Embed Size (px)

Citation preview

JUNE212017

IMPACTASSESSMENTOFODINEPROGRAMME

BYIDC

1

2

Contents

Executivesummary......................................................................................................5

1. Introduction.........................................................................................................7

1.1. Maingoalsandapproach.............................................................................7

1.2. Datasources.................................................................................................8

1.3. Structureofthereport.................................................................................9

2. MappingODINEcompanies................................................................................10

2.1. Europeanlandscape...................................................................................10

2.2. Profilebyage..............................................................................................12

2.3. Profilebynumberofemployees................................................................13

2.4. Typeofoffering..........................................................................................13

2.5. Commercialstrategies................................................................................15

2.6. Conclusions.................................................................................................16

3. EvaluationofODINEservices.............................................................................17

3.1. Overview....................................................................................................17

3.2. EvaluationofBenefits................................................................................19

3.3. Conclusions.................................................................................................20

4. OpenDataBenefits............................................................................................21

4.1. UseofOpenData.......................................................................................21

4.2. BuildinganOpenDataecosystem..............................................................25

4.3. SocialBenefits............................................................................................28

4.4. Conclusions.................................................................................................28

5. EvaluationofBusinessPlans..............................................................................29

5.1. Approach....................................................................................................29

5.2. MeasuringAchievement............................................................................30

5.3. Mainresults................................................................................................31

5.4. Clustering:aninvestor’sview.....................................................................33

5.5. Conclusions.................................................................................................35

5.5.1. AchievementofODINEcompanies.......................................................35

3

5.5.2. ODINEimpact.......................................................................................36

5.5.3. Levelofachievementvs.externalfunding...........................................37

6. ODINEImpactsongrowth..................................................................................38

6.1. Introduction................................................................................................38

6.2. Methodology..............................................................................................39

6.2.1. Step1:BaselineAssumptions–MarketModel....................................39

6.2.2. Step2:ForecastAssumptions–MarketModel....................................43

6.2.3. Survey-BasedModel.............................................................................44

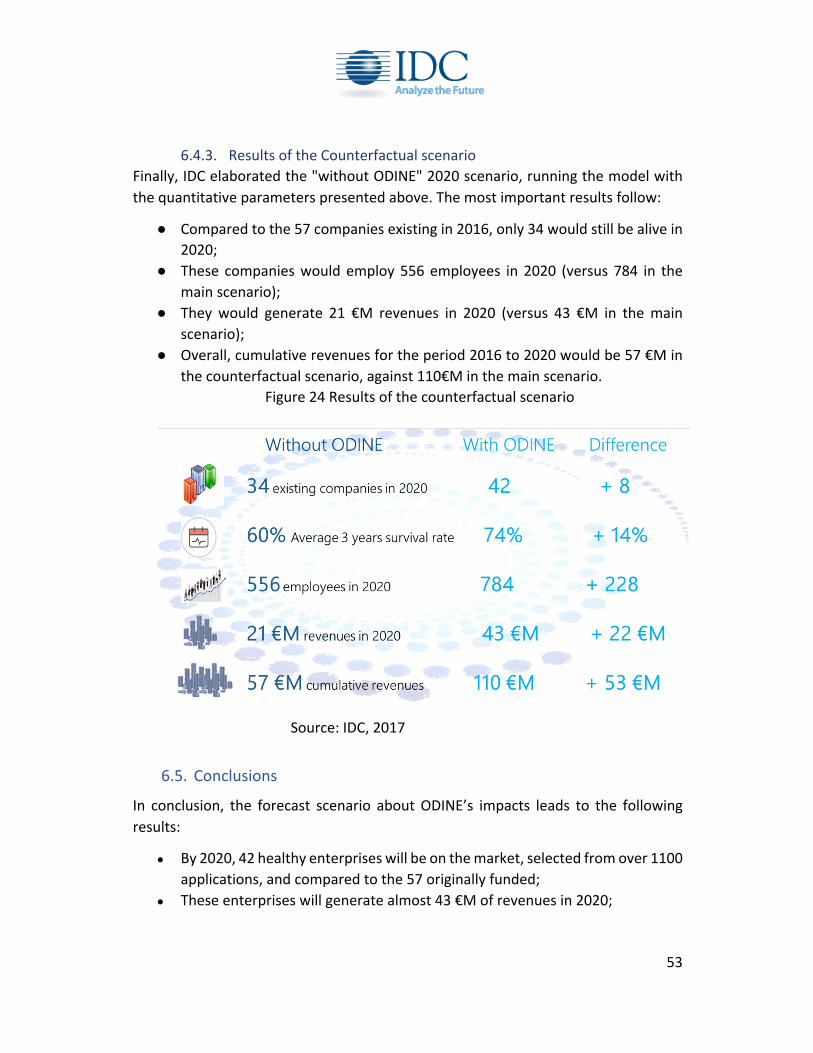

6.3. Impactassessment.....................................................................................45

6.3.1. Modelresults........................................................................................45

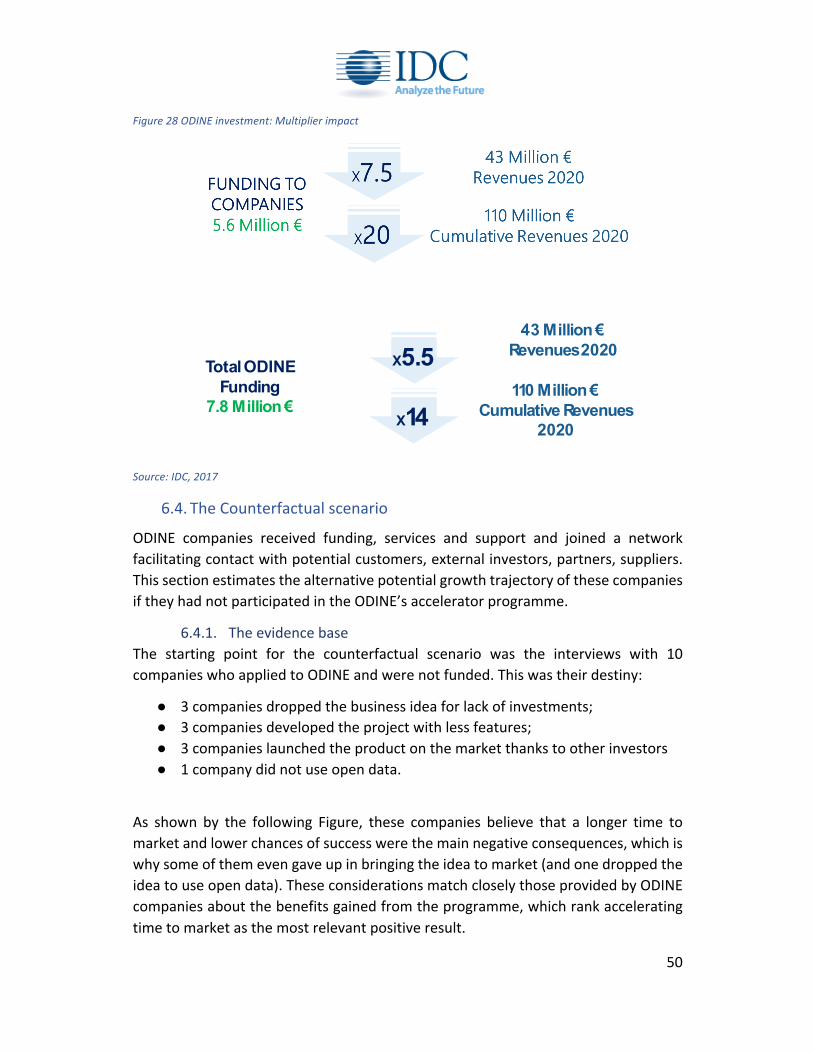

6.3.2. MultiplierImpacts................................................................................49

6.4. TheCounterfactualscenario......................................................................50

6.4.1. Theevidencebase................................................................................50

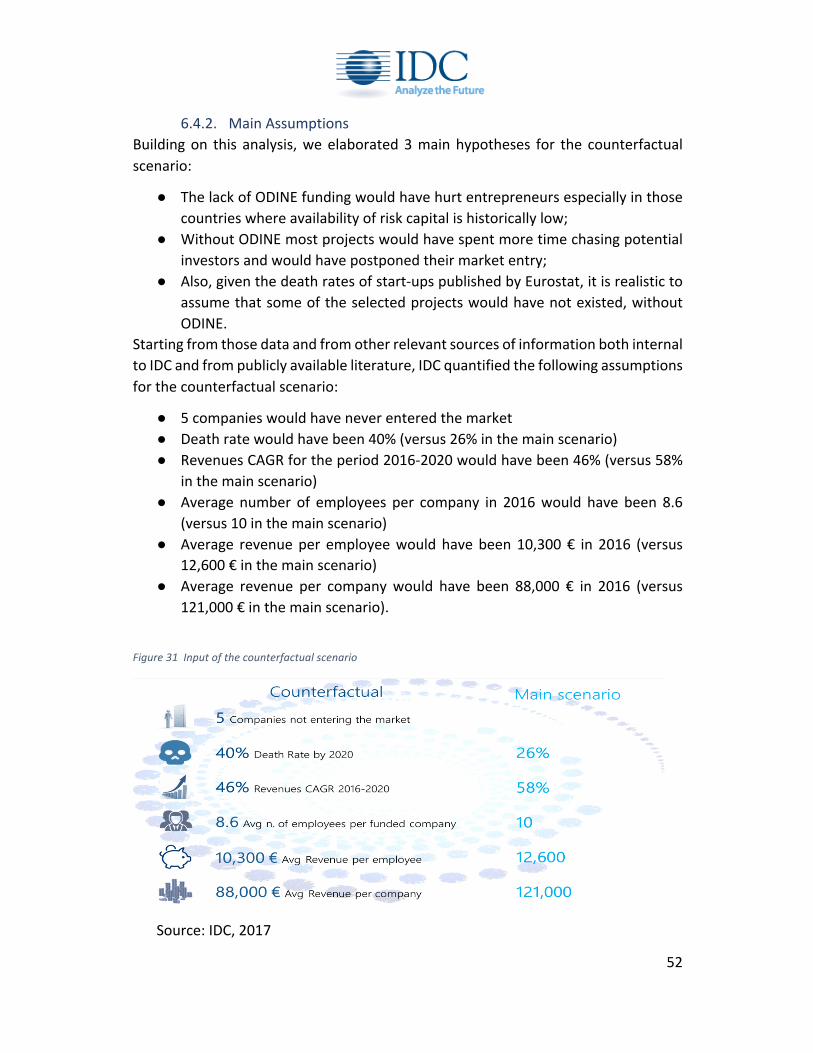

6.4.2. MainAssumptions................................................................................52

6.4.3. ResultsoftheCounterfactualscenario................................................53

6.5. Conclusions.................................................................................................53

7. GeneralConclusions...........................................................................................54

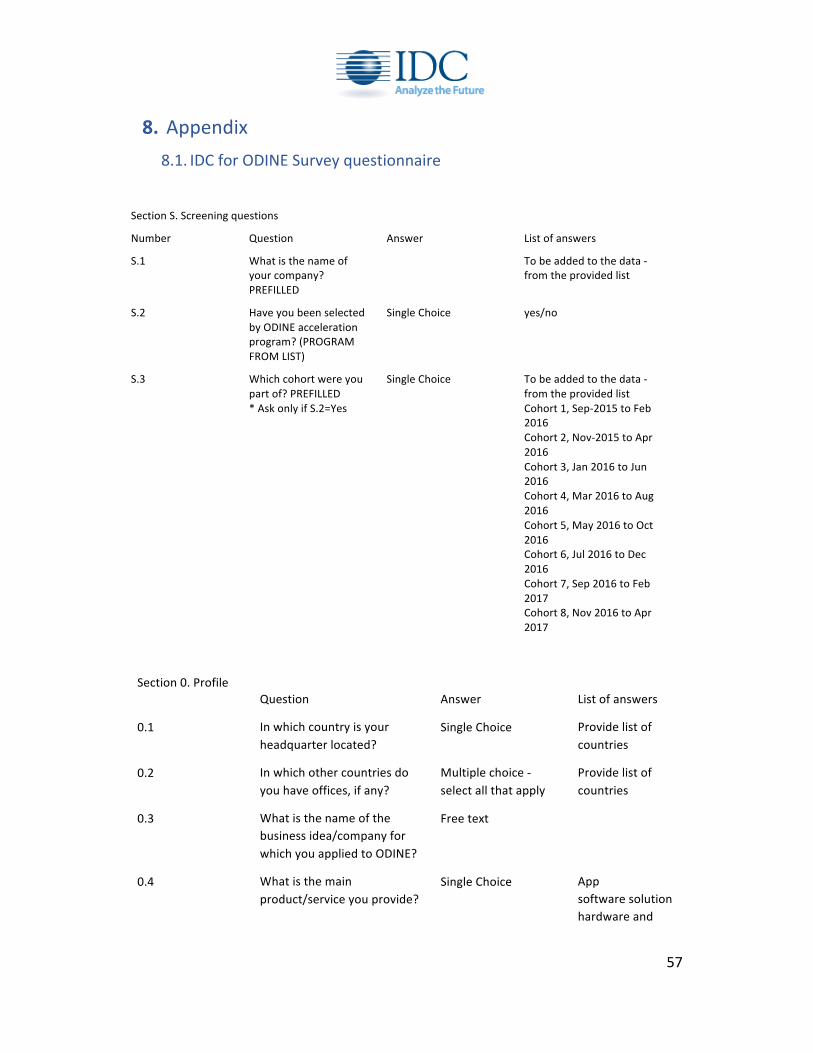

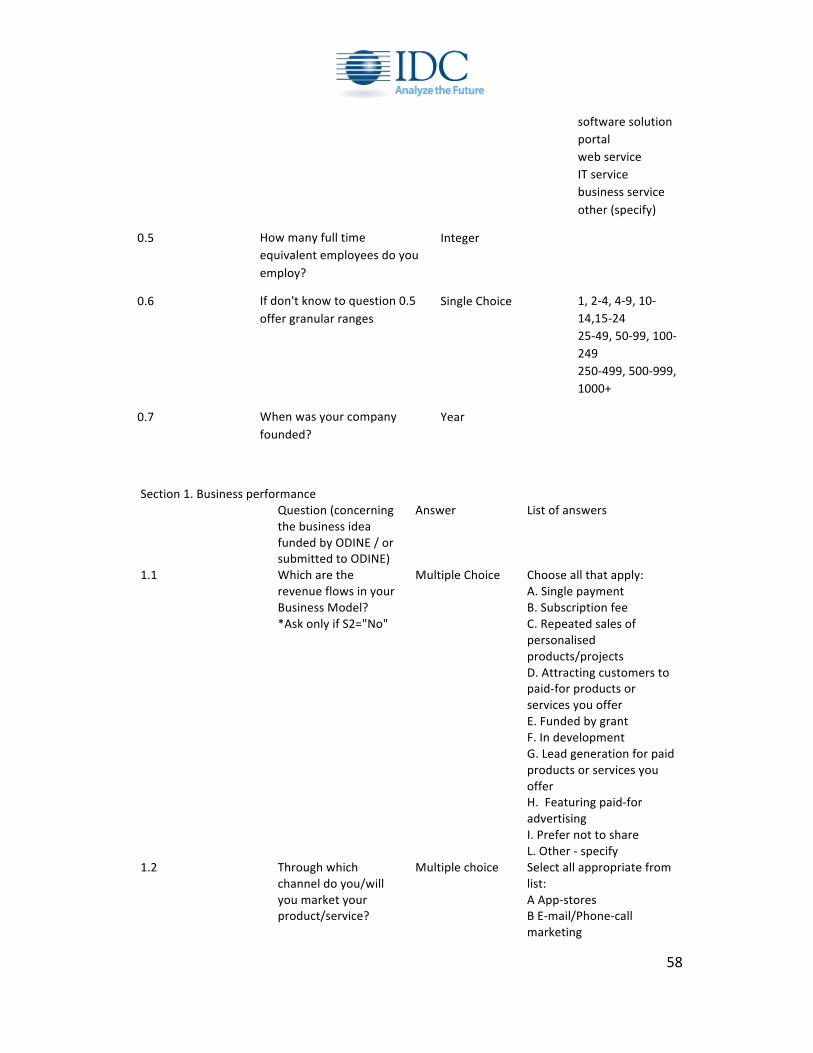

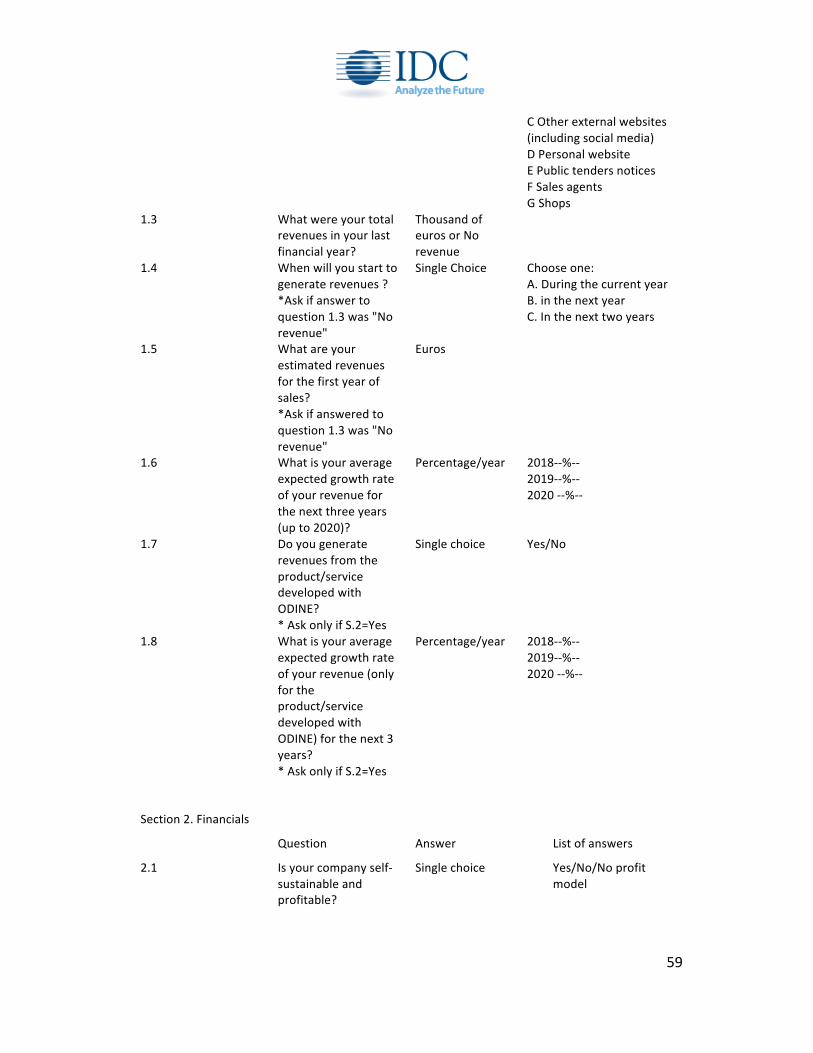

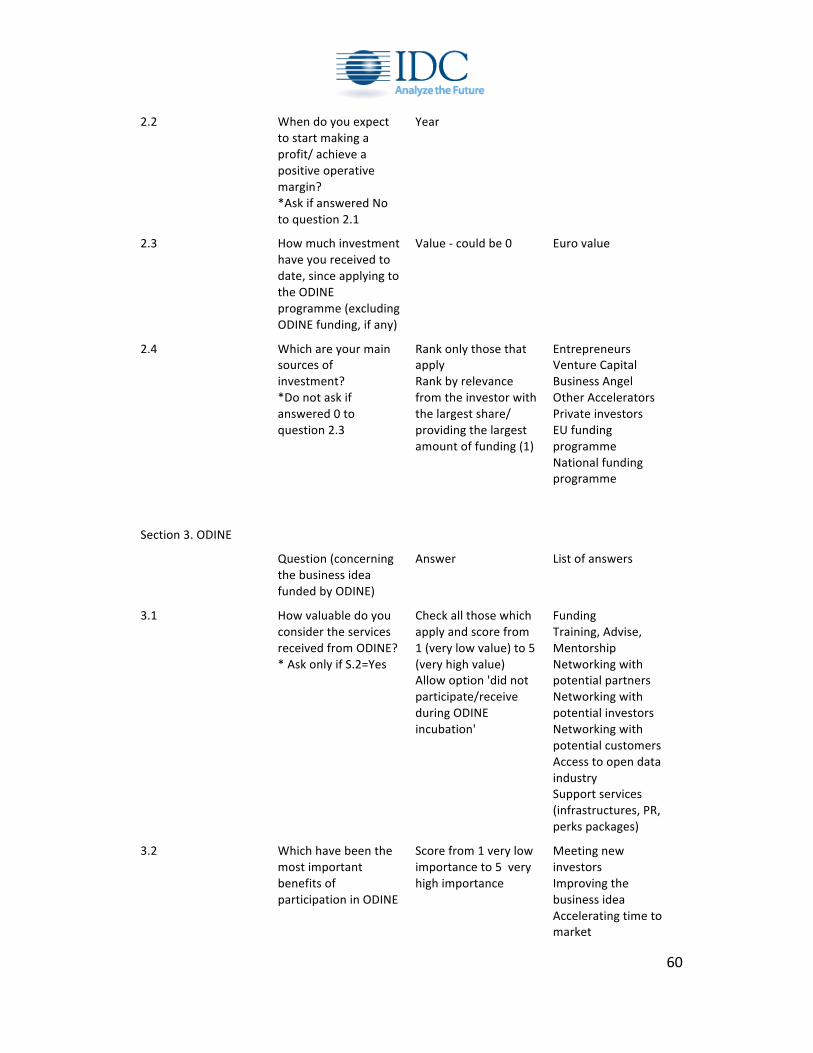

8. Appendix............................................................................................................57

8.1. IDCforODINESurveyquestionnaire..........................................................57

8.2. Descriptionofnon-fundedcompanies.......................................................65

4

Table1DistributionofODINEcompaniesbyMSandOpenDataMaturityCluster...............12Table2ODINEPortfolioofServices......................................................................................17Table3ShareofcompaniesbyageclusterandtypeofOpenDataClusterused..................25Table4ODINEcompanies’classificationbytargetmarket....................................................26Table5AchievementIndicator’sdescription.........................................................................30Table6Selectedcompaniesaveragerevenuesinthe1styear.............................................42Table7Descriptionof10non-fundedcompanies.................................................................65Figure1Geographicaldistributionofthe57fundedcompanies...........................................10Figure2PercentageofODINEcompaniesbyemploymentsizeclasses................................13Figure3DifferentiationofODINEcompaniesbyProductandAge........................................14Figure4ODINEandFIWAREBusinessModelscomparison...................................................15Figure5ODINEandFIWARESalesChannelscomparison.....................................................16Figure6EvaluationofODINEServices...................................................................................19Figure7EvaluationofODINEbenefits...................................................................................20Figure8TypeofOpenDatausedODINEcompanies............................................................21Figure9ClustersofOpenDatabytype..................................................................................22Figure10NumberofcompaniesbytypeofOpenDataCluster.............................................23Figure11CompaniesbyageandtypeofOpenData............................................................24Figure12.MainSocialBenefitsofOpendata.......................................................................28Figure13Achievementindicatorsscoresdistribution(40respondents)...............................31Figure14Valuepropositionscoresbycompanymaturity(40respondents).......................32Figure15Revenueflowscoresbycompanymaturity(40respondents)...............................32Figure16Customeracquisitionscorespointbycompanymaturity(40respondents)..........32Figure17Financialscoresbycompanymaturity(40respondents)......................................33Figure18Clusteringcompaniesbylevelofachievement(40respondents)..........................35Figure19ODINEcompaniesbylevelofachievement(40respondents)..............................36Figure20ODINEimpactbylevelofachievement(37respondents)......................................37Figure21Externalfundingbylevelofachievement(40respondents)..................................38Figure2215ForecastRevenuesto2020byyear...................................................................45Figure23ForecastRevenuesto2020byyear........................................................................46Figure24Averagerevenuespercompanyto2020byyear...................................................47Figure25Numberofemployeesto2020byyear.................................................................47Figure26Numberofusersto2020byyear:Consumerportion............................................48Figure27Numberofusersto2020byyear:Businessportion..............................................49Figure28ODINEinvestment:Multiplierimpact....................................................................50Figure29Consequencesforcompaniesnon-selectedbyODINE..........................................51Figure30Difficultiesfacedbynot-selectedcompanies.........................................................51Figure31Inputofthecounterfactualscenario.....................................................................52

5

ExecutivesummaryBased on IDC’s independent impact assessment, ODINE’s incubation programmeachieveditsmainobjectivetoattractandfundagroupofinnovativedigitalcompanieswithoriginalbusinessideasaboutOpenDataandaccelerateth

eirtimetomarketandchancesofsuccess.ODINE’s57fundedcompanies,ofwhich31 are startups born with the programme, represent a wide variety of valuepropositions based on either software solutions, or software solutionswith somehardwarecomponents(IoTsolutions),orweb-basedservices.TheycontributetothedevelopmentofanOpenDataecosysteminEuropecoveringallsegmentsofthedatavaluechain,withastrongerpresenceinthemoreinnovativecomponents.Overall,wecanseeacommonthreadrunningacrossmanyof thesecompaniesaiming forwhat ODINE calls the triple bottom line, that is achieving economic, social andenvironmentalbenefits.

TheassessmentwascarriedoutinMarch-April2017andwasbasedondatacollectionthrough an independent survey1 of the 57 funded companies and 10 non-fundedcompanies, the information published by the companies, ODINE’s databases anddocuments repositories. IDC developed a forecast model estimating potentialrevenues, jobscreatedandthenumberofcustomersof thesecompaniesto2020,under amain and a counterfactual scenario. The resultswere comparedwith theimpactassessmentof theFiwareacceleratorprogramme,which fundedover1000startupsandSMEs,carriedoutbyIDCin2014-16.

Thekeyresearchquestionsexaminedbytheassessmentwerethefollowing.

WhatimpacthasODINEhadoncompanygrowth?

ODINE’sprogrammewaswellappreciatedbytheparticipants,whogaveithighscoresintermsofvalueadded,withthehighestbenefitsconcerningacceleratingtimetomarket,improvingthebusinessidea,andimprovingtheteamskills.

BasedonIDC’sforecastimpactmodelofthe57fundedcompanies,ODINE’simpacton their growth perspectives was relevant, resulting in an estimated 110 €M ofcumulative revenues in the period 2016-2020, plus 784 jobs created. Averagerevenuespercompanyby2020shouldbearound1€M,correspondingto55,000€of

1Thesurveywassenttoall57companieswithmultiplefollowupsandcollected42respondents(32viatheonlinequestionnaireand10viatelephoneinterview).DatagapswerefilledusingtheODINEquestionnairesurvey

6

revenuesperemployee,sufficientforsustainability.Thismeansthatperourmodelestimates,eacheuroinvestedbytheECintheODINEprojectwillhavegeneratedupto14eurosincumulativerevenuesby2020,whichisagoodmultiplier.

Participantcompaniesshowgrowthratesofrevenues,employmentandusersalignedwith main accelerators and better than the average performance of the 1000companies funded by the FIWARE accelerator program. They also show a goodcapabilitytocollectadditionalfunding,eventhoughmanyarestillintheearlyphaseofdevelopment.

The counterfactual scenario shows that due to longer time to market, greaterdifficulty in getting funding, and higher failure rates, without ODINE only 34companies would have survived to 2020, generating half as much cumulativerevenuesand228lessjobsthaninthemainscenario.

HowsuccessfulwerethebusinessplansofODINE’sparticipants?

Theanalysisofthebusinessplansof40fundedcompaniesand10non-fundedonesshowsagoodlevelofachievementofthemainobjectives,particularlythestartupsofthe group. The influence of ODINE’s mentors in helping several companies inredirectingandimprovingtheirbusinessideaorbusinessplanisclear.ThecompanieswithahighlevelofachievementoftheirbusinessplansarealsomoreappreciativeofODINE’s support in accelerating their time to market and more likely to collectexternalfundingfromothersources.

Whatisthebenefitofopendatatoparticipantbusinesses?

ODINE succeeded in inspiring and promoting a range of new business ideashighlightingthevalueaddedofOpenDatainthedatamarket.Eachofthe57startupsandSMEs leverages2ormoretypesofOpenData,withastrongconcentrationofinterestingeospatial/mappingandenvironmentaldata.WefoundthatstartupsuseawidervarietyofOpenDatathanyoungormaturecompaniesinthegroup,playingthe role of experimenters, combining different typologies of Open Data for theirsolutions.More thanhalfof thegrouphavea strongvertical focusaiming for theemergingneedsofnewandtraditionalsectors.AnotherpriorityofODINEcompaniesistheemergingsustainableorlowcarboneconomy,withseveralcompaniesfocusedonenergysaving,environmentalmonitoring,smartmobility.ThereisalsoapositivecorrelationbetweenthelevelormaturityatcountryleveloftheOpenDatamarket(measuredbyaCapgeministudy)andthenumberofODINEsuccessfulapplicantsbycountrypointsoutthatarichopendataenvironmentprovidesfavorableconditionsforinnovatorsinthisfield.Thismeansthatproactivepoliciesimprovingtheusability

7

and availability of open data sets are likely to stimulate private initiatives for theexploitationofdatainapositivevirtuouscycle.

1. Introduction1.1. Maingoalsandapproach

ThisisthefinalreportofIDC’sindependentimpactassessmentoftheworkdeliveredbyODINE, the incubationprogrammeforstart-ups,SmallandMediumEnterprises(SMEs) working with or in the field of Open Data. This assessment is aimed atanalysing and extrapolating the impacts ofODINE’s activity by collecting evidenceabout the progress and perspectives of the 57 SMEs funded and fast-tracked byODINE.

Thefocusoftheimpactassessment–thekeyresearchquestion–iswhetherthe€7.8MillioninvestedbytheECinODINEwerewellspent,meaningwhethertheyledtoasubstantial acceleration of growth by the SMEs selected by the incubator. Thisevaluationwouldnotbecompletewithouta counterfactual scenariooutlining thealternativeimpacts iftheinvestmenthadnotbeenmade.Thisalternativescenariowas developed based on desk research and the evidence collected from 10unsuccessfulapplicantstotheproject’scalls.

Thereportprovidestheanswersto3mainresearchsub-questionsinwhichtheoverallevaluationwasarticulated,asfollows:

WhatimpacthasODINEhadoncompanygrowth?

ThisimpactwasmeasuredthroughthefollowingKPIs(Keyperformanceindicators)estimatedbyaneconomicmodelprojectingactual2017dataforallthe57fundedcompanies:

● Currentandforecastrevenuesto2020;● Currentandforecastjobscreatedto2020;● Numberandgrowthofonlineusers/customersto2020;● Amountofadditionalfundingcollectedbyprivate/publicsources;

The same indicators were measured for the non-funded SMEs to develop thecounterfactualscenario.ThisallowedtomeasuretheaggregatedeconomicimpactofODINE’sinvestmentto2020andcontrastitwiththepotentialimpactsachievedbyacounterfactualscenario.

HowsuccessfulwerethebusinessplansofODINE’sparticipants?

8

IDCanalysedindepththeachievementofthebusinessplansof40fundedcompanies2and 10 non-funded ones, through a composite achievement indicator measuringsuccessin4keyperformanceareas:effectivenessofthevalueproposition,abilitytogeneraterevenueflows,toacquirecustomers,tofinancebusinessdevelopmentbycapturingadditional funding fromothersourcesbeyondODINE.Asthe incubator’sservices were aimed at improving each company’s performance under all theseaspects,measuringtheseachievementsprovidesanarticulatedevaluationofODINE’svalueadded.Thishelpedtounderstandthedifficultiesfacedbythe10non-fundedcompaniesandtodeveloptheassumptionsforthecounterfactualscenario.

Whatisthebenefitofopendatatoparticipantbusinesses?

ODINE’smainobjectiveistostimulatenewbusinessideasaswellastheOpenDatamarket,whichisnot(contrarytowidelyheldbeliefs)thesameasthePublicSectorInformation(PSI)market.TheuseofOpenDataincombinationwithprivatedatacanleadtoawiderangeofpotentialbusinessopportunities,notnecessarily limitedtonon-profitbusinessmodels,asshownbythe57enterprisessuccessfullyapplyingforODINE’s funding. To evaluate ODINE’s achievement in this area IDC explored themarketpositioningofthe57fundedcompanies,withafocuson:

● Theclassificationofthetypeofopendatatheyused;● Theanalysisofthewayinwhichopendatasetswereleveraged/transformed/

processed;● Theclassificationofthemarketstargetedandtheirtypeofoffering;● Thesocialandenvironmentalbenefitsexpected.

OneofODINE’skeyobjectiveswastoselectandaccelerateenterprisesabletoachievea “triple bottom line” including economic, social and environmental benefits. Thisanalysis therefore helped to establish whether this objective was achieved. TheassessmentbuildsonthemostrecentresearchandanalysesonOpenDatamarkets,firstofallthematuritybenchmarksdevelopedbyCapgeminiConsultinginthestudy“CreatingValue throughOpenData: Studyon the ImpactofRe-useofPublicDataResources”fortheEuropeanDataPortalin2016.3

1.2. DatasourcesThisstudyisbasedonextensivedeskandfieldresearch.Theevidencecollectedcomesfrom:

217companiesdidnotprovidesufficientdataontheirbusinessmodels.3https://www.europeandataportal.eu/sites/default/files/edp_creating_value_through_open_data_0.pdf

9

● An ad-hoc online survey based on a structured questionnaire, with closedanswers,articulatedin6sections(Profile,Businessperformance,Financials,ODINE services, Momentum, Open Data plus a final section only for non-funded companies)4. The survey collected 42 answers (32 online plus 10completedbyphone) in theperiodApril-earlyMay2017,ofwhichonly40providedsufficientdataforthebusinessmodelanalysis.

● 10interviewswith10non-fundedcompanieswiththesamequestionnaire.5Therespondentscamefromthelistof87unsuccessfulapplicantsprovidedbythe ODINE consortium. IDC reached out via email and telephone to all 87potential respondents until it completed a small sample of 10 casesdifferentiated by time of application (cohort) and company age (mixedbetweenstart-upsandalreadyexistingSMEs).

● ODINE’sdatabaseofdeliverables,dataonfundedandnon-fundedcompanies,partners’ interviews and documentation on screening criteria, accelerationactivitiesandsoon.Theresultsof theBusinessmodelsurveyconducted inDecember2016(deliverable6.3)wereparticularlyusefultofillinthegapsofIDC’ssurvey.

● Dataandinformationaboutthecompaniessourcedfromtheirownwebsites;● Data and methodologies from FI-IMPACT, the FP7 CSA (Concertation and

SupportAction)ledbyIDCwithintheFIWAREacceleratorprogrammein2014-2016. The projectmonitored, interviewed and analysed the 1024 start-upsand SMEs funded by 11 Accelerator projects, forecasting their economicimpacts to 2020. These data serve as useful benchmarks for ODINE’scompaniesresults.

● DeskresearchonpublicdatasourcessuchasEurostatandotherAcceleratorsreports.

1.3. Structureofthereport

Thereportisstructuredasfollows:

● Executivesummary● Chapter1describesthegoalsandapproachofthestudy;● Chapter2mapsthemainfeaturesofthefundedcompanies;● Chapter3analysestheinfluenceofODINE’sservices;● Chapter3answerstotheresearchquestiononthebenefitsofopendata;

4Thequestionnaireandthesurveyresultsareannexedtothisreport5Therewasonlyonedifference:InsteadofquestionsaboutODINEservicesthenon-fundedcompanieswereaskedabouttheirdifficultieswithoutODINEsupport.

10

● Chapter5answers the researchquestionon thesuccessfulachievementofbusinessplans;

● Chapter6answerstheresearchquestionontheeconomic impactsandthepotentialconsequencesofacounterfactualscenario;

● Chapter7drawsthefinalconclusions;● TheAppendixincludesthesurveydataandthequestionnaire.

2. MappingODINEcompaniesThis chapter analyses the profile and characteristics of the 57 companies ODINEselected for funding out of over 1000 applicants, describing them in terms ofgeographical location, age, number of employees, type of offering, customerstargeted. After checking for correlations between their characteristics and growthdynamics,wehave found that themost relevantdifferentiating factor is their age(companiesincorporatedlessthan36monthsbeforereceivingODINEfundingversuscompanieswithmorethan36monthsofexistence)whichinfluencestheiruseandapproachtoOpenData,asshowninthefollowingparagraphs.Thevarietyoftheirotherfeaturesandcommercialstrategiesdemonstratesthatthereisnotasinglewaytosuccess(asilverbullet)forthesecompanies.

2.1. Europeanlandscape

ODINE did not select companies based on their geographical location, but on thequalityoftheirbusinessidea.Also,thesestart-upsandSMEsaredigitalbusinesseswhosephysical location is lessrelevantthanitwouldbefortraditionalbusinesses.Nevertheless, thegeographicaldistributionof these companies is auseful startingpoint(Figure1below).

Figure1Geographicaldistributionofthe57fundedcompanies

11

Source:ElaborationonIDCSurvey,April2017andODINEBusinessModelSurvey,December2016.

TheUKhoststhelargestgroupofcompanies(17)followedbyGermany(10).Togethertheyrepresenthalfofthetotal.Exceptfor2fromIsrael,therestofthegroupisspreadaround Europe: Netherlands and Spain have 4 each, Austria 3, Belgium, France,Greece,Ireland,Slovenia2each.Estonia,Finland,Italy,Latvia,Romania,SwitzerlandandSlovakiahave1 fundedcompany.A tentativeobservation couldbe that smalldynamiceconomieswithastrongfocusondigitaltechnologies(Estonia,Ireland)aremore represented thanmostof theEUBig6 (particularly Italy and France, not tomentionPolandwhichisnotpresentatall).Butthesampleistoosmalltoprovidesignificantcorrelationsatthesinglecountrylevel.TheODINEpartnersinchargeofdisseminationwerebasedrespectivelyinUKandGermany,sothiswaslikelyafactorintheprevalenceofapplicantsfromthesecountries.

However,itisinterestingtoinvestigatewhethercountrieswithastrongOpenDatamarket generated more business ideas applying to ODINE. To check this, wecompared thenationalprovenanceofODINEcompanieswith the2016OpenDataMaturitybenchmarkofEUMemberStates6developedbyCapgeminiconsultingonbehalfoftheEC(table1).Countrieshavebeengroupedintoclustersregardingtheirdifferentmaturitylevels.Infact,thelargestgroupofODINEcompanies(34)belongtocountriesintheTrendSetterscluster,characterizedbysolidopendataportalsandadvancedopendatapolicies,togetherwithanationalcoordinationacrossdomains.Another6enterprisescomefromcountriesintheFastTrackerscluster,whichareinagoodpositionintheiropendatajourneybutneedtoexploitbetterthebenefitsofeitheropendatapoliciesorportals.ThisseemstoconfirmthatadvancedOpenData

6https://www.europeandataportal.eu/sites/default/files/edp_landscaping_insight_reportn22016.pdf

12

markets provide a favorable environment for innovatorswith newbusiness ideas,suchasODINE’sfundedcompanies.

Table1DistributionofODINEcompaniesbyMSandOpenDataMaturityCluster

OpenDataMaturityCluster

MemberStates NumberofODINEfundedcompanies

TrendSetters Austria,Bulgaria,Finland,France,Ireland,theNetherlands,Spain,UK

UK(17),NL(4),ES(4),AT(3),FR(2),IE(2),FI(1);Total=33

FastTrackers Estonia,Greece,Slovakia,Romania,Norway,Croatia,Slovenia,,Luxemburg

EL(2),SK(1),SI(2),EE(1),RO(1);Total=7

Followers

Belgium,CzechRepublic,Cyprus,Denmark,Germany,Hungary,Italy,Lithuania,Poland,Portugal,Sweden,Switzerland

BE(2),DE(10),IT(1),CH(1);Total=14

Beginners Liechtenstein,Latvia,Malta LV(1);Total=1Source:IDCelaborationonCapgeminiConsulting7

Theexception isGermany,whichgenerated10successfulapplicantstoODINEbuthasalowOpenDataMaturity,becauseofthefragmentationandlowcoordinationoftheinternalopendataportalssystem(managedattheregional/locallevel),aswellas low usability of Open Data sets. Given the size of the German economy, 10successfulODINEcompaniesarenotsomany:theUKissmallerandgeneratedalmosttwiceasmany.Perhapsthisfactcanbereadintheoppositeway:thattheGermanmarket has a strong innovation potentialwhich is currently hindered andmay berealizedfasterifthenationalOpenDatapolicyandactivitieswillcatchupwithprivateinitiative. A few other countries (Belgium, Italy and Switzerland) in the Followerscluster and 1 in the Beginners cluster (Latvia) host ODINE innovators but theyrepresentasmallminorityofthegroup.

2.2. ProfilebyageStartupsandveryyoungcompaniesaredifferentfromestablishedcompanies,astheytypicallygrowatfasterratesandareathigherriskoffailure.IntermsofagetheODINE57companiescanbeclassifiedin3groups:

● 31arestartups(borninorafter2014);● 15areyoung(bornin2012or2013);● 11aremature(borninorbefore2011).

StartupsandyoungcompaniesderivemostoftheirrevenuesfromthebusinessideafundedbyODINE,sotheprogrammeeconomicimpactonthemisstronger.Maturecompanies already have revenues, and we considered only those generated by

7https://www.europeandataportal.eu/sites/default/files/edp_landscaping_insight_reportn22016.pdf

13

ODINE’sbusinessideafortheeconomicmodel.OverallthoughwecanseethattheroleofODINEwasfundamentalformostofthesample.

2.3. Profilebynumberofemployees

Youngcompaniesandstartupstypicallyhaveaverysmallnumberofemployees,butallthecompaniesinthisgroupareverysmall.Amongthe57,only14%havemorethan 10 employees and only a few havemore than 30. Perhaps also thematurecompaniesinthegroupwerelookingtofindapathtofastergrowthandappliedtoODINEtodoso.

Figure2PercentageofODINEcompaniesbyemploymentsizeclasses

Source:ElaborationonIDCSurvey,April2017andODINEBusinessModelSurvey,December2016.

2.4. TypeofofferingThemaindifferentiationbetweentheODINEcompanies,besidesage,isthetypeofoffering,whichdictatesthebusinessdevelopmentstrategy.Wedefineofferingasthetypeofproductorserviceofferedonthemarketwhichrepresentsthemainsourceofrevenues.Wefoundthatthe57companiescanbeclassifiedin3maingroups:

● Pure software: 29 companies offer software solutions such as apps andsoftwaretools.Thisisthelargestgroup.Forexample:

o Contagt is an app through which visitors can view a buildingmap,navigateindoors and report issues by sending photos to thebuildingoperator.

14

o IPlytics offers an online-based market intelligence tool to analyzetechnology trends, market developments and a company’scompetitiveposition.

● Hardware and software: 6 companies provide hardware componentsembeddedwith a software solution,most frequently these are Internet ofThings(IoT)solutions.Examplesare:

o Liimtec developed PocketDefi, a public access defibrillator which issmall,affordable andprovidesauniqueuserexperiencebybeingmonitoredandservicedthrougha mobilenetwork.

o GreenCitySolutionstriestofighttheproblemofairpollutionwithafour-meter-highCityTree installation,providingcleanandcoolair tohoturbancities.

● Web-based services: 22 companies use digital technologies to provide aservice for businesses or consumers. For example, this can includemarketplaces or peer-to-peer online platforms where companies orconsumers can find information,purchasegoods, look for specific services,andsoon.Examplesare:

o Alephgivesthewholeworldaccesstothebestsourceofinformationaboutoil,gas andmining.

o Resc.info is a service that shares local data with fire departmentslookingtotailorprogrammestoresidentsatrisk.

Breakingdown the groupof companies by age and typeof offering (Figure 3)wenotice that there aremore youngand startup companiesprovidingpure softwaresolutions thanmaturecompanies,who insteadaremore likely toofferweb-basedservices.More interesting, there aremanymore startupsprovidinghardware andsoftwareproducts.SincethesearemainlyIoTsolutions,thismaybeafunctionoftheincreasing attractiveness in timeof the IoTmarket aswell as the greater focusofstartupsoncuttingedgeinnovation.

Figure3DifferentiationofODINEcompaniesbyProductandAge

15

Source:ElaborationonIDCSurvey,April2017,andonODINEdata

2.5. Commercialstrategies

Tounderstandthewayinwhichthevariegatedgroupof57fundedprojectsruntheirbusiness,weaskedcompaniesabouttheirbusinessmodelsandtheirsaleschannel(withmultipleanswersquestions).Thein-depthevaluationofthebusinessmodelsispresentedinchapter5,butislimitedto40companieswhoprovidedadditionaldataontopofthedatashownhere.

WecomparedtheiranswerswiththeresponsesthatwehadfromtheFIWAREproject,tobetterunderstandthematuritylevelofthebusinessoftheODINEparticipants.Wefound similarities, such as the Subscription as themost common business model(chosenby87%ofODINEcompanies),followedbytheSinglePaymentmodel,chosenbyonethirdofcompanies.

Figure4ODINEandFIWAREBusinessModelscomparison

16

Source: IDC for ODINE Survey, April 2017 (42 respondents) plus ODINE Business Survey, December 2016, (15respondents),FI-IMPACTproject2016

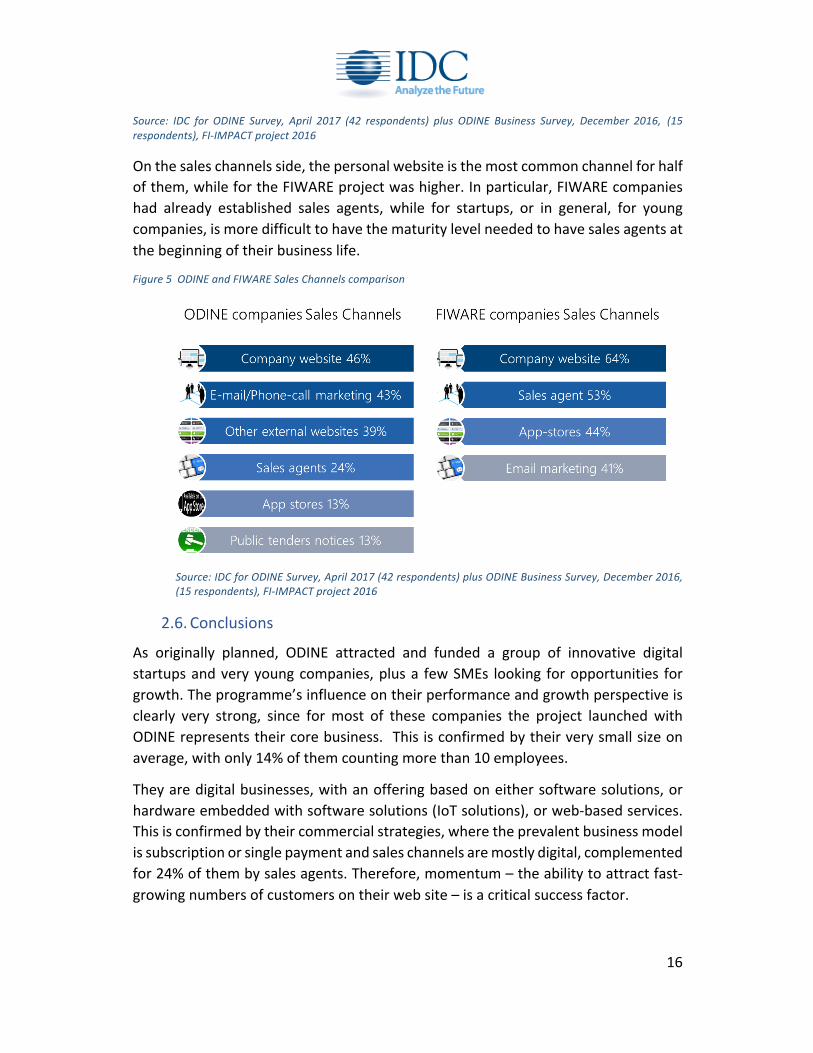

Onthesaleschannelsside,thepersonalwebsiteisthemostcommonchannelforhalfofthem,whilefortheFIWAREprojectwashigher.Inparticular,FIWAREcompanieshad already established sales agents, while for startups, or in general, for youngcompanies,ismoredifficulttohavethematuritylevelneededtohavesalesagentsatthebeginningoftheirbusinesslife.

Figure5ODINEandFIWARESalesChannelscomparison

Source:IDCforODINESurvey,April2017(42respondents)plusODINEBusinessSurvey,December2016,(15respondents),FI-IMPACTproject2016

2.6. ConclusionsAs originally planned, ODINE attracted and funded a group of innovative digitalstartupsandveryyoungcompanies,plusa fewSMEs looking foropportunities forgrowth.Theprogramme’sinfluenceontheirperformanceandgrowthperspectiveisclearly very strong, since formost of these companies the project launchedwithODINErepresentstheircorebusiness.Thisisconfirmedbytheirverysmallsizeonaverage,withonly14%ofthemcountingmorethan10employees.

Theyaredigitalbusinesses,withanofferingbasedoneithersoftwaresolutions,orhardwareembeddedwithsoftwaresolutions(IoTsolutions),orweb-basedservices.Thisisconfirmedbytheircommercialstrategies,wheretheprevalentbusinessmodelissubscriptionorsinglepaymentandsaleschannelsaremostlydigital,complementedfor24%ofthembysalesagents.Therefore,momentum–theabilitytoattractfast-growingnumbersofcustomersontheirwebsite–isacriticalsuccessfactor.

17

Nosignificantcorrelationemergedbetweenspecificofferingsandgrowthdynamics,demonstratingthatthereisnotasinglewaytosuccessforthesecompanies.However,apositivecorrelationbetweennationalmaturityoftheOpenDatamarket(measuredby aCapgemini study) and thenumberofODINE successful applicantsby countrypoints out that a rich open data environment provides favorable conditions forinnovatorsinthisfield.Thismeansthatproactivepoliciesimprovingtheusabilityandavailability of open data sets are likely to stimulate private initiatives for theexploitationofdatainapositivevirtuouscycle.

3. EvaluationofODINEservicesODINE´s acceleration program provided to the selected companies a catalogue ofservices to increase their ability to perform successfully and grow, built on theexpertise from WAYRA, Telefonica´s business accelerator, and ODI’s Startupprogramme. This chapter presents the evaluation of ODINE services by thebeneficiaries,thefundedcompanies.

3.1. OverviewTheaccelerationprogramwastailoredforeachstart-upandSMEneeds,potentialandperformance, with the objective of getting the best results out of each one, in ademandingandconstantlychallengingcontext.Theaccelerationprogramfocusesongaining and increasing business traction for its start-ups and SMEswhile bringinginnovationintowellestablishedcompanieswithadurationofsixmonths.ThemainservicesaredescribedintheTablebelow.

Table2ODINEPortfolioofServices

TRACKING:Followup,challenge,andboosttheprogressofstart-upsandSMEs.

TRAINING:Trainentrepreneursinbusinessareasorskillsrequiredfortheirdevelopment.

ADVICE:Professionalservicesateverystart-upandSMEdisposal,accordingtotheirneeds.

MENTORING:Supportbyprofessionalsofwell-knownexperience(investors,entrepreneurs,experts...)tohelpentrepreneurstomakesoundstrategicdecisions.

NETWORKING:Openupopportunitiesfortheentrepreneursthroughthegenerationofrelevantcontacts.

SPACE:Possibilitytoaccessthespacesprovidedbypartnersinseverallocations.

ACCESSTOINDUSTRY:ProvidelinkingwaysfortheteamswhodevelopinterestingsolutionsforTelefónicaandotherindustrialpartnersclosetotheconsortium.

INFRASTRUCTURE:Provisionoftoolsdevelopedbypartnersthatwillhelpinthemanagementofdifferentactivities.Specialoffersfromprivatecloudproviders

18

PR/COMMS:Supportthepromotionoftheimageandproductofthestart-upsandSMEs,thankstothereachofODINE´spartners,especiallyTheGuardian.

GRANT:Directgrantofupto€100kperteamandsupporttowardstheachievementoffundingfromthirdparties.

INTERNATIONALIZATION:AsaPanEuropeanproject,andleveragingonthepartnersglobalfootprint,theselectedstart-upsandSMEswillhaveopportunitiestointroducethemselvesinothercountries/regions.

EXPERIENCE/BELONGING:EmotionallyengagetheentrepreneurswithODINE,ensuringafruitfulrelationship.

OFFERS:Offers3rdpartyservicesandproductsavailabletostart-upsandSMEs.Source:ODINEDeliverable3.1AcceleratorProgrammePortfolio

Theaccelerationstage(levelofmaturity)ofthecompanyisalsoimportanttoidentifythemostappropriateservices.ODINEdefinedtheaccelerationstagesasfollows:

● PRE-COMMERCIALSTAGE:start-upsandSMEsaremakingfinaladjustmentstotheirbusinessidea,evaluatingitsvalueproposition,completingitsbusinessmodel,reachingaMVP(marketablevalueproposition)andvalidatingit.

● COMMERCIAL STAGE: the start-ups are launching their products and/orservices on the market. The objective is to achieve a marketable valuepropositionandtoobtain“Engagement”(Product-MarketFit)thattranslatesinto Traction. During this stage the start-up or SME often goes through aprocess of constant trial and error and continuous iterations based on thefeedbackof“relevant”customersinordertopolishtheirproduct.

● GROWTHSTAGE/SCALEUP:This isastagethatonlystart-upswiththebestperformancewillachieve.Thefocuswillbetoreachadominantpositionatregionalorinternationallevel.Theaimoftheaccelerationprogramwillbetoconvert“start-ups”intosustainable“scaleups.

ODINEparticipantswereaskedtoassesshowvaluabletheyconsideredtheservicesreceived, on a scale from 1 (very low value) to 5 (very high value). Overall, theevaluation is quite positive,withmost services scored above the “medium value”midpointofthescaleandonlyone(networkingwithpotentialinvestors)under3,asshownintheFigurebelow.

Notsurprisingly, funding is theservicethatgotthehighestscore(4.7).Oneof themainreasonsisthecompanies'profile:youngandverynewcompaniesthatneedtobefundedtojuststarttheirbusiness.Eveniftheactualamountoffundingwassmall,it was sufficient to kick-off their activities and take the first steps in the growthprocess.Also,inEuropeseedmoneyisrelativelyscarceforstartups.

19

Thesecondmostappreciatedserviceistheaccesstoopendata(3.8).Sinceopendataisatthecoreofthecompanies,thishasahighvalueforcompanies.Thethirdandfourth most valuable services are Support services (infrastructure, PR, perkpackages),togetherwithTraining,AdviseandMentorship.Theseservicesarecriticalinthepre-commercialphasebutalsointheearlycommercialstage,whencompaniesarelaunchingtheirservicesonthemarket,andwerewellappreciatedbecauseoftheircontributiontothedevelopmentofthebusinessidea.

Thenetworkingservices(generatingrelevantcontactsfortheentrepreneurs)wereevaluatedatalowerlevelcomparedtothepreviousones,butstillcloseto3(mediumvalue). Networking with potential customers was best appreciated, followed bynetworking with potential partners and only last with potential investors. This isprobablyduetotheearlystageofdevelopmentofthesecompanies,mostofwhomwerenot in the scale-up stageand thereforewerenot ready toengagewithnewinvestorssuchasventurecapitalists.

Figure6EvaluationofODINEServices

Question:“HowvaluabledoyouconsidertheservicesreceivedfromODINE?Scorefrom1(very lowvalue)to5(veryhighvalue)

Source: IDC for ODINE Survey, April 2017 (42 respondents) plus ODINE Business Survey, December 2016, (15respondents)

3.2. EvaluationofBenefitsTheevaluationofbenefitsgainedfromtheparticipationtotheprogrammeconfirmstheevaluationofservices,withanoverallpositiveassessmentscore.ODINEserviceshelpedthemost inacceleratingthetimetomarket, improvingthebusiness idea,and improving the team skills. This confirms the assessment of the stage of

20

developmentofthesecompanies,whoappliedtoODINEtobringtheirideatomarketandreceivedthetypeofsupportneededtodoso.

Coherentlywith thispicture,engagingwithpotentialcustomerswasconsideredofmediumvalue,whilenetworkingwithpotentialornewinvestorswasscoredatlowvalue.

Figure7EvaluationofODINEbenefits

Question:WhichhavebeenthemostimportantbenefitsofparticipationtotheODINEprogramme?Scorefrom1(verylowvalue)to5(veryhighvalue)

Source: IDC for ODINE Survey, April 2017 (42 respondents) plus ODINE Business Survey, December 2016, (15respondents)

3.3. Conclusions

Inconclusion, the57companiesappreciated theacceleratorprogrammeand tookadvantageofthesupportprovided,achievingexactlythemainbenefitaimedfor,thatisfasterentryintothemarketandbetterchancesofsuccess.Thescoringresultsweresimilarinbothsurveys(ODINE'sownsurveyandtheIDConecarriedoutinApril2017),

21

showing consistency in the participants’ opinions. In fact, when asked about thepotentialconsequencesiftheyhadnotbeenselectedbyODINE,97%ofrespondentssaid their time tomarketwouldhavebeen longer,62%said theywouldhavehadlower chances of success. Moreover, 21% of respondents said they would havedropped the business idea and 31%would not have usedOpenData. The resultshighlighttheinfluenceofODINE’sprogrammeoncompanies’behavior.

4. OpenDataBenefitsAmajorgoalofODINEwastoinspireandpromotenewbusinessideasintheopendata market. The analysis of the variety of open data sets used by the ODINEcompaniesandtheirexpectedimpactsprovidesagoodvisibilityonhowthisgoalwasachieved.Thisanalysisisbasedonthesurveyanswersaboutthetypeofopendatausedbyeachcompany,asshowninFigure8below.Datasetswerethengroupedinclusterswithsimilartopics.

4.1. UseofOpenDataODINEcompaniesuseonaverage2ormoretypesofOpenData(Figure8below),first,because theyhavemultiplemarkets focus, second,because theywant to improvetheircompetitivenesswithastrongvalueproposition,and lastly,becausetheyareconscious of the potential economic and social impacts of open data on theecosystem,andtheywanttocontributetoit.

Asshownbythedata,there isa largevarietyofthetypeofdatasetsselectedbutthereisclearlyaconcentrationofinterestingeospatial/mappingandenvironmentaldata.

Figure8TypeofOpenDatausedODINEcompanies

Numberofrespondents,multipleanswers

22

Source: IDC for ODINE Survey, April 2017 (42 respondents) plus ODINE Business Survey, December 2016, (15respondents)

Toinvestigatethemeaningofthislonglistofdatatypologies,wehavegroupedthemin5clustersbasedontheirsimilarities.Theyarethefollowing:

1. Environment: includes Environment, Energy, Geospatial/Mapping, Weather,Tourism,Agriculture&food;

2. Vertical Markets: includes Housing, Manufacturing, Transportation, Business,Legal,Finance;

3. Social comprises Education, Demographics and Social, International/Globaldevelopment,Economics,Science&research;

4. GovernmentincludesGovernmentoperations,PublicSafety,Health/Healthcare;5. ConsumercontainsonlyConsumer.

Figure9ClustersofOpenDatabytype

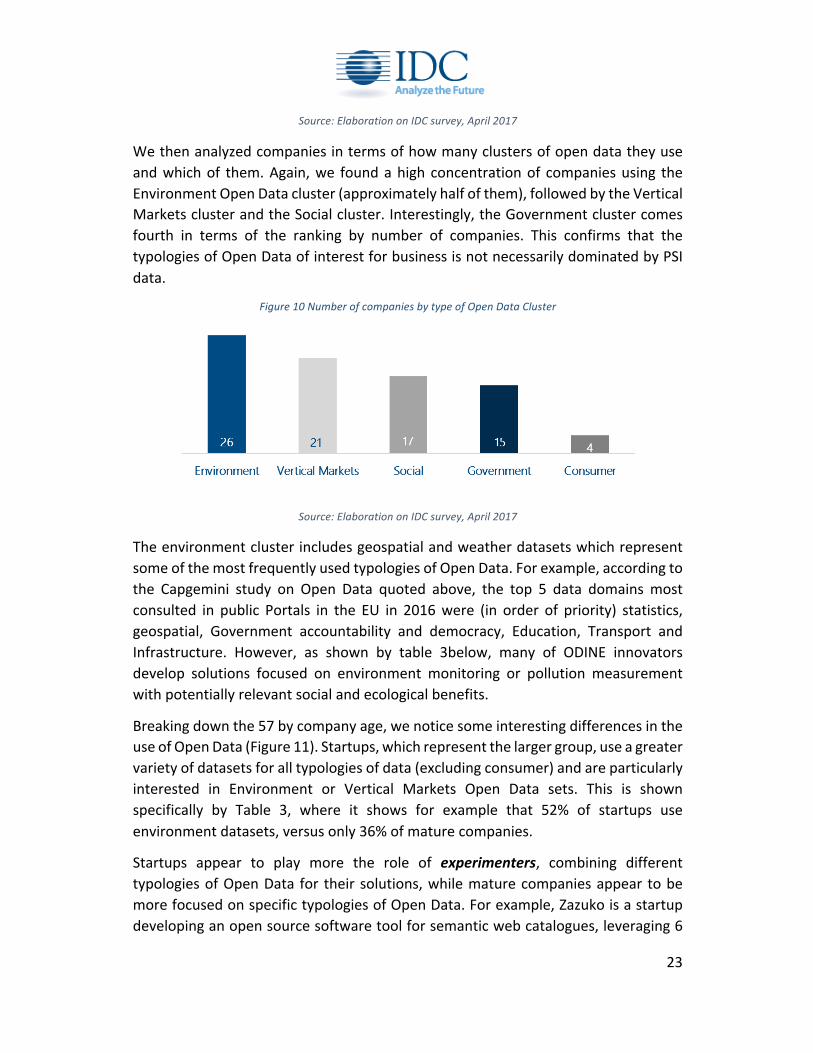

23

Source:ElaborationonIDCsurvey,April2017

Wethenanalyzedcompaniesintermsofhowmanyclustersofopendatatheyuseandwhichof them.Again,we foundahigh concentrationof companiesusing theEnvironmentOpenDatacluster(approximatelyhalfofthem),followedbytheVerticalMarketsclusterandtheSocialcluster.Interestingly,theGovernmentclustercomesfourth in terms of the ranking by number of companies. This confirms that thetypologiesofOpenDataofinterestforbusinessisnotnecessarilydominatedbyPSIdata.

Figure10NumberofcompaniesbytypeofOpenDataCluster

Source:ElaborationonIDCsurvey,April2017

TheenvironmentclusterincludesgeospatialandweatherdatasetswhichrepresentsomeofthemostfrequentlyusedtypologiesofOpenData.Forexample,accordingtothe Capgemini study on Open Data quoted above, the top 5 data domains mostconsulted in public Portals in the EU in 2016were (in order of priority) statistics,geospatial, Government accountability and democracy, Education, Transport andInfrastructure. However, as shown by table 3below, many of ODINE innovatorsdevelop solutions focused on environment monitoring or pollution measurementwithpotentiallyrelevantsocialandecologicalbenefits.

Breakingdownthe57bycompanyage,wenoticesomeinterestingdifferencesintheuseofOpenData(Figure11).Startups,whichrepresentthelargergroup,useagreatervarietyofdatasetsforalltypologiesofdata(excludingconsumer)andareparticularlyinterested in Environment or Vertical Markets Open Data sets. This is shownspecifically by Table 3, where it shows for example that 52% of startups useenvironmentdatasets,versusonly36%ofmaturecompanies.

Startups appear to play more the role of experimenters, combining differenttypologiesofOpenData for their solutions,whilematurecompaniesappear tobemorefocusedonspecifictypologiesofOpenData.Forexample,Zazukoisastartupdevelopinganopensourcesoftwaretoolforsemanticwebcatalogues,leveraging6

24

different types of data: agriculture and food, business, transportation (verticalmarkets cluster); environment, geospatial/mapping (environment cluster),government operations (government cluster). This is an innovative combination.Another startup, Unigraph, has designed a knowledge graph technology to breakdown the open data “silos” and accommodate infinite data inputs, leveraging 6differenttypesofdatabelongingto4differentclusters (business,demographics&social,economics,finance,geospatial/mapping,governmentoperations).

On the other hand, mature companies instead tend to use a smaller number ofdatasets which appear strongly correlated. For example, Brightbook provides aninnovative accounting solution leveraging the Vertical markets datasets cluster(financeandbusinessdata),whileIdalabisfocusedonurbanplanningleveragingthegovernmentoperationscluster.Anotherexample,UNICS/SIRISdevelopscustomizedanalyticsproductsforHighEducationandResearchinstitutionsandfocuseson3maintypologiesofdatasets(education,governmentoperations,andscienceandresearch)buttheyarecloselycorrelatedandfallin2clustersonly.

Figure11CompaniesbyageandtypeofOpenData

25

Source:ElaborationonIDCsurvey,April2017

Table3ShareofcompaniesbyageclusterandtypeofOpenDataClusterused

OpenDataCluster Startups Young Mature total

Environment 52% 40% 36% 46%VerticalMarkets 39% 33% 27% 37%Government 29% 20% 27% 26%Social 32% 27% 27% 30%Consumer 3% 13% 9% 7%total 100% 100% 100% 100%

Source:ElaborationonIDCsurvey,April2017

4.2. BuildinganOpenDataecosystem

ODINE companies consider Open Data as extremely or very important for theirbusinessmodel(88%ofrespondents)oratleastmoderatelyimportant(theremaining12%).Thisisnatural,becausetheuseofOpenDatawasoneofthecriteriaofselectionof thisgroupofcompanies.But,evenmorerelevant, thevarietyofbusiness ideasdeveloped by the ODINE companies naturally compose an Open Data ecosystemcoveringmostsegmentsofthedatavaluechain,withastrongerpresenceinthemoreinnovativecomponentslikedataanalytics.

ThisemergesfromtheclassificationshowninTable4below,whichlookscloselyatODINE companies’ value proposition and their target markets, based on IDC’sexperience and knowledge of emerging demand trends. This classification is not

26

statistically validated8, but highlights how these companies are developing data-driveninnovationbysectorormarketsegment,focusingonthevalueaddedbroughtby thecombinationofOpenDataandcommercialorproprietarydata.This showsODINE’simpactonthedevelopmentofaninnovativeecosysteminEurope,becausedata-driveninnovationlinkscompaniesandcustomersinnewways,providingvalueaddedbasedondata,businessintelligence,matchingdemandwithsupply.

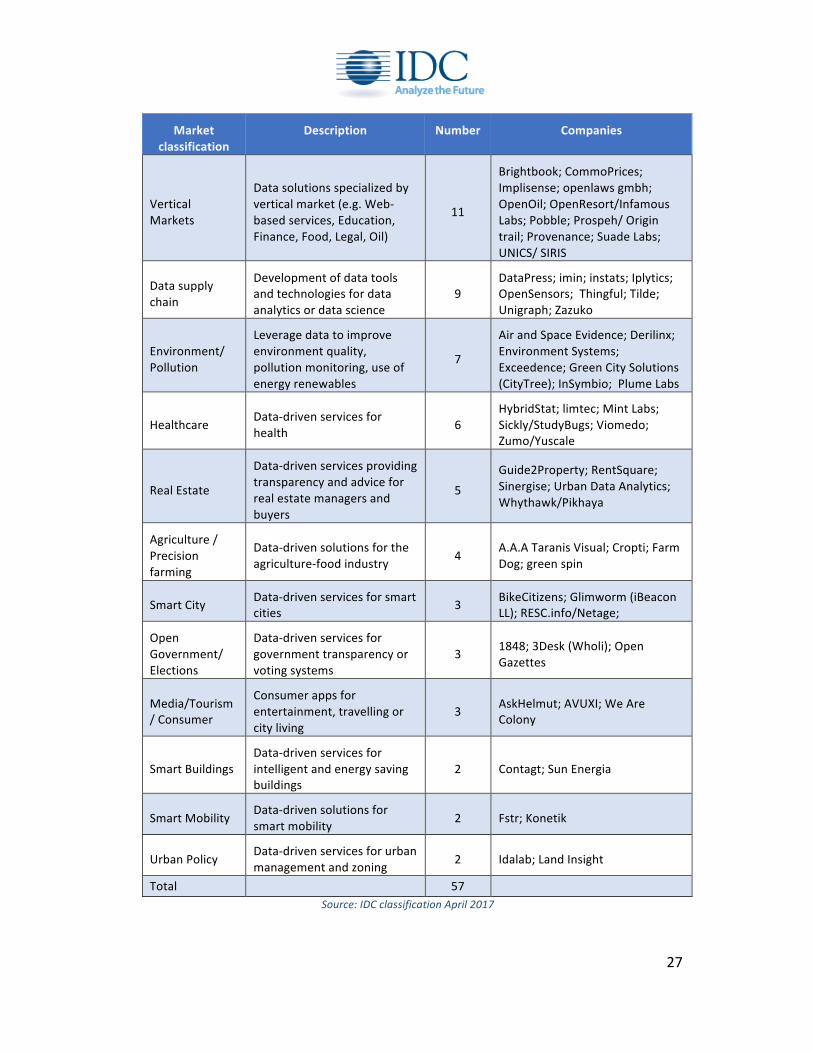

The largestgroupofenterprises (11)developdatasolutionsspecializedbyverticalmarket addressing end-users: ifweadd the6 companies addressinghealthcare, 5active intheRealEstatemarketand4 inagriculturewereachatotalof26ODINEcompanieshelping theEuropean industry adoptdata-driven innovation.We couldalso add to this group the 3 companies developing consumer apps for theentertainment or traveling, as they are focused on end users. Another group ofcompaniesaremorefocusedontechnology:9companiesdeveloptoolsandsolutionsforwhatweseeasbuildingblocksofthedatasupplychain,helpingtoimprovequalityorsolveproblemsindataanalytics.

7 companies address the emerging sustainable economy or low carbon economymarket, with a focus on environmental, energy saving and pollution monitoringsolutions,eitherforconsumers,orpublicauthorities,orotherbusinesses.Asimilarfocus on environmental sustainability is a common element of the 2 companiesdeveloping smart mobility solutions, the 2 companies developing smart buildingsolutions,andthe3companiesdevelopingsolutionsforsmartcities.Finally,thereare3 companies providing data solutions for government transparency or electionsefficiencyand2moresupportingdata-drivenpoliciesintheurbanpolicyfield.Theirfocusonpolicydifferentiatesthemfrom“traditional”ITsolutionsandhighlightstheefforttobringbusinessintelligenceintothepublicsector.

Table4ODINEcompanies’classificationbytargetmarket

8ItisnotbasedonNACE2industryclassification

27

Marketclassification

Description Number Companies

VerticalMarkets

Datasolutionsspecializedbyverticalmarket(e.g.Web-basedservices,Education,Finance,Food,Legal,Oil)

11

Brightbook;CommoPrices;Implisense;openlawsgmbh;OpenOil;OpenResort/InfamousLabs;Pobble;Prospeh/Origintrail;Provenance;SuadeLabs;UNICS/SIRIS

Datasupplychain

Developmentofdatatoolsandtechnologiesfordataanalyticsordatascience

9DataPress;imin;instats;Iplytics;OpenSensors;Thingful;Tilde;Unigraph;Zazuko

Environment/Pollution

Leveragedatatoimproveenvironmentquality,pollutionmonitoring,useofenergyrenewables

7

AirandSpaceEvidence;Derilinx;EnvironmentSystems;Exceedence;GreenCitySolutions(CityTree);InSymbio;PlumeLabs

Healthcare Data-drivenservicesforhealth 6

HybridStat;limtec;MintLabs;Sickly/StudyBugs;Viomedo;Zumo/Yuscale

RealEstate

Data-drivenservicesprovidingtransparencyandadviceforrealestatemanagersandbuyers

5Guide2Property;RentSquare;Sinergise;UrbanDataAnalytics;Whythawk/Pikhaya

Agriculture/Precisionfarming

Data-drivensolutionsfortheagriculture-foodindustry 4 A.A.ATaranisVisual;Cropti;Farm

Dog;greenspin

SmartCity Data-drivenservicesforsmartcities 3 BikeCitizens;Glimworm(iBeacon

LL);RESC.info/Netage;

OpenGovernment/Elections

Data-drivenservicesforgovernmenttransparencyorvotingsystems

3 1848;3Desk(Wholi);OpenGazettes

Media/Tourism/Consumer

Consumerappsforentertainment,travellingorcityliving

3 AskHelmut;AVUXI;WeAreColony

SmartBuildingsData-drivenservicesforintelligentandenergysavingbuildings

2 Contagt;SunEnergia

SmartMobility Data-drivensolutionsforsmartmobility 2 Fstr;Konetik

UrbanPolicy Data-drivenservicesforurbanmanagementandzoning 2 Idalab;LandInsight

Total 57 Source:IDCclassificationApril2017

28

4.3. SocialBenefits

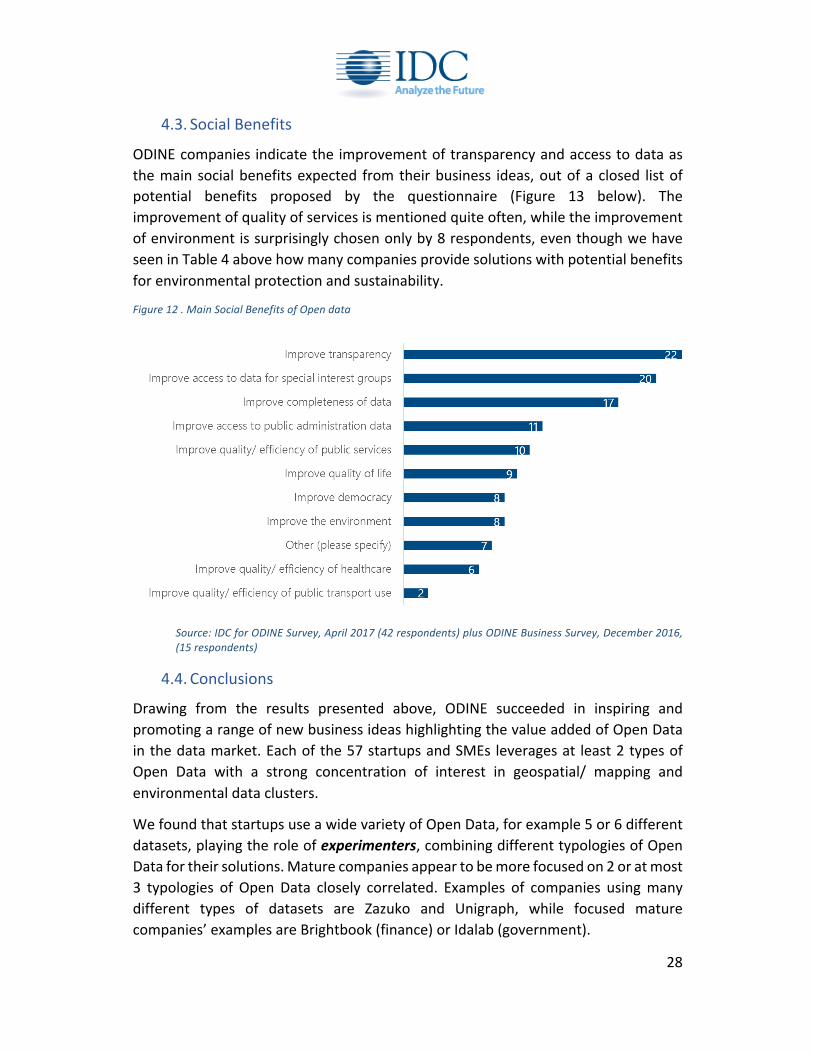

ODINEcompanies indicatetheimprovementoftransparencyandaccesstodataasthemainsocialbenefitsexpected fromtheirbusiness ideas,outofaclosed listofpotential benefits proposed by the questionnaire (Figure 13 below). Theimprovementofqualityofservicesismentionedquiteoften,whiletheimprovementofenvironmentissurprisinglychosenonlyby8respondents,eventhoughwehaveseeninTable4abovehowmanycompaniesprovidesolutionswithpotentialbenefitsforenvironmentalprotectionandsustainability.

Figure12.MainSocialBenefitsofOpendata

Source:IDCforODINESurvey,April2017(42respondents)plusODINEBusinessSurvey,December2016,(15respondents)

4.4. ConclusionsDrawing from the results presented above, ODINE succeeded in inspiring andpromotingarangeofnewbusinessideashighlightingthevalueaddedofOpenDatainthedatamarket.Eachofthe57startupsandSMEs leveragesat least2typesofOpen Data with a strong concentration of interest in geospatial/ mapping andenvironmentaldataclusters.

WefoundthatstartupsuseawidevarietyofOpenData,forexample5or6differentdatasets,playingtheroleofexperimenters,combiningdifferenttypologiesofOpenDatafortheirsolutions.Maturecompaniesappeartobemorefocusedon2oratmost3 typologies of Open Data closely correlated. Examples of companies usingmanydifferent types of datasets are Zazuko and Unigraph, while focused maturecompanies’examplesareBrightbook(finance)orIdalab(government).

29

ThevarietyofbusinessideasdevelopedbytheODINEcompaniesnaturallycomposeanOpenDataecosystemcoveringmany segmentsof thedata value chain,withastronger presence in the more innovative components such as data analytics. AclassificationdevelopedbyIDCbasedontheirvaluepropositionandtargetmarkethighlight how these companies are developing the building blocks of the dataeconomy,helpingtheEuropeanindustrytoadoptdata-driveninnovation.

Overall,26ofODINEcompaniesdevelopsolutionsforverticalmarkets,rangingfromhealthcare(6companies)torealestate(5companies),fromfood-agriculturetoOiland gas. Another priority ofODINE companies is the emerging sustainable or lowcarboneconomy,withseveralcompaniesfocusedonenergysaving,environmentalmonitoring,smartmobility.Aclusterof7companiesaredevelopingclevertechnologysolutionsforthedatavaluechain.

5. EvaluationofBusinessPlans5.1. Approach

Akeyresearchquestionconcernedthe levelofsuccessfulachievementofODINE’sparticipants’ business plans. To investigate it we carried out an evaluation ofindividualbusinessplans,withafocuson:

● Thecompletenessanddepthofplansandbusinessmodels,comparedwithbestpracticestandards;

● The level of validationof businessmodels, basedon the progressmade ingoingtomarketandcapturingearlycustomers’response.

The approach is qualitative, based on our experts’ assessment of the progressachievedbyeachcompanyintheirbusinessmodeldevelopmentandvalidationonthemarket.Thepurposeisnottojudgethequalityoftheassumptionsandforecastmadebycompanies’businessplans,asthesecanonlybevalidatedbytheirsuccess(or not) on themarket, but tomeasure their progress in the period between theoriginaldraftingoftheplanandtheevaluationinMay2017.

Theevidencecollectedwasbasedon:

● Answers to the IDC online survey (40 respondents including 8 directinterviews);

● 10interviewswithnon-fundedcompanies;● Addiitional data from the ODINE business model survey, business plans

documents and other data fromODINE’s repository, for the 40 companiesanalysed.

Intotal,weassessed40ODINEcompaniesand10non-fundedcompanies.

30

5.2. MeasuringAchievement

To compare the level of success of the business plans we designed a set of 4complementaryindicatorsmeasuringthekeyperformanceareasofabusinessplan:

● Value proposition: assessing how much the value proposition has beenprovenbydealingwiththemarket.

● Revenueflow:assessingthelevelofachievementingeneratingrevenuesfromthenewproduct.

● Customer acquisition: assessing the level of achievement in finding arepeatableandscalablewaytoacquirecustomers.

● Financials: assessing the levelof achievement in financing theproductandbusinessdevelopment.

Themeasurementisbasedonascoringscaleof1to4,whereahighscoreindicatesapositive achievement in developing that aspect of the business model. The 4indicators allow assessing both “Product Development” and “CustomerDevelopment”,i.e.,theprocessesdefinedinthepopular“leanstartup”methodology9toiterativelyimprovetheproductandbusinessmodelbygatheringknowledgeofthecustomersandofthetargetmarket,beforeputtinginplaceaconventionalmarketingandsalesstrategy.Table5below,inthe“Definition”column,liststhecriteriausedforattributingscorestotheassessedcompanies,e.g.,ascoreof1in“Valueproposition”has been assigned if the company has not yet validated its value proposition byaccessing the market, either through survey’s, focus groups or through directinvolvementofthefinalcustomer.

Table5AchievementIndicator’sdescription

Score DefinitionValueproposition 1 valuepropositionnotvalidated

2 valuepropositionwithexpert,survey,focusgroupetc.

3 earlyadoptersusingproduct4 recurringsalesonthemarket

Revenueflow 1 hypotheticalbusinessmodel(thecompanyisnotyetgeneratingrevenue)

2 somerevenuesbutnotfromproductsales

9SteveBlank,“ThefourstepstoEpiphany”,2013.

31

3 somerevenuesbutstillinsufficienttogrowtheproductandthecompany

4 revenueflowssufficienttogrow

Customeracquisition 1 Customeracquisitionprocessunderdefinition

2 Definedcustomeracquisitionprocess

3 Customeracquisitionprocessundervalidation

4 Customeracquisitionchannelsandprocessvalidated

Financial 1 Insufficientfundingatthemomenttogoforward

2 Fundingsituationunknown3 Fundingsecureduntil

breakeven4 Breakevenpointreached

Source:IDC,2017

Thescoresassignedtothe40assessedcompaniesplus10non-fundedcompaniesareavailableinanopendataset.

5.3. Mainresults

Figure 13 shows the distribution of scores for the entire population of assessedcompanies.Overall, theODINEcompaniesshowgoodresults,withroughly60%ormorecompaniesscoring3orhigher inall fourAchievementindicators,testifyingagoodprogressinthecorrespondingbusinessmodelarea.

Figure13Achievementindicatorsscoresdistribution(40respondents)

32

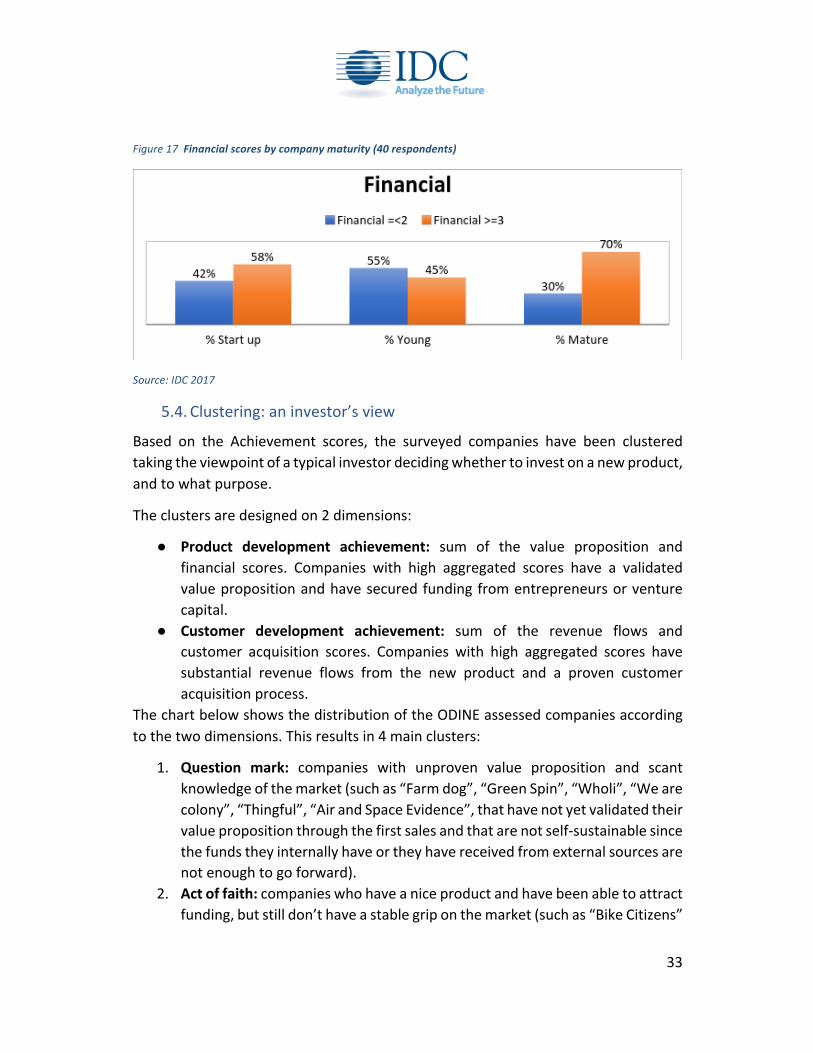

FocusingontheValuepropositionachievementindicator(Figure14),bothstartupsandmature companies arewell positioned, a largemajority of companies havingvalidatedtheirvaluepropositionthroughdirectengagementwithcustomers(earlyadoptersandrecurringsales).AsimilarlevelofachievementcanbeobservedfortheRevenueFlowandCustomerAcquisitionindicators.OntheFinancialindicator(Figure17),maturecompaniesappearasmoreadvanced,whichcanbeexpectedsincetheyhaveanalreadysustainablebusinessthatcansupportnewproductsdevelopment.

Figure14Valuepropositionscoresbycompanymaturity(40respondents)

Figure15Revenueflowscoresbycompanymaturity(40respondents)

Figure16Customeracquisitionscorespointbycompanymaturity(40respondents)

33

Figure17Financialscoresbycompanymaturity(40respondents)

Source:IDC2017

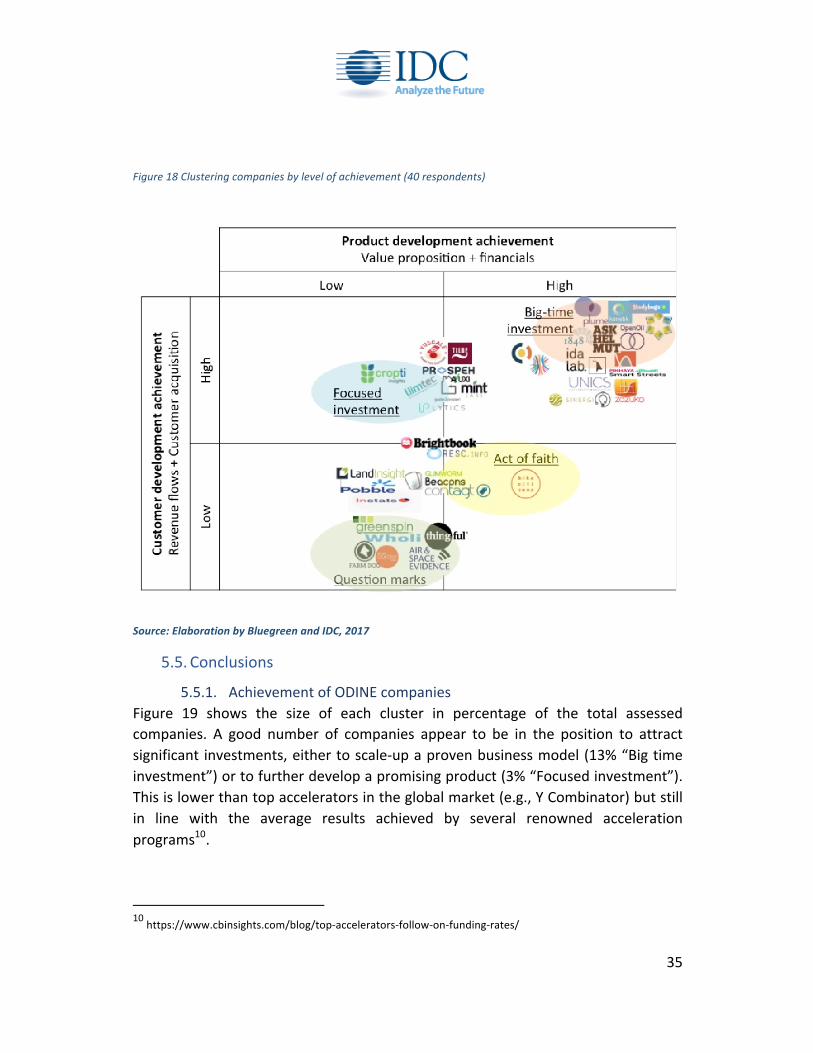

5.4. Clustering:aninvestor’sviewBased on the Achievement scores, the surveyed companies have been clusteredtakingtheviewpointofatypicalinvestordecidingwhethertoinvestonanewproduct,andtowhatpurpose.

Theclustersaredesignedon2dimensions:

● Product development achievement: sum of the value proposition andfinancial scores. Companies with high aggregated scores have a validatedvaluepropositionandhavesecuredfundingfromentrepreneursorventurecapital.

● Customer development achievement: sum of the revenue flows andcustomer acquisition scores. Companies with high aggregated scores havesubstantial revenue flows from the new product and a proven customeracquisitionprocess.

ThechartbelowshowsthedistributionoftheODINEassessedcompaniesaccordingtothetwodimensions.Thisresultsin4mainclusters:

1. Question mark: companies with unproven value proposition and scantknowledgeofthemarket(suchas“Farmdog”,“GreenSpin”,“Wholi”,“Wearecolony”,“Thingful”,“AirandSpaceEvidence”,thathavenotyetvalidatedtheirvaluepropositionthroughthefirstsalesandthatarenotself-sustainablesincethefundstheyinternallyhaveortheyhavereceivedfromexternalsourcesarenotenoughtogoforward).

2. Actoffaith:companieswhohaveaniceproductandhavebeenabletoattractfunding,butstilldon’thaveastablegriponthemarket(suchas“BikeCitizens”

34

that is still defining the customer acquisition process, timing and costs).Investingisan“actoffaith”onhowthepromisingproductwillperformoncebroughtonthemarket.

3. Focused investment: companieswhohaveestablishedsomerevenue flowsand active channels on themarket, but needmore investment to improvetheirvalueproposition(suchas“Cropti”,thatisgeneratingrevenuesbutitisstillvalidatingandrefiningthecustomeracquisitionprocess).Asmallfocusedinvestmentshouldhelpthemdeveloptheirproduct.

4. Big-timeinvestment:companieswhohavebothexcellentproductsandafirmgrip on themarket, producing revenues to enable further growth (such as“PlumeLabs”,“Konetik”,“GreenCitySolutions”,“OpenOil”and“Studybugs”,that have validated their value proposition through recurring sales, havevalidatedthecustomeracquisitionprocessandhavesecuredfundstoreachtheBreakEvenPoint).Largeinvestmentsareneededtoscale-upthebusiness.

Theothercompaniesarenotyetinaclearposition:

- Startupsas“Yuscale”,“Tilde”,“Prospeh”,“Avuxi”,Mint”,“Liimtec”,“IPlytics”and “Guide2Property” are neither Focused Investment nor Big-timeinvestment but they can reach one or the other based on their focus onproduct development, since currently they are validating the valuepropositionthroughearlyadopters,.Inaddition,toworkingonthesalesandmarketingstrategyandarestillvalidatingthecustomeracquisitionprocess.Iftheywillfocusmoreonproductdevelopmentandonhowtogetnewfundsand allocate those already available, they could have more chances tobecameoaBig-timeinvestment.

- Startups as “Commoprices”, “Unigraph”, “Idalab”, “Fstr”, “1848”, “AskHelmut”, “Pikhaya”, “Implisense”, “Hybridstat”, “UNICS”, “Sinergise” and“Zazuko”, are not yet Big-time investment but they are going in the rightdirection to scale-up on themarket, both from the value proposition andfinancialpointofview.

- On the other hand “Land Insight”, “Instats”, “Pobble”, “Brightbook”,“RESC.info”,“Glimworm”and“Contagt”,aresomewhatin-betweentheabovegroups,astheyareinmiddleofatransformationprocess.Theyhavechangedthe revenue business model or customer acquisition process and are stillevaluating thebestway togo forward. Theymust focusbothon customerdevelopmentandproductdevelopmenttohaveachancetoattract furtherinvestments.

35

Figure18Clusteringcompaniesbylevelofachievement(40respondents)

Source:ElaborationbyBluegreenandIDC,2017

5.5. Conclusions

5.5.1. AchievementofODINEcompaniesFigure 19 shows the size of each cluster in percentage of the total assessedcompanies. A good number of companies appear to be in the position to attractsignificant investments,eithertoscale-upaprovenbusinessmodel(13%“Bigtimeinvestment”)ortofurtherdevelopapromisingproduct(3%“Focusedinvestment”).Thisislowerthantopacceleratorsintheglobalmarket(e.g.,YCombinator)butstillin line with the average results achieved by several renowned accelerationprograms10.

10https://www.cbinsights.com/blog/top-accelerators-follow-on-funding-rates/

36

Figure19ODINEcompaniesbylevelofachievement(40respondents)

Source:ElaborationbyBluegreenandIDC,2017

Theanalysisalsoshowsahighshareofcompanieslabeledas“unclearpositioning”.Someofthesecompaniesneedtofurtherexplorethemarketortorefinetheirvalueproposition,butareinagoodpositiontobecomevaluableinvestments.Someothersarestilltestingsignificantchangesontheirbusinessmodel.ThiscanbeexpectedsinceODINEhasselectedideasindifferentstagesofdevelopment.

5.5.2. ODINEimpactFigure20showsODINEbenefitsontheassessedcompanies,groupedbytheirlevelofachievement(clusters).Themostrelevantbenefit is“acceleratingtimetomarket”,highlighted by most companies regardless of their level of achievement. Also,regardless of their achievement, most companies do not recognize “meetinginvestors”asavalue-added.

ThelevelofachievementappearstoberelatedtotheODINEbenefitsasperceivedbythesurveyedcompanies.Thosewhoaremoreadvancedindevelopingtheirproductandbusinessmodel(“Big-timeinvestment”,“Focusedinvestment”..)haveasimilar,high-levelappreciation.Thosewhoarestillbehindintheirdevelopment(“Questionmarks”)showalowerappreciationofallbenefits.

13% 3%

2%

15% 67%

ODINEcompaniesbylevelofachievement(%)

Big-timeinvestment Focusedinvestment ActoffaithQuestionmarks Unclearpositioning

37

Figure20ODINEimpactbylevelofachievement(37respondents)

Source:ElaborationbyBluegreenandIDC,2017

5.5.3. Levelofachievementvs.externalfundingFigure21showsthepercentageofexternalfundingattractedbyODINEcompaniesgrouped by their level of achievement (clusters). There is clearly a relationshipbetween the business model development achievement and the company’sattractiveness to investors (private or public). Only less than a third of “Questionmarks”and“Unclearpositioning”companieshavereceivedexternalfunding,whilecompaniesintheothercategorieshaveinlargemajority(over80%)beenfundedbyexternalsourcesinadditiontoODINE.

1.8 2 21.3

2.43.8 4

3 2.844.4 4

54 44.2 4

5

3.5 3.53.22

5

2.53.2

5

0 0 0

4.3

Big-timeinvestment

Focusedinvestment

Actoffaith Questionmarks Unclearpositioning

ODINEimpactMeetingnewinvestors

Improvingthebusinessidea

Acceleratingtimetomarket

Improvingtheteam(skills,composition)

Meetingandengagingwithpotentialcustomers

Other

38

Figure21Externalfundingbylevelofachievement(40respondents)

Source:ElaborationbyBluegreenandIDC,2017

6. ODINEImpactsongrowth6.1. Introduction

IDCdevelopedtwodifferentapproachestoassessthemarketimpactofODINE.Thetwoapproaches–amarketmodelononesideandasurvey-basedmodelontheotherside–havebeenreconciledinafinalstagetoprovideasinglefullyconsistentandsolidviewofODINEimpacts.

Therefore,thischapterhasthefollowingmainobjectives:

● ToassessthepotentialmarketimpactsofODINE,measuredintermsofthenumberofcompaniessurvivingby2020,theirpotentialrevenues,thenumberofemployees,andtheirpotentialusers;

● Topresentthemainassumptionsdrivingtheforecastestimates;● To discuss the counterfactual scenario, considering the potential

consequencesifthe57selectedcompanieswouldhavenotbeenpartoftheaccelerationprogramandhadnotreceivedthe5.6€Minvestments.

Morespecificallythischapterisdividedintwopartspresentingthemainresultsasfollows:

● Estimateoffundedinitiatives'revenuesto2020.Thispresentstheresultsofthe analysis that calculates the estimated revenues of the ODINE selectedcompanies.Thismodelprojectstherevenuesto2020.Thispartalsoincludestheestimateofthenumberofemployees.

80% 100% 100% 33% 37%

20% 0% 0% 67% 63%

Big-timeinvestment

Focusedinvestment

Actoffaith Questionmarks Unclearpositioning

ExternalfundingYes No

39

● Estimateofthenumberofpotentialbusinessandconsumerusersattractedbytheselectedcompanies.Buildingontheresultsoftherevenueforecast,this model estimates how many businesses and/or consumers will beattracted.

Themodelcoverstheperiodfrom2016to2020.

6.2. Methodology

This section explains the assumptions behind IDCmodels and themethodologicalapproach IDC followed to estimate the total revenues that will be generated byfundedinitiativesupto2020.

Datasourcesthathavebeenleveragedinclude:

● IDCforODINESurvey(April2017);● ODINEbusinessmodelsurvey(December2016);● DataandinformationaboutindividualcompaniesmadeavailablebyODINEor

publiclyavailable(e.g.websites);● RelevantdatafromEurostatandotherpublicsources(e.g.deathrates);● Available literature (forexampleotherEuropeanaccelerators’ reports)was

usedasabenchmark.Estimatingthetotalrevenuegeneratedbyselectedcompanies iscomplexasmanyvariables must be considered both in terms of their characteristics and rate ofdevelopment(e.g.marketentryyear,numberofteammembers,typeofproposedsolution, etc.) and in terms of their possible success once on the market. Themethodologyisarticulatedintwomainsteps:

● Baselineassumptions:understandingthenatureoffundedinitiatives(step1);● Forecastassumptions:Estimatingtheirfuturetrendsandlikelinessofsuccess

(step2).

6.2.1. Step1:BaselineAssumptions–MarketModelFirstofallweneedtounderstandwhotheselectedcompaniesareandwhatdotheydo.Todothisweleveragedourmappinganalysis(seeChapter2)andtheresultsofthe IDC for ODINE Survey (42 compiled questionnaires). In particular, ourmethodologicalapproachbuildsonthefollowingindicators:

● Numberofselectedinitiatives(referencepopulation);● MarketEntryyearforeachinitiative;● Distribution of selected initiatives by type of offering, number of team

members,andgeographicalscope;

40

● Averagerevenuegeneratedbyasingle initiativeduring its firstyearonthemarket.

ReferencePopulationODINEselected57companiestobeacceleratedoutof1,176applicationsfrom731differentcompanies(445re-submissions).Thissamplecoversrounds2to8,withoutfilteringre-submissions.

MarketEntryYearAnalyzingthe57selectedcompanieswefoundthatthemajority(31companies)arestart-up,whichwereborn in2014or later.There is thenagroupof15companieswhichwecalled"Young"whichenteredthemarketbetween2012and2013.Thereisalsoasmallergroupofcompanies(11)whichwerebornin2011orearlier;wecalledthem "Mature" companies. Therefore, the population of companies is not onlycomposedofstart-upsbornwiththeprogramme,butalsoofyoungandmorematureSMEsrelyingontheODINEopportunitytoaccelerateproductdevelopmentandboosttheirbusiness.

ProfileoffundedinitiativesOtherkeyinputsforthemodelconcernthetechnologyofferingoffundedinitiatives,theteamsizeandwhichmarkettheywilladdressandtheirgeographicalscope.

TechnologyofferingAsillustratedinthemappinganalysis(§2.10),wesegmentedtheselectedcompaniesinthreemainclustersdependingonthetypeoftechnologyoffering:purelysoftwaresolutions,hardwarewithembeddedsoftwaresolutions,andweb-basedservices.Thissegmentationisextremelyimportanttoappropriatelyestimaterevenuegenerationoverthenextfewyears.Intermsofbusinessmodelsandrevenuegrowthwehaveadoptedthefollowingassumptions:

● Initiatives offering purely software solutions do not require high capitalinvestmentsandtheirlikelyrevenuesareclosetotheaverageofthereferencesample,withagradualgrowthdynamic.

● Most initiatives offering hardware and software solutions do not producedirectly thehardware components (sensors, devices, screens, etc.) butbuythemfromsub-suppliers.Thisrequiresahigherinitialinvestmentcomparedtopurelysoftwareplayers.Whenweconsiderrevenues(notprofits),thishasan impact as theywill also resell thehardwarewith amark-up. Therefore,companies offering hardware and software solutions are expected to havehigherrevenuesthantheaveragesampleatleastinthefirstyears.

41

● Web-basedservicescompanieshavedifferentcharacteristicswithrespecttotheother twoclusters.Their revenue flowsmaycome fromamixof sales,and/or subscription, and/or advertising, or other sources (e.g. freemiummodels).Basedonempiricalresearch,thistypeofcompaniestendstohavelowaveragerevenuesintheirfirstyears(whentheyarefocusedonincreasingthevolumeofusers,ratherthanrevenues)buttheymaytakeoffveryquicklyoncetheyreachacriticalmassofusers.

NumberofTeammembersThe number of teammembers is closely correlated with revenues. The followingassumptionshavebeenverifiedthroughtheIDCforODINEsurveyandused:

● Smaller teamswith1-2membersgenerate loweraverage revenues in theirfirst years, although higher growth rates, if successful (this as newemploymentwillhaveastrongerimpactintermsofteamrevenuesgrowthon1-2membersteamwithrespecttolargerteamofmorethan10members).

● Theteamdimensionisalsocorrelatedwithpotentialdeathrates.Greenfieldinitiativesstartingfromscratch,with1-personteam,arelikelytosufferhigherdeath rates than youngenterpriseswith a small partnershipbutwhohavealreadysurvivedacoupleofyears.

MarkettargetsTheprimaryindustrysectortargetedbytheselectedcompaniesinitiativeswasusedinthemodelasanadditional factor influencingtherevenuesdynamics(leveragingIDC’sverticalmarketsknowledgeanddemandforecasts).

Themainassumptionswere:

● Selected companies addressing the privatemarket grow faster than thoseaddressingthepublicsector(wherepublicprocurementrequiresalongleadtimeandallkindsofreferencesandguaranteesoffinancialsolidity);

● SelectedcompanieswithaB2BorB2B2CbusinessmodelexperiencehigherbarrierstoentranceandamoregradualgrowthpaththanpureB2Cinitiatives,becausetheyneedtogaintheirbusinesscustomers’trustandinteractwithcomplexsupplychains;however,oncepasttheearlyphase,theyenjoy lessfluctuationsinrevenuesandgreatersolidity;

● Selected companieswith a B2C businessmodelmay take off quickly (withrapidlygrowingrevenues)iftheyachievevisibilitybutmaysufferfromboomandbustcycles,dependingoncustomerloyaltyandtheircapabilitytoreachacriticalmassofuserstriggeringpositivenetworkeffects.

42

● WehavealsoconsideredthedifferentpropensityofindustrysectorstoadoptthetypeofinnovativetechnologiesusedbytheselectedcompaniessuchasIoT,3Dprinting,softwareapplicationcategory.

GeographicalscopeLastly(butnotleast),thegeographicalscopehastobeconsidered,sincethisindicatesthepropensity todevelopan aggressivemarket strategy and therefore to aim forhighergrowth.This indicatorwassourcedfromthe IDCforODINEsurveywiththefollowingassumptions:

● Selected companies declaring to focus on the local or nationalmarketwillgeneratelessrevenuesthanaverageandgrowmoreslowly;

● SelectedcompaniesaddressingmorethanonecountryortheEUortheglobalmarketwillgrowfasterandgeneratehigherrevenuesthanaverage.

Average1styearrevenueThebaselinestartingpointforthemodelistheestimateof1styearaveragerevenuesegmentedbythemain3 initiativeclustersand2categoriesofgeographicalscope(national/international).Thisisusedasaninputforthemodel.

Estimating the average first year (on-the-market) revenues is not that easy, inparticularasmanyfundedinitiativesintheirfirstyearcouldalsohavenorevenuesandjustsurvivethankstofundraising.Afteranalyzingallavailabledataweestimatedthatonaverageselectedcompanieswouldgenerateapproximately€7,500pereachteammemberintheirfirstyearoflife.Thisisbasedontheassumptionthatformanyfunded initiatives themain sourceofmoney in the 1st yearwill be external fundsobtainedfrominvestors.

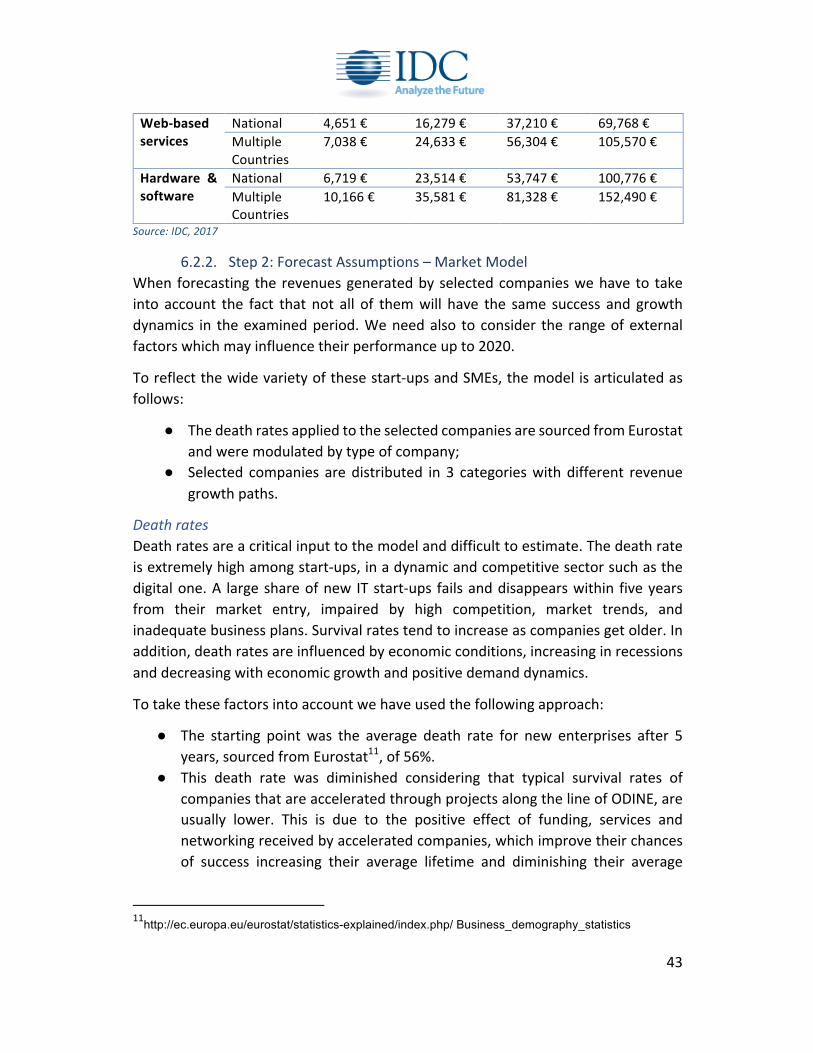

Thisvaluepartiallychangeswithrespecttotheofferingclusterweconsiderandthegeographicalscope,ashighlightedabove.Moreover,amultiplierhastobeappliedtotake intoaccount thedimensionof the team (the larger the team, thehigher therevenuesgeneratedduringitsfirstyearonthemarket).Theindustrysectortargetsarenotassumedtohaveanimpactontheaverage1styearrevenuebutmoreonthegrowthratesduringthenextfewyears(seenextsection).TheTablebelowshowsthe1styearaveragerevenueestimatesappliedtoeachcategory.

Table6Selectedcompaniesaveragerevenuesinthe1styear

TypeofOffering

GeographicalScope

NumberofTeamMembers1 2to5 6to10 10+

Puresoftware

National 5,685€ 19,897€ 45,478€ 85,272€MultipleCountries

8,602€ 30,107€ 68,816€ 129,030€

43

Web-basedservices

National 4,651€ 16,279€ 37,210€ 69,768€MultipleCountries

7,038€ 24,633€ 56,304€ 105,570€

Hardware &software

National 6,719€ 23,514€ 53,747€ 100,776€MultipleCountries

10,166€ 35,581€ 81,328€ 152,490€

Source:IDC,2017

6.2.2. Step2:ForecastAssumptions–MarketModelWhen forecasting the revenuesgeneratedbyselectedcompanieswehave to takeinto account the fact that not all of themwill have the same success and growthdynamics in theexaminedperiod.Weneedalso toconsider the rangeofexternalfactorswhichmayinfluencetheirperformanceupto2020.

Toreflectthewidevarietyofthesestart-upsandSMEs,themodelisarticulatedasfollows:

● ThedeathratesappliedtotheselectedcompaniesaresourcedfromEurostatandweremodulatedbytypeofcompany;

● Selected companies aredistributed in 3 categorieswithdifferent revenuegrowthpaths.

DeathratesDeathratesareacriticalinputtothemodelanddifficulttoestimate.Thedeathrateisextremelyhighamongstart-ups,inadynamicandcompetitivesectorsuchasthedigitalone.A largeshareofnew ITstart-ups failsanddisappearswithin fiveyearsfrom their market entry, impaired by high competition, market trends, andinadequatebusinessplans.Survivalratestendtoincreaseascompaniesgetolder.Inaddition,deathratesareinfluencedbyeconomicconditions,increasinginrecessionsanddecreasingwitheconomicgrowthandpositivedemanddynamics.

Totakethesefactorsintoaccountwehaveusedthefollowingapproach:

● The starting pointwas the average death rate for new enterprises after 5years,sourcedfromEurostat11,of56%.

● This death rate was diminished considering that typical survival rates ofcompaniesthatareacceleratedthroughprojectsalongthelineofODINE,areusually lower. This is due to the positive effect of funding, services andnetworkingreceivedbyacceleratedcompanies,whichimprovetheirchancesof success increasing their average lifetime and diminishing their average

11http://ec.europa.eu/eurostat/statistics-explained/index.php/ Business_demography_statistics

44

deathrates.LiteraturefromotherEuropeanacceleratorsonaveragesurvivalratesofacceleratedcompanieswasusedasabenchmark.

● Thisresultedinanaveragesurvivalrateof74%.

Selectedcompanies’growthtrajectoriesGrowthtrajectoriesovertheperiodto2020canbethereforeclassifiedinto3maingroupsasfollows:

● Onegroupofcompanieswilleventuallyfail.● Another group includes those companies thatwill remain standing after 5

years,by2020.Thesurvivorsareenterprisesthatwillhaveapositiveimpactonthemarketandwhoserevenueswillgrowacrosstheyears.Themajorityofthem will show a regular trend across the years both in terms of yearlyrevenuesincreaseandnewhiredemployeesandtendtowardsstability,eveniftheydifferintermsofwhentheirpeakofgrowthwillbe.

● Finally,weexpectthataminorpercentageofcompanies(potentiallyveryhighachievers,the“stars”ofourpopulation)willstartveryslowduringthefirst2-3 years andwill then take-off,with rapidly increasing revenueswhichmaycontinueclimbingfastbeyond2020,aftertheperiodcoveredbythemodel.Thesehighachieverscanbefoundmoreofteninthewebservicesclusterofselected companies, because of their focus on new, emerging servicesmarkets.Manywebservicesduringtheirearlylifefocusonincrementingtheirusers' database with no direct effect on revenues, postponing profitsgenerationandrevenuesexplosionatalaterstage.Arecentfamousexampleisrepresentedbythecar-sharingserviceBlaBlaCar.Duringitsfirstyears,whilepeople were becoming familiar with the service and word of mouth wasattractingmoreandmoreusers,theonlyincomewasrepresentedbyfundingfromprivate investors. Just in a secondmoment,once that thenumberofusers was considerable, the business model moved to a transaction feesapproach (the service takes a percentage of the transactions done on theserviceplatform)creatinganewrevenuesstream.

6.2.3. Survey-BasedModelIDCconductedasurveyinwhichmostoftheselectedcompaniesprovideddataontheir revenue generation, on the number of people they employ and on theirexpectedgrowthrates,amongotherinformation.Thisdatawasanalyzed,elaboratedandusedbyIDCtocheckandvalidatethemarketmodeloutput.

Therefore,theimpactassessmentandthemodelresultsshowninthenextchapterare fullyalignedwith IDCelaborationof IDCforODINEsurveydataasoutputdatafromthe2approaches,whichwereextremelysimilar,havebeenreconciled.

45

6.3. Impactassessment

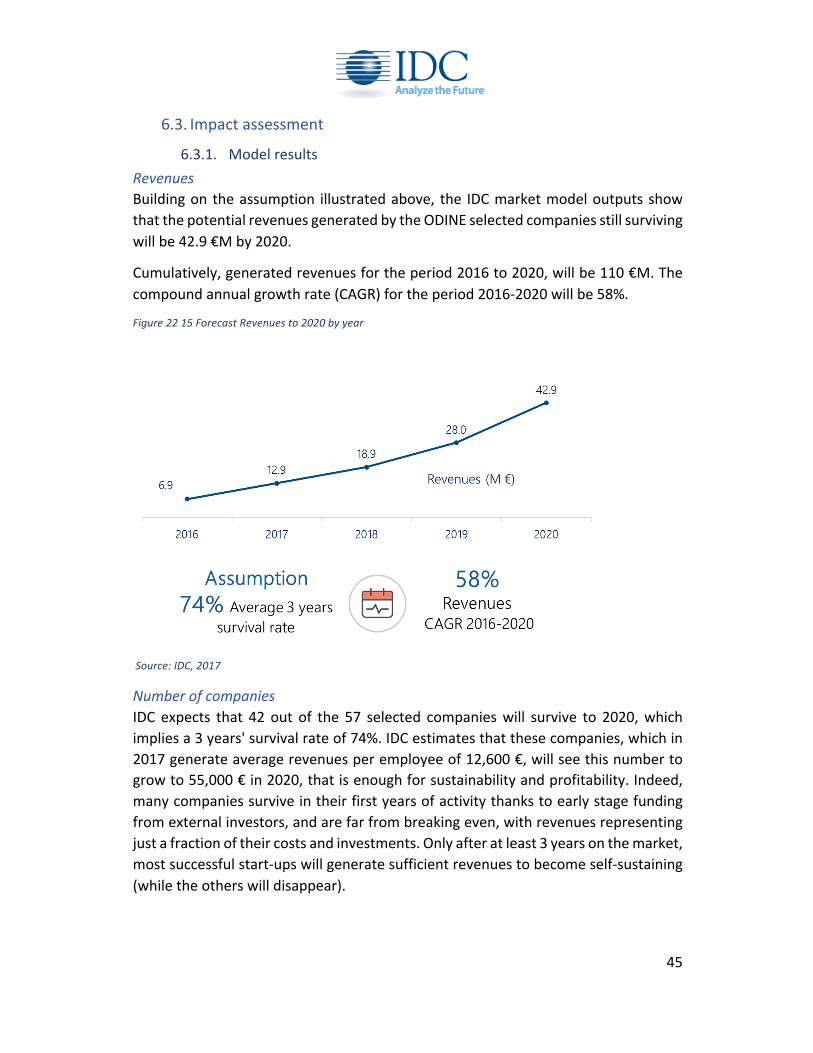

6.3.1. ModelresultsRevenuesBuildingontheassumption illustratedabove, the IDCmarketmodeloutputsshowthatthepotentialrevenuesgeneratedbytheODINEselectedcompaniesstillsurvivingwillbe42.9€Mby2020.

Cumulatively,generatedrevenuesfortheperiod2016to2020,willbe110€M.Thecompoundannualgrowthrate(CAGR)fortheperiod2016-2020willbe58%.

Figure2215ForecastRevenuesto2020byyear

Source:IDC,2017

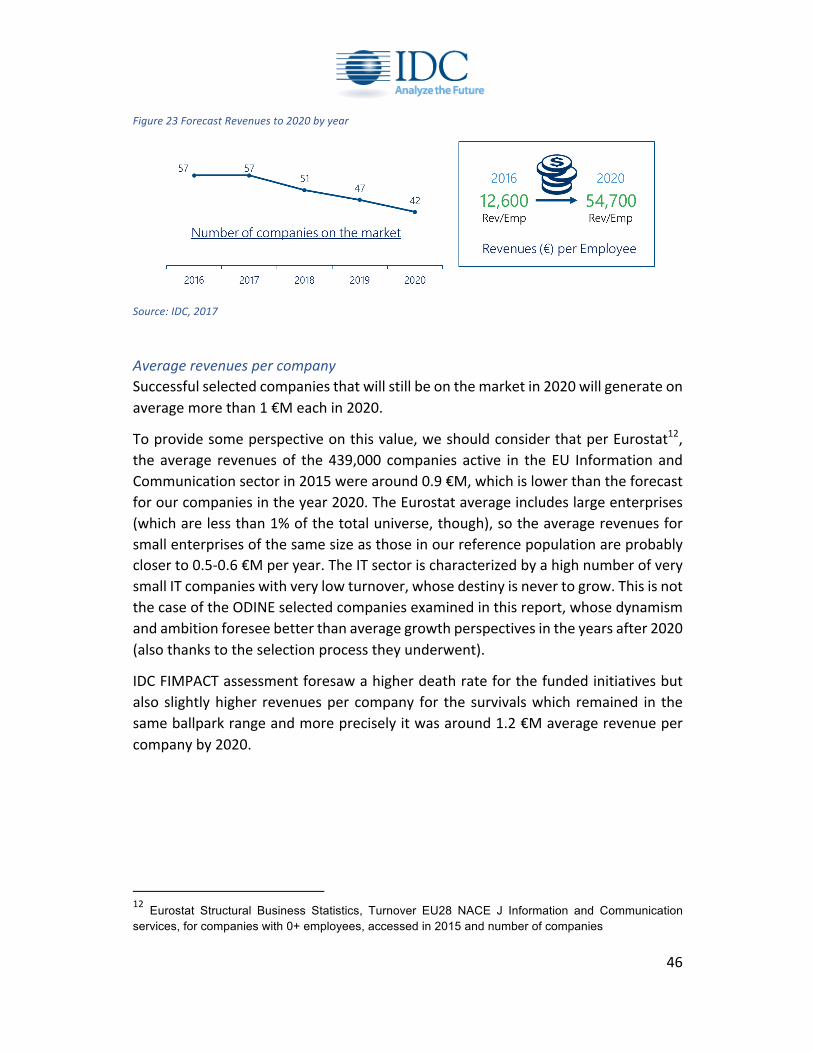

NumberofcompaniesIDC expects that 42 out of the 57 selected companieswill survive to 2020,whichimpliesa3years'survivalrateof74%.IDCestimatesthatthesecompanies,whichin2017generateaveragerevenuesperemployeeof12,600€,willseethisnumbertogrowto55,000€in2020,thatisenoughforsustainabilityandprofitability.Indeed,manycompaniessurviveintheirfirstyearsofactivitythankstoearlystagefundingfromexternalinvestors,andarefarfrombreakingeven,withrevenuesrepresentingjustafractionoftheircostsandinvestments.Onlyafteratleast3yearsonthemarket,mostsuccessfulstart-upswillgeneratesufficientrevenuestobecomeself-sustaining(whiletheotherswilldisappear).

46

Figure23ForecastRevenuesto2020byyear

Source:IDC,2017

AveragerevenuespercompanySuccessfulselectedcompaniesthatwillstillbeonthemarketin2020willgenerateonaveragemorethan1€Meachin2020.

Toprovidesomeperspectiveonthisvalue,weshouldconsiderthatperEurostat12,the average revenuesof the439,000 companies active in the EU Information andCommunicationsectorin2015werearound0.9€M,whichislowerthantheforecastforourcompaniesintheyear2020.TheEurostataverageincludeslargeenterprises(whicharelessthan1%ofthetotaluniverse,though),sotheaveragerevenuesforsmallenterprisesofthesamesizeasthoseinourreferencepopulationareprobablycloserto0.5-0.6€Mperyear.TheITsectorischaracterizedbyahighnumberofverysmallITcompanieswithverylowturnover,whosedestinyisnevertogrow.ThisisnotthecaseoftheODINEselectedcompaniesexaminedinthisreport,whosedynamismandambitionforeseebetterthanaveragegrowthperspectivesintheyearsafter2020(alsothankstotheselectionprocesstheyunderwent).

IDCFIMPACTassessmentforesawahigherdeathrateforthefundedinitiativesbutalso slightlyhigher revenuesper company for the survivalswhich remained in thesameballparkrangeandmorepreciselyitwasaround1.2€Maveragerevenuepercompanyby2020.

12 Eurostat Structural Business Statistics, Turnover EU28 NACE J Information and Communication services, for companies with 0+ employees, accessed in 2015 and number of companies

47

Figure24Averagerevenuespercompanyto2020byyear

Source:IDC,2017

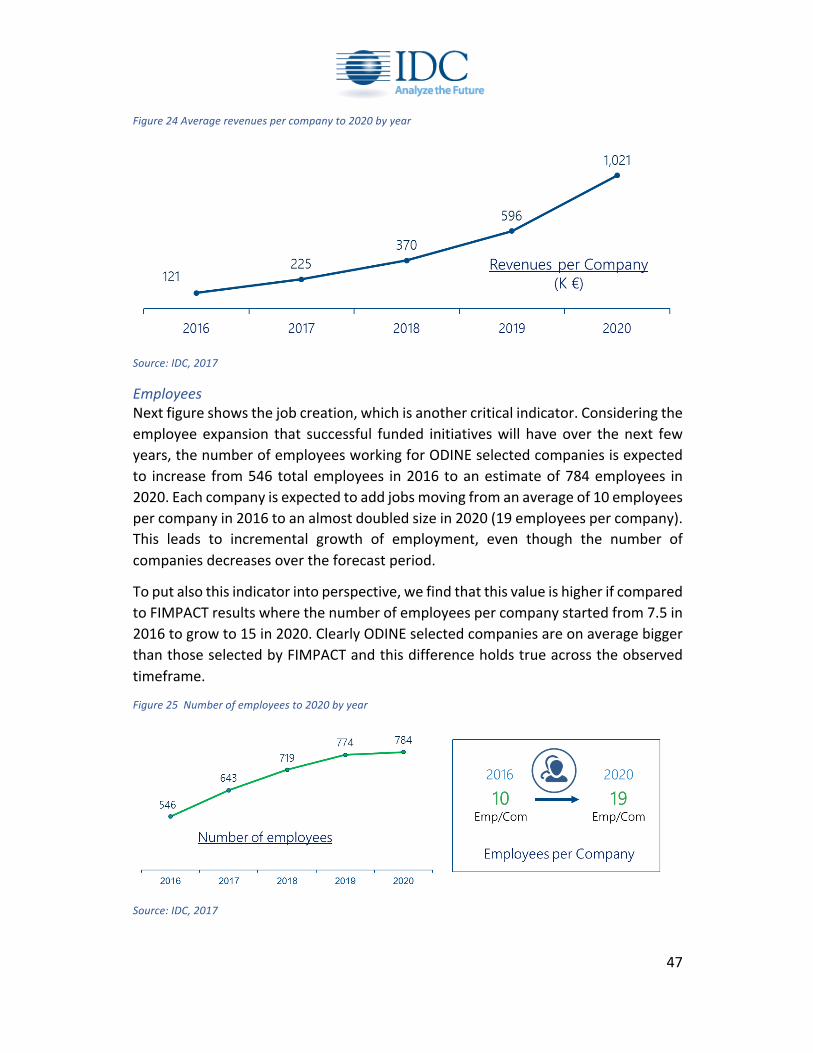

EmployeesNextfigureshowsthejobcreation,whichisanothercriticalindicator.Consideringtheemployeeexpansion that successful funded initiativeswill haveover thenext fewyears,thenumberofemployeesworkingforODINEselectedcompaniesisexpectedto increase from546 totalemployees in2016 toanestimateof784employees in2020.Eachcompanyisexpectedtoaddjobsmovingfromanaverageof10employeespercompanyin2016toanalmostdoubledsizein2020(19employeespercompany).This leads to incremental growth of employment, even though the number ofcompaniesdecreasesovertheforecastperiod.

Toputalsothisindicatorintoperspective,wefindthatthisvalueishigherifcomparedtoFIMPACTresultswherethenumberofemployeespercompanystartedfrom7.5in2016togrowto15in2020.ClearlyODINEselectedcompaniesareonaveragebiggerthanthoseselectedbyFIMPACTandthisdifferenceholdstrueacrosstheobservedtimeframe.

Figure25Numberofemployeesto2020byyear

Source:IDC,2017

48

MomentumThissectiondealswiththenumberofusersoftheselectedcompaniesin2016andprojectionsto2020.

Themomentumanalysishasbeendividedinto2parts.

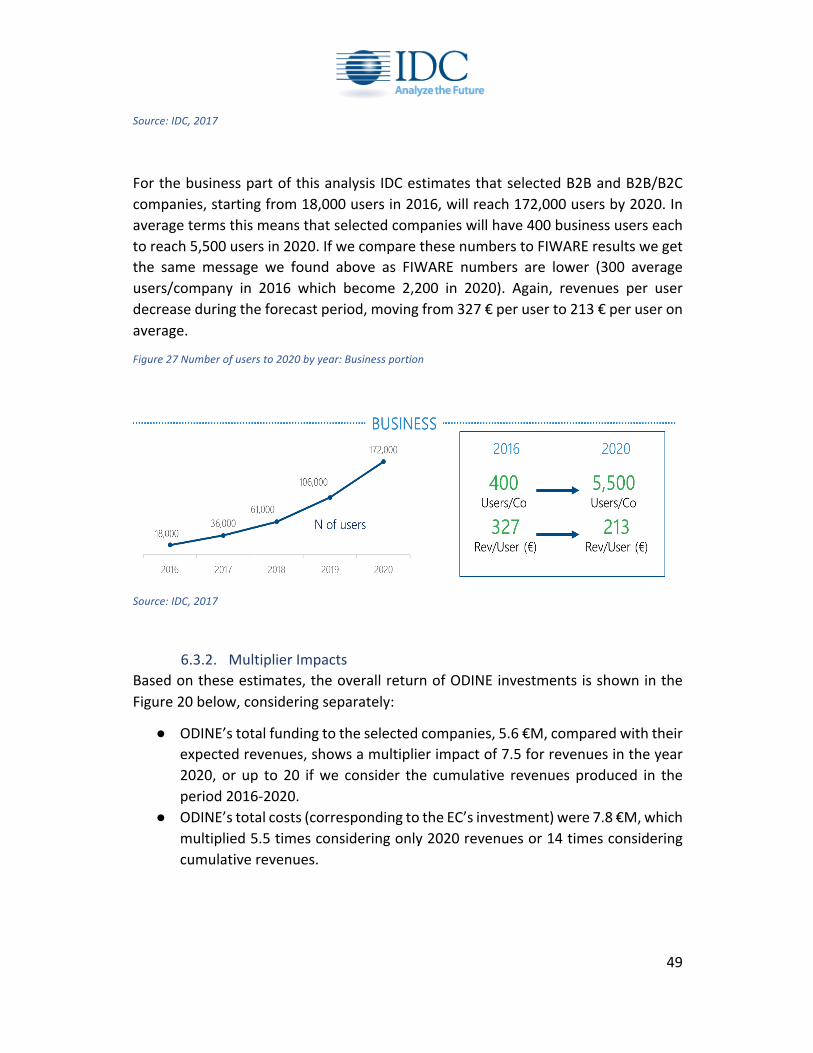

The first one is related to consumers and includes solely B2C companies andcompanies that are both B2C and B2B (32 companieswere considered as B2C orB2C/B2B).Forthelatterones,weextrapolatedtheirB2Cportionofusers.

Similarly, the second part of the analysis dealswith B2B companies and B2B/B2Ccompanies for their sole B2B portion (43 companies were considered as B2B orB2C/B2B).