Embed Size (px)

DESCRIPTION

Image page. Real Fed Funds Rate (r). Monetary Policy Response Schedule (MPR). Macro 101 Michael R. Rosenberg October 2010. r*. Financial Conditions Schedule. p *. FC*. Inflation Rate ( p ). Financial Conditions (FC). - PowerPoint PPT Presentation

Citation preview

1

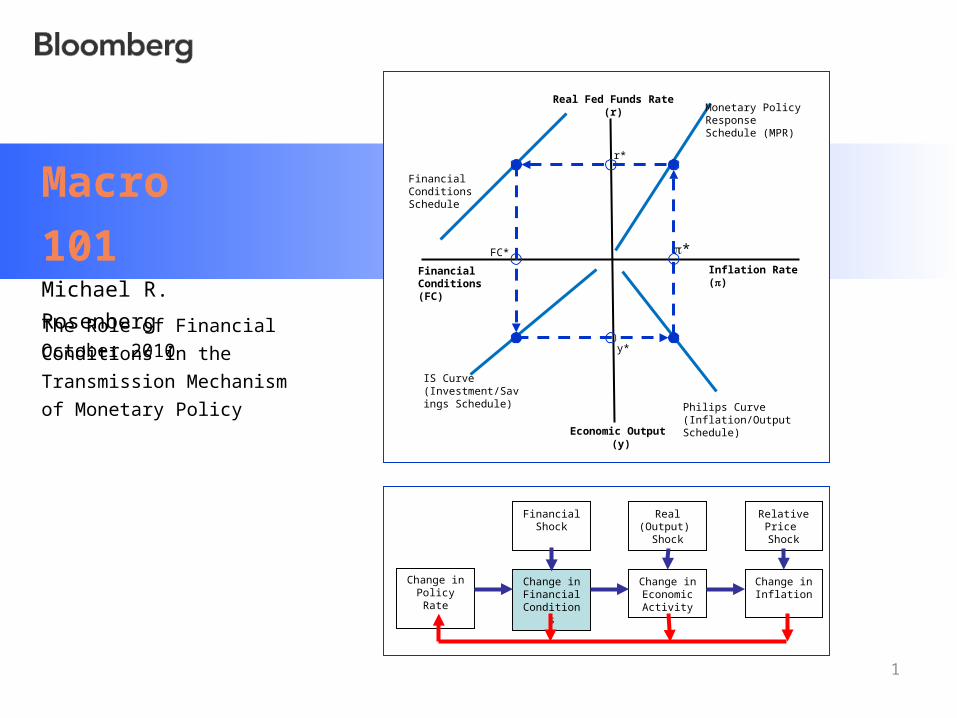

Macro

101Michael R.

RosenbergOctober 2010The Role of Financial

Conditions in the

Transmission Mechanism of

Monetary Policy

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedule (MPR)

Philips Curve(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedule)

Financial Conditions Schedule

r*

y*

FC* *

Change inPolicy Rate

Change in Economic

Activity

Financial Shock

Change in Financial

Conditions

Real (Output)

Shock

Relative Price Shock

Change in Inflation

2

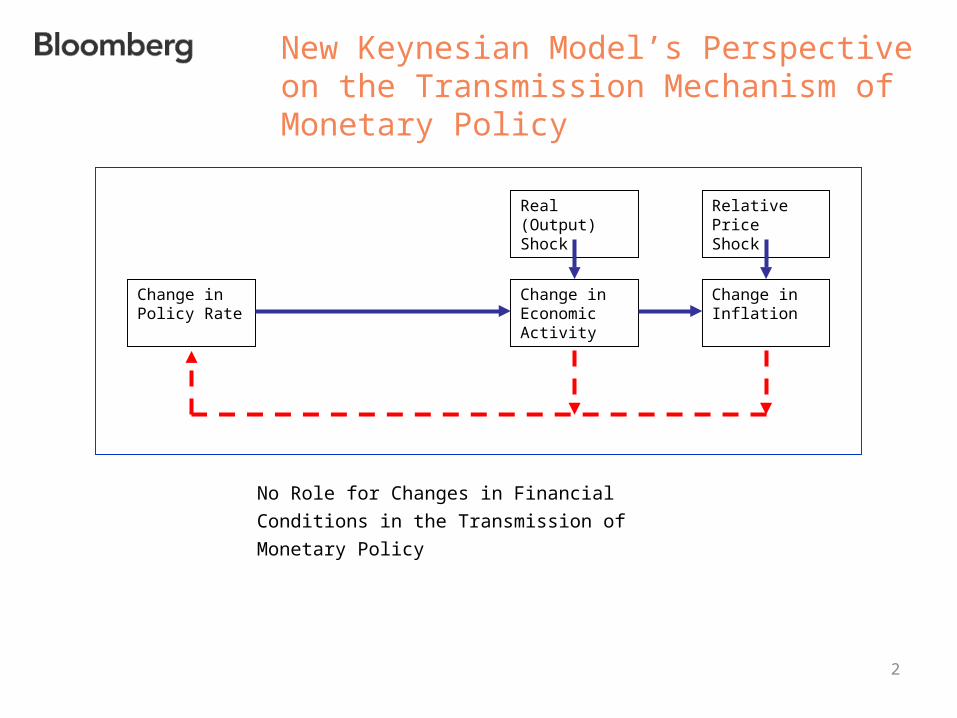

New Keynesian Model’s Perspective on the Transmission Mechanism of Monetary Policy

Change inPolicy Rate

Change in Economic Activity

Real (Output) Shock

Relative Price Shock

Change in Inflation

No Role for Changes in Financial Conditions in

the Transmission of Monetary Policy

3

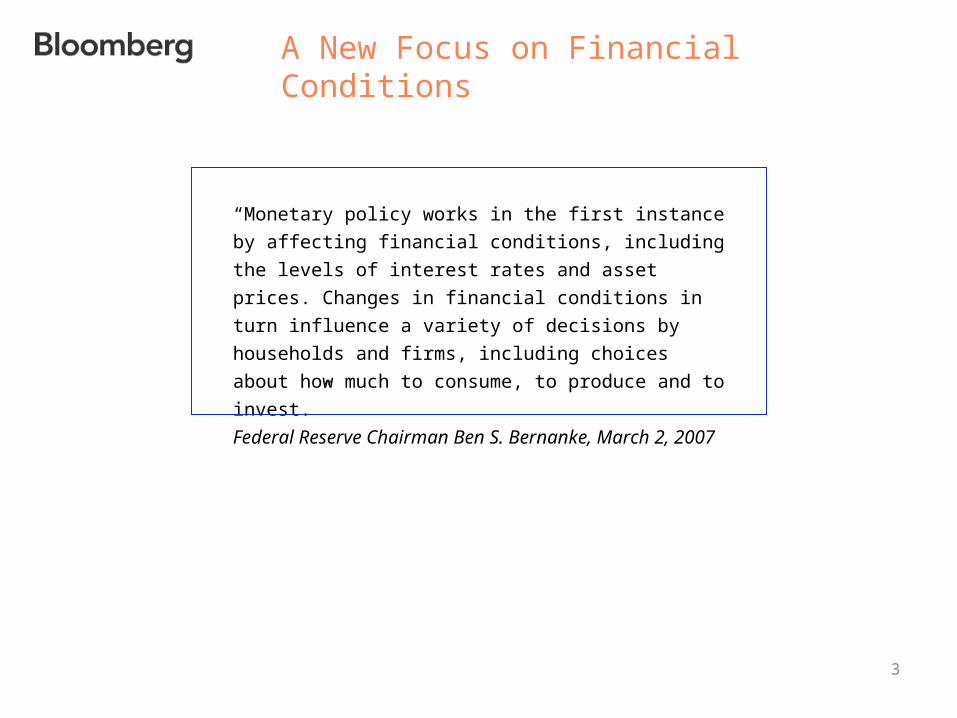

A New Focus on Financial Conditions

“Monetary policy works in the first instance by

affecting financial conditions, including the levels of

interest rates and asset prices. Changes in financial

conditions in turn influence a variety of decisions by

households and firms, including choices about how

much to consume, to produce and to invest.”

Federal Reserve Chairman Ben S. Bernanke, March

2, 2007

4

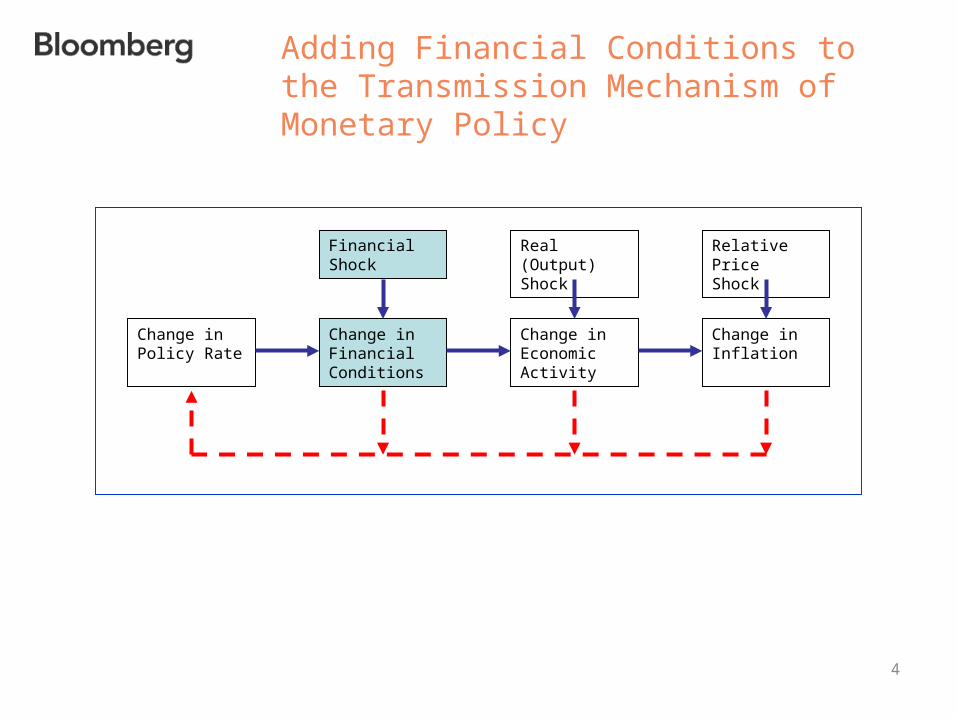

Adding Financial Conditions to the Transmission Mechanism of Monetary Policy

Change inPolicy Rate

Change in Economic Activity

Financial Shock

Change in Financial Conditions

Real (Output) Shock

Relative Price Shock

Change in Inflation

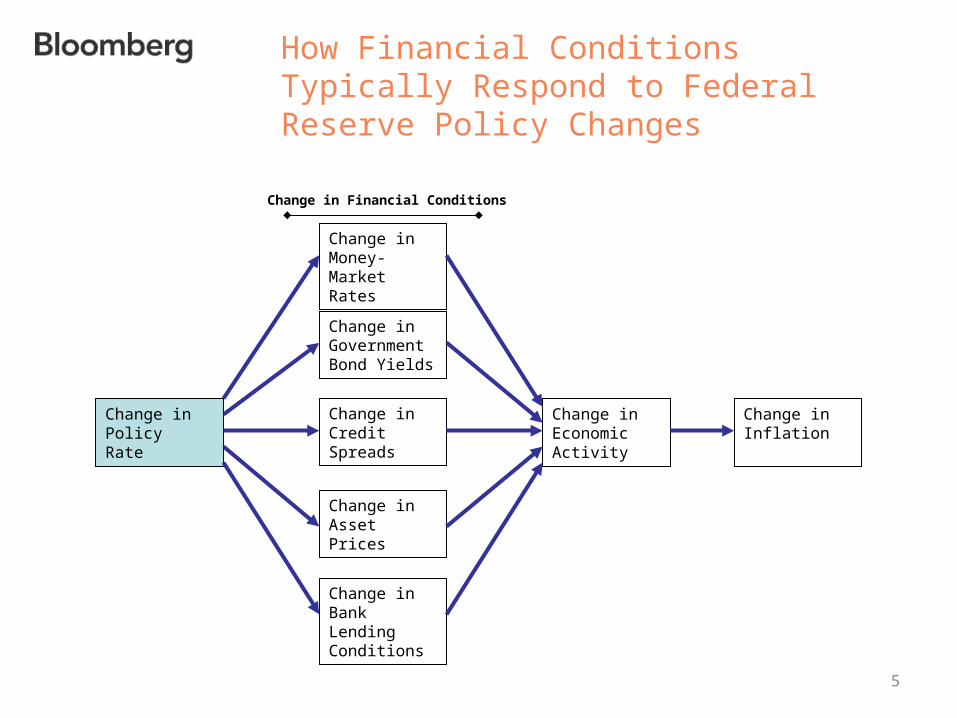

How Financial Conditions Typically Respond to Federal Reserve Policy Changes

Change inCredit Spreads

Change in Economic Activity

Change in Money-Market Rates

Change in PolicyRate

Change in Bank Lending Conditions

Change in Inflation

Change in Government Bond Yields

Change in Asset Prices

Change in Financial Conditions

5

6

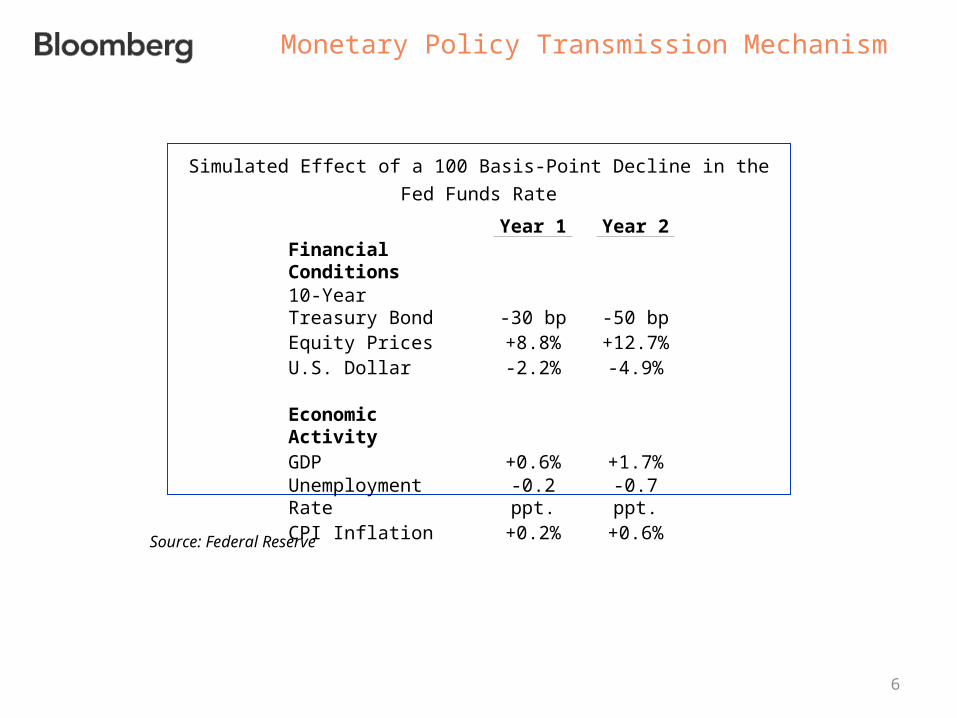

Monetary Policy Transmission Mechanism

Simulated Effect of a 100 Basis-Point Decline in the Fed Funds

Rate

Year 1 Year 2Financial Conditions10-Year Treasury Bond -30 bp -50 bpEquity Prices +8.8% +12.7%U.S. Dollar -2.2% -4.9%

Economic ActivityGDP +0.6% +1.7%Unemployment Rate -0.2 ppt. -0.7 ppt.CPI Inflation +0.2% +0.6%

Source: Federal Reserve

7

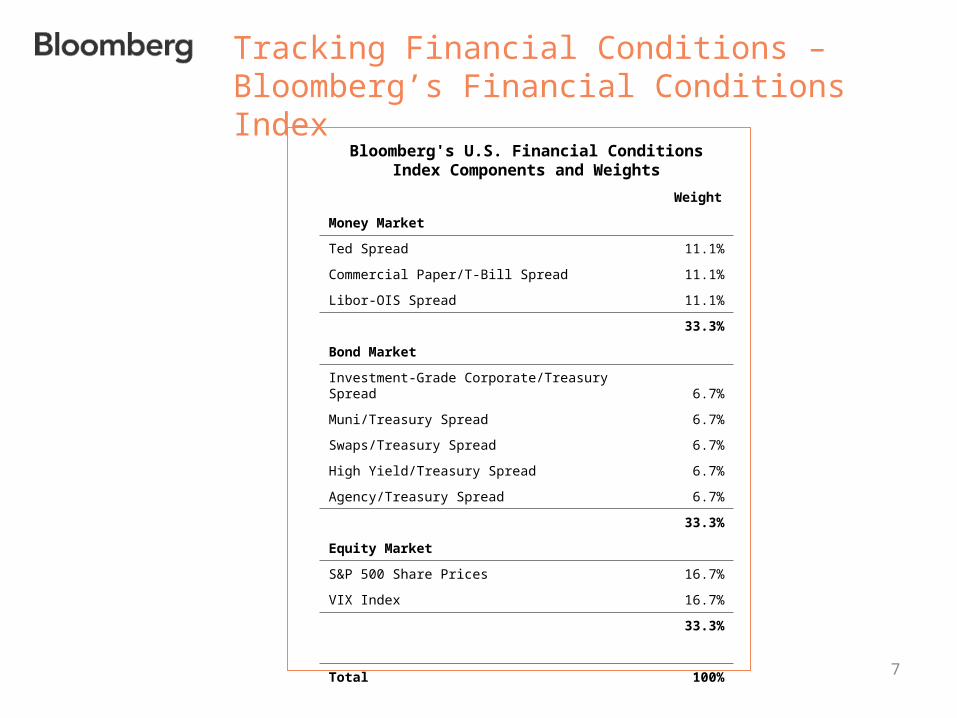

Tracking Financial Conditions –Bloomberg’s Financial Conditions Index

Bloomberg's U.S. Financial Conditions Index Components and Weights

Weight

Money Market

Ted Spread 11.1%

Commercial Paper/T-Bill Spread 11.1%

Libor-OIS Spread 11.1%

33.3%

Bond Market

Investment-Grade Corporate/Treasury Spread 6.7%

Muni/Treasury Spread 6.7%

Swaps/Treasury Spread 6.7%

High Yield/Treasury Spread 6.7%

Agency/Treasury Spread 6.7%

33.3%

Equity Market

S&P 500 Share Prices 16.7%

VIX Index 16.7%

33.3%

Total 100%

8

Bloomberg’s Financial Conditions Index

BFCIUS index <go>Source: Bloomberg

Significantly Below Normal

Significantly Above Normal

Normal

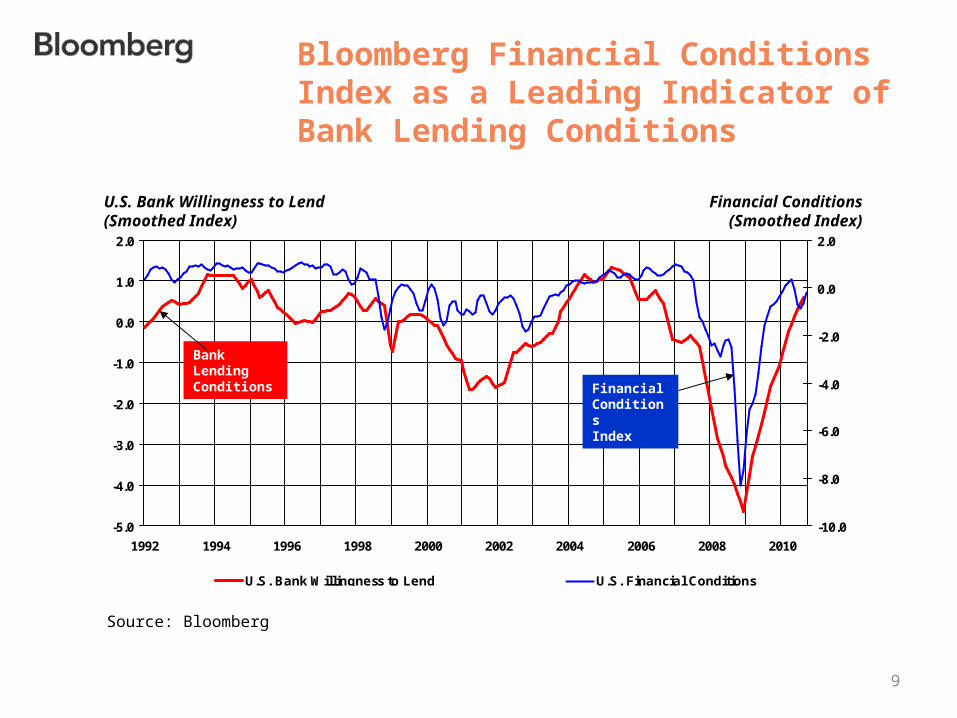

Bloomberg Financial Conditions Index as a Leading Indicator of Bank Lending Conditions

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

U.S. Bank Willingness to Lend U.S. Financial Conditions

U.S. Bank Willingness to Lend(Smoothed Index)

Financial ConditionsIndex

Bank Lending Conditions

Financial Conditions(Smoothed Index)

Source: Bloomberg

9

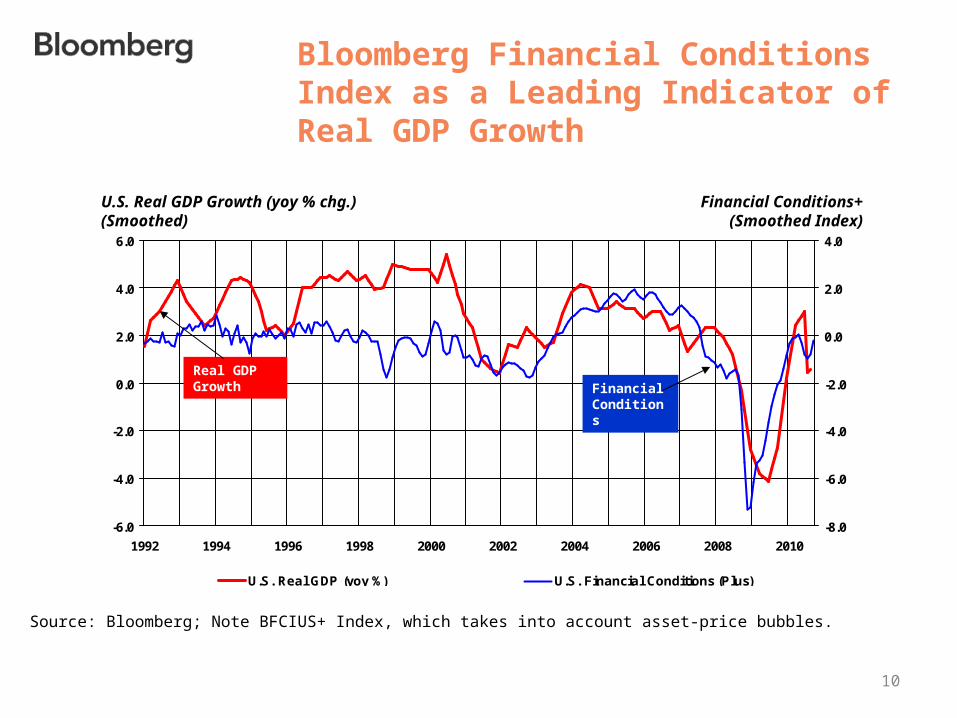

Bloomberg Financial Conditions Index as a Leading Indicator of Real GDP Growth

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

U.S. Real GDP (yoy %) U.S. Financial Conditions (Plus)

U.S. Real GDP Growth (yoy % chg.)(Smoothed)

Financial Conditions

Real GDP Growth

Financial Conditions+(Smoothed Index)

Source: Bloomberg; Note BFCIUS+ Index, which takes into account asset-price bubbles.

10

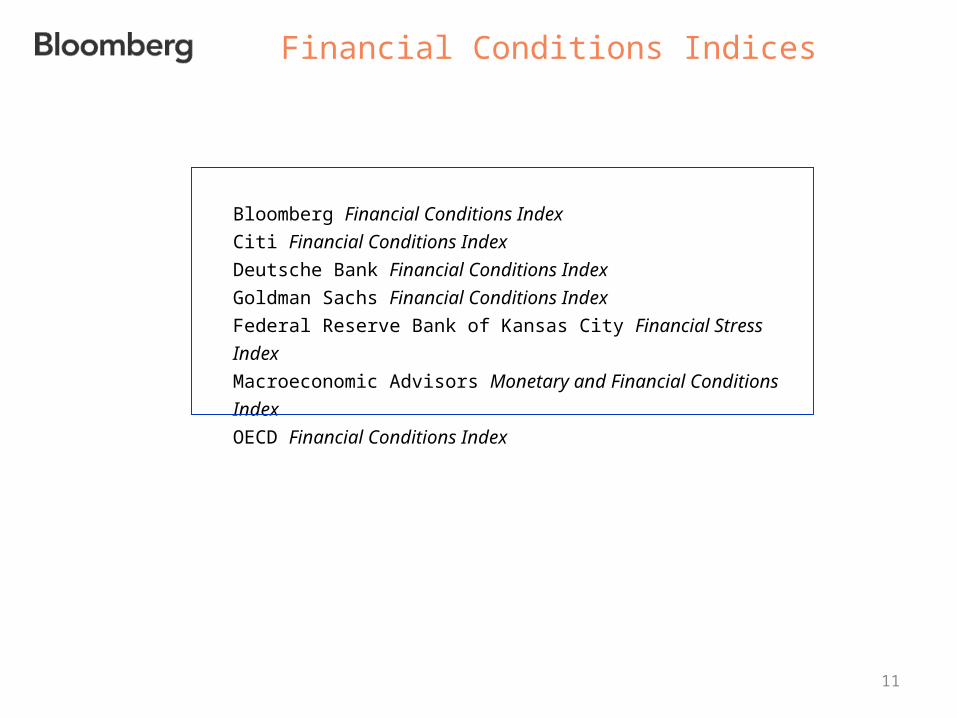

Financial Conditions Indices

11

Bloomberg Financial Conditions Index

Citi Financial Conditions Index

Deutsche Bank Financial Conditions Index

Goldman Sachs Financial Conditions Index

Federal Reserve Bank of Kansas City Financial Stress Index

Macroeconomic Advisors Monetary and Financial Conditions

Index

OECD Financial Conditions Index

12

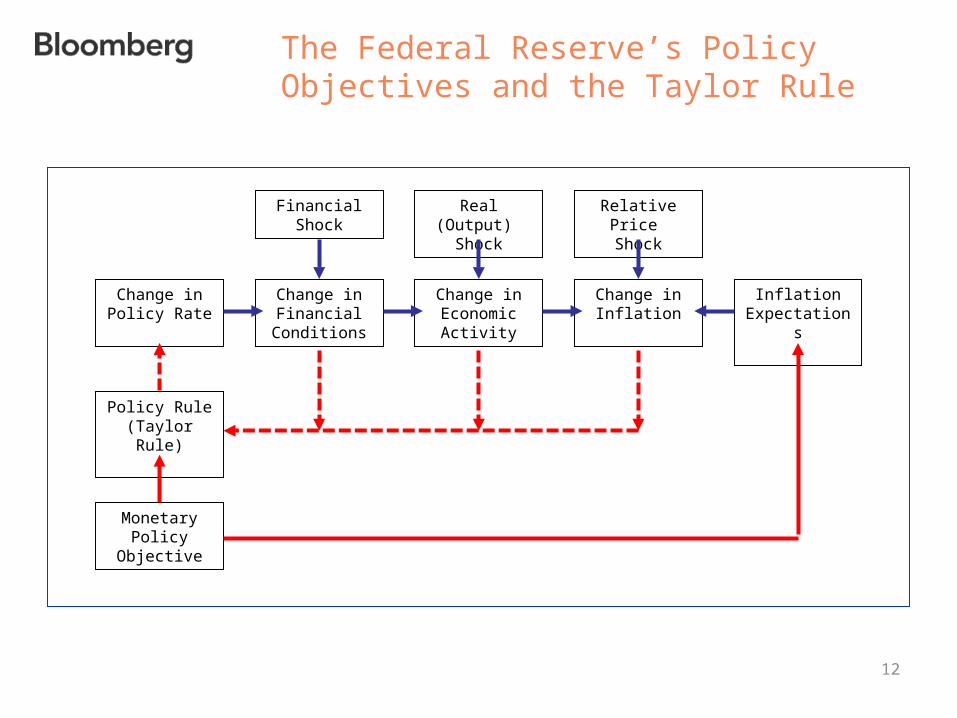

The Federal Reserve’s Policy Objectives and the Taylor Rule

Change inPolicy Rate

Change in Economic

Activity

Financial Shock

Change in Financial

Conditions

Real (Output) Shock

Relative Price Shock

Change in Inflation

Policy Rule(Taylor Rule)

Monetary Policy

Objective

InflationExpectations

13

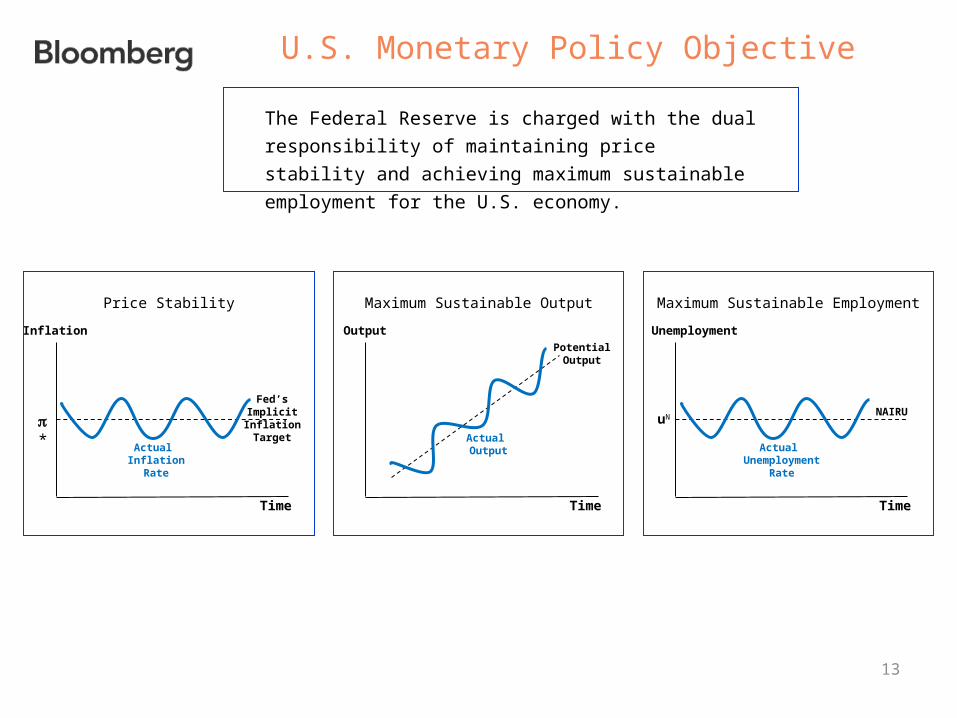

U.S. Monetary Policy Objective

The Federal Reserve is charged with the dual

responsibility of maintaining price stability and

achieving maximum sustainable employment for the

U.S. economy.

Fed’s ImplicitInflation Target

Inflation

Time

*

Actual Inflation

Rate

Price Stability

PotentialOutput

Output

Time

Actual Output

Maximum Sustainable Output

NAIRU

Unemployment

Time

uN

Actual Unemployment

Rate

Maximum Sustainable Employment

14

The Inflation/Output Tradeoff Curve

Output Gap Volatility

B

Std. Dev. (Y-Y*)3

Inflation GapVolatility

The Efficient Policy Frontier

A

CStd. Dev. (Y-Y*)2

Std. Dev. (Y-Y*)1

Std. Dev. (-*)3

Std. Dev. (-*)2

Std. Dev. (-*)1

15

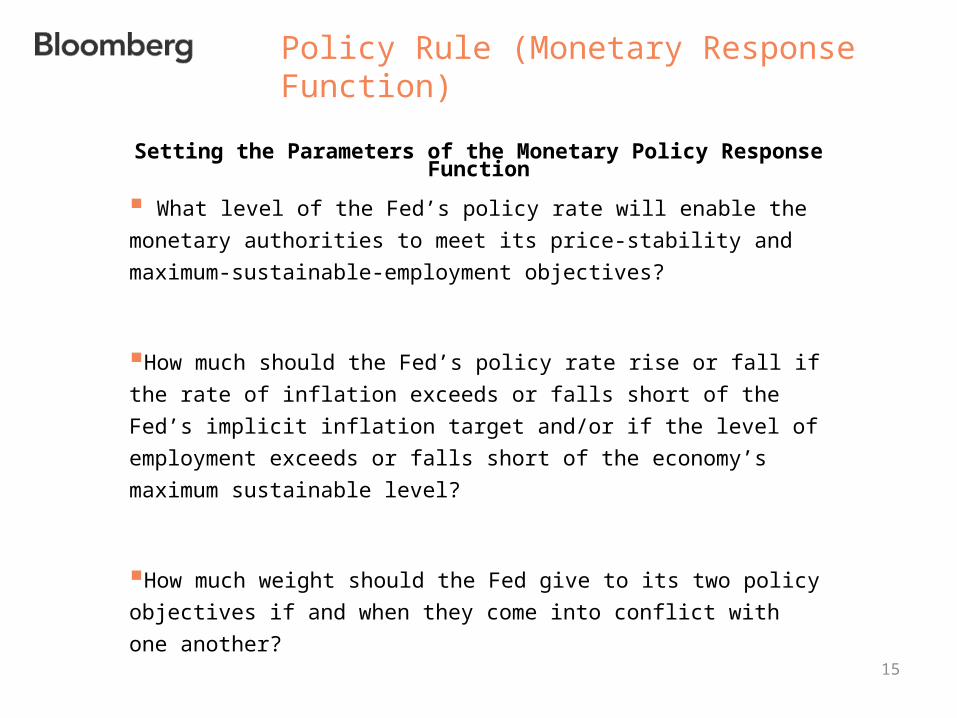

What level of the Fed’s policy rate will enable the monetary authorities

to meet its price-stability and maximum-sustainable-employment

objectives?

How much should the Fed’s policy rate rise or fall if the rate of inflation

exceeds or falls short of the Fed’s implicit inflation target and/or if the

level of employment exceeds or falls short of the economy’s maximum

sustainable level?

How much weight should the Fed give to its two policy objectives if and

when they come into conflict with one another?

Policy Rule (Monetary Response Function)

Setting the Parameters of the Monetary Policy Response Function

16

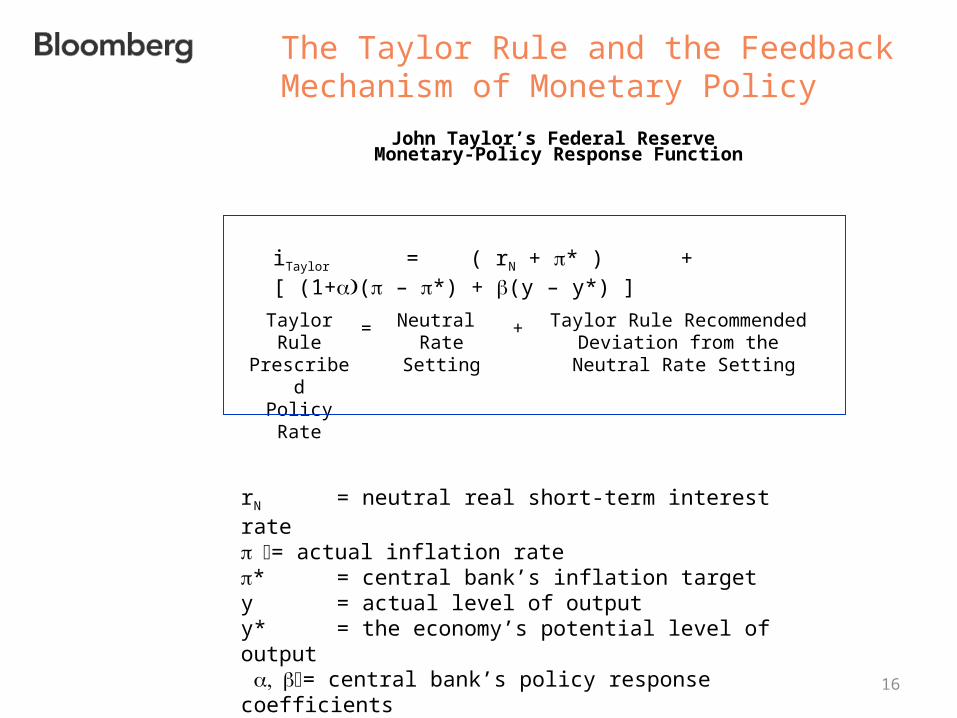

The Taylor Rule and the Feedback Mechanism of Monetary Policy

John Taylor’s Federal Reserve Monetary-Policy Response Function

Taylor Rule PrescribedPolicy Rate

Neutral Rate

Setting

iTaylor = ( rN + * ) + [ (1+( – *) + (y – y*) ]

Taylor Rule Recommended Deviation from the

Neutral Rate Setting

= +

rN = neutral real short-term interest rate= actual inflation rate* = central bank’s inflation targety = actual level of outputy* = the economy’s potential level of output = central bank’s policy response coefficients

17

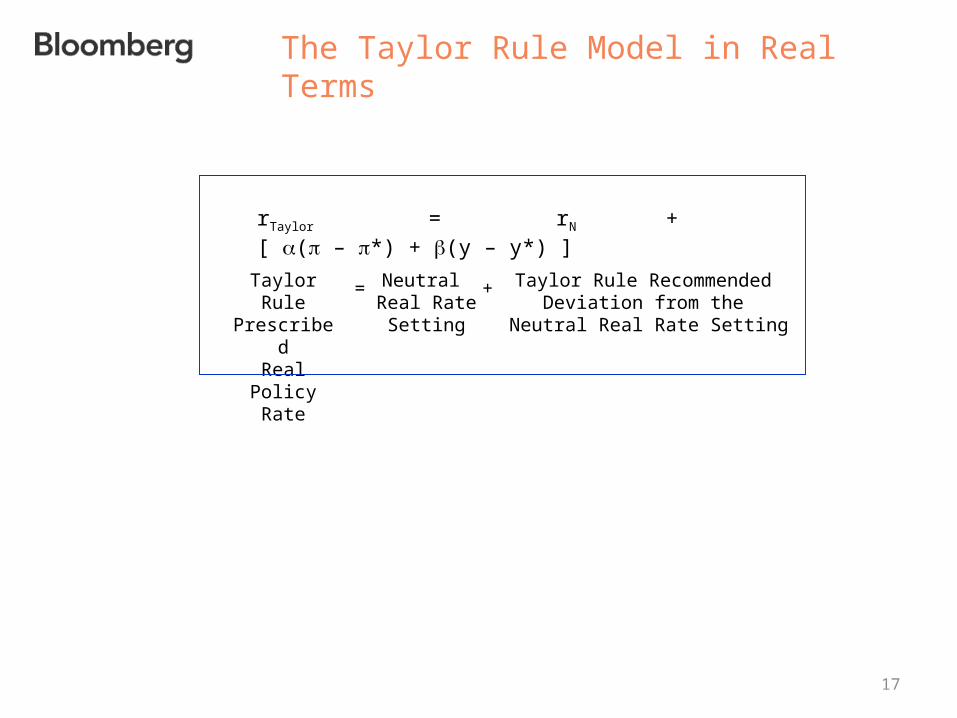

The Taylor Rule Model in Real Terms

Taylor Rule PrescribedReal Policy

Rate

Neutral Real Rate

Setting

rTaylor = rN + [ ( – *) + (y – y*) ]

Taylor Rule Recommended Deviation from the

Neutral Real Rate Setting

= +

18

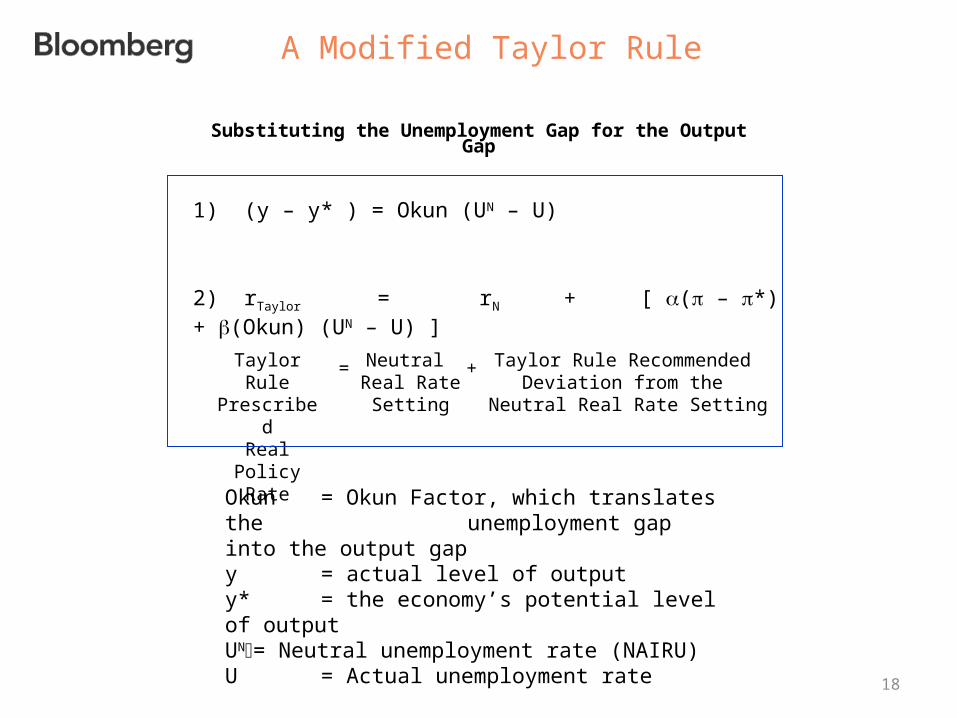

A Modified Taylor Rule

Substituting the Unemployment Gap for the Output Gap

Taylor Rule PrescribedReal Policy

Rate

Neutral Real Rate

Setting

2) rTaylor = rN + [ ( – *) + (Okun) (UN – U) ]

Taylor Rule Recommended Deviation from the

Neutral Real Rate Setting

= +

1) (y – y* ) = Okun (UN – U)

Okun = Okun Factor, which translates the unemployment gap into the output gap

y = actual level of outputy* = the economy’s potential level of outputUN= Neutral unemployment rate (NAIRU)U = Actual unemployment rate

19

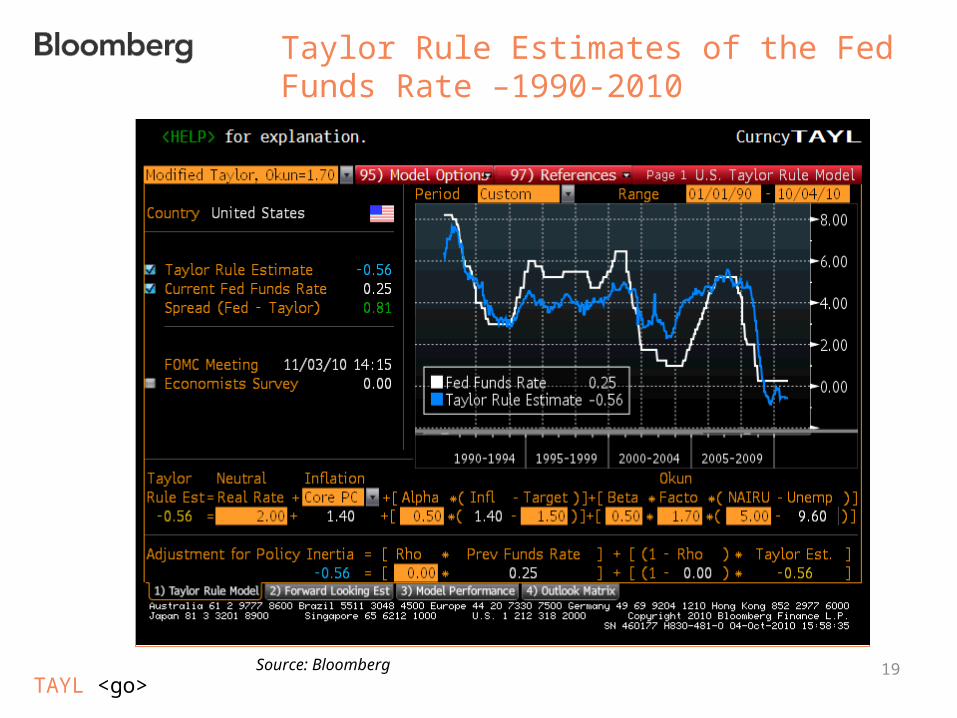

Taylor Rule Estimates of the Fed Funds Rate –1990-2010

TAYL <go>Source: Bloomberg

20

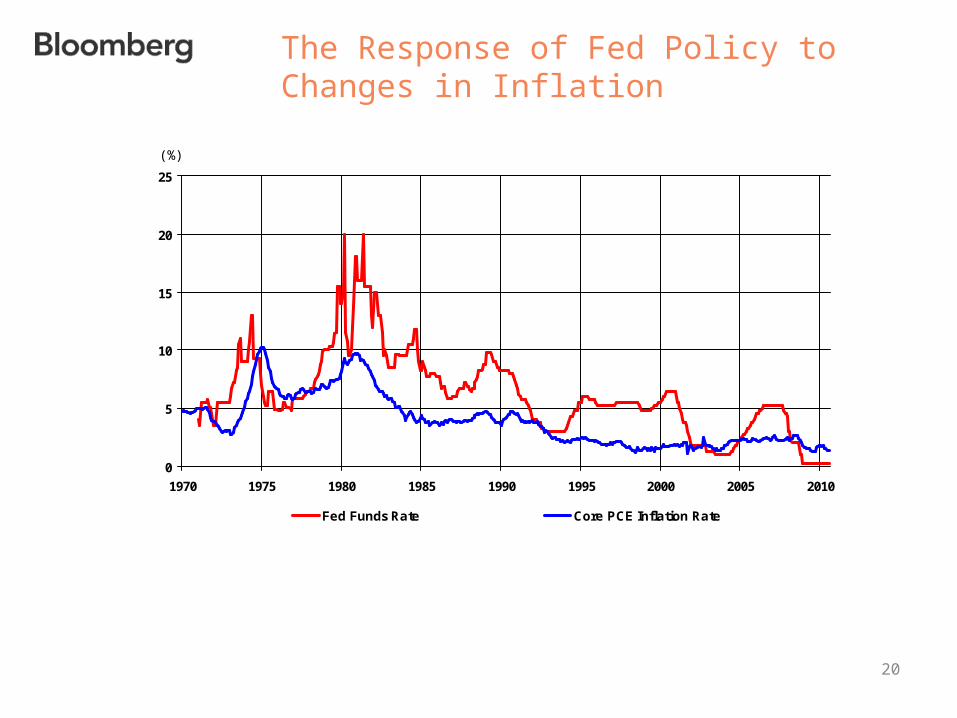

The Response of Fed Policy to Changes in Inflation

0

5

10

15

20

25

1970 1975 1980 1985 1990 1995 2000 2005 2010

Fed Funds Rate Core PCE Inflation Rate

(%)

21

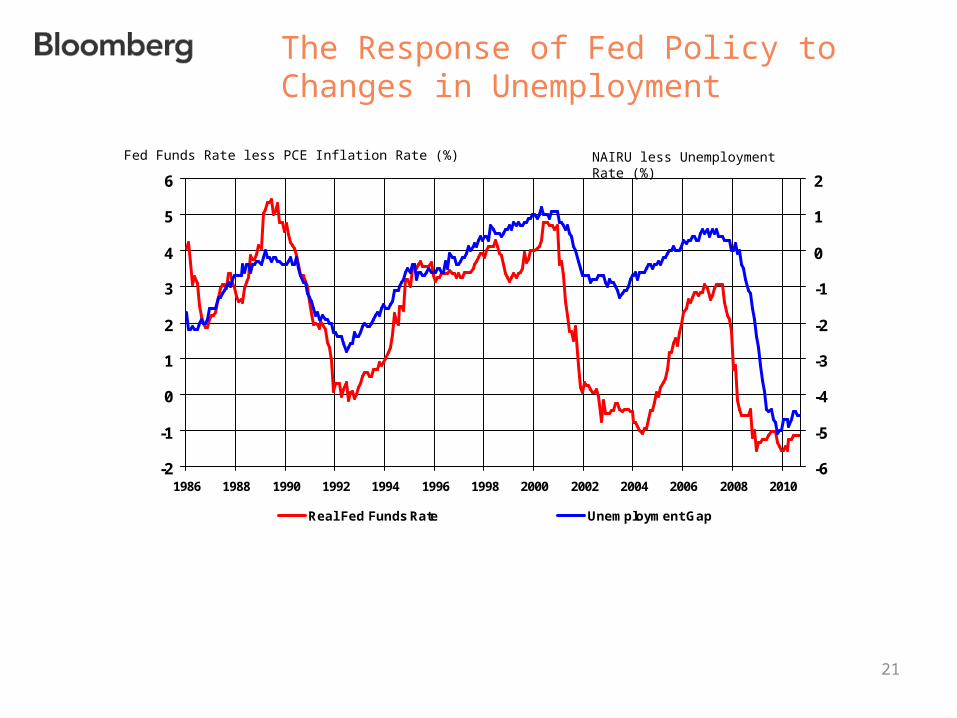

The Response of Fed Policy to Changes in Unemployment

-2

-1

0

1

2

3

4

5

6

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010-6

-5

-4

-3

-2

-1

0

1

2

Real Fed Funds Rate Unemployment Gap

Fed Funds Rate less PCE Inflation Rate (%) NAIRU less Unemployment Rate (%)

22

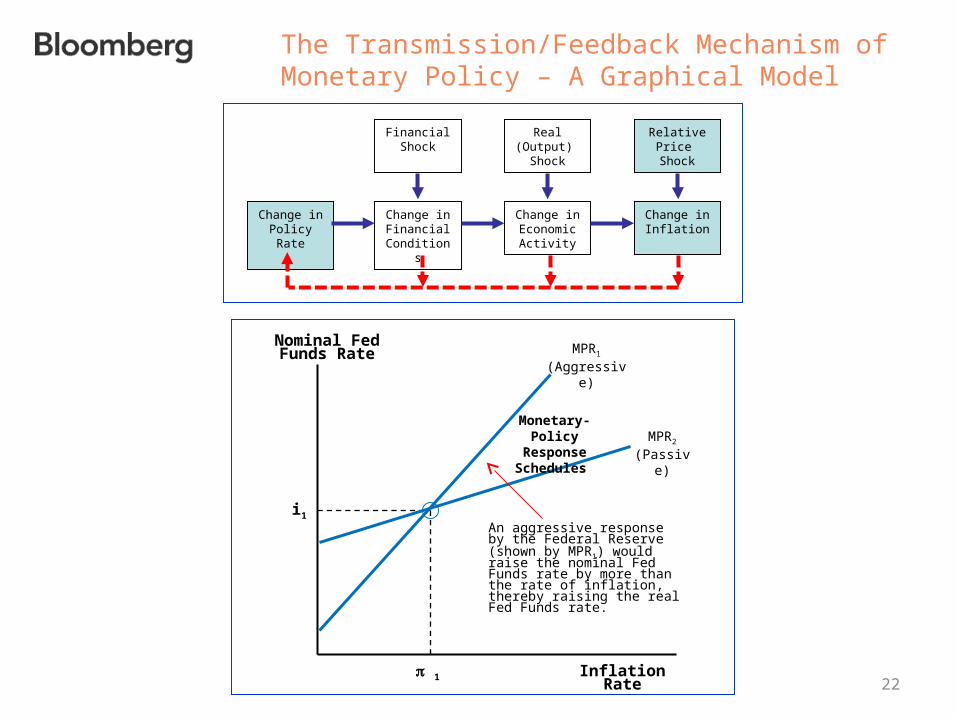

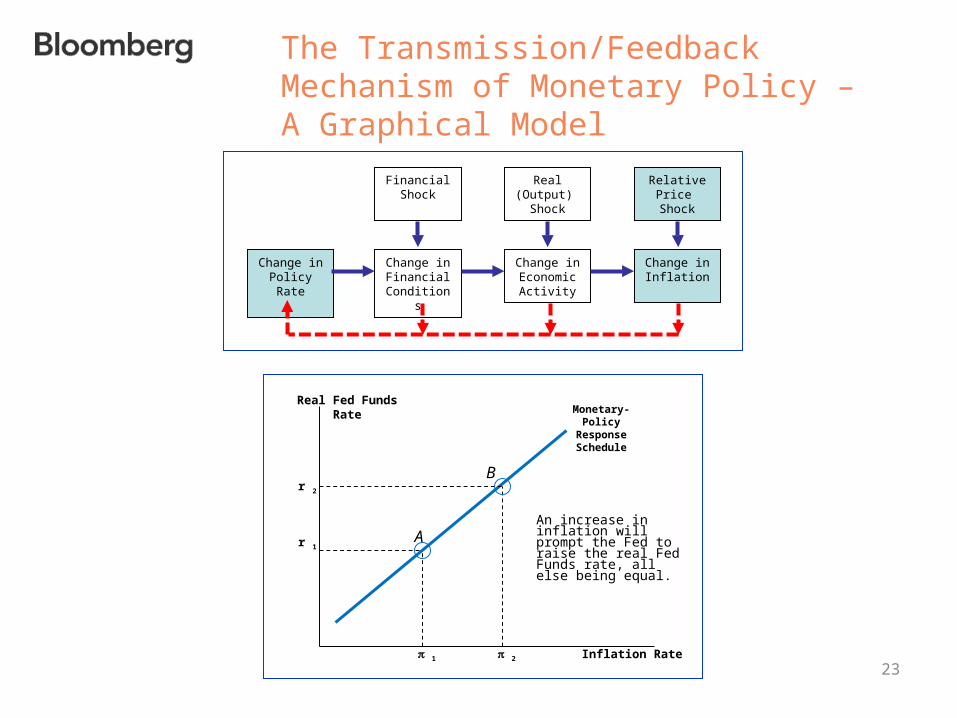

The Transmission/Feedback Mechanism of Monetary Policy – A Graphical Model

Change inPolicy Rate

Change in Economic

Activity

Financial Shock

Change in Financial

Conditions

Real (Output)

Shock

Relative Price Shock

Change in Inflation

Nominal Fed Funds Rate

Inflation Rate

An aggressive response by the Federal Reserve (shown by MPR1) would raise the nominal Fed Funds rate by more than the rate of inflation, thereby raising the real Fed Funds rate.

i1

1

MPR1

(Aggressive)

Monetary-Policy Response Schedules

MPR2

(Passive)

23

The Transmission/Feedback Mechanism of Monetary Policy – A Graphical Model

Change inPolicy Rate

Change in Economic

Activity

Financial Shock

Change in Financial

Conditions

Real (Output)

Shock

Relative Price Shock

Change in Inflation

Monetary-Policy Response Schedule

Real Fed Funds Rate

Inflation Rate 1 2

r 1

r 2

An increase in inflation will prompt the Fed to raise the real Fed Funds rate, all else being equal.

B

A

24

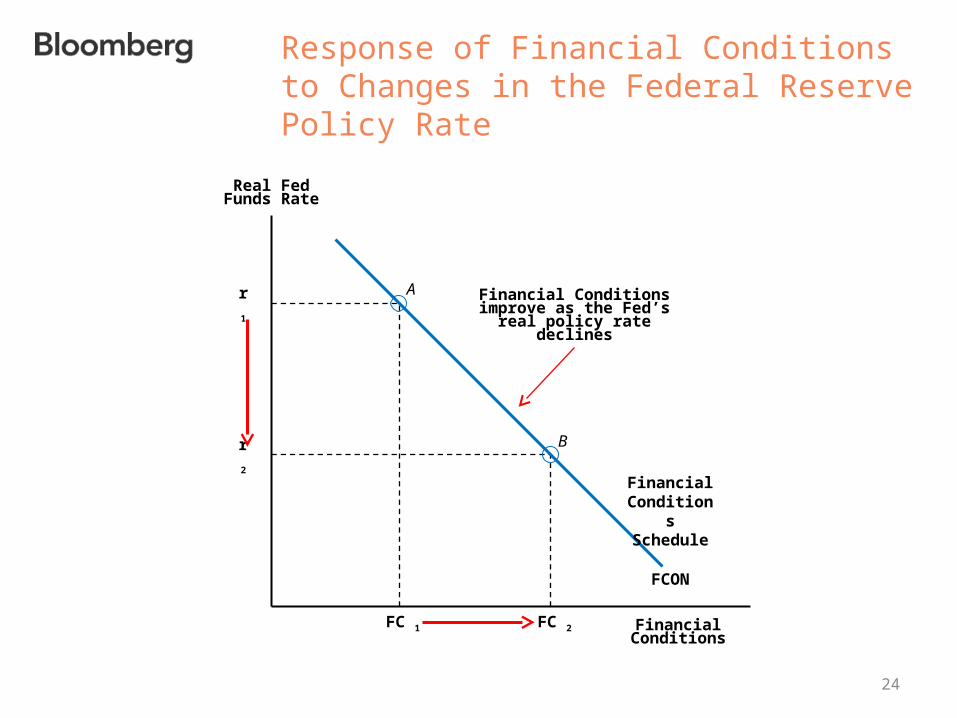

Response of Financial Conditions to Changes in the Federal Reserve Policy Rate

Real Fed Funds Rate

B

Financial Conditions

Financial Conditions improve as the Fed’s real

policy rate declines

Ar 1

r 2

FC 1 FC 2

FCON

Financial Conditions Schedule

25

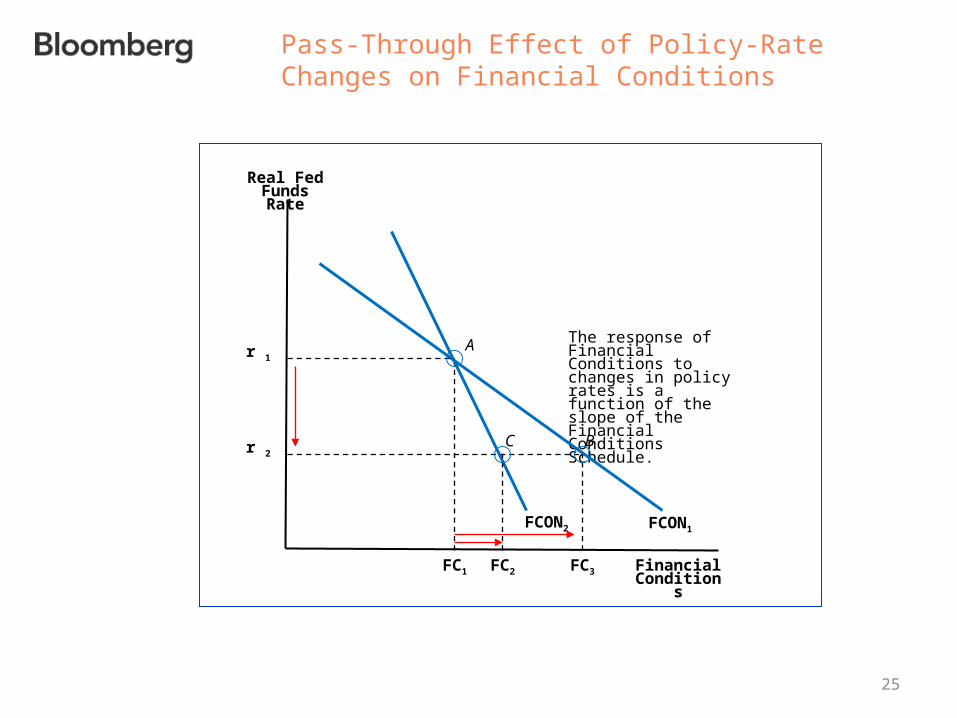

Pass-Through Effect of Policy-Rate Changes on Financial Conditions

Real Fed Funds Rate

B

Financial Conditions

The response of Financial Conditions to changes in policy rates is a function of the slope of the Financial Conditions Schedule.

A

FC1

r 2

FCON1

FC2

C

FCON2

r 1

FC3

26

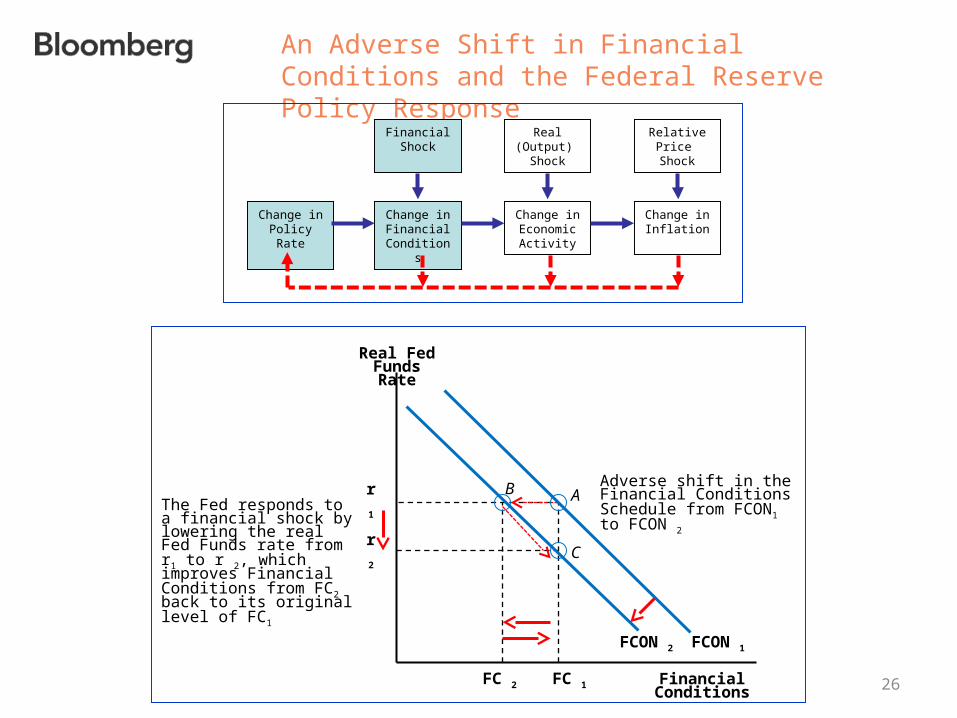

An Adverse Shift in Financial Conditions and the Federal Reserve Policy Response

Change inPolicy Rate

Change in Economic

Activity

Financial Shock

Change in Financial

Conditions

Real (Output)

Shock

Relative Price Shock

Change in Inflation

Real Fed Funds Rate

B

Financial Conditions

Adverse shift in the Financial Conditions Schedule from FCON1 to FCON 2

Ar 1

r 2

FC 1FC 2

C

The Fed responds to a financial shock by lowering the real Fed Funds rate from r1 to r 2, which improves Financial Conditions from FC2 back to its original level of FC1

FCON 1FCON 2

27

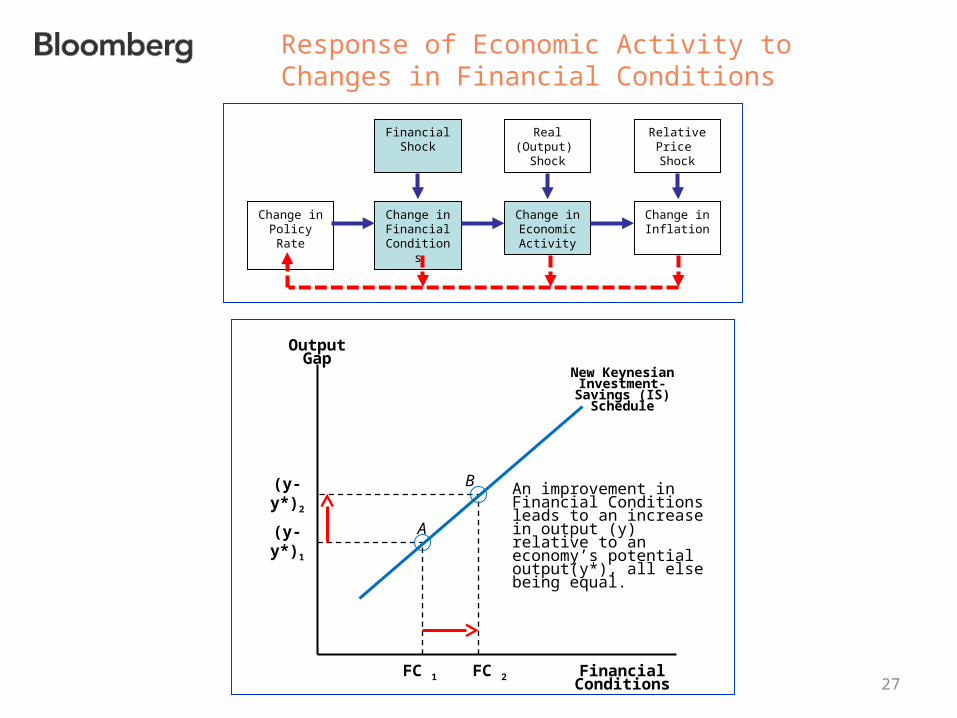

Response of Economic Activity to Changes in Financial Conditions

Change inPolicy Rate

Change in Economic

Activity

Financial Shock

Change in Financial

Conditions

Real (Output)

Shock

Relative Price Shock

Change in Inflation

Output Gap

B

Financial Conditions

An improvement in Financial Conditions leads to an increase in output (y) relative to an economy’s potential output(y*), all else being equal.

A(y-y*)1

FC 2FC 1

New Keynesian Investment-Savings (IS)

Schedule

(y-y*)2

28

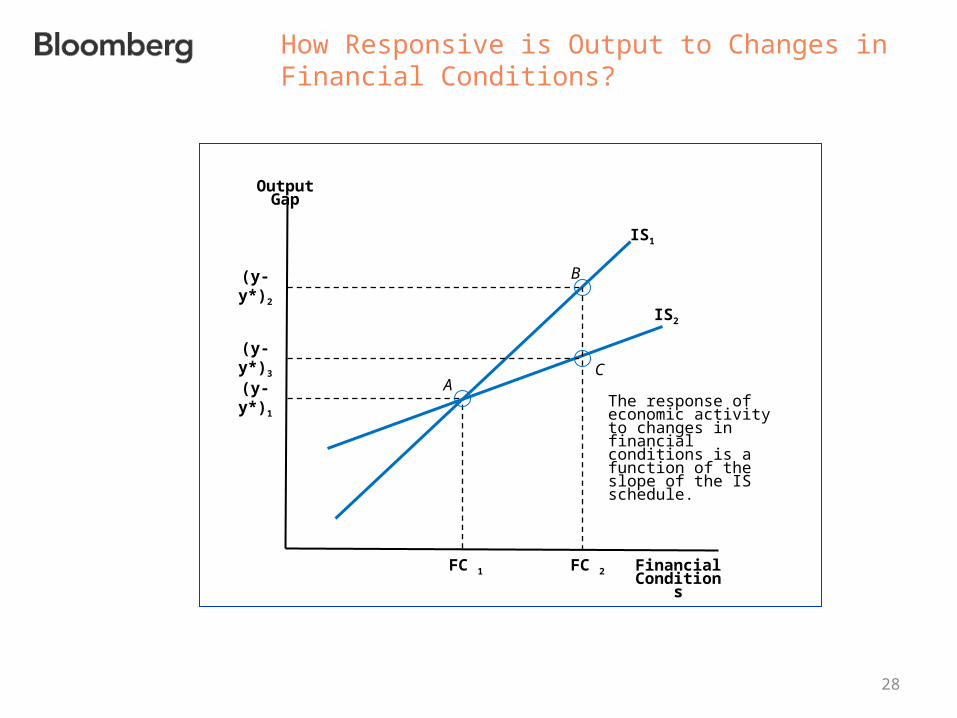

How Responsive is Output to Changes in Financial Conditions?

Output Gap

B

Financial Conditions

The response of economic activity to changes in financial conditions is a function of the slope of the IS schedule.

A(y-y*)1

FC 2FC 1

IS1

(y-y*)2

C(y-y*)3

IS2

29

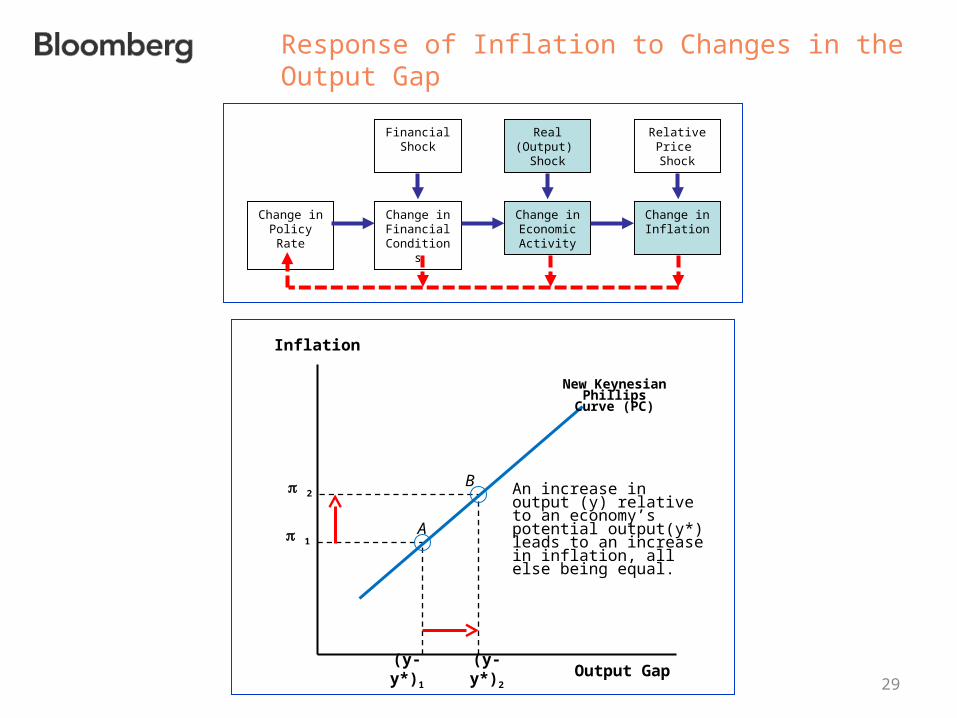

Response of Inflation to Changes in the Output Gap

Change inPolicy Rate

Change in Economic

Activity

Financial Shock

Change in Financial

Conditions

Real (Output)

Shock

Relative Price Shock

Change in Inflation

Inflation

B

Output Gap

An increase in output (y) relative to an economy’s potential output(y*) leads to an increase in inflation, all else being equal.

A

(y-y*)1

2

1

New Keynesian Phillips Curve

(PC)

(y-y*)2

30

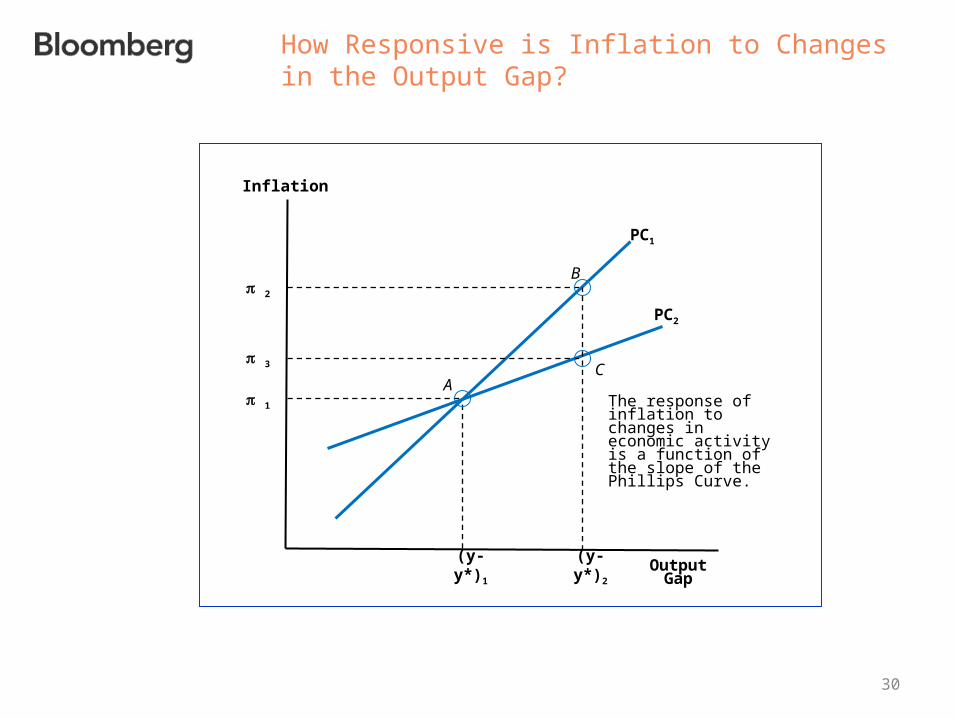

How Responsive is Inflation to Changes in the Output Gap?

Inflation

B

Output Gap

The response of inflation to changes in economic activity is a function of the slope of the Phillips Curve.

A

(y-y*)1

2

PC1

(y-y*)2

C

PC2

1

3

31

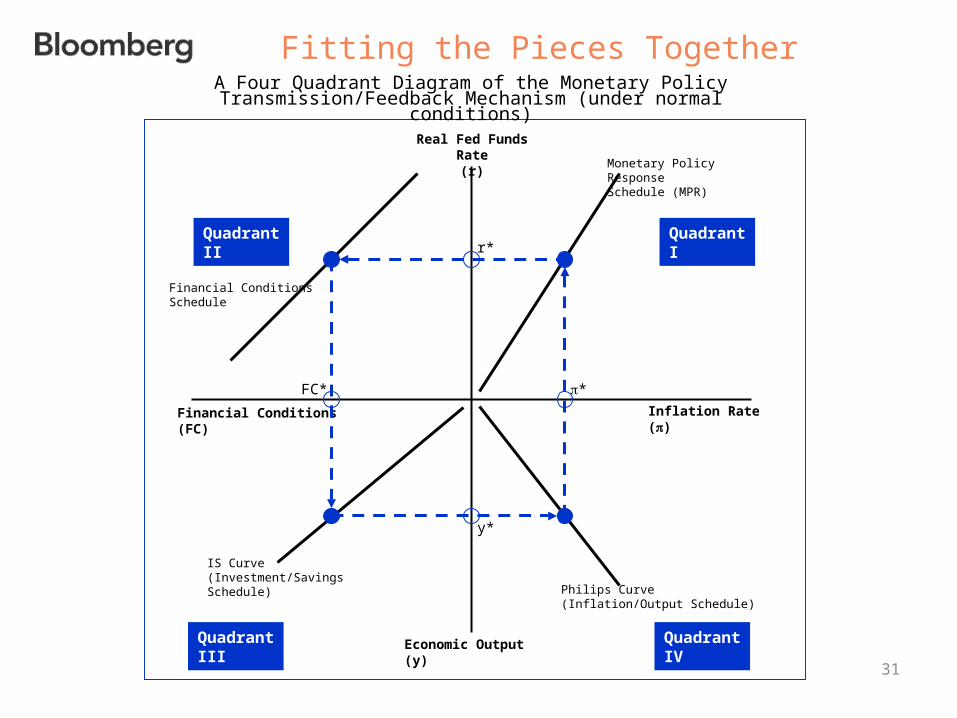

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedule (MPR)

Philips Curve(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedule)

Financial Conditions Schedule

r*

y*

FC* *

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

Fitting the Pieces TogetherA Four Quadrant Diagram of the Monetary Policy

Transmission/Feedback Mechanism (under normal conditions)

32

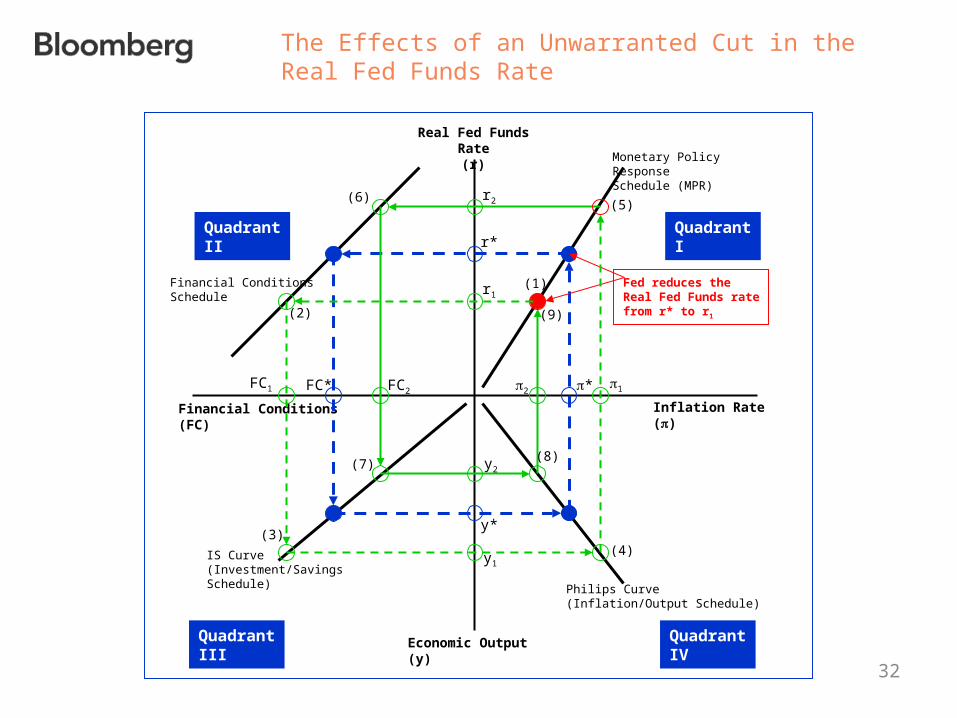

The Effects of an Unwarranted Cut in the Real Fed Funds Rate

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedule (MPR)

Philips Curve(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedule)

Financial Conditions Schedule

r*

y*

FC* *

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

Fed reduces the Real Fed Funds ratefrom r* to r1

r1

21FC2

FC1

y2

y1

r2

(1)

(2)

(3)(4)

(5)(6)

(7)(8)

(9)

33

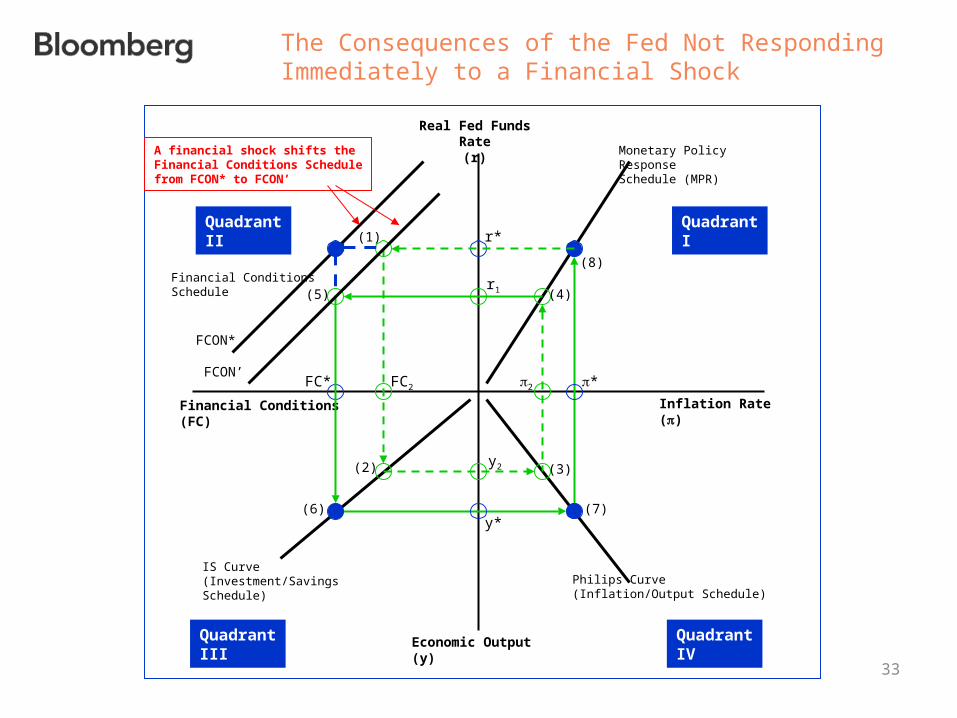

The Consequences of the Fed Not Responding Immediately to a Financial Shock

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedule (MPR)

Philips Curve(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedule)

Financial Conditions Schedule

r*

y*

FC* *

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

r1

2FC2

y2

A financial shock shifts the Financial Conditions Schedulefrom FCON* to FCON’

FCON*

FCON’

(1)

(2) (3)

(4)(5)

(6) (7)

(8)

34

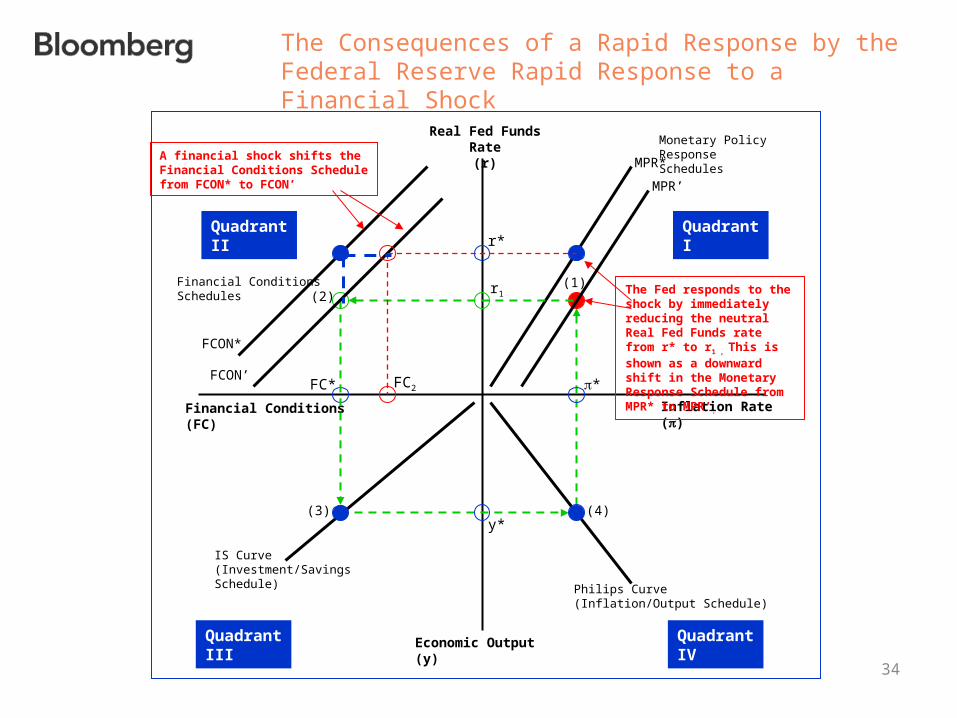

The Consequences of a Rapid Response by the Federal Reserve Rapid Response to a Financial Shock

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedules

Philips Curve(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedule)

Financial Conditions Schedules

r*

y*

FC* *

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

r1

A financial shock shifts the Financial Conditions Schedulefrom FCON* to FCON’

FCON*

FCON’

The Fed responds to the shock by immediately reducing the neutral Real Fed Funds rate from r* to r1 , This is shown as a downward shift in the Monetary Response Schedule from MPR* to MPR’.

MPR*

MPR’

(1)(2)

(3) (4)

FC2

35

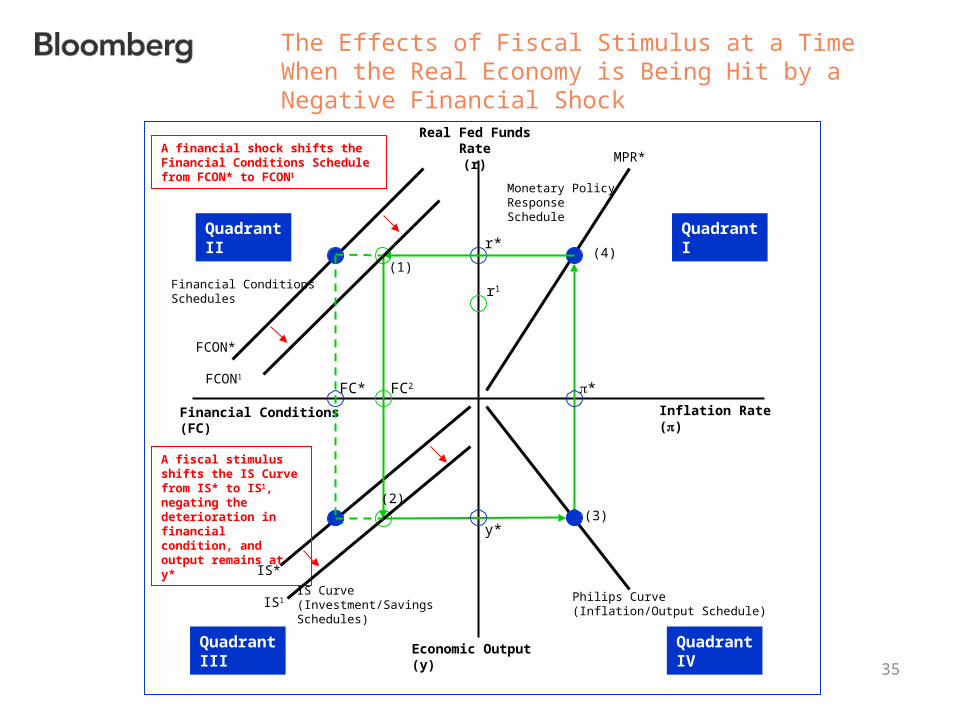

The Effects of Fiscal Stimulus at a Time When the Real Economy is Being Hit by a Negative Financial Shock

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedule

Philips Curve(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedules)

Financial Conditions Schedules

r*

y*

FC* *

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

r1

FC2

A financial shock shifts the Financial Conditions Schedulefrom FCON* to FCON1

FCON*

FCON1

(2)

(1)

(3)

A fiscal stimulus shifts the IS Curve from IS* to IS1, negating the deterioration in financial condition, and output remains at y*

MPR*

(4)

IS*

IS1

36

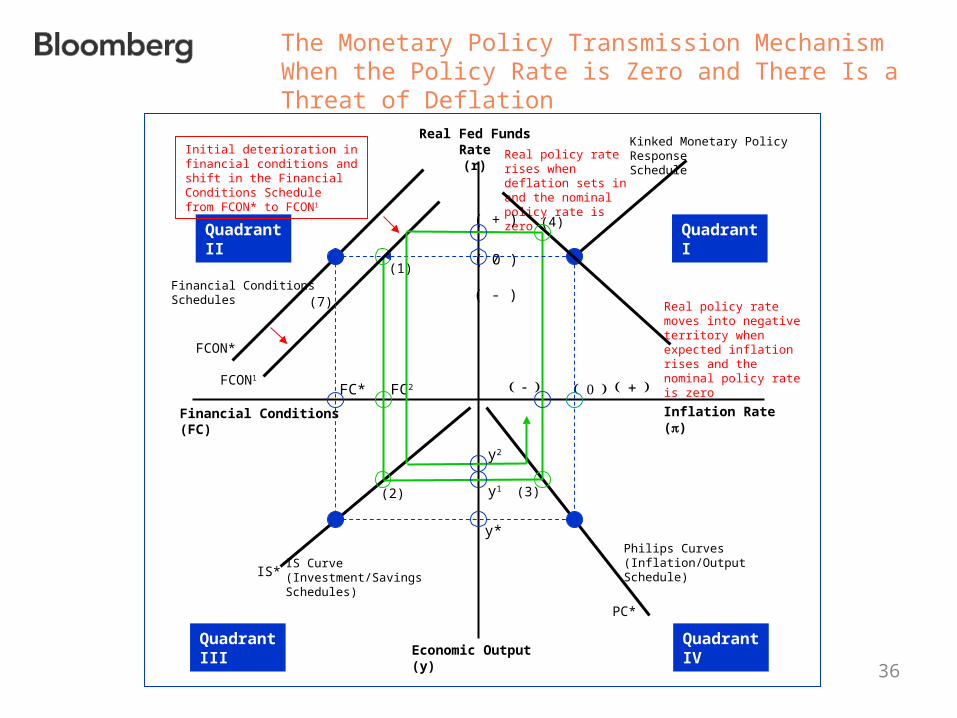

The Monetary Policy Transmission Mechanism When the Policy Rate is Zero and There Is a Threat of Deflation

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Kinked Monetary Policy ResponseSchedule

Philips Curves(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedules)

Financial Conditions Schedules

( 0 )

y*

FC*

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

( - )

FC2

Initial deterioration in financial conditions and shift in the Financial Conditions Schedulefrom FCON* to FCON1

FCON*

FCON1

(2)

(1)

(3)

(4)

IS*

Real policy rate rises when deflation sets in and the nominal policy rate is zero

PC*

Real policy rate moves into negative territory when expected inflation rises and the nominal policy rate is zero

(7)

( + )

.

y2

y1

37

Negating the Real Economy Effects of a Financial Shock by Engineering a Rise in Expected Inflation

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Kinked Monetary Policy ResponseSchedule

Philips Curves(Inflation/Output Schedule)

IS Curve (Investment/Savings Schedules)

Financial Conditions Schedules

y*

FC*

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

FC2

Initial deterioration in financial conditions and shift in the Financial Conditions Schedulefrom FCON* to FCON1

FCON*

FCON1

(2)

(1)

(3)

IS*

Real policy rate rises when deflation sets in and the nominal policy rate is zero

PC*

PC1

Engineered rise inexpected inflation

Real policy rate moves into negative territory when expected inflation rises and the nominal policy rate is zero

(5)

(6)(7)

(8)

(9)

( 0 )

( - )

( + )

.

(4)

38

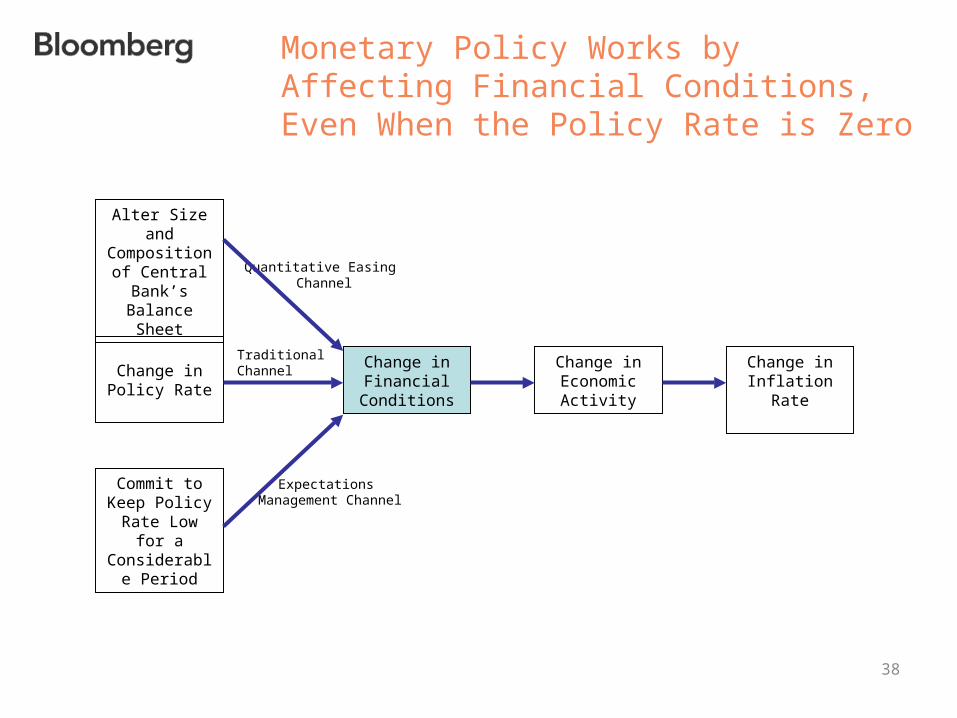

Monetary Policy Works by Affecting Financial Conditions, Even When the Policy Rate is Zero

Change inPolicy Rate

Change in Economic

Activity

Alter Size and Composition of Central Bank’s Balance Sheet

Change in Financial

Conditions

Commit to Keep Policy

Rate Low for a Considerable

Period

Change in Inflation Rate

Quantitative Easing Channel

Expectations Management Channel

Traditional Channel

39

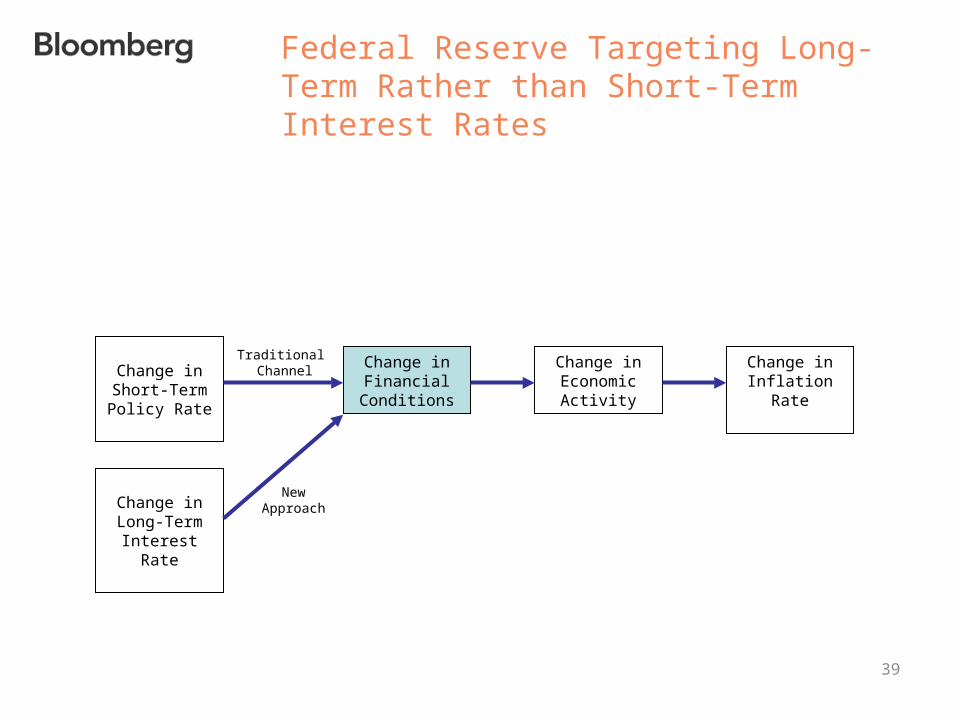

Federal Reserve Targeting Long-Term Rather than Short-Term Interest Rates

Change inShort-Term Policy Rate

Change in Economic

Activity

Change in Financial

Conditions

Change in Long-Term

Interest Rate

Change in Inflation Rate

NewApproach

Traditional Channel

40

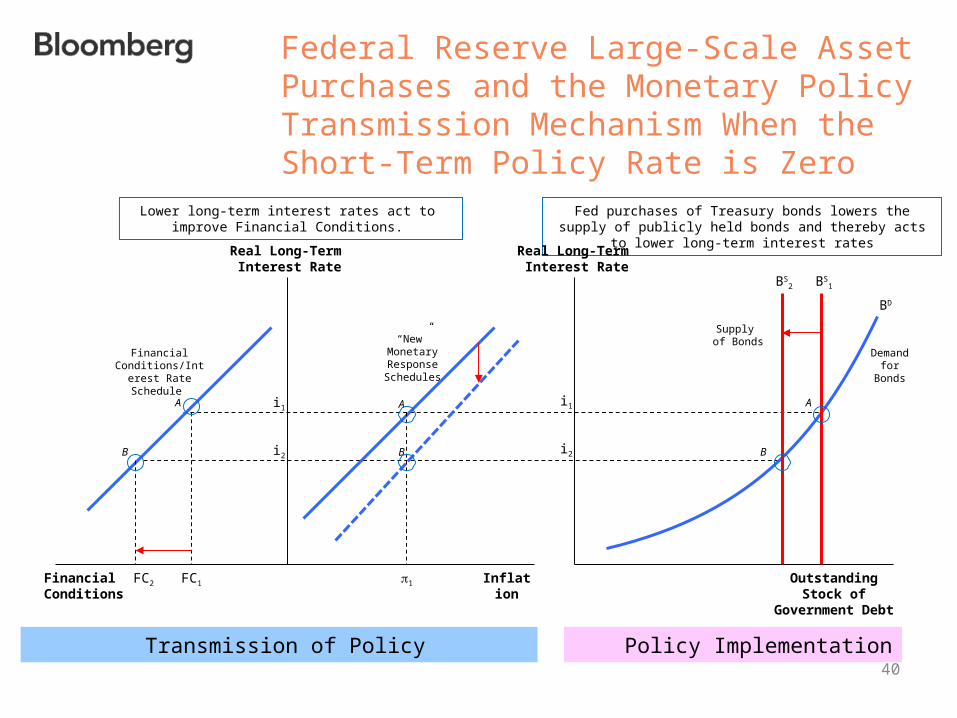

Federal Reserve Large-Scale Asset Purchases and the Monetary Policy Transmission Mechanism When the Short-Term Policy Rate is Zero

Transmission of Policy Policy Implementation

Real Long-Term Interest Rate

Financial Conditions

i1

i2

Outstanding Stock of Government Debt

BS2

Supply of Bonds

FC2 FC1

Fed purchases of Treasury bonds lowers the supply of publicly held bonds and thereby acts to lower long-term interest rates

Lower long-term interest rates act to improve Financial Conditions.

Financial Conditions/Interest

Rate Schedule

“New” Monetary Response Schedules

Real Long-Term Interest Rate

Inflation

i1

i2

1

BS1

Demand for Bonds

BD

A

B

A

B

A

B

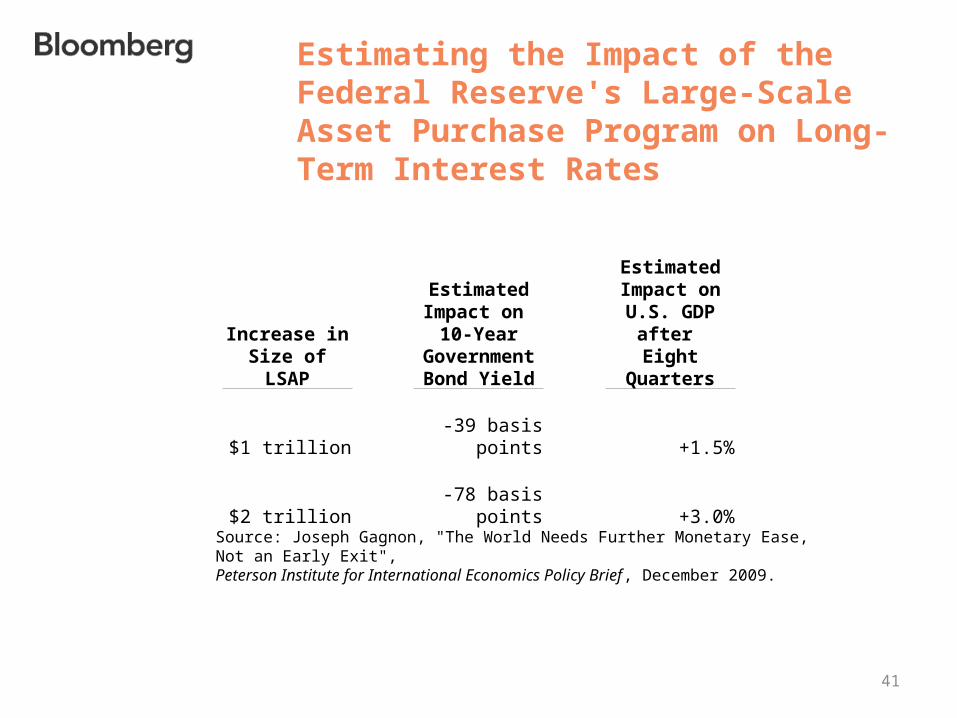

Estimating the Impact of the Federal Reserve's Large-Scale Asset Purchase Program on Long-Term Interest Rates

41

Increase in Size of LSAP

Estimated Impact on

10-Year Government Bond Yield

Estimated Impact on U.S.

GDP after Eight Quarters

$1 trillion -39 basis points +1.5%

$2 trillion -78 basis points +3.0%

Source: Joseph Gagnon, "The World Needs Further Monetary Ease, Not an Early Exit", Peterson Institute for International Economics Policy Brief, December 2009.

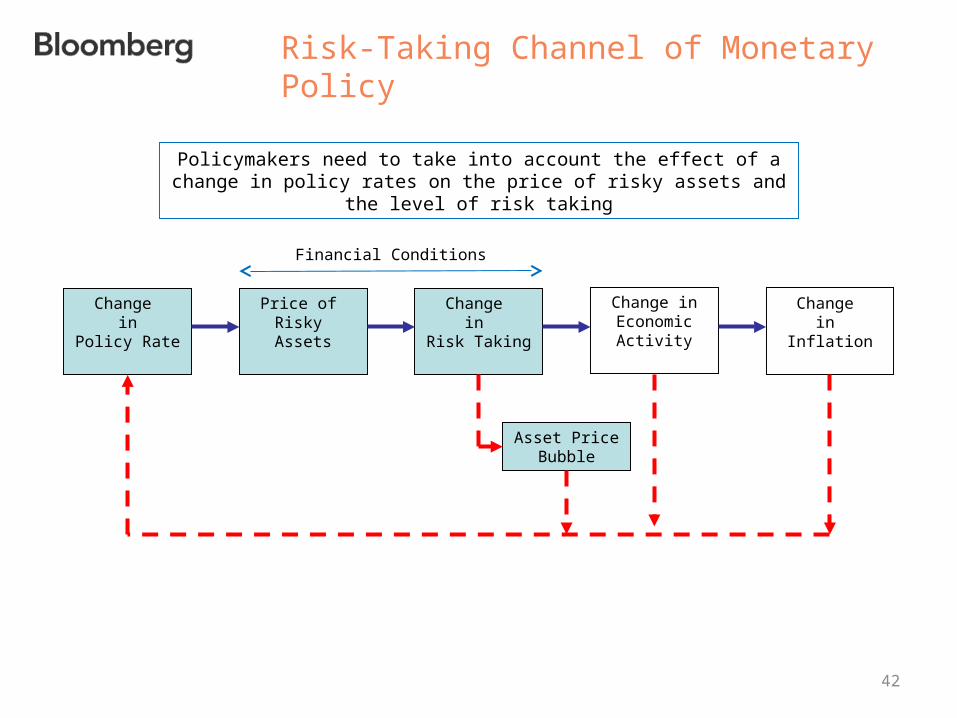

Risk-Taking Channel of Monetary Policy

Change in

Policy Rate

Change in

Risk Taking

Financial Conditions

Price of Risky Assets

Asset Price Bubble

Change in Economic

Activity

Change in

Inflation

42

Policymakers need to take into account the effect of a change in policy rates on the price of risky assets and the level of risk taking

43

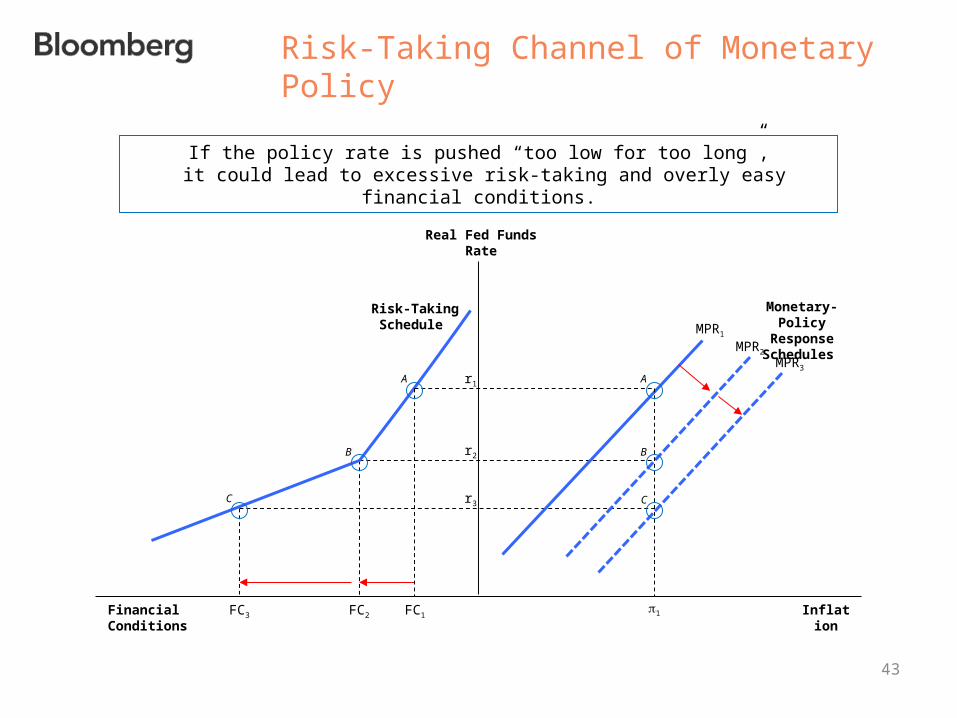

Risk-Taking Channel of Monetary Policy

Real Fed Funds Rate

Financial Conditions

r1

r2

FC2 FC1

If the policy rate is pushed “too low for too long”, it could lead to excessive risk-taking and overly easy financial conditions.

Risk-Taking Schedule

Inflation1

MPR1

Monetary-Policy Response Schedules

r3

FC3

MPR2

MPR3

A

B B

A

CC

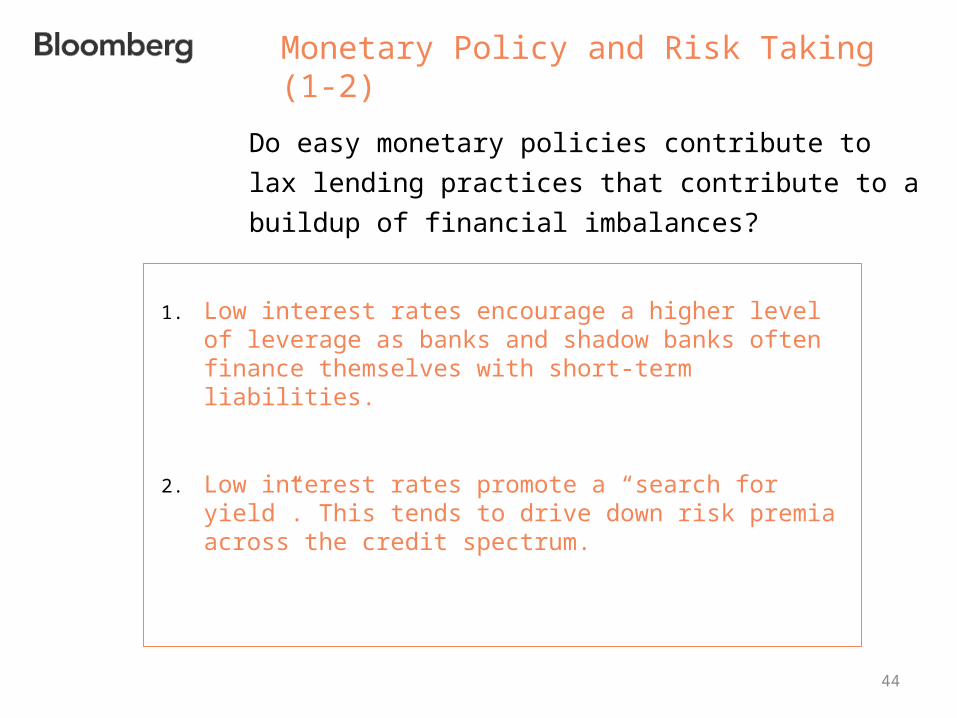

Monetary Policy and Risk Taking (1-2)

44

Do easy monetary policies contribute to lax lending

practices that contribute to a buildup of financial

imbalances?

1. Low interest rates encourage a higher level of leverage as banks and shadow banks often finance themselves with short-term liabilities.

2. Low interest rates promote a “search for yield”. This tends to drive down risk premia across the credit spectrum.

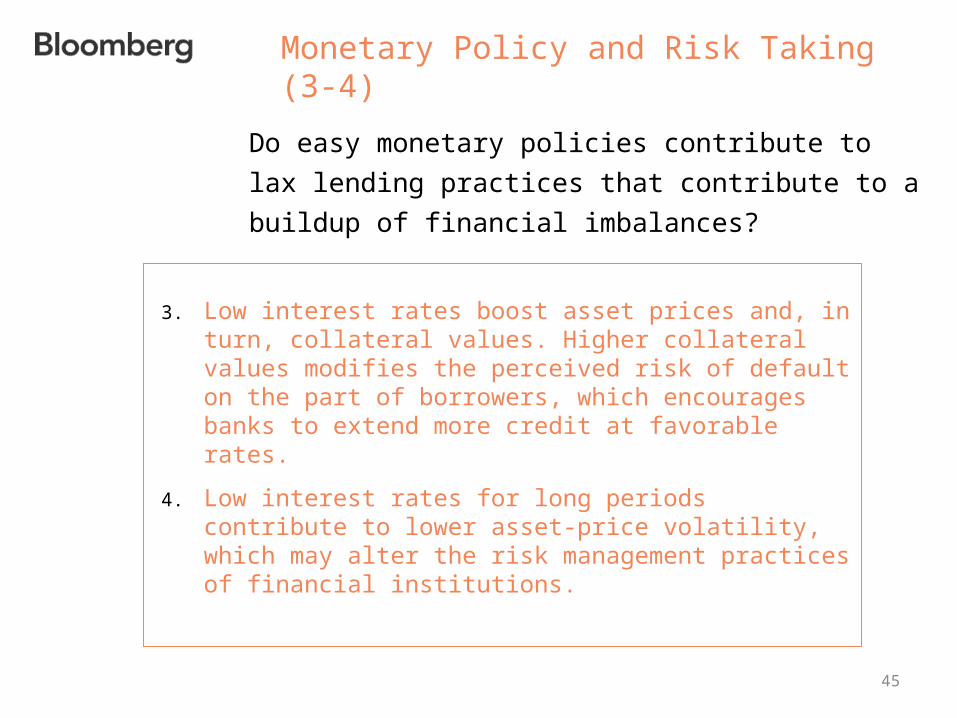

Monetary Policy and Risk Taking (3-4)

45

3. Low interest rates boost asset prices and, in turn, collateral values. Higher collateral values modifies the perceived risk of default on the part of borrowers, which encourages banks to extend more credit at favorable rates.

4. Low interest rates for long periods contribute to lower asset-price volatility, which may alter the risk management practices of financial institutions.

Do easy monetary policies contribute to lax lending

practices that contribute to a buildup of financial

imbalances?

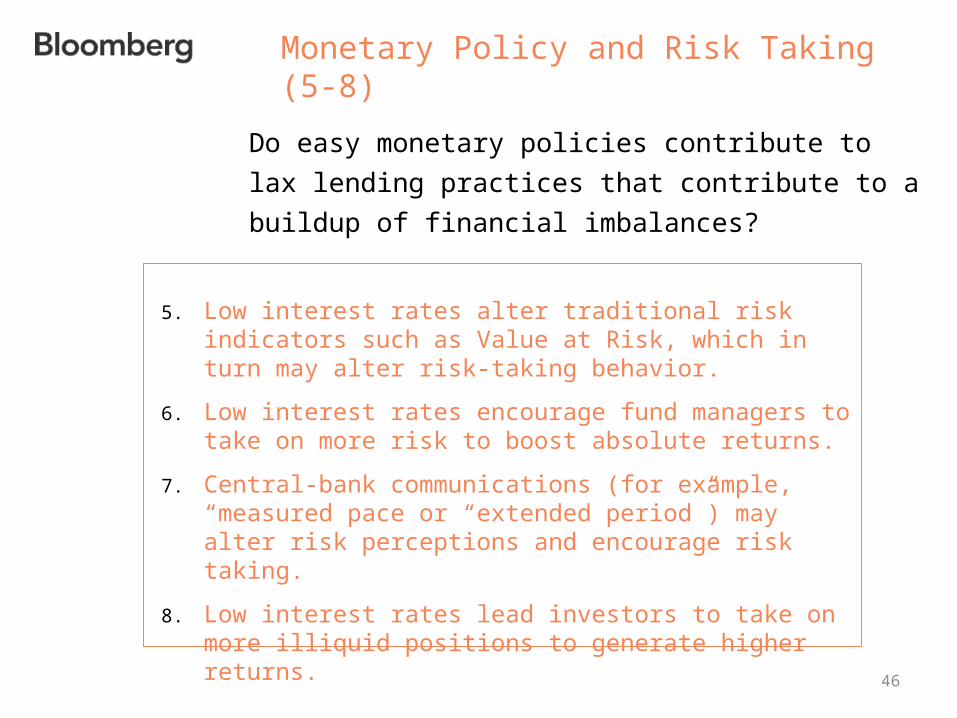

Monetary Policy and Risk Taking (5-8)

46

5. Low interest rates alter traditional risk indicators such as Value at Risk, which in turn may alter risk-taking behavior.

6. Low interest rates encourage fund managers to take on more risk to boost absolute returns.

7. Central-bank communications (for example, “measured pace or “extended period”) may alter risk perceptions and encourage risk taking.

8. Low interest rates lead investors to take on more illiquid positions to generate higher returns.

Do easy monetary policies contribute to lax lending

practices that contribute to a buildup of financial

imbalances?

Monetary Policy and Risk Taking(9-11)

47

9. Federal Reserve may respond asymmetrically to changes in asset prices – easing in response to asset price declines and essentially ignoring asset price gains (the Greenspan put).

10. Credit ratings improve when interest rates are low, which in turn leads to narrower credit spreads.

11. Low interest rates for long periods boost house prices, which encourages household speculation in the housing market

Do easy monetary policies contribute to lax lending

practices that contribute to a buildup of financial

imbalances?

Two Major Criticisms of Federal Reserve Policy

48

Criticism #1 -- Federal Reserve policy was too loose for too long from 2002-2006. Had the Fed not deviated from the Taylor Rule, the housing bubble and the subsequent crisis could have been avoided.

Criticism #2 -- Policymakers did not look beyond inflation and output gaps in setting short-term interest rates in the run-up to the financial crisis. Monetary policy should lean against asset-price movements, even at the cost of more variability in inflation and output.

49

The Taylor Rule on Bloomberg

TAYL <go>

50

Fraction of Time the Real Federal Funds Rate Is Negative by Decade

Source: Board of Governors of the Federal Reserve System and Bureau of Economic Analysis;Note: the real Fed Funds rate equals the nominal Fed Funds rate minus the core PCE inflation rate.

Decade of High Inflation

Decade of Asset Bubbles

51

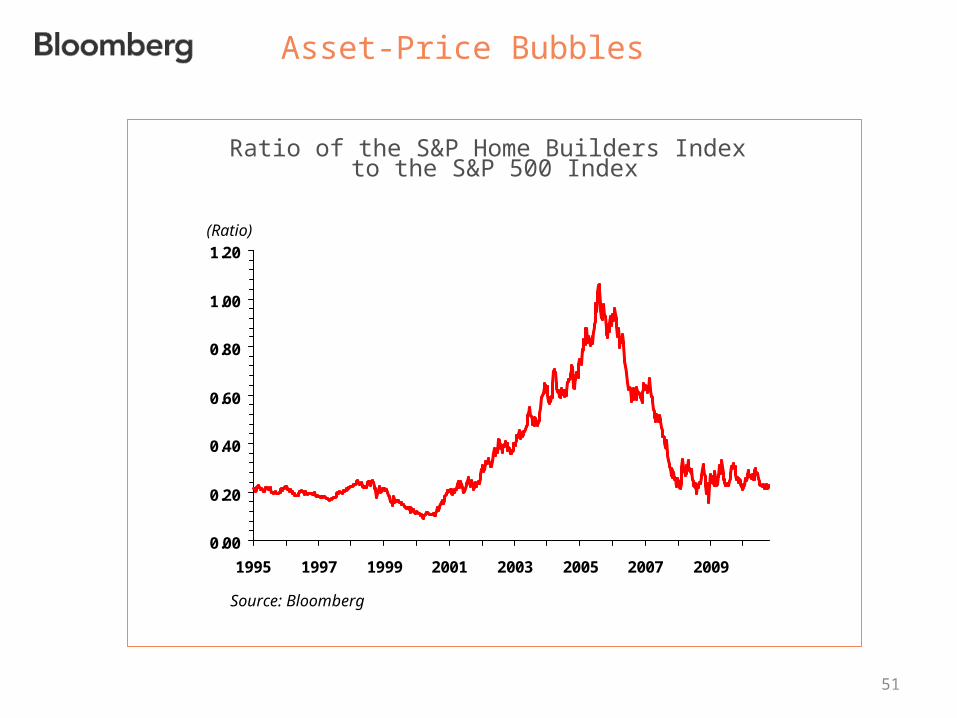

Asset-Price Bubbles

Ratio of the S&P Home Builders Index to the S&P 500 Index

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1995 1997 1999 2001 2003 2005 2007 2009

(Ratio)

Source: Bloomberg

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

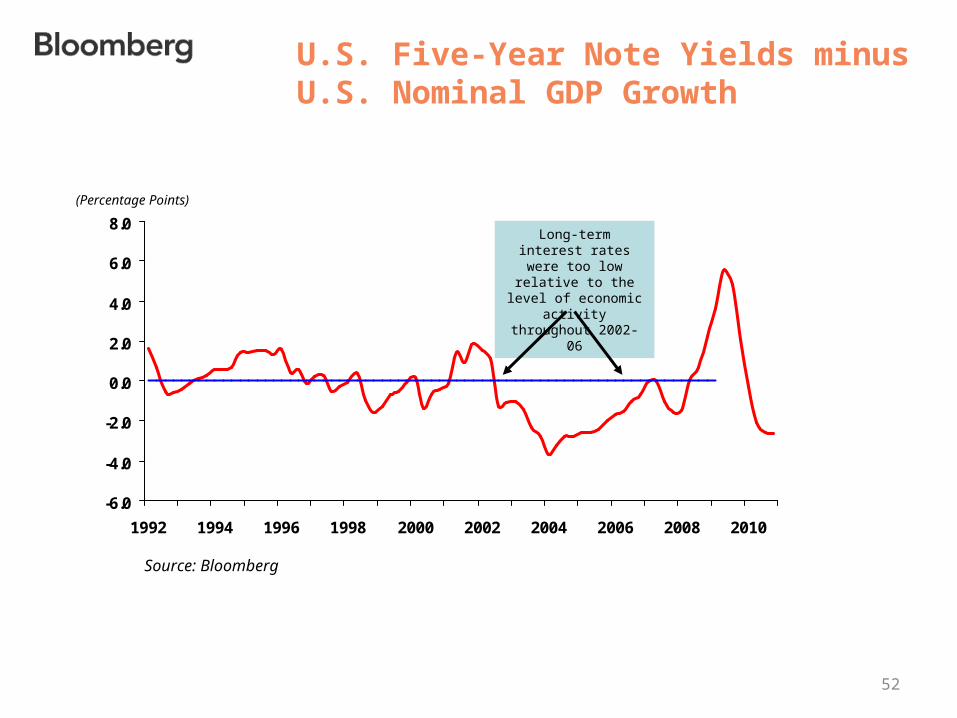

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

U.S. Five-Year Note Yields minus U.S. Nominal GDP Growth

(Percentage Points)

Source: Bloomberg

Long-term interest rates were too low relative to the level of economic

activity throughout 2002-06

52

0

1

2

3

4

5

6

7

8

9

10

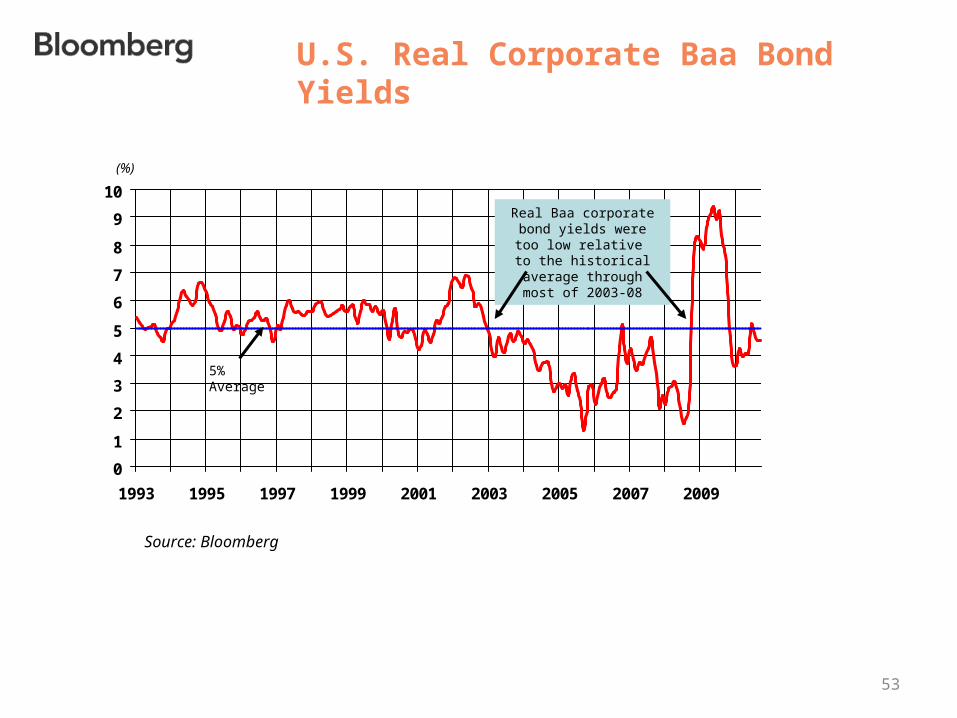

1993 1995 1997 1999 2001 2003 2005 2007 2009

U.S. Real Corporate Baa Bond Yields

(%)

5% Average

Source: Bloomberg

Real Baa corporate bond yields were too low

relative to the historical average through most of

2003-08

53

54

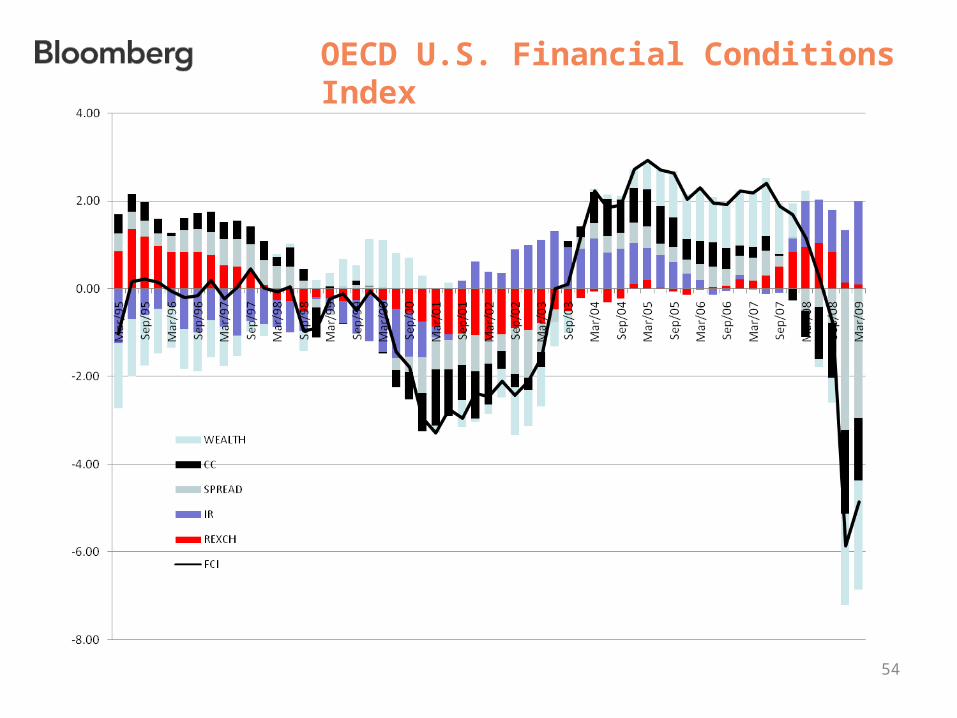

OECD U.S. Financial Conditions Index

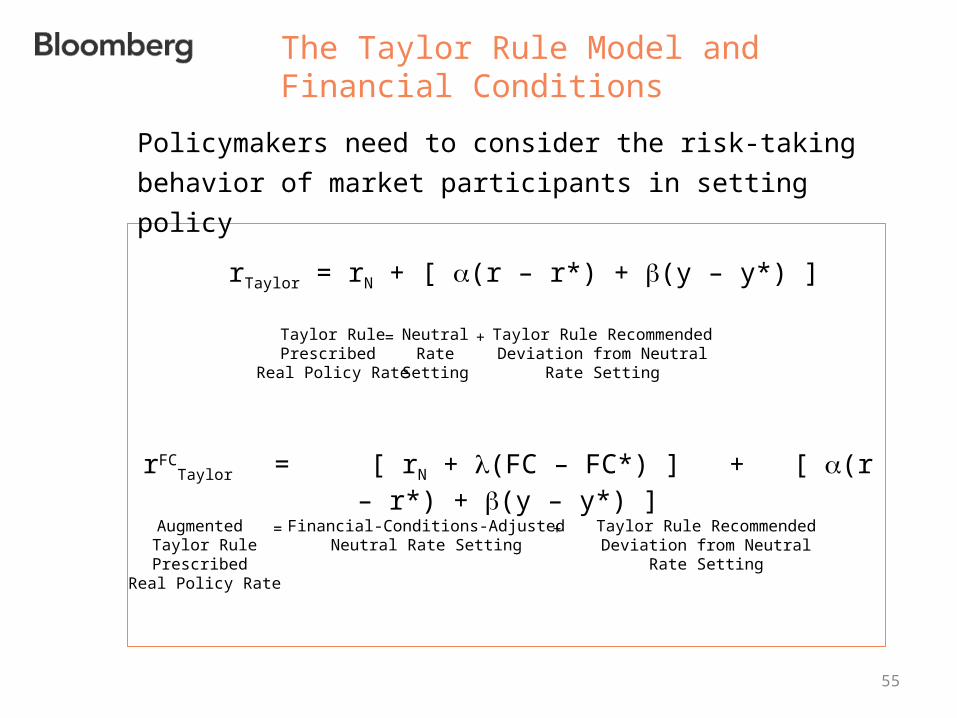

The Taylor Rule Model and Financial Conditions

55

rTaylor = rN + [ (r – r*) + (y – y*) ]

rFCTaylor

= [ rN + (FC – FC*) ] + [ (r – r*) + (y – y*) ]

Taylor RulePrescribed

Real Policy Rate

NeutralRate

Setting

Taylor Rule Recommended Deviation from Neutral Rate

Setting

Augmented Taylor RulePrescribed

Real Policy Rate

Financial-Conditions-AdjustedNeutral Rate Setting

Taylor Rule Recommended Deviation from Neutral Rate

Setting

=

=

+

+

Policymakers need to consider the risk-taking behavior of

market participants in setting policy

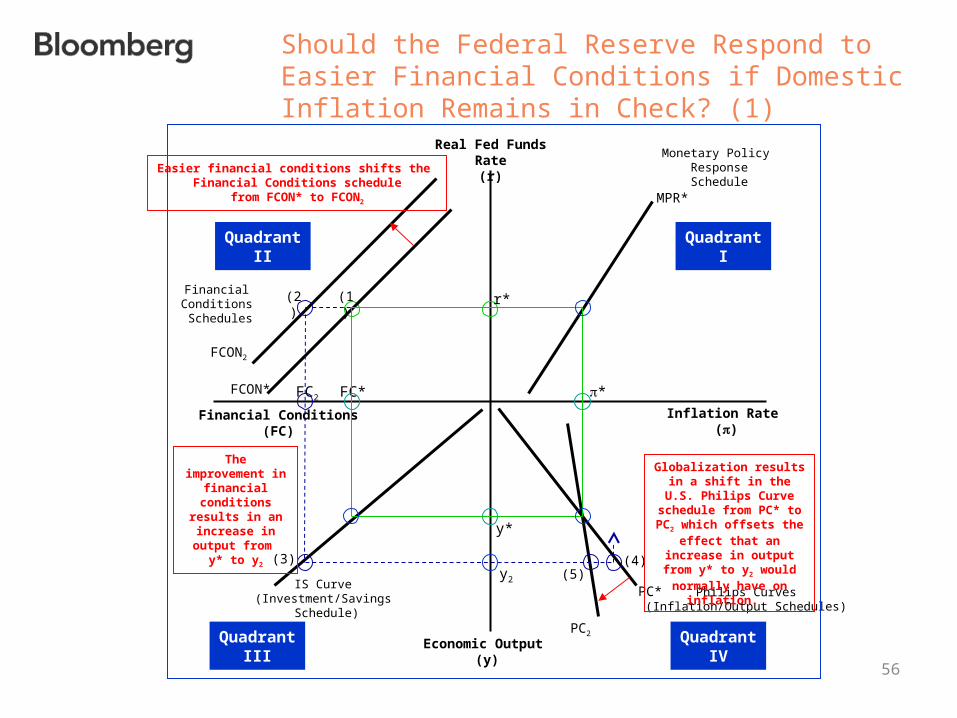

Should the Federal Reserve Respond to Easier Financial Conditions if Domestic Inflation Remains in Check? (1)

56

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedule

Philips Curves(Inflation/Output Schedules)

IS Curve (Investment/Savings

Schedule)

Financial Conditions Schedules

y*

FC* *

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

r*

Easier financial conditions shifts the Financial Conditions schedule

from FCON* to FCON2

FCON*

FCON2

MPR*

(1)

(3) (4)

FC2

PC*

PC2

(2)

(5)y2

Globalization results in a shift in the U.S. Philips

Curve schedule from PC* to PC2 which offsets the effect that an increase in

output from y* to y2 would normally have on

inflation.

The improvement in financial

conditions results in an increase in

output from y* to y2

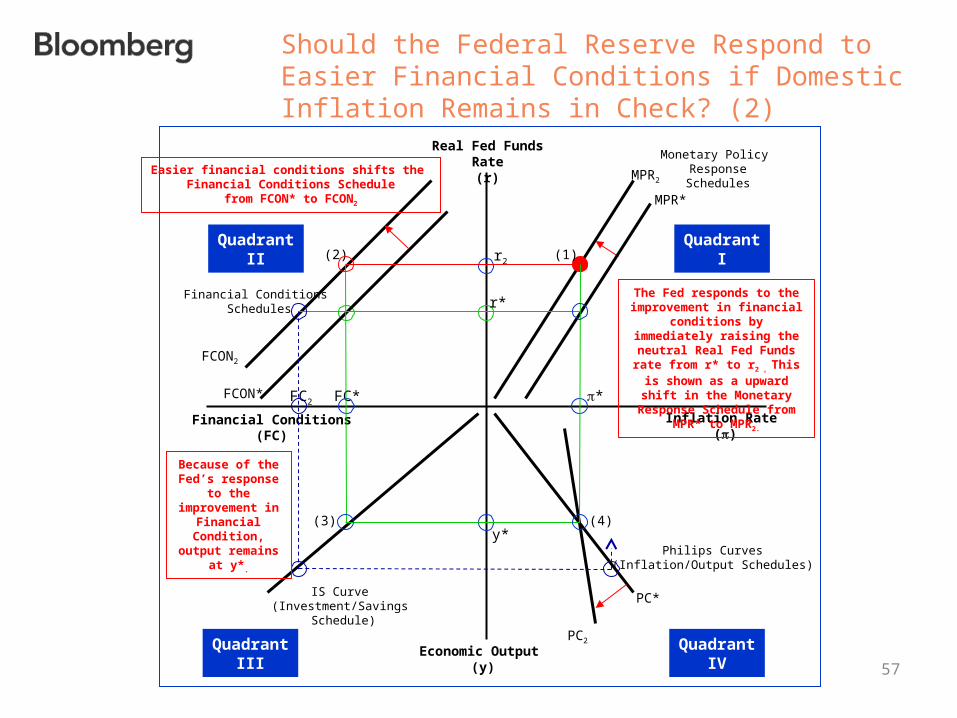

Should the Federal Reserve Respond to Easier Financial Conditions if Domestic Inflation Remains in Check? (2)

57

Real Fed Funds Rate(r)

Economic Output (y)

Financial Conditions(FC)

Inflation Rate ()

Monetary Policy ResponseSchedules

Philips Curves(Inflation/Output Schedules)

IS Curve (Investment/Savings

Schedule)

Financial Conditions Schedules

r2

y*

FC* *

QuadrantI

QuadrantIV

QuadrantII

QuadrantIII

r*

Easier financial conditions shifts the Financial Conditions Schedule

from FCON* to FCON2

FCON*

FCON2

The Fed responds to the improvement in financial

conditions by immediately raising the neutral Real Fed

Funds rate from r* to r2 , This is shown as a upward shift in the Monetary Response Schedule

from MPR* to MPR2.

MPR*

MPR2

(1)(2)

(3) (4)

FC2

PC*

PC2

Because of the Fed’s response to the improvement

in Financial Condition, output

remains at y*.

58

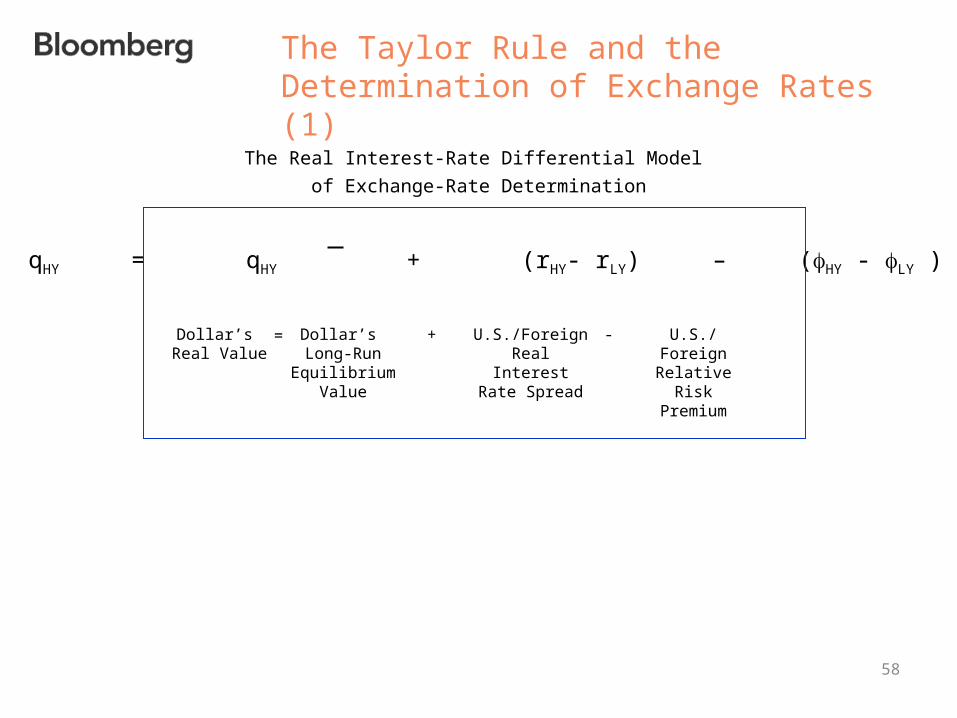

The Taylor Rule and the Determination of Exchange Rates (1)

Dollar’s Real Value

Dollar’s Long-Run Equilibrium

Value

qHY = qHY + (rHY- rLY) – (HY - LY )

U.S./Foreign Real Interest Rate Spread

= + U.S./Foreign Relative Risk

Premium

-

The Real Interest-Rate Differential Model

of Exchange-Rate Determination

59

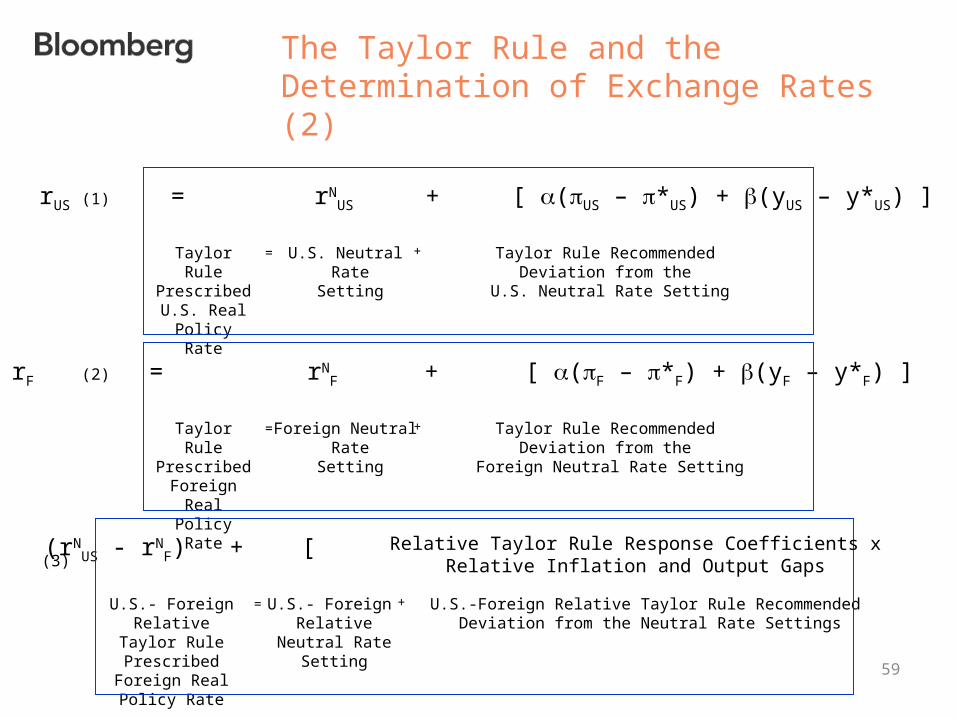

The Taylor Rule and the Determination of Exchange Rates (2)

Taylor Rule PrescribedU.S. Real

Policy Rate

U.S. Neutral Rate

Setting

rUS = rNUS + [ (US – *US) + (yUS – y*US) ]

Taylor Rule Recommended Deviation from the

U.S. Neutral Rate Setting

= +

Taylor Rule Prescribed

Foreign Real Policy Rate

Foreign Neutral Rate

Setting

rF = rNF + [ (F – *F) + (yF – y*F) ]

Taylor Rule Recommended Deviation from the

Foreign Neutral Rate Setting

= +

U.S.- Foreign Relative Taylor Rule Prescribed

Foreign Real Policy Rate

U.S.- Foreign Relative

Neutral RateSetting

rUS - rF = (rNUS - rN

F) + [ ]

U.S.-Foreign Relative Taylor Rule Recommended Deviation from the Neutral Rate Settings

= +

Relative Taylor Rule Response Coefficients xRelative Inflation and Output Gaps

(1)

(2)

(3)

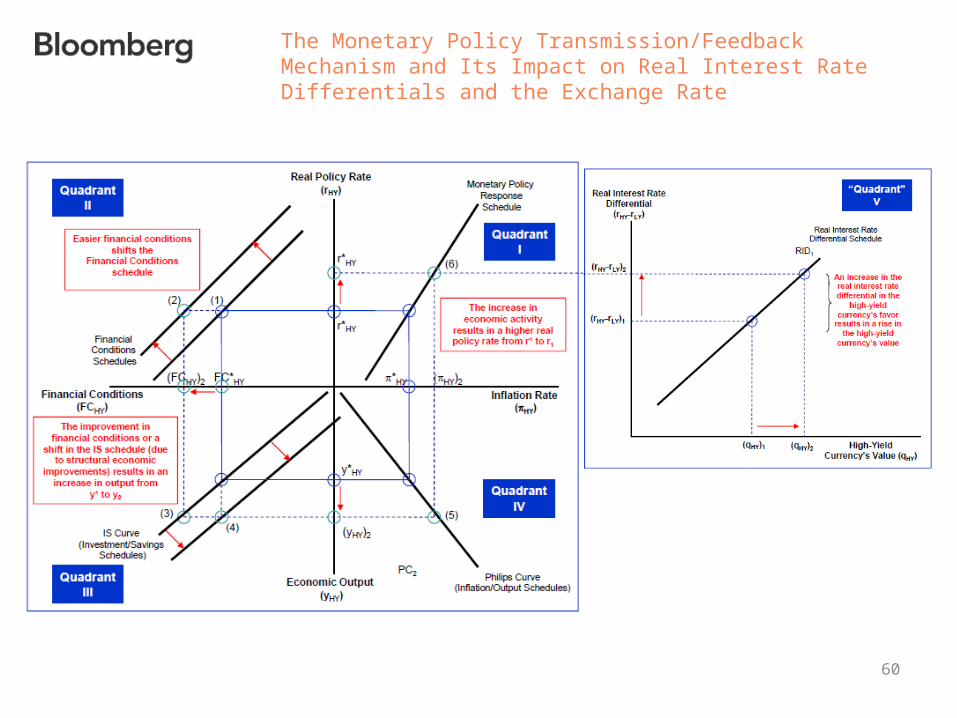

The Monetary Policy Transmission/Feedback Mechanism and Its Impact on Real Interest Rate Differentials and the Exchange Rate

60