Embed Size (px)

Citation preview

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

LUCKNOW BRANCH OF CICASA

ICAI Bhawan, Vikas Khand -1, Gomti Nagar, LucknowE-mail: [email protected]:- 0522-4069931 www.lucknowicai.com

STUDENT'S

E-NEWSLET TERFOR THE MONTH OF MAY

Managing Committee Member

2018-2019

CA. Piyush K. MisraChairman

CA. Joy MukherjeeVice Chairman

CA. Rahul VermaSecretary

CA. Raveesh ChaudhryTreasurer & CICASA Chairman

Ex-Officio

CA. Hemant KumarExecutive Member

CA. Prem S. KhandelwalExecutive Member

CA. Tushar Nagar

Executive Member

CA. Manu AgarwalCCM

Dear students!

It gives me immense pleasure to interact with you all through this newsletter. I

congratulate Chairman CICASA and his team for providing knowledge to the Students

through latest technology i.e. E-News Letter. The new committee is already in action

and we'll give our best to fulfill your expectations. CICASA time to time conducts events

for holistic development of CA students. Thus, I request you all students to participate

as much as you can. I feel proud to share with you all that Lucknow branch of CICASA

is doing commendable job for student activities. Congratulations to the previous

committee members of CICASA and Lucknow branch as well as all the members and

students for their constant support. Hereafter, it's our responsibility to carry forward the

legacy and scale new heights. I assure that we'll leave no stone unturned while

performing the responsibilities conferred upon us. I am glad to inform that during the

past two months we have organized seminar on Bank Audit, Industrial visit on women's

Day and Counseling program for CA Final and IPCC students, all of which were very

successful. This newsletter covers some of the glimpses of these programmes. For

successful conduction of events we're planning to form sub-committees and students

for more information can contact the committee members. The committee is planning to

celebrate various days such as CA day, Independence Day, Yoga day and organize

seminars, elocution contest, quiz, study circles, cultural and sports activities along with

the National Conclave for the students. You now can also ask queries, give valuable

suggestions on our new mail [email protected]. In the end, I request all

students to spare their valuable time and give write ups for upcoming newsletter. I truly

believe that- “On the road to success, the rule is always to look ahead” so my dear

students in the journey of your life never be afraid to take a step forward.

Warm regards,

CA Piyush Kumar Misra

From Chairmen's Desk

CA. PIYUSH KUMAR MISRACHAIRMAN, LUCKNOW BRANCH

From Chairmen's Desk

CA. Raveesh ChaudhryCHAIRMAN, LUCKNOW BRANCH OF CICASA

Dear Students,Greetings to all of my Future Chartered Accountants and i am delighted to communicate to you all as 9th Chairman of CICASA Lucknow. I put on record my gratitude to Chairman CA.Piyush Mishra and all the members of Committee for reposing faith in me and entrusting me with the overall responsibility of CICASA and Treasurer of the Lucknow Branch. I am confident that under the dynamic leadership of Chairman CA. Piyush Mishraand Vice Chairman CA Joy Mukherjee, I shall be able to carry out these responsibilities. With the active cooperation of my enthusiastic CIRC CICSA Chairman, CA. Nilesh Gupta for the year 2018-19, we will be taking new initiatives for the overall benefit of our student fraternity.This is first Student Magazine for the term 2018-19 and i dedicate this month magazine to my GURU/MY GOD Late. CA. K.K Mohindra, who was my principal under whom i had completed my articleship. He was the person under whom CA. Girish Auhja also completed his articleship and reason behind the confidence to do practice after completing the course. Dear Students, While theoretical knowledge provides the necessary foundation, articleship training imparts the necessary skills to apply that knowledge in actual practical situation to maximize learning and value addition, So it is my appeal to all of you to give your articleship required importance as you give to your studies.As you know that the profession of chartered accountancy warrants a strong base on soft skills and IT knowledge. These are the areas where you are expected to concentrate a bit. Soft skills and IT knowledge play an important role in silhouetting career of successful CAs. Never consider the IT training being provided by the Institute lightly. I advise you to participate very seriously in the Institute's programmes on Professional Development Skills and IT Training. It is very easy to pronounce the word 'success'. But it requires a lot of pain and persistent efforts to achieve it. Success comes to those who believe in themselves and work towards it. Strong determination and willpower will definitely help you to achieve your goals. But one thing you must remember that you should have a clear idea about your destination. If you are not clear about what you wish to achieve, you can never end up there. In your journey towards success, you may encounter small setbacks. But never give up. Resume your journey with strong determination. You will be victorious and you will rejoice with the feeling of accomplishment.I also wish " All the best to those who are going to give CA exams in the month of May.

With regards,

CA. Raveesh Chaudhry

(The Only photo with my Guru/God(The Only photo with my Guru/God Late CA.KK Mohindra) Late CA.KK Mohindra)

(The Only photo with my Guru/God Late CA.KK Mohindra)

From Chairmen's Desk

CA. Nilesh GuptaChairman, CICASA of CIRC of ICAI

Dear Students,It gives me immense pleasure to communicate with you all through this

newsletter. Let me begin my communication by wishing you all a very

Happy New Financial Year 2018-19. For us Chartered Accountants, new

financial year has more importance than calendar year. I wish that this new

year you achieve all the success you deserve.I convey my best wishes to team of Lucknow branch of CICASA of ICAI for

their upcoming tenure. It is my belief that the will give their best for overall

development of the students. I also request all the students of Lucknow to

actively participate in the activities that will be organized by the branch. I

would also like students to interact directly with the team members of the

branch and share their feedbacks and suggestions so that a new pathway

can be paved for providing better learning and overall development to

students.“In the journey of success, every finishing line is a new starting line. In your

career, year after year, you have to improve once again. You've to

challenge yourself once again. After every accomplishment, the heartbeat

of success remains, What next? What else? What more? How else?”I conclude my writing with my best wishes to all the students who are

appearing in May 2017 exams with a favourite quote of Napoleon Hill:

“Patience, Persistence and Perspiration make an unbeatable combination

of SUCCESS”

With regards,

CA. Nilesh Gupta

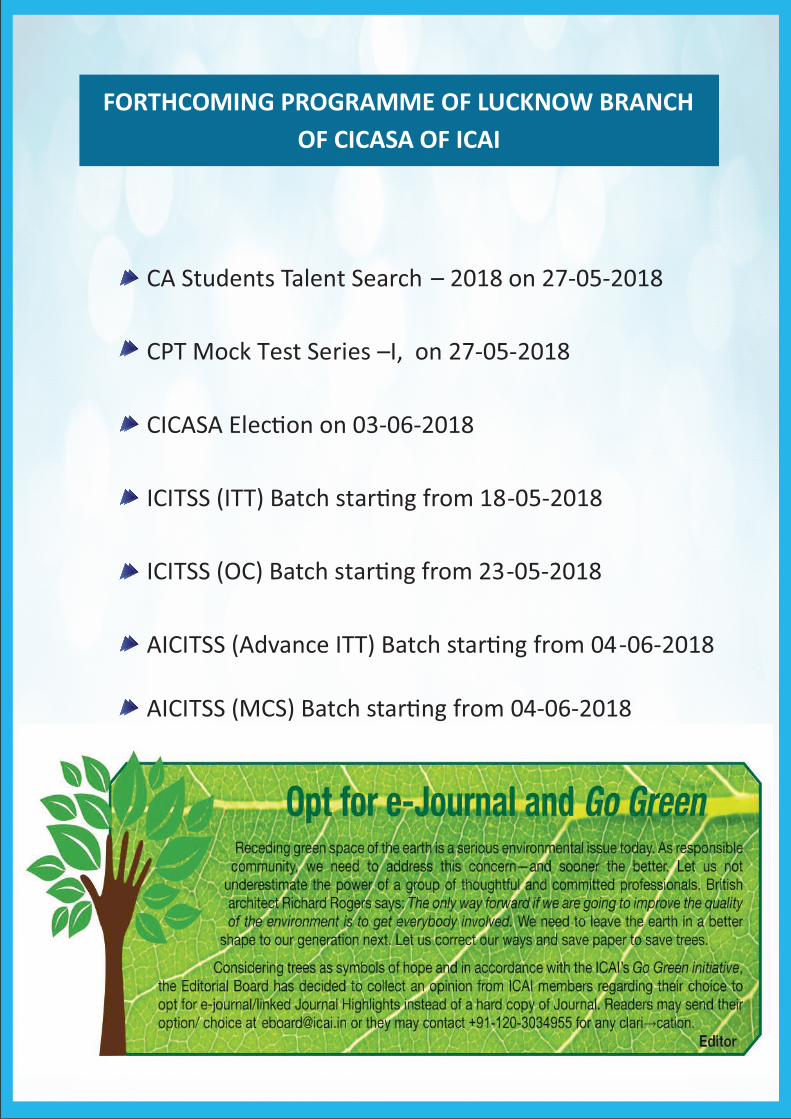

FORTHCOMING PROGRAMME OF LUCKNOW BRANCH

OF CICASA OF ICAI

CA Students Talent Search –

2018 on 27-05-2018

CPT Mock Test Series –I, on

27-05-2018

CICASA Elec�on on 03-06-2018

ICITSS (ITT) Batch star�ng from 18-05-2018

ICITSS (OC) Batch star�ng from 23-05-2018

AICITSS (Advance ITT) Batch star�ng from 04-06-2018

AICITSS (MCS) Batch star�ng from 04-06-2018

Greetings from Lucknow Branch of CIRC of The Institute of Chartered Accountants of India!! We are pleased to inform you that Lucknow Branch of CICASA is organising The First Round of “CA Students Talent Search-2018” the following four contests would be organized:- 1. Quiz2. Elocution3. Instrument music 4. Nukkad Drama The Student Talents would be organized in three stages i.e. Branch, Regional and last at National level. · The Branch level contests to be completed by 31st May, 2018.· The Regional level contest to be completed by 10th June.· The National Level contest will take place on 30th June and 1st July, 2018 At first level, these activities will be organized at the Branch level and the winners of branch level would contest at Regional level and finally the winners of Regional levels will contest in the Grand Finale at National Level for each activity. The contestants for Grand Finale of Elocution contests would be invited one day prior to the event for grooming in various aspects so that they can perform and showcase their talent well during the final Contest. Date27 May 2018 (Sunday)Time9:00 AM to 6:00 PMVenueICAI Bhawan, Gomti Nagar, LucknowFeeNilRegistration is free but mandatoryLunch will be provided to participantsEligibility: Students registered for Final Course and are undergoing articleship and students registered for Intermediate (Integrated Professional Competence) Course are eligible to participate in the CA Students Talent Search-2018. Students have to carry their registration letter or Identity Card (ICAI) with them. You may register by sending an email at [email protected] or contact @ 0522-2301524. Last date of registration is 24 May 2018 by 5:30 PM.Medium of Elocution contest: The medium would be only English.Topics: The contestant can choose any topic from the list but while choosing the topic, they need to bear in mind that they are thorough in that topic as they will be cross questioned to which they should be able to answer. · New ITR Forms - Towards deterring tax avoidance?· Place of supply under GST.· Letter of Undertaking (LOU) whether a boon or bane for banking system in India.· Data privacy over internet.· Impact of automation on employment opportunities in India.· How far revenue is important to assess the financial performance of a company? · Class Action Suit - Remedy for Investors.· Role of Bank Auditors in Present Scenario

CA Students Talent Search-2018

Duration to each contestant: Each contestant will be given twelve minutes time – a warning bell will ring at the end of the tenth minute, signaling the contestant to conclude the discussion in another two minutes.Prizes and certificates:Will be awarded to the first, second and third position holders in the concluding ceremony. Criteria for evaluation of performance: A panel of judges will judge the participants. The following criteria shall be taken into account while evaluating the performance of the participants: Sl.No.CriteriaMarks Allotted1Lucidity of language102Style of delivery103Capacity to engage the attention of the audience 104Precision of expression105Depth of coverage of the subject matter507Adherence to time limit10 Total100 Decision of the judges will be final. Winner and First Runner up will be selected from Branches. The winners of the first round competition of the Branches and Regional Office levels will participate in a Regional level competition. You can participate in the competition and motivate your eligible friends as well. B. Quiz contestNumber of winners at Branch Level:One team, comprising of 2 students, will be selected at Branch Level and will contest at Regional Level. Rules of Contest:(i) Medium of questions in Quiz Contest would be English. However, if any participant wants to speak in Hindi, the option will be given.(ii) There can be a maximum of 5 teams, each team consisting of two students. If there are more participants the 5 teams have to be selected by a process of elimination.(iii) There will be eight rounds of Quiz Contest covering the following areas: - Accounting - Auditing - Corporate Laws - Taxation - Direct and Indirect - Costing/Management Accounting/Financial Management - Information Technology - Economics - General Awareness Additionally, there will be a Rapid-Fire Round. Number of winners at Branch Level:From Branches, 2 winners of contestants selected for Regional Level Contest. Performance & Duration:1. It will be a solo performance of 10 minutes by each participant.2. Participants will bring his / her own instrument. This includes - Casio, Tabla, Keyboard, Piano, harmonium, Guitar, Violin etc.3. ICAI will only provide the platform for performance and the student has to bear the cost of instrument etc.4. Registration Fee: NILL5. Decision of the judges will be final.

D. Nukkad DramaNukkad Drama competition would be one of the major attractions of audience and this will enable the students to unveil their hidden talent and add colour to their act of speaking, character creation, emotional awareness, etc.Number of winners at Branch Level:One team, comprising of maximum 5-6 students, will be selected at Branch Level and will contest at Regional Level. Performance & Duration:1. It will be a team performance on any topic related to Chartered Accountancy Profession/curriculum.2. Each team will be given 10 minutes time for their performance.3. Medium of language for Nukkad Drama will be English, Hindi or both.4. Negative marking will be done for the performances which are not completed within stipulated time frame.5. Participants will bring their own dress, accessories, etc.6. ICAI will only provide the platform for performance and the students have to bear the cost of dress, accessories, etc.7. Registration Fee: NILL8. Decision of the judges will be final.

Date: 07-05-2018

To, All members of Students' Association of Lucknow Branch of CIRC of ICAI

Dear Member, Sub: Notice for Annual General Meeting of the members of the Students' Association of Lucknow Branch

1. This is to inform you that the Annual General Meeting of the members of the Students' Association of Luckow Branch of the Central India Regional Council will be held from 9:00 AM to 6:30 PM on 03-06-2018 (i.e., the Sunday) in the premises of the Lucknow Branch, ICAI BHAWAN “JAGRITI”, Institutional Area, Vikas Khand – I, Gomti Nagar, Lucknow – 226010 for electing 6 members of its Managing Committee for the term 2018-2019.

2. Eligibility

Every student who is a member of the Students' Association of the Lucknow Branch on 01st April, 2018 shall be eligible to stand for election to the Managing Committee of the branch provided the un-expired period of training is not less than 12 months as on 16th September, 2018.

3. Those members, who are desirous of standing for said election, may submit their nomination form duly filled in and signed by the candidate and by the Proposer and Seconder (both of whom shall be entitled to vote in the said branch election) together with a (non – refundable) nomination fee of Rs.5/- by way of Pay Order drawn in favour of the “Lucknow Branch of the CIRC of ICAI” and payable at Lucknow. While submitting the form, the candidate(s) are also required to attach Written Approval from their Principal(s).

4. The nomination form duly filled should be submitted in a sealed cover addressed to CA. Raveesh Chaudhary, Chairman, CICASA at the above address of the Branch against an acknowledgment. The blank nomination form can be had from the CICASA Chairman effective from 10.05.2018 till 5:00 PM. Of 24.05.2018, i.e. the last date of receipt of nominations. The said nomination form is also available on the website of the Branch. (www.lucknowicai.com)

ANNUAL GENERAL MEETING OF THE STUDENTS ASSOCIATION

OF LUCKNOW BRANCH OF CIRC OF ICAI

The important dates relating to the above elections are as given below.

N O M I N A T I O N F O R M F O R E L E C T I O N 2 0 1 8 - 1 9

1. Name of Candidate (in Block Letters)………………………………….........................

2. Registration No. ………………………………………………………………………………….

3. Contact No…………………………………………………………………………………………….

4. E-Mail Id………………………………………………………………………………………………

5. Address…………………………………………………………………………………………………

…………………………………………………………………………………………………...

6. Date of Enrolment…………………………………………………………………………………..

7. Date of Completion of Training………………………………………………………………..

8. Principals Name ……………………………………………………………………………………

9. Name of Firm…………………………………………………………………………………………

10. Address of firm & Contact No………………...........................................................

…………………………………………………………………………………………………….

11. Consent of Principal…………………………………………………………………………………

12. Signature of Principal……………………………………………………………………………….

PROPOSER:

1. Name: …………………………………………………………………………………………………….

2. Registration No………………………………………………………………………………………….

3. Contact No…………………………………………………………………………………………………

4. Date of Enrolment……………………………………………………………………………………..

5. Date of Completion of Training…………………………………………............................

6. Principals Name, Address & Contact No……………………………………………………….

…………………………………………………………………………………………………….

…………………………………………………………………………………………………….

7. Signature of Proposer………………………………………………………………………………….

Seconder:

1. Name: …………………………………………………………………………………………………

2. Registration No………………………………………………………………………………………….

3. Contact No…………………………………………………………………………………………………

4. Date of Enrolment……………………………………………………………………………………..

5. Date of Completion of Training…………………………………………............................

6. Employer's Name, Address & Contact No……………………………………………………

……………………………………………………………………………………………………

……………………………………………………………………………………………………

7. Signature of Seconder………………………………………………………………………………….

Nomination Fees…..………………. PO/ D.D.No…………………………..

Date: …………………………………. Signature of Candidate….............

The Insolvency and Bankruptcy Code, 2016 (IBC) was passed by the Parliament on 11 May 2016, received Presidential assent on 28 May 2016 and was notified in the official gazette on the same day.

New framework

(Provisions of this Code to override other existing laws on matters pertaining to Insolvency and Bankruptcy)

“An act to consolidate and amend the laws relating to reorganization and insolvency resolution of corporate persons, partnership firms and individuals in a time bound manner for maximization of value of assets of such persons, to promote entrepreneurship, availability of credit and balance the interests of all the stakeholders including alteration in the order of priority of payment of Government dues and to establish an Insolvency and Bankruptcy Board of India, and for matters connected therewith or incidental thereto.”

- Objective section of the Act

• Who can applySec 7-Financial Creditors Sec 9-Operational Creditors but after fulfilling the conditions of sec. 8.Sec.10-Corporate applicant i.e. authorized members, person in charge of managing the operations and who has control and supervision of the debtor

• When Upon payment default of a minimum of Rs. 1 Lakh or a Central Government prescribed amount upto Rs 1 Crore – “Statutory” cross-default for financial creditors.

• Classification of creditors Financial creditors ('persons to whom financial debt is due') Operational creditors (Trade creditors, employees etc.)

• Timelines Resolution process to complete within 180 (+90) days - failing which company liquidates compulsorily - 2 years' timeline for liquidation.

ARTICLES

The Insolvency and Bankruptcy Code, 2016

Mr. Akash Mehrotra

The Insolvency and Bankruptcy Code ecosystemNCLT – The adjudicating authority (AA)

IBB – apex body for promoting transparency & governance in the administration of

the IBC; will be involved in setting up the infrastructure and accrediting IPs & IUs.IUs - centralized repository of financial and credit information of borrowers; would

accept, store, authenticate and provide access to financial data provided by

creditors.IPs- persons enrolled with IPA and regulated by Board and IPA will conduct

resolution process; to act as Liquidator/ bankruptcy trustee; appointed by creditors

and override the powers of board of directors.Adjudicating authority (AA) - would be the NCLT for corporate insolvency; to

entertain or dispose any insolvency application, approve/ reject resolution plans,

decide in respect of claims or matters of law/ facts thereof.IPA - registered by the board shall enroll IPs

Process ow chart for insolvency resolution

Corporate InsolvencyResolution and Liquidation

Key highlights

Corporate insolvency resolution process

Application on default – Any financial or operational creditor(s) can apply for insolvency on default of debt or interest payment

Appointment of IP – IP to be appointed by the regulator and approved by the creditor committee. IP will take over the running of the Company.

From date of appointment of IP, power of Board of directors to be suspended and vested in the IP. IP shall have immunity from criminal prosecution and any other liability for anything done in good faith

Moratorium period – Adjudication authority will declare moratorium period during which no action can be taken against the company or the assets of the company. Key focus will be on running the Company on going concern basis. A Resolution plan would have to be prepared and approved by the Committee of creditors

Credit committee - A credit committee of creditors will be constituted. Related party to be excluded from committee. Each creditor shall vote in accordance to voting share assigned if 75% of creditor approve the resolution plan same needs to be implemented.

Liquidation process

Initiation – Failure to approve resolution plan within specified days will cause initiation of Liquidation. Debtor can also opt for voluntary liquidation by a special resolution in a General Meeting.

Liquidator – The IP may act as the liquidator, and exercise all powers of the BOD. The liquidator shall form an estate of the assets, and consolidate, verify, admit and determine value of creditors' claims.

Order of priority for distribution of assets

Insolvency related costs

Secured creditors and workmen dues upto 24 months

Other employee's salaries/dues up to 12 months

Financial debts (unsecured creditors)

Government dues (up to 2 years)

Any remaining debts and dues

Equity

Key aspects of the Insolvency and Bankruptcy Code

WHO CAN

INSOLVENCY BE A PROFFESSIONAL

·Chartered Accountant, Company Secretary, Cost Accountant and Advocate who has enrolled as a member of respective Institute/Bar Council and has ten years of or

·A Graduate who has fifteen years of experience in management, after receiving a Bachelor's degree from a university established or recognized by law or·Successfully completed the National Insolvency Programme, as may be approved by the IBBI or·Successfully completed the Graduate Insolvency Programme, as may approved by the IBBI

·And·has passed the Limited Insolvency Examination within twelve months before the date of his application for enrolment with the insolvency professional

·And·Has completed a pre-registration educational course, as may be prescribed by the IBBI, from an IPA after his enrolment as professional member.

INTRODUCTION: - The Goods & Service Tax popularly known as GST was enacted in INDIA from 1st July 2017, considering the achievement of its ultimate goal “One Nation – One Tax – One Market”.GST is based on concept of simple and easy online procedure, eliminating of cascading effect of tax, self -assessment of tax, promptly identification, confirmation & availment of input tax credit (ITC) in timeliness manner, lessor compliances, ease of doing business and tax filing, documentation etc., reduction in tax evasion, increase in GDP, transparency, self -determination of tax liability etc.In order to ensure thorough compliances of the applicable provision of law within the statutory time limit by taxable person, a contemporary and robust audit mechanism has been framed under GST Act.

DEFINITION OF AUDIT :-Under Section 2 (13) of the CGST Act 2017, “audit” means the examination of records, returns and other documents maintained or furnished by the registered person under this Act or the rules made thereunder or under any other law for the time being in force to verify the correctness of turnover declared, taxes paid, refund claimed and input tax credit availed, and to assess his compliance with the provisions of this Act or the rules made thereunder.”

Thus, the definition of Audit under this act is wider in nature and cover not only examination of records, returns and documents maintained or furnished under this act but also examination of records, returns and documents maintained or furnished under any other law for the time being in force.

The major approach of GST audit is to verify the correctness of tax and concerned details & check whether any tax is short paid, not paid or any input tax credit is erroneously claimed or availed through auditing of relevant records, returns & other documents maintained or furnished under GST law or under any other law for the time being in force.

ARTICLES

GST AUDIT

Mr. NAZRE IMAM(REG. NO. – CRO0327749)

TYPES OF AUDIT:

(2) AUDIT OF ACCOUNTS BY PROFESSIONALS BASED ON THRESHOLD LIMIT:- As per sub section 5 of Section 35 read along with section 44(2) of CGST Act 2017 & Rule 80 of CGST Rules 2017 – Every registered person must get his account audited by a Chartered Accountant or Cost Accountant if his aggregate turnover during a financial year exceeds Rs. 2 Crore under Rule 80 (3) of CGST Rules, 2017.Such registered person is required to furnish electronically through the common portal Annual Return along with a copy of o Audited Annual Accounts ando A Reconciliation Statement, duly certified by Chartered Accountant or Cost Accountant, in prescribed FORM GSTR-9C.

RECONCILIATION STATEMENT UNDER SECTION 44(2) of CGST Act 2017 –Reconciliation statement will reconcile the value of supplies as declared in the GST Returns furnished for financial year with the Audited Annual Financial Statement and also constitute such other particulars as may be prescribed. (2) GENERAL AUDIT AS PER SECTION 65:-· General audit is covered under section 65 of CGST Act 2017. It is routine based audit. It is generally conducted by Tax Authorities itself.· The Commissioner or any officer authorized by him, pass general or specific order, to conduct audit of a registered person for such period and in such manner as may be prescribed in concerned order.· Al least 15 working days, prior to conduct of audit is given to registered person.Due Date of Audit:- Audit shall be completed within 3 months from the date of commencement of audit. However, if commissioner is satisfied, he may for the reasons to be recorded in writing, extend the audit period for subsequent 6 months.Due Date of Audit Report Submission:- Concerned officer shall within 30 days of completion of audit inform the registered person about the findings, his rights and obligations along with reasons.·

Actions:- If the audit result is detection of short paid of tax, not paid of tax or erroneously refunded of tax or wrongly availed or utilized of input tax credit (ITC), further action will be taken as per section 73 or 74 against registered dealer. (3) SPECIAL AUDIT UNDER SECTION 66:-If at any stage of scrutiny, inquiry, investigation or any other proceedings, any officer but not below the rank of Assistant Commissioner, duly approved may avail the services of a Chartered Accountant or Cost Accountant to conduct a detailed examination of specific areas of operations of a registered person in FORM GST ADT-03 by issuing specific directions on the basis of following two grounds:1. Value (Turnover) has not been correctly declared, OR2. Input Tax Credit (ITC) availed is not within the normal limits.

An Assistant Commissioner who wants to conduct special audit of taxable person on the basis of above mentioned two grounds, may obtain prior permission of the · Commissioner to issue such directions in accordance with the provision of Rule 102(1) in Form GST ADT-03.· Identification of expert i.e. Chartered Accountant or Cost Accountant is to be decided by the Commissioner.

The Chartered Accountant or Cost Accountant so appointed shall submit the audit report along with specified particulars, within a period of 90 days directly to the Assistant Commissioner in accordance with the provisions of Rule 102(2) in FORM GST ADT-04.· The registered person shall be given an opportunity of being heard in respect of any material collected on the basis of special audit which is likely to be used in any proceeding against him under this act or rules made thereunder.

Extension of Due Date of Audit:- On the basis of application having material or sufficient reason to Assistant Commissioner by a Chartered Accountant or Cost Accountant or the Registered Person, due date of submission of audit report may be extended for subsequent 90 days.Remunerations:- The expenses for examination and audit including the remuneration payable to the auditor will be determined as well as borne by commissioner.Actions: In case any possible tax liability, detection of tax not paid, short paid of tax or erroneously refunded of tax or wrongly availed or utilized of input tax credit (ITC), actions under section 73 or 74 may be initiated against registered dealer.AUDITING PRACTICES IN RELATION TO GST AUDIT:-During the course of audit, the registered person is required to provide the necessary facility to auditor to verify the books of account and also to furnish the specific information and render assistance for timely completion of the audit. As per the CGST Rules on Assessment and Audit Rules, the auditor shall verify the documents on the basis of which the accounts are maintained and the periodical returns and statements are furnished. While conducting the audit, the auditor will consider and evaluate following significant aspects -

· Verify books & records · Returns & statements· Correctness of turnover, exemptions & deductions· Rate of tax applicable in respect of supply of goods and/or services · The input tax credit claimed/availed/unutilized and refund claimed.

SOME OF THE BEST PRACTICES TO BE ADOPTED FOR GST AUDIT:-

The evaluation of the internal control in relation to GST would indicate the area to be focused at the time of audit. This could be done by verifyingo The Statutory Audit report which has specific disclosure in relation to maintenance of

record, stock and fixed assets of registered dealer.o The internal audit report and Information System Audit report of the registered

dealer.o Internal Control questionnaire designed for GST compliance.o Generalized audit software may be used for the GST audit which would ensure

contemporary practice of risk based audit.o Reconciliation of the Books of Account or Reports from the ERP's to the return is also

useful and effective techniques.o Review of the trial balance for detecting any set off of expenses against expenses.o Review of purchases/expenses to examine and assess possible applicability of

reverse charge to goods/services.o Reconciliation of foreign exchange outgo would also be necessary for identifying the

liability in case of import of services.o Ratio analysis can also provide significant clues as well as information pertaining to

areas of non-compliances of provisions of GST law as well as other applicable law for the time being in force.

IMPORTANAT FORMS

FORM GSTR-9C- Reconciliation Statement FORM ADT-03- Directions to Conduct Special Audit FORM ADT-04- Audit Report of Special Audit

·

An E-way bill is an electronic way bill for movement of goods which can be generated on the GSTN Common Portal.Under GST transporters will need to carry an e-way bill when moving goods from one place to another.A movement of goods of more than ` 50,000/- in value cannot be made by a registered person without an E-way bill.E-way bill will also be allowed to be generated or cancelled through SMS.When an E-way bill is generated a unique E-way bill number (EBN) is allocated and is available to the supplier, recipient and the transporter Types of E-way Bill: As per the CGST Rules, 2017 following are the types of e-way bill forms which have been notified: GST EWB-01: Such e-way bill is required to be generated giving details of goods before the commencement of movement of goods by every registered person causing movement of goods of consignment value exceeding ̀ 50,000/- GST EWB-02: It is a consolidated e-way bill which can be generated by a transporter indicating individual E-way bill numbers of each of multiple consignments which are intended to be transported in a single conveyance. GST EWB-03: Reporting of every inspection of goods in transit made by a proper officer shall be recorded online in this E-way bill within the time limits as specified in the CGST Rules,2017 GST EWB-04: Where a vehicle has been intercepted and detained for a period exceeding 30 minutes, the transporter may upload the said information in this form

Who has to generate E-way Bill? Where Goods are transported by registered person as consignor or consignee in own conveyance, hired conveyance or public conveyance by road, such registered person to generate e-way bill. Where goods are transported by rail, air or vessel e-way bill shall be generated by registered supplier or recipient. Where goods are handed over to transporter and e-way bill has not been generated, registered person shall furnish information relating to transporter on common portal and fill Part A of Form GST EWB-01 and e-way bill shall be generated by transporter. Where movement is caused by an unregistered person in own conveyance, hired conveyance or through transporter, unregistered person or transporter may generate e-way bill.

q What will be the procedure to be followed if transfer of goods takes place from one conveyance to other during transit? Where goods are transferred from one conveyance to other in the course of transit, the consignor, recipient or transporter who has provided information in Part A shall update details of conveyance in Part B of FORM GST EWB-01. However, such conveyance details may not be updated in the e-way bill if such goods are transferred for a distance of up to 50 Kms within state/UT from transporter place of business to place of business of consignee. Further, for updation the consignor, recipient or transporter who has furnished information in Part A may assign the e-way bill number to another registered/enrolled transporter for updating Part B of Form GST EWB-01.

How will the transporter proceed if multiple consignments are to be transported in one conveyance and the e-way bill has been generated earlier?

ARTICLES

Introduction to E-way Bill:

Mr. Bharat Trivedi

After the E-Way Bill has been generated and multiple consignments are intended to be transported in one conveyance the transporter shall: Indicate the serial number of E-Way Bill generated in respect of each such consignment electronically AND Generate a consolidated e-way bill in form GST EWB-02 prior to movement of such goods. What is the validity of such E-way bill or a consolidated e-way bill?Sr.NoDistanceValidity Period (From the Relevant date)1Up to 100 KMS One day in cases other than Over Dimensional Cargo2For every 100 KMS or part thereofOne day in cases other than Over Dimensional Cargo3Up to 20 KMS One day in case of Over Dimensional Cargo4For every 20 KMS or part thereofOne day in case of Over Dimensional Cargo Relevant date means: date on which e-way bill has been generated and period of validity shall be counted from the time at which e-way bill is generated.

Is there any provision for cancellation of E-way bill generated? If an e-way bill has been generated, but goods are not transported OR not transported as per the details furnished in the e-way bill , the e-way bill may be cancelled electronically either directly or through a Facilitation Centre notified by the Commissioner. Such e-way bill should be cancelled within 24 hours of its generation. However, an e-way bill cannot be cancelled if it has been verified in transit.

Whether or not the details of e-way bill be made available to recipient? The details of E-way bill generated shall be made available to REGISTERED supplier/recipient on the common portal, who shall communicate his acceptance or rejection of the consignment covered by the E-way bill. If the registered recipient does not communicate his acceptance or rejection within 72 hours of the details being made available to him or time of delivery of goods, it shall be deemed that he has accepted the said details.

Under what circumstances shall an e-way bill not required to be generated? No E-way bill will be required to be generated: Where the goods transported are specified in the Annexure to Rule 138(14) Where goods are transported by a non-motorized conveyance Where the goods are being transported from the port, airport, air cargo complex and land customs station to an inland container depot or a container freight station for clearance by Customs; In respect of movement of goods within such areas as are notified under rule 138(14)(d) of the Goods and Services Tax Rules of the concerned State. Where the goods, other than de-oiled cake, being transported, are specified in the Schedule appended to Notification 2/2017 Central Tax(Rate) Where the goods being transported are alcoholic liquor for human consumption, petroleum crude, high speed diesel, motor spirit, natural gas or aviation turbine fuel. Where the supply of goods being transported is treated as no supply under Schedule III of the Act Where the goods are being transported— (i) under customs bond from an inland container depot or a container freight station to a customs port, airport, air cargo complex and land customs station, or from one customs station or customs port to another customs station or customs port, or (ii) under customs supervision or under customs seal; Where the goods being transported are transit cargo from or to Nepal or Bhutan Where the goods being transported are exempt from tax under notification No. 7/2017-Central Tax (Rate) Any movement of goods caused by defense formation under Ministry of defense as a consignor or consignee Where the consignor of goods is the Central Government, Government of any State or a local authority for transport of goods by rail Where empty cargo containers are being transported; and Where the goods are being transported up to a distance of twenty kilometers from the place of the business of the consignor to a weighbridge for weighment or from the weighbridge back to the place of the business of the said consignor subject to the condition that the movement of goods is accompanied by a delivery challan issued in accordance with rule 55.

What are the documents and devices to be carried by a person-in-charge of a conveyance? The person in-charge of a conveyance shall carry- The invoice or bill of supply or delivery challan, as the case maybe and A copy of the E-way bill or the E-way bill number, either physically or mapped to a Radio Frequency Identification Device embedded on to the conveyance in such manner as may be notified by the Commissioner. Also a registered person may obtain an Invoice Reference Number(valid for 30 days from date of uploading)from the common portal, by uploading a tax invoice issued by him in FORM GST INV-1 and produce the same for verification by the proper officer instead of a tax invoice.

What are the provisions prescribed for verification of documents and conveyance? The Commissioner or an officer empowered by him may authorize proper officer to intercept any conveyance to verify the E-way bill number in physical form for inter-state and intra-state movement of goods. The Commissioner shall get Radio Frequency Identification Device (RFID) installed at places to verify the movement of vehicles pertaining to a mapped e-way bill. On receipt of specific information about evasion of tax, the physical verification of conveyances can be carried out by any officer after obtaining necessary approval of the Commissioner or an officer authorized by him in this behalf.

What is the utility of form GST EWB-03 and what are the details to filled therein by the Proper Officer? Summary Report of every inspection of goods in transit shall be recorded in Part A of GST EWB-03 within 24 hours by the Proper Officer. Final Report of such inspection shall be recorded within 3 days of such inspection in Part B of GST EWB-03. No Further Verification- Once the physical verification of goods being transported on any conveyance has been done during transit at one place within the State or in any other State then no further physical verification of the said conveyance shall be carried out again in the State. It can be done only if specific information relating to evasion of tax is made available subsequent to the first verification.

Where a vehicle has been stopped and detained, is there any facility for uploading information regarding detention of such vehicle? Detention Beyond 30 Minutes- Where a vehicle has been intercepted and detained for a period exceeding thirty minutes, the transporter may upload the said information in FORM GST EWB-04 on the common portal as provided under Rule 138D of the CGST Rules, 2017.

What are the consequences of non-conformance to the prescribed e-way bill rules? If e-way bills are not issued, wherever required, in accordance with the provisions, the same will be considered as contravention of rules. As per Sec 122 of CGST Act,2017 a taxable person who transports any taxable goods without the cover of specified documents (e-way bill is one of the specified documents) shall be liable to a penalty of 10,000 or tax sought to be evaded, whichever is higher As per Sec 129 of CGST ACT,2017 where any person transports any goods or stores any goods while they are in transit in contravention to the provisions of this Act or rules, all such goods and conveyance used as a means of transport for carrying the said goods and documents relating to such goods and conveyance shall be liable to detention or seizure.

ARTICLES

Mr. Harsh Kesari

INTRODUCTIONThe increasing importance and share of intangible assets in the balance sheet has augmented the need of accurate accounting and disclosure of Intangible Assets in the financial statements. In India, this issue is dealt by the AS-26, “Intangible Assets”, issued by the Institute of Charted Accountant (ICAI), the apex accounting institute of India. This standard was issued in 2002 and came into effect from 1-April-2003 and is mandatory for all enterprises. This standard covers all type of intangible assets except- Intangible assets that are covered by another accounting standards Financial assets. Mineral rights and expenditure on the exploration for, or development and extraction of minerals, oil, natural gas and similar non-regenerative resources. Intangible assets arising in insurance enterprises from contracts with policyholders and Expenditure in respect of termination benefits. This standard is used in combination with standards which deals with those issues which are not covered by AS- 26. For example, this standard does not deal with lease that fall under AS-19, Leases; goodwill arising on an amalgamation (AS-14, Accounting for Amalgamation) and goodwill arising on consolidation (AS-21, Consolidated Financial Statements); deferred tax assets (AS-22, Accounting for Taxes on Income) and lastly intangible assets held by an enterprise for sale in the ordinary course of business (AS-2, Valuation of Inventories and AS-7, Accounting for Construction Contracts). ACCOUNTING STANDARD- 26 This statement addresses the issues of accounting of Intangible assets acquired individually or acquired in a business combination. It also addresses how goodwill and other Intangible assets should be accounted initially and subsequently in the financial statements. The introduction of this standard is an attempt towards recognition and proper valuation of the economic benefits generated by intangible assets. Because of this standard the firms are now able to identify and value their valuable intangible assets, which were used to combine under the heading goodwill. Moreover, it has uniformed the accounting treatment for the intangible assets. The driving force behind this standard is the need of fair valuation of intangible assets as they have taken an important place in the financial statements. RECOGNITION OF INTANGIBLE ASSET An intangible asset can be recognized if it meets the definition and recognition criteria given in the standard. This standard has laid down a proper recognition criteria for intangible assets. According to this standard an intangible asset should be recognized if It is probable that the future economic benefits generated by an intangible asset will flow to the enterprise and The cost of the asset can be measured reliably. Considerable amount of judgment is required by the firm to ascertain the degree of certainty attached with the flow of economic benefits. After understanding when we can recognize an intangible asset, the next step is how to recognize these assets i.e. how to value them. An intangible asset should be measured initially at cost. Standard has divided the recognition part of intangibles into two parts ─ primary recognition and secondary recognition. Under primary recognition intangible assets are valued on the basis on which they have acquired or internally generated. Acquisition can be By way of purchase. By way of amalgamation. By way of government grant. By way of exchange for another asset and By way of exchange for shares. Standard has given different treatment under different types of acquisition which is discussed in the following section.

Intangible Assets

When asked to write about my professional journey andsuccess, I didn't know how to begin. In all honesty,

Idon't know much about success yet, but yes, if you ask me about failures, then I can pen down a novel on

the struggles I've been through.

From failing in Class IXth tobecoming a CA may appear to be a success story from the outside, however,

what lies in between is sheer pain, struggle and fear, teamed with a “won't quit – come what may” attitude.

We all make sacrificesfor success, and I am no different. I gave up a cricketing career and compromised on

my music just to earn this degree. Today I cherish it, as it bringsnot only societal recognition, but empowers

me to take risks, knowing I always have this knowledge to fall back upon.

While preparing for the exams, we feel that passing CA is the “finish line”, and life will follow a set path.

However, today, the demand for CAs is not limited to the standard roles in audit, or consulting – the world is

your oyster! Being a CA helps me in my retail business not only due to the accounting knowledge, but also

in connecting with clients from diverse backgrounds, and bringing in professionalism. Therefore, I would

advise all CA aspirants to think innovatively, and actively seek unconventional opportunities.

I cleared my finals in the Vth attempt, and I thank the trials I faced as every attempt was a learning curve.

Despite the immense demotivation that accompanied eachfailure, I never gave up until I finally passed.

Failures and struggles are necessities to life and how you respond to them speaks volumes of your

character. I hope my story inspires you to keep going and create a path of success that is uniquely your

own!

By CA. Mohit AmarnaniBy CA. Mohit AmarnaniBy CA. Mohit Amarnani

Student ConferenceEvent

Snapshot

Event Snapshotleu 2018

Event Snapshot

BANK AUDIT SEMINAR

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

LUCKNOW BRANCH OF CICASA

ICAI Bhawan, Vikas Khand -1, Gomti Nagar, LucknowE-mail: [email protected]:- 0522-4069931 www.lucknowicai.com