Embed Size (px)

Citation preview

IAG and NRMA Superannuation Plan

Annual Reportfor the year ended 30 June 2004

IAG AND NRMA SUPERANNUATION PLAN ANNUAL REPORT 2004

Trustee: NRMA Staff Superannuation Pty Limited ACN 000 300 934Telephone: (02) 9282 8740 or ext. 28740

Level 13, 388 George Street Sydney NSW 2000

G010282.qxd 15/2/12 9:20 AM Page 2

IAG and NRMA Superannuation Plan

Issued by the Trustee: NRMA Staff Superannuation Pty Limited

For information regarding the Plan, contact:

Superannuation Administration

Insurance Australia Group Services Pty Limited ABN 38 008 435 201

Level 13

388 George Street

SYDNEY NSW 2000

ext. 28780 or (02) 9292 8780

The IAG and NRMA Superannuation Plan ("Plan") is governed by a legal document called the Trust Deed, including a set of

governing rules. The Trust Deed sets out your rights and responsibilities as a Plan member, and the rights and responsibilities

of your Employer and the Trustee. If there is any inconsistency between the Trust Deed and this Annual Report, the Trust

Deed will be the final authority.

In this report, a reference to 'your Employer' means any one of the following companies as appropriate:

Insurance Australia Group Limited and its subsidiaries (IAG)

National Roads and Motorists’ Association Limited and its subsidiaries (NRMA)

Intelematics Australia Pty Limited.

In this report, a reference to the ‘Plan’ is a reference to the sub-plan of your Employer. There are two sub-plans, namely:

The IAG sub-plan for employees and officers of companies in the Insurance Australia Group, and

The NRMA sub-plan for employees and officers of National Roads and Motorists’ Association and its related bodies

corporate, including Intelematics Australia Pty Limited.

This annual report relates to membership of the Plan. You are registered in the sub-plan relevant to your Employer. Where

the features of the sub-plans are different, those differences are disclosed in this annual report.

Generally, you belong to the accumulation section of the Plan if you joined your Employer after 1 October 1998, or if you

have elected to transfer to this section. Otherwise, you belong to the defined benefits section (which has been closed since 1

October 1998). Some members who transferred in from the SGIC Staff Superannuation Fund, the RACV Superannuation

Fund, the CGU Superannuation Fund or the CGU-VACC Pension Fund are also defined benefit members.

There are separate sections for investment performance for accumulation members and defined benefit members.

1 IAG AND NRMA SUPER

IAG AND NRMA SUPER1

*

)

G010282.qxd 15/2/12 9:20 AM Page 1

WORKING FOR YOUR FUTURE 2

If you need more information about the Plan…

Contact the Trustee or Superannuation Administration at the above address. There is no charge for this additional

information.

Be aware that the Trustee cannot provide you with any financial advice. For information and advice regarding superannuation

generally, the selection of an investment option(s) and insurance options, you should speak to a licensed financial adviser.

Additional information is available on request from Superannuation Administration:

the Plan’s Trust Deed and Rules

details of death, TPD and salary continuance benefits under the Plan

the Plan’s investment policy statement

extracts from actuarial reports

the latest audited Plan accounts

the Plan’s Privacy Policy Statement

the rules covering the appointment and removal of member-representative Trustee Directors, and

the Plan’s inquiries and complaints procedures.

The Plan has a process in place for dealing with enquiries and complaints. Additional dispute resolution is available

to members through the Superannuation Complaints Tribunal. For more information, see page 33.

G010282.qxd 15/2/12 9:20 AM Page 2

3 CONTENTS

CONTENTS3

Contents

A Message from the Trustee 4

The Operations of the Plan at a glance 5

Your Plan’s investment performance – accumulation members 7

Recent investment returns 7

Investment options in detail 8

Shares 8

Growth 9

Balanced 11

Conservative 12

Measuring performance 13

Comparing performance 14

Investment information for defined benefit members 15

Plan information for all members 17

Investment environment for year ended 30 June 2004 17

Investment environment in more detail 17

Investment strategy and objectives 19

How the Plan’s assets are managed 19

Large assets of the Plan 19

Use of derivatives 20

The year in review 21

Increased membership and assets 21

The Plan’s financial position 21

Sub-plan reporting 23

How your Plan is managed 24

Whats happening in super 30

More information 33

Questions 34

G010282.qxd 15/2/12 9:20 AM Page 3

WORKING FOR YOUR FUTURE 4

A message from the Trustee

Dear member

Investment returns for 2003/2004

The 2003-04 financial year was a much improved one for investors, with share markets around the world delivering strongreturns on the back of improved investor sentiment as a result of the global economic recovery. Both Australian and Overseasshare markets have rebounded strongly and delivered welcoming positive returns for the year.

Plan changes

There were some significant changes during the year as detailed in this report, including:

198 IMA employees transferred into the Plan as at 1 July 2003 from the RACV Superannuation Fund bringing with themtransfer values totalling $23.5M

Two Sub-Plans were established as at 1 December 2003

3,268 CGU employees and 176 pensioners transferred into the Plan as at 1 December 2003 from the CGUSuperannuation Fund and the CGU-VACC Pension Fund bringing with them transfer values totalling $256M

The Trustee reviewed the asset allocation of each investment option during the year. The Growth, Balanced, andConservative Options now include a specific exposure to Listed Property Trusts

The name of the Plan was changed to the IAG and NRMA Superannuation Plan

Total membership of the Plan now includes over 11,500 members and over 200 pensioners. Plan assets as at 30 June 2004were in excess of $825M.

Government legislation

The Financial Services Reform (FSR) Act became fully operational on 11 March 2004.

Members will notice that the Act requires more regular and more detailed communications from the Trustee.

The Government co-contribution scheme became operative during the year and the level of the co-contribution wasenhanced by the Government as at 1 July 2004.

Any questions?

If you have any questions about your benefits in the Plan, please call me on ext. 28740 or (02) 9292 8740. You can alsocontact any employee of Superannuation Administration (see inside back cover for contact details) or any of the TrusteeDirectors (see page 24).

Joe JanssenManager SuperannuationNRMA Staff Superannuation Pty Limited ACN 000 300 934

G010282.qxd 15/2/12 9:20 AM Page 4

The Operations of the Plan at a glance

This section provides a brief summary of the operations of the Plan during the year. Further details are set out later in the report.

Administration

The Trustee established two sub-plans in the Plan. One sub-plan is in respect of IAG employees and the other sub-plan is in

respect of the NRMA employees.

During the year, 3,466 members transferred into the Plan from the RACV Superannuation Fund, the CGU Superannuation Fund

and the CGU-VACC Pension Fund. In conjunction with the transferring members, the Plan received an amount of $280M from

the three funds.

As at 30 June 2004, the Plan held assets of $826M.

Asset allocations for all investment options were reviewed by the Trustee. As a result, the asset allocations for the Growth,

Balanced and Conservative Options were changed and a specific allocation to a Listed Property Trust was included in each of

these options.

Roger Bruce, Sam Mostyn and Peter Steele were appointed directors of the Trustee replacing Doug Pearce, David Bryant and

Kieran Hickey.

Investments

The following is a summary of the investment returns for the year as well as the average returns over recent years.

5 SUMMARY

SUMMARY5

Defined benefit (long term) members

Annual return for the year Average annul rate of returnended 30 June 2004 over the last 5 years

Credited to member accounts 2.7% 6.8%

Earned on plan assets 13.6% 5.5%

Investment Option Annual return for the year Average annul rate of returnended 30 June 2004 over the last 4 years

Shares 18.5% 2.0%

Growth 13.6% 3.2%

Balanced 10.4% 4.4%

Conservative 6.7% 6.1%

Accumulation members

G010282.qxd 15/2/12 9:20 AM Page 5

WORKING FOR YOUR FUTURE 6

The investment market generally performed much better than it did over the three previous years. This was largely due to the

strong performance in the following sectors:

Australian shares

Overseas shares

Listed Property Trusts

As part of the transfer of the assets from the CGU Superannuation Fund, the Trustee initially retained three of the investment

managers from that Fund. They are:

Maple-Brown Abbott Limited

Credit Suisse Asset Management Australia Limited

AMP Capital Investors Limited

Separately, Alliance Capital Australia Limited was appointed in September 2003 as an additional manager to invest part of the

overseas shares portfolio held in the World Equity Trust.

Government regulations

The Financial Services Reform Act became fully operational in March 2004.

The Government co-contribution scheme commenced on 1 July 2003 and was increased with effect from 1 July 2004.

The surcharge tax rates are reducing in three steps. The original maximum rate of surcharge tax was 15% and is reducing to

10% from 1 July 2005.

The Government has broadened the definition of “dependant” as it applies to the payment of superannuation benefits on

behalf of a deceased member.

The Government announced a new licensing regime whereby trustees are required to become licensed with APRA by

1 July 2006.

Credited to member accounts 13.6%

Defined benefit (CGU transferring) members

Annual return for the yearended 30 June 2004

G010282.qxd 15/2/12 9:20 AM Page 6

Your Plan’s investment performance – accumulation members

Information in this section applies to accumulation members of both sub-plans.

In this section you will find:

Recent investment performance

Overview of each investment option and returns

Measuring performance

Comparing performance

Recent investment returns

The following table shows the relevant earning rates for each investment option since the introduction of member investment

choice on 1 July 2000 and the average rate of net return for four years.

The annual effective rate of net earnings is the actual earning rate less associated taxes and investment expenses.

Investment earnings for an investment option may be positive or negative. The Trustee holds units in each investment option.

The value of the units depends on the performance of your chosen option/s. The price of these units will go up and down as

investment markets shift, affecting the value of your units and consequently the value of your investment.

As you can see from the comparison table above, the market has been volatile, displaying a sharp recovery after the poor

performances of recent years. It is important to be aware that investment returns from this short time frame may not be

indicative of the returns that may be received over the duration of your retirement planning. Time frames of five years or longer

will typically provide a more accurate indication of the overall long-term performance of an investment option.

It is important to understand that past performance, for each portfolio option, should not be relied upon as indicative of

future performance and does not guarantee such performance.

Each option bears a different level of risk, depending on the mix of asset classes that make up the portfolio. More information

about the associated risks and allocation of asset classes for each option are detailed on the following pages of this booklet.

7 INVESTMENT

INVESTMENT7

00-01 01-02 02-03 03-04 00-04

Shares 5.7 -9.2 -4.7 18.5 2.0

Growth 6.0 -5.1 -0.4 13.6 3.2

Balanced 6.5 -1.5 2.6 10.4 4.4

Conservative 7.0 3.5 7.4 6.7 6.1

*The options have been available since 1 July 2000, so the average rate of net return is quoted from this date.

Investment Effective rate of net earnings Average rate of net returnoption % p.a. for the four years since

1 July 2000* % p.a.

G010282.qxd 15/2/12 9:20 AM Page 7

WORKING FOR YOUR FUTURE 8

Your investment options in detail

In this section you’ll find out:

what your investment choices are

the recent investment performance of each option

performance benchmarks

how the investment options compare.

You choose how your super is invested. Choosing an investment option that suits your investment needs and timeframe

could make a big difference to the size of your payout.

Each of the Plan’s options has a specific investment objective and strategy set by the Trustee. Each option has a different risk profile

and the Trustee’s aim is to achieve the best possible returns relative to the level of risk associated with investing in that option.

Be aware that the investment returns for any option may be positive or negative, depending on volatility of investment

markets and the performance of the underlying asset classes.

The performance of each asset type is measured against a benchmark set by the Trustee, who evaluates this performance regularly.

If you do not make an investment choice, your super will be invested in the Growth Option, which is the Default Option.

Option 1 - Shares

Investment objective:

to achieve a high level of returns over the long term, by investing only in shares, which are high growth assets.

Strategy:

aims to invest 65% of assets in Australian shares, and 35% in overseas shares. By sharing the asset allocation, this portfolio is

not completely exposed to either Australian or overseas market forces, giving the advantage of some diversification.

Level of risk - high

Because shares are market driven investments which respond quickly to changes in market conditions, shares are highly

volatile and investors can expect performance to show periods of significantly high growth, as well as periods of poor or even

negative returns. Over a longer period of time, shares generally can be expected to produce higher returns than any other

asset class.

The performance of the Shares Option is measured against a benchmark portfolio, which consists of the target asset allocation

as shown below. Each asset class within the benchmark portfolio is assumed to earn investment returns based on an

appropriate index as shown in the table on page 13.

G010282.qxd 15/2/12 9:20 AM Page 8

9 INVESTMENT OPTIONS

INVESTMENT OPTIONS9

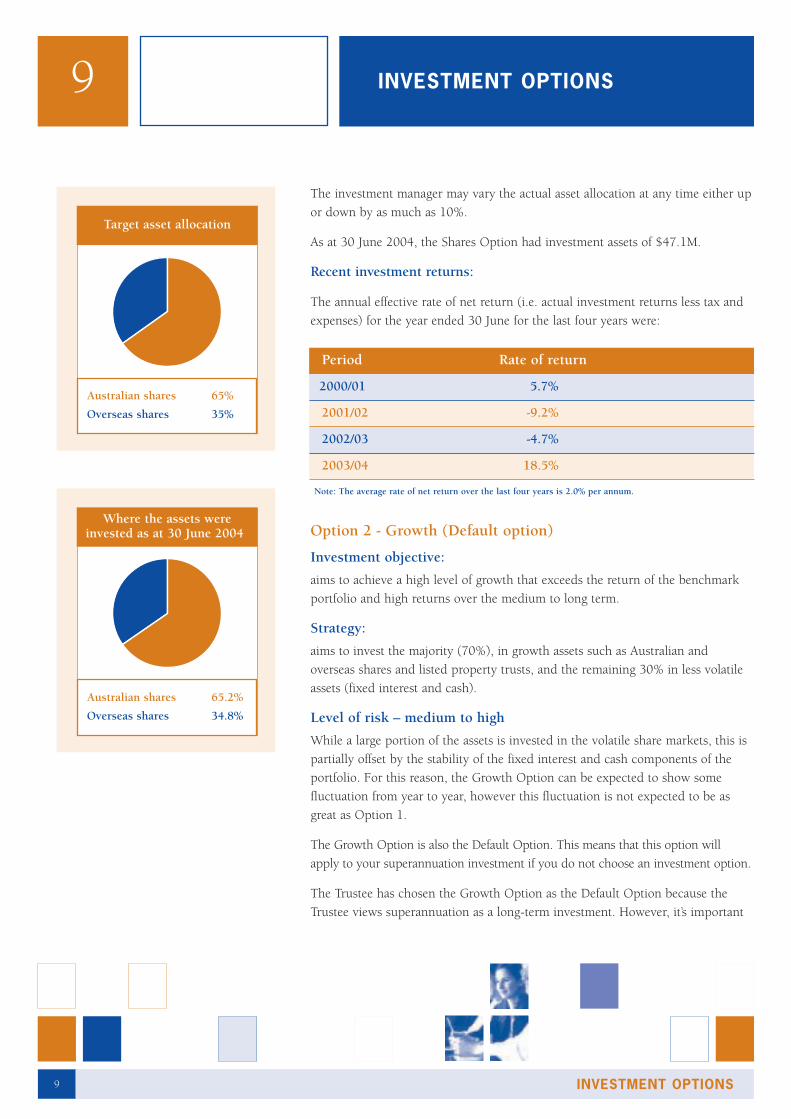

Australian shares 65.2%

Overseas shares 34.8%

Where the assets wereinvested as at 30 June 2004

Australian shares 65%

Overseas shares 35%

Target asset allocation

The investment manager may vary the actual asset allocation at any time either up

or down by as much as 10%.

As at 30 June 2004, the Shares Option had investment assets of $47.1M.

Recent investment returns:

The annual effective rate of net return (i.e. actual investment returns less tax and

expenses) for the year ended 30 June for the last four years were:

Option 2 - Growth (Default option)

Investment objective:

aims to achieve a high level of growth that exceeds the return of the benchmark

portfolio and high returns over the medium to long term.

Strategy:

aims to invest the majority (70%), in growth assets such as Australian and

overseas shares and listed property trusts, and the remaining 30% in less volatile

assets (fixed interest and cash).

Level of risk – medium to high

While a large portion of the assets is invested in the volatile share markets, this is

partially offset by the stability of the fixed interest and cash components of the

portfolio. For this reason, the Growth Option can be expected to show some

fluctuation from year to year, however this fluctuation is not expected to be as

great as Option 1.

The Growth Option is also the Default Option. This means that this option will

apply to your superannuation investment if you do not choose an investment option.

The Trustee has chosen the Growth Option as the Default Option because the

Trustee views superannuation as a long-term investment. However, it’s important

Period Rate of return

2000/01 5.7%

2001/02 -9.2%

2002/03 -4.7%

2003/04 18.5%

Note: The average rate of net return over the last four years is 2.0% per annum.

G010282.qxd 15/2/12 9:20 AM Page 9

WORKING FOR YOUR FUTURE 10

that you individually assess your own situation and retirement planning strategy

(for example, if you are near to retirement age), as the Default Option may not be

appropriate for you. You are encouraged to make your own choice between the

available options.

The performance of the Growth Option is measured against a benchmark

portfolio, which consists of the target asset allocation shown below. Each asset

class within the benchmark portfolio is assumed to earn investment returns based

on an appropriate index as shown in the table on page 13.

Please note that the target asset allocations of the Growth Option were changed in

two stages during the year, with 50% of the change being implemented from 1

December 2003 and the remainder in March 2004.

This change to the asset allocation for the Growth Option may have an impact on

future investment returns.

The investment manager may vary the actual asset allocation at any time either up or

down by as much as 10%. The allocation to cash may be as high as 20%

As at 30 June 2004, the Growth Option had investment assets of $686M (this

includes the assets in respect of defined benefit members as explained on page 15).

Recent investment returns:

The annual effective rate of net return (i.e. actual investment returns less tax and

expenses) for the year ended 30 June for the last four years were:

The average rate of net return over the last four years is 3.2% per annum.

The assets of the Plan in respect of defined benefit members form part of the

assets of this option.

Period Rate of return

2000/01 6.0%

2001/02 -5.1%

2002/03 -0.4%

2003/04 13.6%

Note: The average rate of net return over the last four years is 2.0% per annum.

Australian shares 35%

Overseas shares 25%

Listed property shares 10%

Fixed interest 25%

Cash 5%

Target asset allocation to 30 June 2004

Australian shares 35.1%

Overseas shares 25.1%

Listed property trusts 9.9%

Fixed interest 21.7%

Cash 8.2%%

Where the assets wereinvested as at 30 June 2004

G010282.qxd 15/2/12 9:20 AM Page 10

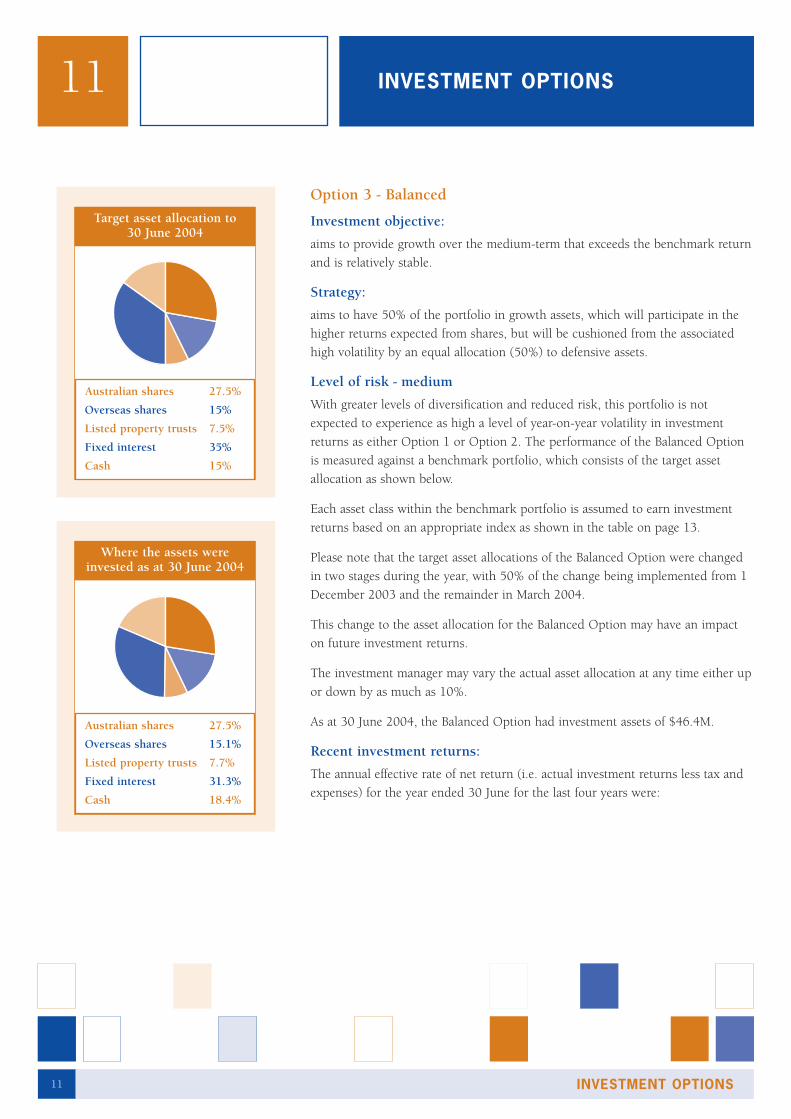

Option 3 - Balanced

Investment objective:

aims to provide growth over the medium-term that exceeds the benchmark return

and is relatively stable.

Strategy:

aims to have 50% of the portfolio in growth assets, which will participate in the

higher returns expected from shares, but will be cushioned from the associated

high volatility by an equal allocation (50%) to defensive assets.

Level of risk - medium

With greater levels of diversification and reduced risk, this portfolio is not

expected to experience as high a level of year-on-year volatility in investment

returns as either Option 1 or Option 2. The performance of the Balanced Option

is measured against a benchmark portfolio, which consists of the target asset

allocation as shown below.

Each asset class within the benchmark portfolio is assumed to earn investment

returns based on an appropriate index as shown in the table on page 13.

Please note that the target asset allocations of the Balanced Option were changed

in two stages during the year, with 50% of the change being implemented from 1

December 2003 and the remainder in March 2004.

This change to the asset allocation for the Balanced Option may have an impact

on future investment returns.

The investment manager may vary the actual asset allocation at any time either up

or down by as much as 10%.

As at 30 June 2004, the Balanced Option had investment assets of $46.4M.

Recent investment returns:

The annual effective rate of net return (i.e. actual investment returns less tax and

expenses) for the year ended 30 June for the last four years were:

11 INVESTMENT OPTIONS

INVESTMENT OPTIONS11

Australian shares 27.5%

Overseas shares 15.1%

Listed property trusts 7.7%

Fixed interest 31.3%

Cash 18.4%

Where the assets wereinvested as at 30 June 2004

Australian shares 27.5%

Overseas shares 15%

Listed property trusts 7.5%

Fixed interest 35%

Cash 15%

Target asset allocation to 30 June 2004

G010282.qxd 15/2/12 9:20 AM Page 11

WORKING FOR YOUR FUTURE 12

Option 4 - Conservative

Investment objective:

aims to achieve stable investment returns in the short to medium-term that

exceed the benchmark while keeping pace with the cost of living (inflation).

Strategy:

invests mainly in fixed interest, inflation linked bonds and cash, which are stable

investments producing a more predictable return that can be expected to be lower

than those of Options 1, 2 or 3 in the longer term. The growth component of this

portfolio is achieved by a relatively small investment in shares and property.

Level of risk – medium to low

Investment returns are expected to remain more stable in the short-term than

Options 1, 2 or 3.

The performance of the Conservative Option is measured against a benchmark

portfolio, which consists of the target asset allocation as shown below. Each asset

class within the benchmark portfolio is assumed to earn investment returns based

on an appropriate index as shown in the table on page 13.

Please note that the target asset allocations of the Conservative Option were

changed in two stages during the year, with 50% of the change being

implemented from 1 December 2003 and the remainder in March 2004.

This change to the asset allocation for the Conservative Option may have an

impact on future investment returns.

The investment manager may vary the actual asset allocation at any time either up

or down by as much as 10%.

As at 30 June 2004, the Conservative Option had investment assets of $41.8M.

Australian shares 10%

Overseas shares 10%

Listed property trusts 5%

Fixed Interest 45%

Cash 30%

Target asset allocation to 30 June 2004

Period Rate of return

2000/01 6.5%

2001/02 -1.5%

2003/04 10.4%

2002/03 2.6%

The average rate of net return over the last four years is 4.4% per annum.

Australian shares 10.3%

Overseas shares 10.2%

Listed property trusts 5.3%

Fixed Interest 41.1%

Cash 33.1%

Where the assets whereinvested as at 30 June 2004

G010282.qxd 15/2/12 9:20 AM Page 12

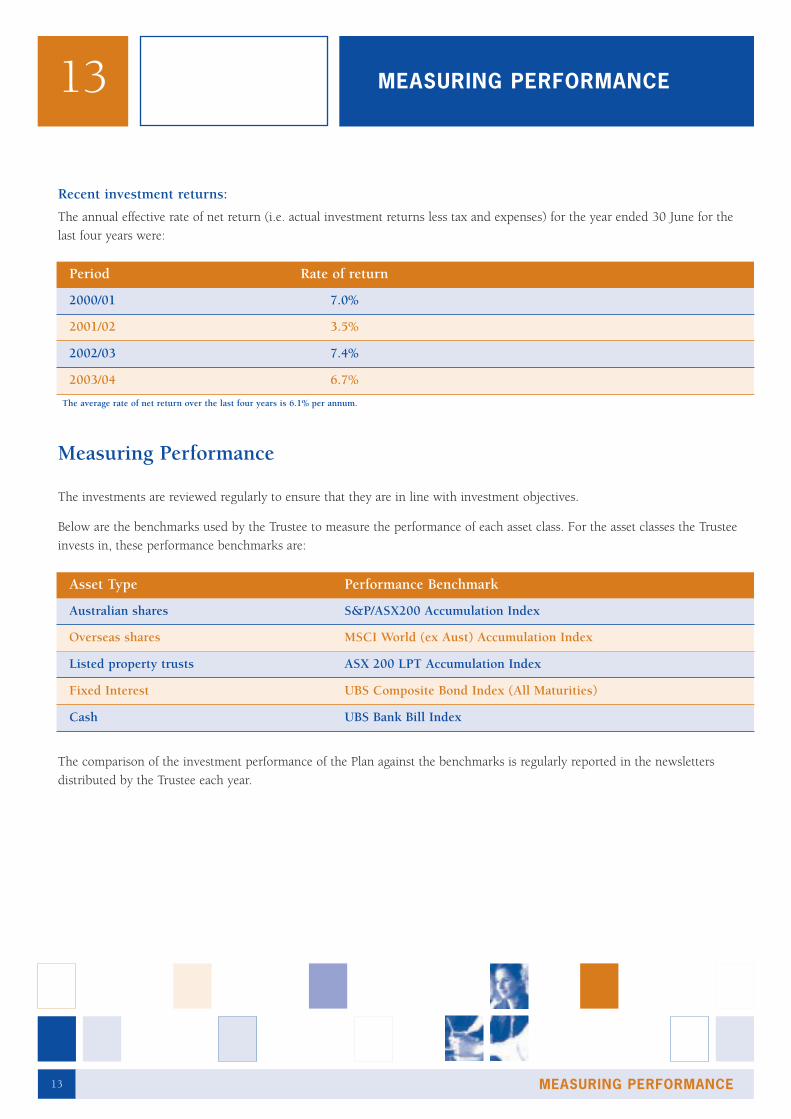

Recent investment returns:

The annual effective rate of net return (i.e. actual investment returns less tax and expenses) for the year ended 30 June for the

last four years were:

Measuring Performance

The investments are reviewed regularly to ensure that they are in line with investment objectives.

Below are the benchmarks used by the Trustee to measure the performance of each asset class. For the asset classes the Trustee

invests in, these performance benchmarks are:

The comparison of the investment performance of the Plan against the benchmarks is regularly reported in the newsletters

distributed by the Trustee each year.

13 MEASURING PERFORMANCE

MEASURING PERFORMANCE13

Asset Type Performance Benchmark

Australian shares S&P/ASX200 Accumulation Index

Overseas shares MSCI World (ex Aust) Accumulation Index

Fixed Interest UBS Composite Bond Index (All Maturities)

Cash UBS Bank Bill Index

Listed property trusts ASX 200 LPT Accumulation Index

Period Rate of return

2000/01 7.0%

2001/02 3.5%

2003/04 6.7%

2002/03 7.4%

The average rate of net return over the last four years is 6.1% per annum.

G010282.qxd 15/2/12 9:20 AM Page 13

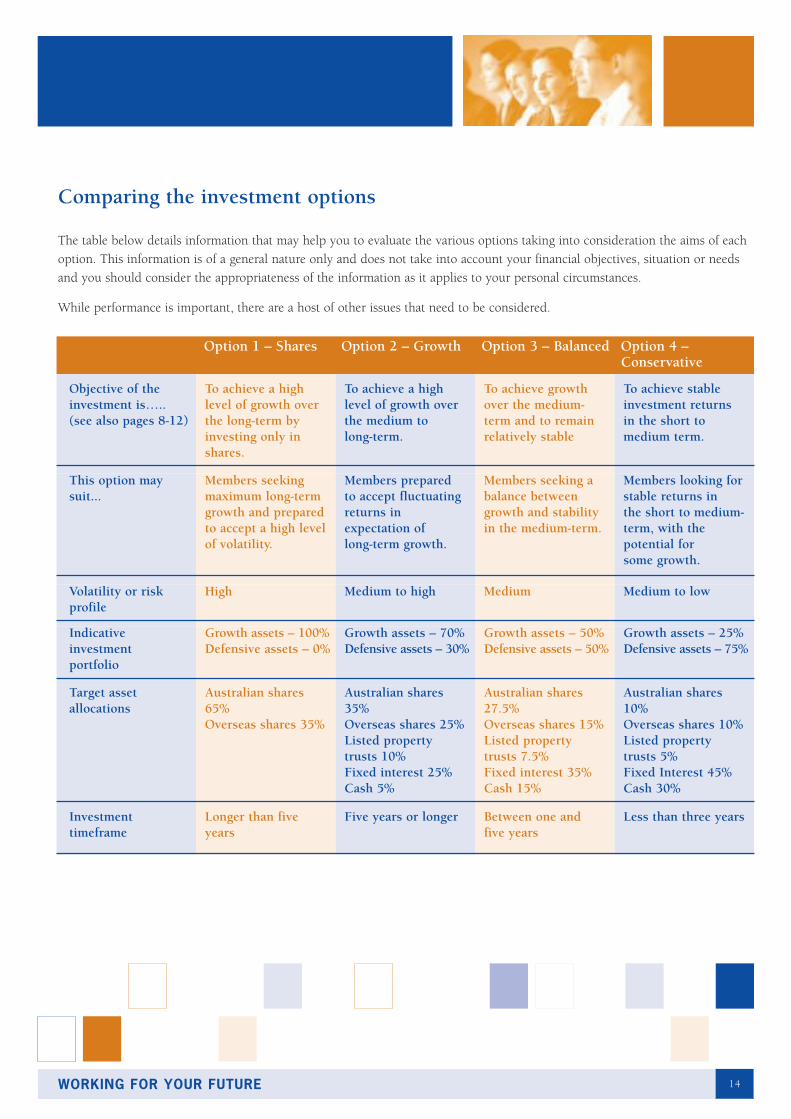

Comparing the investment options

The table below details information that may help you to evaluate the various options taking into consideration the aims of each

option. This information is of a general nature only and does not take into account your financial objectives, situation or needs

and you should consider the appropriateness of the information as it applies to your personal circumstances.

While performance is important, there are a host of other issues that need to be considered.

WORKING FOR YOUR FUTURE 14

Option 1 – Shares Option 2 – Growth Option 3 – Balanced Option 4 – Conservative

Objective of theinvestment is…..(see also pages 8-12)

To achieve a highlevel of growth overthe long-term byinvesting only inshares.

To achieve a highlevel of growth overthe medium to long-term.

To achieve growthover the medium-term and to remainrelatively stable

To achieve stableinvestment returns in the short tomedium term.

This option maysuit...

Members seekingmaximum long-termgrowth and preparedto accept a high levelof volatility.

Members prepared to accept fluctuatingreturns inexpectation of long-term growth.

Members seeking abalance betweengrowth and stabilityin the medium-term.

Members looking forstable returns in the short to medium-term, with thepotential for some growth.

Volatility or riskprofile

High Medium to high Medium Medium to low

Indicativeinvestment portfolio

Growth assets – 100%Defensive assets – 0%

Growth assets – 70%Defensive assets – 30%

Growth assets – 50%Defensive assets – 50%

Growth assets – 25%Defensive assets – 75%

Target assetallocations

Australian shares65%Overseas shares 35%

Australian shares 35%Overseas shares 25%Listed property trusts 10%Fixed interest 25%Cash 5%

Australian shares27.5%Overseas shares 15%Listed property trusts 7.5%Fixed interest 35%Cash 15%

Australian shares10%Overseas shares 10%Listed property trusts 5%Fixed Interest 45%Cash 30%

Investmenttimeframe

Longer than fiveyears

Five years or longer Between one and five years

Less than three years

G010282.qxd 15/2/12 9:20 AM Page 14

15 INVESTMENT FOR DEFINED BENEFITS

INVESTMENT FOR DEFINED BENEFITS15

Investment information for defined benefit members

Information in this section applies to you if you’re a member of the defined benefit section.

Benefits payable if you resign or become redundant prior to age 55 are based on your accumulated balances in the Plan.

Accumulation balances of defined benefit members were credited with an earning rate of 2.7% per annum for the year ended

30 June 2004. This is equal to the average effective rate of return over the last three years.

As at 30 June 2000, the declared rate was the same as the effective rate. In 1999 and earlier years, the declared earning rate

was equal to the average effective rate of return over the previous five years rather than three years.

Comparison of annual effective rates of net return and declared rates 2000 – 2004.

The Plan’s annual effective rate of net investment returns (i.e. actual investment returns less tax and expenses) and declared

earning rates since 2000 are as follows:

The average declared earning rate for defined benefit members over the five years to 30 June 2004 was 6.8% per annum.

The average effective net rate of return for defined benefit members over the past five years was 5.5% per annum.

For defined benefit members who transferred from the CGU Superannuation Fund or the CGU-VACC Pension Fund, the

Trustee is currently using a declared earning rate that is equal to the net investment return. As at 30 June 2004, this was

13.6%.

Further details of the investment performance, investment objectives and strategy of this option are set out on page 9

under the Growth Option of accumulation members.

Defined benefit members leaving during the year

For defined benefit members leaving the Plan during the year, before a final earning rate is available, benefits are calculated

using an interim earning rate. The Trustee reviews interim rates each quarter. The interim rates are partly based on the recent

actual investment performance and partly on an assumed earnings rate based on the ten year Government Bond Rate (less a

10% allowance for tax) as explained below.

Year ened 30 June Effective rate of return % p.a. Declared earning rate % p.a.

2000 15.0 15.0

2001 6.0 11.5

2003 -0.4 0.2

2004 13.6 2.7

2002 -5.1 5.3

Note: Past performance is not an indication of future performance

G010282.qxd 15/2/12 9:20 AM Page 15

The interim earning rate applying from 1 July 2004 is based on:

the actual investment performance for the two year period from 1 July 2002 to 30 June 2004, and

an assumed earnings rate for the one year to 30 June 2005.

After the end of the September 2004 quarter, the Trustee re-calculates the interim rate based on:

the actual investment performance for the two years and three months period to 30 September 2004, and

an assumed earnings rate for the nine months to 30 June 2005.

and so on for each subsequent quarter. For the year ending 30 June 2004, the interim earning rates were calculated on a

similar basis.

For defined benefit members who transferred from the CGU Superannuation Fund or the CGU-VACC Pension Fund, the initial

interim rate is 5.3% which is based on the Government Bond Rate as above. The interim rate will be updated on a quarterly

basis as above by using the actual investment return for the previous quarter.

WORKING FOR YOUR FUTURE 16

G010282.qxd 15/2/12 9:20 AM Page 16

Plan information for all members

This section applies to all members and potential members of the Plan.

In this section you will find:

an overview on the investment environment for the year ended 30 June 2004

investment strategy and objectives

how Plan assets are managed

use of derivatives

Investment environment for year ended 30 June 2004

The 2003/04 financial year began with confirmation that a recovery was underway as a result of positive economic data out

of the US which in turn had a positive influence on Europe and Japan.

The first half of 2004 showed a temporary slowdown both in Australia and overseas.

However, in the closing quarter to the financial year, the economic recovery in the US gained momentum with strong

employment numbers and robust business investment beginning to exert pressure on inflation.

In Australia, economic growth remained strong, but recent signs of moderating growth have emerged. Late in the year the

unemployment rate fell to a 23 year low of 5.5%. Housing finance figures have stabilised and while still indicating strong

credit growth, residential auction clearance rates are at their lowest levels for at least a decade.

The Australian equity market hit record highs in June due to the exceptionally robust earnings picture.

The market recovery this year re-enforces the volatility inherent in higher-risk investments such as shares. It’s very important

to remember that your super is a long-term investment, especially if you’re not retiring for many years.

If you are a defined benefit member, ie your benefits are worked out using a formula, the improved investment returns will

only affect some of your benefits. Check your benefit statement or check with your super contact for details.

The investment environment in more detail

Australian shares - S&P/ASX 200 Accumulation Index (up 21.6% for 12 months to 30 June 2004)

A strong Australian economy produced good growth during the 2003/ 2004 financial year.

The Australian sharemarket slightly outperformed international sharemarkets which returned 19.4% in Australian dollar

terms. This year has been the first positive performing year in the past three years for Australian equities. In terms of

industries, the best returns came from IT, energy and the materials sectors with poorer results from utilities and the financial

sector (excluding property). The Reserve Bank lifted interest rates by a quarter of a percent in both November and December

2003 in response to the strengthening economy.

17 INVESTMENT ENVIRONMENT

INVESTMENT ENVIRONMENT17

G010282.qxd 15/2/12 9:20 AM Page 17

Overseas shares - MSCI World (ex-Australia) Index (in A$) (up 19.4% for 12 months to 30 June 2004)

During the year, fluctuations of the Australian dollar created widespread concern for investors with international equity

portfolios that were unhedged (against currency movements). However, by year end, the outperformance of the hedged

portfolios had been pared back to only a 0.8% differential. The Australian dollar ended the financial year on US$0.70.

The 2003/04 financial year began quite positively. Encouraging economic news and a better-than-expected reporting season

indicated a US-led global recovery. The economic picture in Europe was mixed, while some early GDP figures out of Japan were

positive.

Over the second half of the financial year, the performance of world sharemarkets (in Australian dollar terms) was reasonably flat

due to the depreciation of the Australian dollar over that period. The depreciation of the Australian dollar came as fears that an

economic slowdown in China would dampen both commodity prices and economic growth in the region.

Sector returns were varied, although the majority of sectors managed positive returns for the June quarter. Energy (up 6.5%),

Industrial (up 4.9%) and Health Care (up 2.8%) were particularly strong. Financials (down 1.7%) and Telecoms (down 2.4%)

underperformed the market as a whole.

Listed Property Trusts – S&P/ASX 200 Property Accumulation Index (up 17.2% for 12 months to 30 June 2004)

Listed property also recorded impressive yearly returns. The 2003/04 financial year was largely split into two key themes: the

appreciation of the $A in the first half and ongoing sector consolidation in the second half.

Corporate activity, particularly the announcement of the combining of the three Westfield entities, helped drive this result.

The announcement by Lend Lease of its intentions to merge with General Property Trust was a further contributor to strong

capital growth.

The top performing sectors over the financial year were the Retail (24.5%) and Hotels (24.4%) sectors, while the Commercial

(5.9%) and Industrial (14.3%) sectors underperformed.

Australian fixed interest - UBS Composite Bond Index (All Maturities) (up 2.3% for 12 months to 30 June 2004)

The Reserve Bank of Australia lifted interest rates by 0.25% twice in the first six months of 2003/2004 financial year which

dampened returns from the Australian fixed interest market.

Investment performance comparison

The Plan’s investment performance is regularly monitored against that of its peers. In the Intech* survey as at 30 June 2004, the

Plan’s five year average effective rate of net return for the Growth Option was 5.03%, against the peer group average of 5.02%.

The investment policy for the Growth Option is similar to that used historically by the Plan. Market comparisons for the other

investment options are not provided by Intech.

*Intech Market-linked Pooled Funds Performance Survey

WORKING FOR YOUR FUTURE 18

G010282.qxd 15/2/12 9:20 AM Page 18

Investment strategy and objectives

Although the Plan offers member investment choice for accumulation members, the Trustee retains overall responsibility for

the investment of the assets of the various options in line with their specific investment objectives. However, accumulation

members are responsible for choosing the investment option/s that suit their individual needs and preferences and strike the

right balance between risk and return.

How Plan assets are managed

The assets of the Plan are managed by IAG Asset Management Limited ABN 94 054 552 046 (IAGAM). IAGAM may invest in

securities such as Australian and overseas shares, listed property trusts, fixed interest securities, cash and short-term securities

or any other investments authorised by the Trustee. This can be done directly or through trusts.

Most of the Plan’s assets invested in Australia are managed by investment professionals of IAGAM. As at 30 June 2004, a

small portion of the Australian company share portfolio was managed by Maple-Brown Abbott Limited ABN 73 001 208 564

and Credit Suisse Asset Management Australia Limited ABN 57 007 305 384 and a portion of the property investment

portfolio was managed by AMP Capital Investors Limited ABN 59 001 777 591. Since 1 July 2004, the AMP property

portfolio has been redeemed.

Fixed interest securities and Cash are invested in a fixed interest and cash management trust respectively, which are both

managed by IAGAM.

Overseas investments are managed within the World Equity Trust (WET) established by IAGAM. WET uses the investment

services of specialist external managers: these managers are:

Wellington Management Company (an actively managed portfolio)

State Street Global Index Plus Fund (which invests in line with the World Index)

Alliance Capital Australia Limited (an additional active manager appointed with effect from 1 September 2003).

The WET investment structure enables the Plan to diversify its international investments by using the expertise of a number

of managers with different strategies. This arrangement provides greater diversity and flexibility for entry into and exit from

the international markets. The overseas investments of the Plan are invested on an unhedged basis.

The Plan has a small private equity portfolio that is managed by Horsley Bridge Partners.

IAGAM monitors the activities and performance of all the external managers on behalf of the Trustee.

Large assets of the Plan

Fixed interest securities guaranteed by the Commonwealth or State Governments as at 30 June 2004 were the only

investments in excess of 5% of the Plan assets. The WET, Fixed Interest Trust and Cash Management Trust, all managed by

IAGAM, each hold more than 5% of the Plan’s assets.

19 INVESTMENT MANAGEMENT

INVESTMENT MANAGEMENT19

G010282.qxd 15/2/12 9:20 AM Page 19

Use of derivatives

Derivatives are special contracts — e.g. futures and forward exchange rate agreements—which can be used to manage the risk of

changes in the future value of investments.

The investment manager is permitted to use derivatives in the management of the Plan assets. These instruments are typically

used for the following purposes:

hedging; that is to protect against adverse changes in the market value of assets

to obtain prices that may not be available if assets are bought directly

to reduce the costs of buying and selling assets directly

to change the term of a fixed interest security

to manage cash flows efficiently

to manage asset weighting for the different asset classes.

Derivatives may not be used for speculative purposes.

The Plan held derivatives during the year ended 30 June 2004 in respect of its Australian shares, overseas shares and fixed

interest investments. The Plan’s exposure to derivatives is limited to 20% of the market value of the Plan. Within each asset class,

exposure to derivatives is limited to 20% of the market value of the asset class.

The investment manager reports to the Trustee regularly on the use of derivatives.

The derivative charge ratio of the Plan did not exceed 5% at any time during the year. The derivative charge ratio is the

percentage of the total market value of assets of the Plan (excluding cash) that the Trustee has charged as security for derivative

investments made by the Trustee.

WORKING FOR YOUR FUTURE 20

G010282.qxd 15/2/12 9:20 AM Page 20

The year in review

Increased membership and assets

During the year the following members and assets were transferred into the Plan.

As at 1 July 2003, 198 IMA employees transferred from the RACV Superannuation Fund into the Plan. In conjunction with

this transfer, the Trustee received a transfer value from the RACV Fund of $23.5M.

As at 1 December 2003, the Trustee agreed with the trustees of the CGU Superannuation Fund and the CGU-VACC Pension

Fund to transfer all members and assets of both funds into the Plan on a “successor fund” transfer basis. This involved the

following transfer;

In addition to these transfers, the Trustee processed and paid the termination benefits for another 148 members as their

benefits had not been processed by the previous fund as at 1 December 2003.

The Plan’s financial position

The actuary has advised that the Plan has continued to be in a sound financial position. After each review of the financial

position of the Plan, the actuary advises the amount of contributions that all Employers need to make to the Plan. For the

year ended 30 June 2004, in accordance with the actuary’s advice, the only Employer contributions made to the Plan were

made by IMA on behalf of the members who transferred from the RACV Fund.

A summary of the Plan’s audited accounts for the 2003 and 2004 years is shown below. Copies of the audited accounts and

the auditor’s report are available by contacting Superannuation Administration – see the back page for contact details.

21 PLAN ACCOUNTS

PLAN ACCOUNTS21

Fund Assets Members Pensioners

CGU Superannuation Fund $234M 2,918 172

CGU-VACC Pension Fund $22M 350 4

G010282.qxd 15/2/12 9:20 AM Page 21

WORKING FOR YOUR FUTURE 22

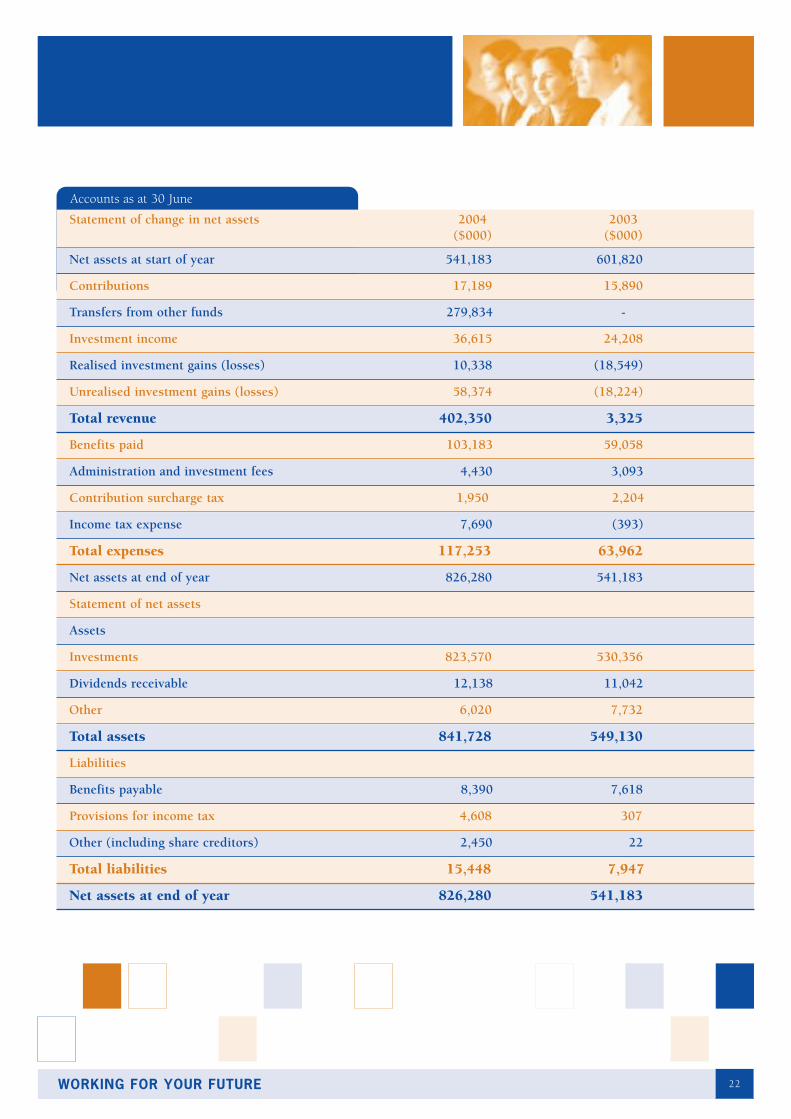

Statement of change in net assets 2004 2003($000) ($000)

Net assets at start of year 541,183 601,820

Contributions 17,189 15,890

Transfers from other funds 279,834 -

Investment income 36,615 24,208

Realised investment gains (losses) 10,338 (18,549)

Unrealised investment gains (losses) 58,374 (18,224)

Total revenue 402,350 3,325

Benefits paid 103,183 59,058

Administration and investment fees 4,430 3,093

Contribution surcharge tax 1,950 2,204

Income tax expense 7,690 (393)

Total expenses 117,253 63,962

Net assets at end of year 826,280 541,183

Statement of net assets

Assets

Investments 823,570 530,356

Dividends receivable 12,138 11,042

Other 6,020 7,732

Total assets 841,728 549,130

Liabilities

Benefits payable 8,390 7,618

Provisions for income tax 4,608 307

Other (including share creditors) 2,450 22

Total liabilities 15,448 7,947

Net assets at end of year 826,280 541,183

Accounts as at 30 June

G010282.qxd 15/2/12 9:20 AM Page 22

Sub-Plan reporting

In accordance with the Plan’s Trust Deed, from 1 December 2003, the Plan has been administered as two Sub-Plans, the IAG

Sub-Plan and the NRMA Sub-Plan.

The following secondary sub-plan report, has been prepared for the period from 1 December 2003 to 30 June 2004.

In accordance with the Plan’s trust deed, the actuary to the Plan partitioned all net assets and benefits as at 1 December 2003.

23 PLAN ACCOUNTS

PLAN ACCOUNTS23

IAG Sub-Plan NRMA Sub-Plan7 months to 30 June 2004 7 months to 30 June 2004

$000 $000

Net assets available to pay benefits at the beginning of the period 1 December 2003 406,491 146,409

Contributions 9,760 584

Transfers from other funds 256,372 -

Investment income 21,628 6,871

Realised and unrealised investment gain 45,312 10,220

Total revenue 333,072 17,675

Benefits paid 54,107 11,769

Administration andinvestment expenses 2,630 251

Contribution surcharge tax 1,494 127

Income tax expense 5,716 1,273

Total expenses 63,947 13,420

Net assets of at the end of the year 675,616 150,664

Statement of net assets

Investments 673,793 149,777

Dividends receivable 9,892 2,246

Other 5,001 1,019

Total assets 688,686 153,042

Liabilities

Benefits payable 7,297 1,093

Provisions for income tax 3,768 840

Other (including share creditors) 2,005 445

Total liabilities 13,070 2,378

Net assets at end of year 675,616 150,664

G010282.qxd 15/2/12 9:20 AM Page 23

How your Plan is managed

Changes to the administration of the Plan

As at 1 December 2003, the Trustee implemented two changes regarding the administration of the Plan;

The name of the Plan was changed to IAG and NRMA Superannuation Plan.

Two Sub-Plans were established within the Plan. One Sub-Plan is for the employees and beneficiaries of IAG and its related

companies. The other Sub-Plan is for the employees and beneficiaries of NRMA and its related companies. Presently, the

level of benefits provided in each Sub-Plan is the same*. However, it is possible that this may vary in future years. You will

be advised if this occurs.

* other than specific arrangements for those members who have transferred from another fund.

The Trustee

The Plan is set up as a trust and is governed by a legal document called the Trust Deed. A Trustee company - NRMA Staff

Superannuation Pty Limited (ACN 000 300 934) manages the Plan.

The Trustee company has nine directors, two of whom are appointed by Insurance Australia Group Limited; two are appointed

by National Roads and Motorists’ Association Limited and four are elected by members of the Plan for a period of three years

and there is one independent director who is appointed by the other Trustee directors.

The directors of the Trustee company as at 30 June 2004 were:

Independent director

Susan Ryan President – Australia Institute of Superannuation Trustees

Company-appointed directors

Ian Brown Deputy Chief Executive Officer – IAG

Roger Bruce General Manager People and Performance - NRMA

Sam Mostyn Group Executive Culture and Reputation - IAG

Peter Steele General Manager Corporate Services and Deputy CEO - NRMA

Member elected directors:

Pam Bardsley Company Secretary - NRMA

Joe Gonzalez Head of Client Advisory Services - IAGAM

Jon Street Road Service Patrol – NRMA

Peter Swan Head of IAG Compulsory Third Party Insurance

WORKING FOR YOUR FUTURE 24

G010282.qxd 15/2/12 9:20 AM Page 24

Director changes during the year

Doug Pearce resigned as a Company-appointed director on 6 February 2004, Kieran Hickey resigned on 9 February 2004

and David Bryant on 11 February 2004. Sam Mostyn was appointed a Company-appointed director on 18 February 2004,

Peter Steele on 19 February and Roger Bruce on 27 February 2004.

A chance to have your say

As member elected directors are elected by the members of the Plan, you get the chance to nominate and vote for

representatives on the Trustee Board. The Plan has a specific set of rules applying to the appointment and removal of member

elected directors and the filling of casual vacancies.

At the time of the next election, due in early 2005, you’ll receive full details on the appointment and removal of member

elected directors. You can also request a set of the election rules from Superannuation Administration at any time.

Indemnity insurance

The Trustee and its directors may be reimbursed and indemnified out of the Plan for all liabilities which they properly incur

in administering the Plan as a result of an ‘honest mistake’.

To protect the assets of the Plan against certain losses arising from the conduct of the Trustee and its directors and

administrators, the Trustee has taken out trustee indemnity insurance cover.

Trust Deed

The Trust Deed may be amended from time to time.

During the year, the Trustee approved the following changes to the Plan:

Provision for the Plan to be split into two sub-plans

Provision for a change of name for the Plan

Provision for a framework to administer the splitting of member benefits with their previous spouse in accordance with

the Family Law Act. These include separate provisions for accumulation members, defined benefit members and defined

benefit pension members

Provisions for members who transferred from the RACV Superannuation Fund as at 1 July 2003. In particular, the Trust

Deed sets out the benefits for the defined benefit members who transferred from the RACV Fund

Provision for members who transferred from the CGU Superannuation Fund as at 1 December 2003. In particular, the

Trust Deed sets out the benefits for the defined benefit members who transferred from the CGU Fund

Provisions for members who transferred from the CGU-VACC Pension Fund as at 1 December 2003. In particular, the

Trust Deed sets out the benefits for the defined benefit members who transferred from the CGU-VACC Fund

A copy of the Trust Deed may be inspected on request.

25 PLAN MANAGEMENT

PLAN MANAGEMENT25

G010282.qxd 15/2/12 9:20 AM Page 25

Concessional tax treatment

In order to qualify for concessional tax rates, funds have to be classified as ‘complying superannuation funds’ under the income

tax laws. To be eligible, funds must report regularly to the Australian Prudential Regulation Authority (APRA) and demonstrate

their compliance with superannuation laws and APRA guidelines.

The Plan is classified as a complying superannuation fund and the Trustee is not aware of any matter that would cause the Plan

to lose its complying status.

Management assistance

The Plan is administered by Superannuation Administration, which performs such functions as determining member benefits,

processing and allocating contributions and ensuring all membership data is correct. Superannuation Administration contact

details can be found on the back page of this report.

The Plan’s compliance status is monitored by Joe Janssen, Manager Superannuation.

The Trustee is assisted by a number of professionals who provide advice and assistance in the administrationof the Plan. These include:

Actuarial and Communication Consulting

Mercer Human Resource Consulting Pty Limited

Auditor

KPMG

Investment Manager

IAG Asset Management

Solicitor

Ebsworth & Ebsworth

Receiving your benefit

When you leave your Employer, you will be asked for payment instructions for your benefit. Your superannuation is an

important investment and you are encouraged to consider carefully where you want to invest it.

If you leave the Plan before you reach your preservation age, part or all of your superannuation benefit will be subject to

preservation and cannot be paid directly to you. However, you can transfer your entitlement to another approved

superannuation entity, including: eligible rollover fund, superannuation fund, deferred annuity, approved deposit fund,

retirement savings account or allocated pension. See page 28 for details on preservation.

When requested for payment instructions, you will have 90 days in which to advise the Trustee how you want your benefit paid,

or to nominate a complying superannuation entity to which you want to roll over your benefit.

WORKING FOR YOUR FUTURE 26

G010282.qxd 15/2/12 9:20 AM Page 26

Eligible Rollover Fund and unclaimed money

If you do not tell the Trustee how you want your benefit paid within 90 days, it will automatically be transferred to an eligible

rollover fund (ERF). An ERF is a fund approved by APRA to receive benefits payable to members who cannot be located, or

who do not advise how and where their benefit is to be paid. The ERF currently used by the Plan is SuperTrace Eligible

Rollover Fund.

Its contact details are:

The Senior Administrator

SuperTrace Eligible Rollover Fund

Locked Bag 5429

Parramatta NSW 2124

Tel:1300 788 750

If you have reached Government pension age when you leave your Employer and you have not given the Trustee instructions

regarding the payment of your benefit from the Plan, and you cannot be contacted, your benefit may be treated as ‘unclaimed

money’ according to superannuation law. In this instance, your benefit will be placed with the Chief Commissioner of State

Revenue for New South Wales.

Your benefit will be considered to be unclaimed money, if you have reached your statutory retirement age and have not told

your Plan how and where to pay your benefit, and you cannot be contacted.

If your benefit is transferred to an ERF or treated as unclaimed money, you will no longer be a member of the Plan. However,

you have rights to claim your benefit from the ERF or the relevant Government body as the case may be.

About SuperTrace

Set out below is a summary of some of the more significant features of the SuperTrace Eligible Rollover Fund (SuperTrace),

current as at the date of this report:

The assets of SuperTrace are invested in a life insurance policy (ERF Policy) issued to Colonial Mutual Superannuation Pty

Ltd (CMSPL) by the Colonial Mutual Life Assurance Society Limited (CMLA). The ERF Policy is invested solely in the

Colonial Stable Fund in CMLA’s No.2L Statutory Fund. There is no choice of investment available to members within

SuperTrace. The investment objective of SuperTrace is to provide medium term moderate real rates of return while aiming to

minimise the occurrence of negative shorter term returns. The investment strategy for the assets in the Colonial Stable Fund

is to invest in a range of assets including Australian and international equities, property, fixed interest securities and cash,

with a heavier weighting towards fixed interest investments.

27 RECEIVING BENEFITS

RECEIVING BENEFITS27

G010282.qxd 15/2/12 9:20 AM Page 27

Members’ accounts are generally credited with interest annually. The crediting rate, which is derived from the earning rate of the

ERF Policy, is net of tax on investment earnings and fees. Earnings can be negative. The following fees and charges apply in

SuperTrace:

an asset charge of 1.65% per annum which is deducted from the earnings of the ERF Policy prior to the crediting rate being

declared; and

a benefit payment fee of $30 is charged for each withdrawal from SuperTrace, subject to member protection legislation, ie it

will only be charged if a member’s account has earned $30 or more in the particular reporting period. If a member's account

has earned less than $30, the lesser amount is taken as the benefit payment fee.

SuperTrace is unable to accept contributions from members or their employers; however rollovers from other superannuation

funds are permitted. SuperTrace does not provide insurance cover.

Restrictions on when you can get access to your benefits

Preservation rules

Superannuation is a long-term investment and the Commonwealth Government has placed restrictions on when a person can

have access to benefits. These restrictions are known as ‘preservation’. When you leave the Plan, some or all of your benefit may

have to be preserved. This means you may not be able to take all your benefit (less tax) in cash when you leave the Plan. Your

benefit statement shows how much of your benefit is preserved.

Preserved benefits must generally be kept in the superannuation system until you:

retire permanently at or after your preservation age (see below)

leave your Employer at or after age 60

reach age 65

become permanently incapacitated as defined by Superannuation Industry Supervision (SIS) law (see below), or

die.

Your preserved amount is shown on your benefit statement.

WORKING FOR YOUR FUTURE 28

G010282.qxd 15/2/12 9:20 AM Page 28

Your preservation age depends on your date of birth according to the table below:

Preservation of disablement benefits

In some cases it is possible that, even though you may have qualified for a total and permanent disablement from the Plan,

the benefit may not be paid to you in cash until you have satisfied one of the above payment triggers. This is due to the

difference in definitions between the terms “Total and Permanent Disablement”, as defined in the Trust Deed and the

definition of the term ‘permanent incapacity’ in SIS.

For preservation purposes, ‘permanent incapacity’, in relation to a member who has ceased to be gainfully employed, means

ill-health (whether physical or mental), where the Trustee is reasonably satisfied that the member is unlikely, because of the

ill-health, ever again to engage in gainful employment for which the member is reasonably qualified by education, training or

experience.

29 PRESERVATION

PRESERVATION29

Date of birth Your preservation age

Before 1 July 1960 55

1 July 1960 to 30 June 1961 56

1 July 1961 to 30 June 1962 57

1 July 1962 to 30 June 1963 58

1 July 1963 to 30 June 1964 59

After 30 June 1964 60

G010282.qxd 15/2/12 9:20 AM Page 29

What’s happening in super

Financial Services Reform legislation now in effect

All superannuation funds are required to comply with the new requirements of the Financial Services Reform legislation which

came into full effect on 11 March 2004. The legislation provides a new legal framework for providers of financial products and

services including super funds. It sets out prescriptive requirements in relation to the information that the Trustee must disclose

to you and prohibits the Trustee from providing financial product advice unless it holds an Australian financial services licence.

The Trustee currently does not hold such a licence.

The aim of the legislation is to provide greater protection to fund members.

Choice of fund – a reality from 1 July 2005

For several years the Government has been trying to pass legislation that would provide employees with a greater choice on the

super fund they join. The legislation has (with some amendments) now been passed by the Senate and will take effect from 1

July 2005. The legislation generally allows an employee to choose the superannuation fund to which his or her employer makes

compulsory (superannuation guarantee) contributions. An employer is not obliged to provide employees with choice of fund if it

is paying superannuation contributions in accordance with a certified agreement. You will be informed about the new legislation

and how this affects you nearer the commencement date.

Matching contribution for low income earners

The Government introduced a scheme during the year to enable low income earners (with an income of less than $40,000),

making personal contributions to super, to receive a matching contribution from the Government of up to $1,000 for the

2003/2004 financial year. For this financial year, the matching contribution phased out for incomes between $27,500

and $40,000.

To be eligible for the co-contribution for the 2003/2004 financial year, the following criteria apply:

You need to have made after-tax member contributions (not before-tax salary sacrifice contributions) during the year

Your income* was less than $40,000

You need to earn at least 10% of your income from employment as an employee, and

You are under age 71 at the end of the financial year.

From 1 July 2004:

The co-contribution will increase to $1.50 for each $1 of after-tax member contributions up to a maximum of $1,500

The maximum co-contribution will apply for income* up to $28,000 and will phase down to zero for incomes of $58,000

* Income is your assessable income plus your reportable fringe benefits.

WORKING FOR YOUR FUTURE 30

G010282.qxd 15/2/12 9:20 AM Page 30

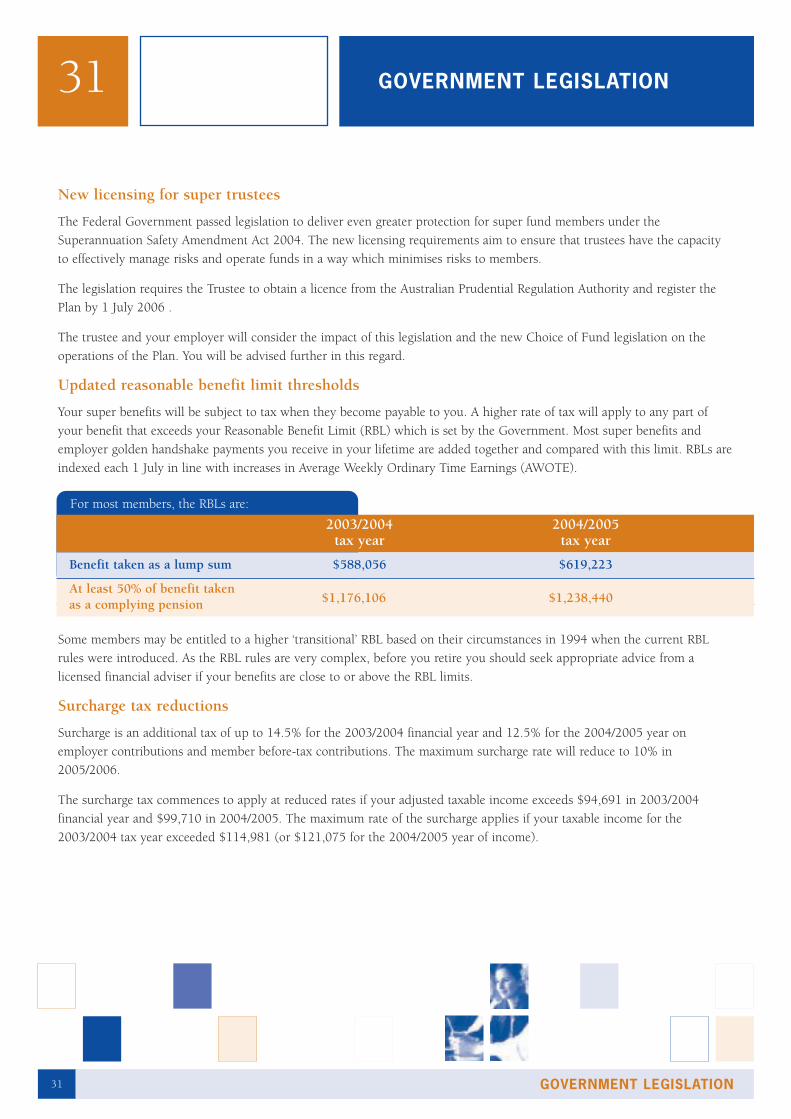

New licensing for super trustees

The Federal Government passed legislation to deliver even greater protection for super fund members under the

Superannuation Safety Amendment Act 2004. The new licensing requirements aim to ensure that trustees have the capacity

to effectively manage risks and operate funds in a way which minimises risks to members.

The legislation requires the Trustee to obtain a licence from the Australian Prudential Regulation Authority and register the

Plan by 1 July 2006 .

The trustee and your employer will consider the impact of this legislation and the new Choice of Fund legislation on the

operations of the Plan. You will be advised further in this regard.

Updated reasonable benefit limit thresholds

Your super benefits will be subject to tax when they become payable to you. A higher rate of tax will apply to any part of

your benefit that exceeds your Reasonable Benefit Limit (RBL) which is set by the Government. Most super benefits and

employer golden handshake payments you receive in your lifetime are added together and compared with this limit. RBLs are

indexed each 1 July in line with increases in Average Weekly Ordinary Time Earnings (AWOTE).

Some members may be entitled to a higher ‘transitional’ RBL based on their circumstances in 1994 when the current RBL

rules were introduced. As the RBL rules are very complex, before you retire you should seek appropriate advice from a

licensed financial adviser if your benefits are close to or above the RBL limits.

Surcharge tax reductions

Surcharge is an additional tax of up to 14.5% for the 2003/2004 financial year and 12.5% for the 2004/2005 year on

employer contributions and member before-tax contributions. The maximum surcharge rate will reduce to 10% in

2005/2006.

The surcharge tax commences to apply at reduced rates if your adjusted taxable income exceeds $94,691 in 2003/2004

financial year and $99,710 in 2004/2005. The maximum rate of the surcharge applies if your taxable income for the

2003/2004 tax year exceeded $114,981 (or $121,075 for the 2004/2005 year of income).

31 GOVERNMENT LEGISLATION

GOVERNMENT LEGISLATION31

For most members, the RBLs are:

2003/2004 2004/2005tax year tax year

Benefit taken as a lump sum $588,056 $619,223

At least 50% of benefit taken $1,176,106 $1,238,440as a complying pension

G010282.qxd 15/2/12 9:20 AM Page 31

These figures increase each year in line with increases in Average Weekly Ordinary Time Earnings (AWOTE). Adjusted taxable

income normally includes taxable income, employer (and member before-tax) superannuation contributions, fringe benefits,

certain trust income and parts of any employer golden handshake payment. Surcharge tax may also automatically apply to you if

you have not provided your tax file number to your Plan, irrespective of what you earn.

If the Plan is required to pay surcharge tax in respect of contributions made for you, the tax payable will be charged to an

account in your name in the Plan. Your surcharge account (including any interest) will be deducted from your benefits when you

leave the Plan.

Check this year’s Benefit Statement to see if surcharge tax has applied to you. If the Plan receives a surcharge assessment after

you have left the Plan it will generally be forwarded to the fund or institution to which you have transferred your benefit.

New definition of “dependant”

New legislation passed through Parliament on Choice of Fund includes amendments to the Income Tax Assessment Act and the

SIS Act. The changes expand the definition of “dependant” in relation to the payment and tax treatment of super death benefits.

The definition of dependant has been broadened under relevant legislation to include “any person with whom the person has an

interdependency relationship”. Two persons have an “interdependency relationship” if they meet all of the following criteria:

they have a close personal relationship

they live together

one or each of them provides the other with financial support

one or each of them provides the other with domestic support and personal care

The definition “dependant” in the Trust Deed does not include an “interdependency relationship”, although the Trust Deed may

be amended to allow for this.

Legislative changes affecting some contributions

There have been some changes to legislation (effective now) which sets out the conditions that must be met for a fund to accept

contributions by or in respect of a member.

In brief, members under age 65 no longer need to be working to make contributions to a super fund (providing the super fund

can accept contributions from persons other than employees).

For members over age 65, there have been changes to the minimum number of hours a person must work before a fund can accept

contributions. Similarly, there have been changes to the legislation which makes it compulsory for a trustee to pay benefits after age

65 if certain conditions are not met. If you require more detailed information please contact Superannuation Administration.

WORKING FOR YOUR FUTURE 32

G010282.qxd 15/2/12 9:20 AM Page 32

Other Government changes in the pipeline

Contribution splitting

New legislation has been proposed that allows members to split their personal and employer contributions with their spouse.

At the date of publication this legislation has not been passed by Federal Parliament.

More information

Resolving disputes and complaints

If you have a question about your benefits in the Plan, please contact Superannuation Administration.

Most inquiries can be dealt with over the phone. If not, you may be asked to put your enquiry in writing and provide a

contact address for the reply. Inquiries will generally be answered within 28 days.

If you have a query or a problem, which is not resolved to your satisfaction, you should send a written complaint (including

all relevant details) to:

The Complaints Officer

NRMA Staff Superannuation Pty Limited

Level 13,

388 George Street

Sydney NSW 2000

The matter will be investigated by the Complaints Officer and, where necessary, the Complaints Committee on behalf of the

Trustee. You will be advised of the Trustee’s decision as soon as possible and within 90 days, or within 30 days of the

Trustee’s decision, whichever is earlier.

Please remember to include an address to which the response can be mailed.

If the Trustee has not responded to your complaint within 90 days, or you are not satisfied with the Trustee’s decision you

may be able to take the matter to a special government body called the Superannuation Complaints Tribunal (see below).

While the Plan has a process in place to deal with complaints from members, the Trustee’s objective is to avoid complaints by

providing a good level of service to members, and if complaints do occur, to resolve them to the satisfaction of all concerned.

A copy of the Plan’s detailed enquiries and complaints procedures is available on request from Superannuation Administration.

33 MORE INFORMATION

MORE INFORMATION33

G010282.qxd 15/2/12 9:20 AM Page 33

Superannuation Complaints Tribunal

The Tribunal is an independent body set up by the Federal Government to provide a low-cost, informal forum for resolving most

superannuation disputes. Before the Tribunal can consider a complaint, it must be satisfied that the matter has been referred to

the Trustee under the procedure set out above.

Any complaints must be lodged with the Tribunal within certain time limits. For more information about requirements and time

limits, you can call the Superannuation Complaints Tribunal on 1300 884 114.

If the Tribunal accepts your complaint, it will try to help you and the Trustee reach a mutual agreement through conciliation. If

conciliation is unsuccessful, the Tribunal can make a determination, which is binding.

If you’d like more information

For accumulation members, full details of the benefits provided by the Plan are set out the Plan’s Product Disclosure Statement.

For defined benefit members, full details of the benefits provided by the Plan are set out in A guide to your super.

As a member of the Plan, you can inspect other Plan documents by contacting Superannuation Administration. These documents

are listed on the inside front cover.

Questions?

If you have questions about your superannuation benefits, please call any of the following in Superannuation Administration:

Rachel Jones ext 29342

Robert Szomolnoki ext 28782

Jacinta Tran ext 28783

Troy Maguire ext 28781

Gloria Matig-a ext 29346

Or (02) 9292 8780 if you are calling externally;

Alternatively, you can write to them at:

Superannuation Administration

Level 13,

388 George Street

Sydney NSW 2000

Issued by NRMA Staff Superannuation Pty Limited ACN 000 300 934 as Trustee of the IAG and NRMA Superannuation Plan

WORKING FOR YOUR FUTURE 34

G010282.qxd 15/2/12 9:20 AM Page 34

G01

0282

11/0

4

G010282.qxd 15/2/12 9:20 AM Page 1