Embed Size (px)

Citation preview

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

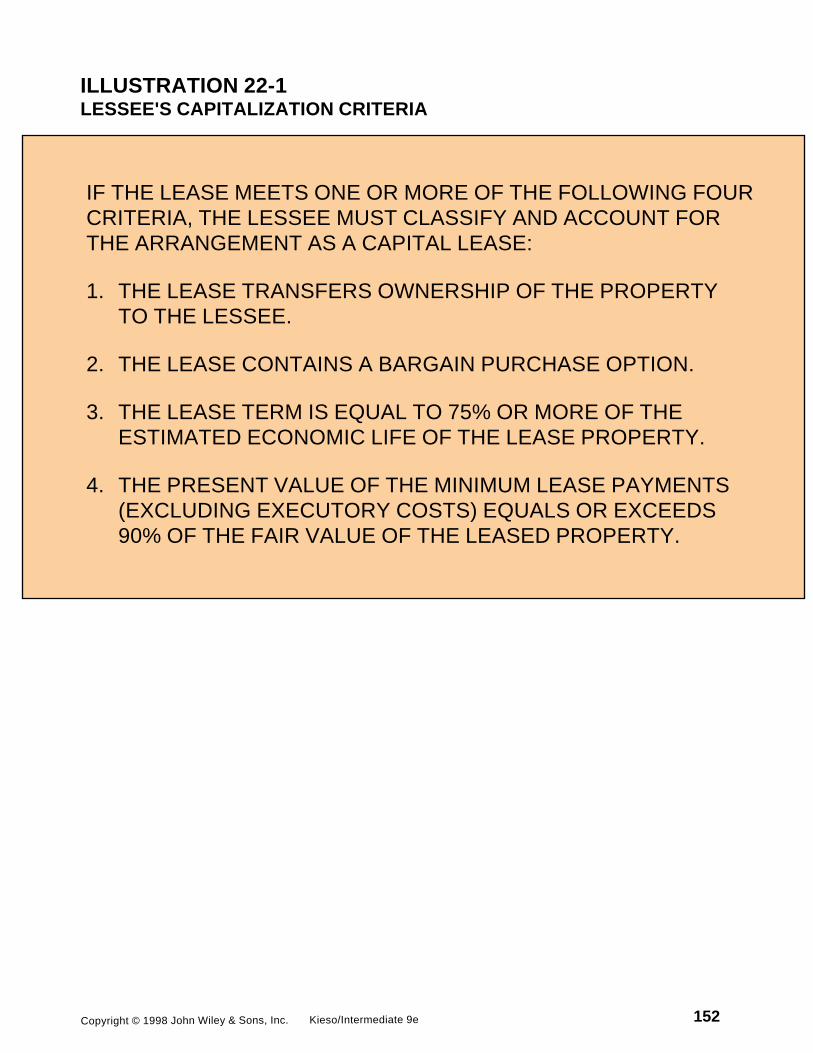

ILLUSTRATION 22-1LESSEE'S CAPITALIZATION CRITERIA

152

IF THE LEASE MEETS ONE OR MORE OF THE FOLLOWING FOURCRITERIA, THE LESSEE MUST CLASSIFY AND ACCOUNT FOR THE ARRANGEMENT AS A CAPITAL LEASE:

1. THE LEASE TRANSFERS OWNERSHIP OF THE PROPERTY TO THE LESSEE.

2. THE LEASE CONTAINS A BARGAIN PURCHASE OPTION.

3. THE LEASE TERM IS EQUAL TO 75% OR MORE OF THE ESTIMATED ECONOMIC LIFE OF THE LEASE PROPERTY.

4. THE PRESENT VALUE OF THE MINIMUM LEASE PAYMENTS (EXCLUDING EXECUTORY COSTS) EQUALS OR EXCEEDS 90% OF THE FAIR VALUE OF THE LEASED PROPERTY.

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

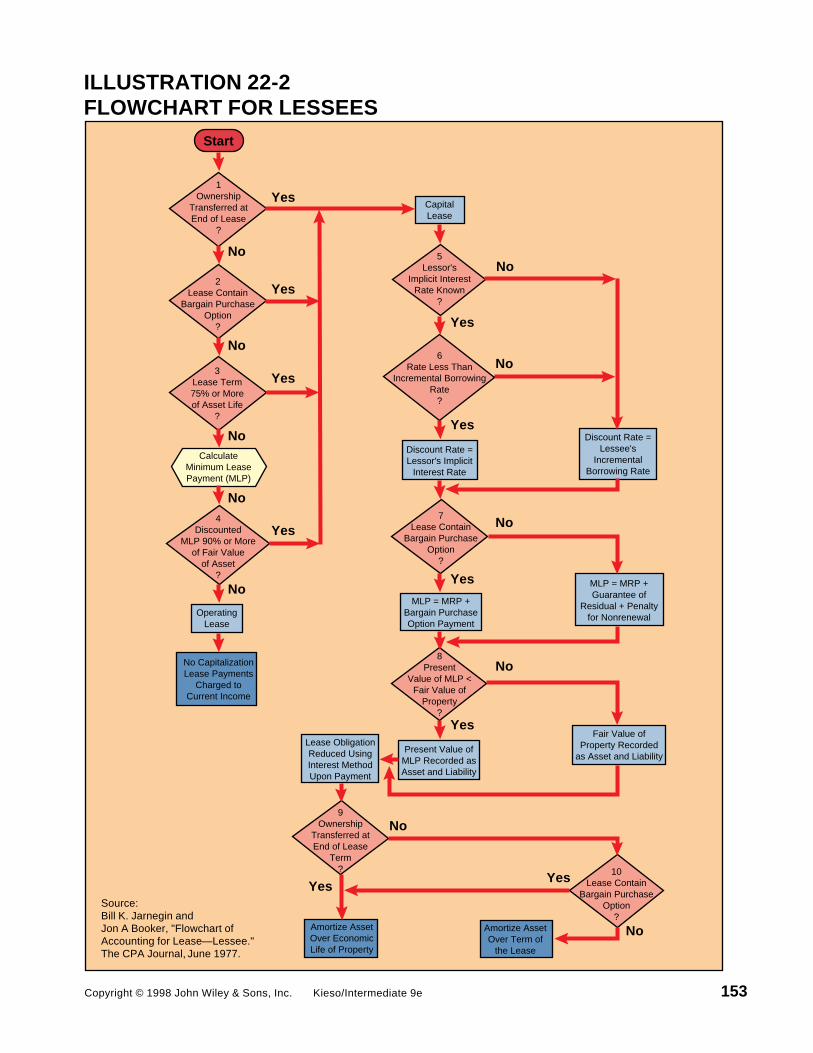

ILLUSTRATION 22-2FLOWCHART FOR LESSEES

153

No

No

Start

1Ownership

Transferred atEnd of Lease

?

2Lease Contain

Bargain PurchaseOption

?

3Lease Term75% or Moreof Asset Life

?

4Discounted

MLP 90% or Moreof Fair Value

of Asset?

CalculateMinimum LeasePayment (MLP)

OperatingLease

No CapitalizationLease Payments

Charged toCurrent Income

CapitalLease

5Lessor's

Implicit InterestRate Known

?

6Rate Less Than

Incremental BorrowingRate

?

Discount Rate =Lessor's Implicit

Interest Rate

7Lease Contain

Bargain PurchaseOption

?

MLP = MRP +Bargain PurchaseOption Payment

8Present

Value of MLP <Fair Value of

Property?

Present Value ofMLP Recorded asAsset and Liability

Lease ObligationReduced UsingInterest MethodUpon Payment

9Ownership

Transferred atEnd of Lease

Term?

Amortize AssetOver EconomicLife of Property

Discount Rate =Lessee's

IncrementalBorrowing Rate

MLP = MRP +Guarantee of

Residual + Penaltyfor Nonrenewal

Fair Value ofProperty Recorded

as Asset and Liability

10Lease Contain

Bargain PurchaseOption

?Amortize AssetOver Term of

the Lease

Yes

Yes

Yes

Yes

YesYes

No

No

No

No

Source: Bill K. Jarnegin andJon A Booker, "Flowchart ofAccounting for Lease—Lessee."The CPA Journal, June 1977.

No

No

No

No

No

Yes

Yes

Yes

Yes

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

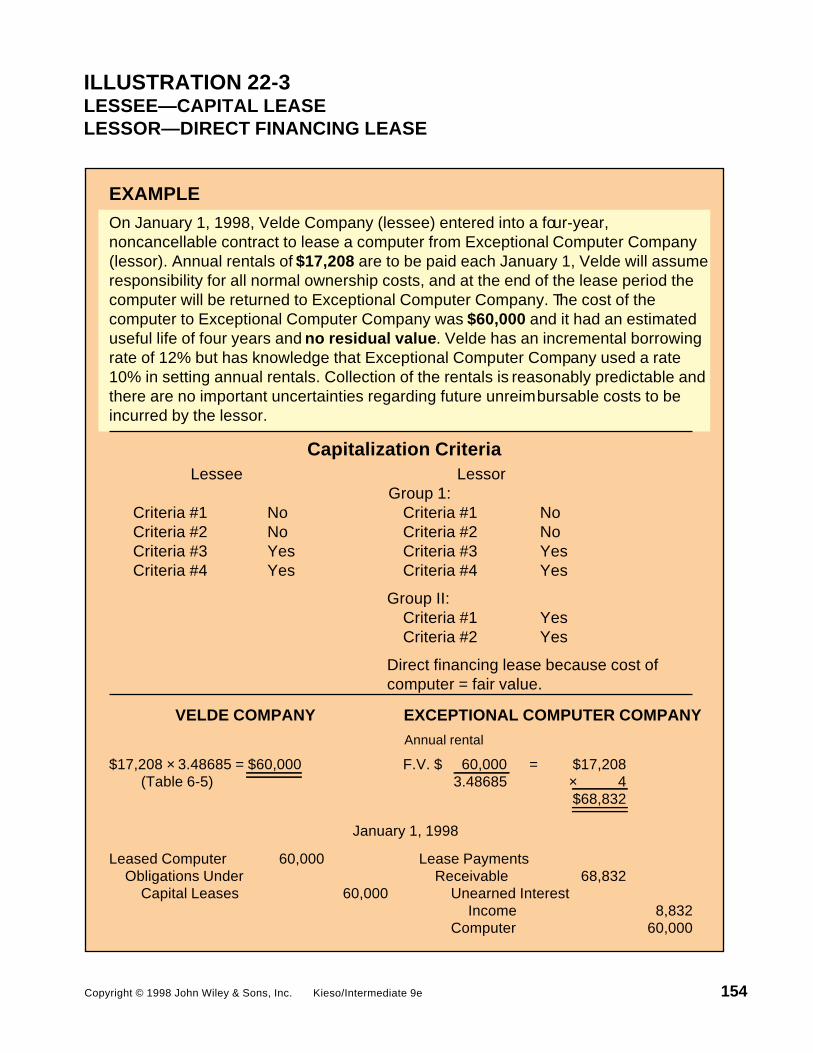

ILLUSTRATION 22-3LESSEE—CAPITAL LEASELESSOR—DIRECT FINANCING LEASE

154

EXAMPLE

On January 1, 1998, Velde Company (lessee) entered into a four-year,noncancellable contract to lease a computer from Exceptional Computer Company(lessor). Annual rentals of $17,208 are to be paid each January 1, Velde will assumeresponsibility for all normal ownership costs, and at the end of the lease period the computer will be returned to Exceptional Computer Company. The cost of the computer to Exceptional Computer Company was $60,000 and it had an estimated useful life of four years and no residual value. Velde has an incremental borrowingrate of 12% but has knowledge that Exceptional Computer Company used a rate 10% in setting annual rentals. Collection of the rentals is reasonably predictable andthere are no important uncertainties regarding future unreimbursable costs to be incurred by the lessor.

Capitalization Criteria Lessee Lessor Group 1:Criteria #1 No Criteria #1 NoCriteria #2 No Criteria #2 NoCriteria #3 Yes Criteria #3 YesCriteria #4 Yes Criteria #4 Yes

Group II: Criteria #1 Yes Criteria #2 Yes

Direct financing lease because cost of computer = fair value.

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

Annual rental

$17,208 ́ 3.48685 = $60,000 F.V. $ 60,000 = $17,208 (Table 6-5) 3.48685 ´ 4 $68,832

January 1, 1998

Leased Computer 60,000 Lease Payments Obligations Under Receivable 68,832 Capital Leases 60,000 Unearned Interest Income 8,832 Computer 60,000

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

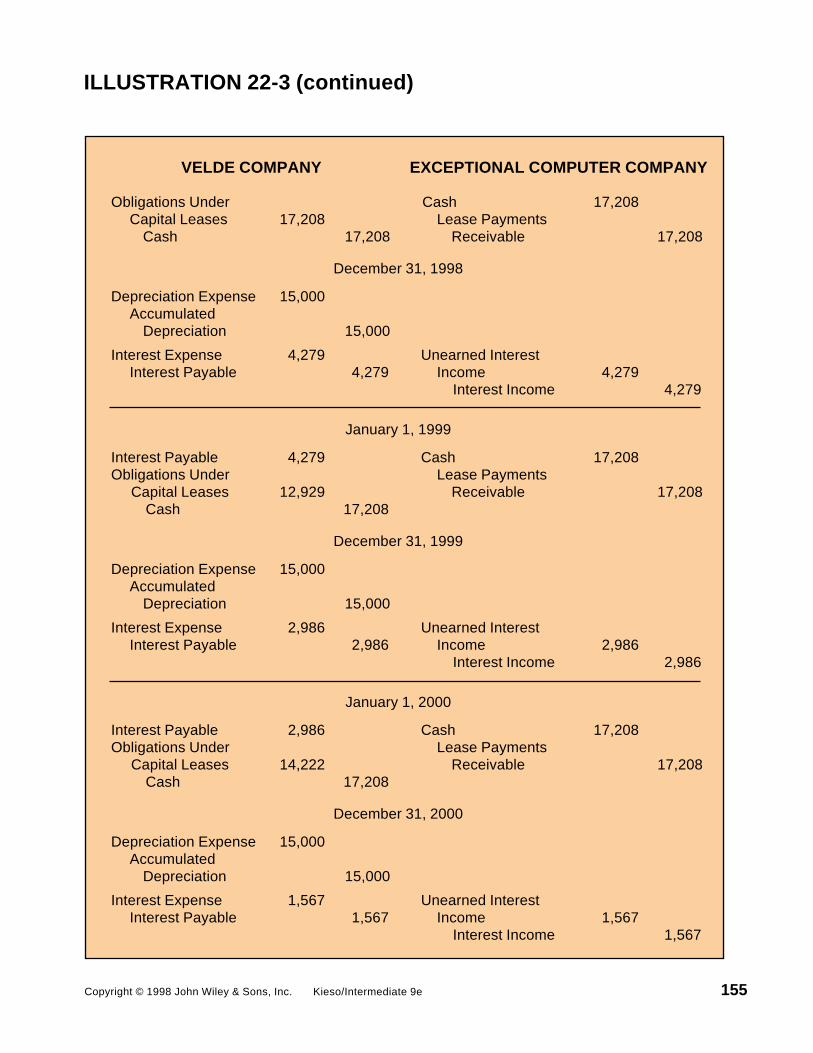

ILLUSTRATION 22-3 (continued)

155

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

Obligations Under Cash 17,208 Capital Leases 17,208 Lease Payments Cash 17,208 Receivable 17,208

December 31, 1998

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Interest Expense 4,279 Unearned Interest Interest Payable 4,279 Income 4,279 Interest Income 4,279

January 1, 1999

Interest Payable 4,279 Cash 17,208Obligations Under Lease Payments Capital Leases 12,929 Receivable 17,208 Cash 17,208

December 31, 1999

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Interest Expense 2,986 Unearned Interest Interest Payable 2,986 Income 2,986 Interest Income 2,986

January 1, 2000

Interest Payable 2,986 Cash 17,208Obligations Under Lease Payments Capital Leases 14,222 Receivable 17,208 Cash 17,208

December 31, 2000

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Interest Expense 1,567 Unearned Interest Interest Payable 1,567 Income 1,567 Interest Income 1,567

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

ILLUSTRATION 22-3 (concluded)

156

January 1, 2001

Interest Payable 1,567 Cash 17,208Obligations Under Lease Payments Capital Leases 15,641 Receivable 17,208 Cash 17,208

December 31, 2001

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Accumulated Depreciation 60,000 Leased Computer 60,000

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

Lease Amortization Schedules

VELDE COMPANY

Annual (10%) Reduction of Lease Date Lease Payment Interest Obligation Obligation

Jan. 1, 1998 $60,000Jan. 1, 1998 $17,208 $ –0– $17,208 42,792Jan. 1, 1999 17,208 4,279 12,929 29,863Jan. 1, 2000 17,208 2,986 14,222 15,641Jan. 1, 2001 17,208 1,567* 15,641 –0–

EXCEPTIONAL COMPUTER COMPANY

Annual (10%) Investment Net Date Lease Payment Interest Recovery Investment

Jan. 1, 1998 $60,000Jan. 1, 1998 $17,208 $ –0– $17,208 42,792Jan. 1, 1999 17,208 4,279 12,929 29,863Jan. 1, 2000 17,208 2,986 14,222 15,641Jan. 1, 2001 17,208 1,567* 15,641 –0–

*Adjusted for rounding.

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

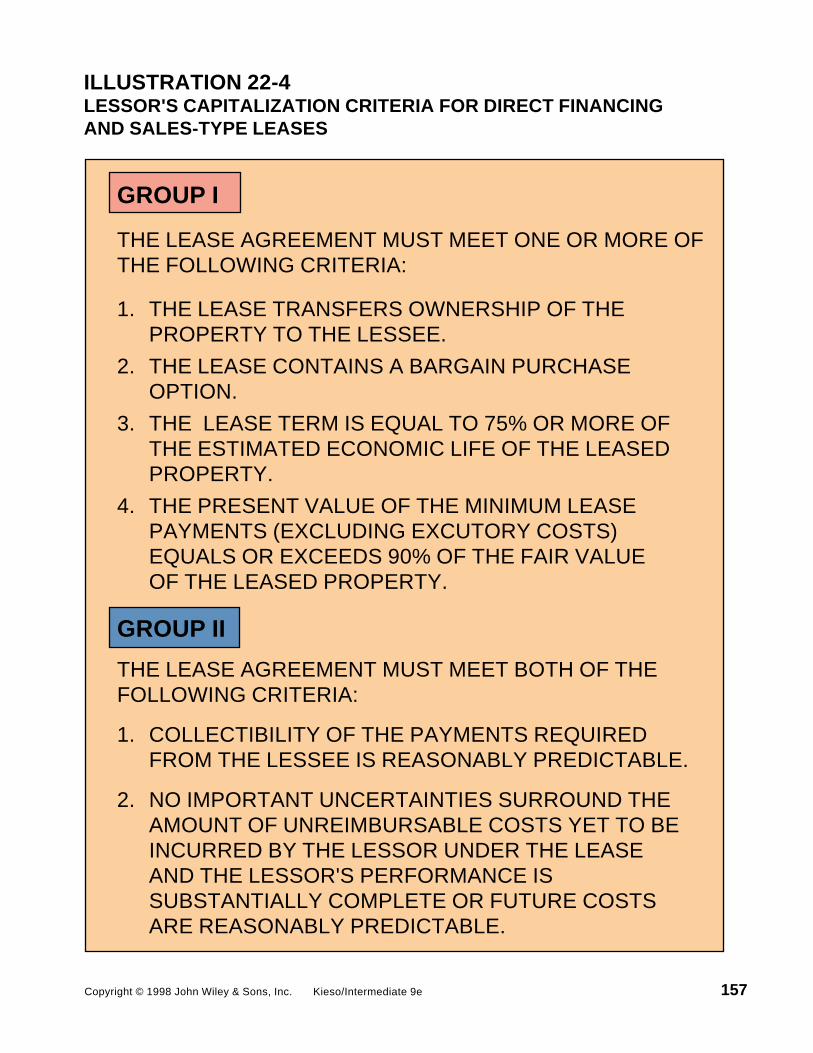

ILLUSTRATION 22-4LESSOR'S CAPITALIZATION CRITERIA FOR DIRECT FINANCINGAND SALES-TYPE LEASES

157

GROUP I

THE LEASE AGREEMENT MUST MEET ONE OR MORE OFTHE FOLLOWING CRITERIA:

1. THE LEASE TRANSFERS OWNERSHIP OF THE PROPERTY TO THE LESSEE.

2. THE LEASE CONTAINS A BARGAIN PURCHASE OPTION.

3. THE LEASE TERM IS EQUAL TO 75% OR MORE OF THE ESTIMATED ECONOMIC LIFE OF THE LEASED PROPERTY.

4. THE PRESENT VALUE OF THE MINIMUM LEASE PAYMENTS (EXCLUDING EXCUTORY COSTS) EQUALS OR EXCEEDS 90% OF THE FAIR VALUE OF THE LEASED PROPERTY.

GROUP II

THE LEASE AGREEMENT MUST MEET BOTH OF THEFOLLOWING CRITERIA:

1. COLLECTIBILITY OF THE PAYMENTS REQUIRED FROM THE LESSEE IS REASONABLY PREDICTABLE.

2. NO IMPORTANT UNCERTAINTIES SURROUND THE AMOUNT OF UNREIMBURSABLE COSTS YET TO BE INCURRED BY THE LESSOR UNDER THE LEASE AND THE LESSOR'S PERFORMANCE IS SUBSTANTIALLY COMPLETE OR FUTURE COSTS ARE REASONABLY PREDICTABLE.

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

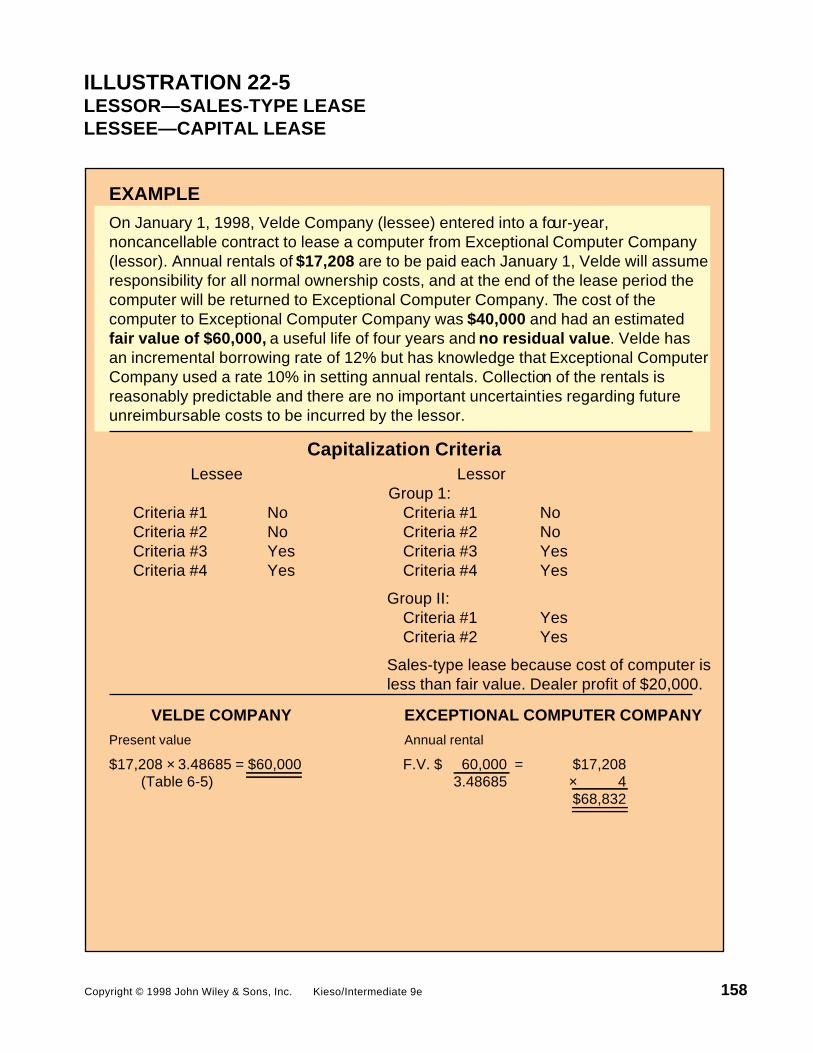

ILLUSTRATION 22-5LESSOR—SALES-TYPE LEASELESSEE—CAPITAL LEASE

158

EXAMPLE

On January 1, 1998, Velde Company (lessee) entered into a four-year,noncancellable contract to lease a computer from Exceptional Computer Company(lessor). Annual rentals of $17,208 are to be paid each January 1, Velde will assumeresponsibility for all normal ownership costs, and at the end of the lease period the computer will be returned to Exceptional Computer Company. The cost of the computer to Exceptional Computer Company was $40,000 and had an estimated fair value of $60,000, a useful life of four years and no residual value. Velde hasan incremental borrowing rate of 12% but has knowledge that Exceptional Computer Company used a rate 10% in setting annual rentals. Collection of the rentals is reasonably predictable and there are no important uncertainties regarding future unreimbursable costs to be incurred by the lessor.

Capitalization Criteria Lessee Lessor Group 1:Criteria #1 No Criteria #1 NoCriteria #2 No Criteria #2 NoCriteria #3 Yes Criteria #3 YesCriteria #4 Yes Criteria #4 Yes

Group II: Criteria #1 Yes Criteria #2 Yes

Sales-type lease because cost of computer is less than fair value. Dealer profit of $20,000.

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

Present value Annual rental

$17,208 ́ 3.48685 = $60,000 F.V. $ 60,000 = $17,208 (Table 6-5) 3.48685 ´ 4 $68,832

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

ILLUSTRATION 22-5 (continued)

159

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

January 1, 1998

Leased Computer 60,000 Lease Payments Obligations Under Receivable 68,832 Capital Leases 60,000 Cost of goods sold 40,000 Inventory 40,000 Unearned Interest Income 8,832 Sales Revenue 60,000

Obligations Under Capital Leases 17,208 Cash 17,208 Lease Payments Cash 17,208 Receivable 17,208

December 31, 1998

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Interest Expense 4,279 Unearned Interest Interest Payable 4,279 Income 4,279 Interest Income 4,279

January 1, 1999

Interest Payable 4,279 Cash 17,208Obligations Under Lease Payments Capital Leases 12,929 Receivable 17,208 Cash 17,208

December 31, 1999

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Interest Expense 2,986 Unearned Interest Interest Payable 2,986 Income 2,986 Interest Income 2,986

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

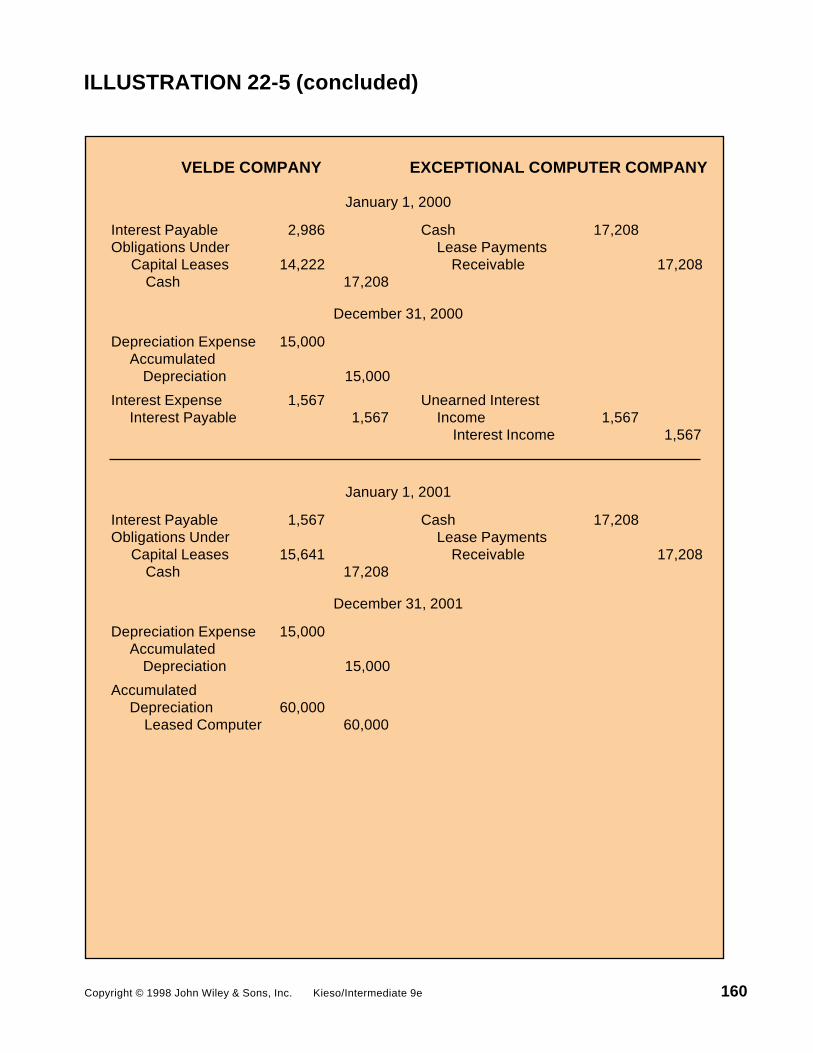

ILLUSTRATION 22-5 (concluded)

160

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

January 1, 2000

Interest Payable 2,986 Cash 17,208Obligations Under Lease Payments Capital Leases 14,222 Receivable 17,208 Cash 17,208

December 31, 2000

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Interest Expense 1,567 Unearned Interest Interest Payable 1,567 Income 1,567 Interest Income 1,567

January 1, 2001

Interest Payable 1,567 Cash 17,208Obligations Under Lease Payments Capital Leases 15,641 Receivable 17,208 Cash 17,208

December 31, 2001

Depreciation Expense 15,000 Accumulated Depreciation 15,000

Accumulated Depreciation 60,000 Leased Computer 60,000

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

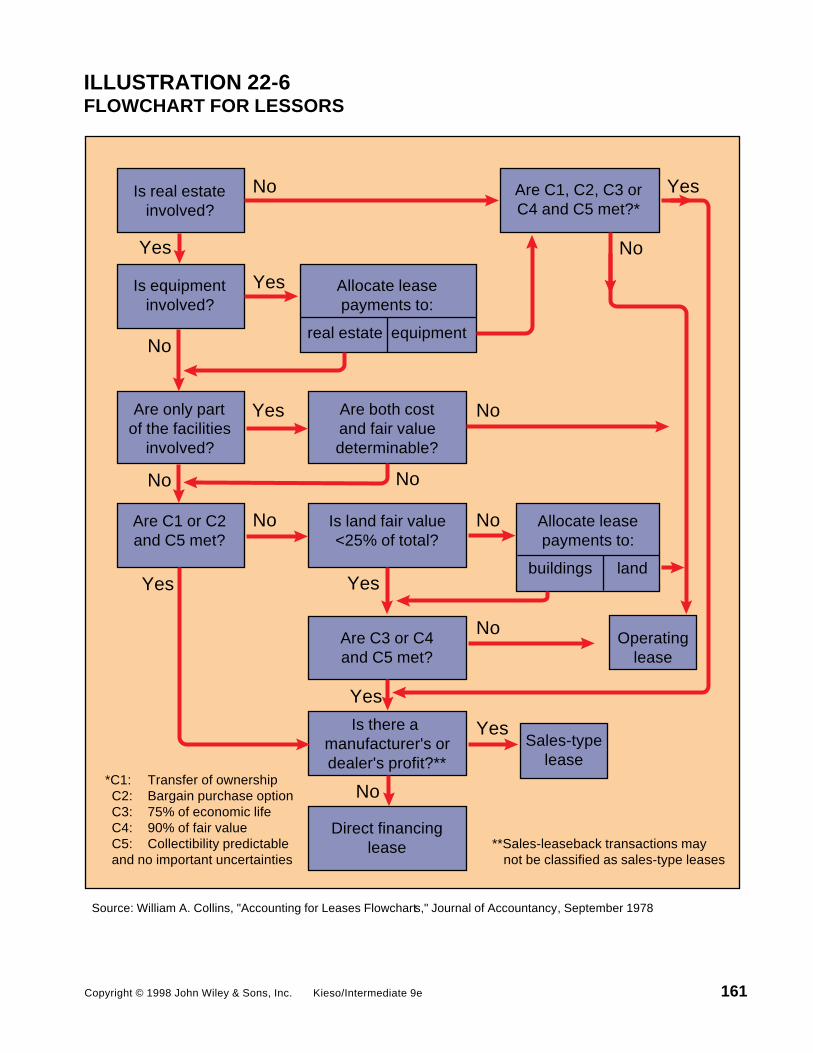

ILLUSTRATION 22-6FLOWCHART FOR LESSORS

161

Is real estateinvolved?

Is equipmentinvolved?

Are only partof the facilities

involved?

Are C1 or C2and C5 met?

*C1: Transfer of ownership C2: Bargain purchase option C3: 75% of economic life C4: 90% of fair value C5: Collectibility predictable **Sales-leaseback transactions may and no important uncertainties not be classified as sales-type leases

Source: William A. Collins, "Accounting for Leases Flowcharts," Journal of Accountancy, September 1978

Allocate leasepayments to:

real estate equipment

Are both costand fair valuedeterminable?

Is land fair value<25% of total?

Are C3 or C4and C5 met?

Is there a manufacturer's ordealer's profit?**

Direct financinglease

Are C1, C2, C3 orC4 and C5 met?*

Allocate leasepayments to:

buildings land

Operatinglease

Sales-typelease

No

Yes

Yes No

No

Yes

No

No No

Yes

No

Yes

Yes

No

Yes

No

No

Yes

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

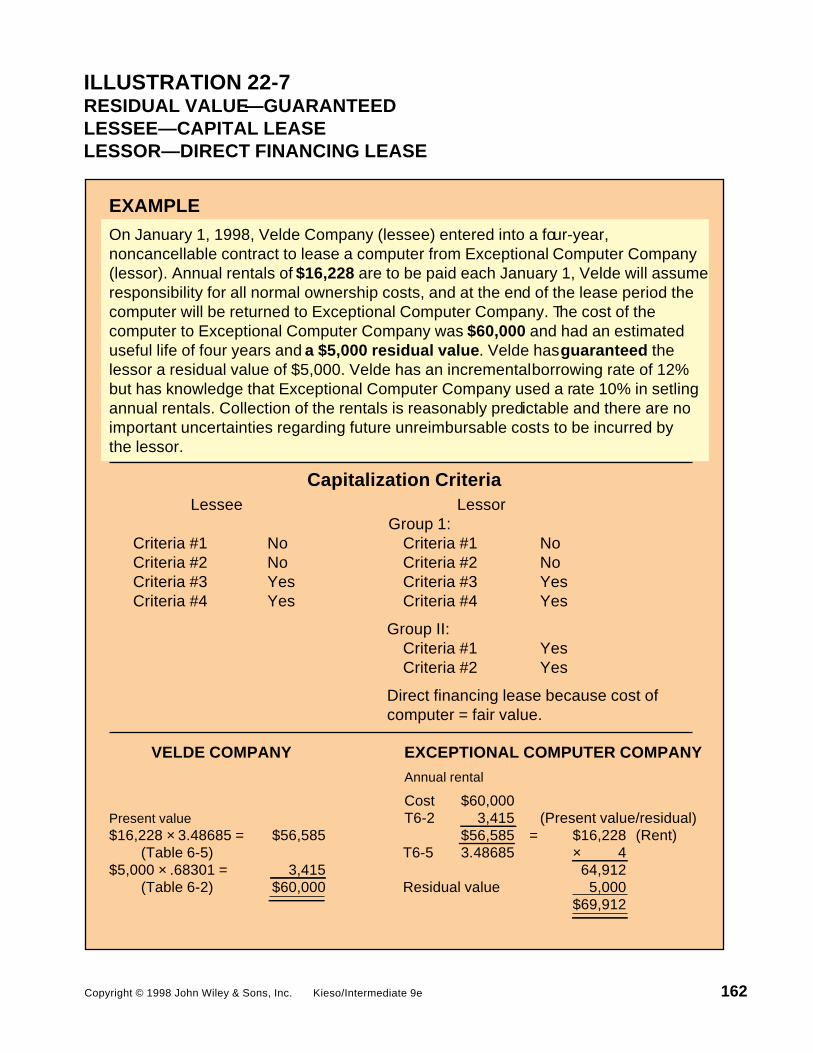

ILLUSTRATION 22-7RESIDUAL VALUE—GUARANTEEDLESSEE—CAPITAL LEASELESSOR—DIRECT FINANCING LEASE

162

EXAMPLE

On January 1, 1998, Velde Company (lessee) entered into a four-year,noncancellable contract to lease a computer from Exceptional Computer Company(lessor). Annual rentals of $16,228 are to be paid each January 1, Velde will assumeresponsibility for all normal ownership costs, and at the end of the lease period the computer will be returned to Exceptional Computer Company. The cost of thecomputer to Exceptional Computer Company was $60,000 and had an estimated useful life of four years and a $5,000 residual value. Velde has guaranteed the lessor a residual value of $5,000. Velde has an incremental borrowing rate of 12% but has knowledge that Exceptional Computer Company used a rate 10% in setling annual rentals. Collection of the rentals is reasonably predictable and there are no important uncertainties regarding future unreimbursable costs to be incurred by the lessor.

Capitalization Criteria Lessee Lessor Group 1:Criteria #1 No Criteria #1 NoCriteria #2 No Criteria #2 NoCriteria #3 Yes Criteria #3 YesCriteria #4 Yes Criteria #4 Yes

Group II: Criteria #1 Yes Criteria #2 Yes

Direct financing lease because cost of computer = fair value.

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

Annual rental

Cost $60,000Present value T6-2 3,415 (Present value/residual)$16,228 ́ 3.48685 = $56,585 $56,585 = $16,228 (Rent) (Table 6-5) T6-5 3.48685 ´ 4$5,000 ́ .68301 = 3,415 64,912 (Table 6-2) $60,000 Residual value 5,000 $69,912

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

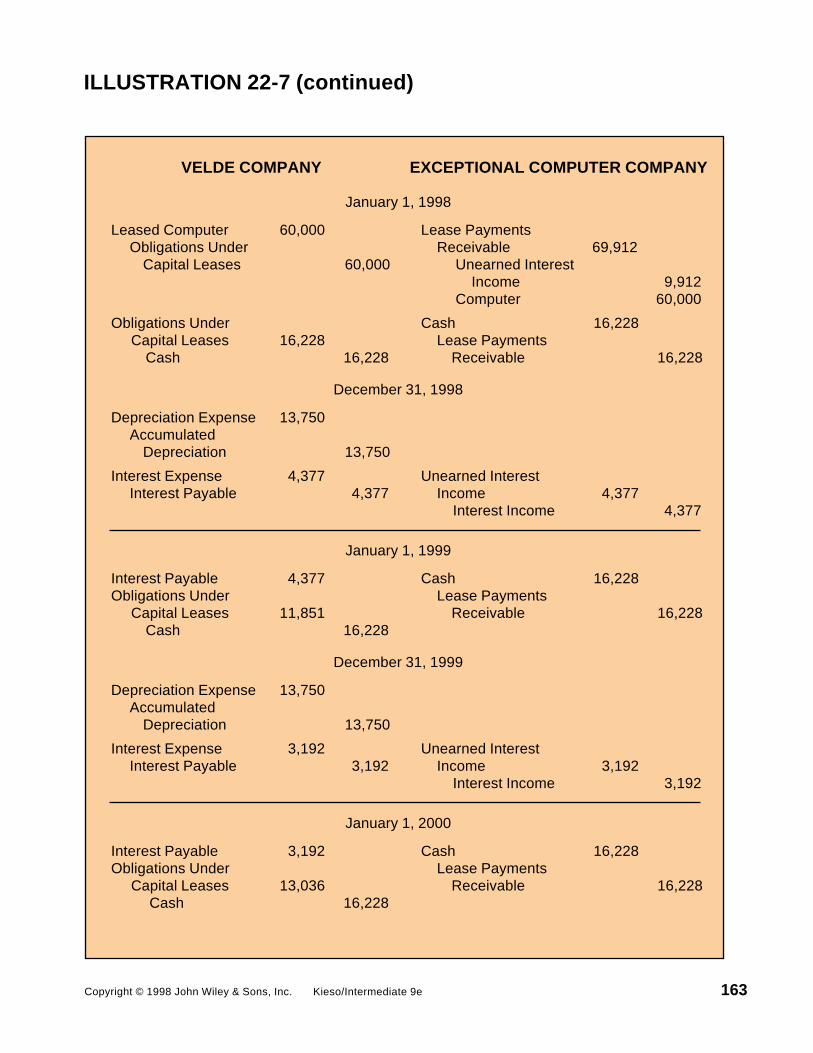

ILLUSTRATION 22-7 (continued)

163

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

January 1, 1998

Leased Computer 60,000 Lease Payments Obligations Under Receivable 69,912 Capital Leases 60,000 Unearned Interest Income 9,912 Computer 60,000

Obligations Under Cash 16,228 Capital Leases 16,228 Lease Payments Cash 16,228 Receivable 16,228

December 31, 1998

Depreciation Expense 13,750 Accumulated Depreciation 13,750

Interest Expense 4,377 Unearned Interest Interest Payable 4,377 Income 4,377 Interest Income 4,377

January 1, 1999

Interest Payable 4,377 Cash 16,228Obligations Under Lease Payments Capital Leases 11,851 Receivable 16,228 Cash 16,228

December 31, 1999

Depreciation Expense 13,750 Accumulated Depreciation 13,750

Interest Expense 3,192 Unearned Interest Interest Payable 3,192 Income 3,192 Interest Income 3,192

January 1, 2000

Interest Payable 3,192 Cash 16,228Obligations Under Lease Payments Capital Leases 13,036 Receivable 16,228 Cash 16,228

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

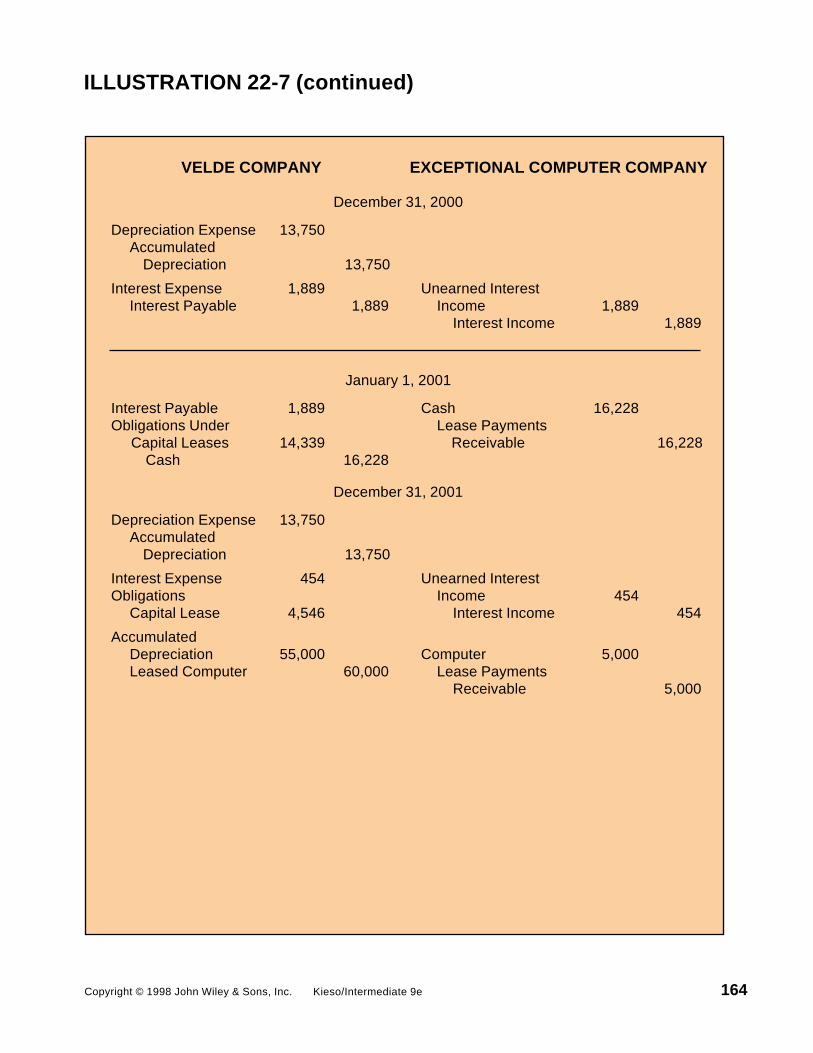

ILLUSTRATION 22-7 (continued)

164

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

December 31, 2000

Depreciation Expense 13,750 Accumulated Depreciation 13,750

Interest Expense 1,889 Unearned Interest Interest Payable 1,889 Income 1,889 Interest Income 1,889

January 1, 2001

Interest Payable 1,889 Cash 16,228Obligations Under Lease Payments Capital Leases 14,339 Receivable 16,228 Cash 16,228

December 31, 2001

Depreciation Expense 13,750 Accumulated Depreciation 13,750

Interest Expense 454 Unearned InterestObligations Income 454 Capital Lease 4,546 Interest Income 454

Accumulated Depreciation 55,000 Computer 5,000 Leased Computer 60,000 Lease Payments Receivable 5,000

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

ILLUSTRATION 22-7 (concluded)

165

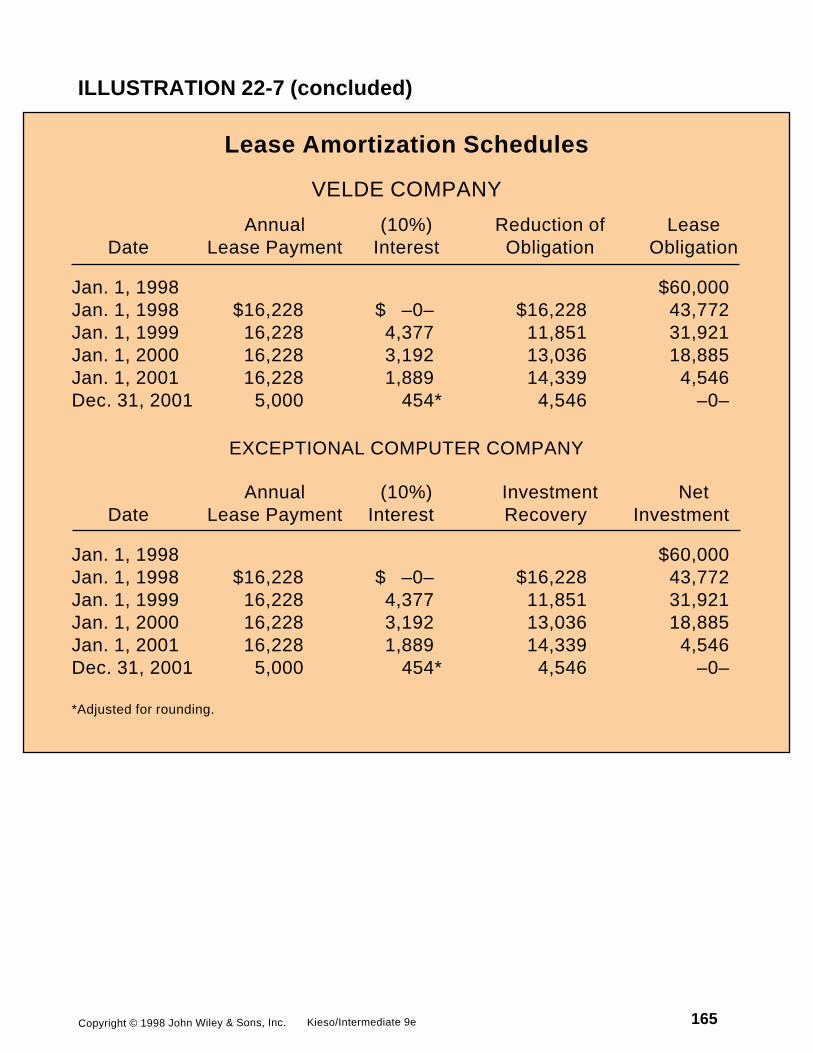

Lease Amortization Schedules

VELDE COMPANY

Annual (10%) Reduction of Lease Date Lease Payment Interest Obligation Obligation

Jan. 1, 1998 $60,000Jan. 1, 1998 $16,228 $ –0– $16,228 43,772Jan. 1, 1999 16,228 4,377 11,851 31,921Jan. 1, 2000 16,228 3,192 13,036 18,885Jan. 1, 2001 16,228 1,889 14,339 4,546Dec. 31, 2001 5,000 454* 4,546 –0–

EXCEPTIONAL COMPUTER COMPANY

Annual (10%) Investment Net Date Lease Payment Interest Recovery Investment

Jan. 1, 1998 $60,000Jan. 1, 1998 $16,228 $ –0– $16,228 43,772Jan. 1, 1999 16,228 4,377 11,851 31,921Jan. 1, 2000 16,228 3,192 13,036 18,885Jan. 1, 2001 16,228 1,889 14,339 4,546Dec. 31, 2001 5,000 454* 4,546 –0–

*Adjusted for rounding.

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

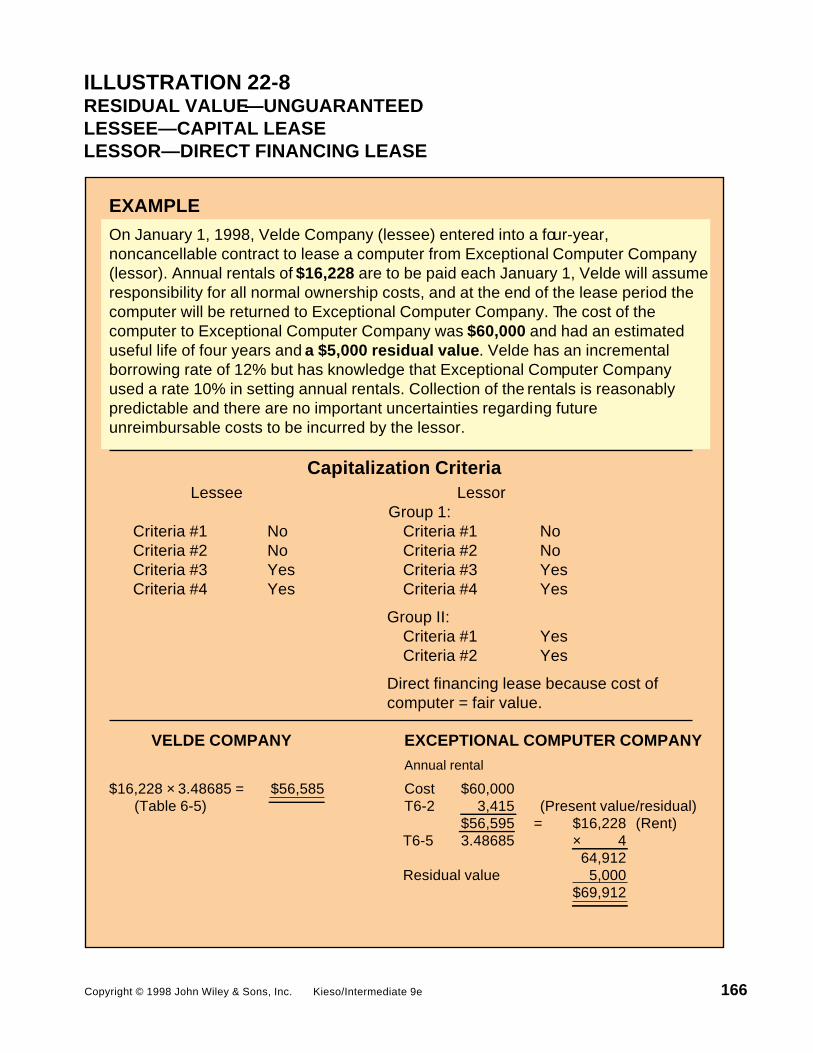

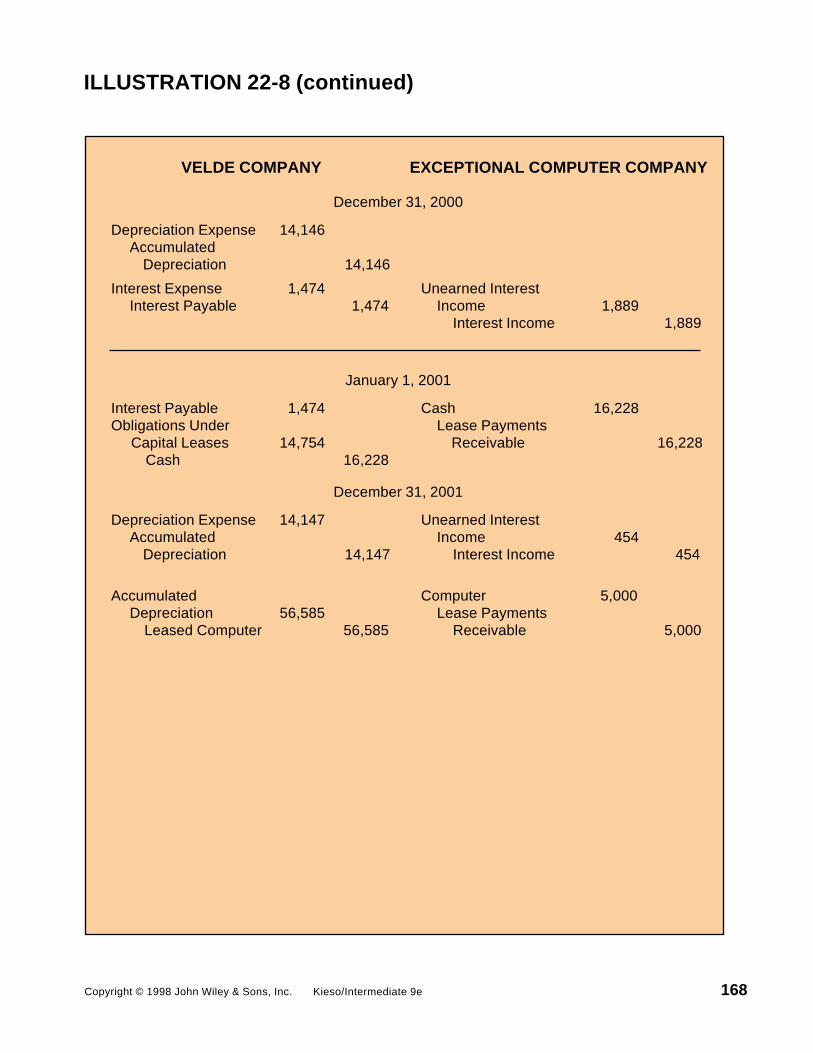

ILLUSTRATION 22-8RESIDUAL VALUE—UNGUARANTEEDLESSEE—CAPITAL LEASELESSOR—DIRECT FINANCING LEASE

166

EXAMPLE

On January 1, 1998, Velde Company (lessee) entered into a four-year,noncancellable contract to lease a computer from Exceptional Computer Company(lessor). Annual rentals of $16,228 are to be paid each January 1, Velde will assumeresponsibility for all normal ownership costs, and at the end of the lease period the computer will be returned to Exceptional Computer Company. The cost of thecomputer to Exceptional Computer Company was $60,000 and had an estimated useful life of four years and a $5,000 residual value. Velde has an incremental borrowing rate of 12% but has knowledge that Exceptional Computer Company used a rate 10% in setting annual rentals. Collection of the rentals is reasonably predictable and there are no important uncertainties regarding future unreimbursable costs to be incurred by the lessor.

Capitalization Criteria Lessee Lessor Group 1:Criteria #1 No Criteria #1 NoCriteria #2 No Criteria #2 NoCriteria #3 Yes Criteria #3 YesCriteria #4 Yes Criteria #4 Yes

Group II: Criteria #1 Yes Criteria #2 Yes

Direct financing lease because cost of computer = fair value.

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

Annual rental

$16,228 ́ 3.48685 = $56,585 Cost $60,000 (Table 6-5) T6-2 3,415 (Present value/residual) $56,595 = $16,228 (Rent) T6-5 3.48685 ´ 4 64,912 Residual value 5,000 $69,912

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

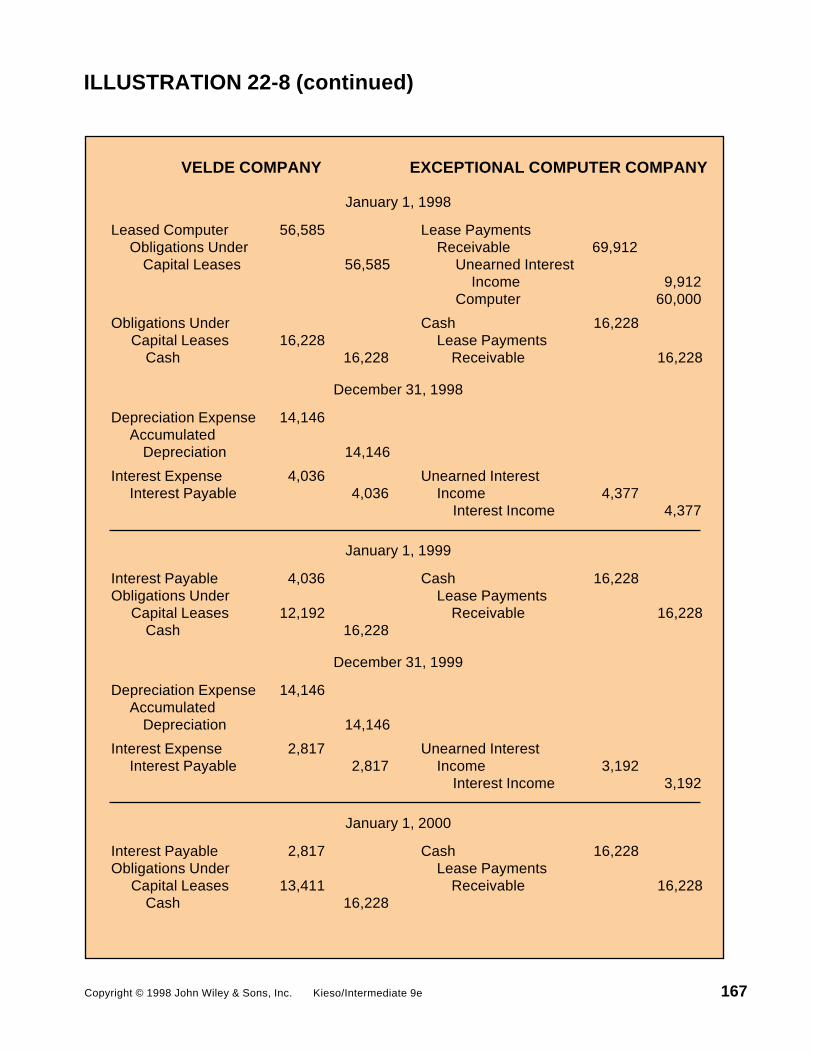

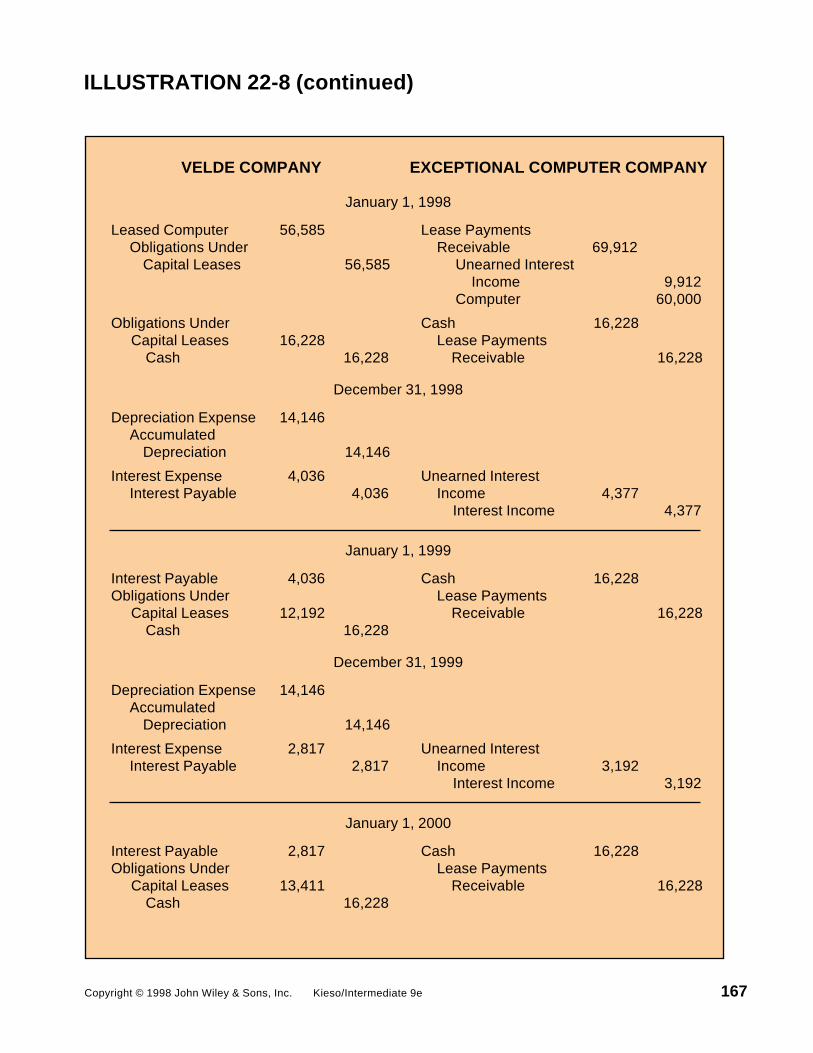

ILLUSTRATION 22-8 (continued)

167

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

January 1, 1998

Leased Computer 56,585 Lease Payments Obligations Under Receivable 69,912 Capital Leases 56,585 Unearned Interest Income 9,912 Computer 60,000

Obligations Under Cash 16,228 Capital Leases 16,228 Lease Payments Cash 16,228 Receivable 16,228

December 31, 1998

Depreciation Expense 14,146 Accumulated Depreciation 14,146

Interest Expense 4,036 Unearned Interest Interest Payable 4,036 Income 4,377 Interest Income 4,377

January 1, 1999

Interest Payable 4,036 Cash 16,228Obligations Under Lease Payments Capital Leases 12,192 Receivable 16,228 Cash 16,228

December 31, 1999

Depreciation Expense 14,146 Accumulated Depreciation 14,146

Interest Expense 2,817 Unearned Interest Interest Payable 2,817 Income 3,192 Interest Income 3,192

January 1, 2000

Interest Payable 2,817 Cash 16,228Obligations Under Lease Payments Capital Leases 13,411 Receivable 16,228 Cash 16,228

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

ILLUSTRATION 22-8 (continued)

167

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

January 1, 1998

Leased Computer 56,585 Lease Payments Obligations Under Receivable 69,912 Capital Leases 56,585 Unearned Interest Income 9,912 Computer 60,000

Obligations Under Cash 16,228 Capital Leases 16,228 Lease Payments Cash 16,228 Receivable 16,228

December 31, 1998

Depreciation Expense 14,146 Accumulated Depreciation 14,146

Interest Expense 4,036 Unearned Interest Interest Payable 4,036 Income 4,377 Interest Income 4,377

January 1, 1999

Interest Payable 4,036 Cash 16,228Obligations Under Lease Payments Capital Leases 12,192 Receivable 16,228 Cash 16,228

December 31, 1999

Depreciation Expense 14,146 Accumulated Depreciation 14,146

Interest Expense 2,817 Unearned Interest Interest Payable 2,817 Income 3,192 Interest Income 3,192

January 1, 2000

Interest Payable 2,817 Cash 16,228Obligations Under Lease Payments Capital Leases 13,411 Receivable 16,228 Cash 16,228

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

ILLUSTRATION 22-8 (continued)

168

VELDE COMPANY EXCEPTIONAL COMPUTER COMPANY

December 31, 2000

Depreciation Expense 14,146 Accumulated Depreciation 14,146

Interest Expense 1,474 Unearned Interest Interest Payable 1,474 Income 1,889 Interest Income 1,889

January 1, 2001

Interest Payable 1,474 Cash 16,228Obligations Under Lease Payments Capital Leases 14,754 Receivable 16,228 Cash 16,228

December 31, 2001

Depreciation Expense 14,147 Unearned Interest Accumulated Income 454 Depreciation 14,147 Interest Income 454

Accumulated Computer 5,000 Depreciation 56,585 Lease Payments Leased Computer 56,585 Receivable 5,000

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

ILLUSTRATION 22-8 (concluded)

169

Lease Amortization Schedules

VELDE COMPANY

Annual (10%) Reduction of Lease Date Lease Payment Interest Obligation Obligation

Jan. 1, 1998 $56,585Jan. 1, 1998 $16,228 $ –0– $16,228 40,357Jan. 1, 1999 16,228 4,036 12,192 28,165Jan. 1, 2000 16,228 2,817 13,411 14,754Jan. 1, 2001 16,228 1,474* 14,754 –0–

EXCEPTIONAL COMPUTER COMPANY

Annual (10%) Investment Net Date Lease Payment Interest Recovery Investment

Jan. 1, 1998 $60,000Jan. 1, 1998 $16,228 $ –0– $16,228 43,772Jan. 1, 1999 16,228 4,377 11,851 31,921Jan. 1, 2000 16,228 3,192 13,036 18,885Jan. 1, 2001 16,228 1,889 14,339 4,546Dec. 31, 2001 5,000 454* 4,546 –0–

*Adjusted for rounding.

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

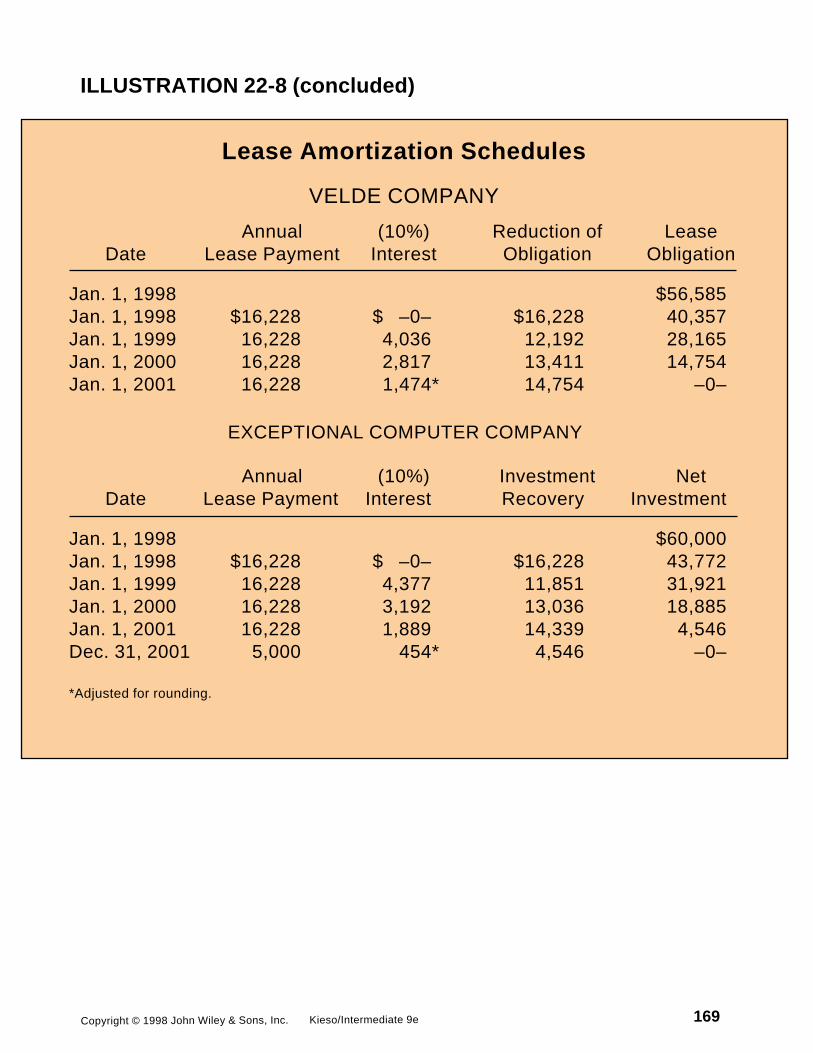

ILLUSTRATION 22-9TREATMENT OF SELECTED ITEMS INACCOUNTING FOR LEASES

170

TREATMENT OF SELECTED ITEMS IN ACCOUNTING FOR LEASES Lessor Lessee Operating Direct financing and Sales Type Operating Capital

Initial Direct Costs Capitalize and amortize Direct financing: N/A N/A over lease term in Record in separate account proportion to rent Add to net investment in lease revenue recognized Compute new effective rate that equates (normally S.L. basis) gross amt. of min. lease payments and unguar. residual value with net invest. Amortize so as to produce constant rate of return over lease term

Sales-type: Expense in period incurred

Bargain Purchases N/A Include in: N/A Include in:Option Minimum lease payments Minimum lease payments 90% test 90% test

Guaranteed N/A Include in: N/A Include in:Residual value Minimum lease payments Minimum lease payments 90% test 90% test Sales-type: Include PV in sales revenues

Unguaranteed N/A Include in: N/A Not included in:Residual value "Gross Investment in Lease" Minimum lease payments Not included in: 90% test 90% test

Sales-type: Exclude from sales revenue Deduct PV from cost of sales

Contingent Rentals Revenue in period Not a part of minimum lease payments, revenue Expense is period Not part of minimum lease payments: in period earned incurred expense in period incurred

Deprec. (Amort.) Amortize down to N/A N/A b Amortize down to estimated residual valuePeriod estimated residual over lease term or estimated economic value over estimated life economic life of asset

a Revenue Rent revenue (normally Direct financing: c Rent expense Interest Expense and Depreciation(Expense) S.L. basis) Interest revenue on net investment in lease (normally S.L. (Amortization) Expense (gross investment less unearned interest basis) income)

Depreciation expense Sales-type: Dealer profit in period of sale (sales revenue less cost of leased asset) Interest revenue on net investment in lease

a Elements of revenue (expense) listed for the above items are not repeated here (e.g., treatment of initial direct costs)b If lease has automatic passage of title or bargain purchase option, use estimated economic life; otherwise, use the lease term.c If payments are not on a S.L. basis, recognize rent expense on a S.L. basis unless another systematic and rational method is more representative of use benefit obtained from the property, in which case, the other method should be used.

Source: Adapted from Delaney, CPA Examination Review, 1994.

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

ILLUSTRATION 22-10DISCLOSURES FOR LESSEES

171

(a) For capital leases: (b) For operating leases having initial or i. The gross amount of assets at each remaining noncancellable lease terms in balance sheet date categorized by excess of one year: nature or function. This information i. Future minimum rental payments may be combined with comparable required as of the latest balance sheet information for owned assets. date, in the aggregate and for each of ii. Future minimum lease payments as the five succeeding fiscal years. of the latest balance sheet date, in ii. Total minimum rentals to be received in the aggregate and for each of five the future under noncancellable subleases succeeding fiscal years. Separate as of the latest balance sheet date. deductions for executory costs (c) For all operating leases, rental expense for included in the minimum lease each period with separate amounts for payments and for the amount of minimum rentals, contingent rentals, and imputed interest necessary to reduce sublease rentals. Rental payments under net minimum lease payments to leases with terms of a month or less that present value. were not renewed need not be included. iii. Total noncancellable minimum sublease (d) A general description of the lessee's rentals to be received in the future, as arrangements including, but not limited to: of the latest balance sheet date. i. The basis on which contingent rental iv. Total contingent rentals. payments are determined. v. Assets recorded under capital leases ii. The existence and terms of renewal or and the accumulated amortization purchase options and escalation thereon shall be separately identified in clauses. the lessee's balance sheet or notes. iii. Restrictions imposed by lease Likewise, related obligations shall be agreements, such as those concerning separately identified as obligations dividends, additional debt, and further under capital leases. Depreciation on leasing. capitalized leased assets should be separately disclosed.

Copyright © 1998 John Wiley & Sons, Inc. Kieso/Intermediate 9e

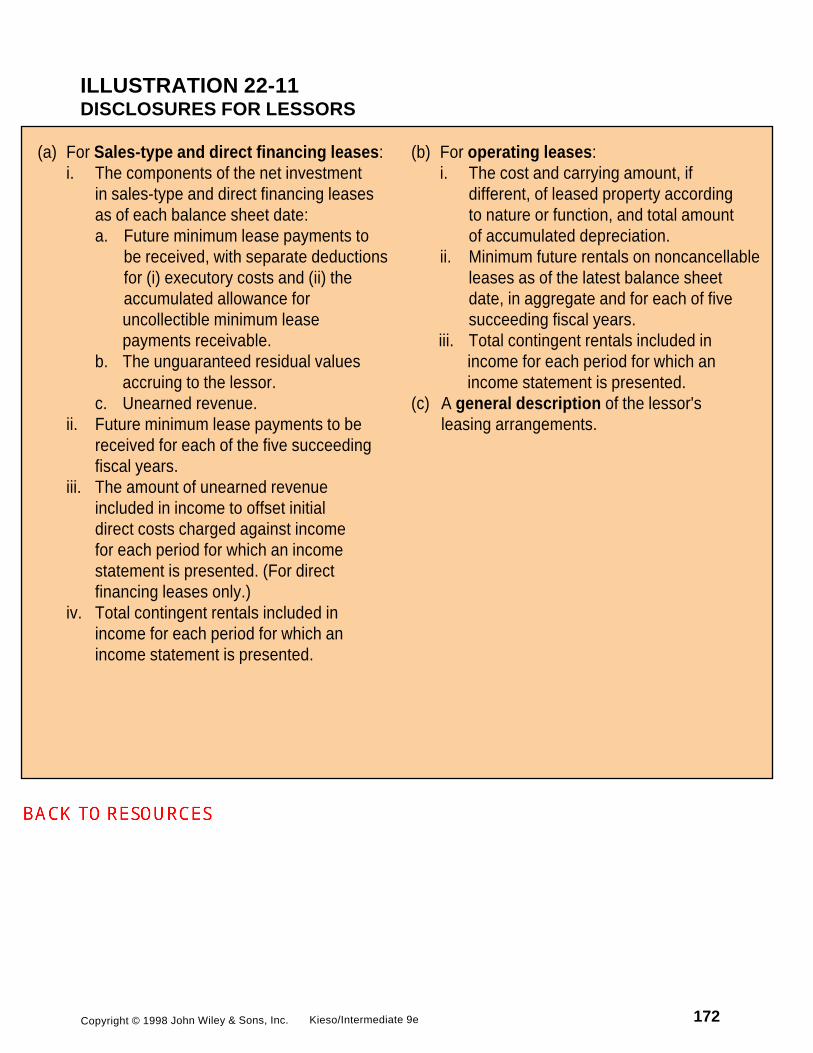

ILLUSTRATION 22-11DISCLOSURES FOR LESSORS

172

(a) For Sales-type and direct financing leases: (b) For operating leases: i. The components of the net investment i. The cost and carrying amount, if in sales-type and direct financing leases different, of leased property according as of each balance sheet date: to nature or function, and total amount a. Future minimum lease payments to of accumulated depreciation. be received, with separate deductions ii. Minimum future rentals on noncancellable for (i) executory costs and (ii) the leases as of the latest balance sheet accumulated allowance for date, in aggregate and for each of five uncollectible minimum lease succeeding fiscal years. payments receivable. iii. Total contingent rentals included in b. The unguaranteed residual values income for each period for which an accruing to the lessor. income statement is presented. c. Unearned revenue. (c) A general description of the lessor's ii. Future minimum lease payments to be leasing arrangements. received for each of the five succeeding fiscal years. iii. The amount of unearned revenue included in income to offset initial direct costs charged against income for each period for which an income statement is presented. (For direct financing leases only.) iv. Total contingent rentals included in income for each period for which an income statement is presented.

![2 김두만.ppt [호환 모드] · 2014-06-27 · AGE content of selected food items: (3) 대한당뇨병학회 35차추계학술대회 AGE content of selected food items: (3) Cbhd](https://img.pdfslide.net/doc/110x75/5f48d02c32902a293a6d6b28/2-eeeoeppt-eeoe-2014-06-27-age-content-of-selected-food-items.jpg)