Embed Size (px)

Citation preview

IDENTIFYING RISKS AND IDENTIFYING RISKS AND CONTROLS IN BUSINESS CONTROLS IN BUSINESS

PROCESSPROCESS

Objectives of Internal Objectives of Internal Control (Control (SAS No. 94)SAS No. 94)

Objectives of Internal Objectives of Internal Control (Control (SAS No. 94)SAS No. 94)

1. Reliability of financial reporting2. Effectiveness and efficiency of

operations3. Compliance with applicable laws and

regulations

A process … designed to provide reasonable assurance regarding the objectives :

1. Control environment2. Risk assessment3. Control activities4. Information and communication 5. Monitoring

Elements of Internal ControlElements of Internal Control

1. Control environment2. Risk assessment3. Control activities4. Information and communication

5. Monitoring

Elements of Internal ControlElements of Internal Control

Integrity, ethical values, Management philosophy and

operating style, and organizational structure influences the control

environment.

Integrity, ethical values, Management philosophy and

operating style, and organizational structure influences the control

environment.

1. Control environment2. Risk assessment3. Control activities4. Information and communication5. Monitoring

Elements of Internal ControlElements of Internal ControlElements of Internal ControlElements of Internal Control

Once risks are identified, they can be analyzed to estimate their significance, to assess their likelihood of occurring, and to determine actions that will minimize them.

Once risks are identified, they can be analyzed to estimate their significance, to assess their likelihood of occurring, and to determine actions that will minimize them.

1. Control environment2. Risk assessment3. Control activities4. Information and communication5. Monitoring

Elements of Internal ControlElements of Internal ControlElements of Internal ControlElements of Internal Control

Control ActivitiesControl ActivitiesControl ActivitiesControl Activities

Performance reviews Segregation of duties Application controls General controls

1. Control environment2. Risk assessment3. Control procedures4. Information and communication5. Monitoring

Elements of Internal ControlElements of Internal ControlElements of Internal ControlElements of Internal Control

The company’s information system is a collection of procedures (automated and manual and records established to

initiate, record, process, and report the events in an entity’s process

Communication involves providing an understanding of individual roles

and responsibilities

The company’s information system is a collection of procedures (automated and manual and records established to

initiate, record, process, and report the events in an entity’s process

Communication involves providing an understanding of individual roles

and responsibilities

1. Control environment2. Risk assessment3. Control procedures4. Information and communication5. Monitoring

Elements of Internal ControlElements of Internal ControlElements of Internal ControlElements of Internal Control

1. Execution2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

1. Execution2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

1. Execution

2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Proper execution of transactions in the revenue and acquisition cycles

1. Execution

2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Proper execution of transactions in the revenue and acquisition cycles

Risk of not achieving execution objectives

1. Execution2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

1. Execution2. Information System

3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Proper recording, updating, and reporting of data in an information system

1. Execution2. Information System

3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Proper recording, updating, and reporting of data in an information system

Risk of not achieving information system objectives

1. Execution2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

1. Execution2. Information System3. Asset protection

4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Safeguarding of assets

1. Execution2. Information System3. Asset protection

4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Safeguarding of assets

Risk of loss or theft of assets

1. Execution2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

1. Execution2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Favorable performance of an organization,Person, department, product, or service

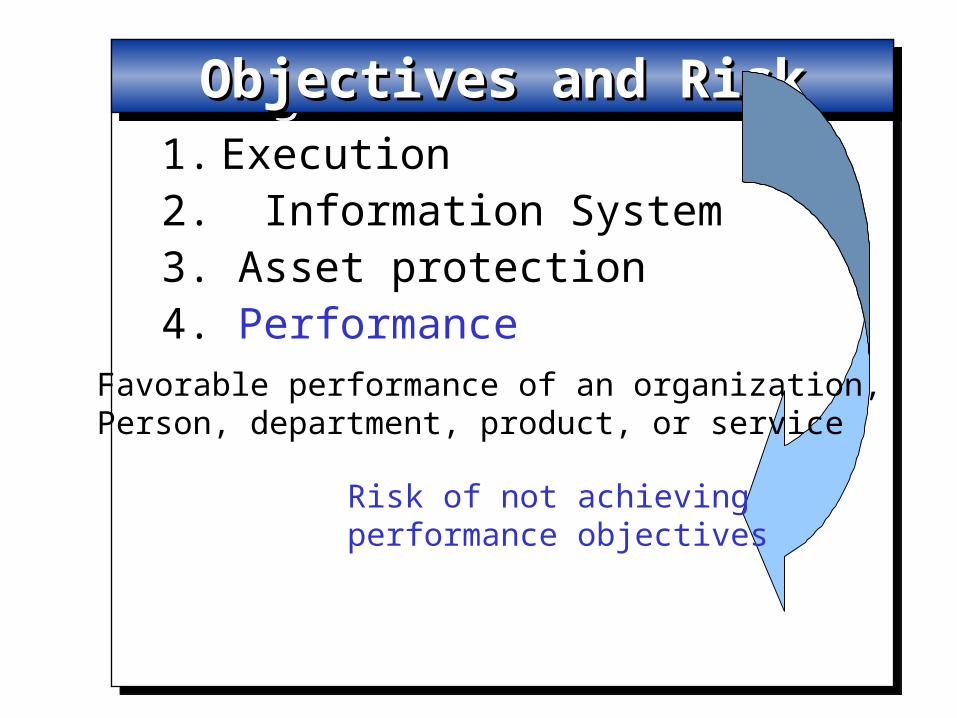

1. Execution2. Information System3. Asset protection4. Performance

Objectives and RiskObjectives and RiskObjectives and RiskObjectives and Risk

Favorable performance of an organization,Person, department, product, or service

Risk of not achieving performance objectives