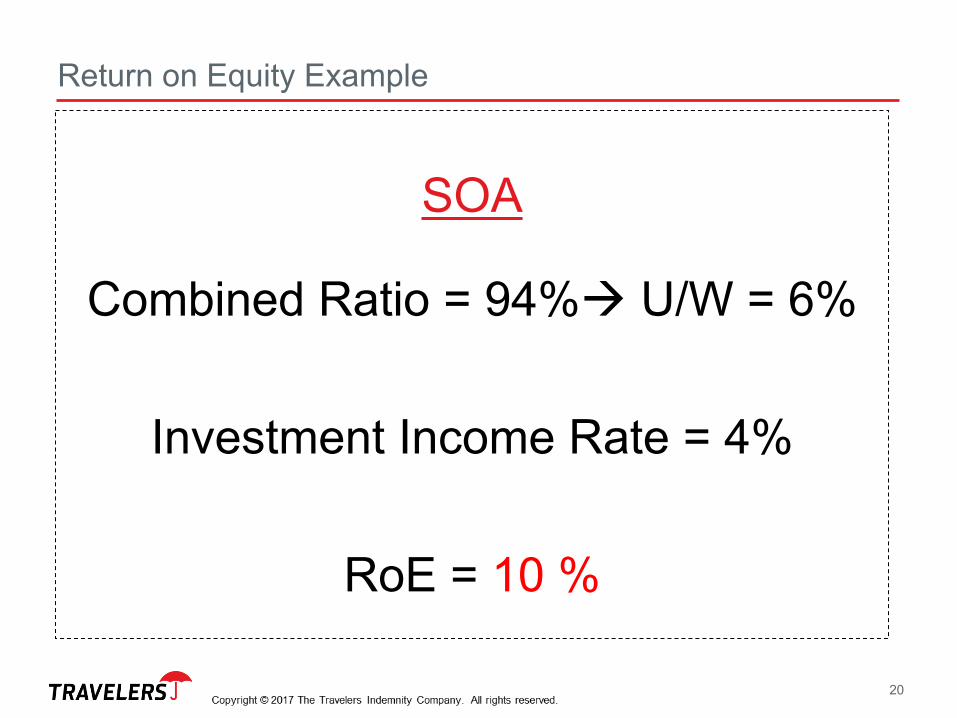

SOA

Combined Ratio = 94%à U/W = 6%

Investment Income Rate = 4%

RoE = 10 %

Return on Equity Example

20

Uh oh! Not Good.

21

CAS

U/W = 6%

II Rate = 4%

RoE = 24 %

SOA

U/W = 6%

II Rate = 4%

RoE = 10 %

Return on Equity Example

22

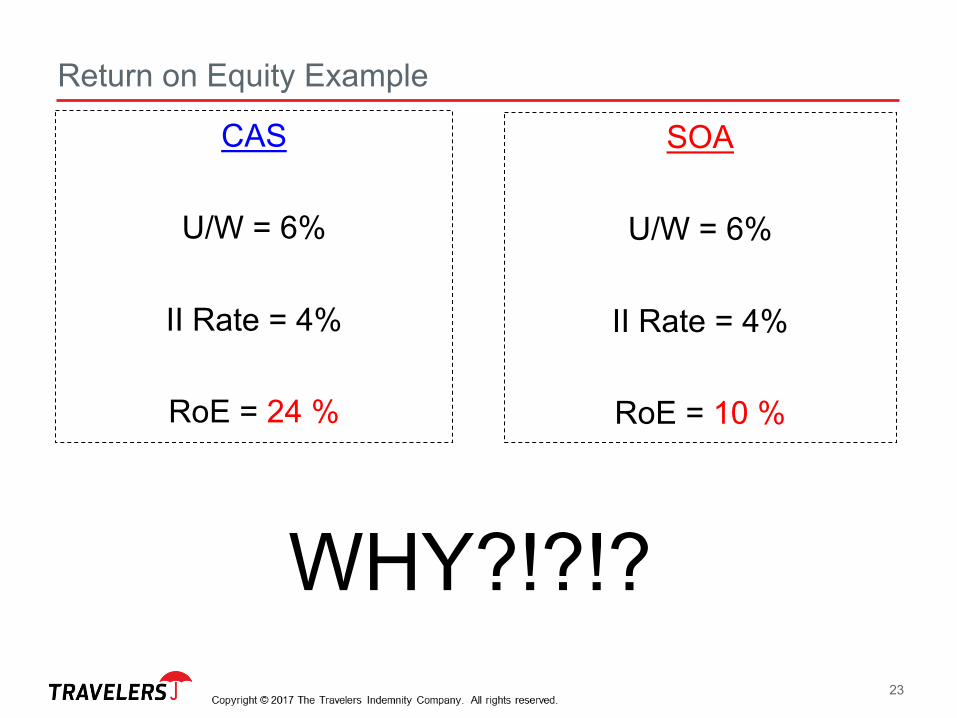

CAS

U/W = 6%

II Rate = 4%

RoE = 24 %

SOA

U/W = 6%

II Rate = 4%

RoE = 10 %

Return on Equity Example

WHY?!?!?23

Magic Lever…?????

24

Magic Lever…Equity Allocation!!

25

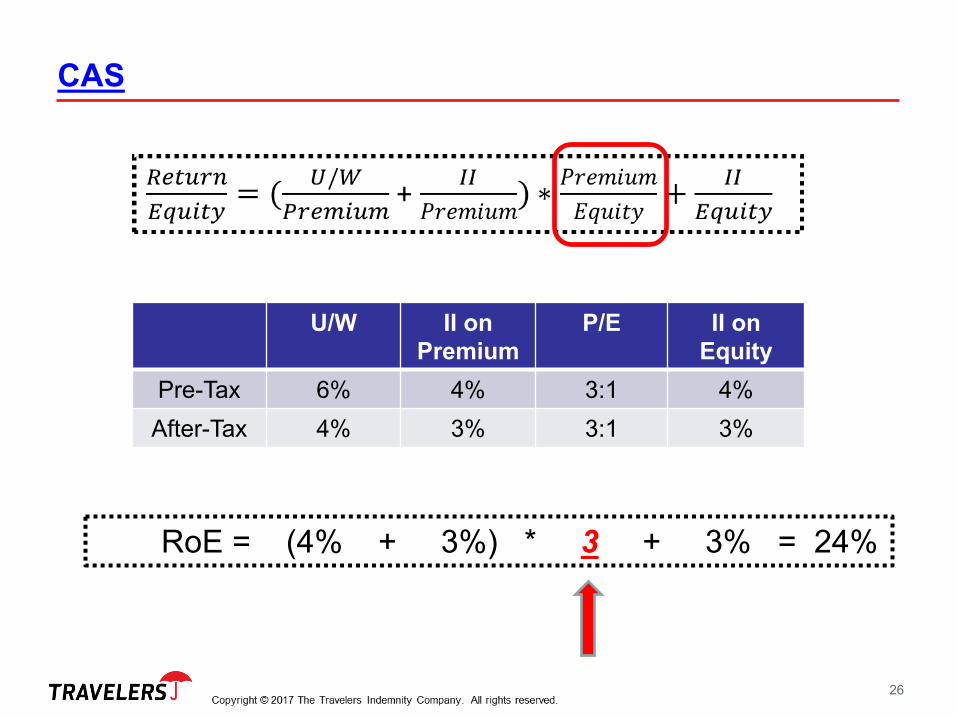

CAS

U/W II on Premium

P/E II on Equity

Pre-Tax 6% 4% 3:1 4%After-Tax 4% 3% 3:1 3%

RoE = (4% + 3%) * 3 + 3% = 24%

26

SOA

U/W II on Premium

P/E II on Equity

Pre-Tax 6% 4% 1:1 4%After-Tax 4% 3% 1:1 3%

RoE = (4% + 3%) * 1 + 3% = 10%

27

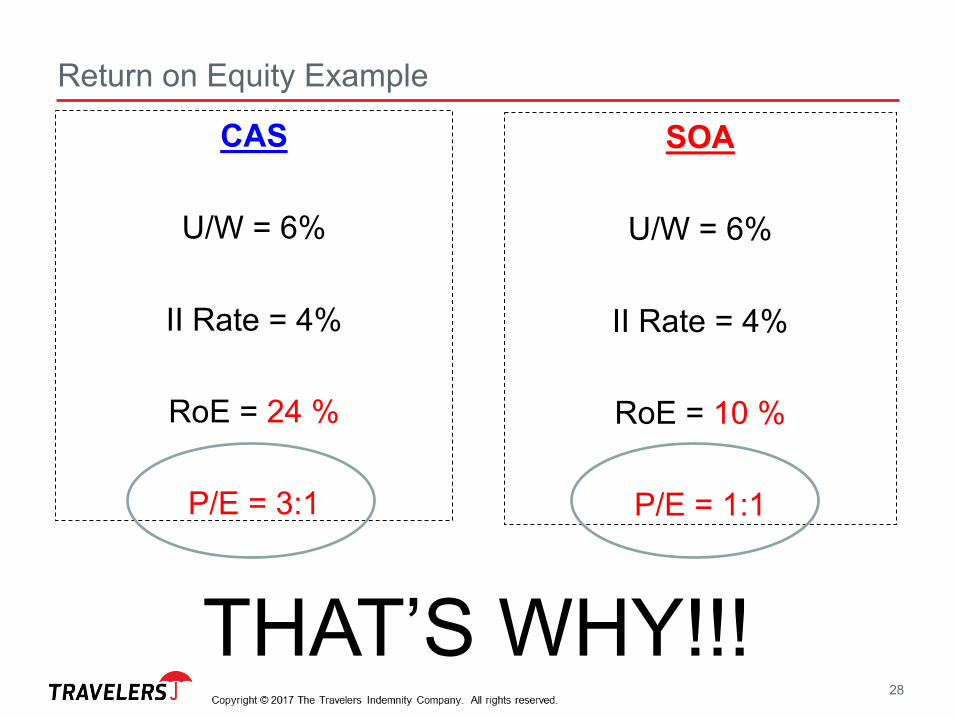

CAS

U/W = 6%

II Rate = 4%

RoE = 24 %

P/E = 3:1

SOA

U/W = 6%

II Rate = 4%

RoE = 10 %

P/E = 1:1

Return on Equity Example

THAT’S WHY!!!28

ERM Output – Measuring and Attributing Risk

ReallyBad Stuff

Risk Capital line$1000 Loss

Expected Loss

$0

29

Fund w/Capital

ERM job is to understand the “really bad stuff”

and have enough $ to withstand

Losses can be greater or less than expected1

2

RisksthatP&CInsurersFace“ReallyBadStuff”

30

Enterprise Risk Management Framework

Identify, evaluate, and quantify risks and their correlations and dependencies from all sources across an organization

Ensure implementation of risk management strategies that leverage risk knowledge to achieve appropriate risk and return tradeoffs inline with organization’s values and goals

Two Primary Goals

31

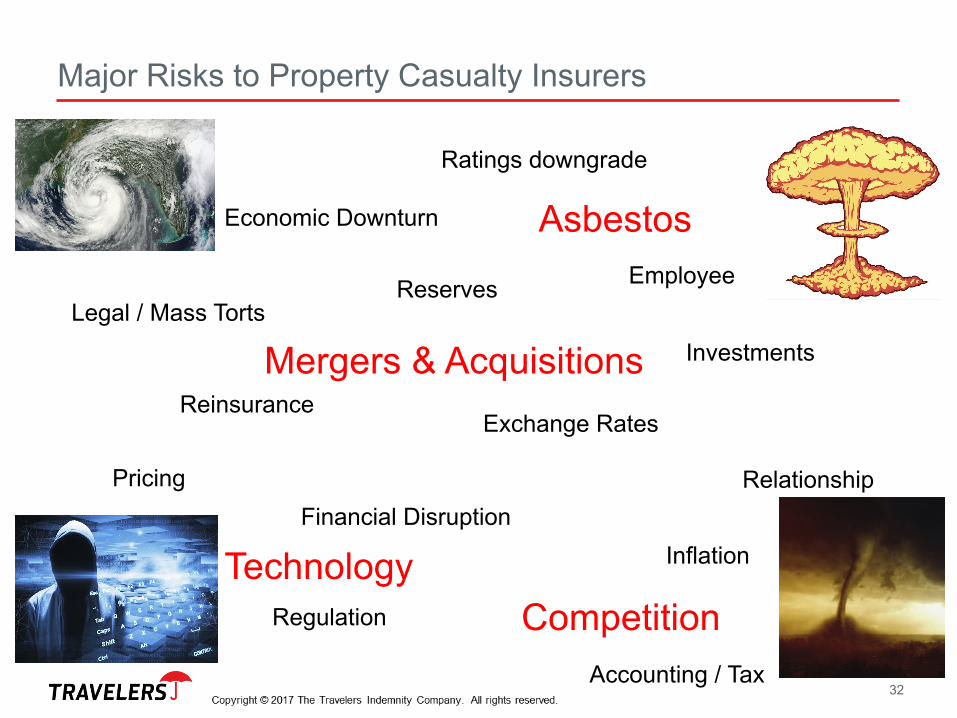

Major Risks to Property Casualty Insurers

32

Asbestos

Reinsurance

Reserves

Investments

Financial Disruption

Economic Downturn

Exchange Rates

Inflation

Legal / Mass Torts

Regulation Competition

Ratings downgrade

Technology

Relationship

Mergers & Acquisitions

Employee

Accounting / Tax

Pricing

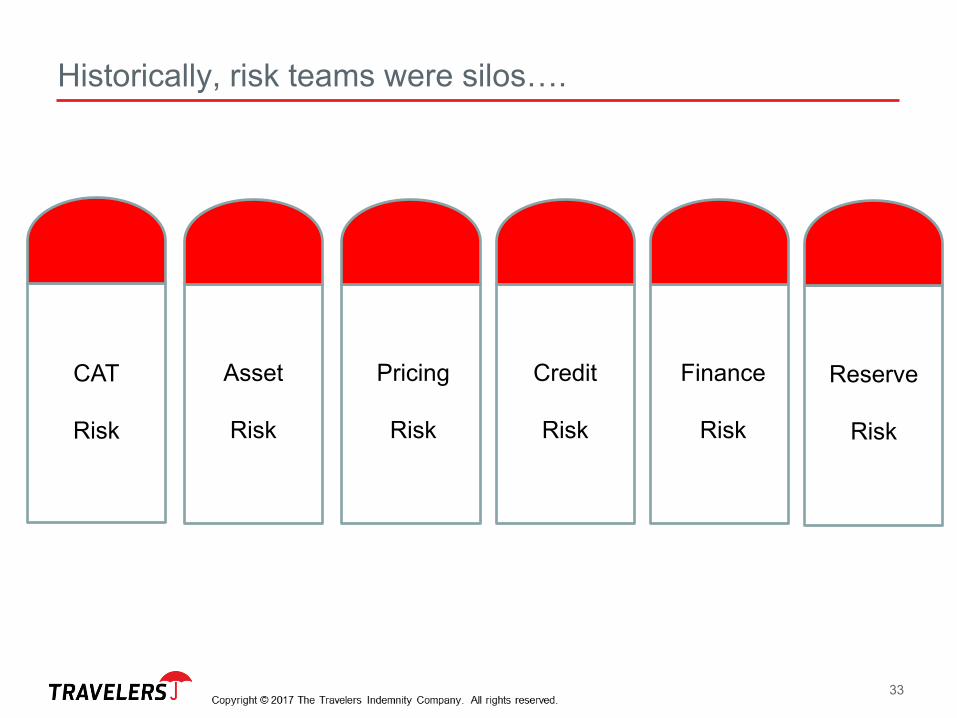

Historically, risk teams were silos….

33

CAT

Risk

Asset

Risk

Pricing

Risk

Credit

Risk

Finance

Risk

Reserve

Risk

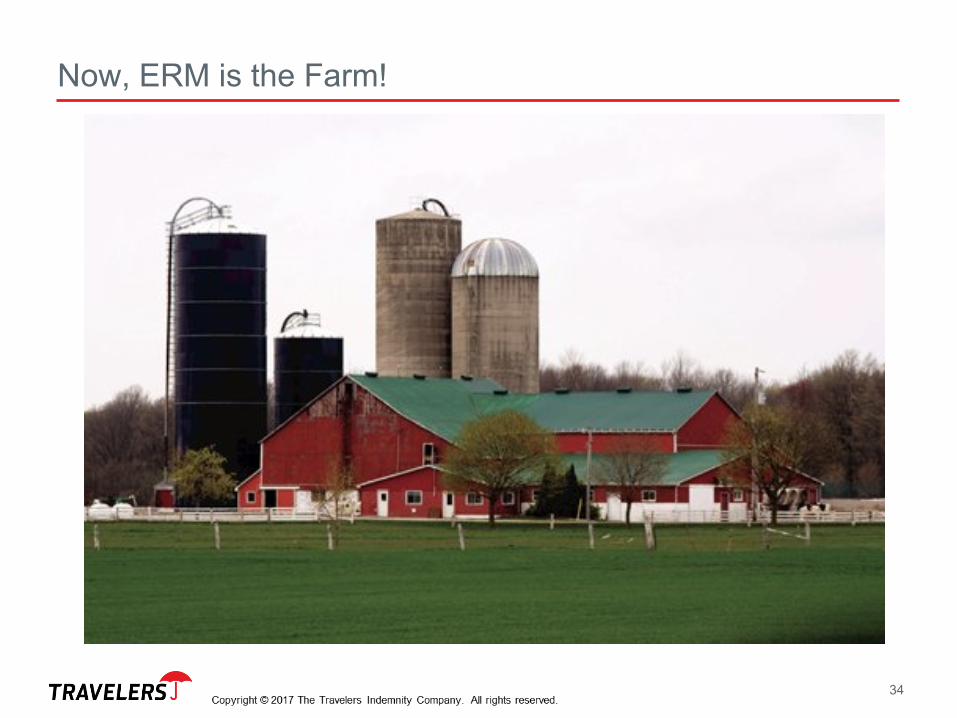

Now, ERM is the Farm!

34

35

Economic Capital Model (ECM) – Diversification

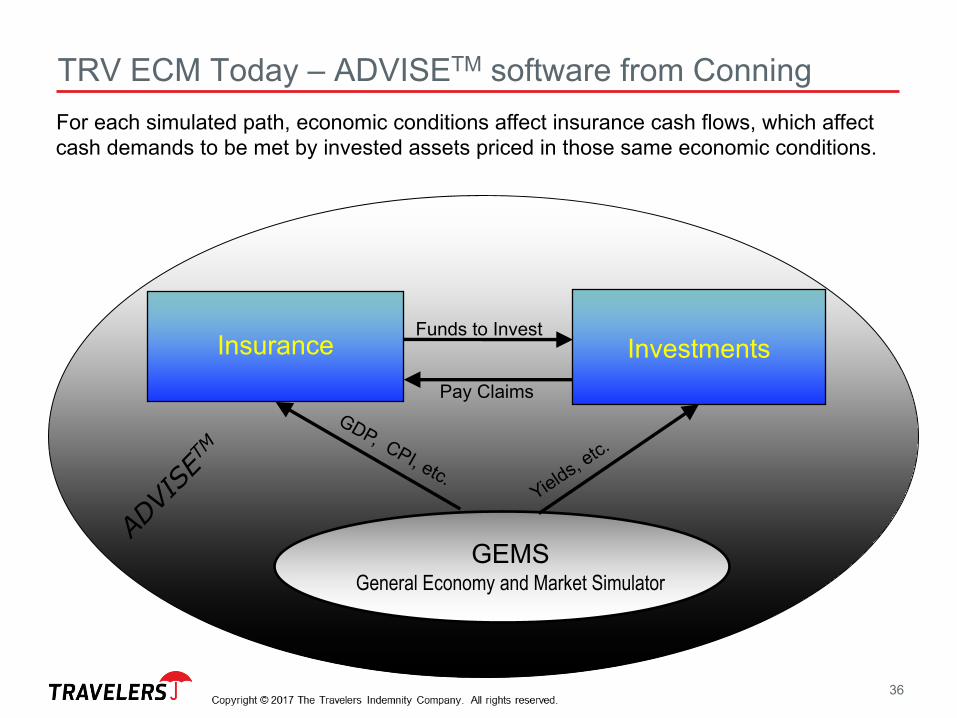

TRV ECM Today – ADVISETM software from ConningFor each simulated path, economic conditions affect insurance cash flows, which affect cash demands to be met by invested assets priced in those same economic conditions.

InvestmentsInsurance

GEMSGeneral Economy and Market Simulator

Funds to Invest

Pay Claims

36

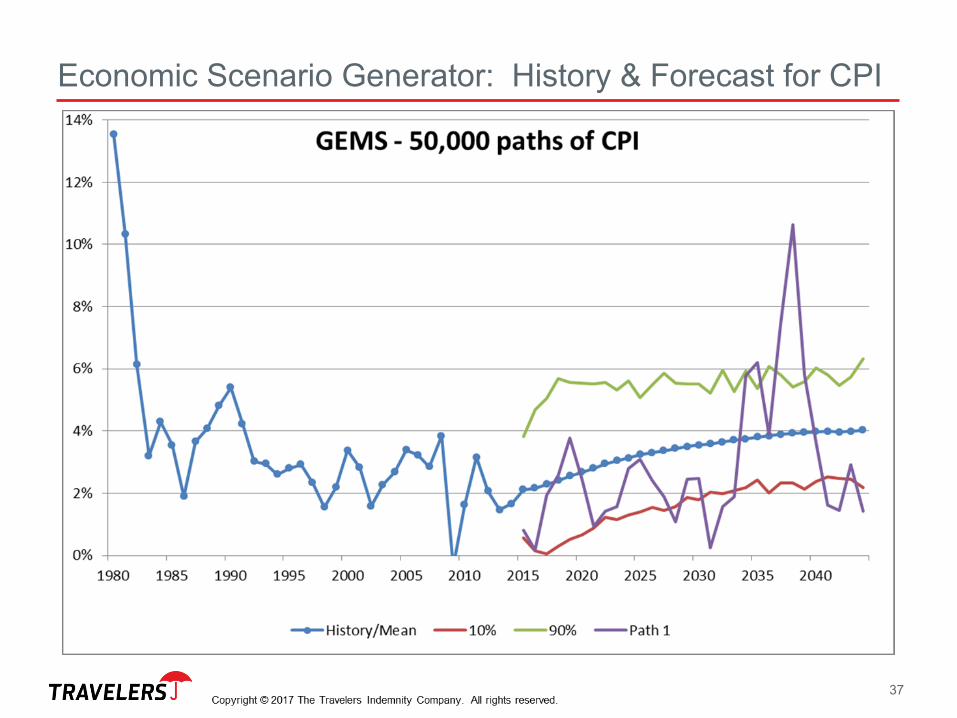

Economic Scenario Generator: History & Forecast for CPI

37

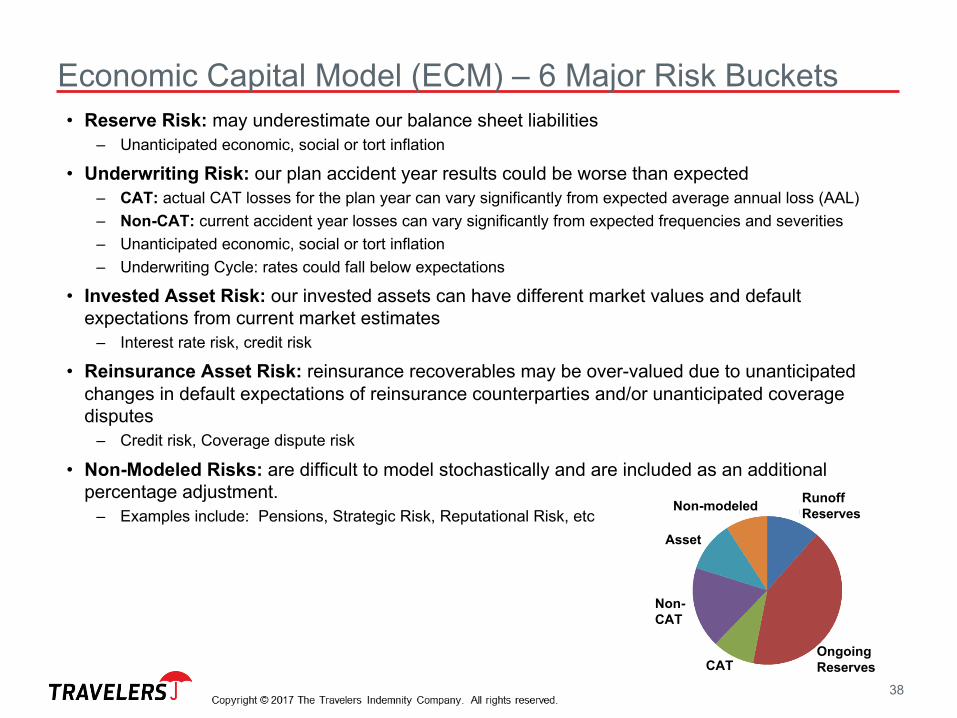

Economic Capital Model (ECM) – 6 Major Risk Buckets

OngoingReserves

RunoffReservesNon-modeled

Asset

Non-CAT

CAT

• Reserve Risk: may underestimate our balance sheet liabilities– Unanticipated economic, social or tort inflation

• Underwriting Risk: our plan accident year results could be worse than expected– CAT: actual CAT losses for the plan year can vary significantly from expected average annual loss (AAL)– Non-CAT: current accident year losses can vary significantly from expected frequencies and severities– Unanticipated economic, social or tort inflation– Underwriting Cycle: rates could fall below expectations

• Invested Asset Risk: our invested assets can have different market values and default expectations from current market estimates

– Interest rate risk, credit risk

• Reinsurance Asset Risk: reinsurance recoverables may be over-valued due to unanticipated changes in default expectations of reinsurance counterparties and/or unanticipated coverage disputes

– Credit risk, Coverage dispute risk

• Non-Modeled Risks: are difficult to model stochastically and are included as an additional percentage adjustment.

– Examples include: Pensions, Strategic Risk, Reputational Risk, etc

38

Travelers ECM - Reserve Risk

Loss Variability

Carried Reservesby Accident Year

Payout Patterns

Inflation Impacts

39

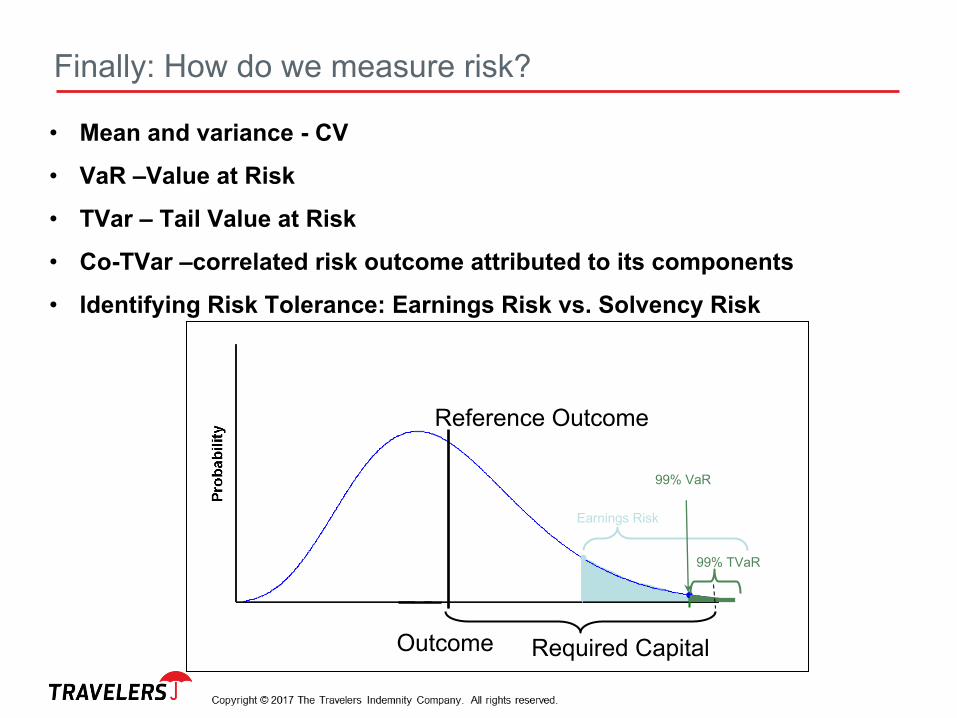

Finally: How do we measure risk?

• Mean and variance - CV

• VaR –Value at Risk

• TVar – Tail Value at Risk

• Co-TVar –correlated risk outcome attributed to its components

• Identifying Risk Tolerance: Earnings Risk vs. Solvency Risk

Required Capital

99% TVaR

Reference Outcome

99% VaR

Earnings Risk

Outcome

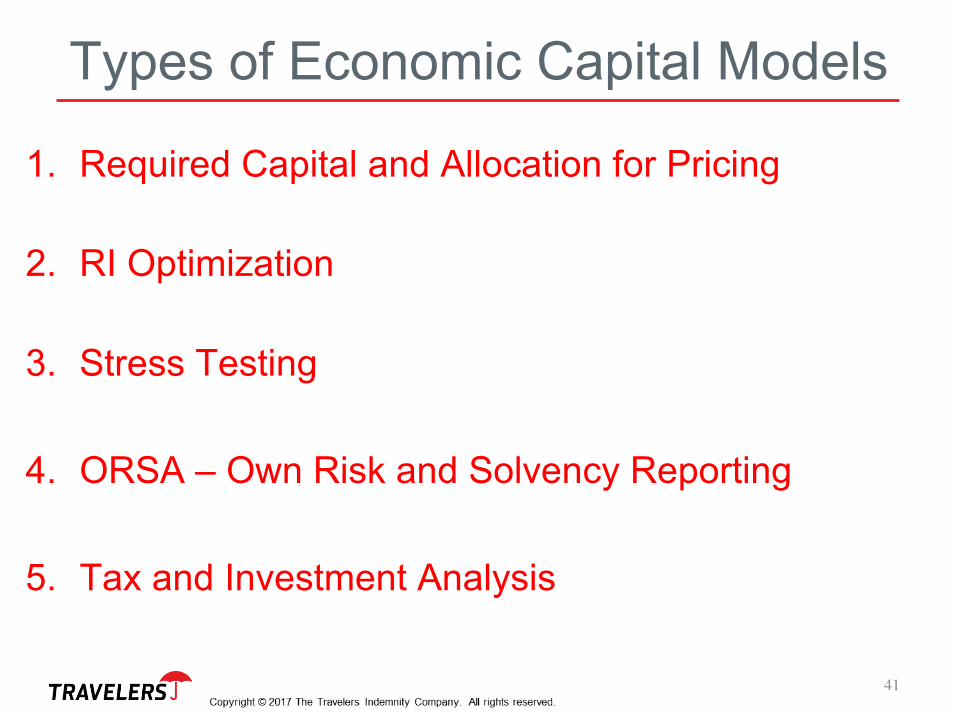

Types of Economic Capital Models

1. Required Capital and Allocation for Pricing

2. RI Optimization

3. Stress Testing

4. ORSA – Own Risk and Solvency Reporting

5. Tax and Investment Analysis

41

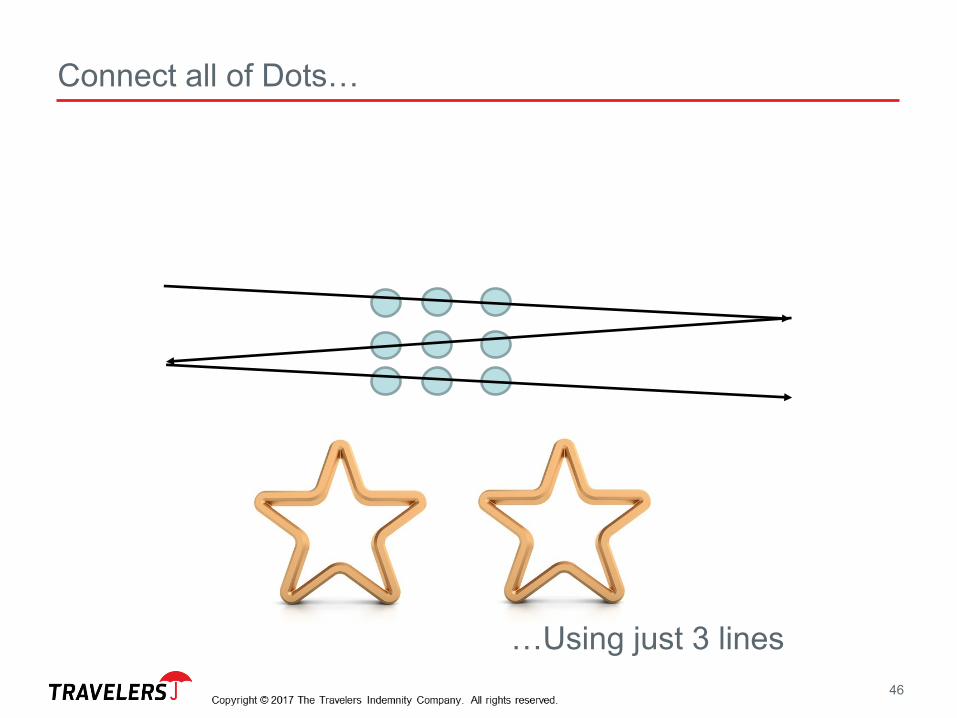

Puzzle“9dots”

42

Connect all of Dots…

43

…Using just 4 lines?

Connect all of Dots…

44

…Using just 4 lines or less

Connect all of Dots…

45

…Using just 3 lines?

Connect all of Dots…

46

…Using just 3 lines

Connect all of Dots…

47

…Using just 1 line!?!?

48

Think outside the box and Model Limitations

49

QA