Embed Size (px)

Citation preview

1Annual Report 2015 | Stock Code: IMO

IMIMOBILE PLCFinancial statements31 March 2015

Company Registration No. 08802718

www.imimobile.com 2

Contents

3

5

17

23

24

26

27

28

29

31

33

72

73

Officers and Professional Advisers

Strategic Report

Directors’ Report

Financial Statements

Statement of Directors’ Responsibilities

Independent auditor’s report

Consolidated Income Statement

Consolidated Statement of Comprehensive Income

Consolidated Statement of Changes in Equity

Consolidated Statement of Financial Position

Consolidated Cash Flow Statement

Notes to the consolidated Financial Statements

Company Balance Sheet

Notes to the Company Financial Statements

3Annual Report 2015 | Stock Code: IMO

Officers and Professional Advisers

DirectorsMr Viswanatha Alluri

Mr John Allwood

Mr Shyamprasad Bhat

Mr Simon Blagden

Mr Michael Jefferies

Mr Jayesh Patel

Registered OfficeTempus Court

Bellfield Road

High Wycombe

HP13 5HA

BankersBarclays Bank Plc

Barclays Corporate

180 Oxford Street

London

W1D 1EA

LawyersBracher Rawlins LLP

77 Kingsway

London

WC2B 6SR

AuditorDeloitte LLP

Chartered Accountants and Statutory Auditor

London, United Kingdom

www.imimobile.com 4

Key financial highlights of the Group

• Revenue up 13% to £48.9m (2014: £43.4m)

• Gross profit up 8% to £30.0m (2014: £27.9m)

• EBITDA¹ up 27% to £9.2m (2014: £7.2m)

• Adjusted profit after tax² up 48% to £5.6m (2014: £3.8m)

• Loss after tax on a statutory basis of £3.4m (2014: £3.9m profit) reflecting share based payments and costs in relation to IPO and

acquisition activities

• Good contribution from Europe with organic³ annual gross profit growth of 26%

• Managed solution growth in MEA of 16%

• Net cash generated from operating activities of £8.2m, representing operating cash conversion⁴ of 90% (2014: 121%)

• Free cash flow⁵ of £6.6m (2014: £6.9m)

• Cash and cash equivalents at 31 March 2015 of £14.6m (2014: £9.3m)

Operational highlights of the Group

• New major client wins in all regions

• Key new contracts signed in India with revenue benefit expected in FY16

• Renewal of several major contracts including the BBC, a multi-national North African telecoms operator and a major motoring

organisation

• Listed on AIM in June 2014 raising net proceeds of approximately £7m for the Company (after considering fees and the

acquisition of the Group) to support significant growth opportunities

• Acquisition and successful integration of TxtLocal Limited (“TextLocal”), trading well since acquisition in October 2014

¹ EBITDA is defined as operating loss / profit before depreciation, amortisation, fees incurred in relation to IPO and acquisition activities, impairment charges, share based compensation and excluding

the impact of the disposal of subsidiaries. See note 10 for a reconciliation.

²Adjusted profit after tax is defined by the Group as loss/profit after tax before fees incurred in relation to IPO and acquisition activities, impairment charges, share based compensation, de-recognition

of deferred tax assets and excluding the impact of the disposal of subsidiaries. See note 10 for a reconciliation.

³Excluding the impact of the TextLocal acquisition.

⁴Calculated as net cash from operating activities as a proportion of EBITDA.

⁵ Free cash flow defined as net cash from operating activities less purchases of intangibles, property, plant & equipment.

Group Highlights

5Annual Report 2015 | Stock Code: IMO

StrategicReport

www.imimobile.com 6

We operate in competitive and fast moving markets and I would

like to thank the wider IMImobile team whose commitment and

drive have made our successes possible. We continue to invest in,

incentivise and reward our stable and growing team. This enables

us to attract and retain the best talent who can drive technological

innovation and sales growth and help us to deliver on our other

strategic objectives.

Our strategy from foundation has been to create intellectual

property that can be deployed in global markets through a

business model of recurring revenues. We believe that our

DaVinci platform, our core product offering and professional

services position us well to take advantage of the structural trends

surrounding mobility, social networking and cloud computing.

Following another year of strong growth for the Group I am

delighted to introduce this year’s annual report and financial

statements. The year to 31 March 2015 was one which saw the

Company list on AIM, make and successfully integrate a significant

acquisition and continue to grow and generate cash. Our product

and solution offering has never been stronger and we are helping

more clients than ever with engaging their customers on mobile

devices.

Since founding the Group we have been focused on the

opportunities created by the expansion of mobile operator

networks and their capacity to carry data services. The continued

evolution and growth of these networks and smartphones provides

the foundations for new business opportunities. Since we started

the business we have remained entrepreneurial in our approach

to product and market development and we shall remain so in

what has become a complex and competitive eco-system.

We maintain our focus on profitable and cash generative growth

and continue to expand the international footprint of our business

to fully leverage the intellectual property created by the Group. I

am very happy to have further consolidated our position in Europe,

welcoming TextLocal to the IMImobile family this year. TextLocal’s

market leading platform for small and medium sized businesses

complements the existing IMImobile offering and presents another

exciting opportunity to leverage our international footprint.

In the year to 31 March 2015 revenues grew by 13% to £48.9m

(2014: £43.4m) with significant growth coming from Europe and

managed solutions contracts across the Middle East and African

region. Although the growth has been tempered by continuing

declines from our Indian and South East Asia region, the year

ended positively with contract wins and new deployments which

will contribute to the region in the coming year. On a statutory

basis the Group made a loss after tax of £3.4m in the year to 31

March 2015 (2014: £3.9m profit), after charging £7.3m of share

based payment expense and £1.6m of non-recurring IPO and

acquisition related costs. On an adjusted basis the profit after tax

of the Group was £5.6m¹ (2014: £3.8m).

Viswanatha Alluri

Founder and Executive Chairman

¹ See note 10 for a reconciliation of statutory loss / profit after tax to adjusted profit after tax.

Chairman’s Statement

7Annual Report 2015 | Stock Code: IMO

Chief Executive’s Report

The year to 31 March 2015 has been another good year of profitable

growth for the Group on an adjusted basis¹ across all of the key

financial metrics. We continue to strengthen our balance sheet,

with strong cash conversion from operations and have made

investments in the sales and marketing areas of our business,

particularly in Europe and the Americas. We have enjoyed very

strong growth in Europe during the year to 31 March 2015 and

have also grown our recurring revenue base in the Middle East

and Africa. Conditions remained challenging in India throughout

the year; however, the year ended strongly in this region with

several key new contract wins which will deliver revenues during

the new financial year.

Market overview

We are living in a period of great change driven by technology, the

ubiquity of mobile networks, increasing processing power of mobile

devices and the falling costs of cloud computing are disrupting

many industries and providing tremendous opportunities for value

creation. The impact of these changes to consumer behaviour

is compelling all consumer-facing businesses to fundamentally

assess how they engage with their customers. At the core of

IMImobile we are a technology company providing a combination

of software and services to enable our clients to fully embrace

the changes taking place whether they create additional revenue

opportunities or help reduce operating costs.

Our strategy has been to ensure that our platforms and services

are network, channel and device agnostic. The guiding principle

being to ensure our clients have a partner that is able to deliver the

right experience for their customers across a customer base that

maybe highly fragmented in its use and adoption of technologies.

Though we operate in a highly competitive, complex and

fast-changing environment we continue to be excited about

technological change. Over the last year we have seen the

successful launch of 4G networks in the UK and expect 4G to be

launched in India later this year, growth of 22% in global smartphone

ownership to over 2 billion devices² and the phenomenal rise

of IP messaging. We believe that better networks, more devices

and more complexity provide great opportunities to leverage

our existing software and are confident that we have the product

roadmaps and resources in place for a promising future.

Products and Platforms

DaVinci ESP

Since foundation we have created and owned all our intellectual

property and at the core is the DaVinci Evolved Service Platform

which has been developed with hundreds of person-years of

engineering effort. It provides a unified, fully integrated and

standards-based environment to create, deliver and manage a

wide range of cross-channel enterprise and consumer services.

The platform utilises a broad spectrum of enablers including

mobile operator connectivity (for messaging, charging, identity

and location), device repositories, over-the-top (OTT) messaging,

payment mechanisms and integrations with OEM environments

and social media platforms.

The platform comprises several distinct yet fully interoperable

modules which are designed to function in a standalone mode or

as part of a fully integrated suite. Each module delivers enterprise-

grade performance, availability and scalability and exposes open

industry-standards based APIs.

The platform includes a flexible metadata driven service creation

layer, which provides an environment for configuring new services.

The ‘configure, not code’ approach means new services can be

launched cost-effectively, reliably and quickly and customisations

can be delivered rapidly.

Our Software Applications

DaVinci CMS

The DaVinci Content Management System has been architected

and developed to support the delivery of a wide array of content

types to the universe of connected devices - from basic feature

phones and PCs to smartphones, tablets and in-car infotainment

systems. The product acts as a digital exchange managing multiple

content owners, content aggregators, developers and service

providers through a single unified environment. Key features

include end-to-end content lifecycle management, partner

management and an in-built portal engine allows user interfaces

to be configured and rendered across thousands of device types.

¹ See note 10 for a reconciliation of statutory loss / profit after tax to adjusted profit after tax.

² Source: http://www.prnewswire.com/news-releases/strategy-analytics-global-smartphone-users-reach-2-billion-in-2014-300041752.html

www.imimobile.com 8

Chief Executive’s Report (continued)

DaVinci CMS has been widely deployed around the world and

currently powers content storefronts for a range of mobile

operators, digital distribution for major music labels and

m-Governance citizen services for Government bodies.

Campaign Manager

Campaign Manager enables omni-channel marketing campaigns.

Supported channels include SMS, MMS, Email, USSD, In-app push

notifications and Voice. The product supports different types of

campaigns such as promotional, event-triggered, interactive,

progressive and multi-wave campaigns. Integration with DaVinci

Profile Manager enables fine-grained target group definition and

the application of analytical models such as propensity modelling

and clustering. Configurable A/B testing and control groups allow

campaigns to be optimized for maximizing campaign effectiveness.

Campaign Manager today is used for cross-sell, up-sell,

information, engagement and customer delight campaigns for

mobile operators, retailers, financial institutions and gaming

companies delivering over a billion customer interactions annually.

OpenHouse

OpenHouse exposes service enablers (messaging, voice, location,

presence etc.), federated within the underlying DaVinci platform,

as a set of APIs which are augmented with tools such as a workflow

designer, call flow builder and a high-performance rules engine

to enable rapid service creation. The multi-tenanted architecture

allows the software to be delivered as a service. OpenHouse

allows customer identities to be linked to individual channel

identities enabling the messaging APIs to be used in a channel-

agnostic way. It provides intelligent message routing based

on customer preferences, channel cost, presence, priority and

other factors. OpenHouse also provides software development

kits or SDKs which not only enable in-app messaging and push

notifications but also facilitate data collection from devices to

provide customer context to enrich communications and trigger

operational workflows.

Transaction alerts, fraud prevention, account notifications, two-

factor authentication and service messages are some examples

of applications built on top of OpenHouse and currently live for

leading enterprises in multiple markets.

TextLocal

TextLocal is a SaaS business messaging tool and has been widely

adopted by SMEs and large brands alike. The product today

delivers nearly 250 million customer interactions annually in the

UK. In addition to basic SMS messaging, TextLocal supports file

attachments, surveys, landing pages, data capture forms, ticketing,

coupons, vouchers, loyalty cards and other value-added features.

It provides sophisticated data import, target group definition,

9Annual Report 2015 | Stock Code: IMO

audit logs and role-based access control which make the product

ideally suited for enterprise usage whilst providing an extremely

intuitive and easy-to-use interface for simpler use cases.

DaVinci Social

DaVinci Social aggregates high volumes of inbound customer

audience messages from multiple channels such as Facebook,

Twitter and SMS. It allows configuration of rules and workflows to

process the inbound messages and includes a curation console

which can be used to identify messages which require further

manual processing such as referring the message to a customer

care agent or a presenter (in a broadcasting scenario).

DaVinci Social has been deployed for leading broadcasters

such as the BBC and other major media houses powering their

audience engagement programmes.

Direct Carrier Billing (DCB)

DCB allows consumers to pay for digital content, in-app purchases,

contests, donations and other such services through their mobile

phone bill. The product includes a merchant portal where

merchants may register themselves, request for specific price

points, get access to a common charging API and view transaction

reports. One single API provides access to multiple mobile

operators thereby insulating merchants from the complexities of

integrating with each mobile operator separately.

Each of the products above has a continual roadmap of

development, which has been developed in discussions with

clients, and analysis of technology and market trends. Over the

next year we expect to continue developing technologies that help

clients use video, IP messaging and the plethora of new devices.

Regional performance

The Group is managed commercially and strategically on a regional

basis with centralised resources for software development, finance

and general management in the UK. A key operating metric for

each region is gross profit as there are considerable differences in

gross margins across regions, product lines and revenue models.

Gross profit also measures most directly the value of the software

and solutions delivered by the Group which excludes the impact

of network infrastructure, third party hardware and content costs.

Europe and the Americas

Europe gross profit £15.7m (2014: £11.0m)

Europe makes up over 52% of Group gross profit. Including the

contribution made by TextLocal, gross profit in Europe grew by

over 43%. Organic¹ annual gross profit growth in the same period

was strong at just over 26%. Gross margins also increased in the

region thanks to favourable mix of delivery models and the falling

costs of third party network infrastructure, a trend we expect will

continue.

The growth in the region comes from a combination of new client

wins across mobile operator, retail and gambling and gaming

sectors and upsell and cross sell to existing customers. No major

clients were lost during the period and we have maintained

investment in our sales and marketing teams during the year to

position ourselves well for future growth. We are very pleased with

the acquisition and integration of TextLocal, it has met expectations

on financial targets and synergies and we shall be leveraging our

global footprint and resources to launch the product in our existing

and new geographies.

All our products and platforms are live in this region and we

continue to be well positioned to exploit the macro trends around

increasing mobile usage and digitisation of business operations.

Our largest clients are mobile operators and with consolidation

taking place in that sector it has provided us with opportunities

to position ourselves as a trusted reliable vendor with deep

Chief Executive’s Report (continued)

¹ Excluding the impact of the TextLocal acquisition.

www.imimobile.com 10

India and SE Asia

Gross profit £5.0m (2014: £5.9m)

The performance in India has been disappointing with a gross

profit decline of 15% compared with the year to 31 March 2014.

In local currency the reduction was 13%. The continued decline

is a direct consequence of the implementation of new consumer

protection regulation that has impacted our customers, chiefly the

mobile network operators. In India our main activity is managing

certain content and value added telecom services for mobile

operators and tighter regulation requiring operators to seek

additional consents to sign customers up to these services led to

a period of transition as new third party consent gateways have

been implemented.

As a Group we have welcomed the changes as overly aggressive

marketing and over-charging had damaged consumer perception

of mobile services and we believe that in the long term the

changes will benefit the overall market and are confident of our

return to growth for mobile services in this region.

During the period we have successfully won multiple managed

solution contracts with additional operators in India, Myanmar

and Nepal which are currently under deployment and which we

expect to contribute to revenue in the coming year. We also

expect additional revenue growth to come from our efforts in

broadening our offering in the region. Over the last year we have

invested in sales and marketing into new sectors and are pleased

with progress having signed new customers in the public sector

and with leading consumer brands. We will continue to invest

in targeting new sectors and expect to launch additional SaaS

products over the coming year.

Outlook

The 2016 financial year has started well, building on the successes

of 2015. Trading is in line with Directors’ expectations.

The contracts won last year will help to enhance revenues and

profitability in 2016 and beyond. Deployments and new product

developments are progressing as planned and the high mix of

repeat and recurring revenues gives us confidence and good

visibility. We continue to invest in sales and marketing activities

which we anticipate will underpin our organic growth forecasts for

the coming years.

We also continue to innovate and are excited about the changes

in our marketplace and we expect to use our financial and cash

integrations. We see significant opportunities in the financial

services sector as digitisation and mobilisation of existing

processes becomes a necessity. We also see opportunities with

large consumer brands that look to engage with their customers

via digital marketing programmes and I am pleased that we have

won several industry accolades, including “Best Relationship

Building / CRM” for a programme run with O2 in the UK and “Best

Mobile CRM/Enterprise Messaging Campaign” for the work we

have done with Ikea.

We continue to invest in establishing our operations in the

US market and are pleased with progress to date. We have

started working with leading operators and developed a good

experienced team on the ground.

Middle East and Africa

Gross profit £8.6m (2014: £10.7m)

Our business in the MEA region performed well in the year, with

gross profit growth of 16% in recurring managed solutions contracts.

The business in MEA is largely based on group relationships with

the leading mobile operators in the region and our growth is based

on new territory and service deployments for existing customers.

In the year to 31 March 2015 we saw new services going live in

Senegal, Ghana, Nigeria, Guinea Conakry and Niger.

There was an expected decline in year-on-year gross profit from

licence revenues following an exceptional year to 31 March 2014.

Gross profit from licence revenue of £2.9m in the year to 31 March

2015 represents a decline of roughly 50% compared to the prior

period, and includes revenue from deployments for a global

Systems Integrator and multiple mobile operators across Africa.

These multi-million US Dollar licence deals are typically for an

installation of the entire DaVinci ESP or multiple modules in the

platform and demonstrate the value inherent in the intellectual

property.

Though deployments can be lengthy and local network

infrastructure and connectivity unstable, the Group has

demonstrated an ability to deliver revenue generating services

successfully in challenging circumstances and as a result is well

placed to benefit from the predicted growth of mobile usage

across MEA. Currently the DaVinci ESP and CMS are the main

offerings in the region sold to mobile operators however over the

coming year we expect to establish our broader product set in the

region catering not only to telecom operators but enterprise and

government as well.

Chief Executive’s Report (continued)

11Annual Report 2015 | Stock Code: IMO

strength to further our ambitions to consolidate a fragmented

market and accelerate our reach into enterprise customers.

I believe IMImobile remains well positioned to exploit the macro

trends around increasing mobile usage and digitisation of business

operations and we remain confident about our prospects for the

future.

Jay Patel

CEO

Chief Executive’s Report (continued)

www.imimobile.com 12

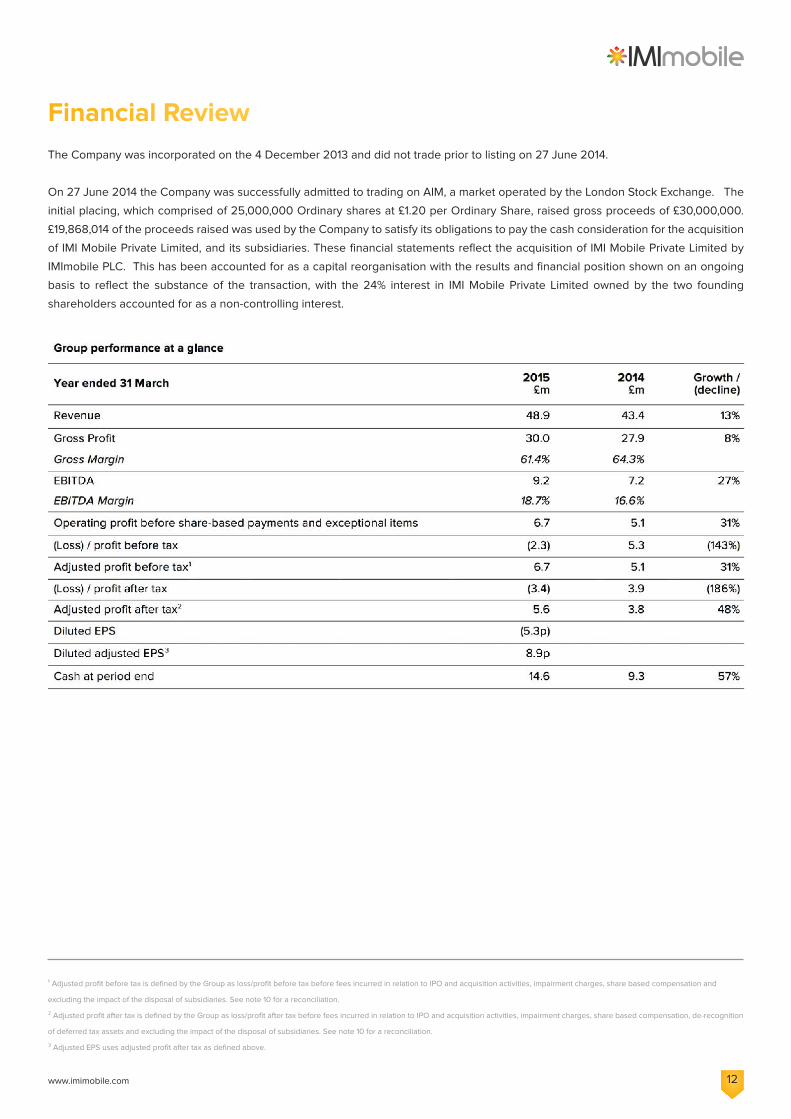

Financial Review

The Company was incorporated on the 4 December 2013 and did not trade prior to listing on 27 June 2014.

On 27 June 2014 the Company was successfully admitted to trading on AIM, a market operated by the London Stock Exchange. The

initial placing, which comprised of 25,000,000 Ordinary shares at £1.20 per Ordinary Share, raised gross proceeds of £30,000,000.

£19,868,014 of the proceeds raised was used by the Company to satisfy its obligations to pay the cash consideration for the acquisition

of IMI Mobile Private Limited, and its subsidiaries. These financial statements reflect the acquisition of IMI Mobile Private Limited by

IMImobile PLC. This has been accounted for as a capital reorganisation with the results and financial position shown on an ongoing

basis to reflect the substance of the transaction, with the 24% interest in IMI Mobile Private Limited owned by the two founding

shareholders accounted for as a non-controlling interest.

¹ Adjusted profit before tax is defined by the Group as loss/profit before tax before fees incurred in relation to IPO and acquisition activities, impairment charges, share based compensation and

excluding the impact of the disposal of subsidiaries. See note 10 for a reconciliation.

² Adjusted profit after tax is defined by the Group as loss/profit after tax before fees incurred in relation to IPO and acquisition activities, impairment charges, share based compensation, de-recognition

of deferred tax assets and excluding the impact of the disposal of subsidiaries. See note 10 for a reconciliation.

³ Adjusted EPS uses adjusted profit after tax as defined above.

13Annual Report 2015 | Stock Code: IMO

Financial Review (continued)

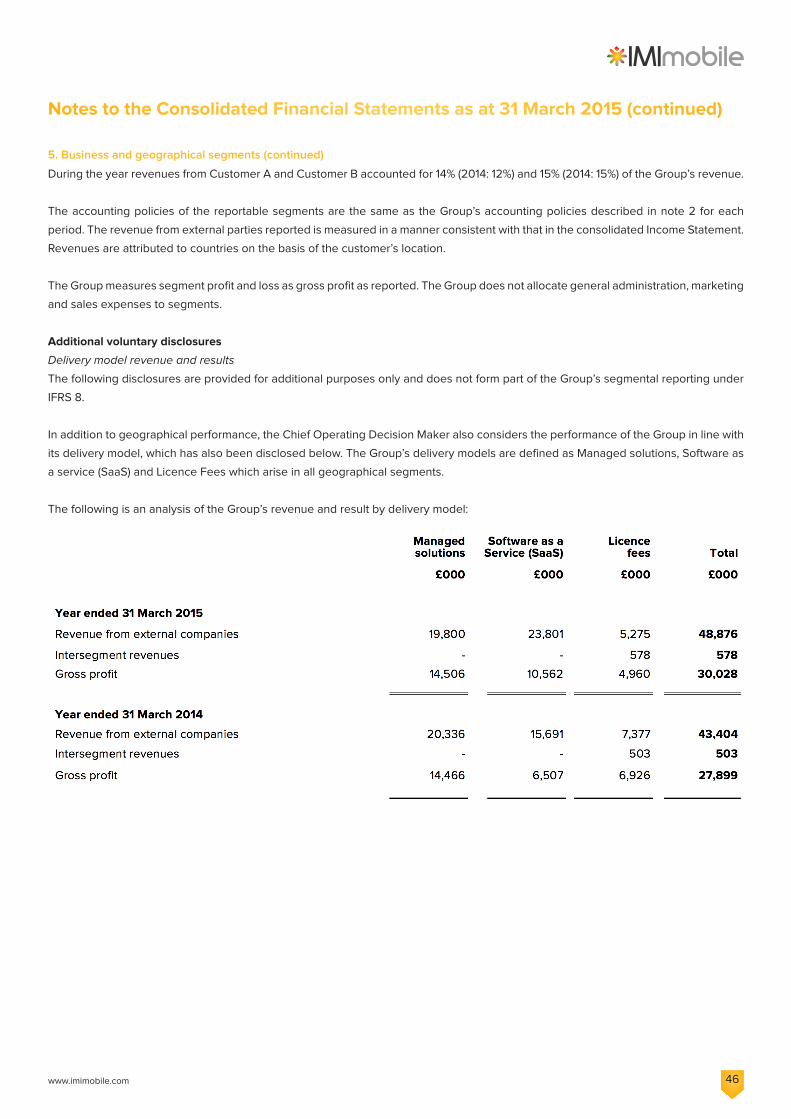

The Europe region gross profit grew by 43% in the year after removing the impact of the non-core Greek subsidiary from the prior

year results which was sold in May 2013. The post-acquisition result of TextLocal represents 17% of the increase in gross profit for the

region. Gross margin in Europe in the year was 57.8% up from 51.8% in 2014 in part as a consequence of the declining cost of third

party network infrastructure.

Gross profit from managed solution contracts increased by 16% in the year, however, licence fee income recognised in the prior year in

the Middle East & Africa (MEA) region were not repeated to the same extent this year, resulting in regional gross profit decreasing by

19% to £8.6m (2014: £10.7m). Gross margin in MEA reduced to 76.2% from 80.6%, again reflecting the decreased proportion of licence

fees recognised during the period.

Key performance indicators (KPIs)

This section sets out the KPIs for the Group during the year ended 31 March 2015.

Group revenue and gross profit

For the year to 31 March 2015 total revenue increased by 13% to £48.9m (2014: £43.4m) and gross profit increased by 8% to £30.0m

(2014: £27.9m). The Board considers that gross profit is the key operational measure of performance in the business.

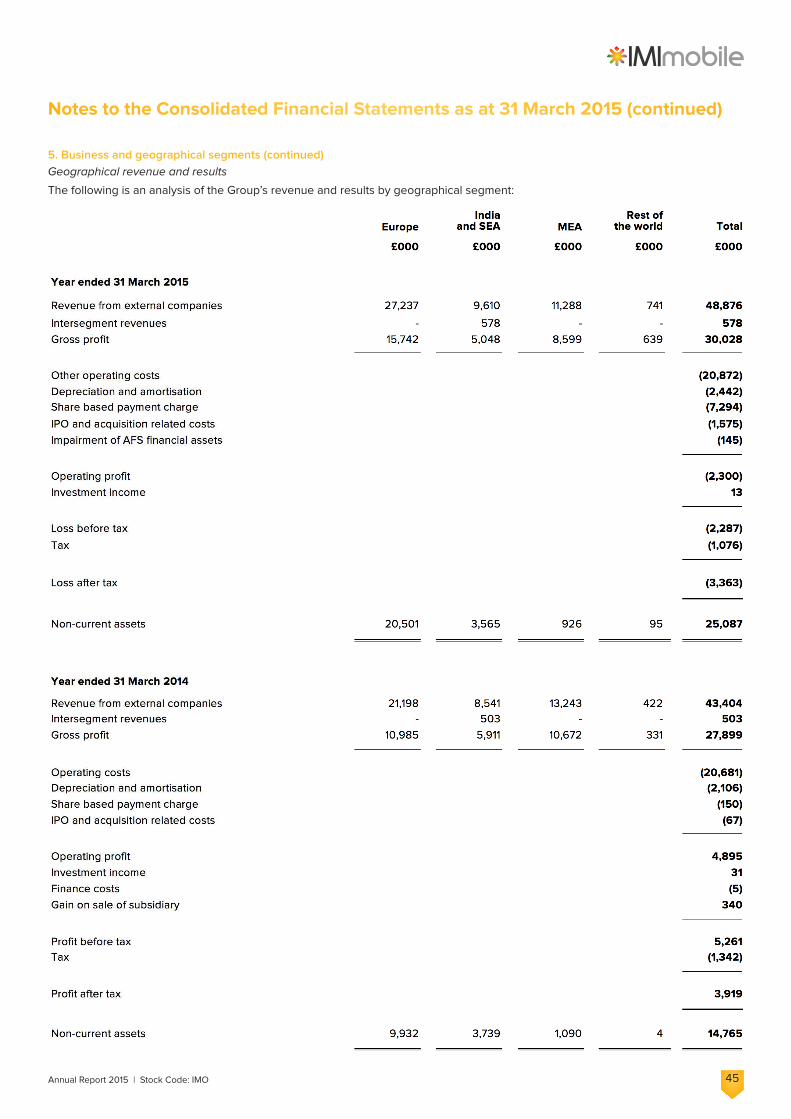

Group geographical split of revenues and gross profit is as follows:

¹ Non-core Greek subsidiary disposed of in May 2013.

www.imimobile.com 14

Operating costs before amortisation, depreciation, impairment costs, share-based payments and exceptional items

Operating costs before amortisation, depreciation, impairment costs, share-based payments and exceptional items in the year were

£20.9m (2014: £20.7m).

EBITDA¹ and operating profit before share-based payments and exceptional items

EBITDA for the year to 31 March 2015 was £9.2m (2014: £7.2m) and operating profit before share-based payments and exceptional

items was £6.7m (2014: £5.1m) representing an increase of 31% against the prior year.

Group cash flow and working capital

Year end cash and cash equivalents were £14.6m (2014: £9.3m). There were no bank borrowings at 31 March 2015 (2014: £nil). Cash

generated from operations was £8.2m (2014: £8.7m) and represents an operating cash flow conversion of 90% of EBITDA (2014: 121%).

The Company listed on AIM on 27 June 2014 raising £6.5m cash for the Company after deducting one-off IPO related expenditure. On

the 13 October 2014 the Group acquired the entire share capital of TextLocal comprising an initial cash consideration of £10.0m, the

value of cash included in the acquired net assets of TextLocal was £2.0m.

Group working capital is made up as follows:

Trade receivables and payables include “pass through” amounts generated from mobile payment transactions. The receivables are

from mobile operators and payables to customers who use IMImobile’s payment APIs. These amounts are excluded from revenues

and cost of sales, as the Group accounts only for the commission earned on such transactions within revenue as it is not the principal

obligor in the arrangement. The value of pass through revenues included in trade and other receivables at 31 March 2015 is £3.2m

(2014: £4.8m) and the value of pass through revenues included in trade and other payables at 31 March 2015 is £5.2m (2014: £6.0m).

Financial Review (continued)

Group loss / profit after tax

Loss after tax was £3.4m (2014: profit of £3.9m) after the impact of IPO and other exceptional costs of £1.6m (2014: £0.1m), share based

payment charges net of deferred tax of £6.7m (2014: £0.1m), impairment of available-for-sale financial assets of £0.1m (2014: £nil),

de-recognition of deferred tax assets of £0.5m (2014: £nil) and a one-off gain from the disposal of a subsidiary of £nil (2014: £0.3m).

Adjusted profit after tax was £5.6m (2014: £3.8m) representing an increase of 48% against the prior year.

¹ EBITDA is defined as operating loss / profit before depreciation, amortisation, fees incurred in relation to IPO and acquisition activities, impairment charges, share based compensation and excluding

the impact of the disposal of subsidiaries. See note 10 for the reconciling items.

In GBP the Indian and SEA region gross profit declined in the year by 15% to £5.0m (2014: £5.9m). A proportion of the year on year

decline was attributable to the weakening of the Indian Rupee against the Pound, and in local currency gross profit fell by 13%. The

major reason for decline in gross profit in local currency was the implementation of regulations in the Indian market imposed by the

Telecom Regulatory Authority of India (“TRAI Regulations”) which affected the managed solutions provided to the mobile operators in

India. The TRAI Regulations include limitations on the volume of promotions that can be sent to consumers and the requirement for

additional third-party consent to be obtained prior to the billing of any consumers for services consumed via the mobile device.

15Annual Report 2015 | Stock Code: IMO

Financial Review (continued)

Earnings per share

Diluted loss per share was 5.3p. Diluted adjusted EPS was 8.9p.

Other financial information

Group taxation

The tax charge for the year was £1.1m (2014: £1.3m). The effective

rate of tax¹ for the year was 16.7% (2014: 26.1%).

Group Capital expenditure

Capital expenditure during the year was £1.5m (2014: £1.9m) split

between plant, property and equipment of £1.0m (2014: £1.7m) and

third party software £0.5m (2014: £0.2m).

Goodwill

Goodwill held at 31 March 2015 was £17.9m (2014: £7.9m) following

the acquisition of TextLocal. There were no other changes to the

carrying amount of goodwill in the year.

Redeemable Preference Shares

There were no redeemable preference shares in issue at 31 March

2015 (2014: £10.9m). The optionally convertible preference shares

that were in issue on 31 March 2014 were converted to equity on

20 June 2014, prior to the listing of the Company.

Principal risks and uncertainties of the Group

Exchange rate fluctuations

A significant proportion of the Group’s revenue is generated

overseas and is denominated in Indian Rupees, US Dollars, South

African Rand and Nigerian Naira. Therefore the Group is exposed

to foreign currency risk due to fluctuations in exchange rates.

This may result in gains or losses with respect to movements

in exchange rates which may be material and may also cause

fluctuations in reported financial information that are not

necessarily related to the Group’s operating results. The Group

naturally mitigates this risk by offsetting its cost base in the same

currencies where possible and by closely monitoring exchange

rate fluctuations.

Customer Relationships

A proportion of the Group’s business is derived from supplying

ongoing services to customers based on formal contracts. Despite

historically low levels of customer attrition and the longevity of

many of the Group’s relationships with its core customers, it is

possible that customer attrition rates may increase in the future

due to increased competition or changes in market demand. The

Group has procedures in place to minimise the risk of events of

this nature occurring such as diversifying its customer’s base, and

maintaining strong relationships with its customers.

Dependence on key personnel

The Group’s future success is substantially dependent on the

continued services and performance of its senior management

including the Group’s Directors, each of whom has significant

relevant experience. The Group provides meaningful long term

incentives to the executive team and key employees as well as

offering competitive remuneration packages.

Regulatory compliance

Certain of the Group’s UK activities are regulated by PhonepayPlus

an agency of OFCOM which has responsibility for the regulation

of mobile payments in the UK. The Group is required to comply

with the PhonepayPlus code of practice when it provides premium

rate services in the UK. PhonepayPlus has the ability to impose

fines, suspend services or impose certain other sanctions where

its code of practice is breached. Such fines, suspensions or

other sanctions can be imposed when the Group has failed to

adequately deal with due diligence and/or risk management of the

customer which has breached the code of practice. The Group

follows detailed procedures for the sign up of new services as well

as regular monitoring and risk assessment of ongoing services. In

addition to this key personnel from the Group meet regularly with

the regulator in order to review market trends and collaborate on

certain matters.

Technological Change

The Group operates in markets that are subject to constant

technological development, evolving industry standards and

changes in customer needs. Therefore the Group is subject to the

effects of actions by competitors in these markets and relies on its

ability to anticipate and adapt to constant technological changes

taking place in the industry. To maintain its strong position in the

market, the Group needs to successfully market its products and

services and respond to both commercial actions by competitors

and other competitive factors affecting these markets, anticipating

and adapting promptly to technological changes, changes in

consumer preferences and general economic, political and social

conditions.

¹ Tax as a proportion of adjusted profit before tax, as reconciled in note 10.

www.imimobile.com 16

The Group spends approximately 4-5% of revenues on research

and development as well as employing product and solution

specialists who monitor market developments and keep the

product offering relevant for the markets in which the Group

operates.

Significant failure or interruption to network or IT systems

The Group’s business depends on providing customers with

highly reliable platforms and services. Unanticipated network, or

other, interruptions (whether accidental or otherwise) may occur

as a result of system failures, including hardware or software

failures, which affect the quality, or cause an interruption in the

Group’s supply of services. Such failures can result from a variety

of factors within the Group’s control, including human error,

equipment failure, power loss, failure of services related to the

internet and telecommunication networks, physical or electronic

security breaches, as well as factors outside of the Group’s control,

such as sabotage, vandalism, system failures of network service

providers, fire, earthquake, adverse weather and other natural

disasters, water damage, fibre optic cable cuts, power loss not

caused by the Group and terrorism. The Group’s infrastructure is

hosted mainly using third party data centres, with major platforms

and systems also benefiting from geographical redundancy. Third

party hardware and software support contracts are in place.

Connectivity to multiple networks also provides mitigation against

elements of this risk.

The Strategic Report was approved by the Board and signed on

its behalf by

Financial Review (continued)

Mike Jefferies

Group Finance Director

22 June 2015

17Annual Report 2015 | Stock Code: IMO

Directors’ Report

www.imimobile.com 18

The Directors present their annual report and audited financial statements on the affairs of IMImobile PLC for the year ended 31 March

2015.

Results and dividends

The results for the year are set out in the consolidated Income Statement on page 29. The Directors are not recommending a dividend

for the year.

Directors

The following Directors served on the Board of the Company during the year:

Executive Directors

• Mr Viswanatha Alluri

• Mr Shyamprasad Bhat

• Mr Michael Jefferies

• Mr Jayesh Patel

Non-executive Directors

• Mr John Allwood

• Mr Simon Blagden

The Directors and their families have the following beneficial interests in the ordinary share capital of the Company:

There were no changes in Directors’ interests between 1 April 2015 and the date of these financial statements.

Details of related party transactions involving Directors of the Company are given in note 18 to the financial statements.

¹ The Company’s issued share capital consists of 48,038,864 ordinary shares with a nominal value of 10p each (“Ordinary Shares”), each share having equal voting rights. The Company does not hold any Ordinary Shares in treasury and

therefore the number of Ordinary Shares with voting rights is 48,038,864. In addition, there are 11,299,599 Ordinary Shares which are issuable to Viswanatha Alluri and Shyamprasad Bhat upon the exercise of rights. Viswanatha Alluri and

Shyamprasad Bhat did not hold any shares in IMImobile PLC on admission however they have an option to convert their shares in IMI Mobile Private Limited into shares in IMImobile PLC. Viswanatha Alluri has an option over shares which

represent 16.2% of the voting rights of the Company. Shyamprasad Bhat has an option over shares which represent 2.8% of the voting rights of the Company. Until such time as the option is exercised the voting rights can be exercised

pursuant to each of the B Shares held by the nominee for Viswanatha Alluri and Shyamprasad Bhat. Therefore, when calculating voting rights, shareholders should use the figure of 59,338,463 as the denominator.

² Comparative figures represent the Directors’ voting rights in the Group prior to Admission only. The number of shares and percentage of share capital in IMI Mobile Private Limited, the ultimate parent company of the Group in the prior year,

are not disclosed as they are not considered comparable to those of the Company in the current year following admission and capital restructuring.

Directors’ Report

19Annual Report 2015 | Stock Code: IMO

Directors’ emoluments

The remuneration of the Directors of the Company was as follows:

¹See note 18 for details of the director loan write off.

Directors’ Report (continued)

Interests in share options

Set out below are details of options granted to the Directors which are ultimately over shares in IMImobile PLC:

No options have been exercised or lapsed during the year.

All options vest over a period of 0-4 years and are dependent upon continuing employment and meeting performance targets for the

Group’s EPS. All options expire 10 years from the grant date.

www.imimobile.com 20

Directors’ Report (continued)

Pension contributions

The number of Directors who:

Highest paid Director

Companies Act 2006 requires certain disclosures about the remuneration of the highest paid Director taking into account emoluments,

gains on exercise of share options and amounts receivable under long-term incentive schemes. On this basis, the highest paid Director

in the year was Mr Jayesh Patel and details of his remuneration are disclosed above.

Strategic Report

The Strategic Report covers pages 8-18. The Company has chosen to set out certain matters in this Strategic Report that would otherwise

be required to be disclosed in the Directors’ Report. These matters include disclosures concerning likely future developments in the

business (pages 12-13).

Financial risk management objectives and policies

Disclosures relating to financial risk management objectives and policies, including our policy for hedging are set out in note 28 to the

consolidated financial statements and disclosures relating to exposure to price risk and credit risk are outlined in note 28.

Contributions paid by the company in respect of such Directors were as follows:

21Annual Report 2015 | Stock Code: IMO

Directors’ Report (continued)

Supplier payment policy

The Company has no trade creditors because it is a parent

company and does not generate trading revenues. Accordingly, no

disclosure can be made of year-end trade creditor days. However,

the Group’s policy is to settle the terms of payment with suppliers

when agreeing the terms of each transaction and to ensure that

suppliers are made aware of the terms of payment and to abide by

the terms of payment. The average trade creditors for the Group,

expressed as a number of days, were 57 (2014: 63).

Related part transactions

Disclosures relating to related party transactions are set out in

note 18 to the consolidated financial statements.

Charitable and political donations

No charitable or political donations were made by the Company.

Charitable donations made by the Group in the year were £40,000

(2014: £65,000). Political donations were £nil in both years.

Employees

The number of employees and their remuneration is set out in

note 6.

Applications for employment by disabled persons are always

fully considered, bearing in mind the aptitudes of the applicant

concerned. In the event of members of staff becoming disabled

every effort is made to ensure that their employment with the

Group continues and that appropriate training is arranged. It

is the policy of the Group that the training, career development

and promotion of disabled persons should, as far as possible, be

identical to that of other employees.

The Group places considerable value on the involvement of its

employees and has continued to keep them informed on matters

affecting them as employees and on the various factors affecting

the performance of the Group. This is achieved through formal

and informal meetings. Employee representatives are consulted

regularly on a wide range of matters affecting their current and

future interests.

The Group complies with all applicable labour laws in the

respective jurisdictions in which it operates.

Going concern

In determining whether the Company’s financial statements can

be prepared on the going concern basis, the Directors considered

the Company, and Groups’, business activities together with

factors likely to affect its future development, performance and its

financial position including cash flows, liquidity position and the

principal risks and uncertainties relating to its business activities,

as given in the Strategic Report.

Based on cash flow forecasts which take into account the

Directors’ best estimate of current sales orders and opportunities,

expenditure forecasts as well as the Group’s current cash balance,

which includes the proceeds of listing, the Directors consider it

appropriate to prepare the Company’s financial statements on the

going concern basis. For further details please refer to note 1.

Auditor

In the case of each of the persons who are Directors of the

Company at the date when this report is approved:

• as far as each of the Directors is aware, there is no relevant

audit information (as defined in the Companies Act 2006) of

which the Company’s auditor is unaware; and

• each of the Directors has taken all the steps that he ought to

have taken as a Director to make himself aware of any audit

information (as defined) and to establish that the Company’s

auditor is aware of that information.

This confirmation should be given and should be interpreted in

accordance with the provisions of section 418 of the Companies

Act 2006.

Deloitte LLP have expressed their willingness to continue in office

as auditor and a resolution to reappoint them will be proposed at

the forthcoming Annual General Meeting.

Approved by the Board of Directors and signed on behalf of the

Board

Mike Jefferies

Group Finance Director

22 June 2015

www.imimobile.com 22

FinancialStatements

23Annual Report 2015 | Stock Code: IMO

The Directors are responsible for preparing the Annual Report and

the financial statements in accordance with applicable law and

regulations.

Company law requires the Directors to prepare financial statements

for each financial year. Under that law the Directors are required

to prepare the group financial statements in accordance with

International Financial Reporting Standards (IFRSs) as adopted by

the European Union and Article 4 of the IAS Regulation and have

elected to prepare the parent company financial statements in

accordance with United Kingdom Generally Accepted Accounting

Practice (United Kingdom Accounting Standards and applicable

law). Under company law the Directors must not approve the

accounts unless they are satisfied that they give a true and fair

view of the state of affairs of the company and of the profit or loss

of the company for that period.

In preparing the parent company financial statements, the

Directors are required to:

• select suitable accounting policies and then apply them

consistently;

• make judgments and accounting estimates that are

reasonable and prudent;

• state whether applicable UK Accounting Standards have

been followed; and

• prepare the financial statements on the going concern basis

unless it is inappropriate to presume that the company will

continue in business.

In preparing the group financial statements, International

Accounting Standard 1 requires that Directors:

• properly select and apply accounting policies;

• present information, including accounting policies, in a

manner that provides relevant, reliable, comparable and

understandable information;

• provide additional disclosures when compliance with the

specific requirements in IFRSs are insufficient to enable users

to understand the impact of particular transactions, other

events and conditions on the entity’s financial position and

financial performance; and

• make an assessment of the company’s ability to continue as

a going concern.

The Directors are responsible for keeping adequate accounting

records that are sufficient to show and explain the company’s

transactions and disclose with reasonable accuracy at any time

the financial position of the company and enable them to ensure

that the financial statements comply with the Companies Act

2006. They are also responsible for safeguarding the assets

of the company and hence for taking reasonable steps for the

prevention and detection of fraud and other irregularities.

The Directors are responsible for the maintenance and integrity of

the corporate and financial information included on the company’s

website. Legislation in the United Kingdom governing the

preparation and dissemination of financial statements may differ

from legislation in other jurisdictions.

Responsibility Statement

We confirm that to the best of our knowledge:

• the financial statements, prepared in accordance with the

relevant financial reporting framework, give a true and fair

view of the assets, liabilities, financial position and profit or

loss of the company and the undertakings included in the

consolidation taken as a whole;

• the Strategic Report includes a fair review of the development

and performance of the business and the position of the

company and the undertakings included in the consolidation

taken as a whole, together with a description of the principal

risks and uncertainties that they face; and

• the annual report and financial statements, taken as a

whole, are fair, balanced and understandable and provide

the information necessary for shareholders to assess the

company’s performance, business model and strategy.

This responsibility statement was approved by the Board of

Directors and is signed on its behalf by

Mike Jefferies

Group Finance Director

22 June 2015

Statement of Directors’ Responsibilities

www.imimobile.com 24

We have audited the financial statements of IMImobile

PLC for the year ended 31 March 2015 which comprise the

Consolidated Income Statement, the Consolidated Statement of

Comprehensive Income, Consolidated Statement of Changes in

Equity, the Consolidated and Parent Company Balance Sheets,

the Consolidated Cash Flow Statement and the related notes 1 to

37. The financial reporting framework that has been applied in the

preparation of the group financial statements is applicable law and

International Financial Reporting Standards (IFRSs) as adopted by

the European Union. The financial reporting framework that has

been applied in the preparation of the parent company financial

statements is applicable law and United Kingdom Accounting

Standards (United Kingdom Generally Accepted Accounting

Practice).

This report is made solely to the company’s members, as a body, in

accordance with Chapter 3 of Part 16 of the Companies Act 2006.

Our audit work has been undertaken so that we might state to

the company’s members those matters we are required to state to

them in an auditor’s report and for no other purpose. To the fullest

extent permitted by law, we do not accept or assume responsibility

to anyone other than the company and the company’s members

as a body, for our audit work, for this report, or for the opinions we

have formed.

Respective responsibilities of Directors and auditor

As explained more fully in the Statement of Directors’

Responsibilities, the Directors are responsible for the preparation

of the financial statements and for being satisfied that they give

a true and fair view. Our responsibility is to audit and express an

opinion on the financial statements in accordance with applicable

law and International Standards on Auditing (UK and Ireland).

Those standards require us to comply with the Auditing Practices

Board’s Ethical Standards for Auditors.

Scope of the audit of the financial statements

An audit involves obtaining evidence about the amounts and

disclosures in the financial statements sufficient to give reasonable

assurance that the financial statements are free from material

misstatement, whether caused by fraud or error. This includes an

assessment of: whether the accounting policies are appropriate

to the group’s and the parent company’s circumstances and

have been consistently applied and adequately disclosed; the

reasonableness of significant accounting estimates made by the

Directors; and the overall presentation of the financial statements.

In addition, we read all the financial and non-financial information

in the annual report to identify material inconsistencies with the

audited financial statements and to identify any information that is

apparently materially incorrect based on, or materially inconsistent

with, the knowledge acquired by us in the course of performing the

audit. If we become aware of any apparent material misstatements

or inconsistencies we consider the implications for our report.

Opinion on financial statements

In our opinion:

• the financial statements give a true and fair view of the state

of the Group’s and of the parent Company’s affairs as at 31

March 2015 and of the group’s and the parent company’s loss

for the year then ended;

• the Group financial statements have been properly prepared

in accordance with IFRSs as adopted by the European Union;

• the parent Company financial statements have been properly

prepared in accordance with United Kingdom Generally

Accepted Accounting Practice; and

• the financial statements have been prepared in accordance

with the requirements of the Companies Act 2006.

Separate opinion in relation to IFRSs as issued by the IASB

As explained in note 1 to the Group financial statements, the group

in addition to applying IFRSs as adopted by the European Union,

has also applied IFRSs as issued by the International Accounting

Standards Board (IASB).

In our opinion the group financial statements comply with IFRSs as

issued by the IASB.

Opinion on other matter prescribed by the Companies Act 2006

In our opinion the information given in the Strategic Report and

the Directors’ Report for the financial year for which the financial

statements are prepared is consistent with the financial statements.

Independent auditor’s report to the members of IMImobile PLC

25Annual Report 2015 | Stock Code: IMO

David Griffin FCA (Senior statutory auditor)

for and on behalf of Deloitte LLP

Chartered Accountants and Statutory Auditor

London, UK

22 June 2015

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters

where the Companies Act 2006 requires us to report to you if, in

our opinion:

• adequate accounting records have not been kept by the

parent Company, or returns adequate for our audit have not

been received from branches not visited by us; or

• the parent Company financial statements are not in agreement

with the accounting records and returns; or

• certain disclosures of Directors’ remuneration specified by

law are not made; or

• we have not received all the information and explanations we

require for our audit.

Independent auditor’s report to the members of IMImobile PLC (continued)

www.imimobile.com 26

IMImobile PLC Consolidated Financial Statements

CONSOLIDATED INCOME STATEMENT

For the year ended 31 March 2015

The accompanying notes are an integral part of the consolidated Financial Statements and are all attributable to continuing

operations.

¹ EBITDA is defined as operating loss / profit before depreciation, amortisation, fees incurred in relation to IPO and acquisition activities, impairment charges, share based compensation and excluding

the impact of the disposal of subsidiaries.

27Annual Report 2015 | Stock Code: IMO

IMImobile PLC Consolidated Financial Statements (continued)

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

For the year ended 31 March 2015

The accompanying notes are an integral part of the consolidated Financial Statements.

www.imimobile.com 28

STATEMENT OF CHANGES IN EQUITY

For the year ended 31 March 2015

The accompanying notes are an integral part of the consolidated Financial Statements.

IMImobile PLC Consolidated Financial Statements (continued)

29Annual Report 2015 | Stock Code: IMO

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

As at 31 March 2015

IMImobile PLC Consolidated Financial Statements (continued)

www.imimobile.com 30

IMImobile PLC Consolidated Financial Statements (continued)

The accompanying notes are an integral part of the consolidated Financial Statements.

The financial statements of IMImobile PLC (Company number: 08802718) were approved by the Board and authorised for issue on

22 June 2015.

Signed on behalf of the Board

Mike Jefferies

Group Finance Director

22 June 2015

31Annual Report 2015 | Stock Code: IMO

CONSOLIDATED CASH FLOW STATEMENT

For the year ended 31 March 2015

IMImobile PLC Consolidated Financial Statements (continued)

The accompanying notes are an integral part of the consolidated Financial Statements.

www.imimobile.com 32

Notes to the Consolidated Financial Statements as at 31 March 2015

1. Basis of preparation

The consolidated Financial Statements for the years ended 31 March 2014 and 2015 have been prepared under the International

Financial Reporting Standards as adopted for use in the European Union in accordance with Article 4 of the IAS Regulation (EC) No.

1606/2002.

The financial information contained in the consolidated Financial Statements for the years ended 31 March 2014 and 2015 has been

prepared applying the recognition and measurement principles set out in International Financial Reporting Standards as adopted for

use in the European Union.

The consolidated Financial Statements of IMImobile PLC and its subsidiaries, hereafter referred to as “the Group”, are prepared under

the historical cost convention. A presentational currency of UK Pounds Sterling has been used and accounts have been translated

from other functional currencies into UK Pounds Sterling. The preparation of the consolidated Financial Statements in conformity with

IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of

applying the Group’s accounting policies.

Going Concern

The Company’s business activities, together with factors likely to affect its future development, performance and position are set out

in the Strategic Report and Director’s Report.

On 27 June 2014 the Company was successfully admitted to AIM. The successful listing resulted in net proceeds for the Company of

approximately £7 million (after considering fees and the acquisition of the Group).

At 31 March 2015 the Group had net assets of £38.9 million including £14.6 million of cash and cash equivalents (31 March 2014: net

assets of £13.9 million including £9.3 million of cash and cash equivalents).

In determining whether the consolidated Financial Statements can be prepared on the going concern basis, the Directors considered

the Company, and the Group’s, business activities together with factors likely to affect its future development, performance and its

financial position including cash flows, liquidity position and the principal risks and uncertainties relating to its business activities.

Based on cash flow forecasts which take into account the Directors’ best estimate of current sales orders and opportunities, expenditure

forecasts as well as the Group’s current cash balance, which includes the proceeds of listing, the Directors consider it appropriate to

prepare the Company’s financial statements on the going concern basis.

Basis of consolidation

The Group financial statements incorporate the financial statements of the Company and entities controlled by the Company (its

subsidiaries) made up to 31 March each year. Control is achieved when the Company:

• has the power over the investee;

• is exposed, or has rights, to variable return from its involvement with the investee; and

• has the ability to use its power to affect its returns.

The results of subsidiaries acquired or disposed of in any year are included in the consolidated Income Statement from the date of

acquisition or up to the date of disposal.

Goodwill is measured as the excess of the sum of consideration transferred. Goodwill is stated at cost less any accumulated impairment

losses. Goodwill is allocated to cash-generating units and is not amortised but is tested annually for impairment.

Where necessary, adjustments are made to the financial information of subsidiaries to bring the accounting policies into line with those

used by the Group. Inter-company balances and transactions, including inter-company profits and unrealised profits and losses are

eliminated on consolidation.

33Annual Report 2015 | Stock Code: IMO

1. Basis of preparation (continued)

The Group applies the acquisition method to account for business combinations. The consideration transferred for the acquisition

of a subsidiary is the fair values of the assets transferred, the liabilities incurred to the former owners of the acquiree and the equity

interests issued by the Group.

Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their

fair values at the acquisition date. The Group recognises any non-controlling interest in the acquiree on an acquisition-by-acquisition

basis. When the Group ceases to have control, any retained interest in the entity is remeasured to its fair value at the date when control

is lost, with the change in carrying amount recognised in the Income Statement.

The acquisition of IMI Mobile Private Limited by IMImobile PLC has been accounted for as a capital reorganisation, presenting the

continuation of the Group’s results and financial position to reflect the substance of the transaction, with the 24% interest in IMI Mobile

Private Limited owned by the two founding shareholders accounted for as a non-controlling interest.

Notes to the Consolidated Financial Statements as at 31 March 2015 (continued)

Entities included under common control

The following entities are considered to be under common control and therefore have been included in the consolidated Financial

Statements for the years ended 31 March 2014 and 2015:

* TxtLocal Limited was added during the year ended 31 March 2015.

New accounting pronouncements adopted on 1 April 2014

On 1 April 2014 the Group adopted the following new accounting policies to comply with amendments to IFRS. The accounting

pronouncements, none of which are considered by the Group as significant on adoption, are:

- Amendments to IAS 32 “Offsetting financial assets and financial liabilities”;

- Amendments to IAS 39 “Novation of derivatives and continuation of hedge accounting”;

- “Improvements to IFRS 2010–2012 cycle”; and

- IFRIC 21 “Levies”

www.imimobile.com 34

Notes to the Consolidated Financial Statements as at 31 March 2015 (continued)

1. Basis of preparation (continued)

New accounting pronouncements to be adopted on 1 April 2015

The following pronouncements which are potentially relevant to the Group have been issued by the IASB are effective for annual

periods beginning on or after 1 July 2014 and have been endorsed for use in the EU:

- Amendments to IAS 19 “Defined Benefit Plans: Employee Contributions”; and

- “Improvements to IFRS 2011–2013 cycle”.

New accounting pronouncements to be adopted on or after 1 April 2016

On 1 April 2016 the Group will adopt “Accounting for Acquisitions of Interests in Joint Operations, Amendments to IFRS 11”, “Clarification

of Acceptable Methods of Depreciation and Amortisation, Amendments to IAS 16 and IAS 38”, “Sale or Contribution of Assets between

an Investor and its Associate or Joint Venture, Amendments to IAS 10 and IAS 28”, “Improvements to IFRS 2012–2014 Cycle” and

“Disclosure Initiative, Amendments to IAS 1” which are effective for accounting periods on or after 1 January 2016 and which have not

yet been endorsed by the EU.

The Group is currently confirming the impacts of the above new pronouncements on its results, financial position and cash flows, which

are not expected to be material.

2. Accounting policies

The principal accounting policies set out below have been applied consistently by the Group entities:

Foreign currencies

Items included in the consolidated Financial Statements of each of the Group’s entities are measured using the currency of the primary

economic environment in which the entity operates (“the functional currency”). The consolidated Financial Statements are presented

in UK Pounds Sterling (“the presentational currency”).

Foreign currency transactions are translated into the presentational currency using the exchange rates prevailing at the dates of the

transactions or valuation where items are re-measured. Foreign exchange gains and losses resulting from the settlement of such

transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies

are recognised in the Income Statement.

Translation differences on non-monetary financial assets, such as equities classified as available for sale, are included in other

comprehensive income.

The results and financial position of all the Group entities (none of which has the currency of a hyper-inflationary economy) that have a

functional currency different from the presentation currency are translated into the presentation currency as follows:

(a) assets and liabilities for each balance sheet presented are translated at the closing rate at the date of that balance sheet;

(b) equity items other than retained earnings have been translated at historical rates in line with IAS 21;

(c) income and expenses for each Income Statement are translated at average exchange rates; and

(d) all resulting exchange differences are recognised in other comprehensive income.

Goodwill arising on the acquisition of a foreign entity is treated as an asset of the foreign entity and translated at the closing rate.

Financial instruments

Financial assets and financial liabilities are recognised on the Group’s balance sheet when the Group becomes a party to the contractual

provisions of the instrument.

Loans and receivables

Trade receivables, loans, and other receivables that have fixed or determinable payments that are not quoted in an active market are

classified as loans and receivables. Loans and receivables are measured at amortised cost using the effective interest method, less

35Annual Report 2015 | Stock Code: IMO

2. Accounting policies (continued)

any impairment. Income is recognised by applying the effective interest rate, except for short-term receivables when the recognition

of interest would be immaterial.

Impairment of financial assets

Financial assets are assessed for indicators of impairment at each balance sheet date. Financial assets are impaired where there is

objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated

future of cash flows of the investment have been impacted.

For certain categories of financial asset, such as trade receivables, assets that are assessed not to be impaired individually are

subsequently assessed for impairment on a collective basis. Objective evidence of impairment for a portfolio of receivables could

include the Group’s past experience of collecting payments, an increase in the number of delayed payments in the portfolio past the

average credit period of 30 days, as well as observable changes in national or local economic conditions that correlate with default

on receivables.

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the exception of trade

receivables, where the carrying amount is reduced through the use of an allowance account. When a trade receivable is considered

uncollectible, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited

against the allowance account. Changes in the carrying amount of the allowance account are recognised in the Income Statement.

Financial liabilities and equity

Financial liabilities and equity instruments are classified according to the substance of the contractual arrangements entered into.

Equity instruments

An equity instrument is any contract that evidences a residual interest in the assets of the Group after deducting all of its liabilities.

Equity instruments issued by the Group are recorded at the proceeds received, net of direct issue costs.

Trade receivables

Trade receivables do not carry any interest and are stated at their nominal value as reduced by appropriate allowances for estimated

irrecoverable amounts.

Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and demand, deposits and other short-term highly liquid investments that are

readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value.

Trade payables

Trade payables are not interest-bearing and are stated at their nominal value.

Available-for-sale financial assets

Available-for-sale financial assets are non-derivatives that are either designated in this category or not classified in any of the other

categories. They are included in non-current assets unless the investment matures or management intends to dispose of it within 12

months of the end of the reporting period and measured at fair value. Fair value changes are recognised directly in equity, through the

statement of changes in equity, except for impairment losses which are recognised in the consolidated income statement.

Cash and cash equivalents

Cash and short–term deposits in the balance sheet comprise cash at bank and in hand and short–term deposits with an original

maturity of three months or less, highly liquid investments that are readily convertible into known amounts of cash and which are

subject to insignificant risk of changes in value. For the purpose of the consolidated Cash Flow Statement, cash and cash equivalents

Notes to the Consolidated Financial Statements as at 31 March 2015 (continued)

www.imimobile.com 36

2. Accounting policies (continued)

consist of cash and cash equivalents as defined above, net of outstanding bank overdrafts.

Trade receivables

Trade receivables are amounts due from customers for merchandise sold or services performed in the ordinary course of business.

If collection is expected in one year or less (or in the normal operating cycle of the business if longer), they are classified as current

assets. If not, they are presented as non-current assets. Trade receivables are recognised initially at fair value and subsequently

measured at amortised cost using the effective interest method, less provision for impairment.

Trade payables

Trade payables are obligations to pay for goods or services that have been acquired in the ordinary course of business from suppliers.

Trade payables are classified as current liabilities if payment is due within one year or less (or in the normal operating cycle of

the business if longer). If not, they are presented as non-current liabilities. Trade payables are recognised initially at fair value and

subsequently measured at amortised cost using the effective interest method.

Borrowings

Borrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are subsequently carried at amortised

cost; any difference between the proceeds (net of transaction costs) and the redemption value is recognised in the Income Statement

over the period of the borrowings using the effective interest method. Fees paid on the establishment of loan facilities are recognised

as transaction costs of the loan to the extent that it is probable that some or all of the facility will be drawn down. In this case, the fee is

deferred until the draw-down occurs. To the extent there is no evidence that it is probable that some or all of the facility will be drawn

down, the fee is capitalised as a pre-payment for liquidity services and amortised over the period of the facility to which it relates.

Preference shares, which are mandatorily redeemable on a specific date, are classified as liabilities. The dividends on these preference

shares are recognised in the Income Statement as interest expense.

Borrowings are classified as current liabilities unless the Group has an unconditional right to defer settlement of the liability for at least

12 months after the end of the reporting period.

Intangible assets

(a) Goodwill

Goodwill arises on the acquisition of subsidiaries and represents the excess of the consideration transferred over the Group’s interest

in the net fair value of the net identifiable assets, liabilities and contingent liabilities of the acquiree and the fair value of the non-

controlling interest in the acquiree.

For the purpose of impairment testing, goodwill acquired in a business combination is allocated to each cash generating unit (“CGU”

or “unit”), or groups of CGUs, that is expected to benefit from the synergies of the combination. Each unit or group of units to which the

goodwill is allocated represents the lowest level within the entity at which the goodwill is monitored for internal management purposes.

Goodwill is monitored at the CGU level.

Goodwill impairment reviews are undertaken annually or more frequently if events or changes in circumstances indicate a potential

impairment. The carrying value of goodwill is compared to the recoverable amount, which is the higher of value in use and the fair value

less costs of disposal. Any impairment is recognised immediately as an expense and is not subsequently reversed.

(b) Trademarks and licences

Separately acquired trademarks and licences are shown at historical cost. Trademarks and licences acquired in a business combination

are recognised at fair value at the acquisition date. Trademarks and licences have a finite useful life and are carried at cost less

Notes to the Consolidated Financial Statements as at 31 March 2015 (continued)

37Annual Report 2015 | Stock Code: IMO

2. Accounting policies (continued)

accumulated amortisation. Amortisation is calculated using the straight-line method to allocate the cost of trademarks and licences

over their estimated useful lives of 10 years.

Acquired computer software licences are capitalised on the basis of the costs incurred to acquire and bring to use the specific software.

These costs are amortised over their estimated useful lives of three to five years.

(c) Computer software

Costs associated with maintaining computer software programmes are recognised as an expense as incurred. Development costs that

are directly attributable to the design and testing of identifiable and unique software products controlled by the Group are recognised

as intangible assets when the following criteria are met:

• it is technically feasible to complete the software product so that it will be available for use;

• management intends to complete the software product and use or sell it;

• there is an ability to use or sell the software product;

• it can be demonstrated how the software product will generate probable future economic benefits;

• adequate technical, financial and other resources to complete the development and to use or sell the software product are

available; and

• the expenditure attributable to the software product during its development can be reliably measured.