Embed Size (px)

Citation preview

Macroeconomic and Financial Management Institute of Eastern and Southern Africa

IMPACT OF BASEL II IMPLEMENTATION: A CASE

STUDY ON ZAMBIA

Author: Lyness Phiri - Mambo

Supervisor: Dr. Blessing Mudavanhu

February, 2015

A Technical Paper Submitted in Partial Fulfillment of the Award of MEFMI

Fellowship

Abstract

The Basel capital framework is the globally accepted capital adequacy standard. This

paper investigates the impact of Basel II implementation on the financial sector in Zambia.

The paper analyses the capital adequacy position of banks in Zambia before and after

implementation of Basel II. Banks are put into three peer groups and an in-depth study of

the impact of implementation of Basel II on each peer group is carried out. Secondly, the

study reviewed developments, post the global financial crisis of 2007 in order to assess

implications for the local banking sector and the Macroeconomic and Financial

Management Institute of Eastern and Southern Africa (MEFMI) member countries and

develop a strategy for future adoption or implementation of the revisions made to the Basel

Capital Accord under Basel 2.5 and Basel III where necessary. In this regard the study

develops a living Dashboard highlighting the progress that MEFMI member countries have

made in adopting the Basel capital frameworks, which will help the Institute to focus and

tailor their capacity building initiatives accordingly.

Table of Contents

Abstract ........................................................................................................................................................ 0

List of Tables ............................................................................................................................................... 0

Acknowledgements .................................................................................................................................... 0

1. Introduction .......................................................................................................................................... 1

1.1. Structure of the Zambian Banking Sector .............................................................................. 1

1.2. Minimum Capital Requirements ............................................................................................... 3

1.3. Evolution of Basel Capital Framework .................................................................................... 5

1.4. Implementation of Basel II: Practical Considerations ........................................................... 7

1.5. Implementation of Basel II in Zambia ...................................................................................... 8

1.6. Problem Statement .................................................................................................................... 9

1.7. Objectives of the Paper ............................................................................................................. 9

1.8. Significance of Study ............................................................................................................... 10

1.9. Limitations of the Study ........................................................................................................... 11

1.10. Research Questions ............................................................................................................ 11

2. Literature Review ............................................................................................................................. 13

2.1. Background ............................................................................................................................... 13

2.2. Pre-Basel Capital Framework ................................................................................................ 14

2.3. BCBS Core Principle for Effective Supervision ................................................................... 16

2.4. Basel I Capital Framework - Overview .................................................................................. 17

2.5. Revised Capital Framework - Basel II ................................................................................... 18

2.5.1. Pillar I ..................................................................................................................................... 20

2.5.2. Pillar II .................................................................................................................................... 20

2.5.3. Pillar II - Shared Responsibility .......................................................................................... 21

2.5.4. Pillar II Governing Principles .............................................................................................. 21

2.5.5. How Pillar II Reinforces Pillar I ........................................................................................... 25

2.5.6. Risks That Might not be Captured under Pillar I .............................................................. 25

2.5.7. Pillar III Market Discipline .................................................................................................... 26

2.6. Criteria for Determining Basel II Banks ................................................................................. 26

2.7. Rationale for Implementing Basel II ...................................................................................... 27

2.8. Basel II Implementation in Zambia ........................................................................................ 27

2.8.1. Advantages of Implementation of Basel II ........................................................................ 27

2.8.2. Expected Value Addition of Adaptation of Basel II for Banks ........................................ 28

2.8.3. Advantages for the Supervisor ........................................................................................... 29

2.8.4. Weakness and challenges of Basel II ............................................................................... 30

2.9. Preferred Basel II Pillar 1 Approaches for Zambia .............................................................. 30

2.9.1. Simplified Standardized Approach for Credit Risk .......................................................... 31

2.9.2. Credit Risk Mitigation ........................................................................................................... 32

2.10. Assessment of Risk Weights for Credit Risk under Basel II in Zambia ....................... 33

2.11. Basic Indicator Approach (BIA) for Operational Risk ...................................................... 34

2.11.1. Migration to Standardised Approach for Operation Risk ............................................ 34

2.12. Standardized Measurement - for Market Risk ................................................................. 34

2.13. Supervisory Review Process .............................................................................................. 35

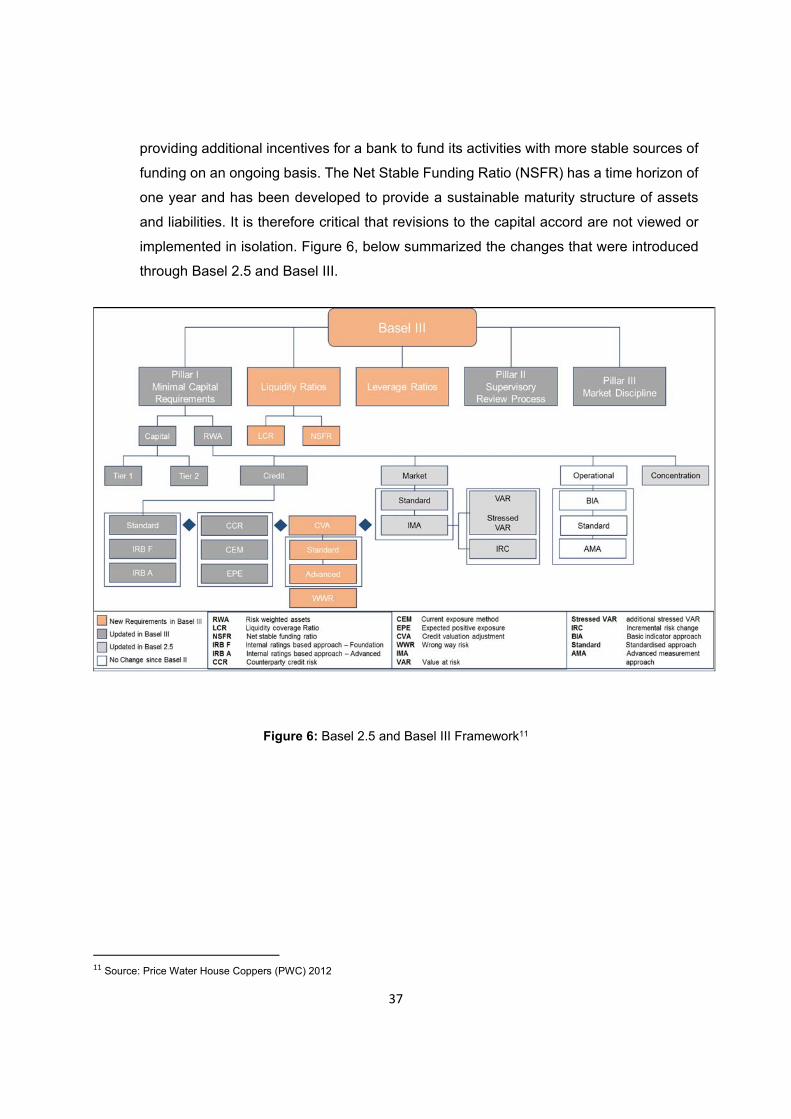

2.14. Basel 2.5 and Basel III Framework .................................................................................... 35

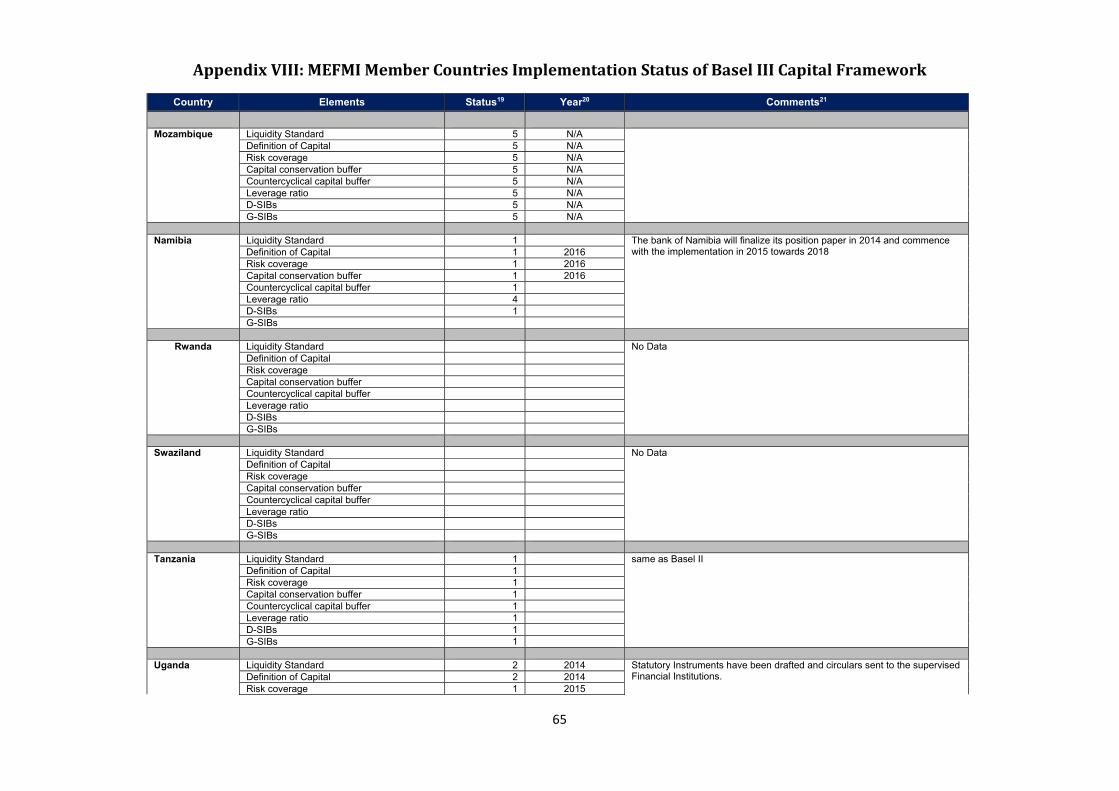

2.15. Progress on Basel II Implementation in MEFMI Member States .................................. 38

3. Methodology ...................................................................................................................................... 40

3.1. Introduction ................................................................................................................................ 40

3.2. Data Description ....................................................................................................................... 41

3.2.1. Distribution of Assets in Banking Sector ........................................................................... 41

3.2.2. Tier 1 banks - banks with assets > ZMW5 bn .................................................................. 42

3.2.3. Tier 2 banks (banks with assets ≥ ZMW1 bn but less than ZMW5 bn) ........................ 43

3.2.4. Tier 3 banks (Banks with Assets < ZMW1 billion) ........................................................... 43

4. Results ............................................................................................................................................... 45

4.1. Distribution of Risk Weighted Assets for Tier 1 Banks ....................................................... 45

4.2. Impact of Basel I Pillar I on Tier 1 Banks .............................................................................. 45

4.3. Distribution of Risk Weighted Assets for Tier 2 Banks ....................................................... 46

4.4. Impact of Basel I Pillar I on Tier 2 banks .............................................................................. 46

4.5. Distribution of Risk Weighted Assets for Tier 3 Banks ....................................................... 47

4.6. Impact of Basel I Pillar I on Tier 3 banks .............................................................................. 48

5. Conclusion and Recommendations ............................................................................................... 50

Bibliography .............................................................................................................................................. 52

List of Figures

Figure 1: Total Assets and Liabilities of the Banking Sector (2011-2013) ..................................... 2

Figure 2: Regulatory Capital, RWA and Capital Adequacy Ratio (2011-2013) ............................. 2

Figure 3: Evolution of Basel Capital Framework ............................................................................ 5

Figure 4: Basel I Capital Accord Architecture .............................................................................. 18

Figure 5: Three Mutually Enforcing Pillars ................................................................................... 19

Figure 6: Basel 2.5 and Basel III Framework ............................................................................... 37

Figure 7: Assets Distribution ......................................................................................................... 42

List of Tables

Table 1: Basel I Asset Classification .............................................................................................. 5

Table 2: Minimum Capital Adequacy Ratios .................................................................................. 6

Table 3: Evolution of Basel Capital Framework ............................................................................. 7

Table 4: ECA Consensus Risk Scores ......................................................................................... 32

Table 5: ECA Consensus Risk Scores ......................................................................................... 32

Table 6: Tier 1 Asset Composition ............................................................................................... 42

Table 7: Tier 2 Assets Composition ............................................................................................. 43

Table 8: Tier 3 Asset Composition ............................................................................................... 44

Table 9: Tier 1 Banks RWA Distribution ....................................................................................... 45

Table 10: Tier 2 Banks RWA Distribution ..................................................................................... 46

Table 11: Tier 3 Banks RWA Distribution ..................................................................................... 48

Acknowledgements

I would like to thank my mentor, Dr. Blessing Mudavanhu for the guidance and support

given during the course of my research.

I would like to extend my sincere gratitude to the Bank of Zambia management their

support throughout my MEFMI fellowship program. I wish to also extend special thanks to

Ms Gladys Chongo Mposha, Mr. Ephraim Musilekwa, Mr. Raphael Kasonde and Mr.

Moses Chatulika for the comments and technical insights during my research. Further I

would like thank the Bank Supervision Department at large for the encouragement and

support provided to me throughout the program.

I am also very grateful to the MEFMI Secretariat, for funding my customized training

program and enhancing my supervisory skills. Furthermore, appreciation is extended to

Dr. Fundanga, Dr. Ngalande, Mr. Ncube, Mr. Mutimba, Mrs. Makamba and the entire

MEFMI secretariat for according me the opportunity to be part of the fellowship program

and their unwavering support.

And finally I wish to extend special thanks to my husband, for his patience and support.

1

List of Acronyms and Abbreviations

AIRB Advanced Internal Ratings–Based Approach

AMA Advanced Measurement Approach

BCBS Basel Committee on Banking Supervision

BCF Basel Capital Framework

BCP Basel Core Principles for Effective Banking Supervision

BIA Basic Indicator Approach

BOZ Bank of Zambia

CAR Capital Adequacy Ratio

CCF Credit Conversion Factors

CRM Credit Risk Mitigation

ECA Export Credit Agencies

FDIC Federal Deposit Insurance Corporation

FIRB Foundation Internal Ratings-Based Approach

FSAP Financial Sector Assessment Programme

GI Gross Income

GRZ Government Republic of Zambia

ICAAP Internal Capital Adequacy Assessment Process

IMF International Monetary Fund

LCR Liquidity Coverage Ratio

MEFMI Macroeconomic and Financial Management Institute

NSFR Net Stable Funding Ratio

OECD Organization of Economic Cooperation and Development

RCAP Regulatory Consistency Assessment Programme

RWA Risk - Weighted Assets

SA Standardized Approach

SADC Southern African Development Community

SREP Supervisory Review and Evaluation Process

SSA Simplified Standardized Approach

TSA The Standardized Approach

1

1. Introduction Banks are among the most highly leveraged institutions due to the roles that they play in

the economy. To draw from Sihna (2014) presentation that the financial system in general

and banks in particular are essential to the economy and their functioning has large

implications for economic growth. This stems from the banks’ role of financial

intermediation between savers and borrowers, promote saving which enhances free

enterprise. Banks take depositors funds, essentially borrowing funds and then at the same

time lending it out to their customers who are in need of financing, this creates a series of

debts. It has been argued by Simpson (2014) that when asset values decline, those assets

are less able to service debt, which in turn makes it difficult for banks to take in more

deposits thereby reducing the banks’ ability to lend. This results in a decrease in the flow

of credit from savers to borrowers and a decline in economic activity. In Zambia, the

banking sector accounts for over 80% of the financial sector’s total assets. The banking

sector is therefore a critical component of the Zambian financial system [Bank of Zambia

Financial Stability Report. 2014].

1.1. Structure of the Zambian Banking Sector

The Zambian banking sector comprised 19 commercial banks as at the end of December,

2013, and of which 13 banks were subsidiaries of foreign banks, 4 banks were locally

incorporated private banks while 2 were quasi-owned by the Government of the Republic

of Zambia. [The Bank Supervision of Zambia, 2013 Annual Report].

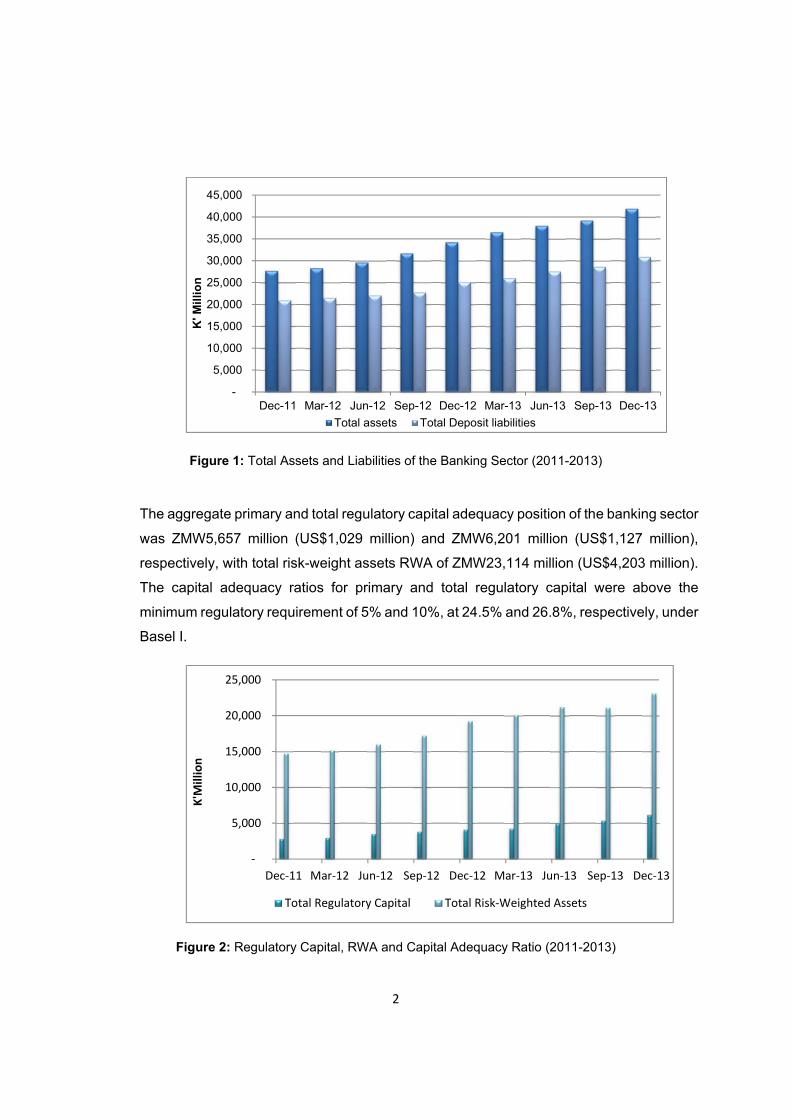

The total assets of the banking sector as at the end the December 2013 was ZMW41,953

million (US$7,628 million). The sector’s assets composition was mainly dominated by net

loans and advances which accounted for the largest share of the sector’s total assets at

43% followed by investment in government securities at 23%. Other significant classes of

assets included balances with the Bank of Zambia at 12%, then balances with foreign

financial institutions at 11% [Bank of Zambia, 2013 Annual Report]. The major funding for

the sector’s assets was customer deposits which accounted for 86% of total liabilities and

74% of total assets. [Bank Supervision, 2013 Annual Report]. Figure 1 depicts the growth

in total assets and deposits over the last three years.

2

Figure 1: Total Assets and Liabilities of the Banking Sector (2011-2013)

The aggregate primary and total regulatory capital adequacy position of the banking sector

was ZMW5,657 million (US$1,029 million) and ZMW6,201 million (US$1,127 million),

respectively, with total risk-weight assets RWA of ZMW23,114 million (US$4,203 million).

The capital adequacy ratios for primary and total regulatory capital were above the

minimum regulatory requirement of 5% and 10%, at 24.5% and 26.8%, respectively, under

Basel I.

Figure 2: Regulatory Capital, RWA and Capital Adequacy Ratio (2011-2013)

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13

K' M

illio

n

Total assets Total Deposit liabilities

‐

5,000

10,000

15,000

20,000

25,000

Dec‐11 Mar‐12 Jun‐12 Sep‐12 Dec‐12 Mar‐13 Jun‐13 Sep‐13 Dec‐13

K'M

illion

Total Regulatory Capital Total Risk‐Weighted Assets

3

1.2. Minimum Capital Requirements

Nearly all jurisdictions with active banking systems require banks to maintain a minimum

level of capital adequacy to minimize disruptions to the financial system. Capital serves

as a cushion against unexpected losses and ensures future growth. Adequate levels of

capital help to promote public confidence in the banking system and enhance the financial

system’s resilience to shocks. The level and type of capital a bank requires has to be

commensurate with risks that a bank is exposed to in order to ensure adequate protection.

Prior to 1988, the requirements governing regulatory capital were country specific.

However, over time it became apparent that international convergence of regulatory

capital was desirable, especially given the increasing global activities of many banks. To

that end International Convergence of Capital Measurement and Capital Standards

(Commonly known as Basel I) was released in 1988, by the Basel Committee on Banking

Supervision (BCBS). Although the Accord was intended for internationally active banks

within the BCBS member countries1, over a 100 countries adopted Basel I, this lead to

increased consistency in defining regulatory capital [Reserve Bank of India Occasion

Papers Vol. 29, No. 2, Monsoon, 2008].

The main objectives of the Basel Committee when developing the regulatory convergence

(Basel I) was that the Basel Accord would strengthen the soundness and stability of the

international banking system; and that the framework would be fair and have a degree of

consistency in its application to banks in different countries with a view of reducing

competitive inequality among international banks [BCBS: International Convergence of

Capital Measurement and Capital Standards]. Basel I however, was considered to have a

narrow focus as it initially only covered credit risk and had a narrow range of risk-weights

which was not based on the riskiness of the underlying asset or instrument. Market risk

was only later included as part of amendments of 1996.

Following the economic turbulence in the world financial system 1997/1998, the risks that

internationally active banks from G-10 countries had to deal with had become more

complex and challenging. The review of the Basel I was designed to improve the way

1 The BCBS comprises bank supervisors from 27 member countries (Argentina, Australia, Belgium, Brazil, Canada, China, France, Germany, Hong Kong SAR, India, Indonesia, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, Turkey, United Kingdom, and the United States).

4

regulatory capital requirements reflect underlying risks. It was also designed to better

address the financial innovation that had occurred, for example, asset securitisation

structures. Such innovations rendered Basel I less effective in ensuring that capital

requirements match a bank’s true risk profile. The review was also aimed at recognizing

the improvements in risk measurement and control that had occurred [Consultative

Document - Overview of the Basel New Capital Accord, 2001]. Subsequently, numerous

improvements were made to the Accord aimed at making capital more risk sensitive, which

resulted in momentous enhancements leading to the issuance of Basel II.

However, the Global Financial Crisis of 2007 highlighted weakness with Basel II and the

BCBS responded with Basel 2.5 and Basel III. Basel II made significant changes to the

methodology for computing risk-weighted assets (RWA). While Basel III proposes to make

significant changes to the definition of capital and asset quality.

5

1.3. Evolution of Basel Capital Framework

Figure 3: Evolution of Basel Capital Framework

Basel I primarily focused on credit risk and appropriate risk-weighting of assets with regard

to credit risk. Banks’ assets were classified and grouped in five classes according to

degree of credit risk as indicated in Table 1 below:

Asset Classification2 Risk

Weight Cash, bullion, Government Securities 0% Claims on domestic public-sector entities, excluding central government, and loans guaranteed by such entities

20%

Loans fully secured by mortgage on residential property that is or will be occupied by the borrower or that is rented

50%

Corporate debt 100% Some assets with no rating for on balance sheet items 100%

Table 1: Basel I Asset Classification

The Basel I also took account of the credit risk in off-balance-sheet exposures by applying

credit conversion factors to the different types of off-balance-sheet items. With the

exception of foreign exchange and interest rate related contingencies, the credit

2 Source: BCBS: International Convergence of Capital Measurement and Capital Standards

6

conversion factors ranged from 0% to 100%. They were derived from the estimated size

and likely occurrence of the credit exposure, as well as the relative degree of credit risk

as identified in the Committee's paper "The management of banks' off-balance sheet

exposures: a supervisory perspective" issued in March 1986. The credit conversion

factors would be multiplied by the weights applicable to the class of the counterparty for

an on-balance-sheet transaction International Convergence of Capital Measurement and

Capital Standards. Banks with international presence were required to hold capital equal

to 4% and 8% of their risk-weighted assets (RWA) for Tier 1 capital and total capital,

respectively.

Minimum Capital Adequacy Ratios

Tier 1 capital ratio = tier 1 capital / all RWA

Total capital ratio = (tier 1 + tier 2 + tier 3 capital) / all RWA

Table 2: Minimum Capital Adequacy Ratios

Basel II represented advancement over Basel I. Basel II is considered significantly more

risk-sensitive as it covers risks that were not covered by Basel I such as operational risk

and other risks such credit concentration risk, liquidity risks, interest rate risk in the banking

book. Further, credit risk has moved from simple credit risk–weighting to modeling credit

risk.

The financial crises of 2007 greatly affected the stability global banking system. It was

apparent that the Basel II Framework was insufficient with regard to its risk coverage

relating to complex securitization and re-securitization activities. Consequently, Basel 2.5

was issued as an interim measure and focused on only additional risks concerning banks’

securitization and re-securitization activities with regard to credit risk and market risk

[Saudi Arabian Monetary Agency’s Approach to Implement Basel 2.5: Saudi Arabian

Monetary Agency Banking Supervision Department, and October 2012]. Basel III provided

further enhancements to Basel I, Basel II and Basel 2.5 by strengthening of the definition

of regulatory capital. Following the 2007 global financial crisis, the Banking Basel

Committee on Banking Supervision embarked on global capital and liquidity reforms

aimed at strengthening the banking sector’s ability to absorb shocks arising from financial

7

and economic stress hence minimizing the risk of spillover from the financial sector to real

economy. Below is a summary of how Basel Capital Framework3 has evolved.

Basel I Basel II Basel 2.5 Basel III Definition of regulatory capital 1988 2010 Simple credit risk - weighting 1988 2004 Modeling credit risk 2004 Market risk 1996 2005 2009 Operational risk 2004 Counterparty risk 1988 2004 2010 Securitization 2004 2009 Pillar 2 2004 2009 Pillar 3 2004 2009 Regulatory capital adequacy ratio (CAR)

1988 2010

Capital conservation buffer 2010 Countercyclical buffer 2010 Leverage ratio 2010 Global systemically important banks

2011

Table 3: Evolution of Basel Capital Framework

1.4. Implementation of Basel II: Practical Considerations4 Following the release of the Basel II in June 2004, the Committee recognised that adoption

of the Revised Framework in the near future would not be a priority for all supervisors in

non-G10 countries in terms of what is needed to strengthen their supervision regime.

The BCBS indicated that Basel II was aimed at building a solid foundation of prudent

capital regulation, supervision, and market discipline and to enhance risk management

and financial stability. As such, the Committee encouraged each national supervisor to

consider cautiously the benefits of the new Framework in the context of their own local

banking system in developing their implementation plan and approach. Considering the

required resources and constraints, the plans were expected to extend beyond the

Committee’s implementation dates. Supervisors were therefore expected to consider

implementation of key elements of the supervisory review and market discipline

3 Data Source: FSIConnect (http://www.fsiconnect.org) 4 Basel Committee on Banking Supervision. 2004. Implementation of Basel II: Practical Considerations

8

components of the new Framework even if the Basel II minimum capital requirements

were not fully implemented by the implementation date. National supervisors were also

expected to ensure that banks that did not implement Basel II were subject to prudent

capital regulation and sound accounting and provisioning policies.

1.5. Implementation of Basel II in Zambia As was the case with Basel I Capital Framework of 1988 which established the first

internationally accepted definition and measure of bank regulatory capital, the Bank of

Zambia (BOZ), made a policy decision to implement the Basel II Capital Framework by

2009. However, this was not achieved as planned and the new implementation date was

moved to 2014.

A project team was established to spearhead the implementation process of Basel II. The

team carried out a number of activities between 2004 and 2007. However, due to staff

constraints and other pressing demands in general, work scaled down considerably from

2008. However, implementation of Basel II remained one of the Bank of Zambia’s strategic

objectives since 2008. In 2009, BOZ appointed a dedicated team to advance the

implementation process and set January, 2014 as the new implementation date. Further,

the adoption of Basel II is a requirement under the SADC Committee of Central Bank

Governors’ Sub-Committee on Banking Supervision, with an implementation target date

of 2014. Basel II comprise of three mutually reinforcing pillars as indicated below:

Pillar I - Minimum Capital Requirements;

Pillar II - Supervisory Review Process; and

Pillar III - Market discipline.

Pillar I, prescribes the minimum capital requirements and banks are supposed to allocate

capital for credit, market and operational risk. While under Pillar II banks are expected to

allocate additional capital for risks that are not covered under Pillar I. Pillar II focuses on

the banks’ internal capital adequacy assessment process (ICAAP) and supervisory review

and evaluation process (SREP). The third pillar deals with market discipline which

reinforce efforts to promote safety and soundness in banks.

Implementation of Basel II is not an end in itself for Zambia as a lot of improvements have

occurred since the global financial crisis of 2007 aimed at enhancing the stability of the

9

financial system. The study therefore, also reviewed the latest developments, post the

global financial crisis of 2007 and develop a strategy for future adoption/implementation

of the revisions that have been made to the Basel Capital Accord under Basel 2.5 and

Basel III.

1.6. Problem Statement

Following the global financial crisis of 2007 a lot of improvements have been done to the

Basel capital framework. Although the Basel capital framework is intended for

internationally active banks, non G-10 countries implement the accords in order to be

competitive. However, countries in the non-G10 countries, such as MEFMI member states

including Zambia are at various stages of implementing Basel Accord, this poses a

challenge when developing strategies to address problems being faced by MEFMI

member countries in the implementation of Basel II.

The integrity of data is considered to posse difficulties in the assessment and

quantification of the impact of adopting Basel II on the banks’ capital adequacy position in

Zambia.

There is no prescribed methodology for allocation of capital for Pillar II risks. Pillar II is

principle based. Under Pillar II, banks are expected to conduct an Internal Capital

Adequacy Assessment Process (ICAAP) and to set aside capital for all risks not covered

under Pillar I. The major challenge for supervisors lies in the limited skills and human

resources required to evaluate the ICAAP document and interrogate banks’ internal

models used in the allocation of capital for pillar II risks. It is therefore important that

regulators develop the right set of skills required to evaluate and validate the models being

used or develop a framework to ensure oversight.

1.7. Objectives of the Paper

10

The primary objective of this paper is to establish the impact of Basel II on the commercial

banks’ capital adequacy in Zambia. In this regard, the paper aims at:

i. Determining the current status of the Basel II project in Zambia and the MEFMI

member countries

ii. Determining the impact of Basel II on the banks’ capital adequacy position.

iii. Establishing the implementation status of Basel 2.5 and Basel III and implication for

Zambia and MEFMI member countries.

1.8. Significance of Study

Globalization and deregulation brought about sweeping changes in the banking sector

across countries. One may wonder about the relevance of the Basel II framework

especially for emerging countries, as it was designed for internationally active banks. The

position of most regulators and indeed that of the Bank of Zambia is that countries have

integrated with the rest of the world. It is for this reason that no country can afford to have

regulatory standards that deviate from global standards, as banking has evolved into a

global industry and physical boundaries no longer have any significant bearing in financial

markets.

To be part of the international financial system and to remain competitive, countries have

to adopt internationally accepted standards and Basel II is the globally accepted standard

by which the banking sector’s solvency is measured. Any deviation would harm a nation’s

financial system stability through perception and also in actual practice. If local standards

are perceived to be lower than the norm, local banks would be at a competitive

disadvantage globally. In practice, it has to be recognized that Basel II provides for

improved risk management systems in banks. It is important that banks have the cushion

afforded by improved risk management systems to withstand external shocks, especially

as they deepen their links with the global financial system.

The aim of this study is to provide an assessment of the impact of Basel II on capital

adequacy position of banks. This will be done using an in-depth study of the 19 banks

currently operating in the Zambia. As the banks are of varying size, banks will be put into

11

three peer groups based on asset size, and then a peer analysis will be conducted. The

study will also explore the status of Basel II implementation in the MEFMI region.

1.9. Limitations of the Study

The main limitation of the study is data integrity; most banks are in the process of

configuring their data and Information technology systems to ensure Basel II compliant.

Zambia like most MEFMI member countries also have less developed secondary markets

for market risk and credit risk mitigation securities such as government or sovereign debt

instruments which will make valuation of the securities difficult. The absence of credible

external rating agents will result in the one size fits all allocation of risk weights for

corporates.

Due to lack of data concerning operational risk under the standardised approach, based

on the banks’ activities which are divided into eight business lines: corporate finance,

trading and sales, retail banking, commercial banking, payment and settlement, agency

services, asset management, and retail brokerage. The study will limit its assessment to

the basic indicator approach as most banks are in the process of reconfiguring their

systems so that data is captured according to the prescribed business lines.

Further, like Zambia most countries in the sub-Saharan Africa region are at varying levels

of Basel II implementation, hence there will be very limited information or comparable data

with regard to allocation of capital to Pillar 2 risks. In addition limited model validation skills

might result in inconsistent capital allocation under pillar II.

An earlier study that was done on Basel II, focused on assessment of the impact of

implementing simpler approaches of Pillar 1 on the regulatory capital of banks in Zambia

(Moses H Chatulika, 2008).

1.10. Research Questions

i. What is the current status of the Basel II project in Zambia and the MEFMI member

countries?

ii. What is the impact of Basel II on the Zambian banks’ capital adequacy position?

12

iii. What is the implementation status of Basel 2.5 and Basel III and implication for

Zambia and MEFMI member countries?

The following chapters seek to address these research questions.

13

2. Literature Review

2.1. Background

The Basel Committee on Banking Supervision (BCBS) has its beginnings in the financial

market crises that followed the collapse of the Bretton Woods System of managed

exchange rates of 1973. After the collapse of Bretton Woods System many banks incurred

huge foreign exchange losses. On 26 June 1974, West Germany’s Federal Banking

Supervisory Office withdrew Bankhaus Herstatt’s banking licence after finding that the

bank’s foreign exchange exposures amounted to three times its capital. Banks outside

Germany took heavy losses on their unsettled trades with Herstatt, adding an international

dimension to the crisis. In October the same year, the Franklin National Bank of New York

also closed its doors after incurring large foreign exchange losses.

To address the above and other interruptions in the international financial markets, the

central bank governors of the G10 countries established a Committee on Banking

Regulations and Supervisory Practices at the end of 1974. The Committee was created

as a forum for regular cooperation between its member countries on banking supervisory

matters. Its aim was and is to enhance financial stability by improving supervisory

knowhow and the quality of banking supervision worldwide. [Basel Committee on Banking

Supervision: A brief history of the Basel Committee, October 2014]

The Committee comprises bank supervisors from 27 member countries5 [Basel

Committee on Banking Supervision: A brief history of the Basel Committee, October

2014]. One of its best known publications is commonly referred to as the Basel Capital

Accord (Basel I), which was published in 1988 and a revised Basel Capital Framework

(BCF), known as Basel II, was published in 2004, followed by Basel III in 2010.

The Basel Capital Accord of 1988, made major developments towards harmonization of

bank capital standards. The Basel Capital Accord has seen a number of amendments

since. Though capital regulation in banking had existed in some form or the other even

5 The Basel Committee on Banking Supervision consists of senior representatives of bank supervisory authorities and central banks from Argentina, Australia, Belgium, Brazil, Canada, China, France, Germany, Hong Kong SAR, India, Indonesia, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States.

14

before the issuance of Basel Accord in 1988, the Accord marked a defining moment

towards harmonization of bank capital regulation across different jurisdictions and more

than 100 countries adopted the Basel I regulatory requirement of capital [Basel Committee

on Banking Supervision-Working Papers, Capital Requirements and Bank Behaviour: The

Impact of the Basle Accord, April 1999].

2.2. Pre-Basel Capital Framework

Prior to Basel Capital Framework, the use of capital ratios to establish minimum regulatory

requirements was being tried world over, but none were universally accepted at that time.

The escalation in bank failures and falling bank capital triggered a regulatory response in

1981 when, for instance, for the first time, the federal banking agencies in the US

introduced explicit numerical regulatory capital requirements. According to the data from

the USA Federal Deposit Insurance Corporation’s (FDIC) Division of Research and

Statistics, from 1980 to 1994, a total of 1,617 commercial and savings banks failed, the

failed banks accounted for US$206.179 billion in assets [FDIC: History of the Eighties -

Lessons for the Future, An Examination of the Banking Crises of the 1980s and Early

1990s Volume 1]. In another study based on FDIC data, 1,043 Thrifts failed or were

otherwise resolved from 1986-1995. In this case the institutions accounted for assets

amounting to $519 billion. The banking crisis of the 1980s was therefore a two-fold, on

one hand it related to the failure of savings and loans (the S&L crisis), which represented

the bulk of the assets and number of banks, and the other linked to the failure of large

commercial banks. When the above bank failures are compared to bank failure data

leading up to the 1980s, then magnitude of the crisis becomes evident. From 1965-1979,

for example, just 0.3% of all existing banks failed [FDIC: History of the Eighties - Lessons

for the Future, An Examination of the Banking Crises of the 1980s and Early 1990s Volume

1].

The increase in the number of bank failures in the 1980s had no single cause or list of

causes. Rather, it resulted from a concurrence of various forces working together to

produce a decade of banking crises. These included economic, financial, legislative, and

regulatory, established the preconditions for the increased number of bank failures at least

in the case of the USA. Further, a series of severe regional and sectoral recessions hit

banks in a number of banking markets and led to a majority of the failures. Furthermore,

15

some of the banks in these markets assumed excessive risks and were insufficiently

restrained by supervisory authorities, with the result that they failed in disproportionate

numbers [FDIC: History of the Eighties - Lessons for the Future, An Examination of the

Banking Crises of the 1980s and Early 1990s Volume 1]

The adopted standards employed a leverage ratio of primary capital (which consisted

mainly of equity and loan loss reserves) to average total assets. However, each regulator

had a different view as to what exactly constituted bank capital. With passage of time,

regulators worked to converge upon a uniform measure. The inadequate capitalization of

Japanese banks and differing banking structures (universal banks of Germany vis-à-vis

narrow banks of US) and varying risk profile of individual banks made agreement on

capital standards problematic.

The US Congress passed legislations in 1983, directing the federal banking agencies to

issue regulations addressing capital adequacy [Peterson Institute for international

Economics, Banking on Basel Preview Chapter 2: Role of Capital Regulations]. The

legislation provided the motivation for a common definition of regulatory capital and final

uniform capital requirements in 1985. By 1986, regulators in the US were concerned about

the failure of primary capital ratio to differentiate among risks and not providing an accurate

measure of the risk exposures associated with innovative and expanding banking

activities, most notably off-balance-sheet activities at larger institutions.

This prompted regulators in the US to start studying the risk-based capital frameworks

other countries like France, the UK and West Germany which had implemented risk-based

capital standards in 1979, 1980 and 1985, respectively. The agencies also revisited the

earlier studies of risk-based capital ratios. Leading the initiative in 1987, the US joined the

UK in announcing a bilateral agreement on capital adequacy, then Japan followed suit.

Subsequently in December 1987 ‘international convergence of capital measures and

capital standards’ was achieved and Basel Accord was released in July 1988.

16

2.3. BCBS Core Principle for Effective Supervision

To ensure effective supervision of banks, the BCBS Committee (the Committee) issued

the Basel Core Principles. The 29 Basel Core Principles are a framework of minimum

standards for sound prudential regulation and supervision of banks and banking systems.

The first 25 core principles were originally issued in 1997 and are used by countries as a

benchmark for assessing the quality of their supervisory systems and for identifying future

work to achieve a baseline level of sound supervisory practices [Basel Committee on

Banking Supervision: A brief history of the Basel Committee, October 2014]. The Core

Principles are also used by the International Monetary Fund (IMF) and the World Bank, in

the context of the Financial Sector Assessment Programme (FSAP), to assess the

effectiveness of countries’ banking supervisory systems and practices [International

Monetary Fund and World Bank, 2002: Implementation of the Basel Core Principles for

Effective Banking Supervision, Experiences, Influences, and Perspectives].

According to the BCBS Core Principle for effective supervision Principle 16 - Capital

Adequacy: The supervisor sets prudent and appropriate capital adequacy requirements

for banks that reflect the risks undertaken by, and presented by, a bank in the context of

the markets and macroeconomic conditions in which it operates. The supervisor defines

the components of capital, bearing in mind their ability to absorb losses. At least for

internationally active banks, capital requirements are not less than the applicable Basel

standards. Supervisors must be satisfied that banks and banking groups have in place a

comprehensive risk management process (including Board and senior management

oversight) to identify, evaluate, monitor and control or mitigate all material risks and to

assess their overall capital adequacy in relation to their risk profile. These processes

should be commensurate with the size and complexity of the institution. The two

fundamental objectives of the Committee’s work on regulatory convergence were:

for the framework to strengthen the soundness and stability of the

international banking system; and

for the framework to be fair and have a high degree of consistency in its

application to banks in different countries with a view to diminishing an existing

source of competitive inequality among international banks.

17

2.4. Basel I Capital Framework - Overview

The main features of Basel I was outlined in ‘International Convergence of Capital

Measurement and Capital Standards’ in three sections. The first two sections described

the framework in terms of the constituents of capital and the risk weighting system and the

third section dealt with the target ratio. The Accord provided a framework for fair and

reasonable degree of consistency in the application of capital standards in different

countries, and a shared definition of capital. The central focus of the Basel I framework

was credit risk and, as a further aspect of credit risk, country transfer risk.

The Committee later amended the Capital Accord to include risks other than credit risk,

which was the focus of the 1988 Accord. In January 1996, the Committee released the

Market Risk Amendment to the Capital Accord. This was designed to incorporate within

the Accord a capital requirement for the market risks arising from banks’ exposures to

foreign exchange, traded debt securities, equities, commodities and options.

The 1988 Capital Accord and its amendments played a significant role in creating a safe

and stable financial system by setting a common minimum capital requirement. However,

as the financial system evolved and become more sophisticated, the deficiencies in the

Accord become apparent and resulted in increased criticism of the Basel I. In its attempt

to close loopholes and re-establish a level playing field the Basel Committee started a

process of establishing a new accord, which would address the deficiencies to much the

changed realities in the financial system Mrak M, (2003).

18

Figure 4: Basel I Capital Accord Architecture

2.5. Revised Capital Framework - Basel II The faster rate of financial innovations, however, brought to the fall deficiencies of Basel I

framework and the need for a more risk-sensitive capital standard. Following years of

consultations and modifications, the revised capital framework, popularly known as Basel

II was issued by the BCBS in June 2004.

In July 2004, the BCBS published a document “Implementation of Basel II: Practical

Consideration”. The Committee encouraged each national supervisor to consider carefully

the benefits of the Basel II in the context of its own domestic banking system. The Basel

Committee was alive to the fact that given resource and other constraints, individual

country plans might extend beyond the Basel Committee's implementation dates.

The main objective of Basel II is to encourage improved risk management through the use

of three mutually reinforcing Pillars. While banks have primary responsibility for

appropriately measuring material risks and maintaining adequate capitalization, the Basel

II Framework recognizes that Pillar I minimum capital requirements cannot be the sole

answer to adequate capitalization and risk management in banks or safety and soundness

19

in a banking system. Strong risk-based supervisory review with early intervention and

market discipline under Pillars II and III, respectively, complement minimum capital

requirements.

It was therefore expected that supervisors in some jurisdictions could wish to retain their

current approach to minimum capital requirements and to focus their efforts on building a

strong supervisory review framework and to enhance market discipline, in line with the

principles underlying Pillars II and III. Assessment of countries’ compliance with the Basel

Committee's BCP provided good indications of areas of supervision that needed

strengthening in order to meet the standard supervisory requirements.

Basel II also prompted supervisors to consider the cross-border implications of the

implementation choice for instance, supervisors must evaluate whether the legal and

regulatory framework foster an effective system of cross-border supervisory exchange of

information, cooperation and co-ordination.

Figure 5: Three Mutually Enforcing Pillars

20

2.5.1. Pillar I

The requirements under Pillar I address and allocate capital for the principal risks faced

by banks, namely credit risk, market risk and operational risk. However, the business of

banking also involves other risks. Although Basel II retained the capital definition as

prescribed under Basel I and the minimum capital adequacy ratio, significant changes

were introduced in measurement of the risks. The key objective of Pillar I was to bring

greater risk-sensitivity in the computation of capital adequacy ratios and, therefore, more

flexibility in the computation of banks’ individual risk Rojas-Suarez L (2001). Under Basel

II, measurement of market risk remained unchanged, while the measurement of credit risk

was made more complex and refined. Operational risk was also included to the risks that

had to be individually quantified and supported by capital Mrak M (2003).

2.5.2. Pillar II

Pillar II acknowledges that banks also face risks not explicitly included under Pillar I. It

also recognizes that risks such as concentration risk are not fully captured under Pillar I

and that the measures used to capture risks under Pillar I, such as operational risk, are

estimates based on proxy measures. Pillar II therefore seeks to ensure that each bank

has sound internal processes in place, based on a thorough evaluation of its risks, to:

ensure that risk management and internal controls are aligned with the entity’s risk

characteristics; and

determine the level of capital that is commensurate with its overall risk profile

However, the Financial Crisis that began in 2007 revealed significant shortcomings in both

risk management and supervision – both of which form the backbone of Pillar II. In

response, the Committee developed enhanced guidance under Pillar II in order to address

a number of flaws highlighted by the crisis. The guidance did not replace, or change, the

Pillar II supervisory review process released as part of the implementation of Basel II, but

rather supplemented it. The supplemental guidance became effective in July 2009

[fsiconnect].

21

2.5.3. Pillar II - Shared Responsibility Bank management has the ultimate responsibility for managing the bank's risks and

determining the level of capital commensurate to the bank's risk profile.

Supervisors have the responsibility for evaluating how well banks assess their capital

adequacy needs relative to their risk profile, including whether banks are appropriately

addressing the relationship between different types of risk. In assessing the adequacy of

a bank's capital levels, supervisors must take into account the relationship between the

amount of capital held by the bank against its risks and the strength and effectiveness of

the bank's risk management and internal control processes.

The supervisory review process involves an active dialogue to promote a better

understanding between bank management and supervisors. This will facilitate prompt and

decisive action to reduce risk and/or increase capital levels when deficiencies are

identified.

2.5.4. Pillar II Governing Principles

Pillar II is principle based and comprises four principles. The first principle relate to the

responsibility of the banks.

The first Principle - states that banks should have a process for assessing their overall

capital adequacy in relation to their risk profile and a strategy for maintaining their capital

levels. Pillar II is also intended to ensure that banks not only hold adequate capital to

support all their risks, but also encourages banks to develop and use better risk

management techniques in monitoring and managing their risks.

The 2009, enhancements to the BCF emphasized the need for improved risk

management, including that senior management have an integrated, firm-wide

perspective of a bank's risk exposures, in order to support its ability to identify and react

to emerging and growing risks in a timely and effective manner.

22

In particular, the BCBS identified the importance of improved risk management to capital

markets activities (including securitization, off-balance sheet exposures, structured credit

and complex trading activities).

A sound risk management system should have the following key features:

active board and senior management oversight

appropriate policies, procedures and limits

comprehensive and timely identification, measurement, mitigation, controlling,

monitoring and reporting of risks

appropriate management information systems, both at the business and firm-wide

levels; and

comprehensive internal controls

A core component of Pillar II is the documentation of each bank's internal capital adequacy

assessment process (ICAAP). The ICAAP should reflect an integrated approach to risk

management and capital management, involving an assessment of the level of, and

appetite for, risk and then ensuring that the level and quality of capital is appropriate to

that risk profile. It is the bank's responsibility to ensure that it holds adequate capital to

support its risks. The BCF does not prescribe a template for the ICAAP, but rather

identifies five main features of a rigorous process. These features are as follows:

Board and senior management oversight

Sound capital assessment

Comprehensive assessment of risks

Monitoring and reporting

Independent internal control review

Further, based on significant weakness brought to light by the 2007 global financial crisis

in the risk management practices of a number of banks, it was apparent that many banks

did not practice prudent risk management against the backdrop of a prolonged period of

favourable economic conditions, rising asset prices, access to cheap funding sources and

intense competition among financial intermediaries. In response to these identified

weaknesses, the BCBS issued supplemental Pillar II guidance in July 2009 that it expects

all banks to incorporate into their ICAAP.

23

The ICAAP is expected to be forward looking. The forward-looking aspect of the ICAAP is

achieved through Stress Testing. A stress test of a bank is an evaluation of its financial

position under a severe but plausible scenario to assist in decision making within the bank.

Stress testing assists banks to understand their risk profile and their risk appetite against

their ability to absorb loss. It also alerts bank management to adverse unexpected

outcomes related to a broad variety of risks and provides an indication of how much capital

might be needed to absorb losses should large shocks occur.

A bank's capital planning process should incorporate rigorous, forward-looking stress tests

that identify possible events or changes in market conditions that could adversely impact

the bank and thus the bank's future capital resources and its capital requirements.

In its 2009 enhancements to the BCF, the BCBS emphasised the role of stress testing.

The BCBS noted that stress testing complements and helps validate other quantitative

and qualitative approaches so that bank management has a more complete understanding

of the bank's risks and the interaction of those risks under stressed conditions. In the

context of Pillar II, the bank's ICAAP must assess capital adequacy under stressed

conditions against a number of capital ratios, including regulatory capital measures.

The second Principle under Pillar II addresses the responsibilities of supervisors for

assessing a bank's ICAAP. Principle 2 - Supervisors should review and evaluate banks’

internal capital adequacy assessments and strategies, as well as their ability to monitor

and ensure their compliance with regulatory capital ratios. Supervisors should take

appropriate supervisory action if they are not satisfied with the result of this process.

The third Principle - Supervisors should expect banks to operate above the minimum

regulatory capital ratios and should have the ability to require banks to hold capital in

excess of the minimum. Pillar II recognises that banks face risks not included under Pillar

I and that many banks choose to operate at capital levels well above those implied by

Pillar I minima. Pillar II expresses the expectation that banks should operate above the

Pillar I minimum. Pillar II is not intended to introduce a system of automatic capital add-

ons driven by general regulatory requirements, nor is it intended to lead to additional

formal across-the-board requirements. Rather, the supervisory review process is intended

to address the circumstances of each bank.

24

The BCF is not prescriptive as to how supervisors should achieve the expectation under

Principle 3 that banks should operate above the minimum regulatory capital ratios.

However, it is clear that, all supervisory authorities should have sufficient powers to require

banks to hold capital in excess of regulatory requirements. Banks are expected to maintain

capital above the minimum Pillar I regulatory ratios as prescribed under the BCF, due to

following:

Pillar I does not impose capital requirements for a number of risks, including (but

not limited to) interest rate risk in the banking book, credit concentrations, strategic

and reputational risks, and business risk (variability in bank earnings).

For those risks that are explicitly covered under Pillar I – credit, market and

operational risks – regulatory capital requirements could be underestimated.

This could be due to, for instance, the proxy-based nature of the standardized

approaches to capital measurement, or because the capital requirement

determined under the advanced approaches is subject to modeling errors (such as

assumptions, data inputs, outputs and so on).

The breach of minimum requirements is a serious matter which may prompt

immediate supervisory actions and could erode market confidence in the bank.

Principle 3 integrates a bank's own assessment of its capital requirements and the

supervisor's response. This response can vary from an expectation about the size

of the buffers above the minimum Pillar I requirements to specification of a bank-

specific ratio.

A bank-specific capital requirement is typically established through the supervisory review

process. A bank-specific capital ratio is the level of capital that is commensurate with the

risk profile of a bank, taking into account both Pillar I and Pillar II risks, including the quality

of risk management. Any bank-specific ratio that is established should be reviewed

periodically, by both the bank and the supervisor, to verify that it continues to reflect the

bank's risk profile. Another supervisory response, adopted in some jurisdictions, is to set

Pillar I requirements above the minimum BCF requirements for all banks that operate in

that jurisdiction.

The fourth Principle states that supervisors should seek to intervene at an early stage to

prevent capital from falling below the minimum levels required to support the risk

25

characteristics of a particular bank and should require rapid remedial action if capital is

not maintained or restored.

2.5.5. How Pillar II Reinforces Pillar I

Pillar I cover material risks with regard to credit, market and operational risk and assigns

explicit capital requirements for those risks. However, these capital requirements are only

estimates. Pillar II involves an evaluation of the entire risk management process and the

risks not covered under Pillar.

When risk management practices or controls are considered inadequate or deficient, the

supervisory review process, as set out in Pillar II, should seek additional capital buffers

and/or improvements in those practices or controls. Likewise, if the methodologies used

by banks under Pillar 1 are considered to underestimate the amount of capital required or

if non-Pillar 1 risks are material, additional capital buffers should be sought through the

implementation of the supervisory review process.

2.5.6. Risks That Might not be Captured under Pillar I

Operation Risk: - Banks' efforts to develop operational risk measures are relatively recent,

and the collected data and the methodologies remain largely untested. Although banks'

approaches to the measurement of operational risk are evolving, they are not as precise

as the quantification of market and credit risk.

The Basic Indicator Approach (BIA) (an approach adopted by BOZ) and the Standardized

Approach (TSA) are the simpler methodologies set out in Pillar I to determine capital

required for operational risk, Gross Income (GI) is used as a proxy for the scale of a bank's

operational risk exposure. Although gross income is an indicator of exposure to

operational risk, it may not accurately reflect the level of such exposure. For instance, for

banks with low earnings base, the use of gross income could potentially underestimate

the amount of capital required for operational risk.

26

For this reason, Pillar II requires banks to incorporate into their ICAAPs a review of how

well Pillar I captures operational risk and whether the operational risk capital requirement

is adequate.

2.5.7. Pillar III Market Discipline

Under Pillar III the Committee introduced disclosure requirements as a way to foster

market discipline. The rationale behind pillar III is that knowledgeable market participants

will reward good risk management and thereby exert pressure on banks to improve their

systems and not take on excessive risk. Detailed disclosure requirements are believed to

create an environment in which effective market discipline can take place. Mrak (2003)

argues that if disclosure is to have a disciplinary function, both banks and other market

participants must recognize the importance of detailed disclosure information and play

their role by changing their behaviour according to the information received. Although the

situation in emerging countries, with regard to disclosure standards is steadily changing,

the likelihood of attaining the level expected under Basel II will not be attained

immediately. Further sensitization of both bank management and other market

participants would be needed, if disclosure requirements are to be used as a successful

tool of enhancing market discipline.

2.6. Criteria for Determining Basel II Banks

Below are some of the factors supervisors are expected to consider when determining the

population of banks to which Basel II would apply:

size of the bank, e.g. assets size ;

nature and complexity of its operations;

involvement in significant activities or business lines;

activities, or possession of a sizeable retail base;

international presence (e.g. proportion of assets held in/income from overseas

operations);

interaction with international markets;

bank's risk profile and risk management capabilities, and

other supervisory considerations, such as resources which will be available for

initial validation and ongoing monitoring, and the trade-off between the additional

27

complexity of implementing and validating these approaches vis-à-vis the

increased sensitivity of the resulting capital requirements.

2.7. Rationale for Implementing Basel II

The decision to implement Basel II was driven by a number of factors including:

Strengthening the soundness and stability of the international banking system

Basel I was found to have a number of flaws and did not, differentiate between

assets having less risk and assets having higher risk. Basel I therefore provided

a ‘one size fits all’ approach to the measurement of risk.

Basel I did not provide a capital charge for operational risk. Further, there was no

consideration for other risks such as concentration risk, liquidity risk, interest rate

risk in the banking book and strategic risk.

Basel II requires the adoption of strong risk management practices that provides a

driving force for bringing improvement in risk management capabilities in banks

Basel II provides an incentive for banks to have good risk management practices

and punishes those that are not managing their risks appropriately by requiring

them to hold higher capital allocations.

2.8. Basel II Implementation in Zambia

The implementation of Basel II shall lead to the overall soundness and stability of the

banking system. The supervised entities, the supervising authority and the country at large

are expected to benefit from the implementing Basel II in the following manner.

2.8.1. Advantages of Implementation of Basel II

The following benefits are expected to accrue when a country implements Basel II:

Financial Stability:- Increased financial system stability because the country will

have a better understanding of the risks that arise in the financial system and their

management;

28

Improved competitive standing: - Jurisdictions and institutions that do not adopt

Basel II (as was the case with Basel I) may find themselves competitively

disadvantaged when accessing international capital.

Moreover, international banks might be hesitant to enter into correspondent

relations with banks whose risk management and governance structures are not

transparent. Jurisdictions whose legal systems, accounting and auditing standards

and supervisory standards are not in line with international best practice may

therefore not be competitive and may thus be disadvantaged.

Enhanced International Perception: - Banking has evolved into a global industry

and physical boundaries no longer have any bearing in financial markets. To be

part of the international financial system and to remain competitive, countries have

to adopt international best practices and in the financial sector, Basel II, as was

the case with Basel I, is the globally accepted standard by which the banking

sector’s solvency is measured.

2.8.2. Expected Value Addition of Adaptation of Basel II for Banks

For banking institutions, the following benefits are expected to accrue when Basel II is

implemented:

Better understanding of Risks: - Basel II will improve the risk sensitivity of capital

as pillar I provide an expanded range of risks which require a capital charge.

Additionally, other risks, e.g. concentration risk, interest rate risk, strategic risk and

liquidity risks could, through the Pillar II process, also attract a capital charge.

Basel II will therefore ensure an improved framework for capital allocation through

the supervisory review process.

Improved Capital management: - Banks will be compelled to ensure that they

provide adequate capital to cushion all business risks that arise in the course of

business and not just credit risk as was the case with Basel I. This will add to the

resilience of the financial system.

Improved Risk Management practices: - Banks will have an incentive to improve

their risk management infrastructure because under Basel II, banks employing

advanced risk management practices have a reduced charge on their capital.

29

Improved pricing of banking products: - Because of improved risk recognition and

measurement, banks will be in a better position to price their products. Products

that carry a higher risk will be priced at a premium.

International best practice: - Basel II reflects international best practice and the

embodiment of improved capital management, risk management and other

corporate governance principles as encapsulated in Basel II enhances a bank’s

profile and its competitive position.

2.8.3. Advantages for the Supervisor

For supervisory authorities, the following benefits are expected to accrue when Basel II is implemented:

Better understanding of Risks: - Basel II will increase supervisors’ understanding

of the risks that banks take in their jurisdiction. A better understanding of banks’

risk profiles will improve the supervisors’ assessment of the financial condition of

banks in their jurisdiction and this will add to financial stability.

Focus on other risks: - Basel II will increase the supervisors’ focus on other risks

like operational risk, concentration risk, strategic risk and business cycle risk which

are ignored in the 1988 Accord. Under Basel II, operational risk will have a specific

capital charge whilst the other risks could also attract a capital charge. This is

expected to enhance the resilience of the financial system.

Process for aligning capital to risks: - Pillar II of Basel will provide the supervisor

with a tool which will enable them require banks to hold additional capital for risks

other than those explicitly covered by Pillar I. It also gives the supervisor a tool to

facilitate early intervention, therefore reducing the risk of bank failures. This is

expected to enhance financial system stability.

Formalization of home/host relationships: - The supervisor will have enhanced

oversight of banks that have cross-border operations through the establishment of

formal home-host supervision arrangements.

Increased disclosure: - The increased disclosure requirements of Pillar III will

assist the supervision of banks through increased market discipline. Increased

disclosure is also expected to lead to the management of financial institutions in a

30

safe and sound manner and thus contribute to stability in the banking sector and

the financial system as a whole.

2.8.4. Weakness and challenges of Basel II

A lot of researchers highlighted a number weakness with Basel II even prior to the global

financial crises of 2007 including the following:

Ward J (2002) argued that Basel II relies on the banks’ own risk estimates and that

the review was largely aimed at addressing the circumvention by large financial

institutions of the rules by regulatory arbitrage. Therefore the Committee tried to

align regulatory capital to economic capital, thereby making the regulatory capital

more ‘risk-sensitive’6.

Ward J (2002) further argued that regulators have not explained or tested the claim

that using sophisticated quantitative models represents “better risk management”

from the point of view of anyone but bank shareholders and yet the Committee

appears to have been so confident that models were better and that the Basel II

contains a capital incentive to move to the more sophisticated approaches.

Basel II strives to encourage the implementation of robust risk management

systems by the banking industry and to align regulatory capital with a bank’s risk

profile. Implementation of Basel II, however, poses a number of challenges for

supervisors, particularly with regard to acquiring and maintaining appropriate

human, financial and technical resources. On the other hand it presents a chance

for supervisors to improve their supervisory frameworks.

2.9. Preferred Basel II Pillar 1 Approaches for Zambia

Basel II allows banks a choice between two broad methodologies for calculating their

capital requirements. Banks can calculate capital requirements for credit, market and

operational risk using either the prescribed Standardized Approach or with supervisory

approved internal model-based approach. Zambia like many MEFMI member states has

6 Ward, J. “The New Basel Accord and Developing Countries: Problems and Alternatives” (2002), Cambridge Endowment of Research Finance, Working Paper No. 4, http://www.cerf.cam.ac.uk/publications/files/Ward04.pdf, p. 11

31

opted to implement the Simplified Standardized Approach (SSA) for credit risk,

Standardized Approach (SA) for market risk and Basic Indicator Approach (BIA) for

operational risk.

Pillar 1 provides a number of options for calculating banks’ minimum regulatory capital

charges for Credit Risk, Operational Risk and Market Risk. These options range from

relatively simple methodologies to more complex approaches that utilize banks’ own

quantitative risk assessments. In providing a wide range of approaches, Basel II

introduces regulatory capital requirements that capture risks more fully and are sensitive

to the differing complexity of banks.

The Bank of Zambia has adopted the Simplified Standardized Approach for credit risk,

Basic Indicator Approach (BIA) for operational risk with a possibility for migration to the

Standardized Approach upon meeting the Bank of Zambia set criteria. The Standardized

Measurement for market risk.

2.9.1. Simplified Standardized Approach for Credit Risk

The Committee permits banks a choice between two broad methodologies for calculating

their capital requirements for credit risk. One option, the Standardized Approach,

measures credit risk in a standardized manner, supported by external credit assessments.

The other alternative, the Internal Ratings-based Approach, which is subject to the explicit

approval of the bank’s supervisor, allows banks to use their internal rating systems for

credit risk.

In determining the risk weights under the standardized approach, banks may use

assessments by external credit assessment institutions recognised as eligible for capital

purposes by national supervisors in accordance with the defined criteria. However, under

the Simplified Standardized Approach, for the purpose of risk weighting claims on

sovereigns, the Bank of Zambia will recognize the country risk scores assigned by Export

Credit Agencies (ECAs), where the agencies publish their risk scores and subscribe to the

Organization of Economic Cooperation and Development (OECD) agreed methodology.

Banks will be required to use the consensus risk scores of ECAs participating in the

“Arrangement on Officially Supported Export Credit”. The OECD agreed methodology has

32

eight (8) risk scores which correspond to risk weight categories as indicated as shown in

Table 4 below:

ECA Risk7 Scores

0 - 1 2 3 4 to 6 7

Risk Weights 0% 20% 50% 100% 150%

Table 4: ECA Consensus Risk Scores8

Claims on foreign banks will be risk-weighted according to the weighting assigned to the

country in which they are incorporated as indicated in the Table 5 (regardless of the

original maturities).

ECA risk scores9 for Sovereigns

0 - 1 2 3 4 to 6 7

Risk Weights 20% 50% 100% 100% 150%

Table 5: ECA Consensus Risk Scores10

The rest of on balance exposures will be risk-weighted based on the assigned risk weights

indicated in Appendix I. While the Off-balance sheet items under the simplified

standardized approach will be converted into credit exposure equivalents through the use

of credit conversion factors (CCF) then will be assigned the risk weights indicated

Appendix II.

2.9.2. Credit Risk Mitigation

Basel II recognises that banks use a number of techniques to mitigate the credit risks to

which they are exposed. Exposure may be collateralized in whole or in part with cash or