Embed Size (px)

Citation preview

ICICI Bank: strategy &

performance

November 2016

Certain statements in these slides are forward-looking statements.

These statements are based on management's current expectations and

are subject to uncertainty and changes in circumstances. Actual results

may differ materially from those included in these statements due to a

variety of factors. More information about these factors is contained in

ICICI Bank's filings with the US Securities and Exchange Commission.

All financial and other information in these slides, other than financial

and other information for specific subsidiaries where specifically

mentioned, is on an unconsolidated basis for ICICI Bank Limited only

unless specifically stated to be on a consolidated basis for ICICI Bank

Limited and its subsidiaries. Please also refer to the statement of

unconsolidated, consolidated and segmental results required by Indian

regulations that has, along with these slides, been filed with the stock

exchanges in India where ICICI Bank’s equity shares are listed and with

the New York Stock Exchange and the US Securities and Exchange

Commission, and is available on our website www.icicibank.com

2

Operating environment 1

3

ICICI Group: positioning & strengths 2

4

Emerging trends in India

Improving macro-economic conditions and structural

changes

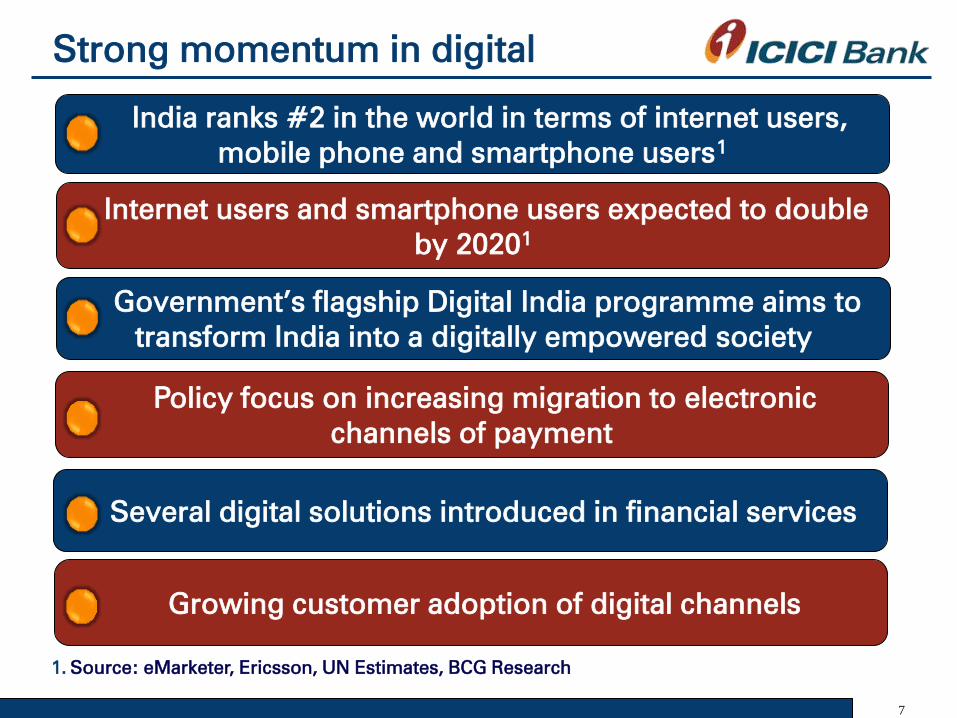

Strong momentum in digital

Scope for increase in penetration of financial services

• Repo rate reduced by 175 basis points since January 2015

• Current account deficit at 0.1% of GDP in Q1-2017

5

Recent trends in the Indian economy

• GDP grew by 7.6% in FY2016 compared to 7.2% in FY2015

• Monsoon deficit of only 3.0% of long period average with

reasonable spatial distribution; crop area under cultivation stable

Continuing improvement in economic conditions

Inflation at 4.3% in September 2016; monetary policy stance

continues to be accommodative

Strong external sector trends: BoP remains in surplus

However, issues remain including weak manufacturing

sector growth, subdued private investments and weak global

environment

6

Significant structural reforms

• Demonetised ₹ 500 and ₹ 1,000 currency notes to curb shadow

economy; expected to support increase in formal financial savings,

low inflation and interest rates, improved fiscal position and impetus

to digital payments

• Liberalised most sectors for foreign investments under the

automatic route

• Progress made on implementation of GST; constitution amendment

for implementation of GST ratified by states, rate structure finalised

by GST Council; plan to implement from FY2018

• Amendments made to debt resolution laws to fast track process;

Insolvency and Bankruptcy Code enacted; 100% FDI in ARCs

allowed

Structural and institutional changes underway

ARCs: Asset Reconstruction Companies

Several digital solutions introduced in financial services

7

Strong momentum in digital

1. Source: eMarketer, Ericsson, UN Estimates, BCG Research

India ranks #2 in the world in terms of internet users,

mobile phone and smartphone users1

Internet users and smartphone users expected to double

by 20201

Government’s flagship Digital India programme aims to

transform India into a digitally empowered society

Policy focus on increasing migration to electronic

channels of payment

Growing customer adoption of digital channels

8

Penetration of financial services

• Net financial savings of household sector increased from 7.2% of

GNDI1 in FY2013 to 7.7% of GNDI

1 in FY2016

Rising financial savings of households

• Life insurance was 2.0% of GNDI1 in FY2016

• Mortality protection gap high at USD 8.5 trillion3

• General insurance penetration at 0.7%2 of GDP in FY2016

Significant under-penetration in insurance

• Equity market turnover4 has almost doubled compared to FY2014

• ~17% y-o-y growth in outstanding corporate bonds and

commercial paper at Sep 30, 2016

Healthy equity and debt capital market flows

1. GNDI: Gross National Disposable Income

2. General insurance premium as % of GDP

3. Swiss Re, Economic Research and Consulting “Mortality Protection Gap Asia-Pacific 2015

4. Daily average; includes cash and derivative turnover

Operating environment 1

9

ICICI Group: performance highlights 2

ICICI Group

Savings

Investments

Capital

flows

Protection

Credit

Spanning the spectrum of financial services

10

11

ICICI Bank: 4 x 4 agenda

Robust funding profile Digital leadership & strong

customer franchise

Continued cost efficiency Focus on capital efficiency

including value unlocking

Monitoring focus Improvement in portfolio

mix

Concentration risk

reduction Resolution of stress cases

En

han

cin

g

fran

ch

ise

Po

rtfo

lio

qu

ality

12

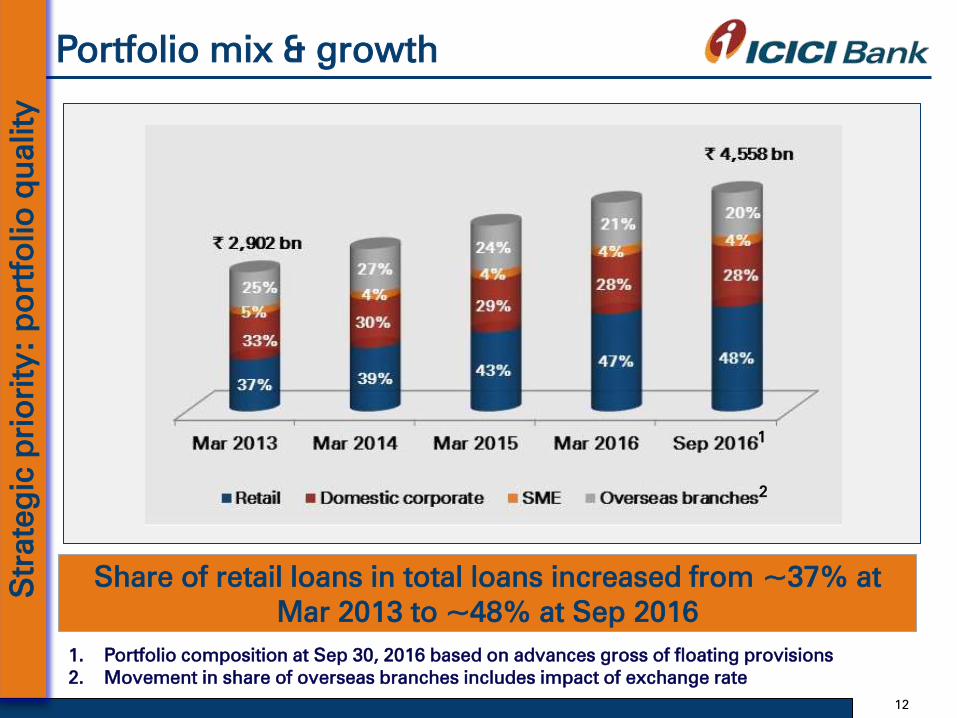

Share of retail loans in total loans increased from ~37% at

Mar 2013 to ~48% at Sep 2016

2

1

1. Portfolio composition at Sep 30, 2016 based on advances gross of floating provisions

2. Movement in share of overseas branches includes impact of exchange rate

Portfolio mix & growth

Strateg

ic p

rio

rit

y: p

ortfo

lio

q

uality

Strong growth across retail products

13

•About one-third of home loan

business originated from

branches in H1-2017

•Auto loans: focus on

profitability

•Commercial vehicles: growth

linked to industry trends

• Focus on granular lending

•Key products include kisan

credit cards, agri term loans,

loans to Self Help Groups and

loans against gold jewelry

Strateg

ic p

rio

rit

y: p

ortfo

lio

q

uality

14

• 65-70% of incremental

disbursements to existing

customers; ~60% sourcing

through internal channels1

•No. of cards-in-force

increased from 2.8 mn in Mar

2013 to 3.9 mn in Sep 2016

•~70% of cards sourced

through internal channels

•Collateral based lending to

small businesses

•Average ticket size of ~` 10

mn

1. Internal channels include branches, online, tele-calling and other direct channels

Strong growth across retail products

Strateg

ic p

rio

rit

y: p

ortfo

lio

q

uality

Corporate business: selective lending

15

CAGR: compounded annual growth rates

•Growth calibrated to trends in the

environment since Mar 2013

• Focus on lending to higher rated

corporates and improving

portfolio mix

•Robust growth in loans other than

non-performing loans,

restructured loans and loans to

companies included in drilldown

exposures, at Sep 30, 2016

Strateg

ic p

rio

rit

y: p

ortfo

lio

q

uality

• Focus on concentration risk

reduction

Monitoring focus

16

Continuous monitoring of delinquency trends in retail

business

• Focus on use of analytics and day-to-day credit monitoring of

wholesale banking and SME customers

• Use of predictive models for stress identification

• Use of internal transaction data and external newsfeeds for

triggers

• Parameters for early warning signals identified

• Credit monitoring dashboard designed and rolled out

Apart from an independent Risk Management Group, Credit

Monitoring Group formed for wholesale & SME business

Strateg

ic p

rio

rit

y: p

ortfo

lio

q

uality

17

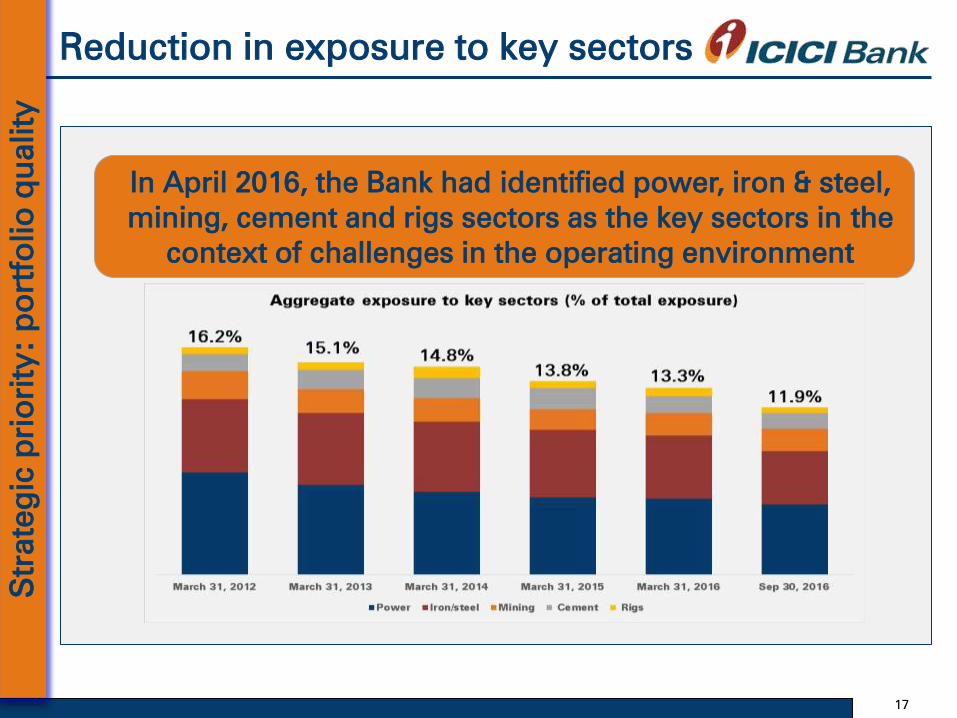

Reduction in exposure to key sectors

In April 2016, the Bank had identified power, iron & steel,

mining, cement and rigs sectors as the key sectors in the

context of challenges in the operating environment

Strateg

ic p

rio

rit

y: p

ortfo

lio

q

uality

18

Drilldown exposures

• Net reduction in exposure and rating upgrades of ₹ 24.61

billion during H1-2017

• Based on the transactions announced by certain

borrowers, significant further reduction expected over

next six to nine months, subject to necessary approvals

and completion of transactions

The Bank had disclosed exposure to ‘below investment

grade’ rated entities in key sectors and promoter entities1

1. Promoter entities where underlying is partly linked to the key sectors

Strateg

ic p

rio

rit

y: p

ortfo

lio

q

uality

Robust funding

19

16.8% y-o-y growth in total deposits at Sep 2016;

proportion of retail deposits at about 76%

• 21.7% y-o-y growth in CASA deposits at Sep 2016

• 18.3% y-o-y growth in period-end CASA deposits at Sep

2016

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Extensive geographical presence

20

Significant investments made in distribution

~52% of branches in semi-

urban and rural areas;

presence across ~2,600

centers

Supplemented by

14,295 ATMs

Branch network

429

318

677

190

23

31

36

210

130

177

34

433

166

59

131

54

80

247

218

5 6

64

10

7

7

2 8

31

239

2

2

262

5

172

0

3

Strateg

ic p

rio

rit

y: en

han

cin

g fran

ch

ise

1,707

4,468

Digital leadership

Digitizing

channels

Digitizing

experience

Digitizing

core

21

Focus on analytics across areas to improve productivity &

efficiency

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Best-in-class mobile application

22

Highest overall score in 2016 India Mobile Banking

Functionality Benchmark study conducted by Forrester

More than 150 services

Industry first features:

Favourites for faster transactions

Chat services & authenticated

call

Rail ticket booking

Touch ID Login & Watch Banking

Instant Tax Payment

SmartKeys: transfer of funds

without switching between

applications

iMobile

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Comprehensive digital wallet: Pockets

23

Over 5.3 million downloads; significant interest from non-ICICI

Bank users

• India’s first digital bank

• Innovation in payments, banking and

shopping

• Sending money through SMS, Email,

WhatsApp, Google+

• Non banking features such as movie tickets,

split bills, gift vouchers

•Amongst the top 4 wallet apps in terms of

time spent on the app1

•Only bank app to figure in the top wallet apps

1. As per Nielsen Whitepaper on Wallets

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Growing payments franchise

Number

of cards

Card spends

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Payment solutions

25

Launched ‘Unified Payments Interface’ (UPI) for its mobile

banking applications

• Offers UPI in ‘Pockets’ and ‘iMobile’

• Enables both P2P (Person to Person)

and P2M (Person to Merchant)

transactions

• Transactions are done using a Virtual

Payment Address (VPA) where bank

account details not required

The Bank worked closely with National Payments Corporation of

India (NPCI) for the launch of the UPI

Over 200,000 Virtual Payment Addresses (VPA) created

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Digitising sales

• KYC through scanned documents

• Demo videos for products and services

• Upsell of mutual funds & insurance

• Being introduced for loan products

26

About 80% of new savings accounts sourced through tab

banking

With digitisation, an account can be opened within a day as

against about four days earlier

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Software robotic systems

• Over 200 software robotic systems

perform over 1.0 million banking

transactions every working day

• Reduced response time for customers

by up to 60%; improved productivity

• Leveraging advancements in artificial

intelligence such as facial and voice

recognition, natural language

processing, machine learning and bots

27

First bank in the country and among few, globally, to roll-out

‘Software robotic systems’

Plan to more than double the software robotic systems to

over 500 business processes by end of FY2017

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

28

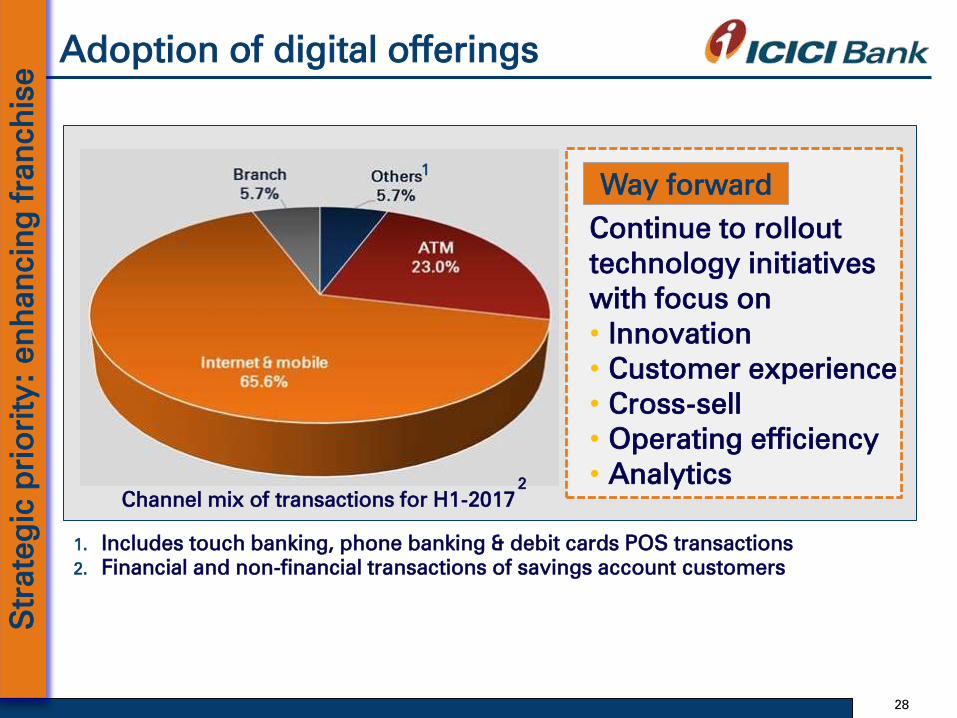

Adoption of digital offerings

1. Includes touch banking, phone banking & debit cards POS transactions

2. Financial and non-financial transactions of savings account customers

Continue to rollout

technology initiatives

with focus on

• Innovation

• Customer experience

• Cross-sell

• Operating efficiency

• Analytics

Way forward

1

Strateg

ic p

rio

rit

y: e

nh

an

cin

g fran

ch

ise

Channel mix of transactions for H1-2017

2

29

Focus on cost efficiency, while investments in franchise

being made

Excluding gains on sale in

shareholding in insurance

subsidiaries; cost-to-income

ratio at 38% and 41% in

FY2016 and H1-2017

respectively

Cost efficiency

Strateg

ic p

rio

rit

y: en

han

cin

g fran

ch

ise

30

Significant value in subsidiaries

Completed initial public offer of ICICI Prudential Life

Insurance Company Limited in Q2-2017

The Bank sold 12.63% stake in the IPO and realised gains

of ₹ 56.82 billion in Q2-2017; shareholding of 54.9% after

the sale

The Bank sold 6.0% stake in ICICI Life and 9.0% stake in

ICICI General in FY2016; aggregate gains of ` 33.74 billion

H1-2017

FY2016

Strateg

ic p

rio

rit

y: en

han

cin

g fran

ch

ise

Capital efficiency

31

1. As per RBI guidelines on Basel III norms

•Capital ratios significantly higher than regulatory requirements

•Tier-1 capital composed almost entirely of core equity capital

•Substantial scope to raise Additional Tier-1 and Tier-2 capital

8.4% y-o-y growth in risk weighted assets compared to 14.4%

y-o-y growth in total assets at September 30, 2016

Strateg

ic p

rio

rit

y: en

han

cin

g fran

ch

ise

Investment in overseas banking subsidiaries decreased from

11.0% of net worth at Mar 2010 to 4.4% of net worth at Sep

2016

Trends in operating revenues

32

Net interest margins

33

Margins impacted by non-accrual of interest on NPAs and

implementation of resolution for stressed borrowers

Fee income

34

Fee income growth has been subdued since fiscal 2014

given the focus on re-orienting corporate lending and weak

corporate activity

Growth in retail fees has

been higher:

• Focus on cross-sell of

third party products to

existing customers

• Leadership in

distribution of

insurance

• Large mutual fund

distribution

Asset quality & exposures

35

36

NPA & restructuring trends

Asset quality trends impacted by challenges in the

corporate segment; retail asset quality healthy and stable

About 79% of the gross additions to NPAs for the

wholesale & and SME businesses in H1-2017 were on

account of slippages relating to companies internally

rated below investment grade in key sectors,

restructured portfolio and accounts classified as non-

performing in earlier periods

Additions to NPA

Movement of NPA

38

38

Drilldown exposures: movement

1. Aggregate fund based limits and non-fund based outstanding

2. Excludes net exposure of ₹ 5.82 bn to central public sector owned undertaking

3. Includes promoter entities where underlying is partly linked to the key sectors

4. Includes non-fund based outstanding in respect of accounts included in the

drilldown exposure where the fund based outstanding has been classified as

non-performing

5. In addition to the above, the non-fund based outstanding to borrowers classified

as non-performing was ₹ 32.86 bn at Sep 30, 2016

Aggregate exposure1,2,3,4

Q2-2017 H1-2017

Opening balance 387.23 440.65

Net reduction in exposure (16.77) (20.36)

Net rating upgrade to ‘investment

grade’ - (4.25)

Classified as non-performing (45.55) (91.14)

Closing balance 324.90 324.90

₹ billion

Sector-wise details

39

Strengthening Balance Sheet

Asset quality and provisioning

Strengthened balance sheet with additional provisioning

Additional provisions in Q2-2017 (` billion) 35.88

Additional provisions for standard loans

Entire loss on sale of NPAs in H1-2017 recognised

upfront (permitted to be amortised as per RBI

guidelines)

16.78

3.95

1

2

3 Floating provisions 15.15

Provisioning coverage ratio on non-performing loans at

59.6% including cumulative technical/ prudential write-offs

and floating provisions

Collective contingency and related reserve of ` 20.55 billion

at Sep 30, 2016

Performance of subsidiaries

40

41

Life insurance

• Sustained leadership in private sector

with an overall market share of 12.4%1

H1-2017

•New business profit margin2

increased from 8.0% in FY2016 to

9.4% in H1-2017

Strong growth

& improvement

in market share

1. Based on retail weighted received premium

2. Based on actual cost

• PAT of ` 16.53 billion in FY2016; ₹ 8.24

billion in H1-2017; ROE of ~28% in H1-

2017

Sustained &

strong

profitability

• AUM at ~` 1,128 billion at September

30, 2016 Growth in AUM

Indian Embedded Value increased from ₹ 139.39 billion at

March 31, 2016 to ₹ 148.38 billion at September 30, 2016

42

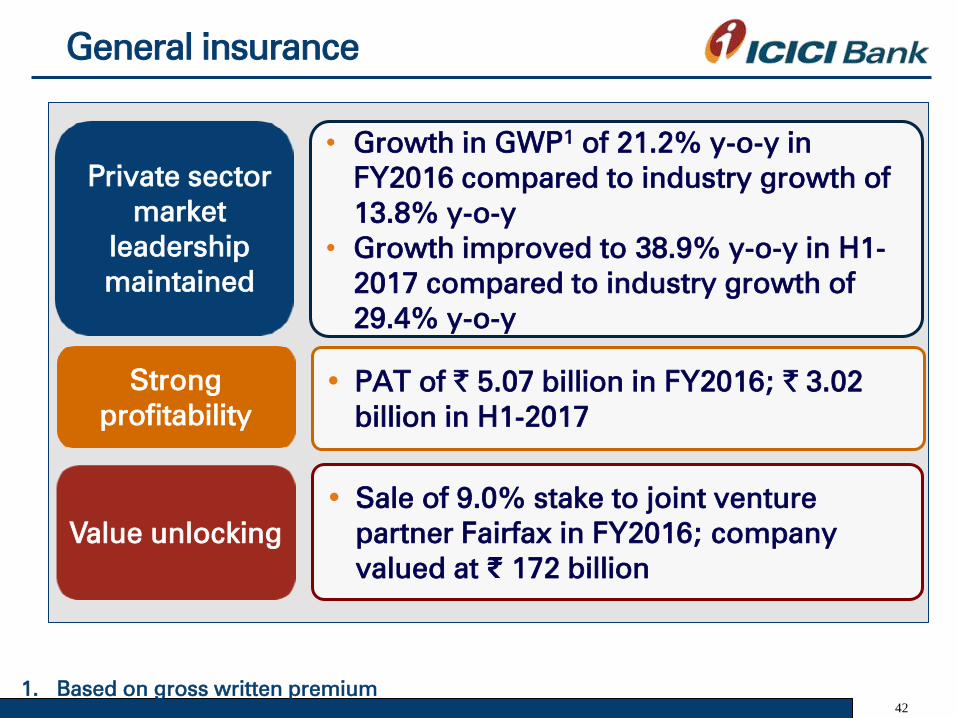

General insurance

• Growth in GWP1 of 21.2% y-o-y in

FY2016 compared to industry growth of

13.8% y-o-y

• Growth improved to 38.9% y-o-y in H1-

2017 compared to industry growth of

29.4% y-o-y

Private sector

market

leadership

maintained

• PAT of ` 5.07 billion in FY2016; ` 3.02

billion in H1-2017

Strong

profitability

• Sale of 9.0% stake to joint venture

partner Fairfax in FY2016; company

valued at ₹ 172 billion

Value unlocking

1. Based on gross written premium

43

Other businesses

• Largest AMC in India based on average

AUM in Q2-2017

• PAT of ` 3.26 billion in FY2016; ` 2.28

billion in H1-2017 (39.0% y-o-y increase)

Asset

management

• Strong platforms for leveraging

favourable markets

• ICICI Securities PD: amongst the leaders

in Indian fixed income & money markets;

PAT of ` 1.95 billion in FY2016; ` 2.47

billion in H1-2017

• ICICI Securities: ~3.9 million customers;

PAT of ` 2.39 billion in FY2016; ` 1.68

billion in H1-2017

Securities &

primary

dealership

44

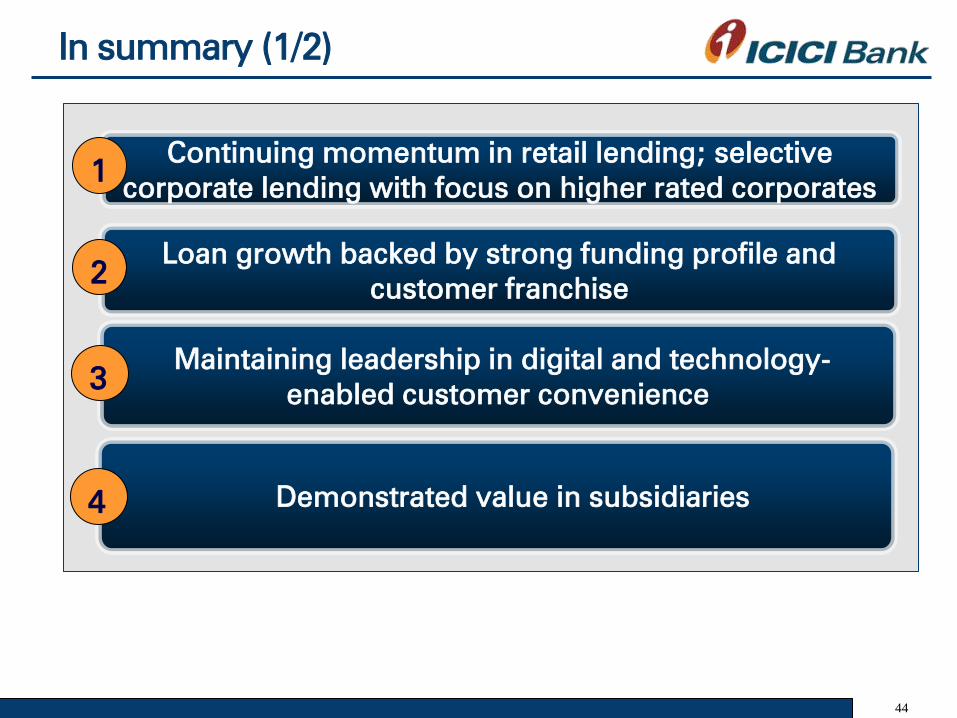

In summary (1/2)

Continuing momentum in retail lending; selective

corporate lending with focus on higher rated corporates 1

Loan growth backed by strong funding profile and

customer franchise 2

Maintaining leadership in digital and technology-

enabled customer convenience 3

Demonstrated value in subsidiaries 4

45

In summary (2/2)

1. Including profits for H1-2017

Strong capital base with Tier-1 capital adequacy of

13.26%1

Encouraging progress on resolution of key sector

exposures 6

Further strengthened balance sheet with additional

provisions

8

Decreasing trend in exposure to key sectors 5

7

Thank you

46

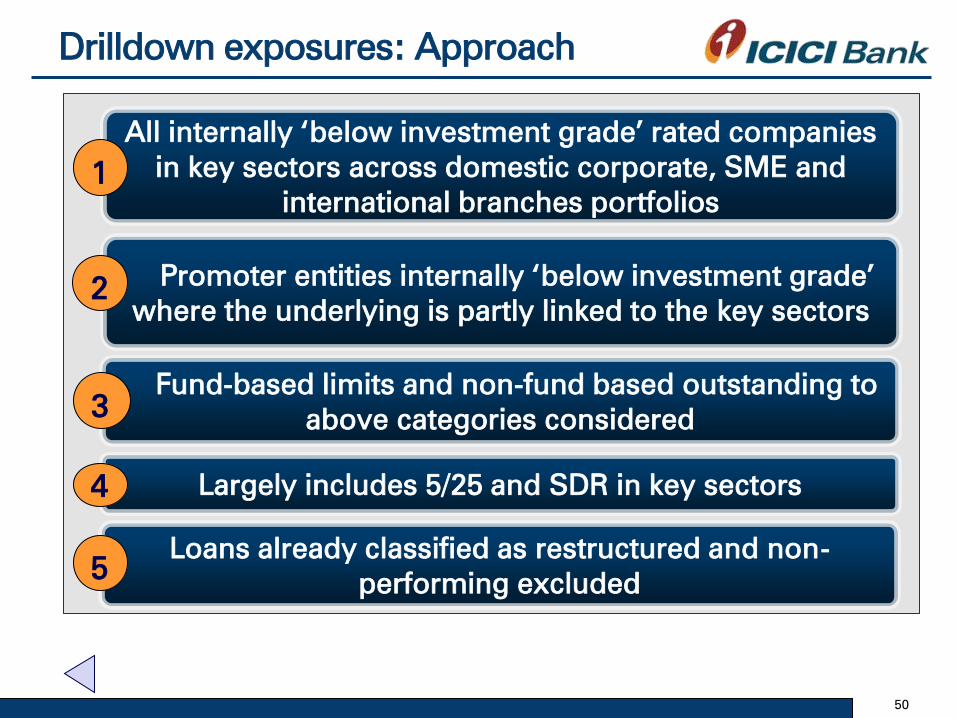

All internally ‘below investment grade’ rated companies

in key sectors across domestic corporate, SME and

international branches portfolios

Promoter entities internally ‘below investment grade’

where the underlying is partly linked to the key sectors

Largely includes 5/25 and SDR in key sectors

Fund-based limits and non-fund based outstanding to

above categories considered

1

2

3

4

Loans already classified as restructured and non-

performing excluded 5

Drilldown exposures: Approach

50

Movement of NPA

1. The Bank sold net NPAs amounting to ` 22.32 billion and ₹ 8.82 billion to ARCs in

Q1-2017 and Q2-2017 respectively. In Q2-2017, the Bank has recognised entire loss

on sale of NPAs in H1-2017, which is permitted to be amortised as per RBI

guidelines

2. Based on customer assets

` billion FY2016 Q2-2016 Q1-2017 Q2-2017

Opening gross NPA

152.42 152.86 267.21 275.63

Add: gross additions

171.13 22.42 82.49 80.29

- of which:

slippages from

restructured assets 53.00 9.31 13.21 12.31

- of which: Slippages from

exposure to ‘below investment

grade’ companies in key sectors

reported - - 45.59 45.55

Less: recoveries & upgrades 21.84 7.09 7.92 8.00

Net additions 149.29 15.33 74.57 72.29

Less: write-offs & sale1

34.50 8.13 66.15 22.44

Closing gross NPAs 267.21 160.06 275.63 325.48

Gross NPA ratio2

5.21% 3.36% 5.28% 6.12%

48

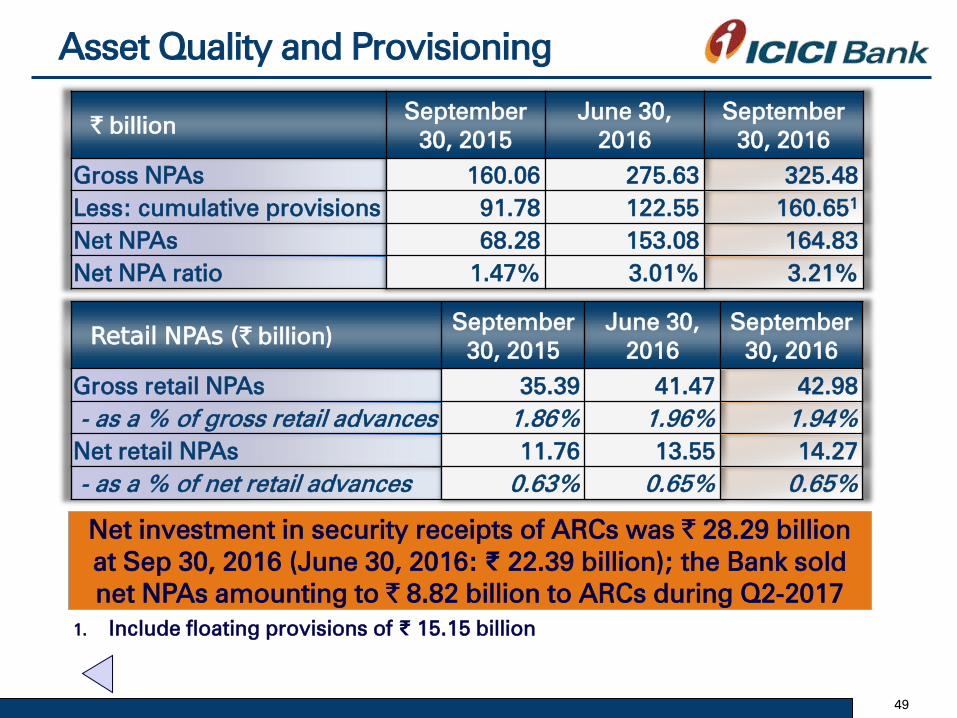

Asset Quality and Provisioning

` billion September

30, 2015

June 30,

2016

September

30, 2016

Gross NPAs

160.06 275.63 325.48

Less: cumulative provisions

91.78 122.55 160.651

Net NPAs 68.28 153.08 164.83

Net NPA ratio

1.47% 3.01% 3.21%

Retail NPAs (` billion) September

30, 2015

June 30,

2016

September

30, 2016

Gross retail NPAs

35.39 41.47 42.98

- as a % of gross retail advances

1.86% 1.96% 1.94%

Net retail NPAs 11.76 13.55 14.27

- as a % of net retail advances

0.63% 0.65% 0.65%

Net investment in security receipts of ARCs was ` 28.29 billion

at Sep 30, 2016 (June 30, 2016: ₹ 22.39 billion); the Bank sold

net NPAs amounting to ` 8.82 billion to ARCs during Q2-2017

1. Include floating provisions of ₹ 15.15 billion

49

Drilldown exposures: Sector-wise details

At March 31, 2016 At September 30, 2016

` billion Exposure1,2,3

% of total

exposure Exposure

1,2,3 % of total

exposure

Power 119.60 1.3% 90.03 0.9%

Mining 90.11 1.0% 75.84 0.8%

Iron/steel 77.76 0.8% 47.13 0.5%

Cement 66.43 0.7% 56.17 0.6%

Rigs 25.13 0.3% 0.44 -

Promoter entities3

61.62 0.7% 55.29 0.6%

1. Aggregate fund based limits and non-fund based outstanding

2. Excludes net exposure of ₹ 5.82 bn to central public sector owned undertaking

3. Includes promoter entities where underlying is partly linked to the key sectors

4. Includes non-fund based outstanding in respect of accounts included in the

drilldown exposure where the fund based outstanding has been classified as

non-performing

5. In addition to the above, the non-fund based outstanding to borrowers classified

as non-performing was ₹ 32.86 bn at Sep 30, 2016

51