Embed Size (px)

Citation preview

IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005 15

Technology Competition and Optimal InvestmentTiming: A Real Options Perspective

Robert J. Kauffman and Xiaotong Li

Abstract—Companies often choose to defer irreversible invest-ments to maintain valuable managerial flexibility in an uncertainworld. For some technology-intensive projects, technology uncer-tainty plays a dominant role in affecting investment timing. Thisarticle analyzes the investment timing strategy for a firm that isdeciding about whether to adopt one or the other of two incompat-ible and competing technologies. We develop a continuous-time sto-chastic model that aids in the determination of optimal timing formanagerial adoption within the framework of real options theory.The model captures the elements of the decision-making processin such a way so as to provide managerial guidance in light of ex-pectations associated with future technology competition. The re-sults of this paper suggest that a technology adopter should deferits investment until one technology’s probability to win out in themarketplace and achieve critical mass reaches a critical threshold.The optimal timing strategy for adoption that we propose can alsobe used in markets that are subject to positive network feedback.Although network effects usually tend to make the market equilib-rium less stable and shorten the process of technology competition,we show why technology adopters may require more technologyuncertainties to be resolved before widespread adoption can occur.

Index Terms—Capital budgeting, decision analysis, investmenttiming, network externalities, option pricing, real options, sto-chastic processes, technology adoption.

I. INTRODUCTION

THE RECENTLY unprecedented development of new tech-nological innovations has yielded many investment oppor-

tunities for firms. However, such innovations are usually asso-ciated with significant uncertainties that derive from the natureof the technology itself, the consistency of investor perceptionsabout the quality of its solution capabilities, and competitionthat is occurring in the market around similar kinds of innova-tions. As a result, adopting the right technology at the right timebecomes a challenging issue that many managers must face headon, if they are to achieve effective decisionmaking on behalf oftheir firms. In this paper, we propose a new model based on thetheory of real options that is intended to provide senior man-agers with a tool to address this issue in a manner that balanceseffective managerial intuition with a depth of insight that is onlypossible with the application of rigorous methods. At the coreof our perspective—and the theory of real options, in a larger

Manuscript received November 1, 2003; revised June 1, 2004. Review of thismanuscript was arranged by Department Editor R. Sabherwal.

R. J. Kauffman is with Information and Decision Sciences, ManagementInformation Systems (MIS) Research Center, Carlson School of Manage-ment, University of Minnesota, Minneapolis, MN 55455 USA (e-mail:[email protected]).

X. Li is with Management Information Systems, Department of Accountingand Management Information Systems, University of Alabama, Huntsville, AL35899 USA (e-mail: [email protected]).

Digital Object Identifier 10.1109/TEM.2004.839962

sense—is the idea that every successful business manager mustunderstand the fundamental tradeoff between risk and reward[2], [7]. Recent efforts have been made to understand poten-tial benefits associated with real options in multiple informa-tion systems (IS) contexts, including software development andenterprise systems module adoption [71], [72], banking IT in-frastructures [62], software development project portfolios [9],and decision support systems [48]. All these papers, however,deal with investment evaluation problems in the absence of tech-nology competition.

A. Investment Decisions for Competing Technologies

Very often, however, senior managers must consider whetherand when to adopt one of two incompatible competing technolo-gies. Leading examples in our time include Sun Microsystems’Java and J2EE software development environment versus theVisual Basic, Visual Studio and the Net development envi-ronments of Microsoft. In addition, there are many cases ofintratechnology competition in which somewhat different, andsomewhat compatible technologies compete within a tech-nology standard [14], increasing the anxiety of the marketplaceas to how fast it will shift to embrace the new technologicalinnovations. We need look no farther than recent developmentsaround the IEEE standards for Wi-Fi fixed location wirelesscomputing. Although many hardware and software vendorshave been working to create compliant products for the 802.11bstandard, the market has recently been shaken up by indicationsthat the 802.11g standard offers faster throughput and greatereffective range.

A typical technology investment project requires a significantinitial outlay of capital and is generally either partially or whollyirreversible. In addition, technology investment projects usuallybear significant business and technological uncertainties, espe-cially in terms of the variance of future cash flows. Moreover,it is typical that some of the uncertainties will be resolved astime passes, changing future period expected values to futureperiod realized values. The “surprise value” of this informationthat is revealed to a decisionmaker in the future has the poten-tial to change the perceived value of a project and to shift thesentiments that senior managers express about willingness toinvest [24].

B. Real Options and Technology Adoption

The characteristics that we have just described—riskexpressed in variance terms, and the value of new informa-tion—make the financial economic theory of real options anappropriate theoretical perspective for evaluating technologyinvestment projects under uncertainty and risk [10]. For ex-ample, some authors have recently written that the theory of

0018-9391/$20.00 © 2005 IEEE

16 IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005

real options has the potential to play a role in the assessmentof technology investments, business strategies and strategicalliances in the highly uncertain and technology-driven digitaleconomy [11], [12], [34], [48]. Although other authors havewritten about some of the shortcomings of applying real optioninvestment evaluation methods [70], its advantages over othercapital budgeting methods [such as static discounted cashflow or distributed coordination function (DCF) analysis] havebeen widely recognized for the analysis of strategic investmentdecisions under uncertainty [1], [53], [54], [73]. (For readerswho are not familiar with the real options theory, we provide abrief and nontechnical introduction in Appendix A.)

Although option pricing theory has been extended beyond theevaluation of financial instruments, it is important that we cau-tion the reader to recognize that there are some technical issueslurking just below the surface of the intuition that deserve ourcomment. First, option pricing theory is founded on the markettradability of the asset on which the option has been created.Unfortunately though, most knowledgeable observers and op-tion pricing theorists will point out that technology investmentprojects are not subject to the valuation of the market. Moreover,technology projects are often specific assets for the firms thatinvest in them, and as a result, it is unlikely that another iden-tical project would ever be available in the market on which tobase a comparison. In financial economics terms and to complywith the requirements of the underlying theory—senior man-agers who wish to find a traded portfolio that can completely du-plicate the risk characteristics of the underlying nontraded assetare likely to be frustrated. Without this twin security, as it isoften referred to in the literature, risk-neutral valuation is diffi-cult to justify [67], [68]. The result is that the standard “methodstoolkit” for option pricing may be inappropriate to apply.

Second, the business value of a potential investment projectis assumed to follow a symmetric stochastic process. The sto-chastic process that is most commonly used in real option anal-ysis is geometric Brownian motion, as illustrated in [57], butmodels that incorporate the Brownian geometric motion sto-chastic process assume that there are no competitive impactson the cash flows and future payoffs of the project. The essenceof the concern is the possibility of competition affecting a tech-nology project investment’s future cash flows. Why? Becausecompetition is likely to cause the distribution of future projectvalues to become asymmetric: higher project values are lesslikely to occur because of the potential competitive erosion ofvalue (e.g., [64]).

As Kulatilaka and Perotti [45] and other business innovatorshave pointed out, the benefits of early preemptive investmentmay strategically dominate the benefits of waiting when thecompetition is very intense. These problems associated with tra-ditional real option modeling motivate us to model technologyinvestments from a new perspective. Instead of stochasticallymodeling the investment project value—as might be the case fortraditional assessment of technology projects using real optionmethods—our insight is that the standard Brownian motion canbe used to directly model the technology competition process.Like Grenadier and Weiss [31], our paper uses the first passagetime of a stochastic process to characterize a random time inthe future. The first passage time is a technical term frequentlyused in stochastic analysis. It is the first time for a Brownian mo-

tion to reach a predetermined threshold. See Domine [23] andRoss [63] for its statistical properties. Grenadier and Weiss [31]use the first passage time of a geometric Brownian motion tocharacterize the random arrival time of a future innovation. Ourpaper uses the first passage time of a standard Brownian mo-tion to characterize the random time at which one technologywins the competition. The appropriateness of this modeling ap-proach depends on whether each state of the stochastic processcan be easily and precisely interpreted. In Grenadier and Weiss[31], each state of the stochastic process corresponds to a cer-tain expected arrival time of the future innovation. Here, eachstate of the stochastic process corresponds to a certain expectedprobability for a technology to win the competition. Therefore,the Brownian motion used in our model can be linked to de-cisionmakers’ expectations of the outcome of the technologycompetition.

C. Process View of Technology Competition

To effectively make our general argument about the appro-priateness of representing the competitive process that occursaround a technology investment project, we first bring intoclearer focus what we mean by the “typical process” of tech-nology competition. Grenadier and Weiss [31] present a modelto describe the IT investment behavior of a company facingsequential technology innovation. In their model, they identifyfour potential technology migration strategies:

• compulsive strategy: purchasing every innovation;• leapfrog strategy: skipping the earliest version, but

adopting the next generation of an innovation;• buy-and-hold strategy: only purchasing the early

innovation;• laggard strategy: waiting for the arrival of new innovation

and then buying the previous innovation.Using the option pricing approach, they give an analytical

solution from which the probability for a company to pursueany of the four strategies can be derived. In today’s dynamicbusiness environment, the process of technology developmentis usually both parallel and serial. Therefore, investors not onlycare about serial technology migration, but also about the kindof parallel technology competition that is our focus here. Wenote four basic elements of the process of technology competi-tion that may affect the real option valuation of technology in-vestment projects. They include the following.

• Problem identification. An important business problemthat the firm faces is identified and new technology solu-tions are sought to solve it.

• Proposed technology solutions. Technology developersand vendors make proposals to the firm for differentapproaches that they believe will solve the problem.

• Solution testing and comparison. The firm observes dif-ferent technologies competing in the market and managersevaluate and test their effectiveness and draw conclusionsbased on the appropriate comparisons.

• Technology standardization. Over time, the marketplacewill reveal which technology or technology solution is thebest. As a result, one can expect to see the application ofthe technology to solve the problem to become increas-ingly standardized.

KAUFFMAN AND LI: TECHNOLOGY COMPETITION AND OPTIMAL INVESTMENT TIMING: A REAL OPTIONS PERSPECTIVE 17

As a company plans a technology investment when a two-technology standards battle is present, it usually will face twoquestions. Which technology is likely to eventually win the stan-dards battle? How long will it take for the technology compe-tition process to end? We will show why the answers to thesetwo related questions play important roles in a firm’s technologyinvestment decisionmaking. More specifically, our model sug-gests that a firm should defer technology adoption and let someof the relevant uncertainties in the world be resolved beforethe technology competition process reaches an investment via-bility threshold. We will shortly lay out the characteristics ofthis threshold. The managerial guidance that we offer is thatfirm should adopt a technology immediately if the current stateof technology competition reaches this threshold. We also con-sider the drivers of competition that affect the market’s abilityto permit this threshold to be reached.

Although our greater focus is on the competition betweenincompatible technologies, we also address the more generalissue of compatibility. We will demonstrate how significantswitching costs and possible technology lock-in may givetechnology adopters the incentive to wait. Our approach tounderstanding this problem is especially accommodating ofscenarios under which strong network effects exist. It turnsout, based on our modeling efforts to develop this theory,that strong network feedback has the potential to shorten thetechnology competition process by increasing the observedvolatility of adopter preferences. The reason why technologyadopters usually will act much more quickly in the presence ofstrong network externalities is not because that they can toleratethe greater uncertainty. Instead, the self-reinforcing networkfeedback effects make technology adopters’ expectations reachthe optimal threshold more quickly.

D. Plan of this Paper

The rest of this paper is structured to communicate the anal-ysis details of the story behind this theory-based interpretation,and to provide an effective basis for the acceptance of the waysthat we will use the theory of real options to create a new evalua-tive methodology. In Section II, we begin with a formal presen-tation of an option-based investment timing model, and showhow we reach a closed-form analytical solution. In Section III,we show the linear relationship between investors’ expectationsand the optimal timing solution generated by our investmentviability proposition. We also explore the roles of technologyswitching costs and network effects in affecting technology in-vestors’ decisions. In Section IV, we present the results of nu-merical analyses and simulations that are aimed at showing therobustness of our modeling approach. Section V concludes thepaper with a discussion of the primary findings and some con-sideration of the next steps in developing this stream of research.

II. REAL OPTIONS MODEL FOR ADOPTING

OF COMPETING TECHNOLOGIES

We next discuss the setup of an option valuation model forthe adoption of competing technologies. The model is designedto capture the technology competition that leads to an estab-lished technological standard as a stochastic process, whosedrift over time presents technology evaluation issues that can be

addressed via the specification of a real option pricing model.Our modeling choices permit us to assess the appropriatetiming for adoption, based on the use of a ratio metric thathelps a firm to know whether it has reached a threshold beyondwhich investment deferral no longer makes sense. (For ease ofreading, our modeling development, we include the modelingnotation and construct definitions in Table I.)

A. Modeling Preliminaries

Consider a risk-neutral firm that faces a technology invest-ment opportunity. Setting aside the potential outcome of tech-nology competition for a moment, we will assume that the ex-pected payoff of the technology investment project is a pos-itive constant as of the time the technology investment ismade. To implement the technology project, the firm must adoptone of two competing technologies, called Technology andTechnology . We use a standard Brownian motion with

to characterize the dynamics of competition betweenTechnology and Technology . The continuous-time sto-chastic process denotes the state of technology competi-tion and is the variance parameter that affects the volatility of

. In , is a Wiener increment that has two prop-erties: 1) with drawn from the normal distribution

and 2) for all .1

In many continuous-time real options models (e.g., [13],[57]), deterministic drift parameters are included, in additionto the stochastic parameter. Most of these models use geo-metric Brownian motions to model investment project valuesthat stochastically increase over time. The drift term is usedto characterize the deterministic part of the value increment,and the Wiener process (standard Brownian motion) is usedto characterize the stochastic project value increment. Unlikethese studies, we use Brownian motion to model the technologycompetition process, instead of the investment project value.Therefore, our model does not need the drift term to quantifythe instantaneous project value increment. All it needs is theWiener increment (standard Brownian motion) that character-izes the uncertainties surrounding the technology competitionprocess.2

After a random time , one of the two technologies andwill prevail and become the standard solution. To model the

time at which the standard emerges, we use an upper boundaryand a lower boundary with .

The technology competition will finish and one technology willemerge as the standard solution when the stochastic technology

1Two problems arise when Brownian motion is used to model technologycompetition. First, it is appropriate to question whether a typical technologycompetition process meets the mathematical conditions that define Brownianmotion. Second, it is hard to find managerially observable variables that can beused to represent a technology competition process. So, it is may be difficult tointerpret the results of the model. To solve these problems, we will provide aproof that there is a linear mapping between each Brownian motion state andthe probability that a technology will become a standard.

2A standard Brownian motion without the drift term is a martingale. Themartingale property is well known in financial economics related to the in-formational efficiency of stock prices [50]. Adding the drift term destroys theproperty. However, the law of iterated expectations implies that well-behavedexpectations should possess the martingale property. Therefore, we intention-ally suppressed the drift term to preserve the martingale property, which allowsus to interpret our analytical results in terms of decisionmakers’ expectations ofthe future technology competition.

18 IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005

TABLE IMODELING NOTATION AND CONSTRUCT DEFINITIONS

competition, , reaches either or . If the stochasticprocess, , reaches first, then Technology will dom-inate Technology to become the standard technology at time

. The result will be opposite if reaches first. So anincrease in will make Technology more likely to prevailin the market and a decrease in will make Technologyless likely to beat Technology in the competition.

The approach that we use to determine the uncertain tech-nology standardization time is similar to the modeling tech-nique used in Black and Cox [16], Leland [49], and Grenadierand Weiss [31]. The outcomes of the technology competitionwill affect the payoff of a technology investment project thatadopts either Technology or Technology . To quantify this,we assume that there is an exogenous gain in investment payoff

at time if the technology adopted becomes the standard. Ifthe solution adopted fails in the competition, then the value gainwill be 0. We also can assume that there is an exogenous valueloss in this case, but this assumption will not enhance the gen-erality of our model since we can easily adjust to normalizethis value loss to 0. It may be more helpful for the reader to thinkof as a bonus for adopting the “right” technology. The readershould also note that we assume that the switching costs be-tween the two incompatible technologies are prohibitively high.This technology lock-in situation gives the firm little flexibilityto switch once it has adopted one technology.

Let the cost of capital for the technology investment projectbe . Since we assumed that is constant over time, thefirm’s technology investment strategy is very simple if no con-sideration is given to the effect of technology competition be-tween and . The firm should invest immediately if

, and never invest otherwise. However, the decisionmaking

problem becomes more complicated when we consider the com-petitive dynamics that may occur between Technology andTechnology . The expected total payoff from the technologyinvestment with technology competition may be greater than thebaseline expected payoff . Why? Because the firm can gainif the technology solution it adopts wins the standards race attime . More importantly—and a factor that makes the theoryof real options especially relevant for our analysis, is that it maybe valuable to defer the investment to resolve the uncertaintysurrounding the two competing technologies.

To derive the firm’s optimal investment strategy, it is neces-sary to quantify the value of the options that are embedded in thetechnology investment opportunity. Before committing to theinvestment, the firm has an option to choose one of the two com-peting technologies. When it decides to invest, the firm exercisesits adoption option, selecting the technology that it believes tobe more promising. The expected investment payoff can be de-rived by dynamic optimization.

Let denote the expected value gain through the stan-dardization bonus if the company decides to invest, where isthe state of technology competition. So the expected investmentpayoff at is . Note that the company can adopteither or at the time of the investment. Let and

denote the expected value gain if the company decidesto adopt and at , respectively. For a rational risk-neutralcompany that always maximizes its expected investment payoff,we know that . So, to calculate theexpected investment payoff, we need to derive values forand .

We first derive . then can be found in a similarway. Since generates no interim cash flows when is

KAUFFMAN AND LI: TECHNOLOGY COMPETITION AND OPTIMAL INVESTMENT TIMING: A REAL OPTIONS PERSPECTIVE 19

between and , Bellman’s principle suggests that theinstantaneous return on should be equal to its expectedcapital gain. So must satisfy the equilibrium equation

.Expanding using Ito’s Lemma3 yields

. By plugging into thisequation, we obtain . Now,since , we can rewrite theequilibrium equation as

or simply.

In addition, must satisfy two boundary conditions atand and

. The first boundary condition says that the firm that adoptsTechnology will gain payoff when the state of technologycompetition, , reaches first, but if the state of technology,

, reaches first, then the firm will gain nothing. So thesolution to this second order differential equation is

, where

and

For , the solution will also satisfy the Bellman equilib-rium equation, but the two boundary conditions areand . The solution is

. Since is monotonically increasing inand , we can prove that

forfor

Since we know the expected investment payoff at the time ofinvestment, we are able to find the optimal timing to make theinvestment. There are both benefits and costs associated with theoption to defer the investment. Waiting will erode the expectedinvestment payoff in terms of its present value at time 0. How-ever, waiting longer will resolve more uncertainties about thecompetition between Technology and Technology .

Consider two extreme cases. In the first one, the firm investsat time 0. So it will maximize the present value of but facesuncertainties in the technology competition. In the other, thefirm waits until one of the two competing technologies becomesthe standard. At that time, the firm’s expected investment payoffwill be , but the waiting time also will erode this compositepayoff in terms of its present value at time 0. Therefore, theoptimal investment timing strategy must balance the benefitsand costs associated with investment deferral. One may guessthat a firm will invest at some threshold of . We prove thisin the first theorem.

Theorem 1—Optimal Investment Timing Strategy Theorem:There are two thresholds and , where .

3Ito’s Lemma is a well-known theorem in stochastic calculus that is used totake the derivatives of a stochastic process. Its primary result is that the secondorder differential terms of a Wiener process become deterministic when they areintegrated over time. The interested reader should see Merton [59] for additionaldetails.

Fig. 1. Symmetric payoffs from firm adoption with competing technologies.

Given , the firm will invest immediately if w isoutside of . Otherwise, it will defer the investmentuntil reaches either or . If reachesfirst, the firm will adopt Technology . If reachesfirst, it will adopt Technology .

(See Appendix B for the proof.) Fig. 1 depicts ,and the continuation region between the optiomal thresholds

and .We can this apply the optimal timing strategy analysis to sev-

eral special cases. When there is no gain associated with se-lecting the right technology , it turns out that .So there will be no need to defer the technology investment.Waiting in this case has a single impact: it decreases the presentvalue of the technology payoff, . When , however, wewill see that . In this case, will degrade to a con-stant and the optimal strategy for the firm will be to invest im-mediately in the technology project. More generally, the optimalstrategy suggests that the firm will be more willing to defer thetechnology investment when is getting smaller or is gettinglarger.

We also find that there is a critical ratio between and inProposition 1 that can guide investment decisionmaking. Thefirm will defer the technology investment until reaches

or when is greater than or equal to the criticalratio.

Proposition 1—Investment Deferral Tradeoff Threshold RatioProposition: There is a critical ratio, the investment deferraltradeoff threshold ratio , between and . If the ratio isgreater than or equal to , the optimal investment timing strategyis to defer the investment until one technology becomes the stan-dard. The optimal timing solution depends only on , andnot on the separate values of either or .

See the proof in Appendix B.The Investment Deferral Tradeoff Threshold Ratio Propo-

sition suggests that the adopting firm’s optimal investmentstrategy is to defer the investment until all of the relevant uncer-tainties associated with technology competition are resolved if

. In other words, the firm should defer the investment

20 IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005

until one technology becomes the standard, if the outcome ofthe standards battle appears likely to have a significant impacton the technology investment’s expected payoff. This propo-sition also says that the actual values of or are irrelevantto the timing decision as long as we know the ratio betweenand , which is intuitively plausible.

For the optimal investment thresholds found in our model, itis important to show how they are affected by the model param-eters. Because of the symmetry of our model, we only need toconduct a comparative static analysis on the positive threshold

. This leads to Proposition 2.Proposition 2—Comparative Statics Proposition: For a pos-

itive investment threshold , the following com-parative static results must hold: , ,

, , and .See Appendix B for this proof also.The results of the comparative static analysis are readily in-

terpreted. First, if the gain from adopting the right technologyis large compared to , the firm will wish to wait for more un-certainty to be resolved with respect to the technology. Second,because increases in and decreases in will tend to prolongthe technology competition process, the firm will tend to adoptsooner because the present value of will be smaller. Finally,increasing the discount rate will make waiting more costlyand, as a result, the firm will tend to shorten its time to adopt.4

We next interpret the results of our model from anotherperspective and demonstrate the significance of technologyadopters’ expectations in technology investment timing.

III. SWITCHING COSTS, ADOPTER EXPECTATIONS, AND

NETWORK EFFECTS

We next consider the problems of switching costs and lock-in,and the role of adopter expectations and network externalities intechnology adoption decisionmaking.

A. Switching Costs and Lock-In

An assumption that we make in this model is that theswitching costs between the two technologies are very high.Although this assumption may seem restrictive at first, sig-nificant switching costs are common in technology-intensiveindustries and often lead to a situation known as technologylock-in [26], [43], [74]. Based on the comparative statics results,we can relax this assumption and examine how decreases inswitching costs affect the optimal investment strategy [52]. Inour model, a decrease in switching costs will affect two param-eters. The switching costs will dwarf the uncertain exogenousvalue gain, , because firms that have adopted the nonstandardtechnology may later choose to switch to the standard one atthe expense of some switching costs. Also, the switching costsincrease the investment payoff because a part of becomescertain. Since the derivatives, and ,decrease in switching costs, this implies that waiting is lessattractive, but clearly, technology adopters are willing to waitbecause they are afraid of getting locked into the nonstandard

4All else equal, the expected time for w(t) to reach +w increases in w .So here we interpret the comparative statics results in terms of the expectedinvestment deferral time rather than the actual investment deferral time.

technology. Without proper coordination, significant switchingcosts may lead to Pareto-inferior equilibria, and possiblyunacceptably slow, inertial adoption. Consequently, sometechnology vendors may voluntarily promote open standardsor technology interoperability to reduce switching costs and toboost potential adopters’ confidence about the future benefitsstream from the technology.

B. Role of Expectations

As we mentioned earlier, one difficulty that managers willface in interpreting our model is that the Brownian motionprocess that represents the technology competitionprocess will be hard to define in practice. In Proposition 3, weshow that can be interpreted as the technology adopter’sexpectations of the outcome of the technology competition.

Proposition 3—Expected Technology Standard Proposition:At point , where , the probabilityfor Technology to defeat Technology and to become thefuture standard is given by . At thesame point in time , the probability for Technology to defeatTechnology and to become the future standard is given by

.The proof is omitted.5 This proposition basically says that

there is a linear mapping between each point of and theexpected probability for a technology to win the competition.This mathematic property, coupled with the martingale prop-erty of the Brownian motion, establishes a direct link betweeneach decisionmaker’s expectations and the technology compe-tition process defined in this paper. With knowledge of therelationship between and the firm’s expectations, we areable to provide a more precise interpretation of the Optimal In-vestment Timing Strategy Theorem.

The optimal timing strategy for the risk-neural firm is to deferthe technology investment until it expects that either Technology

or Technology will win the competition with a probabilityof . Rational decisionmakers will always adoptthe technology that is expected to have a higher probability towin. So if hits first, Technology is expected to winthe competition with a probability of .But if hits first, Technology ought to win with aprobability of . Note that and only dependon , and not on the separate values of either or . Thisinterpretation clearly indicates that the technology adopter’s ex-pectations of future technology competition outcomes play acrucial role in its investment timing decision.

An important question here is: How can managers observethe probability of one technology defeating the other? In busi-ness, decisionmakers cannot observe the state of the stochasticprocess directly. Instead, they must rely on their expectationsformed through adaptive learning. Therefore, managers whowant to apply our model need to rely on their subjective ex-pectations of the future technology competition. Similarly,Grenadier and Weiss [31] use a geometric Brownian motion todepict the technological progress. To interpret the stochastic

5The proposition directly follows from the fact that w(t) is a martingale. Formore details about the hitting probabilities of a martingale upon which the proofis based, we refer the interested reader to Durrett [25].

KAUFFMAN AND LI: TECHNOLOGY COMPETITION AND OPTIMAL INVESTMENT TIMING: A REAL OPTIONS PERSPECTIVE 21

process in their model, decisionmakers also need to rely on theirsubjective expectations to come up with a reasonable guess ofthe expected arrival time of the future innovation. The quality ofmanagers’ technology adoption decisions depends on how closetheir subjective expectations are from the “true” state, whichis generally unobservable. This is not a big problem for thosewho believe Muth’s [60] rational expectations theory (such asAu and Kauffman [4], which offers a first assessment of theuse of rational expectations theory related to IT adoption). Inthis theory, economic agents’ subjective expectations that areformed through adaptive learning should be informed predic-tions of future events. However, boundedly rational managersalso may sometimes form erroneous subjective expectationsthat may negatively affect the quality of their decisions. Indeed,in some cases, even rational decisionmakers have difficultiesin making informed predictions of future events because ofvarious informational or incentive problems [39].

As far as the technology vendors are concerned, their abilitiesto effectively manage their potential customers’ expectations arealso critical. A commonly used strategy in technology compe-tition is penetration pricing, where one technology vendor uni-laterally and aggressively cuts prices to gain market share orpreempt its competitors at an early stage in the technology com-petition. This strategy not only makes a firm’s technology moreattractive because of the lower price. The vendor also affectsother potential adopters’ expectations by showing its own deter-mination to win the standards battle. A similar strategy is sur-vival pricing, where a weak competitor cuts its product’s pricedefensively to escape a defeat in a battle involving standards.A survival strategy is hard to make work, according to Shapiroand Varian [65], because it negatively affects potential adopters’expectations by signaling the product’s weakness.

It is worth noting that our model does not analyze thetwo pricing strategies. Instead, our discussion of the strategicpricing issue serves two purposes. First, managers’ expectationsplay a significant role in technology adoption decisionmaking.The opposite effects of the two similar pricing strategies furtherunderscore the importance of potential adopters’ expectationsin technology competition. Second, technology pricing is anexample of many strategic issues of expectations managementin technology competition. Our discussion here aims to suggestthat many of these issues should be studied in general equi-librium models that consider the dynamic interaction betweenthe adopters and technology vendors. In fact, some recent realoptions studies advocate using real options games for generalequilibrium analyzes of firms’ investment strategies [32],[34], [66].

C. Technology Competition With Network Effects

We use continuous-time Brownian motion to directly modela technology adopter’s expectations that also are subject to con-tinuous changes. Although we have proved that expectations arelinear in , there is another question that we have not yetfully addressed. Is it appropriate to assume that the adopter’s ex-pectations can be characterized by Brownian motion? As longas the adopter’s expectations are rational and consistent, themartingale property of is justified by the law of iterated

expectations.6 Since only unpredictable new information canchange the adopter’s expectations, should have a memo-ryless property.

However, if we use to model some directly observablevariables like each technology’s market share, these two prop-erties are actually much harder to justify.7 One reason is thatmany technology competition processes are subject to positivenetwork feedback that makes a strong technology grow stronger[18], [38], [40]. Network effects stem from the efficiencies asso-ciated with a user base for compatible products. Consequently,the technology with a larger market share can be expected togain more market share from its competitor in our model. Butnote that this directly violates the martingale property and canresult in dependent increments (in lieu of memoryless incre-ments) of the market share. Although network effects do notundermine our modeling assumptions since we directly modeladopter’ expectations, their relationships with our model shouldnot be ignored.

In our model, network effects affect the technology adoptiondynamics through two channels: through the technology adopterand through the market. The externalities created by network ef-fects usually make it more beneficial to adopt the winning tech-nology. In our model, the investment threshold ratiocan become larger due to strong network effects. As a result,the optimal timing threshold will increase. According to ourcomparative static results, the technology adopter will requiremore certainty about the outcome of the standards battle be-fore making an investment decision. This effect requires that thetechnology adopter be more patient and wait longer to let moreuncertainties in the market be resolved.

But strong network effects usually also result in “tippy” mar-kets that can significantly shorten the technology competitionprocess. In markets subject to strong network externalities, anymarket equilibrium will be highly unstable and the expectedwinning technology may be able to obtain a commandingmarket share even in a very short period of time [27], [28]. Wehave recently seen this occur with some of the new wirelesstechnologies and instant messaging services [39]. So networkeffects can reduce the expected duration of the technologycompetition process in our model by increasing the volatilityof . This also will occur because the expectation of therandom variable representing the time at which a technologybecomes standard in the marketplace monotonically de-creases in .

To sum up, our model suggests that network externalities ei-ther cause a delay or expedite technology adoption, but this de-pends on adopter and market-related factors. In general, strong

6The law of iterated expectations states that today’s expectation of what willbe expected tomorrow for some variable in a latter period, is simply today’sexpectation for the variable’s value in the latter period. For additional details,the reader should see Walpole et al. [75].

7Issues of this sort frequently arise in the midst of efforts to bring a theoret-ical perspective into more practical uses for analysis and evaluation. The readershould recognize this as inevitable, just as the application of agency theory forcontract formation and managerial incentives development (e.g., [5] and [8]),or the theory of incomplete contracts for interorganizational IS investments andgovernance (e.g., [6] and [33]) is founded on relatively strict assumptions. Inspite of this, the theoretical perspectives and the modeling approaches that com-plement them still offer rich and meaningful managerial insights.

22 IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005

Fig. 2. Optimal timing strategy: no guarantee technology adopted becomes standard.

network effects tend to result in very fast adoption of the tech-nology that adopters believe will be most likely to win the stan-dards competition. In some cases, however, network externali-ties will make people adopt a technology too early, even thoughwaiting is Pareto-preferred [3], [20]. A final point suggestedby our model is that technology adopters actually require moreassurance about the future technology standard outcome whenthey make technology investment decisions, although networkeffects usually speed up their decisions to adopt.

IV. SIMULATION, NUMERICAL EXPERIMENTS,AND INTERPRETATION

This section discusses a firm-level decisionmaking simula-tion for technology adoption in the presence of a standards battlebetween two technologies.

A. Simulation Setup and Outcome

Entry Conditions: We assume that the investment decisionwill be irreversible. Once it is made, the firm will be locked intothe costs and benefits stream associated with the adopted tech-nology. Our goal is to determine the firm’s optimal technologyadoption timing strategy . To initiate this simulation, we re-quire that the decisionmaker who is contemplating adopting thetechnology at the firm will know the following information.

• The decisionmaker’s current expectations of each tech-nology’s probability to win the standards battle will deter-mine , the initial state of technology competition.

• The decisionmaker’s current estimate of the duration ofthe technology competition process will determine the ap-propriate values of and .

• The decisionmaker should be able to make a reasonableestimate of , the ratio between the bonus for adoptingthe technology that becomes the standards battle winner,and the firm’s baseline payoff from investing in the tech-nology project, regardless of the technology choice.

• The decisionmaker should know the discount rate thataffects the costs of waiting.

We normalize and to 1 for the numerical analysis. Thediscount rate is assumed to be 10%. The likelihood that ei-ther technology will become the standard is 0.50, from whichfollows that at time 0. The firm also expects that one of

the two technologies will emerge as the winner in four years.This assumption causes the numerical value of the standard de-viation, , to be around 0.50. We also set the value of , theexogenous gain in business value if the technology becomes astandard at 0.5 V.

Optimal Timing Results. With these specified parametervalues, we find that the optimal investment threshold is0.2717. Thus, the optimal timing strategy in this case is toadopt the new technology when the firm expects that thetechnology’s probability to win is greater than or equal to

. The optimal timing strategy helps thefirm to maximize its expected total investment payoff, but itdoes not guarantee that the technology adopted will eventuallybecome the standards battle winner. Fig. 2 shows two samplepaths that illustrate that the technology adopted at the optimalthresholds or can either succeed or fail in the stan-dards competition. (See Fig. 2.)

According to the derivation of given in the InvestmentDeferral Tradeoff Threshold Ratio Proposition, we find that

. So, in this case, if the exogenous gain in businessvalue when the technology becomes a standard is larger than2.075 V, the result is that the optimal investment strategy is towait until one technology emerges as the winner.

B. Model Robustness

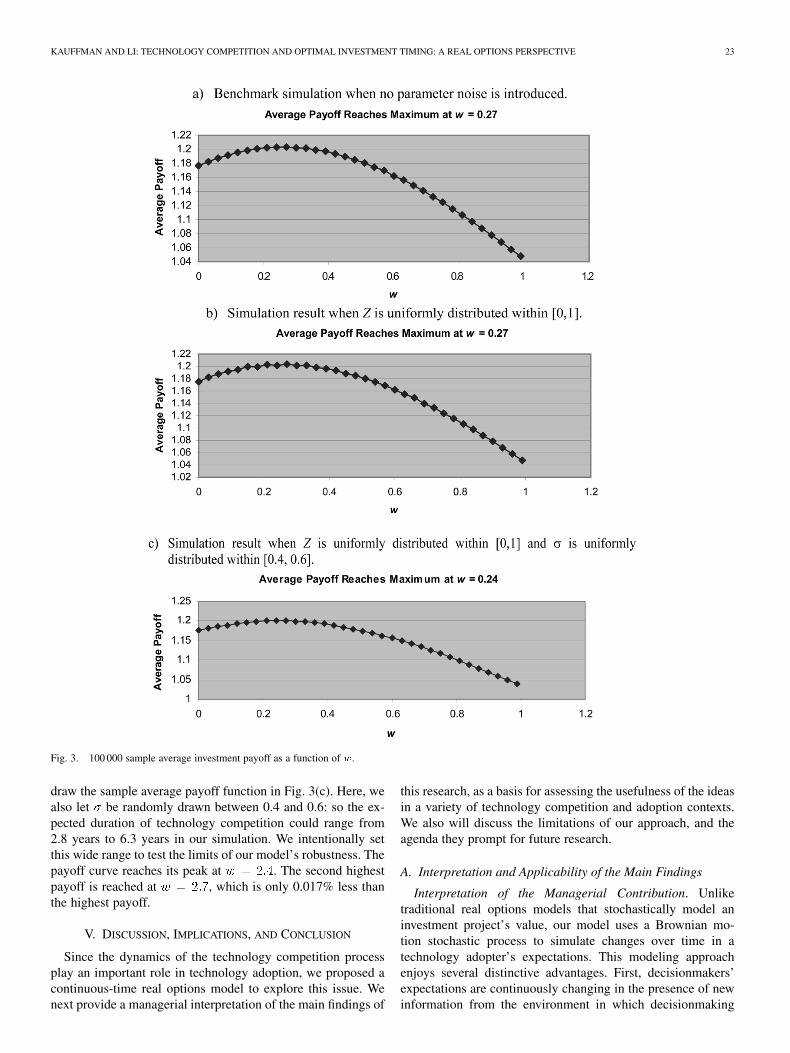

We also use computer simulation to obtain some Monte Carloresults. Because a closed form solution is given in our model,the primary goal of computer simulation is to test its robustnessrather than to generate numeric solutions. We used ANSI C tocode the simulation. With 0.03 as an increment in , we drawthe 100 000 sample average investment payoffs as a function of

in Fig. 3. We set the number of sample paths used in our simu-lation to be sufficiently large to make sure that these sample av-erage payoffs are very close to the expected investment payoffs.

Fig. 3(a) is a benchmark simulation where no parameter noisehas been introduced. It shows that the sample average payofffunction achieves its maximum at , which is veryclose to the closed-form solution , given that theincrement in is 0.03 in the simulation. Fig. 3(b) shows the av-erage sample payoffs when is uniformly distributed between0 and 1. Again, the payoff function achieves its maximum at

. We let and both be uniformly distributed and

KAUFFMAN AND LI: TECHNOLOGY COMPETITION AND OPTIMAL INVESTMENT TIMING: A REAL OPTIONS PERSPECTIVE 23

Fig. 3. 100 000 sample average investment payoff as a function of w.

draw the sample average payoff function in Fig. 3(c). Here, wealso let be randomly drawn between 0.4 and 0.6: so the ex-pected duration of technology competition could range from2.8 years to 6.3 years in our simulation. We intentionally setthis wide range to test the limits of our model’s robustness. Thepayoff curve reaches its peak at . The second highestpayoff is reached at , which is only 0.017% less thanthe highest payoff.

V. DISCUSSION, IMPLICATIONS, AND CONCLUSION

Since the dynamics of the technology competition processplay an important role in technology adoption, we proposed acontinuous-time real options model to explore this issue. Wenext provide a managerial interpretation of the main findings of

this research, as a basis for assessing the usefulness of the ideasin a variety of technology competition and adoption contexts.We also will discuss the limitations of our approach, and theagenda they prompt for future research.

A. Interpretation and Applicability of the Main Findings

Interpretation of the Managerial Contribution. Unliketraditional real options models that stochastically model aninvestment project’s value, our model uses a Brownian mo-tion stochastic process to simulate changes over time in atechnology adopter’s expectations. This modeling approachenjoys several distinctive advantages. First, decisionmakers’expectations are continuously changing in the presence of newinformation from the environment in which decisionmaking

24 IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005

occurs. Unfortunately, multistage discrete-time models usu-ally cannot accommodate this feature of the decisionmakingprocess. Second, the information that arrives typically does soin random fashion. But so long as managerial expectations arerational and consistent, the memoryless and martingale proper-ties of the stochastic process that we discussed turn out to be nottoo hard to justify. So, in spite of some initial concerns that wepointed out, we believe that our use of the standard Brownianmotion representation is a suitable modeling tool. Third, manyobservers believe that managerial decisionmakers’ expectationsplay a fundamental role in many strategic decisionmakingprocesses. By characterizing managers’ expectations directly,and incorporating them into a decisionmaking model for com-peting technologies, the modeling approach that we used maycreate power to analyze other decisionmaking problems underuncertainty.

A major implication of our model is that a firm’s technologyadoption decisions are directly affected by what senior man-agement decisionmakers expect to happen in the future. Sincewaiting is usually expensive in a competitive environment, atechnology adopter needs an investment timing strategy to bal-ance the tradeoff between waiting and preemption. Our modelshows that in a partial equilibrium setting the optimal invest-ment time can be directly expressed as a function of the deci-sionmaker’s expectations about the outcome of the standardsbattle.

We also addressed the issues of technology switching costsand lock-in within the context of technology investment timing.If competing technologies are more compatible or they competewithin an open standard, the technology uncertainties may besignificantly reduced and firms may become more aggressive inadopting new technologies. The major results of our model areespecially applicable to technology competition processes sub-ject to strong network externalities. We have argued that tech-nology adopters’ expectations may become more volatile in a“tippy” market, and that this is caused by positive network feed-back. Consequently, waiting may be more beneficial to adoptersbecause the technological uncertainties will be resolved soonerdue to the increase in the volatility of expectations. The actualwaiting time, as a result, may be significantly shortened becausethe competition process itself usually ends much more quickly.

Breadth of Application. This approach to thinking abouttechnology competition and adoption has ready application in anumber of interesting new business environments involving IT.For example, in the domain of digital wireless phone technolo-gies, we currently see a proliferation of technology standardsaround the world. Kauffman and Techatassanasoontorn [41],[42] report empirical results at the national level of adoptionamong countries throughout the world to show that the pres-ence of multiple wireless standards slows down diffusion. Inthis context, there are problems that exist at the level of thefirm, where the kind of managerial decisionmaking issuesarise that we have described. However, there is another aspect:technology policymaking by regulators and government admin-istrators may affect the technology economy. In the presenceof uncertainty about the outcome of technology competition,these decisionmakers will be faced with the possibility ofcreating technology adoption distortions through policymaking

that lead to inefficient growth and diffusion, as the informationthey tap into and their expectations blend together. The primaryfear is that inappropriate expectations, possibly amplified bythe regulator’s distance from the actual process of firm-leveldecisionmaking, may drive inefficient economic outcomes.

The same can be said for what may happen when firm-leveldecisionmakers are unable to effectively process informationabout competing technologies, and end up with inappropriateexpectations about the likely outcome. Kauffman and Li [39]argue that there is a risk of rational herding, when decision-makers at potential technology adopting firms misinterpret thesignals that are sent and received in the marketplace. Au andKauffman [4] further argue that this is a problem of rationalexpectations, in which the information for technology adoptiondecisionmaking is not able to be assembled all at once. Instead,decisionmakers obtain impressions that are later weakened orconsolidated, based on their interactions with other potentialadopters in the marketplace, as well as vendors and other thirdparties that may play an important role in the outcome. Theypoint out that the problem of gauging the potential of competingtechnologies to achieve the status of de facto standard has oc-curred with electronic bill payment and presentment technolo-gies diffusion in the United States, slowing diffusion in the ab-sence of an acknowledged standard.

A similar problem has been occurring with the diffusion offixed location wireless telephony, the so-called “Wi-Fi” tech-nologies, but here also, we see an environment in the UnitedStates characterized by the near simultaneous emergence intime of multiple standards (including 802.11b, 802.11a, and802.11g, etc.). The difficulties arise for manufacturers ofelectronics products who wish to embed compatible wirelesstechnologies into their products, including handheld computersand PDAs, sound electronics, electronic shelf managementtechnologies, computer peripherals, and wireless routers andnetwork equipment. They are faced with making uncertaindecisions about two aspects of the wireless standards: whichones will become widely accepted by potential consumers ofthe products they make, and how long the standards will be inuse before they are supplanted by the next innovation. Althoughour model does not directly address this issue of “standardsstability,” the reader should recognize that the value of the realoptions that an adopter possesses by making a commitment to acurrent version of a standard is affected by a variety of market,vendor, and technology innovation issues that are beyond themanagerial control of adopting firms. Indeed, this is generallytrue in many technology adoption settings.

B. Limitations and Future Research

Limitations. We note three limitations of this research that de-serve comment before we close out our discussion. First, eventhough the underlying mathematics of the competing technolo-gies analysis that we present are fairly complex, the conceptsthat we have presented are relatively straightforward in concep-tual terms for use by senior managers. Some may argue thatour first concerns should be with the technical details of themodeling formulation—in particular, ensuring that the assump-tions that go along with a standard Brownian motion stochasticprocess with martingale features are precisely met. We chose a

KAUFFMAN AND LI: TECHNOLOGY COMPETITION AND OPTIMAL INVESTMENT TIMING: A REAL OPTIONS PERSPECTIVE 25

different approach though. Our goal was to find a way to makean analogy between the technical details of the decision modeland the exigencies of its application in an appropriate manage-rial context. We offered a technical argument to assuage thereader’s fears that some of our model’s assumptions are toostringent. However, we believe that the single best way to thinkabout our approach is in terms of the new capabilities it opensup in support of managerial decisionmaking.

Second, although we have done some initial numerical anal-ysis with our model to gauge its robustness across a numberof parameter values, there is a higher level test for robustnessthat our model still has not measured up to: construct robust-ness in various applied settings. Even though additional anal-ysis work is beyond the scope of the present work, it will be ap-propriate to conduct additional tests to see whether other issuesinvolving uncertainty that affect adoption decisionmaking canbe incorporated. Several related questions immediately come tomind. What will happen when signals on the state of the tech-nology relative to its becoming a standard in the market are fil-tered or garbled or misread by an adopter, or are misrepresentedby a technology vendor? How can the model handle changesin the key parameters, such as changed estimates of volatility,or shifting perceptions of the adoption time line that firms face,over the duration of the adoption period? Clearly, there is ad-ditional evaluative work to be done with respect to the generalaspects of the modeling approach that we have presented.

Third, we have not yet fully validated this approach with areal world test—something which also is beyond the scope ofthe present work. This is desirable because we will need to findways to simplify the approach so that senior management de-cisionmakers can work with the modeling parameters and con-cepts. In prior work on the application of real options, for ex-ample, Benaroch and Kauffman [12] found that managers didnot understand the concept of risk variances and the distribu-tional mechanics that represent stochastic outcomes. This putsa limitation on the application of the methods, since senior man-agement decisionmakers need to be able to work within themodeling constructs of a recommended evaluation approach torepresent their understanding of the technology adoption val-uation issues in an applied, real world context. Understandingrisks and variances is critical to successful use of the approachthat we propose.

Future Research. Since technology vendors can proactivelyinfluence adopters’ timing decisions, an interesting directionfor future research is to address the timing issue in a generalequilibrium model, to determine policies for adopting firms in amultipartite (i.e., with multiple vendors and adopters) competi-tive context. In such a model, game theory is arguably the idealtool, as suggested by Huisman [34], Grenadier [32], and Zhu[76], and the role of strategic expectations should be the focalpoint. Once vendors’ strategies become endogenous to a deci-sionmaking model, the information asymmetry between tech-nology adopters and vendors will emerge, affecting the mannerin which each approaches a decision about when to adopt andwhen to push toward the next standard. In most cases, tech-nology vendors will hold private information about their firms’plans with the technology, the schedule for releasing the next-generation versions, the speed of development, and so on. As a

result, informational asymmetry should be built into adopters’expectations. Game-theoretic real options analysis can also beapplied to situations where the competitive dynamics betweentechnology adopters significantly impact their equilibrium in-vestment strategies. For example, the technological innovationinvestment model in Grenadier and Weiss [31] is generalizedby Huisman and Kort [35] to a duopolistic real options game.Huisman and Kort [36] further extend their duopolistic gameto scenarios where the future technology arrives stochastically.Their insightful works clearly indicate one promising directionin which our model can be extended. Specifically, future studiesshould consider not only the technology competition as mod-eled here, but also the business competition among technologyadopters whose investment strategies dynamically interact witheach other.

This paper only models the dynamics of competition betweentwo technologies, but we believe that there are at least two ap-proaches that can help extend our model to the more generalscenario, where a manager tries to adopt one of competingtechnologies. The first approach requires the use of a multidi-mensional Brownian motion. The increment of such a Brownianmotion has an -dimensional normal distribution. A band canbe defined on each axis, and a winning technology will emergethe first time when the coordinates of the Brownian motion gobeyond the band associated with the technology. Mathemati-cally, the bands defined on the axes can establish a compactset. Each point in this set can represent a vector of probabilities

, where is the probability for technologyto win the competition. So the Brownian motion can stochasti-cally characterize the uncertainties surrounding the competitionamong the technologies. The advantage of this approach isthat the standard properties of multidimensional Brownian mo-tion can be applied. For example, the martingale property ofmultidimensional Brownian motion can still be used to link itto decisionmakers’ expectations.8

The second approach only needs a standard Brownian motiondefined in a two-dimensional Euclidean space, but it requiressome geometric manipulation. For example, the trajectory of astandard Brownian motion in a triangle, as in Fig. 4, can be usedto depict the competition process of three technologies.

Mathematically, each point in such a triangle can charac-terize the expected probability and time for each technologyto win the competition. For both approaches, we doubt thatclosed-form optimal threshold solutions are derivable in mostsituations. However, recent advances in computation power andoptimization algorithms should make it relatively straightfor-ward to find numerical solutions.

Because it is impossible to give closed-form solutions formany complicated real options models, computer simulationsand other computationally intensive approaches are suitable re-search tools [19], [29]. Although we derived a closed-form so-lution in this study of competing technologies, the reader shouldrecognize that closed-from solutions are very difficult to de-rive in many other situations where real options analysis is ap-propriate. Fortunately, the newly available capabilities of com-

8See Durrett [25] for a proof. The downside of this approach is that rigor-ously applying multidimensional martingales requires mathematical knowledgebeyond a first graduate course in real analysis (e.g., [69]).

26 IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005

Fig. 4. Brownian motion characterization of the standards battle among threecompeting technologies.

puting resources make it possible, consistent with widespreadadvances in methodologies for computational finance, statisticsand econometrics, to do numerical experiments and simulationsthat would not have been cost-effective only a few years ago.These new computationally intensive methods permit us to asknew and more refined research questions involving real optionsvaluation in important applied settings. The answers that we arenow able to obtain will help to guide senior management de-cisionmaking related to technology adoption and advance thefrontiers of management science for decisionmaking under un-certainty.

APPENDIX AUNDERSTANDING REAL OPTIONS: A BRIEF INTRODUCTION

The seminal works of Black and Scholes [15] and Merton[58] offer us a standard pricing model for financial options. To-gether with another colleague at MIT, Stewart Myers, they rec-ognized that option pricing theory could be applied to real as-sets and nonfinancial investments. To differentiate options onreal assets from financial options traded in the market, Myerscoined the term “real options.” Today, that term has been widelyaccepted in the academic and business world. Many observersbelieve that the real options approach can play an important rolein financial evaluation related to projects that are undertaken inthe highly uncertain and technology-driven digital economy. Wewill present a simple example to give readers some useful intu-ition and an illustration of the value associated with real optionsand their significance in capital budgeting.

A. Real Options Example: This Year or Next Year?

Imagine that a software company is facing a new investmentopportunity. It plans to spend $100 000 to make its best-sellingdatabase system compatible with an emerging operating system(OS) in the market, but new OS is still in its infancy, so the com-pany is not sure whether it will be widely accepted in the future.Suppose that uncertainty about the new OS can be totally re-solved next year, and that the company is trying to maximize

its expected return from the $100 000 investment project. Ac-cording to the company’s estimation, the new OS has a 50%chance to be widely accepted next year. In this case, the ex-pected increased cash inflow from this investment is estimatedto be $15 000 a year. In the case that the OS is not popular nextyear, the expected annual net cash inflow from this project willbe $7000. Further suppose that the discount rate for this invest-ment project is 10%, the net present value (NPV) of this projectcan be calculated as

Since the NPV of this project is positive, it seems that thefirm should go ahead with this project. However, the conclusionis incorrect. Why? It does not account for the value of the optionto defer the investment to the next year. Next, suppose that thecompany waits one year to watch the market’s reaction to thenew OS. If a favorable situation occurs, then it will proceed toinvest; otherwise, it will no longer pursue the project. Then, theNPV of this project will be

Evidently, it is better to take the option of deferring theinvestment to the next year. The value of this option is$22 727 $10 000 $12 727. Let us further suppose thatsomeone in the company argues that the investment costs willincrease in the next year. But still, further calculation showsthat the option will be valuable even if the costs rise as high as$127 000 in the next year. Basically, this simple example showsthe value of an option of deferring investment.

We now review the basic tools and concepts of option pricingtheory, beginning with a definition. An option is the right, butnot the obligation, to buy (a call) or sell (a put) an asset at aprespecified price on or before a specified date. For financialoption contracts, the underlying assets are usually stocks. Untilthe late 1960s, researchers in Finance were unable to find a rig-orous method to price options on stock. However, Black andScholes [15] and Merton [58], using methods from infinitesimalcalculus and the concept of dynamic portfolio hedging, success-fully specified the fundamental partial differential equation thatmust be satisfied by the value of the call option, which permittedthem to give the analytical solution known as the Black–Scholesformula for the value of an option.

Following the revolution in option pricing theory that theBlack–Scholes model caused, many researchers recognized thenew potential of this theory in capital budgeting. TraditionalDCF methods were recognized for their inherent limitations:they did not yield effective estimates of value related to projectinvestments with strategic options and many uncertainties.Myers [61] showed that a firm’s discretionary investmentoptions are components of its market value. Mason and Merton[55] discussed the role of option pricing theory in corporatefinance. Kulatilaka and Marks [44] also discuss the strategicvalue of managerial flexibility and its option like properties.Table II lists the similarities between an American call optionon a stock and a real option on an investment project. Despite

KAUFFMAN AND LI: TECHNOLOGY COMPETITION AND OPTIMAL INVESTMENT TIMING: A REAL OPTIONS PERSPECTIVE 27

TABLE IICOMPARISON BETWEEN AN AMERICAN CALL OPTION AND A REAL OPTION ON A PROJECT

the close analogy, some still question the applicability of optionpricing theory to real options that usually are not traded in amarket. However, Cox, et al. [21] and McDonald and Siegel[56] suggest that a contingent claim on nontraded assets can bepriced with the adjustment of its growth rate by subtracting adividend-like risk premium.

Based on this solid theoretical foundation, many researchershave investigated the valuation of various real options in thebusiness world. One of the most basic real options models wasdeveloped by McDonald and Siegel [57]. In their model, theydiscuss the optimal time for a firm to invest in a proprietaryproject whose value evolves according to a stochastic processcalled geometric Brownian motion. Their results suggest that theoption to defer an investment may be very valuable under somecircumstances. Ingersoll and Ross [37] also discussed the optionof waiting to invest and its relation with uncertainty. Brennanand Schwartz [17] examined the joint decisions to invest andabandon a project. Kulatilaka and Trigeorgis [46] adopted realoption theory to value the managerial flexibility to switch inputsand outputs. Grenadier [30] discussed how to value lease con-tracts by real options theory. The interested reader should seeLi [51] for additional details on the applications of real optionstheory to technology related business problems.

APPENDIX BMATHEMATICAL PROOFS OF KEY FINDINGS

A. Proof of Theorem 1—Optimal Investment Timing StrategyTheorem

Before a company invests in a new technology project, it willhave an option to invest in the project. This value of this op-tion is denoted by . It must satisfy a Bellman equilibriumdifferential equation, , in the con-tinuation region, where there are values of for which it is notoptimal to invest.

Note that we need three conditions to solve the differentialequation. The reason is that the optimal investment threshold

is a free boundary of the continuation region. The first con-dition is a value-matching condition , which

says that upon investing, the expected payoff will be .The second condition is a smooth-pasting condition,

, that is necessary to guarantee that the threshold pointis the true optimal exercise point for the real option [22].

The third is a symmetry condition , whichcomes directly from the symmetric structure of our model’sspecification.

We note that, in some cases, will be outside .This means that the continuation region goes beyond the de-cision region, and so the optimal strategy is to invest whenreaches either or , the boundaries of the decision re-gion. To satisfy the equilibrium differential equation and thethird condition, it turns out that the solution must take the form

. In this expression, isa constant to be computed and values of occur within the con-tinuation region. The other two conditions can be used to solvefor the two remaining unknowns, the constant and the op-timal investment threshold . The positive optimal investmentthreshold and constant must also satisfy the equationsshown at the bottom of the page, where and are definedwhere we derive . The solution to the system of equationsis given by

The reader should note that we assume , and, otherwise. Similarly, the negative threshold and can

be solved as follows:

The negative optimal investment threshold will be ifis beyond . We also know the values of the two

thresholds and , where . So for a given, the firm should invest immediately if is out-

side of . If , the firm should adopt atechnology once reaches either or . If reaches

28 IEEE TRANSACTIONS ON ENGINEERING MANAGEMENT, VOL. 52, NO. 1, FEBRUARY 2005

first, then the firm will adopt Technology since, but if it reaches first, then Technology will be

adopted because .

B. Proof of Proposition 1—Investment Deferral TradeoffThreshold Ratio Proposition

From Theorem 1, we know that the optimal investmentthreshold is or if the following inequality,

,

holds. Since is monotonically increasing, the inequalityis equivalent to

. The term , can be simplified as. This inequality will hold if

. Otherwise, the inequality will beequivalent to .As .We prove that the optimal investment threshold will be-come and when is greater than or equal to ,where . Theremainder of the proposition directly follows from the factthat

. This com-pletes the proof.

C. Proof of Proposition 2—Comparative Statics Proposition)

We know that for any , we have

. Inthe proof for Proposition 1, we showed that the term, , canbe simplified as . Fromthis, we can prove that ,

, and . Since ,and is monotonically increasing, we can further

deduce that , , and .In addition, we know that and

. This permits us toconclude that and . This completesthe proof.

ACKNOWLEDGMENT

Early versions of this paper have been circulated at CaseWestern Reserve University, INSEAD, University of Michigan,University of Texas at Dallas, Drexel University, Universityof Wisconsin, University of Minnesota and University ofMississippi. The authors thank I. Bardhan, J. Conlon, Q. Dai,W. Lovejoy, J. Johnson, J. Smith, P. Tallon, V. Wang, K. Womer,and K. Zhu for helpful suggestions and comments. They alsoappreciate the input of the Senior Editor, R. Sabherwal, andanonymous reviewers. R. Kauffman acknowledges the MISResearch Center for partial support.

REFERENCES

[1] M. Amram and N. Kulatilaka, Real Options: Managing Strategic In-vestment in an Uncertain World. Cambridge, MA: Harvard BusinessSchool Press, 1999.

[2] M. Amram, N. Kulatilaka, and J. C. Henderson, “Taking an option onIT,” CIO Enterprise Mag., vol. 12, no. 17, pp. 46–46, 1999.

[3] Y. Au and R. J. Kauffman, “Should we wait? Network externalities, com-patibility and electronic billing adoption,” J. Manage. Inf. Syst., vol. 18,no. 2, pp. 47–64, 2001.

[4] , “What do you know? Rational expectations in information tech-nology adoption and investment,” J. Manage. Inf. Syst., vol. 20, no. 2,pp. 49–76, 2003.

[5] R. D. Austin, “The effects of time pressure on quality in software devel-opment: An agency model,” Inf. Syst. Res., vol. 12, no. 2, pp. 195–207,2001.

[6] J. Y. Bakos and B. R. Nault, “Ownership and investment in electronicnetworks,” Inf. Syst. Res., vol. 8, no. 4, pp. 321–341, 1997.

[7] P. Balasubramian, N. Kulatilaka, and J. C. Storck, “Managing informa-tion technology investments using a real options approach,” J. StrategicInf. Syst., vol. 9, pp. 39–62, 1999.

[8] R. D. Banker and C. F. Kemerer, “Performance evaluation metrics forinformation systems development: A principal-agent model,” Inf. Syst.Res., vol. 3, no. 4, pp. 379–401, 1992.

[9] I. Bardhan, S. Bagchi, and R. Sougstad, “Prioritization of a portfolio ofIT investment projects,” J. Manage. Inf. Syst., vol. 21, no. 2, 2004.

[10] M. Benaroch, “Managing information technology investment risk: Areal options perspective,” J. Manage. Inf. Syst., vol. 19, no. 2, pp. 43–84,2002.

[11] M. Benaroch and R. J. Kauffman, “A case for using real options pricinganalysis to evaluate information technology project investment,” Inf.Syst. Res., vol. 10, no. 1, pp. 70–86, 1999.

[12] , “Justifying electronic banking network expansion using real op-tions analysis,” MIS Quart., vol. 24, no. 2, pp. 197–225, 2000.

[13] A. Bernardo and B. Chowdhry, “Resources, real options and corporatestrategy,” J. Financial Econ., vol. 63, no. 2, pp. 211–234, 2002.

[14] S. Besen and J. Farrell, “Choosing how to compete: Strategies and tacticsin standardization,” J. Econ. Perspectives, vol. 8, no. 2, pp. 117–131,1994.

[15] F. Black and M. Scholes, “The pricing of options and corporate liabili-ties,” J. Pol. Econ., vol. 81, no. 3, pp. 637–659, 1973.

[16] F. Black and J. C. Cox, “Valuing corporate securities: Some effects ofbond indenture provisions,” J. Finance, vol. 31, no. 2, pp. 351–367,1976.

[17] M. Brennan and E. Schwartz, “Evaluating natural resource investments,”J. Bus., vol. 58, no. 2, pp. 135–57, 1985.

[18] E. Brynjolfsson and C. Kemerer, “Network externalities in microcom-puter software: An econometric analysis of the spreadsheet market,”Manage. Sci., vol. 42, no. 12, pp. 1627–1647, 1996.

[19] D. Calistrate, M. Paulhus, and G. Sick, “Real options for managing risk:Using simulation to characterize gain in value,” Dept. Math., Univ. Cal-gary, Calgary, CA, Working Paper, 1999.

[20] J. P. Choi and M. Thum, “Market structure and the timing of technologyadoption with network externalities,” Eur. Econ. Rev., vol. 42, no. 2, pp.225–244, 1998.

[21] J. Cox, J. Ingersoll, and S. Ross, “An intertemporal general equilibriummodel of asset prices,” Econometrica, vol. 53, no. 2, pp. 363–84, 1985.

[22] D. Dixit and R. Pindyck, Investment Under Uncertainty. Princeton,NJ: Princeton Univ. Press, 1994.

[23] M. Domine, “Moments of the first passage time of a wiener processwith drift between two elastic barriers,” J. Appl. Probability, vol. 32,pp. 1007–1013, 1995.

[24] B. L. Dos Santos, “Justifying investments in new information technolo-gies,” J. Manage. Inf. Syst., vol. 7, no. 4, pp. 71–90, 1991.

[25] R. Durrett, Brownian Motion and Martingales in Analysis. Belmont,CA: Wadsworth, 1984.

[26] J. Farrell and C. Shapiro, “Optimal contracts with lock-in,” Amer. Econ.Rev., vol. 79, no. 1, pp. 51–68, 1989.

[27] J. Farrell and M. Katz, “Competition or predation? Schumpeterian ri-valry in network markets,” Univ. California, Berkeley, Berkeley, CA,Working Paper, 2001.

[28] J. Farrell and P. Klemperer, “Coordination and lock-in: Competition withswitching costs and network effects,” in Handbook of Industrial Organ-ization, M. Armstrong and R. H. Porter, Eds. Amsterdam, The Nether-lands: Elsevier, 2004, vol. 3.

[29] A. Gamba, “Real options valuation: A Monte Carlo simulation ap-proach,” Faculty of Management, Calgary, CA, Working Paper, 2002.

[30] S. Grenadier, “Valuing lease contracts: A real options approach,” J. Fi-nancial Econ., vol. 38, no. 3, pp. 297–331, 1995.

[31] S. Grenadier and A. Weiss, “Investment in technological innovations: Anoption pricing approach,” J. Financial Econ., vol. 44, no. 3, pp. 397–416,1997.

[32] S. Grenadier, “Option exercise games: An application to the equilibriuminvestment strategies of firms,” Rev. Financial Studies, vol. 15, no. 3, pp.691–721, 2002.

KAUFFMAN AND LI: TECHNOLOGY COMPETITION AND OPTIMAL INVESTMENT TIMING: A REAL OPTIONS PERSPECTIVE 29

[33] K. Han, R. J. Kauffman, and B. R. Nault, “Information exploitation andinterorganizational systems ownership,” J. Manage. Inf. Syst., vol. 21,no. 2, 2004.

[34] K. Huisman, Technology Investment: A Game Theoretic Real OptionsApproach. Dordrecht, The Netherlands: Kluwer, 2001.

[35] K. Huisman and P. Kort, “Strategic investment in technology innova-tions,” Eur. J. Oper. Res., vol. 144, no. 1, pp. 209–223, 2003.

[36] , “Strategic technology adoption taking into account future tech-nological improvements: A real options approach,” Eur. J. Oper. Res.,2004.

[37] J. Ingersoll and S. Ross, “Waiting to invest: Investment and uncertainty,”J. Bus., vol. 65, no. 1, pp. 1–29, 1992.

[38] M. Katz and C. Shapiro, “System competition and network effects,” J.Econ. Perspectives, vol. 8, no. 2, pp. 93–115, 1994.

[39] R. J. Kauffman and X. Li, “Payoff externalities, informational cas-cades and managerial incentives: A theoretical framework for ITadoption herding,” in Proc. 2003 INFORMS Conf. Inf. Syst. Technol.,A. Bharadwaj, S. Narasimhan, and R. Santhanam, Eds., Atlanta, GA,2003. Available on CD-ROM.

[40] R. J. Kauffman, J. J. McAndrews, and Y. Wang, “Opening the ’Blackbox’ of network externalities in network adoption,” Inf. Syst. Res., vol.11, no. 1, pp. 61–82, 2000.