Embed Size (px)

Citation preview

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 1

IBISWorld Industry Report 71394Gym, Health & Fitness Clubs in the USJanuary 2016 Sarah Turk

Working out: As disposable incomes rise, more individuals will purchase gym memberships

2 About this Industry2 Industry Definition

2 Main Activities

2 Similar Industries

3 Additional Resources

4 Industry at a Glance

5 Industry Performance5 Executive Summary

5 Key External Drivers

7 Current Performance

9 Industry Outlook

11 Industry Life Cycle

13 Products & Markets13 Supply Chains

13 Products & Services

14 Demand Determinants

15 Major Markets

16 International Trade

17 Business Locations

19 Competitive Landscape19 Market Share Concentration

19 Key Success Factors

19 Cost Structure Benchmarks

21 Basis of Competition

22 Barriers to Entry

23 Industry Globalization

24 Major Companies

26 Operating Conditions26 Capital Intensity

27 Technology & Systems

27 Revenue Volatility

28 Regulation & Policy

29 Industry Assistance

30 Key Statistics30 Industry Data

30 Annual Change

30 Key Ratios

31 Jargon & Glossary

www.ibisworld.com | 1-800-330-3772 | [email protected]

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 2

This industry operates fitness and recreational sports facilities that feature exercise and other active physical fitness conditioning or recreational sports

activities, such as swimming, skating or racquet sports. Operators are also involved in facilities management and fitness instruction.

The primary activities of this industry are

Operating aerobic dance and exercise centers

Operating athletic club facilities for physical fitness

Operating body building studios for physical fitness

Operating fitness centers, health clubs and gyms

Operating recreational sports club facilities

Operating ice or roller skating rinks

Operating spas

Operating squash, racquetball or tennis clubs

Operating swimming pools

71399 Golf Driving Ranges & Family Fun Centers in the USEstablishments in this industry operate recreational sports clubs (i.e. sports teams), but do not operate sports facilities.

72111 Hotels & Motels in the USEstablishments in this industry are primarily engaged in operating health resorts and spas where recreational facilities are combined with accommodations.

81219a Weight Loss Services in the USEstablishments in this industry are primarily engaged in providing nonmedical services to assist clients in attaining or maintaining a desired weight.

81219c Tanning Salons in the USEstablishments in this industry are primarily engaged in providing artificial tanning services.

Industry Definition

Main Activities

Similar Industries

About this Industry

The major products and services in this industry are

Athletic instruction (excluding personal training services)

Guest admission sales

Meals and beverages

Membership fees

Merchandise sales

Personal training services

Spa services

Other

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 3

About this Industry

For additional information on this industry

www.ihrsa.org International Health, Racquet and Sportsclub Association

www.physicalfitness.org National Association for Health and Fitness

www.sfia.org Sports and Fitness Industry Association

Additional Resources

IBISWorld writes over 700 US industry reports, which are updated up to four times a year. To see all reports, go to www.ibisworld.com

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 4

hour

s pe

r day

per

cap

ita

5.4

5.0

5.1

5.2

5.3

2006 08 10 12 14 16 18Year

Time spent on leisure and sports

SOURCE: WWW.IBISWORLD.COM

% c

hang

e

12

-6

-3

0

3

6

9

2208 10 12 14 16 18 20Year

Revenue Employment

Revenue vs. employment growth

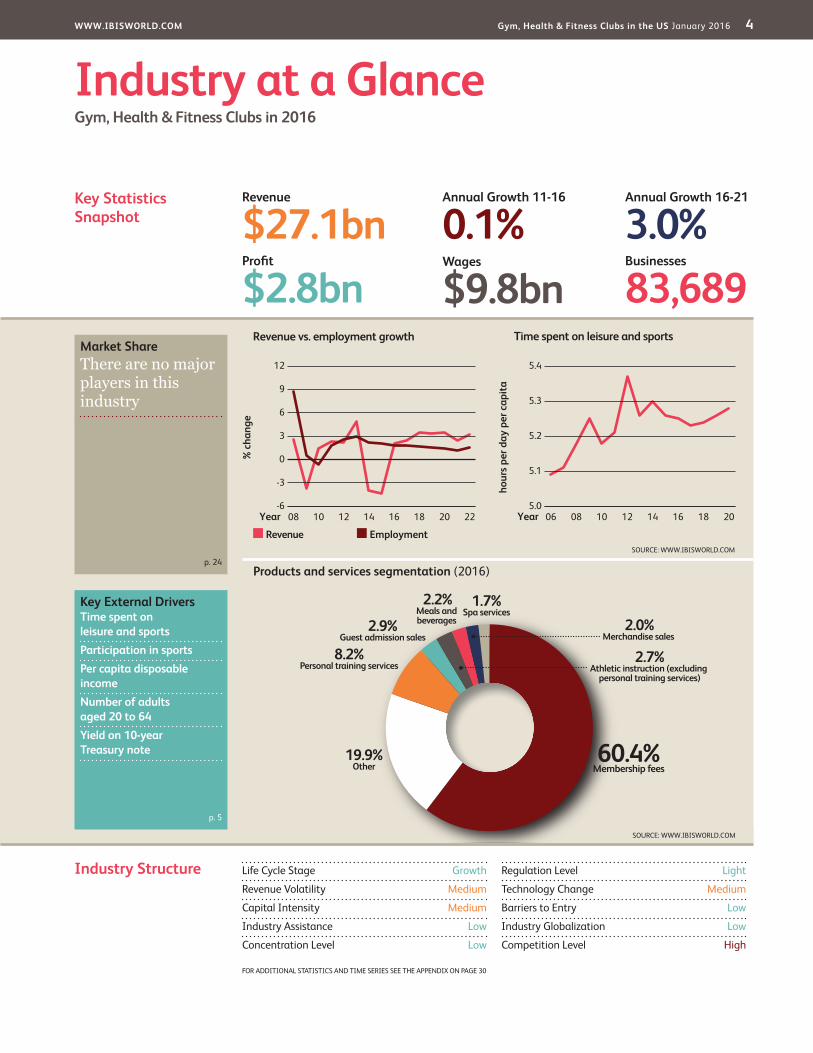

Products and services segmentation (2016)

60.4%Membership fees

2.2%Meals and beverages

19.9%Other

2.0%Merchandise sales

1.7%Spa services

8.2%Personal training services

2.9%Guest admission sales

2.7%Athletic instruction (excluding

personal training services)

SOURCE: WWW.IBISWORLD.COM

Key Statistics Snapshot

Industry at a GlanceGym, Health & Fitness Clubs in 2016

Industry Structure Life Cycle Stage Growth

Revenue Volatility Medium

Capital Intensity Medium

Industry Assistance Low

Concentration Level Low

Regulation Level Light

Technology Change Medium

Barriers to Entry Low

Industry Globalization Low

Competition Level High

Revenue

$27.1bnProfit

$2.8bnWages

$9.8bnBusinesses

83,689

Annual Growth 16-21

3.0%Annual Growth 11-16

0.1%

Key External DriversTime spent on leisure and sportsParticipation in sportsPer capita disposable incomeNumber of adults aged 20 to 64Yield on 10-year Treasury note

Market ShareThere are no major players in this industry

p. 24

p. 5

FOR ADDITIONAL STATISTICS AND TIME SERIES SEE THE APPENDIX ON PAGE 30

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 5

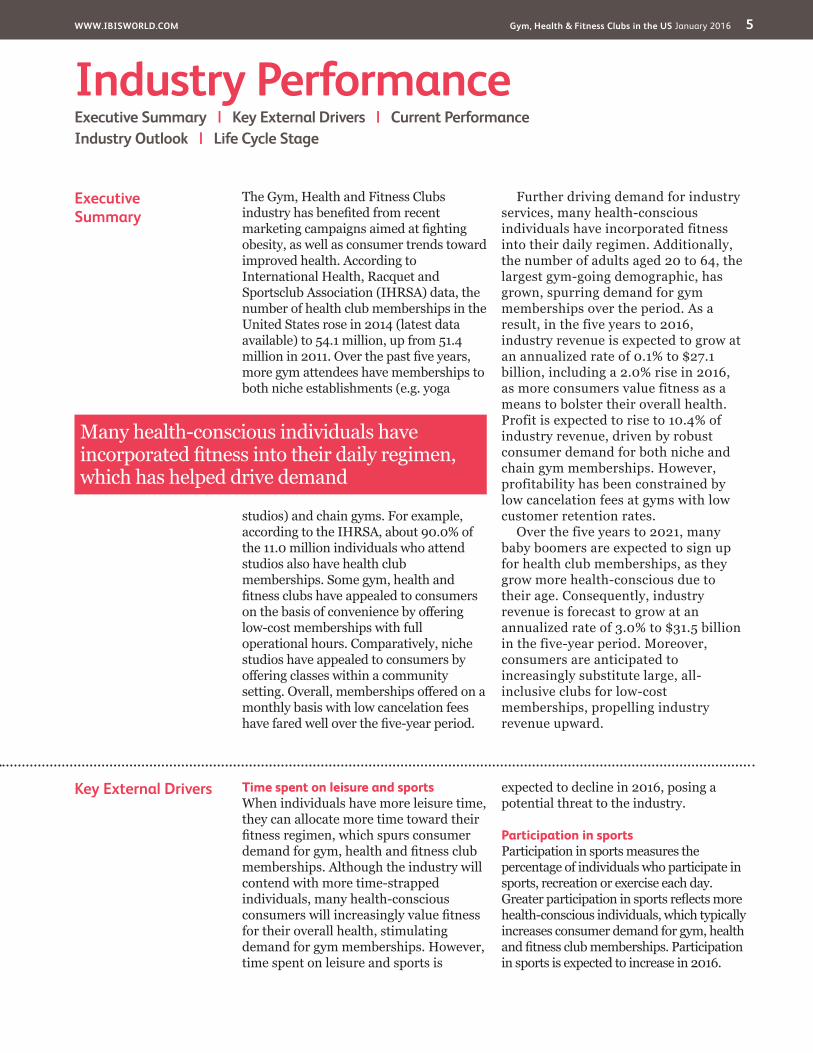

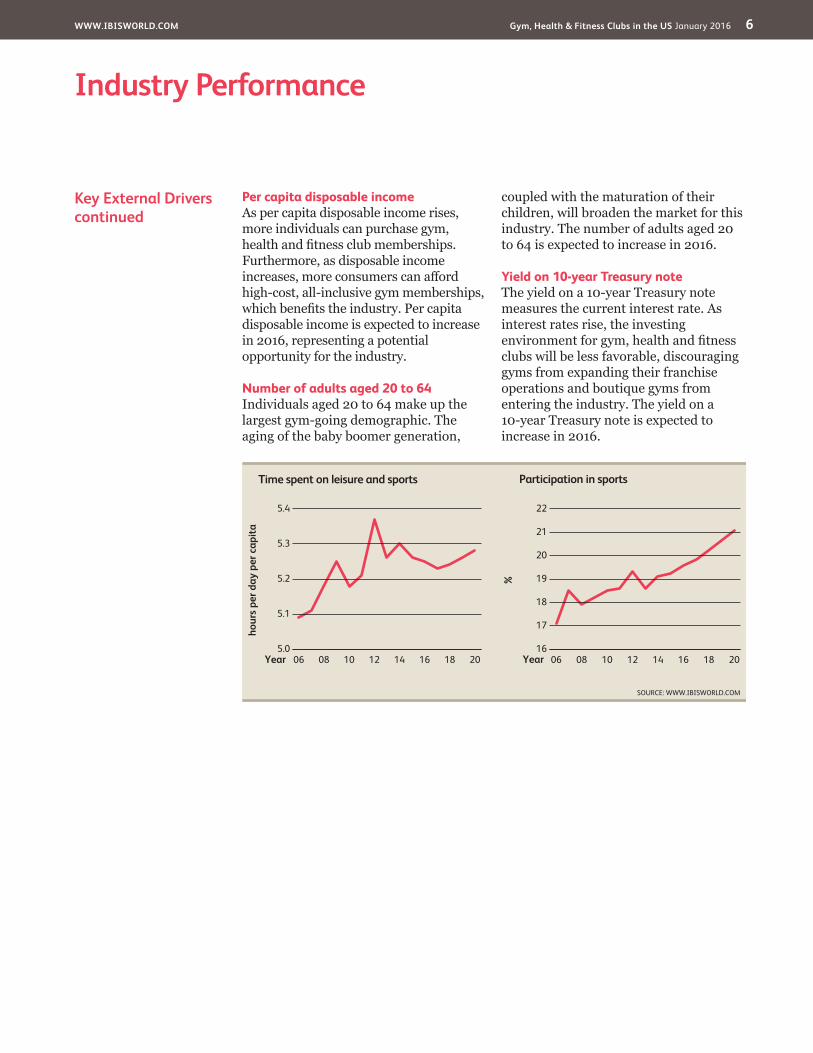

Key External Drivers Time spent on leisure and sportsWhen individuals have more leisure time, they can allocate more time toward their fitness regimen, which spurs consumer demand for gym, health and fitness club memberships. Although the industry will contend with more time-strapped individuals, many health-conscious consumers will increasingly value fitness for their overall health, stimulating demand for gym memberships. However, time spent on leisure and sports is

expected to decline in 2016, posing a potential threat to the industry.

Participation in sportsParticipation in sports measures the percentage of individuals who participate in sports, recreation or exercise each day. Greater participation in sports reflects more health-conscious individuals, which typically increases consumer demand for gym, health and fitness club memberships. Participation in sports is expected to increase in 2016.

Executive Summary

The Gym, Health and Fitness Clubs industry has benefited from recent marketing campaigns aimed at fighting obesity, as well as consumer trends toward improved health. According to International Health, Racquet and Sportsclub Association (IHRSA) data, the number of health club memberships in the United States rose in 2014 (latest data available) to 54.1 million, up from 51.4 million in 2011. Over the past five years, more gym attendees have memberships to both niche establishments (e.g. yoga

studios) and chain gyms. For example, according to the IHRSA, about 90.0% of the 11.0 million individuals who attend studios also have health club memberships. Some gym, health and fitness clubs have appealed to consumers on the basis of convenience by offering low-cost memberships with full operational hours. Comparatively, niche studios have appealed to consumers by offering classes within a community setting. Overall, memberships offered on a monthly basis with low cancelation fees have fared well over the five-year period.

Further driving demand for industry services, many health-conscious individuals have incorporated fitness into their daily regimen. Additionally, the number of adults aged 20 to 64, the largest gym-going demographic, has grown, spurring demand for gym memberships over the period. As a result, in the five years to 2016, industry revenue is expected to grow at an annualized rate of 0.1% to $27.1 billion, including a 2.0% rise in 2016, as more consumers value fitness as a means to bolster their overall health. Profit is expected to rise to 10.4% of industry revenue, driven by robust consumer demand for both niche and chain gym memberships. However, profitability has been constrained by low cancelation fees at gyms with low customer retention rates.

Over the five years to 2021, many baby boomers are expected to sign up for health club memberships, as they grow more health-conscious due to their age. Consequently, industry revenue is forecast to grow at an annualized rate of 3.0% to $31.5 billion in the five-year period. Moreover, consumers are anticipated to increasingly substitute large, all-inclusive clubs for low-cost memberships, propelling industry revenue upward.

Industry PerformanceExecutive Summary | Key External Drivers | Current Performance Industry Outlook | Life Cycle Stage

Many health-conscious individuals have incorporated fitness into their daily regimen, which has helped drive demand

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 6

Industry Performance

Key External Driverscontinued

Per capita disposable incomeAs per capita disposable income rises, more individuals can purchase gym, health and fitness club memberships. Furthermore, as disposable income increases, more consumers can afford high-cost, all-inclusive gym memberships, which benefits the industry. Per capita disposable income is expected to increase in 2016, representing a potential opportunity for the industry.

Number of adults aged 20 to 64Individuals aged 20 to 64 make up the largest gym-going demographic. The aging of the baby boomer generation,

coupled with the maturation of their children, will broaden the market for this industry. The number of adults aged 20 to 64 is expected to increase in 2016.

Yield on 10-year Treasury noteThe yield on a 10-year Treasury note measures the current interest rate. As interest rates rise, the investing environment for gym, health and fitness clubs will be less favorable, discouraging gyms from expanding their franchise operations and boutique gyms from entering the industry. The yield on a 10-year Treasury note is expected to increase in 2016.

%22

16

17

18

19

20

21

2006 08 10 12 14 16 18Year

Participation in sports

SOURCE: WWW.IBISWORLD.COM

hour

s pe

r day

per

cap

ita

5.4

5.0

5.1

5.2

5.3

2006 08 10 12 14 16 18Year

Time spent on leisure and sports

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 7

Industry Performance

Industry landscape Over the five years to 2016, the industry has benefited from rising consumer demand for health club memberships. According to the International Health, Racquet and Sportsclub Association (IHRSA), gym membership increased at an annualized rate of 1.7% to 54.1 million memberships from 2011 to 2014 (latest data available). Although this bolstered industry revenue, many gyms still compete on the basis of price. Gyms that have offered low-cost, contract-free memberships with fewer amenities have fared well over the period, which is in line with strong demand from budget-conscious consumers. The industry has contended with consumer time constraints over the period, with many individuals struggling to allocate time

toward fitness. Nevertheless, health-conscious individuals are still increasingly incorporating fitness into their regimen.

Demographic trends have helped shape the industry’s landscape over the past five years. For example, the aging of the baby-boomer generation and the maturation of their offspring have broadened the industry’s market. Moreover, government-sponsored programs, such as Michelle Obama’s “Let’s Move!” initiative, which aims to fight childhood obesity, have increased awareness to the benefits of physical exercise for consumers of all ages. Over the past five years, this and other health programs have provided a boon to the industry.

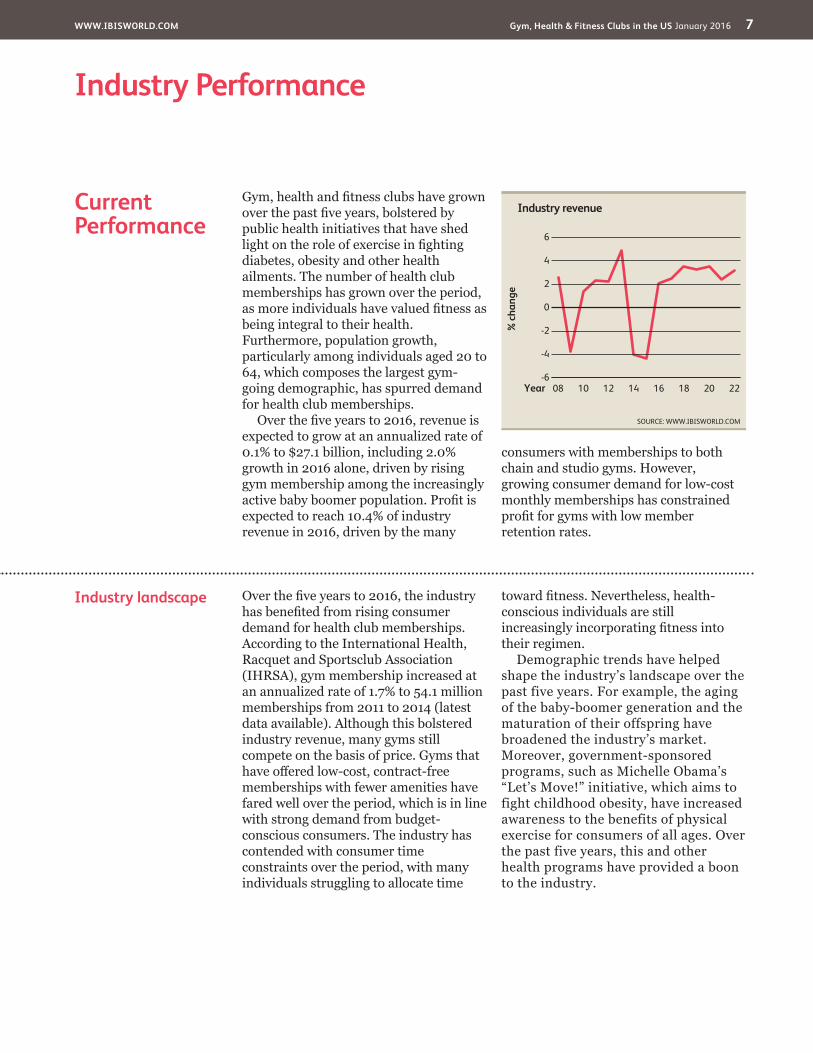

Gym, health and fitness clubs have grown over the past five years, bolstered by public health initiatives that have shed light on the role of exercise in fighting diabetes, obesity and other health ailments. The number of health club memberships has grown over the period, as more individuals have valued fitness as being integral to their health. Furthermore, population growth, particularly among individuals aged 20 to 64, which composes the largest gym-going demographic, has spurred demand for health club memberships.

Over the five years to 2016, revenue is expected to grow at an annualized rate of 0.1% to $27.1 billion, including 2.0% growth in 2016 alone, driven by rising gym membership among the increasingly active baby boomer population. Profit is expected to reach 10.4% of industry revenue in 2016, driven by the many

consumers with memberships to both chain and studio gyms. However, growing consumer demand for low-cost monthly memberships has constrained profit for gyms with low member retention rates.

Current Performance

% c

hang

e

6

-6

-4

-2

0

2

4

2208 10 12 14 16 18 20Year

Industry revenue

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 8

Industry Performance

As operators try to attract consumers with low-cost, contract-free and low-amenity memberships, many industry players have limited their expansion to control operational costs. However, industry establishments have grown at an annualized rate of 0.7% to 91,758 facilities over the five years to 2016, despite many large industry players acquiring small, niche gyms that cater to local clientele.

To address consumers’ preference for local, boutique gyms and fitness centers,

some gyms are increasingly providing smaller facilities. For example, Curves has significantly streamlined its number of franchise locations over the five-year period, partly because some of its franchises were unable to compete with local, low-cost gyms that offer longer operating hours. During the five-year period, employment in the industry is expected to grow an annualized 2.3% to 713,171 workers as demand for fitness instructors increases in line with growth in health club memberships.

Enterprises and employment

The emergence of the budget-conscious gym member has also considerably changed the industry’s landscape. A growing preference for easily accessible, smaller gyms with fewer amenities has benefited boutique gyms that cater to a niche local market. The market share of budget gyms is consequently growing, as consumers have substituted these gyms for expensive, all-inclusive clubs that include related facilities, such as tennis and racquetball courts, ice rinks and swimming pools.

For example, Planet Fitness is the fastest-growing full-size health club franchise in the United States, with the company offering low membership prices that range from $10.00 to $19.99 a month. Moreover, the company has attempted to appeal to new gym goers by providing a

“Judgement Free Zone.” Since 2011, the number of Planet Fitness locations has skyrocketed from about 616 to more than 1,000 locations. Other growing franchises include Snap and Anytime Fitness, which have both demonstrated the popularity of chain gyms that target budget-conscious clientele. Moreover, consumers who seek individualized fitness programs, specific fitness goals or are uncomfortable exercising in larger gyms have particularly favored such small-scale gyms.

Fitness trends The emergence of the budget-conscious gym member has considerably changed the industry

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 9

Industry Performance

New demographics Over the next five years, demographic changes will increasingly drive revenue growth. For example, the baby boomer population, which is becoming increasingly active, will purchase gym memberships to maintain healthier lifestyles. Additional revenue streams will also play an integral part in industry growth. In particular, as healthcare costs continue to escalate, health insurance providers may implement incentives to promote preventive health practices, including the use of fitness centers among individuals within their provider network. Furthermore, the number of obese individuals in the United States is increasing. According to a study by the Centers for Disease Control and Prevention, an estimated 42.0% of Americans will be considered obese by 2030. Consequently, to cut healthcare costs, many health insurance providers will attempt to lower individuals’ risk for type 2 diabetes, heart disease, dementia, cancer and high blood pressure, among other health ailments. Additionally, initiatives that shed light on the health benefits of exercise will likely proliferate over the next five years, stimulating industry revenue.

Employers are increasingly viewing exercise as a vital component of employee

health due to studies indicating that fitness can boost worker productivity. As a result, employers may increasingly subsidize gym memberships for their employees, providing a boon to the industry. Furthermore, as many families become health- and fitness-conscious, more consumers aged 17 and younger will purchase gym memberships. Less physical education in schools, coupled with growing concerns regarding childhood obesity, will prompt gym membership sales for this age demographic. As consumers become increasingly time strapped, many will invest in fitness classes and individual or group sessions with trainers to obtain their fitness goals more efficiently. In the next five years, group classes are expected to increase in popularity, especially fusion classes that combine yoga, Pilates, ballet, dance and surfing.

Industry Outlook

Over the five years to 2021, the Gym, Health and Fitness Clubs industry will lift itself to success, benefiting from an expected revitalization in discretionary consumer spending. As consumers’ disposable incomes rise, more individuals will purchase gym memberships that include a plethora of amenities, compared with low-cost memberships that fared well over the previous period. Moreover, while many individuals will be time-strapped over the period, which may constrain demand for gym memberships, growing demand for results-driven gyms that can help individuals achieve fitness goals will

continue to drive growth. For example, personal and group trainers, as well as fitness classes, will be popular.

In the five years to 2021, revenue is forecast to grow at an annualized rate of 3.0% to $31.5 billion as more consumers purchase high-cost industry services, such as cohesive, individualized health plans that include trainers and nutritional guidance. Profit is also expected to rise from 10.4% of industry revenue in 2016 to 12.4% by 2021, as many gyms offer more high-margin services, such as group personal training sessions, to strengthen their product portfolio and bolster member retention rates.

Employers are increasingly viewing exercise as a vital component of employee health

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 10

Industry Performance

Industry landscape While large-scale gyms will continue to dominate the industry landscape by offering a diverse portfolio of services, many small gyms will persist in attracting a niche local market. In particular, small operators will attempt to entice local, time-strapped customer bases by offering conveniently located establishments in unsaturated areas. However, large industry operators can somewhat mitigate this trend by attracting consumers via technology, such as phone applications that enable gym users to access their fitness statistics from previous sessions.

In the five years to 2021, the number of industry enterprises is anticipated to contract at an annualized rate of 0.8% to

80,483 operators, as some small, independently operated gyms and fitness clubs exit the market due to strong competition from chain gyms and fitness clubs. Additionally, the number of industry employees is expected to grow at an annualized rate of 1.5% to 768,659 people over the same period, as industry operators implement a larger workforce to provide additional services, such as fitness classes and spa services, to develop and retain their clientele.

Many small gyms will persist in attracting a niche local market

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 11

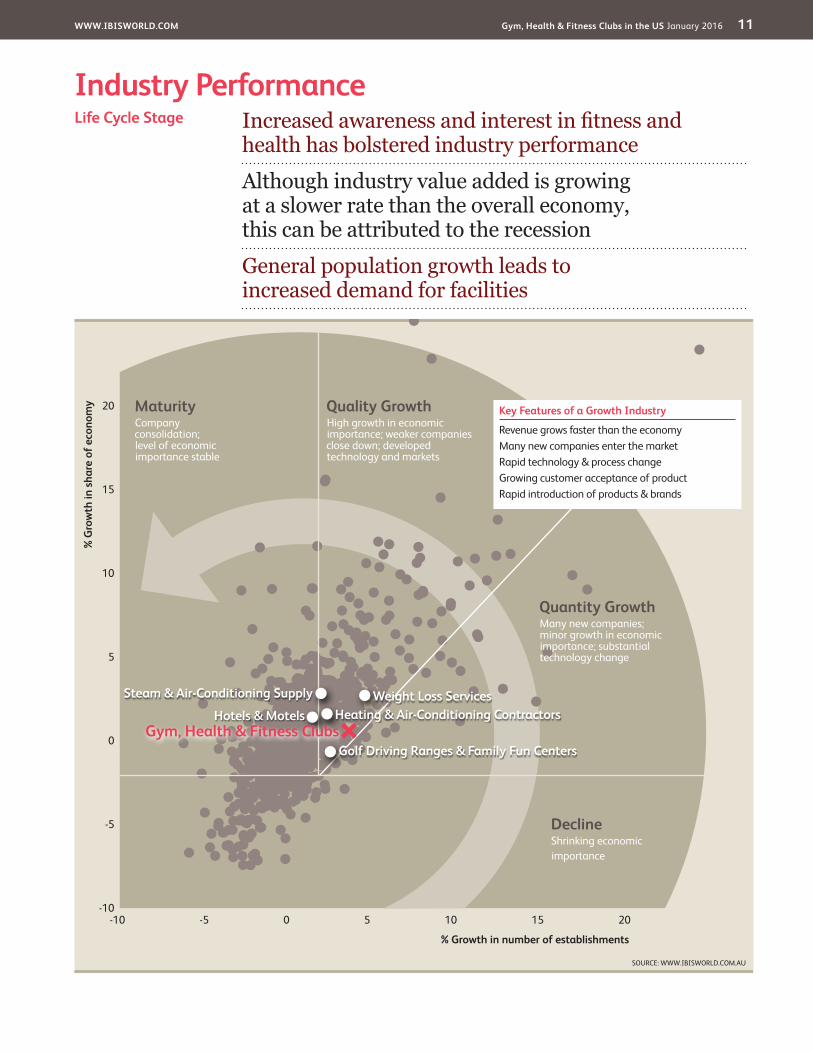

Industry PerformanceIncreased awareness and interest in fitness and health has bolstered industry performance

Although industry value added is growing at a slower rate than the overall economy, this can be attributed to the recession

General population growth leads to increased demand for facilities

Life Cycle Stage

SOURCE: WWW.IBISWORLD.COM.AU

20

15

10

5

0

-5

-10

% G

row

th in

sha

re o

f eco

nom

y

% Growth in number of establishments

-10 -5 0 5 10 15 20

DeclineShrinking economicimportance

Quality GrowthHigh growth in economic importance; weaker companies close down; developed technology and markets

MaturityCompany consolidation;level of economic importance stable

Quantity GrowthMany new companies; minor growth in economic importance; substantial technology change

Key Features of a Growth Industry

Revenue grows faster than the economyMany new companies enter the marketRapid technology & process changeGrowing customer acceptance of productRapid introduction of products & brands

Golf Driving Ranges & Family Fun Centers

Steam & Air-Conditioning Supply

Hotels & Motels Heating & Air-Conditioning ContractorsWeight Loss Services

Gym, Health & Fitness Clubs

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 12

Industry Performance

Industry Life Cycle The Gym, Health and Fitness Clubs industry is in the growth life cycle stage, because consumers continue to be interested in exercise to boost their fitness and health. During the 10 years to 2021, industry value added (IVA), a measure of an industry’s contribution to the overall economy, is expected to grow at an annualized rate of 2.9%. Comparatively, GDP is anticipated to grow an annualized 2.3% over the same period.

Since many consumers were budget conscious, some purchased low-cost gym memberships with fewer amenities, hampering industry profitability and constraining industry revenue growth. However, IBISWorld expects a growing per capita disposable income and

declining leisure time to encourage consumers to purchase personal trainers to accomplish fitness goals, reversing the trend toward low-cost memberships.

As public health campaigns spread awareness about the health benefits of fitness, consumers will increasingly perceive gym and fitness club membership as a vital expense. As gym memberships become more entrenched in the average American’s life, revenue growth will slow to match population growth, bringing the industry from growth to maturity. Future growth areas will likely be in participative sports for women and older sections of the community. These factors will support continued growth for gyms and health clubs over the five years to 2021.

This industry is Growing

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 13

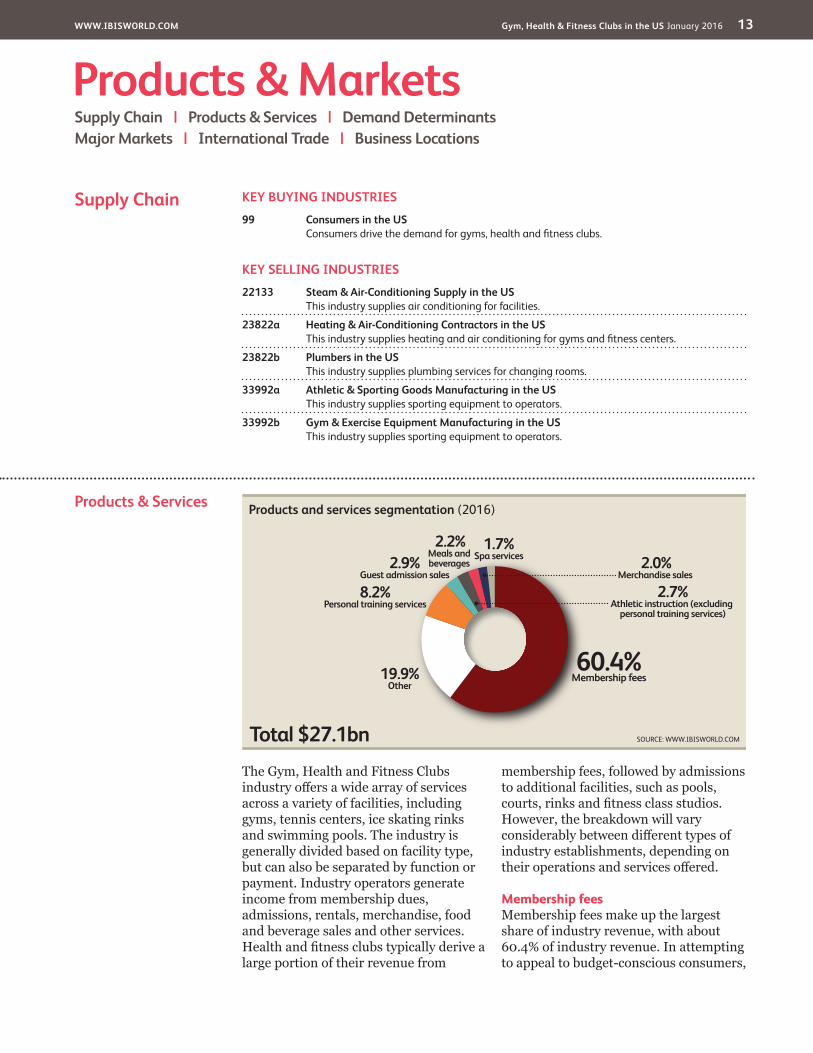

Products & Services

The Gym, Health and Fitness Clubs industry offers a wide array of services across a variety of facilities, including gyms, tennis centers, ice skating rinks and swimming pools. The industry is generally divided based on facility type, but can also be separated by function or payment. Industry operators generate income from membership dues, admissions, rentals, merchandise, food and beverage sales and other services. Health and fitness clubs typically derive a large portion of their revenue from

membership fees, followed by admissions to additional facilities, such as pools, courts, rinks and fitness class studios. However, the breakdown will vary considerably between different types of industry establishments, depending on their operations and services offered.

Membership feesMembership fees make up the largest share of industry revenue, with about 60.4% of industry revenue. In attempting to appeal to budget-conscious consumers,

Products & MarketsSupply Chain | Products & Services | Demand Determinants Major Markets | International Trade | Business Locations

KEY BUYING INDUSTRIES

99 Consumers in the US Consumers drive the demand for gyms, health and fitness clubs.

KEY SELLING INDUSTRIES

22133 Steam & Air-Conditioning Supply in the US This industry supplies air conditioning for facilities.

23822a Heating & Air-Conditioning Contractors in the US This industry supplies heating and air conditioning for gyms and fitness centers.

23822b Plumbers in the US This industry supplies plumbing services for changing rooms.

33992a Athletic & Sporting Goods Manufacturing in the US This industry supplies sporting equipment to operators.

33992b Gym & Exercise Equipment Manufacturing in the US This industry supplies sporting equipment to operators.

Supply Chain

Products and services segmentation (2016)

Total $27.1bn

60.4%Membership fees

2.2%Meals and beverages

19.9%Other

2.0%Merchandise sales

1.7%Spa services

8.2%Personal training services

2.9%Guest admission sales

2.7%Athletic instruction (excluding

personal training services)

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 14

Products & Markets

Demand Determinants

Across the United States, increasing awareness of the need for exercise, weight control, good nutrition and healthy lifestyle choices among adults and children is having a positive effect on fitness and recreational sports centers. Demand for services provided by the Gym, Health and Fitness Clubs industry is determined by a number of factors, including household disposable income, consumer confidence, leisure time availability, participation in recreation and sports, seasonal conditions, attitudes toward health and fitness and the cost of services relative to other recreation options.

Household disposable income is particularly relevant to industry demand, as the level of disposable income within a household will determine the amount spent at fitness and recreational sports centers. As discretionary spending rises, demand for gyms and fitness clubs typically increases. Similarly, industry growth is impacted by consumer confidence, as an increase leads to higher

demand and willingness to spend on the industry’s services.

Overall, demand is also sensitive to seasonal and weather conditions; for example, cold weather can reduce the level of swimming pool attendance (particularly for outdoor pools), while also increasing attendance at ice skating rinks. Additionally, the beginning of the calendar year marks the busiest season for new sales. A large portion of new gym members sign on in January or February, often because of New Year’s resolutions.

Leisure time availability also influences demand, with time-poor consumers finding it difficult to incorporate industry services into their routine. As work hours decline, people find more ways to attend gyms and use facilities. The link between leisure time and demand relates to health and fitness awareness, as people view fitness as a valuable way to use their spare time. While health crazes generally have a

Products & Servicescontinued

some gyms have offered low-cost memberships, which have caused consumer demand for gym memberships to rise. Many gym, health and fitness clubs offer memberships that cover basic amenities, such as free weights and elliptical equipment, but require an additional fee for services such as yoga classes and pool access. Overall, this product segment is expected to have grown over the five years to 2016.

Personal trainersPersonal trainers generate an estimated 8.2% of total revenue. Typically, gym, health and fitness clubs offer private trainers for individuals or private groups. Over the next five years, demand for personal trainers is expected to rise, driven by time-strapped consumers who want to achieve their fitness goals quickly. According to the Bureau of Labor

Statistics, many gyms will focus on personal training services, which are being demanded by an increasingly active baby boomer population. For example, some gyms may offer personal training services to elderly individuals who require fitness classes tailored to their injuries and illnesses (e.g. chronic ailments such as arthritis).

OtherThe other product segment is expected to collectively account for 19.9% of total revenue. In addition, merchandise sales, which typically include athletic apparel, are estimated to make up 2.0% of total revenue. Comparatively, roller and ice skating rink services and spa services (if included in gym, health and fitness clubs’ operations) are expected to account for 3.8% and 1.7% of total revenue, respectively.

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 15

Products & Markets

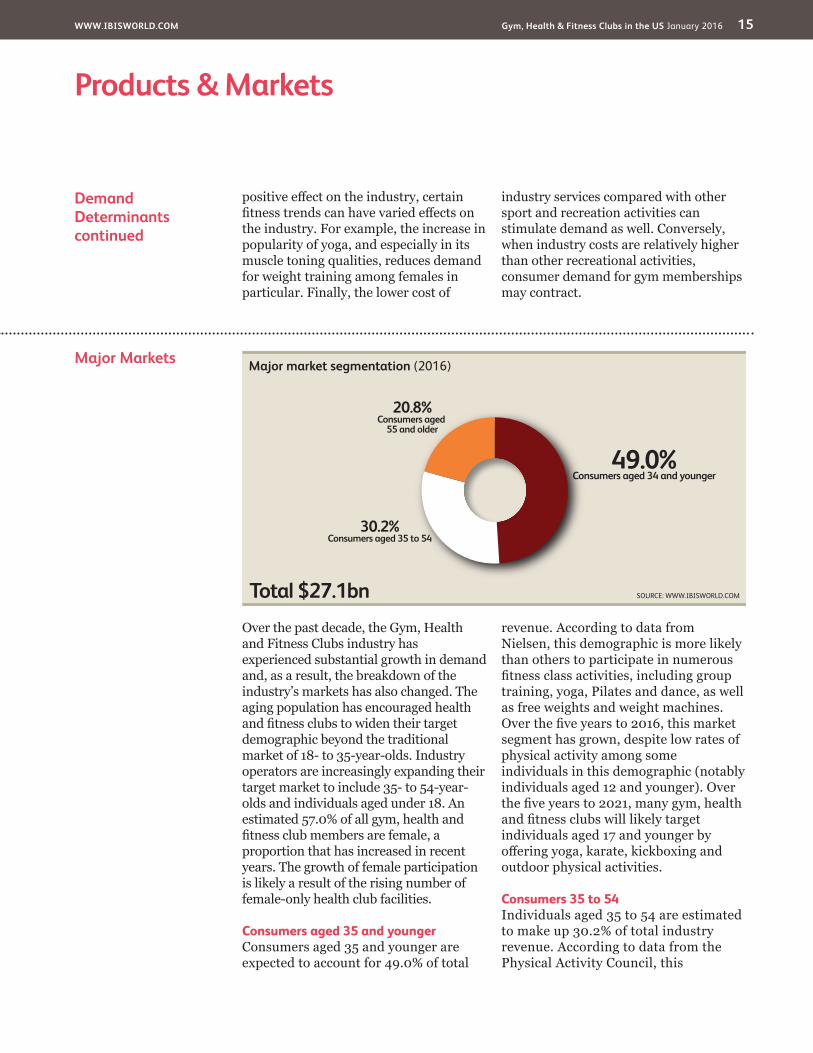

Major Markets

Over the past decade, the Gym, Health and Fitness Clubs industry has experienced substantial growth in demand and, as a result, the breakdown of the industry’s markets has also changed. The aging population has encouraged health and fitness clubs to widen their target demographic beyond the traditional market of 18- to 35-year-olds. Industry operators are increasingly expanding their target market to include 35- to 54-year-olds and individuals aged under 18. An estimated 57.0% of all gym, health and fitness club members are female, a proportion that has increased in recent years. The growth of female participation is likely a result of the rising number of female-only health club facilities.

Consumers aged 35 and youngerConsumers aged 35 and younger are expected to account for 49.0% of total

revenue. According to data from Nielsen, this demographic is more likely than others to participate in numerous fitness class activities, including group training, yoga, Pilates and dance, as well as free weights and weight machines. Over the five years to 2016, this market segment has grown, despite low rates of physical activity among some individuals in this demographic (notably individuals aged 12 and younger). Over the five years to 2021, many gym, health and fitness clubs will likely target individuals aged 17 and younger by offering yoga, karate, kickboxing and outdoor physical activities.

Consumers 35 to 54Individuals aged 35 to 54 are estimated to make up 30.2% of total industry revenue. According to data from the Physical Activity Council, this

Demand Determinantscontinued

positive effect on the industry, certain fitness trends can have varied effects on the industry. For example, the increase in popularity of yoga, and especially in its muscle toning qualities, reduces demand for weight training among females in particular. Finally, the lower cost of

industry services compared with other sport and recreation activities can stimulate demand as well. Conversely, when industry costs are relatively higher than other recreational activities, consumer demand for gym memberships may contract.

Major market segmentation (2016)

Total $27.1bn

49.0%Consumers aged 34 and younger

30.2%Consumers aged 35 to 54

20.8%Consumers aged

55 and older

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 16

Products & Markets

International Trade International trade does not generally apply to the US Gym, Health and Fitness Clubs industry, as it is a service-oriented sector with no measurable imports or exports. International trading of fitness and exercise

equipment is recorded at the manufacturing level for fitness or sporting goods (IBISWorld report 33992a). For more information on global operations, please refer to the Industry Globalization section.

Major Marketscontinued

demographic is the most likely to participate in sports, providing a boon to the industry. Furthermore, activities such as swimming, running and weight lifting appeal to this demographic, which has incited many gym, health and fitness clubs to offer these services to cater to this market segment. Over the next five years, this market segment is expected to remain stagnant, as many industry operators focus on appealing to other market segments.

Consumers aged 55 and olderAccording to the Physical Activity Council, this demographic is the most likely to be inactive: 32.8% of individuals aged 55 to 64 and 37.8% of those over the age of 65 are considered inactive. However, this demographic has a relatively high participation rate in fitness sports as well as outdoor sports. Over the past five years, the burgeoning elderly population has become increasingly health conscious, stimulating demand for industry services.

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 17

Products & Markets

Business Locations 2016

MO1.9

West

West

West

Rocky Mountains Plains

Southwest

Southeast

New England

VT0.3

MA3.5

RI0.5

NJ4.2

DE0.4

NH0.6

CT1.6

MD2.2

DC0.2

1

5

3

7

2

6

4

8 9

Additional States (as marked on map)

AZ1.5

CA10.8

NV0.6

OR1.5

WA2.6

MT0.4

NE0.7

MN2.0

IA1.1

OH3.8 VA

2.8

FL5.5

KS0.8

CO1.8

UT0.7

ID0.5

TX6.0

OK0.9

NC3.4

AK0.3

WY0.2

TN1.6

KY1.2

GA2.6

IL4.2

ME0.5

ND0.3

WI2.2 MI

3.0 PA4.7

WV0.5

SD0.3

NM0.5

AR0.7

MS0.7

AL1.2

SC1.4

LA1.4

HI0.3

IN2.0

NY7.1 5

67

8

321

4

9

SOURCE: WWW.IBISWORLD.COM

Mid- Atlantic

Establishments (%)

Less than 3% 3% to less than 10% 10% to less than 20% 20% or more

Great Lakes

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 18

Products & Markets

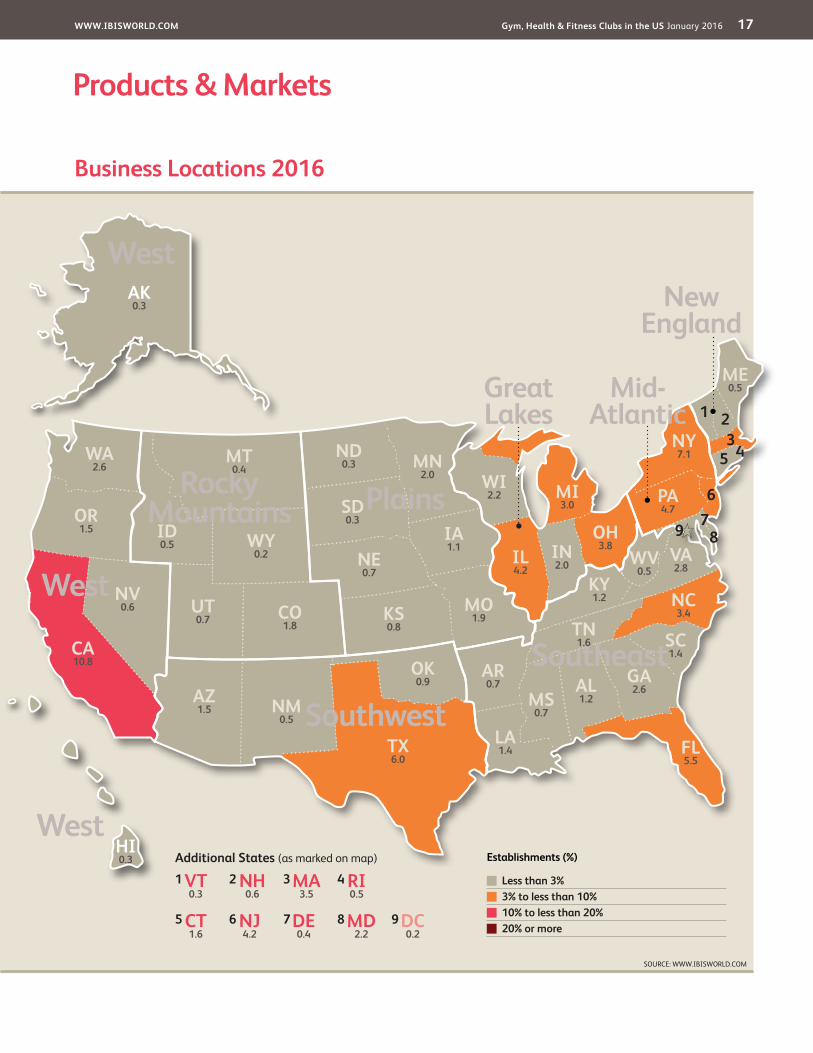

Business Locations The four regions that encompass the greatest percentages of gyms and health and fitness clubs include the Southeast (23.1% of establishments), the Mid-Atlantic (18.9%), the West (16.1%) and the Great Lakes (15.2%) regions of the United States. Together these four regions account for 73.0% of total industry establishments. Establishments are particularly concentrated in the following states: with 10.8% of establishments in California, New York (7.1%), Texas (6.0%), Florida (5.5%) and Pennsylvania (4.7%). Typically, highly populated regions have a higher portion of industry establishments. This trend can be attributed to consumer’s lack of willingness to travel excessive distances to perform exercise or become a member of a fitness or recreational sports center.

However, geographical locations can also determine the popularity of a fitness activity as many areas have climates that are not conducive to particular sports. For example, the population of Maine is twice as likely to participate in ice-skating compared with the national average. Similarly, the population of Arizona is about twice as likely to participate in swimming at a pool compared with the national average. As a result, areas across the United States will have a greater amount of establishments dedicated to a

particular activity depending on climate and other related factors.

Changes in geographic distribution over the past five years have been minimal, with no region increasing or declining in share by more than one percentage point. The West and Southwest regions have experienced slight growth in the past five years, whereas the Rocky Mountains, New England and Great Lakes observed small declines. These changes can be attributed to shifting demographics and varying demand levels.

%

30

0

10

20

Sout

hwes

t

Wes

t

Gre

at L

akes

Mid

-Atla

ntic

New

Eng

land

Plai

ns

Rock

y M

ount

ains

Sout

heas

t

EstablishmentsPopulation

Distribution of establishments vs. population

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 19

Cost Structure Benchmarks

ProfitMember retention is a key component in fitness centers’ profitability, as many gym, health and fitness centers have fixed overhead costs. According to the International Health, Racquet & Sportsclub Association, the average attrition rate for gyms in the United States is up to 45.0%, meaning that 45 out of 100 individuals will cancel their gym memberships each year.

Furthermore, the cost of recruiting a new member is more than twice the cost of retaining an existing member. As a result, many health clubs will continue to direct funds toward retaining existing members in 2016 by prioritizing excellent customer service, adding amenities and lowering membership cancelation penalties. In 2016, profit, measured as earnings before taxes and interest, is expected to make up 10.4% of total revenue. Over the past five

Key Success Factors Easy access for clientsA high profile location offering easy access and parking can provide a competitive advantage for operators in this industry.

Effective product promotionBeing able to promote a business effectively increases awareness and attracts greater membership and local patronage.

Economies of scaleFitness operators that have a large number of establishments and provide a wide range of services are able to attract and retain new and existing members, as well as reduce costs per member.

Provision of appropriate facilitiesProviding appropriate equipment and maintaining it regularly is essential to attracting and retaining customers.

Having a good technical knowledge of the productSkilled employees who can demonstrate the use of various types of equipment and assist participants are important to attract repeat customers.

Business expertise of operatorsThe long-term success of an operator in this industry depends on the skill of the operator in running a business profitably over time.

Market Share Concentration

The Gym, Health and Fitness Clubs industry exhibits a low level of market share concentration, with the top four operators in the industry comprising less than 18.0% of total revenue in 2016. The industry’s low level of market concentration can be attributed to high fragmentation, due to many industry operators having a market niche with local clientele. Additionally, a large number of fitness and gym centers only employ one person or are nonemploying establishments. The percentage of nonemployers is substantial because the industry’s low

barriers to entry and low startup capital costs.

The larger players in this industry have numerous locations throughout the United States, while small players are generally independently owned and operate in one or two states. However, over the past five years, the proportion of businesses that employs 20 people or more has increased, indicating that concentration is rising. The industry’s market share will become more concentrated over the next five years, as larger operators acquire small, niche gym and health and fitness clubs.

Competitive LandscapeMarket Share Concentration | Key Success Factors | Cost Structure Benchmarks Basis of Competition | Barriers to Entry | Industry Globalization

Level Concentration in this industry is Low

IBISWorld identifies 250 Key Success Factors for a business. The most important for this industry are:

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 20

Competitive Landscape

Cost Structure Benchmarkscontinued

years, industry profitability has grown, due to rising consumer demand for high-margin services (e.g. massages, spa services and personal trainers).

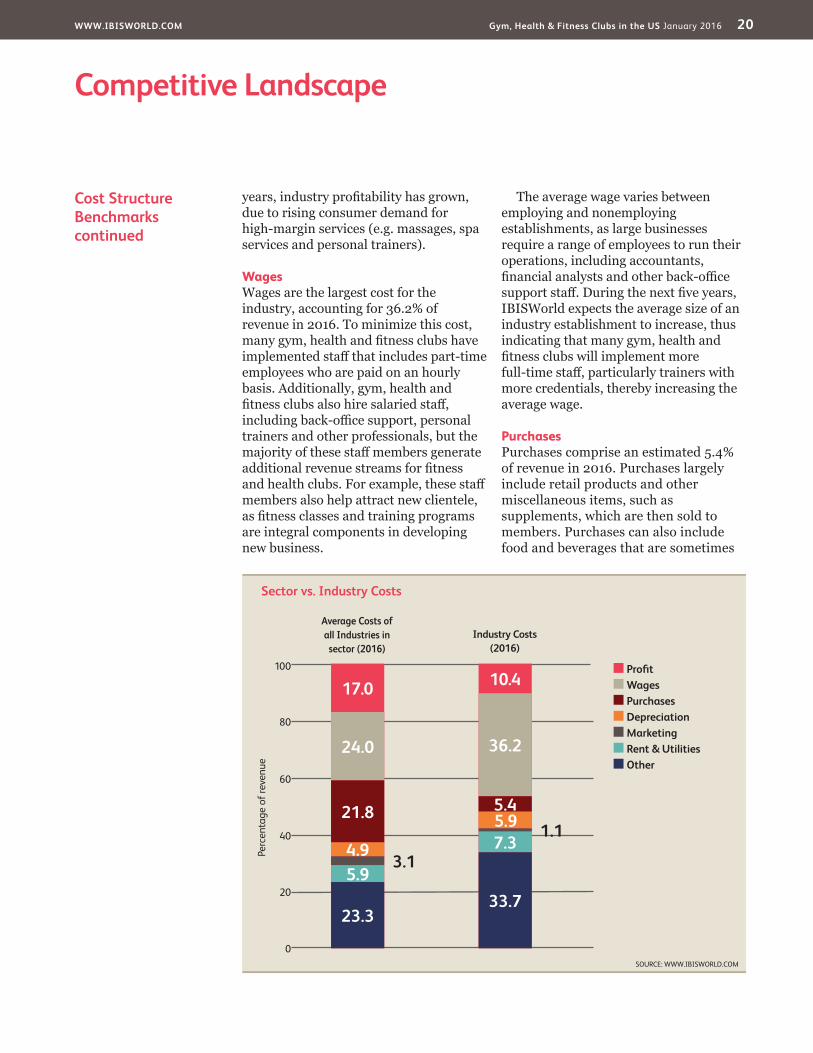

WagesWages are the largest cost for the industry, accounting for 36.2% of revenue in 2016. To minimize this cost, many gym, health and fitness clubs have implemented staff that includes part-time employees who are paid on an hourly basis. Additionally, gym, health and fitness clubs also hire salaried staff, including back-office support, personal trainers and other professionals, but the majority of these staff members generate additional revenue streams for fitness and health clubs. For example, these staff members also help attract new clientele, as fitness classes and training programs are integral components in developing new business.

The average wage varies between employing and nonemploying establishments, as large businesses require a range of employees to run their operations, including accountants, financial analysts and other back-office support staff. During the next five years, IBISWorld expects the average size of an industry establishment to increase, thus indicating that many gym, health and fitness clubs will implement more full-time staff, particularly trainers with more credentials, thereby increasing the average wage.

PurchasesPurchases comprise an estimated 5.4% of revenue in 2016. Purchases largely include retail products and other miscellaneous items, such as supplements, which are then sold to members. Purchases can also include food and beverages that are sometimes

Sector vs. Industry Costs

n Profi tn Wagesn Purchasesn Depreciationn Marketingn Rent & Utilitiesn Other

Average Costs of all Industries in sector (2016)

Industry Costs (2016)

0

20

40

60

Perc

enta

ge o

f rev

enue

80

100

SOURCE: WWW.IBISWORLD.COM

17.0 10.4

33.7

7.31.15.9

5.4

36.2

23.3

5.93.1

4.9

21.8

24.0

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 21

Competitive Landscape

Basis of Competition During the past five years, the Gym, Health and Fitness Clubs industry has become increasingly competitive. Well-financed competitors have entered the industry, and existing regional and national operators have expanded their operations. Gym and fitness clubs typically compete for high consumer retention rates on the basis of price, customer service, brand recognition and types of services offered. For example, industry operators may offer additional services, including nutritional programs, meal planning and facial services. While facials and nutritional programs are not included in industry revenue, operators that offer additional services may increase their consumer retention rates, which boosts industry revenue.

Internal competitionIndustry operators compete for brand recognition and member’s word-of-mouth to generate revenue. Many operators rely on retaining and developing large membership rates to cover their operational costs. Operators also compete on the basis of price. For example, gym and health clubs that offer low initiation fees and monthly membership will attract first-time gym members in particular. Additionally, low-cost membership on a month-by-month basis appeals to both budget-conscious consumers and individuals who do not want to lock in a year contract. Also, industry operators may compete for customer service. In particular, strong customer

Cost Structure Benchmarkscontinued

sold in the fitness and recreational sports centers.

Rent and utilitiesRent and utilities make up about 7.3% of industry revenue in 2016. Many businesses in this industry do not own their fitness facilities, and as a result they must rent their buildings. Additionally, some equipment used in recreational and fitness centers are not purchased entirely, but on a “rental” basis, thus adding to the cost in this segment. Industry operators incur utility costs because the industry requires electricity for lighting, treadmills, cross-trainers, steppers and other electronic equipment. To lower utility costs, some centers have implemented energy-efficient lighting fixtures and automatic switches and timers.

Depreciation and other costsDepreciation of buildings and equipment represents another significant expense item for the industry, accounting for 5.9% of revenue in 2016. Expenditure on capital includes purchasing new and replacing old

equipment, such as treadmills and weight machines. To operate both efficiently and profitably, enterprises must continually acquire up-to-date fitness technology to maintain and attract their customer base, which adds to depreciation costs. Other costs include general administration, IT expenses and insurance costs, which account for an estimated 33.7% of revenue.

Many businesses have had to insure their products against damage, which increases insurance costs as more consumers use fitness equipment frequently. The industry is expected to spend about 1.1% of its revenue on advertising in 2016, as strong marketing support is essential for attracting new clientele in such a highly competitive market. Operators advertise via TV, direct mail, newspapers, telephone directories, radio, billboards, internet websites and other promotional activities. Advertisements aim to differentiate operators from competitors by focusing on amenities, prices, services and promotional offers. Operators also try to appeal to the public’s desire to lose weight, look better and improve health.

Level & Trend Competition in this industry is High and the trend is Increasing

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 22

Competitive Landscape

Barriers to Entry Overall, barriers to entry are relatively low for the Gym, Health and Fitness Clubs industry. Leasing, rather than owning industry facilities, provides a low-cost option for potential industry entrants, thus keeping barriers to entry relatively low. Additionally, average wages in the industry tend to be low, as staff are typically unskilled and provide training services on a part-time basis. Equipment costs are relatively low as well, and have long life spans. Many start-up gyms with either use second-hand exercise equipment to reduce costs or will rent their equipment. Barriers to entry in urban markets include restrictive zoning laws, lengthy permit processes and a shortage of appropriate real estate. New entrants may also incur heavy costs when acquiring or leasing the required equipment for members and participants to use.

Access to capital to fund these startup costs are therefore essential. The high cost and lengthy time needed to build brand reputation is a potential barrier to entry. Existing players have already established trade names, and new entrants will have to invest financial resources and time to persuade consumers to shift away from established, brand-name gyms and fitness

centers. According to data from the International Health, Racquet and Sportsclub Association (IHRSA), the number of health club memberships and health clubs has risen, demonstrating that the industry exhibits relatively low barriers to entry. As more consumers have become health conscious, more gym, health and fitness clubs have entered the market to cater to demand. However, over the next five years, barriers to entry for new industry entrants may rise. As some businesses partner with health insurers, the implementation of corporate wellness programs may result in strong demand for large-scale gym memberships, intensifying barriers to entry for new companies.

Basis of Competitioncontinued

service boosts both member attrition rates and also develops a strong customer base of individuals who may be new to gym memberships.

Operators in this industry also compete with other commercial fitness centers and recreational facilities that are established and operated by local governments. Nonprofit and government organizations have an edge on commercial gyms and fitness clubs because they can obtain land and build centers at lower costs. Additional services offered by hospitals, businesses and salons are another source of competition, adding to the highly competitive environment. These operators typically compete based on location,

which is the greatest convenience factor for the consumer.

External competitionOperators also experience external competition from entertainment and retail businesses for the discretionary income of the specific target markets in this industry. Industry operators compete with amenity and condominium clubs, exercise studios, country clubs, weight-loss centers and home fitness equipment businesses. Many other leisure industries, such as bowling alleys and marinas, also compete with this industry for leisure time, albeit without the fitness aspect.

Barriers to Entry checklist

Competition HighConcentration LowLife Cycle Stage GrowthCapital Intensity MediumTechnology Change MediumRegulation & Policy LightIndustry Assistance Low

SOURCE: WWW.IBISWORLD.COM

Level & Trend Barriers to Entry in this industry are Low and Steady

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 23

Competitive Landscape

Industry Globalization

The Gym, Health and Fitness Clubs industry has a low level of globalization; the majority of operators are small local operators, employing between one and 19 people or are nonemployers, which account for about 85.0% of the industry’s total operators. While the industry is not typified by a high level of globalization, some of the industry’s larger players are increasingly becoming globalized. For example, Gold’s Gym

International Inc. and Curves International Inc. have subsidiaries that operate in global markets. Gold’s Gym International operates in more than 25 countries, while 24 Hour Fitness also enjoys a global presence with locations throughout Asia. Globalization is increasing as national and regional competitors expand the scope of their operations, but at this stage, it is relatively low.

Level & Trend Globalization in this industry is Low and the trend is Increasing

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 24

Other Companies Due to the fragmented nature of this industry, no player holds a market share greater than 5.0%. Moreover, there is limited financial information available for players in this industry because many are private organizations with franchised operations and, therefore, annual revenue figures are unavailable.

24 Hour Fitness Worldwide Inc. Estimated market share: 4.8%24 Hour Fitness Worldwide Inc. is a large, privately owned and operated fitness center chain. Established in 1983, the company’s first club location opened in California. With more than 400 clubs across the United States, 24 Hour serves nearly 4.0 million members. The company also offers a plethora of gym services, including personal training, group exercise classes and a variety of strength, cardio and functional training equipment. Furthermore, the company is one of the largest supporters of amateur athletics in the United States, serving as the official fitness center sponsor of the US Olympic and Paralympic Teams. 24 Hour also uses celebrities and professional athletes to advertise its brand; for example, the company is partners with the reality TV show The Biggest Loser. These marketing strategies help differentiate 24 Hour Fitness from its competitors, which allows the company to strengthen its market share.

In 2005, 24 Hour Fitness entered a partnership with New York-based private equity firm Forstmann Little & Co. Financier Theodore J. Forstmann acquired the company for $1.6 billion and has continued to promote 24 Hour Fitness as a leader within the fitness industry, with the aim of continual expansion. Since 24 Hour Fitness is a privately held company, limited financial information is available; however, IBISWorld expects the company to generate revenue of $1.3 billion in 2016.

Life Time Fitness Estimated market share: 4.7%Life Time Fitness Inc. operates more than 114 centers under the Life Time Fitness and Life Time Athletic brands. The company offers a range of services, such as group fitness, yoga, swimming, running, racquetball, squash, tennis, Pilates, rock climbing and kid activities and camps. The company designs and develops its own centers, with a focus on providing members with products and services in the areas of exercise, education and nutrition. The company currently operates in Canada and the United States, primarily in suburban locations. Life Time Fitness’ business model includes attracting a larger customer base within the first three years after a center opens, as well as retaining members and controlling expenses. In 2012, the company acquired the Racquet Club of the South, a tennis facility in Atlanta that the company rebranded as Life Time Fitness Atlanta. Additionally, in 2011, Life Time Fitness acquired nine fitness facilities from Lifestyle Family Fitness in Indiana, North Carolina and Ohio. In 2016, IBISWorld expects the company to generate $1.3 billion in revenue.

Gold’s Gym International Inc. Estimated market share: 4.2%Established in 1965, Gold’s Gym International Inc. has 273 US franchises and 150 company-owned locations. The company offers gym services that include cardio and strength training, Zumba, yoga, group cycling, mixed martial arts, muscle endurance training and Pilates.

In addition to opening franchises, the company buys smaller regional health clubs and converts them into Gold’s Gyms. The company also licenses the Gold’s Gym name for products like fitness equipment and accessories, luggage, T-shirts and sportswear. In 2004, TRT Holdings acquired Gold’s Gym for $158.0 million. The company aims to develop a

Major CompaniesThere are no Major Players in this industry | Other Companies

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 25

Major Companies

Other Companiescontinued

budget-conscious consumer base by developing Gold’s Gym Express, which provides low-cost gym facilities. Gold’s Gym also continues to maintain its core weightlifting tradition, which generated its early success with the company’s initial Venice Beach, CA location. In 2016, IBISWorld expects the company to generate $1.1 billion in revenue.

Curves International Inc. Estimated market share: 3.8%Founded in 1992, Curves International Inc. developed a market niche in fitness and weight-loss facilities that targeted women. The company developed a customer base of 4.0 million members in 90 countries, with more than 10,000 Curves for Women fitness centers. Curves offers 30-minute health and weight-loss sessions for women in Australia, Canada, the Caribbean, Europe, Mexico, New Zealand, South America and the United States.

In 2008, the company opened franchises in Ukraine, Slovakia, Botswana, Bahrain, Qatar and Saudi Arabia. It also added franchise establishments in Belgium, Finland, Jordan, Malta and Senegal. Moreover, in 2009, Curves opened centers in China, India and the Philippines. Prior to the current five-year period, Curves was one

of the fastest-growing franchises in the domestic market. However, according to data from Forbes, Curves has closed 65.0% of its franchise locations throughout North America since 2007. IBISWorld expects its US revenue to decline to $1.0 billion in 2016.

Town Sports International Holdings Inc. Estimated market share: 1.6%Town Sports International Holdings Inc. (TSI) is the largest owner and operator of fitness clubs in the Northeast and Mid-Atlantic regions of the United States. TSI owns and operates a number of brands, including New York Sports Clubs, Boston Sports Clubs, Washington Sports Clubs and Philadelphia Sports Clubs. Founded in 1974, the company now operates about 153 fitness clubs and three BFX Studio locations. As of September 2015 (latest data available), the company has about 534,000 members.

The company’s business strategy involves serving densely populated metropolitan regions and developing locations near TSI’s targeted customer base. TSI targets individuals aged 21 to 50 years old with annual incomes of $50,000 to $150,000. In 2016, IBISWorld expects TSI to earn revenue of $440.3 million.

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 26

Capital Intensity The Gym, Health and Fitness Clubs industry is moderately capital intensive. In 2016, for every dollar spent on wages, the industry incurs an estimated $0.16 in capital costs. Wage costs are expected to account for 36.2% of total industry revenue. Capital costs are moderate for the industry and includes the cost of fitness equipment, buildings, vehicles, furniture and computers. Nevertheless, labor costs remain high because of administration, training, supervision and maintenance requirements. Gyms and fitness centers seek to minimize their labor costs by employing a part-time labor force and employing instructors and personal trainers on an as-needed basis. The industry has moderate capital intensity despite the

low barriers to entry; the total startup costs are low but are split relatively evenly between capital and labor.

Operating ConditionsCapital Intensity | Technology & Systems | Revenue VolatilityRegulation & Policy | Industry Assistance

Tools of the Trade: Growth Strategies for Success

SOURCE: WWW.IBISWORLD.COM

Labo

r Int

ensi

veCapital Intensive

Change in Share of the Economy

New Age Economy

Recreation, Personal Services, Health and Education. Firms benefi t from personal wealth so stable macroeconomic conditions are imperative. Brand awareness and niche labor skills are key to product differentiation.

Traditional Service Economy

Wholesale and Retail. Reliant on labor rather than capital to sell goods. Functions cannot be outsourced therefore fi rms must use new technology or improve staff training to increase revenue growth.

Old Economy

Agriculture and Manufacturing. Traded goods can be produced using cheap labor abroad. To expand fi rms must merge or acquire others to exploit economies of scale, or specialize in niche, high-value products.

Investment Economy

Information, Communications, Mining, Finance and Real Estate. To increase revenue fi rms need superior debt management, a stable macroeconomic environment and a sound investment plan.

Golf Driving Ranges & Family Fun Centers

Steam & Air-Conditioning SupplyHotels & Motels

Heating & Air-Conditioning ContractorsWeight Loss Services

Gym, Health & Fitness Clubs

Capital intensity

0.5

0.0

0.1

0.2

0.3

0.4

SOURCE: WWW.IBISWORLD.COMDotted line shows a high level of capital intensity

Capital units per labor unit

Gym, Health & Fitness Clubs

Arts, Entertain-ment and Recreation

Economy

Level The level of capital intensity is Medium

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 27

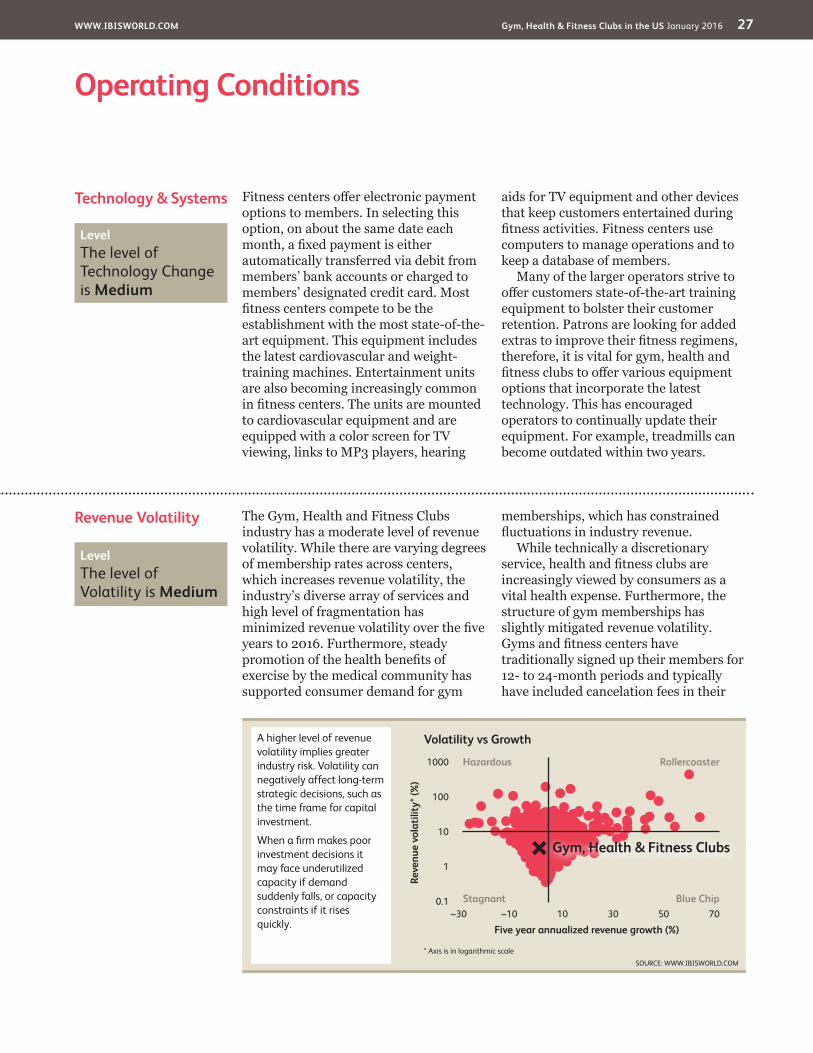

Operating Conditions

Revenue Volatility The Gym, Health and Fitness Clubs industry has a moderate level of revenue volatility. While there are varying degrees of membership rates across centers, which increases revenue volatility, the industry’s diverse array of services and high level of fragmentation has minimized revenue volatility over the five years to 2016. Furthermore, steady promotion of the health benefits of exercise by the medical community has supported consumer demand for gym

memberships, which has constrained fluctuations in industry revenue.

While technically a discretionary service, health and fitness clubs are increasingly viewed by consumers as a vital health expense. Furthermore, the structure of gym memberships has slightly mitigated revenue volatility. Gyms and fitness centers have traditionally signed up their members for 12- to 24-month periods and typically have included cancelation fees in their

Technology & Systems Fitness centers offer electronic payment options to members. In selecting this option, on about the same date each month, a fixed payment is either automatically transferred via debit from members’ bank accounts or charged to members’ designated credit card. Most fitness centers compete to be the establishment with the most state-of-the-art equipment. This equipment includes the latest cardiovascular and weight-training machines. Entertainment units are also becoming increasingly common in fitness centers. The units are mounted to cardiovascular equipment and are equipped with a color screen for TV viewing, links to MP3 players, hearing

aids for TV equipment and other devices that keep customers entertained during fitness activities. Fitness centers use computers to manage operations and to keep a database of members.

Many of the larger operators strive to offer customers state-of-the-art training equipment to bolster their customer retention. Patrons are looking for added extras to improve their fitness regimens, therefore, it is vital for gym, health and fitness clubs to offer various equipment options that incorporate the latest technology. This has encouraged operators to continually update their equipment. For example, treadmills can become outdated within two years.

Level The level of Technology Change is Medium

Level The level of Volatility is Medium

SOURCE: WWW.IBISWORLD.COM

Volatility vs Growth

Reve

nue

vola

tility

* (%

)

1000

100

10

1

0.1

Five year annualized revenue growth (%)–30 –10 10 30 50 70

Hazardous

Stagnant

Rollercoaster

Blue Chip

* Axis is in logarithmic scale

A higher level of revenue volatility implies greater industry risk. Volatility can negatively affect long-term strategic decisions, such as the time frame for capital investment.

When a fi rm makes poor investment decisions it may face underutilized capacity if demand suddenly falls, or capacity constraints if it rises quickly.

Gym, Health & Fitness Clubs

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 28

Operating Conditions

Regulation & Policy The general rules and regulations of the Federal Trade Commission and of other federal, state, provincial and local consumer protection agencies apply to franchising, advertising, sales and other trade practices. State and provincial statutes and regulations relevant to the fitness industry have been enacted or proposed in all of the states and provinces across the United States. Typically, these statutes and regulations prescribe certain forms and regulate the terms and provisions of membership contracts, including: giving members the right to cancel the contract, often within three business days of signing; requiring an escrow for funds received from preopening sales or the posting of a bond or proof of financial responsibility; and in some cases, establishing maximum prices and terms for membership contracts and limitations on the financing term of contracts.

Operators are subject to numerous other types of federal, state and provincial regulations governing the sale, financing and collection of memberships, including both the Truth-in-Lending Act and Regulation Z, as well as state and provincial laws governing the collection of debts. These laws and regulations are

subject to varying interpretations by a large number of state and federal enforcement agencies.

Under the “cooling-off” statutes employed in most states and provinces, new fitness center members have the right to cancel their memberships within a period of three to fifteen days after the date the contract was entered and they are entitled to refunds of any payment made. The amount of time new members have to cancel their membership contract depends on the applicable state or provincial law.

Advertising of nutritional products is subject to regulation by one or more federal agencies, including the Food and Drug Administration (FDA) and the Federal Trade Commission (FTC). For example, the FDA regulates the formulation, manufacture and labeling of vitamins and other nutritional supplements, while the FTC principally regulates marketing and advertising claims. Industry operators are also subject to several state and federal labor laws governing the relationship with employees, such as minimum wage requirements, overtime, working conditions and citizenship requirements.

Revenue Volatilitycontinued

Level & Trend The level of Regulation is Light and the trend is Steady

contracts. These fees often deter customers from cancelling their memberships. As competition has increased over the past five years, many gyms have offered more flexible

membership options, such as shorter contract periods and rolling contracts. As flexible membership options become more prevalent, revenue volatility is expected to increase in the coming years.

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 29

Operating Conditions

Industry Assistance The level of industry assistance is low, but it is increasing as more institutions promote the benefits of assistance. Such assistance is a significant benefit for the industry, as it reduces expenses and creates demand. The Department of Health and Human Services, under its Community Prevention umbrella, has allocated $16.0 million toward obesity prevention and fitness.

The National Association for Health and Fitness (NAHF) is a nonprofit organization that promotes physical fitness and sports and supports Governor and State Councils that promote such activities. The association produces newsletters on strategies and successful approaches to increasing physical activity and improving health. The International Health, Racquet & Sportsclub Association also supports the industry and is a nonprofit trade association representing more than 10,000 health, racquet and sports clubs worldwide. This association

provides media articles and press releases that promote the benefits of keeping fit and active. Therefore, this association helps drive industry demand.

The Fifty-Plus Fitness Association (FPFA) is another nonprofit organization, which was established 20 years ago. This association’s mission is to promote an active lifestyle for the older population. The organization started at Stanford University as an outgrowth of some medical research on the value of exercise for older persons. The FPFA currently has about 1,000 members across the United States. The association also publishes a newsletter and distributes books and videos. In the past, it has offered a six-week “Fifty-Plus Fitness Challenge Camp” on the Stanford University campus that involved the participants in a variety of physical activities. Some facilities are initially established with the assistance of government grants.

Level & Trend The level of Industry Assistance is Low and the trend is Increasing

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 30

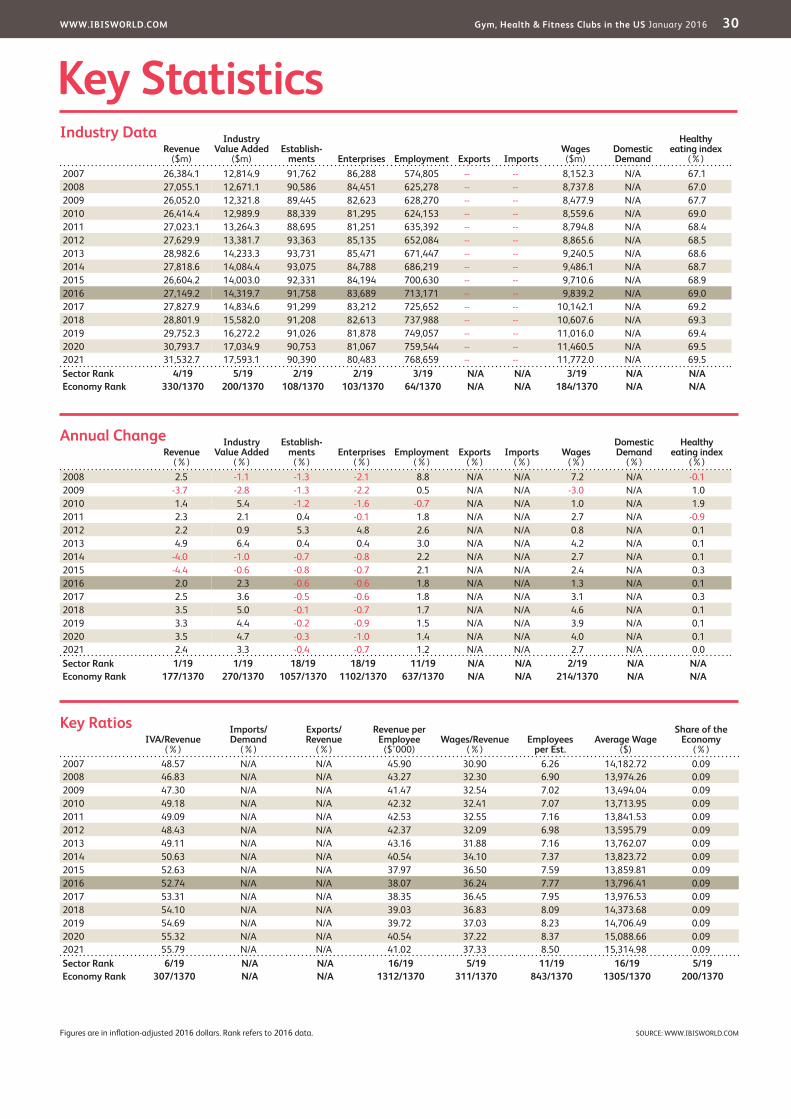

Key StatisticsRevenue

($m)

Industry Value Added

($m)Establish-

ments Enterprises Employment Exports ImportsWages ($m)

Domestic Demand

Healthy eating index

(%)2007 26,384.1 12,814.9 91,762 86,288 574,805 -- -- 8,152.3 N/A 67.12008 27,055.1 12,671.1 90,586 84,451 625,278 -- -- 8,737.8 N/A 67.02009 26,052.0 12,321.8 89,445 82,623 628,270 -- -- 8,477.9 N/A 67.72010 26,414.4 12,989.9 88,339 81,295 624,153 -- -- 8,559.6 N/A 69.02011 27,023.1 13,264.3 88,695 81,251 635,392 -- -- 8,794.8 N/A 68.42012 27,629.9 13,381.7 93,363 85,135 652,084 -- -- 8,865.6 N/A 68.52013 28,982.6 14,233.3 93,731 85,471 671,447 -- -- 9,240.5 N/A 68.62014 27,818.6 14,084.4 93,075 84,788 686,219 -- -- 9,486.1 N/A 68.72015 26,604.2 14,003.0 92,331 84,194 700,630 -- -- 9,710.6 N/A 68.92016 27,149.2 14,319.7 91,758 83,689 713,171 -- -- 9,839.2 N/A 69.02017 27,827.9 14,834.6 91,299 83,212 725,652 -- -- 10,142.1 N/A 69.22018 28,801.9 15,582.0 91,208 82,613 737,988 -- -- 10,607.6 N/A 69.32019 29,752.3 16,272.2 91,026 81,878 749,057 -- -- 11,016.0 N/A 69.42020 30,793.7 17,034.9 90,753 81,067 759,544 -- -- 11,460.5 N/A 69.52021 31,532.7 17,593.1 90,390 80,483 768,659 -- -- 11,772.0 N/A 69.5Sector Rank 4/19 5/19 2/19 2/19 3/19 N/A N/A 3/19 N/A N/AEconomy Rank 330/1370 200/1370 108/1370 103/1370 64/1370 N/A N/A 184/1370 N/A N/A

IVA/Revenue (%)

Imports/Demand

(%)

Exports/Revenue

(%)

Revenue per Employee

($’000)Wages/Revenue

(%)Employees

per Est.Average Wage

($)

Share of the Economy

(%)2007 48.57 N/A N/A 45.90 30.90 6.26 14,182.72 0.092008 46.83 N/A N/A 43.27 32.30 6.90 13,974.26 0.092009 47.30 N/A N/A 41.47 32.54 7.02 13,494.04 0.092010 49.18 N/A N/A 42.32 32.41 7.07 13,713.95 0.092011 49.09 N/A N/A 42.53 32.55 7.16 13,841.53 0.092012 48.43 N/A N/A 42.37 32.09 6.98 13,595.79 0.092013 49.11 N/A N/A 43.16 31.88 7.16 13,762.07 0.092014 50.63 N/A N/A 40.54 34.10 7.37 13,823.72 0.092015 52.63 N/A N/A 37.97 36.50 7.59 13,859.81 0.092016 52.74 N/A N/A 38.07 36.24 7.77 13,796.41 0.092017 53.31 N/A N/A 38.35 36.45 7.95 13,976.53 0.092018 54.10 N/A N/A 39.03 36.83 8.09 14,373.68 0.092019 54.69 N/A N/A 39.72 37.03 8.23 14,706.49 0.092020 55.32 N/A N/A 40.54 37.22 8.37 15,088.66 0.092021 55.79 N/A N/A 41.02 37.33 8.50 15,314.98 0.09Sector Rank 6/19 N/A N/A 16/19 5/19 11/19 16/19 5/19Economy Rank 307/1370 N/A N/A 1312/1370 311/1370 843/1370 1305/1370 200/1370

Figures are in inflation-adjusted 2016 dollars. Rank refers to 2016 data.

Revenue (%)

Industry Value Added

(%)

Establish-ments

(%)Enterprises

(%)Employment

(%)Exports

(%)Imports

(%)Wages

(%)

Domestic Demand

(%)

Healthy eating index

(%)2008 2.5 -1.1 -1.3 -2.1 8.8 N/A N/A 7.2 N/A -0.12009 -3.7 -2.8 -1.3 -2.2 0.5 N/A N/A -3.0 N/A 1.02010 1.4 5.4 -1.2 -1.6 -0.7 N/A N/A 1.0 N/A 1.92011 2.3 2.1 0.4 -0.1 1.8 N/A N/A 2.7 N/A -0.92012 2.2 0.9 5.3 4.8 2.6 N/A N/A 0.8 N/A 0.12013 4.9 6.4 0.4 0.4 3.0 N/A N/A 4.2 N/A 0.12014 -4.0 -1.0 -0.7 -0.8 2.2 N/A N/A 2.7 N/A 0.12015 -4.4 -0.6 -0.8 -0.7 2.1 N/A N/A 2.4 N/A 0.32016 2.0 2.3 -0.6 -0.6 1.8 N/A N/A 1.3 N/A 0.12017 2.5 3.6 -0.5 -0.6 1.8 N/A N/A 3.1 N/A 0.32018 3.5 5.0 -0.1 -0.7 1.7 N/A N/A 4.6 N/A 0.12019 3.3 4.4 -0.2 -0.9 1.5 N/A N/A 3.9 N/A 0.12020 3.5 4.7 -0.3 -1.0 1.4 N/A N/A 4.0 N/A 0.12021 2.4 3.3 -0.4 -0.7 1.2 N/A N/A 2.7 N/A 0.0Sector Rank 1/19 1/19 18/19 18/19 11/19 N/A N/A 2/19 N/A N/AEconomy Rank 177/1370 270/1370 1057/1370 1102/1370 637/1370 N/A N/A 214/1370 N/A N/A

Annual Change

Key Ratios

Industry Data

SOURCE: WWW.IBISWORLD.COM

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 31

Jargon & Glossary

BARRIERS TO ENTRY High barriers to entry mean that new companies struggle to enter an industry, while low barriers mean it is easy for new companies to enter an industry.

CAPITAL INTENSITY Compares the amount of money spent on capital (plant, machinery and equipment) with that spent on labor. IBISWorld uses the ratio of depreciation to wages as a proxy for capital intensity. High capital intensity is more than $0.333 of capital to $1 of labor; medium is $0.125 to $0.333 of capital to $1 of labor; low is less than $0.125 of capital for every $1 of labor.

CONSTANT PRICES The dollar figures in the Key Statistics table, including forecasts, are adjusted for inflation using the current year (i.e. year published) as the base year. This removes the impact of changes in the purchasing power of the dollar, leaving only the “real” growth or decline in industry metrics. The inflation adjustments in IBISWorld’s reports are made using the US Bureau of Economic Analysis’ implicit GDP price deflator.

DOMESTIC DEMAND Spending on industry goods and services within the United States, regardless of their country of origin. It is derived by adding imports to industry revenue, and then subtracting exports.

EMPLOYMENT The number of permanent, part-time, temporary and seasonal employees, working proprietors, partners, managers and executives within the industry.

ENTERPRISE A division that is separately managed and keeps management accounts. Each enterprise consists of one or more establishments that are under common ownership or control.

ESTABLISHMENT The smallest type of accounting unit within an enterprise, an establishment is a single physical location where business is conducted or where services or industrial operations are performed. Multiple establishments under common control make up an enterprise.

EXPORTS Total value of industry goods and services sold by US companies to customers abroad.

IMPORTS Total value of industry goods and services brought in from foreign countries to be sold in the United States.

INDUSTRY CONCENTRATION An indicator of the dominance of the top four players in an industry. Concentration is considered high if the top players account for more than 70% of industry revenue. Medium is 40% to 70% of industry revenue. Low is less than 40%.

INDUSTRY REVENUE The total sales of industry goods and services (exclusive of excise and sales tax); subsidies on production; all other operating income from outside the firm (such as commission income, repair and service income, and rent, leasing and hiring income); and capital work done by rental or lease. Receipts from interest royalties, dividends and the sale of fixed tangible assets are excluded.

INDUSTRY VALUE ADDED (IVA) The market value of goods and services produced by the industry minus the cost of goods and services used in production. IVA is also described as the industry’s contribution to GDP, or profit plus wages and depreciation.

INTERNATIONAL TRADE The level of international trade is determined by ratios of exports to revenue and imports to domestic demand. For exports/revenue: low is less than 5%, medium is 5% to 20%, and high is more than 20%. Imports/domestic demand: low is less than 5%, medium is 5% to 35%, and high is more than 35%.

LIFE CYCLE All industries go through periods of growth, maturity and decline. IBISWorld determines an industry’s life cycle by considering its growth rate (measured by IVA) compared with GDP; the growth rate of the number of establishments; the amount of change the industry’s products are undergoing; the rate of technological change; and the level of customer acceptance of industry products and services.

NONEMPLOYING ESTABLISHMENT Businesses with no paid employment or payroll, also known as nonemployers. These are mostly set up by self-employed individuals.

PROFIT IBISWorld uses earnings before interest and tax (EBIT) as an indicator of a company’s profitability. It is calculated as revenue minus expenses, excluding interest and tax.

Industry Jargon

IBISWorld Glossary

BABY BOOMER A person born between 1946 and 1964 accounting for a major proportion of the population.

CARDIOVASCULAR EQUIPMENT Equipment used for aerobic exercise, meant to be used at light to medium intensity for a long period of time, e.g. treadmills, elliptical trainers and stationary bikes.

PILATES A physical fitness system developed in the early 20th century by Joseph Pilates with a focus on the strength and endurance of core muscle groups.

RETENTION RATE A rate comparing the number of new gym memberships to canceled gym memberships.

WWW.IBISWORLD.COM Gym, Health & Fitness Clubs in the US January 2016 32

Jargon & Glossary

VOLATILITY The level of volatility is determined by averaging the absolute change in revenue in each of the past five years. Volatility levels: very high is more than ±20%; high volatility is ±10% to ±20%; moderate volatility is ±3% to ±10%; and low volatility is less than ±3%.

WAGES The gross total wages and salaries of all employees in the industry. The cost of benefits is also included in this figure.

IBISWorld Glossary continued

Disclaimer

This product has been supplied by IBISWorld Inc. (‘IBISWorld’) solely for use by its authorized licenses strictly in accordance with their license agreements with IBISWorld. IBISWorld makes no representation to any other person with regard to the completeness or accuracy of the data or information contained herein, and it accepts no responsibility and disclaims all liability (save for liability which cannot be lawfully disclaimed) for loss or damage whatsoever suffered or incurred by any other person resulting from the use

of, or reliance upon, the data or information contained herein. Copyright in this publication is owned by IBISWorld Inc. The publication is sold on the basis that the purchaser agrees not to copy the material contained within it for other than the purchasers own purposes. In the event that the purchaser uses or quotes from the material in this publication - in papers, reports, or opinions prepared for any other person - it is agreed that it will be sourced to: IBISWorld Inc.

At IBISWorld we know that industry intelligence is more than assembling factsIt is combining data with analysis to answer the questions that successful businesses askIdentify high growth, emerging & shrinking marketsArm yourself with the latest industry intelligenceAssess competitive threats from existing & new entrantsBenchmark your performance against the competitionMake speedy market-ready, profit-maximizing decisions

Who is IBISWorld?We are strategists, analysts, researchers, and marketers. We provide answers to information-hungry, time-poor businesses. Our goal is to provide real world answers that matter to your business in our 700 US industry reports. When tough strategic, budget, sales and marketing decisions need to be made, our suite of Industry and Risk intelligence products give you deeply-researched answers quickly.

IBISWorld MembershipIBISWorld offers tailored membership packages to meet your needs.

Copyright 2016 IBISWorld Inc

www.ibisworld.com | 1-800-330-3772 | [email protected]