Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no

longer permitted.

IC-DISC Tax Law Challenges: Structuring and Planning Techniques to Maximize Tax Savings Post-Tax ReformNavigating Applicable IRC Sections, Formation and Qualification Issues

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, MAY 24, 2018

Presenting a live 90-minute webinar with interactive Q&A

Mehrdad Ghassemieh, Partner, Harlowe & Falk, Tacoma, Wash.

Michelle Rizzo, CPA, MBA, Tax Manager, WithumSmith+Brown, Princeton, N.J.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-328-9525 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the

problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone

listening is no longer permitted.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you

will receive immediately following the program.

For CPE credits, attendees must participate until the end of the Q&A session and

respond to five prompts during the program plus a single verification code. In addition,

you must confirm your participation by completing and submitting an Attendance

Affirmation/Evaluation after the webinar.

For additional information about continuing education, call us at 1-800-926-7926 ext. 2.

FOR LIVE EVENT ONLY

IC- DISC Export Tax Incentive

Mehrdad Ghassemieh

Harlowe & Falk, LLP

4

Overview

• IC-DISC Basics

• Tax Savings – Post TCJA

• IC-DISC Requirements• Export Gross Receipts Test• Qualified Export Property Test• Export Assets Test

• IC-DISC Implementation

• IC-DISC Structuring Alternatives

5

IC-DISCExport Tax Incentive

6

IC-DISC Basics

• IC-DISC - Interest charge domestic international sales corporation

• Domestic corporation

• Elect to be treated as an IC-DISC by filing IRS Form 4876-A

• An IC-DISC is not subject to federal income tax (IRC 991).

7

Structure without IC-DISC

Individual Owners

ForeignCustomers US

MFG

Flow Through Income

(taxed to individual at

marginal rates )$ for goods

Export goods

8

Structure with IC-DISC

Individual Owners

ForeignCustomers US

MFG

Flow Through Income

(taxed to individual at

marginal rates)

$ for goods

Export goods

IC-DISC

Commission

Dividend (taxed at dividend

rates)

9

IC-DISCTax Savings – Post TCJA

10

Tax Savings – Flow Through Entities• Section 199A

– 20% - Qualified business income deduction

– Potential Effective Rate of 29.6% for owners

• Limitation – W2 or Depreciable Property Limit

11

Tax Savings – Flow Through Entities

Individual Owners

US MFG

Flow Through TI $100 * tax rate 37%Tax $37

Export Income $100

Total Tax $37

12

Individual Owners

US MFG

Flow Through TI $100Sec. 199A - $20Taxable Income $80 * tax rate 37%Tax $30

Export Income $100

Total Tax $30

Total Tax $30- $37

No Sec. 199A Deduction

Full Sec. 199A Deduction

Tax Savings – Flow Through Entities

Individual Owners

US MFG

IC-DISC

Commission

Export Income $100DISC Commission $100Export TI $ 0

$100

Dividend income $100 * Dividend tax rate 23.8%Tax $23.8

Commission receipts $100* DISC tax rate 0%Tax $0

Total Tax $24

13

Expected Tax Savings

6% - 13%

Tax Savings - Corporations• Foreign Derived Intangible Income

– To encourage corporations to keep their intangible property in the U.S., the FDII rules reduce the U.S. tax rate on foreign source income.

• “Foreign Derived Intangible Income (FDII)” receives a 37.5% deduction to reduce effective tax rate to 13.125%. (21% tax * 62.5% of FDII) . §250(a)(1)(A)

• FDII = Deemed Intangible Income * percentage of foreign revenue– Foreign revenue = sales of property to foreign customers for use outside the U.S., and sales of services to

foreign customers. §250(b)(4)

• Deemed Intangible Income = “Deduction Eligible Income” – “Deemed Tangible Income Return”.• Deduction Eligible Income = Gross Income excluding certain foreign net income subject to US tax under other rules

(Subpart F, GILTI, branch income, and CFC dividends), also excluding certain financial services and oil & gas income. §250(b)(3)

• Deemed Tangible Income Return = 10% * Qualified Business Asset Investment (QBAI = Tax basis in tangible business property). §250(b)(2)(B)

• Expected Tax Savings – 13.125% - 21%

14

Amounts paid by an operating company to its related IC-DISC (usually commissions)are deductible to the operating company. An IC-DISC does not pay corporate incometax on its income. This yields two primary benefits:

1) Lower Tax Rate: Companies without an IC-DISC realize income at ordinary rates.Income permitted to flow through the IC-DISC reduces the income taxed at theserates, and such income is not taxed in the hands of the IC-DISC. When the IC-DISCdistributes earnings to the shareholders, they represent dividend income, whichmay be taxable at qualified rates.

2) Tax Deferral- An IC-DISC is permitted to retain earnings attributable to the first$10,000,000 of gross receipts, deferring taxation to its shareholders. An interestcharge is imposed on the deferred tax amounts, and the rate is determined by the“base period T-bill rate” (currently a fraction of a percent). This amounts to a lowinterest loan from the government in the amount of the deferred tax liability, andmay be an attractive borrowing option in the current low-interest rateenvironment. Funds retained by an IC-DISC may generally be loaned back to therelated business (subject to conditions which requirecareful monitoring).

15

IC-DISC Benefits

IC-DISCRequirements

16

IC-DISC – No Operational Changes

• If statutory requirements of DISC met, no operationalchanges are needed

• DISC can be a “paper company”. Treasury Regulations state DISC isnot required to have employees, bear risk, or otherwise have anyeconomic substance.

• Accounting costs: • Requires separate books and records• Must file 1120-IC-DISC

17

DISC Requirements • Corporation incorporated within the United States

• Single class of stock

• Stock par value > $2,500

• Elect to be treated as IC-DISC (F4876A)

• Not in same controlled group as a foreign sales corp (FSC)

• Maintain own books and records

• 95% of receipts must be “qualified export receipts”

• 95% of adjusted basis of assets must be “qualified export assets” at the end of the tax year.

18

Qualified Export Property

• Produced in U.S. Test: Manufactured, produced, grown or extracted in the U.S. by a party other than a DISC

• Destination Test: Held primarily for sale, lease or rental, in the ordinary course of trade or business, by or to a DISC for direct use, consumption or disposition outside the U.S.

• FMV Test: Less than 50% of the fair market value of which is attributable to articles imported into the U.S.

19

Manufactured or Produced Test

•Substantial Transformation. If property “substantiallytransformed”; Examples woodpulp to paper, steel rod toscrews, canning of fish.

•Operations Generally Constitute Manufacturing: Activity is“substantial in nature” and generally constitutesmanufacturing.

•Value Add Test: property conversion costs (direct labor andfactory burden including packaging and assembly) accountsfor 20% or more of the COGS.

20

Destination Test

• Destination Test: In order to qualify as “export property,”property must be “sold or leased for direct use,consumption or disposition outside the United States”.

• Direct delivery outside of the United States; or

• if property is delivered “[w]ithin the United States to a purchaser orlessee, if such property is ultimately delivered, directly used, or directlyconsumed outside the United States (including delivery to a carrier orfreight forwarder for delivery outside the United States) by the purchaseror lessee (or a subsequent purchaser or sublessee) within 1 year aftersuch sale or lease.”

21

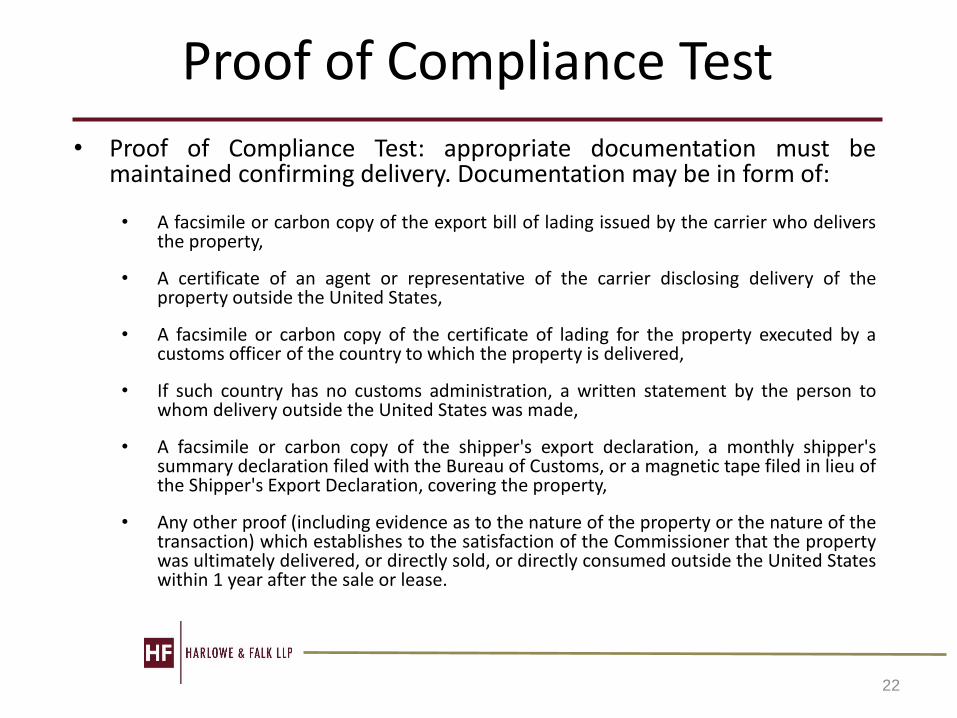

Proof of Compliance Test

• Proof of Compliance Test: appropriate documentation must bemaintained confirming delivery. Documentation may be in form of:

• A facsimile or carbon copy of the export bill of lading issued by the carrier who deliversthe property,

• A certificate of an agent or representative of the carrier disclosing delivery of theproperty outside the United States,

• A facsimile or carbon copy of the certificate of lading for the property executed by acustoms officer of the country to which the property is delivered,

• If such country has no customs administration, a written statement by the person towhom delivery outside the United States was made,

• A facsimile or carbon copy of the shipper's export declaration, a monthly shipper'ssummary declaration filed with the Bureau of Customs, or a magnetic tape filed in lieu ofthe Shipper's Export Declaration, covering the property,

• Any other proof (including evidence as to the nature of the property or the nature of thetransaction) which establishes to the satisfaction of the Commissioner that the propertywas ultimately delivered, or directly sold, or directly consumed outside the United Stateswithin 1 year after the sale or lease.

22

Excluded Property

•Export property does not include:

• Patents, inventions, models, designs, formulas, or processes, whether or notpatented, copyrights (other than films, tapes, records, software or othersimilar reproductions for commercial or home use), goodwill, trademarks,trade brands, franchises, and other like property.

• Certain products of a character for which a deduction for depletion isallowable (e.g., unprocessed/unrefined oil, gas, coal, or uranium products).

• Property leased by a DISC for use by any member of a controlled group.

• Export property subsidized by the U.S.

• Products for which export is prohibited under Export Admin Act of 1979.

• Unprocessed timber which is a softwood.

23

Services

• Related & Subsidiary. Services that are related to and subsidiary to any qualified sale, exchange, lease or disposition of export property.

• Engineering & Architectural. Engineering and architectural services for construction projects outside the United States.

24

Computer Software

•Computer software qualification for disc benefits

• Classification of Computer Software - Treasury Regulations under1.861-18 (“-18 Regs”)

• Transfer of computer program classified as one of the following:• (i) A transfer of a copyright right in the computer program;

• (ii) A transfer of a copy of the computer program (a copyrightedarticle);

• (iii) The provision of services for the development or modificationof the computer program; or

• (iv) The provision of know-how relating to computer programmingtechniques.

25

Computer Software

•Computer software qualification for disc benefits

• Transfers creating a copyright right – 1.861-18(c)(2):

• (i) The right to make copies of the computer program for

purposes of distribution to the public by sale or other transfer of

ownership, or by rental, lease or lending;

• (ii) The right to prepare derivative computer programs based

upon the copyrighted computer program

• (iii) The right to make a public performance of the computer

program; or

• (iv) The right to publicly display the computer program.

26

Computer Software

•Computer software qualification for disc benefits

• Transfers creating a copyright right – 1.861-18(c)(2):

• (i) The right to make copies of the computer program for purposes ofdistribution to the public by sale or other transfer of ownership, or byrental, lease or lending;

• (ii) The right to prepare derivative computer programs based uponthe copyrighted computer program

• (iii) The right to make a public performance of the computer program;or

• (iv) The right to publicly display the computer program.

• Means of transfer not to be taken into account. The rules of thissection shall be applied irrespective of the physical or electronic orother medium used to effectuate a transfer of a computer program.Treas. Reg. Sec. 1.861-18(g)(2).

27

Qualified Export Assets

• Export property (i.e., inventory)• Export property assets • Accounts receivable • Temporary investments of working capital • Producer’s loans • Stock or securities in a related foreign export corporation • Export-Import Bank and Foreign Credit Insurance

Association obligations • Export sales finance obligations • Temporary bank deposits in U.S.

28

29

IC-DISCImplementation

30

Corporate Setup

• Entity Type. Must be a Corporation.

• Place of Incorporation. Must be within the United States. • Consider State and Local Tax Exposure.

• Look at Washington State for incorporation. See ETA 3178.2013.

• Corporate Documents. Articles, Bylaws, Organizational Consent, etc.

• Include DISC specific language; for example: • Single class of stock• Stock par value > $2,500• Export Receipts & Export Assets Test

31

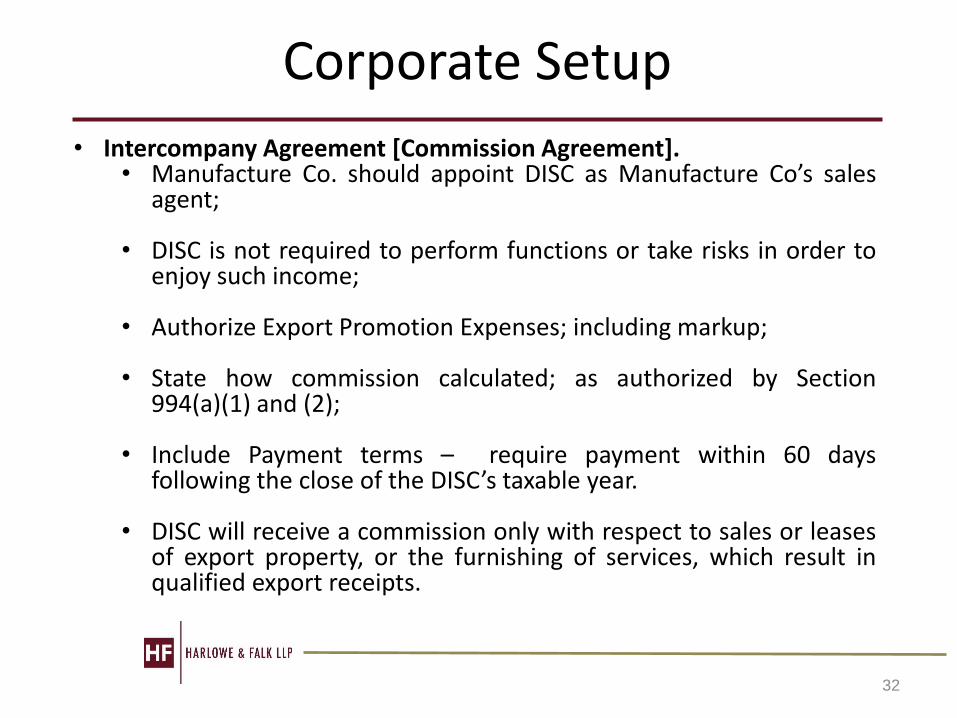

Corporate Setup

• Intercompany Agreement [Commission Agreement].• Manufacture Co. should appoint DISC as Manufacture Co’s sales

agent;

• DISC is not required to perform functions or take risks in order toenjoy such income;

• Authorize Export Promotion Expenses; including markup;

• State how commission calculated; as authorized by Section994(a)(1) and (2);

• Include Payment terms – require payment within 60 daysfollowing the close of the DISC’s taxable year.

• DISC will receive a commission only with respect to sales or leasesof export property, or the furnishing of services, which result inqualified export receipts.

32

Corporate Setup

33

• Treas. Reg. 1.992-2

• File Form 4876A

• Timing:

• New Corp: within 90 days after thebeginning of such taxable year.

• Existing Corp: within 90 prior to yearend.

• Consent – Shareholders must consent

• In Community property states, bothspouses must consent

IC-DISCStructuring Alternatives

34

IC-DISC – Typical DISC Structure

• U.S. Manufacturer (Partnership or S Corp) directly exports product

35

Individual Owners

ForeignCustomers

US MFG

$ for goods

Export goods

IC-DISC

Commission Dividend

IC-DISC – Typical DISC Structure

• U.S. Manufacturer (C Corp) directly exports product

36

Individual Owners

ForeignCustomers

$ for goods

Export goods

IC-DISCCommissionUS MFG

Dividend

IC-DISC – Ultimate Export Structure

• U.S. Manufacturer that indirectly exports goods

ForeignCustomers US

MFG

$ for goods

Export goods

Buy/SellDistributor

$ for goods

Export goods

• Goods must be exported within 1 year of sale; • Need compliance of Distributor to meet the “proof of

compliance test”.

37

IC-DISC

Commission

IC-DISC – Operating DISC Structure

• Buy/Sell distributor involved in exports

ForeignCustomers US

MFG

$ for goods

Export goods

Buy/SellDistributor

$ for goods

Export goods

• Distributor enters into buy/sell agreements with unrelated third parties;

• Use of 482 method; • Distributor company can be DISC company, all export

profits DISC eligible

38

DISC Company

Buy/Sell Distributor w/Domestic Sales• Buy/Sell distributor involved in exports

ForeignCustomers

US MFG

$ for goods

Export

goods

Buy/SellDistributor

$

Export

goods

• Opco Distributor sets up new DISC company.

• DISC contracts with US MFG & foreign clients

• Existing Opco contracts with US MFG & domestic clients

• DISC pays Opco a service fee for services performed by Opco on behalf of DISC

DISC

Company

Buy/Sell Distributor

DomesticCustomers

$ for goods

Domestic

goods

$

Domestic

goods

Service Fee $

IC-DISC – Operating DISC Structure

• Broker for export sales

ForeignCustomers US

MFG

$ for goods

Broker

$ Commission

Export goods

• Broker earns commission for export sales; • Use of 482 method; • Broker company can be DISC company, all export commissions

DISC eligible; • Need compliance of US MFG to meet proof of compliance test.

40

DISC Company

41

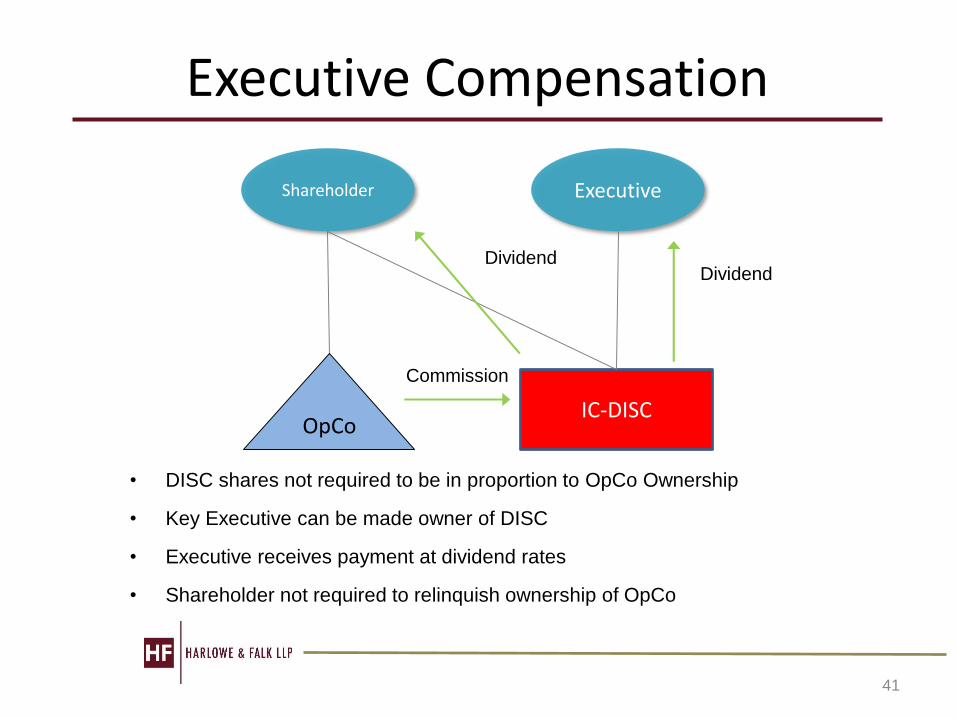

Executive Compensation

Shareholder

IC-DISC

Executive

• DISC shares not required to be in proportion to OpCo Ownership

• Key Executive can be made owner of DISC

• Executive receives payment at dividend rates

• Shareholder not required to relinquish ownership of OpCo

DividendDividend

Commission

OpCo

42

Estate Planning

Shareholder

OpCoIC-DISC

Next Generation

• Commission payments not included in estate for estate tax purposes

• Risk: See Rev. Rul. 81-54 (deemed gift)

• See Hellweg v. Commissioner, T.C. Memo. 2011-58

Dividend

Commission

Owners

ForeignCustomers OpCo

Flow

Through

Income

(taxed to

individual at

marginal

rates)

$ for goods

Export

goods

IC-DISCCommission

Dividend

Roth IRA

Holding Company

Dividend

IRA Planning

43

• Summa Holdings v. Commissioner, 848 F.3d 779 (6th Cir.)

• Benenson v. Comm. (1st Cir.)

• Benenson v. Comm. (2nd Cir.)

• Mazzei v. Commissioner, 150 T.C. No. 7

Contact Information

Mehrdad Ghassemieh• Harlowe & Falk LLP

• Phone: (253) 284-4424

• Email: [email protected]

44

45

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

46

SM

IC-DISCMichelle Rizzo CPA, MBA

Tax Manager

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

47

SM

HOW AN IC-DISC CAN BENEFIT YOUR BUSINESS

What does the IC-DISC do?

How are the tax savings calculated?

Establishing and maintaining the IC-DISC.

Who is eligible?

What property qualifies? vs What is excluded?

Tax compliance requirements.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

48

SM

IC-DISC – WHAT IS IT? AND WHAT DOES IT DO?

1

1) Converts ordinary incomeinto qualified dividend income

2

2) Defers income.

48

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

49

SM

STRUCTURING THE IC-DISC FOR C-CORPS WITHOUT AN IC-DISC

Individuals

Operating Company (C-Corp)

$1,000,000 earnings$210,000, 21% corporate income tax

$790,000 cash after taxes

$790,000 dividend$158,000, 20% capital gain tax, $632,000 left

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

50

SM

STRUCTURING THE IC-DISC FOR C-CORPS WITH AN IC-DISC

Individual owners

Operating Company (C-Corp)

IC-DISC

$1,000,000 commission0% tax

$1,000,000 dividend$200,000, 20% capital gain tax,

$800,000 left

$800,000-$632,000

$168,000 Savings

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

51

SM

STRUCTURING THE IC-DISC FOR PASSTHROUGHS WITHOUT AN IC-DISC

Individuals

Operating Company (LLC, S-Corp, Partnership)

$1,000,000 earnings$370,000, 37% ordinary income tax $630,000 net

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

52

SM

STRUCTURING THE IC-DISC FOR PASSTHROUGHS WITH AN IC-DISC

Individuals

Operating Company (LLC, S-Corp, Partnership)

IC-DISC

$1,000,000 commission

0% tax

$1,000,000 dividend

$1,000,000 dividend20% capital gain rate

$800,000 net

$800,000$630,000

$170,000 Savings

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

53

SM

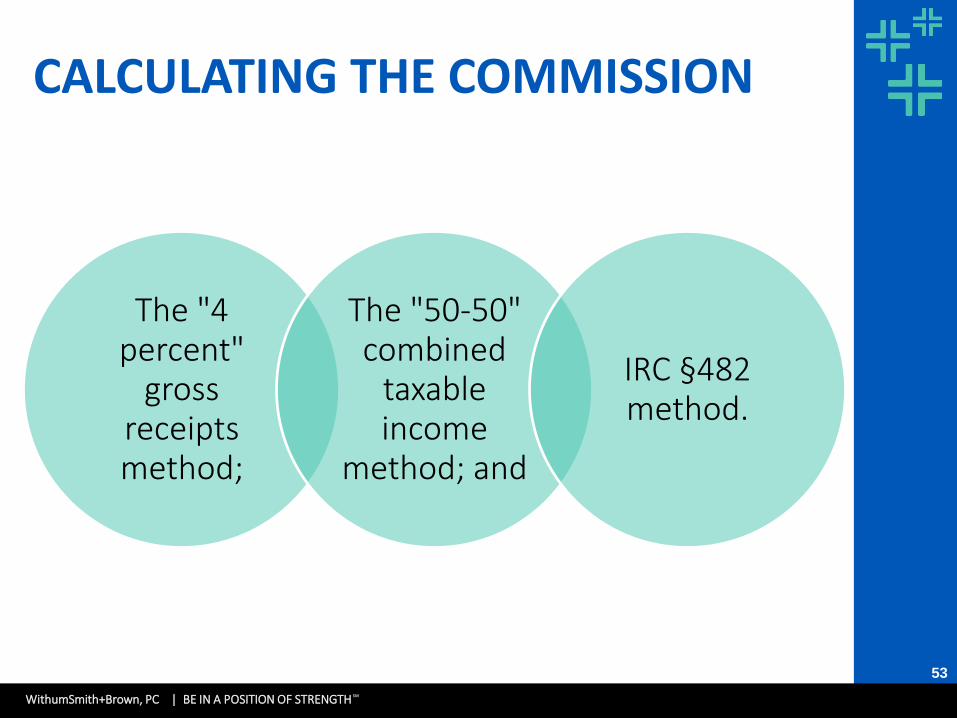

CALCULATING THE COMMISSION

The "4 percent"

gross receipts method;

The "50-50" combined

taxable income

method; and

IRC §482 method.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

54

SM

EXAMPLE

▪ A corporation manufactures children’s toys and exports 100% of its inventory overseas. In 2017, it has $10 million of qualified gross receipts from these sales. It’s net income is $2 million.

▪ Using the 4% of sales method gives us a commission of $400,000 (4 percent of $10 million).

▪ Using the 50% of net income method gives us a commission of $1 million (50 % of $2 million)

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

55

SM

C CORPORATION EXAMPLE

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

56

SM

Impact of the Medicare and Net Investment Income Tax to Corporations

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

57

SM

Impact of the Medicare and Net Investment Income Tax to Flow Throughs

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

58

SM

IC-DISC – DEFERRAL OF TAX / INTEREST CHARGES

▪ An IC-DISC may choose not to pay a dividend to its shareholders. In this case, an interest charge would apply to the deferred tax (hence the entity’s name). The interest charges are based on Treasury bill rates, so at this time the potential interest charges are small. The interest charge is imposed on the shareholder and not the DISC.

▪ The shareholder reports the interest charge on Form 8404, Interest Charge on DISC-Related Deferred Tax Liability.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

59

SM

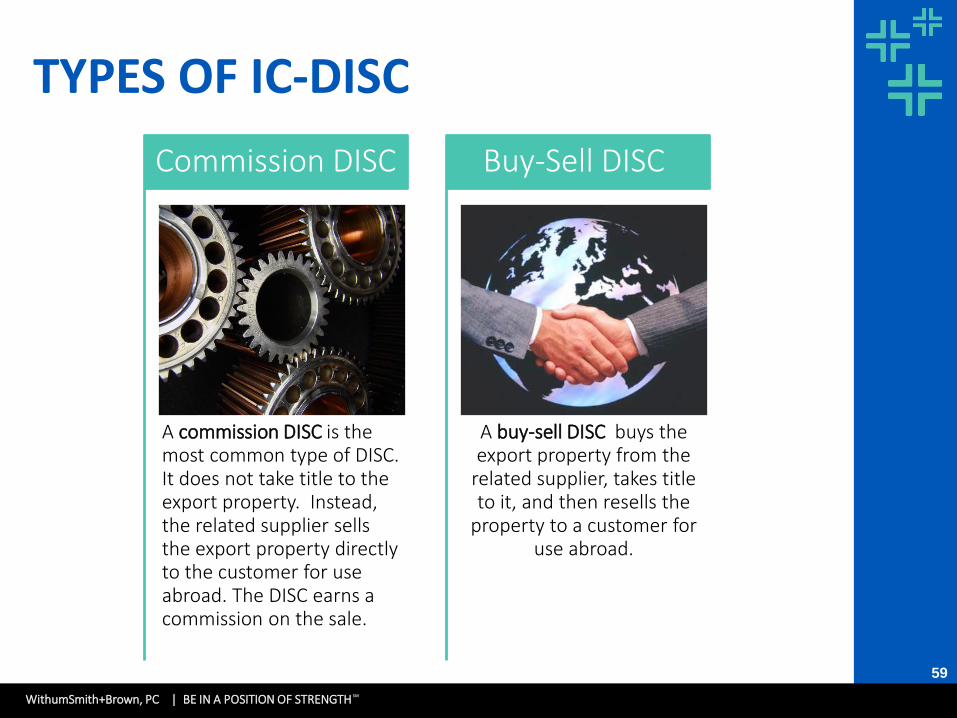

TYPES OF IC-DISC

A commission DISC is the most common type of DISC. It does not take title to the export property. Instead, the related supplier sells the export property directly to the customer for use abroad. The DISC earns a commission on the sale.

Commission DISC

A buy-sell DISC buys the export property from the

related supplier, takes title to it, and then resells the

property to a customer for use abroad.

Buy-Sell DISC

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

60

SM

THE TAX BENEFIT DOES NOT APPLY TO LOSS COMPANIES

Under Treas. Reg. §1.994-1(e)(1), IC-DISCs cannot cause a taxable loss for

the related supplier in any year subject to certain

exceptions.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

61

SM

QUALIFYING AND MAINTAINING IC-DISC STATUS

In addition to the formation requirements,

to qualify as an IC-DISC,

the entity must maintain

the following requirements

annually:

• At least 95% of the IC-DISC’s gross receipts must be qualified export receipts (QER);

• At least 95% of the total adjusted basis of all the IC-DISC’s assets must be qualified export assets (QEA);

• An IC-DISC tax return, Form 1120-IC-DISC, must be filed annually by the 15th day of the ninth month following the close of the IC-DISC’s taxable year.

• The IC-DISC’s taxable year must be the same as that of its principal shareholder.

• Extensions are not permitted; and

• International boycott operations must be disclosed.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

62

SM

EXPORT PROPERTY

Property that is manufactured, produced, grown, or extracted in the U.S. with an ultimate destination outside the U.S.;

Property that is held primarily for sale, lease, or rental, in the ordinary course of trade or business for direct use, consumption, or disposition outside the U.S.; and

• Goods must be exported within a year from sale;

• The use test focuses on where the property is ultimately used, consumed, or disposed; and

• Property sold to any person whose principal business consists of selling from inventory to retail customers at retail outlets outside of the U.S. will be considered to be used predominantly outside the U.S.

At least 50% of the property’s fair market value must be from articles made in the U.S.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

63

SM

QUALIFIED EXPORT PROPERTY EXCLUSIONS Property leased or rented by a DISC for use by any member of a controlled group;

Certain Intangible Property -Patents, inventions, models, designs, formulas, or processes, whether or not patented, copyrights (other than books, films, tapes, records, or similar reproductions, for commercial or home use), good will, trademarks, trade brands, franchises, or other like property (Computer software may qualify as export property);

Depletable Products - Products of a character with respect to which a deduction for depletion is allowable (including oil, gas, coal, or uranium products) under section 613 or 613A;

Export Controlled Products - Products whose export is prohibited or curtailed under section 7(a) of the Export Administration Act of 1979 to effectuate the policy set forth in paragraph (2)(c) of section 3 of such Act (relating to the protection of the domestic economy); or

Any unprocessed timber that is a softwood.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

64

SM

QUALIFIED EXPORT RECEIPTS

Gross receipts from the sale, exchange, or other disposition of export property;

Gross receipts from the lease or rental of export property, which is used by the lessee of such property outside the U.S.;

Gross receipts for services which are related and subsidiary to any qualified sale, exchange, lease, rental, or other disposition of export property by such corporation;

Gross receipts from the sale, exchange, or other disposition of qualified export assets (other than export property);

Dividends (or amounts includible in gross income under section 951) with respect to stock of a related foreign export corporation (as defined in subsection (e));

Interest on any obligation which is a qualified export asset;

Gross receipts for engineering or architectural services for construction projects located (or proposed for location) outside the U.S.; and

Gross receipts for the performance of managerial services in furtherance of the production of other qualified export receipts of a DISC.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

65

SM

QUALIFIED EXPORT RECEIPTS -EXCLUSIONS

Sales, exchanges, leases, rentals, or other

dispositions, or furnishing of services that is for ultimate

use in the U.S.;

Receipts that are accomplished by a subsidy granted by the U.S. or any

instrumentality thereof; and

Receipts from the U.S. or any instrumentality thereof where the use of such

export property or services is required by law or

regulation.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

66

SM

ESTABLISHING THE IC-DISC

• The corporation must have only one class of stock;

• The par value of the stock must be at least $2,500 for each day of the tax year;

The IC-DISC must be set up as a U.S. corporation; and

• The election is made on Form 4876-A, Election to Be Treated as an Interest Charge DISC.

• Must be filed within 90 days of the beginning of the tax year in which the election will take effect.

An election is made to treat the entity as an IC-DISC.

The corporation maintains separate books and records.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

67

SM

FOREIGN ASPECTS

The dividends paid from an IC-DISC to its shareholders are generally considered to be foreign-source income. This makes the use of an IC-DISC particularly valuable to U.S. shareholders with passive foreign tax

credit carryovers because this foreign income may be eligible to release the

foreign tax credits.

An IC-DISC is also allowed to have foreign shareholders as long as the foreign shareholder agrees to be treated as

engaged in a trade or business in the U.S.

(Note: Certain tax treaties may serve to override this rule).

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

68

SM

DEEMED DISTRIBUTIONS

An IC-DISC shareholder is taxable on the last day of the IC-DISC’s tax year on a deemed distribution, whether or not actually received, on the following amounts:

• IC-DISC income attributable to qualified export receipts in excess of $10 million;

• Gross income derived on producers loans;

• Gain recognized by the IC-DISC on the sale of property, whether or not the property is a qualified export asset;

• 50% of IC-DISC income attributable to military property;

• One seventeenth of IC-DISC taxable income for the year before the deemed distributions;

• Income attributable to international boycott operations; and

• Illegal bribes, kickbacks, or other payments made on behalf of an IC-DISC.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

69

SM

DEEMED DISTRIBUTION EXAMPLE

• $20 million qualified export receipts

• $8 million in net income on these receipts

• 50% of net income or $4 million is able to be paid in commission income to the IC-DISC

Facts

• Because $20 million is twice $10 million, half of the commission income is considered to be a deemed dividend

• Therefore, $2 million is deemed distributed while $2 million can remain in the DISC tax deferred.

Result

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

70

SM

FORM 4876-A

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

71

SM

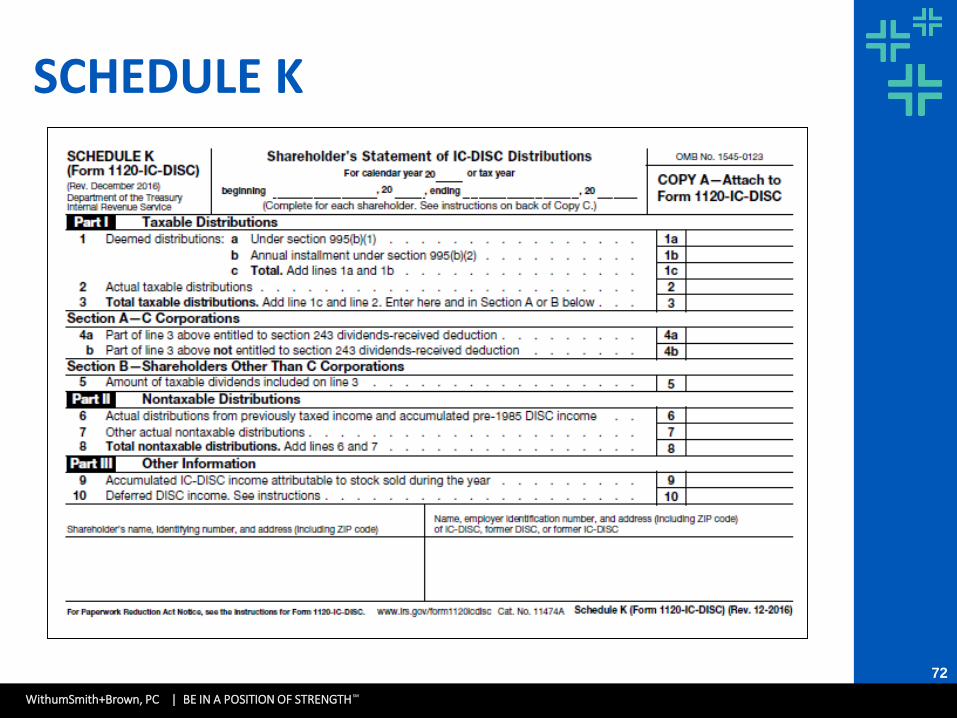

1120-IC-DISC

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

72

SM

SCHEDULE K

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

73

SM

FORM 8404

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

74

SM

MOST COMMON MISTAKES

MUST keep a separate bank account with at least $2,500 for the par value of the stock and a separate set of books and records.

Timing of the elections and timing of the commission payment.

Rushing to complete the IC-DISC return before the related supplier’s return is finalized and its taxable income has been determined.

An entity structure other than a C Corporation being established to be used as an IC-DISC.

Assets on the balance sheet that are invested in securities accounts.

1

2

3

4

5

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

75

SM

State implications

• Some states follow federal treatment of zero tax

• Some states treat the IC-DISC as an ordinary corporation subject to the state’s corporate tax rate

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

76

SM

IC-DISC AND ROTH IRA!

Roth IRA

Holding Company

IC-DISC

Roth IRA

Summa Holdings Inc

Commissions

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

77

SM

REFERENCES

1. Form 4876-A, Election To Be Treated as an Interest Charge DISC and Instructions.

2. Form 8404, Interest Charge on DISC-Related Deferred Tax Liability and Instructions.

3. Form 1120-IC-DISC, Schedule K, Shareholder’s Statement of IC-DISC Distributions and Instructions.

4. IRC §1.995(f)-(1)(j)(2).

5. IRC §991-996.

6. IRC §1.991-1(a).

7. Treas. Reg. §1.993-4.

8. Treas. Reg. § §1.993-1; 1.993-3.

9. Treas. Reg. §1.994-1.

10. IRS’ IC-DISC Audit Guide

11. Summa Holdings Inc., v Commissioner of Internal Revenue

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

78

SM

THANK YOU

Michelle Rizzo, CPA, MBATax Manager International Tax Group(609) 945 [email protected]

Follow @WithumCPA on Social Media!