Embed Size (px)

Citation preview

GE Confidential

1@#GECON&*

IEA Gas and Oil Technologies Collaboration Initiative, GOTCIExperiences after 2 years

Jostein Dahl Karlsen, styreformann GOT/OED

GE Confidential

2@#GECON&*

IEA Gas and Oil Technologies Initiative, GOT

Points

1) GOT background

2) Membership & Focus

3) Activities

GE Confidential

3@#GECON&*

IEA Olje- og gassteknologi:

• 2013: IEA GOT

GE Confidential

4@#GECON&*

GOT founding countries, June 2013

Switzerland Norway Netherlands Spain

GE Confidential

5@#GECON&*

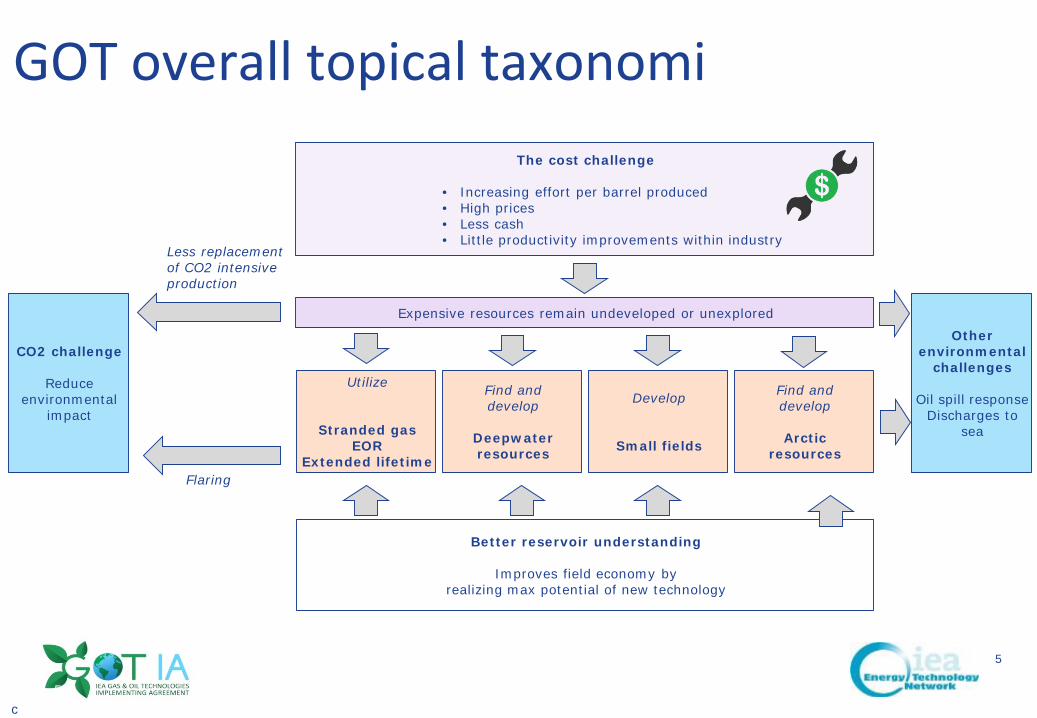

GOT overall topical taxonomi

c

The cost challenge

• Increasing effort per barrel produced• High prices• Less cash• Little productivity improvements within industry

Expensive resources remain undeveloped or unexplored

Find and develop

Deepwaterresources

Develop

Small fields

Utilize

Stranded gasEOR

Extended lifetime

Find and develop

Arcticresources

Better reservoir understanding

Improves field economy byrealizing max potential of new technology

Less replacement of CO2 intensive production

Flaring

CO2 challenge

Reduce environmental

impact

Other environmental

challenges

Oil spill responseDischarges to

sea

5

GE Confidential

6@#GECON&*

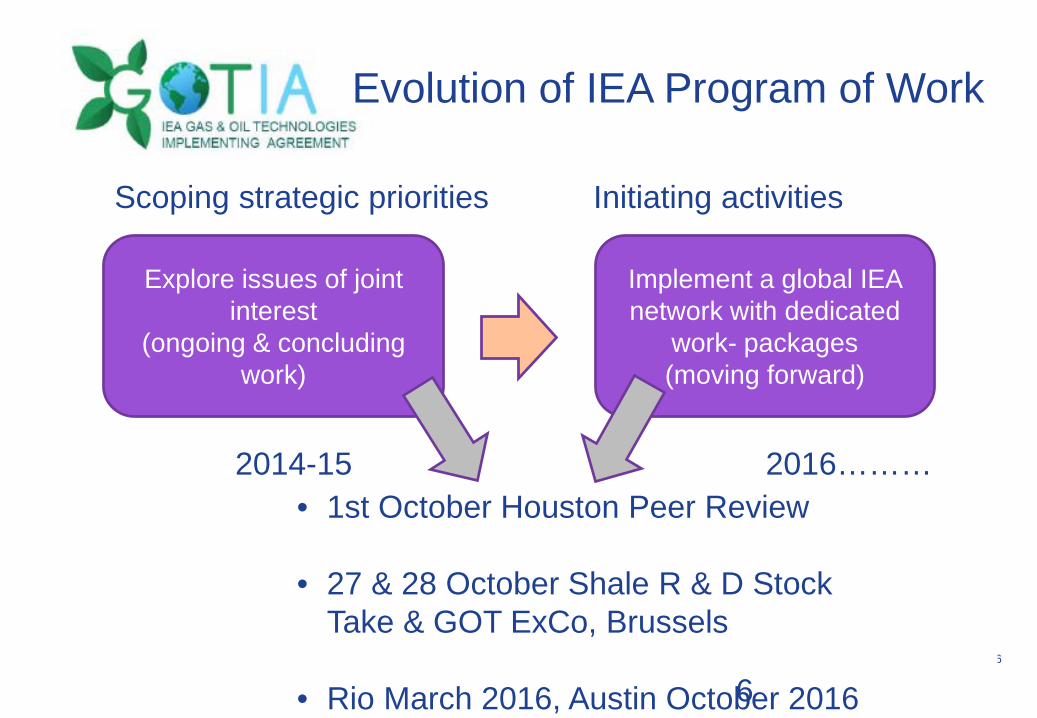

Explore issues of joint interest

(ongoing & concludingwork)

Implement a global IEA network with dedicated

work- packages(moving forward)

Scoping strategic priorities Initiating activities

Evolution of IEA Program of Work

2014-15 2016………• 1st October Houston Peer Review

• 27 & 28 October Shale R & D Stock Take & GOT ExCo, Brussels

• Rio March 2016, Austin October 20166

GE Confidential

7@#GECON&*

2015: US and Australia joining GOT

GE Confidential

8@#GECON&*

New Member: EU Commission DG Research

GE Confidential

9@#GECON&*

• Keynote Overviewes• National & Regional Research• Topical Sessions – Issues involved

- water- induced seismicity- public acceptance

Outline of event:Venue:Brussels 27-28 October '15- With European, North-American and Australian Research Champions

Where and who:

9

GE Confidential

10@#GECON&*

Overall observations:

2015

University of Texasat Austin, TX10-11 th October '16

1

GE Confidential

11@#GECON&*

11

GE Confidential

12@#GECON&*

GOT at Arctic Frontiers, Tromsø

GE Confidential

13@#GECON&*

GOT Executive Committee

Next meeting:London, 14 June 2016

1

GE Confidential

14@#GECON&*

Involvement by Industry & Academia

GOT Outreach

Stanford UniversityUT at AustinRice UniversityUHColorado School of MinesUniversity of Bergen

14

GE Confidential

15@#GECON&*

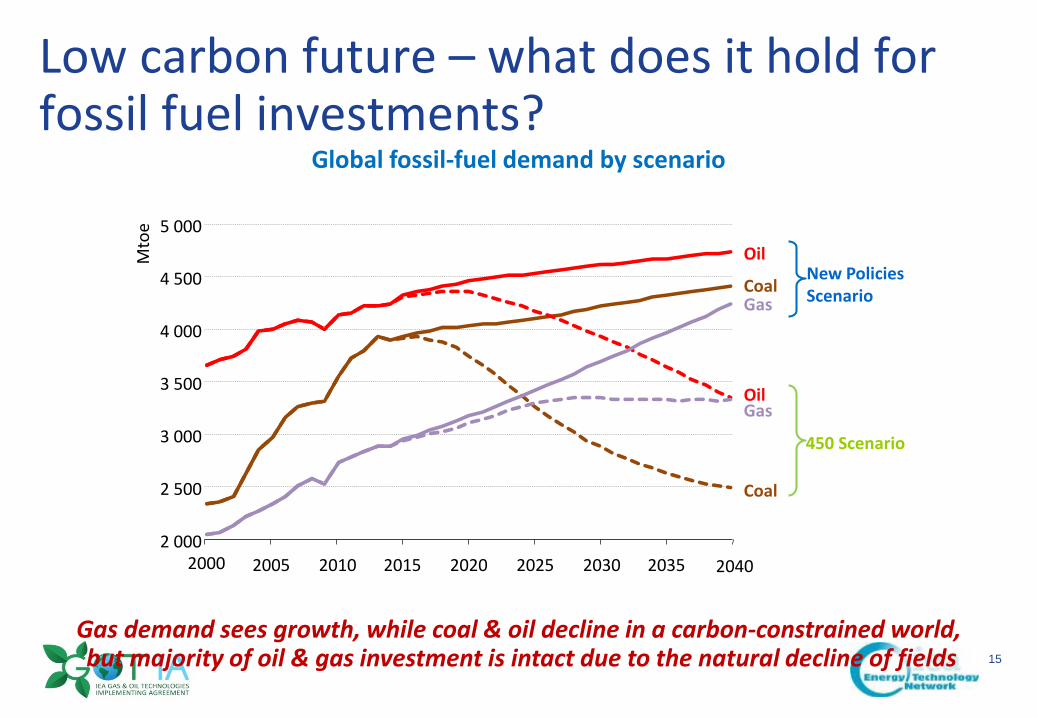

Low carbon future – what does it hold for fossil fuel investments?

Global fossil-fuel demand by scenario

Gas demand sees growth, while coal & oil decline in a carbon-constrained world,but majority of oil & gas investment is intact due to the natural decline of fields

2 000

2 500

3 000

3 500

4 000

4 500

5 000

2000 2005 2010 2015 2020 2025 2030 2035 2040

Mto

e

Oil

CoalGas

New PoliciesScenario

Oil

Coal

Gas

450 Scenario

GE Confidential

16@#GECON&*

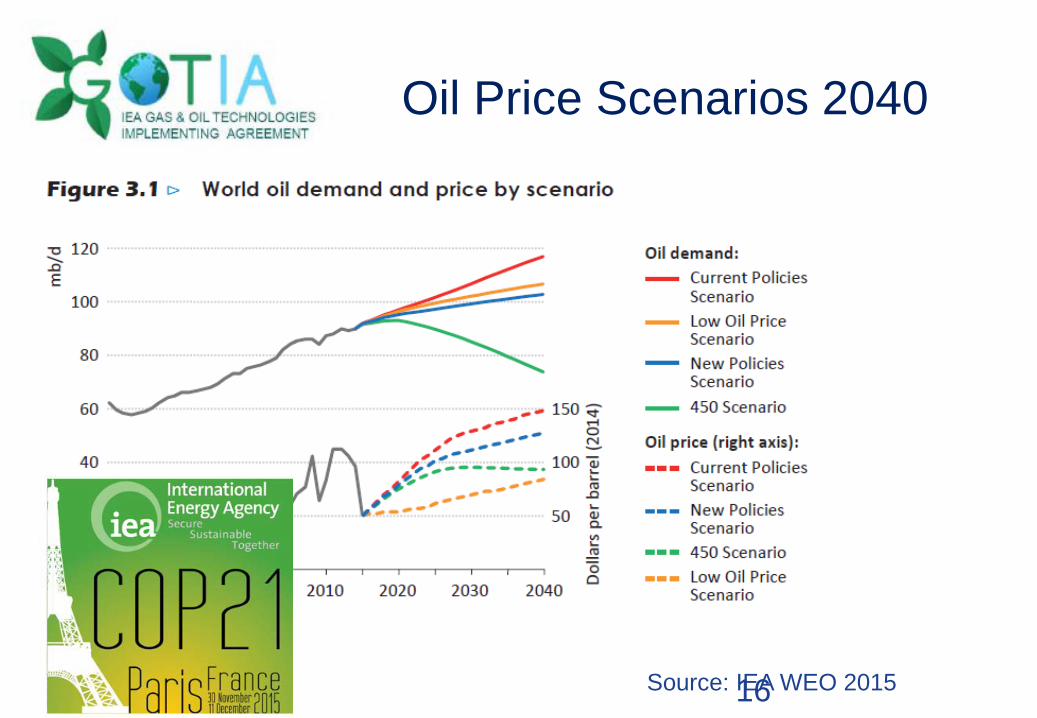

Oil Price Scenarios 2040

Source: IEA WEO 201516

GE Confidential

17@#GECON&*

Lower oil prices affect the competitiveness of fuels

Change in global primary energy demand by fuel in the Low Oil Price Scenario relative to the New Policies Scenario

As well as increases in oil, natural gas benefits (for a while), particularly in regions where import prices are indexed to oil: with coal pushed out in the power sector

-400

-300

-200

-100

0

100

200

300

2015 2020 2025 2030 2035 2040

Mto

e OilGasCoalRenewable

Source: IEA WEO 2015

GE Confidential

18@#GECON&*

GE Confidential

19@#GECON&*

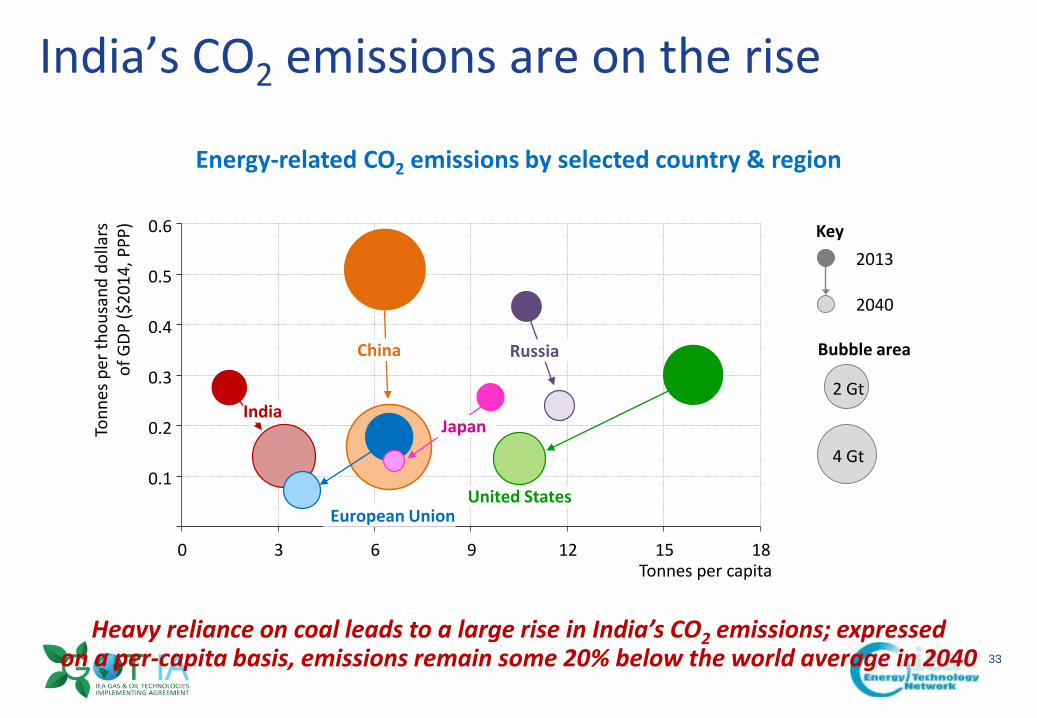

India’s CO2 emissions are on the rise

Energy-related CO2 emissions by selected country & region

Heavy reliance on coal leads to a large rise in India’s CO2 emissions; expressedon a per-capita basis, emissions remain some 20% below the world average in 2040

0.1

0.2

0.3

0.4

0.5

0.6

0 3 6 9 12 15 18Tonnes per capita

Tonn

espe

r tho

usan

d do

llars

of

GDP

($20

14, P

PP)

Bubble area

2 Gt

4 Gt

Russia

European Union

China

IndiaJapan

United States

Key2013

2040

GE Confidential

20@#GECON&*

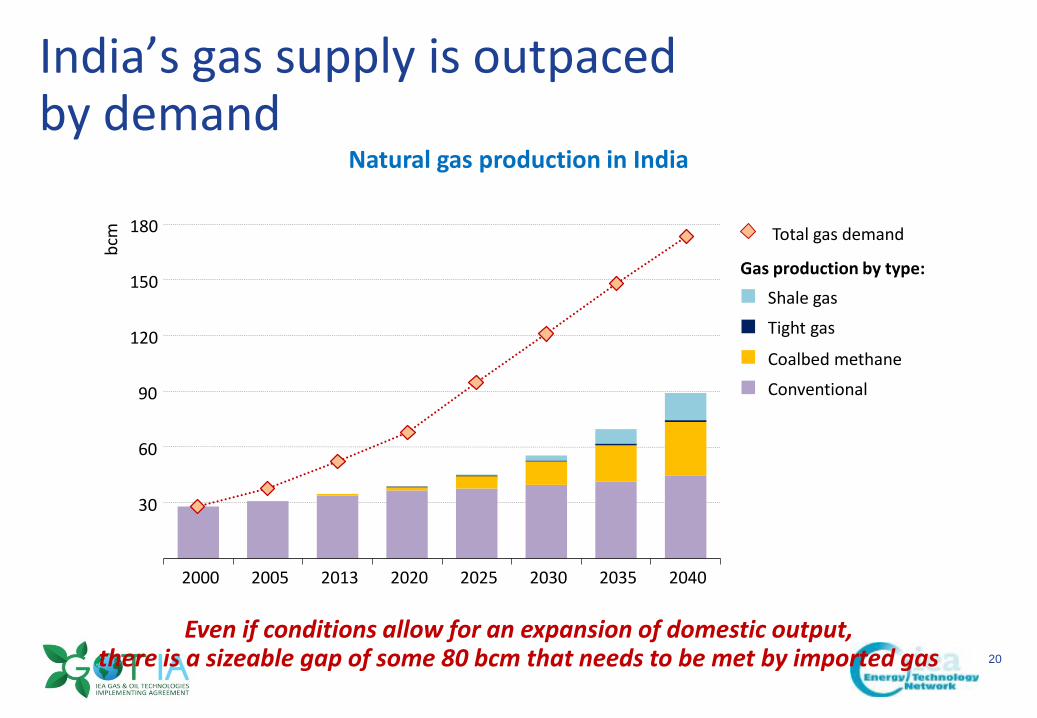

India’s gas supply is outpacedby demand

Natural gas production in India

Even if conditions allow for an expansion of domestic output,there is a sizeable gap of some 80 bcm that needs to be met by imported gas

30

60

90

120

150

180

2000 2005 2013 2020 2025 2030 2035 2040

bcm

Shale gas

Tight gas

Coalbed methane

Conventional

Gas production by type:

Total gas demand

GE Confidential

21@#GECON&*

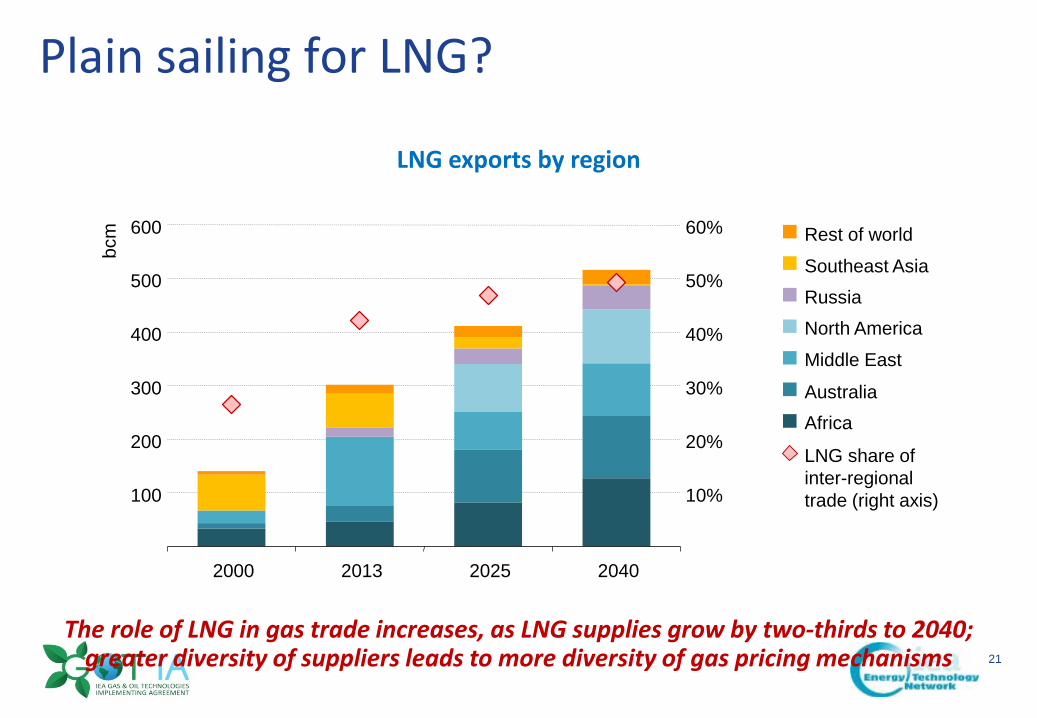

Plain sailing for LNG?

LNG exports by region

The role of LNG in gas trade increases, as LNG supplies grow by two-thirds to 2040;greater diversity of suppliers leads to more diversity of gas pricing mechanisms

100

200

300

400

500

600

2000 2013 2025 2040

bcm

10%

20%

30%

40%

50%

60% Rest of worldSoutheast AsiaRussiaNorth AmericaMiddle East

AustraliaAfrica

LNG share ofinter-regionaltrade (right axis)

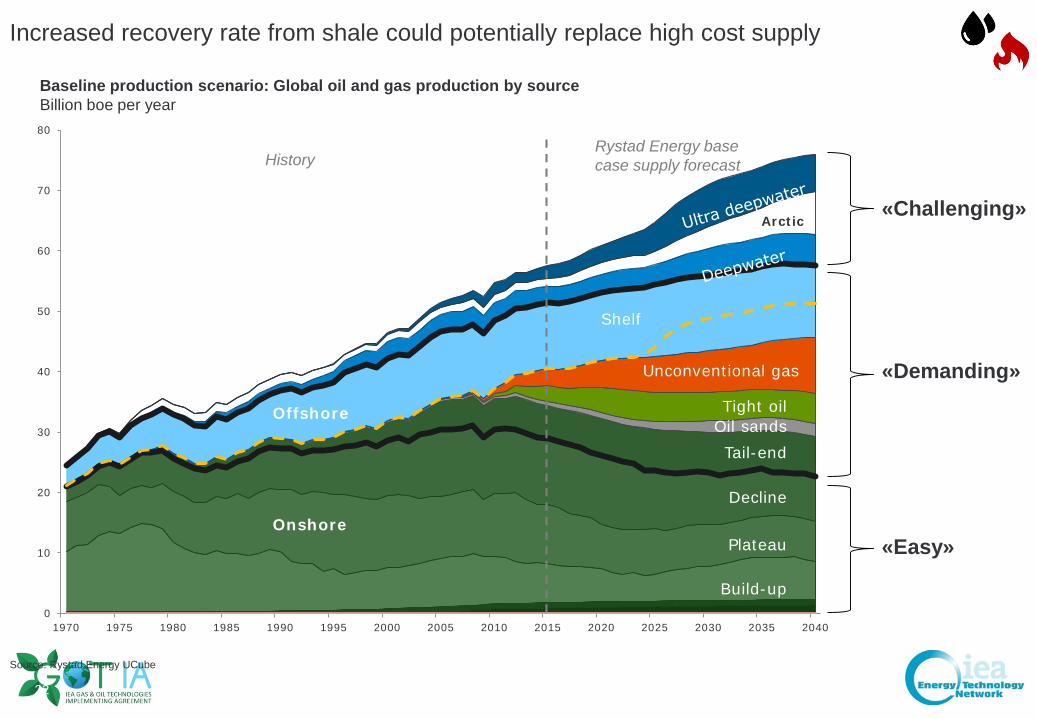

Increased recovery rate from shale could potentially replace high cost supply

Source: Rystad Energy UCube

0

10

20

30

40

50

60

70

80

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Onshore

Build-up

Plateau

Decline

Tail-endOil sandsTight oil

Unconventional gas

Shelf

Offshore

Arctic

Baseline production scenario: Global oil and gas production by source Billion boe per year

HistoryRystad Energy base case supply forecast

«Easy»

«Demanding»

«Challenging»

22

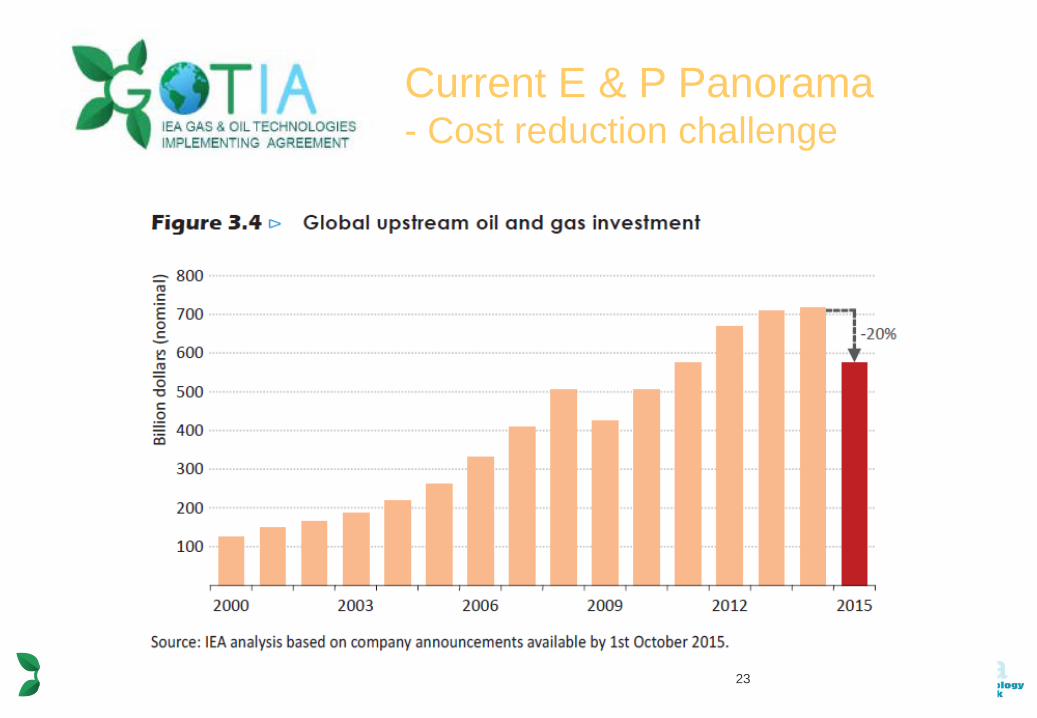

Current E & P Panorama- Cost reduction challenge

23

GE Confidential

24@#GECON&*

Finalisation of GOT-studyValue of closing global E & P gaps

24

GE Confidential

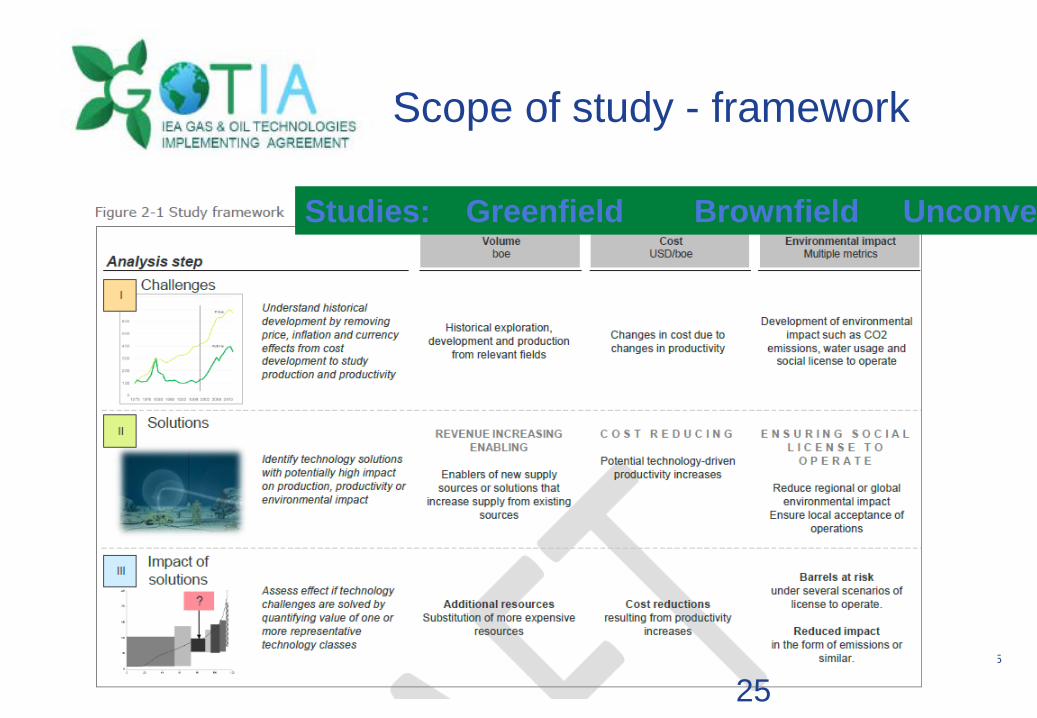

25@#GECON&*

.

Overall observations:

Scope of study - framework

Studies: Greenfield Brownfield Unconve

25

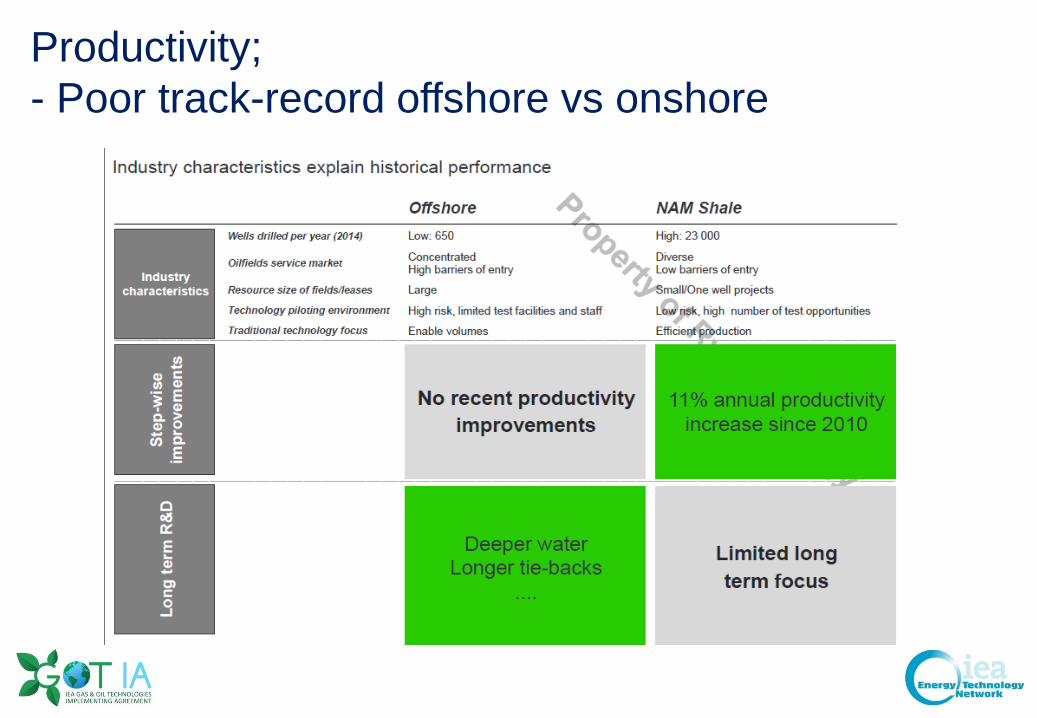

Productivity;- Poor track-record offshore vs onshore

IEA GOT FINEP - Deepwater Technology Forum

Repsol participation?

27

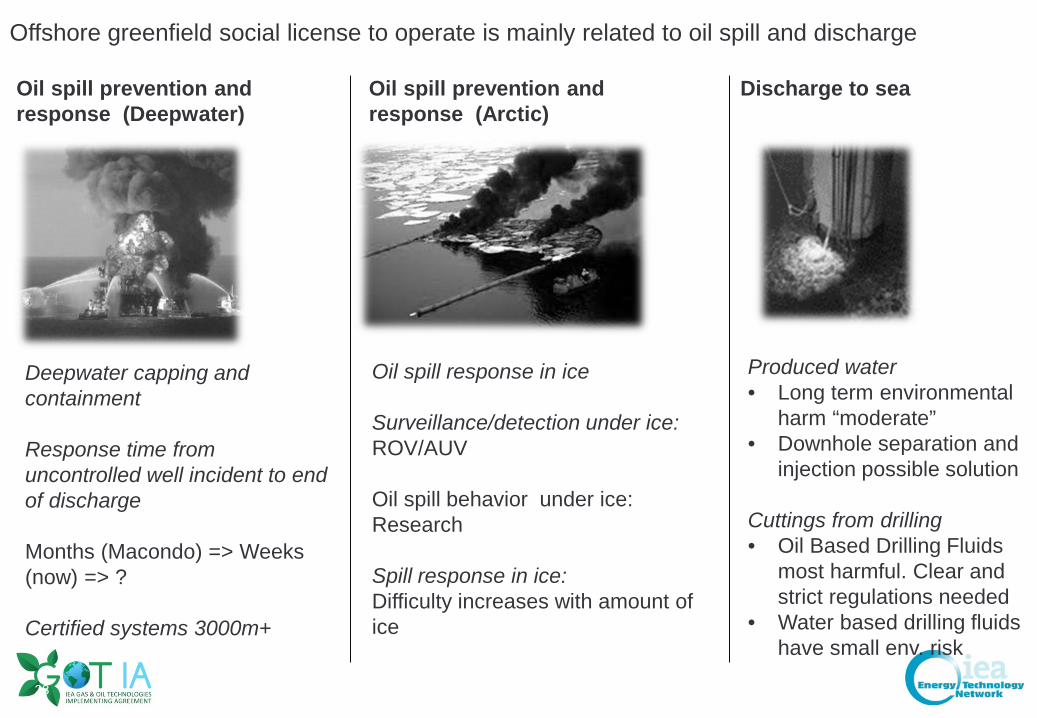

Offshore greenfield social license to operate is mainly related to oil spill and discharge

Oil spill prevention and response (Deepwater)

Deepwater capping and containment

Response time from uncontrolled well incident to end of discharge

Months (Macondo) => Weeks (now) => ?

Certified systems 3000m+

Oil spill prevention and response (Arctic)

Oil spill response in ice

Surveillance/detection under ice: ROV/AUV

Oil spill behavior under ice: Research

Spill response in ice: Difficulty increases with amount of ice

Discharge to sea

Produced water• Long term environmental

harm “moderate”• Downhole separation and

injection possible solution

Cuttings from drilling• Oil Based Drilling Fluids

most harmful. Clear and strict regulations needed

• Water based drilling fluids have small env. risk

28

Thank you

29

GE Confidential

30@#GECON&*

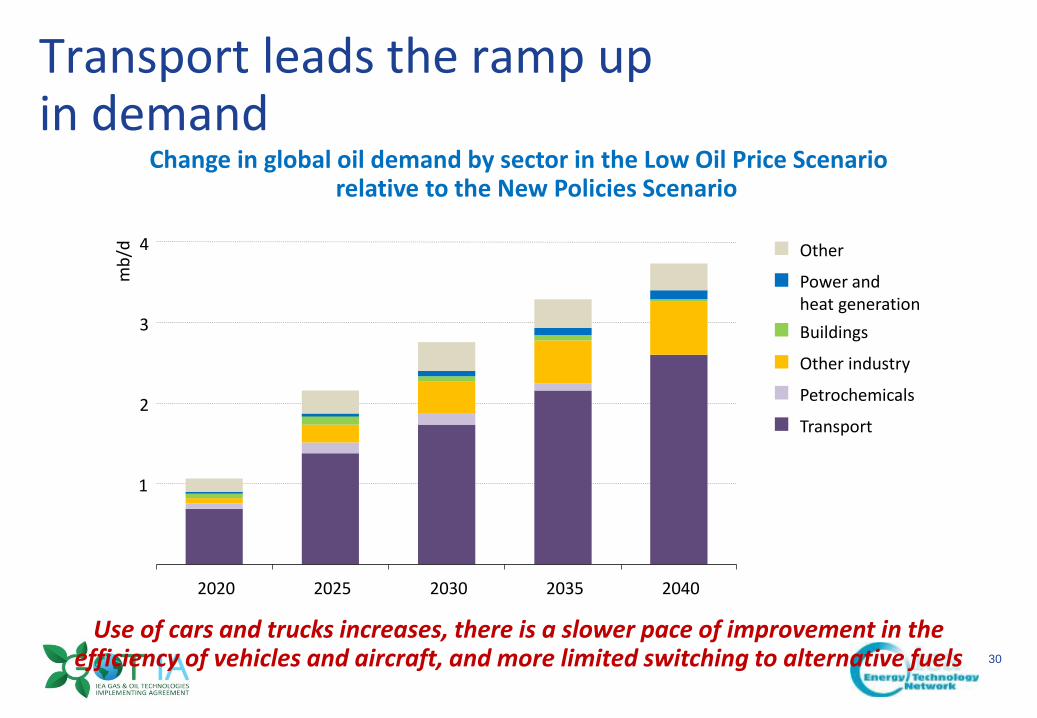

Transport leads the ramp upin demand

Change in global oil demand by sector in the Low Oil Price Scenariorelative to the New Policies Scenario

Use of cars and trucks increases, there is a slower pace of improvement in the efficiency of vehicles and aircraft, and more limited switching to alternative fuels

1

2

3

4

2020 2025 2030 2035 2040

mb/

d Other

Power andheat generationBuildings

Other industry

Petrochemicals

Transport

GE Confidential

31@#GECON&*

Mtoe

-300

0

300

600

900

1 200

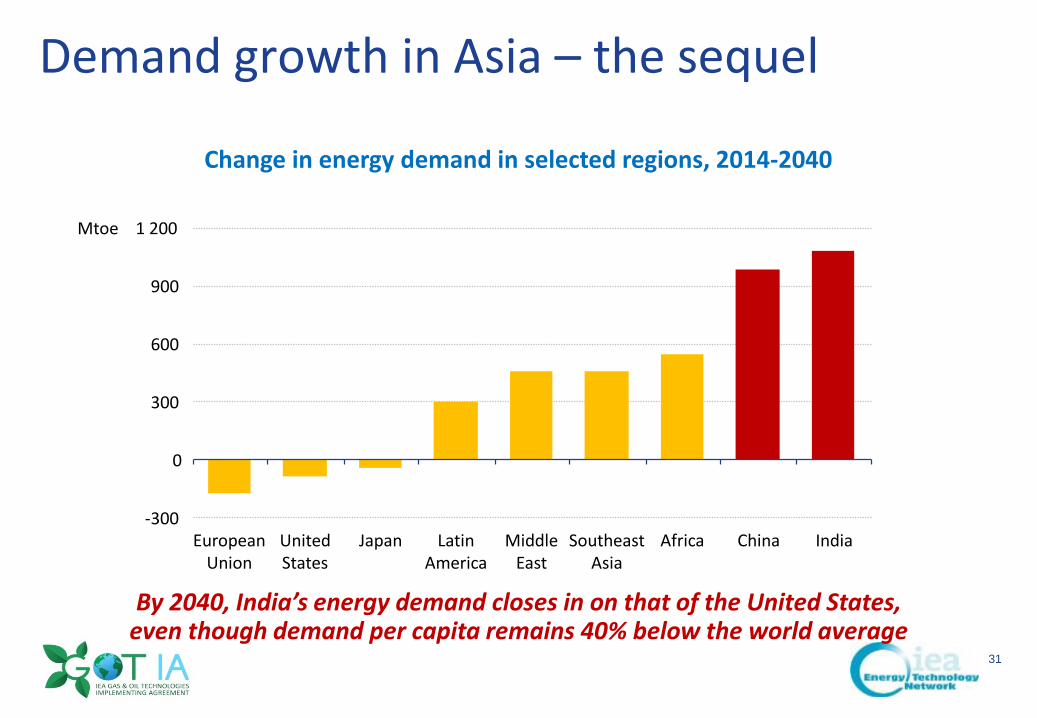

Demand growth in Asia – the sequel

By 2040, India’s energy demand closes in on that of the United States, even though demand per capita remains 40% below the world average

EuropeanUnion

UnitedStates

Japan LatinAmerica

MiddleEast

SoutheastAsia

Africa China India

Change in energy demand in selected regions, 2014-2040

GE Confidential

32@#GECON&*

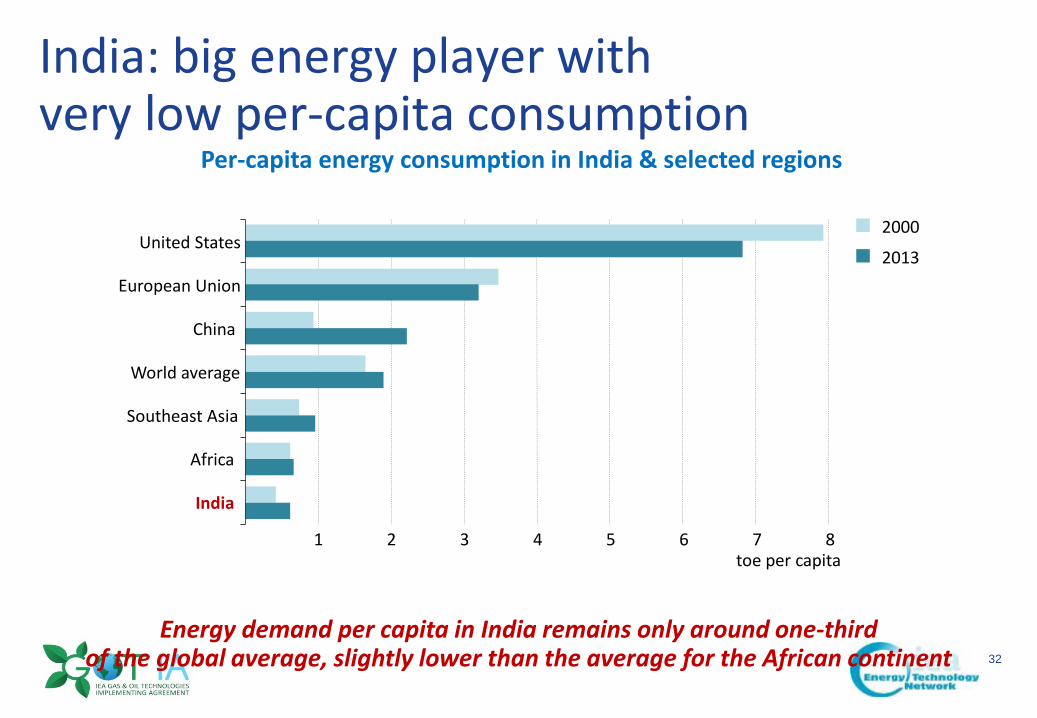

India: big energy player withvery low per-capita consumption

Per-capita energy consumption in India & selected regions

Energy demand per capita in India remains only around one-thirdof the global average, slightly lower than the average for the African continent

1 2 3 4 5 6 7 8

United States

European Union

China

World average

Southeast Asia

Africa

toe per capita

2000

2013

India

GE Confidential

33@#GECON&*

India’s CO2 emissions are on the rise

Energy-related CO2 emissions by selected country & region

Heavy reliance on coal leads to a large rise in India’s CO2 emissions; expressedon a per-capita basis, emissions remain some 20% below the world average in 2040

0.1

0.2

0.3

0.4

0.5

0.6

0 3 6 9 12 15 18Tonnes per capita

Tonn

espe

r tho

usan

d do

llars

of

GDP

($20

14, P

PP)

Bubble area

2 Gt

4 Gt

Russia

European Union

China

IndiaJapan

United States

Key2013

2040

GE Confidential

34@#GECON&*

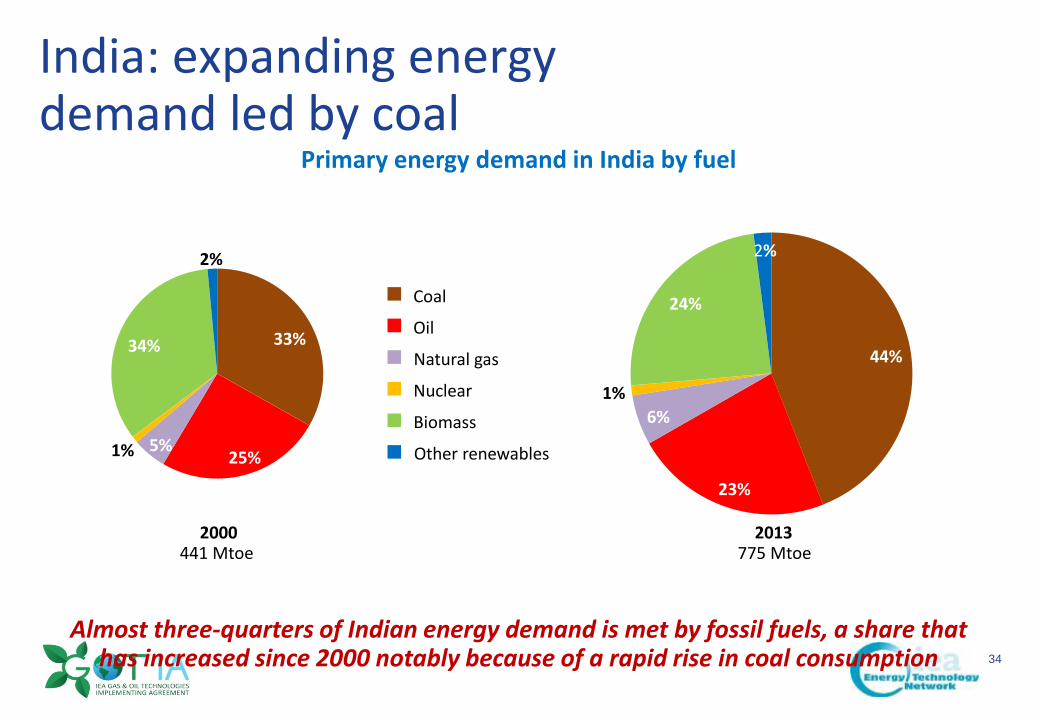

India: expanding energydemand led by coal

Primary energy demand in India by fuel

Almost three-quarters of Indian energy demand is met by fossil fuels, a share that has increased since 2000 notably because of a rapid rise in coal consumption

33%

25%5%1%

34%

2%

2000441 Mtoe

Coal

Oil

Natural gas

Nuclear

Biomass

Other renewables

44%

23%

6%1%

24%

2%

2013775 Mtoe

GE Confidential

35@#GECON&*

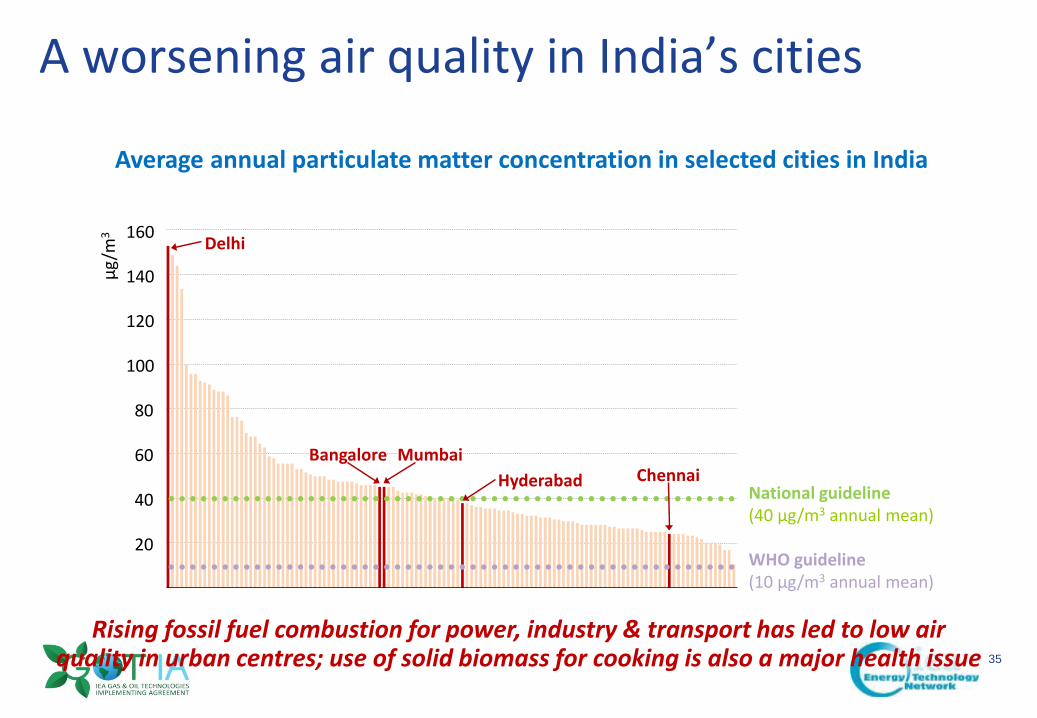

A worsening air quality in India’s cities

Average annual particulate matter concentration in selected cities in India

Rising fossil fuel combustion for power, industry & transport has led to low air quality in urban centres; use of solid biomass for cooking is also a major health issue

20

40

60

80

100

120

140

160

μg/m

3

HyderabadMumbai

ChennaiBangalore

National guideline(40 μg/m3 annual mean)

Delhi

WHO guideline(10 μg/m3 annual mean)

GE Confidential

36@#GECON&*

Role of Arctic Oil and Gas

GE Confidential

37@#GECON&*

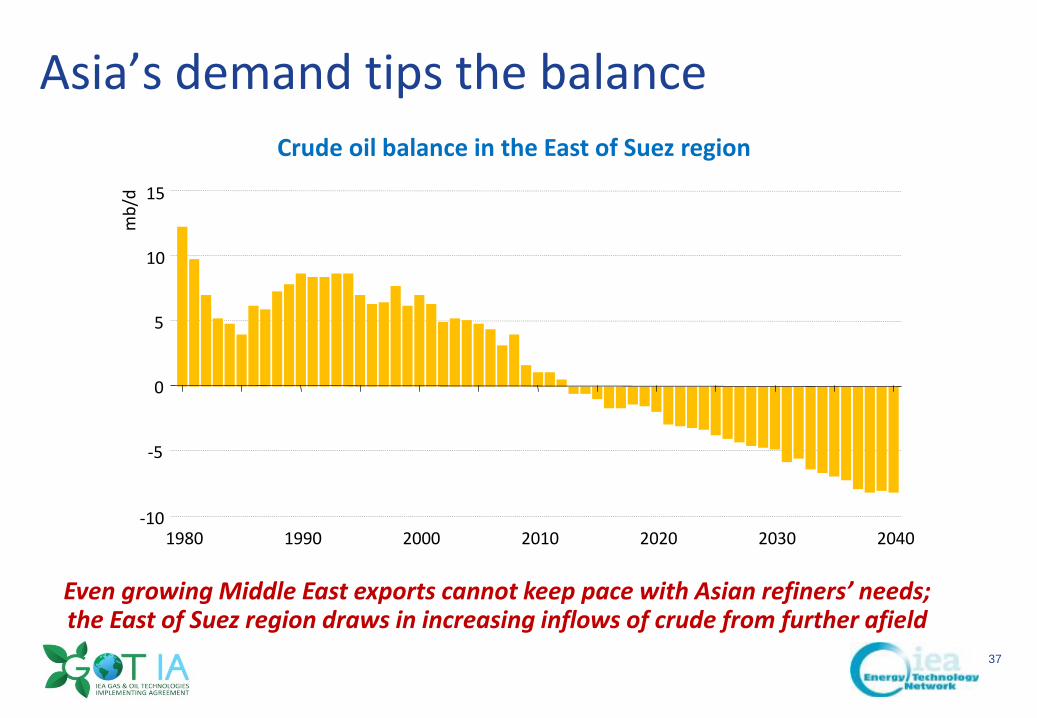

Asia’s demand tips the balanceCrude oil balance in the East of Suez region

Even growing Middle East exports cannot keep pace with Asian refiners’ needs; the East of Suez region draws in increasing inflows of crude from further afield

-10

-5

0

5

10

15

1980 1990 2000 2010 2020 2030 2040

mb/

d

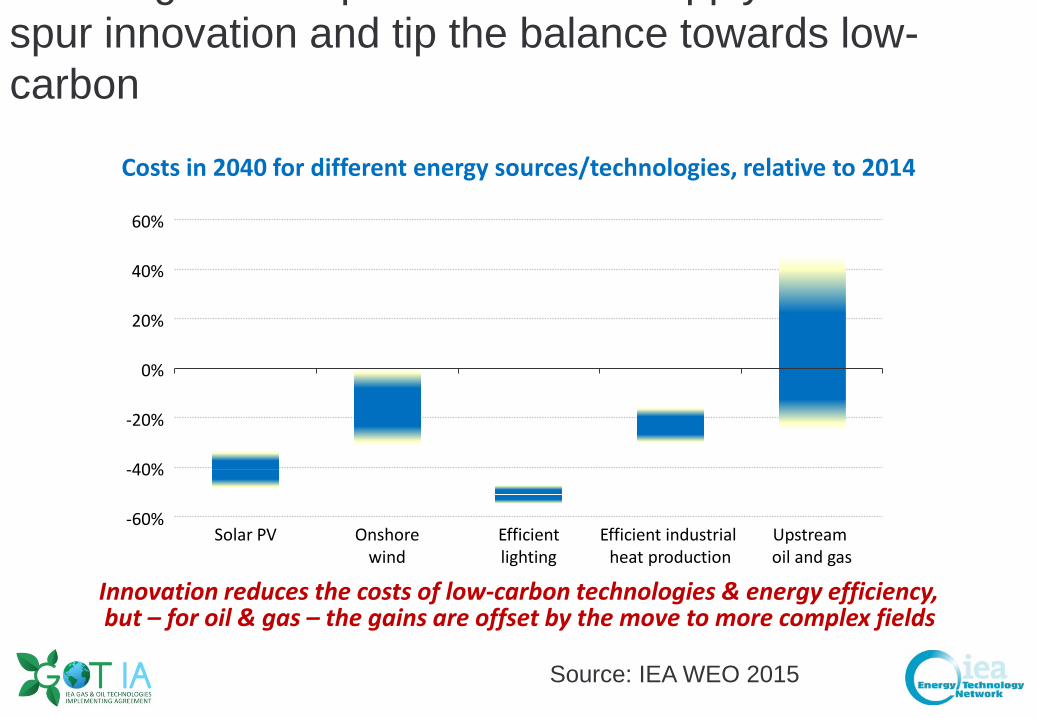

but – for oil & gas – the gains are offset by the move to more complex fields

g p pp y spur innovation and tip the balance towards low-carbon

Costs in 2040 for different energy sources/technologies, relative to 2014

-60%

-40%

-20%

0%

20%

40%

60%

Solar PV Onshorewind

Efficient industrial heat production

Efficientlighting

Upstream oil and gas

Innovation reduces the costs of low-carbon technologies & energy efficiency,

Source: IEA WEO 2015

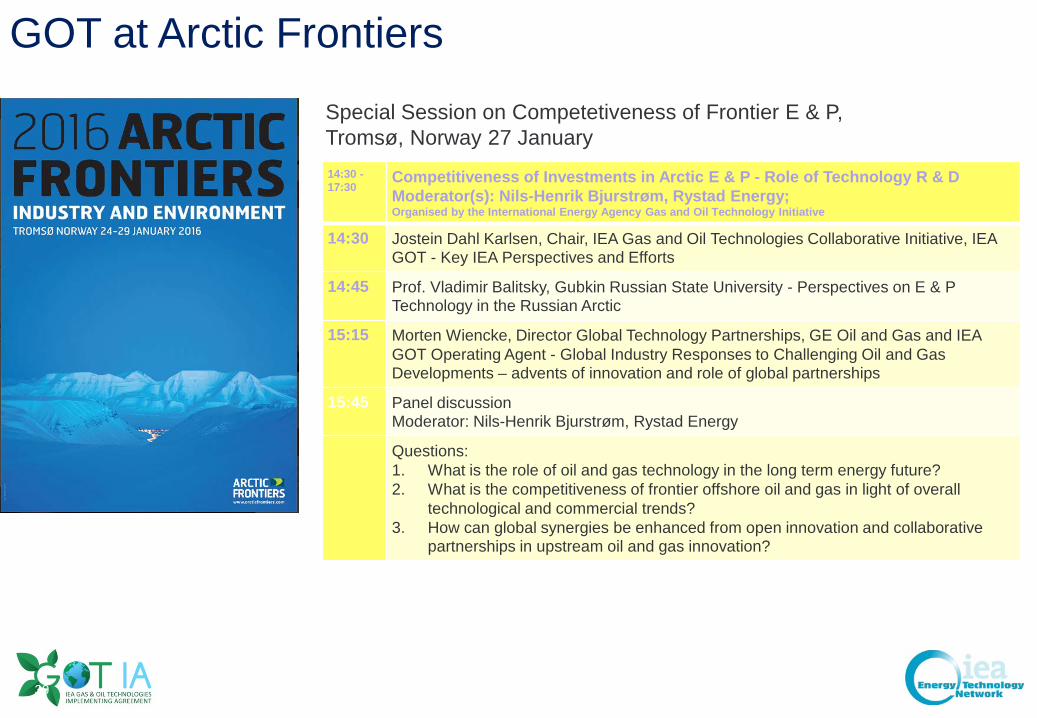

GOT at Arctic Frontiers

14:30 -17:30

Competitiveness of Investments in Arctic E & P - Role of Technology R & DModerator(s): Nils-Henrik Bjurstrøm, Rystad Energy;Organised by the International Energy Agency Gas and Oil Technology Initiative

14:30 Jostein Dahl Karlsen, Chair, IEA Gas and Oil Technologies Collaborative Initiative, IEA GOT - Key IEA Perspectives and Efforts

14:45 Prof. Vladimir Balitsky, Gubkin Russian State University - Perspectives on E & P Technology in the Russian Arctic

15:15 Morten Wiencke, Director Global Technology Partnerships, GE Oil and Gas and IEA GOT Operating Agent - Global Industry Responses to Challenging Oil and Gas Developments – advents of innovation and role of global partnerships

15:45 Panel discussionModerator: Nils-Henrik Bjurstrøm, Rystad Energy

Questions:1. What is the role of oil and gas technology in the long term energy future?2. What is the competitiveness of frontier offshore oil and gas in light of overall

technological and commercial trends?3. How can global synergies be enhanced from open innovation and collaborative

partnerships in upstream oil and gas innovation?

Special Session on Competetiveness of Frontier E & P, Tromsø, Norway 27 January

39

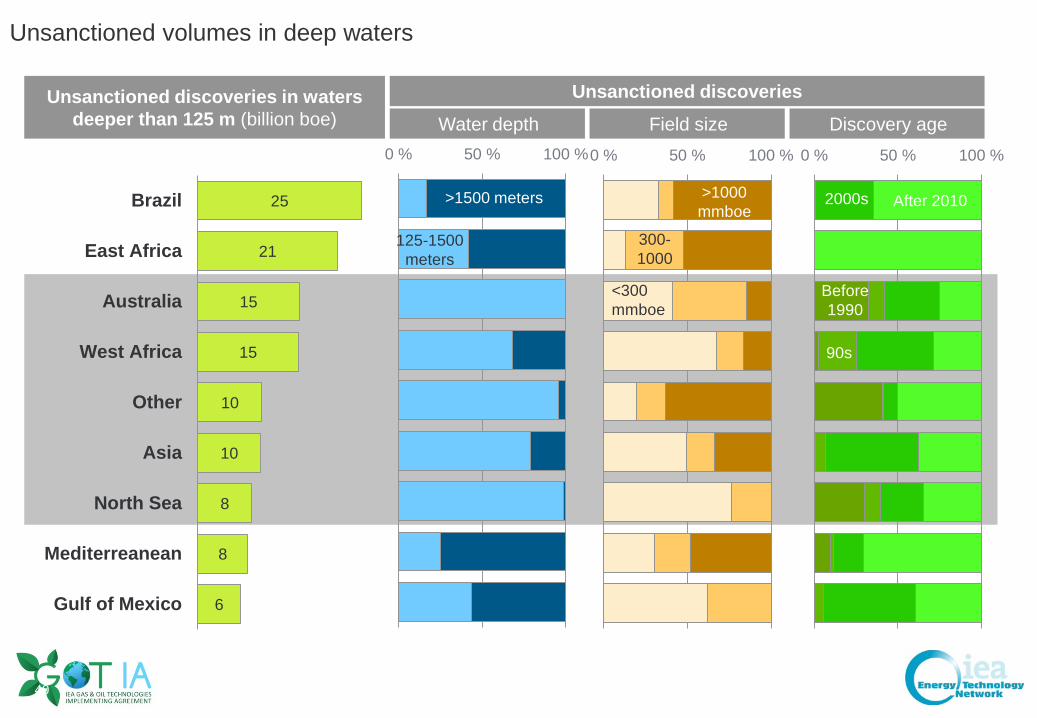

Unsanctioned volumes in deep waters

25

21

15

15

10

10

8

8

6

Brazil

East Africa

Australia

West Africa

Other

Asia

North Sea

Mediterreanean

Gulf of Mexico

Unsanctioned discoveries in waters deeper than 125 m (billion boe) Water depth

0 % 50 % 100 %0 % 50 % 100 % 0 % 50 % 100 %

Unsanctioned discoveriesField size Discovery age

>1500 meters

<300 mmboe

300-1000

>1000 mmboe

125-1500 meters

Before 1990

90s

2000s After 2010

40

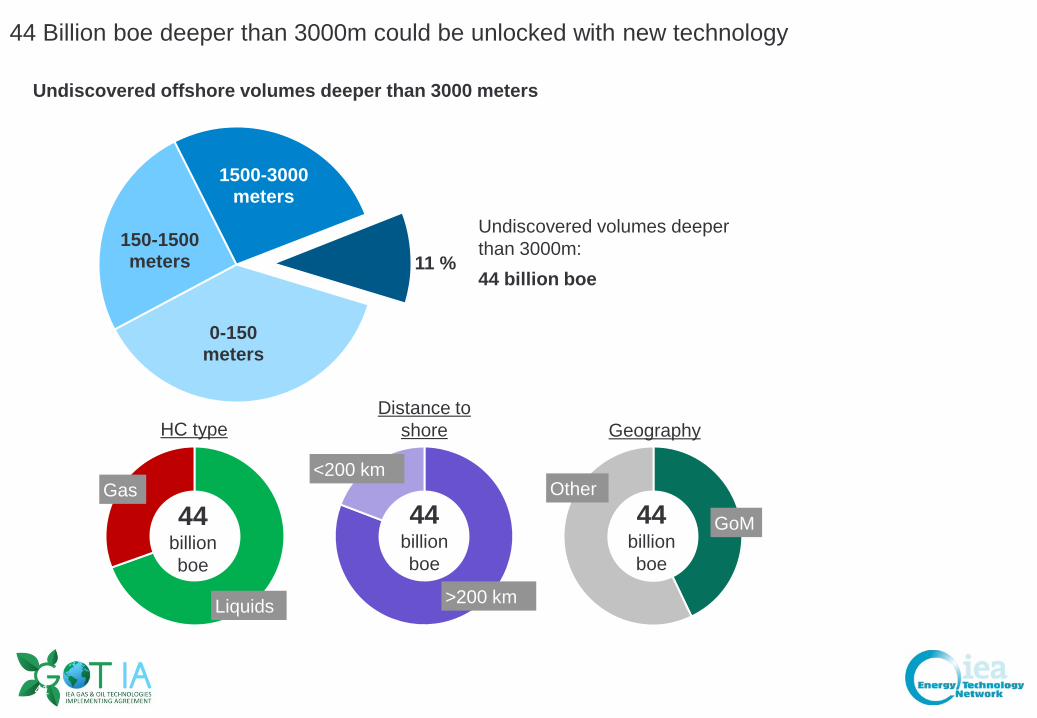

44 Billion boe deeper than 3000m could be unlocked with new technology

Undiscovered offshore volumes deeper than 3000 meters

0-150 meters

150-1500 meters

1500-3000 meters

11 %

Undiscovered volumes deeper than 3000m:44 billion boe

Liquids

Gas44

billion boe

>200 km

44billion boe

GoM

Other44

billion boe

HC typeDistance to

shore

<200 km

Geography

41

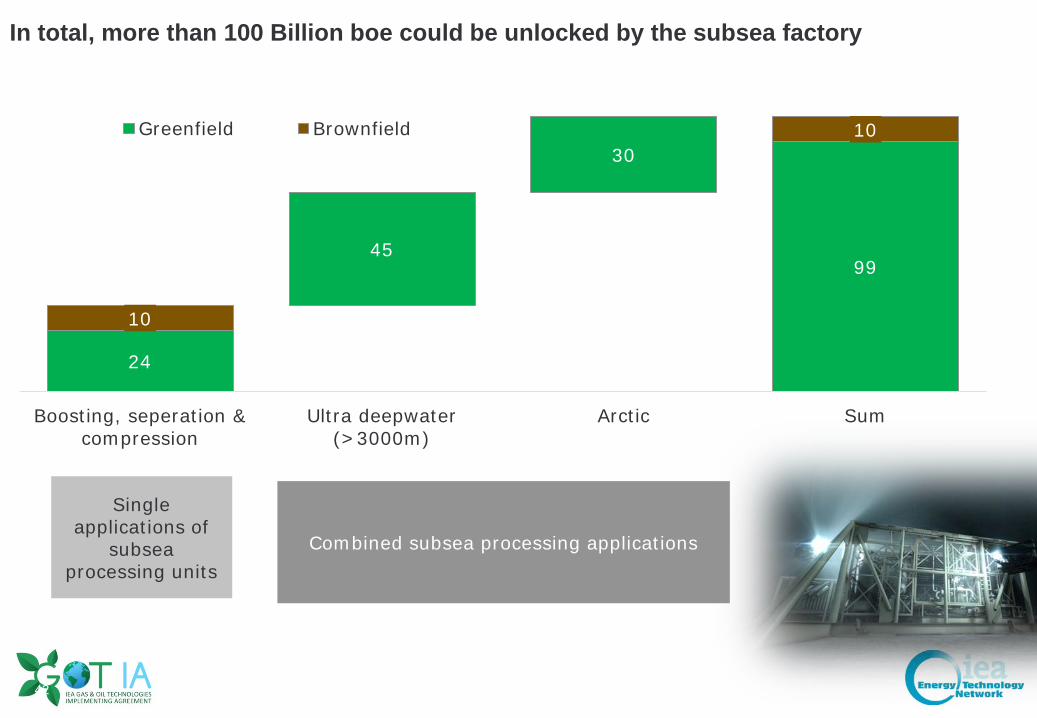

In total, more than 100 Billion boe could be unlocked by the subsea factory

24

45

30

99

10

10

Boosting, seperation &compression

Ultra deepwater(>3000m)

Arctic Sum

Greenfield Brownfield

Combined subsea processing applications

Single applications of

subsea processing units

42

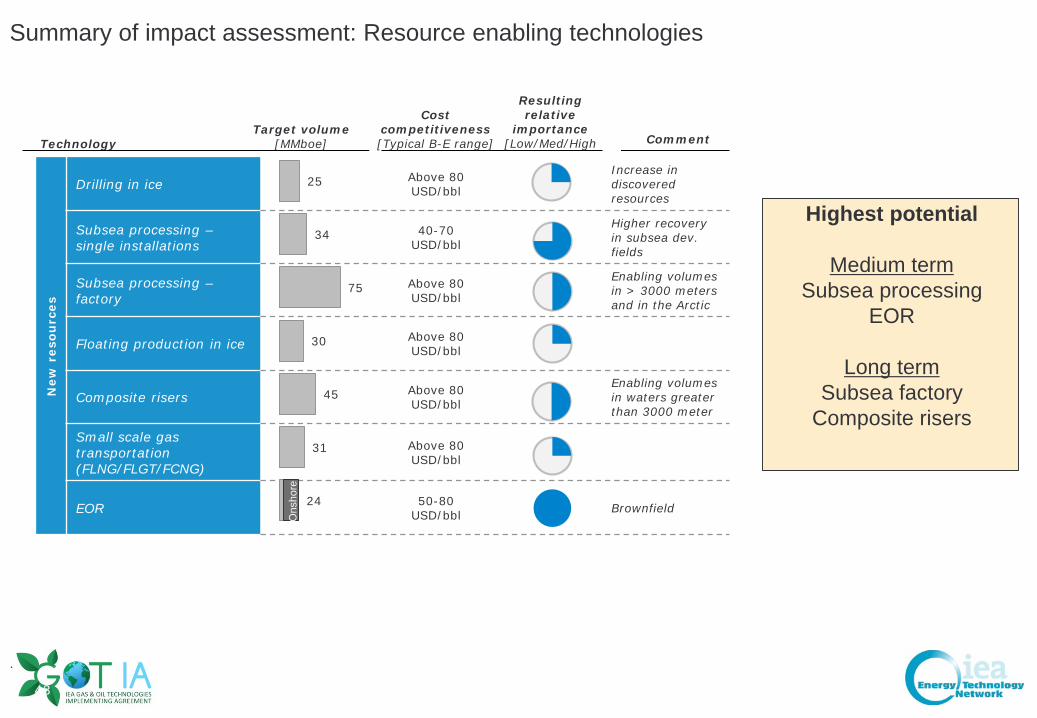

Summary of impact assessment: Resource enabling technologies

.

New

res

ourc

es

Drilling in ice Above 80 USD/bbl

Increase in discoveredresources

Subsea processing –single installations

40-70USD/bbl

Higher recovery in subsea dev. fields

Subsea processing –factory

Above 80 USD/bbl

Enabling volumes in > 3000 meters and in the Arctic

Floating production in ice Above 80 USD/bbl

Composite risers Above 80 USD/bbl

Enabling volumes in waters greater than 3000 meter

Small scale gas transportation (FLNG/FLGT/FCNG)

Above 80 USD/bbl

EOR 50-80USD/bbl Brownfield

25

34

75

30

45

31

24

TechnologyTarget volume

[MMboe]

Cost competitiveness[Typical B-E range]

Resulting relative

importance[Low/Med/High Comment

Ons

hore

Highest potential

Medium termSubsea processing

EOR

Long termSubsea factory

Composite risers

43

Back-up

44

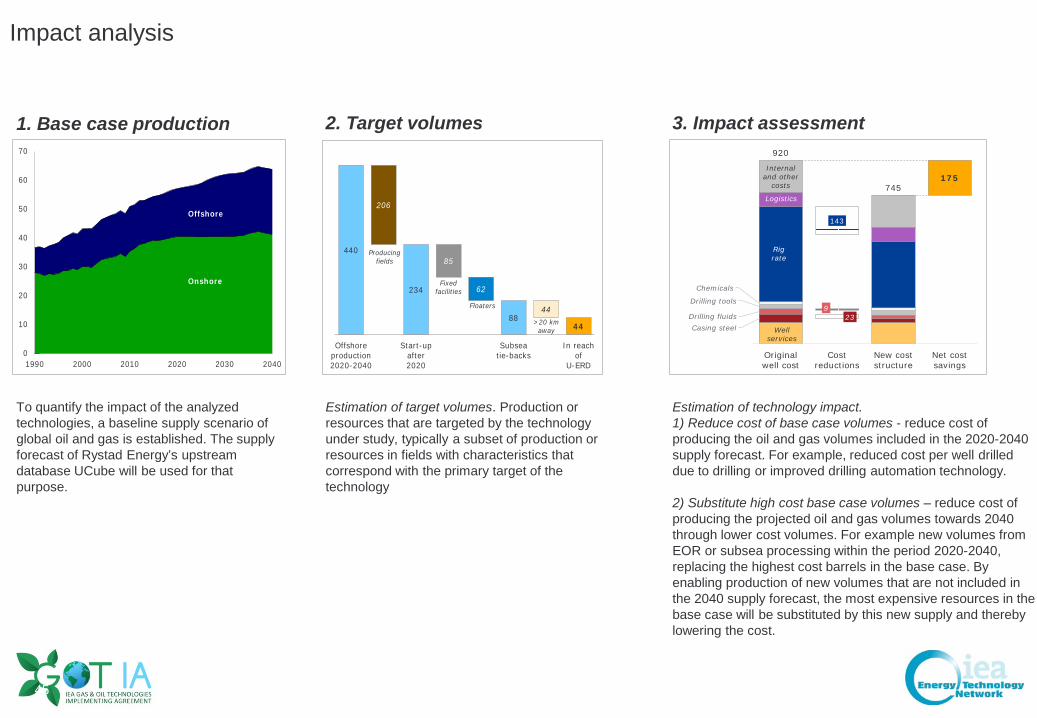

Impact analysis

0

10

20

30

40

50

60

70

1990 2000 2010 2020 2030 2040

Offshore

Onshore

1. Base case production

440

234

8844

206

85

62

44

Offshoreproduction2020-2040

Start-upafter2020

Subseatie-backs

In reachof

U-ERD

Fixedfacilities

>20 km away

Floaters

Producingfields

2. Target volumes

Estimation of target volumes. Production or resources that are targeted by the technology under study, typically a subset of production or resources in fields with characteristics that correspond with the primary target of the technology

Estimation of technology impact.1) Reduce cost of base case volumes - reduce cost of producing the oil and gas volumes included in the 2020-2040 supply forecast. For example, reduced cost per well drilled due to drilling or improved drilling automation technology.

2) Substitute high cost base case volumes – reduce cost of producing the projected oil and gas volumes towards 2040 through lower cost volumes. For example new volumes from EOR or subsea processing within the period 2020-2040, replacing the highest cost barrels in the base case. By enabling production of new volumes that are not included in the 2040 supply forecast, the most expensive resources in the base case will be substituted by this new supply and thereby lowering the cost.

Casing steel23Drilling fluids

9Drilling tools

Chemicals

143

175

920

745

Originalwell cost

Costreductions

New coststructure

Net costsavings

Well services

Rig rate

Logistics

Internaland other

costs

3. Impact assessment

To quantify the impact of the analyzed technologies, a baseline supply scenario of global oil and gas is established. The supply forecast of Rystad Energy’s upstream database UCube will be used for that purpose.

45

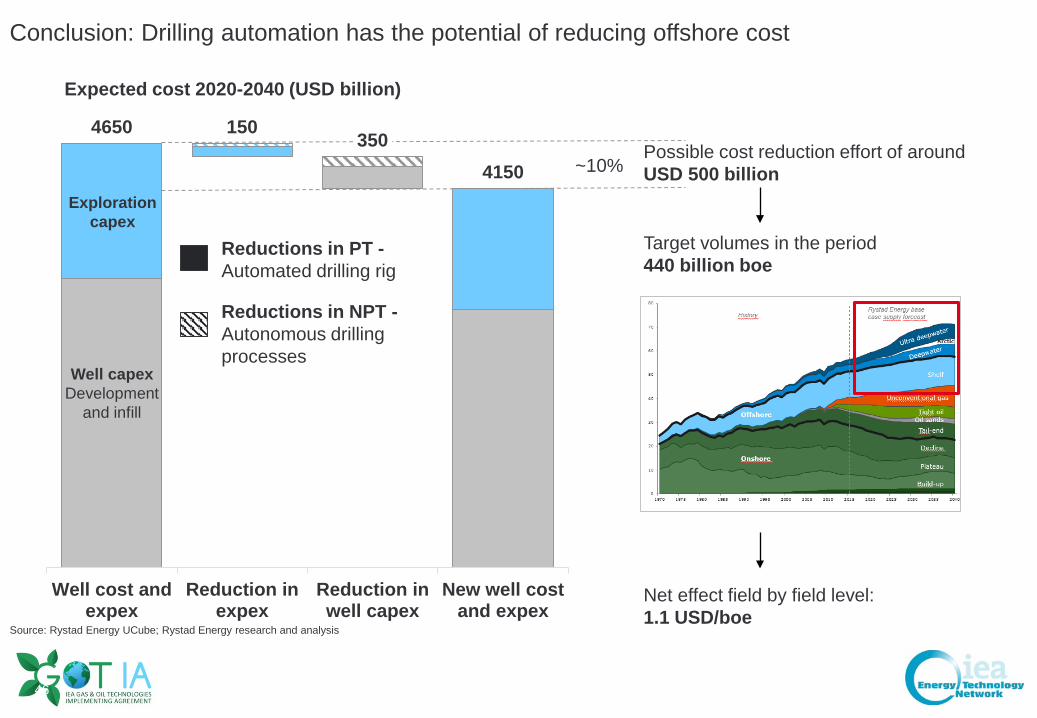

Conclusion: Drilling automation has the potential of reducing offshore cost

4650 150 3504150

Well cost andexpex

Reduction inexpex

Reduction inwell capex

New well costand expex

Source: Rystad Energy UCube; Rystad Energy research and analysis

Exploration capex

Well capexDevelopment

and infill

Possible cost reduction effort of around USD 500 billion

Target volumes in the period440 billion boe

Net effect field by field level: 1.1 USD/boe

Reductions in PT -Automated drilling rig

Reductions in NPT -Autonomous drilling processes

Expected cost 2020-2040 (USD billion)

~10%

46

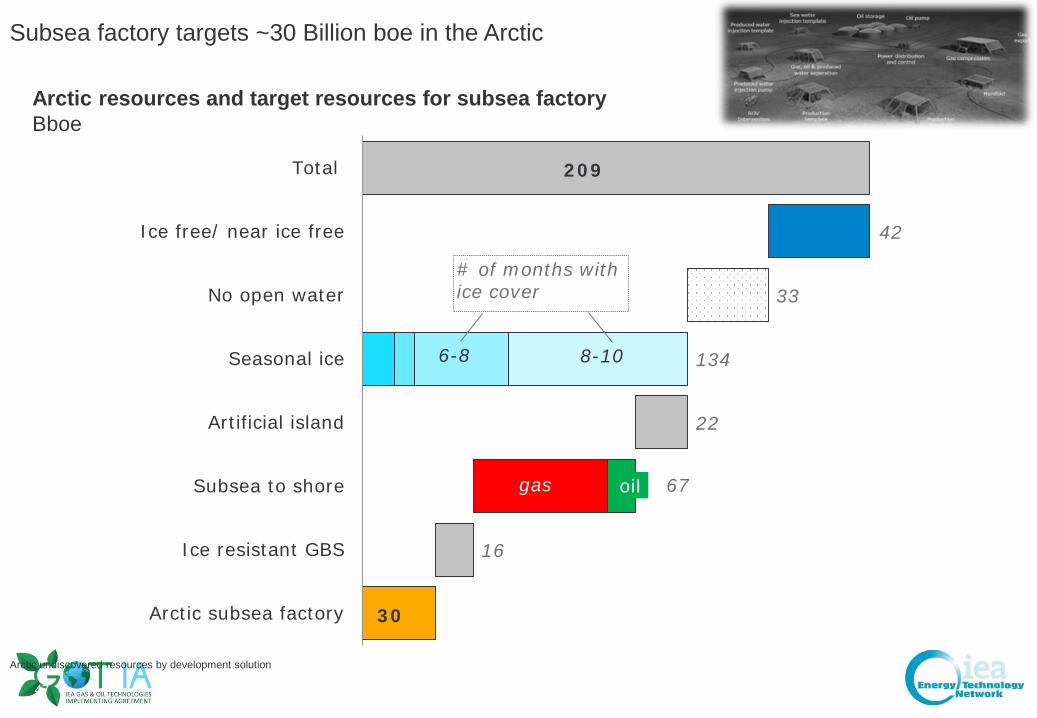

Subsea factory targets ~30 Billion boe in the Arctic

Arctic undiscovered resources by development solution

30

16

67

22

134

33

42

209

Arctic subsea factory

Ice resistant GBS

Subsea to shore

Artificial island

Seasonal ice

No open water

Ice free/ near ice free

Total

# of months with ice cover

8-106-8

gas oil

Arctic resources and target resources for subsea factoryBboe

47

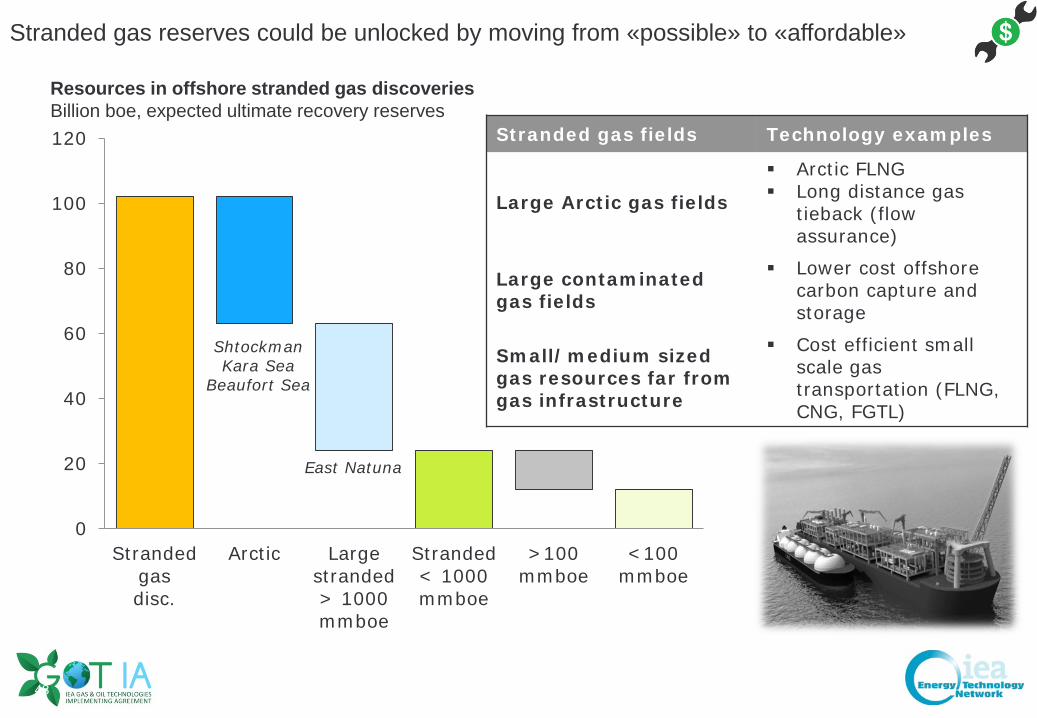

Stranded gas reserves could be unlocked by moving from «possible» to «affordable»

0

20

40

60

80

100

120

Strandedgasdisc.

Arctic Largestranded> 1000mmboe

Stranded< 1000mmboe

>100mmboe

<100mmboe

ShtockmanKara Sea

Beaufort Sea

Resources in offshore stranded gas discoveries Billion boe, expected ultimate recovery reserves

East Natuna

Stranded gas fields Technology examples

Large Arctic gas fields

Arctic FLNG Long distance gas

tieback (flow assurance)

Large contaminated gas fields

Lower cost offshore carbon capture and storage

Small/medium sized gas resources far from gas infrastructure

Cost efficient small scale gas transportation (FLNG, CNG, FGTL)

48

Back-up

49

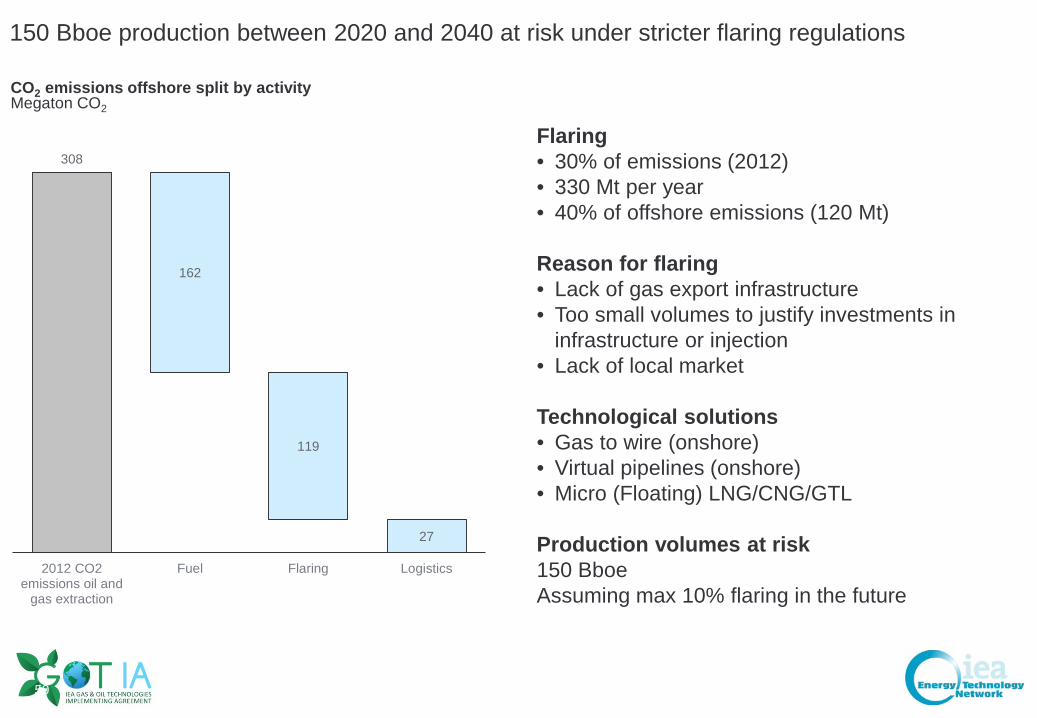

150 Bboe production between 2020 and 2040 at risk under stricter flaring regulations

CO2 emissions offshore split by activityMegaton CO2

162

119

27

308

2012 CO2emissions oil and

gas extraction

Fuel Flaring Logistics

Flaring• 30% of emissions (2012)• 330 Mt per year• 40% of offshore emissions (120 Mt)

Reason for flaring• Lack of gas export infrastructure• Too small volumes to justify investments in

infrastructure or injection• Lack of local market

Technological solutions• Gas to wire (onshore)• Virtual pipelines (onshore)• Micro (Floating) LNG/CNG/GTL

Production volumes at risk150 BboeAssuming max 10% flaring in the future

50

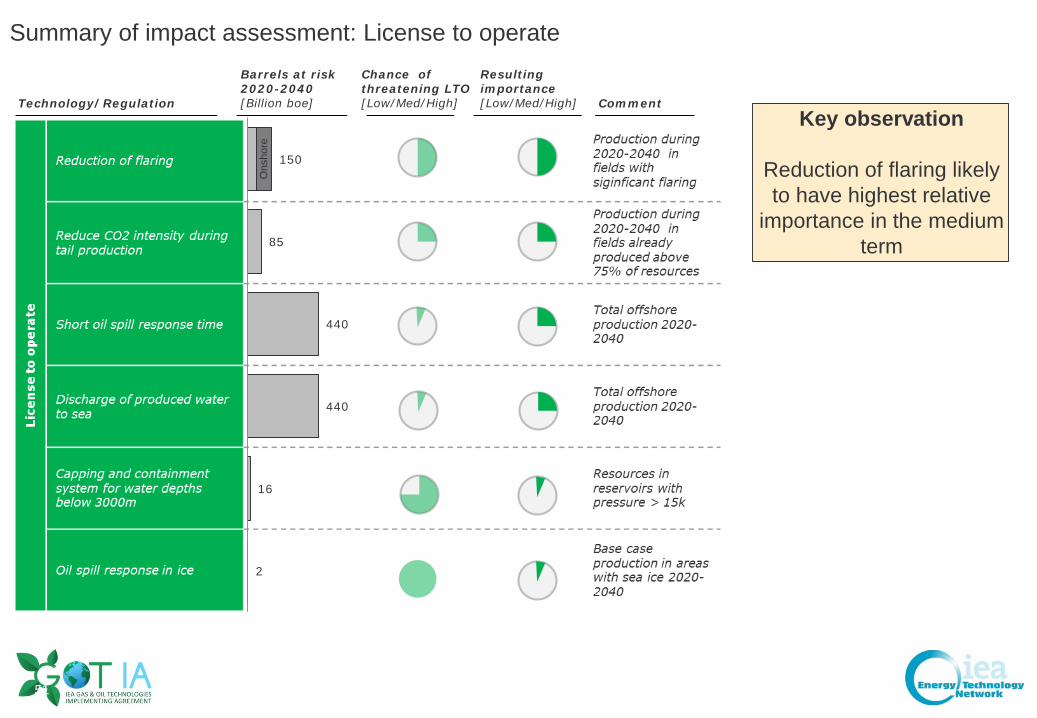

Summary of impact assessment: License to operate

Technology/Regulation

Barrels at risk 2020-2040[Billion boe]

Chance of threatening LTO[Low/Med/High]

Resultingimportance[Low/Med/High] Comment

150

85

440

440

16

2

Ons

hore

Key observation

Reduction of flaring likely to have highest relative

importance in the medium term

51