Embed Size (px)

Citation preview

Highlights:

Power Africa: Country risk dynamics

Egypt scenarios: Islamism, security and democratisation

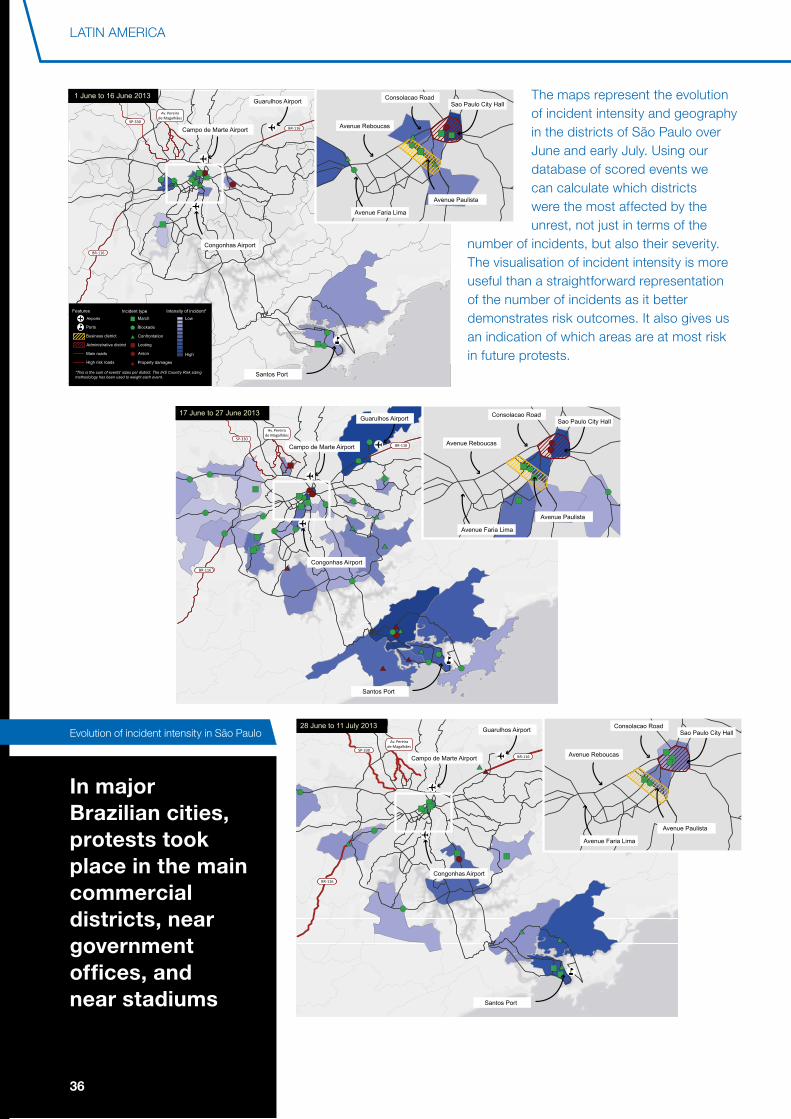

Brazil: The changing nature of protest

IHS Country Risk Quarterly

2

IHS CounTry rISkBuilding on the unique capabilities and coverage of Global Insight, WMrC, Jane’s and Exclusive

Analysis, IHS Country risk supports clients with easy data access, precise forecasting and innovative

workflow solutions. We provide more than 200 full-time economists, country risk analysts and

consultants, helping your organisation to enter new markets quickly and safely, navigate uncertainty

and prepare for every eventual outcome.

ABouT IHS (WWW.IHS.CoM) IHS (nySE: IHS) is the leading source of information, insight and analytics in critical areas that shape

today’s business landscape. Businesses and governments in more than 165 countries around the globe

rely on the comprehensive content, expert independent analysis and flexible delivery methods of IHS

to make high-impact decisions and develop strategies with speed and confidence. IHS has been in

business since 1959 and became a publicly traded company on the new york Stock Exchange in 2005.

Headquartered in Englewood, Colorado, uSA, IHS is committed to sustainable, profitable growth and

employs more than 8,000 people in 31 countries around the world.

THIrd PArTy dETAIlS And WEBSITESAny third party details and websites are given for information and reference purposes only and IHS

does not control, approve or endorse these third parties or third party websites. Further, IHS does not

control or guarantee the accuracy, relevance, availability, timeliness or completeness of the information

contained on any third party website. Inclusion of any third party details or websites is not intended

to reflect their importance, nor is it intended to endorse any views expressed, products or services

offered, nor the companies or organisations in question. you access any third party websites solely

at your own risk.

CoPyrIGHT noTICE And lEGAl dISClAIMEr© 2013 IHS. For internal use only. no portion of this publication may be reproduced, reused,

or otherwise distributed in any form without prior written consent of IHS. Content reproduced or

redistributed with IHS’ permission must display IHS’ legal notices and attributions of authorship.

The information contained in this publication is from sources considered reliable but its accuracy and

completeness are not warranted, nor are the opinions and analyses which are based upon it, and to

the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or

expense incurred by reliance on information or any statement contained herein.

TrAdEMArkSIHS and the IHS globe design are trademarks of IHS.

11 october 2013

3

EdITorIAlHeloise Capon Mike Simms

MAPSJulien Grossmann

dESIGndan Seffens

SuBSCrIPTIon EnQuIrIESHeloise [email protected]

ConTEnTS

ForEWord: 4 PoWEr AFrICA: Country risk dynamics 6 PoWEr ProJECTS In WEST AFrICA: Project risk and location analytics 14 EGyPT SCEnArIoS: Islamism, security and democratisation 22 BrAZIl: The changing nature of protest 32 IndIA: Structural vulnerabilities and outlook for policy 40

4

The IHS Country risk team faces many of the same challenges as our clients, of whom a large proportion are themselves professional analysts. The role of the analyst has changed in the era of ‘big data’. Before the information revolution, the challenge was finding information, gathering data and drawing messages from data trends. Information is now largely free and/or publicly available, and there are a number of tools for finding patterns in publicly available data. The challenge for the analyst of the future is to manage the noise, to filter through the daily avalanche of information in order to determine what is new, what is game-changing, and what really matters.

4

FOREWORD - THE ANALYST OF THE FUTURE

4

developments in what would otherwise be a complex web of influence groups and stakeholders or a steady stream of terrorist attacks or protests. Critically, these tools also mitigate the inherent downsides of working in discrete teams or matrix organisations, by making it possible to visualise and quantify the full spectrum of risks to a project, supply chain or portfolio in one holistic, coherent system.

For instance, the ability to track riots and protests in near-real time – and to understand the sentiment, interests, location, access and connections within social movements – is unprecedented. However, to add value, analysts need tools and techniques that can cope with the wide variety of social media sources, the sheer volume of data, the speed with which data is posted and the assessment of accuracy and reliability of posts. IHS Country risk is fusing open source, social media, geospatial, and human intelligence expertise, with deep country knowledge and best in class network and data science. In this issue of the IHS Country risk Quarterly, Carlos Caicedo assesses the role of social media in the June 2013 protests in Brazil, and looks forward to the 2014 World Cup, and the 2016

The challenge is not to gather more information on the issues that are keeping our clients up at night. The challenge is not even to present that information in a client-friendly, actionable format. The challenge is to identify what is likely to keep clients up at night three months, a year, three years, or ten years from now. The challenge is to provide the foresight necessary for clients to be able to factor these forthcoming issues into risk-discounted cash flows, strategic plans, contingency measures, and enterprise risk management models.

We are using an ‘all source’ approach and new techniques to facilitate faster, better development of specific risk indicators, and collection of data points that are early warnings of change to analysts’ underlying analysis assumptions and, in turn, their forecasts.

We are also developing new tools that help analysts to structure their own hypotheses and manage information overload. These tools allow analysts to proactively identify and track tripwires (events that, if they occur, signal a potential sea change). These tools also enable analysts to track dynamic

ForEWord

Kirsten Parker Senior director, IHS Country risk

5

that Federal tapering would not start immediately, Hanna luchnikava identifies a convergence of political and economic risks in India. In her feature, she assesses the corresponding policy challenges to reversing slowing growth, a sizeable current account deficit, high inflation, declining investment, and fiscal imbalances.

Finally, mapping the key influence groups in a complex case like Egypt, and identifying how the relationships between key players are likely to evolve, is a critical input into scenario analysis. Beyond the initial scenario analysis, identification of early warning indicators of change allows analysts to monitor those scenarios over time. Meda Al rowas outlines three potential scenarios for Egypt’s transition over the next year. In each case, indicators are highlighted which, if they were to happen, would make that scenario more likely to occur. She also outlines the major implications of each scenario.

As ever, we are eager for your feedback on our techniques, the topics we’ve selected, and the conclusions and forecasts we’ve reached. Interaction with our customers ensures our vision of innovation in data, analysis, and forecasting methodology is tested and is as robust and useful as possible.

Finally, please stop by and see us. We have a daily analysis and forecasting meeting (9:15am) in london and we welcome guests and feedback

Foreword

olympic Games. Two case studies on the predictive value of integrated social media analysis in Turkey and Bahrain are also featured.

Geospatial tools are also key components of the toolkit for the analyst of the future. Geospatial platforms allow analysts to visualise and quantify risks to specific projects and portfolios. Following uS President Barack obama’s announcement of the ‘Power Africa’ initiative to enhance power infrastructure in six African countries, natznet Tesfay looks at infrastructure plans and measures to encourage local value addition in the region, before examining nigeria more closely as a case study. david Hunt shows how the use of location Analytics produces unique insight, and allows the quantification of those intelligence assessments so that risks can be compared, differentiated, modelled, and integrated into strategy and planning decision-making. david demonstrates the use of these tools to assess power projects in West Africa, helping strategy and business development teams to identify risks and opportunities. He then looks in granular detail at projects in nigeria to show how geospatial intelligence can deliver deep insight into risks to security, supply chain, project cargo, and personnel.

As a global team, with a range of technical and industry expertise, IHS is uniquely placed to identify cross-border risks. For instance, as a large and liquid emerging market with deteriorating fundamentals, India has been exposed to portfolio adjustments away from emerging market investments. despite the September 2013 announcement by Ben Bernanke

CrQ

The Analytics dashboard from Foresight location Analytics is one of the ways in which IHS Country risk is fusing intelligence inputs, local knowledge, and geospatial tools to visualise and quantify risk.

AFRICA

6

Natznet Tesfay Senior Manager, Africa, IHS Country risk

POWER AFRICA: COUNTRY RISK DYNAMICS

In July 2013, uS President Barack obama announced the ‘Power Africa’ initiative, pledging uSd7 billion to enhance power infrastructure in six African countries (nigeria, Ghana, liberia, Ethiopia, kenya, and Tanzania). This will be matched by uSd9 billion private sector investment, including uSd2 billion in loans from Standard Chartered Bank. As investors increasingly demonstrate an appetite for investing in power projects in sub-Saharan Africa, natznet Tesfay looks at plans to reduce the current infrastructure deficit in the region and measures to encourage local value addition, before examining the situation in nigeria and risk mitigation strategies more closely.

WHy PoWEr AFrICA?

The ‘Power Africa’ announcement comes in the context of increasing donor and domestic government focus on the power sector, as unreliable power supply and high costs negatively affect individual firms’ productivity, reducing countries’ competitiveness, and slowing economic growth. A 2010 French development Agency report estimated that electricity shortfalls can cost up to 5% of annual GdP, with a 2013 World Bank report identifying that 39 sub-Saharan countries experience daily power outages. In 2013, the World Bank reported that the manufacturing sector experiences power outages for an average of 56 days per year. A 2009 report identified that frequent blackouts (60 days or more each year) cost firms in the region of approximately 10–12% of sales.

WHy PoWEr AFrICA?

Sub-Saharan Africa has approximately 80GW of installed capacity, of which 46GW is located in South Africa. To reach the goal of universal access to electricity by 2030, the International renewable Energy Agency estimated in January 2012 that the region would need an additional 250GW capacity, which would in turn require at least uSd40 billion in investment per year to refurbish and construct power plants. Considering that the region is currently installing approximately 1–2GW capacity per year, this goal is unlikely to be achieved.

According to the African development Bank, the key obstacle to increasing power generation capacity is the high cost of production, with the majority of dedicated expenditure spent on maintenance of ageing infrastructure and operations. In recent years, there has been increasing momentum behind legislative reform in the sub-Saharan region to engage the private sector in the roll-out of critical power supply infrastructure. The prioritisation of electricity provision in the development agenda is the cornerstone of many African economic growth plans.

Ethiopia provides a prime example, embarking on an ambitious plan to build the continent’s largest hydroelectric project, the 6,000MW capacity Grand Ethiopian renaissance dam, which is planned to be commissioned in 2018. To construct the controversial megaproject, the Ethiopian government has required local financial institutions to buy government bonds. Its high import needs have also contributed to the depletion of the country’s foreign exchange reserves, which currently stand at approximately two months’ import cover.

6

Power Africa - Country risk dynamics 7

POWER AFRICA: COUNTRY RISK DYNAMICS

However, with competitive labour costs in Ethiopia, the project is in line with the government’s broader economic objectives of becoming a manufacturing powerhouse as operating costs rise in Asia, and exporting higher value goods.

To keep the benefits of such manufacturing and related services local in a region characterised by low tax receipts, high unemployment, and a high proportion of young people, a number of African governments have put forward legislation over the past two years to penalise firms for exporting unprocessed natural resources. This ranges from higher export levies to outright bans.

However, to comply with local beneficiation regulations, companies have to pay high input costs for emergency diesel generated power when there are power cuts. Furthermore, while these policies for local value addition provide employment opportunities, reducing one potential driver of civil unrest, power grids with limited capacity cannot cope with increased demand. As a result, risks of service delivery protests, which have already broken out in Senegal, Guinea, and South Africa, will heighten. unrest provoked by shortfalls will place heavy power users and generation firms at the most risk of disruption by affected communities, who often expect the provision of utilities alongside investment.

Power Africa - Country risk dynamics 7

PA-11247177

AFRICA

8

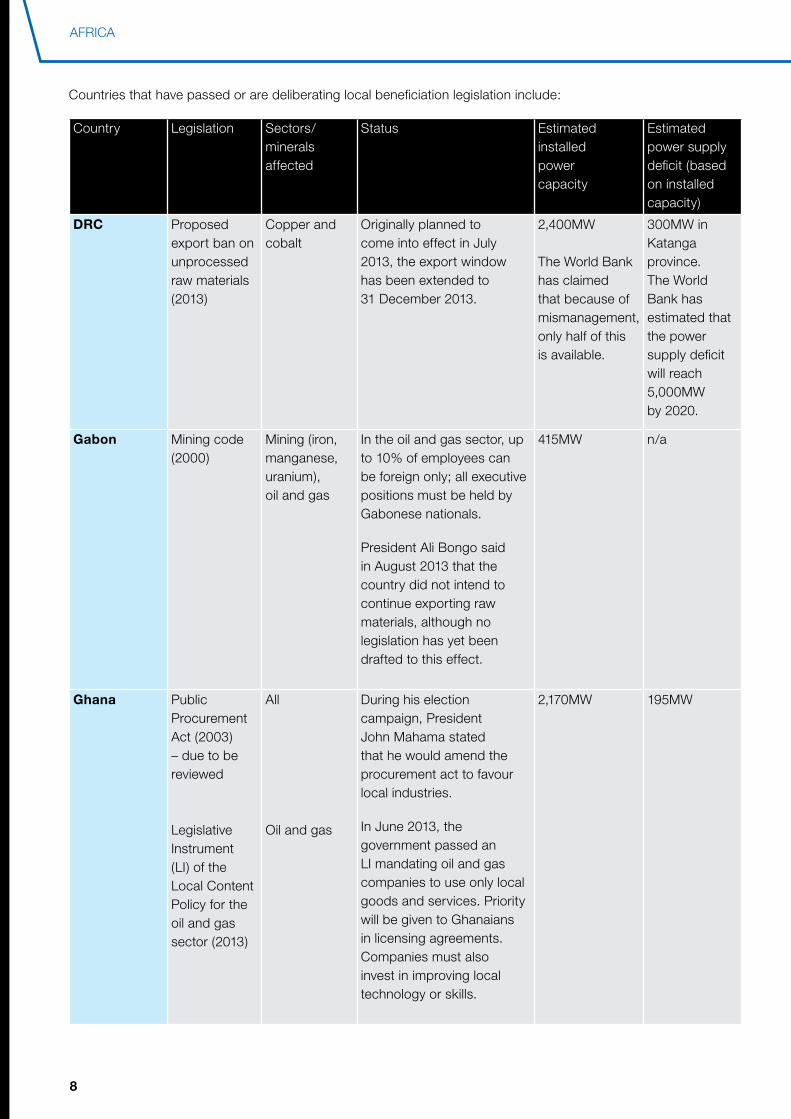

Countries that have passed or are deliberating local beneficiation legislation include:

Country legislation Sectors/ minerals affected

Status Estimated installed power capacity

Estimated power supply deficit (based on installed capacity)

DRC Proposed export ban on unprocessed raw materials (2013)

Copper and cobalt

originally planned to come into effect in July 2013, the export window has been extended to 31 december 2013.

2,400MW The World Bank has claimed that because of mismanagement, only half of this is available.

300MW in katanga province. The World Bank has estimated that the power supply deficit will reach 5,000MW by 2020.

Gabon Mining code (2000)

Mining (iron, manganese, uranium), oil and gas

In the oil and gas sector, up to 10% of employees can be foreign only; all executive positions must be held by Gabonese nationals.

President Ali Bongo said in August 2013 that the country did not intend to continue exporting raw materials, although no legislation has yet been drafted to this effect.

415MW n/a

Ghana Public Procurement Act (2003) – due to be reviewed legislative Instrument (lI) of the local Content Policy for the oil and gas sector (2013)

All oil and gas

during his election campaign, President John Mahama stated that he would amend the procurement act to favour local industries.

In June 2013, the government passed an lI mandating oil and gas companies to use only local goods and services. Priority will be given to Ghanaians in licensing agreements. Companies must also invest in improving local technology or skills.

2,170MW 195MW

Power Africa - Country risk dynamics 9

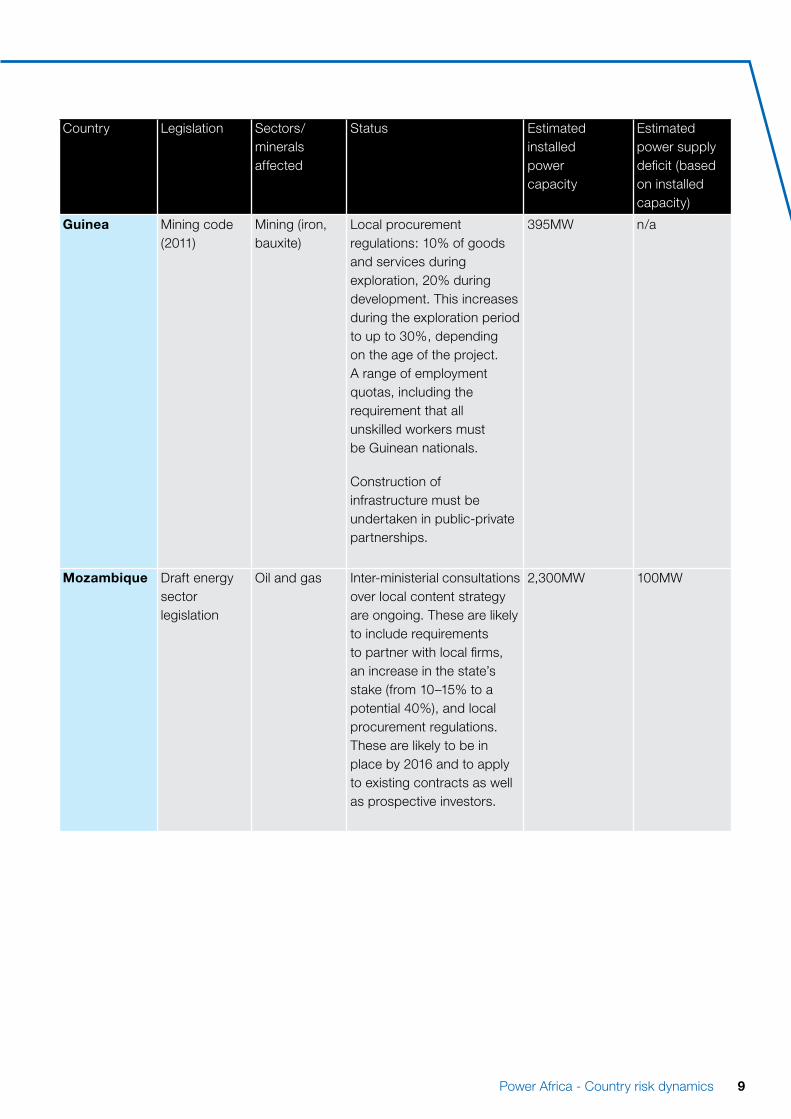

Country legislation Sectors/ minerals affected

Status Estimated installed power capacity

Estimated power supply deficit (based on installed capacity)

Guinea Mining code (2011)

Mining (iron, bauxite)

local procurement regulations: 10% of goods and services during exploration, 20% during development. This increases during the exploration period to up to 30%, depending on the age of the project. A range of employment quotas, including the requirement that all unskilled workers must be Guinean nationals.

Construction of infrastructure must be undertaken in public-private partnerships.

395MW n/a

Mozambique draft energy sector legislation

oil and gas Inter-ministerial consultations over local content strategy are ongoing. These are likely to include requirements to partner with local firms, an increase in the state’s stake (from 10–15% to a potential 40%), and local procurement regulations. These are likely to be in place by 2016 and to apply to existing contracts as well as prospective investors.

2,300MW 100MW

AFRICA

10

Country legislation Sectors/ minerals affected

Status Estimated installed power capacity

Estimated power supply deficit (based on installed capacity)

South Africa draft Mineral and Petroleum resources development Act

Mining (diamond, gold, platinum, coal, manganese), oil and gas

Amendments are still at the hearing stage. These would allow the minister of mineral resources to declare certain mineral resources as strategic and allow for an increase in government ownership of companies or projects. The minister would also be able to determine the percentage and developmental pricing conditions required for benefication. Power company Eskom has called for coal to be protected.

44,175MW

Eskom reported that only 34,970MW was available in June 2013.

394MW

Tanzania Government directive (August 2013) – no set legislation yet

Mining (gold) The government has announced that the 13 largest foreign mining companies must procure at least 80% of goods and services from local businesses by 2015. As of August 2013, the companies had acquired an average of 38.6% locally.

1,509MW 133MW

Uganda Petroleum (refining, Conversion, Transmission and Midstream Storage) Act (2013) Export ban (January 2013)

oil and gas Mining (iron)

The law allows for the construction of the 30,000bpd Greenfield refinery (originally the government had pushed for 180,000bpd capacity). The government has agreed to construct a pipeline for crude exports. In January 2013, President yoweri Museveni banned the export of iron ore in order to promote the local steel industry.

550MW 170MW (october 2012)

The supply deficit has probably decreased from this level as capacity has since been ramped up.

Power Africa - Country risk dynamics 11

Country legislation Sectors/ minerals affected

Status Estimated installed power capacity

Estimated power supply deficit (based on installed capacity)

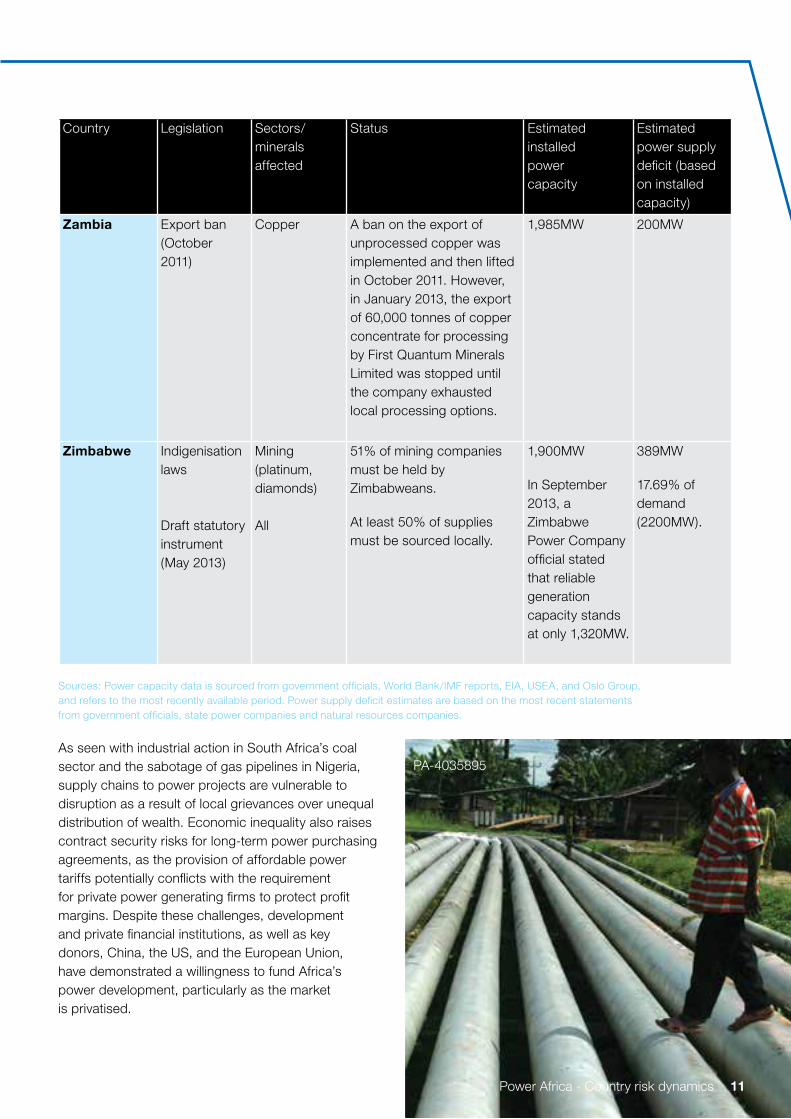

Zambia Export ban (october 2011)

Copper A ban on the export of unprocessed copper was implemented and then lifted in october 2011. However, in January 2013, the export of 60,000 tonnes of copper concentrate for processing by First Quantum Minerals limited was stopped until the company exhausted local processing options.

1,985MW 200MW

Zimbabwe Indigenisation laws draft statutory instrument (May 2013)

Mining (platinum, diamonds) All

51% of mining companies must be held by Zimbabweans.

At least 50% of supplies must be sourced locally.

1,900MW

In September 2013, a Zimbabwe Power Company official stated that reliable generation capacity stands at only 1,320MW.

389MW

17.69% of demand (2200MW).

Sources: Power capacity data is sourced from government officials, World Bank/IMF reports, EIA, uSEA, and oslo Group, and refers to the most recently available period. Power supply deficit estimates are based on the most recent statements from government officials, state power companies and natural resources companies.

As seen with industrial action in South Africa’s coal sector and the sabotage of gas pipelines in nigeria, supply chains to power projects are vulnerable to disruption as a result of local grievances over unequal distribution of wealth. Economic inequality also raises contract security risks for long-term power purchasing agreements, as the provision of affordable power tariffs potentially conflicts with the requirement for private power generating firms to protect profit margins. despite these challenges, development and private financial institutions, as well as key donors, China, the uS, and the European union, have demonstrated a willingness to fund Africa’s power development, particularly as the market is privatised.

Power Africa - Country risk dynamics 11

PA-4035895

AFRICA

12

Development plans

President Goodluck Jonathan has prioritised power provision as a flagship reform and key electoral promise. nigeria has one of the region’s most comprehensive power reform plans.

The government has targeted a ten-fold increase in power to 40,000MW by 2020, requiring an estimated uSd80 billion investment. In July 2013, it announced major deals signed during Jonathan’s visit to China, including a uSd20 billion memorandum of understanding (Mou) with Power Construction Corporation of China to generate 20,000MW of electricity. The government also signed an Mou with General Electric Company in March 2012 for the company to invest uSd10 billion in power plants.

The reform programme also includes the sale of 17 successor companies of the underperforming power parastatal, the Power Holding Company of nigeria (PHCn). In october 2013, the Bureau for Public Enterprises (BPE) announced that the sale of 60% equity stakes in nine distribution companies, and between 51% and 100% stakes in five generation companies, had raised over uSd2.3 billion, and that the government would hand over operations at these facilities on 1 november 2013. The government also handed over management control of the Transmission Company of nigeria (TCn) to Canadian firm Manitoba Hydro International in March 2013 for a uSd24 million management contract spanning three years.

The next phase of privatisations within the power industry will be the niger delta Power Holding Company (ndPHC)’s bidding round for 10 integrated power plants, constructed as part of former-President olusegun obasanjo’s 2004 national Integrated Power Project (nIPP) initiative, and designed to generate between 190MW–1,074MW each. Successful bidders are slated to take control of acquired nIPP assets by June 2014. As PHCn’s unbundling comes to a close, the nigerian Electricity regulatory Commission will be developing a regulatory framework for the sector.

The nigerian government is seeking to replicate the success of the 2001 deregulation of mobile telephony, which profited from the strong growth in consumer spending for services. The involvement of local business moguls – especially those profiting

CASE STudy: nIGErIA

from diesel and generator imports, in PHCn’s privatisation – points to the drive within nigeria’s private sector to see through this power reform. This is notable given previous unsuccessful attempts.

While momentum and optimism over the power sector’s re-structuring has grown, risks of contract frustration are likely to emerge as a result of the following factors:

• domestic businesses associated with the political elite are likely to seek to leverage influence and secure preferential treatment during tender and bidding processes. resultant contracts will be exposed to higher risks of politically motivated probes.

• disputes between government agencies with overlapping authority are likely to delay the award of licences. For example, in november 2012, local media claimed members of the government were calling for the TCn management contract to be cancelled as the BPE was not authorised to award such a contract by the 2007 Public Provision Act – although it was not clear which other body would be authorised to do so.

• outstanding debts, repairs or other unresolved issues such as wage disputes affecting acquired assets may not emerge until investors take over operations. Additionally, while plans to enhance electricity supply are underway, the expansion in transmission capacity is lagging.

Increased opposition to Jonathan makes politically motivated contract reviews or corruption probes particularly likely

on 31 August, seven state governors who oppose Jonathan’s expected re-election bid at the 2015 elections, broke away from the ruling People’s democratic Party (PdP) to form the new PdP faction. on 3 September, 57 PdP members from the House of representatives and 26 senators also voiced their support for the new PdP. The number of members of the House of representatives pledging support to the new PdP is expected to rise, particularly in light of the increasing antagonism between the president and the lower house, demonstrated by MPs’ launch of probes into contracts awarded by Jonathan’s administration and repeated attempts to impeach the president. The president no longer enjoys a majority in either house,

12

Power Africa - Country risk dynamics 13

frustrating his ability to pass legislation through the national Assembly, notably the Petroleum Industry Bill (PIB). The PIB has already been stalled for five years and the consequent regulatory uncertainty has nearly halted new investments. It is probable that a fragile agreement will be reached between the PdP and the new PdP to maintain party integrity, although this is unlikely to include a pledge from Jonathan not to stand in the 2015 election. Members of the new PdP are increasingly likely to stall Jonathan’s reform agenda, probably manifested by more probes into contracts awarded under his tenure, to undermine his public image and pressure him to concede to their demands.

Inconsistent gas supply is a further obstacle to power reform

Many gas pipelines are still under construction, including the government’s proposed uSd5 billion northern and Eastern pipeline networks connecting Ajaokuta-kaduna-kano and Qua Ibo/Calabar-Ajaokuta respectively. The okoloma and Escravos pipelines, operated by royal dutch Shell Plc and Chevron Corp respectively, were damaged in attacks, limiting distribution to eight power stations. The power minister said that increased rainfall and vegetation along the transmission lines amplified the damage. Pipelines leading from the niger delta to other regions face the highest risk of attack, with youth and militant groups resentful that the state’s resources are being used to develop the rest of the country despite local shortfalls. regulatory uncertainty stemming from the delayed passage of the PIB has also hampered the development of the gas sector. Furthermore, oil producers are at risk of fines for non-compliance with government directives to reduce gas flaring, especially in the event of insufficient gas supplies for power generation.

Risk mitigation strategies for capital intensive, long term projects

Alongside local stakeholder engagement strategies, guarantees can mitigate investors’ risks in long-term projects. Private sector insurance markets offer competitive rates, but cover is likely to be short-term for a power project. When covering delayed or non-payment risks, private sector insurers prefer industries earning foreign exchange, and, in the case of utility firms, worry that governments will bow to popular pressure and force them to lower their tariffs, impairing their payment capacity.

Guarantees from public bodies like the Multilateral Investment Guarantee Agency (MIGA), the overseas Private Investment Corporation (oPIC), and export-credit agencies, can give investors payment protection over periods suitable for long-term capital intensive projects. rates are higher than private markets and coverage is likely to be subject to greater scrutiny (e.g. environmental impact assessments), as a result of the World Bank’s reputational risk concerns.

In countries like nigeria, with newly created bulk buyers of power, and with either a poor or unproven payment record, MIGA can obtain guarantees from finance ministries. Concerns over the country’s reputation, and consequent access to grants and loans, provide a deterrent against payment or contract violation on a MIGA insured project. loss claims here are therefore very rare.

Further guarantees can be sought under the World Bank’s International development Association’s (IdA) Partial risk Guarantees (PrG). IdA PrG programmes are only offered in some countries, including nigeria, Angola, kenya, Cameroon, Mozambique, Tanzania, Ethiopia, uganda, and Ghana. These provide liquidity support to help entities avoid termination of payment (a precursor to claiming for a lose from MIGA). The African development Bank is also beginning to offer liquidity support similar to PrG.

In nigeria, improved electricity supply and consequent job growth would boost public confidence in a government plagued by jihadist attacks, oil theft and regional polarisation. However, optimism over restructuring is not entirely shared, and lingering grievances pose risks of disruption to the power sector, either immediately – in the form of strikes by PHCn workers who fear mass retrenchment – or after 2015, when the niger delta amnesty programme for former militants is due to expire, exposing gas supply lines to higher risks of sabotage. like nigeria, many other African countries aim to leverage their natural resources, including gas, coal, and even uranium, to fuel electricity generation more sustainably. Still, for power sector investors, competing ownership claims over resources, as in the niger delta, and expectation management, make local stakeholder engagement strategies essential alongside other means of investment guarantees CrQ

13Power Africa - Country risk dynamics

AFRICA

14

David Hunt Senior Manager, risk Indicators & Analytics, IHS Country risk

POWER PROJECTS IN WEST AFRICA: PROJECT RISK AND LOCATION ANALYTICS

In reaction to ‘Power Africa’, david Hunt shows how location Analytics can make sense of a spectrum of risks across dozens of power projects in West Africa, helping strategy and business development teams to identify opportunities in what is considered by many to be an extremely high risk environment. He then looks in granular detail at projects in nigeria to show how geospatial intelligence can deliver insight into risks that affect project security, supply chain and project cargo and personnel.

There are two key complementary aspects to location Analytics – the use of geospatial intelligence to better understand risks in granular detail and produce unique insight, and the quantification of those intelligence assessments so that risks can be compared, differentiated, modelled and integrated into strategy and planning decision-making.

1414

In this graphic, planned project capacity (MW) is represented by bubble size. Relative political and security risk as forecast by IHS Country Risk is represented by colour. It is evident that the highest risk projects are not the largest by capacity. However, there are a number of large-scale projects, mostly in Nigeria that are towards the mid/top end of risk

Power projects in West Africa: Project risk and location analytics 15

SoubreCote d'Ivoire

SouapitiGuinea

SendouSenegal

Onitsha (Hydro)Nigeria

Makurdi (Hydro)Nigeria

LokojaNigeria

Kpone KTPP(VRA)

KandadjiNiger

KaletaGuinea

Juale

IkomNigeria

GouinaMali

GambouNiger

Fomi

Felou

EnuguNigeria

Egbema (NIPP)Nigeria

DomunliGhana

BuiGhana

Bonny Island(ExxonMobil)

Nigeria

Alaoji (NIPP)Nigeria

Akwa Ibom(NIPP)

AdjaralaBeninAba IPP

GhanaNzema

(NIPP)Omoku

Low risk High risk

POWER PROJECTS IN WEST AFRICA: PROJECT RISK AND LOCATION ANALYTICS

15

SoubreCote d'Ivoire

SouapitiGuinea

SendouSenegal

Onitsha (Hydro)Nigeria

Makurdi (Hydro)Nigeria

LokojaNigeria

Kpone KTPP(VRA)

KandadjiNiger

KaletaGuinea

Juale

IkomNigeria

GouinaMali

GambouNiger

Fomi

Felou

EnuguNigeria

Egbema (NIPP)Nigeria

DomunliGhana

BuiGhana

Bonny Island(ExxonMobil)

Nigeria

Alaoji (NIPP)Nigeria

Akwa Ibom(NIPP)

AdjaralaBeninAba IPP

GhanaNzema

(NIPP)Omoku

Low risk High risk

PA-4443973

AFRICA

1616

PArT 1: ProJECT rISk CoMPArISon

This case study is not an investment analysis, but a study of political and security risks. We looked at 48 power generation projects listed as planned or under construction in the West African countries of Senegal, Mali, niger, Guinea, Cote d’Ivoire, Ghana, Togo, Benin, and nigeria, representing nearly 11,000MW of total planned capacity.

our starting point was to access detailed project data from the IHS EdIn database, and country-level political risk scores from the IHS Foresight

Political risk platform. As standard, we do not provide political risk scores at a higher geographical granularity than country-level as – although risks can vary markedly by sector and project – they are not typically highly differentiated by location within a country. We also queried location-specific scores from the IHS Foresight location Analytics risk maps for political violence – this model reflects the high differentiation of terrorism, civil unrest and war risks within a country – producing scores at 500m2 resolution. The scores are combined in a custom weighted index of highest to lowest risk projects.

The evolution of risk over time is critically important for business planning. As well as helping to identify emergent opportunities or new threats, risk volatility indicates the stability of a country and the potential for future downside risks. on the next page, you can see the significant change in security risk for projects in Mali between 2012 and 2013 (increases of up to 200% as the country suffered a major insurgency in the north).

While risks have declined from their peak after French-led intervention displaced Islamist insurgents, violent risks in northern areas are still far higher than previously. Elsewhere in West Africa, risks have, by and large, declined at the project locations.

While the very highest risk (red) projects are not the largest by capacity, there is a tier of large-scale projects, mostly in nigeria, that are towards the mid/top end of forecast risk.

differentiating by risk type allows planning to be tailored more precisely to the specific nature of the risks faced by a project. Civil unrest scores for each project location forecast the risk of property damage and operational disruption due to strikes, riots or civil commotion. The scatter plot on the right benchmarks the location-specific score for a project against the overall country score. This reveals if the project is located in a relative civil unrest hotspot within the country.

MaliNiger

Nigeria

Mauritania

Ghana

Guinea

Gabon

Cameroon

Côte d'Ivoire

Senegal

Burkina Faso

Benin

Liberia

TogoSierra Leone

Algeria

Congo

Guinea-Bissau

Equatorial Guinea

High MWA production

Low MWA production

Low High

Total MWA produced

Project Distribution

Kpone KTPP (VRA)

Katsina (Solar)Sambangalou

Dadin-KowaKaduna IPP

Calavi IPPLekki EPZ

KandadjiGambou

Hemang

Adjarala

Domunli

Souapiti

Sendou

Kiri IPP

Soubre

Gouina

Nzema

Gurara

Bissau

Kenie

Mopti

Juale

Kano

Fomi

Ikom

IlorinBui

Project distribution

Power projects in West Africa: Project risk and location analytics 17

Ilorin Enugu Kano Makurdi (Hydro)

Soubre

Sendou

MoptiKenie

Souapiti

Kpone KTPP (VRA)

Sambangalou

Adjarala

Kandadji

Tiopo-Kogon river

Asset is at a lower riskthan the country average

Guinea: Outside of civil unresthotspot Conakry, but protestsoften triggered by disruptions topower supplies

Senegal: Protests oftenrelated to discontent with disrupted power supplies

Asset is at a higher risk than the country average

5.0

4.0

3.0

2.0

1.0

4.5

3.5

2.5

1.5

0.5

0.0

4.03.02.01.0 4.53.52.51.50.50.0

Civil unrest asset specific location score

Civ

il un

rest

cou

ntry

sco

re

-0.6 2.2

% change

COUNTRY PLANT NAMEBenin Adjarala

Calavi IPPDyodyon

Cote d'Ivoire SoubreGhana Bui

DomunliHemangJualeKpone KTPP (VRA)NzemaTema (Osonor)

Mali FelouGouinaKenieMopti

Nigeria Aba IPPAgbara IPP (Anita)Agbara IPP (Shoreline)Akwa Ibom (NIPP)Alaoji (NIPP)Bonny Island (ExxonMobil)Dadin-KowaEgbema (NIPP)EnuguGuraraIkomIlorinKaduna IPPKanoKashimbillaKatsina (Solar)Kiri IPPLekki EPZLokojaMagboroMakurdi (Hydro)Omoku (NIPP)Onitsha (Hydro)

-0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2

Change in risk to projects 2012-2013

Project civil unrest scores

Tracking the evolution of risks to a project over time is possible through location-specific intelligence monitoring. From IHS Foresight location Analytics you could set up a weekly alert based on intelligence events occurring within 5km of all the project locations. This alert might highlight protests specifically targeting your construction project. other intelligence may not identify actions specifically targeted at the power projects, but may indicate security risks to the facility, its personnel or supply chain.

AFRICA

18

once project opportunities have been evaluated across the region, location Analytics can be deployed to deliver drill down insights into the specific risks to project viability through delay, disruption or security threats.

The inset shows the Foresight risk map for nigeria, which applies a global risk scale, with the areas forecast to be at highest risk in dark red.

PArT 2: nIGErIA – rISk MAnAGEMEnT And SECurITy PlAnnInG CASE STudy

Evolution of security risks to kaduna IPP

Plant typeCombined Cycle

Hydro

Renewable

Single Cycle

Thermal

Total MWA produced

Low High

Katsina (Solar)

Kiri IPP

Dadin-KowaKano

Kaduna IPP

Gurara

Agbara IPP (Shoreline)

Ilorin

Lokoja Makurdi (Hydro)

Kashimbilla

Ikom

Enugu

Onitsha (Hydro)

Alaoji (NIPP)

Bonny Island (ExxonMobil)

Omoku (NIPP)

Mali

Niger

Nigeria

Ghana

Cameroon

Benin

Togo

High MWA production

Low MWA production

Project locations

The main map highlights project locations, applying a relative risk scale covering these locations alone to provide clearer differentiation; the lowest risk nigeria project is green, and the highest is red. The icons are sized according to project capacity. This shows that kaduna IPP, in north-central nigeria, while not the largest project by capacity, is forecast to be at highest risk.

0

20

40

60

80

100

120

140

160

180

200

1-Oct-

12

1-Nov

-12

1-Dec

-12

1-Ja

n-13

1-Fe

b-13

1-Mar-

13

1-Arp

-13

1-May

-13

1-Ju

n-13

1-Ju

l-13

1-Aug

-13

1-Sep

-13

Ris

k sc

ore

(exp

onen

tial s

cale

)

2012 2013

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Political violence

Civil unrest

Terrorism

War

Power projects in West Africa: Project risk and location analytics 19

0

5

10

15

20

25

Q32010

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q32011 2012 2013

While we forecast kaduna IPP to be at the highest risk of our nigeria projects sample, Political Violence forecast scores have all declined over the last year. In part this is due to a reappraisal of the intelligence assessment based on a lack of observed indicators for significant attacks in this area. The key dynamic has been the establishment of major military operations against the Islamist militant group Boko Haram. In recent months the military has pushed Boko Haram back to its main operational heartland in the north of the country, focused on Borno state.

Here you can see the rapid expansion of Boko Haram operations between 2010 and 2013, and the subsequent shift in the group’s centre of gravity back to the north east (and indeed over the border into Chad) in 2013. Crucially, this shift has pushed the group’s operating area away from the power projects being assessed. While security risks are still higher than many other projects in West Africa, and the group retains significant operational capabilities, the threat to areas outside its heartlands has reduced.

Agbara IPP

Kaduna IPP

Egbema (NIPP)

Agbara IPP

Kaduna IPP

Egbema (NIPP)

Boko Haram activities

Boko Haram events per state

0

1 - 5

6 - 10

11 - 20

21 - 30

31 - 40

41 - 50

51 - 60

61 - 70

71 - 80

Boko Haram events

Boko Haram directional distribution

Planned electricity plant

Boko Haram activity

2012 2013

2010 2011

Agbara IPP

Kaduna IPP

Egbema (NIPP)

Agbara IPP

Kaduna IPP

Egbema (NIPP)

Boko Haram activity

Security events intensity (30km) There has been a decline in the intensity of security incidents within a 30km range of kaduna over the last three years. The chart measures both the frequency of incidents and their severity, to give a better measure of the true relevance of those events.

AFRICA

20

Agbara IPP

Kaduna IPP

Egbema (NIPP)

Events within 30km range of plant

Other events

Electricity plant

Pipeline

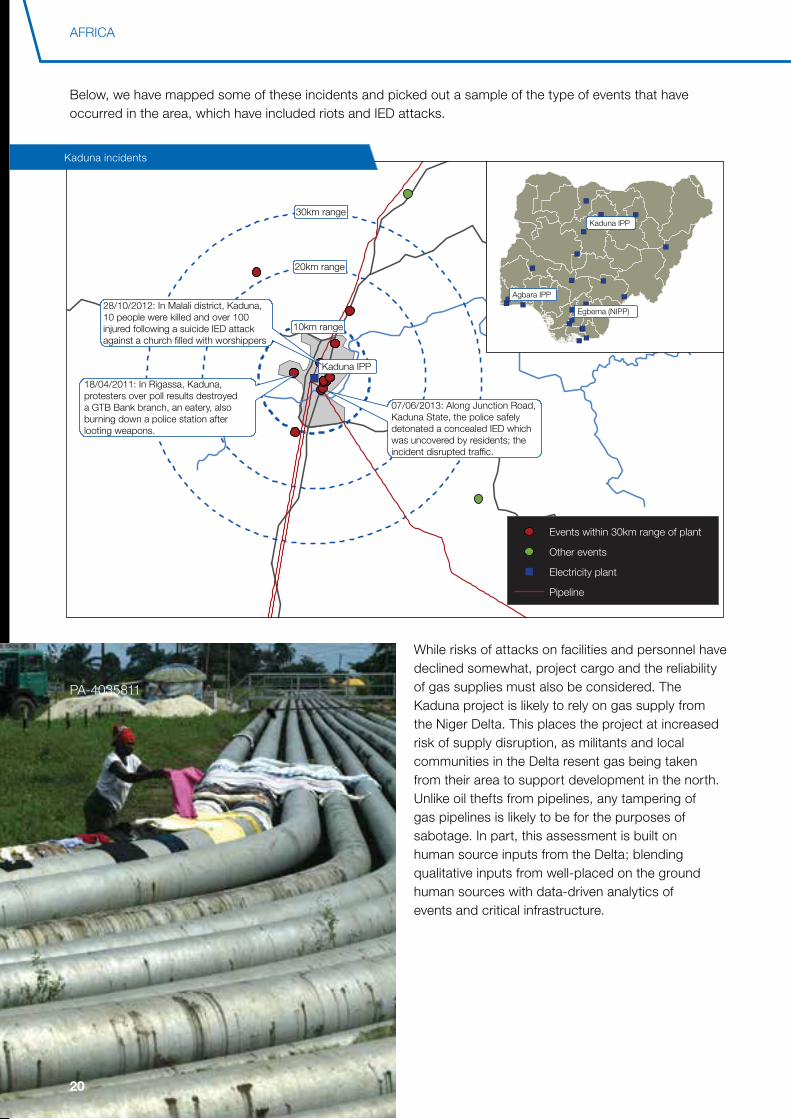

28/10/2012: In Malali district, Kaduna,10 people were killed and over 100injured following a suicide IED attackagainst a church filled with worshippers

18/04/2011: In Rigassa, Kaduna,protesters over poll results destroyeda GTB Bank branch, an eatery, also burning down a police station afterlooting weapons.

07/06/2013: Along Junction Road,Kaduna State, the police safelydetonated a concealed IED whichwas uncovered by residents; theincident disrupted traffic.

Kaduna IPP

10km range

20km range

30km range

While risks of attacks on facilities and personnel have declined somewhat, project cargo and the reliability of gas supplies must also be considered. The kaduna project is likely to rely on gas supply from the niger delta. This places the project at increased risk of supply disruption, as militants and local communities in the delta resent gas being taken from their area to support development in the north. unlike oil thefts from pipelines, any tampering of gas pipelines is likely to be for the purposes of sabotage. In part, this assessment is built on human source inputs from the delta; blending qualitative inputs from well-placed on the ground human sources with data-driven analytics of events and critical infrastructure.

Below, we have mapped some of these incidents and picked out a sample of the type of events that have occurred in the area, which have included riots and IEd attacks.

kaduna incidents

20

PA-4035811

Power projects in West Africa: Project risk and location analytics 21

Kaduna to Niger Delta gas pipeline, 769km 20 energy-relevant events within 5 km of the route

15/06/2013: The militant group MEND claimed that it detonated two fuel tankers near an NNPC depot in Abaji, Abuja.

Kaduna IPP

Abuja

Lagos

Port Harcourt

Energy-relevant events from IHS Foresight

14/07/13: In Ishiagu, Ebonyi state,the NNPC reportedly complained abouta recent rise in the theft of petroleum products by pipeline vandals.

07/10/12: Shell announced a force majeure on gas deliveries from its BonnyLNG plant following an arson incidenton its Bomu-Bonny pipeline.

location Analytics helps decision-makers to cut through noise, identify opportunities that others miss, and generate the specific level of information needed to plan and execute an effective development strategy. While location information is critical, and often maps are the best way to visualise analysis, many of the most valuable insights come from risk metrics that are not necessarily maps. We also believe that in order to summarise high level insights it is necessary to first drill into the detail of specific projects. This not only delivers different, more valuable insights at a macro level, but supports integrated communication and planning of risk across multiple teams involved in a project, from strategy right through to operational security planning and insurance purchasing

21

Pipeline incidents

August 2013 report from source in Niger Delta: “The possibility of attacks is more with plants that are seen to be feeding from gas in the niger delta and considered to be serving a far off region. The perception among delta youth and militant groups is that gas, their local resource, is being accessed to power distant places while the plants serving the niger delta community are not been given enough attention.”

By placing specific details of an asset or operation at the forefront of risk assessment, we can reveal insights into risks that enable commercial opportunities to be identified where information-disadvantaged competitors fear to tread

CrQ

MIDDLE EAST AND NORTH AFRICA

22

THE TrAnSITIon CHAllEnGE

Following the ousting of former President Mohamed Morsi of the Muslim Brotherhood on 3 July 2013, the army designated a 50-member committee to amend the 2012 constitution introduced by Morsi’s government. With only two Islamist seats, the composition of the committee looks designed to severely curtail Islamist influence. The remaining 48 seats were allocated to representatives of unions, political parties, the judiciary, minority rights groups, the army, and the police.

The Al-nour party, a Salafist (hardline) Islamist party, supported Morsi’s removal. This probably partly reflected an expectation that, by working with the army, it could replace the Muslim Brotherhood as Egypt’s dominant political party. However, the army has since made it clear that nour will not hold sway over the next government, allowing it only one of the two Islamist seats on the constitutional committee. The army, probably correctly, judges the public mood to be overwhelmingly against the Islamists. This mood is sustained by intensive state and secular independent media coverage of the Islamist terrorist threat. This threat was formerly limited to Sinai but, as a result of the army’s repression of the Muslim Brotherhood, has now spread to other areas, including Cairo and other cities.

delineating the current transition period as a ‘war on terrorism’ serves the army well. It shores up support for strengthening security forces, and promotes acceptance of an enhanced police presence on the

EgYPT SCENARIOS: ISLAMISM, SECURITY AND DEMOCRATISATION

Meda Al rowas outlines three potential scenarios for Egypt’s transition over the next year. In each case, indicators are highlighted which, if they were to happen, would make that scenario more likely to occur (these indicators may occur in more than one scenario). She also outlines the major commercial implications of each scenario, and looks at three key groups in Egypt. In Meda’s view, the appointment of a secular civilian government, accompanied by the effective exclusion of Islamists from the political process is, by quite a margin, the most probable scenario. There is a lower likelihood of the army overtly consolidating control by appointing a military-dominated cabinet. reconciliation with the Islamists is the least likely scenario.

Meda Al Rowas Senior Analyst, Middle East & north Africa, IHS Country risk

22

PA-17831539

Egypt scenarios – Islamism, security and democratisation 23

Calls for reconciliation with Islamist factions are likely to be met with fierce public resistance

streets. The focus on ‘Islamist terror’ also suggests that calls for reconciliation with, and inclusion of, Islamist factions by any other non-Islamist political faction, are likely to be met with fierce public resistance, at least until parliamentary and presidential elections take place in early 2014.

despite the army’s popularity, secular groups are fearful of the return of the state curtailment of civil liberties seen in Mubarak’s era, especially if, as is likely, the army retains its autonomy and circumvents civilian oversight after the new constitution is passed. The Tamarrod movement, which organised the protests that helped the army intervention to remove Morsi, is supportive of the army. The movement will now attempt to establish an electoral coalition and probably has the capacity to mobilise support for a pro-army coalition, even if it includes Mubarak- era and ex-military figures. nevertheless, some secular and labour groups, including the April 6 youth movement, and a minority of leaders within the Egyptian Federation of Independent Trade unions (EFITu), mistrust the army and are warning against the return of the police state.

BETWEEn A roCk And A HArd PlACE

Although foreign aid from Saudi Arabia, the uAE, kuwait and others will probably prevent Egypt from defaulting on debt and enable it to pay for food and fuel imports for the next six months, the Egyptian government’s funding requirements are too large to be sustained on foreign aid indefinitely.

The next government, irrespective of its composition, will be faced with the challenge of economic reform and securing the uSd4.8 billion IMF loan and contingent financing. Securing the IMF loan is now almost synonymous with the restoration of investor confidence in Egypt, which is necessary to rejuvenate foreign direct investment flows and improve access to credit markets.

The conditionalities attached to an IMF loan are very likely to include the cutting of fuel and food subsidies and redirection of resources to target the poorest components of Egyptian society. regardless, the next government is unlikely to be able to boost employment or undertake the necessary infrastructure investment to the levels required to improve living standards. Consequently, protests over localised economic issues are likely to recur. The likelihood of civil unrest and other risks becoming political destabilising over the coming year are explored in the following three scenarios.

In all the three scenarios presented, we assess that the army will retain its privileged position, including immunity from civilian oversight, its commercial interests, and control of the levers of power. We assess that the army’s authority is unlikely to be challenged, as long as there is sufficient popular support for the army’s public role and its anti-Islamist stance, and it is not forced, as a result of police ineffectiveness, into taking on a confrontational public order role that would put the loyalty of its junior ranks, especially conscript soldiers, at risk.

MIDDLE EAST AND NORTH AFRICA

2424

A SECulAr CIVIlIAn GoVErnMEnT IS APPoInTEd; ISlAMISTS ArE EFFECTIVEly ExCludEd FroM THE PolITICAl ProCESS

The army retains its popularity and cements its role as political arbitrator and dominant influence over the government. It does this through allowing democratic elections and the appointment of a secular civilian cabinet. Islamists are marginalised in the elections and the judiciary deems some Islamist candidates ineligible. The army succeeds in cementing the police state, albeit in a less invasive form than under past administrations. The military uses rising terrorism risks to justify the reintroduction of curbs against freedom of speech and association, targeting Islamist groups. Secular forces like April 6 and leftist union-backed political groups probably denounce the army’s takeover of the state, but this fails to engender mass opposition to the army in 2014.

Scenario indicators

The clause banning political parties with a religious agenda is retained in the final draft of the constitution, which is passed in a popular referendum.

The nour party and the Salafi da’wa vote against the constitution, but the referendum is passed. It is boycotted by the Brotherhood.

The Brotherhood’s Freedom and Justice political party is dissolved.

The dismissal or re-assignment of suspected Brotherhood affiliates within educational institutions escalates into a sustained campaign.

Arrest warrants issued by the public prosecutor’s office start to include political activists from the secular opposition to the army, and independent journalists.

The media campaign against ‘Islamist terrorism’ is sustained at least until elections are held.

Scenario 1

24

PA-17832332

Egypt scenarios – Islamism, security and democratisation 25

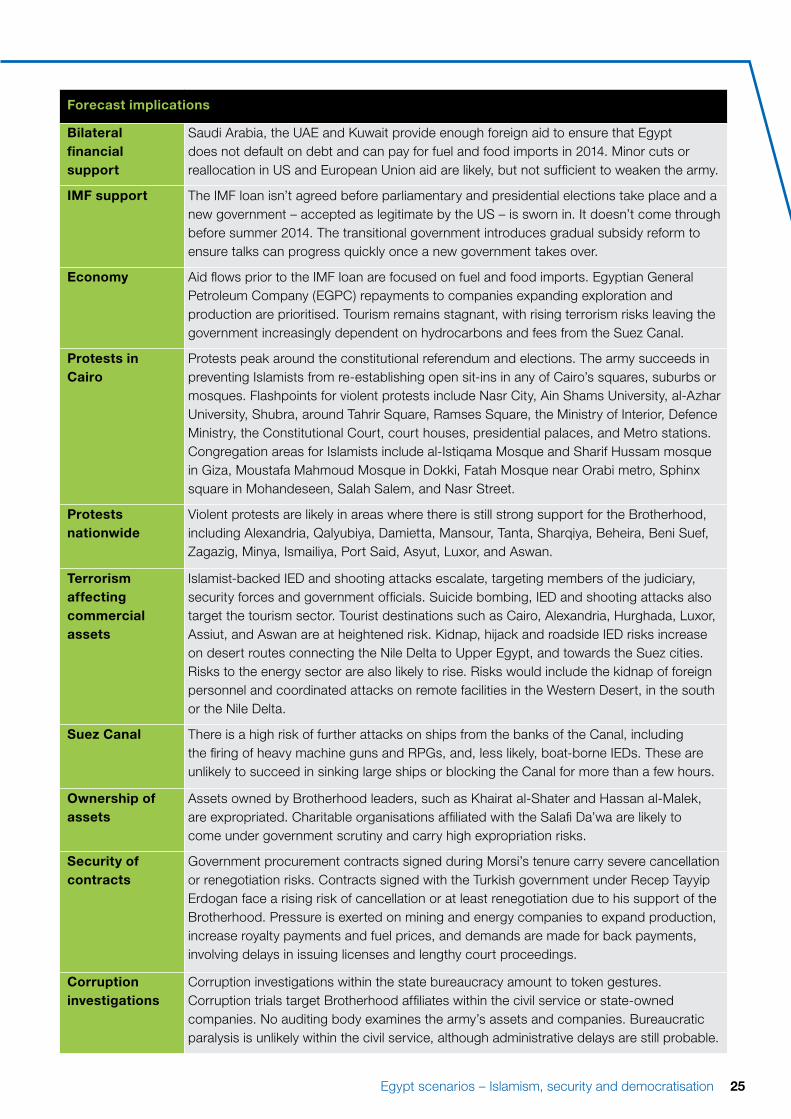

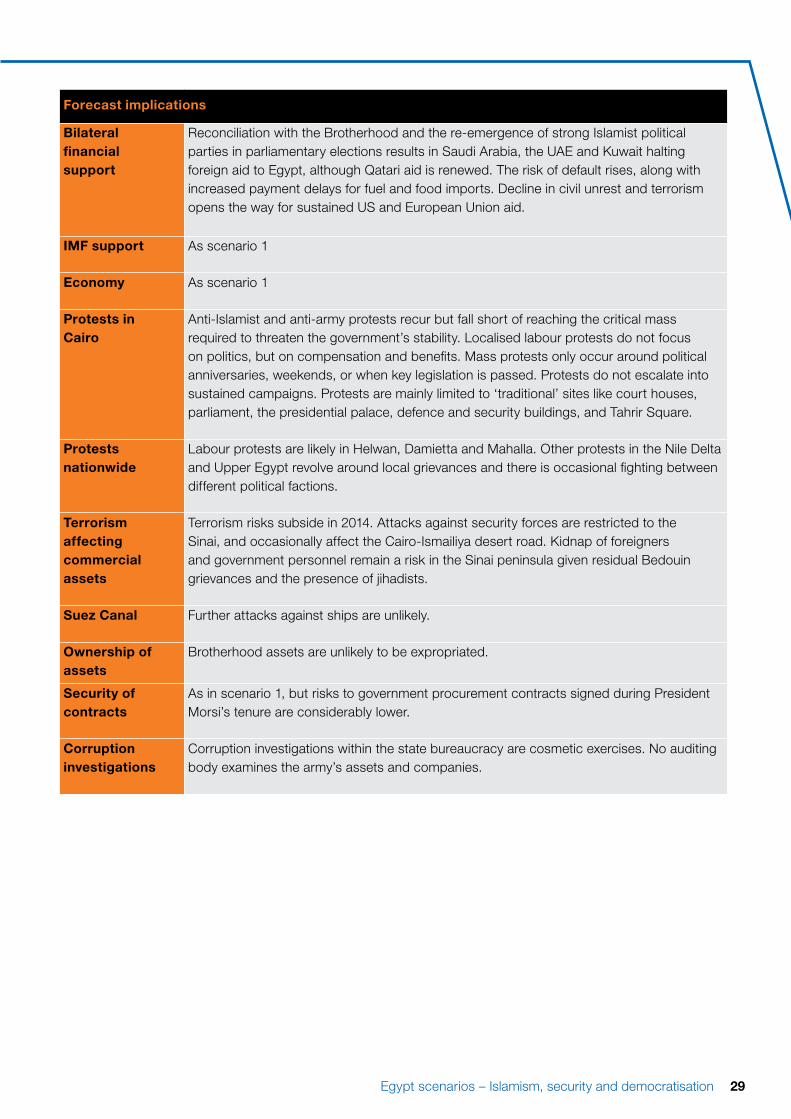

Forecast implications

Bilateral financial support

Saudi Arabia, the uAE and kuwait provide enough foreign aid to ensure that Egypt does not default on debt and can pay for fuel and food imports in 2014. Minor cuts or reallocation in uS and European union aid are likely, but not sufficient to weaken the army.

IMF support The IMF loan isn’t agreed before parliamentary and presidential elections take place and a new government – accepted as legitimate by the uS – is sworn in. It doesn’t come through before summer 2014. The transitional government introduces gradual subsidy reform to ensure talks can progress quickly once a new government takes over.

Economy Aid flows prior to the IMF loan are focused on fuel and food imports. Egyptian General Petroleum Company (EGPC) repayments to companies expanding exploration and production are prioritised. Tourism remains stagnant, with rising terrorism risks leaving the government increasingly dependent on hydrocarbons and fees from the Suez Canal.

Protests in Cairo

Protests peak around the constitutional referendum and elections. The army succeeds in preventing Islamists from re-establishing open sit-ins in any of Cairo’s squares, suburbs or mosques. Flashpoints for violent protests include nasr City, Ain Shams university, al-Azhar university, Shubra, around Tahrir Square, ramses Square, the Ministry of Interior, defence Ministry, the Constitutional Court, court houses, presidential palaces, and Metro stations. Congregation areas for Islamists include al-Istiqama Mosque and Sharif Hussam mosque in Giza, Moustafa Mahmoud Mosque in dokki, Fatah Mosque near orabi metro, Sphinx square in Mohandeseen, Salah Salem, and nasr Street.

Protests nationwide

Violent protests are likely in areas where there is still strong support for the Brotherhood, including Alexandria, Qalyubiya, damietta, Mansour, Tanta, Sharqiya, Beheira, Beni Suef, Zagazig, Minya, Ismailiya, Port Said, Asyut, luxor, and Aswan.

Terrorism affecting commercial assets

Islamist-backed IEd and shooting attacks escalate, targeting members of the judiciary, security forces and government officials. Suicide bombing, IEd and shooting attacks also target the tourism sector. Tourist destinations such as Cairo, Alexandria, Hurghada, luxor, Assiut, and Aswan are at heightened risk. kidnap, hijack and roadside IEd risks increase on desert routes connecting the nile delta to upper Egypt, and towards the Suez cities. risks to the energy sector are also likely to rise. risks would include the kidnap of foreign personnel and coordinated attacks on remote facilities in the Western desert, in the south or the nile delta.

Suez Canal There is a high risk of further attacks on ships from the banks of the Canal, including the firing of heavy machine guns and rPGs, and, less likely, boat-borne IEds. These are unlikely to succeed in sinking large ships or blocking the Canal for more than a few hours.

Ownership of assets

Assets owned by Brotherhood leaders, such as khairat al-Shater and Hassan al-Malek, are expropriated. Charitable organisations affiliated with the Salafi da’wa are likely to come under government scrutiny and carry high expropriation risks.

Security of contracts

Government procurement contracts signed during Morsi’s tenure carry severe cancellation or renegotiation risks. Contracts signed with the Turkish government under recep Tayyip Erdogan face a rising risk of cancellation or at least renegotiation due to his support of the Brotherhood. Pressure is exerted on mining and energy companies to expand production, increase royalty payments and fuel prices, and demands are made for back payments, involving delays in issuing licenses and lengthy court proceedings.

Corruption investigations

Corruption investigations within the state bureaucracy amount to token gestures. Corruption trials target Brotherhood affiliates within the civil service or state-owned companies. no auditing body examines the army’s assets and companies. Bureaucratic paralysis is unlikely within the civil service, although administrative delays are still probable.

MIDDLE EAST AND NORTH AFRICA

26

THE ArMy oVErTly ConSolIdATES ConTrol oVEr THE STATE; An Ex-MIlITAry PrESIdEnT IS ElECTEd And A nEW CABInET IS doMInATEd By Ex-MIlITAry oFFICErS or MuBArAk-ErA PolITICIAnS

Islamist groups are excluded from the political process as a military president (or one with a military/Mubarak era background) and former senior officers dominate the new cabinet. The army, rather than the government, is blamed for economic failings, eroding its support. The Salafis, including nour and the Brotherhood, unite against the army and succeed in mobilising mass civil unrest. Secular groups, fearful of the return of the Mubarak-era police state, join anti-army protests and are eventually joined by unions. Civil unrest becomes politically destabilising in 2014 as the intensity and scale of protests grows in the run-up to the referendum, is sustained following the referendum, rises again around elections, and is sustained post-election.

Scenario 2

Scenario indicators

Islamists, including the Strong Egypt Party of Abdul Mon’em Abul Futouh, the Wasat Party, and the nour Party, boycott the constitutional referendum and/or the elections.

The Muslim Brotherhood and the Salafis start making joint statements.

Islamist candidates are excluded from participating in elections. Secular and opposition figures denounce elections as fraudulent and rigged by the army.

Egypt’s foreign backers, especially the uS, reject Egypt’s election results as invalid and criticise the election of a military president.

A military candidate, such as current Chief of Staff Abdul-Fatah al-Sisi, is elected president.

The government disbands social welfare schemes operated by Islamist groups in poorer nile delta and upper Egypt provinces, but lacks the will, administrative capacity or funding to replace them.

unions and April 6 leaders meet with those Muslim Brotherhood youth and mid-level leaders who are not in jail.

unions join Islamist protests, or initiate strikes at the same time, especially in Mahalla, damietta and Helwan.

Protests against fuel subsidy cuts in multiple provinces cause closures of train services, ports and road transport for more than three weeks.

Strikes spread to ports, state-owned enterprises in the energy sector, and the civil service.

Egypt scenarios – Islamism, security and democratisation 27

Forecast implications

Bilateral financial support

Saudi Arabia, the uAE, and kuwait provide foreign aid to the Egyptian government at levels sufficient to ensure that Egypt does not default on debt and can pay for fuel and food imports in 2014. Mass arrests and state-sanctioned violence restrict, if not halt, uS and European union aid.

IMF support The IMF announces that it will resume loan negotiations with an internationally recognised government. Parliamentary and presidential elections are not recognised as ‘free and fair’ by key backers such as the uS, leading to the indefinite postponement of the loan and contingent investment.

Economy As scenario 1

Protests in Cairo

Flashpoints are similar to those in scenario 1, but the scale of anti-army protests increases to tens of thousands of protesters in urban centres. There is a high risk that unions will join protesters and coordinate strikes across sectors.

Protests nationwide

Economically-motivated protests frequently disrupt the agricultural road connecting Cairo to Alexandria. Protests spread across cities in the nile delta and upper Egypt, including Alexandria, Mansoura, Tanta, Sharqiya, Gharbiya, Minya, Helwan, Mahalla, Port Said, Ismailiya, Suez City, Asyut, Aswan, luxor, and Beni Suef.

Terrorism affecting commercial assets

As Islamist protests gain momentum, terrorist attacks focus on security forces, officials and members of the judiciary, rather than expanding to tourism and energy. Attacks intended to cause mass civilian casualties are unlikely. Sinai-based militants still target the Suez Canal, and expand attacks against the army and security forces in Canal cities, and sustain attacks on security force targets in Sinai.

Suez Canal As scenario 1

Ownership of assets

As scenario 1

Security of contracts

As scenario 1

Corruption investigations

Corruption investigations target Islamists and anyone sympathetic to the Brotherhood or the Salafi da’wa. Fears of scapegoating, dismissal or re-assignment lead bureaucratic paralysis to return to levels observed under President Morsi.

27Egypt scenarios – What’s next?

PA-17832135

MIDDLE EAST AND NORTH AFRICA

2828

rEHABIlITATIon oF SElECTEd ISlAMISTS, InCludInG MEMBErS oF THE MuSlIM BroTHErHood, FolloWInG A dEAl donE WITH THE ArMy

key Brotherhood leaders remain in jail. others reach an accommodation with the army as the price of their rehabilitation, enabling the Brotherhood to resume its social welfare activities and, within limits set by the army, its participation in the political process. Terrorism and civil unrest risks fall. The Brotherhood participates in elections, winning approximately 20% of seats, and is allowed to re-open its media channels or establish new ones.

Scenario 3

Scenario indicators

Brotherhood youth groups and mid-level leaders renounce affiliation with their jailed leaders and meet with secular political leaders and army officials.

Calls to reinstate ousted President Morsi subside.

The ‘war on terrorism’ media campaign subsides before the constitutional referendum, or before elections.

Some Islamists, including non-senior members of the Brotherhood, are released from jail.

no clause banning Islamist parties is included in the constitution, and there is no Islamist boycott of the constitutional referendum.

Brotherhood charitable organisations are allowed to continue operations.

Attacks against security forces outside the Sinai stop.

The Brotherhood wins its appeal against a court ruling to ban the organisation; the freeze of its assets is reversed.

Brotherhood ministers are appointed in the next cabinet.

28

PA-17819282

Egypt scenarios – Islamism, security and democratisation 29

Forecast implications

Bilateral financial support

reconciliation with the Brotherhood and the re-emergence of strong Islamist political parties in parliamentary elections results in Saudi Arabia, the uAE and kuwait halting foreign aid to Egypt, although Qatari aid is renewed. The risk of default rises, along with increased payment delays for fuel and food imports. decline in civil unrest and terrorism opens the way for sustained uS and European union aid.

IMF support As scenario 1

Economy As scenario 1

Protests in Cairo

Anti-Islamist and anti-army protests recur but fall short of reaching the critical mass required to threaten the government’s stability. localised labour protests do not focus on politics, but on compensation and benefits. Mass protests only occur around political anniversaries, weekends, or when key legislation is passed. Protests do not escalate into sustained campaigns. Protests are mainly limited to ‘traditional’ sites like court houses, parliament, the presidential palace, defence and security buildings, and Tahrir Square.

Protests nationwide

labour protests are likely in Helwan, damietta and Mahalla. other protests in the nile delta and upper Egypt revolve around local grievances and there is occasional fighting between different political factions.

Terrorism affecting commercial assets

Terrorism risks subside in 2014. Attacks against security forces are restricted to the Sinai, and occasionally affect the Cairo-Ismailiya desert road. kidnap of foreigners and government personnel remain a risk in the Sinai peninsula given residual Bedouin grievances and the presence of jihadists.

Suez Canal Further attacks against ships are unlikely.

Ownership of assets

Brotherhood assets are unlikely to be expropriated.

Security of contracts

As in scenario 1, but risks to government procurement contracts signed during President Morsi’s tenure are considerably lower.

Corruption investigations

Corruption investigations within the state bureaucracy are cosmetic exercises. no auditing body examines the army’s assets and companies.

MIDDLE EAST AND NORTH AFRICA

30

Cai

ro

Asw

an

Ale

xand

ria

Nile

Del

ta:

- E

leva

ted

risk

of ro

adsi

de IE

Ds

and

sho

otin

gs a

t che

ckpo

ints

, t

arge

ting

milit

ary

or p

olic

e v

ehic

les

and

pers

onne

l but

a

lso

posi

ng c

olla

tera

l ris

ks to

c

argo

and

pas

seng

er v

ehic

les

- M

oder

ate

risk

of s

mal

l IE

Ds

tar

getin

g ra

ilway

line

s C

airo

:-

Hig

h ris

k of

sho

otin

g, g

rena

de

and

low

-cap

abilit

y IE

D a

ttac

ks

on

polic

e an

d ar

my

targ

ets

- E

leva

ted

risk

of lo

w-c

apab

ility

phy

sica

l ass

aults

or

shoo

tings

t

arge

ting

fore

igne

rs, i

nclu

ding

a

roun

d to

uris

t are

as

- M

oder

ate

risk

of la

rger

IED

s t

arge

ting

gove

rnm

ent p

erso

nnel

o

r bu

ildin

gs, o

r pu

blic

are

as w

here

for

eign

ers

cong

rega

te

Oil

& G

as f

ield

s-W

este

rn E

gyp

t:-

Mod

erat

e ris

k of

att

acks

on

wes

tern

des

ert e

nerg

y si

tes

due

to

thei

r lo

catio

n on

a m

ain

wea

pons

sm

uggl

ing

rout

e fro

m L

ibya

Por

t Sai

d

Sue

z

Luxo

r

Dam

iett

a

Ben

i Sue

f

Sue

z C

anal

:-

Ele

vate

d ris

k of

RP

G a

ttac

ks o

n s

hipp

ing

caus

ing

min

imal

to m

inor

d

amag

e; lo

w r

isk

of b

oat-

born

e I

ED

att

acks

- E

leva

ted

risk

of ro

adsi

de IE

Ds

and

sh

ootin

gs a

t che

ckpo

ints

, tar

getin

g

milit

ary

or p

olic

e ve

hicl

es a

nd

pe

rson

nel

- M

oder

ate

risk

of s

mal

l IE

Ds

targ

etin

g r

ailw

ay li

nes

Sin

ai:

- H

igh

risk

of k

idna

p to

per

sonn

el a

nd t

ouris

ts in

tran

sit t

hrou

gh d

eser

t are

as

- In

Sou

th S

inai

, ele

vate

d ris

k of

I

ED

att

acks

targ

etin

g ho

tels

and

t

ouris

t site

s

- In

Nor

th S

inai

, sev

ere

risk

of

roa

dsid

e IE

Ds,

sho

otin

gs a

t pol

ice

or

arm

y as

sets

and

per

sonn

el o

r R

PG

att

acks

on

al-A

rish

Inte

rnat

iona

l A

irpor

t

Luxo

r an

d A

swan

are

a:-

Hig

h ris

k of

sho

otin

g, g

rena

de a

nd

low

-cap

abilit

y IE

D a

ttac

ks o

n po

lice

an

d ar

my

targ

ets

- E

leva

ted

risk

of lo

w-c

apab

ility

phy

sica

l ass

aults

or

shoo

tings

t

arge

ting

fore

igne

rs

Terrorism risks for Scenario 1

Egypt scenarios – Islamism, security and democratisation 31

THE Al-nour

The Al-nour political party was founded after the 25 January 2011 uprising and is often depicted as the political arm of the ultra-orthodox Sunni Salafi da’wa. nour won 22% of the lower house of parliament (Majlis al-Sha’b) in the 2011-2012 elections, coming in second only to the FJP. Within its charter, nour calls for economic and political reform as well as reform across security institutions. It demands that Islamic Sharia remains the main source of legislation, limiting the powers of the president, and expanding the power of elected parliamentary bodies. The party holds a single seat on the 50-member constitutional committee, and although its representative has repeatedly walked out of sessions in protest, the party has not withdrawn from the committee. nour supported the army intervention to remove President Morsi, and has since attempted to exclude other Islamist groups to enlarge its own support base and establish itself as the dominant Islamist political party. The army will probably use this aspiration to gradually eliminate nour’s rivals. However, the perception of collaboration with the army is likely to drive its own supporters to pressure nour’s leadership to reject the political process altogether in favour of militancy and anti-army protests.

THE THIrd SQuArE InITIATIVE

The Third Square Initiative brands itself as an anti-army and anti-Muslim Brotherhood centrist movement. Many Egyptians see it as strongly associated with former Brotherhood leader Aboul Fotouh, who now leads the Strong Egypt Party. Aboul Fotouh has called for his supporters to participate in the constitutional vote, but to vote ‘no’ in protest at the military’s dominance of the process. The Ahrar umbrella group, also backing this initiative, comprises supporters of radical cleric Hazem Abu Ismail, as well as Zamalek ultras football fans protesting against the detention without charge since 5 July of their leader, a supporter of Hazem. Ahrar indicated on 27 August that it intends to begin an ‘intifada’ or uprising, and that it would join Third Square protesters in Sphinx Square, Mohandiseen. The army used tear gas and live ammunition to disperse Ahrar supporters in Sphinx Square on 30 August on the pretext that live fire had been used by protesters. Further use of force is very likely at future Ahrar protests

THE MuSlIM BroTHErHood

The Muslim Brotherhood was founded in Egypt in 1928, emerging as one of the most powerful political groups in the country after several decades of persecution under successive governments. President Morsi was elected in June 2012 through the gains of its political platform, the Freedom and Justice Party (FJP). The controversial 2012 constitution was passed during Morsi’s term, sparking recurrent and growing civil unrest denouncing the Brotherhood. Following nationwide mass protests, the army intervened to remove Morsi from office, and proceeded to arrest senior leaders. on 23 September, the judiciary ruled to ban the Brotherhood. during the Mubarak-era, Brotherhood figures were represented in parliament as independents, but the constitutional committee has now proposed rewriting electoral law to ensure that only candidates from government-approved parties can stand for parliament. on 24 September the army raided and closed down an Islamist school in Bani Suef, one day after the court order banned the Brotherhood. This action suggests that the army will move to dissolve or reduce the wide network of Brotherhood-affiliated schools, clinics and social services that existed under Mubarak. This would probably shift support towards Islamic militancy and away from the nour party and its conciliatory position with the army.

key groups

CrQ

LATIN AMERICA

32

Carlos Caicedo Senior Principal Analyst, latin America, IHS Country risk other contributor: The risk Indicators & Analytics team, IHS Country risk

BRAZIL – THE CHANgINg NATURE OF PROTESTIn June 2013, Brazil unexpectedly experienced the largest anti-government protests in two decades. More than one million people took to the streets in 120 cities nationwide, with the police using tear gas and rubber bullets to contain crowds.

Here, Carlos Caicedo looks at the role of social media in the protests in Brazil and casts an eye forward to the World Cup in 2014 and the 2016 olympic Games. Two social media research case studies from the IHS Country risk team’s work on Turkey and Bahrain are also featured.

32

Bus fare hikes helped spark the protests, but wider social concerns led their escalation

on 6 June 2013, fringe activist group the Free Fare Movement (Movimento Passe livre: MPl) demonstrated against a 10% increase in bus fares. Videos of the military police beating protesters were posted online and were rapidly circulated on Facebook. This prompted many young Brazilians to join the protests, which engulfed Brazil for the next three weeks. The protests coincided with the Confederations Cup, attracting international attention and highlighting the anger many Brazilians felt at spending on the World Cup and olympics. other key factors driving the subsequent unrest were frustration at the high cost of living, inadequate urban transport, poor public services and corruption.

WHo ProTESTEd?

Many of Brazil’s protesters were middle class and were not seeking to unseat President dilma rousseff. They wanted the government’s attention.

Surveying protesters in seven cities on 20 June, Brazilian pollster Ibope found that almost half came from households with incomes of more than five times the minimum wage. These protesters felt empowered, with 94% saying that they expected their demands to be answered. only 4% identified themselves as party affiliates, and 14% members of trade unions. Protesters were mainly young (63% under 30 years old) and well-educated (only 8% had not completed secondary education).

Brazil – The changing nature of protest 33

SoCIAl MEdIA AS A kEy ProTEST Tool

Social media is playing an increasingly prominent role in protests. Just as during the ‘Arab Spring’ movement and in the protests around Gezi Park in Turkey earlier in 2013, Facebook and Twitter (supported by Instagram and youTube) became platforms to express political views and disseminate information throughout Brazil, and were used as tools to coordinate direct action in real time.

Frustration at the high cost of living, inadequate urban transport, poor public services, and corruption were factors in the unrest

33PA-16871086

LATIN AMERICA

34

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

0

11

10

9

8

7

6

5

4

3

2

1

12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Day (June 2013)

Twee

ts (1

,000

s)

Pro

test

ers

(1,0

00s)

Tweets

Protesters

Monroy-Hernández and Emma Spiro in a Microsoft Fuse labs blog published on 4 July 2013.

Twitter activity peaked three days before the protest numbers reached their highest point, with a rapid decline after President rousseff’s 21 June address to the nation on TV.

The fall in tweets as protests peaked seems counterintuitive. After all, Twitter was also being used to share real time video footage of the protests and to outmanoeuvre the police, identifying checkpoints, changes to protest routes, and sharing information regarding safety precautions.

Facebook and Twitter Brazil has the second largest Facebook community globally, with over 65 million users. 71% of respondents to a datafolha survey found out about one of the first large-scale protests on 17 June in São Paulo through Facebook. The sharing of information on Facebook was vital in the spread of the protests from São Paulo and rio to other cities.