Embed Size (px)

Citation preview

IAS 32/39 Financial Instruments: IAS 32/39 Financial Instruments: Disclosure and PresentationDisclosure and PresentationRecognition and MeasurementRecognition and Measurement

AgendaAgenda Scope and definitions Scope and definitions IAS 32IAS 32

– Liability and equityLiability and equity

– Offsetting a financial asset and financial liabilityOffsetting a financial asset and financial liability

IAS 39IAS 39– Classification of financial instruments Classification of financial instruments

– Measurement of financial assets and liabilitiesMeasurement of financial assets and liabilities

– Derivatives and embedded derivativesDerivatives and embedded derivatives

– Recognition and derecognitionRecognition and derecognition

– Hedging and hedge accountingHedging and hedge accounting

IAS 32 – Disclosure requirementsIAS 32 – Disclosure requirements Case studyCase study

History and Effective DateHistory and Effective Date IAS 32 IAS 32

– Effective for accounting periods beginning on or after 1 January 1996.Effective for accounting periods beginning on or after 1 January 1996.

– Other related interpretationsOther related interpretations SIC 5 Classification of Financial Instruments – Contingent Settlement Provisions.SIC 5 Classification of Financial Instruments – Contingent Settlement Provisions. SIC 16 Share Capital – Reacquired Own Equity Instruments (Treasury Shares).SIC 16 Share Capital – Reacquired Own Equity Instruments (Treasury Shares). SIC 17 Equity – Costs of an Equity Transaction.SIC 17 Equity – Costs of an Equity Transaction.

IAS 39IAS 39

– Effective for accounting periods beginning on or after 1 January 2001Effective for accounting periods beginning on or after 1 January 2001

– Other related guidanceOther related guidance Interpretation Guidance issued by IGC.Interpretation Guidance issued by IGC.

IAS 32/39 (Revised 2003 and 2004 for Portfolio Hedge of Interest Rate Risk)IAS 32/39 (Revised 2003 and 2004 for Portfolio Hedge of Interest Rate Risk)

– Effective for accounting period beginning on or after 1 January 2005.Effective for accounting period beginning on or after 1 January 2005. DraftDraft

– Amendments to IAS 39 Financial Instruments: Recognition and Measurement: The Fair Amendments to IAS 39 Financial Instruments: Recognition and Measurement: The Fair Value Option.Value Option.

– Issued on 21 April 2004.Issued on 21 April 2004.

ObjectiveObjective

IAS 32 IAS 32 – To enhance financial statement users’ To enhance financial statement users’

understanding of the significance of financial understanding of the significance of financial instruments to an entity’s financial position, instruments to an entity’s financial position, performance and cash flows.performance and cash flows.

IAS 39IAS 39– The objective of this Statement is to establish The objective of this Statement is to establish

principles for principles for recognisingrecognising, , measuringmeasuring financial assets, financial assets, financial liabilities and some contracts to buy and sell financial liabilities and some contracts to buy and sell non-financial items.non-financial items.

Scope and DefinitionsScope and Definitions

Scope Exclusion:Scope Exclusion:

..IAS 32IAS 32 IAS 39IAS 39

Interests in subsidiaries, associates and joint ventures in Interests in subsidiaries, associates and joint ventures in consolidated accounts (IAS 27, 28 and 31)consolidated accounts (IAS 27, 28 and 31) xx xxRights and obligations under leases (IAS 17) except for Rights and obligations under leases (IAS 17) except for derecognition and embedded derivativesderecognition and embedded derivatives xxEmployers’ assets and liabilities under employee benefit Employers’ assets and liabilities under employee benefit plans (IAS 19)plans (IAS 19) xx xxRights and obligations under insurance contracts (IFRS Rights and obligations under insurance contracts (IFRS 4)4) xx xxInstruments issued by the reporting enterprise that Instruments issued by the reporting enterprise that meet the definition of equity (IAS 32)meet the definition of equity (IAS 32) xxCertain loans commitments and financial guarantee Certain loans commitments and financial guarantee contracts (IAS 37 and 18)contracts (IAS 37 and 18) xxContracts for contingent consideration in a business Contracts for contingent consideration in a business combination for the acquirer (IAS 22/IFRS 3)combination for the acquirer (IAS 22/IFRS 3) xx xxContracts that require payment based on climatic, Contracts that require payment based on climatic, geological or other physical variables (IFRS 4)geological or other physical variables (IFRS 4) xx xx

Scope : Non-financial item contractsScope : Non-financial item contracts

Contracts to buy or sell a non-financial item that Contracts to buy or sell a non-financial item that can be settled net in cash or another financial can be settled net in cash or another financial instrument are treated as financial instruments: instrument are treated as financial instruments:

unless the non-financial item contracts:unless the non-financial item contracts:

– were entered into and continue to be held were entered into and continue to be held for the purpose of the receipt or delivery of for the purpose of the receipt or delivery of a non-financial item in accordance with the a non-financial item in accordance with the entity’s expected purchase, sale or usage entity’s expected purchase, sale or usage requirements.requirements.

Definition : What is a Financial Definition : What is a Financial Instrument?Instrument?

A contract that gives rise to:A contract that gives rise to:

and

in one enterprise

in another enterprise

Definition of Financial AssetDefinition of Financial AssetAny asset that is:Any asset that is: cash;cash; a contractual right to receive cash or another financial asset a contractual right to receive cash or another financial asset

from another entity;from another entity; a contractual right to exchange financial instruments with a contractual right to exchange financial instruments with

another enterprise under conditions that are potentially another enterprise under conditions that are potentially favourable;favourable;

an equity instrument of another entity;an equity instrument of another entity; a contract that will or may be settled in the entity’s own a contract that will or may be settled in the entity’s own

equity instruments and is:equity instruments and is:– A non-derivative for which the entity is or may be obliged to receive A non-derivative for which the entity is or may be obliged to receive

a variable number of the entity’s own equity instruments;a variable number of the entity’s own equity instruments;– A derivative that will or may be settled other than by the exchange A derivative that will or may be settled other than by the exchange

of a fixed amount of cash or another financial asset for a fixed of a fixed amount of cash or another financial asset for a fixed number of the entity’s own equity instruments.number of the entity’s own equity instruments.

Definitions of Financial Liability/Equity Definitions of Financial Liability/Equity Financial LiabilityFinancial LiabilityAny liability that is a contractual obligation:Any liability that is a contractual obligation:

– to deliver cash or another financial asset to another enterprise; to deliver cash or another financial asset to another enterprise; oror

– to exchange financial instruments with another enterprise under to exchange financial instruments with another enterprise under conditions that are potentially unfavourableconditions that are potentially unfavourable

– a contract that will or may be settled in the entity’s own equity a contract that will or may be settled in the entity’s own equity instrument and is:instrument and is:

A non-derivative for which the entity is or may be obliged to deliver a A non-derivative for which the entity is or may be obliged to deliver a variable number of the entity’s own equity instruments;variable number of the entity’s own equity instruments;

A derivative that will or may be settled other than by the exchange of A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number a fixed amount of cash or another financial asset for a fixed number of the entity’s own equity instruments.of the entity’s own equity instruments.

Equity instrumentEquity instrumentAny contract that evidences a residual interest in the Any contract that evidences a residual interest in the assets of an enterprise after deducting all of its liabilitiesassets of an enterprise after deducting all of its liabilities

Types of Financial InstrumentsTypes of Financial Instruments

CombinationsCombinations

– Convertible debtConvertible debt– Exchangeable debtExchangeable debt– Dual currency bondDual currency bond

DerivativesDerivatives

– Forwards / futuresForwards / futures– Financial optionsFinancial options– SwapsSwaps– Caps and collarsCaps and collars– Financial Financial

guaranteesguarantees– Letters of creditLetters of credit

PrimaryPrimary

– Deposits of cashDeposits of cash– Bonds, loans, Bonds, loans,

borrowingsborrowings– Receivables / Receivables /

payables payables (including (including finance leases)finance leases)

– Equity Equity instrumentsinstruments

Financial InstrumentsFinancial Instruments

IAS 32 - PresentationIAS 32 - Presentation

IAS 32 – PresentationIAS 32 – Presentation

•Liability and equityLiability and equity•Offsetting a financial asset and a financial Offsetting a financial asset and a financial liabilityliability

IAS 32 – Liability and EquityIAS 32 – Liability and Equity•Classify the instrument, or its Classify the instrument, or its component partscomponent parts, on initial , on initial recognition as a financial liability, a financial asset or an recognition as a financial liability, a financial asset or an equity instrument in accordance with the equity instrument in accordance with the substancesubstance of the of the contractual arrangement and the definitions of a financial contractual arrangement and the definitions of a financial liability, a financial asset and an equity instrumentliability, a financial asset and an equity instrument..

•If a financial instrument contains both a liability and an If a financial instrument contains both a liability and an equity element, the instrument’s component parts should equity element, the instrument’s component parts should be classified separately.be classified separately.

•Debt Securities with an embedded conversion option, Debt Securities with an embedded conversion option, such as a convertible bond, should be separated into the such as a convertible bond, should be separated into the liability component and the equity component on the liability component and the equity component on the balance sheet.balance sheet.

IAS 32 – Liability and Equity IAS 32 – Liability and Equity LiabilityLiabilityContractual obligation to deliver cash or Contractual obligation to deliver cash or another financial asset.another financial asset.– Mandatory redeemable preference shares.Mandatory redeemable preference shares.– A “puttable instrument” by the holder.A “puttable instrument” by the holder.

Liability if the obligation is conditional.Liability if the obligation is conditional.– Conditional upon approval by regulatory authority.Conditional upon approval by regulatory authority.– Conditional upon the counter-party exercising its Conditional upon the counter-party exercising its

right to redeem. right to redeem.

IAS 32 – Liability and Equity IAS 32 – Liability and Equity Settlement in the entity’s own equity instrument.Settlement in the entity’s own equity instrument.

– Not an equity instrument solely because settlement is Not an equity instrument solely because settlement is through delivery or receipt of the entity’s own equity.through delivery or receipt of the entity’s own equity.

– Liability if the contractual obligation is a fixed amount so that Liability if the contractual obligation is a fixed amount so that the value of the equity instrument equals the amount of the value of the equity instrument equals the amount of contractual obligation. contractual obligation.

Settlement optionsSettlement options– When a derivative financial instrument gives one party a When a derivative financial instrument gives one party a

choice over how it is settled (eg. the issuer or the holder can choice over how it is settled (eg. the issuer or the holder can choose settlement net in cash or by exchanging shares for choose settlement net in cash or by exchanging shares for cash), it is a financial asset or a financial liability unless all cash), it is a financial asset or a financial liability unless all settlement alternatives would result in it being an equity settlement alternatives would result in it being an equity instrument.instrument.

IAS 32 – Liability and Equity IAS 32 – Liability and Equity Contingent settlement provisionContingent settlement provision

– Liability if the obligation to deliver cash or another Liability if the obligation to deliver cash or another financial instrument arises only on the occurrence financial instrument arises only on the occurrence or non-occurrence of uncertain future events that or non-occurrence of uncertain future events that are beyond the control of both the issuer and are beyond the control of both the issuer and holder, holder, unless unless

The contingent event is restricted only in the event of The contingent event is restricted only in the event of liquidation of the issuer; orliquidation of the issuer; or

The contingent event that trigger the obligation is The contingent event that trigger the obligation is considered to be not genuine.considered to be not genuine.

IAS 32 – Liability and Equity IAS 32 – Liability and Equity Treasury SharesTreasury Shares

– Acquisition of own equity instruments (treasury Acquisition of own equity instruments (treasury shares) should be deducted from equity. No gain or shares) should be deducted from equity. No gain or loss shall be recognised in profit or loss on the loss shall be recognised in profit or loss on the purchase, sale, issue or cancellation of an entity’s purchase, sale, issue or cancellation of an entity’s own equity instruments.own equity instruments.

– However, an obligation to purchase own equity However, an obligation to purchase own equity instruments for cash or another financial asset instruments for cash or another financial asset gives rise to a financial liability for the present gives rise to a financial liability for the present value of the redemption amount.value of the redemption amount.

IAS 32 – Liability and Equity IAS 32 – Liability and Equity Compound InstrumentCompound Instrument

– An financial instrument that contains both liability and equity An financial instrument that contains both liability and equity components should be classified and presented separately.components should be classified and presented separately.

– Example: A bond that is convertible, either mandatory or at the Example: A bond that is convertible, either mandatory or at the option of the holder into equity shares of the issuer.option of the holder into equity shares of the issuer.

Method of separating the liability and equity componentMethod of separating the liability and equity component– The liability component is fair valued first, and this provides the The liability component is fair valued first, and this provides the

initial carrying amount of the liability component.initial carrying amount of the liability component.– The fair value of the liability component is then deducted from the The fair value of the liability component is then deducted from the

fair value of the instrument with the residual amount representing fair value of the instrument with the residual amount representing the equity component.the equity component.

– Transaction costs are usually allocated to the liability and equity Transaction costs are usually allocated to the liability and equity components based on proportion of fair value. components based on proportion of fair value.

IAS 32 – Liability and Equity IAS 32 – Liability and Equity Interest, Dividends, Losses and GainsInterest, Dividends, Losses and Gains

– Interest, dividends, losses and gains relating to a Interest, dividends, losses and gains relating to a financial instrument or a component that is a financial financial instrument or a component that is a financial liability shall be recognised as income or expense in liability shall be recognised as income or expense in profit and loss. profit and loss.

– Distributions to holders of an equity instrument shall be Distributions to holders of an equity instrument shall be debited by the entity directly to equity.debited by the entity directly to equity.

IAS 32 – Offsetting of a financial asset IAS 32 – Offsetting of a financial asset and a financial liabilityand a financial liabilityA financial asset and a financial liability shall A financial asset and a financial liability shall be offset and the net amount presented in the be offset and the net amount presented in the balance sheet when, and only when, an entity:balance sheet when, and only when, an entity:– Currently has a legally enforceable right to set off Currently has a legally enforceable right to set off

the recognised amounts; the recognised amounts; andand– Intends either to settle on a net basis, or to realise Intends either to settle on a net basis, or to realise

the asset and settle the liability simultaneously.the asset and settle the liability simultaneously.

IAS 39 IAS 39

Classification of Financial Classification of Financial

Assets Assets

and Liabilitiesand Liabilities

Financial Assets : Held for TradingFinancial Assets : Held for Trading

Acquired or incurred principally for the Acquired or incurred principally for the

purpose of selling or repurchasing it in the purpose of selling or repurchasing it in the

near term.near term.

Regardless of why it was acquired, the Regardless of why it was acquired, the

financial asset is a part of a portfolio for financial asset is a part of a portfolio for

which there is evidence of a recent actual which there is evidence of a recent actual

pattern of short-term profit-taking.pattern of short-term profit-taking.

Financial Assets : Held for Trading Financial Assets : Held for Trading (Continued)(Continued)

• Derivative financial assets and derivative Derivative financial assets and derivative financial liabilities are:financial liabilities are:

-- always deemed held for tradingalways deemed held for trading

UNLESSUNLESS

-- they are designated and are they are designated and are effective effective hedging instruments.hedging instruments.

Financial Assets : Designated upon initial Financial Assets : Designated upon initial recognitionrecognition

Any financial asset or financial liability within the Any financial asset or financial liability within the

scope of this Standard may be designated when scope of this Standard may be designated when

initially recognised as a financial asset or financial initially recognised as a financial asset or financial

liability at fair value thru P&L;liability at fair value thru P&L;

except forexcept for::

investments in equity instruments that do not have a investments in equity instruments that do not have a

quoted market price in an active market and whose quoted market price in an active market and whose

fair value cannot be reliably measured.fair value cannot be reliably measured.

Note: ED issued on 21 April 2004 potentially will limit the types of financial Note: ED issued on 21 April 2004 potentially will limit the types of financial

assets and financial liabilities to which this option may be applied.assets and financial liabilities to which this option may be applied.

Financial Assets : Held-to-MaturityFinancial Assets : Held-to-MaturityAssets with fixed or determinable payments and fixed Assets with fixed or determinable payments and fixed

maturity:maturity:

• which the enterprise has the which the enterprise has the positive intentpositive intent and and

abilityability to hold to maturity to hold to maturity

other thanother than

• loans and receivables; andloans and receivables; and

• those that the entity upon initial recognition

designates as at fair value through profit & loss or

those that the entity designates as available for sale.

Financial Assets : Held-to-Maturity Financial Assets : Held-to-Maturity (Continued)(Continued)An enterprise An enterprise should notshould not classify any financial assets as held-to-maturity classify any financial assets as held-to-maturity

if it (IAS 39R.9):if it (IAS 39R.9):

• sold, transferred or exercised put options on more than an sold, transferred or exercised put options on more than an insignificant amount of held-to-maturity investments before maturity insignificant amount of held-to-maturity investments before maturity during the current year or two preceding years during the current year or two preceding years (TAINTING)(TAINTING)

OTHER THANOTHER THAN• sales close enough to maturity or the exercised call date so that sales close enough to maturity or the exercised call date so that

interest rate changes did not have significant effect on fair value; interest rate changes did not have significant effect on fair value; • sales after the enterprise has already collected substantially all of the sales after the enterprise has already collected substantially all of the

financial asset’s original principal; orfinancial asset’s original principal; or• sales due to an isolated event that is beyond the enterprise’s control, sales due to an isolated event that is beyond the enterprise’s control,

is non-recurring and could not have been reasonably anticipated. is non-recurring and could not have been reasonably anticipated.

Financial Assets : Loans and Financial Assets : Loans and Receivables Receivables

Financial assets with fixed or determinable payments that are not quoted in an active market, other than: those that are intended for sale immediately or in

the near term, which should be classified as held for trading; and

those that are designated upon initial recognition as fair value thru P&L; or

those that are designated upon initial recognition as available for sale; or

those for which the holder may not recover substantially all of its initial investment, other than because of credit deterioration, which shall be classified as available for sale.

Financial Assets : Available-for-SaleFinancial Assets : Available-for-Sale

Those financial assets that are Those financial assets that are designated as designated as

available for saleavailable for sale or or are not classifiedare not classified as: as:

a) a) loans and receivables;loans and receivables;

b)b) held-to-maturity investments, orheld-to-maturity investments, or

c) c) financial assets at fair value thru P&Lfinancial assets at fair value thru P&L

Financial Liabilities : At fair value thru Financial Liabilities : At fair value thru P&L P&L

ComprisesComprisesa) Financial liabilities held for trading:a) Financial liabilities held for trading: derivative liabilities that are not hedging instrumentsderivative liabilities that are not hedging instruments the obligation to deliver securities borrowed by a short seller (an the obligation to deliver securities borrowed by a short seller (an

enterprise that sells securities that it does not yet own)enterprise that sells securities that it does not yet own) Financial liabilities that are incurred with an intention to repurchase Financial liabilities that are incurred with an intention to repurchase

them in the near termthem in the near term Financial liabilities that are part of a portfolio of identified financial Financial liabilities that are part of a portfolio of identified financial

instruments that are managed together and for which there is instruments that are managed together and for which there is evidence of a recent pattern of short-term profit-takingevidence of a recent pattern of short-term profit-taking

b) Designated as “fair value thru P/L” upon initial recognitionb) Designated as “fair value thru P/L” upon initial recognition

The fact that a liability is used to fund trading activities does not The fact that a liability is used to fund trading activities does not make that liability one held for tradingmake that liability one held for trading

IAS 39 IAS 39

Measurement of Financial Assets Measurement of Financial Assets

and Liabilitiesand Liabilities

Initial Measurement Initial Measurement

On initial recognition: On initial recognition:

– financial assets and financial liabilities should financial assets and financial liabilities should

be measured at be measured at fair valuefair value, PLUS , PLUS

– in the case of financial assets / liabilities not in the case of financial assets / liabilities not

at fair value thru P&L, at fair value thru P&L, transaction coststransaction costs that that

are directly attributable to the acquisition or are directly attributable to the acquisition or

issue of the financial asset or financial issue of the financial asset or financial

liability.liability.

Initial Measurement Initial Measurement

The The fair valuefair value of a financial instrument on of a financial instrument on initial recognition is normally the initial recognition is normally the transaction transaction priceprice..

However, if part of the consideration given or However, if part of the consideration given or received is for something other than the received is for something other than the financial instrument, the fair value is financial instrument, the fair value is estimated using a valuation technique.estimated using a valuation technique.

Initial Measurement Initial Measurement The fair value of a long-term loan that carried The fair value of a long-term loan that carried no no

interestinterest can be estimated as the PV of all future can be estimated as the PV of all future cash receipts cash receipts discounteddiscounted using the prevailing using the prevailing market rate of interest for a similar instrument market rate of interest for a similar instrument (similar as to currency, term, type of interest rate (similar as to currency, term, type of interest rate and other factors) with a similar credit rating.and other factors) with a similar credit rating.

The fair value of a financial liability with a The fair value of a financial liability with a demand demand featurefeature (e.g. a demand deposit) is (e.g. a demand deposit) is not lessnot less than than the amount payable on demand, discounted from the amount payable on demand, discounted from the first date that the amount could be required to the first date that the amount could be required to be paid.be paid.

1. 1. Held-to-Maturity Investments: Held-to-Maturity Investments: Amortised CostAmortised Cost

Financial assets with fixed or determinable payments and Financial assets with fixed or determinable payments and fixed maturity that an enterprise has the positive intent and fixed maturity that an enterprise has the positive intent and ability to hold to maturityability to hold to maturity

Amortised costAmortised cost is: is:

Subsequent Measurement : Subsequent Measurement : Held-to-Maturity InvestmentsHeld-to-Maturity Investments

Initial cost Principal repayments

Cumulative amortisation of

difference between initial amount and maturity amount

Write-down for impairment or uncollectibility

- +/- -

Gain/loss from amortisation is recognised in net profit/loss

Subsequent Measurement : Subsequent Measurement : Loans and ReceivablesLoans and Receivables

2.2. Loans and Receivables : Loans and Receivables : Cost or Amortised CostCost or Amortised Cost

Created by the enterprise by providing money, goods, Created by the enterprise by providing money, goods, or services directly to a debtor, other than those or services directly to a debtor, other than those intended for sale in the short termintended for sale in the short term

Examples: receivables from sales of goods, originated Examples: receivables from sales of goods, originated mortgage loans, credit card loans, government or mortgage loans, credit card loans, government or corporate securities acquired at originationcorporate securities acquired at origination

Gain/loss from amortisation is recognised in net Gain/loss from amortisation is recognised in net profit/lossprofit/loss

Subsequent Measurement : Subsequent Measurement : Fair Value thru Profit and LossFair Value thru Profit and Loss3.3. Fair value thru profit and loss : Fair value thru profit and loss : Fair Value Fair Value

– Acquired or incurred principally for the purpose of generating Acquired or incurred principally for the purpose of generating a profit from short-term fluctuations in price or dealer’s margin;a profit from short-term fluctuations in price or dealer’s margin;

OROR– Part of a portfolio with a recent pattern of short-term profit-Part of a portfolio with a recent pattern of short-term profit-

taking;taking; OROR

– Designated upon initial recognition.Designated upon initial recognition.

Examples: trading portfolio of marketable securities, all derivatives Examples: trading portfolio of marketable securities, all derivatives unless qualifying as a hedgeunless qualifying as a hedge

Gain/loss from fair value changes is recognised in net profit/lossGain/loss from fair value changes is recognised in net profit/loss

Subsequent Measurement : Subsequent Measurement : Available-for-SaleAvailable-for-Sale4.4. Available-for-Sale : Available-for-Sale : Fair valueFair value

Financial assets which are Financial assets which are designated as available for designated as available for sale orsale or not in one of the other three categories. not in one of the other three categories.

Example: equities not held for trading, including Example: equities not held for trading, including strategic investments; debt securities with no positive strategic investments; debt securities with no positive intent/ability to hold to maturityintent/ability to hold to maturity

Gain/loss from fair value changes is recognised directly in equity Gain/loss from fair value changes is recognised directly in equity

until sold, collected, disposed, at which time include in profit or until sold, collected, disposed, at which time include in profit or

loss. Interest calculated using effective interest rate method is loss. Interest calculated using effective interest rate method is

recognised in the P&L.recognised in the P&L.

Subsequent Measurement:Subsequent Measurement:Exception from Fair Value Exception from Fair Value RequirementRequirementPresumption:Presumption:

Fair value can be reliably determined for most financial assets Fair value can be reliably determined for most financial assets

classified as available for sale or held for trading.classified as available for sale or held for trading.

But:But:

Presumption can be overcome for:Presumption can be overcome for:

– investment in equity instrument that does not have a quoted investment in equity instrument that does not have a quoted

market price in an active market and for which other methods of market price in an active market and for which other methods of

estimating fair value are clearly inappropriate/unworkableestimating fair value are clearly inappropriate/unworkable

– derivatives linked to and settled by delivery of such an investmentderivatives linked to and settled by delivery of such an investment

Subsequent Measurement : Subsequent Measurement : ImpairmentImpairment At each balance sheet date, the enterprise should At each balance sheet date, the enterprise should

assess whether there is any objective evidence of assess whether there is any objective evidence of impairment (eg. financial difficulty of issuer, breach impairment (eg. financial difficulty of issuer, breach of contract, historical pattern of non-collectibility of contract, historical pattern of non-collectibility etc).etc).

If any evidence exists, the enterprise should provide If any evidence exists, the enterprise should provide for any impairment to recoverable amount for debt for any impairment to recoverable amount for debt instruments (ie. the present value of expected future instruments (ie. the present value of expected future cash flows discounted at the financial instrument’s cash flows discounted at the financial instrument’s original effective interest rateoriginal effective interest rate) or to their estimated ) or to their estimated fair values (for equity instruments).fair values (for equity instruments).

Subsequent Measurement : Subsequent Measurement : ImpairmentImpairment Assess existence of any objective evidence of impairmentAssess existence of any objective evidence of impairment::

– significant financial difficulty of issuersignificant financial difficulty of issuer

– actual breach of contract such as failure to make interest/principal paymentsactual breach of contract such as failure to make interest/principal payments

– high probability of bankruptcyhigh probability of bankruptcy

– disappearance of active market for financial assetdisappearance of active market for financial asset

– historical pattern indicating entire face value of portfolio will not be collectedhistorical pattern indicating entire face value of portfolio will not be collected

Discount expected future cash flows at original effective interest rate to determine Discount expected future cash flows at original effective interest rate to determine

recoverable amount.recoverable amount.

Write down to recoverable amount through net profit/loss.Write down to recoverable amount through net profit/loss.

Impairment loss for financial assets carried at cost (unquoted equity) should not be Impairment loss for financial assets carried at cost (unquoted equity) should not be

reversed.reversed.

Impairment loss for available for sale equity instrument cannot be reversed thru P&L, Impairment loss for available for sale equity instrument cannot be reversed thru P&L,

any subsequent increase in fair value is recognised in equity.any subsequent increase in fair value is recognised in equity.

IAS 39 IAS 39

Derivatives and Derivatives and

Embedded DerivativesEmbedded Derivatives

Derivatives:Derivatives:

Definition and Definition and

ClassificationClassification

A derivative is a financial instrument:A derivative is a financial instrument:

a)a) whose value changes in response to the whose value changes in response to the change in a specified change in a specified underlyingunderlying;;

b)b) that requires that requires no initial net investmentno initial net investment or or an an initial net investment that is smallerinitial net investment that is smaller than than would be required for other types of would be required for other types of contracts that would be expected to have a contracts that would be expected to have a similar response to changes in market similar response to changes in market factors; ANDfactors; AND

c)c) that is that is settled at a future datesettled at a future date..

Definition of DerivativesDefinition of Derivatives

A financial instrument whose value changes in response A financial instrument whose value changes in response to the change in a specified to the change in a specified underlyingunderlying:: – Underlyings are defined as:Underlyings are defined as:

specified interest ratespecified interest rate security pricesecurity price commodity pricecommodity price foreign exchange rateforeign exchange rate index of prices or ratesindex of prices or rates a credit rating or credit indexa credit rating or credit index other variablesother variables

Definition of Derivatives : Definition of Derivatives : Response to Changes in UnderlyingsResponse to Changes in Underlyings

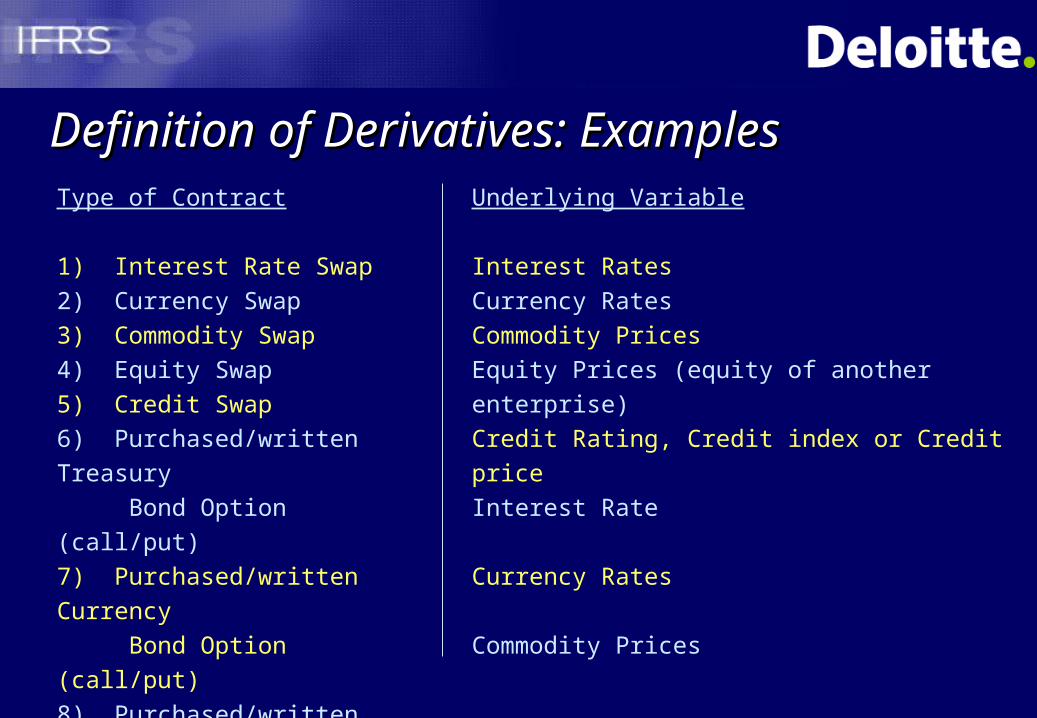

Definition of Derivatives: ExamplesDefinition of Derivatives: ExamplesUnderlying Variable

Interest Rates

Currency Rates

Commodity Prices

Equity Prices (equity of another enterprise)

Credit Rating, Credit index or Credit price

Interest Rate

Currency Rates

Commodity Prices

Type of Contract

1) Interest Rate Swap

2) Currency Swap

3) Commodity Swap

4) Equity Swap

5) Credit Swap

6) Purchased/written Treasury

Bond Option (call/put)

7) Purchased/written Currency

Bond Option (call/put)

8) Purchased/written

Commodity Option (call/put)

Definition of Derivatives : Examples Definition of Derivatives : Examples (Continued)(Continued)

Underlying Variable

Equity Prices (equity of another Enterprise)

Interest Rates

Currency Rates

Commodity Prices

Currency Rates

Commodity Prices

Equity Prices (equity of another enterprise)

Type of Contract

9) Purchased/written Stock

Option (call/put)

10) Interest Rate Futures

Linked to Government

Debt (Treasury Futures)

11) Currency Futures

12) Commodity Futures

13) Currency Forward

14) Commodity Forward

15) Equity Forward

Derivative normally has a notional amount Derivative normally has a notional amount which is an amount of currency, a number of which is an amount of currency, a number of shares, units of weight or volume or other shares, units of weight or volume or other units specified in contractunits specified in contract

Alternatively could require a fixed payment Alternatively could require a fixed payment as a result of some future event that is as a result of some future event that is unrelated to a notional amount (eg. pay CU1 unrelated to a notional amount (eg. pay CU1 million if interest rates increase by 100 basis million if interest rates increase by 100 basis points)points)

Definition of Derivatives:Definition of Derivatives:Response to Changes in UnderlyingsResponse to Changes in Underlyings

A financial instrument that requires A financial instrument that requires no initial net no initial net investmentinvestment or or an initial net investment that is an initial net investment that is smallersmaller than would be required for other types of than would be required for other types of contracts that would be expected to have a similar contracts that would be expected to have a similar response to changes in market factors:response to changes in market factors:– Little initial net investment has wide interpretation Little initial net investment has wide interpretation

and requires professional judgementand requires professional judgement Focus is on relativity between initial net Focus is on relativity between initial net

investment and comparable primary financial investment and comparable primary financial instrumentinstrument

Criterion failed if investment is “equal or close to” Criterion failed if investment is “equal or close to” equivalent investmentequivalent investment

Definition of Derivatives : Definition of Derivatives : Initial Net Initial Net InvestmentInvestment

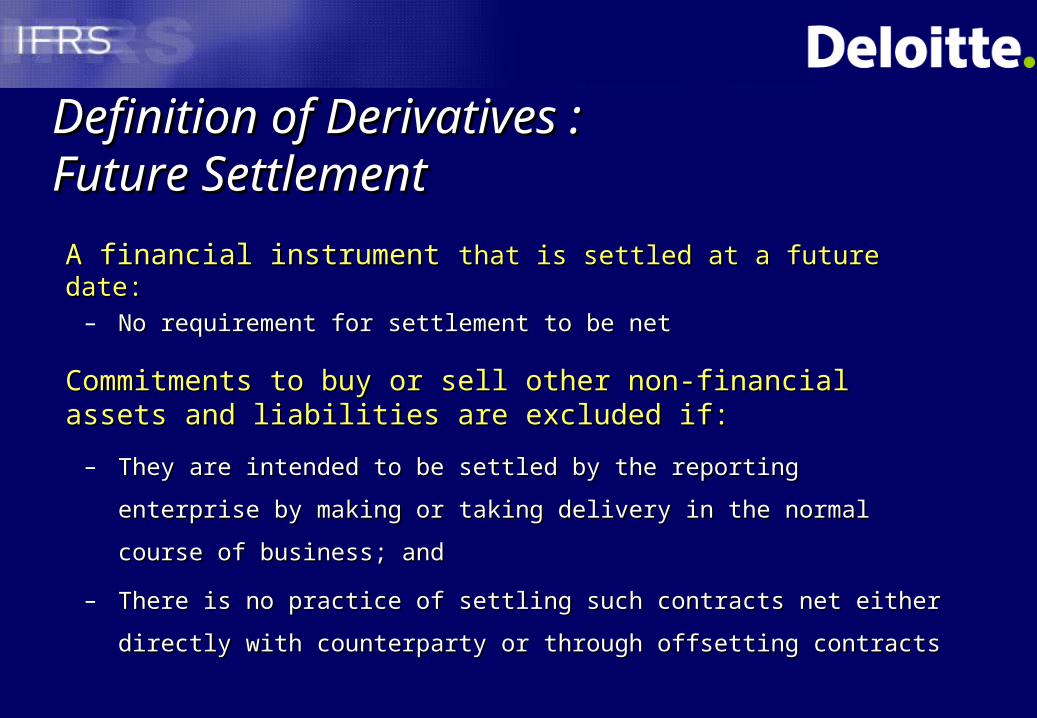

A financial instrument A financial instrument that is settled at a future date: that is settled at a future date: – No requirement for settlement to be netNo requirement for settlement to be net

Commitments to buy or sell other non-financial assets Commitments to buy or sell other non-financial assets and liabilities are excluded if:and liabilities are excluded if:

– They are intended to be settled by the reporting enterprise They are intended to be settled by the reporting enterprise

by making or taking delivery in the normal course of by making or taking delivery in the normal course of

business; andbusiness; and

– There is no practice of settling such contracts net either There is no practice of settling such contracts net either

directly with counterparty or through offsetting contractsdirectly with counterparty or through offsetting contracts

Definition of Derivatives : Definition of Derivatives : Future SettlementFuture Settlement

Embedded Derivatives:Embedded Derivatives:

Definition and TreatmentDefinition and Treatment

Definition : EDefinition : Embedded Derivativesmbedded Derivatives

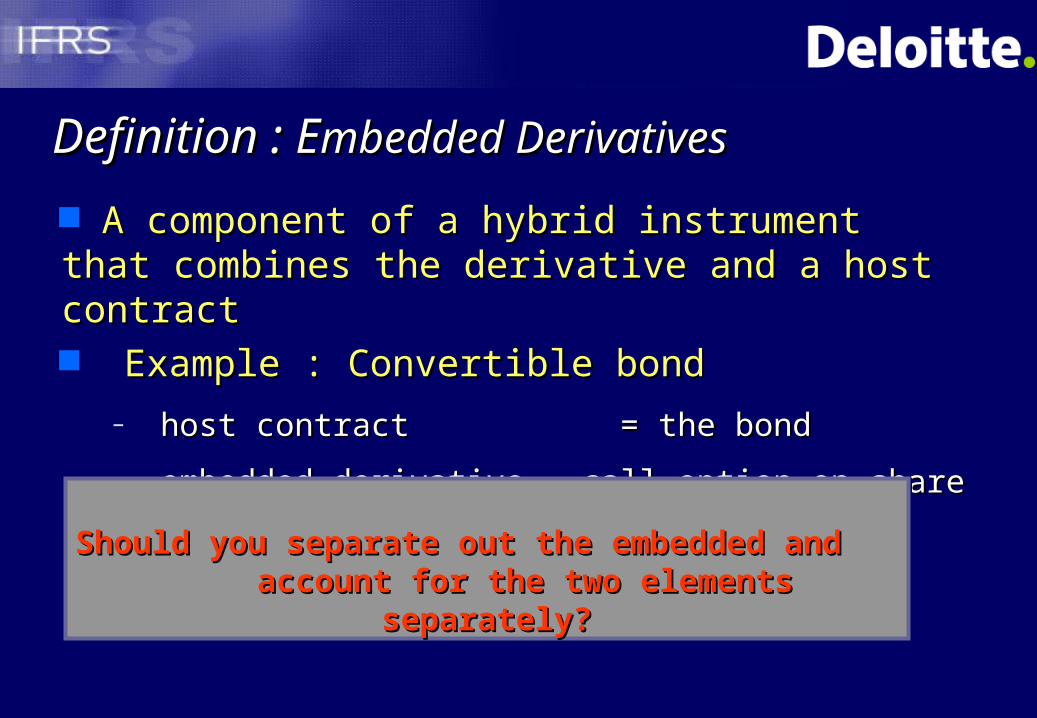

A component of a hybrid instrument that A component of a hybrid instrument that combines the derivative and a host contract combines the derivative and a host contract Example : Convertible bond Example : Convertible bond

– host contract host contract = the bond= the bond

– embedded derivative = call option on shareembedded derivative = call option on share

Should you separate out the embedded and Should you separate out the embedded and

account for the two elements separately?account for the two elements separately?

Should you separate out the embedded and Should you separate out the embedded and

account for the two elements separately?account for the two elements separately?

The economic characteristics and risks of the The economic characteristics and risks of the embedded derivative embedded derivative are not closely relatedare not closely related to the to the economic characteristics and risks of the host economic characteristics and risks of the host contract,contract,

A separate instrument with the same terms as the A separate instrument with the same terms as the embedded derivative would embedded derivative would meet the definition of meet the definition of a derivativea derivative; and; and

The hybrid (combined) instrument The hybrid (combined) instrument is not measured is not measured at fair valueat fair value with changes in fair value reported in with changes in fair value reported in net profit or loss. net profit or loss.

Embedded DerivativesEmbedded DerivativesSeparate Measurement is Appropriate Separate Measurement is Appropriate When:When:

** to the embedded derivative to the embedded derivative

Embedded Derivatives:Embedded Derivatives:Evaluating When to Separate from a Evaluating When to Separate from a Host ContractHost Contract

Is the contract carried at fairvalue through

earnings?

Would it be a derivative if it

were freestanding?

Is it closely related

to the hostcontract?

Do Not Apply IAS 39*

Apply IA

S 39*

No Yes No

Yes No Yes

Embedded Derivatives:Embedded Derivatives:What are the Consequences of What are the Consequences of Separation?Separation? If separated:

– Host contract: apply

applicable IAS

– Derivative: apply IAS 39 ie.

fair value the derivative and

it may qualify as a hedging

instrument

If not required to separate:If not required to separate:

– Apply applicable IAS to Apply applicable IAS to

the combined contractthe combined contract If required to separate, but If required to separate, but

unable to measure the unable to measure the derivative:derivative:

– The combined contract is The combined contract is

treated as a financial treated as a financial

instrument held for instrument held for

trading, carried at fair trading, carried at fair

value, and does not qualify value, and does not qualify

for hedge accountingfor hedge accounting

How should the initial carrying amounts of a host and How should the initial carrying amounts of a host and embedded derivative be determined if separation is embedded derivative be determined if separation is required? required?

Initial Carrying = Cost for the Hybrid - Fair Value of EmbeddedInitial Carrying = Cost for the Hybrid - Fair Value of Embedded

Amount of HostAmount of Host Instrument Instrument Derivative Derivative

Note:Note: More than one embedded derivative may be More than one embedded derivative may be separated from a host contract provided that they separated from a host contract provided that they represent different risks.represent different risks.

Embedded Derivatives : Embedded Derivatives : Impact of SeparationImpact of Separation

IAS 39 IAS 39

RecognitionRecognition

RecognitionRecognition

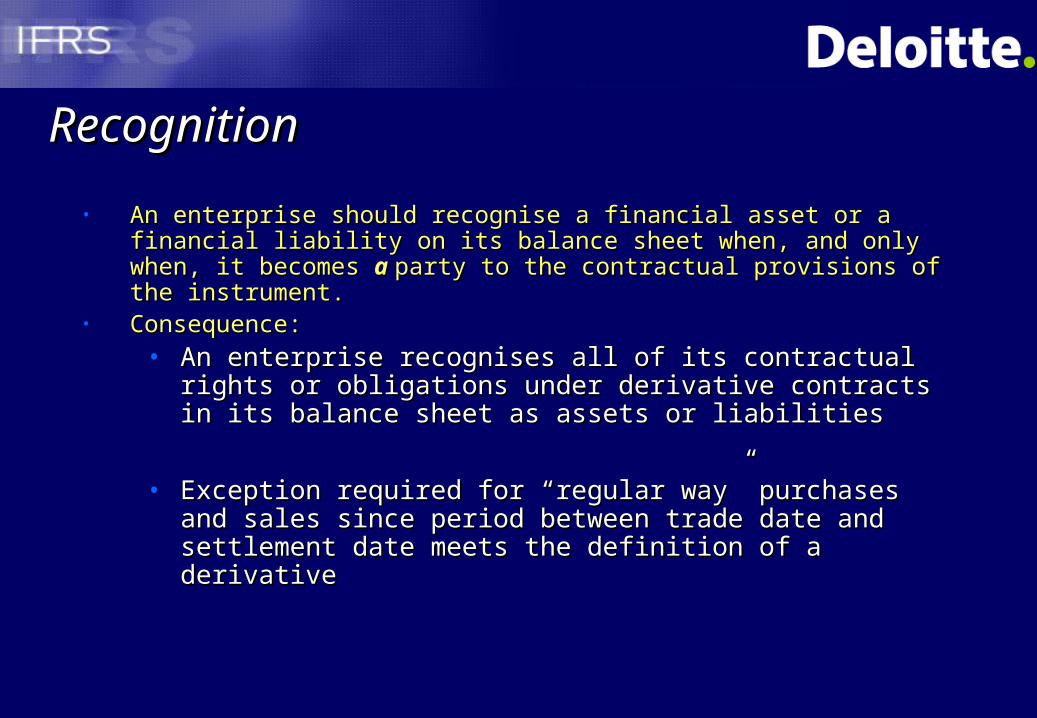

• An enterprise should recognise a financial asset or a financial An enterprise should recognise a financial asset or a financial liability on its balance sheet when, and only when, it liability on its balance sheet when, and only when, it becomes becomes a a party to the contractual provisions of the party to the contractual provisions of the instrument.instrument.

• Consequence:Consequence:• An enterprise recognises all of its contractual rights An enterprise recognises all of its contractual rights

or obligations under derivative contracts in its or obligations under derivative contracts in its balance sheet as assets or liabilitiesbalance sheet as assets or liabilities

• Exception required for “regular way” purchases and Exception required for “regular way” purchases and sales since period between trade date and sales since period between trade date and settlement date meets the definition of a derivativesettlement date meets the definition of a derivative

Recognition : “Regular Way” Recognition : “Regular Way” Purchases and SalesPurchases and Sales• A “regular way” contract for the purchase or sale of financial A “regular way” contract for the purchase or sale of financial

assets requires delivery of the assets within the time frame assets requires delivery of the assets within the time frame generally established by regulation or convention in the generally established by regulation or convention in the market place concerned market place concerned

• If the fixed price commitment between trade date and If the fixed price commitment between trade date and settlement date meets the definition of a derivative it is a settlement date meets the definition of a derivative it is a forward contractforward contract

• In view of the short duration of the derivative contract, In view of the short duration of the derivative contract, “regular way” contracts are specifically exempted from IAS “regular way” contracts are specifically exempted from IAS 3939

• A “regular way” purchase or sale of financial assets should A “regular way” purchase or sale of financial assets should therefore be recognised using either trade date accounting therefore be recognised using either trade date accounting or settlement date accounting, with consistent application or settlement date accounting, with consistent application for each category of financial assetsfor each category of financial assets

IAS 39 IAS 39

DerecognitionDerecognition

IAS 39: Derecognition IAS 39: Derecognition Provides guidance/conditions on derecognition Provides guidance/conditions on derecognition

of financial assets/liabilities.of financial assets/liabilities. Applicable to:Applicable to:

– Securitisation transactions.Securitisation transactions.

– Debts/receivables factoring.Debts/receivables factoring.

– Refinancing of loans.Refinancing of loans.

IAS 39: Derecognition of Financial IAS 39: Derecognition of Financial assetsassetsDerecognise a financial asset when and only when:Derecognise a financial asset when and only when:

Primary Condition - Transfer of AssetsPrimary Condition - Transfer of Assets Contractual rights to the cash flows expire; orContractual rights to the cash flows expire; or Entity transfers the financial assets Entity transfers the financial assets

– Transfers the contractual rights to receive cash flows; orTransfers the contractual rights to receive cash flows; or

– Retains the contractual rights to receive cash flows, but assumes a Retains the contractual rights to receive cash flows, but assumes a contractual obligation to pay cash flows to eventual recipients. In such case, contractual obligation to pay cash flows to eventual recipients. In such case, if and only if, all of the following conditions are met:if and only if, all of the following conditions are met:

Entity is not obligated to pay amounts to eventual recipients unless it collects Entity is not obligated to pay amounts to eventual recipients unless it collects

equivalent amounts from the original asset; equivalent amounts from the original asset;

Entity is prohibited from selling/pledging the original asset other than as securityEntity is prohibited from selling/pledging the original asset other than as security

Entity is obligated to remit any cash flows it collects on behalf of the eventual Entity is obligated to remit any cash flows it collects on behalf of the eventual

recipients without material delay.recipients without material delay.

IAS 39: Derecognition - transfers of IAS 39: Derecognition - transfers of financial assetfinancial asset

Secondary Condition – SignificantSecondary Condition – Significant Qualify for derecognitionQualify for derecognition if the entity: if the entity:

– Has Has transferred substantiallytransferred substantially all the risks and rewards of all the risks and rewards of ownership; orownership; or

– Has Has not retained controlnot retained control of the asset, in the case if entity has of the asset, in the case if entity has neither transferred nor retained substantially all the risks and neither transferred nor retained substantially all the risks and rewards of ownershiprewards of ownership

Do not qualify for derecognitionDo not qualify for derecognition if the entity: if the entity:– Has Has retained substantiallyretained substantially all the risks and rewards of all the risks and rewards of

ownership; orownership; or– Has Has retained controlretained control of the asset, in the case if entity has of the asset, in the case if entity has

neither transferred nor retained substantially all the risks and neither transferred nor retained substantially all the risks and rewards of ownership (rewards of ownership (also known asalso known as continuing involvement) continuing involvement)

Derecognition : Derecognition : Financial LiabilitiesFinancial Liabilities The conditions for derecognition are The conditions for derecognition are metmet when either: when either:

(i) the debtor discharges the liability by paying the creditor, (i) the debtor discharges the liability by paying the creditor, normally with cash, other financial assets, goods, or services; ornormally with cash, other financial assets, goods, or services; or

(ii) the debtor is legally released from primary responsibility for (ii) the debtor is legally released from primary responsibility for the the

liability (or part thereof) either by process of law or by the liability (or part thereof) either by process of law or by the creditor (the fact that the debtor may have given a guarantee creditor (the fact that the debtor may have given a guarantee does not necessarily mean that this condition is not met).does not necessarily mean that this condition is not met).

The condition is The condition is not metnot met when payment is made to a third party when payment is made to a third party (in substance defeasance) unless there is legal release of the (in substance defeasance) unless there is legal release of the debtor’s obligation to the creditor.debtor’s obligation to the creditor.

Derecognition : Derecognition : Financial LiabilitiesFinancial Liabilities An exchange between an existing borrower and lender of debt An exchange between an existing borrower and lender of debt

instruments with instruments with substantially different terms/modification of termssubstantially different terms/modification of terms should be accounted for as an extinguishment of the original financial should be accounted for as an extinguishment of the original financial liability and the recognition of new liability.liability and the recognition of new liability.

The terms are substantially different if the discounted present value of The terms are substantially different if the discounted present value of the cash flows under the new terms, including any fees paid net of any the cash flows under the new terms, including any fees paid net of any fees received and discounted using the original effective interest rate is at fees received and discounted using the original effective interest rate is at least 10% different from the discounted PV of the remaining cash flows of least 10% different from the discounted PV of the remaining cash flows of the original liability.the original liability.

If accounted as extinguishment, any costs and fees incurred are If accounted as extinguishment, any costs and fees incurred are recognised as part of the gain or loss on the extinguishment.recognised as part of the gain or loss on the extinguishment.

If not accounted as extinguishment, any costs or fees incurred adjust the If not accounted as extinguishment, any costs or fees incurred adjust the carrying value of the liability and are amortised over the remaining term carrying value of the liability and are amortised over the remaining term of the modified liability.of the modified liability.

IAS 39 IAS 39

Hedging and Hedge AccountingHedging and Hedge Accounting

HedgingHedging for accounting purposes means for accounting purposes means designating one or more hedging instruments so designating one or more hedging instruments so that their change in fair value is an offset, in whole that their change in fair value is an offset, in whole or in part, to the change in fair value or cash flows or in part, to the change in fair value or cash flows of a hedged item.of a hedged item.

Hedge effectivenessHedge effectiveness is the degree to which is the degree to which offsetting changes in fair value or cash flows offsetting changes in fair value or cash flows attributable to a hedged risk are achieved by the attributable to a hedged risk are achieved by the hedging instrument.hedging instrument.

Hedging : DefinitionsHedging : Definitions

A hedging instrument for hedge accounting purposes is:A hedging instrument for hedge accounting purposes is:

• a designated derivative; a designated derivative;

OROR

• (in limited circumstances) another financial asset or liability whose fair (in limited circumstances) another financial asset or liability whose fair

value or cash flows are expected to offset changes in the fair value or cash value or cash flows are expected to offset changes in the fair value or cash

flows of a designated hedged item. flows of a designated hedged item.

Under this Standard, a non-derivative financial asset or liability may be Under this Standard, a non-derivative financial asset or liability may be

designated as a hedging instrument for hedge accounting purposes designated as a hedging instrument for hedge accounting purposes

only if it hedges the risk of changes in foreign currency exchange rates.only if it hedges the risk of changes in foreign currency exchange rates.

Hedging Instrument : DefinitionHedging Instrument : Definition

Hedged Item : DefinitionHedged Item : Definition

A hedged itemA hedged item is an asset, liability, firm is an asset, liability, firm commitment, or forecasted future transaction that :commitment, or forecasted future transaction that :

• exposes the enterprise to risk of changes exposes the enterprise to risk of changes in fair value or changes in future cash in fair value or changes in future cash flows; flows;

and thatand that• for hedge accounting purposes, is for hedge accounting purposes, is

designated as being hedged.designated as being hedged.

Hedged Item : Hedged Item : What Items Can Be What Items Can Be Hedged?Hedged?

Recognised assets and liabilities - eg. bonds, loansRecognised assets and liabilities - eg. bonds, loans

Unrecognised firm commitments - eg. lease Unrecognised firm commitments - eg. lease

rentals, firm contractsrentals, firm contracts

Highly probable future transactions - eg. future Highly probable future transactions - eg. future

sales and purchasessales and purchases

A net investment in a foreign operationA net investment in a foreign operation

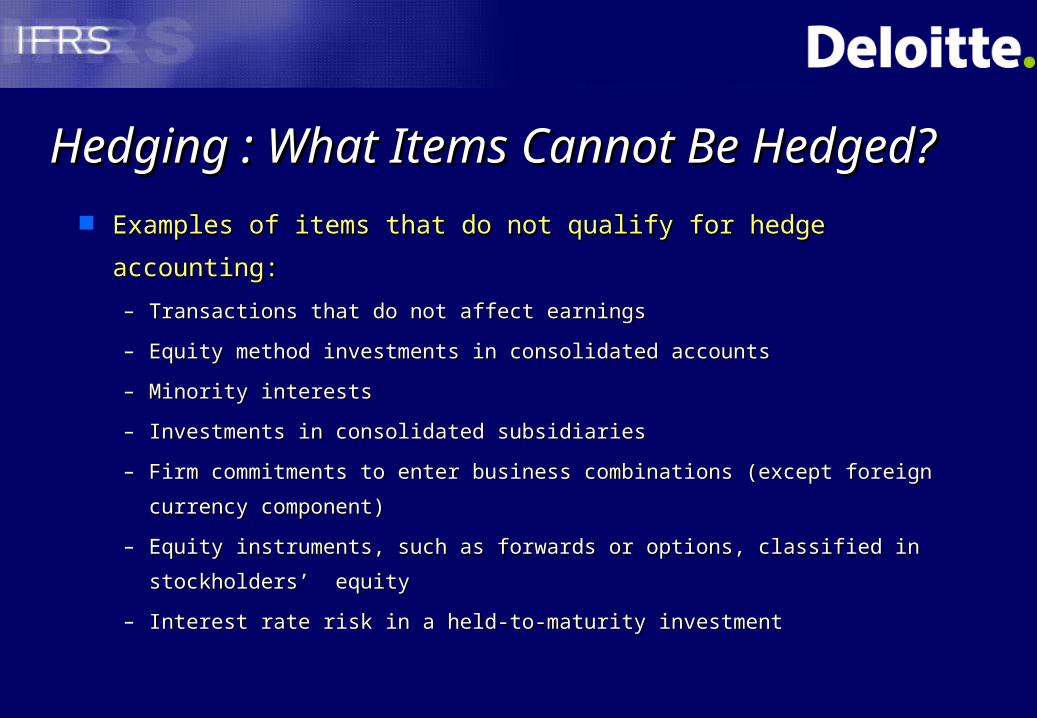

Hedging : What Items Cannot Be Hedging : What Items Cannot Be Hedged?Hedged?

Examples of items that do not qualify for hedge accounting: Examples of items that do not qualify for hedge accounting:

– Transactions that do not affect earningsTransactions that do not affect earnings

– Equity method investments in consolidated accountsEquity method investments in consolidated accounts

– Minority interestsMinority interests

– Investments in consolidated subsidiaries Investments in consolidated subsidiaries

– Firm commitments to enter business combinations (except foreign Firm commitments to enter business combinations (except foreign

currency component)currency component)

– Equity instruments, such as forwards or options, classified in Equity instruments, such as forwards or options, classified in

stockholders’ equitystockholders’ equity

– Interest rate risk in a held-to-maturity investmentInterest rate risk in a held-to-maturity investment

Hedging : Permitted Hedging Hedging : Permitted Hedging StrategiesStrategies Transaction based hedging: single risk (ie. foreign Transaction based hedging: single risk (ie. foreign

exchange or interest rate risk) hedged by a single exchange or interest rate risk) hedged by a single hedging instrumenthedging instrument

Single hedging instrument hedging more than one Single hedging instrument hedging more than one identifiable type of risk (eg. cross-currency interest identifiable type of risk (eg. cross-currency interest rate swaps)rate swaps)

Portfolios of assets or liabilities which share the same Portfolios of assets or liabilities which share the same risk exposurerisk exposure

Combinations of hedging instruments (provided that Combinations of hedging instruments (provided that they only offset the risks of the hedged items)they only offset the risks of the hedged items)

Dynamic hedging strategies (eg. delta hedging)Dynamic hedging strategies (eg. delta hedging)

Hedging : Prohibited Hedging Hedging : Prohibited Hedging StrategiesStrategies Macro hedging (except for a portfolio hedge Macro hedging (except for a portfolio hedge

of interest rate risk under certain conditions)of interest rate risk under certain conditions) Intra-group or intra-division hedging Intra-group or intra-division hedging

strategies (eg. between banking book and strategies (eg. between banking book and trading book)trading book)

Portfolio hedging where assets or liabilities do Portfolio hedging where assets or liabilities do not share the same risknot share the same risk

Use of written options (other than to hedge Use of written options (other than to hedge purchased options)purchased options)

Hedging of interest rate risk on held-to-Hedging of interest rate risk on held-to-maturity financial assetsmaturity financial assets

Hedge Accounting : What Conditions Hedge Accounting : What Conditions Are Necessary?Are Necessary?

Formal documentation (hedging relationship and risk Formal documentation (hedging relationship and risk

management objectives and strategy)management objectives and strategy)

Hedge is expected to be highly effective Hedge is expected to be highly effective

Effectiveness of the hedge can be measured and is assessed on Effectiveness of the hedge can be measured and is assessed on

an ongoing basis throughout the financial reporting periodan ongoing basis throughout the financial reporting period

Hedged forecasted transactions must be highly probable and Hedged forecasted transactions must be highly probable and

must present an exposure to variations in cash flows that must present an exposure to variations in cash flows that

ultimately affect reported net profit or lossultimately affect reported net profit or loss

Hedge Accounting : Documentation Hedge Accounting : Documentation RequirementsRequirements

The hedging documentation dealing with hedges against The hedging documentation dealing with hedges against particular risks should be formal and include the following particular risks should be formal and include the following elements:elements:

– nature of hedging relationshipnature of hedging relationship– risk management objective and strategy for undertaking hedgerisk management objective and strategy for undertaking hedge– identification of the hedging instrumentidentification of the hedging instrument– identification of the related hedged item or transactionidentification of the related hedged item or transaction– the nature of the risk being hedged (particular risk)the nature of the risk being hedged (particular risk)– description of how the enterprise will assess the hedging description of how the enterprise will assess the hedging

instrument’s effectiveness in offsetting the exposure to instrument’s effectiveness in offsetting the exposure to changes in the hedged item’s fair value or the hedged changes in the hedged item’s fair value or the hedged transaction’s cash flows that is attributable to the hedged risk.transaction’s cash flows that is attributable to the hedged risk.

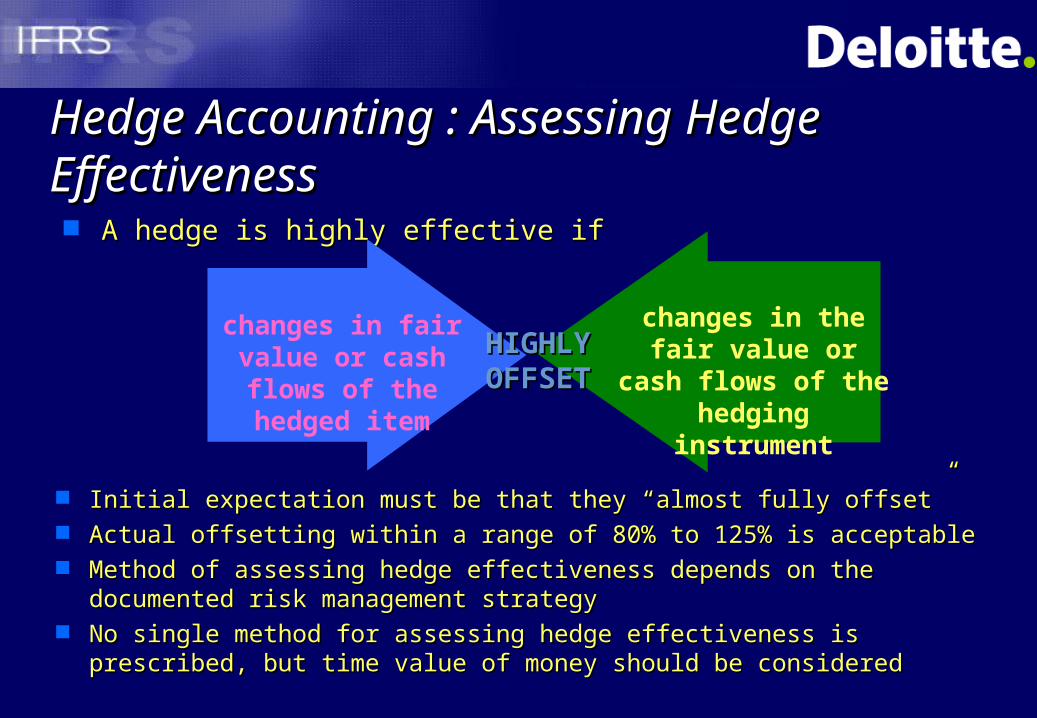

Hedge Accounting : Assessing Hedge Hedge Accounting : Assessing Hedge EffectivenessEffectiveness A hedge is highly effective ifA hedge is highly effective if

changes in fair value or cash flows of the

hedged item

changes in the fair value or cash flows

of the hedging instrument

HIGHLYHIGHLYOFFSETOFFSET

Initial expectation must be that they “almost fully offset”Initial expectation must be that they “almost fully offset” Actual offsetting within a range of 80% to 125% is acceptableActual offsetting within a range of 80% to 125% is acceptable Method of assessing hedge effectiveness depends on the Method of assessing hedge effectiveness depends on the

documented risk management strategy documented risk management strategy No single method for assessing hedge effectiveness is prescribed, No single method for assessing hedge effectiveness is prescribed,

but time value of money should be consideredbut time value of money should be considered

Types of Hedging Types of Hedging RelationshipsRelationships

Hedge Accounting : Hedge Accounting : Types of Hedging Types of Hedging Relationships Relationships

1.1. Fair value hedge - hedge of the variability of Fair value hedge - hedge of the variability of changes in fair changes in fair value of a recognised asset or liability or a firm commitment value of a recognised asset or liability or a firm commitment (e.g. an interest rate swap that hedges the risk that the fair (e.g. an interest rate swap that hedges the risk that the fair value of a fixed rate bond will fluctuate, or a hedge of a firm value of a fixed rate bond will fluctuate, or a hedge of a firm commitment to buy an asset at a fixed price) commitment to buy an asset at a fixed price)

2.2. Cash flow hedge - hedge of exposure to Cash flow hedge - hedge of exposure to variability in cash variability in cash flowsflows on a recognised asset or liability, or a forecasted on a recognised asset or liability, or a forecasted transactiontransaction(e.g.. an interest rate swap that hedges the risk that the cash flows on a variable rate bond will fluctuate, or a hedge of a forecasted purchase /sale of asset)

3.3. Hedge of a Hedge of a net investment in foreign operationsnet investment in foreign operations (IAS 21) (IAS 21)

Definition of a Fair Value HedgeDefinition of a Fair Value Hedge

A fair value hedge is: A fair value hedge is: ““a hedge of the exposure to changes in the fair a hedge of the exposure to changes in the fair value of a recognised asset or liability or a firm value of a recognised asset or liability or a firm commitment, or an identified portion of such an commitment, or an identified portion of such an asset or liability, that is attributable to a asset or liability, that is attributable to a particular risk and that will affect reported net particular risk and that will affect reported net income”income”

Key issues:Key issues: hedged asset or liability must be recognised on hedged asset or liability must be recognised on

balance sheetbalance sheet hedged risk must give rise to a risk of changes in hedged risk must give rise to a risk of changes in

fair value of hedged asset or liabilityfair value of hedged asset or liability

Cash flow hedge: Cash flow hedge: a hedge of the a hedge of the exposure to variability in exposure to variability in cash flowscash flows that: that:• is attributable to a is attributable to a particular risk associated particular risk associated

with a recognised assetwith a recognised asset or liabilityor liability (such as all (such as all or some future interest payments on variable or some future interest payments on variable rate debt) or a rate debt) or a forecasted transactionforecasted transaction (such as (such as an anticipated purchase or sale) and that an anticipated purchase or sale) and that

• will will affect reported net profit or lossaffect reported net profit or loss..

Definition of a Definition of a Cash Cash FFlow low HHedge edge

Hedge of a Firm Commitment Hedge of a Firm Commitment

A hedge of a firm commitment:A hedge of a firm commitment: Represents a fair value exposureRepresents a fair value exposure

Except forExcept for A hedge of the foreign currency risk of a A hedge of the foreign currency risk of a

firm commitment which could be firm commitment which could be accounted for as a fair value hedge or as a accounted for as a fair value hedge or as a cash flows hedge.cash flows hedge.

Hedge accounting: Hedge accounting: Hedges of a Net Hedges of a Net Investment in a Foreign Operations Investment in a Foreign Operations

Hedges of net investments in a foreign operations, including a hedge Hedges of net investments in a foreign operations, including a hedge of a monetary item that is accounted for as part of the net investment, of a monetary item that is accounted for as part of the net investment, should be accounted for in the same way as cash flow hedges:should be accounted for in the same way as cash flow hedges:

the portion of the gain or loss on the hedging instrument that is the portion of the gain or loss on the hedging instrument that is effectiveeffective should be recognised in should be recognised in equityequity

the the ineffectiveineffective portion should be reported immediately in net portion should be reported immediately in net profit or lossprofit or loss

The effective portion’s gain / loss recognised in equity should be The effective portion’s gain / loss recognised in equity should be recognised in recognised in profit or lossprofit or loss upon disposalupon disposal of foreign operations of foreign operations

Hedge Accounting - SummaryHedge Accounting - Summary

Hedge accounting is a privilege not a rightHedge accounting is a privilege not a right Designation and documentation are essential prior to Designation and documentation are essential prior to

beginning hedge accountingbeginning hedge accounting Common hedging strategies, including macro hedging Common hedging strategies, including macro hedging

and use of internal derivatives, may not be permittedand use of internal derivatives, may not be permitted Only derivatives can be designated as hedging Only derivatives can be designated as hedging

instruments other than for foreign exchange risk, instruments other than for foreign exchange risk, where non-derivative instruments can be usedwhere non-derivative instruments can be used

Hedge accounting is available for recognised assets Hedge accounting is available for recognised assets and liabilities, firm commitments and forecasted and liabilities, firm commitments and forecasted transactionstransactions

Disclosure RequirementsDisclosure Requirements

IAS 32: Disclosure RequirementsIAS 32: Disclosure Requirements ObjectiveObjective

– To provide information to enhance understanding of financial instruments to an entity’s financial position, performance and cash flows, and assist in assessing the amounts, To provide information to enhance understanding of financial instruments to an entity’s financial position, performance and cash flows, and assist in assessing the amounts, timing and certainty of future cash flows.timing and certainty of future cash flows.

Format, location and classes of financial instrumentsFormat, location and classes of financial instruments– IAS 32 does not prescribe either the format of information required or its location within the financial statements.IAS 32 does not prescribe either the format of information required or its location within the financial statements.

Key disclosure requirementsKey disclosure requirements– Risk management policies and hedging activities.Risk management policies and hedging activities.– Terms, conditions and accounting policies.Terms, conditions and accounting policies.– Interest rate risk.Interest rate risk.– Credit risk.Credit risk.– Fair value.Fair value.– Other disclosures. Other disclosures.

Questions and AnswersQuestions and Answers