Embed Size (px)

Citation preview

Shilpa KumarMD & CEO

ICICI Securities Ltd.

The beauty of our tax system is such that not only does it help you make investments that save tax but also align those investments to help meet your life goals. Just like planning for our financial goals is a continuous process, so is the process of planning investments to save tax. However, many of us overlook the fact that our tax obligations change broadly with our age and changing financial circumstances.

I t is crucial that we invest according to our life stage and are aware of the options available which best suit that life stage. For example taxable income is relatively lower at the start of one career and tends to increase as our career progresses. This stage is also the beginning of establishing an asset base, there is little income from capital gains or interest and fewer deductions.

But most importantly investors here have the advantage of having time on their side. Equity oriented investments make perfect sense at this stage, more importantly products like equity linked savings scheme (ELSS). The three year lock in also ensures discipline and investing for the long term. Additional it also has benefit of tax exemption under section 80C.

As you grow, your income and responsibilities also tend to increase. At this stage usually these is a family and some serious goal planning begins. Tax, at this stage, can be managed while achieving financial goals like buying a house, investing in insurance to safeguard the future of your dependents and also starting to invest to build a kitty for retirement. Tax breaks on home loan repayment combined with

1ICICIdirect Money Manager December 2017

tax concessions on life insurance premiums and contribution to pension schemes like Provident Fund (PF) and National Pension System (NPS) and help increase income and achieve life goals.

Additionally, buying health insurance not only helps in times of a medical emergency but also helps save tax under Section 80D. Taxes on tuition fees of children and education loan are also subject to deduction up to certain limit.

This life stage, also usually signals the peak in expenses and liabilities. Therefore, making optimum use of tax-saving instruments under all permissible sections is a must for assessing tax saving investments. However, it is equally important to factor in your risk appetite and time horizon to achieve the goal before investing in tax-efficient plans.

Moving on, tax-saving portfolio of those moving towards retirement should be focused on the goal of capital protection. Also, in this phase, with debt obligations reduced and the tax bracket being at the highest slab, it is prudent to focus more on tax saving options. While Senior citizen saving schemes (SCSS) is a great tax-saving investment for senior citizens, other opportunities can be discovered depending upon risk profile and life expectancy of the assesse. Individuals can also consider tax saving through non-investment related instruments like charity and donations.

However, tax commitments, financial circumstances, life-stage goals, risk appetite and liquidity requirement of every individual are distinct, no standard tax-planning strategy can be applied to all. Taking professional help to manage taxes is thus highly recommended. The bottom line is to consider taxation before making or revising financial plan at every life stage.

Our message remains the same - 'Keep investing and stay invested for your life goals'. Through this magazine and our website www.icicidirect.com we want to make an earnest attempt to help investors know more on investing, make them aware of the options they have and to partner with them in setting and achieving their financial goals. We welcome you to write to us or visit our branches to assist you.

2

Our efforts to invest in tax-saving instruments are at the peak around this time of the year. While this is an ad hoc approach towards tax-planning, treating tax-related investments as other goal-based investments is in fact, a potent financial strategy. All elements considered before making an investment like time horizon, risk-return equation and asset allocation should also be accounted while investing in a tax-saving avenue.

In other words, tax planning should fit into your overall financial goals. For instance, including equity linked tax-saving products like ELSS (equity-linked savings scheme) and NPS (national pension system) in your portfolio can accomplish two goals: tax deduction up to Rs. 2 lakhandaccumulate retirementcorpus. Similarly, investment in tax-saving FDs can be utilized to achieve short-term goals.Insurance, the most popular tax-saving player amongst Indians, should be primarily purchased for the risk coverage. Tax benefit should be an incidental benefit.I suggest, consider investing in ULIP (unit linked insurance plan), to earn a combination of life coverand capital appreciation.

The nature of your tax-efficient portfolioprimarily depends on your risk profile, income, tax-bracket and age. But the most suitable tax-saving plan is the one that is aligned with your life-stage goals and helps you achieve it on time.

There are a host of products that are tax-efficient and would fit into your investment plan. The December edition of Money Manager offers comprehensive information and analysis on these products and the relevant tax-friendly tips for different age groups. We hope this will help you plan your taxes more efficiently and in sync with your financial goals.

The edition also contains a panel interview with mutual fund experts - P. V. K. Mohan (Principal Pnb AMC), Anand Radhakrishnan, Chief Investment Officer (Franklin- Equity India, Franklin Templeton Asset Management), Deepak Gupta, (Kotak Asset Management) and Lalit Nambiar (UTI Mutual Fund), where they share their views on current market scenario.

This edition offers comprehensive information and analysis on equity diversified funds. If you wish to get clarity on different aspects of personal finance or any other money matter through 'Ask our Planner', you may write to us at [email protected]. So read on, stay updated and involved. Do write in with your feedback and share your thoughts.

Your magazine is now also available on www.magzter.com, a digital newsstand.

ICICIdirect Money Manager December 2017

Editor & Publisher : Abhishake Mathur, CFA

Editorial Board : Sameer Chavan, CWM®, Pankaj Pandey

CMEditorial Team : Nithyakumar VP CFP , Sachin Jain, Research Team

Coordinating Editor : Namrata Lonkar

3ICICIdirect Money Manager December 2017

MD Desk ...................................................................................................1

Editorial ....................................................................................................2

Contents ...................................................................................................3

News ........................................................................................................4

Stock ideas: MM Forgings & Narayana Hrudayalaya......................................5

Flavour of the Month: Manage taxes at every life stageWe often don't realize that changes in inflow and outflow of our income significantly impacts our tax liabilities, which makes tax planning a dynamic process. There's a tax-saving strategy suitable for every individual, it's just a matter of assessing your current financial health and adopting a product that benefits the most at current life stage. Check out these key takeaways ….........................14

Tête-à-tête:Fund managers discuss current economic scenarioIn talk with P. V. K. Mohan (Principal Pnb AMC), Anand Radhakrishnan, Chief Investment Officer (Franklin- Equity India, Franklin Templeton Asset Management), Deepak Gupta, (Kotak Asset Management) and LalitNambiar (UTI Mutual Fund) ...........................................................25

Ask Our PlannerOur financial expert answers How tax deduction under government-backed schemes works? And your other personal finance queries...33

Mutual Fund Analysis Which are the top performing mutual funds in current market scenario? Check these top three funds recommended by our research team........................................................................................37

This month on iCommunityTake a look at the latest activities on our unique information platform- iCommunity (for December 2017)........................................................47

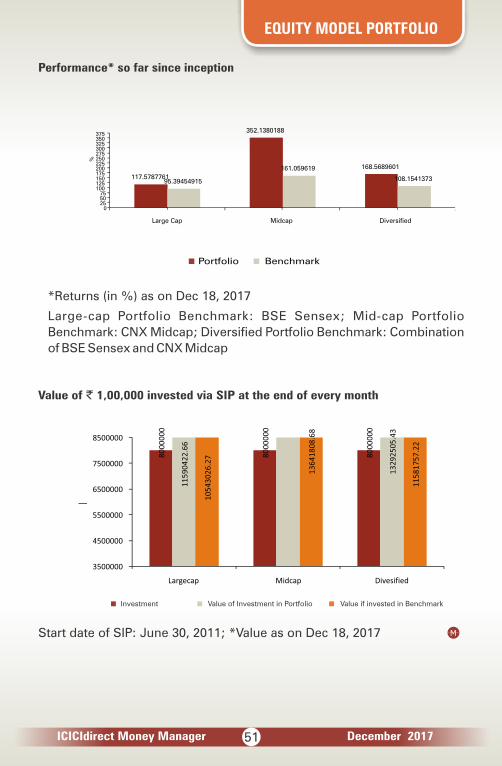

Equity Model Portfolio ..............................................................................48

Quiz Time ................................................................................................52

Prime Numbers ........................................................................................53

4

Hike Messenger has doubled its wallet transactions to 10 million within a month, and will launch features like cab bookings, movie ticketing, food ordering, bill payments and other in-app offerings in the first quarter of 2018, to stimulate usage of the wallet among users.

The app's founder Kavin Mittal told ET that he was open for more funding, but was slowly using funds from Chinese major Tencent which invested $175 million in August 2016. A quarter of the company's 100 million ..

Mittal feels this move would resonate with smartphone users across all tiers and specially those who have mid-level or entry level phones that offer limited storage, and therefore are not able to download many apps.

Courtesy: Economic Times

Hike wallet transactions touch 10 million

2018-19 budget may focus on rural areas

India's government will likely increase funding for the farm and rural sectors in the budget for the coming fiscal year, finance ministry officials said, to shore up political support in the countryside ahead of a raft of elections.

“The next budget will focus on farmers, rural jobs and infrastructure while making all attempts to follow a fiscal prudence path,” a senior finance ministry official told Reuters.

Annual farm growth dipped to 1.7% in the three months ending September, mainly on lower prices and output, while economic growth accelerated to 6.3% after growing at a three-year low of 5.7% in the previous quarter.

Courtesy: The Hindu

ICICIdirect Money Manager December 2017

The liquidity rush in the financial system since demonetisation has led to "unprecedented

fund flows to both equity and debt mutual funds", which is showing some signs of risk,

according to the Reserve Bank of India's (RBI's) Financial Stability Report

Given the significant increase in the mutual funds (MFs) corpus and an excess monthly

return of almost 250 basis points (annualised) from a representative money market fund,

"there seems to be some risk migration from the banks to the mutual funds", the FSR said.

Courtesy: Business Standard

Risk building up in mutual fund segment: RBI's Financial Stability Report

Hero MotoCorp to hike motorcycle prices from January

Two-wheeler market leader Hero MotoCorp said it will increase prices of its motorcycles across models by about Rs 400 per model on an average from January to partially offset rising input costs.

“The price hike translates to about Rs 400 per model. The exact quantum of the increase will vary, basis the model and the specific market,” Hero MotoCorp said in a statement.

Automobile firms usually announce price hikes in December as they try to woo customers, who usually postpone purchases to acquire vehicles in the new year.

Courtesy: Indian Express

5

STOCK IDEAS

ICICIdirect Money Manager December 2017

MM Forgings– Forging its way ahead…

Company BackgroundMM Forgings (MMF) started its operations in 1974 and is a south-based closed die forging player catering the forging requirement of OEMs. The company manufactures raw, semi-machined and machined forging products (like spindles, knuckles, axle beam, gears, hub, yoke and other t ransmiss ion parts) wi th weight ranging from 0.3- 45/kg. In FY17, its total capacity was at 53,000 MT. In terms of revenue mix, the automotive segment account for 86% of revenue (of which CV & PV account for 60% & 26%, respectively) while the non-automotive segment (off highway, oil & gas and valve) accounts for 14% of revenue. Further, the export, domestic revenue mix is at 63: 37, respectively, for FY17. Its top five customers account for ~65% of its revenue.

Investment Rationale

Cyclical revival to drive revenue growthMMF is expected to post revenue CAGR of 13% in FY17-

20E to | 693 crore, attributable to an upswing in demand of heavy commercial vehicles in both domestic & international market. The North America class 8 truck (~18% of MMF revenue) net order is firmly in the growth territory, up 55.7% YoY a t 220 ,916 un i t s in 10MCY17, a lead indicator of p roduc t ion g rowth . The f a v o u r a b l e l a b o u r c o s t arbitrage will accentuate the demand for imported forged components from India, which will benefit MMF. There are multiple catalysts for domestic M&HCV g rowth , v i z . - 1 ) buoyant outlook on road project awarding/construction & m i n i n g , 2 ) s t r i c t implementation of overloading ban, 3) potential regulatory positives like scrappage policy and 4) CV cycle yet to peak. R a p i d u r b a n i s a t i o n , a favourable macro backdrop & new launches will drive the domestic PV growth, aiding MMF's PV business.

Higher utilisation & value addition to drive margin: MMF manufactures raw, semi-machined & machined forging

6ICICIdirect Money Manager December 2017

STOCK IDEAS

products with weight ranging from 0.3- 45/kg. Over the last 26 years, the company has added capacity 9x, from 15000 T in FY95 to 53000 T in FY17. Every capacity expansion was accompanied by an increase in r e a l i s a t i o n ( A S P s h a v e i n c r e a s e d ~ 1 0 % o n a n average), which gives an insight into MMF's focus on value addition & diversification of products. The company has a forging press in the range of 1600 T to 4000 T. Introduction of 8000 T press in Q4FY18E will take its total capacity to 65000 T. This new press will have the capability to manufacture products weighing 60-100/kg, thereby enhancing MMF's value offering in terms of products & segments. The new press line will produce higher margin machined products, thereby increasing the overall share of machined products (currently at ~25% of sales) in the product mix. MMF's effort in making a transition from hammer to press forging can lead to increase in productivity & profitability by 20% & 10%, respect ive ly. We expect EBITDA margins to improve 151 bps to 20.9% in FY20E.

S t a b l e b u s i n e s s , a l l u r i n g valuations: MMF has a track record of stable financials. In the last 10 years, its revenue, EBITDA & PAT have registered CAGR of 10%, 9%, 12%, respectively. With the major capex cycle behind them, MMF is expected to be in a sweet spot in terms of net cash position & FCF yield of ~ 9 % b y F Y 2 0 E . Commissioning of the 8000 T press will propel MMF in a strong growth trajectory with its revenue & profit expected to register CAGR of 13% & 26%, respectively, in FY17-20E. Increasing asset utilisation & margin accretion will lead to increase in RoCE from 12.6% in FY17 to 20.3% in FY20E. On the valuation front, MMF is trading at ~40% discount to the market leader despite having almost a comparable return ratio profile. Hence, we believe there is scope of re-rating in the stock. We value MMF at 19x PE of its FY20E EPS of | 71.6, resulting in a fair of | 1360, with BUY rating on the stock.

7ICICIdirect Money Manager December 2017

STOCK IDEAS

Stock Data

Key Financials

Valuations Summary

` crore FY16 FY17 FY18E FY19E FY20E

Net Sales 502 478 535 609 693

EBITDA 108 93 107 125 145

EBITDA (%) 21.5 19.4 20.0 20.5 20.9

Net Profit 50 43 51 67 86

EPS 41.5 36.0 42.1 55.7 71.6

FY16 FY17 FY18E FY19E FY20E

P/E 24.6 28.4 24.2 18.3 14.3

Target P/E 32.8 37.8 32.3 24.4 19.0

EV / EBITDA 12.0 13.8 12.1 9.8 7.9

P/BV 4.4 3.9 3.4 3.0 2.5

RoNW 17.9 13.8 14.2 16.2 17.6

RoCE 16.0 12.6 13.7 16.4 20.3

Market Capitalization ` 1231.2 Crore

Total Debt (FY17) 182.8

Cash and Investments (FY17) 133.8

EV (FY17) 1280.2

52 week H/L (`) 1063 / 411

Equity capital ` 12.1 Crore

Face value ` 10

FII Holding (%) 0.7

DII Holding (%) 19.2

8ICICIdirect Money Manager December 2017

STOCK IDEAS

Key risks include:

Unable to develop products based

on changing technology – The Evolution of electric

vehicles (EVs) is picking up

pace across the globe. Higher

penetration of EVs worldwide

can pose a risk to forging

companies that predominantly

manufacture engine based

forged products. At present,

the management believes

~10% of its business can be

exposed to the risk of EVs. We

believe if MMF is unable to

develop products based on

changing technology (EVs) it

may impact i ts business

model, going forward.

Under-utilization of its new 8,000

MT capacity – The company is currently in a

pilot phase of its new 8,000 MT

press, which is expected to be

operational in Q4FY18E. The

higher tonnage press has the

capability to produce higher

weight and fully machined

components, which are margin

& RoCE accretive. The market

for machined products is hard

to break into. Vendors need to

establish a long track record.

Hence, a slower ramp up of the

new press entails a downside

risk to our margin and return

ratio assumptions. Historically,

every capacity expansion in

MMF has led to a significant

rise in realizations

9ICICIdirect Money Manager December 2017

STOCK IDEAS

ANALYST CERTIFICATION We /I, Nishit Zota (MBA), and Vidrum Mehta (MBA), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:ICICI Securities Limited (ICICI Securities) is full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India's largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Nishit Zota (MBA), and Vidrum Mehta (MBA), Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed that Nishit Zota (MBA), and Vidrum Mehta (MBA), Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

10ICICIdirect Money Manager December 2017

STOCK IDEAS

Narayana Hrudayalaya Ltd. – Asset right + Affordable + flexible

Company BackgroundIncorporated by renown cardiac surgeon Dr. Devi P r a s a d S h e t t y i n 2 0 0 0 , Narayana Hrudayalaya Ltd (NH) operates as a chain of mul t ispecia l ty hospi ta ls . Started predominantly in Karnataka and Eastern India, the company is growing footsteps in western and northern India as well. We in i t ia te coverage on the company as we believe NH is well poised to thrive in the domestic healthcare delivery (Hospitals) space on the back of its asset right business model with focus on quality and affordability

Investment Rationale

Blended model of affordable + high-quality servicesNH has a legacy model based on affordability over the years. Because of strict control over costs and capital the company w a s m a k i n g r e a s o n a b l e profits. However, as it looks for scaling up in other regions, where the consideration for quality has more weight than

affordability, the model is likely t o b e m o d i f i e d f r o m ' 'a f fordable ' ' to a mix of a f f o r d a b l e + q u a l i t y a t premium. Cases in point are the recent acquisit ion of Gurugram hospital and buying out of partner in the Cayman Islands hospital internationally where the acquisition costs were optically higher.

''Asset right model'' and likely ARPOB improvement to improve return ratiosUnder this model the company engages with partners who invest in land and building while it takes care of medical equipments and hospital management on a revenue share basis. This is why NH's balance sheet is one of the l i g h t e s t a m o n g p e e r s . However, the management has maintained flexible approach in this regard, thus it also owns some hospitals where the opportunity is right. Due to this focus on balance sheet and likely improvement in Average realisation per operating bed (ARPOB) by optimising case

11ICICIdirect Money Manager December 2017

STOCK IDEAS

mix, we expect improvement in ROCE from 12.5% to 19% during FY17-20E.

After effective cost and capital management focus shifts to improving ARPOBIn a conducive but challenging space of Indian healthcare delivery, plagued by longer g e s t a t i o n p e r i o d s , l o w operating margins, leveraged balance sheets and low return ratios, we believe NH is the best placed candidate among peers to sail through. Its legacy model is based on affordability and hence conscious efforts towards cost and capital control is embedded in the

management 's long term strategy. This becomes even more pertinent in the backdrop of incremental government intervention via schemes and control over procedures and products. On the other hand it is also determined to improve the ARPOB by improving case mix, occupancies thus fine tuning af fordabi l i ty wi th profitability. We value NH on SOTP basis by valuing the matured hospitals at 14x FY20E EV/EBITDA, Cayman Islands hospital at 14x FY20 EV/EBITDA, other hospitals and other businesses at 1.0x FY20E EV/sales. Our SOTP target price arrives at | 365

Valuations Summary FY17 FY18E FY19E FY20E

P/E 69.0 65.5 42.8 28.6

Target P/E 82.3 78.1 51.0 34.2

EV / EBITDA 26.1 24.0 19.3 14.2

P/BV 6.0 5.5 4.9 4.2

RoNW 8.8 8.5 11.5 14.6

RoCE 12.5 11.9 14.4 18.7

Key Financials

` Crore FY17 FY18E FY19E FY20E

Net Sales 1878.2 2269.7 2665.0 3021.5

EBITDA 228.9 254.3 311.4 409.7

EBITDA (%) 12.2 11.2 11.7 13.6

Net Profit 84.4 89.0 136.2 203.4

EPS (`) 4.1 4.4 6.7 10.0

12ICICIdirect Money Manager December 2017

STOCK IDEAS

Stock Data

Market Capitalization (` crore) 5824.3

Debt (` crore) 216.7

Cash and Cash Equivalent (` crore) 116.3

EV (` crore) 5924.7

52 Week High / Low (`) 350/282

Equity Capital 204.4

Face Value 10.0

FII Holding (%) 7.7

DII Holding (%) 6.7

Key risks include:

Government RegulationsIn past six months the government has voluntarily shifted cardiac stents and knee implants under the national list of essential medicines (NLEM) list to cap the prices of both devices. Government has a l so put s ix months o f restriction on hospitals for making any changes to the procedural prices. NH derived 48% of FY17 revenues from cardiac treatment. Although NH's model is low cost, the disturbance in supplies on account of shortage and uncertainty of stent availability has direct impact on the procedural revenues. The management expects |40-45 crore of loss in FY18 due to cardiac stent price regulation. Off late the government also brought knee implants under the NLEM ambit. These kinds of interventions are detrimental to the revenues if the government also starts regulating the procedures. Recently two state governments West Bengal and

Karnataka has recently passed laws capping the prices of select private healthcare services.

The PPP model in healthcare can be unviable with CGHS rates

The NHP 2017 advocates active participation of private healthcare providers with government acting as service purchaser. The Niti Ayog's report on PPP gives details about the rates that can be charged to patients who aren't covered by National Health Protection Schemes (NHPS), Rashtriya Swasthya Bima Yojana (RSBY), Central Government Health Scheme (CGHS) or state insurance schemes. The proposal suggests that where NHPS, RSBY and state insurance schemes aren't applicable, patients cannot be charged over CGHS rates. Note that the CGHS rates are substantially lower than even the average rates for different procedures hence any player entering into these kind arrangements will face substantially longer payback achievement.

13ICICIdirect Money Manager December 2017

STOCK IDEAS

ANALYST CERTIFICATION We /I, Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta M. Tech (Biotechnology) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India's largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER Mitesh Shah MS (Finance), Harshal Mehta MTech (Biotechnology) Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

14

FLAVOUR OF THE MONTH

Manage taxes at every life stage

ICICIdirect Money Manager December 2017

An ideal tax-management strategy is the one that is adaptable and revised

according to individual's changing financial circumstances. We often don't realize

that changes in inflow and outflow of our income significantly impacts our tax

liabilities, which makes tax planning a dynamic process. Each life stage has its

distinct perks and challenges. But there's a tax-saving strategy suitable for every

individual, it's just a matter of assessing your current financial health and adopting

a product that benefits the most at current life stage.

Why incorporate taxes in financial planning?

Almost all our financial decisions affect taxes. By overlooking them while making any financial plan, one may end up paying more taxes than he would have otherwise. Aligning tax-planning along with our financial goals, can, in fact, enhance the probability of accomplishing these goals. Analyzing current as well as future tax l iabi l i t ies and adopting tax strategies to minimize the payable tax is an effective way to manage our current and future expenses. Thus, tax planning is a key element of establishing a successful financial plan.

Often investors invest in a product just to save taxes and fail to look at other influential aspects of investments such as risk capacity, age and time

h o r i z o n o f i n v e s t m e n t . Unfortunately, this is simply an ad hoc approach towards financial planning.

It is important to focus on f i n a n c i a l g o a l s a n d t a x planning should be a part of your financial planning, and not an end-goal in itself. Tax planning is not a one-time exercise that you should undertake once a year. Essen-tially, it should be a year-round process.

In order to clarify tax-management strategies, we have divided tax-payers into four age groups. Age is taken as a distinguishing criteria mainly because age r isk to l e rance and expec ted returns are closely related– for instance, lower the age, higher the risk tolerance and the potential returns.

15

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

Life stages and tax structureAge (years) Income source Asset base Risk tolerance Tax bracket

20-30 Wages

None

Highest

Low

31-40 Wages / investment Accumulating High / moderate Higher

41-50 Wages / investment

Growing

Moderate / low

High

51 and above Investment Depleting Lowest High / highest

20- 30

Twenties are usually the start of

our careers, and probably

means relatively lower income

a n d l o w e r t a x l i a b i l i t y.

However, risk tolerance can be

highest at this stage since

longer time can be given to

investments to grow and

overcome losses. Investments

made in this stage can benefit

from the power of

compounding in the long haul.

Here are some tax-saving

strategies for this age group:

- Salaried individuals can

availtax deduction overEPF

(employee provident fund)

contribution under section

80C of Income Tax Act. The

employee's share is subject

t o d e d u c t i o n ( 1 2 % o f

employee's basic salary),

whereas, contribution from

employer is exempt from

tax.

- Another popular tax-saving

instrument under section

80C is public provident fund

(PPF). The current interest

rate of PPF is 7.8%. Though

the return rate varies from

year to year, investors in this

age group should focus on

investments producing

more aggressive returns.

- With time on your side, this is

the idea l t ime to s tar t

investing for long-term

goals. Invest small amount in

equity or equity mutual

funds to build corpus for

goals like property purchase.

E q u i t y l i n k e d s a v i n g s

scheme (ELSS) offer triple

benefits of tax-deduction,

capital appreciation and tax-

free returns.

- Investments in equity related

p r o d u c t s a r e h i g h l y

b e n e f i c i a l f o r y o u n g

investors with long-time

16

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

investment horizon in mind.

Long-term capital gains on

equity are also tax-free.

- If you are repaying the

education loan your parents

had taken, you can claim

deduction on that amount

too. However, this deduction

is only applicable on the

interest paid. There's no

upper limit on this amount.

I n d i v i d u a l s r e p a y i n g

education loan of spouse

can also avail this benefit.

- Investors in this age group

should prioritize equity over

provident funds for tax

saving, unless they have

sufficient equity investments

in their investment portfolio,

over and above tax saving

investments.

- First-time home buyers can

even earn tax deduction of

Rs. 50,000 over and above

Rs. 1.5 lakh of section 80C.

31-40

This is commonly the phase

where we start a family.

F i n a n c i a l l y d e p e n d e n t

members in the family is the

biggest change for most

adults. Increased income,

responsibilities, and liabilities

also mean increased taxes.

Since risk tolerance is still very

strong in thirties, investments

can be started for long-term

horizon.

- Hike in salary will reflect into

EPF contr ibut ion. With

higher contribution you can

save more taxes under

section 80C.

- Invest early in pension plans

to cut down on the premium.

ELSS a long with other

mutual funds can build a tax-

efficient retirement portfolio.

- This is the right time to invest

in NPS (national pension

s y s t e m ) . G o v e r n m e n t

initiated retirement security

avenue while reducing tax

liability of the investor.

- A married person has to look

after his/her spouse and

c h i l d r e n a s w e l l . L i f e

insurance is one way to

protect your family, while

availing tax benefit on its

annual premiums.

- H e a l t h c a r e i s a n o t h e r

important goal at this life

17

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

stage. Remember, health

insurance premiums for self,

spouse, dependent children

and parents are eligible for

tax deduction under Section

80D.Even if one is covered

for medicals by the em

ployer, it is advisable to take

an additional health cover for

self and family.

- Parents of young children

can save tax by deducting

children's tuition fees and

certain school fee expenses

from taxable income.

- If you have a daughter below

10, take advantage of the

Sukanya Samriddhi Yojana

that enjoys same tax break

as provident funds but at

superior interest rate (8.3%).

- Those repaying home loans

have tax advantage over

both principal and interest

amount under sec t ion

80Cand 24 respectively.

41- 50

At this stage of life one should

increase the insurance cover-

age as he has dependent chil-

dren, and there are expenses

like children's education, their

marriage, etc. Further, periodic

cash flow is needed at this

stage and so it is recom-

mended to keep a part of the

investments in bank deposits.

- Investing in children's plan or

ULIP can give higher protec

tion to the child's future even

if you are not around to

w i tness i t . Re t i rement

planning should also feature

prominently.

- Pre-retirees have to increase

their exposure towards pen

sion plan and PPF for their

retirement needs.

- Exposure to equity may be

brought down, but don't

exclude it altogether. Making

equity part of your portfolio

willhelp add some extra

muscle to the saved-up

corpus.

- Tax breaks on home loan

repayments continue to be

part of tax-saving strategy

for people in this age group.

- Parents of children pursuing

higher studies can claim

deduction on the interest

paid on children's education

loan u/s 80E.

18

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

- Those having ten more years

to retirement can continue

investing in ELSS, NPS or

balanced mutual funds and

a c c o m p l i s h g o a l s o f

securing retirement and tax-

saving.

51 and above

Senior citizens get more tax-

breaks. This is also the time

when the investments made in

retirement plans help you

maintain the standard of living.

The health insurance plan

taken earlier gives the comfort

of being insured for medical

expenses at much lower

premium. There is a need for

stable and steady income. So

PPF and bank FD/NSC is rec-

ommended.

- With increased life expectancy

rate, a small equity exposure

is recommended at this stage.

- Invest small amounts in fixed

income instruments covered

under section 80C like NSC,

tax-saving FDs, monthly

income scheme. Along with

tax rebate benefit, these

schemes o f fe r re tu rns

between the ranges of 7 to 8

per cent, for the period of 3

to 10 years.

- An individual of the age of 60

years or more can open

Senior Ci t i zen Savings

Scheme (SCSS) Account

and claim deduction on its

deposits. Their return rate at

8.4% is the highest among

other post office savings

schemes.

Tax- saving investment optionsEmployee provident fund (EPF)

Most companies have EPF for

the benefit of employees. An

employee can contribute 12

percent of the salary towards

EPF. The employer also con-

tributes 12 percent of salary.

This is a good tool to build a

retirement corpus. EPF enjoys

an EEE tax status, meaning,

money in this account is

exempt from taxes at the time

of investment, accumulation

and withdrawal (on maturity

only).

Public provident fund (PPF)This is another tool to build the

retirement corpus. Anyone can

open a PPF account with a

minimum contribution of 500.

Premature closure is not

19

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

allowed before 15 years. Wit

drawal facility is available after

6 years. This is a good tool for

those who are not covered by

EPF to fund their retirement.

Even those covered under EPF

can also contribute to PPF, for a

larger retirement corpus.

National Saving Certificate (NSC)

Money invested in NSC is de-

ductible u/s 80C. The minimum

investment is Rs. 1 ,000.

Investment up to Rs. 1, 00,000

per annum qualifies for IT

Rebate under section 80C of

Income Tax Act. This is a highly

safe investment as it is backed

by government security and is

best suited for the risk-averse

investor. Further, a bank loan is

available against NSC.

National Pension System (NPS)

This is another government

initiated avenue, but offering

market linked returns. Tax-free

contribution to NPS tier I

account is capped at Rs. 50,000

under section 80 CCD, which is

over and above the existing

limit of Rs. 1.5 lakh. Both

deposits and interest of NPS

account are free of tax burden

but pre-mature withdrawals

are taxed as per investor's tax

bracket. NPS is an opportunity

to invest in equity, government

securities or corporate debt

securities as per our choice.

The investor has liberty to

allocate his money across

these three classes based on

his risk profile.

The NPS falls under EET

taxation, meaning, deposits

and accumulations are tax free,

but not the maturity amount. At

maturity, 40% of withdrawal is

t a x e x e m p t . H o w e v e r,

according to budget 2017, NPS

account holders can with

drawup to 25% of the i r

contributions under certain

circumstances.

Equity Linked Savings Scheme

(ELSS)

Another stock market driven

investment with lock-in period

of 3 years. Its tax deductions

are included in the same cap of

Rs. 1.5 lakh under section 80C.

Lump sum amount invested in

ELSS will be deducted from

taxable income of respective

f inancial year and entire

amount can be withdrawn after

20

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

3 years. But when invested via

Systematic Investment Plan

(SIP), total amount can be

withdrawn only after each

instalment completes the lock-

in period of 3 years.

Senior Citizen Savings Scheme

(SCSS)

Deposits made to Senior

C i t i zen Sav ings Scheme

(SCSS) are deductible but

interest earned on it is taxable

i ncome. SCSS p rov ides

returns at the fixed rate of

8.4%. Eligible only for retirees

above the age of 60, SCSS can

be held for 5 years and

stretched up to 3 years later

that. However, only lump sum

investment, not exceeding Rs.

15 lakh is allowed in one

account.

Unit Linked Insurance Plans

(ULIPs)

This is one of the reliable

i n v e s t m e n t p r o d u c t s

considering protection cover,

hea l thy re tu rns and tax

advantage, all combined in one

product. Insured person's

premiums are invested in a mix

of debt and equity assets to

offer productive returns, while

he enjoys tax deduction under

80C cover at the same time. He

also has liberty to choose asset

classes and switch from one to

another. Both death benefit

and maturity payouts under

ULIP avail tax benefits.

The only condition with ULIPs

is - premium amount should be

less than 10% of the sum

assured. For instance, if the

sum assured is Rs. 10lakh and

annual premium costs less

than Rs. 1lakh, then the entire

premium is subject to tax

deduction. But if the premium

is Rs. 1.5 lakh (more than 10%

of the sum assured) deduction

for only permissible limit i.e.

Rs. 1 lakh can be availed.

Tax-saver fixed deposits

Tax-saving fixed deposits and

post office time deposit with

the lock-in period of 5 years are

also eligible for 80C tax benefit.

Please note that not all fixed

deposi ts qual i fy for th is

concession. Only tax-saving

FDs come under this category.

21

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

Comparison between tax-saving investmentsInvestment Interest rate* (%) Lock-in Period Tax benefit

ELSS 12-15 % expected 3 years Deduction up to Rs. 1.5

lakh under section 80C

EPF 8.65 15 years Deduction up to Rs. 1.5

lakh under section80C

PPF 7.8

15 years

Deduction up to Rs. 1.5

lakh under section 80C

NPS 10-12 expected

Till retirement

Deduction up to Rs. 50,000

under section 80 CCD, over

and above the existing limit

of Rs. 1.5 lakh

NSC 7.8 5 years Deduction up to Rs. 1.5

lakh under section 80C

Tax-saver FD Around 6- 8 %

5 years

Deduction up to Rs. 1.5

lakh under section 80CULIPs 8-10% expected

5 years

Tax exemption under

section 80C and 10 (10D)

SukanyaSamriddhiYojana 8.3% Till a/c holder attains age

of 18 years

Deductionup to Rs. 1.5

lakh under section 80C

SCSS 8.4% 5 years Deduction up to Rs. 1.5

lakh under section 80C

* Interest rates as on December 2017

Mutual fund suitability matrix

Source: Economic times

22

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

Tax- saving non-investment options

Life insurance

Annual premiums paid for

one's life cover and even for

the policy that covers his/her

family (spouse and children)

are tax exempted. Please note

that the entire amount paid

towards insurance premiums

cannot be deducted while

calculating taxable income. For

the policies issued before

March 31, 2012 amount up to

20% of total sum assured and

for the policies issued on or

after April 1, 2012 maximum of

10% of the sum assured is

e l i g i b l e f o r d e d u c t i o n .

Meaning, if you have taken an

insurance cover of Rs. 1 lakh in

2013 you can claim deduction

up to Rs. 10,000 (10% of Sum

Assured) and not on the

premium above this limit.

Home loan repaymentsEquated Monthly Instalment

(EMI) paid towards repayment

of home loan is one of the

eligible deductions under Rs.

1.5 lakh limit of section 80C.

This benefit can be availed only

for self-occupied or rented

property and not for the under

construction home. However,

pre-EMI paid in the same

financial year can also be

claimed if the construction is

completed before the end of

financial year. Interest paid

towards home loan up to Rs. 2

lakh is also eligible for tax

deduction under section 24 of

Income Tax Act.

B o t h b o r r o w e r a n d c o -

borrower can claim tax-benefit

for the same home loan. In

addition to principal and

i n t e r e s t a m o u n t o t h e r

expenses l ike home loan

insurance premium, stamp

duty cost, registration fee,

processing fee can also avail

tax benefit.

First time home buyers enjoy

Rs. 50,000 deduction benefit

for the interest on home loan

over and above section 80C

and Section 24 home loan tax

deductions. Home loan that is

sanctioned in FY 2016-17 and

doesn't exceed Rs. 35 lakh is

eligible for this category.

House rent allowance (HRA)Sa la r ied ind iv idua l who

r e c e i v e s H R A f r o m h i s

employer and live in a rented

23

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

accommodation, can utilize tax

exemption under section 10.

Even if one doesn't get such

allowance from the employer,

he can claim deduction up to

Rs. 60,000 under section 80

GG. A person living in a rented

place but repaying a home

loan of his/her own, can claim

tax deduction/ exemption for

both expenses.

Health insuranceThe premium paid towards

health insurance is exempt u/s

80D of the Income Tax Act.

Premium paid towards a health

insurance policy of spouse, de-

pendent children and depend-

ent parents is tax-free. The

maximum limit of deduction is

`15,000 and `20,000 in case of

senior citizens. One can claim

maximum up to Rs. 25,000 for

t h e p r e m i u m s p a i d f o r

insurance payee himself,

his/her spouse, dependent

children and parents. Senior

citizens (above 60 years) can

claim deduction up to Rs.

30,000 and even children

paying insurance premiums

for their senior citizen parents

can avail maximum of Rs.

30,000 deduction.

Moreover, sect ion 80DD

p r o v i d e s b e n e f i t t o t h e

taxpayer who is paying for

treatment of his/her disabled

family member. This is capped

at Rs. 75,000. However, the

limit for severe disability is set

at Rs. 1, 25,000

Education loanInterest paid during repayment

of education loan is eligible for

tax deduction under section

80E. This benefit is not implied

for principal amount. An

individual can claim this

concession over education

loan taken for higher studies of

self, spouse and children.

Higher studies include any

regular or vocational course

pursued after completion of

senior secondary examination

or equivalent exam from any

school or board or university.

This benefit is also applicable if

an individual is the legal

guardian of a student.

Charity and donations Contribution made towards

donations and charity are

acknowledged for absolute or

partial tax deduction, as per

24

FLAVOUR OF THE MONTH

ICICIdirect Money Manager December 2017

given rules, under section 80G

of Income Tax Act. Individual,

HUF (Hindu Undivided Family)

and company can avail this

benefit irrespective of their

source of income.

Bottom line:Tax-management is a financial

goal in itself. With a little

homework and advance

planning one can not only save

taxes but make appropriate

investment choices that can

help him meet major life-stage

goals. However, it is wiser to

invest with the clarity and

foresight of long term capital

growth and protection rather

than investing with the short-

term advantage of only saving

taxes. Pay attention while

interpreting various provisions

under different sections of the

Income Tax Act. Better yet,

consult an expert to avoid

impulsive decisions.

The views expressed in the article are personal views of the author and do not necessarily represent the views of ICICI Securities

25

Tête-à-tête

ICICIdirect Money Manager December 2017

Fund managers on current economic scenario, rupee changes and state elections

In talk with ICICIdirect Money Manager, P. V. K. Mohan (Principal Pnb AMC), Anand Radhakrishnan, Chief Investment Officer (Franklin- Equity India, Franklin Templeton Asset Management), Deepak Gupta, (Kotak Asset Management) and Lalit Nambiar (UTI Mutual Fund) share their views on latest market trends. Excerpt:

Q. Can you tell our readers about

current economic situation, on

both global and domestic fronts?

A. P.V.K Mohan- Global growth

cont inues to be s t rong,

according to IMF global

growth in CY 18 is expected

3.7% which is a new high in

recent times, the growth is

broad based & covering Euro

zone, Japan, Emerging Asian &

European countries & Russia.

On domestic front, with GST &

demonetization behind us,

clear signs of uptake in growth

is visible which was even

endorsed by Moody's upward

revision of growth rate from

6.7% in current year to 7.5% in

FY 18

Anand R - An upswing in global economic activity, positive macroeconomic developments and conduc ive f inanc ia l conditions favor global growth a c c e l e r a t i o n . P o s i t i v e macroeconomic data, strong corpora te ea rn ings and optimism over tax reform with prospects of lower corporate tax rates have been supporting the US equity markets. Eurozone economic momentum has also started to accelerate however political uncertainty in Germany and Brexit related negotiations would be keenly watched. Lower US inflation has prompted expectations of a milder pace of rate hike by the US Federal Reserve. That said, most

P. V. K. Mohan

Principal Pnb AMC

Lalit NambiarUTI Mutual Fund

Deepak Gupta,

Kotak Asset Management

Anand Radhakrishnan,Chief Investment Officer

Franklin- Equity India,Templeton Asset Management

26

Tête-à-tête

ICICIdirect Money Manager December 2017

economies are in the process of interest rate tightening. The Bank of England recently announced its first rate hike in a decade. China's industrial and trade activity has been moderating though new economy related sectors remain strong. Chinese government has opened access to the financial services sectors and will gradually remove the limit of foreign ownership in the next 3-5 years.

A slew of sentiment-boosting events have taken the domestic equity markets to new life highs. India rose 30 notches higher to the 100th rank in the World Bank's Ease of Doing Business� rankings. Acknowledging the po l icy re form measures undertaken by the Indian government in the recent years, M o o d y ' s r a t i n g a g e n c y upgraded India's sovereign rating one notch up to Baa2 from Baa3 (lowest investment grade) with change in outlook to p o s i t i v e f r o m s t a b l e . Simplification of compliance procedure under GST and amendments to the insolvency and bankruptcy code are some recent examples of policy measures. Government is

attempting to push growth t h r o u g h s p e n d i n g o n infrastructure projects and housing sector. This could potentially lead to improvement in credit offtake growth as well a s h i g h e r e m p l o y m e n t generation over the next few years. Sustained momentum in consumption and exports is expected to lift corporate revenue and capacity utilization. Improvement in balance sheets of banks on account of recent recapitalization measures, resolution of stressed assets and improv ing capac i ty utilization as demand picks up should contribute to private capex recovery going forward.

Deepak Gupta- On the global front, economic growth and employment are picking up in US with inflation remaining lower than expectations. The rest of the developed world is still fighting for growth. In India, the growth in the last one year has been impacted because of demonitisation and imp lementa t ion o f GST. Though these have disrupted the growth in the short term, these are very, very positive measures from medium to

27

Tête-à-tête

ICICIdirect Money Manager December 2017

long term. We expect the formalization of economy to pick up pace which will result in buoyancy in tax revenues and fair competition amongst the industry participants.

Lalit Nambiar- Liquidity is a major force globally as well as locally and cannot be ignored. Global central banks led by the US Fed may gradually begin tightening even as the RBI has decided to stay neutra l . Several Wall Street economists believe that 2018 may see the biggest tightening of monetary policy in more than a decade. Against this there is a r i s ing r isk o f complacence setting into global equity markets as exhibited by the VIX which shows global risk aversion to be at multi-decade lows. Closer home in India, partly due to growing investor awareness as well as education and partly due to the paucity perceived or otherwise of alternative investment avenues, money continues to flow into equities raising v a l u a t i o n s , e v e n a s a n earnings pickup continues to e l u d e u s . T h e f a c t t h a t

domestic credit is showing signs of a pickup may well mean that the flow of money to equities may slow a bit but h o p e f u l l y i t w i l l b e compensated by the ensuing earnings growth. The silver lining for India is that it has wea thered two mass ive disruptions in a short period, demonetisation and GST, and has emerged stronger for it, underlining the economy's resi l ience. Hence from a medium term view of say 3-5 years, I would think India is bet ter p laced than most economies even if there were to be a slight tightening at the global level.

Q. In terms of sectors, where do you see the opportunities for investors in the current scenario?

A. P.V.K Mohan - Domestic & Global cyclicals like Auto, Cements, Metals ,Chemicals & Financials will through huge g r o w t h o p p o r t u n i t i e s . Consumption driven sectors will benefit from increase in Agri income domestically.

Anand R - Positive trends from the rural sector should bode well for consumer oriented

28

Tête-à-tête

ICICIdirect Money Manager December 2017

s e c t o r s i n Q 3 F Y 1 8 . Recapitalization in PSU banks should provide visibility of asset quality clean-up with enhanced provisioning. This could bring the focus back on growth and drive a cyclical recovery in the medium term. Bottoming out of asset quality and decl ine in sl ippages should support private bank earnings going forward.

Deepak Gupta- Some of the themes that investors can focus on are:

1. F o r m a l i s a t i o n o f t h e economy i.e. sectors where the informal sector was a major player will benefit as the informal sector will become uncompetitive.

2. Financia l isat ion of the economy. With money coming out of cupboards and mattresses into the banking system because of demonitisation, the financial sector benefits

3. Rural economy is looking upt h

b e c a u s e o f 7 p a y commission, farm loan waiver, good monsoon, MSP hikes

4. Focus on clean energy could

benefit sectors like gas utilities

L a l i t N a m b i a r - T h e r u r a l economy is expected to get an impetus from government policy tailwinds which are likely to boost rural incomes and thus rural consumption is likely to be up sharply over the next several years. This should benefit auto, consumer white a n d b r o w n , F M C G , construction and agri-related industries. At the same time there are nascent signs of a possible credit revival round the corner supporting an investment- led recovery. Sectors such as capital goods, industrial manufacturing and cement are well placed when the investment recovery picks up pace.

Q. What is your view on the rupee going ahead?

A. P.V.K Mohan - It may mildly depreciate.

Anand R – The INR has seen an uptrend from the start of CY2017, gaining about 6% YTD t i l l Nov. Improv ing macroeconomic data, benign crude prices, policy reforms and weakness in the USD have

29

Tête-à-tête

ICICIdirect Money Manager December 2017

contributed to this rise so far this year. Currently, trade and f i sca l de f i c i t r i sks have emerged on account of rising crude prices and expectations of f iscal sl ippage due to incrementa l government spending and a possibility of stimulus to boost growth. These risks around rising twin deficit are likely to turn foreign portfolio investors cautious in the near term and could weigh on INR. The INR could see a moderate weakening from current levels over the 3-12 month period.

D e e p a k G u p t a - The fo rex reserves are at a comfortable level now. Because of this, we don't expect much volatility in INR unless there is some big adverse global event. At the same time, the central bank won't be comfortable with steep appreciation in INR as it hurts export competitiveness. So, the view is that INR should be in 64-68 range over next one year

Lalit Nambiar- I do not claim to be an expert but the broad hypothesis would be, that given Crude oil is at a long term disadvantage due to structural

factors in the energy market including electric vehicles and solar tech prices, the scenario is favourable for the INR. Our twin deficits seem to well u n d e r c o n t r o l , g i v e n a responsible government and level headed policies from the RBI. Overall there should only b e a s t e a d y a n d s m a l l depreciation over the next few years in line with inflation differentials with the USD.

Q. How likely will the outcomeof the state elections influence the direction of our fiscal policies?

A . P. V. K M o h a n - F i s c a l consolidation will continue & will have no Impact of state elections.

Anand R – While the possibility o f p re - e lec t ion popu l i s t measures stoking inflation h o v e r s , w e e x p e c t t h e government to focus on bringing about amendments and enhancements to existing p o l i c y r e f o r m s a l r e a d y undertaken rather than pursue new structural reforms. Thrust on rural expenditure will continue to remain key with fiscal allocation to affordable housing, rural roads and

30

Tête-à-tête

ICICIdirect Money Manager December 2017

electr i f icat ion. Increased efforts are expected to be taken to t ransfer power subsidy through the Direct B e n e f i t Tr a n s f e r ( D B T ) m e c h a n i s m . H e a l t h y budgetary allocation to road projects should likely continue in the coming year. In case of relaxation of fiscal deficit target from 3.2% to 3.5%, we may see the incremental allocation being channelized to the rural schemes.

Deepak Gupta- A thumping majority for the NDA would mean that the voters have given a thumbs up to the central government's policies which wil l embolden the government to continue on the reforms path. A loss would mean that the government might have to go slow on big reforms

Lalit Nambiar- I think state elections occupy market fancy only for a few days before and after the event. Hence it is more a focus for traders than for long term investors; after all one cannot extrapolate these to predict broader pol i t ica l events such as general election results in

2019. Historically, the ability of forecasters and pol i t ica l pundits to predict outcomes a c c u r a t e l y h a s p r o v e n somewhat inadequate and strong business fundamentals have usually been able to trump short term whims and fancies of the market.

Q. Can you tell us something about your stock-selection process?

A. P.V.K Mohan - We follow a multi-cap strategy with focus on identifying stocks which are dominant or niche players in t h e i r s e c t o r, w i t h g o o d earnings growth prospects and available at attractive valuations. Our portfol io construction is typically more of a bottom-up approach as we b e l i e v e s u p e r i o r s t o c k selection leads to sustainable out performance.

A n a n d R – A b o t t o m - u p approach to stock selection is followed at FT, although sector weight ings are reviewed regularly. After identifying the stock universe, our research analysts analyse the financial data, visit companies, meet management and evaluate future potential of companies.

31

Tête-à-tête

ICICIdirect Money Manager December 2017

Once the team identif ies certain investment ideas, a rigorous quantitative and qualitative analysis of the business is done to determine p o t e n t i a l , c o m p e t i t i v e position, risks and catalysts for value recognition.

Typical ly the analysis of businesses involves meetings with competition, distributors, c l i e n t s , e x - e m p l o y e e s whenever possible and also tracking of relevant global trends & standards. During this p h a s e , t h e d e e p understanding of various businesses and industries built over the past decade or so helps us in taking a long term view and ignoring the short-term distractions. From this investible universe, based on investment objectives of the respective funds stocks are shortlisted for constructing the portfolios.